INTRODUCTION TO THE 2013 BENCHMARKING GUIDE

|

|

|

- Jonas Wright

- 7 years ago

- Views:

Transcription

1

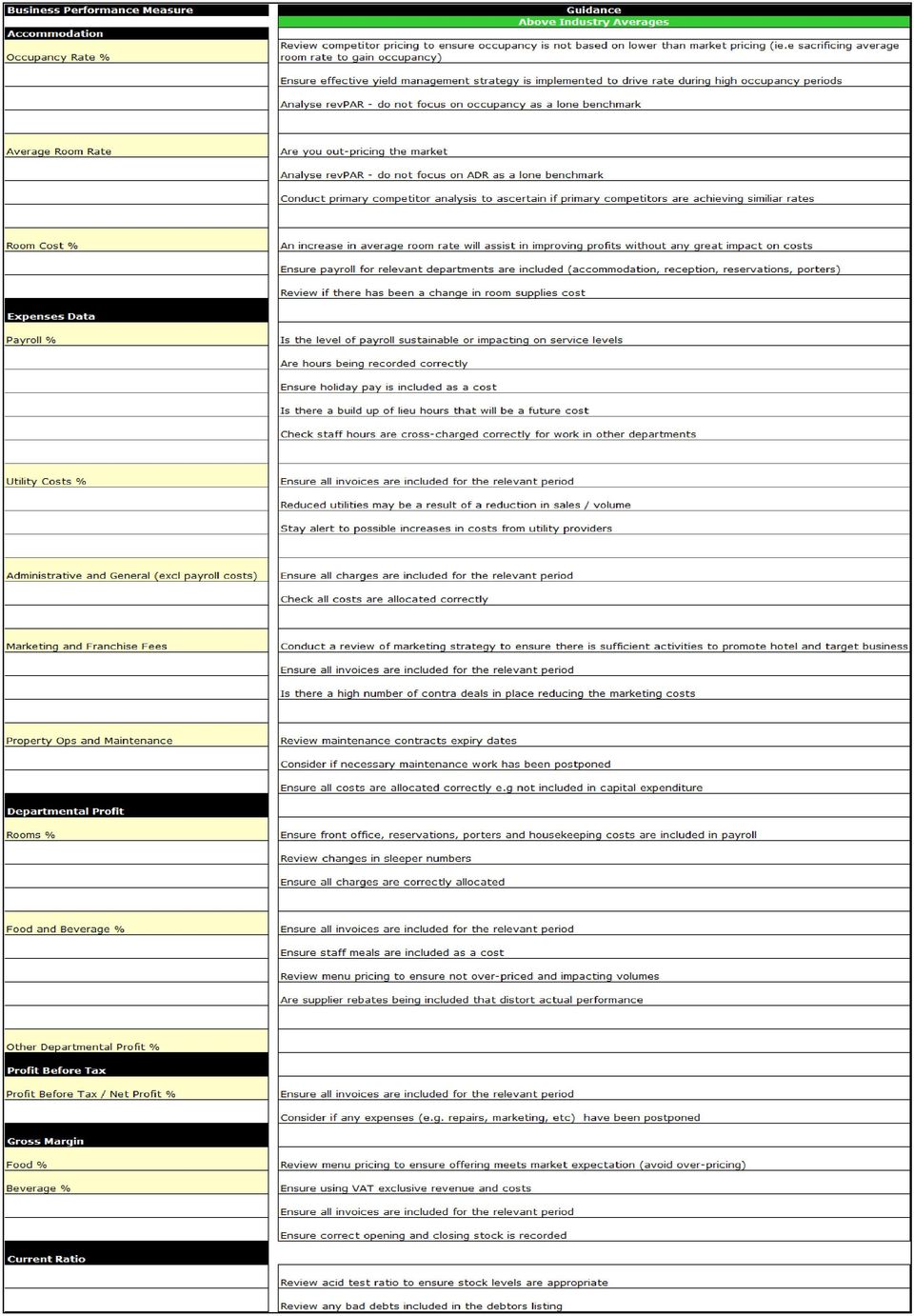

2 INTRODUCTION TO THE 2013 BENCHMARKING GUIDE This guide is a supporting document for the Business Diagnostic Indicator for Hotels. It has been designed to be used by hoteliers who have completed the Business Diagnostic for their property for the 2012 financial year. Section 2 of the Business Diagnostic provides a snapshot of your property s performance across important business dimensions. The information you provide is primarily based on percentages and for some measures you can compare your property to industry benchmark. This guide follows each of these industry benchmarks and provides explanations to assist in interpreting the results. The guidance notes identify practical actions that can be taken if your property is performing above or below industry. Utilising this document in conjunction with the Business Diagnostic Indicator will enable you to identify areas for improvement and introduce corrective action. Please note that some performance measures included in the Below Industry Averages section apply to your results being higher than the industry average (e.g. Room Cost %, Payroll %, Utility Costs %, Administrative and General, Marketing and Franchise Fees, Property Ops and Maintenance). This also applies for these results in the Above Industry Averages section. This guide cannot be regarded as a comprehensive guide to providing solutions or recommendations for your business and it may be necessary to extend beyond the sample of guidance notes provided.

3

4

5

6 Explanation of Terms and Bases Used ACCOMMODATION Occupancy Percentage Rooms occupied by hotel guests on a paid basis. Average Room Rate The average room rate is defined as room sales divided by the total number of rooms occupied. RevPAR Revenue per available room is calculated by multiplying average room rate by annual occupancy level. Rooms Cost % Room costs as a percentage of room sales. OVERALL REVENUE BREAKDOWN Rooms Revenues derived from the rental of sleeping rooms at the hotel, net of Value Added Tax and any rebates and discounts. Food Revenues derived from the sale of food, including coffee, milk and tea. Beverage Revenues derived from the sale of beverages, including beer, ale, wine and liquors. Other Revenues derived from all other sources, e.g. health club, spa, conferences, telephone, service charge etc. EXPENSES DATA Payroll Payroll costs to include labour costs such as salaries, wages and employee benefits for all staff members. Utility Costs Utility Costs typically include electricity, fuel (oil, gas and coal), purchased steam and water, waste removal etc. Administrative and General (A&G) Included in this category are office supplies, computer services, accounting and legal fees, liability insurance, cash overages and shortages, bad debt expenses, travel insurance and credit card commissions. Marketing & Franchise Fees Marketing expense includes direct sales expenses, advertising and promotions, travel expenses for the sales staff and civic and community projects. Franchise Fees includes all fees charged by franchise company including royalty fees. Property Operation and Maintenance This category includes the cost of maintenance supplies, cost of repairs and maintenance of the building, furniture and equipment and the grounds. GROSS OPERATING PROFIT Gross operating profit is defined as total revenue less all departmental and undistributed operating expenses. DEPARTMENTAL PROFIT Departmental profit is defined as the departmental sales less the departmental costs. Rooms Room costs (payroll and expenses) divided by room revenue, expressed as a percentage. Food and Beverage (F&B) F&B costs (payroll, cost of sale and payroll) divided by F&B revenue, expressed as a percentage. Other Department Profit Other expenses would comprise of those expenses, including labour, which offset the revenue generated by items in the corresponding revenue areas. PROFIT BEFORE TAX / NET PROFIT Profitability after accounting for operational costs. Profit before debt service. GROSS MARGIN Gross Margin is defined as revenue less costs of sales (excluding payroll). COUNTRY OF ORIGIN The country in which the booking originated in. CHANNEL OF BUSINESS The distribution channel which delivered the business to the hotel. MARKET SEGMENT Corporate / Business Consortia, corporate direct and GDS bookings. Leisure Direct individual leisure, FIT, leisure promotional rates. Groups Groups delivering 10 rooms or more. Meeting Participants (MICE) Guests attending a meeting, incentive conference, conference or exhibition. Web/Internet 3rd party intermediary bookings, web direct bookings (if a promo code is given to a corporate booker these room nights should be allocated to the Corporate / Business market segment). Airline Aircrew room nights and delayed flight crew / passengers. Other Room nights generated that do not pertain to the above market segments. PERFORMANCE RATIOS Current Ratio This ratio will inform you of the hotel s ability to meet its current financial obligations. Current Assets (stock, cash, debtors, etc.) divided by Current Liabilities (supplier invoices, revenue liabilities, debts payable within 1 year, etc.). Average Debtor Days The average number of days it takes to receive payment from your trade debtors. To calculate divide total trade debtors by credit sales and multiply by 365. Average Creditor Days The average number of days it takes to pay your trade creditors. To calculate - divide unpaid creditors by cost of sales and multiply by 365. HUMAN RESOURCES Employee Turnover The number of employees that left a company within a certain time period and had to be replaced. To calculate this as a percentage divide the number of employees that had to be replaced in a given time period by the total number of employees in the hotel and multiply by 100. Absenteeism Rate Absenteeism refers to employees who miss part or whole days of work due to illness, unpaid holidays, etc. To calculate this as a percentage divide the number of absent days by the total number of employees within the time period and multiply by 100. QUALITY MANAGEMENT Total Cost of Complaints Revenue lost as a result of a complaint (e.g. rate corrections) or cost of providing services to a complainant as a percentage of total revenue.

How To Measure Performance In The Accommodation Industry

Key Performance Indicators A guide to help you understand the key financial drivers in your business Running any business effectively requires good decision making which is based on good and timely management

Key Performance Indicators A guide to help you understand the key financial drivers in your business Running any business effectively requires good decision making which is based on good and timely management

Frequently Used Formulas for Managing Operations

Frequently Used Formulas for Managing Operations Chapter 1 - Hospitality Industry Accounting Revenue Expenses = Profit Assets = Liabilities + Owners Equity Chapter 2 - Accounting Fundamentals Review Assets

Frequently Used Formulas for Managing Operations Chapter 1 - Hospitality Industry Accounting Revenue Expenses = Profit Assets = Liabilities + Owners Equity Chapter 2 - Accounting Fundamentals Review Assets

CENTRE FOR CONTINUING EDUCATION BBA (AVIATION OPERATION)

") CENTRE FOR CONTINUING EDUCATION BBA (AVIATION OPERATION) BATCH: SEMESTER: NAME: ROLL NO: ASSIGNMENT 1 & 2 FOR BUSINESS ACCOUNTING BBCF 131 UNIVERSITY OF PETROLEUM & ENERGY STUDIES Assignment-1 Note: All

CENTRE FOR CONTINUING EDUCATION BBA (AVIATION OPERATION) BATCH: SEMESTER: NAME: ROLL NO: ASSIGNMENT 1 & 2 FOR BUSINESS ACCOUNTING BBCF 131 UNIVERSITY OF PETROLEUM & ENERGY STUDIES Assignment-1 Note: All

THE NEF APPLICATION FORM R250 000 - R75 million

THE NEF APPLICATION FORM R250 000 - R75 million Name */ Male/Female Contribution Shareholding % (Pre-NEF funding) Shareholding % (Post-NEF funding) TOTAL D D M M Y Y Y Y PARTICIPATION IN: Current Future

THE NEF APPLICATION FORM R250 000 - R75 million Name */ Male/Female Contribution Shareholding % (Pre-NEF funding) Shareholding % (Post-NEF funding) TOTAL D D M M Y Y Y Y PARTICIPATION IN: Current Future

How To Write A Report On The Unaudited Accounts Of A Sole Trader

Accounts 31 December 2007 Approval statement I approve these accounts which comprise the Profit and Loss Account, Balance Sheet and related notes. I acknowledge my responsibility for the accounts, including

Accounts 31 December 2007 Approval statement I approve these accounts which comprise the Profit and Loss Account, Balance Sheet and related notes. I acknowledge my responsibility for the accounts, including

Income Measurement and Profitability Analysis

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

Using Accounts to Interpret Performance

Using s to Interpret Performance ing information is used by stakeholders to judge the performance and efficiency of a business Different stakeholders will look for different things: STAKEHOLDER Shareholders

Using s to Interpret Performance ing information is used by stakeholders to judge the performance and efficiency of a business Different stakeholders will look for different things: STAKEHOLDER Shareholders

FI3300 Corporation Finance

Learning Objectives FI3300 Corporation Finance Spring Semester 2010 Dr. Isabel Tkatch Assistant Professor of Finance Explain the objectives of financial statement analysis and its benefits for creditors,

Learning Objectives FI3300 Corporation Finance Spring Semester 2010 Dr. Isabel Tkatch Assistant Professor of Finance Explain the objectives of financial statement analysis and its benefits for creditors,

PRICING YOUR TOURISM BUSINESS A PRACTICAL STEP BY STEP GUIDE TO HELP YOU COMPLETE THE TOURISM BOOST ONLINE PRICING TOOLS

PRICING YOUR TOURISM BUSINESS A PRACTICAL STEP BY STEP GUIDE TO HELP YOU COMPLETE THE TOURISM BOOST ONLINE PRICING TOOLS INTRODUCTION It is very important to price your tourism business correctly. Basing

PRICING YOUR TOURISM BUSINESS A PRACTICAL STEP BY STEP GUIDE TO HELP YOU COMPLETE THE TOURISM BOOST ONLINE PRICING TOOLS INTRODUCTION It is very important to price your tourism business correctly. Basing

Chart of Accounts - Sole Trader

Chart of Accounts - Sole Trader The basic road map into any accounting system is the chart of accounts. It is this chart that helps establish the information that will be captured by your accounting system,

Chart of Accounts - Sole Trader The basic road map into any accounting system is the chart of accounts. It is this chart that helps establish the information that will be captured by your accounting system,

Assumptions Worksheet

Cash Budget, Page 1 Exhibit IV Cash Budget Assumptions Worksheet Name of Business: Preparer: Date: Use these guidelines in preparing your assumptions: Minimum Cash Balance 1. The amount of cash required

Cash Budget, Page 1 Exhibit IV Cash Budget Assumptions Worksheet Name of Business: Preparer: Date: Use these guidelines in preparing your assumptions: Minimum Cash Balance 1. The amount of cash required

Part I: The New Guidelines and Operating Statements for 2015

A Close Look at the USALI 11th Revised Edition Part I: The New Guidelines and Operating Statements for 2015 By Raymond S. Schmidgall, Ph.D., CPA and Agnes DeFranco, Ed.D., CHE, CHAE With the new edition

A Close Look at the USALI 11th Revised Edition Part I: The New Guidelines and Operating Statements for 2015 By Raymond S. Schmidgall, Ph.D., CPA and Agnes DeFranco, Ed.D., CHE, CHAE With the new edition

Chart of Accounts AA Corp Tax 0000-1020 / page 1. Sales. Income from participating interests. Income from other fixed asset investments

0000-1020 / page 1 0000 Sales 0001 Sales type A 0002 Sales type B 0003 Sales type C 0004 Sales type D 0005 Sales type E 0006 Sales type F 0007 Sales type G 0008 Sales type H 0009 Sales type I 0100 UK sales

0000-1020 / page 1 0000 Sales 0001 Sales type A 0002 Sales type B 0003 Sales type C 0004 Sales type D 0005 Sales type E 0006 Sales type F 0007 Sales type G 0008 Sales type H 0009 Sales type I 0100 UK sales

Understanding Financial Statements. For Your Business

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Ratio Analysis. A) Liquidity Ratio : - 1) Current ratio = Current asset Current Liability

Liquidity Ratio : - 1) Current ratio = Current asset Current Liability") A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

B. Division of Costs The purpose of a Manufacturing Account is to ascertain Cost of Production ( ).

.") Manufacturing Accounts ( ) S5 Manufacturing Account/LWL A. Function of a Manufacturing Acccount For those businesses which deal with manufacturing products. It is common in today s business to act both

Manufacturing Accounts ( ) S5 Manufacturing Account/LWL A. Function of a Manufacturing Acccount For those businesses which deal with manufacturing products. It is common in today s business to act both

Discussion Outline. Evolution of Physician Practice Practice Operations. Questions and Other Topics. Evolution of Physician Practice

Physician Practice Management Oklahoma Academy of Family Practice June 20, 2014 Presented by Steve Powell Vice President Delivery System Integration SSM Health Care of Oklahoma, Inc. Discussion Outline

Physician Practice Management Oklahoma Academy of Family Practice June 20, 2014 Presented by Steve Powell Vice President Delivery System Integration SSM Health Care of Oklahoma, Inc. Discussion Outline

TRADING ACCOUNT (Horizontal Format) for the year ended. Particulars. Rs.

for the year ended. Particulars. Rs.") Dr. To Opening Stock To Purchases Less: Returns outwards () To Frieght & Carriage To Customs & Insurance To Wages To Gas, Water & Fuel To Factory Expenses To Royalty on Production To Cargo Expenses To

Dr. To Opening Stock To Purchases Less: Returns outwards () To Frieght & Carriage To Customs & Insurance To Wages To Gas, Water & Fuel To Factory Expenses To Royalty on Production To Cargo Expenses To

December 2013 exam. (4CW) SME cash and working capital. Instructions to students. reading time.

SME cash and working capital. Instructions to students. reading time.") 1 December 2013 exam (4CW) SME cash and working capital Instructions to students 1. Time allowed is 3 hours and 10 minutes, which includes 10 minutes reading time. 2. This is a closed book exam. 3. Use

1 December 2013 exam (4CW) SME cash and working capital Instructions to students 1. Time allowed is 3 hours and 10 minutes, which includes 10 minutes reading time. 2. This is a closed book exam. 3. Use

NCEA Level 2 Accounting (91176) 2012 page 1 of 8. Sales 990 000 P. Cost of goods sold 586 000 P. Gross profit 404 000 S* Rent (received) 24 000 V

2012 page 1 of 8. Sales 990 000 P. Cost of goods sold 586 000 P. Gross profit 404 000 S* Rent (received) 24 000 V") Assessment Schedule 2012 NCEA Level 2 Accounting (91176) 2012 page 1 of 8 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176) Evidence Statement Question

Assessment Schedule 2012 NCEA Level 2 Accounting (91176) 2012 page 1 of 8 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176) Evidence Statement Question

Club Financial Management

12 Club Financial Management This chapter was written and contributed by Raymond S. Schmidgall, Hilton Hotels Professor, Michigan State University, East Lansing, Michigan A CLUB GENERAL MANAGER S main

12 Club Financial Management This chapter was written and contributed by Raymond S. Schmidgall, Hilton Hotels Professor, Michigan State University, East Lansing, Michigan A CLUB GENERAL MANAGER S main

Associated Files: Ratios worksheet

Unit 4 Business accounting Ratios Instructions and answers for Teachers These instructions should accompany the OCR resource Ratios which supports the OCR Level 3 Cambridge Technicals in Business Unit

Unit 4 Business accounting Ratios Instructions and answers for Teachers These instructions should accompany the OCR resource Ratios which supports the OCR Level 3 Cambridge Technicals in Business Unit

ITEM 7 ESTIMATED INITIAL INVESTMENT

ITEM 7 ESTIMATED INITIAL INVESTMENT Below are estimates of your initial investment with respect to your prototypical restaurant. These estimates are subject to increases based upon the restaurant s location,

ITEM 7 ESTIMATED INITIAL INVESTMENT Below are estimates of your initial investment with respect to your prototypical restaurant. These estimates are subject to increases based upon the restaurant s location,

Chapter 2: Financial Statements & Operations

Chapter 2: Financial Statements & Operations To analyze a liquor store s operations a close look must be taken at the day to day operations as well as examining the liquor store s financial history. Usually

Chapter 2: Financial Statements & Operations To analyze a liquor store s operations a close look must be taken at the day to day operations as well as examining the liquor store s financial history. Usually

A contractor s chart of accounts is the heart of the accounting system. Of particular importance is the cost of sales section (beginning in the 41000

CHART OF ACCOUNTS A contractor s chart of accounts is the heart of the accounting system. Of particular importance is the cost of sales section (beginning in the 41000 series and ending in 43000). This

CHART OF ACCOUNTS A contractor s chart of accounts is the heart of the accounting system. Of particular importance is the cost of sales section (beginning in the 41000 series and ending in 43000). This

Statistical release P6421

Statistical release (Preliminary) Embargoed until: 2 December 2010 9:00 Enquiries: User Information Services 012 310 8600/8351 1 Table of contents 1. Summary of findings for the year 2009...2 Figure 1

Statistical release (Preliminary) Embargoed until: 2 December 2010 9:00 Enquiries: User Information Services 012 310 8600/8351 1 Table of contents 1. Summary of findings for the year 2009...2 Figure 1

CONTENTS. Kevin O Riordan 2000 ISBN 1841 31 3750. Folens Publishers, Hibernian Industrial Estate, Greenhills Road. Tallaght, Dublin 24.

CONTENTS Chapter 2: Double-Entry Book-keeping and the Trial Balance... 1 Chapter 3: Profit Measurement and Balance Sheet Preparation... 5 Chapter 4: Value Added Tax and Statutory Deductions... 8 Chapter

CONTENTS Chapter 2: Double-Entry Book-keeping and the Trial Balance... 1 Chapter 3: Profit Measurement and Balance Sheet Preparation... 5 Chapter 4: Value Added Tax and Statutory Deductions... 8 Chapter

Financial Plan. A) Estimated One-Time Financial Requirements. Part One

Estimated One-Time Financial Requirements. Part One") Financial Plan The Financial Plan is perhaps one of the most important components of your Business Plan (see Business Plan Handout). Not only is it essential if you are seeking external financing it is

Financial Plan The Financial Plan is perhaps one of the most important components of your Business Plan (see Business Plan Handout). Not only is it essential if you are seeking external financing it is

Accounting and Book-keeping Level 3

Accounting and Book-keeping Level 3 8991-03-003 2012 Sample paper Candidate s name (Block letters please) Centre no Date Time allowed: 2 hours 30 minutes (plus 5 minutes' reading time) Note making is not

Accounting and Book-keeping Level 3 8991-03-003 2012 Sample paper Candidate s name (Block letters please) Centre no Date Time allowed: 2 hours 30 minutes (plus 5 minutes' reading time) Note making is not

Financial Statements for Manufacturing Businesses

Management Accounting 31 Financial Statements for Manufacturing Businesses Importance of Financial Statements Accounting plays a critical role in decision-making. Accounting provides the financial framework

Management Accounting 31 Financial Statements for Manufacturing Businesses Importance of Financial Statements Accounting plays a critical role in decision-making. Accounting provides the financial framework

Guide to cash flow management

Guide to cash flow management Cash flow management What is cash flow management? For a business to be successful, good cash flow management is crucial. Cash flow is the primary indicator of a business

Guide to cash flow management Cash flow management What is cash flow management? For a business to be successful, good cash flow management is crucial. Cash flow is the primary indicator of a business

tutor2u Working Capital Introduction to the Management of Working Capital AS & A2 Business Studies PowerPoint Presentations 2005

Working Capital Introduction to the Management of Working Capital AS & A2 Business Studies PowerPoint Presentations 2005 Introduction All businesses need cash to survive Cash is needed to: Invest in fixed

Working Capital Introduction to the Management of Working Capital AS & A2 Business Studies PowerPoint Presentations 2005 Introduction All businesses need cash to survive Cash is needed to: Invest in fixed

Business Plan for XXX

Business Plan for XXX Version: 1.0 Date: [Elements in italics are indications to explain the business plan concepts: they should be deleted and not appear in the completed version of the business plan.

Business Plan for XXX Version: 1.0 Date: [Elements in italics are indications to explain the business plan concepts: they should be deleted and not appear in the completed version of the business plan.

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS 0452 ACCOUNTING. 0452/01 Paper 1 (Multiple Choice), maximum mark 40

, maximum mark 40") www.xtremepapers.com UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education MARK SCHEME for the June 2004 question papers 0452 ACCOUNTING 0452/01 Paper

www.xtremepapers.com UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education MARK SCHEME for the June 2004 question papers 0452 ACCOUNTING 0452/01 Paper

tutor2u Cash Management How and Why Businesses Need to Manage their Cash AS & A2 Business Studies PowerPoint Presentations 2005

Cash Management How and Why Businesses Need to Manage their Cash AS & A2 Business Studies PowerPoint Presentations 2005 Importance of Cash (1) A business can exist for a while without making profits but

Cash Management How and Why Businesses Need to Manage their Cash AS & A2 Business Studies PowerPoint Presentations 2005 Importance of Cash (1) A business can exist for a while without making profits but

CHECKLIST FOR INTERNAL AUDIT

CHECKLIT FOR INTERNAL AUDIT Client s Name: Nature of Audit:.. Period covered by the Audit:.. INTERNAL CONTROL QUETIONNAIRE (Evaluation of Internal Control) ACCOUNTING FUNCTION: WAGE & PAYROLL / CAH & BANK

CHECKLIT FOR INTERNAL AUDIT Client s Name: Nature of Audit:.. Period covered by the Audit:.. INTERNAL CONTROL QUETIONNAIRE (Evaluation of Internal Control) ACCOUNTING FUNCTION: WAGE & PAYROLL / CAH & BANK

Topic 4 Working Capital Management. 1. Concept of Working Capital 2. Measuring Working Capital and Net Working Capital. 4.

Topic 4 Working Capital Management 1. Concept of Working Capital 2. Measuring Working Capital and Net Working Capital 3. Optimization i i of Working Capital 4. Applications 80 Learning objectives This

Topic 4 Working Capital Management 1. Concept of Working Capital 2. Measuring Working Capital and Net Working Capital 3. Optimization i i of Working Capital 4. Applications 80 Learning objectives This

Ford Computer Systems Ltd ACCOUNTS FOR THE YEAR ENDED 30/06/2005

Registered number: 1111111 ACCOUNTS FOR THE YEAR ENDED 30/06/2005 Prepared By: Bloggs & Co ACCOUNTS FOR THE YEAR ENDED 30/06/2005 DIRECTORS D G Ford SECRETARY S J Ford REGISTERED OFFICE 65 High Street

Registered number: 1111111 ACCOUNTS FOR THE YEAR ENDED 30/06/2005 Prepared By: Bloggs & Co ACCOUNTS FOR THE YEAR ENDED 30/06/2005 DIRECTORS D G Ford SECRETARY S J Ford REGISTERED OFFICE 65 High Street

ESSENTIALS OF ENTREPRENEURSHIP AND SMALL BUSINESS MANAGEMENT 6E

CHAPTER 11 Creating a Successful Financial Plan The Importance of a Financial Plan Financial planning is essential to running a successful business and is not that difficult! Common mistake among business

CHAPTER 11 Creating a Successful Financial Plan The Importance of a Financial Plan Financial planning is essential to running a successful business and is not that difficult! Common mistake among business

WEEK 6. Objective 1: Sales Transaction Cycle Risks

WEEK 6 CSA ch4 & GS ch10: pp457-488 Objective 1: Sales Transaction Cycle Risks The major assertions of interest to the auditor in ST of balances for account receivable are existence and valuation and allocation.

WEEK 6 CSA ch4 & GS ch10: pp457-488 Objective 1: Sales Transaction Cycle Risks The major assertions of interest to the auditor in ST of balances for account receivable are existence and valuation and allocation.

Paper 5- Financial Accounting

Paper 5- Financial Accounting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 5- Financial Accounting Full Marks:100 Time allowed:

Paper 5- Financial Accounting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 5- Financial Accounting Full Marks:100 Time allowed:

ACCOUNTS PRODUCTION OPEN SANS FONT FOR 2013 TAXCALC HUB AND ACCOUNTS PRODUCTION CHART OF ACCOUNTS - LIMITED COMPANY

OPEN SANS FONT FOR 2013 TAXCALC HUB AND ACCOUNTS PRODUCTION CHART OF ACCOUNTS - LIMITED COMPANY Contents Sales 1 Other Operating Income 1 Income from Shares in Group Undertakings 1 Income from Participating

OPEN SANS FONT FOR 2013 TAXCALC HUB AND ACCOUNTS PRODUCTION CHART OF ACCOUNTS - LIMITED COMPANY Contents Sales 1 Other Operating Income 1 Income from Shares in Group Undertakings 1 Income from Participating

6.3 PROFIT AND LOSS AND BALANCE SHEETS. Simple Financial Calculations. Analysing Performance - The Balance Sheet. Analysing Performance

63 COSTS AND COSTING 6 PROFIT AND LOSS AND BALANCE SHEETS Simple Financial Calculations Analysing Performance - The Balance Sheet Analysing Performance Analysing Financial Performance Profit And Loss Forecast

63 COSTS AND COSTING 6 PROFIT AND LOSS AND BALANCE SHEETS Simple Financial Calculations Analysing Performance - The Balance Sheet Analysing Performance Analysing Financial Performance Profit And Loss Forecast

Ratio Analysis CBDC, NB. Presented by ACSBE. February, 2008. Copyright 2007 ACSBE. All Rights Reserved.

Ratio Analysis CBDC, NB February, 2008 Presented by ACSBE Financial Analysis What is Financial Analysis? What Can Financial Ratios Tell? 7 Categories of Financial Ratios Significance of Using Ratios Industry

Ratio Analysis CBDC, NB February, 2008 Presented by ACSBE Financial Analysis What is Financial Analysis? What Can Financial Ratios Tell? 7 Categories of Financial Ratios Significance of Using Ratios Industry

The Profit & Loss Account Accounting for Revenue & Expenses

The Profit & Loss Account Accounting for Revenue & Expenses Chapter 3 Luby & O Donoghue (2005) Profit & Loss Account The main reason why people set up in business is to make a profit. The profit and loss

The Profit & Loss Account Accounting for Revenue & Expenses Chapter 3 Luby & O Donoghue (2005) Profit & Loss Account The main reason why people set up in business is to make a profit. The profit and loss

CHAPTER 2 ACCOUNTING FOR TRANSACTIONS

CHAPTER 2 ACCOUNTING FOR TRANSACTIONS Key Terms and Concepts to Know Double entry accounting: Debits and Credits Total debits must always equal total credits Accounting Books: Accounts General Journal

CHAPTER 2 ACCOUNTING FOR TRANSACTIONS Key Terms and Concepts to Know Double entry accounting: Debits and Credits Total debits must always equal total credits Accounting Books: Accounts General Journal

Creating a Successful Financial Plan

CHAPTER 11 Creating a Successful Financial Plan The Importance of a Financial Plan Financial planning is essential to running a successful business and is not that difficult! Common mistake among business

CHAPTER 11 Creating a Successful Financial Plan The Importance of a Financial Plan Financial planning is essential to running a successful business and is not that difficult! Common mistake among business

HOW TO READ FINANCIAL STATEMENTS

HOW TO READ FINANCIAL STATEMENTS By Michael Collins ACMA, TMITI 1 INTRODUCTION Financial statements such as a profit and loss account and a balance sheet can cause considerable confusion to business people

HOW TO READ FINANCIAL STATEMENTS By Michael Collins ACMA, TMITI 1 INTRODUCTION Financial statements such as a profit and loss account and a balance sheet can cause considerable confusion to business people

B312 Hospitality and Tourism Management. Module Synopsis

B312 Hospitality and Tourism Management Module Synopsis According to United Nation World Tourism Organization (UNWTO) report, Tourism Highlights (2008), tourism has been experiencing positive growth over

B312 Hospitality and Tourism Management Module Synopsis According to United Nation World Tourism Organization (UNWTO) report, Tourism Highlights (2008), tourism has been experiencing positive growth over

UNIFORM SYSTEM OF ACCOUNTS FOR THE LODGING INDUSTRY. HFTP Annual Convention & Trade Show October 22, 2015. Speaker

UNIFORM SYSTEM OF ACCOUNTS FOR THE LODGING INDUSTRY HFTP Annual Convention & Trade Show October 22, 2015 Speaker Ralph Miller, CPA, CA, CBV, CHA, CHAE President, Inntegrated Hospitality Management Ltd.

UNIFORM SYSTEM OF ACCOUNTS FOR THE LODGING INDUSTRY HFTP Annual Convention & Trade Show October 22, 2015 Speaker Ralph Miller, CPA, CA, CBV, CHA, CHAE President, Inntegrated Hospitality Management Ltd.

C02-Fundamentals of financial accounting

Sample Exam Paper Question 1 The difference between an income statement and an income and expenditure account is that: A. An income and expenditure account is an international term for an Income statement.

Sample Exam Paper Question 1 The difference between an income statement and an income and expenditure account is that: A. An income and expenditure account is an international term for an Income statement.

Bachelor of Business International Event Management

Bachelor of Business International Event Unit name Aim Topics covered Level 1 BUS101 Accounting Fundamentals The aim of the unit is to provide students with the fundamental skills and knowledge to understand

Bachelor of Business International Event Unit name Aim Topics covered Level 1 BUS101 Accounting Fundamentals The aim of the unit is to provide students with the fundamental skills and knowledge to understand

BUSINESS SEMINAR SECURE YOUR BUSINESS AND FUTURE. www.idealtax.com.au

BUSINESS SEMINAR SECURE YOUR BUSINESS AND FUTURE www.idealtax.com.au SEMINAR OUTLINE 1. Federal Budget 2011 2. Small Business Benchmarks 3. Small Business Concessions 4. Tax Return Tips 5. Superannuation

BUSINESS SEMINAR SECURE YOUR BUSINESS AND FUTURE www.idealtax.com.au SEMINAR OUTLINE 1. Federal Budget 2011 2. Small Business Benchmarks 3. Small Business Concessions 4. Tax Return Tips 5. Superannuation

Discussion Board Articles Ratio Analysis

Excellence in Financial Management Discussion Board Articles Ratio Analysis Written by: Matt H. Evans, CPA, CMA, CFM All articles can be viewed on the internet at www.exinfm.com/board Ratio Analysis Cash

Excellence in Financial Management Discussion Board Articles Ratio Analysis Written by: Matt H. Evans, CPA, CMA, CFM All articles can be viewed on the internet at www.exinfm.com/board Ratio Analysis Cash

Basic Benchmarking Data Definitions

Basic Benchmarking Data Definitions INCOME STATEMENT Actual Values Description Revenue 2012-13 2011-12 Operating Revenue Commonwealth Subsidies State Grants Resident/Client Charges Bond Retentions (if

Basic Benchmarking Data Definitions INCOME STATEMENT Actual Values Description Revenue 2012-13 2011-12 Operating Revenue Commonwealth Subsidies State Grants Resident/Client Charges Bond Retentions (if

Illinois Department of Revenue Regulations TITLE 86: REVENUE CHAPTER I: DEPARTMENT OF REVENUE PART 130 RETAILERS' OCCUPATION TAX

Illinois Department of Revenue Regulations Title 86 Part 130 Section 130.2145 Vendors of Meals Section 130.2145 Vendors of Meals TITLE 86: REVENUE CHAPTER I: DEPARTMENT OF REVENUE PART 130 RETAILERS' OCCUPATION

Illinois Department of Revenue Regulations Title 86 Part 130 Section 130.2145 Vendors of Meals Section 130.2145 Vendors of Meals TITLE 86: REVENUE CHAPTER I: DEPARTMENT OF REVENUE PART 130 RETAILERS' OCCUPATION

CHTP REVIEW: Hotel Technology. Cihan Cobanoglu, Ph.D., CHTP University of South Florida Sarasota- Manatee May 5, 2011

CHTP REVIEW: Hotel Technology Cihan Cobanoglu, Ph.D., CHTP University of South Florida Sarasota- Manatee May 5, 2011 What To Expect Multiple Choice and True/False 4 Sections 250 Choose most correct answer

CHTP REVIEW: Hotel Technology Cihan Cobanoglu, Ph.D., CHTP University of South Florida Sarasota- Manatee May 5, 2011 What To Expect Multiple Choice and True/False 4 Sections 250 Choose most correct answer

COST AND MANAGEMENT ACCOUNTING

EXECUTIVE PROGRAMME COST AND MANAGEMENT ACCOUNTING SAMPLE TEST PAPER (This test paper is for practice and self study only and not to be sent to the institute) Time allowed: 3 hours Maximum marks : 100

EXECUTIVE PROGRAMME COST AND MANAGEMENT ACCOUNTING SAMPLE TEST PAPER (This test paper is for practice and self study only and not to be sent to the institute) Time allowed: 3 hours Maximum marks : 100

STATE BANK OF INDIA BRANCH. Interview Form For Loans above Rs.25,000/- (To be submitted to the Sanctioning Authority along with the Application Form)

") Annexure-SBF/3 STATE BANK OF INDIA BRANCH SMALL BUSINESS FINANCE Interview Form For Loans above 25,000/- (To be submitted to the Sanctioning Authority along with the Application Form) To be used for :

Annexure-SBF/3 STATE BANK OF INDIA BRANCH SMALL BUSINESS FINANCE Interview Form For Loans above 25,000/- (To be submitted to the Sanctioning Authority along with the Application Form) To be used for :

Chapter 4 Adjustments, Financial Statements, and the Quality of Earnings

Chapter 4 Adjustments, Financial Statements, and the Quality of Earnings ANSWERS TO QUESTIONS 1. Adjusting entries are made at the end of the accounting period to record all revenues and expenses that

Chapter 4 Adjustments, Financial Statements, and the Quality of Earnings ANSWERS TO QUESTIONS 1. Adjusting entries are made at the end of the accounting period to record all revenues and expenses that

Vol. 2, Chapter 15 Ratio Analysis

Vol. 2, Chapter 15 Ratio Analysis Problem 1: Solution Transaction Total CurrentWorking Current No. Assets Capital Ratio 1 0 0 0 2 + + + 3 0 0 0 4 0 - - 5-0 + 6 - - - 7 0 0 0 8 0 0 0 9 - - - 10-0 + Problem

Vol. 2, Chapter 15 Ratio Analysis Problem 1: Solution Transaction Total CurrentWorking Current No. Assets Capital Ratio 1 0 0 0 2 + + + 3 0 0 0 4 0 - - 5-0 + 6 - - - 7 0 0 0 8 0 0 0 9 - - - 10-0 + Problem

WORKING CAPITAL MANAGEMENT

CHAPTER 9 WORKING CAPITAL MANAGEMENT Working capital is the long term fund required to run the day to day operations of the business. The company starts with cash. It buys raw materials, employs staff

CHAPTER 9 WORKING CAPITAL MANAGEMENT Working capital is the long term fund required to run the day to day operations of the business. The company starts with cash. It buys raw materials, employs staff

How to Prepare a Cash Flow Forecast

The Orangeville & Area Small Business Enterprise Centre (SBEC) 87 Broadway, Orangeville ON L9W 1K1 519-941-0440 Ext. 2286 or 2291 sbec@orangeville.ca www.orangevillebusiness.ca Supported by its Partners:

The Orangeville & Area Small Business Enterprise Centre (SBEC) 87 Broadway, Orangeville ON L9W 1K1 519-941-0440 Ext. 2286 or 2291 sbec@orangeville.ca www.orangevillebusiness.ca Supported by its Partners:

UNITED STATES BANKRUPTCY COURT NORTHERN & EASTERN DISTRICTS OF TEXAS REGION 6 MONTHLY OPERATING REPORT

ACCRUAL BASIS JUDGE: UNITED STATES BANKRUPTCY COURT NORTHERN & EASTERN DISTRICTS OF TEXAS REGION 6 MONTHLY OPERATING REPORT MONTH ENDING: MONTH YEAR IN ACCORDANCE WITH TITLE 28, SECTION 1746, OF THE UNITED

ACCRUAL BASIS JUDGE: UNITED STATES BANKRUPTCY COURT NORTHERN & EASTERN DISTRICTS OF TEXAS REGION 6 MONTHLY OPERATING REPORT MONTH ENDING: MONTH YEAR IN ACCORDANCE WITH TITLE 28, SECTION 1746, OF THE UNITED

110 Questions(with Answers) On Accounting Basics FREE E-book from http://basiccollegeaccounting.com

On Accounting Basics FREE E-book from http://basiccollegeaccounting.com") (http://basiccollegeaccounting.com) Dedicated to helping Students & Teachers NOTE: 110 Questions & Answers on True Or False on Accounting Basics ACCOUNTING CONCEPTS & DOUBLE ENTRY SYSTEM True False 1.

(http://basiccollegeaccounting.com) Dedicated to helping Students & Teachers NOTE: 110 Questions & Answers on True Or False on Accounting Basics ACCOUNTING CONCEPTS & DOUBLE ENTRY SYSTEM True False 1.

Basic Business Plan Outline

Basic Business Plan Outline A business plan needs to be a well thought out, honest, appraisal of the business and opportunity. This outline is meant to be used for your road map. It should be a living

Basic Business Plan Outline A business plan needs to be a well thought out, honest, appraisal of the business and opportunity. This outline is meant to be used for your road map. It should be a living

Interpretation of Financial Statements

Interpretation of Financial Statements Author Noel O Brien, Formation 2 Accounting Framework Examiner. An important component of most introductory financial accounting programmes is the analysis and interpretation

Interpretation of Financial Statements Author Noel O Brien, Formation 2 Accounting Framework Examiner. An important component of most introductory financial accounting programmes is the analysis and interpretation

In accordance with regulation 24(c) of the National Standards Bodies Regulations of 1998, the Standards Generating Body (SGB) for

of the National Standards Bodies Regulations of 1998, the Standards Generating Body (SGB) for") 32 No. 26122: GOVERNMENT GAZETTE, 5 MARCH 2004 No. 291 5 March 2004 SOUTH AFRICAN QUALIFICATIONS AUTHORIN (SAQA) In accordance with regulation 24(c) of the National Standards Bodies Regulations of 1998,

32 No. 26122: GOVERNMENT GAZETTE, 5 MARCH 2004 No. 291 5 March 2004 SOUTH AFRICAN QUALIFICATIONS AUTHORIN (SAQA) In accordance with regulation 24(c) of the National Standards Bodies Regulations of 1998,

PERSONAL FINANCIAL STATEMENT

PERSONAL FINANCIAL STATEMENT As of, 20 BUSINESS PLAN GUIDELINES Name: Residence Phone: Residence Address: City, State, Zip Code: Social Security Number: PERSONAL ASSETS PERSONAL LIABILITIES Cash in Bank

PERSONAL FINANCIAL STATEMENT As of, 20 BUSINESS PLAN GUIDELINES Name: Residence Phone: Residence Address: City, State, Zip Code: Social Security Number: PERSONAL ASSETS PERSONAL LIABILITIES Cash in Bank

ACCOUNTING RATIOS I. MODULE - 6A Analysis of Financial Statements. Accounting Ratios - I. Notes

MODULE - 6A Accounting Ratios - I 8 ACCOUNTING RATIOS I In the previous lesson, you have learnt the relationship between various items of the financial statements. You have also learnt various tools of

MODULE - 6A Accounting Ratios - I 8 ACCOUNTING RATIOS I In the previous lesson, you have learnt the relationship between various items of the financial statements. You have also learnt various tools of

Discretionary Owner Earnings (%) Firms Analyzed 2011 2,736 2012 2,982 2013 2,979 2014 2,814 2015 2,392

Firms Analyzed 2011 2,736 2012 2,982 2013 2,979 2014 2,814 2015 2,392") Industry Financial Report release date: June 216 ALL US [23822] Plumbing, Heating, and Air-Conditioning Contractors Sector: Construction Sales Class: $5m - $9.99m Contents Income-Expense statement - dollar-based

Industry Financial Report release date: June 216 ALL US [23822] Plumbing, Heating, and Air-Conditioning Contractors Sector: Construction Sales Class: $5m - $9.99m Contents Income-Expense statement - dollar-based

Turnover between 320,000 and 13,000,000 ( 250,000) and ( 10,000,000)

and ( 10,000,000)") Accounts Information for General Traders Turnover between 320,000 and 13,000,000 ( 250,000) and ( 10,000,000) File Returns and Accounts Information online at www.revenue.ie Revenue On-Line Service Paper

Accounts Information for General Traders Turnover between 320,000 and 13,000,000 ( 250,000) and ( 10,000,000) File Returns and Accounts Information online at www.revenue.ie Revenue On-Line Service Paper

Trading Profit and Loss Account

Trading Profit and Loss Account Trading Account The trading account shows the income from sales and the direct costs of making those sales. It includes the balance of stocks at the start and end of the

Trading Profit and Loss Account Trading Account The trading account shows the income from sales and the direct costs of making those sales. It includes the balance of stocks at the start and end of the

NOTES TO ASSIST COMPLETION OF BUSINESS QUESTIONNAIRE

NOTES TO ASSIST COMPLETION OF BUSINESS QUESTIONNAIRE Never change company shareholding without conferring with us because there are tax implications. Please note the following comments 1. Cars If you sell

NOTES TO ASSIST COMPLETION OF BUSINESS QUESTIONNAIRE Never change company shareholding without conferring with us because there are tax implications. Please note the following comments 1. Cars If you sell

MEETINGS & EVENTS COLLECTION TERMS & CONDITIONS

MEETINGS & EVENTS COLLECTION The Meetings & Events Collection Offer ( Offer ) is available for new meeting or event group bookings consisting of a minimum of 10 bedroom bookings for a minimum 1 night stay

MEETINGS & EVENTS COLLECTION The Meetings & Events Collection Offer ( Offer ) is available for new meeting or event group bookings consisting of a minimum of 10 bedroom bookings for a minimum 1 night stay

Small Company Limited. Report and Accounts. 31 December 2007

Registered number 123456 Small Company Limited Report and Accounts 31 December 2007 Report and accounts Contents Page Company information 1 Directors' report 2 Accountants' report 3 Profit and loss account

Registered number 123456 Small Company Limited Report and Accounts 31 December 2007 Report and accounts Contents Page Company information 1 Directors' report 2 Accountants' report 3 Profit and loss account

WORKING CAPITAL MANAGEMENT

WORKING CAPITAL MANAGEMENT What is Working Capital Working capital management is the set of activities that are required to run day to day operations of the business to ensure that cash is adequate to

WORKING CAPITAL MANAGEMENT What is Working Capital Working capital management is the set of activities that are required to run day to day operations of the business to ensure that cash is adequate to

Studyguide.PK Accounts Revision Notes Page 1

BOOKS OF ORIGINAL ENTRIES These are the books of first entry. The transactions are first recorded in these books before being entered in the ledger books. These books are also called as books of Prime

BOOKS OF ORIGINAL ENTRIES These are the books of first entry. The transactions are first recorded in these books before being entered in the ledger books. These books are also called as books of Prime

Discretionary Owner Earnings (%) Firms Analyzed 2011 45 2012 42 2013 41 2014 43 2015 39

Firms Analyzed 2011 45 2012 42 2013 41 2014 43 2015 39") Industry Financial Report release date: June 216 Harrisburg, PA Metro Area [23822] Plumbing, Heating, and Air-Conditioning Contractors Sector: Construction Sales Class: $1m - $2.49m Contents Income-Expense

Industry Financial Report release date: June 216 Harrisburg, PA Metro Area [23822] Plumbing, Heating, and Air-Conditioning Contractors Sector: Construction Sales Class: $1m - $2.49m Contents Income-Expense

Article Accounting Terminology

Article Accounting Terminology Contents Page 1. Accounting Period... 4 2. Accounts Payable (Sundry Creditors)... 4 3. Accounts Receivable (Sundry Debtors)... 4 4. Assets... 4 5. Benchmarks... 4 6. B.O.S.

Article Accounting Terminology Contents Page 1. Accounting Period... 4 2. Accounts Payable (Sundry Creditors)... 4 3. Accounts Receivable (Sundry Debtors)... 4 4. Assets... 4 5. Benchmarks... 4 6. B.O.S.

Accounting Skills Assessment Practice Exam Page 1 of 10

NAU ACCOUNTING SKILLS ASSESSMENT PRACTICE EXAM & KEY 1. A company received cash and issued common stock. What was the effect on the accounting equation? Assets Liabilities Stockholders Equity A. + NE +

NAU ACCOUNTING SKILLS ASSESSMENT PRACTICE EXAM & KEY 1. A company received cash and issued common stock. What was the effect on the accounting equation? Assets Liabilities Stockholders Equity A. + NE +

ACCOUNTING GLOSSARY. Charities/IPCs should retain relevant documents to support their valuation.

ACCOUNTING GLOSSARY S/N Accounting Terms Explanations INCOME 1. Donations Gifts to Charities/Approved Institution of A Public Character (hereinafter referred to as IPCs) comprise donations in cash and

ACCOUNTING GLOSSARY S/N Accounting Terms Explanations INCOME 1. Donations Gifts to Charities/Approved Institution of A Public Character (hereinafter referred to as IPCs) comprise donations in cash and

6. Show all your workings. icpar

CERTIFIED PUBLIC ACCOUNTANT FOUNDATION LEVEL 1 EXAMINATION F1.3: FINANCIAL ACCOUNTING MONDAY: 10 JUNE 2013 INSTRUCTIONS: 1. Time Allowed: 3 hours 15 minutes (15 minutes reading and 3 hours writing). 2.

CERTIFIED PUBLIC ACCOUNTANT FOUNDATION LEVEL 1 EXAMINATION F1.3: FINANCIAL ACCOUNTING MONDAY: 10 JUNE 2013 INSTRUCTIONS: 1. Time Allowed: 3 hours 15 minutes (15 minutes reading and 3 hours writing). 2.

FINANCIAL STATEMENTS-II

MODULE - 3 15 FINANCIAL STATEMENTS-II You have learnt that Income Statement i.e. Trading & Profit and Loss Account and Position Statement i.e., Balance Sheet are two financial statements, which are prepared

MODULE - 3 15 FINANCIAL STATEMENTS-II You have learnt that Income Statement i.e. Trading & Profit and Loss Account and Position Statement i.e., Balance Sheet are two financial statements, which are prepared

A PRACTICAL GUIDE TO WRITING A BUSINESS PLAN

A PRACTICAL GUIDE TO WRITING A BUSINESS PLAN Louisiana Small Business Development Center At Southeastern Louisiana University 1514 Martens Drive Hammond, LA 70401 Phone: (985) 549-3831 Fax: (985) 549-2127

A PRACTICAL GUIDE TO WRITING A BUSINESS PLAN Louisiana Small Business Development Center At Southeastern Louisiana University 1514 Martens Drive Hammond, LA 70401 Phone: (985) 549-3831 Fax: (985) 549-2127

GCE. Accounting. Mark Scheme for January 2012. Advanced GCE Unit F013: Company Accounts and Interpretation. Oxford Cambridge and RSA Examinations

GCE Accounting Advanced GCE Unit F013: Company Accounts and Interpretation Mark Scheme for January 2012 Oxford Cambridge and RSA Examinations OCR (Oxford Cambridge and RSA) is a leading UK awarding body,

GCE Accounting Advanced GCE Unit F013: Company Accounts and Interpretation Mark Scheme for January 2012 Oxford Cambridge and RSA Examinations OCR (Oxford Cambridge and RSA) is a leading UK awarding body,

Reputation Management & Social Media Optimization

Reputation Management & Social Media Optimization with The Customer Experience Step 1: Customer books your hotel Step 2: Customer checks In Step 3: Customer has a wonderful experience and writes about

Reputation Management & Social Media Optimization with The Customer Experience Step 1: Customer books your hotel Step 2: Customer checks In Step 3: Customer has a wonderful experience and writes about

The Interpretation of Financial Statements. Why use ratio analysis. Limitations. Chapter 16

The Interpretation of Financial Statements Chapter 16 1 Luby & O Donoghue (2005) Why use ratio analysis Provides framework Comparison to previous years Trends identified Identify areas of concern Targets

The Interpretation of Financial Statements Chapter 16 1 Luby & O Donoghue (2005) Why use ratio analysis Provides framework Comparison to previous years Trends identified Identify areas of concern Targets

Report Description. Business Counts. Top 10 States (by Business Counts) Page 1 of 16

Page 1 of 16") 5-Year County-Level Financial Profile Industry Report Architectural Services (SIC Code: 8712) in Prince George County, Maryland Sales Range: $500,000 - $999,999 Date: 11/07/08 Report Description This 5-Year

5-Year County-Level Financial Profile Industry Report Architectural Services (SIC Code: 8712) in Prince George County, Maryland Sales Range: $500,000 - $999,999 Date: 11/07/08 Report Description This 5-Year

Statistical release P5002

Statistical release (Preliminary) Embargoed until: 22 November 2012 13:00 Enquiries: User Information Services 012 310 8600/8351 1 Table of Contents 1. Summary of findings for the year 2011... 2 Figure

Statistical release (Preliminary) Embargoed until: 22 November 2012 13:00 Enquiries: User Information Services 012 310 8600/8351 1 Table of Contents 1. Summary of findings for the year 2011... 2 Figure

2006 VCE VET Financial Services GA 2: Written examination

VCE VET Financial Services GA 2: Written examination GENERAL COMMENTS Students were well prepared for the VCE VET Financial Services examination, and a significant number achieved pleasing results. It

VCE VET Financial Services GA 2: Written examination GENERAL COMMENTS Students were well prepared for the VCE VET Financial Services examination, and a significant number achieved pleasing results. It

LEADing Practice Financial Scorecard Measurements

LEADing Practice Financial Scorecard Measurements Scorecard Area Finance & Accounting Scorecard Group Accounting ratios Balance sheet Scorecard Performance Measurement Deferred revenue as % of total revenue

LEADing Practice Financial Scorecard Measurements Scorecard Area Finance & Accounting Scorecard Group Accounting ratios Balance sheet Scorecard Performance Measurement Deferred revenue as % of total revenue

KPI ENCYCLOPEDIA FINANCE. A Comprehensive Collection of KPI Definitions for. www.opsdog.com info@opsdog.com 201.526.1200

KPI ENCYCLOPEDIA A Comprehensive Collection of KPI Definitions for FINANCE www.opsdog.com info@opsdog.com 201.526.1200 Table of Contents KPI Encyclopedia OpsDog Services Overview...2 Metric Definitions....3

KPI ENCYCLOPEDIA A Comprehensive Collection of KPI Definitions for FINANCE www.opsdog.com info@opsdog.com 201.526.1200 Table of Contents KPI Encyclopedia OpsDog Services Overview...2 Metric Definitions....3

BUSINESS FINANCIAL STATEMENT. Limited Liability Company Partnership Corporation Other. Statement of Financial Condition as of, 20 for the period, to,

BUSINESS FINANCIAL STATEMENT Name of Business Applicant Prepared By Title (Position) Limited Liability Company Partnership Corporation Other Statement of Financial Condition as of, 20 for the period, to,

BUSINESS FINANCIAL STATEMENT Name of Business Applicant Prepared By Title (Position) Limited Liability Company Partnership Corporation Other Statement of Financial Condition as of, 20 for the period, to,

Unallowable Cost Categories (in alphabetical order)

") Unallowable Cost Definitions Unallowable costs are those costs that cannot be charged to the Federal Government or included in the Facilities and Administrative (indirect) cost rate. Overview The Office

Unallowable Cost Definitions Unallowable costs are those costs that cannot be charged to the Federal Government or included in the Facilities and Administrative (indirect) cost rate. Overview The Office

A guide to business cash flow management

A guide to business cash flow management Contents 01. Cash flow management 01 02. Practical steps to managing cash flow 04 03. Improving everyday cash flow 06 04. How to manage cash flow surpluses and

A guide to business cash flow management Contents 01. Cash flow management 01 02. Practical steps to managing cash flow 04 03. Improving everyday cash flow 06 04. How to manage cash flow surpluses and

Ratios from the Statement of Financial Position

For The Year Ended 31 March 2007 Ratios from the Statement of Financial Position Profitability Ratios Return on Sales Ratio (%) This is the difference between what a business takes in and what it spends

For The Year Ended 31 March 2007 Ratios from the Statement of Financial Position Profitability Ratios Return on Sales Ratio (%) This is the difference between what a business takes in and what it spends

Management Accounting and Decision-Making

Management Accounting 15 Management Accounting and Decision-Making Management accounting writers tend to present management accounting as a loosely connected set of decision making tools. Although the

Management Accounting 15 Management Accounting and Decision-Making Management accounting writers tend to present management accounting as a loosely connected set of decision making tools. Although the

Sample Due Diligence Checklist

Sample Due Diligence Checklist 01.0. CORPORATE ORGANIZATION AND HISTORY 1.1. - Overview of corporate legal structure, banking relationships (other than transaction financing), organizational charts and

Sample Due Diligence Checklist 01.0. CORPORATE ORGANIZATION AND HISTORY 1.1. - Overview of corporate legal structure, banking relationships (other than transaction financing), organizational charts and

Accounting Notes. Purchasing Merchandise under the Perpetual Inventory system:

Systems: Perpetual VS Periodic " Keeps running record of all goods " Does not keep a running record bought and sold " is counted once a year " is counted at least once a year " Used for all types of goods

Systems: Perpetual VS Periodic " Keeps running record of all goods " Does not keep a running record bought and sold " is counted once a year " is counted at least once a year " Used for all types of goods