Rethinking Home Ownership Policy for Low-Income Families

|

|

|

- Pauline Stevens

- 8 years ago

- Views:

Transcription

1 Rethinking Home Ownership Policy for Low-Income Families Informing Tenure Choices and Improving Financing Choices and Outcomes J. Michael Collins University of Wisconsin Madison A Home For Everyone 2013: Creating Housing That Works July 25, 2013 Eau Claire, Wisconsin J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 1 / 35

2 1 Why Ownership? 2 Why Low-Income Ownership? 3 Policies to Subsidize Low Income Ownership 4 What s Next? J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 2 / 35

")

3 Why Ownership? Long History of Support for Owned Property Settlement 160 acres 1920s campaigns for ownership Depression era recovery GI Bill and VA loans 1990s-2000s campaigns promoting homebuying J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 3 / 35

4 Economic Rationale Why Ownership? Home as basis of household consumption Home equity as financial asset Community investment J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 4 / 35

")

5 Why Ownership? Strong Constituencies Supporting Home Sales Development, sales transactions, re-sales Mortgage finance Real estate sales Home builders Home maintenance & services % of GDP J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 5 / 35

6 Historic Growth in Homeownership Last Decade

7 Wisconsin Ownership Higher than US Average

8 But Recession Has Been Hard

9 Rethinking Policy Supports for Ownership 2008 Housing Bust Credit market pullback Collapse of Fannie Mae and Freddie Mac 4.4 million foreclosures so far, another 1 million possible Range of policy options to respond to foreclosures...now questions about future... Ex. Changes in mortgage deduction Time to re-think?

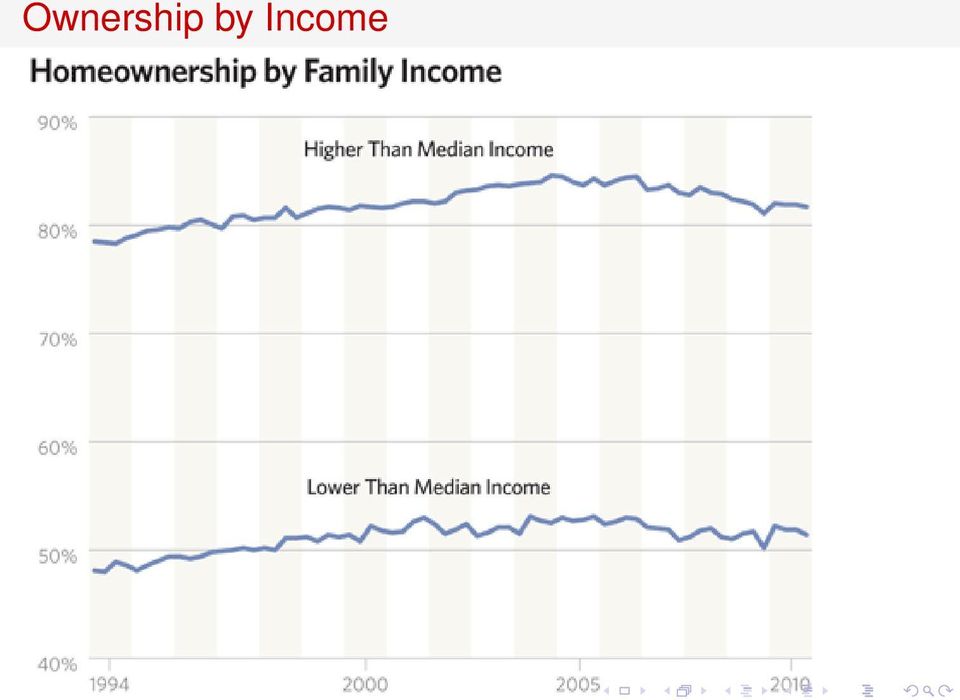

10 Ownership by Income

11 Why Low-Income Ownership? Low-Income Home Ownership Really is Not Policy Discussion Much debate who can handle their own home Subprime borrowers were not low income What even is low income? Generally define at less than 80% area median income Handful of policies even target low income Lots of mis-information: low-income borrower, lower-credit quality borrower, owner of lower-priced home all related to defaults in different ways. J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 11 / 35

12 Default by Income CTS Default Rates by Income Categories Default % <$40k $40k-$60k $60k-$80k $80k-$100k $100k-$150k >$150k Income

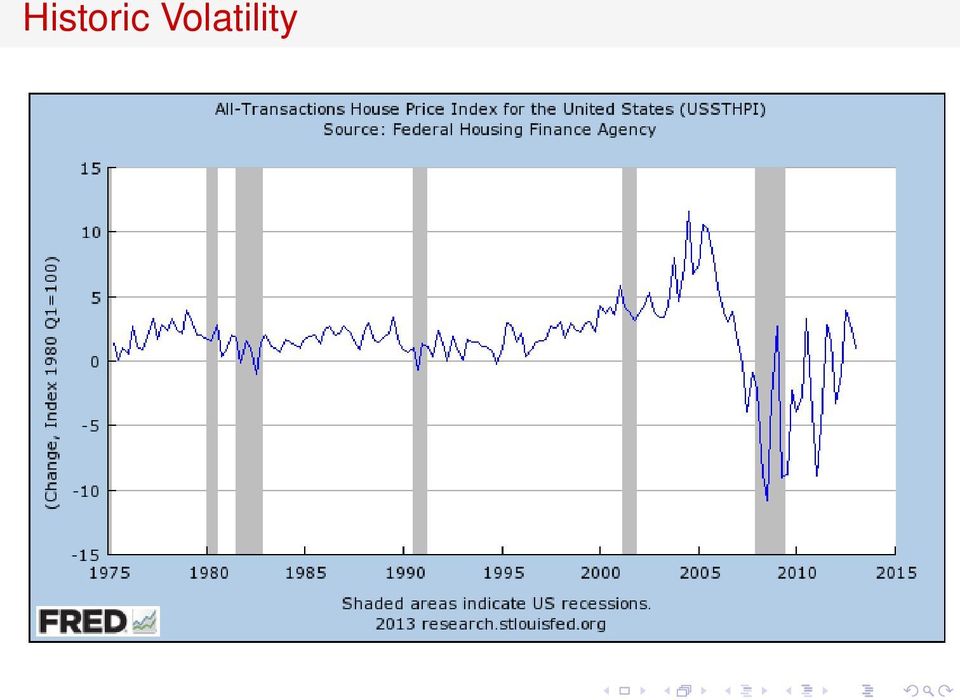

13 Historic Volatility

14 Also Variation by Price Tier

15 Why Low-Income Ownership? Why Focus on Low-Income Homeownership? Rationale: Low-income households need extra boost to gain private benefits of ownership Benefits include: Leveraged investment (loans) and force paydown of principal Stability relative to rental contracts: imputed rent Inflation protection: 75% of the wealth of lowest quartile of household wealth is stored as home equity Also potential public benefits of ownership Improved child outcomes (maybe) and civic engagement (likely) Community impacts J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 15 / 35

and civic engagement (likely) Community")

16 Patterns Also by Race

17 Few Policy Options Why Low-Income Ownership? Barrier to homeownership? Income. Consumption Subsidies Lower Monthly Payments Lower Purchase Price (which lowers payments) Credit Standards / underwriting (still might be called subsidy) Dodd-Frank qualified mortgage (QM) standards proposed Forthcoming QRM risk retention standards Downpayment barrier can be thought of as credit issue Informational Supports Education and counseling; campaigns Subsidies central to promoting ownership J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 17 / 35

18 Limited Options Why Low-Income Ownership? Renters age average $2100 in net wealth 33% of applicants with incomes under 50% of AMI are denied Debt to income ratios (DTI) pushed by other debt, especially student loan debt for younger households Lack of affordable inventory in some areas J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 18 / 35

19 Why Low-Income Ownership? Subsidies 1 Lowering monthly payments Mortgage Interest, Mortgage Rate Subsidy 2 Lowering the initial purchase price Shared equity models, Development subsidies 3 Providing down payment assistance Grants, Loans, Savings Programs J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 19 / 35

20 Monthly Payment Savings from Reducing Interest Rates Imagine: $160,000 house; 45,000 Income; 11,500 in consumer debt Downpayment and Closing Costs: $19,200 Saving 5% of income and 5% return: 7.5 years to save up Monthly Payment: $730 (at 4.5 mortgage rate) Debt-to-Income: 0.44 Monthly Payment: $647 (3.5 subsidized rate) Debt-to-Income: 0.42

Debt-to-Income: 0.44 Monthly Payment: $647 (3.")

21 Subsidy Impact: Monthly Payment Savings $180 Savings on 10% Downpayment, 160k home, 4% market 30 FRM $160 $140 $120 $100 $80 $60 $40 $20 $- Market 1% Rate Subsidy 10% more down...both

22 Scale of Targeted Policies is Small

23 Policies to Subsidize Low Income Ownership Mortgage Interest Deduction MID : Largest policy today Through tax filings; Need income to maximize value Most of value (90%) goes to one-third of taxpayers with highest incomes Not low-income focused Subsidy for borrowing, not buying Value highest at highest income brackets Only 10% of people with income under median itemize J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 23 / 35

24 Policies to Subsidize Low Income Ownership Mortgage Revenue Bonds MRB: Offered by WHEDA or MHFA Key feature is tax subsidy for bond income (although narrow spreads right now) But also exemptions from proposed QM regulations Loans originated and serviced by private firms Often paired with FHA insured loans Lower interest rate plus other flexibility features Also often paired with downpayment assistance J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 24 / 35

25 Policies to Subsidize Low Income Ownership Downpayment Assistance Loan to value ratios to matter. DPA: Downpayment Assistance Help with savings shortfall, but... Savings subsidies: example IDAs Make savings habit observable for underwriting But small in scale; often too shallow to have effects Lottery? J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 25 / 35

26 Policies to Subsidize Low Income Ownership Price Subsidies Produce (or renovate) affordable homes. HOME, CDBG, FHLB, etc Supply side matters! Location impacts But, starfish in the ocean issue...typically a handful of units Oversight is critical. (Headline risk.) Also don t want financially vulnerable families in structurally vulnerable units. J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 26 / 35

27 Equity Models Policies to Subsidize Low Income Ownership Land Trusts & variations place based Shared ownership and/or equity Cooperatives, Limited Equity Cooperatives Exciting but still quite rare, but used internationally. Need to think through life cycle and oversight/administration. J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 27 / 35

28 Policies to Subsidize Low Income Ownership Low-income Ownership Policies Force Tradeoffs: Scale vs. targeting Wealth creation vs. recycling/recapture Help buyer vs. help neighborhood Immediate costs vs. ongoing costs of subsidy Screening buyers vs. oversight of prior years buyers J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 28 / 35

29 What s Next? Federal Policy Landscape Unpredictable Housing crisis is passing Mortgage Interest and MRB might be swept up in tax reform Dedicated revenue models for housing trust have potential but maybe too tempting for other uses Subsidy programs can be costly to administer and politically risky Tax code is where the action is? QM and QRM debates (hopefully) settled this fall J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 29 / 35

30 What s Next? State and Local Policies At mercy of federal tax and other policies How subsidies are designed locally is important Targeted savings incentives could be developed Supply side strategic development/re-development Shared equity, Cooperative and Land Trust experiments are worth watching Other Common Questions Structure type preferences? Location impact? Disadvantage renters or owners (tenure neutrality)? J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 30 / 35

31 What s Next? Proposed Framework for Evaluating Options 1 Scalable lottery or really impacting behavior... 2 Marginal Effect but for... 3 Targeted getting to buyer in most need 4 Admin. Costs over the whole ownership period 5 Recapture prevent abuse 6 Recycle return subsidy for next generation 7 Neigh. Revital. distressed areas + low-income=too much? 8 Default Risk tradeoffs on terms 9 Mobility Limits limits to asset building/job changes J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 31 / 35

32 What s Next? Local Programs Have No Magic Bullets Be careful of loan pools, seconds and special products Don t neglect power of downpayments Quality of unit purchased really matters Preservation and post-purchase support must be a major focus of all programs Homeownership programs that extend beyond the first day across the threshold J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 32 / 35

33 Homeownership and Feeling of Well-being

34 Additional Resources What s Next? Joint Center for Housing Studies National Community Land Trust Network NeighborWorks National Housing Conference NYU Furman Center J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 34 / 35

35 What s Next? Contact J. Michael Collins Center for Financial Security wisc.edu cfs.wisc.edu ssc.wisc.edu/~jmcollin/ J. Michael Collins (University of Wisconsin) Homeownership Policy Home for Everyone 35 / 35

NEIGHBORHOOD LAND BANK

NEIGHBORHOOD LAND BANK Purpose: Contribute to the community stabilization, revitalization and preservation of San Diego County s communities, particularly San Diego s low and moderate income communities,

NEIGHBORHOOD LAND BANK Purpose: Contribute to the community stabilization, revitalization and preservation of San Diego County s communities, particularly San Diego s low and moderate income communities,

Developing Effective Subsidy Mechanisms for. Low-Income Homeownership

Joint Center for Housing Studies Harvard University Developing Effective Subsidy Mechanisms for Low-Income Homeownership J. Michael Collins University of Wisconsin-Madison October 2013 HBTL-08 Paper originally

Joint Center for Housing Studies Harvard University Developing Effective Subsidy Mechanisms for Low-Income Homeownership J. Michael Collins University of Wisconsin-Madison October 2013 HBTL-08 Paper originally

Summary of the Housing and Economic Recovery Act of 2008

Summary of the Housing and Economic Recovery Act of 2008 On July 30, President Bush signed major housing legislation, HR 3221, the Housing and Economic Recovery Act of 2008. The bill restructures regulation

Summary of the Housing and Economic Recovery Act of 2008 On July 30, President Bush signed major housing legislation, HR 3221, the Housing and Economic Recovery Act of 2008. The bill restructures regulation

The FHA Does Not Produce Sustainable Homeownership

The FHA Does Not Produce Sustainable Homeownership Government Involvement in Residential Mortgage Markets Sponsored by: the Federal Reserve Bank of Atlanta Edward Pinto, Resident Fellow American Enterprise

The FHA Does Not Produce Sustainable Homeownership Government Involvement in Residential Mortgage Markets Sponsored by: the Federal Reserve Bank of Atlanta Edward Pinto, Resident Fellow American Enterprise

The TBA Market and Risk Retention Robert Barnett January, 2011

The TBA Market and Risk Retention Robert Barnett January, 2011 The Dodd-Frank Act ( DFA ) imposes a mandate on various regulators acting jointly to promulgate regulations implementing the risk retention

The TBA Market and Risk Retention Robert Barnett January, 2011 The Dodd-Frank Act ( DFA ) imposes a mandate on various regulators acting jointly to promulgate regulations implementing the risk retention

VHDA. Homeownership Program Guidelines for Realtors & Lenders. Updated 04/04

VHDA Homeownership Program Guidelines for Realtors & Lenders Updated 04/04 2 Benefits of a VHDA Loan: Creative financing programs Reduced interest rates Lower monthly payments More house for less money

VHDA Homeownership Program Guidelines for Realtors & Lenders Updated 04/04 2 Benefits of a VHDA Loan: Creative financing programs Reduced interest rates Lower monthly payments More house for less money

Long-term affordable homeownership: Program design and research findings

Long-term affordable homeownership: Program design and research findings Brett Theodos February 12, 2015 AN INTRO TO LONG-TERM AFFORDABLE HOMEOWNERSHIP Shared Equity Homeownership: A Quick Intro Allows

Long-term affordable homeownership: Program design and research findings Brett Theodos February 12, 2015 AN INTRO TO LONG-TERM AFFORDABLE HOMEOWNERSHIP Shared Equity Homeownership: A Quick Intro Allows

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners July 2014 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners July 2014 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners March 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners March 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners April 2014 U.S. Department U.S Department of Housing of Housing and Urban and Urban Development Development

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners April 2014 U.S. Department U.S Department of Housing of Housing and Urban and Urban Development Development

MSHDA's Down Payment Assistance and Mortgage Credit Certificate. May 21, 2010 (3:30 5:00 p.m.) Facilitated by: Carol Brito (MSHDA) Sponsored by:

Facilitated by: Carol Brito (MSHDA) Sponsored by:") MSHDA's Down Payment Assistance and Mortgage Credit Certificate May 21, 2010 (3:30 5:00 p.m.) Facilitated by: Carol Brito (MSHDA) Sponsored by: CREDIT UNIONS A DRIVING FORCE OF COMMUNITIES MSHDA Overview

MSHDA's Down Payment Assistance and Mortgage Credit Certificate May 21, 2010 (3:30 5:00 p.m.) Facilitated by: Carol Brito (MSHDA) Sponsored by: CREDIT UNIONS A DRIVING FORCE OF COMMUNITIES MSHDA Overview

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners August 2013 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners August 2013 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

Financing Residential Real Estate

Financing Residential Real Estate Chapter 1: Finance and Investment Borrowing Money to Buy a Home Investments and Returns Types of Investments Ownership Investments Debt Investments Securities Investment

Financing Residential Real Estate Chapter 1: Finance and Investment Borrowing Money to Buy a Home Investments and Returns Types of Investments Ownership Investments Debt Investments Securities Investment

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners June 2013 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners June 2013 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

Affordable Housing Partnership Housing Counseling Program

Affordable Housing Partnership Housing Counseling Program ORGANIZATION AND STAFF INFORMATION Name of Organization: Affordable Housing Partnership of the Capital Region Inc. 255 Orange Street Albany, New

Affordable Housing Partnership Housing Counseling Program ORGANIZATION AND STAFF INFORMATION Name of Organization: Affordable Housing Partnership of the Capital Region Inc. 255 Orange Street Albany, New

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners July 2013 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners July 2013 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

Obama Administration Efforts to Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners March 21 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners March 21 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

Brooklyn Park Economic Development Authority

Brooklyn Park Economic Development Authority Neighborhood Stabilization Program NSP HOMEBUYER ASSISTANCE PROGRAM FOR CITY/PARTNER ACQUISITION AND REHAB Program Description & Guidelines July 2011 TABLE

Brooklyn Park Economic Development Authority Neighborhood Stabilization Program NSP HOMEBUYER ASSISTANCE PROGRAM FOR CITY/PARTNER ACQUISITION AND REHAB Program Description & Guidelines July 2011 TABLE

Why rent when you can buy?

Why rent when you can buy? Are you unsure about becoming a HOMEOWNER? Thinking that you can t afford to BUY a home? Are you worried about whether homebuying is a good INVESTMENT? Buying a first home can

Why rent when you can buy? Are you unsure about becoming a HOMEOWNER? Thinking that you can t afford to BUY a home? Are you worried about whether homebuying is a good INVESTMENT? Buying a first home can

2013 DENVER METRO MORTGAGE ASSISTANCE PLUS

2013 DENVER METRO MORTGAGE ASSISTANCE PLUS PROGRAM Down Payment Assistance of 4% (3% + 1% Origination) of the total mortgage amount - in exchange for a slightly higher mortgage interest rate! HISTORICALLY

2013 DENVER METRO MORTGAGE ASSISTANCE PLUS PROGRAM Down Payment Assistance of 4% (3% + 1% Origination) of the total mortgage amount - in exchange for a slightly higher mortgage interest rate! HISTORICALLY

A Presentation On the State of the Real Estate Crisis 1/30/2009

A Presentation On the State of the Real Estate Crisis 1/30/2009 Presented by Mike Anderson, CRMS President, Essential Mortgage, a Latter & Blum Realtors Company Immediate past president/legislative Chair

A Presentation On the State of the Real Estate Crisis 1/30/2009 Presented by Mike Anderson, CRMS President, Essential Mortgage, a Latter & Blum Realtors Company Immediate past president/legislative Chair

Support Under the Homeowner Affordability and Stability Plan: Three Cases

Support Under the Homeowner Affordability and Stability Plan: Three Cases Family A: Access to Refinancing In 2006: Family A took a 30-year fixed rate mortgage of $207,000 on a house worth $260,000 at the

Support Under the Homeowner Affordability and Stability Plan: Three Cases Family A: Access to Refinancing In 2006: Family A took a 30-year fixed rate mortgage of $207,000 on a house worth $260,000 at the

Secondary Mortgage Market Policy Fannie Mae to QRM. Kevin Park PLAN 761 September 19, 2012

Secondary Mortgage Market Policy Fannie Mae to QRM Kevin Park PLAN 761 September 19, 2012 History of Mortgage Lending Traditional Bank Lending e.g., Bailey Building and Loan Association Mortgage Payments

Secondary Mortgage Market Policy Fannie Mae to QRM Kevin Park PLAN 761 September 19, 2012 History of Mortgage Lending Traditional Bank Lending e.g., Bailey Building and Loan Association Mortgage Payments

Financial Education for Homeowners

Financial Education for Homeowners Tax Time Coalition of Central Ohio MISSION: To provide the central Ohio community with information about, and access to, free, high-quality tax assistance services and

Financial Education for Homeowners Tax Time Coalition of Central Ohio MISSION: To provide the central Ohio community with information about, and access to, free, high-quality tax assistance services and

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

Down Payment Assistance Programs

Down Payment Assistance Programs Schedule an Appointment 6 8 hour Homebuyers Education Course 2-hour Pre-Purchase Counseling The Homeowners Employment Corporation SunTrust Bank Building - A 1530 Georgia

Down Payment Assistance Programs Schedule an Appointment 6 8 hour Homebuyers Education Course 2-hour Pre-Purchase Counseling The Homeowners Employment Corporation SunTrust Bank Building - A 1530 Georgia

Agencies and Resources

The following local, state and federal agencies administer programs or provide funds for housing programs and projects: Murray County EDA P.O. Box 57 Slayton, MN 56172 Contact: Amy Hoglin, Economic Development

The following local, state and federal agencies administer programs or provide funds for housing programs and projects: Murray County EDA P.O. Box 57 Slayton, MN 56172 Contact: Amy Hoglin, Economic Development

Making Home Affordable Updated Detailed Program Description

Making Home Affordable Updated Detailed Program Description The deep contraction in the economy and in the housing market has created devastating consequences for homeowners and communities throughout

Making Home Affordable Updated Detailed Program Description The deep contraction in the economy and in the housing market has created devastating consequences for homeowners and communities throughout

July 27, 2011. Re: Credit Risk Retention Proposed Rule. To Whom It May Concern:

July 27, 2011 Department of the Treasury Office of the Comptroller of the Currency 250 E Street, SW., Mail Stop 2-3 Washington, DC 20219 Docket No. OCC-2011-0002, RIN 1557-AD40 Board of Governors of the

July 27, 2011 Department of the Treasury Office of the Comptroller of the Currency 250 E Street, SW., Mail Stop 2-3 Washington, DC 20219 Docket No. OCC-2011-0002, RIN 1557-AD40 Board of Governors of the

910 17 th Street, NW 5 th Floor Washington, DC 20006. Tel: 202.349.1860 / Fax: 202.289.9009 www.self-help.org

Dangerous lending practices and loose underwriting in the subprime mortgage market have left more than 2.2 million families in danger of losing their homes to foreclosure over the next few years. Self-

Dangerous lending practices and loose underwriting in the subprime mortgage market have left more than 2.2 million families in danger of losing their homes to foreclosure over the next few years. Self-

Housing Assistance Opportunities for Duluth Residents October 15, 2010

Housing Assistance Opportunities for Duluth Residents October 15, 2010 City of Duluth Building Safety City of Duluth Community Development City Hall Room 210, Duluth, MN 55802 City Hall Room 407, Duluth,

Housing Assistance Opportunities for Duluth Residents October 15, 2010 City of Duluth Building Safety City of Duluth Community Development City Hall Room 210, Duluth, MN 55802 City Hall Room 407, Duluth,

Homeownership Division

Michigan Credit Union League & Affiliates Annual Convention and Exposition Helping Credit Unions Serve, Grow and Remain Strong #mculace MSHDA s Homeownership Programs Delivering the Dream to Michigan Families

Michigan Credit Union League & Affiliates Annual Convention and Exposition Helping Credit Unions Serve, Grow and Remain Strong #mculace MSHDA s Homeownership Programs Delivering the Dream to Michigan Families

THE MORTGAGE INTEREST DEDUCTION Frequently Asked Questions

THE MORTGAGE INTEREST DEDUCTION Frequently Asked Questions Prepared by the National Low Income Housing Coalition Updated April 2013 Owning one s home is a strong American value. Most Americans consider

THE MORTGAGE INTEREST DEDUCTION Frequently Asked Questions Prepared by the National Low Income Housing Coalition Updated April 2013 Owning one s home is a strong American value. Most Americans consider

ReNew Grant Guidelines

Brooklyn Center ReNew Buyer Incentive Program Greater Metropolitan Housing Corporation Program Summary The Economic Development Authority (EDA) of Brooklyn Center, Minnesota (EDA) has partnered with the

Brooklyn Center ReNew Buyer Incentive Program Greater Metropolitan Housing Corporation Program Summary The Economic Development Authority (EDA) of Brooklyn Center, Minnesota (EDA) has partnered with the

Why home values may take decades to recover. by Dennis Cauchon, USA TODAY

Why home values may take decades to recover by Dennis Cauchon, USA TODAY 200 180 160 140 120 100 80 The history of housing as an investment 1950 1952 1954 1956 1958 1960 1962 1964 1966 1968 1970 1972 1974

Why home values may take decades to recover by Dennis Cauchon, USA TODAY 200 180 160 140 120 100 80 The history of housing as an investment 1950 1952 1954 1956 1958 1960 1962 1964 1966 1968 1970 1972 1974

DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT

DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT Funding Highlights: Provides $44.8 billion, an increase of 3.2 percent, or $1.4 billion, above the 2012 program funding level. Increases are made to protect

DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT Funding Highlights: Provides $44.8 billion, an increase of 3.2 percent, or $1.4 billion, above the 2012 program funding level. Increases are made to protect

More than just housing... CO-OP HOUSING

More than just housing... CO-OP HOUSING How you can profit by living in a housing cooperative. Introduction A combination of factors including the rising cost of housing in recent years, have forced many

More than just housing... CO-OP HOUSING How you can profit by living in a housing cooperative. Introduction A combination of factors including the rising cost of housing in recent years, have forced many

2. Inventory available public property within the site area. Include publiclyheld property, tax-foreclosures, and donated property.

Land Assembly and Redevelopment What is it? Land is location, and location is the most valuable asset in successful real estate development. The right land transaction is crucial to each of the twin objectives

Land Assembly and Redevelopment What is it? Land is location, and location is the most valuable asset in successful real estate development. The right land transaction is crucial to each of the twin objectives

FUNDING SOURCES WITH POTENTIAL APPLICABILITY TO AFFORDABLE HOUSING AT HUNTING TOWERS

FUNDING SOURCES WITH POTENTIAL APPLICABILITY TO AFFORDABLE HOUSING AT HUNTING TOWERS REHABILITATION There are a variety of funding sources that can be used for the rehabilitation (with or without acquisition)

FUNDING SOURCES WITH POTENTIAL APPLICABILITY TO AFFORDABLE HOUSING AT HUNTING TOWERS REHABILITATION There are a variety of funding sources that can be used for the rehabilitation (with or without acquisition)

Pre-Purchase Counseling Application

Pre-Purchase Counseling Application Guidance on purchasing a home and qualifying for downpayment assistance Pre-purchase counseling helps prepare the first-time homebuyer for the home purchase process

Pre-Purchase Counseling Application Guidance on purchasing a home and qualifying for downpayment assistance Pre-purchase counseling helps prepare the first-time homebuyer for the home purchase process

The Aspen Institute Initiative on Financial Security (Aspen IFS) proposes. incentives available to low- and middleincome

proposes. incentives available to low- and middleincome") BACK TO BASICS: A SAVINGS APPROACH TO HOMEOWNERSHIP Homeownership is a core American value. It epitomizes the American Dream and the be a springboard to the acquisition of other important assets like a

BACK TO BASICS: A SAVINGS APPROACH TO HOMEOWNERSHIP Homeownership is a core American value. It epitomizes the American Dream and the be a springboard to the acquisition of other important assets like a

Home Buying Seminar. A presentation by The Summit Federal Credit Union

Summit Branches are located in Rochester (7), Seneca Falls (1), Buffalo (3), Syracuse (5) and Cortland (2) Home Buying Seminar A presentation by The Summit Federal Credit Union What We Will Cover Today

Summit Branches are located in Rochester (7), Seneca Falls (1), Buffalo (3), Syracuse (5) and Cortland (2) Home Buying Seminar A presentation by The Summit Federal Credit Union What We Will Cover Today

Funding Programs: HUD Performance Funding System (operating subsidy for PHA) Private foundation operating grants

Private foundation operating grants") Funding Programs by Funding Tools Federal Funding Programs 1. Owner or participant investment - An investment of funds from agency operation or fees paid by a participant to offset the cost of providing

Funding Programs by Funding Tools Federal Funding Programs 1. Owner or participant investment - An investment of funds from agency operation or fees paid by a participant to offset the cost of providing

ACEEE Greening the Mortgage Process. Michelle Winters March 2012

ACEEE Greening the Mortgage Process Michelle Winters March 2012 NeighborWorks America Working Together for Strong Communities Support Homeownership Homeownership and foreclosure counseling Provide Affordable

ACEEE Greening the Mortgage Process Michelle Winters March 2012 NeighborWorks America Working Together for Strong Communities Support Homeownership Homeownership and foreclosure counseling Provide Affordable

The Federal Home Loan Banks, Community Investment, and Affordable Housing

The Federal Home Loan Banks, Community Investment, and Affordable Housing John Stocchetti Executive Vice President Federal Home Loan Bank of Chicago March 26, 2012 Today s Presentation Introduction to

The Federal Home Loan Banks, Community Investment, and Affordable Housing John Stocchetti Executive Vice President Federal Home Loan Bank of Chicago March 26, 2012 Today s Presentation Introduction to

Access and Sustainability for First Time Homebuyers: The Evolving Role of State Housing Finance Agencies

Joint Center for Housing Studies Harvard University Access and Sustainability for First Time Homebuyers: The Evolving Role of State Housing Finance Agencies Stephanie Moulton The Ohio State University

Joint Center for Housing Studies Harvard University Access and Sustainability for First Time Homebuyers: The Evolving Role of State Housing Finance Agencies Stephanie Moulton The Ohio State University

Federal Reserve Monetary Policy

Federal Reserve Monetary Policy To prevent recession, earlier this decade the Federal Reserve s monetary policy pushed down the short-term interest rate to just 1%, the lowest level for many decades. Long-term

Federal Reserve Monetary Policy To prevent recession, earlier this decade the Federal Reserve s monetary policy pushed down the short-term interest rate to just 1%, the lowest level for many decades. Long-term

REAL ESTATE REPORT 3RD QUARTER 2015 SOURCES: BUFFINI & COMPANY,

REAL ESTATE REPORT 3RD QUARTER 2015 SOURCES: BUFFINI & COMPANY, INDUSTRY FACTS MEDIAN DAYS ON THE MARKET: 39 Days in April 2015 vs. Home sales in April reached a seasonally adjusted rate of 5.04 million,

REAL ESTATE REPORT 3RD QUARTER 2015 SOURCES: BUFFINI & COMPANY, INDUSTRY FACTS MEDIAN DAYS ON THE MARKET: 39 Days in April 2015 vs. Home sales in April reached a seasonally adjusted rate of 5.04 million,

PIMA COUNTY COMMUNITY LAND TRUST HOME BUYER SELECTION POLICIES & PROCEDURES

PIMA COUNTY COMMUNITY LAND TRUST HOME BUYER SELECTION POLICIES & PROCEDURES I. OVERVIEW This policy paper is intended to guide the development and implementation of both general and projectspecific homebuyer

PIMA COUNTY COMMUNITY LAND TRUST HOME BUYER SELECTION POLICIES & PROCEDURES I. OVERVIEW This policy paper is intended to guide the development and implementation of both general and projectspecific homebuyer

THE FIVE-POINT PLAN. Refocusing the Future of Minority Homeownership

THE FIVE-POINT PLAN Refocusing the Future of Minority Homeownership The Asian Real Estate Association of America (AREAA), the National Association of Hispanic Real Estate Professionals (NAHREP), and the

THE FIVE-POINT PLAN Refocusing the Future of Minority Homeownership The Asian Real Estate Association of America (AREAA), the National Association of Hispanic Real Estate Professionals (NAHREP), and the

The Wealth Building Home Loan: A Straight, Broad Highway to Greater Wealth for Low- and Middle-Income Households

The Wealth Building Home Loan: A Straight, Broad Highway to Greater Wealth for Low- and Middle-Income Households Stephen Oliner and Edward Pinto American Enterprise Institute Presented at NYU Stern Center

The Wealth Building Home Loan: A Straight, Broad Highway to Greater Wealth for Low- and Middle-Income Households Stephen Oliner and Edward Pinto American Enterprise Institute Presented at NYU Stern Center

Mortgage Alternatives: The Risks and Opportunities 1

Fact Sheet HE 3226 Mortgage Alternatives: The Risks and Opportunities 1 Virginia Peart, Ph.D. 2 Buying a home involves a difficult decision process. Today s mortgages are complex, and homeownership is

Fact Sheet HE 3226 Mortgage Alternatives: The Risks and Opportunities 1 Virginia Peart, Ph.D. 2 Buying a home involves a difficult decision process. Today s mortgages are complex, and homeownership is

HOME AFFORDABLE MODIFICATION PROGRAM BASE NET PRESENT VALUE (NPV) MODEL SPECIFICATIONS

MODEL SPECIFICATIONS") Overview HOME AFFORDABLE MODIFICATION PROGRAM BASE NET PRESENT VALUE (NPV) MODEL SPECIFICATIONS As a part of the Making Home Affordable Program, we are providing standardized guidance and a base net present

Overview HOME AFFORDABLE MODIFICATION PROGRAM BASE NET PRESENT VALUE (NPV) MODEL SPECIFICATIONS As a part of the Making Home Affordable Program, we are providing standardized guidance and a base net present

A Privatized U.S. Mortgage Market

A Privatized U.S. Mortgage Market Dwight Jaffee Haas School of Business University of California, Berkeley Presented to Conference on The GSEs, Housing, and The Economy Reagan Center, Washington DC, January

A Privatized U.S. Mortgage Market Dwight Jaffee Haas School of Business University of California, Berkeley Presented to Conference on The GSEs, Housing, and The Economy Reagan Center, Washington DC, January

The City of MIDWEST CITY GRANTS MANAGEMENT DEPARTMENT Terri L. Craft, Grants Manager. MIDWEST CITY Homebuyer Assistance Program

The City of MIDWEST CITY GRANTS MANAGEMENT DEPARTMENT Terri L. Craft, Grants Manager Grant Amount: $5,000.00 MIDWEST CITY Homebuyer Assistance Program The Homebuyer Assistance Program promotes homeownership

The City of MIDWEST CITY GRANTS MANAGEMENT DEPARTMENT Terri L. Craft, Grants Manager Grant Amount: $5,000.00 MIDWEST CITY Homebuyer Assistance Program The Homebuyer Assistance Program promotes homeownership

We can now say that our loan products can meet the full spectrum of homebuyers to those who meet the qualifications.

Rhode Island Housing Rhode Island Housing mortgages: More than just for first-time homebuyers Homeownership: Empowering New Buyers Page 1 of 3 Rhode Island Housing Mortgages: More than just for first-time

Rhode Island Housing Rhode Island Housing mortgages: More than just for first-time homebuyers Homeownership: Empowering New Buyers Page 1 of 3 Rhode Island Housing Mortgages: More than just for first-time

Homebuyer Program Orientation

Homebuyer Program Orientation 1405 E. McDowell Rd, Suite 100 Phoenix, Arizona 85006 Telephone: (602) 258-1659 1 Website: www.nhsphoenix.org History of NHS Phoenix NHS Phoenix was founded in 1975 and is

Homebuyer Program Orientation 1405 E. McDowell Rd, Suite 100 Phoenix, Arizona 85006 Telephone: (602) 258-1659 1 Website: www.nhsphoenix.org History of NHS Phoenix NHS Phoenix was founded in 1975 and is

Michigan State Housing Development Authority. Office of Community Development MSHDA MISSION

Michigan State Housing Development Authority Office of Community Development MSHDA MISSION The Michigan State Housing Development Authority (MSHDA) provides financial and technical assistance through public

Michigan State Housing Development Authority Office of Community Development MSHDA MISSION The Michigan State Housing Development Authority (MSHDA) provides financial and technical assistance through public

Homeownership in the Inland Empire Past, Present, and Future. Brought to you by:

Homeownership in the Inland Empire Past, Present, and Future Brought to you by: The Real Estate Roller Coaster The Subject : The Average Home The Date : July 2002 The Place : Total Monthly Sales: 419 Riverside

Homeownership in the Inland Empire Past, Present, and Future Brought to you by: The Real Estate Roller Coaster The Subject : The Average Home The Date : July 2002 The Place : Total Monthly Sales: 419 Riverside

California Home Finance Authority (CHF)

") Presentation for Real Estate Professionals California Home Finance Authority (CHF) 1215 K Street, Suite 1650, Sacramento, CA 95814 www.chfloan.org (855) 740-8422 Often first point of contact for a new

Presentation for Real Estate Professionals California Home Finance Authority (CHF) 1215 K Street, Suite 1650, Sacramento, CA 95814 www.chfloan.org (855) 740-8422 Often first point of contact for a new

Down Payment & Closing Cost Assistance Programs & Primary Mortgage Lender Guidelines

437 S. Jackson St. Green Bay, WI 54301 920-448-3075 www.nwgreenbay.org Down Payment & Closing Cost Assistance Programs & Primary Mortgage Lender Guidelines Housing Counselors: Jeff Van Rens Belinda Pynenberg

437 S. Jackson St. Green Bay, WI 54301 920-448-3075 www.nwgreenbay.org Down Payment & Closing Cost Assistance Programs & Primary Mortgage Lender Guidelines Housing Counselors: Jeff Van Rens Belinda Pynenberg

Joplin Homebuyer s Assistance Program (J-HAP)

") Joplin Homebuyer s Assistance Program (J-HAP) Community Development Block Grant Disaster Recovery (CDBG-DR) Program City of Joplin, Missouri HOMEBUYER ASSISTANCE AGREEMENT THIS AGREEMENT, entered into

Joplin Homebuyer s Assistance Program (J-HAP) Community Development Block Grant Disaster Recovery (CDBG-DR) Program City of Joplin, Missouri HOMEBUYER ASSISTANCE AGREEMENT THIS AGREEMENT, entered into

Housing Tax Credit Essentials

Housing Tax Credit Essentials 1 Background Part of 1986 Tax Reform to encourage the construction and rehabilitation of low-income rental housing Contained in Section 42 of the tax code Emphasis on private

Housing Tax Credit Essentials 1 Background Part of 1986 Tax Reform to encourage the construction and rehabilitation of low-income rental housing Contained in Section 42 of the tax code Emphasis on private

The GSEs Are Helping to Stabilize an Unstable Mortgage Market

Update on the Single-Family Credit Guarantee Business Rick Padilla Director, Corporate Relations & Housing Outreach The Changing Economy: The New Community Lending Environment June 1, 29 The GSEs Are Helping

Update on the Single-Family Credit Guarantee Business Rick Padilla Director, Corporate Relations & Housing Outreach The Changing Economy: The New Community Lending Environment June 1, 29 The GSEs Are Helping

The Coordinated Plan. to Address Foreclosures in Minnesota

The Coordinated Plan to Address Foreclosures in Minnesota An overview of the Goals, Strategies, and Successes of the Minnesota Foreclosure Partners Council September 2010 The Crisis The number of mortgage

The Coordinated Plan to Address Foreclosures in Minnesota An overview of the Goals, Strategies, and Successes of the Minnesota Foreclosure Partners Council September 2010 The Crisis The number of mortgage

Homeownership. b y B R A D S H U ST E R

INDUSTRY TRENDS Millennials AND Homeownership b y B R A D S H U ST E R Homeownership is not as out of reach as millennials may think. Many misperceptions abound that the industry could help dispel. In

INDUSTRY TRENDS Millennials AND Homeownership b y B R A D S H U ST E R Homeownership is not as out of reach as millennials may think. Many misperceptions abound that the industry could help dispel. In

Appendix 11: AFFORDABLE HOUSING TERMS & CRITERIA

Appendix 11: AFFORDABLE HOUSING TERMS & CRITERIA (Provided by the Southampton Housing Authority March 18, 2013) What is Affordable Housing? There are a number of definitions of affordable housing as federal

Appendix 11: AFFORDABLE HOUSING TERMS & CRITERIA (Provided by the Southampton Housing Authority March 18, 2013) What is Affordable Housing? There are a number of definitions of affordable housing as federal

Exiting Homeownership: The Influences of Transfers on Exits from Owner-Occupied Housing in the United States

Exiting Homeownership: The Influences of Transfers on Exits from Owner-Occupied Housing in the United States University of Wisconsin-Madison IRP Seminar, March 29 2012 Outline 1 2 3 4 Exiting Do Subsidies/Transfers

Exiting Homeownership: The Influences of Transfers on Exits from Owner-Occupied Housing in the United States University of Wisconsin-Madison IRP Seminar, March 29 2012 Outline 1 2 3 4 Exiting Do Subsidies/Transfers

Dr. Debra Sherrill Central Piedmont Community College

Dr. Debra Sherrill Central Piedmont Community College 1 2 Describe the benefits and pitfalls of renting versus owning a home. List the steps required to obtain a mortgage loan. Identify mortgage options

Dr. Debra Sherrill Central Piedmont Community College 1 2 Describe the benefits and pitfalls of renting versus owning a home. List the steps required to obtain a mortgage loan. Identify mortgage options

Faculty and Staff Home Buyer s Guide

Faculty and Staff Home Buyer s Guide Table of contents Welcome Welcome Should I buy or rent? Renting vs. Buying Comparison Pre-approval Process Mortgage Programs 3 4 5 6 7 The University Housing & Relocation

Faculty and Staff Home Buyer s Guide Table of contents Welcome Welcome Should I buy or rent? Renting vs. Buying Comparison Pre-approval Process Mortgage Programs 3 4 5 6 7 The University Housing & Relocation

About Northwest Counseling Service

About Northwest Counseling Service Non Profit Agency No Cost Housing Counseling Services Any Service Related To A Home Specialize In Mortgage Delinquency 96% Rate In Keeping Residents In Homes HUD Certified/OHCD

About Northwest Counseling Service Non Profit Agency No Cost Housing Counseling Services Any Service Related To A Home Specialize In Mortgage Delinquency 96% Rate In Keeping Residents In Homes HUD Certified/OHCD

ILLINOIS ASSOCIATION OF REALTORS HOUSING POLICY

ILLINOIS ASSOCIATION OF REALTORS HOUSING POLICY ILLINOIS ASSOCIATION OF REALTORS HOUSING POLICY As an Association, we reaffirm our commitment to the goal of decent housing and a suitable living environment

ILLINOIS ASSOCIATION OF REALTORS HOUSING POLICY ILLINOIS ASSOCIATION OF REALTORS HOUSING POLICY As an Association, we reaffirm our commitment to the goal of decent housing and a suitable living environment

RURAL HOUSING SERVICE

For release only by The Committee on Appropriations RURAL HOUSING SERVICE Statement of Tony Hernandez, Administrator Before the Subcommittee on Agriculture, Rural Development, Food and Drug Administration,

For release only by The Committee on Appropriations RURAL HOUSING SERVICE Statement of Tony Hernandez, Administrator Before the Subcommittee on Agriculture, Rural Development, Food and Drug Administration,

Guide to Fair Mortgage Lending and Home Preservation

Guide to Fair Mortgage Lending and Home Preservation Fair Housing Legal Support Center & Clinic Guide to Fair Mortgage Lending and Home Preservation What does this guide cover? What is Fair Lending? What

Guide to Fair Mortgage Lending and Home Preservation Fair Housing Legal Support Center & Clinic Guide to Fair Mortgage Lending and Home Preservation What does this guide cover? What is Fair Lending? What

MSHDA s Homeownership Counseling Program. Sharon Evans Homeownership Division May 24, 2011

MSHDA s Homeownership Counseling Program Sharon Evans Homeownership Division May 24, 2011 The Homeownership Counseling Program supports the Michigan State Housing Development Authority s (MSHDA) mortgage

MSHDA s Homeownership Counseling Program Sharon Evans Homeownership Division May 24, 2011 The Homeownership Counseling Program supports the Michigan State Housing Development Authority s (MSHDA) mortgage

How Subsidized Rents are Set: Area Median Incomes and Fair Markets Rents

How Subsidized Rents are Set: Area Median Incomes and Fair Markets Rents Many NMHC and NAA members own and/or operate apartment communities that provide affordable housing throughout the country using

How Subsidized Rents are Set: Area Median Incomes and Fair Markets Rents Many NMHC and NAA members own and/or operate apartment communities that provide affordable housing throughout the country using

4 HOUR NONTRADITIONAL MORTGAGE TYPES

NMLS Approved Provider ID 1400051 353 West 48th St, Suite 333, New York, NY 10036 4 HOUR NONTRADITIONAL MORTGAGE TYPES Course Approval: 1156/1008/1699 Course Material Date: 10/26/2015 Course Approval Date:

NMLS Approved Provider ID 1400051 353 West 48th St, Suite 333, New York, NY 10036 4 HOUR NONTRADITIONAL MORTGAGE TYPES Course Approval: 1156/1008/1699 Course Material Date: 10/26/2015 Course Approval Date:

Homebuyers Guide Homeownership Program

Homebuyers Guide Homeownership Program s:\housing\homeownership\marketing\website\manuals\buyer-guide.docx 2 Table of Contents Welcome!... 3 Programs Summary... 4 Homeworks Permanently Affordable Program

Homebuyers Guide Homeownership Program s:\housing\homeownership\marketing\website\manuals\buyer-guide.docx 2 Table of Contents Welcome!... 3 Programs Summary... 4 Homeworks Permanently Affordable Program

Homeownership. Your First Steps toward. Getting Started. Know Your Finances. Which Mortgage Is Right for You?

Your First Steps toward Homeownership Identify the type of mortgage that meets your specific financial needs Getting Started Many people don t consider buying a home because they re afraid they can t afford

Your First Steps toward Homeownership Identify the type of mortgage that meets your specific financial needs Getting Started Many people don t consider buying a home because they re afraid they can t afford

Steven Young, Jr's. REAL ESTATE REPORT WINTER 2015

Steven Young, Jr's. REAL ESTATE REPORT WINTER 2015 Steven Young, Jr's Real Estate Report PAGE 1 INDUSTRY FACTS MEDIAN DAYS ON THE MARKET: 56 Days in September 2014 Existing home sales in September increased

Steven Young, Jr's. REAL ESTATE REPORT WINTER 2015 Steven Young, Jr's Real Estate Report PAGE 1 INDUSTRY FACTS MEDIAN DAYS ON THE MARKET: 56 Days in September 2014 Existing home sales in September increased

Request for Information: Enterprise/FHA REO Asset Disposition

Request for Information: Enterprise/FHA REO Asset Disposition The Federal Housing Finance Agency (FHFA), in consultation with the U.S. Department of the Treasury and the U.S. Department of Housing and

Request for Information: Enterprise/FHA REO Asset Disposition The Federal Housing Finance Agency (FHFA), in consultation with the U.S. Department of the Treasury and the U.S. Department of Housing and

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410 Written Testimony of Carol Galante Assistant Secretary for Housing/Federal Housing Administration Commissioner U.S. Department of Housing

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410 Written Testimony of Carol Galante Assistant Secretary for Housing/Federal Housing Administration Commissioner U.S. Department of Housing

PROGRAM DESCRIPTION FY 2007 ANNUAL PROGRAM PERFORMANCE MEASURES. APPROPRIATION UNIT: Michigan State Housing Development Authority Date:02/12/08

PROGRAM DESCRIPTION FY 2007 ANNUAL PROGRAM PERFORMANCE MEASURES DEPARTMENT: Michigan Department of Labor & Economic Growth APPROPRIATION UNIT: Michigan State Housing Development Authority Date:02/12/08

PROGRAM DESCRIPTION FY 2007 ANNUAL PROGRAM PERFORMANCE MEASURES DEPARTMENT: Michigan Department of Labor & Economic Growth APPROPRIATION UNIT: Michigan State Housing Development Authority Date:02/12/08

HOMEOWNERSHIP HOMEOWNERSHIP TRENDS NEIGHBORHOOD LOSSES JOINT CENTER FOR HOUSING STUDIES OF HARVARD UNIVERSITY

4 HOMEOWNERSHIP The downtrend in homeownership stretched to a decade in 214. Rates fell across nearly all age groups, incomes, household types, and markets despite the affordability of first-time homebuying.

4 HOMEOWNERSHIP The downtrend in homeownership stretched to a decade in 214. Rates fell across nearly all age groups, incomes, household types, and markets despite the affordability of first-time homebuying.

Salt Lake Housing Forecast

2015 Salt Lake Housing Forecast A Sustainable Housing Market By James Wood Director of the Bureau of Economic and Business Research Commissioned by the Salt Lake Board of REALTORS By year-end 2013 home

2015 Salt Lake Housing Forecast A Sustainable Housing Market By James Wood Director of the Bureau of Economic and Business Research Commissioned by the Salt Lake Board of REALTORS By year-end 2013 home

Homeownership HOMEOWNERSHIP TRENDS JOINT CENTER FOR HOUSING STUDIES OF HARVARD UNIVERSITY

4 Homeownership The national homeownership rate marked its ninth consecutive year of decline in 213, affecting most segments of the population. The drop among minorities is particularly troubling, given

4 Homeownership The national homeownership rate marked its ninth consecutive year of decline in 213, affecting most segments of the population. The drop among minorities is particularly troubling, given

GLOSSARY OF TERMS. Amortization Repayment of a debt in regular installments of principal and interest, rather than interest only payments

GLOSSARY OF TERMS Ability to Repay (ATR) The Ability to Repay rule protects consumers from taking on mortgages that exceed their financial means, by mandating the documentation / proof of income and assets.

GLOSSARY OF TERMS Ability to Repay (ATR) The Ability to Repay rule protects consumers from taking on mortgages that exceed their financial means, by mandating the documentation / proof of income and assets.

A mortgage is a loan that is used to finance the purchase of your home. It consists of 5 parts: collateral, principal, interest, taxes, and insurance.

A mortgage is a loan that is used to finance the purchase of your home. It consists of 5 parts: collateral, principal, interest, taxes, and insurance. When you agree to a mortgage, you enter into a legal

A mortgage is a loan that is used to finance the purchase of your home. It consists of 5 parts: collateral, principal, interest, taxes, and insurance. When you agree to a mortgage, you enter into a legal

Financing Residential Real Estate: SAFE Comprehensive 20 Hours

Financing Residential Real Estate: SAFE Comprehensive 20 Hours COURSE ORGANIZATION and DESIGN Roy L. Ponthier, Ph.D., Ed.D., CDEI, DREI Executive Director Module 1: Finance and Investment Mortgage loans

Financing Residential Real Estate: SAFE Comprehensive 20 Hours COURSE ORGANIZATION and DESIGN Roy L. Ponthier, Ph.D., Ed.D., CDEI, DREI Executive Director Module 1: Finance and Investment Mortgage loans

Lesson 8 Section 143 Qualified Mortgage Bonds

Lesson 8 Overview Introduction In Phase I, Lesson 4, you learned about the private activity bond tests, including the consumer loan test. Lesson 4 of Phase II discussed the various types of exempt facility

Lesson 8 Overview Introduction In Phase I, Lesson 4, you learned about the private activity bond tests, including the consumer loan test. Lesson 4 of Phase II discussed the various types of exempt facility

Loan Foreclosure Analysis and Comparison. A Briefing To The Housing Committee March 3, 2008

Loan Foreclosure Analysis and Comparison A Briefing To The Housing Committee March 3, 2008 Purpose To determine the cause of the Subprime mortgage crisis which was triggered by a sharp rise in home foreclosures

Loan Foreclosure Analysis and Comparison A Briefing To The Housing Committee March 3, 2008 Purpose To determine the cause of the Subprime mortgage crisis which was triggered by a sharp rise in home foreclosures

Chapter 19. Residential Real Estate Finance: Mortgage Choices, Pricing and Risks. Residential Financing: Loans

Chapter 19 Residential Real Estate Finance: Mortgage Choices, Pricing and Risks 10/25/2005 FIN4777 - Special Topics in Real Estate - Professor Rui Yao 1 Residential Financing: Loans Loans are classified

Chapter 19 Residential Real Estate Finance: Mortgage Choices, Pricing and Risks 10/25/2005 FIN4777 - Special Topics in Real Estate - Professor Rui Yao 1 Residential Financing: Loans Loans are classified

U.S. and Regional Housing Markets

U.S. and Regional Housing Markets House Prices Boom, Bust and Rebound Index, 1991: Q1=1* 3 CoreLogic house price index Real FHFA house price index 25 2 15 1 5 1991 199 1997 2 23 26 29 212 215 *Seasonally

U.S. and Regional Housing Markets House Prices Boom, Bust and Rebound Index, 1991: Q1=1* 3 CoreLogic house price index Real FHFA house price index 25 2 15 1 5 1991 199 1997 2 23 26 29 212 215 *Seasonally

Virginia Housing Development Authority

Virginia Housing Development Authority CFED s Asset & Opportunity Institute Workshop September 23, 2009 Michele Watson, Director of Homeownership Programs About VHDA The General Assembly established VHDA

Virginia Housing Development Authority CFED s Asset & Opportunity Institute Workshop September 23, 2009 Michele Watson, Director of Homeownership Programs About VHDA The General Assembly established VHDA

CFPB FINAL RULES SUN WEST IMPLEMENTATION GUIDE

CFPB FINAL RULES SUN WEST IMPLEMENTATION GUIDE January 02, 2015 In case of any queries regarding the information available in this guide, please reach us at qmteam@swmc.com. Sun West Mortgage Company,

CFPB FINAL RULES SUN WEST IMPLEMENTATION GUIDE January 02, 2015 In case of any queries regarding the information available in this guide, please reach us at qmteam@swmc.com. Sun West Mortgage Company,

Mortgage Lending During the Great Recession: HMDA 2009

F U R M A N C E N T E R F O R R E A L E S T A T E & U R B A N P O L I C Y N E W Y O R K U N I V E R S I T Y S C H O O L O F L AW WA G N E R S C H O O L O F P U B L I C S E R V I C E N O V E M B E R 2 0

F U R M A N C E N T E R F O R R E A L E S T A T E & U R B A N P O L I C Y N E W Y O R K U N I V E R S I T Y S C H O O L O F L AW WA G N E R S C H O O L O F P U B L I C S E R V I C E N O V E M B E R 2 0

Q. What are the terms of the NeighborhoodLIFT funding?

Frequently Asked Questions: Q. What are the terms of the NeighborhoodLIFT funding? A. NeighborhoodLIFT funds are provided as a 5 year forgivable loan program for owner occupied properties. As long as the

Frequently Asked Questions: Q. What are the terms of the NeighborhoodLIFT funding? A. NeighborhoodLIFT funds are provided as a 5 year forgivable loan program for owner occupied properties. As long as the

LOW-INCOME HOUSING TAX CREDIT PROGRAM OVERVIEW

LOW-INCOME HOUSING TAX CREDIT PROGRAM OVERVIEW September 2015 TAX CREDIT OVERVIEW The credit is a 10-year tax incentive to encourage the development of residential rental housing at or below 60% of area

LOW-INCOME HOUSING TAX CREDIT PROGRAM OVERVIEW September 2015 TAX CREDIT OVERVIEW The credit is a 10-year tax incentive to encourage the development of residential rental housing at or below 60% of area

SHARED EQUITY HOUSING IMPLEMENTATION IN TEXAS A WHITE PAPER FROM HOMEBASE & AUSTIN HABITAT FOR HUMANITY, SPONSORED BY CITI FOUNDATION

SHARED EQUITY HOUSING IMPLEMENTATION IN TEXAS A WHITE PAPER FROM HOMEBASE & AUSTIN HABITAT FOR HUMANITY, SPONSORED BY CITI FOUNDATION JANUARY 2014 INTRODUCTION In its most efficient form, homeownership

SHARED EQUITY HOUSING IMPLEMENTATION IN TEXAS A WHITE PAPER FROM HOMEBASE & AUSTIN HABITAT FOR HUMANITY, SPONSORED BY CITI FOUNDATION JANUARY 2014 INTRODUCTION In its most efficient form, homeownership