How to achieve quality retirement outcomes for your members

|

|

|

- Hilary Price

- 8 years ago

- Views:

Transcription

1 How to achieve quality retirement outcomes for your members Speakers Andrew Pennie, Marketing Director, Intelligent Pensions Steve Patterson, Managing Director, Intelligent Pensions Chair John Moret, Chairman, Intelligent Pensions

2 George s Big Budget Announcement

3 How to achieve quality retirement outcomes for your members Pension decumulation is changing with annuities no longer the standard default Retirees will have more choice and increased flexibility over how they take their pension benefits and will need more support and guidance in the run up to retirement What does a quality outcome look like where the traditional 'cash + annuity option is not suitable? What are the key decision points and actions that drive quality outcomes? Fulfilling your obligations as trustees under the DC code

4 FCA s Risk Outlook for 2014 The decumulation phase of retirement income can cause risks to consumer outcomes over the long term. While recent proposals for pension reform plan to allow consumers to access any amount of their pension pot at age 55, the need for consumers to understand the options available to them at retirement is still paramount.

5 A global look at retirement and decumulation.. Andrew Pennie Intelligent Pensions

6 George Osborne s Budget Pensioners will have complete freedom to draw down as much or as little of their pension pot as they want, anytime they want. No caps. No drawdown limits. Let me be clear. No one will have to buy an annuity.

7 Options under DC pension liberalisation

8 Intelligent Pensions DC Pension Survey findings.. Annuity Purchase Historic Annuity Purchase post reforms Other 6% Annuity 94% Other 67% Annuity 33% Annuity Other Annuity Other Forecasting a fall in the number of members buying an annuity at retirement to 33%. But 92% currently using a de-risking (annuity) default investment strategy!

9

10

11 Schematic of the global annuity market

12 Annuity rates in the UK...

13 Options under DC pension liberalisation

14 The retirement planning fundamentals have not changed... How much can I afford to spend to live life today and have the peace of mind to have enough for all my tomorrows?

15 The longevity problem...

16 Distribution of death given (male) age now...

17

18

19 Will UK retirees blow their pension funds?

20 Australia: Risk of running out of money 20 years of compulsory pension contributions Annuity market share very small: 4% in 2012 But up from 0.2% in % took full pension withdrawal in early years Down to 50% now Of those, 25% have spent all pension savings by 70 But a lack of tax barriers for withdrawal and means-tested benefits encourages spending Fresh calls for restricting access to pensions

21

22 Intelligent Pensions DC Pension Survey findings: Top 3 challenges for better outcomes % of Respondents Lack of member engagement Lack of information about members' individual needs and objectives Delivering alternative investment options to match the new retirement choices. Timing of guidance guarantee (is 6 months before retirement too late?) External market conditions (e.g. falling annuity rates) Cost of delivering effective member support services and solutions

23 Engagement is vital to deliver better outcomes... Everybody s retirement will be different A more personalised and hands-on approach is required Guidance guarantee is positive but key decisions need to be taken years before delivery The UK is playing catch-up in many aspects of accumulation and decumulation particularly engagement.

24 How to achieve quality retirement outcomes for your members Speakers Andrew Pennie, Marketing Director Intelligent Pensions Steve Patterson, Managing Director Intelligent Pensions Chair John Moret, Chairman Intelligent Pensions

25 How to achieve quality retirement outcomes for your members When should DC members start considering their decumulation options? What factors should be considered? How would a drawdown exit strategy impact on asset allocation in the years approaching retirement? Most scheme members are in default investment strategies These are almost always predicated on the traditional cash + annuity option

26 Helping Members In The Run Up To Retirement Steve Patterson Intelligent Pensions

27 Retirement Means Different Things To Different People...

28 TPR s Retirement Communications Timeline

29 TPR s Retirement Communications Timeline Member support through new Guidance Guarantee

30 TPR s Retirement Communications Timeline Education and warm up but retirement still remote

31 TPR s Retirement Communications Timeline This is the period when members need to seriously consider their retirement options

32 TPR s Retirement Communications Timeline This is the period when members need to seriously consider their retirement options and look ahead to their financial future?

33 The Four Stages of Pension Decumulation 1. Our Annuity or Not online tool to help members assess several years ahead of retirement which option will be most suitable a) Cash + Annuity (or full cash out decision closer to retirement = guidance guarantee) b) Cash + Pension Drawdown c) Cash + Annuity + Drawdown d) Phased cash + phased annuity and/or drawdown 2. For those for whom the traditional cash + annuity or cash out option is unlikely to be suitable individual analysis and guidance Including guidance on the investment strategy in the years running up to retirement 3. Implementation of the at retirement solution 4. Ongoing management until all benefits are ultimately secured under annuities The Intelligent Pensions Solution

34 Our Annuity or Not tool involves 5 simple steps giving a RED, AMBER or GREEN result

35 For AMBER or RED outputs members are invited to book a free online consultation

36 INTELLIGENT PENSIONS analysis helping members look ahead

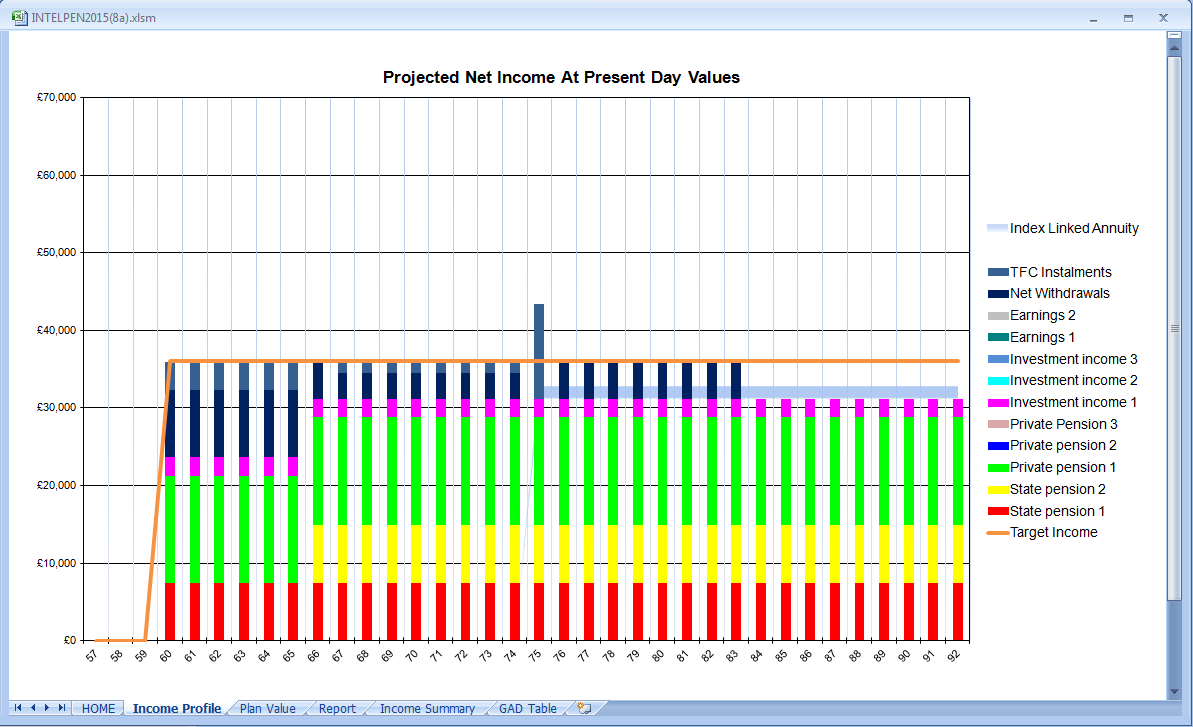

37 CASE STUDY Louise Bolan Louise is 57 and a member of he employer s DC scheme Her husband, Donald, works in Local Government and is 62, planning to retire at 65 Louise wants to know if she can give up work at 60 and, if she does, whether she should take an annuity or adopt the new flexi-access pension option announced in the Budget She feels that annuity rates are unattractive at present and likes the idea of being able to take out as much or little as she needs She and Donald have run stocks and shares ISA accounts for many years and she is quite comfortable about taking investment risk although she doesn t see herself as a gambler She decides to complete the Annuity or NOT online tool...

38

39

40

41

42

43 CASE STUDY Louise Bolan Having run the tool Louise sees that an annuity may not be the right option She is keen to explore the matter further and decides to book a free online consultation She completes a simple booking request and submits this to Intelligent Pensions She receives a call back within an hour from a retirement analyst at Intelligent Pensions to make the arrangements As Louise wants her husband to participate the consultation is booked for an evening Within a few minutes Louise receives a confirmation , which includes a request to return some basic financial information in advance of the appointment

44

45 15,000 80,000 7,500 7,500 20, ,000 60,000

46

47

48

49

50

51

52

53

54

55

56

57 CASE STUDY Louise Bolan As a result of the online consultation Louise and Donald were convinced that pension drawdown was the best option for Louise s DC benefits Donald asked what impact this would have on the current investment strategy for Louise s fund Louise said she had checked and she was still in her original default strategy which was based on retiring at 60 and was now 20% in cash, 50% in gilts, and 30% in a UK FTSE ALL Share tracker In their follow up report Intelligent Pensions said the level of equity exposure was too low, and that based on the analysis and Louise s personal risk profile this should be increased to 70%, with the balance being in a mix of property and fixed interest with the emphasis on corporate bond rather than gilts Louise is now looking at the alternative funds available

58 What Affects The Recommended Investment Mix? Risk profile Age Attitude to risk Dependency Benefit shape Cash flow analysis informs the strategy Early years are critical Defensive holdings essential Main portfolio risk graded balance of risk adjusted over time Lastly stress tested to assess capacity for loss (and continuously retested annually thereafter)

59

60 What Does The Pensions Regulator Expect? Trustees will clearly communicate to members the options available at retirement in a way which supports them in choosing the option most appropriate to their circumstances. Trustees should make members aware of the range of ways in which they can receive their retirement income. Communications to members should clearly describe these options and the importance of members making choices tailored to their own circumstances. Trustees should consider communicating with members between two and five years before retirement about their retirement options and encourage them to start considering these. Due to the complexity of the decisions that members need to take at retirement, trustees should emphasise the importance and advantages of taking financial advice in all of their retirement communications.

61 Talking to your employees about pensions a guide for employers (TPR & FCA) Question: How can I help my employees when they ask me which investment funds to choose for their pension? Suggest that members check what type of fund they invest in and decide whether it is appropriate for their circumstances (for example, many schemes offer a range of funds with different levels of risk), and explain that it is important that members regularly review the funds they are invested in. Suggest that employees consider seeing a financial adviser authorised by the FSA Question: What could I be doing when employees approach their retirement dates? Consider providing access to an adviser. The cost of this advice (up to 150 an employee each tax year) is not classed as a benefit-in-kind for employees, as long as it relates only to pensions and is not general financial and tax advice.

62 Pathways to Retirement Andrew Pennie Intelligent Pensions

63 Intelligent Pensions Pathways Service Available to all employees when they are within 5 years of scheme pension age Rolling 12 month service contract with employer Online Annuity or Not tool supplied free of charge Members with RED or AMBER outcome have option to receive a free online consultation with a qualified Retirement Analyst And a follow up report including copy of online analysis and suggested equity exposure for scheme fund choice Guidance is purely generic no product recommendations Charged at 150 per member session Maximum member sessions 1 per year

64 Pathways to Retirement

65 Pathways to Retirement Drawdown Annuity

66 TO FIND OUT MORE ABOUT OUR PATHWAYS SERVICE, VIEW OUR ONLINE TOOLS OR SEE A DEMONSTRATION OF OUR ONLINE ANALYSIS VISIT US AT STAND 402 INTELLIGENT PENSIONS LTD. AUTHORISED AND REGULATED BY THE FINANCIAL CONDUCT AUTHORITY

67

How can you help your employees get. pension world? Andrew Pennie May 2015

How can you help your employees get the best retirement outcome in the new pension world? Andrew Pennie May 2015 Pension freedoms.. Come with... Pension decumulation.. Decumulation vvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvv

How can you help your employees get the best retirement outcome in the new pension world? Andrew Pennie May 2015 Pension freedoms.. Come with... Pension decumulation.. Decumulation vvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvv

Investment Association response to the FCA s Retirement income market study: Interim Report

Investment Association response to the FCA s Retirement income market study: Interim Report 30 th January 2015 General comments 1. The Investment Association 1 is a long-standing supporter of greater flexibility

Investment Association response to the FCA s Retirement income market study: Interim Report 30 th January 2015 General comments 1. The Investment Association 1 is a long-standing supporter of greater flexibility

A new toolbox for retirement planning

Insights A new toolbox for retirement planning Part 1: Risk measurement: an essential tool for retirement income planning This is an updated version of a report first presented at Barrie & Hibbert s Retirement

Insights A new toolbox for retirement planning Part 1: Risk measurement: an essential tool for retirement income planning This is an updated version of a report first presented at Barrie & Hibbert s Retirement

Basic Guide to Retirement Income Options

Basic Guide to Retirement Income Options Can I afford to retire? Which retirement income solution is best for me? Should I take all my tax-free cash entitlement? Will my family benefit from my pension

Basic Guide to Retirement Income Options Can I afford to retire? Which retirement income solution is best for me? Should I take all my tax-free cash entitlement? Will my family benefit from my pension

How to... Help your clients use their pensions freedom wisely

How to... Help your clients use their pensions freedom wisely How To Guide Introduction The new pension freedoms that came into effect in April 2015, may, at first, seem like a very attractive prospect.

How to... Help your clients use their pensions freedom wisely How To Guide Introduction The new pension freedoms that came into effect in April 2015, may, at first, seem like a very attractive prospect.

Preparing for 6 April 2015 Are you ready for Question Time?

Are you ready for Question Time? Background The new flexible pension regime will come into effect on 6 April 2015 There is already extensive press coverage of the changes In understanding the changes it

Are you ready for Question Time? Background The new flexible pension regime will come into effect on 6 April 2015 There is already extensive press coverage of the changes In understanding the changes it

Your guide to the investment changes

Your guide to the investment changes This announcement sets out changes to both the Lifecycle Strategy and Freechoice fund range. Please read it carefully. A quick reminder of how the Scheme works Every

Your guide to the investment changes This announcement sets out changes to both the Lifecycle Strategy and Freechoice fund range. Please read it carefully. A quick reminder of how the Scheme works Every

A BETTER RETIREMENT PORTFOLIO FOR MEMBERS IN DC INVESTMENT DEFAULTS

A BETTER RETIREMENT PORTFOLIO FOR MEMBERS IN DC INVESTMENT DEFAULTS JUNE 2014 TALENT HEALTH RETIREMENT INVESTMENTS EXECUTIVE SUMMARY The majority of defined contribution (DC) plan members typically end

A BETTER RETIREMENT PORTFOLIO FOR MEMBERS IN DC INVESTMENT DEFAULTS JUNE 2014 TALENT HEALTH RETIREMENT INVESTMENTS EXECUTIVE SUMMARY The majority of defined contribution (DC) plan members typically end

For professional investors and advisors only. Not suitable for retail clients. Schroder Life Flexible Retirement Fund

May 2016 For professional investors and advisors only. Not suitable for retail clients. Schroder Life Flexible Retirement Fund Improving the DC journey Members in a defined contribution (DC) pension scheme

May 2016 For professional investors and advisors only. Not suitable for retail clients. Schroder Life Flexible Retirement Fund Improving the DC journey Members in a defined contribution (DC) pension scheme

KEY GUIDE. Investing for income when you retire

KEY GUIDE Investing for income when you retire Planning the longest holiday of your life There comes a time when you stop working for your money and put your money to work for you. For most people, that

KEY GUIDE Investing for income when you retire Planning the longest holiday of your life There comes a time when you stop working for your money and put your money to work for you. For most people, that

M&G Guide to Retirement Income

M&G Guide to Retirement Income 2 Working out how to make adequate financial provision for retirement is one of the most important financial decisions most of us will ever face. However, it can be a daunting

M&G Guide to Retirement Income 2 Working out how to make adequate financial provision for retirement is one of the most important financial decisions most of us will ever face. However, it can be a daunting

Investment Guide. Understanding how your pension is invested

Understanding how your pension is invested Introduction The Creative Pension Trust ( the Scheme ) is an occupational money purchase pension scheme. It operates as a master trust, which means that many

Understanding how your pension is invested Introduction The Creative Pension Trust ( the Scheme ) is an occupational money purchase pension scheme. It operates as a master trust, which means that many

JUST RETIREMENT (HOLDINGS) LIMITED ( JUST RETIREMENT OR THE GROUP )

LIMITED ( JUST RETIREMENT OR THE GROUP )") INTERIM RESULTS 9 April 2013 INTERIM RESULTS JUST RETIREMENT (HOLDINGS) LIMITED ( JUST RETIREMENT OR THE GROUP ) Just Retirement, the specialist UK life assurance group focusing on the provision of financial

INTERIM RESULTS 9 April 2013 INTERIM RESULTS JUST RETIREMENT (HOLDINGS) LIMITED ( JUST RETIREMENT OR THE GROUP ) Just Retirement, the specialist UK life assurance group focusing on the provision of financial

WHAT IS CHANGING? 1 JULY 2014 27 MARCH 2014 APRIL 2015

BUDGET 2014 PENSIONS AND SAVINGS RULES Our simple Q&A looks at the changes happening in the pensions and savings industry and how you may be affected. THE 2014 BUDGET STATEMENT ANNOUNCED SOME SIGNIFICANT

BUDGET 2014 PENSIONS AND SAVINGS RULES Our simple Q&A looks at the changes happening in the pensions and savings industry and how you may be affected. THE 2014 BUDGET STATEMENT ANNOUNCED SOME SIGNIFICANT

The Investment Challenges of Decumulation

The Investment Challenges of Decumulation Part 2 March 2016 This communication is for investment professionals only and should not be distributed to or relied upon by retail clients. The Investment Challenges

The Investment Challenges of Decumulation Part 2 March 2016 This communication is for investment professionals only and should not be distributed to or relied upon by retail clients. The Investment Challenges

COMPANY OVERVIEW. Company Overview - 1

COMPANY OVERVIEW Company Overview - 1 The Rowan Tree The European Rowan tree (Sorbus aucuparia) has a long tradition in European mythology and folklore. It was thought to be a magical tree and give protection

COMPANY OVERVIEW Company Overview - 1 The Rowan Tree The European Rowan tree (Sorbus aucuparia) has a long tradition in European mythology and folklore. It was thought to be a magical tree and give protection

Financial Conduct Authority Retirement Income Market Data

Financial Conduct Authority Retirement Income Market Data July September 2015 Contents Introduction 1 1 Executive summary 2 2 Our sample 5 3 Consumer choices 6 4 Withdrawals 12 5 Use of regulated advisers

Financial Conduct Authority Retirement Income Market Data July September 2015 Contents Introduction 1 1 Executive summary 2 2 Our sample 5 3 Consumer choices 6 4 Withdrawals 12 5 Use of regulated advisers

The Partnership Enhanced Retirement Account

For financial advisers only not for retail clients The Partnership Enhanced Retirement Account ADVISER GUIDE 2 ENHANCED RETIREMENT ACCOUNT Contents Introduction 3 The ERA an all-in-one solution 4 Benefits

For financial advisers only not for retail clients The Partnership Enhanced Retirement Account ADVISER GUIDE 2 ENHANCED RETIREMENT ACCOUNT Contents Introduction 3 The ERA an all-in-one solution 4 Benefits

The Fiducia Guide to Retirement Planning

The Fiducia Guide to Retirement Planning September 2012 Fiducia Wealth Management Limited Dedham Hall Business Centre, Brook Street Colchester, Essex, CO7 6AD Fiducia Wealth Management Limited is authorised

The Fiducia Guide to Retirement Planning September 2012 Fiducia Wealth Management Limited Dedham Hall Business Centre, Brook Street Colchester, Essex, CO7 6AD Fiducia Wealth Management Limited is authorised

A GUIDE TO FINANCIAL GUIDE. New Pensions Freedom GIVING PEOPLE MORE CONFIDENCE TO SAVE INTO A PENSION

FINANCIAL GUIDE A GUIDE TO New Pensions Freedom GIVING PEOPLE MORE CONFIDENCE TO SAVE INTO A PENSION WELCOME Giving people more confidence to save into a pension Welcome to our Guide to New Pensions Freedom.

FINANCIAL GUIDE A GUIDE TO New Pensions Freedom GIVING PEOPLE MORE CONFIDENCE TO SAVE INTO A PENSION WELCOME Giving people more confidence to save into a pension Welcome to our Guide to New Pensions Freedom.

Products covered by the reporting requirement in SUP 16.11. This is the guidance referred to in SUP 16.11.6G.

16 Annex 20G Products covered by the reporting requirement in SUP 16.11 G This is the guidance referred to in SUP 16.11.6G. SUP 16.11.3R, SUP 16.11.5R and SUP 16.11.5AR require certain firms to report

16 Annex 20G Products covered by the reporting requirement in SUP 16.11 G This is the guidance referred to in SUP 16.11.6G. SUP 16.11.3R, SUP 16.11.5R and SUP 16.11.5AR require certain firms to report

Pension reforms in the UK: what can be learned from other countries?

Agenda Advancing economics in business Pension reforms in the UK: what can be learned from other countries? Reforms in the UK pensions market announced by the Chancellor of the Exchequer, George Osborne,

Agenda Advancing economics in business Pension reforms in the UK: what can be learned from other countries? Reforms in the UK pensions market announced by the Chancellor of the Exchequer, George Osborne,

NEST consultation response from Dr. Ros Altmann. Independent Pensions Policy Expert

6 January 2015 NEST consultation response from Dr. Ros Altmann. Independent Pensions Policy Expert 1. How will the trend for changing retirement patterns and provision affect a. What members need b. What

6 January 2015 NEST consultation response from Dr. Ros Altmann. Independent Pensions Policy Expert 1. How will the trend for changing retirement patterns and provision affect a. What members need b. What

Delayed Pension Payment Bulk Purchase Annuity

Delayed Pension Payment Bulk Purchase Annuity For employee benefit consultants, pension professionals and financial advisers only. Not approved for use with pension scheme members. Contents Delayed Pension

Delayed Pension Payment Bulk Purchase Annuity For employee benefit consultants, pension professionals and financial advisers only. Not approved for use with pension scheme members. Contents Delayed Pension

Welcome to Finance Shop. Independent Financial Advisers

F inance Welcome to Finance Shop S hop Independent Financial Advisers Contents Finance Shop - Overview Finance Shop: an overview........... 02 Finance Shop Values................. 03 Retirement Planning..............

F inance Welcome to Finance Shop S hop Independent Financial Advisers Contents Finance Shop - Overview Finance Shop: an overview........... 02 Finance Shop Values................. 03 Retirement Planning..............

PENSION INVESTMENT APPROACHES GUIDE. More detailed information

PENSION INVESTMENT APPROACHES GUIDE More detailed information OUR COMMITMENT TO YOU We want to do everything we can to help you achieve what you need from your plan. Aiming for investment growth is vital,

PENSION INVESTMENT APPROACHES GUIDE More detailed information OUR COMMITMENT TO YOU We want to do everything we can to help you achieve what you need from your plan. Aiming for investment growth is vital,

Guide to SIPPs. Investment Helpdesk: 0131 550 1212. www.cs-d.co.uk

Investment Helpdesk: 0131 550 1212 www.cs-d.co.uk SIPP stands for Self Invested Personal Pension. SIPPs are a flexible type of personal pension. Like most, they are designed to provide a retirement pot

Investment Helpdesk: 0131 550 1212 www.cs-d.co.uk SIPP stands for Self Invested Personal Pension. SIPPs are a flexible type of personal pension. Like most, they are designed to provide a retirement pot

Freedom and choice in pensions RESPONSE FROM ICAS TO HM TREASURY

Freedom and choice in pensions RESPONSE FROM ICAS TO HM TREASURY 11 June 2014 CA House 21 Haymarket Yards Edinburgh EH12 5BH enquiries@icas.org.uk +44 (0)131 347 0100 icas.org.uk Direct: +44 (0)131 347

Freedom and choice in pensions RESPONSE FROM ICAS TO HM TREASURY 11 June 2014 CA House 21 Haymarket Yards Edinburgh EH12 5BH enquiries@icas.org.uk +44 (0)131 347 0100 icas.org.uk Direct: +44 (0)131 347

Insights. Building a sustainable retirement plan. From asset allocation to product allocation

Insights Building a sustainable retirement plan From asset allocation to product allocation Philip Mowbray Philip.Mowbray@barrhibb.com Against a background of increased personal retirement wealth, low

Insights Building a sustainable retirement plan From asset allocation to product allocation Philip Mowbray Philip.Mowbray@barrhibb.com Against a background of increased personal retirement wealth, low

With new options available from April 2015, we can help you plan your finances for a worry-free retirement

Your retirement With new options available from April 2015, we can help you plan your finances for a worry-free retirement Life is full of financial decisions and planning your retirement is one of the

Your retirement With new options available from April 2015, we can help you plan your finances for a worry-free retirement Life is full of financial decisions and planning your retirement is one of the

Planning a prosperous retirement

Planning a prosperous retirement Towry s Guide to Retirement Planning About Towry We are one of the UK s leading Wealth Advisers and specialise in providing high quality, expert financial advice to private

Planning a prosperous retirement Towry s Guide to Retirement Planning About Towry We are one of the UK s leading Wealth Advisers and specialise in providing high quality, expert financial advice to private

Annuities and decumulation phase of retirement. Chris Daykin UK Government Actuary Chairman, PBSS Section of IAA

Annuities and decumulation phase of retirement Chris Daykin UK Government Actuary Chairman, PBSS Section of IAA CASH LUMP SUM AT RETIREMENT CASH INSTEAD OF PENSION > popular with pension scheme members

Annuities and decumulation phase of retirement Chris Daykin UK Government Actuary Chairman, PBSS Section of IAA CASH LUMP SUM AT RETIREMENT CASH INSTEAD OF PENSION > popular with pension scheme members

Our Guide to the 2015 Pension Reforms

Our Guide to the 2015 Pension Reforms The overhaul of the pension system will significantly impact your retirement planning, opening up a whole new world of flexibility over how you spend, save and invest

Our Guide to the 2015 Pension Reforms The overhaul of the pension system will significantly impact your retirement planning, opening up a whole new world of flexibility over how you spend, save and invest

THE END OF PENSIONS? Consultants Corner

THE END OF PENSIONS? By Charlotte Moore It s no exaggeration to call the pension changes announced in this year s Budget revolutionary: this reform could herald the end of pensions and usher in a new era

THE END OF PENSIONS? By Charlotte Moore It s no exaggeration to call the pension changes announced in this year s Budget revolutionary: this reform could herald the end of pensions and usher in a new era

Collective Retirement Account

Key features of the Collective Retirement Account The Financial Conduct Authority is a financial services regulator. It requires us, Old Mutual Wealth, to give you this important information to help you

Key features of the Collective Retirement Account The Financial Conduct Authority is a financial services regulator. It requires us, Old Mutual Wealth, to give you this important information to help you

AGGREGATE COMPLAINTS STATISTICS: 2006 to 2014 H1

AGGREGATE COMPLAINTS STATISTICS: 2006 to 2014 H1 (Click on the hyperlinks below) Table: 1 Complaints by product and cause Complaints by product group and cause of complaint (2014 H1) 2 Volumes 2.1 Number

AGGREGATE COMPLAINTS STATISTICS: 2006 to 2014 H1 (Click on the hyperlinks below) Table: 1 Complaints by product and cause Complaints by product group and cause of complaint (2014 H1) 2 Volumes 2.1 Number

WELCOME TO THE AIRBUS GROUP UK RETIREMENT PLAN

WELCOME TO THE AIRBUS GROUP UK RETIREMENT PLAN Investment guide The is an important part of your reward package. This guide aims to help you choose the funds in which to invest your personal Retirement

WELCOME TO THE AIRBUS GROUP UK RETIREMENT PLAN Investment guide The is an important part of your reward package. This guide aims to help you choose the funds in which to invest your personal Retirement

Making the most of your tax-free allowances

UNISONMONEYTALK The personal finance newsletter for UNISON members published by Lighthouse Financial Advice Autumn 2015 Making the most of your tax-free allowances A key consideration for anyone with money

UNISONMONEYTALK The personal finance newsletter for UNISON members published by Lighthouse Financial Advice Autumn 2015 Making the most of your tax-free allowances A key consideration for anyone with money

Pension Reforms. Key points: By Nigel Aston UK Head of Defined Contribution

Pension Reforms Herald New Era By Nigel Aston UK Head of Defined Contribution Key points: Rather than most people having to secure a pension income by purchasing an annuity, people retiring from April

Pension Reforms Herald New Era By Nigel Aston UK Head of Defined Contribution Key points: Rather than most people having to secure a pension income by purchasing an annuity, people retiring from April

THIS DOCUMENT IS FOR USE WITH A FINANCIAL ADVISER ONLY OLD MUTUAL GENERATION FUNDS INVESTING FOR RETIREMENT INCOME

THIS DOCUMENT IS FOR USE WITH A FINANCIAL ADVISER ONLY OLD MUTUAL GENERATION FUNDS INVESTING FOR RETIREMENT INCOME INSIDE 1 2 4 6 9 10 11 12 13 13 Retirement calls Key considerations What are the Generation

THIS DOCUMENT IS FOR USE WITH A FINANCIAL ADVISER ONLY OLD MUTUAL GENERATION FUNDS INVESTING FOR RETIREMENT INCOME INSIDE 1 2 4 6 9 10 11 12 13 13 Retirement calls Key considerations What are the Generation

19,000. years. Retirement. Uncovered 4,700. Average income GAP. Lifting the lid on retirement income in the UK today. Expected.

Average income 19,000 Expected retirement 21 years Reality 4,700 GAP Expected Retirement Income Uncovered Lifting the lid on retirement income in the UK today contents Foreword carlton hood 3 Executive

Average income 19,000 Expected retirement 21 years Reality 4,700 GAP Expected Retirement Income Uncovered Lifting the lid on retirement income in the UK today contents Foreword carlton hood 3 Executive

A guide to the pension changes in April 2015

A guide to the pension changes in April 2015 106027837.indd 1 05/01/2015 10:00 Contents What do the changes mean for you? 3 Summary of the changes from 6 April 2015 5 What s changed in practice? 6 How

A guide to the pension changes in April 2015 106027837.indd 1 05/01/2015 10:00 Contents What do the changes mean for you? 3 Summary of the changes from 6 April 2015 5 What s changed in practice? 6 How

Freedom and Choice in Pensions. Your guide to the changes

Freedom and Choice in Pensions Your guide to the changes Contents Freedom and Choice 3-5 in Pensions Buy an annuity 6-7 Remain invested - 8-9 entering drawdown Take a cash lump sum 10 Will providers offer

Freedom and Choice in Pensions Your guide to the changes Contents Freedom and Choice 3-5 in Pensions Buy an annuity 6-7 Remain invested - 8-9 entering drawdown Take a cash lump sum 10 Will providers offer

John and Deena Smith SaidSo Client Number: 3xampl3

John and Deena Smith SaidSo Client Number: 3xampl3 YOUR SAIDSO FINANCIAL PLANNING REPORT ed [Pick the date] [Type the abstract of the document here. The abstract is typically a short summary of the contents

John and Deena Smith SaidSo Client Number: 3xampl3 YOUR SAIDSO FINANCIAL PLANNING REPORT ed [Pick the date] [Type the abstract of the document here. The abstract is typically a short summary of the contents

KEY FEATURES OF YOUR BUYOUT BOND ILLUSTRATION KEY FEATURES. and Conditions, available from your financial adviser.

00000 Old Mutual Wealth Life Assurance Limited is a provider of long-term life assurance. It is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential

00000 Old Mutual Wealth Life Assurance Limited is a provider of long-term life assurance. It is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential

Self Select Investment Guide move ahead

Self Select Investment Guide move ahead For members of The Barclays Bank UK Retirement Fund (the UKRF) 2 Self Select Investments move ahead Inside this guide Welcome to Self Select 2 Investments Choosing

Self Select Investment Guide move ahead For members of The Barclays Bank UK Retirement Fund (the UKRF) 2 Self Select Investments move ahead Inside this guide Welcome to Self Select 2 Investments Choosing

Spring 2015 reforms: the new DC flexibilities

Spring 2015 reforms: the new DC flexibilities THE REFORMS AT A GLANCE y Until April 2015, members usually faced serious tax penalties if they did not spend at least 75% of their DC pots on an annuity meeting

Spring 2015 reforms: the new DC flexibilities THE REFORMS AT A GLANCE y Until April 2015, members usually faced serious tax penalties if they did not spend at least 75% of their DC pots on an annuity meeting

KEY GUIDE. Pensions freedom drawing from your pension

KEY GUIDE Pensions freedom drawing from your pension Radical reform The changes revealed in the 2014 Budget were described by some retirement planning experts as a pensions revolution. The radical proposals

KEY GUIDE Pensions freedom drawing from your pension Radical reform The changes revealed in the 2014 Budget were described by some retirement planning experts as a pensions revolution. The radical proposals

Guaranteed Drawdown. Giving you confidence about your retirement income

Guaranteed Drawdown Giving you confidence about your retirement income 1 The new retirement landscape As you approach retirement, it s time to make those important financial decisions that will see you

Guaranteed Drawdown Giving you confidence about your retirement income 1 The new retirement landscape As you approach retirement, it s time to make those important financial decisions that will see you

MORE CHOICE MORE FREEDOM

LOOK FORWARD TO MORE CHOICE MORE FREEDOM A guide to Income Release Pension Portfolio royallondon.com WELCOME TO ROYAL LONDON We re a mutual organisation and, unlike a PLC, we don t have any shareholders

LOOK FORWARD TO MORE CHOICE MORE FREEDOM A guide to Income Release Pension Portfolio royallondon.com WELCOME TO ROYAL LONDON We re a mutual organisation and, unlike a PLC, we don t have any shareholders

GUIDE TO RETIREMENT PLANNING FINANCIAL GUIDE. Making the most of the new pension rules to enjoy freedom and choice in your retirement

GUIDE TO RETIREMENT PLANNING Making the most of the new pension rules to enjoy freedom and choice in your retirement FINANCIAL GUIDE WELCOME Making the most of the new pension rules to enjoy freedom and

GUIDE TO RETIREMENT PLANNING Making the most of the new pension rules to enjoy freedom and choice in your retirement FINANCIAL GUIDE WELCOME Making the most of the new pension rules to enjoy freedom and

BS2551 Money Banking and Finance. Institutional Investors

BS2551 Money Banking and Finance Institutional Investors Institutional investors pension funds, mutual funds and life insurance companies are the main players in securities markets in both the USA and

BS2551 Money Banking and Finance Institutional Investors Institutional investors pension funds, mutual funds and life insurance companies are the main players in securities markets in both the USA and

Should I Buy an Income Annuity?

Prepared For: Valued Client Prepared By: CPS The purchase of any financial product involves a trade off. For example when saving for retirement, you are often faced with making a trade off between how

Prepared For: Valued Client Prepared By: CPS The purchase of any financial product involves a trade off. For example when saving for retirement, you are often faced with making a trade off between how

Your investment choices and charges. Explaining the investment options and charges for our Active Money Self Invested Personal Pension

Your investment choices and charges Explaining the investment options and charges for our Active Money Self Invested Personal Pension Contents 02 Level 1 investments 04 Level 2 investments 06 Level 3 investments

Your investment choices and charges Explaining the investment options and charges for our Active Money Self Invested Personal Pension Contents 02 Level 1 investments 04 Level 2 investments 06 Level 3 investments

KEY GUIDE. Investing for income at retirement

KEY GUIDE Investing for income at retirement Introduction The decisions you make at retirement could have repercussions for the rest of your life. That might be considerably longer than you think, as the

KEY GUIDE Investing for income at retirement Introduction The decisions you make at retirement could have repercussions for the rest of your life. That might be considerably longer than you think, as the

Products covered by the reporting requirement in SUP 16.11

16 Annex 20G Products covered by the reporting requirement in SUP 16.11 G This is the guidance referred to in SUP 16.11.6G. SUP 16.11.3R requires certain firms to report product sales data. For reporting

16 Annex 20G Products covered by the reporting requirement in SUP 16.11 G This is the guidance referred to in SUP 16.11.6G. SUP 16.11.3R requires certain firms to report product sales data. For reporting

Key features of the Zurich Retirement Account

Key features of the Zurich Retirement Account Helping you decide This important document gives you a summary of the Zurich Retirement Account. Please read this before you decide to invest, and keep it

Key features of the Zurich Retirement Account Helping you decide This important document gives you a summary of the Zurich Retirement Account. Please read this before you decide to invest, and keep it

Telegraph Investor SIPP Payment of Benefits Guidance Notes

Under the HMRC pension legislation you can take your benefits from age 55, or younger on ill health grounds (see section below). Please note that you do not have to leave employment to draw your benefits

Under the HMRC pension legislation you can take your benefits from age 55, or younger on ill health grounds (see section below). Please note that you do not have to leave employment to draw your benefits

GW Contracted-out Money Purchase Scheme ( the Scheme ) Statement of Investment Principles

Statement of Investment Principles") GW Contracted-out Money Purchase Scheme ( the Scheme ) Statement of Principles This Statement of Principles (SIP) covers the defined contribution section of the Scheme. It is set out in three parts: 1)

GW Contracted-out Money Purchase Scheme ( the Scheme ) Statement of Principles This Statement of Principles (SIP) covers the defined contribution section of the Scheme. It is set out in three parts: 1)

HOW WE MANAGE THE PHOENIX LIFE LIMITED SPI WITH-PROFITS FUND

HOW WE MANAGE THE PHOENIX LIFE LIMITED SPI WITH-PROFITS FUND A guide for trustees with Simplified Pension Investment deposit administration policies invested in this fund The aims of this guide The guide

HOW WE MANAGE THE PHOENIX LIFE LIMITED SPI WITH-PROFITS FUND A guide for trustees with Simplified Pension Investment deposit administration policies invested in this fund The aims of this guide The guide

Growth assets, bonds and annuities finding the right mix? Nick Callil Watson Wyatt Australia

Growth assets, bonds and annuities finding the right mix? Nick Callil Watson Wyatt Australia Living longer more likely than we think Probability 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 73% chance of 1

Growth assets, bonds and annuities finding the right mix? Nick Callil Watson Wyatt Australia Living longer more likely than we think Probability 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 73% chance of 1

Retirement Income Service FOR INTERMEDIARIES

Retirement Income Service FOR INTERMEDIARIES 1 We recognise how hard your clients work throughout their lives to enjoy a comfortable retirement. With extensive experience in providing tailor-made retirement

Retirement Income Service FOR INTERMEDIARIES 1 We recognise how hard your clients work throughout their lives to enjoy a comfortable retirement. With extensive experience in providing tailor-made retirement

April 2015: Forthcoming Pension Changes. Retirement options for money purchase pension schemes (including SSAS).

.") April 2015: Forthcoming Pension Changes Significant changes to pension regulations are being introduced on the 6 th April 2015. The legislation will be covered in the Taxation of Pensions Bill 2014 and

April 2015: Forthcoming Pension Changes Significant changes to pension regulations are being introduced on the 6 th April 2015. The legislation will be covered in the Taxation of Pensions Bill 2014 and

University of Reading Pension Scheme

Human Resources University of Reading Pension Scheme Investing for Retirement Introduction After deciding how much to save for retirement, where to invest the contributions that you and the University

Human Resources University of Reading Pension Scheme Investing for Retirement Introduction After deciding how much to save for retirement, where to invest the contributions that you and the University

WITHDRAWING MONEY PURCHASE FUNDS

WITHDRAWING MONEY PURCHASE FUNDS WITHDRAWING MONEY PURCHASE FUNDS Pension commencement lump sum plus annuity Uncrystallised funds pension lump sum Flexi -access drawdown Small pots PRESERVE YOUR FUTURE

WITHDRAWING MONEY PURCHASE FUNDS WITHDRAWING MONEY PURCHASE FUNDS Pension commencement lump sum plus annuity Uncrystallised funds pension lump sum Flexi -access drawdown Small pots PRESERVE YOUR FUTURE

Wealth management Guide for financial advisers

Wealth management Guide for financial advisers Wealth management 1 Contents 01 Welcome to Standard Life Wealth 03 Why choose Standard Life Wealth to work with? 04 How we aim to meet your clients financial

Wealth management Guide for financial advisers Wealth management 1 Contents 01 Welcome to Standard Life Wealth 03 Why choose Standard Life Wealth to work with? 04 How we aim to meet your clients financial

Average income 6,300. Expected. Reality GAP REDEFINING RETIREMENT HOW THE UK IS ADAPTING TO THE NEW WORLD OF RETIREMENT

Average income 19,700 Reality 6,300 GAP Expected REDEFINING RETIREMENT HOW THE UK IS ADAPTING TO THE NEW WORLD OF RETIREMENT CONTENTS FOREWORD CARLTON HOOD 3 EXECUTIVE SUMMARY 4 SECTION 1 THE RETIREMENT

Average income 19,700 Reality 6,300 GAP Expected REDEFINING RETIREMENT HOW THE UK IS ADAPTING TO THE NEW WORLD OF RETIREMENT CONTENTS FOREWORD CARLTON HOOD 3 EXECUTIVE SUMMARY 4 SECTION 1 THE RETIREMENT

FINANCIAL PLANNING Tariff of charges

FINANCIAL PLANNING Tariff of charges Customers receiving advice Ways to Invest with Nationwide There are two ways to invest through Nationwide: with advice via one of our Nationwide financial advisers

FINANCIAL PLANNING Tariff of charges Customers receiving advice Ways to Invest with Nationwide There are two ways to invest through Nationwide: with advice via one of our Nationwide financial advisers

Equity release - an integral feature in a retirement account

Equity release - an integral feature in a retirement account September 2015 www.aquilaheywood.co.uk 1 - Synopsis 2 2 - A holistic retirement proposition 3 3 - Equity release 4 4 - Can the market deliver?

Equity release - an integral feature in a retirement account September 2015 www.aquilaheywood.co.uk 1 - Synopsis 2 2 - A holistic retirement proposition 3 3 - Equity release 4 4 - Can the market deliver?

A simple solution to the investment puzzle. Multi-asset Funds. Ready-made investment funds matched to your attitude to risk

A simple solution to the investment puzzle Multi-asset Funds Ready-made investment funds matched to your attitude to risk Contents Why Aviva Investors? 2 A simple solution to investing 3 Are these funds

A simple solution to the investment puzzle Multi-asset Funds Ready-made investment funds matched to your attitude to risk Contents Why Aviva Investors? 2 A simple solution to investing 3 Are these funds

Your investment options University of Reading Pension Scheme

Human Resources Your investment options University of Reading Pension Scheme Introduction If you are a member of the University of Reading Pension Scheme (the Scheme) you and your employer pay contributions

Human Resources Your investment options University of Reading Pension Scheme Introduction If you are a member of the University of Reading Pension Scheme (the Scheme) you and your employer pay contributions

The Personal Range Key Features of the Individual Personal Pension Transfer Value Account

The Personal Range Key Features of the Individual Personal Pension Transfer Value Account Reference MPEN11/F 07.15 The Financial Conduct Authority is a financial services regulator. It requires us, Friends

The Personal Range Key Features of the Individual Personal Pension Transfer Value Account Reference MPEN11/F 07.15 The Financial Conduct Authority is a financial services regulator. It requires us, Friends

SOCIAL CARE FUNDING: STATEMENT OF INTENT

SOCIAL CARE FUNDING: STATEMENT OF INTENT The Department of Health ( the Department ) and the Association of British Insurers on behalf of the insurance industry ( the industry ) both want to help people

SOCIAL CARE FUNDING: STATEMENT OF INTENT The Department of Health ( the Department ) and the Association of British Insurers on behalf of the insurance industry ( the industry ) both want to help people

Personal Pension Account

Personal Pension Account Contents Introduction... 1 A Closer Look At Our Personal Pension Account... 2 What Are The Tax Advantages?... 3 Flexible Contribution Options... 4 You Control Your Investment...

Personal Pension Account Contents Introduction... 1 A Closer Look At Our Personal Pension Account... 2 What Are The Tax Advantages?... 3 Flexible Contribution Options... 4 You Control Your Investment...

Wealth Management. from NEWBY CASTLEMAN (FINANCIAL SERVICES) LIMITED. 15236_GAM - Wealth Management booklet.indd 1 22/7/09 12:21:53

LIMITED. 15236_GAM - Wealth Management booklet.indd 1 22/7/09 12:21:53") Wealth Management from NEWBY CASTLEMAN (FINANCIAL SERVICES) LIMITED 15236_GAM - Wealth Management booklet.indd 1 22/7/09 12:21:53 2 Contents Wealth Management with no upfront fees Wealth Management 2 Information

Wealth Management from NEWBY CASTLEMAN (FINANCIAL SERVICES) LIMITED 15236_GAM - Wealth Management booklet.indd 1 22/7/09 12:21:53 2 Contents Wealth Management with no upfront fees Wealth Management 2 Information

Wealth management. Guide for private clients

Wealth management Guide for private clients Contents 01 Welcome to Standard Life Wealth 03 Understanding your financial goals 04 Different goals, different approaches 07 What you can expect as a client

Wealth management Guide for private clients Contents 01 Welcome to Standard Life Wealth 03 Understanding your financial goals 04 Different goals, different approaches 07 What you can expect as a client

Pension Flexibility 2015

Pension Flexibility 2015 Who is likely to be affected? Individuals who have reached the normal minimum pension age, (normally age 55), who have money purchase pension savings in a registered pension scheme

Pension Flexibility 2015 Who is likely to be affected? Individuals who have reached the normal minimum pension age, (normally age 55), who have money purchase pension savings in a registered pension scheme

Justifying the investment budget

Justifying the investment budget Professional Pensions DC Conference, 12 April 2016 Tim Horne DC Investment Solutions Manager, Schroders For professional investors only. This material is not suitable for

Justifying the investment budget Professional Pensions DC Conference, 12 April 2016 Tim Horne DC Investment Solutions Manager, Schroders For professional investors only. This material is not suitable for

Pensions Tax Reliefs. 03333 219 000 advice@bishopfleming.co.uk. www.bishopfleming.co.uk

Pensions Tax Reliefs Types of pension schemes There are two broad types of pension schemes from which an individual may eventually be in receipt of a pension: Workplace pension schemes Personal Pension

Pensions Tax Reliefs Types of pension schemes There are two broad types of pension schemes from which an individual may eventually be in receipt of a pension: Workplace pension schemes Personal Pension

Investment management. Tailor-made investment solutions

Investment management Tailor-made investment solutions ABOUT US Tilney Bestinvest is a leading investment and financial planning firm that builds on a heritage of more than 150 years. We look after more

Investment management Tailor-made investment solutions ABOUT US Tilney Bestinvest is a leading investment and financial planning firm that builds on a heritage of more than 150 years. We look after more

MILSTED LANGDON FINANCIAL PLANNING

MILSTED LANGDON: BUSINESS ADVANTAGE PEACE OF MIND MILSTED LANGDON FINANCIAL PLANNING WORKING TOGETHER TO PROVIDE A BETTER FUTURE www.mlifa.co.uk/financial-planning advice@mlifa.co.uk CHOOSING THE RIGHT

MILSTED LANGDON: BUSINESS ADVANTAGE PEACE OF MIND MILSTED LANGDON FINANCIAL PLANNING WORKING TOGETHER TO PROVIDE A BETTER FUTURE www.mlifa.co.uk/financial-planning advice@mlifa.co.uk CHOOSING THE RIGHT

WHERE EXPERIENCE COUNTS

Investment Services Guide Retail & Corporate Stockbrokers WHERE EXPERIENCE COUNTS Our Advisory Investment Services are designed specifically for investors seeking specialist expertise and advice on investments

Investment Services Guide Retail & Corporate Stockbrokers WHERE EXPERIENCE COUNTS Our Advisory Investment Services are designed specifically for investors seeking specialist expertise and advice on investments

Freedom and choice in pensions

Freedom and choice in pensions Response from NEST Overview The recent liberalisation of the rules on decumulation present us with a welcome opportunity to think about what our members need from their pension

Freedom and choice in pensions Response from NEST Overview The recent liberalisation of the rules on decumulation present us with a welcome opportunity to think about what our members need from their pension

The Retirement Account. Certainty, flexibility and simplicity for life

Certainty, flexibility and simplicity for life Introducing Retirement Advantage Previously known as MGM Advantage and Stonehaven, we are a well-established company that can trace our roots back over 150

Certainty, flexibility and simplicity for life Introducing Retirement Advantage Previously known as MGM Advantage and Stonehaven, we are a well-established company that can trace our roots back over 150

1. Alice has the following income and benefits in the tax year 2016/17

1. Alice has the following income and benefits in the tax year 2016/17 Salary 100,000 Company car 5,000 Dividends 4,000 Income from a rental property 10,000 Employer pension contribution 60,000 (carry

1. Alice has the following income and benefits in the tax year 2016/17 Salary 100,000 Company car 5,000 Dividends 4,000 Income from a rental property 10,000 Employer pension contribution 60,000 (carry

Welplan Pensions. Flexibility for members from 6 April 2016. Spotlight on flexibility:

Welplan Pensions Flexibility for members from 6 April 2016 Spotlight on flexibility: Pension freedom is great news for members Changes in the law mean that from 6 April 2015 many members of pension schemes

Welplan Pensions Flexibility for members from 6 April 2016 Spotlight on flexibility: Pension freedom is great news for members Changes in the law mean that from 6 April 2015 many members of pension schemes

Pension benefits guide How you can use your pension pot to suit your needs

Pension benefits guide How you can use your pension pot to suit your needs axawealth.co.uk With the flexibility you have to take benefits through your pension, it can be difficult to know what s best for

Pension benefits guide How you can use your pension pot to suit your needs axawealth.co.uk With the flexibility you have to take benefits through your pension, it can be difficult to know what s best for

BAE SYSTEMS PENSIONS BECAUSE PLANNING IS PART OF THE JOURNEY RETIREMENT ACCOUNT GUIDE LEVEL 100+ MARCH 2015

BAE SYSTEMS PENSIONS BECAUSE PLANNING IS PART OF THE JOURNEY RETIREMENT ACCOUNT GUIDE LEVEL 100+ MARCH 2015 CONTENTS Where your Scheme benefits come from 4 Your choices affect your retirement account 5

BAE SYSTEMS PENSIONS BECAUSE PLANNING IS PART OF THE JOURNEY RETIREMENT ACCOUNT GUIDE LEVEL 100+ MARCH 2015 CONTENTS Where your Scheme benefits come from 4 Your choices affect your retirement account 5

Daly, Hoggett & Co. is a firm of Chartered Accountants and Independent Financial Advisers established in 1966, with offices in central London and

Daly, Hoggett & Co. is a firm of Chartered Accountants and Independent Financial Advisers established in 1966, with offices in central London and Rickmansworth, Hertfordshire. The firm is authorised and

Daly, Hoggett & Co. is a firm of Chartered Accountants and Independent Financial Advisers established in 1966, with offices in central London and Rickmansworth, Hertfordshire. The firm is authorised and

MEETING THE RETIREMENT INCOME CHALLENGE APRIL 2013

MEETING THE RETIREMENT INCOME CHALLENGE APRIL 2013 INTRODUCTION The Australian retirement system is generally regarded globally as being well advanced, ranking third in the 2012 Mercer Melbourne Global

MEETING THE RETIREMENT INCOME CHALLENGE APRIL 2013 INTRODUCTION The Australian retirement system is generally regarded globally as being well advanced, ranking third in the 2012 Mercer Melbourne Global

Your investment choices made easy

Your investment choices made easy PathFinder guide The Fidelity PathFinder range An easy way to invest Our PathFinder range is exclusively available to customers of Fidelity s Personal Investing service.

Your investment choices made easy PathFinder guide The Fidelity PathFinder range An easy way to invest Our PathFinder range is exclusively available to customers of Fidelity s Personal Investing service.

Annuities. A Quick Guide. CIB Retirement Solutions

CIB Retirement Solutions Annuities A Quick Guide CIB Retirement Solutions Beta House, Laser Quay, Culpeper Close, Rochester, Kent. ME2 4HU Tel: 01634 729990 Fax: 0845 528 1116 Email: pensions@cibretirement.com

CIB Retirement Solutions Annuities A Quick Guide CIB Retirement Solutions Beta House, Laser Quay, Culpeper Close, Rochester, Kent. ME2 4HU Tel: 01634 729990 Fax: 0845 528 1116 Email: pensions@cibretirement.com

Creating a Secondary Annuity Market: a response by the National Association of Pension Funds

Creating a Secondary Annuity Market: a response by the National Association of Pension Funds June 2015 www.napf.co.uk Creating a secondary annuity market: a response by the NAPF Contents Executive Summary

Creating a Secondary Annuity Market: a response by the National Association of Pension Funds June 2015 www.napf.co.uk Creating a secondary annuity market: a response by the NAPF Contents Executive Summary

Nurturing your investment

helping life flow smoothly UNITED UTILITIES PENSION SCHEME Investment choices Nurturing your investment Contents Investment choices 1. A BRIEF GUIDE TO INVESTMENTS A reminder of the main different types

helping life flow smoothly UNITED UTILITIES PENSION SCHEME Investment choices Nurturing your investment Contents Investment choices 1. A BRIEF GUIDE TO INVESTMENTS A reminder of the main different types

Pensions - Tax Reliefs

Pensions - Tax Reliefs Types of pension schemes There are two broad types of pension schemes from which an individual may eventually be in receipt of a pension: Occupational schemes Personal Pension schemes.

Pensions - Tax Reliefs Types of pension schemes There are two broad types of pension schemes from which an individual may eventually be in receipt of a pension: Occupational schemes Personal Pension schemes.

Pensions Tax Reliefs

Our Vision Pensions Tax Reliefs To become the Best Provider of Solutions for Businesses in Coventry & Warwickshire Types of pension schemes There are two broad types of pension schemes from which an individual

Our Vision Pensions Tax Reliefs To become the Best Provider of Solutions for Businesses in Coventry & Warwickshire Types of pension schemes There are two broad types of pension schemes from which an individual

TD Direct Investing A Guide to SIPPs

TD Direct Investing A Guide to SIPPs Introduction If you are considering investing for retirement, there are a number of ways to approach it. One way is to embark on the do it yourself (DIY) self investment

TD Direct Investing A Guide to SIPPs Introduction If you are considering investing for retirement, there are a number of ways to approach it. One way is to embark on the do it yourself (DIY) self investment

HMT / DWP CONSULTATION RESPONSE CREATING A SECONDARY ANNUITY MARKET

HMT / DWP CONSULTATION RESPONSE CREATING A SECONDARY ANNUITY MARKET INTRODUCTION TISA is a not-for-profit membership association operating within the financial services industry. TISA s membership comprises

HMT / DWP CONSULTATION RESPONSE CREATING A SECONDARY ANNUITY MARKET INTRODUCTION TISA is a not-for-profit membership association operating within the financial services industry. TISA s membership comprises

KEY GUIDE. Investing for income when you retire

KEY GUIDE Investing for income when you retire Planning the longest holiday of your life There comes a time when you stop working for your money and put your money to work for you. For most people, that

KEY GUIDE Investing for income when you retire Planning the longest holiday of your life There comes a time when you stop working for your money and put your money to work for you. For most people, that