Descartes audit methodology and software

|

|

|

- Gerard Leonard

- 9 years ago

- Views:

Transcription

1 Descartes audit methodology and software Den norske Revisorforening/ The Norwegian Institute of Public Accountants Den norske Revisorforening

2 Introduction The Norwegian Institute of Public Accountants (DnR) is the professional body for public accountants in Norway Approximately 5000 members side 2

3 Background Until 2011 Statutory audits for all limited liability companies ISAs implemented in 1998 More than 50 % of the statutory audits performed by SMPs Public oversight in Norway for decades Few regulative amendments to national law (implemented the Audit directive) Systematic quality assurance reviews since 1991 side 3

Systematic quality assurance reviews since 1991")

4 Why develop Descartes? Only Big Firms had sophisticated audit methodologies and tools Institute s goal was to give all members access to a high quality methodology supported by an IT-application for planning, performing and documenting the audit side 4

5 About Descartes Descartes is owned by The Norwegian Institute of Public Accountants Bouvet ASA (listed company) is our IT partner side 5

is our IT")

6 Why Descartes? French philosopher and mathematician René Descartes ( ), known for statements like: Always go forward carefully and systematically Do not think that something is true until you are sure of it Dissolve any problem as far as possible Increasing enumeration and control is the only path to full answers side 6

7 About Descartes Launched in 1998 The risk based standards implemented in 2006 Clarified ISAs implemented in 2010 Additional engagement types in 2011: ISA 805, ISRE 2400 and ISRS 4410 New major version in June 2014 (same methodology) side 7

")

8 About Descartes Number of licenses 2568 Norway 110 Slovenia 43 - Iceland In addition to auditors of financial statements Descartes is used by: Municipality auditors The internal audit department in Norway's largest bank (DNB Nor) Business schools and universities in Norway and Iceland (educational purposes) The public oversight body in Norway The National Audit Office in Iceland side 8

The public oversight body in Norway The National Audit Office in")

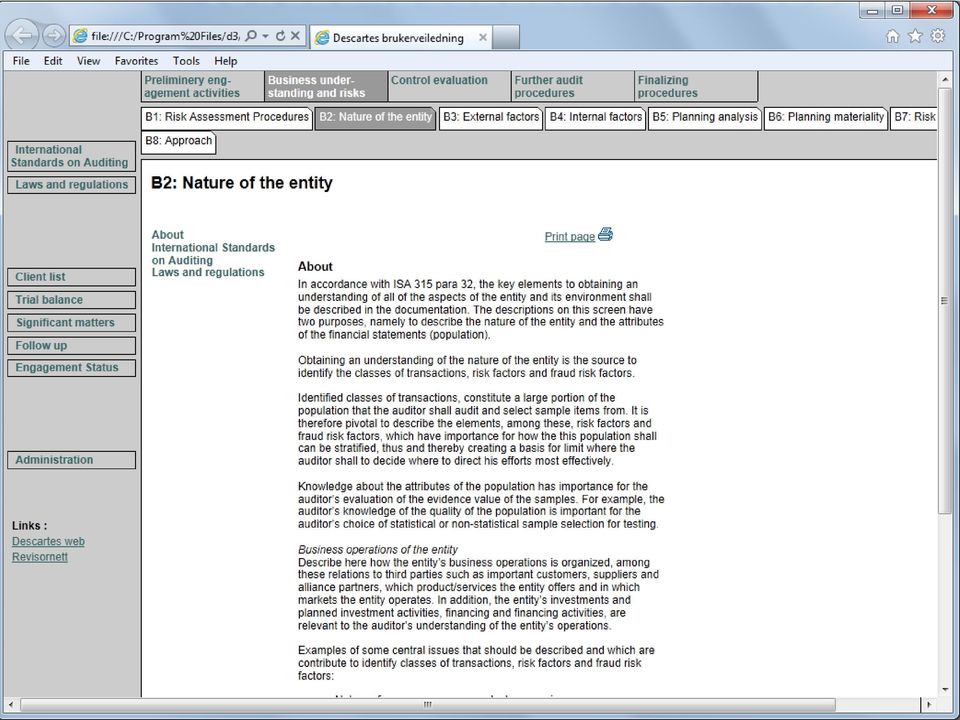

9 About Descartes ISA compliant Using the same expressions and wording as the ISAs White fields/textboxes = ISA requirement Support the audit work flow (phases and audit steps) side 9

")

10 Phases in Descartes A. Preliminary engagement activities B. Understanding the entity & identifying Risks C. Assessment of controls by audit area D. Further audit procedures by area E. Finalizing audit procedures side 10

11 The risk model Preliminary engagement activities DOCUMENTATION Risk assessment procedures Understanding the entity Risk factors/classes of transactions assertions Evaluating internal controls Auditor s risk assessment assessed risks Further audit procedures Completion activities/conclusions Reporting/Communication

12 Prelimenary procedures Audit procedures Conclusion Financial Statement Reasonable assurance Auditors report IC IR A B C D E side 12

13 Assessed risks INHERENT RISK X CONTROL RISK X DETECTION RISK Phase A Risk assessment procedures Phases B and C Further audit procedures, Phase D Phase E Identification Classes of transactions risks fraud factors Identification and testing of controls Substantive analytical procedures Tests of details ISA 315 ISA 240 ISA 315 ISA 240 ISA 330 ISA 330 ISA 240 side 13

14 About Descartes Help the auditors comply and document their audit in compliance with ISAs Flexible regarding the extent of documentation: Directly in the tool Attachments side 14

15 side 15

16 About Descartes Integration with the ISAs. Sophisticated help function : o purpose of the phase and subphase o relevant ISAs o relevant national regulation side 16

17 side 17

18 side 18

19 side 19

20 About Descartes Scalable and flexible fits all engagements, small large What makes it scalable? The numbers of audit areas The type and extent of procedures to perform Extent of documentation side 20

21 About Descartes Follow-up for each engagement: Engagement status Follow-up Significant matters Open issues Summary of assertions side 21

22 Skjermdump Engagement status side 22

23 About Descartes Portfolio overview - a list of all clients: Important dates within each engagement Date of audit report and responsible auditor Team members, review partner and experts Hours spent on planning, interim audit and year end audit Can be exported to excel for additional analysing side 23

24 About Descartes - Technology Windows client using.net Minimal requirements for each computer Simple internet based installation Automatic distribution of program updates on a continuous basis side 24

25 About Descartes - Technology Online and offline/synchronising: Saves all data in a buffer memory locally Synchronised when the database is accessible Data is stored in one or several databases: Clients are shared by the users All file types can be stored in the database as attachments side 25

26 About Descartes - Technology Minimum requirements for server/database: Operating system: MS Windows Database: MS SQL Server or SQL Express (free versions) Memory: 1024 MB side 27

27 Impacts experienced with Descartes Efficiency 20 % time saved (BDO) Reduction of paper files (80 90 %) Recruitment motivates young people Access and security of client files side 28

28 Descartes ensures: relevant information is obtained and assessed that required procedures are performed (risk assessment) important assessments are made (risk, materiality and audit evidence) sufficient documentation => effective ISA compliant SME audits side 29

29 About Descartes abroad Iceland and Slovenia: Iceland English Slovenia - Slovenian Co-operation with the national institutes: National laws and regulations Translation Training Technical support side 30

30 About Descartes abroad Training: Assist the institutes with training courses Recommend a one day course for beginners Support: Web-based IT-support Web-page Newsletters side 31

31 Pricing The yearly license fee (subscription) is currently NOK 7700 (approx. EUR 1000) for the application (incl. database). The price for an additional user is NOK 2400 (approx. EUR 315). Minimum +/- 100 users. side 32

32 Descartes A high quality audit methodology operationalizing the ISAs supported by a modern IT application is the only way to an effective quality audit fully in compliance with the ISAs. side 33

33 For more information about Descartes Descartes web-page: Download the demo version side 34

Action Plan Developed by Den norske Revisorforening (DnR) BACKGROUND NOTE ON ACTION PLANS

BACKGROUND NOTE ON ACTION PLANS") BACKGROUND NOTE ON ACTION PLANS Action Plans are developed by IFAC members and associates to address policy matters identified through their responses to the IFAC Compliance Self-Assessment Questionnaires.

BACKGROUND NOTE ON ACTION PLANS Action Plans are developed by IFAC members and associates to address policy matters identified through their responses to the IFAC Compliance Self-Assessment Questionnaires.

Comparison of ISA 330 with AS-402 Objectives and Requirements Only

Comparison of ISA 330 with AS-402 Objectives and Requirements Only International Standard on Auditing 330 (Redrafted): The Auditor s INTRODUCTION Scope of this ISA 1. This International Standard on Auditing

Comparison of ISA 330 with AS-402 Objectives and Requirements Only International Standard on Auditing 330 (Redrafted): The Auditor s INTRODUCTION Scope of this ISA 1. This International Standard on Auditing

SESSION 3 AUDIT PLANNING

SESSION 3 AUDIT PLANNING Learning Objectives: identify and explain the need for planning an audit identify and describe the contents of the overall audit strategy and the audit plan explain the difference

SESSION 3 AUDIT PLANNING Learning Objectives: identify and explain the need for planning an audit identify and describe the contents of the overall audit strategy and the audit plan explain the difference

ISRE 2400 (Revised), Engagements to Review Historical Financial Statements

, Engagements to Review Historical Financial Statements") International Auditing and Assurance Standards Board Exposure Draft January 2011 Comments requested by May 20, 2011 Proposed International Standard on Review Engagements ISRE 2400 (Revised), Engagements

International Auditing and Assurance Standards Board Exposure Draft January 2011 Comments requested by May 20, 2011 Proposed International Standard on Review Engagements ISRE 2400 (Revised), Engagements

Risk Assessment Standards

Risk Assessment Standards Virginia Government Finance Officer's Association Spring Conference May 23, 2008 P R C P KMPG LLP J M P C B H H H T M AICPA Presentation Objectives 1. Discuss background of risk

Risk Assessment Standards Virginia Government Finance Officer's Association Spring Conference May 23, 2008 P R C P KMPG LLP J M P C B H H H T M AICPA Presentation Objectives 1. Discuss background of risk

Interim report 1st quarter 2016

Interim report 1st quarter 2016 About Komplett Bank ASA Komplett Bank ASA started banking operations on 21 March 2014 when the company received its banking licence from the Norwegian authorities. Komplett

Interim report 1st quarter 2016 About Komplett Bank ASA Komplett Bank ASA started banking operations on 21 March 2014 when the company received its banking licence from the Norwegian authorities. Komplett

GUIDELINES FOR AUDITS OF COUNTY AND CITY HOSPITALS BY INDEPENDENT CERTIFIED PUBLIC ACCOUNTING FIRMS

GUIDELINES FOR AUDITS OF COUNTY AND CITY HOSPITALS BY INDEPENDENT CERTIFIED PUBLIC ACCOUNTING FIRMS ISSUED JUNE 2002 INTRODUCTION On March 21, 2002, Public Law 91, 2002 amended IC 16-22-3-12 to allow county

GUIDELINES FOR AUDITS OF COUNTY AND CITY HOSPITALS BY INDEPENDENT CERTIFIED PUBLIC ACCOUNTING FIRMS ISSUED JUNE 2002 INTRODUCTION On March 21, 2002, Public Law 91, 2002 amended IC 16-22-3-12 to allow county

Risks (Audit Risk Formula)

") Risks (Audit Risk Formula) Component of Audit Risk Inherent risk Errors likely to occur In client s financial statements Control risk Detection risk Audit risk Errors not detected by controls Errors that

Risks (Audit Risk Formula) Component of Audit Risk Inherent risk Errors likely to occur In client s financial statements Control risk Detection risk Audit risk Errors not detected by controls Errors that

About Komplett Bank ASA. Outlook. Developments to date

Interim report 3 rd quarter 2015 About Komplett Bank ASA Komplett Bank ASA started banking operations on 21 March 2014 when the company received its banking licence from the Norwegian authorities. Komplett

Interim report 3 rd quarter 2015 About Komplett Bank ASA Komplett Bank ASA started banking operations on 21 March 2014 when the company received its banking licence from the Norwegian authorities. Komplett

Work Plan for 2015 2016: Enhancing Audit Quality and Preparing for the Future. The IAASB s Work Plan for 2015 2016 December 2014

The IAASB s Work Plan for 2015 2016 December 2014 International Auditing and Assurance Standards Board Work Plan for 2015 2016: Enhancing Audit Quality and Preparing for the Future This document was developed

The IAASB s Work Plan for 2015 2016 December 2014 International Auditing and Assurance Standards Board Work Plan for 2015 2016: Enhancing Audit Quality and Preparing for the Future This document was developed

INTERNATIONAL STANDARD ON REVIEW ENGAGEMENTS 2410 REVIEW OF INTERIM FINANCIAL INFORMATION PERFORMED BY THE INDEPENDENT AUDITOR OF THE ENTITY CONTENTS

INTERNATIONAL STANDARD ON ENGAGEMENTS 2410 OF INTERIM FINANCIAL INFORMATION PERFORMED BY THE INDEPENDENT AUDITOR OF THE ENTITY (Effective for reviews of interim financial information for periods beginning

INTERNATIONAL STANDARD ON ENGAGEMENTS 2410 OF INTERIM FINANCIAL INFORMATION PERFORMED BY THE INDEPENDENT AUDITOR OF THE ENTITY (Effective for reviews of interim financial information for periods beginning

About Komplett Bank ASA. Outlook. Developments to date

Interim report 4th quarter 2015 About Komplett Bank ASA Komplett Bank ASA started banking operations on 21 March 2014 when the company received its banking licence from the Norwegian authorities. Komplett

Interim report 4th quarter 2015 About Komplett Bank ASA Komplett Bank ASA started banking operations on 21 March 2014 when the company received its banking licence from the Norwegian authorities. Komplett

BDO Seidman, LLP Accountants and Consultants

BDO Seidman, LLP Accountants and Consultants 330 Madison Avenue New York, NY 10017 (212) 885-8000 Phone (212) 697-1299 Fax Via E-mail: [email protected] Office of the Secretary Public Company Accounting

BDO Seidman, LLP Accountants and Consultants 330 Madison Avenue New York, NY 10017 (212) 885-8000 Phone (212) 697-1299 Fax Via E-mail: [email protected] Office of the Secretary Public Company Accounting

INTERNATIONAL STANDARD ON AUDITING 401 AUDITING IN A COMPUTER INFORMATION SYSTEMS ENVIRONMENT CONTENTS

INTERNATIONAL STANDARD ON AUDITING 401 AUDITING IN A COMPUTER INFORMATION SYSTEMS ENVIRONMENT (This Standard is effective, but will be withdrawn when ISA 315 and 330 become effective) * CONTENTS Paragraph

INTERNATIONAL STANDARD ON AUDITING 401 AUDITING IN A COMPUTER INFORMATION SYSTEMS ENVIRONMENT (This Standard is effective, but will be withdrawn when ISA 315 and 330 become effective) * CONTENTS Paragraph

Audit Quality Thematic Review

Thematic Review Professional discipline Financial Reporting Council December 2014 Audit Quality Thematic Review The audit of loan loss provisions and related IT controls in banks and building societies

Thematic Review Professional discipline Financial Reporting Council December 2014 Audit Quality Thematic Review The audit of loan loss provisions and related IT controls in banks and building societies

STANDING ADVISORY GROUP MEETING

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202)862-8430 www.pcaobus.org STANDING ADVISORY GROUP MEETING AUDIT CONFIRMATIONS APRIL 2, 2009 Introduction Confirmations

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202)862-8430 www.pcaobus.org STANDING ADVISORY GROUP MEETING AUDIT CONFIRMATIONS APRIL 2, 2009 Introduction Confirmations

Addressing Disclosures in the Audit of Financial Statements

Exposure Draft May 2014 Comments due: September 11, 2014 Proposed Changes to the International Standards on Auditing (ISAs) Addressing Disclosures in the Audit of Financial Statements This Exposure Draft

Exposure Draft May 2014 Comments due: September 11, 2014 Proposed Changes to the International Standards on Auditing (ISAs) Addressing Disclosures in the Audit of Financial Statements This Exposure Draft

70-671. Designing and Providing Microsoft Volume Licensing Solutions to. Small and Medium Organizations Exam. http://www.examskey.com/70-671.

Microsoft 70-671 Designing and Providing Microsoft Volume Licensing Solutions to Small and Medium Organizations Exam TYPE: DEMO http://www.examskey.com/70-671.html Examskey Microsoft70-671 exam demo product

Microsoft 70-671 Designing and Providing Microsoft Volume Licensing Solutions to Small and Medium Organizations Exam TYPE: DEMO http://www.examskey.com/70-671.html Examskey Microsoft70-671 exam demo product

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities. Volume 1 Core Concepts Second Edition

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1 Core Concepts Second Edition Small and Medium Practices Committee International Federation

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1 Core Concepts Second Edition Small and Medium Practices Committee International Federation

ISA 200, Overall Objective of the Independent Auditor, and the Conduct of an Audit in Accordance with International Standards on Auditing

International Auditing and Assurance Standards Board Exposure Draft April 2007 Comments are requested by September 15, 2007 Proposed Revised and Redrafted International Standard on Auditing ISA 200, Overall

International Auditing and Assurance Standards Board Exposure Draft April 2007 Comments are requested by September 15, 2007 Proposed Revised and Redrafted International Standard on Auditing ISA 200, Overall

The purpose of internal control within the Cegedim Group are based on the following topics:

CHAIRMAN OF THE BOARD OF DIRECTORS REPORT ON THE PREPARATION AND ORGANIZATION OF THE BOARD S WORK AND ON THE INTERNAL CONTROL PROCEDURES IMPLEMENTED BY THE COMPANY INTERNAL CONTROL PROCEDURES Purpose of

CHAIRMAN OF THE BOARD OF DIRECTORS REPORT ON THE PREPARATION AND ORGANIZATION OF THE BOARD S WORK AND ON THE INTERNAL CONTROL PROCEDURES IMPLEMENTED BY THE COMPANY INTERNAL CONTROL PROCEDURES Purpose of

EU Project N MARKT/2007/15/F LOT 2

EU Project N MARKT/2007/15/F LOT 2 Evaluation of the differences between International Standards on Auditing (ISA) and the standards of the US Public Company Accounting Oversight Board (PCAOB) Maastricht

EU Project N MARKT/2007/15/F LOT 2 Evaluation of the differences between International Standards on Auditing (ISA) and the standards of the US Public Company Accounting Oversight Board (PCAOB) Maastricht

The Audit Plan for West Mercia Energy Joint Committee

The Audit Plan for West Mercia Energy Joint Committee Year ended 31 March 2015 16th February 2015 Jon Roberts Partner T 0121 232 5410 E [email protected] Andrew Davies Manager T 0121 232 5417 E [email protected]

The Audit Plan for West Mercia Energy Joint Committee Year ended 31 March 2015 16th February 2015 Jon Roberts Partner T 0121 232 5410 E [email protected] Andrew Davies Manager T 0121 232 5417 E [email protected]

ANNEX VI MODEL TERMS OF REFERENCE FOR THE CERTIFICATE ON THE FINANCIAL STATEMENTS PART ï

'4. J ' S., --t r - i^v. ^l- ' 1 I Version of 18.11.2013 EUROPEAN COMMISSION DIRECTORATE-GENERAL FOR EDUCATION AND CULTURE Lifelong learning: higher education and international affairs Cooperation and

'4. J ' S., --t r - i^v. ^l- ' 1 I Version of 18.11.2013 EUROPEAN COMMISSION DIRECTORATE-GENERAL FOR EDUCATION AND CULTURE Lifelong learning: higher education and international affairs Cooperation and

Audit Documentation 2029. See section 9339 for interpretations of this section.

Audit Documentation 2029 AU Section 339 Audit Documentation (Supersedes SAS No. 96.) Source: SAS No. 103. See section 9339 for interpretations of this section. Effective for audits of financial statements

Audit Documentation 2029 AU Section 339 Audit Documentation (Supersedes SAS No. 96.) Source: SAS No. 103. See section 9339 for interpretations of this section. Effective for audits of financial statements

Annual Assessment of the External Auditor

Annual Assessment of the External Auditor TOOL FOR AUDIT COMMITTEES January 2014 ENHANCING AUDIT QUALITY AUDIT COMMITTEES iii Table of Contents Introduction 1 1. Determine the scope, timing and process

Annual Assessment of the External Auditor TOOL FOR AUDIT COMMITTEES January 2014 ENHANCING AUDIT QUALITY AUDIT COMMITTEES iii Table of Contents Introduction 1 1. Determine the scope, timing and process

Strategy for 2015 2019: Fulfilling Our Public Interest Mandate in an Evolving World

The IAASB s Strategy for 2015 2019 December 2014 International Auditing and Assurance Standards Board Strategy for 2015 2019: Fulfilling Our Public Interest Mandate in an Evolving World This document was

The IAASB s Strategy for 2015 2019 December 2014 International Auditing and Assurance Standards Board Strategy for 2015 2019: Fulfilling Our Public Interest Mandate in an Evolving World This document was

International Standards on Auditing (ISA) and their Use for Second Level Control of European Territorial Cooperation Programmes

and their Use for Second Level Control of European Territorial Cooperation Programmes") International Standards on Auditing (ISA) and their Use for Second Level Control of European Territorial Cooperation Programmes by Susanne Volz, Financial Control Expert The Programming Period 2007-2013

International Standards on Auditing (ISA) and their Use for Second Level Control of European Territorial Cooperation Programmes by Susanne Volz, Financial Control Expert The Programming Period 2007-2013

University Hospital Southampton NHS Foundation Trust

University Hospital Southampton NHS Foundation Trust EDGE was developed within the National Cancer Research Network in 2000 as an information system solution to help front line clinical research staff

University Hospital Southampton NHS Foundation Trust EDGE was developed within the National Cancer Research Network in 2000 as an information system solution to help front line clinical research staff

GIEK in 2010: Records, risk and limited resources. Wenche Nistad

The year 10 GIEK in 2010: Records, risk and limited resources «GIEK s revenues from premiums and fees passed NOK 1 billion in 2010. This proves that there is a great need for our services, and that GIEK

The year 10 GIEK in 2010: Records, risk and limited resources «GIEK s revenues from premiums and fees passed NOK 1 billion in 2010. This proves that there is a great need for our services, and that GIEK

Office of the Auditor General Western Australia. Audit Practice Statement

Office of the Auditor General Western Australia Audit Practice Statement Office of the Auditor General Western Australia 7th Floor Albert Facey House 469 Wellington Street Perth Mailing Address Perth BC

Office of the Auditor General Western Australia Audit Practice Statement Office of the Auditor General Western Australia 7th Floor Albert Facey House 469 Wellington Street Perth Mailing Address Perth BC

Auditing Standard ASA 600 Special Considerations Audits of a Group Financial Report (Including the Work of Component Auditors)

") ASA 600 (October 2009) Auditing Standard ASA 600 Special Considerations Audits of a Group Financial Report (Including the Work of Component Auditors) Issued by the Auditing and Assurance Standards Board

ASA 600 (October 2009) Auditing Standard ASA 600 Special Considerations Audits of a Group Financial Report (Including the Work of Component Auditors) Issued by the Auditing and Assurance Standards Board

Enhancing the Corporate Financial Reporting Infrastructure in Poland Henri Fortin, Head, CFRR

Enhancing the Corporate Financial Reporting Infrastructure in Poland Henri Fortin, Head, CFRR KIBR Annual Auditing Conference 26 October 2011 Poland Financial Reporting Technical Assistance Program (FRTAP)

Enhancing the Corporate Financial Reporting Infrastructure in Poland Henri Fortin, Head, CFRR KIBR Annual Auditing Conference 26 October 2011 Poland Financial Reporting Technical Assistance Program (FRTAP)

Auditing Standard ASA 330 The Auditor's Responses to Assessed Risks

ASA 330 (October 2009) Auditing Standard ASA 330 The Auditor's Responses to Assessed Risks Issued by the Auditing and Assurance Standards Board Obtaining a Copy of this Auditing Standard This Auditing

ASA 330 (October 2009) Auditing Standard ASA 330 The Auditor's Responses to Assessed Risks Issued by the Auditing and Assurance Standards Board Obtaining a Copy of this Auditing Standard This Auditing

Guidance Statement GS 007 Audit Implications of the Use of Service Organisations for Investment Management Services

GS 007 (March 2008) Guidance Statement GS 007 Audit Implications of the Use of Service Organisations for Investment Management Services Issued by the Auditing and Assurance Standards Board Obtaining a

GS 007 (March 2008) Guidance Statement GS 007 Audit Implications of the Use of Service Organisations for Investment Management Services Issued by the Auditing and Assurance Standards Board Obtaining a

Chapter 5- External I-9 Attorney Audits

Chapter 5- External I-9 Attorney Audits 5.0 The External I-9 Audit The private external compliance audit contains the Form I-9 audit, the compliance program audit (Chapter 6) the liability audit (Chapter

Chapter 5- External I-9 Attorney Audits 5.0 The External I-9 Audit The private external compliance audit contains the Form I-9 audit, the compliance program audit (Chapter 6) the liability audit (Chapter

Plan for the audit of the 2011 financial statements

INTERNATIONAL TRAINING CENTRE OF THE ILO Board of the Centre 73rd Session, Turin, 3-4 November 2011 CC 73/5/2 FOR INFORMATION FIFTH ITEM ON THE AGENDA Plan for the audit of the 2011 financial statements

INTERNATIONAL TRAINING CENTRE OF THE ILO Board of the Centre 73rd Session, Turin, 3-4 November 2011 CC 73/5/2 FOR INFORMATION FIFTH ITEM ON THE AGENDA Plan for the audit of the 2011 financial statements

FusionRisk Regulation Software overview. A complete solution to changing regulatory challenges. Stay on top of the compliance game

FusionRisk Regulation Software overview A complete solution to changing regulatory challenges Stay on top of the compliance game FusionRisk enabled us to draw a full circle between asset liability management,

FusionRisk Regulation Software overview A complete solution to changing regulatory challenges Stay on top of the compliance game FusionRisk enabled us to draw a full circle between asset liability management,

[300] Accounting and internal control systems and audit risk assessments

![[300] Accounting and internal control systems and audit risk assessments](/thumbs/25/6464424.jpg "[300] Accounting and internal control systems and audit risk assessments") [300] Accounting and internal control systems and audit risk assessments (Issued March 1995) Contents Paragraphs Introduction 1 12 Inherent risk 13 15 Accounting system and control environment 16 23 Internal

[300] Accounting and internal control systems and audit risk assessments (Issued March 1995) Contents Paragraphs Introduction 1 12 Inherent risk 13 15 Accounting system and control environment 16 23 Internal

Gjensidige in brief. Attractive position in Nordic GI. Balanced retail portfolio. Private and SME exposure 80 % direct distribution

1 Gjensidige in brief Attractive position in Nordic GI Balanced retail portfolio Accident & Health 21% Motor 33% Property 36% 200 years history Earned premiums : NOK bn 19 Equity: NOK bn 26 Market cap:

1 Gjensidige in brief Attractive position in Nordic GI Balanced retail portfolio Accident & Health 21% Motor 33% Property 36% 200 years history Earned premiums : NOK bn 19 Equity: NOK bn 26 Market cap:

Paper F8 (INT) Audit and Assurance (International) Thursday 5 December 2013. Fundamentals Level Skills Module

Audit and Assurance (International) Thursday 5 December 2013. Fundamentals Level Skills Module") Fundamentals Level Skills Module Audit and Assurance (International) Thursday 5 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be

Fundamentals Level Skills Module Audit and Assurance (International) Thursday 5 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be

Planning an Audit 255

Planning an Audit 255 AU-C Section 300 Planning an Audit Source: SAS No. 122; SAS No. 128. Effective for audits of financial statements for periods ending on or after December 15, 2012. Introduction Scope

Planning an Audit 255 AU-C Section 300 Planning an Audit Source: SAS No. 122; SAS No. 128. Effective for audits of financial statements for periods ending on or after December 15, 2012. Introduction Scope

INTERNATIONAL STANDARD ON AUDITING 230 AUDIT DOCUMENTATION CONTENTS

INTERNATIONAL STANDARD ON AUDITING 230 AUDIT DOCUMENTATION (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction Scope of this

INTERNATIONAL STANDARD ON AUDITING 230 AUDIT DOCUMENTATION (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction Scope of this

Risikobaseret tilgang til revision

Risikobaseret tilgang til revision Hvordan får vi egentlig forholdt os praktisk til ISA 315? v/henrik Nørgaard & Thomas Kühn Structure of the Global Audit Methodology September 2013 Page 2 Phase 1 Planning

Risikobaseret tilgang til revision Hvordan får vi egentlig forholdt os praktisk til ISA 315? v/henrik Nørgaard & Thomas Kühn Structure of the Global Audit Methodology September 2013 Page 2 Phase 1 Planning

The Terms of Reference should be completed by the Beneficiary and be agreed with the Auditor

ANNEX V-A FORM - TERMS OF REFERENCE FOR THE CERTIFICATE OF FINANCIAL STATEMENTS TABLE OF CONTENTS TERMS OF REFERENCE FOR AN INDEPENDENT REPORT OF FACTUAL FINDINGS ON COSTS CLAIMED UNDER A ERC GRANT AGREEMENT

ANNEX V-A FORM - TERMS OF REFERENCE FOR THE CERTIFICATE OF FINANCIAL STATEMENTS TABLE OF CONTENTS TERMS OF REFERENCE FOR AN INDEPENDENT REPORT OF FACTUAL FINDINGS ON COSTS CLAIMED UNDER A ERC GRANT AGREEMENT

Upgrading from VAM/SQL MS303 to VAM/SQL MS401

Upgrading from VAM/SQL MS303 to VAM/SQL MS401 First Release: April, 1999 The information contained in this document represents the current view of AccountMate Software Corporation on the issues discussed

Upgrading from VAM/SQL MS303 to VAM/SQL MS401 First Release: April, 1999 The information contained in this document represents the current view of AccountMate Software Corporation on the issues discussed

COMMUNICATIONS WITH AUDIT COMMITTEES OVERVIEW OF PCAOB AUDITING STANDARD NO. 16

FEBRUARY 2013 www.bdo.com AN OFFERING FROM BDO S CORPORATE GOVERNANCE PRACTICE BDO USA CORPORATE GOVERNANCE PRACTICE BDO USA s Corporate Governance Practice was developed to provide guidance to corporate

FEBRUARY 2013 www.bdo.com AN OFFERING FROM BDO S CORPORATE GOVERNANCE PRACTICE BDO USA CORPORATE GOVERNANCE PRACTICE BDO USA s Corporate Governance Practice was developed to provide guidance to corporate

Act of 5 July 2002 No. 64 on the Registration of Financial Instruments (Securities Register Act)

") FINANSTILSYNET Norway Translation update: November 2014 This translation is for information purposes only. Legal authenticity remains with the official Norwegian version as published in Norsk Lovtidend.

FINANSTILSYNET Norway Translation update: November 2014 This translation is for information purposes only. Legal authenticity remains with the official Norwegian version as published in Norsk Lovtidend.

Algeta includes a Corporate Governance review in its annual report and has implemented a set of ethical guidelines.

Corporate governance principles and review As a Norwegian public limited liability company, Algeta is subject to the regulation of the Public Limited Liability Companies Act of 1997, as amended (the Act

Corporate governance principles and review As a Norwegian public limited liability company, Algeta is subject to the regulation of the Public Limited Liability Companies Act of 1997, as amended (the Act

Application of software tools during audits. Ing. Martin Lejsal September 2011

Application of software tools during audits. Ing. Martin Lejsal September 2011 1.1Introduction of software tools CIS Control information system (CIS) supports: planning of the audits realization of the

Application of software tools during audits. Ing. Martin Lejsal September 2011 1.1Introduction of software tools CIS Control information system (CIS) supports: planning of the audits realization of the

Data sheet. MainManager IT

Data sheet MainManager IT Mainmanger IT is helping IT Managers and other IT responsible in companies, municipalities and organisations to plan and increase the return of investments in IT equipment. This

Data sheet MainManager IT Mainmanger IT is helping IT Managers and other IT responsible in companies, municipalities and organisations to plan and increase the return of investments in IT equipment. This

Auditing Module 7 June 2009. Suggested Solutions

Auditing Module 7 June 2009 Suggested Solutions 1 Question 1 1. Tests of control are tests carried out to obtain assurance about the operating and effectiveness of controls. An example of such a test would

Auditing Module 7 June 2009 Suggested Solutions 1 Question 1 1. Tests of control are tests carried out to obtain assurance about the operating and effectiveness of controls. An example of such a test would

ISSAI 1300. Planning an Audit of Financial Statements. Financial Audit Guideline

The International Standards of Supreme Audit Institutions, ISSAI, are issued by the International Organization of Supreme Audit Institutions, INTOSAI. For more information visit www.issai.org. Financial

The International Standards of Supreme Audit Institutions, ISSAI, are issued by the International Organization of Supreme Audit Institutions, INTOSAI. For more information visit www.issai.org. Financial

BOARD OF AUDITORS ANNUAL REPORT TO THE BOARD OF GOVERNORS

BOARD OF AUDITORS ANNUAL REPORT TO THE BOARD OF GOVERNORS for the period ended 31 December 2015 Board of Auditors European Stability Mechanism 2 1. INTRODUCTION The Board of Auditors of the European Stability

BOARD OF AUDITORS ANNUAL REPORT TO THE BOARD OF GOVERNORS for the period ended 31 December 2015 Board of Auditors European Stability Mechanism 2 1. INTRODUCTION The Board of Auditors of the European Stability

Lifetime Investment Service. For the financial year ended 30 June 2013 ARSN 088 043 234. 2013 Annual Report to Members

For the financial year ended 30 June 2013 ARSN 088 043 234 13 2013 Annual Report to Members Directors Report The directors of IOOF Investment Management Limited (ABN 53 006 695 021), the Responsible Entity

For the financial year ended 30 June 2013 ARSN 088 043 234 13 2013 Annual Report to Members Directors Report The directors of IOOF Investment Management Limited (ABN 53 006 695 021), the Responsible Entity

How To Audit A Financial Statement

INTERNATIONAL STANDARD ON 400 RISK ASSESSMENTS AND INTERNAL CONTROL (This Standard is effective, but will be withdrawn when ISA 315 and 330 become effective) * CONTENTS Paragraph Introduction... 1-10 Inherent

INTERNATIONAL STANDARD ON 400 RISK ASSESSMENTS AND INTERNAL CONTROL (This Standard is effective, but will be withdrawn when ISA 315 and 330 become effective) * CONTENTS Paragraph Introduction... 1-10 Inherent

Josephine Mathias. Kenneth J. Horowitz Phone: 609-586-4800 Ext. 3468 e-mail: [email protected]

ACC204 Auditing Administrative Outline Course Information Organization Mercer County Community College Course Number ACC204 Credits 3 Lecture/Lab 3/1 Catalog Description Investigation into and application

ACC204 Auditing Administrative Outline Course Information Organization Mercer County Community College Course Number ACC204 Credits 3 Lecture/Lab 3/1 Catalog Description Investigation into and application

Fundamental Principles of Public-Sector Auditing

ISSAI 100 The International Standards of Supreme Audit Institutions, or ISSAIs, are issued by INTOSAI, the International Organisation of Supreme Audit Institutions. For more information visit www.issai.org

ISSAI 100 The International Standards of Supreme Audit Institutions, or ISSAIs, are issued by INTOSAI, the International Organisation of Supreme Audit Institutions. For more information visit www.issai.org

By Kim Michael Thon Business Development

By Kim Michael Thon Business Development Working Language Deutschsprachige Kontakperson English is the working language Saves costly translations Mitigates risk of mistakes occuring in translation Introduction

By Kim Michael Thon Business Development Working Language Deutschsprachige Kontakperson English is the working language Saves costly translations Mitigates risk of mistakes occuring in translation Introduction

Audit Sampling. AU Section 350 AU 350.05

Audit Sampling 2067 AU Section 350 Audit Sampling (Supersedes SAS No. 1, sections 320A and 320B.) Source: SAS No. 39; SAS No. 43; SAS No. 45; SAS No. 111. See section 9350 for interpretations of this section.

Audit Sampling 2067 AU Section 350 Audit Sampling (Supersedes SAS No. 1, sections 320A and 320B.) Source: SAS No. 39; SAS No. 43; SAS No. 45; SAS No. 111. See section 9350 for interpretations of this section.

ISA 620, Using the Work of an Auditor s Expert. Proposed ISA 500 (Redrafted), Considering the Relevance and Reliability of Audit Evidence

, Considering the Relevance and Reliability of Audit Evidence") International Auditing and Assurance Standards Board Exposure Draft October 2007 Comments are requested by February 15, 2008 Proposed Revised and Redrafted International Standard on Auditing ISA 620, Using

International Auditing and Assurance Standards Board Exposure Draft October 2007 Comments are requested by February 15, 2008 Proposed Revised and Redrafted International Standard on Auditing ISA 620, Using

Corporate governance. 1. Implementation and reporting on corporate governance. 2. IDEX s business. 3. Equity and dividends

Corporate governance Update resolved by the board of directors of IDEX ASA on 16 April 2015. This statement outlines the position of IDEX ASA ( IDEX or the Company ) in relation to the recommendations

Corporate governance Update resolved by the board of directors of IDEX ASA on 16 April 2015. This statement outlines the position of IDEX ASA ( IDEX or the Company ) in relation to the recommendations

INTERNATIONAL STANDARD ON ASSURANCE ENGAGEMENTS 3000 ASSURANCE ENGAGEMENTS OTHER THAN AUDITS OR REVIEWS OF HISTORICAL FINANCIAL INFORMATION CONTENTS

INTERNATIONAL STANDARD ON ASSURANCE ENGAGEMENTS 3000 ASSURANCE ENGAGEMENTS OTHER THAN AUDITS OR REVIEWS OF HISTORICAL FINANCIAL INFORMATION (Effective for assurance reports dated on or after January 1,

INTERNATIONAL STANDARD ON ASSURANCE ENGAGEMENTS 3000 ASSURANCE ENGAGEMENTS OTHER THAN AUDITS OR REVIEWS OF HISTORICAL FINANCIAL INFORMATION (Effective for assurance reports dated on or after January 1,

New Audit Standards: How Will They Impact the Audit

New Audit Standards: How Will They Impact the Audit Process? Presented by Robinson, Farmer, Cox Associates The Commonwealth s premier source of financial expertise since 1953. Presentation Objectives Discuss

New Audit Standards: How Will They Impact the Audit Process? Presented by Robinson, Farmer, Cox Associates The Commonwealth s premier source of financial expertise since 1953. Presentation Objectives Discuss

Auditing Standard ASA 520 Analytical Procedures

ASA 520 (October 2009) Auditing Standard ASA 520 Issued by the Auditing and Assurance Standards Board Obtaining a Copy of this Auditing Standard This Auditing Standard is available on the Auditing and

ASA 520 (October 2009) Auditing Standard ASA 520 Issued by the Auditing and Assurance Standards Board Obtaining a Copy of this Auditing Standard This Auditing Standard is available on the Auditing and

Guide to Accounting Officer Reporting Engagements

Guide to Accounting Officer Reporting Engagements EXPRESSION OF INTEREST FOR TRAINING PROVIDERS TO PROVIDE APPROVED TRAINING PROGRAMMES TO SAICA MEMBERS SOUTHERN AFRICAN INSTITUTE FOR BUSINESS ACCOUNTANTS

Guide to Accounting Officer Reporting Engagements EXPRESSION OF INTEREST FOR TRAINING PROVIDERS TO PROVIDE APPROVED TRAINING PROGRAMMES TO SAICA MEMBERS SOUTHERN AFRICAN INSTITUTE FOR BUSINESS ACCOUNTANTS

European Commission Green Paper on Audit Policy: Lessons from the Crisis. Opinion of the Chamber of Auditors of the Czech Republic

(1) Do you have general remarks on the approach and purposes of this Green Paper? We have no general remarks on the approach of this Green Paper and on its purpose, and we fully support the discussion

(1) Do you have general remarks on the approach and purposes of this Green Paper? We have no general remarks on the approach of this Green Paper and on its purpose, and we fully support the discussion

CITY OF VINCENT. Audit Completion Report to the Audit Committee For the Year Ended 30 June 2015

CITY OF VINCENT Audit Completion Report to the Audit Committee For the Year Ended 30 June 2015 20 November 2015 Table of Contents 1. Executive Summary... 1 1.1 Status of Audit... 1 1.2 Deliverables...

CITY OF VINCENT Audit Completion Report to the Audit Committee For the Year Ended 30 June 2015 20 November 2015 Table of Contents 1. Executive Summary... 1 1.1 Status of Audit... 1 1.2 Deliverables...

Communicating Internal Control Related Matters Identified in an Audit

Communicating Internal Control 1843 AU Section 325 Communicating Internal Control Related Matters Identified in an Audit (Supersedes SAS No. 112.) Source: SAS No. 115. Effective for audits of financial

Communicating Internal Control 1843 AU Section 325 Communicating Internal Control Related Matters Identified in an Audit (Supersedes SAS No. 112.) Source: SAS No. 115. Effective for audits of financial

Technology Partners. Acceleratio Ltd. is a software development company based in Zagreb, Croatia, founded in 2009.

Acceleratio Ltd. is a software development company based in Zagreb, Croatia, founded in 2009. We create innovative software solutions for SharePoint, Office 365, MS Windows Remote Desktop Services, and

Acceleratio Ltd. is a software development company based in Zagreb, Croatia, founded in 2009. We create innovative software solutions for SharePoint, Office 365, MS Windows Remote Desktop Services, and

INTERNATIONAL STANDARD ON AUDITING 250 CONSIDERATION OF LAWS AND REGULATIONS IN AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

INTERNATIONAL STANDARD ON AUDITING 250 CONSIDERATION OF LAWS AND REGULATIONS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction

INTERNATIONAL STANDARD ON AUDITING 250 CONSIDERATION OF LAWS AND REGULATIONS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction

Presented by Vuyelwa Toni Penxa, Samuel Isaacs, Joe Samuels and Mark Albertyn

Presented by Vuyelwa Toni Penxa, Samuel Isaacs, Joe Samuels and Mark Albertyn 1 Positioning The NQF And SAQA Change and Corporate Governance Annual Financial Report Continuity Matters raised previously

Presented by Vuyelwa Toni Penxa, Samuel Isaacs, Joe Samuels and Mark Albertyn 1 Positioning The NQF And SAQA Change and Corporate Governance Annual Financial Report Continuity Matters raised previously

The Auditor General's Act

The Auditor General's Act Consolidation of Consolidating Act No. 3 of 7 January 1997 as amended by Act No. 590 of 13 June 2006 Audit of State Accounts etc (Consolidation) Act 1.- (1) The audit according

The Auditor General's Act Consolidation of Consolidating Act No. 3 of 7 January 1997 as amended by Act No. 590 of 13 June 2006 Audit of State Accounts etc (Consolidation) Act 1.- (1) The audit according

Practice guide. quality assurance and IMProVeMeNt PrograM

Practice guide quality assurance and IMProVeMeNt PrograM MarCh 2012 Table of Contents Executive Summary... 1 Introduction... 2 What is Quality?... 2 Quality in Internal Audit... 2 Conformance or Compliance?...

Practice guide quality assurance and IMProVeMeNt PrograM MarCh 2012 Table of Contents Executive Summary... 1 Introduction... 2 What is Quality?... 2 Quality in Internal Audit... 2 Conformance or Compliance?...

LEGISLATIVE AUDIT DIVISION MEMORANDUM

LEGISLATIVE AUDIT DIVISION Tori Hunthausen, Legislative Auditor Deborah F. Butler, Legal Counsel Deputy Legislative Auditors: Cindy Jorgenson Angie Grove MEMORANDUM TO: FROM: DATE: January 2012 CC: RE:

LEGISLATIVE AUDIT DIVISION Tori Hunthausen, Legislative Auditor Deborah F. Butler, Legal Counsel Deputy Legislative Auditors: Cindy Jorgenson Angie Grove MEMORANDUM TO: FROM: DATE: January 2012 CC: RE:

ISAE 3000 (Revised), Assurance Engagements Other Than Audits or Reviews of Historical Financial Information

, Assurance Engagements Other Than Audits or Reviews of Historical Financial Information") International Auditing and Assurance Standards Board Exposure Draft April 2011 Comments requested by September 1, 2011 Proposed International Standard on Assurance Engagements (ISAE) ISAE 3000 (Revised),

International Auditing and Assurance Standards Board Exposure Draft April 2011 Comments requested by September 1, 2011 Proposed International Standard on Assurance Engagements (ISAE) ISAE 3000 (Revised),

Action Plan Developed by. KHT-yhdistys Finnish Institute of Authorised Public Accountants BACKGROUND NOTE ON ACTION PLANS

Kht-Yhdistys - Finnish of Authorised Public Accountants BACKGROUND NOTE ON ACTION PLANS Action Plans are developed by IFAC members and associates to address policy matters identified through their responses

Kht-Yhdistys - Finnish of Authorised Public Accountants BACKGROUND NOTE ON ACTION PLANS Action Plans are developed by IFAC members and associates to address policy matters identified through their responses

Gjensidige Pensjonsforsikring AS (GPF) Investor presentation. June 2016

Investor presentation. June 2016") Gjensidige Pensjonsforsikring AS (GPF) Investor presentation June 2016 Disclaimer This presentation and the information contained herein have been prepared by and is the sole responsibility of Gjensidige

Gjensidige Pensjonsforsikring AS (GPF) Investor presentation June 2016 Disclaimer This presentation and the information contained herein have been prepared by and is the sole responsibility of Gjensidige

Corporate Governance. Document Request List Funds

Document Request List Funds Please provide documents noted below, as applicable, in English. For new funds or existing funds where requested documents are currently being developed, please provide draft

Document Request List Funds Please provide documents noted below, as applicable, in English. For new funds or existing funds where requested documents are currently being developed, please provide draft

Term Sheet ISIN: NO 0010672827. FRN Marine Harvest ASA Senior Unsecured Open Bond Issue 2013/2018 (the Bonds or the Loan )

") Term Sheet ISIN: NO 0010672827 FRN Marine Harvest ASA Senior Unsecured Open Bond Issue 2013/2018 (the Bonds or the Loan ) Settlement date: Expected to be 12 March 2013 Issuer: Currency: Loan Amount / First

Term Sheet ISIN: NO 0010672827 FRN Marine Harvest ASA Senior Unsecured Open Bond Issue 2013/2018 (the Bonds or the Loan ) Settlement date: Expected to be 12 March 2013 Issuer: Currency: Loan Amount / First

placing people first SALARY REPORT Summary of 2014 Bratislava

placing people first SALARY REPORT Summary of 2014 1 / Cpl Jobs Salary Report Table of content 3 / Summary of 2014 / About Cpl Jobs 4 / IT 7 / Finance 9 / BPO/SSC 2 / Cpl Jobs Salary Report Summary of

placing people first SALARY REPORT Summary of 2014 1 / Cpl Jobs Salary Report Table of content 3 / Summary of 2014 / About Cpl Jobs 4 / IT 7 / Finance 9 / BPO/SSC 2 / Cpl Jobs Salary Report Summary of

Finance and Accounting Control, Record Keeping and Reporting Services

Position Title: Finance Officer Job Description Department: Reports To: Finance Financial Analyst Purpose The Finance Officer is responsible for the maintenance of finance and accounting transactions and

Position Title: Finance Officer Job Description Department: Reports To: Finance Financial Analyst Purpose The Finance Officer is responsible for the maintenance of finance and accounting transactions and