Pension Fund Regulatory and Development Authority

|

|

|

- Solomon Cain

- 9 years ago

- Views:

Transcription

1 Pension Fund Regulatory and Development Authority PFRDA, First Floor, ICADR Building, Phase II, Plot No 6, Vasant Kunj Institutional Area, New Delhi

2 Presentation Topics Indian Pension Scenario National Pension System Milestones Sectors at a Glance (NPS Statistics) NPS Corporate Model Basic Features & Eligibility Registration Process Asset Classes Contribution & Investment Options Tax Benefits To Employers & Employees Additional Tax Benefits to NPS Subscribers Charges Exit & Withdrawal 2

3 By 2050, every fifth Indian will be 60 years old compared to one in 12 today. There are nearly 100 million people aged 60 or more in India today. The number will TRIPLE by 2050; most of them financially insecure in the sunset years if a social security net doesn t start NOW. The Need of the Hour- A multifold increase in pension coverage to private sector. 3

4 Formal Pension coverage to mere 12% of the population i.e. approx. 1 in every 8. Most of the formal pension coverage available to Government employees. For Corporate sector, mainly EPS under EPFO is available as pension product, mandatory* for the employees earning upto Rs. 15,000/- p.m. *- Changes proposed in this vide Budget discussed later 4

5 February 2003 December 2003 Announcement of National Pension System (NPS) based on Defined Contribution; mandatory for CG employees joining on or after Notification for setting up a statutory Pension Fund Regulatory and Development Authority, brought about. May 2009 NPS made available to all citizens of India on May 01 st December 2011 A customized version of NPS, known as NPS-Corporate Sector Model introduced. September 2013 PFRDA Act, 2013 passed in Parliament. February 2014 Notification of PFRDA Act,

6 Age Group 0 to to Onwards NPS provides a platform for saving to create corpus, to enable subscriber for purchasing Annuity post retirement What is NPS? A highly efficient, technology driven system to save small amounts today, to build a fund for life s second innings. Who Can Join? You can join, if you are any or all of the following: Citizen of India; Resident or Non-Resident Age between years, as on date of joining Salaried or Self Employed Complies with KYC norms 6

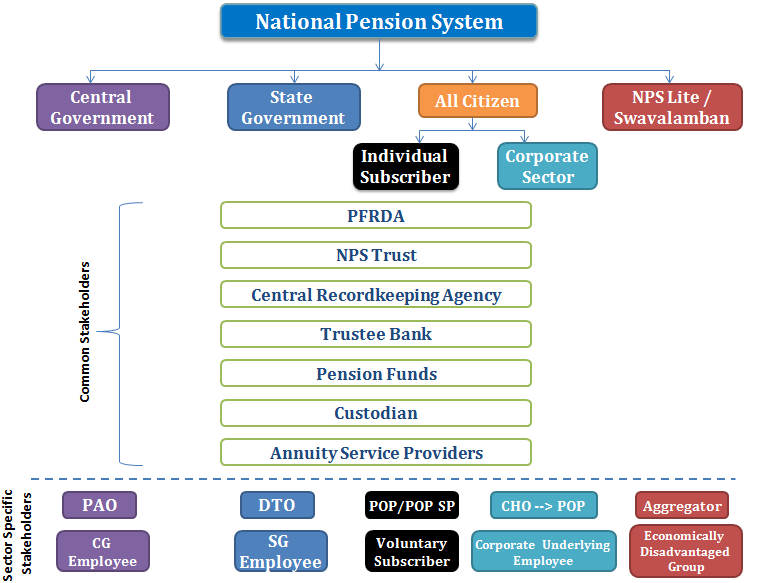

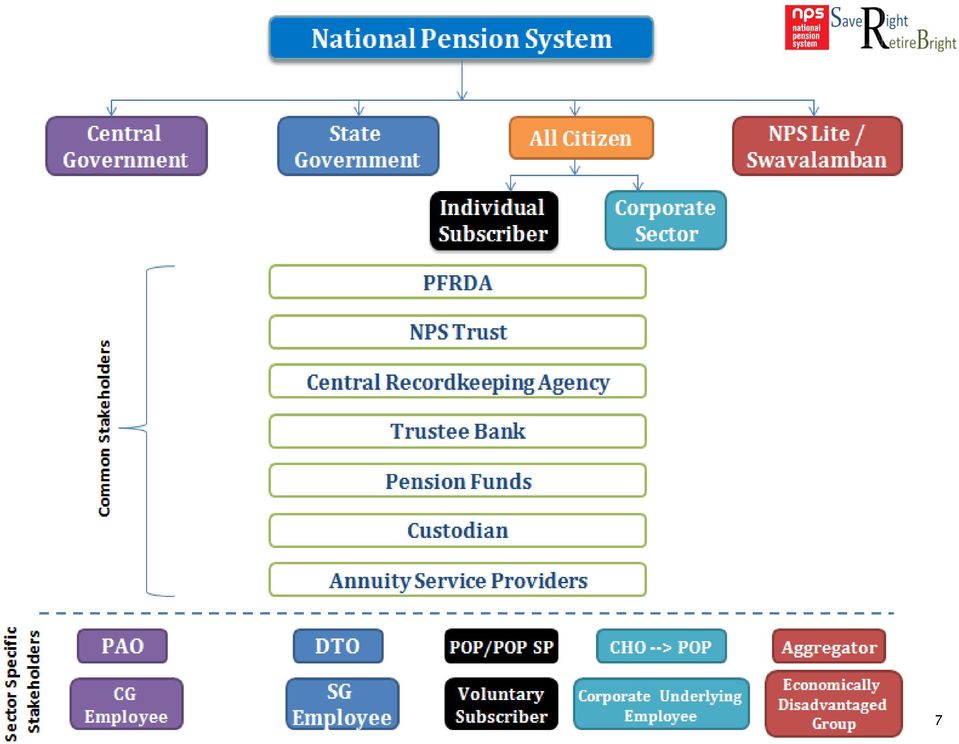

7 7

8 Sector Number of Subscribers (In Lacs) Contribution (Rs Crores) (A) Total Assets Under Management (Rs Crores) Central Government 15,11,528 27, , State Government 26,30,194 29, , Corporate 3,73,273 4, , Unorganized 86, NPS Lite 41,46,880 1, , Total 87,48,649 63, , As on March 31 st

9 , , , , , , , , , , ,000 0 `March- 13 `March-14 `March-15 No. of Corporates registered AUM (Rs. In Crs.) No. of Subscribers registered 0 As on March 31 st

10 PFRDA launched a separate model to provide NPS to the employees of corporate entities, including PSUs, during Dec Customized version of the Core NPS Model to suit various Organizations. Existing as well as new employees can be brought under NPS platform. NPS can be run parallel to Superannuation, Gratuity, PF, EPF and any other pension schemes offered to the employees of organized entities. In the Budget it has been announced that employee will be given option to choose between EPF and NPS. 10

11 Built on a highly efficient, technology driven platform Unmatched Lowest cost of Investment* Attractive Tax Benefits for Employees and Employers* Prudentially Regulated by PFRDA Attractive Market Linked Returns Investments managed by experienced Pension Funds Safe, Secure and Easily Portable *- Discussed in detail, later in the presentation 11

12 Tier-I account: Employer / Employee contribute for retirement into this non-withdrawal account. Income Tax benefits as per IT Act, 1961 available for both employer and employee contributions. Tier-II account: Voluntary savings facility, where the subscriber can avail fund management facility at very low costs. Subscribers are free to withdraw amount from this account. However, tax benefits are not available. Note : *Total Corpus of Rs.2000/- is required at the end of Financial Year. 12

13 Eligible entities to register under NPS Corporate Model Entities registered under Companies Act Entities registered under various Co-operative Acts Central & State Public Sector Enterprises Registered Partnership firms & Limited Liability Partnerships (LLPs) Any entity incorporated under any act of Parliament or State legislature or by order of Central / State Govt. Proprietorship concern Society/Trust 13

14 Corporate has to select POP and tie-up with it. The Corporate submits the CHO-1 Form to the POP. POP would submit the form to CRA CRA registers the Corporate in the CRA system and allots Corporate Registration Number (CRN) to Corporate. 14

15 New Initiative Proposed vide POP Regulations, 2015 As per Regulation, the following entities may opt for registration as a Point of Presence Corporate: Central and State PSUs Any other entity, organization or company with minimum employee strength of three hundred Corporate will be required to submit specified application alongwith Rs.10,000/- for registration as POP- Corporate After verification and necessary due diligence, PFRDA will grant the Certificate of Registration as POP- Corporate to the corporate The Corporate submits the CHO-1 Form to the CRA. CRA registers the Corporate in the CRA system and allots Corporate Registration Number (CRN) to Corporate. 15

16 As per Regulation- KYC Verification, Addressing/ handling queries/ grievances of subscribers (existing/potential), providing & displaying information regarding NPS point of interaction between subscriber and the CRA receive & process, with adequate checks, the applications of subscribers for registration under NPS collection, transmission of contribution funds within specified timeframes to the TB and maintenance of complete records of transactions Handling withdrawal requests 16

17 Employees fill up & submit CS-S1 forms with required KYC Documents to Corporates (employer). Corporate verifies the employment details and sends these forms to the attached POP. POP does KYC verification and sends these forms to CRA. CRA registers the employees and generate PRAN. PRANs are dispatched to Corporate or employees as per their choice. 17

18 Three flexible variations of contributions from employer and employee Equal contributions by employer and employee Unequal contribution by the employer and the employee Contribution from either the employer or the employee 18

19 Investment Option can be exercised at At Corporate Level At Subscriber Level 19

20 Selection of Investment Option 1. Selection of Pension Fund 2. Selection of Investment Choice (Selection of Asset Mix of E, C & G) 20

21 Selection of any one PF out of the following: SBI Pension Funds Pvt. Limited LIC Pension Fund Limited UTI Retirement Solutions Limited ICICI Prudential Pension funds Management Company Limited Kotak Mahindra Pension Fund Limited Reliance Capital Pension Fund Limited HDFC Pension Fund Limited Pension fund to be incorporated by Birla Sun Life Insurance company limited 21

22 Active Choice Auto Choice Subscriber selects the allocation of his / her funds among 3 Asset Classes, with contribution in Asset Class E be restricted to 50% of total Contribution. Fund invested, divided among 3 Asset Classes determined by a Pre-Defined portfolio ratio. 22

23 G-Secs Up to 100% G E C Equity Up to 50% Corporate Debt Up to 100% Pension Corpus 23

24 E C G Age- upto 35 years Age- 45 years Age- 55 years & above 24

25 To Employers Contributions made by the employer (upto 10% of Basic + DA) is allowed as a business expense under Section 36 (1) iv (a) of Income Tax Act To Employees Employees own contribution is eligible for tax deduction under sec 80 CCD (1) of Income Tax Act up to 10% of salary (Basic + DA). This is within the overall ceiling of Rs Lacs under Sec. 80 CCE of the Income Tax Act. Employee also gets tax deduction for the contribution made by the employer under section 80 CCD (2) of IT act upto 10% of salary (Basic + DA)which is in addition to the tax benefits available under Sec. 80 CCE. 25

26 Budget Announcements and resultant Tax Benefits Tax deduction limit under sec 80 CCD (1) ceiling raised from Rs Lac to Rs Lacs. From F.Y , subscriber will be allowed tax deduction in addition to the deduction allowed under Sec. 80CCD(1) for additional contribution in his NPS account subject to maximum of Rs. 50,000/- under sec. 80CCD 1(B). Effective Tax benefits in NPS has increased on investments from Rs Lac in FY to Rs Lacs in FY

27 Intermediary Charge Head Service Charge Method of Deduction Initial Subscriber Registration Rs. 100 POP Initial Contribution All Subsequent Contribution 0.25% Min: Rs. 20 & Max : Rs.25,000 To be Collected Upfront All Non-Financial Transaction Rs. 20 PRA Opening (One Time) Rs. 50 CRA PRA Maitenance (Per Annum) Rs. 190 Per Transaction ( Financial/Non-Financial) Rs. 4 Custodian Asset Serving (Per Annum) % Through NAV cancellation/deduction PFM Investment Management (Per Annum) 0.01% 27

28 Pre mature Retirement Vesting Criteria At any point in time before 60 years of Age Conditions for Withdrawal Normal Retirement Vesting Criteria On attaining the Age of 60 years and up to 70 years of age Death of subscriber Vesting Criteria Death due to any cause 28

29 Vesting Criteria Benefit At any point in time before 60 years of Age (allowed to subscriber who have been in NPS for at least 10 years) On attaining the Age of 60 years or age of superannuation as prescribed in service rules) and upto 70 years of age Compulsory Annuitisation- minimum 80% Lump sum withdrawal- maximum 20% If Corpus< Rs Lac, complete withdrawal Annuitisation- minimum 40% Lump sum withdrawal- maximum 60% If Corpus< Rs Lac, complete withdrawal - Subscriber can stay invested in the NPS upto the age of 70 years. Fresh contributions are allowed during such a period of deferment. - Can defer the withdrawal of eligible lump sum amount till the age of 70 years. -Annuity purchase can also be deferred for maximum period of 3 years at the time of exit. Death due to any cause In such an unfortunate event, option will be available to the nominee to receive 100% of the NPS pension wealth in lump sum. However, if the nominee wishes to continue with the NPS, he/she shall have to subscribe to NPS individually after following due KYC procedure. Partial Withdrawal Subscriber will have the option to withdraw up to 25% of his own contribution in certain circumstances. 29

30 Empanelled ASPs Life Insurance Corporation of India SBI Life Insurance Co. Ltd. ICICI Prudential Life Insurance Co. Ltd. Bajaj Allianz Life Insurance Co. Ltd. Star Union Dai-ichi Life Insurance Co. Ltd. Reliance Life Insurance Co. Ltd. HDFC Standard Life Insurance Co. Ltd. 30

31 31

FREQUENTLY ASKED QUESTIONS. NATIONAL PENSION SYSTEM for NON RESIDENT INDIANS

FREQUENTLY ASKED QUESTIONS NATIONAL PENSION SYSTEM for NON RESIDENT INDIANS About NPS 1. What is National Pension System? NPS is an easily accessible, low cost, tax-efficient, flexible and portable retirement

FREQUENTLY ASKED QUESTIONS NATIONAL PENSION SYSTEM for NON RESIDENT INDIANS About NPS 1. What is National Pension System? NPS is an easily accessible, low cost, tax-efficient, flexible and portable retirement

National Pension System. for Corporate NPS

National Pension System for Corporate NPS Pension Fund Regulatory and Development Authority 1st Floor, ICADR Building, Plot No.6, Vasant Kunj Institutional Area, Phase II, New Delhi Tel: (011) 26897948

National Pension System for Corporate NPS Pension Fund Regulatory and Development Authority 1st Floor, ICADR Building, Plot No.6, Vasant Kunj Institutional Area, Phase II, New Delhi Tel: (011) 26897948

FREQUENTLY ASKED QUESTIONS ON NATIONAL PENSION SYSTEM ALL CITIZENS MODEL

FREQUENTLY ASKED QUESTIONS ON NATIONAL PENSION SYSTEM ALL CITIZENS MODEL What is National Pension System? NPS is an easily accessible, low cost, tax-efficient, flexible and portable retirement savings

FREQUENTLY ASKED QUESTIONS ON NATIONAL PENSION SYSTEM ALL CITIZENS MODEL What is National Pension System? NPS is an easily accessible, low cost, tax-efficient, flexible and portable retirement savings

National Pension System (Nps) Welcome to the National Pension System

Welcome to the National Pension System") National Pension System (Nps) NPS, regulated by PFRDA, is an important milestone in the development of a sustainable and efficient voluntary defined contribution pension system in India. It has the following

National Pension System (Nps) NPS, regulated by PFRDA, is an important milestone in the development of a sustainable and efficient voluntary defined contribution pension system in India. It has the following

PENSION FUND REGULATORY AND DEVELOPMENT AUTHORITY

PENSION FUND REGULATORY AND DEVELOPMENT AUTHORITY EXPOSURE DRAFT ON PROPOSED OPERATIONAL WITHDRAWAL PROCESS FOR NPS SUBSCRIBERS Issued on: 26 th December, 2013 Last date to accept Comments: 31 st January,

PENSION FUND REGULATORY AND DEVELOPMENT AUTHORITY EXPOSURE DRAFT ON PROPOSED OPERATIONAL WITHDRAWAL PROCESS FOR NPS SUBSCRIBERS Issued on: 26 th December, 2013 Last date to accept Comments: 31 st January,

National Pension System (NPS)

") OFFER DOCUMENT National Pension System (NPS) Pension Fund Regulatory and Development Authority (PFRDA) originally established by the Government of India through a resolution dated 10 th October, 2003 &

OFFER DOCUMENT National Pension System (NPS) Pension Fund Regulatory and Development Authority (PFRDA) originally established by the Government of India through a resolution dated 10 th October, 2003 &

Frequently Asked Questions. NPS: Frequently Asked Questions

New Pension System (01 January 2004) Frequently Asked Questions Department of Economic Affairs Ministry of Finance, Government of India North Block, New Delhi 110 001 For any further questions or clarifications,

New Pension System (01 January 2004) Frequently Asked Questions Department of Economic Affairs Ministry of Finance, Government of India North Block, New Delhi 110 001 For any further questions or clarifications,

Introduction to Retirement Planning

Introduction to Retirement Planning for School Students Retirement: is a stage in the life cycle of an individual when one stops being an active part of the productive/ working population on account of

Introduction to Retirement Planning for School Students Retirement: is a stage in the life cycle of an individual when one stops being an active part of the productive/ working population on account of

SOCIAL SECURITY AND PENSIONS IN INDIA

SOCIAL SECURITY AND PENSIONS IN INDIA PRESENTATION APRIL 2-3, 2003 COLOMBO (SRI LANKA) U.KSINHA MINISTRY OF FINANCE, GOI, NEW DELHI FRAMEWORK OF THE PRESENTATION BASIC FACTS ON INDIAN ECONOMY COMPONENTS

SOCIAL SECURITY AND PENSIONS IN INDIA PRESENTATION APRIL 2-3, 2003 COLOMBO (SRI LANKA) U.KSINHA MINISTRY OF FINANCE, GOI, NEW DELHI FRAMEWORK OF THE PRESENTATION BASIC FACTS ON INDIAN ECONOMY COMPONENTS

ATAL PENSION YOJANA (APY) - SUBSCRIBER REGISTRATION FORM

- SUBSCRIBER REGISTRATION FORM") ATAL PENSION YOJANA (APY) - SUBSCRIBER REGISTRATION FORM (Administered by Pension Fund Regulatory and Development Authority) To, The Branch Manager, Bank Branch Dear Sir/Madam, I hereby request that an

ATAL PENSION YOJANA (APY) - SUBSCRIBER REGISTRATION FORM (Administered by Pension Fund Regulatory and Development Authority) To, The Branch Manager, Bank Branch Dear Sir/Madam, I hereby request that an

Atal Pension Yojana (APY) 1 Details of the Scheme. 1. Introduction

1 Details of the Scheme. 1. Introduction") Atal Pension Yojana (APY) 1 Details of the Scheme 1. Introduction 1.1 The Government of India is extremely concerned about the old age income security of the working poor and is focused on encouraging

Atal Pension Yojana (APY) 1 Details of the Scheme 1. Introduction 1.1 The Government of India is extremely concerned about the old age income security of the working poor and is focused on encouraging

HEARTY GREETINGS LIC S NEW GROUP SUPERANNUATION SCHEME

HEARTY GREETINGS TO LIC S NEW GROUP SUPERANNUATION SCHEME Why Superannuation Benefit EMPLOYER: Support Employment Policies Attract and Retain key talented Employees Reduces Attrition Levels Provides Tax

HEARTY GREETINGS TO LIC S NEW GROUP SUPERANNUATION SCHEME Why Superannuation Benefit EMPLOYER: Support Employment Policies Attract and Retain key talented Employees Reduces Attrition Levels Provides Tax

PENSION FUND REGULATORY AND DEVELOPMENT AUTHORITY. PFRDA/ 2013/2/ PDEX / 2 January 22, 2013

PFRDA/ 2013/2/ PDEX / 2 January 22, 2013 To, All POP s, Aggregators, CRA, Central and State Governments, Dear Sir/ Madam, Sub: Master Circular on Product design and Exit from National Pension System (NPS)

PFRDA/ 2013/2/ PDEX / 2 January 22, 2013 To, All POP s, Aggregators, CRA, Central and State Governments, Dear Sir/ Madam, Sub: Master Circular on Product design and Exit from National Pension System (NPS)

TAX Saving Guide. Compiled Date: 11/04/2011 www.prodigytechnologies.in

TAX Saving Guide Compiled Date: 11/04/2011 www.prodigytechnologies.in Objective 1. This document will help salaried person to reduce tax liability. 2. Give insight of various sections under which a person

TAX Saving Guide Compiled Date: 11/04/2011 www.prodigytechnologies.in Objective 1. This document will help salaried person to reduce tax liability. 2. Give insight of various sections under which a person

Best Investment Options Under Section 80C to save tax

Best Investment Options Under Section 80C to save tax -Prathiba Girish Executive Summary - Most of the Income Tax payers try to save tax by saving under Section 80C of the Income Tax Act. However, it is

Best Investment Options Under Section 80C to save tax -Prathiba Girish Executive Summary - Most of the Income Tax payers try to save tax by saving under Section 80C of the Income Tax Act. However, it is

CHAPTER 5 FINANCIAL REPORTING PRACTICES OF LIFE INSURANCE COMPANIES

CHAPTER 5 FINANCIAL REPORTING PRACTICES OF LIFE INSURANCE COMPANIES CHAPTER 5 FINANCIAL REPORTING PRACTICES OF LIFE INSURANCE COMPANIES Life Insurance Corporation of India (LIC) was a sole player in the

CHAPTER 5 FINANCIAL REPORTING PRACTICES OF LIFE INSURANCE COMPANIES CHAPTER 5 FINANCIAL REPORTING PRACTICES OF LIFE INSURANCE COMPANIES Life Insurance Corporation of India (LIC) was a sole player in the

Retirement planning with Group Superannuation. ICICI Prudential Group Superannuation Plan. Eligibility. Superannuation Benefits payable

Retirement planning with Group Superannuation After a valuable professional career with an organization, employees require the security of a regular income flow when they retire. Organizations help employees

Retirement planning with Group Superannuation After a valuable professional career with an organization, employees require the security of a regular income flow when they retire. Organizations help employees

Section A Subscriber s Personal Details:

Annexure A1 Form 102-GP Page 1 National Pension System (NPS) Withdrawal Form for Claim of Accumulated Pension Wealth on exiting before the age of normal superannuation for Government Employees (To be filled

Annexure A1 Form 102-GP Page 1 National Pension System (NPS) Withdrawal Form for Claim of Accumulated Pension Wealth on exiting before the age of normal superannuation for Government Employees (To be filled

Frequently Asked Questions-Atal Pension Yojana

Frequently Asked Questions-Atal Pension Yojana 1. What is Pension? Why do I need it? A Pension provides people with a monthly income when they are no longer earning. Need for Pension: Decreased income

Frequently Asked Questions-Atal Pension Yojana 1. What is Pension? Why do I need it? A Pension provides people with a monthly income when they are no longer earning. Need for Pension: Decreased income

Chapter - VI FUND UTILISATION OF LIFE INSURANCE COMPANIES

Chapter - VI FUND UTILISATION OF LIFE INSURANCE COMPANIES The previous chapters have given the details pertaining to the direct and indirect funding made by LIC in Kerala, the sector wise and industry

Chapter - VI FUND UTILISATION OF LIFE INSURANCE COMPANIES The previous chapters have given the details pertaining to the direct and indirect funding made by LIC in Kerala, the sector wise and industry

INDIAN BANKS: SENIOR CITIZEN BENEFITS & SCHEMES

INDIAN BANKS: SENIOR CITIZEN BENEFITS & SCHEMES Union Bank of India: Interest Rate Benefit in Term Deposits to Senior Citizens (Source of Information: www.unionbankofindia.co.in/personal_benifit_senior_citizen.aspx,

INDIAN BANKS: SENIOR CITIZEN BENEFITS & SCHEMES Union Bank of India: Interest Rate Benefit in Term Deposits to Senior Citizens (Source of Information: www.unionbankofindia.co.in/personal_benifit_senior_citizen.aspx,

most important SBI LIFE - CAPASSURE GOLD UIN: 111N091V01

Secure your most important asset : your employees SBI LIFE - CAPASSURE GOLD UIN: 111N091V01 SBI Life Insurance Company Limited (SBI Life) offers SBI Life CapAssure Gold plan, featuring stable growth with

Secure your most important asset : your employees SBI LIFE - CAPASSURE GOLD UIN: 111N091V01 SBI Life Insurance Company Limited (SBI Life) offers SBI Life CapAssure Gold plan, featuring stable growth with

Safeguard your family's future against life's uncertainties

Safeguard your family's future against life's uncertainties Birla Sun Life Insurance Easy Protect Plan A traditional term insurance plan INTRODUCING BSLI Easy Protect Plan You are successful in your career

Safeguard your family's future against life's uncertainties Birla Sun Life Insurance Easy Protect Plan A traditional term insurance plan INTRODUCING BSLI Easy Protect Plan You are successful in your career

4.2 ANALYSIS OF THE PRIVATE LIFE INSURERS AND THEIR COMPARISON WITH THE PUBLIC LIFE INSURANCE SECTOR:

4.2 ANALYSIS OF THE PRIVATE LIFE INSURERS AND THEIR COMPARISON WITH THE PUBLIC LIFE INSURANCE SECTOR: The structure of the insurance industry has undergone a drastic change since liberalization, privatization

4.2 ANALYSIS OF THE PRIVATE LIFE INSURERS AND THEIR COMPARISON WITH THE PUBLIC LIFE INSURANCE SECTOR: The structure of the insurance industry has undergone a drastic change since liberalization, privatization

1 March 2006. An individual suffers from the risk of dying early and the risk of living too long. A term assurance plan covers the risk of dying.

1 March 2006 Term Plans: A Comprehensive Research Report An individual suffers from the risk of dying early and the risk of living too long. A covers the risk of dying. A can also be used as a cover against

1 March 2006 Term Plans: A Comprehensive Research Report An individual suffers from the risk of dying early and the risk of living too long. A covers the risk of dying. A can also be used as a cover against

The life insurance sector

BY: DR A. MUTHUSAMY AND A. MEERA WINDS OF CHANGE MARK LIFE INSURANCE MARKET IN INDIA India is still an under-insured country and holds the 18th position in the life insurance market of the world. The life

BY: DR A. MUTHUSAMY AND A. MEERA WINDS OF CHANGE MARK LIFE INSURANCE MARKET IN INDIA India is still an under-insured country and holds the 18th position in the life insurance market of the world. The life

FAQ on PF Act 1 What is the Contribution for Provident Fund both by the Employer & Employee?

FAQ on PF Act 1 What is the Contribution for Provident Fund both by the Employer & Employee? Ans : The Employee contributes 12% of his /her Basic Salary & the same amount is contributed by the Employer.

FAQ on PF Act 1 What is the Contribution for Provident Fund both by the Employer & Employee? Ans : The Employee contributes 12% of his /her Basic Salary & the same amount is contributed by the Employer.

HDFC Retirement Savings Fund

Feb 05, 2016 NFO Note HDFC Savings Fund Prologue: HDFC Mutual Fund has launched a New Fund named HDFC Savings Fund, an open ended tax savings cum pension fund. The NFO has opened for subscription on Feb

Feb 05, 2016 NFO Note HDFC Savings Fund Prologue: HDFC Mutual Fund has launched a New Fund named HDFC Savings Fund, an open ended tax savings cum pension fund. The NFO has opened for subscription on Feb

SBI LIFE -PRODUCT FEATURES

SBI LIFE -PRODUCT FEATURES KEYMAN INSURANCE Why a keyman policy? Person covered Min. & Max. at entry Maximum Cover Age Minimum Term To protect the Corporate against the financial consequences due to the

SBI LIFE -PRODUCT FEATURES KEYMAN INSURANCE Why a keyman policy? Person covered Min. & Max. at entry Maximum Cover Age Minimum Term To protect the Corporate against the financial consequences due to the

Unit-Linked Insurance Policies in the Indian Market- A Consumer Perspective

Unit-Linked Insurance Policies in the Indian Market- A Consumer Perspective R. Rajagopalan 1 Dean (Academic Affairs) T.A. Pai Management Institute Manipal-576 104 Email: [email protected] 1 The author

Unit-Linked Insurance Policies in the Indian Market- A Consumer Perspective R. Rajagopalan 1 Dean (Academic Affairs) T.A. Pai Management Institute Manipal-576 104 Email: [email protected] 1 The author

In this policy, the investment risk in the investment portfolio is borne by the policyholder. Type of Cover Basic Standard Enhanced

The road to your financial goals has many twists, turns and probably a few unexpected roadblocks. You need a plan that balances your savings and protection needs with ease, along with the benefit of liquidity

The road to your financial goals has many twists, turns and probably a few unexpected roadblocks. You need a plan that balances your savings and protection needs with ease, along with the benefit of liquidity

Max Life Partner Care Rider A Rider for Unit Linked Insurance Plans UIN: 104A023V01

Life Insurance Coverage is available in this Rider. About Max Life Insurance Max Life Partner Care Rider A Rider for Unit Linked Insurance Plans UIN: 104A023V01 Max Life Insurance, the leading non-bank

Life Insurance Coverage is available in this Rider. About Max Life Insurance Max Life Partner Care Rider A Rider for Unit Linked Insurance Plans UIN: 104A023V01 Max Life Insurance, the leading non-bank

Frequently Asked Questions (FAQs) on HDFC RGESS- Series 2

on HDFC RGESS- Series 2") Frequently Asked Questions (FAQs) on HDFC RGESS- Series 2 1. What is Rajiv Gandhi Equity Savings Scheme (RGESS)? With an objective to encourage flow of savings and to improve the depth of the domestic

Frequently Asked Questions (FAQs) on HDFC RGESS- Series 2 1. What is Rajiv Gandhi Equity Savings Scheme (RGESS)? With an objective to encourage flow of savings and to improve the depth of the domestic

Keep achieving milestones Even after retirement

Keep achieving milestones Even after retirement» Analyse your Retirement needs» Understand the product in detail» Know the tenure of Renewal Premium Payments Retirement means giving up work and continuing

Keep achieving milestones Even after retirement» Analyse your Retirement needs» Understand the product in detail» Know the tenure of Renewal Premium Payments Retirement means giving up work and continuing

Max Life Guaranteed Lifetime Income Plan Pension (A Traditional Non Linked Non Participating Immediate Annuity Pension Plan) UIN: 104N076V01

UIN: 104N076V01") About Max Life Max Life Guaranteed Lifetime Income Plan Pension (A Traditional Non Linked Non Participating Immediate Annuity Pension Plan) UIN: 104N076V01 Max Life Insurance, one of the leading non-bank

About Max Life Max Life Guaranteed Lifetime Income Plan Pension (A Traditional Non Linked Non Participating Immediate Annuity Pension Plan) UIN: 104N076V01 Max Life Insurance, one of the leading non-bank

Max Life Platinum Wealth Plan A Non Participating Unit Linked Insurance Plan UIN: 104L090V01

Max Life Platinum Wealth Plan A Non Participating Unit Linked Insurance Plan UIN: 104L090V01 LIFE INSURANCE COVERAGE IS AVAILABLE IN THIS PRODUCT. IN THIS POLICY, THE INVESTMENT RISK IN THE INVESTMENT

Max Life Platinum Wealth Plan A Non Participating Unit Linked Insurance Plan UIN: 104L090V01 LIFE INSURANCE COVERAGE IS AVAILABLE IN THIS PRODUCT. IN THIS POLICY, THE INVESTMENT RISK IN THE INVESTMENT

Value what your family values the most, you. Protect yourself now in 3 easy steps.

Value what your family values the most, you. Protect yourself now in 3 easy steps. Birla Sun Life Insurance Protect@Ease A traditional online term insurance plan INTRODUCING BSLI Protect@Ease You are successful

Value what your family values the most, you. Protect yourself now in 3 easy steps. Birla Sun Life Insurance Protect@Ease A traditional online term insurance plan INTRODUCING BSLI Protect@Ease You are successful

No. Fin (Pen) A (3)-5/2006 Government of Himachal Pradesh Finance (Pension) Department. Dated: Shimla-171002, 11 th June, 2010

A (3)-5/2006 Government of Himachal Pradesh Finance (Pension) Department. Dated: Shimla-171002, 11 th June, 2010") No. Fin (Pen) A (3)-5/2006 Government of Himachal Pradesh Finance (Pension) Department Dated: Shimla-171002, 11 th June, 2010 OFFICE MEMORANDUM Subject:- Adoption of PFRDA approved New Pension System (NPS)

No. Fin (Pen) A (3)-5/2006 Government of Himachal Pradesh Finance (Pension) Department Dated: Shimla-171002, 11 th June, 2010 OFFICE MEMORANDUM Subject:- Adoption of PFRDA approved New Pension System (NPS)

This chapter deals with the description of the sample of 1000 policyholders focused

CHAPTER -5 DATA ANALYSIS, INTERPRETATION AND FINDINGS This chapter deals with the description of the sample of 1000 policyholders focused on demographic factors (gender, age, religion, residence) data

CHAPTER -5 DATA ANALYSIS, INTERPRETATION AND FINDINGS This chapter deals with the description of the sample of 1000 policyholders focused on demographic factors (gender, age, religion, residence) data

Chapter 7 SUMMARY- FINDINGS AND SUGGESTIONS

Chapter 7 SUMMARY- FINDINGS AND SUGGESTIONS In academic field the research is an ongoing process that knows no limits and no full stops. Even then the main findings emerging out of the present study have

Chapter 7 SUMMARY- FINDINGS AND SUGGESTIONS In academic field the research is an ongoing process that knows no limits and no full stops. Even then the main findings emerging out of the present study have

CRISIL - AMFI ELSS Fund Performance Index. Factsheet March 2016

CRISIL - AMFI ELSS Fund Performance Index Factsheet March 2016 Table of Contents About the Index... 3 Features and Characteristics... 3 Methodology... 3 CRISIL - AMFI ELSS Fund Performance Index: Constituent

CRISIL - AMFI ELSS Fund Performance Index Factsheet March 2016 Table of Contents About the Index... 3 Features and Characteristics... 3 Methodology... 3 CRISIL - AMFI ELSS Fund Performance Index: Constituent

CRISIL - AMFI Diversified Equity Fund Performance Index. Factsheet September 2015

CRISIL - AMFI Diversified Equity Fund Performance Index Factsheet September 2015 Table of Contents About the Index... 3 Features and Characteristics... 3 Methodology... 3 CRISIL - AMFI Diversified Equity

CRISIL - AMFI Diversified Equity Fund Performance Index Factsheet September 2015 Table of Contents About the Index... 3 Features and Characteristics... 3 Methodology... 3 CRISIL - AMFI Diversified Equity

Bajaj Allianz Group Term Life. Bajaj Allianz Group Term Life. Bajaj Allianz Life Insurance Co. Ltd. A Traditional Group Term Insurance Plan

Bajaj Allianz A Traditional Group Term Insurance Plan Bajaj Allianz Life Insurance Co. Ltd. Bajaj Allianz Giving your members and their families the heartening reassurance of your care. Giving your members

Bajaj Allianz A Traditional Group Term Insurance Plan Bajaj Allianz Life Insurance Co. Ltd. Bajaj Allianz Giving your members and their families the heartening reassurance of your care. Giving your members

Impact of Claim Settlement on Sales of Life Insurance policies A Case Study of LIC of India

International Letters of Social and Humanistic Sciences Vol. 23 (2014) pp 1-6 Online: 2014-03-02 (2014) SciPress Ltd., Switzerland doi:10.18052/www.scipress.com/ilshs.23.1 Impact of Claim Settlement on

International Letters of Social and Humanistic Sciences Vol. 23 (2014) pp 1-6 Online: 2014-03-02 (2014) SciPress Ltd., Switzerland doi:10.18052/www.scipress.com/ilshs.23.1 Impact of Claim Settlement on

Retirement Planning- Issues and Challenges in the Indian Context

IFIE /IOSCO Global Investor Education Conference, Washington DC Retirement Planning- Issues and Challenges in the Indian Context S. Raman Whole Time Member Securities and Exchange Board of India 22 May

IFIE /IOSCO Global Investor Education Conference, Washington DC Retirement Planning- Issues and Challenges in the Indian Context S. Raman Whole Time Member Securities and Exchange Board of India 22 May

Bajaj Allianz Life Insurance Co. Ltd. FY 2006-07. Bajaj Allianz Life Insurance Co. Ltd. <25 th June 2007>

Bajaj Allianz Life Insurance Co. Ltd. FY 2006-07 1 Index Private Life Insurance Market Key Highlights : FY 2006-2007 BALIC Growth in New Business Key Financial Highlights Growth in Assets NBAP FY 2006-07

Bajaj Allianz Life Insurance Co. Ltd. FY 2006-07 1 Index Private Life Insurance Market Key Highlights : FY 2006-2007 BALIC Growth in New Business Key Financial Highlights Growth in Assets NBAP FY 2006-07

SHRIRAM PENSION PLAN (UIN 128L022V01)

") SHRIRAM PENSION PLAN (UIN 128L022V01) Retirement need not necessarily mean a life full of compromises. With Shriram Pension Plan you continue to enjoy the lifestyle you are used to and lead a no compromise,

SHRIRAM PENSION PLAN (UIN 128L022V01) Retirement need not necessarily mean a life full of compromises. With Shriram Pension Plan you continue to enjoy the lifestyle you are used to and lead a no compromise,

Frequently Asked Questions on EPF.

Frequently Asked Questions on EPF. Q1.Who are required to be enrolled to PF? Any person employed directly or indirectly by the establishment, working in or in connection with the establishment, including

Frequently Asked Questions on EPF. Q1.Who are required to be enrolled to PF? Any person employed directly or indirectly by the establishment, working in or in connection with the establishment, including

Filing Assets and Liabilities is mandatory for every Public Servants

Filing Assets and Liabilities is mandatory for every Public Servants Section 44 of the Lokpal and Lokayuktas Act, 2013 mandates that every public servant (as defined in the Act, which includes Ministers,

Filing Assets and Liabilities is mandatory for every Public Servants Section 44 of the Lokpal and Lokayuktas Act, 2013 mandates that every public servant (as defined in the Act, which includes Ministers,

G R AT U I T Y GROUP PLAN A Unit Linked Group Gratuity Insurance Plan

G R AT U I T Y GROUP PLAN A Unit Linked Group Gratuity Insurance Plan KOTAK GRATUITY GROUP PLAN A Unit Linked Group Gratuity Insurance Plan "In this policy, the investment risk in investment portfolio

G R AT U I T Y GROUP PLAN A Unit Linked Group Gratuity Insurance Plan KOTAK GRATUITY GROUP PLAN A Unit Linked Group Gratuity Insurance Plan "In this policy, the investment risk in investment portfolio

Note: The paid up value would be payable only on due maturity of the policy.

Section II Question 6 The earning member of a family aged 35 years expects to earn till next 25 years. He expects an annual growth of 8% in his existing net income of Rs. 5 lakh p.a. If he considers an

Section II Question 6 The earning member of a family aged 35 years expects to earn till next 25 years. He expects an annual growth of 8% in his existing net income of Rs. 5 lakh p.a. If he considers an

Advance Diploma in Banking & Financial Planning IMS PROSCHOOL WWW.PROSCHOOLONLINE.COM

Advance Diploma in Banking & Financial Planning INDEX About Advance Diploma in Banking & Financial Planning Benefits of the Advance Diploma in Banking & Financial Planning Highlights and Curriculam IMS

Advance Diploma in Banking & Financial Planning INDEX About Advance Diploma in Banking & Financial Planning Benefits of the Advance Diploma in Banking & Financial Planning Highlights and Curriculam IMS

GROUP TERM LIFE PLUS

GROUP TERM LIFE PLUS About MetLife 143 years (Founded in 1868) experience serving over 90 million customers across the world MetLife holds leading market positions in the United States, Japan, Latin America,

GROUP TERM LIFE PLUS About MetLife 143 years (Founded in 1868) experience serving over 90 million customers across the world MetLife holds leading market positions in the United States, Japan, Latin America,

Max Life Guaranteed Lifetime Income Plan Pension (A Traditional Non Linked Non Participating Immediate Annuity Pension Plan) UIN: 104N076V01

UIN: 104N076V01") IN THIS POLICY, THE INVESTMENT RISK IN THE INVESTMENT PORTFOLIO IS BORNE BY THE POLICYHOLDER LIFE INSURANCE COVERAGE IS AVAILABLE IN THIS PRODUCT About Max Life Max Life Insurance, ne of the leading non-bank

IN THIS POLICY, THE INVESTMENT RISK IN THE INVESTMENT PORTFOLIO IS BORNE BY THE POLICYHOLDER LIFE INSURANCE COVERAGE IS AVAILABLE IN THIS PRODUCT About Max Life Max Life Insurance, ne of the leading non-bank

Income Tax 2013-14. Income Tax Slabs & Rates for Assessment Year 2014-15

Income Tax 2013-14 we have provided here a detailed guide for Income Tax 2013-14 Assessment Year 2014-15 applicable to Salaried Class Employees. Government has brought three important changes this year

Income Tax 2013-14 we have provided here a detailed guide for Income Tax 2013-14 Assessment Year 2014-15 applicable to Salaried Class Employees. Government has brought three important changes this year

Max Life Group Super Life Plus A Group Term Life Insurance Plan UIN: 104N073V01

LIFE INSURANCE COVERAGE IS AVAILABLE IN THIS PRODUCT About Max Life Max Life Insurance, one of the leading private life insurers, is a joint venture between Max India Ltd. and Mitsui Sumitomo Insurance

LIFE INSURANCE COVERAGE IS AVAILABLE IN THIS PRODUCT About Max Life Max Life Insurance, one of the leading private life insurers, is a joint venture between Max India Ltd. and Mitsui Sumitomo Insurance

Online Life Insurance Market in India 2015-2019

Brochure More information from http://www.researchandmarkets.com/reports/3196694/ Online Life Insurance Market in India 2015-2019 Description: Online life insurance products and services Life insurance

Brochure More information from http://www.researchandmarkets.com/reports/3196694/ Online Life Insurance Market in India 2015-2019 Description: Online life insurance products and services Life insurance

IND AS 19 Impacts and Examples

IND AS 19 Impacts and Examples Khushwant Pahwa, FIAI, FIA Founder and Consulting Actuary KPAC (Actuaries and Consultants) www.kpac.co.in +91-9910267727 [email protected] Agenda Modelling Gratuity Limit

IND AS 19 Impacts and Examples Khushwant Pahwa, FIAI, FIA Founder and Consulting Actuary KPAC (Actuaries and Consultants) www.kpac.co.in +91-9910267727 [email protected] Agenda Modelling Gratuity Limit

Reliance Traditional Group Superannuation Plan. A step towards creating value for your employees

Reliance Traditional Group Superannuation Plan A step towards creating value for your employees Reliance Traditional Group Superannuation Plan A non-linked non-par variable fund-based group insurance plan

Reliance Traditional Group Superannuation Plan A step towards creating value for your employees Reliance Traditional Group Superannuation Plan A non-linked non-par variable fund-based group insurance plan

What is ICICI Pru CashBak?

In your life, you always look forward to certain milestones. It may be the birth of a child in your family, the education of your children or purchasing a new home. These milestones have financial liabilities

In your life, you always look forward to certain milestones. It may be the birth of a child in your family, the education of your children or purchasing a new home. These milestones have financial liabilities

IOPS Member country or territory pension system profile: TRINIDAD AND TOBAGO. Update as of 15 February 2013

IOPS Member country or territory pension system profile: TRINIDAD AND TOBAGO Report 1 issued on September 2011, validated by the Central Bank of Trinidad and Tobago Update as of 15 February 2013 1 This

IOPS Member country or territory pension system profile: TRINIDAD AND TOBAGO Report 1 issued on September 2011, validated by the Central Bank of Trinidad and Tobago Update as of 15 February 2013 1 This

A STUDY ON PERFORMANCE OF UNIT-LINKED INSURANCE PLANS (ULIP) OFFERED BY INDIAN PRIVATE INSURANCE COMPANIES

OFFERED BY INDIAN PRIVATE INSURANCE COMPANIES") A STUDY ON PERFORMANCE OF UNIT-LINKED INSURANCE PLANS (ULIP) Dr. G Nagarajan * Mr. A. Asif Ali ** Mr. N. Sathyanarayana** OFFERED BY INDIAN PRIVATE INSURANCE COMPANIES Abstract: Indian Insurance Industry

A STUDY ON PERFORMANCE OF UNIT-LINKED INSURANCE PLANS (ULIP) Dr. G Nagarajan * Mr. A. Asif Ali ** Mr. N. Sathyanarayana** OFFERED BY INDIAN PRIVATE INSURANCE COMPANIES Abstract: Indian Insurance Industry

Worry-free retirement, fully paid

Birla Sun Life Insurance Immediate Annuity Plan Traditional, non-participating, single premium plan for regular income after retirement Worry-free retirement, fully paid Through your working years, you

Birla Sun Life Insurance Immediate Annuity Plan Traditional, non-participating, single premium plan for regular income after retirement Worry-free retirement, fully paid Through your working years, you

Pay only one premium. Get regular lifetime income post retirement.

IN THIS POLICY, THE INVESTMENT RISK IN THE INVESTMENT PORTFOLIO IS BORNE BY THE POLICY HOLDER Pay only one premium. Get regular lifetime income post retirement. IN THIS POLICY, THE INVESTMENT RISK IN INVESTMENT

IN THIS POLICY, THE INVESTMENT RISK IN THE INVESTMENT PORTFOLIO IS BORNE BY THE POLICY HOLDER Pay only one premium. Get regular lifetime income post retirement. IN THIS POLICY, THE INVESTMENT RISK IN INVESTMENT

Birla Sun Life Insurance Platinum Advantage Plan. Birla Sun Life Insurance Company Limited

Birla Sun Life Insurance Platinum Advantage Plan Investment risk in the investment portfolio is borne by the policyholder. The premiums paid in Unit Linked Insurance policies are subject to investment

Birla Sun Life Insurance Platinum Advantage Plan Investment risk in the investment portfolio is borne by the policyholder. The premiums paid in Unit Linked Insurance policies are subject to investment

Key Features of Budget 2015-2016 Employee specific. 2015 Copyright JB ARSEN

Key Features of Budget 2015-2016 Employee specific 2015 Copyright JB ARSEN 2015 Copyright JB ARSEN A. Rates of Income-tax Rates of Income-Tax Basic Rates The income tax rates remains unchanged for individuals.

Key Features of Budget 2015-2016 Employee specific 2015 Copyright JB ARSEN 2015 Copyright JB ARSEN A. Rates of Income-tax Rates of Income-Tax Basic Rates The income tax rates remains unchanged for individuals.

Worry-free retirement, fully paid

Birla Sun Life Insurance Immediate Annuity Plan Traditional, non-participating, single premium plan for regular income after retirement Worry-free retirement, fully paid Through your working years, you

Birla Sun Life Insurance Immediate Annuity Plan Traditional, non-participating, single premium plan for regular income after retirement Worry-free retirement, fully paid Through your working years, you

CRISIL - AMFI Short Term Debt Fund Performance Index. Factsheet March 2014

CRISIL - AMFI Short Term Debt Fund Performance Index Factsheet March 2014 Table of Contents About the Index... 3 Features and Characteristics... 3 Methodology... 3 CRISIL - AMFI Short Term Debt Fund Performance

CRISIL - AMFI Short Term Debt Fund Performance Index Factsheet March 2014 Table of Contents About the Index... 3 Features and Characteristics... 3 Methodology... 3 CRISIL - AMFI Short Term Debt Fund Performance

Employees Provident Fund and Miscellaneous Provisions Act

Employees Provident Fund and Miscellaneous Provisions Act Introduction The Supreme Court has stated in Andhra University v. R.P.F.C. 1985 (51) FLR 605 (SC) that in construing the provisions of the Employees

Employees Provident Fund and Miscellaneous Provisions Act Introduction The Supreme Court has stated in Andhra University v. R.P.F.C. 1985 (51) FLR 605 (SC) that in construing the provisions of the Employees

International Journal of Advance Research in Computer Science and Management Studies

Volume 2, Issue 11, November 2014 ISSN: 2321 7782 (Online) International Journal of Advance Research in Computer Science and Management Studies Research Article / Survey Paper / Case Study Available online

Volume 2, Issue 11, November 2014 ISSN: 2321 7782 (Online) International Journal of Advance Research in Computer Science and Management Studies Research Article / Survey Paper / Case Study Available online

PERFORMANCE EVALUATION OF SELECT EQUITY FUNDS IN INDIA

PERFORMANCE EVALUATION OF SELECT EQUITY FUNDS IN INDIA DR. KUBERUDU BURLAKANTI*; RAVI VARMA CHIRUVOORI** *PROFESSOR & HEAD - DEPARTMENT OF MANAGEMENT STUDIES ANDHRA UNIVERSITY CAMPUS, KAKINADA - 533005

PERFORMANCE EVALUATION OF SELECT EQUITY FUNDS IN INDIA DR. KUBERUDU BURLAKANTI*; RAVI VARMA CHIRUVOORI** *PROFESSOR & HEAD - DEPARTMENT OF MANAGEMENT STUDIES ANDHRA UNIVERSITY CAMPUS, KAKINADA - 533005

Frequently Asked Questions (FAQs): Provident Fund with RPFC

: Provident Fund with RPFC") Frequently Asked Questions (FAQs): Provident Fund with RPFC 1.1 What is Employees Provident Fund & Miscellaneous Provisions Act, 1952? It is social security legislation for the future benefit of employees

Frequently Asked Questions (FAQs): Provident Fund with RPFC 1.1 What is Employees Provident Fund & Miscellaneous Provisions Act, 1952? It is social security legislation for the future benefit of employees

Everyone wishes to see their child graduate. For the Child s Benefit. 14 Insurance Plans Compared BFSI

For the Child s Benefit 14 Plans Compared As a parent or guardian, it is but your instinct to want to secure your ward s future and financial planning is a critical part of it. You want to make sure that

For the Child s Benefit 14 Plans Compared As a parent or guardian, it is but your instinct to want to secure your ward s future and financial planning is a critical part of it. You want to make sure that

SECTION NATURE OF DEDUCTION REMARKS

The chart given below describes the deductions allowable under chapter VIA of the I.T. Act from the gross total income of the assessees having income from salaries. SECTION NATURE OF DEDUCTION REMARKS

The chart given below describes the deductions allowable under chapter VIA of the I.T. Act from the gross total income of the assessees having income from salaries. SECTION NATURE OF DEDUCTION REMARKS

Complete peace of mind with 4.6 times your Sum Assured guaranteed Lump sum on maturity after 25 years

Complete peace of mind with 4.6 times your Sum Assured guaranteed Lump sum on maturity after 25 years Birla Sun Life Insurance Income Assured Plan A traditional non-participating life insurance plan Flexibility

Complete peace of mind with 4.6 times your Sum Assured guaranteed Lump sum on maturity after 25 years Birla Sun Life Insurance Income Assured Plan A traditional non-participating life insurance plan Flexibility

PENSION FUND REGULATORY AND DEVELOPMENT AUTHORITY

PENSION FUND REGULATORY AND DEVELOPMENT AUTHORITY REQUEST FOR PROPOSAL FOR SELECTION OF PROJECT MANAGEMENT CONSULTANT FOR MONITORING CRA SYSTEM 2015 1 P a g e Glossary ASP CRA CRA FC DFS DoE GOI I PIN

PENSION FUND REGULATORY AND DEVELOPMENT AUTHORITY REQUEST FOR PROPOSAL FOR SELECTION OF PROJECT MANAGEMENT CONSULTANT FOR MONITORING CRA SYSTEM 2015 1 P a g e Glossary ASP CRA CRA FC DFS DoE GOI I PIN

Key benefits. How does the ICICI Pru Guaranteed Savings Insurance Plan work? Pay premiums for a limited period while enjoying a long term savings

Life has many important milestones: your house, your child s education and marriage, your retirement kitty. It would be your dream to achieve them all with certainty. However, this would need careful planning

Life has many important milestones: your house, your child s education and marriage, your retirement kitty. It would be your dream to achieve them all with certainty. However, this would need careful planning

Frequently Asked Questions

Frequently Asked Questions 1. What is tax planning? Tax planning is an essential part of financial planning. Tax planning is use to reduce tax liability by optimally using the provisions of tax exemptions

Frequently Asked Questions 1. What is tax planning? Tax planning is an essential part of financial planning. Tax planning is use to reduce tax liability by optimally using the provisions of tax exemptions

Commonly Asked Questions on BSE StAR MF

Say Goodbye to Mutuall Funds Applliicatiion Forms Commonly Asked Questions for Mutual Fund Distributors (MFDs) Commonly Asked Questions on BSE StAR MF 1. How is StAR MF different from the existing process

Say Goodbye to Mutuall Funds Applliicatiion Forms Commonly Asked Questions for Mutual Fund Distributors (MFDs) Commonly Asked Questions on BSE StAR MF 1. How is StAR MF different from the existing process

Life Insurance Industry An Overview

Life Insurance Industry An Overview Dr. Rajas Parchure Professor, National Insurance Academy & RBI Chair Professor, Gokhale Institute of Politics and Economics, Pune Historical Perspective Entry of Life

Life Insurance Industry An Overview Dr. Rajas Parchure Professor, National Insurance Academy & RBI Chair Professor, Gokhale Institute of Politics and Economics, Pune Historical Perspective Entry of Life

INVESTMENT PLAN DECLARATION

INVESTMENT PLAN DECLARATION Important Guidelines 1. Please note that investments/payments intended to be made during the Financial Year April 2016- March 2017 alone can be declared. 2. If your Investment

INVESTMENT PLAN DECLARATION Important Guidelines 1. Please note that investments/payments intended to be made during the Financial Year April 2016- March 2017 alone can be declared. 2. If your Investment

MAKE A ONE TIME INVESTMENT FOR A LIFETIME OF REGULAR INCOME.

MAKE A ONE TIME INVESTMENT FOR A LIFETIME OF REGULAR INCOME. 5 Smart Reasons to Buy: Guaranteed lifetime income Family gets the safety net in case of eventuality Single life & Joint life annuity options

MAKE A ONE TIME INVESTMENT FOR A LIFETIME OF REGULAR INCOME. 5 Smart Reasons to Buy: Guaranteed lifetime income Family gets the safety net in case of eventuality Single life & Joint life annuity options

Advance learning on Retirement Benefits (Theoretical)

") Advance learning on Retirement Benefits (Theoretical) Major retirement benefits An employee gets various retirement benefits, viz: Retirement benefits Leave encashment Gratuity Un-commuted pension Commuted

Advance learning on Retirement Benefits (Theoretical) Major retirement benefits An employee gets various retirement benefits, viz: Retirement benefits Leave encashment Gratuity Un-commuted pension Commuted

Analysis of Children Insurance Plans in the Present Context

IJMT, Volume 2 Number 1 January-June, 2012 pp. 39-45 Analysis of Children Insurance Plans in the Present Context G. BALACHANDAR 1, PANCHANATHAM 2 & K. SHEIK MYTHEEN 3 INTRODUCTION Life insurance in our

IJMT, Volume 2 Number 1 January-June, 2012 pp. 39-45 Analysis of Children Insurance Plans in the Present Context G. BALACHANDAR 1, PANCHANATHAM 2 & K. SHEIK MYTHEEN 3 INTRODUCTION Life insurance in our

Squeeze TAX to the MAX. by Subhash Lakhotia

FY 2014-15 Squeeze TAX to the MAX by Subhash Lakhotia 1 Quick guide to Save Tax for FY 2014-15 1 Section 80C investment limit increased to ` 1.5 Lakhs. Invest and save tax upto ` 46,350*. 2 Gifts received

FY 2014-15 Squeeze TAX to the MAX by Subhash Lakhotia 1 Quick guide to Save Tax for FY 2014-15 1 Section 80C investment limit increased to ` 1.5 Lakhs. Invest and save tax upto ` 46,350*. 2 Gifts received

Max Life Platinum Protect II Non Participating Regular Pay Term Insurance Plan (UIN: 104N060V02)

") LIFE INSURANCE COVERAGE IS AVAILABLE IN THIS PRODUCT. About Max Life Insurance Max Life Insurance, one of the leading life insurers, is a joint venture between Max India Ltd. and Mitsui Sumitomo Insurance

LIFE INSURANCE COVERAGE IS AVAILABLE IN THIS PRODUCT. About Max Life Insurance Max Life Insurance, one of the leading life insurers, is a joint venture between Max India Ltd. and Mitsui Sumitomo Insurance

MLC MasterKey Super & Pension Fundamentals MLC MasterKey Super & Pension How to Guide

MLC MasterKey Super & Pension Fundamentals MLC MasterKey Super & Pension How to Guide Preparation date 1 July 2015 Issued by The Trustee, MLC Nominees Pty Limited (MLC) ABN 93 002 814 959 AFSL 230702 The

MLC MasterKey Super & Pension Fundamentals MLC MasterKey Super & Pension How to Guide Preparation date 1 July 2015 Issued by The Trustee, MLC Nominees Pty Limited (MLC) ABN 93 002 814 959 AFSL 230702 The

THE INTERNATIONAL JOURNAL OF BUSINESS & MANAGEMENT

THE INTERNATIONAL JOURNAL OF BUSINESS & MANAGEMENT Performance of ULIP Schemes in Indian Insurance Market D. Jogish Professor & Head of the Department, Sai Vidya Institute of Technology, Bangalore, India

THE INTERNATIONAL JOURNAL OF BUSINESS & MANAGEMENT Performance of ULIP Schemes in Indian Insurance Market D. Jogish Professor & Head of the Department, Sai Vidya Institute of Technology, Bangalore, India

Government Amendments to the Finance Bill 2016. Clause 3

Government Amendments to the Finance Bill 2016 Clause 3 Clause (29A) of section 2 of the Income-tax Act defines "long-term capital asset" to mean a capital asset which is not a short-term capital asset.

Government Amendments to the Finance Bill 2016 Clause 3 Clause (29A) of section 2 of the Income-tax Act defines "long-term capital asset" to mean a capital asset which is not a short-term capital asset.

Gratuity - the loyalty reward. ICICI Prudential Group Gratuity Plan. Eligibility. What is the gratuity benefit payable? Bundled life cover

Gratuity - the loyalty reward Gratuity is a statutory benefit paid to the employees under the Payment of Gratuity Act, 1972 who have rendered continuous service for at least five years. The employee is

Gratuity - the loyalty reward Gratuity is a statutory benefit paid to the employees under the Payment of Gratuity Act, 1972 who have rendered continuous service for at least five years. The employee is