Genie. The core mission of the Finance

|

|

|

- Ashlee Joy Rich

- 8 years ago

- Views:

Transcription

1 The core mission of the Finance Genie Institute ( TFI ) is lead generation to the Alternative Finance Industry. TFI delivers on this mission by quickly training, guiding and supporting an elite consultant network across North America. offering the most informationpacked, true-to-life-virtual training and support programs available in the industry today. All of our programs have been developed by leading industry practitioners that harness their knowledge, experience and success in delivering comprehensive but, practical training that anyone can follow to do this right now and make money. Whether you re a Business Professional, Entrepreneur, Real Estate - Financial Pro, Corporate Expatriate or Job Seeker.. TFI has the educational program and support system for you!

2 The History of Factoring Genie Cloud Recorded history reveals that the concept of turning future payments into cash ( or cash equivalents) dates back thousands of years. Much like today, the need for liquidity, or cash to pay everyday expenses, has always been a great need. Think of the days when merchants would travel the seas in search of various treasures. Ships would be filled with those in need of food and necessities to survive. Financiers offered payments against future rewards as a means to earn a return on their investment. This financing was an integral part of the success in establishing world trade. Thus, the concept of factoring was born dating back some four thousand years. Prior to the 1980 s, factoring was used primarily in the garment, textile, and furniture industries typically only available to larger companies. Entrepreneurial funding companies, coupled with the creation of a consultant (broker) network, changed all this in the late 1990 s. Factoring is now a widely-accepted financing alternative. Due to the credit crisis and economic meltdown of years gone by, factoring has quickly become one of the alternative financing industries tools of choice. Today, businesses are holding onto their cash for as long as they can. This means that suppliers to these businesses are becoming stretched out with regard to payments. 2

3 The Facts Genie Cloud A recent study conducted by the Credit Research Foundation found nearly 80% of North American companies report that the economy has had a direct negative effect on their business with a majority citing lack of available working capital, tightening of cash flow and a slowdown in customer payments! As three major issues that are having disastrous affects on the viability of their businesses. In addition: 33% say the financial crisis is straining their availability to gain working capital 67% report that they are experiencing a general slowdown in customer payments 68% say their customers are experiencing tightening of bank financing 67% report tightened A/R collections Companies that were accustomed to receiving payment on their invoices in 30 days are faced with the reality that the payment cycle is now surpassing 60 days or longer. The national average for invoices to be paid across North America is a Staggering 73 days! The trickle down effect of this is tremendous. Without the needed cash flow, companies are forced to make tough decisions. Employees are being let go (no money for payroll), supplier payments are delayed (resulting in delayed or cancelled shipments for future orders), delaying payment of operating expenses (negatively affecting the company s credit history which will adversely affect their purchasing power), payment of taxes are delayed (resulting in judgments and tax liens) and the list goes on. 3

4 Genie Cloud What drives the economy? Is it interest and/or Mortgage rates? No, they are currently hitting record lows and the economy is still bad. Simply said, when consumers spend their money, the economy thrives. Therefore, the question is: why are consumers choosing to save their money as opposed to spending it? 4

5 Understanding the trends We have all heard the term Baby Boomers. Baby now seems to be a misnomer as over 10,000 boomers turn 65 each day and this trend will continue for the next 15 years! So, how does this have an effect on our economy? Statistics show an individual s highest earning capacity is between the ages of 35 and 55. Spending is typically concurrent with earnings the more you make, the more you spend. The opposite is true as well. The less you make, the less you spend. Since the boomers are earning less, they are spending less. In addition, the unemployment rate is higher than it has been in decades. The average unemployed person has been out of work for at least 9 months. Finally, throw the real estate and stock market disasters (in 2008) into the mix and you have the recipe for an economic collapse. The demand for credit has shrunk amongst consumers in spite of the stimulus plan and bank bailouts. Banks are circling the wagons in an effort to stabilize their existing loan portfolios, and are turning down small business loan applications at an unprecedented rate. 5

6 So what are we left with? Genie Cloud Our economies are driven by small business. Banks are not lending and we are witnessing the potential demise of the small business - As small businesses decline, employment declines and consumer confidence tumbles. However, there is a solution! When cash flow is tight, where do companies turn? Traditionally, this answer has been to banks. Pick up today s paper, listen to the news, research the internet and you will see that banks are NOT the solution. Banks are looking to the federal government (remember the stimulus plan) for help in overcoming astronomical losses due to loosened credit policies in the past. Their directive is to protect their existing portfolios, while becoming extremely conservative in providing new loans (if any). Factoring has now become the financing tool of choice. And in many cases the only choice. 6

7 So, what is factoring? Genie Cloud The definition of Factoring is simple: The purchase of business to business (B2B) or business to government (B2G) accounts receivable (invoices) for products delivered or services that were rendered in the past, at a discount. Factoring is NOT A LOAN and NO INTEREST is charged. It is simply the discounted purchase (sale) of a company s non performing asset (accounts receivable an invoice that is paid over time) 7

8 So, what is factoring? Genie Cloud The definition of Factoring is simple: The purchase of business to business (B2B) or business to government (B2G) accounts receivable (invoices) for products delivered or services that were rendered in the past, at a discount. Factoring is NOT A LOAN and NO INTEREST is charged. It is simply the discounted purchase (sale) of a company s non performing asset (accounts receivable an invoice that is paid over time) 7

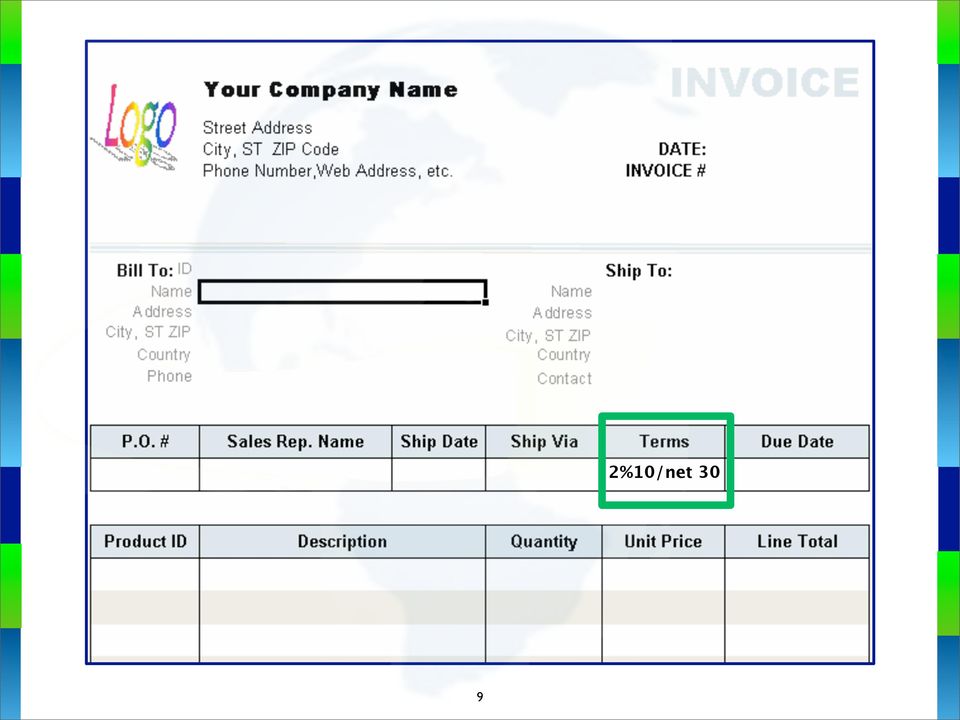

9 Is factoring just for a few select industries? Genie Cloud Factoring related transactions are somewhat vast. By definition, invoices must be from one business to another business or, from a business to the government. With this in mind, the number of potential prospects is HUGE! At the time of publishing this E-book, there were over 55 million small businesses scattered all across North America (United States and Canada). This number is sure to increase due to new start up companies that have sprouted up recently, mainly as a result of those individuals that have been downsized and subsequently have started their own businesses. Ask yourself this question: How many businesses do you know of that provide a product or service to another business or the government? Now ask yourself: How many of those businesses are getting paid in over 30 days? 45 days? 60 days? 90 days? Since just about everything in a factoring transaction is centered on an invoice, let s see what a typical invoice may look like. 8

10 9 2%10/net 30

11 There are a number of components that make up an invoice. Let s quickly highlight and describe these components. Genie Cloud Bill To: Identifies the customer or the payee information in the sales transaction Description: Identifies the products that were manufactured and shipped, products that were redistributed or services that were rendered. Quantity: Identifies the number of units of the products that were shipped or services that were rendered. Unit Price: Is the individual price of each product that was shipped or the services that were rendered. Line Total: Is calculated by multiplying quantity times the unit price. One of the most important components that make up an invoice is the TERMS of payment. Typical terms in business are: 2% 10/net 30 days which means if the customer pays for the invoice within 10 days they will receive a 2% discount off the face (total value) of the invoice. If the customer pays for their invoice after ten days, they are required to pay the total (face value) of the invoice. This is fundamental for the factoring industry. The longer the terms (time to receive payment), the larger the ultimate burden on cash flow. 10

12 How Factoring Works Genie Cloud First, let s define the participants in any factoring transaction. Payee (Seller of invoices) The Payee, also referred to as the Seller, is the company that has manufactured a product and shipped that product or rendered a service. In the factoring process, we call the seller a prospect/client. That company will now create an invoice for a sales transaction that has taken place. Buyer (factor) The buyer (factor) is the company that supplies the capital in a factoring transaction. The factor is commonly referred to as a funding source that buys invoices at a discount. Payor (also known as the debtor or customer) 11

The buyer (factor) is the company that supplies the capital in a factoring transaction.")

13 The payor is a company (customer) or government Genie Cloud agency that makes payments against an invoice of the Payee, the seller (prospect/client). The factoring process begins when a Payee (client) is introduced to a Buyer (Factor/Funding Source). The Buyer then makes their funding decisions based on whether or not the Payor has the credit strength to pay for the invoices and how long they typically take to pay for their invoices. Factors will also consider its ability to verify the delivery of products and/or services rendered to a Payor. The opportunity to make money in the factoring business is two fold. 1.As a Broker/Consultant Finding a Payee (company) that is in need of cash flow to assist them in growing their business or alternatively, needed to survive. 2.As an Investor or Funding Source Buying the payment or stream of payments (invoices) from a Payor (Customer) to a Payee (Company). 12

14 Genie Cloud Two Key Disbursements There are two key disbursements that are associated with a factoring facility. The first disbursement is called an Advance and the second disbursement is called the Reserve. Advance the client receives up to 90% of the face value (total) of the invoice when the invoice has been purchased by the factor. The advance rate depends on the risks involved with the transaction the greater the risk, the lower the advance. Reserve the client receives the reserve balance once the customer has paid for the invoice less the discount fee charged by the factor. For example - if the invoice is $1, and the Advance has been set at 85% by the factor, then the Reserve would be 15% (100% of invoice - 85% = 15%). The reserve is released once the invoice has been paid by the customer (typically referred to as a debtor). 13

15 Genie Cloud Two Key Disbursements There are two key disbursements that are associated with a factoring facility. The first disbursement is called an Advance and the second disbursement is called the Reserve. Advance the client receives up to 90% of the face value (total) of the invoice when the invoice has been purchased by the factor. The advance rate depends on the risks involved with the transaction the greater the risk, the lower the advance. Reserve the client receives the reserve balance once the customer has paid for the invoice less the discount fee charged by the factor. For example - if the invoice is $1, and the Advance has been set at 85% by the factor, then the Reserve would be 15% (100% of invoice - 85% = 15%). The reserve is released once the invoice has been paid by the customer (typically referred to as a debtor). 13

16 Factoring Terms Genie Cloud To help you better understand how Factoring works lets define some of the most commonly used terms that are used in a Factoring transaction: 1. Invoice - a business document defining the amount owed for a service rendered or product sold and delivered. An invoice can also be referred to as a legal document, or a short term note to the customer, when terms are listed on the invoice. 2. Accounts Receivable - an invoice (or group of invoices) that remain unpaid and is due to be payable in the future 3. Due Diligence- The process of evaluating the risks involved in funding a client. In factoring, this typically includes a number of actions including: review of financial statements, credit reviews on the clients customers, and payment history on past invoices. 4. Prospect A company in need of improved cash flow that is seeking alternative financing options 5. Client Once a prospect commits to a funding source (typically by signing a legal document called a Factoring and Security agreement), they become a client. 14

that remain unpaid and is due to be payable in the future 3. Due Diligence- The process of evaluating the risks involved in funding a client.")

17 Genie Cloud 6. Customer/Debtor the entity that has received a product or service and is now indebted to the client for payment. In most alternative financing scenarios, this must be a credit approved business or some form of public entity (government) 7. Factor a commercial entity that provides alternative financing options to various business. Factors specialize in purchasing business-to -usiness or business to-government accounts receivables at a discount. 8. Consultant typically a trained individual that acts as a match maker in a factoring transaction. Simply put, the consultant finds and introduces a prospect that is in need of financing to a funding source, such as a factor. 9. Discount Fee - the fee charged by the factor. The discount fee is typically charged on the face value (total) of the invoices and increases as the invoice ages. 15

18 Genie Cloud How do factors make money? When entering a discussion on how a factoring (funding Source) company makes money, you must first embrace the idea that a factor is not a lender. This is a grave error perpetrated by many who not only enter the field, but also by those companies who are considering using factoring as a tool to accelerate cash flow in their business. Why is this important, you ask? It is important for a few reasons: Annual Percentage Rate: We are all conditioned to believe the only way to get money is through a bank. After all, our first account was a passbook savings account at a bank. When we grew older and it was time to get a checking account, we secured this at a bank. To further the example, we ask: Where does the business owner turn to get a business checking account or a loan for his/her company? One thinks that the only place to get these things is at a bank. Therefore, it is safe to assume that whenever you are talking to a company about financing, they will equate you and in this case, factoring, to a bank. We must emphasize again that banks charge interest on money they lend while Factors buy invoices at a discount fee. No Lending, Different Regulations: Since factors are actually purchasing assets at a discount and not lending money, they are not regulated in the same way that banks are. This flexibility allows factors to pursue funding opportunities that are typically avoided by the banks (eg new start ups, companies with historic losses or liens against them). 16

19 Genie Cloud When a bank says No, why will a factor say Yes? Said another way, why would a factor fund a company that a bank won t lend to? When a bank makes a loan to a company, they are relying on that company s ability to pay back the loan. They look to hard assets like property, equipment, inventory and cash as security in the event the company defaults on the repayment of the loan. When a factor purchases an invoice at a discount, they are simply relying on the client s customer/debtor to pay the outstanding invoices, in full. To summarize, factors prosper by taking a different approach to commercial financing. Banks are making their credit decisions based on the strength of the borrower s assets. Factors make their credit decisions based on the credit strength of the Borrower s customers. 17

20 How do factors protect themselves against non payment (or short payment) of invoices? Genie Cloud The following is an example to demonstrate how this works: Invoice Amount: $100, Amount Advanced to Client = 80%: $ 80, Amount Held In Reserve = 20%: $ 20, Days Later: Amount paid by client s customer: $100, Advance amount back to factor: - 80, Discount Fee = 2.5% of invoice: Amount rebated to client: $

21 During the transaction, the amount held back Genie Cloud in Reserve serves to protect the factoring company against any potential credit offsets taken by the client s customer (debtor). If there were a credit taken by the client s customer, that amount would be subtracted from the reserve before rebating the remaining monies to the client. As you can see, in total, the client received an advance of $80,000 and a reserve rebate of $17,500 for a total of $97,500. The factor received a discount fee of $2500 for the service. Now imagine a factor managing hundreds of thousands of invoices at any given time, all of which are being purchased at a discount. The yield can certainly add up for the factor! Best of all, the client is getting the use of working capital which will make them stronger. A stronger client creates more invoices. In many cases that client will grow and factor all of their invoices. 19

22 How Do Cash Flow Consultants (YOU!) Make Money? The factoring industry is unique in that there Genie are Cloud several ways to get involved in the industry and make money. You can participate on any level, depending on your comfort level. Below are the most common ways to earn income: Consultants earn a residual fee or commission! As a consultant (broker) you will spend most of your time Finding and screening prospective small - to - medium sized businesses that are in need of accelerating their cashflow. Once you have identified a good prospect, you can now consolidate the initial information (asking them to complate a short client profile). The Finance Institute File Manager and the Factor will then take over and complete their due diligence. When the transaction closes, you will earn a residual fee. The great thing about being a consultant in the factoring industry is you continue to earn a fee or commission (residual) each and every time a factor buys invoices, the customer(s) pays for the invoice and the factor earns a fee. You continue to get paid your commission for the length of the relationship between the factor and the business client. This model applies to most, if not all factoring transactions. Typical commissions paid in the industry are up to fifteen percent (15%) of the factor s earned discount fee (the TFI pays 15%), depending on the type of transaction, the size of deal, and the fee the factor earns (As a consultant, you can stay involved in the transaction from start to finish or you can simply refer the transaction and let us and the factor perform the rest of the work.) After you accumulate money as a consultant, you may decide to factor some of your own transactions. However, we recommend that you only do this once you ve become familiar with all risks involved in managing a factoring portfolio. 20

23 Factoring Case Studies Genie Cloud Here are some real life case studies that will serve to better illustrate the benefits of factoring. Health Care Staffing First, we must define the players in the transaction. Payee Health care staffing company providing nurses to hospitals on a temporary employment basis (client) Buyer Funding Source (factor) Payor Hospitals (customer) Background: The health care staffing company sought out a consultant (an individual just like you) after being turned down by a local bank for funding. The consultant introduced and educated the staffing company on the benefits of factoring. The Current situation: Client was providing temporary nursing services to various hospitals. Client s major operating expense was in meeting the payroll demands of its temporary workforce (nursing) on a weekly basis. Client was receiving payment on invoices to hospitals in 60 days. However, the client had the ability to cash flow these expenditures out of current working capital. 21

24 Client received a phone call from a very large hospital informing them they had been awarded Genie Cloud a contract for 50 nurses to be employed 40 hours per week. The hospital was mandating 60 day payment terms on all invoices. The Math: Client (health care staffing company) pays its nurses (on average) $24.00 per hour. Client charges it s customers (on average) $32.00 per hour for hours worked. Hospital pays its invoices for services provided by the client in eight weeks or every 60 days. Client must pay nurses weekly for hours worked. In order to fulfill this new contract, the client is faced with the reality of having to come up with $384,000 in cash to cover the payroll burden: 50 (nurses) X $24.00 (average hourly pay) x 40 (hours worked per week) x 8 (number of weeks for hospital to pay) = $384,000. The Issue - The Bank: Client approaches the bank to request a loan for $500,000. Bank declines the loan due to insufficient collateral only asset is accounts receivables. In addition, the health care staffing company had only been in business for 16 months and did not have enough financial history. 22

25 The Solution: Genie Cloud Client is introduced to factor. The Factor reviews the credit history of the payor (hospital) and determines it to be a solid credit risk. The Factor agrees to advance 90% against invoices purchased. Keep in mind, the $24.00 per hour was not the amount that the client charged the hospital. If it were then the client would not earn a profit. In this transaction the client charged the hospital $32.00 per hour, so the client earned $8.00 per hour (gross profit) for each hour the nurses worked ($32.00 amount charged to hospital - $24.00 amount paid to each nurse = $8.00) 50 (nurses) X $32.00 (average hourly pay) x 40 (hours worked per week) x 8 (number of weeks for hospital to pay) = $512,000 The Factor will Advance (first key disbursement) 90% against invoices created: $512,000 X 90% = $460,800 Note: Keep in mind that Factor will fund weekly based on verified hours worked per nurse. This figure provides an aggregrate amount that is funded over the 8 week period. Since the payroll burden is $384,000, The Factor s advance of $460,800 is more than enough to cover the payroll and provide additional working capital over the eight week time period. The client now has additional working capital to source out new contracts, and to help meet fixed costs like rent, telephone, utility payments, etc. A win-win situation! 23

26 Delta Components Situtation Genie Cloud Delta Components, Inc. ( Delta ) is a relatively small distribution company located in Reston, VA. Delta currently has just over $500,000 in revenues and during the past year, Delta enjoyed significant sales growth. While most business owners would be thrilled to experience the growth that Delta has, Ron Cotton (Principal), was very concerned that his company s cash flow status would be unable to keep pace with its sales growth. The majorities of Delta s customers are strong financially and have a history of paying their invoices on time. However, on time these days means 45 to 60 days. Delta pays their employees every week and they must pay their vendors in 30 days. The discrepancy between the time Delta needs to pay their employees and vendors has, and will continue to create a cash flow problem for Delta. In an effort to meet his internal cash flow needs, Ron has delayed vendor payments resulting in placing his purchasing power at risk. This could result in his vendors implementing more restrictive payment policies (basically, Delta would need to pay faster, if not up front, in order to receive future shipments from the vendors). This lack of cash flow has also caused Ron to take a pass on a number of significant business opportunities. In Ron s mind, it did not make sense to just take on new orders if it meant increasing his inability to pay his vendors on time, and most importantly, hindering his need to pay his employees on time. To better illustrate Delta s current position, review the following table: 24

27 Genie Cloud Delta Components, Inc. Current financial position (without factoring) Yearly Sales $500,000 Variable costs (70% of sales) $350,000 Fixed Costs $50,000 Total Costs $400,000 Gross Profit/Loss (Sales - Costs) $100,000 Note: Ron has calculated that he has lost close to $200,000 in sales opportunities due to the fact that he did not have the cash needed to pay his vendors on time, nor to pay his employees, which were both needed to fulfill on these commitments. Ron was being forced to make a decision that would dictate the future success or failure of Delta. Find a way to increase the cash flow within the company or continue to turn down future sales/growth opportunities. Ron reviewed his options for improving his cash flow. 25

28 First, Ron reviewed the options that were available to him without seeking financing: Genie Cloud 1. Demand more strict payment terms from his customers 2. Increase the sale price of his products 3. Negotiate more conservative payment terms to his vendors 4. Reduce employee cash burdens (eg... insurance, bonus, wage increases or possible layoffs) 5. Delay his payment of payroll taxes After much thought, Ron came to the following conclusions: Options 1 and 2 were not possible. Demanding his customers to pay their invoices faster was a recipe for disaster as his competitors were offering more liberal payment terms now in an effort to induce his customers to conduct business with them. Raising his prices would position him as unattractive option to his customers. Ron was in a very competitive business, and his customers would simply choose to buy their products from another, less expensive resource. Option 3 was not possible. His vendors had already placed him on credit hold. Asking them to now give him more liberal payment terms would be counter intuitive. Option 4 was not possible: Simply put, if Ron were to increase his business, he would need all his employees, if not more, to work for him. In order for him to either keep current or attract new employees, he would have to offer competitive wages and benefits to bring them to Delta. 26

29 Option 5 was an option, but, a potential death Genie Cloud blow to Delta. Avoiding the payment of employee tax burdens to the government is never a good long term solutions. Although the impact of not paying the taxes will result in an immediate improvement in cash flow, the long term implications could amount to tax liens and high financial penalties due. If Ron was unable to recover cash by making internal changes to his business, he must now look to outside financing to help him. Ron viewed his outside financing options as: 1. A line of credit with a bank 2. Offering ownership (equity) in his company, in exchange for working capital 3. Factoring Delta s accounts receivables It is necessary to keep in mind that while Ron was considering all options, he was losing orders (daily) with potential customers that may never return. Ron knew that a line of credit with a bank was not a valid option, as he attempted this in recent memory and knew that he did not have the collateral needed to secure a loan. Ron had been approached in the past by a few potential investors, but this option came at a very high price, as he would have to give up ownership and control of his company in exchange for cash. 27

30 Genie Cloud Ron determined that an accounts receivable factoring line of working capital would be the best solution to help his company strengthen his company s financial position. This would enable Delta to now accept new orders and to pay both vendors and employees on time. In fact, the acceleration of cash into his business would put Ron into a position of strength with vendors in that he could now be in a position to negotiate early payment discounts. Ron negotiated a 90% advance with The Factor and a discount rate of 2.5% (per 30 days). Since Delta was now getting paid on average in 60 days, Ron budgeted a discount rate of 5%. Ron then reconstructed his financial statements by adding the following: 1. The 5% factoring discount rate 2. The projected $200,000 increase in new business 3. Supplier discounts offered for quick pay. 28

31 Delta Components, Inc. projected financial position (with Factoring) Genie Cloud Yearly Sales $700,000 (Note: Increase of $200,000 from new orders) Variable costs (65% of sales) $455,000 (Note: 5% supplier discounts) Factoring discount fees (Note: 5% of sales) $35,000 Fixed Costs $50,000 Total Costs $540,000 Gross Profit/Loss (Sales - Costs) $160,000 Additional Profit of $60,000, or 60%! Therefore, by selling his invoices and ultimately giving a 5% discount to the factor, Delta gained 60% in profits - truly, addition by subtraction! 29

32 Genie Cloud The Finance Institute s FEES Principle What are the steps to funding a factoring prospect? Everything begins with YOU, the "Consultant". Understanding the FEES principal and the steps involved are crucial to closing deals. Similar to building a sturdy house, your factoring business must begin with a strong foundation. This foundation must be reinforced through proper education and training. Reading this E-book is a good first step. It is crucial that you understand the FEES principle as it creates the building blocks to success in this dynamic industry. Let s now break down the term FEES and show you how this relates to your success in this industry. F (F)ind them As a consultant your core mission is to find a business (prospect) that is need of cash flow to help them grow or in many cases survive. 30

Genie. Who Should Read This Report?

Genie The core mission of the Finance Institute ( TFI ) is lead generation to the Alternative Finance Industry. TFI delivers on this mission by quickly educating, guiding and supporting an elite consultant

Genie The core mission of the Finance Institute ( TFI ) is lead generation to the Alternative Finance Industry. TFI delivers on this mission by quickly educating, guiding and supporting an elite consultant

Learn to Profit from Factoring

Learn to Profit from Factoring 2005-2016 The Finance Institute The History of Factoring Recorded history reveals that the concept of turning future payments into cash ( or cash equivalents) dates back

Learn to Profit from Factoring 2005-2016 The Finance Institute The History of Factoring Recorded history reveals that the concept of turning future payments into cash ( or cash equivalents) dates back

Genie. and ongoing education programs available in the industry today.

Genie The core mission of the Finance Institute ( TFI ) is to educate, enlighten and inspire individuals to transform their actions into success. TFI delivers on this mission by offering the most informationpacked,

Genie The core mission of the Finance Institute ( TFI ) is to educate, enlighten and inspire individuals to transform their actions into success. TFI delivers on this mission by offering the most informationpacked,

Factoring Facts Revealed

Factoring Facts Revealed Everything you need to know about the Factoring Industry and how it could benefit your business! Williamsville, New York, USA Toronto, Ontario, Canada Asheville, NC, USA 1 P a

Factoring Facts Revealed Everything you need to know about the Factoring Industry and how it could benefit your business! Williamsville, New York, USA Toronto, Ontario, Canada Asheville, NC, USA 1 P a

Rethinking Seller-Financing!

Jeff Bennett 201-580-4228 jeff@thenotecoach.com www.thenotecoach.com Rethinking Seller-Financing! How Real Estate Agents Can Close More Deals and Earn Higher Commissions By Jeff Bennett As a real estate

Jeff Bennett 201-580-4228 jeff@thenotecoach.com www.thenotecoach.com Rethinking Seller-Financing! How Real Estate Agents Can Close More Deals and Earn Higher Commissions By Jeff Bennett As a real estate

- Your Business Credit and Funding System - We secure Funding for your Business

We secure Funding for your Business Your Business Credit and Funding System It is said that almost 50% of new businesses fail in their first 2 years. The reason for their failure in many cases is lack

We secure Funding for your Business Your Business Credit and Funding System It is said that almost 50% of new businesses fail in their first 2 years. The reason for their failure in many cases is lack

How To Get Credit Risk Out Of Your Business

Receivables insurance Protection against the biggest unidentified exposure facing Canadian business Presentation to: Alberta Trade Contractors Coalition By: Ian Miller Receivables Insurance Association

Receivables insurance Protection against the biggest unidentified exposure facing Canadian business Presentation to: Alberta Trade Contractors Coalition By: Ian Miller Receivables Insurance Association

How to Assess Your Financial Planning and Loan Proposals By BizMove Management Training Institute

How to Assess Your Financial Planning and Loan Proposals By BizMove Management Training Institute Other free books by BizMove that may interest you: Free starting a business books Free management skills

How to Assess Your Financial Planning and Loan Proposals By BizMove Management Training Institute Other free books by BizMove that may interest you: Free starting a business books Free management skills

Small Business Brief How to Build and Use Credit Policies to Your Advantage

How to Build and Use Credit Policies to Your Advantage Customers are your bread and butter, but they can also be your biggest risk. Now more than ever, small businesses need to take a page from some of

How to Build and Use Credit Policies to Your Advantage Customers are your bread and butter, but they can also be your biggest risk. Now more than ever, small businesses need to take a page from some of

Toll Free: 1.888.XPORTSK (9767875) (in North America) Email: inquire@sasktrade.sk.ca www.sasktrade.sk.ca

(in North America) Email: inquire@sasktrade.sk.ca www.sasktrade.sk.ca") These manuals are created as resource guides for members of Saskatchewan Trade and Export Partnership (STEP). For more information on these manuals please contact Saskatchewan Trade and Export Partnership

These manuals are created as resource guides for members of Saskatchewan Trade and Export Partnership (STEP). For more information on these manuals please contact Saskatchewan Trade and Export Partnership

ABOUT FINANCIAL RATIO ANALYSIS

ABOUT FINANCIAL RATIO ANALYSIS Over the years, a great many financial analysis techniques have developed. They illustrate the relationship between values drawn from the balance sheet and income statement

ABOUT FINANCIAL RATIO ANALYSIS Over the years, a great many financial analysis techniques have developed. They illustrate the relationship between values drawn from the balance sheet and income statement

The Entrepreneur s Guide to Financial Maturity Factoring - Financing for Companies Seeking Fast Cash

The Entrepreneur s Guide to Financial Maturity Factoring - Financing for Companies Seeking Fast Cash A healthy cash flow is an essential part of any successful business. Some entrepreneurs claim that a

The Entrepreneur s Guide to Financial Maturity Factoring - Financing for Companies Seeking Fast Cash A healthy cash flow is an essential part of any successful business. Some entrepreneurs claim that a

WHAT DO BANKERS LOOK FOR IN A BUSINESS LOAN APPLICATION

WHAT DO BANKERS LOOK FOR IN A BUSINESS LOAN APPLICATION Whether you are applying to a bank for a line of home equity credit, a line of credit for business working capital, a commercial short-term loan,

WHAT DO BANKERS LOOK FOR IN A BUSINESS LOAN APPLICATION Whether you are applying to a bank for a line of home equity credit, a line of credit for business working capital, a commercial short-term loan,

Factoring. from a Business Owner s Perspective

Factoring from a Business Owner s Perspective History Factoring Basics Factoring is the act of selling an asset at a discount for the advantage of immediate cash. As a business, it has been around for

Factoring from a Business Owner s Perspective History Factoring Basics Factoring is the act of selling an asset at a discount for the advantage of immediate cash. As a business, it has been around for

Equity Release Guide. www.seniorissues.co.uk

Equity Release Guide www.seniorissues.co.uk For more information or to speak to one of our trained advisers please telephone our Senior Issues Team on 0845 855 4411 The Caesar & Howie Group 7/3/2008 EQUITY

Equity Release Guide www.seniorissues.co.uk For more information or to speak to one of our trained advisers please telephone our Senior Issues Team on 0845 855 4411 The Caesar & Howie Group 7/3/2008 EQUITY

Arizona Property Advisors LLC

PRIVATE MORTGAGE INVESTING ARIZONA PROPERTY ADVISORS LLC www.buyazcashflow.com 480-228-3336 Table of Contents The Basics of Private Mortgages 1 What is a Private Mortgage? 1 Why Would Someone Borrow From

PRIVATE MORTGAGE INVESTING ARIZONA PROPERTY ADVISORS LLC www.buyazcashflow.com 480-228-3336 Table of Contents The Basics of Private Mortgages 1 What is a Private Mortgage? 1 Why Would Someone Borrow From

Tips for First Time Home Buyers

Tips for First Time Home Buyers Thinking about buying your first home? Andrew L. Jaloza & Associates will help you understand the process of home ownership so you can make informed decisions about your

Tips for First Time Home Buyers Thinking about buying your first home? Andrew L. Jaloza & Associates will help you understand the process of home ownership so you can make informed decisions about your

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account.

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account. Account fee the amount charged by a financial institution for the

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account. Account fee the amount charged by a financial institution for the

C&I LOAN EVALUATION UNDERWRITING GUIDELINES. A Whitepaper

C&I LOAN EVALUATION & UNDERWRITING A Whitepaper C&I Lending Commercial and Industrial, or C&I Lending, has long been a cornerstone product for many successful banking institutions. Also known as working

C&I LOAN EVALUATION & UNDERWRITING A Whitepaper C&I Lending Commercial and Industrial, or C&I Lending, has long been a cornerstone product for many successful banking institutions. Also known as working

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Simply put, factoring is a transaction where a company sells its invoices at a discount in exchange for quick funds.

Imagine your growing business just made a six-figure sale to a company across the country. The problem? The buyer has 60 days to pay, but your cash flow is limited, meaning you can t afford the immediate

Imagine your growing business just made a six-figure sale to a company across the country. The problem? The buyer has 60 days to pay, but your cash flow is limited, meaning you can t afford the immediate

Referral Agents Wanted: Realizing Your Opportunity

The Cash Flow Solution Business Accelerator Referral Agents Wanted: Realizing Your Opportunity Alternative Financing Solutions Presentation Presented by: Gary T Phillips, Director/Business Consultant Office:

The Cash Flow Solution Business Accelerator Referral Agents Wanted: Realizing Your Opportunity Alternative Financing Solutions Presentation Presented by: Gary T Phillips, Director/Business Consultant Office:

Course 4: Managing Cash Flow

Excellence in Financial Management Course 4: Managing Cash Flow Prepared by: Matt H. Evans, CPA, CMA, CFM This course provides an introduction to cash flow management. This course is recommended for 2

Excellence in Financial Management Course 4: Managing Cash Flow Prepared by: Matt H. Evans, CPA, CMA, CFM This course provides an introduction to cash flow management. This course is recommended for 2

How To Factoring

THE BASICS OF FACTORING A Guide to Understanding Accounts Receivable Financing The Basics of Factoring Table of Contents What is Factoring?.. 1 Benefits of Factoring 4 What Types of Businesses Utilize

THE BASICS OF FACTORING A Guide to Understanding Accounts Receivable Financing The Basics of Factoring Table of Contents What is Factoring?.. 1 Benefits of Factoring 4 What Types of Businesses Utilize

GETTING A BUSINESS LOAN

GETTING A BUSINESS LOAN With few exceptions, most businesses require an influx of cash now and then. Sometimes it is for maintaining growth; sometimes it is for maintaining the status quo. From where does

GETTING A BUSINESS LOAN With few exceptions, most businesses require an influx of cash now and then. Sometimes it is for maintaining growth; sometimes it is for maintaining the status quo. From where does

HOME LOAN GUIDE. Call 1300 17 87 87 1ststreet.com.au

HOME LOAN GUIDE Call 1300 17 87 87 1ststreet.com.au CONTENTS FIND ALL YOU NEED TO KNOW 4 6 8 10 12 16 18 19 22 24 26 1st Street The Story Your 1st Street Mortgage Broker Lender Options The Plan Lenders

HOME LOAN GUIDE Call 1300 17 87 87 1ststreet.com.au CONTENTS FIND ALL YOU NEED TO KNOW 4 6 8 10 12 16 18 19 22 24 26 1st Street The Story Your 1st Street Mortgage Broker Lender Options The Plan Lenders

FundingEdge / Power2Fund

Factoring Defined In the world of finance, factoring is a transaction in which a business sells its account receivables to a third party--called a "factor"--in return for immediate cash, generally working

Factoring Defined In the world of finance, factoring is a transaction in which a business sells its account receivables to a third party--called a "factor"--in return for immediate cash, generally working

The Business Credit & Funding Platform

Your Business Credit and Funding suite The Business Credit & Funding Platform 2012 Dispute Suite, all rights reserved. No reproduction or use of any portion of the content or work or the entire work is

Your Business Credit and Funding suite The Business Credit & Funding Platform 2012 Dispute Suite, all rights reserved. No reproduction or use of any portion of the content or work or the entire work is

SMALL BUSINESS OWNER S HANDBOOK

SMALL BUSINESS OWNER S HANDBOOK PART II: FINANCIAL PLANNING FOR SMALL BUSINESSES Introduction Financial Planning Methods of Financing Your Business Other Types of Funds & Financing How to Approach Lenders

SMALL BUSINESS OWNER S HANDBOOK PART II: FINANCIAL PLANNING FOR SMALL BUSINESSES Introduction Financial Planning Methods of Financing Your Business Other Types of Funds & Financing How to Approach Lenders

THE FACTORING ESSENTIALS

THE FACTORING ESSENTIALS New Cash Flow Consultants often come to Working Capital Company asking for help ranging from how to make a sales call to writing sample marketing letters. WCC has listened to our

THE FACTORING ESSENTIALS New Cash Flow Consultants often come to Working Capital Company asking for help ranging from how to make a sales call to writing sample marketing letters. WCC has listened to our

Business Plan Workbook

Business Plan Workbook Developed by the staff of the Niagara County Community College Small Business Development Center 3111 Saunders Settlement Rd Sanborn, NY 14132 7162102515 www.niagarasbdc.org Call

Business Plan Workbook Developed by the staff of the Niagara County Community College Small Business Development Center 3111 Saunders Settlement Rd Sanborn, NY 14132 7162102515 www.niagarasbdc.org Call

Mortgage Advisers. The Mortgage Guide Helping you find the right mortgage for you

Mortgage Advisers The Mortgage Guide Helping you find the right mortgage for you Hello. We re the Which? Mortgage Advisers team. Buying a house is the biggest financial commitment most of us ever make.

Mortgage Advisers The Mortgage Guide Helping you find the right mortgage for you Hello. We re the Which? Mortgage Advisers team. Buying a house is the biggest financial commitment most of us ever make.

Financial. Management FOR A SMALL BUSINESS

Financial Management FOR A SMALL BUSINESS 1 Agenda Welcome, Pre-Test, Agenda, and Learning Objectives Benefits of Financial Management Budgeting Bookkeeping Financial Statements Business Financing Key

Financial Management FOR A SMALL BUSINESS 1 Agenda Welcome, Pre-Test, Agenda, and Learning Objectives Benefits of Financial Management Budgeting Bookkeeping Financial Statements Business Financing Key

WELCOME COURSE OUTLINE

WELCOME COURSE OUTLINE Dear Home Buyer: Thank you for giving us the opportunity to help guide you through your home lending process. It is typically the largest financial transaction you will make and

WELCOME COURSE OUTLINE Dear Home Buyer: Thank you for giving us the opportunity to help guide you through your home lending process. It is typically the largest financial transaction you will make and

First Time Home Buyer Glossary

First Time Home Buyer Glossary For first time home buyers, knowing and understanding the following terms are very important when purchasing your first home. By understanding these terms, you will make

First Time Home Buyer Glossary For first time home buyers, knowing and understanding the following terms are very important when purchasing your first home. By understanding these terms, you will make

Outsourcing Accounts Receivable to Increase Cash Flow

Outsourcing Accounts Receivable to Increase Cash Flow Outsourcing Accounts Receivable to Increase Cash Flow In the current economic environment, small and medium-size businesses are facing unprecedented

Outsourcing Accounts Receivable to Increase Cash Flow Outsourcing Accounts Receivable to Increase Cash Flow In the current economic environment, small and medium-size businesses are facing unprecedented

Guide to Purchasing a Home

Your journey to homeownership starts at your credit union. Purchasing your first home is a big decision, and it may even seem overwhelming. Rest assured Beacon Credit Union is here to assist you in understanding

Your journey to homeownership starts at your credit union. Purchasing your first home is a big decision, and it may even seem overwhelming. Rest assured Beacon Credit Union is here to assist you in understanding

The Mortgage Guide. Helping you find the right mortgage for you. Brought to you by. V0050713a

The Mortgage Guide Helping you find the right mortgage for you Brought to you by Hello. Contents We re the Which? Mortgage Advisers team. Buying a house is the biggest financial commitment most of us ever

The Mortgage Guide Helping you find the right mortgage for you Brought to you by Hello. Contents We re the Which? Mortgage Advisers team. Buying a house is the biggest financial commitment most of us ever

How to Sell Your Property Fast and For Top Dollar!

SPECIAL REPORT How to Sell Your Property Fast and For Top Dollar! A Guide for Home Sellers to Help Attract An Unlimited Number of Buyers for Your Property This publication is designed to provide accurate

SPECIAL REPORT How to Sell Your Property Fast and For Top Dollar! A Guide for Home Sellers to Help Attract An Unlimited Number of Buyers for Your Property This publication is designed to provide accurate

Financing you can count on! www.thnlending.com

Financing you can count on! www.thnlending.com What s included in the Acquisition of THN Lending THN Lending has a perfect credit rating (Debt Free) 2 American Express Credit Cards with limits of $20k

Financing you can count on! www.thnlending.com What s included in the Acquisition of THN Lending THN Lending has a perfect credit rating (Debt Free) 2 American Express Credit Cards with limits of $20k

First Timer s Guide PREParing First Time Homebuyers

First Timer s Guide PREParing First Time Homebuyers SO MANY QUESTIONS Maybe you live in the best apartment with a great landlord and don t want to change a thing. Or maybe you ve looked at the rent going

First Timer s Guide PREParing First Time Homebuyers SO MANY QUESTIONS Maybe you live in the best apartment with a great landlord and don t want to change a thing. Or maybe you ve looked at the rent going

Using Credit to Your Advantage.

Using Credit to Your Advantage. Topic Overview. The Using Credit To Your Advantage topic will provide participants with all the basic information they need to understand credit what it is and how to make

Using Credit to Your Advantage. Topic Overview. The Using Credit To Your Advantage topic will provide participants with all the basic information they need to understand credit what it is and how to make

Evaluate Performance: Balance Sheet

Excerpted from FastTrac GrowthVenture Financial statements and reports must be read together to learn the whole financial story. For example, an Income Statement may report a large sale to a new customer,

Excerpted from FastTrac GrowthVenture Financial statements and reports must be read together to learn the whole financial story. For example, an Income Statement may report a large sale to a new customer,

Financial. Management FOR A SMALL BUSINESS

Financial Management FOR A SMALL BUSINESS Welcome 1. Agenda 2. Ground Rules 3. Introductions FINANCIAL MANAGEMENT 2 Objectives Explain the concept of financial management and its importance to a small

Financial Management FOR A SMALL BUSINESS Welcome 1. Agenda 2. Ground Rules 3. Introductions FINANCIAL MANAGEMENT 2 Objectives Explain the concept of financial management and its importance to a small

B NR Consulting Network - The Truth About Business Credit

2007-2008 Edition BNR Consulting Network 11/17/2007 2 What is business credit? Many business owners are unaware of corporate credit and how to obtain it. BNR Consulting Network is proud to be one of very

2007-2008 Edition BNR Consulting Network 11/17/2007 2 What is business credit? Many business owners are unaware of corporate credit and how to obtain it. BNR Consulting Network is proud to be one of very

Understanding Financial Statements. For Your Business

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Real Estate & Mortgage Investment Specialists

Your Real Estate & Mortgage Investment Specialists Private Lending FAQ s 1. Why Should I Invest In A Mortgage? A mortgage is a loan in which real estate or property is used as collateral. When an individual

Your Real Estate & Mortgage Investment Specialists Private Lending FAQ s 1. Why Should I Invest In A Mortgage? A mortgage is a loan in which real estate or property is used as collateral. When an individual

THE WORKING CAPITAL CYCLE IN INTERNATIONAL TRADE

THE WORKING CAPITAL CYCLE IN INTERNATIONAL TRADE Introduction The working capital cycle is the period of time which elapses between the points at which cash is used in the supply/production process, to

THE WORKING CAPITAL CYCLE IN INTERNATIONAL TRADE Introduction The working capital cycle is the period of time which elapses between the points at which cash is used in the supply/production process, to

Structured Settlements: A Buyer s Guide

Learn more about court-ordered structured settlement transfers, what makes them attractive and how they can help you reach your financial goals for the future. WHAT IS A STRUCTURED SETTLEMENT? For the

Learn more about court-ordered structured settlement transfers, what makes them attractive and how they can help you reach your financial goals for the future. WHAT IS A STRUCTURED SETTLEMENT? For the

Business finance. a practical guide BUILDING YOUR KNOWLEDGE. smallbusiness.wa.gov.au. The small business specialists

Business finance a practical guide BUILDING YOUR KNOWLEDGE Small Business Development Corporation 13 12 49 smallbusiness.wa.gov.au The small business specialists A practical guide to business finance An

Business finance a practical guide BUILDING YOUR KNOWLEDGE Small Business Development Corporation 13 12 49 smallbusiness.wa.gov.au The small business specialists A practical guide to business finance An

Xynergy Commercial Capital LLC

Xynergy Commercial Capital LLC How Can Work For You The Problem Short of cash and must pay suppliers, lease, bills and salaries? No need for stress, get your payments in advance for your invoices and pay

Xynergy Commercial Capital LLC How Can Work For You The Problem Short of cash and must pay suppliers, lease, bills and salaries? No need for stress, get your payments in advance for your invoices and pay

Small-Business Financing: Why are companies choosing to factor and how does it work?

Small-Business Financing: Why are companies choosing to factor and how does it work? Small-Business Financing: Why are companies choosing to factor and how does it work? Your company just received a big

Small-Business Financing: Why are companies choosing to factor and how does it work? Small-Business Financing: Why are companies choosing to factor and how does it work? Your company just received a big

Guide. for. Adapted with

Disaster Recovery Guide for r Business Presented : You may be in business for yourself but you don t have to be in business by yourself Adapted with permission from the Hawai i SBDC Disaster Recovery Guide

Disaster Recovery Guide for r Business Presented : You may be in business for yourself but you don t have to be in business by yourself Adapted with permission from the Hawai i SBDC Disaster Recovery Guide

6 GOLDEN RULES FOR SECURING YOUR COMPANY S FINANCIAL FUTURE

6 GOLDEN RULES FOR SECURING YOUR COMPANY S FINANCIAL FUTURE w w w. u n i v e r s a l f u n d i n g. c o m 1-800- 4 9 9-1 2 1 8 TABLE OF CONTENTS Introduction Why we wrote this and how you can use it to

6 GOLDEN RULES FOR SECURING YOUR COMPANY S FINANCIAL FUTURE w w w. u n i v e r s a l f u n d i n g. c o m 1-800- 4 9 9-1 2 1 8 TABLE OF CONTENTS Introduction Why we wrote this and how you can use it to

How To Fund A Cash Flow Strong Business

STRUCTURE YOUR LABOUR HIRE BUSINESS SO CASHFLOW IS NEVER A PROBLEM EDGEVIEW DIRECT 1 REVENUE IS VANITY MARGIN IS SANITY CASH IS KING! - KEITH C. MACDONALD EDGEVIEW DIRECT 2 It s often touted as common

STRUCTURE YOUR LABOUR HIRE BUSINESS SO CASHFLOW IS NEVER A PROBLEM EDGEVIEW DIRECT 1 REVENUE IS VANITY MARGIN IS SANITY CASH IS KING! - KEITH C. MACDONALD EDGEVIEW DIRECT 2 It s often touted as common

Alternative Financing: Using Corporate Payment Solutions to Help Manage Cash Flow

AMERICAN EXPRESS PAYMENT SOLUTIONS Alternative Financing: Using Corporate Payment Solutions to Help Manage Cash Flow Global Corporate Payments Alternative Financing: Using Corporate Payment Solutions to

AMERICAN EXPRESS PAYMENT SOLUTIONS Alternative Financing: Using Corporate Payment Solutions to Help Manage Cash Flow Global Corporate Payments Alternative Financing: Using Corporate Payment Solutions to

Investing in unlisted property schemes?

Investing in unlisted property schemes? Independent guide for investors about unlisted property schemes This guide is for you, whether you re an experienced investor or just starting out. Key tips from

Investing in unlisted property schemes? Independent guide for investors about unlisted property schemes This guide is for you, whether you re an experienced investor or just starting out. Key tips from

In this chapter, we build on the basic knowledge of how businesses

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

The. Path. Refinancing. www.totalmortgage.com October. totalmortgage.com 877-868-2503

The Path Refinancing totalmortgage.com 877-868-2503 www.totalmortgage.com October 1 2012 The Path Refinancing Over time, many things change and need adjustment, and the reality is your home financing is

The Path Refinancing totalmortgage.com 877-868-2503 www.totalmortgage.com October 1 2012 The Path Refinancing Over time, many things change and need adjustment, and the reality is your home financing is

Best Practices: B2B Small Business Accounts Receivable

Best Practices: B2B Small Business Accounts Receivable Best Practices: B2B Small Business Accounts Receivable By Dan Drechsel For most business to business companies, their largest asset is also the most

Best Practices: B2B Small Business Accounts Receivable Best Practices: B2B Small Business Accounts Receivable By Dan Drechsel For most business to business companies, their largest asset is also the most

Q: Will I have to pay federal taxes on the money my lender loses in the short sale?

Q: What is a Short Sale? Answer: In a short sale, the lender agrees to settle the debt owed on the property for less than the full amount. Settled means that the lender is writing off the debt (which is

Q: What is a Short Sale? Answer: In a short sale, the lender agrees to settle the debt owed on the property for less than the full amount. Settled means that the lender is writing off the debt (which is

Short Term Loans and Lines of Credit

Short Term Loans and Lines of Credit Disadvantaged Business Enterprise (DBE) Supportive Services Program The contents of this training course reflect the views of the author who is responsible for the

Short Term Loans and Lines of Credit Disadvantaged Business Enterprise (DBE) Supportive Services Program The contents of this training course reflect the views of the author who is responsible for the

BSM Connection elearning Course

BSM Connection elearning Course Basics of Medical Practice Finance: Part 2 2009, BSM Consulting All rights reserved. Table of Contents OVERVIEW... 1 PRACTICE PERFORMANCE RATIOS... 1 UNDERSTANDING THE CONCEPT

BSM Connection elearning Course Basics of Medical Practice Finance: Part 2 2009, BSM Consulting All rights reserved. Table of Contents OVERVIEW... 1 PRACTICE PERFORMANCE RATIOS... 1 UNDERSTANDING THE CONCEPT

Prepare for business. Prepare for success

Prepare for business Decisions you take in the early years of your business can be the most difficult as well as the most important, particularly if you are a first-time entrepreneur. Prepare for success

Prepare for business Decisions you take in the early years of your business can be the most difficult as well as the most important, particularly if you are a first-time entrepreneur. Prepare for success

Performance Review for Electricity Now

Performance Review for Electricity Now For the period ending 03/31/2008 Provided By Mark Dashkewytch 780-963-5783 Report prepared for: Electricity Now Industry: 23821 - Electrical Contractors Revenue:

Performance Review for Electricity Now For the period ending 03/31/2008 Provided By Mark Dashkewytch 780-963-5783 Report prepared for: Electricity Now Industry: 23821 - Electrical Contractors Revenue:

UNDERSTANDING WHERE YOU STAND. A Simple Guide to Your Company s Financial Statements

UNDERSTANDING WHERE YOU STAND A Simple Guide to Your Company s Financial Statements Contents INTRODUCTION One statement cannot diagnose your company s financial health. Put several statements together

UNDERSTANDING WHERE YOU STAND A Simple Guide to Your Company s Financial Statements Contents INTRODUCTION One statement cannot diagnose your company s financial health. Put several statements together

MANAGING YOUR BUSINESS S CASH FLOW. Managing Your Business s Cash Flow. David Oetken, MBA CPM

MANAGING YOUR BUSINESS S CASH FLOW Managing Your Business s Cash Flow David Oetken, MBA CPM 1 2 Being a successful entrepreneur takes a unique mix of skills and practices. You need to generate exciting

MANAGING YOUR BUSINESS S CASH FLOW Managing Your Business s Cash Flow David Oetken, MBA CPM 1 2 Being a successful entrepreneur takes a unique mix of skills and practices. You need to generate exciting

WHAT YOU SHOULD KNOW!! By Speare Valasakos & Lance D. Churchill, J.D. Compliments of:

TRUST DEED INVESTMENTS WHAT YOU SHOULD KNOW!! By Speare Valasakos & Lance D. Churchill, J.D. Compliments of: F FRONTLINE Financing L 967 E. Parkcenter Blvd., #311 Boise, ID 83706 Phone: 208 846 9644 Fax:

TRUST DEED INVESTMENTS WHAT YOU SHOULD KNOW!! By Speare Valasakos & Lance D. Churchill, J.D. Compliments of: F FRONTLINE Financing L 967 E. Parkcenter Blvd., #311 Boise, ID 83706 Phone: 208 846 9644 Fax:

STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

WELCOME TO THE MASCIA LAW FIRM NEW CLIENT PACKAGE

In these trying times you need a law firm that believes in you, A firm that will make the impossible, POSSIBLE. WELCOME TO THE MASCIA LAW FIRM NEW CLIENT PACKAGE A WELCOME LETTER FROM MASCIA LAW FIRM On

In these trying times you need a law firm that believes in you, A firm that will make the impossible, POSSIBLE. WELCOME TO THE MASCIA LAW FIRM NEW CLIENT PACKAGE A WELCOME LETTER FROM MASCIA LAW FIRM On

ReverseMortgages.com, Inc. A Guide to Reverse Mortgages

ReverseMortgages.com, Inc. A Guide to Reverse Mortgages Table of of Contents Introduction Introduction Our Commitment to You Is a Reverse Mortgage Right for You? Getting Your Reverse Mortgage: Questions

ReverseMortgages.com, Inc. A Guide to Reverse Mortgages Table of of Contents Introduction Introduction Our Commitment to You Is a Reverse Mortgage Right for You? Getting Your Reverse Mortgage: Questions

Foreclosure Prevention Guide

Foreclosure Prevention Guide 8 Ways to Stop Your Foreclosure in Today s Challenging Economy About Foreclosure Foreclosure begins when a Homeowner is unable to make their mortgage payments on the scheduled

Foreclosure Prevention Guide 8 Ways to Stop Your Foreclosure in Today s Challenging Economy About Foreclosure Foreclosure begins when a Homeowner is unable to make their mortgage payments on the scheduled

Smart strategies for using debt 2012/13

Smart strategies for using debt 2012/13 Appreciating the value of debt William Shakespeare wrote, Neither a borrower nor a lender be, but the fact is debt can be a very useful tool when used properly.

Smart strategies for using debt 2012/13 Appreciating the value of debt William Shakespeare wrote, Neither a borrower nor a lender be, but the fact is debt can be a very useful tool when used properly.

The ABC s of 123 s. (The Simple Secrets to Accounting Wisdom.)

") The ABC s of 123 s (The Simple Secrets to Accounting Wisdom.) Thank You for attending our QuickBooks seminar today. Your time is valuable and our goal is to make sure it is well spent. QuickBooks is a

The ABC s of 123 s (The Simple Secrets to Accounting Wisdom.) Thank You for attending our QuickBooks seminar today. Your time is valuable and our goal is to make sure it is well spent. QuickBooks is a

Using debt effectively Smart strategies for 2015 2016

Using debt effectively Smart strategies for 2015 2016 William Shakespeare wrote, Neither a borrower nor a lender be, but the fact is debt can be a very useful tool when used properly. Contents The value

Using debt effectively Smart strategies for 2015 2016 William Shakespeare wrote, Neither a borrower nor a lender be, but the fact is debt can be a very useful tool when used properly. Contents The value

A Guide to Equity Release in Retirement

A Guide to Equity Release in Retirement 1. Introduction For the retirement you deserve 2. What is Equity Release? 3. Equity Release Plans The options available to you 4. The Application Process 5. Questions

A Guide to Equity Release in Retirement 1. Introduction For the retirement you deserve 2. What is Equity Release? 3. Equity Release Plans The options available to you 4. The Application Process 5. Questions

How To Prepare A Business Plan

How To Prepare A Business Plan A Step By Step Guide North Central Development P.O. Box 1208 Thompson, Manitoba R8N 1P1 Phone: 204 677 1490 Toll Free: 1 888 847 7878 Fax: 204 778 5672 E mail: ncd@northcentraldevelopment.ca

How To Prepare A Business Plan A Step By Step Guide North Central Development P.O. Box 1208 Thompson, Manitoba R8N 1P1 Phone: 204 677 1490 Toll Free: 1 888 847 7878 Fax: 204 778 5672 E mail: ncd@northcentraldevelopment.ca

So You Want to Borrow Money to Start a Business?

So You Want to Borrow Money to Start a Business? M any small business owners cannot understand why a lending institution would refuse to lend them money. Others have no trouble getting money, but they

So You Want to Borrow Money to Start a Business? M any small business owners cannot understand why a lending institution would refuse to lend them money. Others have no trouble getting money, but they

Table of contents. Introduction to Small Business Cash Flow. Calculating your Company s Cash Flow. Timing your Cash Flow. Monitoring your Cash Flow

INTRODUCTION TO Table of contents Introduction to Small Business Cash Flow Calculating your Company s Cash Flow Timing your Cash Flow Monitoring your Cash Flow Meeting Cash Flow Challenges When and How

INTRODUCTION TO Table of contents Introduction to Small Business Cash Flow Calculating your Company s Cash Flow Timing your Cash Flow Monitoring your Cash Flow Meeting Cash Flow Challenges When and How

HOME LOAN ADVICE CENTRE e-course (PART 1)

") HOME LOAN ADVICE CENTRE e-course (PART 1) Welcome to the Home Loan Advice Centre e-course. The information contained within this e-course is Home Loan Advice Centre s compilation of information, tips,

HOME LOAN ADVICE CENTRE e-course (PART 1) Welcome to the Home Loan Advice Centre e-course. The information contained within this e-course is Home Loan Advice Centre s compilation of information, tips,

Having cash on hand is costly since you either have to raise money initially (for example, by borrowing from a bank) or, if you retain cash out of

or, if you retain cash out of") 1 Working capital refers to liquid funds used to purchase materials and pay workers. This is in contrast to long term capital such as buildings and machinery. Part of working capital management is cash

1 Working capital refers to liquid funds used to purchase materials and pay workers. This is in contrast to long term capital such as buildings and machinery. Part of working capital management is cash

SMALL BUSINESS LOAN GUIDE JANUARY 2014. A guide to help small business owners navigate the loan application process

JANUARY 2014 A guide to help small business owners navigate the loan application process TABLE OF CONTENTS Contents WHY THIS GUIDE? 1 EQUITY INVESTMENT 2 CASH FLOW PROJECTIONS 4 WORKING CAPITAL 6 COLLATERAL

JANUARY 2014 A guide to help small business owners navigate the loan application process TABLE OF CONTENTS Contents WHY THIS GUIDE? 1 EQUITY INVESTMENT 2 CASH FLOW PROJECTIONS 4 WORKING CAPITAL 6 COLLATERAL

Financial Terms & Calculations

Financial Terms & Calculations So much about business and its management requires knowledge and information as to financial measurements. Unfortunately these key terms and ratios are often misunderstood

Financial Terms & Calculations So much about business and its management requires knowledge and information as to financial measurements. Unfortunately these key terms and ratios are often misunderstood

Declaring Personal Bankruptcy

Declaring Personal Bankruptcy DECLARING PERSONAL BANKRUPTCY A declaration of personal bankruptcy doesn t carry the stigma it once did but it is, nonetheless, an admission that one is no longer able to

Declaring Personal Bankruptcy DECLARING PERSONAL BANKRUPTCY A declaration of personal bankruptcy doesn t carry the stigma it once did but it is, nonetheless, an admission that one is no longer able to

Finding and Financing Your Small Business. Hosted by Susan Strong 77

Finding and Financing Your Small Business Hosted by Susan Strong 77 Welcome! we will begin the webinar at the top of the hour Finding and Financing A Business... Find out the benefits and facts Agenda

Finding and Financing Your Small Business Hosted by Susan Strong 77 Welcome! we will begin the webinar at the top of the hour Finding and Financing A Business... Find out the benefits and facts Agenda

Is a Reverse Mortgage Right for You?

The information contained herein has been obtained from sources that we believe to be reliable, but its accuracy and completeness are not guaranteed. Any examples shown on this website are purely hypothetical

The information contained herein has been obtained from sources that we believe to be reliable, but its accuracy and completeness are not guaranteed. Any examples shown on this website are purely hypothetical

Preparing A Business Ready For Sale

Preparing A Business Ready For Sale Because A Business That s Ready For Sale Is Well Worth Keeping! Facilitator Workbook Presented by John E Denton FOR 1 Agenda Outline Why prepare a business ready for

Preparing A Business Ready For Sale Because A Business That s Ready For Sale Is Well Worth Keeping! Facilitator Workbook Presented by John E Denton FOR 1 Agenda Outline Why prepare a business ready for

Can t Get 30 Day Credit Terms With Your Suppliers? Get Business Credit Assurance.

Can t Get 30 Day Credit Terms With Your Suppliers? Get Business Credit Assurance. WWW.NET30CREDIT.COM How Credit Assurance Works. Once your credit is approved, we can issue credit assurance to your qualified

Can t Get 30 Day Credit Terms With Your Suppliers? Get Business Credit Assurance. WWW.NET30CREDIT.COM How Credit Assurance Works. Once your credit is approved, we can issue credit assurance to your qualified

NATIONAL INTERACTIVE STUDY GROUP UNIT 8 QUESTIONS

NATIONAL INTERACTIVE STUDY GROUP UNIT 8 QUESTIONS National Interactive Study Group 2 SESSION 8 JOHN MATHIS Notes for Tonight 1. To MUTE your phone line use *6 2. To UNMUTE your phone line use #6 3. Chat

NATIONAL INTERACTIVE STUDY GROUP UNIT 8 QUESTIONS National Interactive Study Group 2 SESSION 8 JOHN MATHIS Notes for Tonight 1. To MUTE your phone line use *6 2. To UNMUTE your phone line use #6 3. Chat

Financing a New Venture

Financing a New Venture A Canadian Innovation Centre How-To Guide 1 Financing a new venture New ventures require financing to fund growth Forms of financing include equity (personal, family & friends,

Financing a New Venture A Canadian Innovation Centre How-To Guide 1 Financing a new venture New ventures require financing to fund growth Forms of financing include equity (personal, family & friends,

The Business Case For SBA 7a Lending For Community Banks

The Business Case For SBA 7a Lending For Community Banks How Community Banks Can Prudently Make Loans to Small Business By: Joanne Thompson SBA OneSource, LLC This paper examines the business reasons for

The Business Case For SBA 7a Lending For Community Banks How Community Banks Can Prudently Make Loans to Small Business By: Joanne Thompson SBA OneSource, LLC This paper examines the business reasons for

THE BUSINESS CASH INFUSION ebook

G114 THE BUSINESS CASH INFUSION ebook 6 reasons to consider factoring as part of your business financial strategy ecapital.com WANT MORE CASH FOR YOUR BUSINESS? START HERE. Businesses large and small all

G114 THE BUSINESS CASH INFUSION ebook 6 reasons to consider factoring as part of your business financial strategy ecapital.com WANT MORE CASH FOR YOUR BUSINESS? START HERE. Businesses large and small all

Your essential guide to equity release. from the UK s No. 1 specialist

Your essential guide to equity release from the UK s No. 1 specialist 03 03 04 05 06 07 08 09 10 15 Contents What is equity release? How could equity release help you? Why choose Key Retirement? Mr & Mrs

Your essential guide to equity release from the UK s No. 1 specialist 03 03 04 05 06 07 08 09 10 15 Contents What is equity release? How could equity release help you? Why choose Key Retirement? Mr & Mrs

CIMA F3 Course Notes. Chapter 3. Short term finance

CIMA F3 Course Notes c Chapter 3 Short term finance Personal use only - not licensed for use on courses 31 1. Conservative, Aggressive and Matching strategies There are three over-riding approaches to

CIMA F3 Course Notes c Chapter 3 Short term finance Personal use only - not licensed for use on courses 31 1. Conservative, Aggressive and Matching strategies There are three over-riding approaches to

How to Buy and Sell Property FAST in Today s Market!

How to Buy and Sell Property FAST in Today s Market! A land contract is a written agreement between a person who has sold property ("the Seller or Vendor") and the person who bought that property ("the

How to Buy and Sell Property FAST in Today s Market! A land contract is a written agreement between a person who has sold property ("the Seller or Vendor") and the person who bought that property ("the

First Time Buyer Mortgage Information

First Time Buyer Mortgage Information If you re thinking about a Mortgage for your first home talk to us today A good time to talk to us? We re here to listen and help you whenever you need to talk to

First Time Buyer Mortgage Information If you re thinking about a Mortgage for your first home talk to us today A good time to talk to us? We re here to listen and help you whenever you need to talk to

Financial Management for a Small Business

Table of Contents Welcome... 3 What Do You Know? Financial Management for a Small Business... 4 Pre-Test... 5 Benefits of Financial Management... 7 Budgeting... 7 Discussion Point #1: Budgeting... 7 Bookkeeping...

Table of Contents Welcome... 3 What Do You Know? Financial Management for a Small Business... 4 Pre-Test... 5 Benefits of Financial Management... 7 Budgeting... 7 Discussion Point #1: Budgeting... 7 Bookkeeping...

Fifth Third Home Buying Guide. A Guide to Residential Home Buying.

Fifth Third Home Buying Guide A Guide to Residential Home Buying. Important Contacts and Numbers. Use this page to record important information as you move through the homebuying process. Realtor/Builder

Fifth Third Home Buying Guide A Guide to Residential Home Buying. Important Contacts and Numbers. Use this page to record important information as you move through the homebuying process. Realtor/Builder

Incisive Business Guide to Factoring

Incisive Guide to Factoring Factoring Guide Summary This guide from Incisive outlines the features and benefits for your business from using factoring and invoice discounting services. Factoring is commonly

Incisive Guide to Factoring Factoring Guide Summary This guide from Incisive outlines the features and benefits for your business from using factoring and invoice discounting services. Factoring is commonly