Lima One Capital Broker Program OnBoarding Presentation Welcome Package

|

|

|

- Shavonne Gordon

- 9 years ago

- Views:

Transcription

1 Lima One Capital Broker Program OnBoarding Presentation Welcome Package

2 Welcome Brokers 2 Thank you for taking the time to attend our Broker Onboarding Presentation Please type your first and last name and address in the chat box for attendance; you will be muted during this webinar For all questions or concerns please type into the chat box

3 Agenda 3 Background on Lima One Capital FixNFlip Loan Program Rental30 Loan Program Fix2Rent Loan Program Broker Submission Process

4 Benefits of Lima One Capital s Broker Program 4 HUD protection Streamlined and efficient process for brokers Open communication channels via the Operations Analyst assigned to your client Quick Closings

5 What We Offer 5 By partnering with Lima One Capital you re offering your clients: Fully capitalized funding source Competitive terms Excellent customer service

6 Three Lima One Capital Loan Programs 6

7 Program Highlights ` 7 FixNFlip Down Payment Features 10% - Domestic Borrowers 35% - Foreign Nationals Credit Score Minimum 630* Amortization Term Interest Only Balloon Note Prepayment Penalty No Seasoning Requirement for Assets, Properties, or Business Entities Minimum/Max Loan Amount Portfolio loans Closing Time Frame Appraisal Cost No No Minimum, No Maximum No Estimated 7-10 business days Estimated $375-$575/property

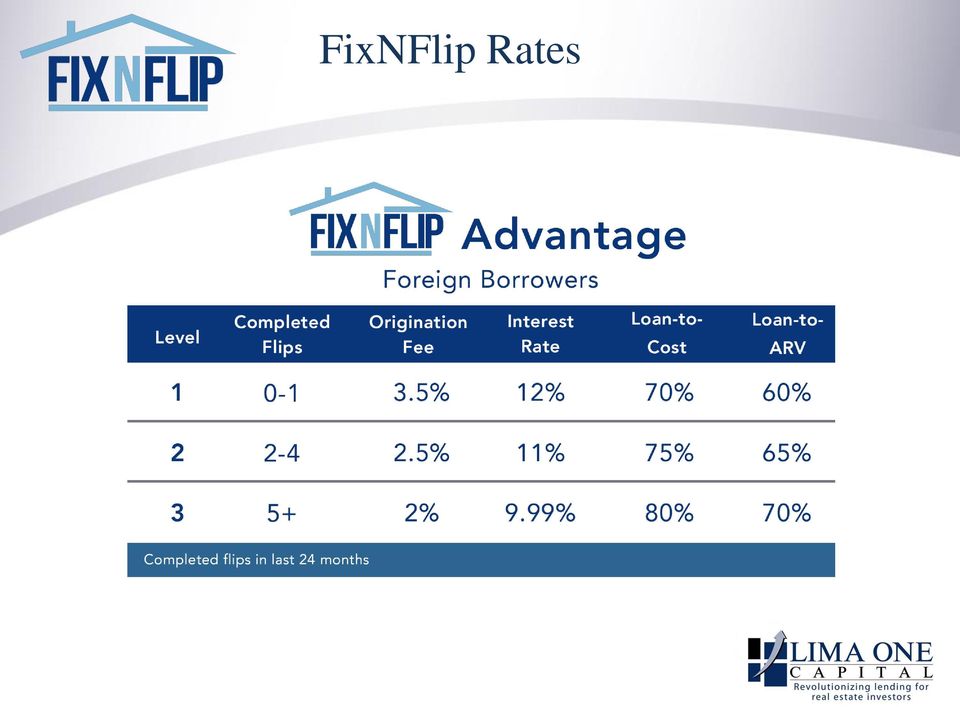

8 FixNFlip Rates 8

9 FixNFlip Rates 9

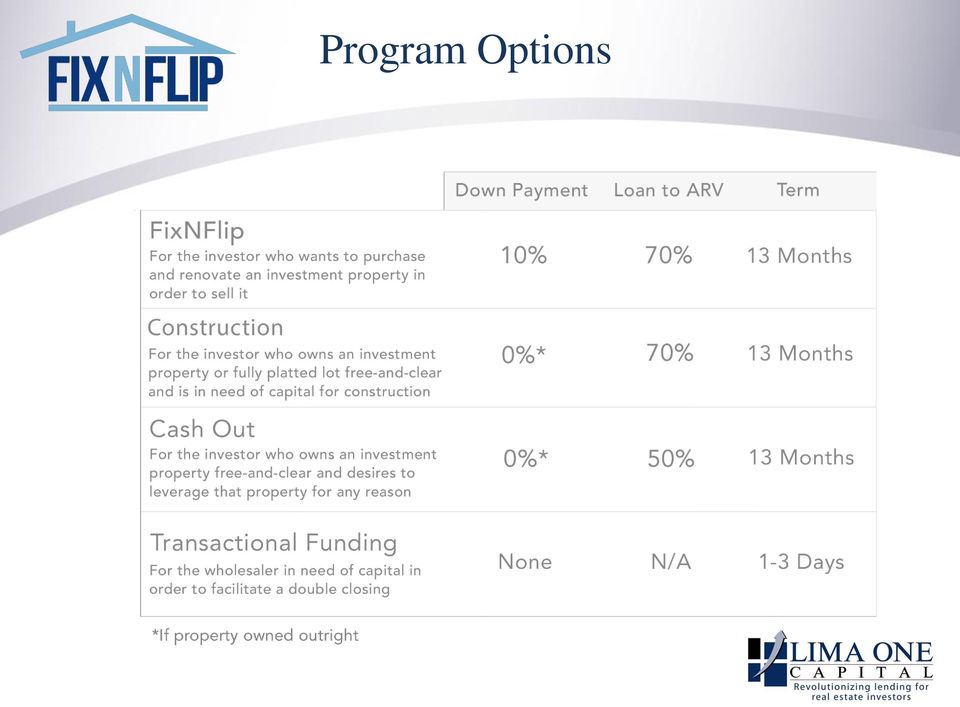

10 Program Options 10

11 Loan Requirements All loans must close in an entity (Limited Liability Company, S-corporation, Corporation, etc.) All borrowers in the entity have to sign a personal guarantee and must provide a copy of the ID as well as contact information. Recourse loan unless it is a foreign national.

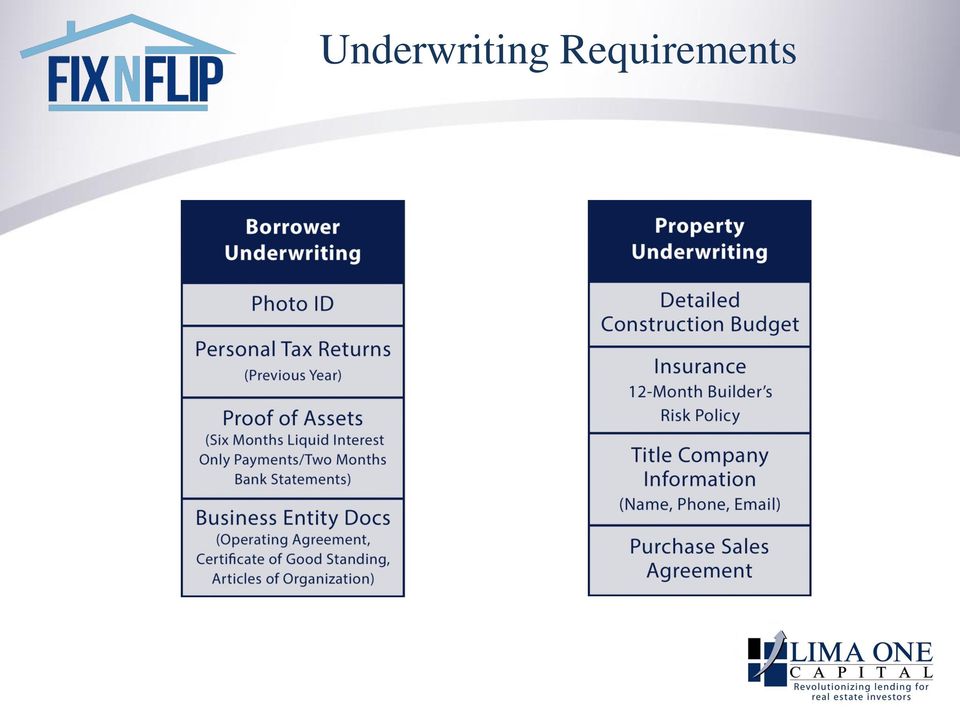

12 Underwriting Requirements 12

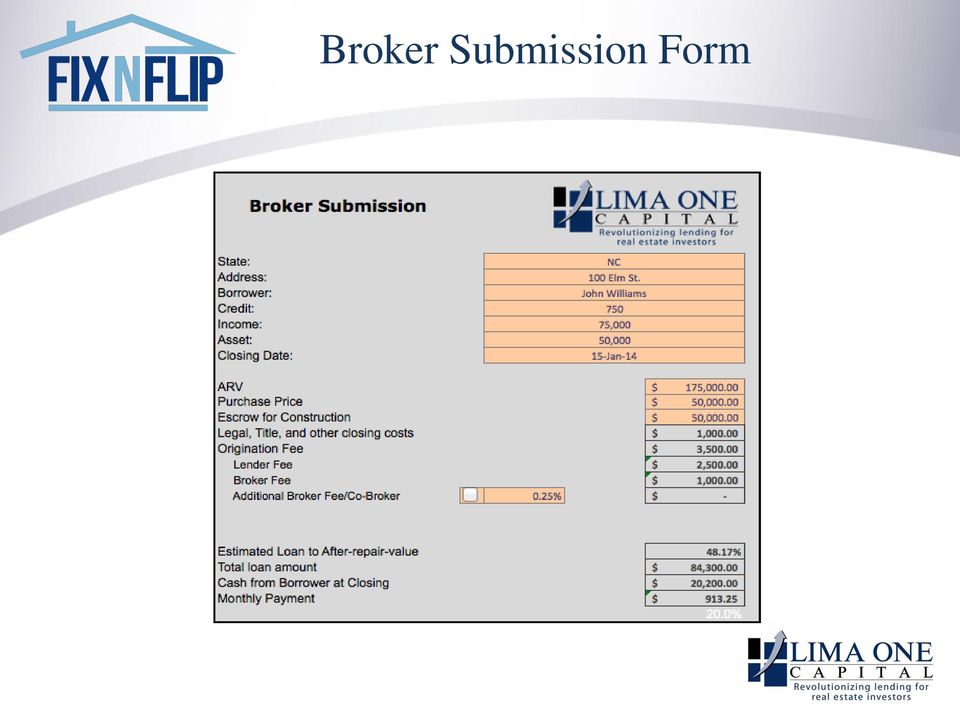

13 Broker Submission Form 13

14 Detailed Construction Budget 14 Include the Construction Budget in the submission .

15 Program Highlights 15 Rental30 Maximum LTV Features 75% - Domestic Borrowers 70%- Foreign Nationals Credit Score Minimum 630* Amortization Term Prepayment Penalty Seasoning Requirement for Assets and Properties Minimum/Max Loan Amount 30 year, fixed rate, fully amortized Yes Assets 2 month seasoning Properties 12 month seasoning $45,000 Minimum No Maximum Interest Rate 6.50%-8.85% Closing Time Frame Appraisal Cost Minimum Property Size 30 Business Days $450-$600/property 700 sq ft

16 Broker Points Unrestricted Broker points Broker fee is based off the Gross Total Loan Amount minus our Origination Fee All Broker points will be assessed in addition to Lima One Capital s 2% origination fee ($3,500 minimum)

17 Portfolio Loan Requirements 17 Each property included in the portfolio must appraise at a minimum of $45,000 All properties in the portfolio must be in the same state

18 Loan Requirements All loans must close in an entity (Limited Liability Company, S- corporation, Corporation, IRA, etc.) All loans must be personally guaranteed by each borrower unless the borrower is a Solo 401K or an Individual Retirement Account (IRA) IRA loans will receive an upward rate adjustment of 0.50%

IRA loans")

19 Property Seasoning Requirement 19 Refinance/Cash Out owned less than 12 months: Up to 75% LTV of the lesser of the purchase price or appraised value Will lend on the full appraised value if material changes to the property have been made in order to significantly increase the value

20 Eligible Property Types 1-4 Unit non-owner occupied (investment) properties Properties with 2 acres Fannie Mae Warrantable Condos

21 Secondary Financing Secondary financing is not permitted. This includes but is not limited to: Lines of credit Gift funds Loan from family/friend

22 Debt Service Coverage Ratio (DSCR) DSCR= Monthly Rental Income Monthly Payment/PITIA The Monthly Rental Income is the gross rental income realized from the property. The Monthly Payment (PITIA) includes principal (P), interest (I), taxes (T), insurance (I), and homeowner s association dues (A), as applicable. Minimum Qualifying DSCR is 1.3

23 Underwriting Requirements 23

24 Landlord Experience Properties Financed Requirements 1-2 No experience required year experience or licensed property manager years experience or licensed property manager 8+ Licensed property manager is required

25 Prepayment Penalty 5% stepping down 1% every year Applies only to the portion of any payment that exceeds 20% of the scheduled principal balance

26 Broker Submission Form `

27 Estimate of Cost

28 Program Highlights 28 Perfect loan for your borrowers who want to rehab a property to add to their portfolio Borrower receives 0.50% discount on the Rental30 origination fee Borrower will be underwritten in both FixNFlip and Rental30

29 Lima One Capital s Submission Process

30 Step One: Broker Submits Deal Send your Broker Submission Form to with the subject line as follows: For example: Rental30 White, Betty FixNFlip Martin, Steve (123 Main St) Fix2Rent Williams, Robin (456 Court Lane) All required cells must be filled out correctly and in full. You will receive a response within 24 business hours.

31 Step Two: Submit Borrower and Property Underwriting Documents If the submission is approved: In one label with the loan program and the client s name, submit all the required documents that were requested. Have your borrower apply online with your unique application link (to be provided). Generally a same-day response.

32 Step Three: Underwriting begins Your file will be assigned to an Operations Analyst who will underwrite your client The Operations Analyst will work the file all the way to closing All additional documentation needed for your clients file should be directed to assigned Operations Analyst

33 Step Four: Closing We require an approved HUD, title commitment, broker invoice and broker wiring instructions 48 hours prior to closing Broker fee will be disbursed by the closing agent at time of funding

34 Submission Tips 34 Send each Broker Submission in a separate Processors need to state the Broker s name they are submitting on behalf of for each deal Send documents in individual attachments We cannot accept documents sent through DropBox Do not have your client apply until after the deal submission has been approved and you have sent over all the requested documents

35 Questions? Questions or comments? Phone: (864) We look forward to working with you!

Achieving your goals through Financing. Cooperative Financing Models that may work for you

Achieving your goals through Financing Cooperative Financing Models that may work for you Overview Cooperative Financing Overview of the environment Interest Rates Why now is the best time to borrow Reasons

Achieving your goals through Financing Cooperative Financing Models that may work for you Overview Cooperative Financing Overview of the environment Interest Rates Why now is the best time to borrow Reasons

GETTING STARTED WITH Southern Home Loans A Division of Goldwater Bank NMLS# 452955

2016 GETTING STARTED WITH Southern Home Loans A Division of Goldwater Bank NMLS# 452955 YOUR PLAY-BY-PLAY GUIDE TO RESPONSIBLE NON-PRIME LENDING Highlights No Seasoning on Foreclosure, BK or Short Sale

2016 GETTING STARTED WITH Southern Home Loans A Division of Goldwater Bank NMLS# 452955 YOUR PLAY-BY-PLAY GUIDE TO RESPONSIBLE NON-PRIME LENDING Highlights No Seasoning on Foreclosure, BK or Short Sale

ditech BUSINESS LENDING FREDDIE MAC ELIGIBLE ARM PRODUCT CORRESPONDENT ONLY

1. PRODUCT DESCRIPTION Conventional Conforming five year/one year adjustable rate mortgage Servicing retained 30-year term Fully amortizing Non-convertible ARM Plan ID 2725 Manufactured homes not eligible

1. PRODUCT DESCRIPTION Conventional Conforming five year/one year adjustable rate mortgage Servicing retained 30-year term Fully amortizing Non-convertible ARM Plan ID 2725 Manufactured homes not eligible

Sierra Lending Group LLC Document Check List

Sierra Lending Group LLC Document Check List The following documents will be needed for full credit approval: Application 1. Fully completed and signed initial 1003. Please make sure to provide all assets

Sierra Lending Group LLC Document Check List The following documents will be needed for full credit approval: Application 1. Fully completed and signed initial 1003. Please make sure to provide all assets

Achieving your goals through Financing. Cooperative Financing Models that may work for you

Achieving your goals through Financing Cooperative Financing Models that may work for you Overview Cooperative Financing Mortgage programs for Cooperatives Overview of current rate environment Reasons

Achieving your goals through Financing Cooperative Financing Models that may work for you Overview Cooperative Financing Mortgage programs for Cooperatives Overview of current rate environment Reasons

FHA Office of Single Family Housing. Training: Origination Through Post-Closing/ Endorsement

Training: Origination Through Post-Closing/ Endorsement 1 Module 8A Programs and Products: Refinance Single Family Housing Policy Handbook 4000.1 Title II Insured Housing Program Forward Mortgages Origination

Training: Origination Through Post-Closing/ Endorsement 1 Module 8A Programs and Products: Refinance Single Family Housing Policy Handbook 4000.1 Title II Insured Housing Program Forward Mortgages Origination

Conventional Jumbo seven year/one year adjustable rate mortgage 30 year term Fully amortizing

1. PRODUCT DESCRIPTION Conventional Jumbo fixed rate mortgage 15 and 30 year terms Fully amortizing Conventional Jumbo five year/one year adjustable rate mortgage 30 year term Fully amortizing Conventional

1. PRODUCT DESCRIPTION Conventional Jumbo fixed rate mortgage 15 and 30 year terms Fully amortizing Conventional Jumbo five year/one year adjustable rate mortgage 30 year term Fully amortizing Conventional

Non-Recourse Financing for a Self-Directed IRA Investment

Non-Recourse Financing for a Self-Directed IRA Investment Transaction Summary Date: September 2012 Property Description: 12,720 SF retail building built in 2001 in good condition. The property is 100%

Non-Recourse Financing for a Self-Directed IRA Investment Transaction Summary Date: September 2012 Property Description: 12,720 SF retail building built in 2001 in good condition. The property is 100%

Dr. Debra Sherrill Central Piedmont Community College

Dr. Debra Sherrill Central Piedmont Community College 1 2 Describe the benefits and pitfalls of renting versus owning a home. List the steps required to obtain a mortgage loan. Identify mortgage options

Dr. Debra Sherrill Central Piedmont Community College 1 2 Describe the benefits and pitfalls of renting versus owning a home. List the steps required to obtain a mortgage loan. Identify mortgage options

Conventional DU Refi Plus

Endeavor America Loan Services Conventional DU Refi Plus Guidelines Conventional Guidelines... 3 Matrix... 3 Overview... 3 Program Expiration... 3 Loan Purpose... 4 Maximum LTV, CLTV, and HCLTV Ratios

Endeavor America Loan Services Conventional DU Refi Plus Guidelines Conventional Guidelines... 3 Matrix... 3 Overview... 3 Program Expiration... 3 Loan Purpose... 4 Maximum LTV, CLTV, and HCLTV Ratios

Mortgage Assistance Program Down Payment Assistance

Mortgage Assistance Program Down Payment Assistance DISCLOSURE NOTICE - APPLICATION PROCESS You are applying for financial assistance to purchase a home through the City of Livermore Mortgage Assistance

Mortgage Assistance Program Down Payment Assistance DISCLOSURE NOTICE - APPLICATION PROCESS You are applying for financial assistance to purchase a home through the City of Livermore Mortgage Assistance

HARP DU REFI PLUS Training

HARP DU REFI PLUS Training Offered by FIRST MORTGAGE CORPORATION JUNE 14, 2013 Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie Mac. This

HARP DU REFI PLUS Training Offered by FIRST MORTGAGE CORPORATION JUNE 14, 2013 Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie Mac. This

FREQUENTLY ASKED QUESTIONS Updated April 3, 2009

FREQUENTLY ASKED QUESTIONS Updated April 3, 2009 Making Home Affordable: How Genworth Mortgage Insurance Supports the Home Affordable Refinance Program Created to support a recovery in the housing market,

FREQUENTLY ASKED QUESTIONS Updated April 3, 2009 Making Home Affordable: How Genworth Mortgage Insurance Supports the Home Affordable Refinance Program Created to support a recovery in the housing market,

Housing Trust Silicon Valley ( HTSV ) Mortgage Assistance Program (MAP)

Mortgage Assistance Program (MAP)") Housing Trust Silicon Valley ( HTSV ) Mortgage Assistance Program (MAP) Program Description: Housing Trust Silicon Valley s Mortgage Assistance Program (MAP) is an amortizing second loan that is now available

Housing Trust Silicon Valley ( HTSV ) Mortgage Assistance Program (MAP) Program Description: Housing Trust Silicon Valley s Mortgage Assistance Program (MAP) is an amortizing second loan that is now available

ditech BUSINESS LENDING FREDDIE MAC ELIGIBLE FIXED RATE TEXAS HOME EQUITY PRODUCT

1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage Servicing retained 10 to 30 years in 5 year increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans are permitted Qualified

1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage Servicing retained 10 to 30 years in 5 year increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans are permitted Qualified

What s s New With FHA?

What s s New With FHA? Presented By: Bill Ladewig 866.204.9733 http://www.mortgage- FHA Calculator Calculates everything needed to quote or qualify FHA loans Click to Open: http://www.themtgmentor.com/fha_mortgage_calculator.html

What s s New With FHA? Presented By: Bill Ladewig 866.204.9733 http://www.mortgage- FHA Calculator Calculates everything needed to quote or qualify FHA loans Click to Open: http://www.themtgmentor.com/fha_mortgage_calculator.html

GMAC BANK JUMBO FIXED RATE PRODUCT

GMAC BANK PRODUCT 1. PRODUCT DESCRIPTION Conventional Jumbo Fixed Rate 10 to 30 years in five-year increments Fully amortizing 2. PRODUCT CODES 002 15 Yr Jumbo Fixed 004 30 Yr Jumbo Fixed 3. INDEX N/A

GMAC BANK PRODUCT 1. PRODUCT DESCRIPTION Conventional Jumbo Fixed Rate 10 to 30 years in five-year increments Fully amortizing 2. PRODUCT CODES 002 15 Yr Jumbo Fixed 004 30 Yr Jumbo Fixed 3. INDEX N/A

Get Your Multifamily Deal Done With FHA

January 7, 2009 Get Your Multifamily Deal Done With FHA Arbor Commercial Mortgage, LLC Overview In 2008, the housing finance system came to a near standstill as creditors began losing confidence in the

January 7, 2009 Get Your Multifamily Deal Done With FHA Arbor Commercial Mortgage, LLC Overview In 2008, the housing finance system came to a near standstill as creditors began losing confidence in the

FHA MIP TRAINING (Mortgage Insurance Premium)

") FHA MIP TRAINING (Mortgage Insurance Premium) Offered by FIRST MORTGAGE CORPORATION APRIL 10, 2013 Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark

FHA MIP TRAINING (Mortgage Insurance Premium) Offered by FIRST MORTGAGE CORPORATION APRIL 10, 2013 Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark

FHA Streamline Refinance Guidelines

The following guidelines apply to all DIRECTORS MORTGAGE s FHA Streamline Refinance loan program. All loans must adhere to the criteria of these guidelines or the individual loan programs. While DIRECTORS

The following guidelines apply to all DIRECTORS MORTGAGE s FHA Streamline Refinance loan program. All loans must adhere to the criteria of these guidelines or the individual loan programs. While DIRECTORS

FHA STREAMLINE REFINANCE PRODUCT PROFILE

Terms 30 Year Terms 15 Year Terms Maximum LTV/CLTV LTV/CLTV Score LTV/CLTV Score Non-Credit Qualifying N/A N/A Credit Qualifying 97.75% 97.75% Applies to Case Numbers assigned on or after January 26, 2015

Terms 30 Year Terms 15 Year Terms Maximum LTV/CLTV LTV/CLTV Score LTV/CLTV Score Non-Credit Qualifying N/A N/A Credit Qualifying 97.75% 97.75% Applies to Case Numbers assigned on or after January 26, 2015

Assumable mortgage: A mortgage that can be transferred from a seller to a buyer. The buyer then takes over payment of an existing loan.

MORTGAGE GLOSSARY Adjustable Rate Mortgage (ARM): A mortgage loan with payments usually lower than a fixed rate initially, but is subject to changes in interest rates. There are a variety of ARMs that

MORTGAGE GLOSSARY Adjustable Rate Mortgage (ARM): A mortgage loan with payments usually lower than a fixed rate initially, but is subject to changes in interest rates. There are a variety of ARMs that

Section 2.08 - Jumbo Solution Second Mortgage

- In This Product Description This product description contains the following topics: Overview... 2 Related Bulletins... 3 Loan Terms... 4 Assumptions... 4 Eligible First and Second Mortgage Products...

- In This Product Description This product description contains the following topics: Overview... 2 Related Bulletins... 3 Loan Terms... 4 Assumptions... 4 Eligible First and Second Mortgage Products...

First Time Home Buyer Glossary

First Time Home Buyer Glossary For first time home buyers, knowing and understanding the following terms are very important when purchasing your first home. By understanding these terms, you will make

First Time Home Buyer Glossary For first time home buyers, knowing and understanding the following terms are very important when purchasing your first home. By understanding these terms, you will make

Multiple Financed Properties Program Fannie Mae/Freddie Mac. Table of Contents

Table of Contents 1. Category... 2 2. High Balance... 2 3. Property Types...2 4. Applying the Multiple Financed property Policy to Manually Underwritten Loans... 2 5. Applying the Multiple Financed property

Table of Contents 1. Category... 2 2. High Balance... 2 3. Property Types...2 4. Applying the Multiple Financed property Policy to Manually Underwritten Loans... 2 5. Applying the Multiple Financed property

Introduction to the Fannie Mae HomeStyle Renovation Mortgage. Presented by Damon Richardson, Program Specialist - American Financial Resources, Inc.

Introduction to the Fannie Mae HomeStyle Renovation Mortgage Presented by Damon Richardson, Program Specialist - American Financial Resources, Inc. About the Presenter With 12 years of mortgage industry

Introduction to the Fannie Mae HomeStyle Renovation Mortgage Presented by Damon Richardson, Program Specialist - American Financial Resources, Inc. About the Presenter With 12 years of mortgage industry

Solar Leases FHA/VA. Term of lease must be greater than the loan term

Solar Leases FHA/VA Term of lease must be greater than the loan term The monthly payment for the lease must be included in the debt to income ratios for the borrower Must have like comps (with solar panel

Solar Leases FHA/VA Term of lease must be greater than the loan term The monthly payment for the lease must be included in the debt to income ratios for the borrower Must have like comps (with solar panel

Mortgage Insurance Fund Underwriting Guidelines

Mortgage Insurance Fund Underwriting Guidelines Table of Contents Philosophy...1 MassHousing Home Ownership Program...1 Non-MassHousing Loans...1 Loan Types (Eligible)...2 Loan Types (Ineligible)...2 Loan

Mortgage Insurance Fund Underwriting Guidelines Table of Contents Philosophy...1 MassHousing Home Ownership Program...1 Non-MassHousing Loans...1 Loan Types (Eligible)...2 Loan Types (Ineligible)...2 Loan

The SAPPHIRE. Program Training. Offered through FIRST MORTGAGE CORPORATION

The SAPPHIRE Program Training Offered through FIRST MORTGAGE CORPORATION Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie Mac. This presentation

The SAPPHIRE Program Training Offered through FIRST MORTGAGE CORPORATION Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie Mac. This presentation

EFFECTIVE FOR FHA CASE NUMBER ASSIGNMENTS ON AND AFTER SEPTEMBER 14, 2015 OVERLAY MATRIX: GOVERNMENT

Appraisals Attached PUDs Automated Findings Condominiums Credit History VA: Form 2055 Appraisal dated prior to the Note Date required on IRRRLs if current VA loan is not serviced by BB&T. FHA: Property

Appraisals Attached PUDs Automated Findings Condominiums Credit History VA: Form 2055 Appraisal dated prior to the Note Date required on IRRRLs if current VA loan is not serviced by BB&T. FHA: Property

1030HARP DU REFI PLUS (6/8/12)

") 1030HARP DU REFI PLUS (6/8/12) DESCRIPTION REQUIRED BORROWER BENEFIT DU Refi Plus is a limited cash-out refinance program that allows for expanded eligibility criteria, as well as reduced documentation

1030HARP DU REFI PLUS (6/8/12) DESCRIPTION REQUIRED BORROWER BENEFIT DU Refi Plus is a limited cash-out refinance program that allows for expanded eligibility criteria, as well as reduced documentation

FHA Streamline (Full Credit and Non-Credit Qualifying)

") . This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for FHA guidelines. Users are expected to know and comply

. This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for FHA guidelines. Users are expected to know and comply

VA Product Guidelines

July 16, 2015 VA Product Guidelines Purchase Occupancy Units LTV CLTV Minimum Credit Score Primary 1-4 100 100 620 Rate/Term Refinance Occupancy Units LTV CLTV Minimum Credit Score Primary 1-4 90 90 620

July 16, 2015 VA Product Guidelines Purchase Occupancy Units LTV CLTV Minimum Credit Score Primary 1-4 100 100 620 Rate/Term Refinance Occupancy Units LTV CLTV Minimum Credit Score Primary 1-4 90 90 620

E MORTGAGE MANAGEMENT LLC 303 DU REFI PLUS

E MORTGAGE MANAGEMENT LLC 303 DU REFI PLUS PRODUCT GUIDELINES 12/8/2014 MORTGAGE ELIGIBILITY Product Description and Product Codes Code Short Description Long Description CF30RP 30 YR REFI PLUS CF30RP

E MORTGAGE MANAGEMENT LLC 303 DU REFI PLUS PRODUCT GUIDELINES 12/8/2014 MORTGAGE ELIGIBILITY Product Description and Product Codes Code Short Description Long Description CF30RP 30 YR REFI PLUS CF30RP

Revolving Debt & Other Agency Guideline Revisions Note: SunTrust specific overlays are underlined.

Assets Section 2.04 DU Refi Plus Loan Program DU Refi Plus STM to STM Transactions Asset Documentation Requirements Assets must be documented in accordance with DU Refi Plus eligible DU Findings report.

Assets Section 2.04 DU Refi Plus Loan Program DU Refi Plus STM to STM Transactions Asset Documentation Requirements Assets must be documented in accordance with DU Refi Plus eligible DU Findings report.

Section 1: Loan Characteristics

Home Flex Quick Reference: Program Summary The following is an outline of the underwriting and closing requirements of New Hampshire Housing Home Flex program, which is available to lenders who have signed

Home Flex Quick Reference: Program Summary The following is an outline of the underwriting and closing requirements of New Hampshire Housing Home Flex program, which is available to lenders who have signed

Disclosure Specialist Responsibilities. Lock Procedures. Processor Responsibilities. Appraisal Ordering

FHA 203K Streamline - Policies & Procedures FHA 203K Streamline will now be underwritten and funded in house. These applications should be originated in Mortgage Builder under the FHA203K-SR program code.

FHA 203K Streamline - Policies & Procedures FHA 203K Streamline will now be underwritten and funded in house. These applications should be originated in Mortgage Builder under the FHA203K-SR program code.

VA Refinance Cash Out

VA Refinance Cash Out This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for VA guidelines. Users are expected

VA Refinance Cash Out This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for VA guidelines. Users are expected

Announcement 08-16 June 25, 2008

Announcement 08-16 June 25, 2008 Amends these Guides: Selling Bankruptcy, Foreclosure, and Conversion of Principal Residence Policy Changes; and Revised Property Value Representation and Warranty Requirements

Announcement 08-16 June 25, 2008 Amends these Guides: Selling Bankruptcy, Foreclosure, and Conversion of Principal Residence Policy Changes; and Revised Property Value Representation and Warranty Requirements

2010 NSP FIRST Mortgage Loan Program Summary Approved by THDA 05/07/2010

Description: Eligible Applicants: Maximum Household Interest Rate: Loan Term/ Type: Pre-Payment Penalty Subject to Recapture: Required Reserves: Down Payment Minimum Investment: Maximum Loan Amount: Homebuyer

Description: Eligible Applicants: Maximum Household Interest Rate: Loan Term/ Type: Pre-Payment Penalty Subject to Recapture: Required Reserves: Down Payment Minimum Investment: Maximum Loan Amount: Homebuyer

Conforming Fixed RateTexas Section 50(a)(6) (Texas Cash-out)

(6) (Texas Cash-out)") Minimum Credit Score: 620 Doc Type: Full Doc Maximum LTV: Maximum CLTV: 80% Maximum Loan Amount: $417,000 AUS: DU Approve/ 80% Maximum DT: 45% Standard Fixed Rate Purpose Units LTV CLTV Cash-out 1 80%

Minimum Credit Score: 620 Doc Type: Full Doc Maximum LTV: Maximum CLTV: 80% Maximum Loan Amount: $417,000 AUS: DU Approve/ 80% Maximum DT: 45% Standard Fixed Rate Purpose Units LTV CLTV Cash-out 1 80%

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

CREATIVE FINANCING STRATEGIES. 2015 Affordable Housing Conference

CREATIVE FINANCING STRATEGIES 2015 Affordable Housing Conference Panelist Moderator: Lewis Diaz, Partner Dinsmore & Shohl LLP [email protected] Speakers: Jeff Banker, Vice President Lancaster Pollard

CREATIVE FINANCING STRATEGIES 2015 Affordable Housing Conference Panelist Moderator: Lewis Diaz, Partner Dinsmore & Shohl LLP [email protected] Speakers: Jeff Banker, Vice President Lancaster Pollard

PORTFOLIO ARM CLOSED END 2 ND TD. Table of Contents

Table of Contents 1. Program Codes...2 2. Product Overview...2 3. Product Summary...2 4. Documentation...2 5. Underwriting...2 6. Qualifying Rate...2 7. Borrower Eligibility...2 8. Appraisal...3 9. Appraised

Table of Contents 1. Program Codes...2 2. Product Overview...2 3. Product Summary...2 4. Documentation...2 5. Underwriting...2 6. Qualifying Rate...2 7. Borrower Eligibility...2 8. Appraisal...3 9. Appraised

CHAPTER 9 PRODUCT MATRIX

Contents CHAPTER 9 PRODUCT MATRIX Conventional Conforming Loans 2 Secondary Market Arms... 4 HARP (Fannie DU Refi Plus & Freddie Open Access)... 5 Rural Housing 5 VA Programs. 5 Jumbo Programs 5 My Community

Contents CHAPTER 9 PRODUCT MATRIX Conventional Conforming Loans 2 Secondary Market Arms... 4 HARP (Fannie DU Refi Plus & Freddie Open Access)... 5 Rural Housing 5 VA Programs. 5 Jumbo Programs 5 My Community

ditech BUSINESS LENDING FHA STANDARD REFINANCE PRODUCT FOR CASE NUMBERS ASSIGNED ON OR AFTER 9/14/15

1. PRODUCT FHA Fixed Rate and ARM Mortgages for Rate and Term Refinance, Cash-Out Refinance and Simple Refinance Transactions DESCRIPTION Fixed Rate 5 to 30 year term in annual increments Fully amortizing

1. PRODUCT FHA Fixed Rate and ARM Mortgages for Rate and Term Refinance, Cash-Out Refinance and Simple Refinance Transactions DESCRIPTION Fixed Rate 5 to 30 year term in annual increments Fully amortizing

Refinancing may be an option for you to consider if your loan is adjusting to an interest rate that's higher than the current market rates.

How does an adjustable rate mortgage (ARM) work? Like many homebuyers, you may have been attracted to the low initial interest rate of an adjustable-rate mortgage (ARM). While adjustable-rate mortgages

How does an adjustable rate mortgage (ARM) work? Like many homebuyers, you may have been attracted to the low initial interest rate of an adjustable-rate mortgage (ARM). While adjustable-rate mortgages

Texas Home Equity Program Guide Fixed Rate

Fixed Rate Wholesale Lending July 20, 2015 Table of Contents Texas Home Equity Program Guide... 1 Fixed Rate... 1 Program Overview... 2 Employee Loan Policy... 2 Credit Philosophy... 2 Ability to Repay

Fixed Rate Wholesale Lending July 20, 2015 Table of Contents Texas Home Equity Program Guide... 1 Fixed Rate... 1 Program Overview... 2 Employee Loan Policy... 2 Credit Philosophy... 2 Ability to Repay

FHA STREAMLINE REFINANCE GUIDELINES

Table of Contents FHA STREAMLINE REFINANCE GUIDELINES Maximum Mortgage Amount Calculations... 1 Streamline With Appraisal... 1 Streamline Without Appraisal... 2 Underwriting and Eligibility Criteria...

Table of Contents FHA STREAMLINE REFINANCE GUIDELINES Maximum Mortgage Amount Calculations... 1 Streamline With Appraisal... 1 Streamline Without Appraisal... 2 Underwriting and Eligibility Criteria...

A Simplified Overview of FHA Loan Origination

Introduction to FHA Origination A Simplified Overview of FHA Loan Origination Topics of Discussion Introduction to FHA Fundamentals of Loan Origination FHA Loan Limits Borrower Eligibility Property Eligibility

Introduction to FHA Origination A Simplified Overview of FHA Loan Origination Topics of Discussion Introduction to FHA Fundamentals of Loan Origination FHA Loan Limits Borrower Eligibility Property Eligibility

ORIGINAL 5/5 ADJUSTABLE RATE MORTGAGE LOAN 5/5 POWER PURCHASE MORTGAGE LOAN

5/5 ARM HOME LOAN RATES AND TERMS Effective October, 015 and subject to change. Get flexibility, stability and no closing costs 1 with SDCCU s 5/5 Adjustable Rate Mortgage Home Loan. Your rate can only

5/5 ARM HOME LOAN RATES AND TERMS Effective October, 015 and subject to change. Get flexibility, stability and no closing costs 1 with SDCCU s 5/5 Adjustable Rate Mortgage Home Loan. Your rate can only

FHA STREAMLINE REFINANCE GUIDELINES

Table of Contents FHA STREAMLINE REFINANCE GUIDELINES Maximum Mortgage Amount Calculations... 1 Underwriting and Eligibility Criteria... 2 Documentation Requirements... 4 Appraisal Requirements... 5 Maximum

Table of Contents FHA STREAMLINE REFINANCE GUIDELINES Maximum Mortgage Amount Calculations... 1 Underwriting and Eligibility Criteria... 2 Documentation Requirements... 4 Appraisal Requirements... 5 Maximum

Desktop Originator/Desktop Underwriter Release Notes DU Version 9.2

Desktop Originator/Desktop Underwriter Release Notes DU Version 9.2 October 14, 2014 Last updated December 8, 2014 During the weekend of December 13, 2014, Fannie Mae will implement Desktop Underwriter

Desktop Originator/Desktop Underwriter Release Notes DU Version 9.2 October 14, 2014 Last updated December 8, 2014 During the weekend of December 13, 2014, Fannie Mae will implement Desktop Underwriter

Automated Underwriting. Classroom Text

Automated Underwriting Classroom Text Chapter Four Page 1 Automated Underwriting The Reasoning Behind Automated Underwriting The mortgage industry is rapidly moving into the automated age. Lead-generation

Automated Underwriting Classroom Text Chapter Four Page 1 Automated Underwriting The Reasoning Behind Automated Underwriting The mortgage industry is rapidly moving into the automated age. Lead-generation

Debt Service Coverage Ratio (DSCR) Calculations and Examples

Calculations and Examples") April 15, 2014 Debt Service Coverage Ratio (DSCR) Calculations and Examples This document provides product-specific information and sample calculations for the debt service coverage ratio that is disclosed

April 15, 2014 Debt Service Coverage Ratio (DSCR) Calculations and Examples This document provides product-specific information and sample calculations for the debt service coverage ratio that is disclosed

Section 2.04 - DU Refi Plus Loan Program

Section 2.04 - DU Refi Plus Loan Program In This Product Description This product description contains the following topics: Overview... 2 Related Bulletins... 5 Existing Mortgage Eligibility Requirements...

Section 2.04 - DU Refi Plus Loan Program In This Product Description This product description contains the following topics: Overview... 2 Related Bulletins... 5 Existing Mortgage Eligibility Requirements...

Texas Home Equity Section 50(a)(6)

(6)") Texas Home Equity Section 50(a)(6) Revised 09/16/2015 rev. 16 Plaza s Underwriting Guidelines are designed to provide guidance as a standard to underwriting loans. There are cases where specific loan programs

Texas Home Equity Section 50(a)(6) Revised 09/16/2015 rev. 16 Plaza s Underwriting Guidelines are designed to provide guidance as a standard to underwriting loans. There are cases where specific loan programs

NOTE: This matrix includes overlays, which may be more restrictive than FHA requirements. A thorough reading of this matrix is recommended.

This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for FHA guidelines. Users are expected to know and comply

This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for FHA guidelines. Users are expected to know and comply

FHA Streamline Refi. LTV w/o Sec Fin. CLTV w/ Sec Fin. Varies by County (a) None (b) 125 (b,d) 31/43 (c)

None (b) 125 (b,d) 31/43 (c)") SERIES 3 Primary Residence Units Minimum Credit Score Max Loan Amount Continental US 1-4 680 (f) Varies by County (a) 1-4 680 (f) Varies by County (a) Max Loan Amount Hawaii LTV w/o Sec Fin STREAMLINE

SERIES 3 Primary Residence Units Minimum Credit Score Max Loan Amount Continental US 1-4 680 (f) Varies by County (a) 1-4 680 (f) Varies by County (a) Max Loan Amount Hawaii LTV w/o Sec Fin STREAMLINE

PRODUCT GUIDELINES CONVENTIONAL NON-CONFORMING FIXED 15-20-30 YEAR HEF

Several states and local municipalities have enacted legislation that define High Cost loans based on APR and fee thresholds which may or may not relate to the HOEPA thresholds. These types of loans typically

Several states and local municipalities have enacted legislation that define High Cost loans based on APR and fee thresholds which may or may not relate to the HOEPA thresholds. These types of loans typically

LOAN PROGRAMS AND INFO WWW.PRIVATEHARDMONEY.LOAN

LOAN PROGRAMS AND INFO WWW.PRIVATEHARDMONEY.LOAN PRIVATE LENDING & HARD MONEY The biggest problem facing real estate investors is where to find the money to fund their deals. Private Hard Money Loans provides

LOAN PROGRAMS AND INFO WWW.PRIVATEHARDMONEY.LOAN PRIVATE LENDING & HARD MONEY The biggest problem facing real estate investors is where to find the money to fund their deals. Private Hard Money Loans provides

ditech BUSINESS LENDING DU REFI PLUS TEXAS HOME EQUITY PRODUCT

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING DU REFI PLUS TEXAS HOME EQUITY PRODUCT Conventional Conforming fixed rate mortgage DU Version 9.3 Servicing retained 10, 15, 20, 25 and 30 year terms Fully

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING DU REFI PLUS TEXAS HOME EQUITY PRODUCT Conventional Conforming fixed rate mortgage DU Version 9.3 Servicing retained 10, 15, 20, 25 and 30 year terms Fully

CALHOME MORTGAGE ASSISTANCE PROGRAM GUIDELINES

PLANNING AND DEVELOPMENT DEPARTMENT HOUSING AND COMMUNITY DEVELOPMENT DIVISION CALHOME MORTGAGE ASSISTANCE PROGRAM GUIDELINES PROGRAM OVERVIEW The CalHome Mortgage Assistance Program is a program funded

PLANNING AND DEVELOPMENT DEPARTMENT HOUSING AND COMMUNITY DEVELOPMENT DIVISION CALHOME MORTGAGE ASSISTANCE PROGRAM GUIDELINES PROGRAM OVERVIEW The CalHome Mortgage Assistance Program is a program funded

HUD Mortgage Insurance Program Section 232 LEAN

HUD Mortgage Insurance Program Section 232 LEAN Skilled Nursing, Intermediate Care, Assisted Living, Board & Care Benefits: The LEAN program offers more efficient processing through a centralized application,

HUD Mortgage Insurance Program Section 232 LEAN Skilled Nursing, Intermediate Care, Assisted Living, Board & Care Benefits: The LEAN program offers more efficient processing through a centralized application,

Share Loan and Underlying Mortgage Financing. Jeremy Morgan, NCB Larry Mathe, NCB

Share Loan and Underlying Mortgage Financing Jeremy Morgan, NCB Larry Mathe, NCB About NCB NCB is the premier lender to housing cooperatives nationwide. NCB has financed over $6 Billion to housing cooperatives

Share Loan and Underlying Mortgage Financing Jeremy Morgan, NCB Larry Mathe, NCB About NCB NCB is the premier lender to housing cooperatives nationwide. NCB has financed over $6 Billion to housing cooperatives

CITY OF SOLEDAD FIRST-TIME HOMEBUYER ASSISTANCE PROGRAM FIRST MORTGAGE LENDER INSTRUCTIONS 248 MAIN STREET, SOLEDAD CA 93960

FIRST MORTGAGE LENDER INSTRUCTIONS Maximum Home Sales Price Home sale prices cannot exceed 95% of the area median home value for Soledad (see Table 1: Maximum Purchase Price per Unit). Maximum Loan-to-Value

FIRST MORTGAGE LENDER INSTRUCTIONS Maximum Home Sales Price Home sale prices cannot exceed 95% of the area median home value for Soledad (see Table 1: Maximum Purchase Price per Unit). Maximum Loan-to-Value

USDA Business & Industry (B&I) Guaranteed Loan Program

Guaranteed Loan Program") USDA Business & Industry (B&I) Guaranteed Loan Program B&I Program To Create And Maintain Employment And Improve Economic And Environmental Climate In Rural Communities Administered By The Rural Business

USDA Business & Industry (B&I) Guaranteed Loan Program B&I Program To Create And Maintain Employment And Improve Economic And Environmental Climate In Rural Communities Administered By The Rural Business

13 DOWNPAYMENT PROGRAMS

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Home Advantage Downpayment Assistance Program can

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Home Advantage Downpayment Assistance Program can

GLOSSARY COMMONLY USED REAL ESTATE TERMS

GLOSSARY COMMONLY USED REAL ESTATE TERMS Adjustable-Rate Mortgage (ARM): a mortgage loan with an interest rate that is subject to change and is not fixed at the same level for the life of the loan. These

GLOSSARY COMMONLY USED REAL ESTATE TERMS Adjustable-Rate Mortgage (ARM): a mortgage loan with an interest rate that is subject to change and is not fixed at the same level for the life of the loan. These

Comparison of SONYMA Mortgages vs. FHA

Levels of loan approval FHA self insures Lenders Direct Endorsement Underwriters approve loans 3* Levels of loan approval Lender PMI/Pool Insurer *Pre Closing SONYMA compliance review will be eliminated

Levels of loan approval FHA self insures Lenders Direct Endorsement Underwriters approve loans 3* Levels of loan approval Lender PMI/Pool Insurer *Pre Closing SONYMA compliance review will be eliminated

Ability to Repay & QM Regulations

Ability to Repay & QM Regulations 2013 Rushmore Loan Management Services LLC. All Rights Reserved. This is intended as educational material only. It does not provide legal advice. Revised December 2013

Ability to Repay & QM Regulations 2013 Rushmore Loan Management Services LLC. All Rights Reserved. This is intended as educational material only. It does not provide legal advice. Revised December 2013

COMMUNITY ACQUISITION REHABILITATION LOAN CARL CARL TERM SHEET AND GUIDELINES

COMMUNITY ACQUISITION REHABILITATION LOAN I. PROGRAM OBJECTIVE CARL CARL TERM SHEET AND GUIDELINES URBAN REDEVELOPMENT AUTHORITY OF PITTSBURGH PITTSBURGH COMMUNITY REINVESTMENT GROUP The main objective

COMMUNITY ACQUISITION REHABILITATION LOAN I. PROGRAM OBJECTIVE CARL CARL TERM SHEET AND GUIDELINES URBAN REDEVELOPMENT AUTHORITY OF PITTSBURGH PITTSBURGH COMMUNITY REINVESTMENT GROUP The main objective

Underwriting Guideline Matrix

: Program / Product Codes: 30 Year Fixed (W130) 15 Year Fixed (W132) Subject to Change Without Notice Valid as of: 06/10/2014 Copyright 2015 Skyline Financial Corp. dba Skyline Home Loans Nationwide Mortgage

: Program / Product Codes: 30 Year Fixed (W130) 15 Year Fixed (W132) Subject to Change Without Notice Valid as of: 06/10/2014 Copyright 2015 Skyline Financial Corp. dba Skyline Home Loans Nationwide Mortgage

Announcement 08-22 September 5, 2008. Miscellaneous Eligibility, Policy, and Pricing Updates

Announcement 08-22 September 5, 2008 Amends these Guides: Selling Miscellaneous Eligibility, Policy, and Pricing Updates Introduction This Announcement contains updates and clarifications to Fannie Mae

Announcement 08-22 September 5, 2008 Amends these Guides: Selling Miscellaneous Eligibility, Policy, and Pricing Updates Introduction This Announcement contains updates and clarifications to Fannie Mae

THE OXBRIDGE FHA FACILITY FHA TERM SHEETS

THE OXBRIDGE FHA FACILITY FHA TERM SHEETS Set forth below are the various types of FHA Loans for which the Oxbridge FHA Facility will provide GAP funding (i.e. funding of borrower equity requirement) to

THE OXBRIDGE FHA FACILITY FHA TERM SHEETS Set forth below are the various types of FHA Loans for which the Oxbridge FHA Facility will provide GAP funding (i.e. funding of borrower equity requirement) to

MORTGAGE TERMS. Assignment of Mortgage A document used to transfer ownership of a mortgage from one party to another.

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

VA Product Guidelines

August 10, 2015 VA Product Guidelines Purchase Occupancy Units LTV CLTV Primary 1-4 100 100 620 Rate/Term Refinance Occupancy Units LTV CLTV Primary 1-4 100 100 620 IRRRL Occupancy Units LTV CLTV Primary

August 10, 2015 VA Product Guidelines Purchase Occupancy Units LTV CLTV Primary 1-4 100 100 620 Rate/Term Refinance Occupancy Units LTV CLTV Primary 1-4 100 100 620 IRRRL Occupancy Units LTV CLTV Primary

Deal Maker First & Second Mortgage

Click Here For PDF Version ALL PROGRAMS REQUIRE FULL DOCUMENTATION FIRST MORTGAGE Owner Occupied SINGLE FAMILY PROPERTY Purchase & Refinance Credit Score Max. LTV / CLTV Max. Loan Amount Max. Mortgage

Click Here For PDF Version ALL PROGRAMS REQUIRE FULL DOCUMENTATION FIRST MORTGAGE Owner Occupied SINGLE FAMILY PROPERTY Purchase & Refinance Credit Score Max. LTV / CLTV Max. Loan Amount Max. Mortgage

Announcement 09-29 September 22, 2009

Announcement 09-29 September 22, 2009 Amends these Guides: Selling Updates to Minimum Credit Scores, Mortgage Insurance, Pricing for Certain Desktop Underwriter Loans, Biweekly Loans, and Special Feature

Announcement 09-29 September 22, 2009 Amends these Guides: Selling Updates to Minimum Credit Scores, Mortgage Insurance, Pricing for Certain Desktop Underwriter Loans, Biweekly Loans, and Special Feature

Lake County Homebuyer Programs Lender Guidelines as of 1/22/2014

Lake County Homebuyer Programs Lender Guidelines as of 1/22/2014 ABOUT THE AFFORDABLE HOUSING CORPORATION OF LAKE COUNTY AHC is a nonprofit agency that increases and preserves affordable housing opportunities

Lake County Homebuyer Programs Lender Guidelines as of 1/22/2014 ABOUT THE AFFORDABLE HOUSING CORPORATION OF LAKE COUNTY AHC is a nonprofit agency that increases and preserves affordable housing opportunities

Announcement 08-05 March 6, 2008. Temporary Increase to Our Conventional Loan Limits

Announcement 08-05 March 6, 2008 Amends these Guides: Selling Temporary Increase to Our Conventional Loan Limits Introduction The Economic Stimulus Act of 2008, signed into law on February 13, 2008, establishes

Announcement 08-05 March 6, 2008 Amends these Guides: Selling Temporary Increase to Our Conventional Loan Limits Introduction The Economic Stimulus Act of 2008, signed into law on February 13, 2008, establishes

Oklahoma Housing Finance Agency. Lee Ann Smith Director, Single Family Programs September 16, 2015

1 Oklahoma Housing Finance Agency Lee Ann Smith Director, Single Family Programs September 16, 2015 2 OHFA Description OHFA Advantage program provides first mortgage financing and down payment assistance

1 Oklahoma Housing Finance Agency Lee Ann Smith Director, Single Family Programs September 16, 2015 2 OHFA Description OHFA Advantage program provides first mortgage financing and down payment assistance

Oaktree Funding Corporation

Freddie Mac s Relief Refinance Open Access Agenda What is Relief Refinance Mortgages Open Access? AUS and Qualifications FAQ s Questions 2 What is Relief Refinance Mortgages Open Access? The Freddie Mac

Freddie Mac s Relief Refinance Open Access Agenda What is Relief Refinance Mortgages Open Access? AUS and Qualifications FAQ s Questions 2 What is Relief Refinance Mortgages Open Access? The Freddie Mac

96.50% Refinance Cash-Out 620 75% 75% Purchase 620 96.50% 96.50% 45% Refinance, No Cash- 620 97.75% 97.75% 45%

GNMA Portfolio Program Summary Product Types Eligible Programs 30-year Fixed FHA loans 203(b) 1-4 family, 234(c) Condominiums, Standard Balance Loan Purpose Minimum FICO Maximum LTV Maximum CLTV Purchase

GNMA Portfolio Program Summary Product Types Eligible Programs 30-year Fixed FHA loans 203(b) 1-4 family, 234(c) Condominiums, Standard Balance Loan Purpose Minimum FICO Maximum LTV Maximum CLTV Purchase

Are you eligible for an ACCION Chicago small business loan?

Lending. Supporting. Inspiring. Are you eligible for an ACCION Chicago small business loan? Y/ N Are you looking for a loan between 200 and 15,000 for your start-up business (less than 6 months of revenue

Lending. Supporting. Inspiring. Are you eligible for an ACCION Chicago small business loan? Y/ N Are you looking for a loan between 200 and 15,000 for your start-up business (less than 6 months of revenue

The Math Behind Loan Modification

The Math Behind Loan Modification A Webinar for Housing Counselors and Loan Modification Specialists Presented by Bill Allen Deputy Director, HomeCorps Overview Types of loan modifications Estimating eligibility

The Math Behind Loan Modification A Webinar for Housing Counselors and Loan Modification Specialists Presented by Bill Allen Deputy Director, HomeCorps Overview Types of loan modifications Estimating eligibility

CalStar Mortgage Inc. For All Your Financing Needs

CalStar Mortgage Inc. For All Your Financing Needs Jasmen Vartanian Tel: 818-952-2701 Email: [email protected] www.calstarmortgage.com Excellent Service since 1987 1033 Foothill Blvd. La Canada Flintridge,

CalStar Mortgage Inc. For All Your Financing Needs Jasmen Vartanian Tel: 818-952-2701 Email: [email protected] www.calstarmortgage.com Excellent Service since 1987 1033 Foothill Blvd. La Canada Flintridge,

RESIDENTIAL MORTGAGE LOAN BOOKLET. ICBC (USA) Residential Mortgage Products. No.1 FNMA Loan No. 2 Flex ARM No. 3 Flex ARM Plus No.

Residential Mortgage Products. No.1 FNMA Loan No. 2 Flex ARM No. 3 Flex ARM Plus No.") ICBC (USA) Residential Mortgage Products No.1 FNMA Loan No. 2 Flex ARM No. 3 Flex ARM Plus No. 4 CRES ARM ICBC(USA)NA RESIDENTIAL MORTGAGE LOAN BOOKLET ICBC (USA) NA www.icbc-us.com [email protected]

ICBC (USA) Residential Mortgage Products No.1 FNMA Loan No. 2 Flex ARM No. 3 Flex ARM Plus No. 4 CRES ARM ICBC(USA)NA RESIDENTIAL MORTGAGE LOAN BOOKLET ICBC (USA) NA www.icbc-us.com [email protected]

ditech BUSINESS LENDING FHA STREAMLINE REFINANCE PRODUCT FOR CASE NUMBERS ASSIGNED ON OR AFTER 9/14/15

NON- 1. PRODUCT DESCRIPTION 2. ELIGIBLE PROGRAMS 3. CURRENT FIRST MORTGAGE ELIGIBILITY FHA Fixed Rate and ARM Mortgages for Streamline Refinance Transactions Fixed Rate 5 to 30 year term in annual increments

NON- 1. PRODUCT DESCRIPTION 2. ELIGIBLE PROGRAMS 3. CURRENT FIRST MORTGAGE ELIGIBILITY FHA Fixed Rate and ARM Mortgages for Streamline Refinance Transactions Fixed Rate 5 to 30 year term in annual increments

Cooperative Housing/ Share Loan Financing. Larry Mathe Chris Goettke National Cooperative Bank

Cooperative Housing/ Share Loan Financing Larry Mathe Chris Goettke National Cooperative Bank The NCB Story NCB delivers banking and financial services to cooperative organizations complemented by a special

Cooperative Housing/ Share Loan Financing Larry Mathe Chris Goettke National Cooperative Bank The NCB Story NCB delivers banking and financial services to cooperative organizations complemented by a special

FHA HIGH BALANCE FIXED PROGRAM HIGHLIGHTS

Product Summary These guidelines represent underwriting requirements for FHA fixed rate and ARM mortgages with increased loan size limits with a minimum floor of greater than $417,000. These guidelines

Product Summary These guidelines represent underwriting requirements for FHA fixed rate and ARM mortgages with increased loan size limits with a minimum floor of greater than $417,000. These guidelines

Variable Names & Descriptions

Variable Names & Descriptions Freddie Mac provides loan-level information at PC issuance and on a monthly basis for all newly issued fixed-rate and adjustable-rate mortgage (ARM) PC securities issued after

Variable Names & Descriptions Freddie Mac provides loan-level information at PC issuance and on a monthly basis for all newly issued fixed-rate and adjustable-rate mortgage (ARM) PC securities issued after

Ability to Repay/Qualified Mortgages FAQ

The Ability to Repay (ATR)/Qualified Mortgages (QM) provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act require lenders to make a reasonable, good faith determination of a borrower

The Ability to Repay (ATR)/Qualified Mortgages (QM) provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act require lenders to make a reasonable, good faith determination of a borrower

Evaluating the HECM product

Evaluating the HECM product March 26, 2015 Presented by Garrett M. Kolb [email protected] Senior Managing Director Reverse Mortgage Solutions, Inc. For Mortgage Professionals Only These materials are designed

Evaluating the HECM product March 26, 2015 Presented by Garrett M. Kolb [email protected] Senior Managing Director Reverse Mortgage Solutions, Inc. For Mortgage Professionals Only These materials are designed