This chapter deals with the description of the sample of 1000 policyholders focused

|

|

|

- Jennifer York

- 8 years ago

- Views:

Transcription

1 CHAPTER -5 DATA ANALYSIS, INTERPRETATION AND FINDINGS This chapter deals with the description of the sample of 1000 policyholders focused on demographic factors (gender, age, religion, residence) data analysis and its interpretation. The chapter has been divided into three major sections. Section 5.1 deals with important descriptive statistics, demographic profile of the policyholders, and frequency distribution. The section 5.2 deals with designing of the constructs with respect to objective and hypotheses of the study, analyzing the validity of various constructs related to the study. The construct validity includes convergent, discriminant as well as face validity. After analyzing the constructs validity the structural model was tested and explained. Section 5.3 provides associations with the variables with respect to various demographic characteristics of the policyholders. In this section comparison of mean values, p-values, z-statistics and t-statistics is also provided for the purpose of testing various hypotheses. 5.1 DEMOGRAPHIC PROFILE OF THE POLICYHOLDERS The marketing concept was born out of the awareness that marketing starts with the determination of policyholder wants and ends with satisfaction of those wants. The entire business environment operates in a dynamic scenario where it is not easy to solve the puzzle of buyer decision making. Policyholders vary tremendously in terms of age, income and educational levels. Marketers also find it useful to distinguish different policyholder groups and segments and to develop product and services tailored to these needs. Thus presentation of sample profile would provide a clearer understanding of the marketing environment in which policyholders are placed. Policyholders purchase decisions are significantly influenced by their cultural, social and geographical factors that are uncontrollable by marketers. Therefore this section elaborates profile of the policyholders. 211

2 TABLE 5.1: Characteristics of the policyholders on the basis of location or residence (N=1000) Region Frequency Percent Rural % Urban % Total % As policyholder behaviour of Indian policyholder forms a part of this study, an attempt has been made to draw a broad sketch of rural and urban policyholders. As the country is vast geographically, market by great diversity in climate, religion, region, language, life style, educational level and economic status, Indian policyholder present a varied view. Hence the sample comprised of rural and urban areas, from different regions and religions. The total numbers of policyholders were 1000, where 500 policyholders were those from rural background and 500 policyholders were from urban areas as shown in table 5.1. The graphical representation is also provided herewith. TABLE 5.2: Characteristics of the policyholders on the basis of Gender (N=1000) Gender Frequency Percent Male % Female % Total % 212

3 The second important demographic variable was gender which is an important variable for marketers in more than one aspect. In this chapter it is proposed to discuss demographic and socio-economic profile of the policyholders. Demographic characteristics deal with vital statistics about the policyholder such as their age, sex, religion, location, marital status and education whereas socio-economic characteristics deal with financial position, occupation, income, wealth and other such attributes. The total number of policyholders was 1000 where 230 (23%) policyholders were females and 770 (77%) policyholders were males as shown in table 5.2. The graph also represents that there was a fair percentage of male policyholders. TABLE 5.3: Characteristics of the policyholders on the basis of Age groups (N=1000) Age Group Frequency Percent Below 25 years % years % years % years % years % 64 or Above % Total % 213

4 People buy goods and services during their life time. Segmenting the market by age provides useful insight into the potential size of markets. As shown in the table 5.3 the policyholders were grouped in six categories and 195 (19.5%) policyholders were below 25 years of age, 309 (30.9%) policyholders were years old, 192 policyholders (19.2%) were years old, 96 (9.6%) policyholders were years old, 176 (17.6%) policyholders were years old and only 32 (3.2%) policyholders were those above 64 years of age. The graph also indicates there was a fair representation of young policyholders who purchased life insurance. TABLE 5.4: Characteristics of the policyholders on the basis of Income groups (N=1000) Income Group (Annual) Frequency Percent Less than 1 Lakh % 1 to 1.5 Lakh % 1.5 to 2.5 Lakh % 2.5 to 5 Lakh % 5 to 10 Lakh % 10 Lakh and above % Total % 214

5 It is obvious that unless people have money or assurance of acquiring it, they cannot be regarded as potential policyholders. The amount of money they can spend will also affect the types of goods they are likely to buy. For this reason most of the analyst study income data. On the social scene the emergence of a large middleclass perhaps the most significant of all developments from the marketing point of view. The middle class in now emerging as the Consumption Community in the country are recognized as educated and rational policyholders. On the basis of income groups of the policyholders it was observed that 88 (8.8%) policyholders were those earning less than `1 lakh, 109 (10.9%) policyholders were those earning between ` lakh, 184 (18.4%) policyholders were those earning between ` lakh, 257 (27.5%) policyholders were those earning between ` lakh, 264 (26.4%) were those earning between 5-10 lakh and only 80 (8%) were earning `10 lakh and above as shown in the table 5.4. The graph also represents that there was a fair percentage of policyholders falls in the middle class income group of ` lakh followed by 5-10 lakh. TABLE 5.5: Characteristics of the policyholders on the basis of owner s wealth (N =1000) Owner s Wealth Frequency Percent Below 10 Lakh % Lakh % 50 Lakh-1 Crore % 1-5 Crore % 5-10 Crore % More Than 10 Crore % 215

6 Owner s Wealth Frequency Percent Below 10 Lakh % Lakh % 50 Lakh-1 Crore % 1-5 Crore % 5-10 Crore % More Than 10 Crore % Total % Consumption is also shaped by family wealth and expenditure pattern therefore it is important to consider owners wealth for analysis. As shown in the table above the policyholders grouped in six groups on the basis of owner s wealth. The table 5.5 shows that 283 (28.3%) policyholders had wealth below ` 10 lakh, 325 (32.5%) policyholders had wealth of ` lakh, 192 (19.2%) policyholders had wealth of ` 50 lakh-1 crore, 72 (7.2%) policyholders had wealth of ` 1-5 crore, 104 (10.4%) policyholders had wealth of ` 5-10 crore and only 24 (2.4%) policyholders had wealth of more than ` 10 crore. The graph also represents that there was a fair percentage of policyholders acquired wealth between ` lakh. 216

7 TABLE 5.6: Characteristics of the policyholders on the basis of family head (N =1000) Head of family Frequency Percent Grand Father % Father % Brother/Sister % Mother % You % Spouse % Total % As shown in the table 5.6 the policyholders showed mixed responses related to heads in their families, in 69 (6.9%) cases grandfather was head of the family, in 539 (53.9%) cases father was the head of the family, in 56 (5.6%) cases sibling (brother or sister) was heads of the family, in 40 (4%) cases mother was head of the family, in 200 (20%) cases policyholders themselves were head of their family and only in 96 (9.6%) cases spouse of the policyholder was head of the family. 217

8 Table 5.7: Characteristics of the policyholders on the basis of occupations of the policyholders (N =1000) Occupation Frequency Percent Agriculture % Self Employed-Shop % Self Employed-Other % Business Owner % Service Professionals Pvt % Govt. Employees % Dependent % Retired from Pvt. Job 8.8% Retired from Govt. Job % Total % The rapid social and economic development taking place in the country is more apparent in the economic activities of policyholder in insurance. With growth in urbanization large number of policyholders entering in the job market. As shown in the table 5.7 policyholders were surveyed from different occupational backgrounds. Seventy two (7.2%) policyholders were farmers, 109 (10.9%) policyholders were shop owners, 80 (8.0%) policyholders were self employed, 125 (12.5%) policyholders were business owner, 302 (30.2%) policyholders were serving private sector, 208 (20.8%) were government employees, 50 (5.6%) policyholders were dependent, 8 (0.8%) were retired from private jobs and 40 (4.0%) policyholders were retired from government jobs. The graph also represents that there was a fair percentage of service professionals followed by 218

9 government employees in the sample size. TABLE 5.8: Characteristics of the policyholders on the basis of educational qualifications of the policyholders (N =1000) Educational Qualifications Frequency Percent Below 10 th % 10th Pass % 12th Pass % Graduate % Diploma Holder % Post Graduate % Professional % Total % Education is a means to provide systematic instruction to make the policyholders intellectually superior and rational. Spread of education certainly leads to liberal attitude, information sharing, social and legal reforms and a desire to acquire high standard of living. Education therefore is determining a factor which is likely to bring about a change for the better in the society and to enhance the status of policyholder awareness. As shown in the table 5.8 policyholders were from different educational backgrounds. In the sample surveyed 64 (6.4%) policyholders were studied up to below tenth standard, 61 (6.1%) policyholders were studied up to tenth standard, 152 (15.2%) policyholders were studied up to twelfth standard. It was also observed that out of 1000 only 301 (30.1%) policyholders were graduates, 128 (12.8%) 219

10 policyholders were diploma holders, 230 (23%) policyholders were post graduates and 64 (6.4%) policyholders were professionally qualified. The graph also represents that there was a fair percentage of graduate policyholders. TABLE 5.9: Characteristics of the policyholders on the basis of Life cycle stage (N =1000) Personal Status (Life-cycle- stage) Frequency Percent Single(Unmarried) % Married, no child % Married, child/children below 5 years % Married, children 5-18 years % Married, Children in College % Married, living with working children % Separated, without children 8.8% Married, child/children separated % Separated, living with children 8.8% Widow/widower and Single % Remarried 8.8% Total % With the tremendous economic and social changes, transformation in attitude and beliefs, increased geographical mobility in search of income, wealth, occupation, increased standard of living the extended families will becoming less popular. Nuclear family has become the vogue of family life styles in India. In the present study a family which has two adults and one to three children is treated as small or nuclear 220

11 family. Big family or extended family is one which has more than two adults and more than three children. As shown in the table 5.9 in the sample surveyed 270 (27%) policyholders were unmarried, 96 (9.6%) policyholders were married and had no child, 112 (11.2%) policyholders were married and had child/children below 5 years of age, 266 (26.6%) policyholders were married and had child/children between 5-18 years of age, 72 (7.2%) policyholders were married and had college going child/children, 112 (11.2%) policyholders had working child/children, 8 (0.8%) policyholders were not living with their child/children, 24 (2.4%) policyholders were widow or widower and only 8 (0.8%) policyholders were remarried. The graph presented above also represents that there was a sound number of singles and married policyholders who had children between 5-18 years. TABLE 5.10: Number of children in the family of policyholder (N =1000) No of children Frequency Percent Nil % % % % 4 or more % Total % The family is defined as two or more persons related by blood, marriage or adoption who resides together. In a more dynamic sense individual who constitute a family might be described as members of the most basis social group who live together and interact to satisfy their personal and mutual needs. Family is a primary group 221

12 exercising considerable influence on policyholder behaviour. The table 5.10 shows that 381(38.1%) policyholders had no child, 219 (21.9%) policyholders had single child, 240 (24%) policyholders had two children, 128 (12.8%) policyholders had three children and only 32 (3.2%) policyholders had four or more children. The graph also represents that there was a fair percentage of policyholders who had no child in their family followed by number of policyholders who had two children in their family. TABLE 5.11: Earning members in family of policyholder (N =1000) Earning Members Frequency Percent % % % 4 or more % Total % Family may be extended, joint or nuclear. Policyholder behaviour researches have revealed that in every family there is role specialisation for example Karta in joint family decides the household products to be bought, in extended family the decider may be one of the grand parent and in nuclear it is the housewife who has a more decisive role to play. The table 5.11 shows that 269 (26.9%) policyholders had only one earning member in their family, 571 (57.1%) policyholders had two earning members in their family, 120 (12%) policyholders had three earning members in their 222

13 family and only 40 (4.0%) policyholders had four or more earning members in their family. The graph also represents that there was a fair percentage of policyholders who had 2 earning members in their family. TABLE 5.12: Religion of policyholders (N =1000) Religion Frequency Percent Hindu % Muslim % Sikh % Christian % Others % Total % The table 5.12 shows that the policyholders were surveyed from different religions, 896 (89.6%) policyholders were Hindus, 24 (2.4%) policyholders were Muslims, 48 (4.8%) policyholders were Sikhs, 16 (1.6%) were Christians and 16 (1.6%) were from other religions not listed in the questionnaire. The graph also represents that there was a fair percentage of Hindu policyholders followed by Sikhs and Muslims. 223

14 TABLE 5.13: Home ownership of policyholders (N =1000) Home ownership Frequency Percent Yes % No % Total % The table 5.13 shows that 771 (77.1%) policyholders had home ownership whereas 229 (22.9%) policyholders had no home ownership. The graph also represents that there was a fair percentage of home owners in the sample size. TABLE 5.14: Type of vehicle policyholders posses (N =1000) Type of Vehicle Frequency Percent Heavy Motor Vehicle % Light Motor Vehicle % Motor Cycle/Scooter geared % Scooter non-geared % None % Total % 224

15 The table 5.14 shows that in the sample surveyed 117 (11.7%) policyholders had heavy motor vehicle, 547 (54.7%) had light motor vehicle, 192 (19.2%) policyholders had geared motor cycle/scooter, 40 (4%) had non-geared scooter whereas only 104 (10.4%) policyholders had no vehicle. The graph also represents that there was a fair percentage of policyholders those who posses light motor vehicle. TABLE 5.15: Type of back accounts policyholders operates (N =1000) Type of Bank Account Frequency Percent Personal % Joint % Both % Total % The table 5.15 shows that 643 (64.3%) policyholders were operating personal bank account, 96 (9.6%) had joint account whereas 261 (26.1%) were operating both joint as well as personal accounts. The graph also represents that there was a fair percentage of policyholders who were operating personal account. 225

16 TABLE 5.16: Property of policyholders (N =1000) Own Property (Agriculture/ Commercial land) Frequency Percent Yes % No % Total % The table 5.16 shows that 640 (64%) policyholders were property owner (agriculture or commercial) whereas 360 (36%) policyholders were not owner of any kind of property. TABLE 5.17: Card policyholders operates (N =1000) Type of credit/debit card Frequency Percent Credit Card % Debit Card/ATM % Kisan Credit Card % Master/Visa card % Total % The table 5.17 shows that 189 (18.9%) policyholders were credit card holders, 739 (73.9%) were debit card holders, 24 (2.4%) were kisan credit card holders and only

17 (4.8%) were master/visa card holders. DEMOGRAPHIC PROFILE OF RURAL AND URBAN POLICYHOLDERS TABLE 5.18: Gender and Region (N =1000) Gender Gender Regionality Rural Urban Total Male Female Total The table 5.18 shows that the number of male policyholders was more in rural (407) as well as urban areas (363) as compare to female policyholders in rural (93) and urban areas (137). TABLE 5.19: Age Group and Region (N =1000) Age Group Age Group Regionality Rural Urban Total Below 25 years years years years years or Above Total

as well as in urban area (below 25 years was 49 and below 35 was 147), followed by the")

18 The table-5.19 shows that number of young policyholders was more in rural (below 25 years 146, below 35 years was 162) as well as in urban area (below 25 years was 49 and below 35 was 147), followed by the policyholders of 55 to 64 years of age (69 in rural and 107 in urban area)there was a fare participation of each age group in the sample. TABLE 5.20: Income Group and Region (N =1000) Income Group (Annual) Regionality Rural Urban Total Less than 1 Lakh to 1.5 Lakh to 2.5 Lakh to 5 Lakh to 10 Lakh Lakh and above Total Income group of an individual plays a vital role in buying insurance policy. The above table 5.20 provide the details about the income groups of the policyholders. In 228

19 the sample surveyed 59 rural and 29 urban policyholders were earning less than ` 1 lakh, 78 rural and 31 urban policyholders were earning between ` lakh, 91 rural and 93 urban policyholders were earning between ` 1.5 to 2.5 lakh, 176 rural and 99 urban policyholders were earning between ` 2.5 to 5 lakh, 74 rural and 190 urban policyholders were earning between ` 5 to 10 lakh and 22 rural and 58 urban policyholders were earning above ` 10 lakh per annum. TABLE 5.21: Owner s Wealth and Region (N =1000) Owner's Wealth in family Regionality Rural Urban Total Below 10 Lakh Lakh Lakh-1 Crore Crore Crore More Than 10 Crore Total It was observed on the basis of owners wealth of a household that in the sample surveyed owners of 194 rural and 89 urban policyholders had a wealth below 10 lakhs,191 rural and 31 urban policyholders had wealth between ` lakhs 229

20 followed by 58 rural policyholders and 134 urban policyholders had the wealth between ` 50 to 1 Crore as shown in table TABLE 5.22: Head of Family and Region (N =1000) Owner/head of your family Rural Regionality Urban Total Grand Father Father Brother/Sister Mother You Spouse Total The table 5.22 shows that in case of 57 rural and 12 urban policyholders head of the family was Grand Father where as in case of 255 rural policyholders and 284 urban policyholders father was the head of family. It was also observed in case of 114 rural and 86 urban policyholders were the head in their families. 230

21 TABLE 5.23: Occupation and Region (N =1000) Occupation Regionality Total Rural Urban Agriculture Self Employed-Shop Self Employed-Other Business Owner Service Professionals Pvt Govt. Employees Dependent Retired from Pvt. Job Retired from Govt. Job Total The table 5.23 shows that there were a fair percentage of service professionals (121 in rural and 181 urban areas), government employees (93 rural and 115 urban policyholders) followed by self-employed and farmers in the sample surveyed. 231

22 TABLE 5.24: Educational Qualifications and Region (N =1000) Educational Qualifications Regionality Total Rural Urban Below 10th th Pass th Pass Graduate Diploma Holder Post Graduate Professional Total The information in the table 5.24 reveals that 48 rural and 16 urban policyholders were not educated up to 10 th standard, 49 rural and 12 urban policyholders were studied up to 10 th standard, 114 rural and 38 urban policyholders were educated up to 12 th standard. It was also observed that 131 rural and 170 urban policyholders were graduates, 48 rural and 80 urban policyholders were diploma holders, 90 rural and 140 urban policyholders were post graduates whereas 20 rural and 44 urban policyholders were professionally qualified. 232

23 TABLE 5.25: Personal Status (Life-stage) and Region (N =1000) Personal Status of the policyholders Rural Regionality Urban Total Single (Unmarried) Married, no child Married, child/children below 5 years Married, children 5-18 years Married, Children in College Married, living with working children Separated, without children Married, child/children separated Separated, living with children Widow/widower and Single Remarried Total The table 5.25 make clear that there was 181 rural and 89 urban policyholders were unmarried, 33 rural and 63 policyholders were married without children, 68 rural and 44 urban policyholders were married and living with children. It was also observed that 1 rural and 7 urban policyholders were separated and have no issues, 11 rural and 233

24 13 urban policyholders were married and their children were not living with them, 8 rural policyholders were separated and living with their children, 18 rural and 6 urban policyholders were widow/widowers. There were a fair percentage of married policyholders in urban 147 and rural 119 areas that had children aged between 5-18 years of age. TABLE 5.26: Earning Members in Family and Region (N =1000) Earning Members in family Rural Regionality Urban Total or more Total The information in the table 5.26 reveals that 121 rural and 147 urban policyholders had only one earning member in their family, 323 rural and 248 urban policyholders had two earning members in their family, 29 rural and 91urban policyholders had 234

25 three earning members in their family followed by 26 rural and 14 urban policyholders had four or more earning members in their family. TABLE 5.27: Number of Children and Region (N =1000) Number of Children Regionality Total Rural Urban Nil or more Total The information in the table 5.27 reveals that 212 rural and 169 urban policyholders had no child, 122 rural and 97 urban policyholders had one child, 74 rural and 166 urban policyholders has two children, 68 rural and 60 urban policyholders had three children and 24 rural and 8 urban policyholders had four or more children in their family. 235

26 TABLE 5.28: Religion and Region (N =1000) Religion of the policyholders Regionality Total Rural Urban Hindu Muslim Sikh Christian Others Total The table 5.28 shows that there were 465 rural and 431 urban policyholders were Hindus, 9 rural and 15 urban policyholders were Muslims, 9 rural and 39 policyholders were Sikhs, 9 rural and 7 urban policyholders were Christians and 8 rural and 8 urban policyholders were from other religion. 236

27 TABLE 5.29: Home Ownership and Region (N =1000) Home Ownership Regionality Rural Urban Total Yes No Total The table 5.29 shows 372 rural and 399 urban policyholders had home ownership whereas 128 rural and 101 urban policyholders do not have their own homes. TABLE 5.30: Type of Vehicle and Region (N =1000) Type of Vehicle Rural Regionality Urban Total Heavy Motor Vehicle Light Motor Vehicle Motor Cycle/Scooter geared Scooter non-geared None Total

28 The information in the table 5.30 reveals that 48 rural and 69 urban policyholders were owner of heavy motor vehicle, 215 rural and 332 urban policyholders were owner of light motor vehicle, 141 rural and 51 urban policyholders had geared two wheeler, 24 rural and 16 urban policyholders had non-geared two wheeler and only 72 rural and 32 urban policyholders were not owner of any vehicle. TABLE 5.31: Type of Bank Account and Region (N =1000) Type of bank account Regionality Rural Urban Total Personal Joint Both Total

29 The information in the table 5.31 reveals that 48 rural and 69 urban policyholders were owner of heavy motor vehicle, 215 rural and 332 urban policyholders were owner of light motor vehicle, 141 rural and 51 urban policyholders had geared two wheeler, 24 rural and 16 urban policyholders had non-geared two wheeler and only 72 rural and 32 urban policyholders were not owner of any vehicle. TABLE 5.32: Property Ownership and Region (N =1000) Own property(agriculture/commercial/land) and Regionality Regionality Total Rural Urban Yes No Total The table 5.32 shows 316 rural and 324 urban policyholders were owner of property whereas 184 rural and 174 urban policyholders do not own property. 239

30 TABLE 5.33: Type of Card and Region (N =1000) Type of credit/debit Rural Regionality Urban Total Credit Card Debit Card/ATM Kisan Credit Card Master/Visa card Total The information in the table 5.33 reveals that 77 rural and 112 urban policyholders were owner of credit cards, 383 rural and 356 urban policyholders were owner of debit cards/atms, 16 rural and 8 urban policyholders were owner of kisan credit cards whereas 24 rural and 24 urban policyholders were owner of master visa cards. TABLE 5.34: Insured Amount and Region (N =1000) Approximate amount insured by the policyholders in life insurance policy/policies Rural Urban Frequency Percent Frequency Percent 1-3 Lakh Lakh More than 7Lakh Total

31 The information in the table 5.34 reveals that 83.2 percent rural and 72.6 percent urban policyholders insured approximately ` 1 to 3 laks of, 13 percent rural and 20 percent urban policyholders insured ` 4 to 7 laks and 3.8 rural and 8.4 percent urban policyholders insured more than ` 7 laks. PREFERENCES OF INSURANCE POLICIES AND REGION The information collected from the respondent revealed that policyholders posses more than one policy of same company of different companies. Therefore, the data related to types of insurance plan chosen by policy holders and detail of the insurer provided below: TABLE 5.35: Whole Life Scheme Whole Life Scheme Rural Urban Frequency Percent Frequency Percent Yes No Total The information in the table 5.35 reveals that only 14 percent rural and 16.4 percent urban policyholders had whole life insurance policy. The whole life policies were not popular among rural and urban policyholders. 241

32 TABLE 5.36: Endowment Scheme Endowment Scheme Rural Urban Frequency Percent Frequency Percent Yes No Total The information in the table 5.36 reveals that 67.8 percent rural and 53.8 percent urban policyholders had endowment life insurance scheme. Therefore it is stated that endowment schemes were quite popular among rural and urban policyholders. TABLE 5.37: Term Insurance Plan Term Insurance Plan Rural Urban Frequency Percent Frequency Percent Yes No Total

33 The information in the table 5.37 reveals that only 12 percent rural and 10.4 percent urban policyholders had Term insurance plans. Term insurance plans were not popular among rural and urban policyholders. TABLE 5.38: Periodic Money Back Plan Periodic Money Back Plan Rural Urban Frequency Percent Frequency Percent Yes No Total

34 The information in the table 5.38 reveals that only 6.8 percent rural and 2.8 percent urban policyholders had periodic money back plan. Periodic money bank plans were least preferred by the sample policyholders. TABLE 5.39: Medical Benefits Linked Insurance Medical Benefits Linked Insurance Rural Urban Frequency Percent Frequency Percent Yes No Total The information in the table 5.39 reveals that only 7.6 percent rural and 16.4 percent urban policyholders had medical benefit linked insurance. Medical benefit linked insurance plans were least preferred by the sample policyholders. 244

35 TABLE 5.40: Children Plan Children Plan Rural Urban Frequency Percent Frequency Percent Yes No Total The information in the table 5.40 reveals that only 21 percent rural and 16.8 percent urban policyholders had children plan. Children plan were opted by rural and urban policyholders but were not popular among sample policyholders. TABLE 5.41: Joint Life Plan Joint Life Plan Rural Urban Frequency Percent Frequency Percent Yes No Total

36 The information in the table 5.41 reveals that only 12.2 percent rural and 18.2 percent urban policyholders had whole life insurance policy. The joint life plan were least preferred by the sample policyholders. TABLE 5.42: Capital Market Limited Plan Capital Market Limited Plan Rural Urban Frequency Percent Frequency Percent Yes No Total

37 The information in the table 5.42 reveals that only 3.6 percent rural and 1.2 percent urban policyholders had capital market linked plan. Capital market linked plans were least preferred by the sample policyholders. TABLE 5.43: Group Schemes Group Schemes Rural Urban Frequency Percent Frequency Percent Yes No Total The information in the table 5.43 reveals that only 4.8 percent rural policyholders had group life insurance schemes. Group schemes were least preferred by the sample policyholders in rural as well as urban segment. TABLE 5.44: Social Security Social Security Rural Urban Frequency Percent Frequency Percent Yes No Total

38 The information in the table 5.44 reveals that only 3.2 percent rural policyholders had social security schemes. Social security plans were least preferred by the sample policyholders. TABLE 5.45: Education Plan Education Plan Rural Urban Frequency Percent Frequency Percent Yes No Total

39 The information in the table 5.45 reveals that only 3.6 percent rural and 1.2 percent urban policyholders had educational plan. Educational plans were least preferred by the sample policyholders. TABLE 5.46: Pension Plan Pension Plan Rural Urban Frequency Percent Frequency Percent Yes No Total The information in the table 5.46 reveals that only 5.2 percent rural and 7.6 percent urban policyholders had pension plan. Pension plans were least preferred by the sample policyholders in rural and urban segments. 249

40 TABLE 5.47: Growth Plan Growth Plan Rural Urban Frequency Percent Frequency Percent Yes No Total The information in the table 5.47 reveals that only 7.4 percent rural and 7 percent urban policyholders had capital market linked plan. Growth plans were least preferred by the sample policyholders. TABLE 5.48: Unit Linked Plan Unit Linked Plan Rural Urban Frequency Percent Frequency Percent Yes No Total

41 The information in the table 5.48 reveals that only 13.6 percent rural and 20 percent urban policyholders had unit linked plan. Unit linked plans were less poplar among the sample policyholders. TABLE 5.49: Systematic Investment Plan Systematic Investment Plan Rural Urban Frequency Percent Frequency Percent Yes No Total

42 The information in the table 5.49 reveals that only 4.8 percent rural and 1.6 percent urban policyholders had systematic investment plan. Systematic investment plans were least preferred by the sample policyholders. TABLE 5.50: Individual Plan Individual Plan Rural Urban Frequency Percent Frequency Percent Yes No Total The information in the table 5.50 reveals that only 61.2 percent rural and 28.4 percent urban policyholders had individual plan. Individual plans were quite popular among the rural policyholders. TABLE 5.51: Money Back Plan Money Back Plan Rural Urban Frequency Percent Frequency Percent Yes No Total

43 The information in the table 5.51 reveals that only 28.8 percent rural and 11.2 percent urban policyholders had capital money back plan. Money back plans were also less preferred by the sample policyholders in both the segments. TABLE 5.52: Special Plan Special Plan Rural Urban Frequency Percent Frequency Percent Yes No Total The information in the table 5.52 reveals that only 3.2 percent rural policyholders had special plan. Special plans were least preferred by the sample policyholders. 253

44 TABLE 5.53: Health Plan Health Plan Rural Urban Frequency Percent Frequency Percent Yes No Total The information in the table 5.53 reveals that only 5 percent rural and 4.6 percent urban policyholders had health plan. Health plans were least preferred by the sample policyholders in rural and urban segments. TABLE 5.54: Multiplier Plan Multiplier Plan Rural Urban Frequency Percent Frequency Percent Yes No Total

45 The information in the table 5.54 reveals that only 3.2 percent rural and 1.6 percent urban policyholders had Multiplier plan. Multiplier plans were least preferred by the sample policyholders. TABLE 5.55: Plan with Flexible Investment Option Plan with Flexible Investment Option Rural Urban Frequency Percent Frequency Percent Yes No Total

46 The information in the table 5.55 reveals that only 3.2 percent rural and 1.6 percent urban policyholders had plan with flexible investment option. Plans with flexible investment option were least preferred by the sample policyholders in both the segments. TABLE 5.56: Security Security Rural Urban Frequency Percent Frequency Percent Yes No Total The information in the table 5.56 reveals that only 76.8 percent rural and 60.8 percent urban policyholder s posses a policy with security. Social security is one of the criteria thee policyholders expect to be part of most of the policies. 256

47 TABLE 5.57: Security and Critical Pension Security and critical pension Rural Urban Frequency Percent Frequency Percent Yes No Total The information in the table 5.57 reveals that only 12 percent rural and 20 percent urban policyholders had a policy with security and critical pension plan features. TABLE 5.58: Systematic Investment Plan Systematic Investment Plan Rural Urban Frequency Percent Frequency Percent Yes No Total

48 The information in the table 5.58 reveals that only 3 percent rural and 13 percent urban policyholders opted for a policy with systematic investment plan. TABLE 5.59: Saving Plan Saving Plan Rural Urban Frequency Percent Frequency Percent Yes No Total The information in the table 5.59 reveals that only 73.2 percent rural and 48.4 percent urban policyholders preferred a policy offering saving plan. 258

49 TABLE 5.60: Risk Disability Risk Disability Rural Urban Frequency Percent Frequency Percent Yes No Total The information in the table 5.60 reveals that only 3.2 percent rural and 1.6 percent urban policyholders preferred a policy with risk disability plan. TABLE 5.61: Critical Plan Critical Pension Rural Urban Frequency Percent Frequency Percent Yes No Total

50 The information in the table 5.61 reveals that only 3 percent rural and 9.8 percent urban policyholders chosen life insurance with critical pension plan. TABLE 5.62: Security Illness Security Illness Rural Urban Frequency Percent Frequency Percent Yes No Total The information in the table 5.62 reveals that only 1.8 percent rural and 6.2 percent urban policyholders preferred a policy with security illness plan. TABLE 5.63: Annuity Insurance Annuity Insurance Rural Urban Frequency Percent Frequency Percent Yes No Total

51 The information in the table 5.63 reveals that only 1.6 percent rural and 1.6 percent urban policyholders chosen a policy with annuity schemes. TABLE 5.64: Flexibility Investment Portfolio Flexible Investment Portfolio Rural Urban Frequency Percent Frequency Percent Yes No Total

52 The information in the table 5.64 reveals that only 1.6 percent rural and 6.4 percent urban policyholders opted for life insurance with flexible investment portfolio plan. TABLE 5.65: Payer s Benefit Payer's Benefit Frequency Percent Frequency Percent Yes No Total The information in the table 5.65 reveals that only 1.6 percent rural and 1.6 percent urban policyholders opted for life insurance with payer s benefit plan. TABLE 5.66: Risk Coverage Risk Coverage Frequency Percent Frequency Percent Yes No Total

53 The information in the table 5.66 reveals that only 68.2 percent rural and 50.2 percent urban policyholders favored life insurance with maximum risk coverage plan. TABLE 5.67: Investment in Equity Funds Investment in equity funds Frequency Percent Frequency Percent Yes No Total The information in the table 5.67 reveals that only 1.6 percent rural and 8 percent urban buyer preferred a policy where investment in equity funds is offered to the policyholders. 263

54 TABLE 5.68: Investment in Growth Funds ` Frequency Percent Frequency Percent Yes No Total The information in the table 5.68 reveals that only 1.6 percent rural and 3.2 percent urban policyholders had preferred a policy with growth funds. TABLE 5.69: Investment in Debts Funds Investment in debts funds Frequency Percent Frequency Percent Yes No Total

55 The information in the table 5.69 reveals that only 2.6 percent rural and 5.4 percent urban policyholders opted for a policy with debt funds. TABLE 5.70: Investment in Liquid Funds Investment in liquid funds Frequency Percent Frequency Percent Yes No Total The information in the table 5.70 reveals that only 1.6 percent rural policyholders preferred policy where money is invested in liquid funds. 265

56 TABLE 5.71: Maturity Safety Switch Options Maturity Safety Switch Options Frequency Percent Frequency Percent Yes No Total The information in the table 5.71 reveals that only 43.6 percent rural and 24.6 percent urban policyholders opted for life insurance with maturity safety switch options. TABLE 5.72: Auto Fund Rebalancing Auto Fund Rebalancing Frequency Percent Frequency Percent Yes No Total

57 The information in the table 5.72 reveals that only 1.6 percent rural policyholders opted for a life insurance policy where the money is invested in auto fund rebalancing scheme. TABLE 5.73: Milestone Withdrawals Milestone Withdrawals Frequency Percent Frequency Percent Yes No Total The information in the table 5.73 reveals that only 1.6 percent rural policyholders 267

58 preferred a plan where milestone withdrawals are possible. TABLE 5.74: Partial Withdrawals Partial Withdrawals Frequency Percent Frequency Percent Yes No Total The information in the table 5.74 reveals that only 16.0 percent rural and 9.6 percent urban policyholders preferred a policy where partial withdrawals are possible. TABLE 5.75: Settlement Options Settlement Options Frequency Percent Yes No Total The information in the table 5.75 reveals that only 11.2 percent rural and 12.8 percent urban policyholders preferred a life insurance where settlement options is provided to them. 268

59 TABLE 5.76: Revival Policy Revival of Policy Frequency Percent Frequency Percent Yes No Total The information in the table 5.76 reveals that only 60.4 percent rural and 38.8 percent urban policyholders preferred a life insurance where revival of policy is easier. 269

60 TABLE 5.77: Policyholders of Different Life Insurance Companies Insurance Company No. of Policyholders Bajaj 189 HDFC 112 SBI Life 355 Aviva 16 Canara Bank HSBC 24 AMP Sanmar 0 ICICI 200 ING Vysya 24 Birla Sunlife 24 Sahara 16 Max New York 149 Shriram Life 8 LIC 920 Tata AIG 235 Reliance Life 32 Kotak Mahindra 40 Metlife India 0 Others 16 Total 2360 The table values indicated that the approached policyholders were holding different life insurance policies from different companies and there were many policyholders who had more than one policy from the same or different companies. The majority of policyholders bought LIC policy and they preferred to continue the association with the company. SBI life, Tata AIG and ICICI are also holding good position in the minds of policyholder. 270

61 The graph 5.77 indicates that there was a fair representation of LIC policyholders in the sample size (920) followed by SBI life insurance and TATAAIG. Therefore it is inferred that LIC is holding major market share in the insurance sector and winning policyholders faith. 271

62 CORRELATIONS ANALYSIS TABLE 5.78: Correlation between Region and Type of Insurance Policy Rationality Type of Insurance Policy Rural Urban Whole Life Scheme.451** Endowment Scheme.125**.118** Term Insurance Plan.492** Periodic Money Back Plan.673** -.122* Medical Benefits Linked Insurance.634** -.156* Children Plan.353** Joint Life Plan.488** Capital Market Limited Plan.041* Group Schemes.810**.00 Social Security 1.000** 1.000** Education Plan.969** Pension Plan.776**.445** Growth Plan.643** -.135* Unit Linked Plan.458** -.164* Systematic Investment Plan Individual Plan.145** Money Back Plan.286** -.145* Special Plan Health Plan.793** Multiplier Plan Plan with Flexible Investment Option.000* The above table reveals the information that Endowment Scheme, Periodic Money Back Plan, Medical Benefits Linked Insurance, ULIPS, Social Security, Pension Plan are closely linked with the urban region as there is a significant correlation between urban region and above plans. Therefore because of information search and awareness of urban respondents these plans were popular among urban policyholders. Periodic, Money Back Plan, Medical Benefits Linked Insurance, ULIPS and Growth Plan show 272

63 negative correlation with rural region due to poor awareness of rural policyholders. TABLE 5.79: Correlation between Gender and Type of Insurance Policy Gender Type of Insurance Policy Rural Urban Whole Life Scheme * Endowment Scheme ** Term Insurance Plan ** Periodic Money Back Plan.129**.104* Medical Benefits Linked Insurance * Children Plan.146**.084 Joint Life Plan.162** Capital Market Limited Plan.092*.068 Group Schemes.107* 0.00 Social Security Education Plan.090*.073 Pension Plan.112*.041 Growth Plan.135**.169** Unit Linked Plan.175**.049 Systematic Investment Plan.107*.078 Individual Plan.094* -.150** Money Back Plan.304** -.123** Special Plan Health Plan ** Multiplier Plan Plan with Flexible Investment Option The above table reveals the information that Periodic Money Back Plan, Children Plan, Joint Life Plan, Capital Market Limited Plan, Pension Plan, ULIPS, Systematic Investment Plan, Individual Plan, Money Back Plan are closely linked with the gender in urban region as there is a significant positive correlation. Whereas Endowment, 273

64 Term Insurance Plan, Individual, Money back plans shows negative correlation with gender in rural region. TABLE 5.80: Correlation between Occupation and Type of Insurance Plan Occupation Type of Insurance Policy Rural Urban Whole Life Scheme -.191** Endowment Scheme Term Insurance Plan ** Periodic Money Back Plan Medical Benefits Linked Insurance -.161** Children Plan -.243**.081 Joint Life Plan ** Capital Market Limited Plan -.214** -.295** Group Schemes -.168** 0.00 Social Security -.178** 0.00 Education Plan -.176** Pension Plan -.179** -.290** Growth Plan -.172**.056 Unit Linked Plan -.135**.171** Systematic Investment Plan -.202** Individual Plan.251**.222** Money Back Plan ** Special Plan -.178** 0.00 Health Plan -.227**.107* Multiplier Plan -.178** Plan with Flexible Investment Option -.178** The above table reveals that occupation has negative correlation with several plans rural and urban segments such as Capital market plan, Pension plan, ULIPs etc. 274

65 TABLE 5.81: Correlation between Age and Type of Insurance Plan Age Type of Insurance Policy Rural Urban Whole Life Scheme -.202** -.281** Endowment Scheme.214**.312** Term Insurance Plan -.375**.026 Periodic Money Back Plan -.366** -.162** Medical Benefits Linked Insurance -.204** -.109* Children Plan -.223** -.172** Joint Life Plan -.312**.262** Capital Market Limited Plan -.400** -.225** Group Schemes -.279** 0.00 Social Security -.370** 0.00 Education Plan -.370** Pension Plan -.244** Growth Plan -.168** Unit Linked Plan.367**.193** Systematic Investment Plan -.330** -.168** Individual Plan.331**.040 Money Back Plan -.286**.194** Special Plan -.370** 0.00 Health Plan -.270**.078 Multiplier Plan -.370**.109* Plan with Flexible Investment Option -.370**.017 The above table reveals that age is also associated with type of Insurance plans. Endowment schemes and ULIPs had a positive correlation with age whereas Whole life, Money back, Children and Capital market linked plans had negative correlation with age of the policyholders. 275

66 TABLE 5.82: Correlation between educational level and type of insurance Education Type of Insurance Policy Rural Urban Whole Life Scheme -.202** -.281** Endowment Scheme.214**.312** Term Insurance Plan -.375**.026 Periodic Money Back Plan -.366** -.162** Medical Benefits Linked Insurance -.204**.262** Children Plan -.223**.168** Joint Life Plan -.312**.262** Capital Market Limited Plan -.400** -.177** Group Schemes -.279**.085 Social Security -.370**.065 Education Plan -.370**.470** Pension Plan -.244**.114* Growth Plan.168**.145** Unit Linked Plan -.367**.193** Systematic Investment Plan -.330** -.168** Individual Plan.331**.613** Money Back Plan -.286**.194** Special Plan -.370**.008 Health Plan -.270**.078 Multiplier Plan -.370**.109* Plan with Flexible Investment Option -.370**.017 The above table reveals that education is also linked with type of insurance plan selected by the policyholders. Education level have negative correlation with different types of insurance plans such as Systematic investment plan, Capital market plan, Whole life and periodic money back plans in both the region. Education was positively correlated with Endowment and Growth plans in both the regions. 276

67 TABLE 5.83: Correlation between income group and type of insurance Income Type of Insurance Policy Rural Urban Whole Life Scheme.260**.208** Endowment Scheme.132**.275** Term Insurance Plan -.149** -.183** Periodic Money Back Plan.187**.174** Medical Benefits Linked Insurance.169**.253** Children Plan.252** -.161** Joint Life Plan.205**.356** Capital Market Limited Plan -.311** -.154** Group Schemes.268**.098 Social Security -.285**.078 Education Plan.298**.167** Pension Plan.166**.033 Growth Plan.264** Unit Linked Plan.184** Systematic Investment Plan.213** Individual Plan.249**.582** Money Back Plan Special Plan.285** Health Plan.281** 136** Multiplier Plan -.285**.203** Plan with Flexible Investment Option -.285** -.179** The above table reveals that income of respondents had positive correlation with type of Insurance plans. Whole Life Scheme, Endowment Scheme, Periodic Money Back Scheme, Medical Benefit Linked Scheme, Joint Life Plan, Individual Plan and Health Plan have positive correlation with income group whereas Capital Market Plan and Term Insurance had negative correlation with income group. 277

68 TABLE 5.84: Correlation between Personal status and type of insurance Personal Status Type of Insurance Policy Rural Urban Whole Life Scheme -.159** -.164** Endowment Scheme ** Term Insurance Plan -.186**.073 Periodic Money Back Plan -.252** -.285** Medical Benefits Linked Insurance -.201** Children Plan -.223** -.148** Joint Life Plan -.308**.118** Capital Market Limited Plan -.306** -.108* Group Schemes -.173**.073 Social Security -.296**.063 Education Plan -.292** Pension Plan -.192** -.111* Growth Plan Unit Linked Plan -.275**.229** Systematic Investment Plan -.269** -.125** Individual Plan.123**.544** Money Back Plan -.246**.237** Special Plan -.296**.023 Health Plan -.200**.018 Multiplier Plan -.296**.051 Plan with Flexible Investment Option -.296** The above table reveals that personal status of respondents also shown negative correlation with type of Insurance plans in rural and urban segment in case of Whole Life Scheme, Periodic Money Back Plan, Children Plan, Capital Market Linked Plan, Pension Plan and Systematic Plan. 278

69 TABLE 5.85: Correlation between amount insured and other variables Approximate amount insured by you in life insurance policy/policies Gender -.096* Age Group.302** Income Group (Annual).303** Owner's Wealth in family.461** Owner/head of your family.257** Your Occupation.358** Educational Qualifications Personal Status.366** Earning Members in family residing with you.152** Number of Children you have.237** Regionality.258* Religion.273** Home Ownership.184** Type of Which Vehicle you posses -.111* Type of bank account you have.458** Own property(agriculture/commercial/land) Type of credit/debit card used.191** The above table reveals that amount of life insurance is positively correlated with age, income, wealth, occupation, head in family, personal status of respondents, earning members in family, region, religion, home ownership, type of bank account etc. 279

70 5.2 CONFIRMATORY FACTOR ANALYSIS AND DESIGNING OF THE CONSTRUCTS Confirmatory factor analysis (CFA) is a statistical technique used to verify the factor structure of a set of observed variables. CFA allows the researcher to test the hypothesis that a relationship between observed variables and their underlying latent constructs exists. The researcher uses knowledge of the theory, empirical research, or both, postulates the relationship pattern a priori and then tests the hypothesis statistically CFA allows the researcher to test the hypothesis that a relationship underlying latent construct(s) exists. The researcher uses knowledge of the theory, empirical research, or both, postulates the relationship pattern a priori and then tests the hypothesis statistically. The use of CFA could be impacted by: The research hypothesis being testing The requirement of sufficient sample size (e.g., 5-20 cases per parameter estimate) Measurement instruments Multivariate normality Parameter identification Outliers Missing data Interpretation of model fit indices A suggested approach to CFA proceeds through the following process: Review the relevant theory and research literature to support model specification Specify a model (e.g., diagram, equations) Determine model identification (e.g., if unique values can be found for parameter estimation; the number of degrees of freedom, (df), for model testing is positive) collect data Conduct preliminary descriptive statistical analysis (e.g., scaling, missing data, 280

71 collinearity issues, outlier detection) estimate parameters in the model assess model fit present and interpret the results. Confirmatory factor analysis (CFA) provides enhanced control for assessing unidimensionality (i.e., the extent to which items on a factor measure one single construct) than exploratory factor analysis (EFA) and is more in line with the overall process of construct validation. In this study, confirmatory factor analysis model is run through AMOS software. Confirmatory Factor Analysis is a statistical technique used to verify the factor structure of a set of observed variables. Confirmatory Factor Analysis (CFA) allows the researcher to test the hypothesis that a relationship between observed variable and the underlying latent construct exists. The researcher uses the knowledge of the theory, empirical research or both, postulates the relationship patter a priori and than tests the hypothesis statistically. Confirmatory Factor Analysis could occur with the development of measurement instruments such as satisfaction scales, attitude or policyholder service questionnaires. In this research a blueprint is developed, questions written, appropriate scales were determined. The research instrument was used after conducting spade work and pilot survey, data collected and Confirmatory Factor Analysis completed. Confirmatory Factor Analysis allows the researcher to test the hypothesis that a relationship between the observed variables and their underlying latent construct (s) exists. Various dimensions of Confirmatory Factor Analysis are defined below: Validity Analysis The validity of scale may be defined as the extant to which differences in observed scale reflect true differences among objects on the characteristics being measured, rather than systematic or random errors. Some of the important validity tests generally considered includes content, construct, discriminant and criterion related validity. Content validity Content validity also called face validity which consists of a subjective but systematic evaluation of the repetitiveness of the contents of a scale. The content validity of a 281

72 construct can be defined as the degree to which the measure spans the domain of the constructs. For the present study, the content validity of the instrument was ensured as the service quality dimensions and items were identified from the literature and were thoroughly reviewed by professionals and academicians. Construct Validity Construct validity is a type of validity that addresses the construct or characteristic of the defined measuring scale. Construct validity require the a sound theory of the nature the construct being measured and how it is related to other construct. It involves the assessment of the degree to which an operationalization correctly measures its targeted variables. Establishing construct validity involves the empirical assessment of unidimensionality, reliability and validity (convergent and discriminant validity). In the present study, in order to check for unidimensionality, a measurement model was specified for each construct and CFA was run for all the constructs. Individual items in the model were examined to see how closely they represent the same construct. A comparative fit index (CFI) of 0.90 or above for the model implies that there is a strong evidence of unidimensionality. The CFI values obtained for all the six dimensions in the scale are equal to or above 0.90 as shown in the respective constructs. This indicates a strong evidence of unidimensionality for the scale. Once unidimensionality and reliability of a scale is established, it is further subjected to validation analysis. Convergent Validity It is a measure of construct validity that measures the extant to which the scale correlates positively with other measures of the same construct. It is the degree to which multiple methods of measuring a variable provide the same results. Convergent validity can be established using a coefficient called Bentler-Bonett coefficient. Scale with values of 0.90 or above shows strong evidence of convergent validity (Bentler and Bonett, 1980). The values for the Bentler- Bonett coefficient are summarized for all the six dimensions. All the dimensions have a value of more than 0.90, thereby demonstrating strong convergent validity. 282

73 Discriminant Validity Discrminant validity assesses the extant to which a measure does not correlate with other construct from which it is suppose to differ. It involves demonstrating a lack of correlation among differing a construct. It is the degree to which the measures of different latent variables are unique. Discriminant validity is ensured if a measure does not correlate very highly with other measures from which it is supposed to differ. For assessing discriminant validity, two chi-square comparison models were considered. The two comparison models are referred as Model 1 and Model 2. The comparison of chi-square statistic for Model 1 and Model 2 provides support for discriminant validity. Criterion-related Validity It is a type of validity that examines whether a scale performs as expected in to other variables selected as meaningful criteria.it is established when a criterion, external to the measurement instrument is correlated with the factor structure. In the present study, criterion validity is established by correlating the policyholder perceived service quality scale scores with overall service quality, which is considered to be the outcome construct. The correlations values also supports that all the dimensions have significant positive correlations with overall service quality. Thus, criterion related validity is established for all the dimensions. A construct can be defined as the latent variable which cannot or difficult to be measured directly from the policyholders. Hence a set of variables is to be included in the construct for its measurement. Before finalizing the set of variables in the construct the content validity is to be assured. The best practice to ensure the content validity is to show the set of possible variables in the construct to five academicians as well as five industry experts. After analyzing the advice received from these experts the constructs along with the set of variables is finalized. In this way the issue of content validity is resolved. After ascertaining the content validity the next issue was to analyze the validity of each individual construct. The construct validity consists of convergent validity, discriminant validity and face validity. The 283

74 convergent validity can be tested with help of factor loadings of each individual variable to the construct. The high Factor loadings indicate convergent validity and since high factor loadings indicate that the variable is highly explained by the construct, hence it will not be explained by any other construct which indicates the presence of discriminant validity. The description of various constructs, the set of variables in each construct and their factor loadings are shown as below:- Table 5.86: Possible Construct Name of Construct First Construct: Second Construct: Third Construct: Fourth Construct: Fifth Construct: Sixth Construct: Seventh Construct: Eight Construct: Ninth Construct: Parameter Selection Criteria (recommendation) Source of Information Purpose of Buying Feeling and Attitude Service Attributes Product Attributes Service Attributes Agents Attributes Other Attributes Structural Equation Modeling Traditional statistical methods normally utilize one statistical test to determine the significance of the analysis. However, Structural Equation Modeling (SEM), CFA specifically, relies on several statistical tests to determine the adequacy of model fit to the data. The chi-square test indicates the amount of difference between expected and observed covariance matrices. A chi-square value close to zero indicates little difference between the expected and observed covariance matrices. In addition, the probability level must be greater than 0.05 when chi-square is close to zero. The Comparative Fit Index (CFI) is equal to the discrepancy function adjusted for sample size. CFI ranges from 0 to 1 with a larger value indicating better model fit. Acceptable model fit is indicated by a CFI value of 0.90 or greater (Hu &Bentler, 1999). 284

75 Policyholder decision making process an analysis The policyholder decision to purchase or reject a product is the moment of final truth for the marketer. It signifies whether the marketing strategy has been wise, insightful and effective or whether it was poorly planned and missed the mark. Thus the marketers are particularly interested in policyholder decision making process. Therefore various aspects of decision making process were considered and constructs were designed accordingly. Root Mean Square Error of Approximation (RMSEA) is related to residual in the model. RMSEA values range from 0 to 1 with a smaller RMSEA value indicating better model fit. Acceptable model fit is indicated by an RMSEA value of 0.06 or less (Hu & Bentler, 1999). If model fit is acceptable, the parameter estimates are examined. The ratio of each parameter estimate to its standard error is distributed as a z statistic and is significant at the 0.05 level if its value exceeds 1.96 and at the 0.01 level it its value exceeds 2.56 (Hoyle, 1995). Unstandardized parameter estimates retain scaling information of variables and can only be interpreted with reference to the scales of the variables. Standardized parameter estimates are transformations of unstandardized estimates that remove scaling and can be used for informal comparisons of parameters throughout the model. Standardized estimates correspond to effect-size estimates. 285

76 Table 5.87: Construct Selection criteria on the basis of Recommendations (buying decision) Source of Information Purpose of buying Feelings and attitude Service attribute Product attributes Agents attributes Other factors My own decision. My employer s suggestion. Recommended by family member My Friend s suggestion Insurance agent s suggestion. My spouse s suggestion. Recommended during advertisement News paper /magazines Television Internet / s Agent Office/Workplace Circular/Notices Spouse/children Friends Insurance Experts/advisors Extra money at the time of my retirement. Extra money at the time of my retirement. Extra money in case of emergency (illness, accident). To avoid incurring unnecessary costs of insurance in future To maintain same life style over years Death protection for family members To provide financial support to spouse To save tax Premium amount gives me adequate coverage Feel secure after buying adequate insurance Insurance is better than investment in stock market Premium instalments are affordable for me I will receive guaranteed fund value Insurance policy will grant loan facility Flexible investment option plans are risky Reputation and loyalty Ambience and experience Comfort and promptness Quality of services offered Hassel free paper work and documentation Presentation, appearance and surroundings Clarity of contract and terms in document SMS/Reminders about premium payment Type of insurance plan Risk coverage Premium or cost of coverage Variety and associated range of products Tax benefits Payment option (mode of payment) Product flexibility (surrender, loan, revival) Maturity period and grace period Agent provides error free services Committed to fulfill promises timely Perform the service right in first instance Provides accuracy (such as payment record) Providing satisfactory services. Prompt, responsive and reliable. Cooperative and friendly. Known and trustworthy. The State financial policy and interest rates Novelty products on the insurance market. Details of insurance terms and conditions. Legal aspects of the policy I consider. 286

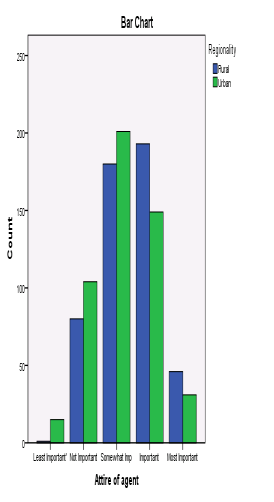

77 Selection criteria on the basis of Recommendations (buying decision) Source of Information Purpose of buying Feelings and attitude Service attribute Product attributes Agents attributes Other factors Word of mouth SMS/Reminder alerts about new products Growth and benefits Properly remind about the due premium. Bankers Information brochures, leaflets and letters Explain features, advantages and benefits of the policy Promotional telephone call/sms Application of latest technology in providing services Memorable advertisement Thoroughness of follow up on questions/ enquiries/ requests prior to purchase decision Attire of the agent is acceptable Attitude of agent towards policyholders is good Behaviour of agent is good with policyholders Agent have enough past experience in the field Attention focused on your priorities Awareness about terms and conditions of policy. 287

78 5.2.1 Analyzing the Construct Validity After ascertaining the content validity the next issue is to analyze the validity of each individual construct. The construct validity consists of convergent validity, discriminant validity and face validity. The convergent validity can be tested with help of factor loadings of each individual variable to the construct. The high Factor loadings indicate convergent validity and since high factor loadings indicate that the variable is highly explained by the construct, hence it will not be explained by any other construct which indicates the presence of discriminant validity. In describing a construct three types of variables were used in this structural modeling. Manifest variable (Observed behavior, usually dependent) Latent Variable (Unobserved behavior, explanatory) Residual Variable (Unobserved behavior, unexplained) The description of various constructs, the set of variables in each construct and their factor loadings are shown as below: Factors Influencing Policyholders in Selecting the Insurance Policy (Selection Criteria) The first construct defined as the factors influencing policyholders in selecting the insurance policy along with the set of variables are shown below in figure 5.1. The first construct consists of seven manifest, seven residual and one latent variable. The regression weights of each variable as result of the construct are shown in table As shown in the table all the regression weights are high and significant. Hence the construct validity is ensured and can be concluded that the construct significantly explains the variables. The standardized regression weights as well as the multiple squared correlations are shown in table The high value of the standardized weights indicates the higher influence of the construct to the variable. The squared multiple correlations indicate the percentage of variance of the measured variable that can be explained with the help of the variations in the construct. The results as shown in table 5.88 indicate that the agent of the insurance company is the most influencing 288

79 criteria for the policyholder of the insurance policy followed by the friends and family members. The agents being the most informed source has maximum influence on the policyholders as compared to other sources especially in rural segment. The advertisements of the insurance companies also influence the policyholders in deciding the insurance policy. The squared multiple correlation of insurance agent indicates that the 67 percent of the variance of the impact of insurance agent that can be explained with the help of the selection criteria. The fit of the model is shown in table The results indicate that the model is fit. TABLE 5.88: Regression Weights Selection Criteria Suggestion of Buying the Insurance Nobody influenced me, it was my own decision. My employer s suggestion. Recommended by family member My Friend s suggestion Insurance agent s suggestion. My spouse s suggestion. Recommended during advertisement Estimate Standardised Regression Weight Squared Multiple Correlation S.E. C.R. P *** *** *** *** *** *** TABLE 5.89: Model Fit Selection Criteria Model Fit Statistic Chi-square CFI.725 NFI.722 RFI.583 RMSEA.210 LO HI

for acceptable model. The model fit statistics from AMOS output is shown in the table 5.89.")

80 The Chi-square value is presented in the matrices. The RMSEA value indicates the amount of unexplained variance or residual is large than 0.06 or less critical. CFI and NFI value are not in complete agreement but are very close to the criteria (0.90 or larger) for acceptable model. The model fit statistics from AMOS output is shown in the table FIGURE: Sources of Information Influencing Policyholders in Selecting the Insurance Policy In order to increase the awareness about the importance of insurance policies among the investors, the insurance companies uses different sources to pass on the necessary 290

81 information to their prospective policyholders. The various source of information may be TV, newspapers, agents, phone calls, internet, s, mobile SMS, print media etc. The second construct represents the impact of various sources of information in influencing the policyholders in selecting the insurance policy along with the set of variables. The construct consists of eleven manifest, eleven residual and one latent variables are shown below in fig People have easy access to news papers and variety of other sources of communication due to which policyholders are exposed to new products, opinions and advertisements. In the present study the importance of various sources of communication was analysed. The regression weights of each variable as result of the construct are shown in table As shown in the table all the regression weights are high (more than 0.5) and significant. Hence the construct validity is ensured and can be concluded that the construct significantly explains the variables. The standardized regression weights as well as the multiple squared correlations are shown in table 5.90.The standardizes regression weights indicates comparative influence of the construct to its variables. The high value of the standardized weights indicates the higher influence of the construct to the variable. The squared multiple correlations indicate the percentage of variance of the measured variable that can be explained with the help of the construct. It is found from the results that the most influential source of information for policyholders was insurance agent and friends. This is due to the fact that still today the policyholders from the rural background do not have the enough awareness about the websites and internet. The insurance agents in most of the rural areas are actually the persons who commands good position in the society and can influence the policyholders in deciding and buying the insurance policies. The office workplace notifications/ circulars also influence the policyholders in selecting the insurance policy especially for the service class policyholders. The squared multiple correlations of insurance agent and friends indicate that the 81 percent of the variance of the impact of insurance agent and friends that can be explained with the help of the selection criteria. The fit of the model is shown in table The results indicate that the construct is fit. 291

82 TABLE 5.90: Regression Weights Sources of Information Sources of Information News paper /magazines Estimate Standardised Regression Weight Squared Multiple Correlation S.E. C.R. P Television *** Internet / s Agent *** Office/Workplace Circular/Notices *** Spouse/children *** Friends *** Insurance Experts/advisors *** Word of mouth *** Bankers Promotional telephone call/sms *** TABLE 5.91: Model Fit Sources of Information Model Fit Statistic Chi-square CFI.538 NFI.535 RFI.419 RMSEA.275 LO HI The Chi-square value is presented in the matrices. The RMSEA value indicates the amount of unexplained variance or residual is large than 0.06 or less critical. CFI and NFI value are not in complete agreement but are very close to the criteria (0.90 or larger) for acceptable model. The model fit statistics from AMOS output is shown in the table

83 FIGURE: Purpose of Buying the Insurance Policy The policyholder buy the product or a service in order to satisfy some need or wants. The insurance policy is a service which actually covers the risk of loss due to some unwanted happenings with the person insured. The insurance policies also help the persons in saving their income tax and provide them lump sum money at the time of maturity of the policy so that the long term liabilities can be fulfilled with that money. The third construct is defined as the purpose of buying the insurance policy consists of eight manifest, eight residual and one latent variable. The third construct represents the perception of the policyholders about the different purpose of buying the insurance policy. The construct along with the set of variables are shown below in fig The regression weights of each variable as result of the construct are shown in table As shown in the table all the regression weights are high and significant. Hence the construct validity is ensured and can be concluded that the construct significantly explains the variables. The standardized regression weights as well as the multiple squared correlations are shown in table 5.92.The standardizes regression weights indicates comparative influence of the construct to its variables. The high 293

84 value of the standardized weights indicates the higher influence of the construct to the variable. The squared multiple correlations indicate the percentage of variance of the measured variable that can be explained with the help of the construct. The results indicate that the most important purpose of buying insurance policy is to provide death protection for family members in case of any untoward incident as well as the saving of the income tax. The results also indicate that another important purpose of buying insurance to provided once self some extra money in case of emergency (illness, accident). It can be concluded from the results that the purpose to cover the risk of life and to save the family members from the financial loss due to unwanted events in the life is the main purpose to buy the insurance policies. For service class policyholders the saving of income tax is another main reason to buy the insurance policy. TABLE 5.92: Regression Weights Purpose of Buying Purpose of Buying Estimate Standardised Regression Weight Squared Multiple Correlation S.E. C.R. P To provide myself with some extra money at the time of my retirement. To provide my dear ones with some extra money at the time of my retirement. To provide myself with some extra money in case of emergency (illness, accident). To avoid incurring unnecessary costs of insurance in future To invest/save money to maintain same life style over years To provide death protection for family members in case of any untoward incident To provide financial support to spouse *** *** *** *** *** *** To save tax *** 294

85 TABLE 5.93: Model Fit Purpose of Buying Model Fit Statistic Chi-square CFI.602 NFI.600 RFI.439 RMSEA.281 LO HI The squared multiple correlation of death protection, indicates that the 78 percent of the variance of the impact of insurance agent and friends can be explained with the help of the selection criteria. The statistics for goodness of fit of the model is shown in table The results indicate that the model is fit. The Chi-square value is presented in the matrices. The RMSEA value indicates the amount of unexplained variance or residual is large than 0.06 or less critical. CFI and NFI value are not in complete agreement but are very close to the criteria (0.90 or larger) for acceptable model. The model fit statistics from AMOS output is shown in the table FIGURE:

86 5.2.5 Buying Experience of the Policyholders Every policyholder is having the experience (good or bad) with the product or a service after buying it. To analyse the buying experience of the policyholder after the purchase of product is one of the purpose of the companies. Hence in the study the policyholders were asked to provide their perceptions regarding various aspects of their experience related with the insurance policy after buying it. The fourth construct is defined as the buying experience consists of 15 variable; seven manifest, seven residual and one latent variable. The fourth construct represents the factors related with various aspects of the buying experience of policyholders consists of seven manifest, seven residual and one latent variable. The construct along with the set of variables are shown below in figure 5.4. The regression weights (unstandardised and standardized) of each variable as result of the construct are shown in table As shown in the table all the regression weights are high and significant. Hence the construct validity is ensured and can be concluded that the construct significantly explains the variables. The standardized regression weights as well as the multiple squared correlations are shown in table 5.94.The standardizes regression weights indicates comparative influence of the construct to its variables. The high value of the standardized weights indicates the higher influence of the construct to the variable. The squared multiple correlations indicate the percentage of variance of the measured variable that can be explained with the help of the construct. The results indicate that the policyholder found that insurance is better than investing in stock market and also consider flexible investment plans to be risky. The rural policyholders with most of the urban policyholders may be risk averse and avoids investments in stocks and instruments related to stocks. When they compare the insurance policies with these instruments, they found it safe and feel better with the insurance policies. It can be concluded that although most of the insurance policies are not the investment products (except the ULIP or stock market related policies) but the policyholders have a tendency to compare then with the other investment plans and found it safe to put their money in insurance policies and feel safe. The squared multiple correlation of insurance is better than investment in stock market and flexible investment plans indicates that the 61 percent of the variance can be explained with 296

87 the help of buying experience. The fit of the model is shown in table The results indicate that the model is fit. TABLE 5.94: Regression Weights Buying Experience Buying Experience Premium amount gives me adequate coverage I feel secure after buying adequate insurance Insurance is better than investment in stock market Premium installments affordable for me I will receive guaranteed fund value Insurance policy will grant loan facility Flexible investment option plans are risky Estimate Standardise d Regression Weight Squared Multiple Correlation S.E. C.R. P *** *** *** *** *** *** TABLE 5.95: Model Fit Buying Experience Model Fit Statistic Chi-square CFI.787 NFI.784 RFI.676 RMSEA.215 LO HI The Chi-square value is presented in the matrices. The RMSEA value indicates the amount of unexplained variance or residual is large than 0.06 or less critical. CFI and NFI value are not in complete agreement but are very close to the criteria (0.90 or larger) for acceptable model. The model fit statistics from AMOS output is shown in the table

88 FIGURE: Service Attributes Influencing Policyholders in Selecting the Insurance Policy The services associated with the products increases the perceptive quality in the mind of policyholders. Their buying behavior and level of satisfaction also depends with the various attributes of services rendered by the company, agents, regulatory bodies etc. The fifth construct named as the service attributes influencing policyholders in selecting the insurance policy along with the set of variables are shown below in figure 5.5. The regression weights of each variable as result of the construct are shown in table 5.96 The fifth construct represents the various aspects of the service attributes and consists of twelve manifest, twelve residual and one latent variable. As shown in the table all the regression weights are high and significant. Hence the construct validity is ensured and can be concluded that the construct significantly explains the variables. The standardized regression weights as well as the multiple 298