2014 Higher Education Accounting Forum

|

|

|

- Joleen Welch

- 8 years ago

- Views:

Transcription

1 2014 Higher Education Accounting Forum The Accounting of RCM April 28, 2014

2 Conference Session Speakers Name Title Organization Andrew L. Laws Managing Director (session facilitator) Huron Consulting Group (312) Amy Douglas Controller Auburn University (334) Sharon Loiland Controller University of North Dakota (701)

844-3604 douglak@auburn.")

3 Discussion Topics Responsibility Center Management Budget Redesign Efforts University of North Dakota Auburn University Redesign Topics of Interest for Controllers 3

4 Budget Redesign Context From 2008 to 2011, ~20% of institutions and ~25% of doctoral institutions reported new approaches to resource allocation (1) Source: Inside Higher Ed Survey of College & University Business Officers; Huron Consulting Group benchmarking 4

5 Available Resources Publications Curry, et. al: Responsibility Center Management, A Guide to Balancing Academic Entrepreneurship with Fiscal Responsibility (2103) Goldstein: A Guide to College and University Budgeting, Foundations for Institutional Effectiveness (2012) Priest, et. al: Incentive-Based Budgeting Systems in Public Universities (2002) Whalen: Responsibility Center Budgeting: An approach to decentralized management for institutions of higher education (1991) Presentations SACUBO Annual Meeting University of Virginia NACUBO Budget Forum: Drexel University University of Kentucky Texas Tech University NACUBO Annual Meeting University of California, Davis Iowa State University 5

Whalen: Responsibility Center Budgeting: An approach to decentralized management for institutions of")

6 Session Objectives Expand on existing resources by adding a controller s perspective Specific Objectives: Identify common accounting implications Help participants better understand key topics of consideration to share on their campuses Share how other institutions have addressed selected issues 6

7 Incentive-Based Budgeting (RCM)

8 Overview of Budgeting Models Common Budgeting Models 1 Incremental Budgeting Formula Funding Performance Funding Incentive-Based (RCM) Centrally driven Current budget acts as base Increments (decrements) adjust the base Focus is on expenses Used by 60% of institutions Used by 79% of public doctoral institutions Unit-based model Focus on providing equitable funding Unit are input-based Annual fluctuations are driven primarily by the quantity Used by 26% of institutions Used by 45% of public doctoral institutions Unit-based model Focus on rewarding mission delivery Unit rates are output based Annual fluctuations are driven primarily by changing production Used by 20% of institutions Used by 26% of public doctoral institutions Focus on academic units Devolves revenue ownership Allocates costs to revenue generating units Utilizes a centrally managed subvention pool Used by 14% of institutions Used by 21% of public doctoral institutions (1) Adoption rates from the 2011 Inside Higher Education Survey of College and University Business Officers; Percentages do not add to 100% due to hybrid budgeting models 8

9 Incentive-Based Budgeting Spectrum Contemporary RCM Higher degree of central control Incentive-Based Budget Model Iterations Traditional RCM Some centralized control Each Tub on its Own Bottom (ETOB) Extremely de-centralized model Local units keep a majority of their revenue but pay a higher subvention tax Through increased tax revenue, central administration has greater ability to subsidize colleges and fund strategic initiatives Higher tax rates, typically between 15 and 20% (in addition to indirect cost rates) Most commonly implemented since 2005 Local units keep most of the revenue they generate, but give up some to a central pool through a subvention tax paid Taxes generated can be used by the central administration to subsidize colleges and fund strategic initiatives Tax rates are generally less than 10% (in addition to indirect cost rates) Most frequently implemented from 1990 to 2004 Academic units essentially operate as their own financial entities Very little central strategic control Under-performing units must cut costs or generate more revenue to cover any losses incurred Few U.S. institutions use this extreme iteration 9

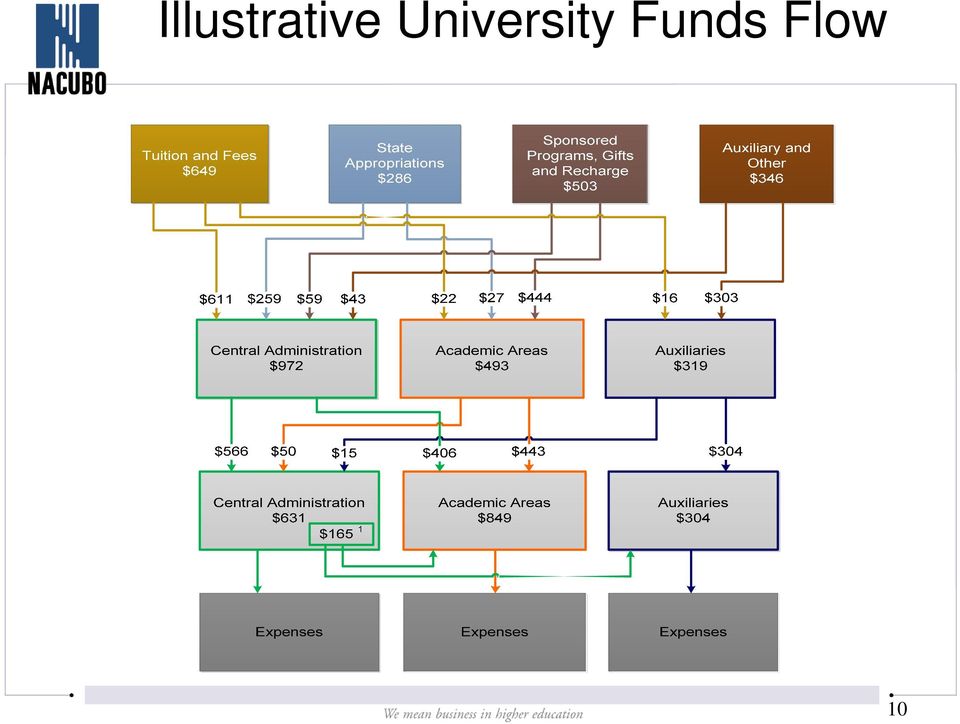

10 Illustrative University Funds Flow 10

11 Illustrative RCM Funds Flow 11

12 University of North Dakota

13 University of North Dakota Institution Overview FY13 Operating Expenditures: $423.8 million Number of Colleges: 8 Number of Students: 15,143 University Designations: Carnegie Classification: Public Space Grant High research Current Budget Model: Time in Budget Model Redesign: Incremental 8 months 13

14 University of North Dakota Implementation Overview The University of North Dakota began a budget model redesign initiative in August UND has completed a preliminary pro forma model, and is currently engaged in stakeholder outreach and consensus building. The model development support team has included representatives from the Budget Office, CIO Office, Controller s Office, and Facilities Management. 14

15 University of North Dakota Illustrative Challenge #1: Fund Selection Goal The model needed to reflect an all-funds, cash operating basis that could be reconciled to the annual financial statement. Challenge Financial activity posted to three ledgers, which comprised actuals, accrual adjustments, and internal adjustments for financial statement purposes. Resolution The Controller s Office identified the appropriate ledger entries to use in the model, while eliminating double counting of revenues and expenses. 15

16 University of North Dakota Illustrative Challenge #2: Revenue Tracking Goal The model needed to track and allocate tuition and fee revenue streams according to revenue source, student residency, and student level. Challenge Tuition and fee revenue posted to a single account code, making differentiation and allocation by student level and residency difficult. Resolution The Controller s Office worked with Office of Institutional Research and the Budget Office to accurately devolve and allocate tuition and fee revenue at the necessary level of detail. 16

17 Auburn University

18 Auburn University Institution Overview FY13 Operating Expenditures: $885.7 million Number of Colleges: 12 Number of Students: 29,960 University Designations Carnegie Classification Current Budget Model: Time in Budget Model Redesign: Public Land, Sea & Space Grant High research Incremental 14 months 18

19 Auburn University Implementation Overview Auburn University began a budget model redesign initiative in January Auburn has completed a preliminary pro forma model and stakeholder outreach and consensus building, and is currently engaged in infrastructure development. The model development support team has included the Provost and representatives from the Budget Office, Controller s Office, Office of Institutional Research, Facilities, and Student Financial Services. 19

20 Auburn University Illustrative Challenge #1: Reconciliation to Audited Statement Goal Model revenue and expense totals needed to tie out to the audited financial statement. Challenge All financial statement data needed to be included in the model while still reconciling to the audited financial statement. Resolution Reviewed and discussed year-end accrual entries, elimination entries, reclassification entries, and asset capitalization/depreciation to ensure it was handled appropriately. 20

21 Auburn University Illustrative Challenge #2: Chart of Accounts Alignment Goal The model should accurately reflect expense and revenue activity in the divisions and units where it occurred. Challenge The chart of accounts for select divisions did not align with the main campus chart of accounts. In the initial model development stage, this caused a misalignment of how expenses were classified and posted to select organizational units. Resolution It was necessary to conduct a deep review of the chart of accounts for select divisions and correct the points of misalignment to ensure consistency in reporting in future years. 21

22 Auburn University Illustrative Challenge #3: Revenue Tracking Goal The model needed to differentiate between sources of tuition and fee revenue to ensure appropriate allocation methodologies could be used. Challenge Tuition and fees are tracked in detail in a separate system, but are only distinguished by residency status in the general ledger. Resolution Crosswalks were developed so that tuition and fees could be devolved to the appropriate level of detail. The Controller s Office is now investigating the development of a reporting function that will automate the process in future years. 22

23 Additional Questions/Topics

24 Additional Questions/Topics 1. What is the scope of funds? 2. How does revenue tracking change? 3. How does expense tracking change? 4. What are the cost allocation assumptions? 5. How are recharges handled? 6. How is building depreciation handled? 7. How are fund balances incorporated? 8. How do reporting expectations change? 9. How are taxes used to generate central funds? 10. Do funds flow in real-time? 24

25 (1) Scope of Funds Decentralized budgets are generally managed on an all-funds, cash operating basis. The all-funds approach routinely includes general, direct and indirect research, auxiliary, and gift funds. Assumes that optimal decisions cannot be made unless all resources are considered Revenue focus through attempt to de-color money Accrual entries and other financial reporting adjustments are still necessary for external reporting Foundations are typically excluded 25

26 Scope of Funds Illustrative College XYZ Current Designated Restricted Sponsored Total Revenues Student Fees $ 3,213,294 $ 177,155 $ - $ - $ 3,390,449 Net Undergraduate Tuition 77,760, ,760,104 Net Graduate Tuition 6,872, ,872,270 DeL Tuition 3,874, ,874,246 Other Tuition - 3,447, ,447,890 Student Tuition and Fees 95,914,528 3,625, ,539,573 Federal Grants and Contracts ,948,437 7,948,437 State Grants and Contracts , ,085 Other Grants and Contracts , ,390 Grants and Contracts Overhead 2,408,463 Revenue from affiliates - 13, ,206 Private gifts 5,000 N/A 198,697 N/A 203,697 Endow ment income , ,058 Investment income Other income - 91, ,205 Total Revenues 95,919,528 3,729, ,755 9,276, ,043,188 Revised Budget Focus Traditional Budget Focus Expenses Faculty Salaries $ 22,912,087 $ 1,733,828 $ 194,809 $ 1,258,249 $ 26,098,973 Non-Faculty Salaries 3,922,872 1,427, ,651 1,360,506 6,887,455 Student Salaries 3,177, ,962 36, ,152 4,216,971 Other Salaries 3, ,383 Fringe Benefits 7,243, ,656 97, ,442 8,857,131 Compensation Total 37,259,237 4,094, ,455 4,204,349 46,063,913 General Expenses 2,209, , ,609 4,108,702 7,004,586 Expense Recovery 15,789 (167,347) (10,075) (521,078) (682,712) Patient Care Activities ,607 2,698 Purchased Services 120, ,707 9, ,834 1,176,737 Tuition Remission & Restricted Scholarships 2,097,883 36, , ,628 2,623,056 Debt Service 2,752, ,752,730 Rent Payment - Tenet 190, ,868 Transfers 379,659 (379,659) Adjustments (1,224) Total Expenses 45,026,191 4,365, ,754 9,030,042 59,130,652 Unit Margin Before A&S Allocations $ 50,893,337 $ (636,628) $ 1 $ 246,140 $ 52,912,536 26

27 (2) Revenue Tracking Schools and colleges earn tuition and fee revenue through instruction and enrollment of students. The chart of accounts should allow revenue intended for specific functions or campus units to post directly to the recipients. Algorithms must be created for non-specific revenues This facilitates opportunities to study margins, leading to more informed decision-making Differential fees/tuition may eventually be introduced to help offset high costs of certain disciplines 27

28 Revenue Tracking Illustrative Direct Tuition Revenue Tuition revenues for programs tracked specifically within academic units are identified within the general ledger Those revenues are directly assigned to the appropriate academic unit General Tuition Revenue The general tuition revenue pool is divided according to the proposed instruction-record split Sub-grouping allocated according to the academic unit s share of either instructed or enrolled credit hours Academic Unit Direct Tuition Revenue General Tuition Revenue 25% Record 75% Instruction 28

29 (3) Expense Tracking Limited change is needed for expense tracking, though direct allocations are generally encouraged. The chart of accounts should support detailed expense reporting needed to understand unit operations. Treatment of centrally-born expenses may change: - Ex: centrally-paid fringe benefits Allocations should not create perverse incentives: - Ex: May be preferential to allocate undergraduate scholarships on an average basis to avoid any financial need biases. 29

30 (4) Cost Allocations Administrative & Support Unit net expenses are charged out to primary units based on select variables. Number of cost pools should be carefully considered Common allocation variables include share of direct expenses, square footage, and student headcount. Number of pools and allocation variables should attempt to balance simplicity with economic reality Indirect allocations may not match existing overhead assessment rates, which generally do not reflect the full net cost of A&S unit operations. 30

31 Cost Allocations Illustrative Few Number of Pools Many Simple Increases transparency Drives academic focus to revenues Provides flexibility to central administration Avoids functional witch-hunts Reduces time spent in committees Reduces perception of allocating uncontrollable costs Supports implementation buy-in Closer approximation of economic reality Provides functional accountability Connects costs and service levels Allows adjustments to balance start points 31

32 (5) Recharges Recharges are often in place to supplement the cost of administrative and support unit. Recharges should be used when: Free nature of a good results in over-consumption Service accrues disproportionately to one group Service is deemed unwarranted, or is not in demand, by all units Service-level agreements are negotiated annually to ensure all units understand core services covered by indirect cost allocations. The chart of accounts must be able to accurately track additional non-core services charged by administrative and support units. 32

33 Allocation/Recharges Illustrative Illustrative Allocation: Square Footage (SQFT) Facilities square feet allocated evenly by square foot occupancy Allocated costs are net of unit revenues Illustrative allocation formula : Allocation PU n SQFTPU n = SU n SUn SQFTPU Sum of all n ( Revenues Expenditures ) Primary Unit s share of square feet Support Unit s margin or (net expenditures) Allocation Formula Notes: PU = Primary Unit; SU = Support Unit For PUn, n represents each individual primary unit (academic units, centers & institutes, auxiliaries) 33

34 (6) Building Depreciation Allocation of building depreciation commonly serves as a proxy for deferred maintenance. Depreciation is often the only non-cash expense allocated as part of decentralized models Allocation is needed to reflect the changing expectations for space quality, which come with space charges If deferred maintenance costs are not traditionally funded, the allocation of depreciation may need to be phased-in, ensuring against the introduction of a new expense 34

35 (7) Fund Balances Colleges are allowed to carry-forward funds balances and must accrue liabilities for negative bottom lines. Fund balances should be incorporated into annual budget conversations. Build up of local fund balances is encouraged. These funds should be considered substitutes for central resources. Capital budgets should be integrated with both operating budgets and plans for fund balances. 35

36 (8) Reporting Expectations Increased accountability typically creates a need for more frequent, timely, detailed, and accurate reporting. Unit-level budget-to-actuals reports should be produced regularly to track budget performance. Deans may need department-level financial details to effectively manage and forecast budget performance. Demand increases for clean, useful, and easy-toaccess financial and non-financial (e.g. credit hours, enrollment, square footage) data, potentially requiring new systems to facilitate access. 36

37 (9) Taxation Central revenues are often generated through revenue taxes on college-level funds. Tax receipts create central funds known as a subvention fund. Taxes should draw upon a diverse portfolio of revenues, while acknowledging taxation restrictions. The tax rate and size of the subvention fund should be large enough to enable leadership to steer the University and provide neutral starting points at implementation. 37

38 Taxation Illustrative Commonly Taxed Revenues Undergraduate Tuition Graduate and Professional Tuition Program and Course Fees General State Appropriations Indirect Cost Recovery (F & A Distribution) Investment Income Sales and Services Auxiliary Enterprises Other Revenue Commonly Excluded Revenues Grants and Contracts Direct State Appropriations Gifts Mandatory Student Fees Endowment Earned Income Distribution Pass-through monies (e.g. Pell Grants) 38

39 (10) Timing Decisions must be made with regard to the timing of revenue and expense allocations. Some institutions opt for the allocation of revenues in real-time, to maximize rewards, while others implement smoothing rules Administrative cost allocations are typically based on budgeted expenses and historical consumption proxies (drivers) 39

40 Timing Illustrative Considerations How quickly should leadership behavior changes be rewarded? Should drivers include projections as part of multi-year averages? Should end of year adjustments be made to more accurately portray economic reality? Should drivers be updated from budget process planning at the beginning of fiscal year operations? 40

41 Concluding Thoughts

42 Impact on Decision Making Incentive-based models have the potential to change institutions by changing the culture of decision making. President s Executive Council: remove luxury of all things to all people by forcing difficult decisions President, Provost, and VP for Finance and Operations: force clarity regarding priorities and strategic initiatives Deans: know the full-cost of activities (academic programs, research, etc.) and prioritize them through cross-subsidies between their revenue generating activities and their mission-driven activities Administrative Units: connect service levels and resource levels Department Chairs and Faculty Members: see how activities drive funding for their respective units 42

43 Controller s Office Controllers serve in key leadership and accountability roles as the models are developed and implemented. Controllers should be consulted from the start of the model development phase to ensure an accurate scope of funds are considered. Controllers routinely serve on budget steering committees to help set and review annual budgets and budget performance. The Controller s Office reports on budget-to-actuals performance and helps school business officers develop more accurate projections. 43

44 Review of Discussion Items Topic Scope of Funds Revenue Tracking Reporting Expectations Timing Cost Allocations Depreciation Fund Balances Taxes Expense Tracking Recharges Impact of Change High High High High Moderate Moderate Moderate Moderate Low Low 44

45 Concluding Thoughts 1. Institutional strategy must drive budget model, do not let budget model drive strategy. 2. Must balance simplicity with economic reality. 3. Some chart of accounts updates may be needed to accurately capture and account for revenue generation. 4. Budget models are often managed via Microsoft Excel, with no impact to general ledger reporting / accounting. 5. Decentralized models promote accountability, which requires enhanced tools and may have material impacts for management reporting. 45

Budget Model Redesign Initiative Stakeholder Discussions

Budget Model Redesign Initiative Stakeholder Discussions February 18, 2014 University of Memphis Budget Redesign Why should the University of Memphis Explore a budget model redesign? Financial Challenges

Budget Model Redesign Initiative Stakeholder Discussions February 18, 2014 University of Memphis Budget Redesign Why should the University of Memphis Explore a budget model redesign? Financial Challenges

Provost Town Hall October 20, 2015

Provost Town Hall October 20, 2015 Facts and Figures 17,458 full-time undergraduate students, including 764 in the AA program; 764 parttime Full-time population is 39% Delaware residents and 61% nonresidents

Provost Town Hall October 20, 2015 Facts and Figures 17,458 full-time undergraduate students, including 764 in the AA program; 764 parttime Full-time population is 39% Delaware residents and 61% nonresidents

Incentive-based Budgeting (IBB) First meeting of the IBB Steering Committee September 2013 D. Rosowsky and A. Citarella

First meeting of the IBB Steering Committee September 2013 D. Rosowsky and A. Citarella") Incentive-based Budgeting (IBB) First meeting of the IBB Steering Committee September 2013 D. Rosowsky and A. Citarella 1 David Rosowsky Provost Alberto Citarella Budget Director David Rosowsky Provost

Incentive-based Budgeting (IBB) First meeting of the IBB Steering Committee September 2013 D. Rosowsky and A. Citarella 1 David Rosowsky Provost Alberto Citarella Budget Director David Rosowsky Provost

Budgeting and Planning Process

Budgeting and Planning Process Summary The budget is an important annual planning document for the university and reflects choices, priorities and tactics set forth as the result of intensive planning.

Budgeting and Planning Process Summary The budget is an important annual planning document for the university and reflects choices, priorities and tactics set forth as the result of intensive planning.

Budget 101: RCM Budget Orientation

Budget 101: RCM Budget Orientation 1 Guiding Principles The following set of principles will guide the implementation and application of Responsibility Center Management (RCM) at Ohio University. These

Budget 101: RCM Budget Orientation 1 Guiding Principles The following set of principles will guide the implementation and application of Responsibility Center Management (RCM) at Ohio University. These

Financial Planning in an Uncertain Environment

Financial Planning in an Uncertain Environment Business Officers of Nursing Schools Annual Meeting, April 26, 2012 Christine Ash VP for University Planning & Institutional Research Case Western Reserve

Financial Planning in an Uncertain Environment Business Officers of Nursing Schools Annual Meeting, April 26, 2012 Christine Ash VP for University Planning & Institutional Research Case Western Reserve

Planning and Budget Process

Planning and Budget Process The University s planning framework, The Highest Order of Excellence II, is the framework for strategic planning at all levels of the institution. Oversight for the strategic

Planning and Budget Process The University s planning framework, The Highest Order of Excellence II, is the framework for strategic planning at all levels of the institution. Oversight for the strategic

Presentation of Simplified Method for Preparing the Facilities and Administrative Cost Rate Proposal. Jason Guilbeault, Senior Consultant

Presentation of Simplified Method for Preparing the Facilities and Administrative Cost Rate Proposal Jason Guilbeault, Senior Consultant MAXIMUS, 2014 Agenda 1. What is the Facilities and Administrative

Presentation of Simplified Method for Preparing the Facilities and Administrative Cost Rate Proposal Jason Guilbeault, Senior Consultant MAXIMUS, 2014 Agenda 1. What is the Facilities and Administrative

BEST PRACTICES IN COMMUNITY COLLEGE BUDGETING

BEST PRACTICES IN COMMUNITY COLLEGE BUDGETING 6B Allocate Costs of Shared Support Services to Subunits to Better Understand the True Cost of Offering Services SUMMARY Key Points: Support services and facilities

BEST PRACTICES IN COMMUNITY COLLEGE BUDGETING 6B Allocate Costs of Shared Support Services to Subunits to Better Understand the True Cost of Offering Services SUMMARY Key Points: Support services and facilities

RCM at Rutgers, The State University of New Jersey

Rutgers Investor Update 12-18-13 2.ppt\16 DEC 2013\7:05 PM\1 RCM at Rutgers, The State University of New Jersey APLU CIMA Summer Meeting July 13, 2015 J. Michael Gower Senior Vice President for Finance

Rutgers Investor Update 12-18-13 2.ppt\16 DEC 2013\7:05 PM\1 RCM at Rutgers, The State University of New Jersey APLU CIMA Summer Meeting July 13, 2015 J. Michael Gower Senior Vice President for Finance

CALIFORNIA STATE UNIVERSITY, SAN MARCOS. Financial Statements. June 30, 2005 and 2004. (With Independent Auditors Report Thereon)

") Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Management s Discussion and Analysis 3 Financial Statements: Statements of Net Assets

Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Management s Discussion and Analysis 3 Financial Statements: Statements of Net Assets

Kirsten Volpi Senior Vice President for Finance and Administration

TO: FROM: Board of Trustees Kirsten Volpi Senior Vice President for Finance and Administration DATE: May 23, 2011 SUBJECT: FY 2012 Budget I. BACKGROUND INFORMATION Fiscal Year 2012 Operating Budget Summary

TO: FROM: Board of Trustees Kirsten Volpi Senior Vice President for Finance and Administration DATE: May 23, 2011 SUBJECT: FY 2012 Budget I. BACKGROUND INFORMATION Fiscal Year 2012 Operating Budget Summary

ABA Budget Discussion

ABA Budget Discussion Executive Vice Chancellor Suresh Subramani Assistant Vice Chancellor Debbie McGraw Director Kathy Farrelly Assistant Vice Chancellor Sylvia Lepe-Askari April 1, 2014 Student-centered,

ABA Budget Discussion Executive Vice Chancellor Suresh Subramani Assistant Vice Chancellor Debbie McGraw Director Kathy Farrelly Assistant Vice Chancellor Sylvia Lepe-Askari April 1, 2014 Student-centered,

Exploring Alternative Budget Models

Business Affairs Forum Exploring Alternative Budget Models Budget Model Review, Transitions, and Outcomes Custom Research Brief eab.com Business Affairs Forum Cate Auerbach Research Associate Lauren Edmonds

Business Affairs Forum Exploring Alternative Budget Models Budget Model Review, Transitions, and Outcomes Custom Research Brief eab.com Business Affairs Forum Cate Auerbach Research Associate Lauren Edmonds

The University of Financial Plan - A Summary

Multi-Year Financial Plan Academic Division FY2015-16 through FY2021-22 1 Multi-Year Financial Plan The accompanying projection has been prepared for the use of the Board of Visitors and administration

Multi-Year Financial Plan Academic Division FY2015-16 through FY2021-22 1 Multi-Year Financial Plan The accompanying projection has been prepared for the use of the Board of Visitors and administration

UNIVERSITY COUNCIL PLANNING AND PRIORITIES COMMITTEE FOR INFORMATION ONLY. Planning and Priorities Committee

AGENDA ITEM NO: 8.2 UNIVERSITY COUNCIL PLANNING AND PRIORITIES COMMITTEE FOR INFORMATION ONLY PRESENTED BY: Bob Tyler, Chair Planning and Priorities Committee DATE OF MEETING: November 15, 2012 SUBJECT:

AGENDA ITEM NO: 8.2 UNIVERSITY COUNCIL PLANNING AND PRIORITIES COMMITTEE FOR INFORMATION ONLY PRESENTED BY: Bob Tyler, Chair Planning and Priorities Committee DATE OF MEETING: November 15, 2012 SUBJECT:

The California State University GAAP Reporting Manual Effective June 2012 CHAPTER 6 STATEMENT OF CASH FLOWS

CHAPTER 6 STATEMENT OF CASH FLOWS OVERVIEW GASB Statement No. 34 requires the presentation of a statement of cash flows based on the provisions of GASB Statement No. 9. It further requires the use of the

CHAPTER 6 STATEMENT OF CASH FLOWS OVERVIEW GASB Statement No. 34 requires the presentation of a statement of cash flows based on the provisions of GASB Statement No. 9. It further requires the use of the

Clinical Faculty Remuneration Policy. Date: January 27, 2015 Policy ID: 1.630 Status: Final

Clinical Faculty Remuneration Policy Date: Policy ID: 1.630 Status: Final Contact Office: Controller Dean s Office, School of Medicine PO Box 800796 Charlottesville, VA 22908 phone: 434-924-8412 fax: 434-924-8173

Clinical Faculty Remuneration Policy Date: Policy ID: 1.630 Status: Final Contact Office: Controller Dean s Office, School of Medicine PO Box 800796 Charlottesville, VA 22908 phone: 434-924-8412 fax: 434-924-8173

The Colleges of the Seneca Financial Statements May 31, 2007 and 2006

Financial Statements PricewaterhouseCoopers LLP 1100 Bausch & Lomb Place Rochester NY 14604-2705 Telephone (585) 232 4000 Facsimile (585) 454 6594 Report of Independent Auditors To the Board of Trustees

Financial Statements PricewaterhouseCoopers LLP 1100 Bausch & Lomb Place Rochester NY 14604-2705 Telephone (585) 232 4000 Facsimile (585) 454 6594 Report of Independent Auditors To the Board of Trustees

83. Standard 9. Financial Resources. 1. Description. 1.1. Financial stability

83. Standard 9. Financial Resources 1. Description 1.1. Financial stability Bentley University has not reported an operating deficit since it became a not-for-profit organization in 1948. Fiscal year 2012

83. Standard 9. Financial Resources 1. Description 1.1. Financial stability Bentley University has not reported an operating deficit since it became a not-for-profit organization in 1948. Fiscal year 2012

This glossary provides explanations of financial terms used throughout UDW+ reports and

Introduction This glossary provides explanations of financial terms used throughout UDW+ reports and dashboards. It also introduces the underlying concepts that should be understood to utilize the information

Introduction This glossary provides explanations of financial terms used throughout UDW+ reports and dashboards. It also introduces the underlying concepts that should be understood to utilize the information

Accounting for Colleges & Universities. Chapter 17

Accounting for Colleges & Universities Chapter 17 Learning Objectives Understand why most government C&Us choose to report as business-type only special purpose governments Explain unique aspects of C&U

Accounting for Colleges & Universities Chapter 17 Learning Objectives Understand why most government C&Us choose to report as business-type only special purpose governments Explain unique aspects of C&U

Review of Undergraduate and Graduate Program Costs and Revenues

Review of Undergraduate and Graduate Program Costs and Revenues October 28, 2005 Committee Members: Richard Elenich Dan Greenlee Amy Hughes Sue Laajala Bill Predebon Kurt Pregitzer Dave Reed Marilyn Vogler

Review of Undergraduate and Graduate Program Costs and Revenues October 28, 2005 Committee Members: Richard Elenich Dan Greenlee Amy Hughes Sue Laajala Bill Predebon Kurt Pregitzer Dave Reed Marilyn Vogler

How To Understand The Chart Of Accounts Class For The Org Chart Of Account Class For Dartmouth College

Welcome to the Oracle chart of accounts class for GL and OGA chart strings. My name is Susan Wells and I will be one of two instructors for this class. The other instructor is Susan Mockus. We are financial

Welcome to the Oracle chart of accounts class for GL and OGA chart strings. My name is Susan Wells and I will be one of two instructors for this class. The other instructor is Susan Mockus. We are financial

Syracuse University Interdepartmental Recharge Centers

Syracuse University Interdepartmental Recharge Centers Policy Implementation Recharge Centers Recharge centers are departments or functional units that provide goods and services primarily for the benefit

Syracuse University Interdepartmental Recharge Centers Policy Implementation Recharge Centers Recharge centers are departments or functional units that provide goods and services primarily for the benefit

Financial Report to the Board of Trustees

Financial Report to the Board of Trustees February 27, 2013 FY12 Closeout and FY13 Six Month Update Financial Report to the Board of Trustees February 27 2013 Table of Contents Page(s) University of Connecticut

Financial Report to the Board of Trustees February 27, 2013 FY12 Closeout and FY13 Six Month Update Financial Report to the Board of Trustees February 27 2013 Table of Contents Page(s) University of Connecticut

Multi Year Financial Plan Academic Division FY2016-17 through FY2022-23

Multi Year Financial Plan Academic Division FY2016-17 through FY2022-23 Multi Year Financial Plan The Multi-Year Financial Plan was developed in concert with the Finance Committee and approved by the Board

Multi Year Financial Plan Academic Division FY2016-17 through FY2022-23 Multi Year Financial Plan The Multi-Year Financial Plan was developed in concert with the Finance Committee and approved by the Board

Research Administration at The University of Chicago

Research Administration at The University of Chicago Mary Ellen Sheridan, Ph.D. Associate Vice President for Research University Research Administration University of Chicago Outline of JST Seminar Facts

Research Administration at The University of Chicago Mary Ellen Sheridan, Ph.D. Associate Vice President for Research University Research Administration University of Chicago Outline of JST Seminar Facts

ASSOCIATED STUDENTS OF CALIFORNIA STATE UNIVERSITY, LOS ANGELES, INC. (A Component Unit of California State University, Los Angeles)

") CALIFORNIA STATE UNIVERSITY, LOS ANGELES, INC. (A Component Unit of California State University, Los Angeles) Independent Auditor's Report, Financial Statements and Supplemental Information For the Years

CALIFORNIA STATE UNIVERSITY, LOS ANGELES, INC. (A Component Unit of California State University, Los Angeles) Independent Auditor's Report, Financial Statements and Supplemental Information For the Years

I. BACKGROUND INFORMATION

TO: FROM: Board of Trustees Kirsten M. Volpi Executive Vice President for Finance and Administration DATE: May 18, 2015 SUBJECT: FY 2016 Budget I. BACKGROUND INFORMATION As we approach fiscal year 2016

TO: FROM: Board of Trustees Kirsten M. Volpi Executive Vice President for Finance and Administration DATE: May 18, 2015 SUBJECT: FY 2016 Budget I. BACKGROUND INFORMATION As we approach fiscal year 2016

CONTENTS. Independent Auditors Report... 1. Consolidated Statements of Financial Position... 2. Consolidated Statements of Activities...

CONTENTS Independent Auditors Report... 1 Consolidated Statements of Financial Position... 2 Consolidated Statements of Activities...3-4 Consolidated Statements of Cash Flows... 5 Notes to the Consolidated

CONTENTS Independent Auditors Report... 1 Consolidated Statements of Financial Position... 2 Consolidated Statements of Activities...3-4 Consolidated Statements of Cash Flows... 5 Notes to the Consolidated

How To Read A University Or College'S Financial Statement

Understanding College and University Financial Statements By Rudy Fichtenbaum Professor of Economics Department of Economics Wright State University Dayton, OH 45435 (937) 775-3085 rfichtenbaum@sbcglobal.net

Understanding College and University Financial Statements By Rudy Fichtenbaum Professor of Economics Department of Economics Wright State University Dayton, OH 45435 (937) 775-3085 rfichtenbaum@sbcglobal.net

Transparency. Financial Accountability Report. Fiscal Year 2011 Financial Highlights. Peer Institution Comparisons.

Transparency Financial Accountability Report Fiscal Year 2011 Financial Highlights Cost to Students Economic Impact to the State of Colorado Peer Institution Comparisons Financial Accountability Dr. Anthony

Transparency Financial Accountability Report Fiscal Year 2011 Financial Highlights Cost to Students Economic Impact to the State of Colorado Peer Institution Comparisons Financial Accountability Dr. Anthony

Rutgers - UMDNJ Integration: The Path Forward from Good to Great and The Role of Responsibility Center Management (RCM)

") Rutgers - UMDNJ Integration: The Path Forward from Good to Great and The Role of Responsibility Center Management (RCM) Terri Goss Kinzy, Ph.D., Associate Vice President for Research Kathleen Bramwell,

Rutgers - UMDNJ Integration: The Path Forward from Good to Great and The Role of Responsibility Center Management (RCM) Terri Goss Kinzy, Ph.D., Associate Vice President for Research Kathleen Bramwell,

WITH REPORTS OF INDEPENDENT AUDITORS

As of and for the Years Ended JUNE 30, 2013 AND JUNE 30, 2014 Financial Statements and Schedule of Expenditures of Federal Awards WITH REPORTS OF INDEPENDENT AUDITORS AUDITED FINANCIAL STATEMENTS Independent

As of and for the Years Ended JUNE 30, 2013 AND JUNE 30, 2014 Financial Statements and Schedule of Expenditures of Federal Awards WITH REPORTS OF INDEPENDENT AUDITORS AUDITED FINANCIAL STATEMENTS Independent

STRATEGIC FINANCIAL PLANNING SANTA CLARA UNIVERSITY GUIDELINES FOR BUDGETING AND FINANCIAL MANAGEMENT OF CURRENT OPERATIONS

STRATEGIC FINANCIAL PLANNING SANTA CLARA UNIVERSITY GUIDELINES FOR BUDGETING AND FINANCIAL MANAGEMENT OF CURRENT OPERATIONS INTRODUCTION The University faces a significant challenge in providing the financial

STRATEGIC FINANCIAL PLANNING SANTA CLARA UNIVERSITY GUIDELINES FOR BUDGETING AND FINANCIAL MANAGEMENT OF CURRENT OPERATIONS INTRODUCTION The University faces a significant challenge in providing the financial

PENSIONS POLICY INSTITUTE. Tax relief for pension saving in the UK

Tax relief for pension saving in the UK This report is sponsored by Age UK, the Institute and Faculty of Actuaries, Partnership and the TUC. The PPI is grateful for the support of the following sponsors

Tax relief for pension saving in the UK This report is sponsored by Age UK, the Institute and Faculty of Actuaries, Partnership and the TUC. The PPI is grateful for the support of the following sponsors

PROFESSIONAL MASTERS

PROFESSIONAL MASTERS PROGRAM GUIDELINES West Lafayette Campus August 2012 Definition of Professional Masters Program The characteristics of a Professional Masters program at Purdue as outlined below provide

PROFESSIONAL MASTERS PROGRAM GUIDELINES West Lafayette Campus August 2012 Definition of Professional Masters Program The characteristics of a Professional Masters program at Purdue as outlined below provide

Capital Area Council of Governments FY 2015 Cost Allocation Plan

Capital Area Council of Governments FY 2015 Cost Allocation Plan The Capital Area Council of Governments uses the cost allocation method prescribed in OMB Circular A 87, Department of Health and Human

Capital Area Council of Governments FY 2015 Cost Allocation Plan The Capital Area Council of Governments uses the cost allocation method prescribed in OMB Circular A 87, Department of Health and Human

Outline for the Main Campus Three Year Financial Strategic Plan

Outline for the Main Campus Three Year Financial Strategic Plan Preamble The mission of the University of New Mexico is to serve as New Mexico s flagship institution of higher learning through demonstrated

Outline for the Main Campus Three Year Financial Strategic Plan Preamble The mission of the University of New Mexico is to serve as New Mexico s flagship institution of higher learning through demonstrated

Office of Budget and Financial Planning

The Office of Budget and Financial Planning (OBFP) is a professional service organization in the Institute s financial administration area. The mission of the office is to provide value added integrated

The Office of Budget and Financial Planning (OBFP) is a professional service organization in the Institute s financial administration area. The mission of the office is to provide value added integrated

KANSAS CITY, MISSOURI RESPONSES TO THE FISCAL YEAR 2013 AUDIT MANAGEMENT LETTER

KANSAS CITY, MISSOURI RESPONSES TO THE FISCAL YEAR 2013 AUDIT MANAGEMENT LETTER Material Weaknesses (0) No material weaknesses were reported for FY 2013. Significant Deficiencies (1) Grant Receivable Accounting

KANSAS CITY, MISSOURI RESPONSES TO THE FISCAL YEAR 2013 AUDIT MANAGEMENT LETTER Material Weaknesses (0) No material weaknesses were reported for FY 2013. Significant Deficiencies (1) Grant Receivable Accounting

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL AUDIT OF COMMUNITY SERVICE AND OTHER SELECTED GRANTS AT KENTUCKY AUTHORITY FOR EDUCATIONAL TELEVISION, INC., KET-TV, LEXINGTON, KENTUCKY

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL AUDIT OF COMMUNITY SERVICE AND OTHER SELECTED GRANTS AT KENTUCKY AUTHORITY FOR EDUCATIONAL TELEVISION, INC., KET-TV, LEXINGTON, KENTUCKY

THE WILLIAM PATERSON UNIVERSITY OF NEW JERSEY (A Component Unit of the State of New Jersey)

") Financial Statements and Management s Discussion and Analysis (With Independent Auditors Report Thereon) Table of Contents Management s Discussion and Analysis 1 Independent Auditors Report 12 Financial

Financial Statements and Management s Discussion and Analysis (With Independent Auditors Report Thereon) Table of Contents Management s Discussion and Analysis 1 Independent Auditors Report 12 Financial

Presentation at the NACUBO Budgeting Forum Budget Balancing Strategies for Multi Year Plans: Case Study of the University of Michigan Rowan Miranda,

Presentation at the NACUBO Budgeting Forum Budget Balancing Strategies for Multi Year Plans: Case Study of the University of Michigan Rowan Miranda, Ph.D. AVP for Finance September 24, 2012 1 Agenda 1

Presentation at the NACUBO Budgeting Forum Budget Balancing Strategies for Multi Year Plans: Case Study of the University of Michigan Rowan Miranda, Ph.D. AVP for Finance September 24, 2012 1 Agenda 1

BUDGET AND FINANCIAL PLAN SUMMARY FILE

REVENUE & FINANCING SOURCES Operating Revenues Charges for services Rental & financing income Last Year (Actual) 2014 Other operating revenues 0 Nonoperating Revenues Current Year (Estimated) 2015 Next

REVENUE & FINANCING SOURCES Operating Revenues Charges for services Rental & financing income Last Year (Actual) 2014 Other operating revenues 0 Nonoperating Revenues Current Year (Estimated) 2015 Next

REPORT NO. 2012-155 MARCH 2012 MIAMI DADE COLLEGE. Financial Audit

REPORT NO. 2012-155 MARCH 2012 Financial Audit For the Fiscal Year Ended June 30, 2011 BOARD OF TRUSTEES AND PRESIDENT Members of the Board of Trustees and President who served during the 2010-11 fiscal

REPORT NO. 2012-155 MARCH 2012 Financial Audit For the Fiscal Year Ended June 30, 2011 BOARD OF TRUSTEES AND PRESIDENT Members of the Board of Trustees and President who served during the 2010-11 fiscal

Office of the President Phone: 774.455.7710 333 South Street, Suite 400 Fax: 774-455-7730

Office of the President Phone: 774.455.7710 333 South Street, Suite 400 Fax: 774-455-7730 Shrewsbury, Massachusetts 01545 www.massachusetts.edu As part of the Commonwealth s budget process, the University

Office of the President Phone: 774.455.7710 333 South Street, Suite 400 Fax: 774-455-7730 Shrewsbury, Massachusetts 01545 www.massachusetts.edu As part of the Commonwealth s budget process, the University

Ohio University (a component unit of the State of Ohio) Financial Statements for the Years Ended June 30, 2014 and 2013

Financial Statements for the Years Ended June 30, 2014 and 2013") (a component unit of the State of Ohio) Financial Statements for the Years Ended Contents Independent Auditor s Report 1-3 Financial Statements Management s Discussion and Analysis 4-14 Statements of Net

(a component unit of the State of Ohio) Financial Statements for the Years Ended Contents Independent Auditor s Report 1-3 Financial Statements Management s Discussion and Analysis 4-14 Statements of Net

Purpose. This accounting policy documents authoritative literature for the accounting treatment of accounts payable and accrued expenses.

1. Title 2. Policy Accounts Payable and Accrued Expenses Sec. 1 Sec. 2 Sec. 3 Sec. 4 Sec. 5 Policy Statement. The accrual basis of accounting should be utilized in measuring financial position and operating

1. Title 2. Policy Accounts Payable and Accrued Expenses Sec. 1 Sec. 2 Sec. 3 Sec. 4 Sec. 5 Policy Statement. The accrual basis of accounting should be utilized in measuring financial position and operating

BUDGET AND FINANCIAL PLAN SUMMARY FILE

BUDGET AND FINANCIAL PLAN SUMMARY FILE BUDGETED REVENUES, EXPENDITURES, AND CHANGES IN CURRENT NET ASSETS Last Year (Actual) 2013 Current Year (Estimated) 2014 Adopted 2015 Proposed 2016 Proposed 2017

BUDGET AND FINANCIAL PLAN SUMMARY FILE BUDGETED REVENUES, EXPENDITURES, AND CHANGES IN CURRENT NET ASSETS Last Year (Actual) 2013 Current Year (Estimated) 2014 Adopted 2015 Proposed 2016 Proposed 2017

COLLEGE AND UNIVERSITY COST IDENTIFICATION AND ALLOCATION

NATIONAL ASSOCIATION OF COLLEGE AND UNIVERSITY BUSINESS OFFICERS COLLEGE AND UNIVERSITY COST IDENTIFICATION AND ALLOCATION INTRODUCTION... 2 FINANCIAL / FUND ACCOUNTING...2 WHY FUND ACCOUNTING?... 2 WHAT

NATIONAL ASSOCIATION OF COLLEGE AND UNIVERSITY BUSINESS OFFICERS COLLEGE AND UNIVERSITY COST IDENTIFICATION AND ALLOCATION INTRODUCTION... 2 FINANCIAL / FUND ACCOUNTING...2 WHY FUND ACCOUNTING?... 2 WHAT

UNIVERSITY OF OKLAHOMA/NORMAN CAMPUS OFFICE OF RESEARCH SERVICES Procedures Guide. Recharge Center Operations

UNIVERSITY OF OKLAHOMA/NORMAN CAMPUS OFFICE OF RESEARCH SERVICES Procedures Guide Recharge Center Operations Overview 3 Establishing a Recharge Center 3 Information that Will Need to be Determined 3 Rate

UNIVERSITY OF OKLAHOMA/NORMAN CAMPUS OFFICE OF RESEARCH SERVICES Procedures Guide Recharge Center Operations Overview 3 Establishing a Recharge Center 3 Information that Will Need to be Determined 3 Rate

Annual Accountability Sub-Report on University Private Support February 2009

Annual Accountability Sub-Report on University Private Support February 2009 Annual Accountability Sub-Report on University Private Support UC Gifts & National Campus Endowments Perspective Programs Millions

Annual Accountability Sub-Report on University Private Support February 2009 Annual Accountability Sub-Report on University Private Support UC Gifts & National Campus Endowments Perspective Programs Millions

REPORT NO. 2012-121 MARCH 2012 BROWARD COLLEGE. Financial Audit

REPORT NO. 2012-121 MARCH 2012 Financial Audit For the Fiscal Year Ended June 30, 2011 BOARD OF TRUSTEES AND PRESIDENT Members of the Board of Trustees and President who served during the 2010-11 fiscal

REPORT NO. 2012-121 MARCH 2012 Financial Audit For the Fiscal Year Ended June 30, 2011 BOARD OF TRUSTEES AND PRESIDENT Members of the Board of Trustees and President who served during the 2010-11 fiscal

Strategic Direction 7 Vision for Shared Administrative Services

Strategic Direction 7 Vision for Shared Administrative Services Strategic Direction 7 - Centralize the System s business/administrative functions, where appropriate, in order to leverage resources and

Strategic Direction 7 Vision for Shared Administrative Services Strategic Direction 7 - Centralize the System s business/administrative functions, where appropriate, in order to leverage resources and

WORKING PAPER, V2 Revised December 2011

WORKING PAPER, V2 Revised December 2011 Incentive-Based Budget Model Undergraduate Tuition Allocation *New or revised material is indicated by an asterisk. The following information is intended to provide

WORKING PAPER, V2 Revised December 2011 Incentive-Based Budget Model Undergraduate Tuition Allocation *New or revised material is indicated by an asterisk. The following information is intended to provide

NORTHWEST COMMI SSI ON ON COLLEGES AND UNIVERSITIES

NORTHWEST COMMI SSI ON ON COLLEGES AND UNIVERSITIES BASIC INSTITUTIONAL DATA FORM Information and data provided in the institutional self-evaluation are usually for the academic and fiscal year preceding

NORTHWEST COMMI SSI ON ON COLLEGES AND UNIVERSITIES BASIC INSTITUTIONAL DATA FORM Information and data provided in the institutional self-evaluation are usually for the academic and fiscal year preceding

WESTERN WASHINGTON UNIVERSITY BELLINGHAM, WASHINGTON ASSOCIATED STUDENTS BOOKSTORE FINANCIAL REPORT JUNE 30, 2005

WESTERN WASHINGTON UNIVERSITY BELLINGHAM, WASHINGTON ASSOCIATED STUDENTS BOOKSTORE FINANCIAL REPORT JUNE 30, 2005 C O N T E N T S Page INDEPENDENT AUDITORS' REPORT...1 MANAGEMENT DISCUSSION AND ANALYSIS...

WESTERN WASHINGTON UNIVERSITY BELLINGHAM, WASHINGTON ASSOCIATED STUDENTS BOOKSTORE FINANCIAL REPORT JUNE 30, 2005 C O N T E N T S Page INDEPENDENT AUDITORS' REPORT...1 MANAGEMENT DISCUSSION AND ANALYSIS...

Program Policy Guidance OSHC-2011-06

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT Office of Sustainable Housing and Communities WASHINGTON, DC 20410-0050 Date: April 13, 2011 Program Policy Guidance OSHC-2011-06 Subject: Indirect Cost

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT Office of Sustainable Housing and Communities WASHINGTON, DC 20410-0050 Date: April 13, 2011 Program Policy Guidance OSHC-2011-06 Subject: Indirect Cost

Office of Budget and Financial Planning

The Office of Budget and Financial Planning (OBFP) is a professional service organization for financial planning and resource allocation and management. Our mission is to deliver value-added planning and

The Office of Budget and Financial Planning (OBFP) is a professional service organization for financial planning and resource allocation and management. Our mission is to deliver value-added planning and

University of California, Berkeley MANAGEMENT S DISCUSSION AND ANALYSIS (UNAUDITED)

") The objective of Management s Discussion & Analysis (MD&A) is to help readers of the financial statements of the University of California, Berkeley (Berkeley) better understand the financial position and

The objective of Management s Discussion & Analysis (MD&A) is to help readers of the financial statements of the University of California, Berkeley (Berkeley) better understand the financial position and

VANCOUVER COMMUNITY COLLEGE

Financial Statements of VANCOUVER COMMUNITY COLLEGE KPMG Enterprise Metrotower II 4720 Kingsway, Suite 2400 Burnaby, BC V5H 4N2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 Internet www.kpmg.ca/enterprise

Financial Statements of VANCOUVER COMMUNITY COLLEGE KPMG Enterprise Metrotower II 4720 Kingsway, Suite 2400 Burnaby, BC V5H 4N2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 Internet www.kpmg.ca/enterprise

The University of Alabama in Huntsville

The University of Alabama in Huntsville FINANCIAL REPORT 2012-2013 Table of Contents Independent Auditor s Report......... 2 Management s Discussion and Analysis (Unaudited)..... 4 Statements of Net Position............

The University of Alabama in Huntsville FINANCIAL REPORT 2012-2013 Table of Contents Independent Auditor s Report......... 2 Management s Discussion and Analysis (Unaudited)..... 4 Statements of Net Position............

Ohio University Telecommunications Center A Public Telecommunications Entity (A Department of Ohio University)

") Ohio University Telecommunications Center A Public Telecommunications Entity (A Department of Ohio University) Financial Statements for the Years Ended June 30, 2004 and 2003 and Independent Auditors Report

Ohio University Telecommunications Center A Public Telecommunications Entity (A Department of Ohio University) Financial Statements for the Years Ended June 30, 2004 and 2003 and Independent Auditors Report

How Do You Stack Up?

How Do You Stack Up? Charles Tegen Associate Vice President for Finance Clemson University 2014 Managerial Analysis and Decision Support Charlotte, North Carolina November 13, 2014 Session Outline Benchmarking

How Do You Stack Up? Charles Tegen Associate Vice President for Finance Clemson University 2014 Managerial Analysis and Decision Support Charlotte, North Carolina November 13, 2014 Session Outline Benchmarking

Winter Symposium 2012

Winter Symposium 2012 January 19, 2012 SMSU Ballroom Roy Koch, Provost and Vice President for Academic Affairs Kevin Reynolds, Vice Provost for Fiscal Strategies and Planning Monica Rimai, Vice President

Winter Symposium 2012 January 19, 2012 SMSU Ballroom Roy Koch, Provost and Vice President for Academic Affairs Kevin Reynolds, Vice Provost for Fiscal Strategies and Planning Monica Rimai, Vice President

West Texas A&M University: Review of Physical Plant Operations PROJECT SUMMARY. Summary of Significant Results

PROJECT SUMMARY Overview Table of Contents Project Summary... 1 Detailed Observations... 4 Basis of Review... 12 Audit Team Information... 14 Distribution List... 14 Controls within certain areas of West

PROJECT SUMMARY Overview Table of Contents Project Summary... 1 Detailed Observations... 4 Basis of Review... 12 Audit Team Information... 14 Distribution List... 14 Controls within certain areas of West

The University of Research and Development Centers

Centers & Institutes Description Centers and institutes are established within the University to strengthen and enrich programs of research, instruction or public service conducted by the faculty and staff.

Centers & Institutes Description Centers and institutes are established within the University to strengthen and enrich programs of research, instruction or public service conducted by the faculty and staff.

JAMES A. MICHENER ART MUSEUM

FINANCIAL STATEMENTS YEAR ENDED DECEMBER 31, 2010 CONTENTS INDEPENDENT AUDITOR'S REPORT 1 FINANCIAL STATEMENTS Statement of Financial Position 2 Statement of Activities 3 Statement of Functional Expenses

FINANCIAL STATEMENTS YEAR ENDED DECEMBER 31, 2010 CONTENTS INDEPENDENT AUDITOR'S REPORT 1 FINANCIAL STATEMENTS Statement of Financial Position 2 Statement of Activities 3 Statement of Functional Expenses

FUND ACCOUNTING TRAINING

FUND ACCOUNTING TRAINING Module 2 Current Funds The University of Texas System OBJECTIVES Obtain understanding of: Difference between Current Funds and Noncurrent Funds Difference between Unrestricted

FUND ACCOUNTING TRAINING Module 2 Current Funds The University of Texas System OBJECTIVES Obtain understanding of: Difference between Current Funds and Noncurrent Funds Difference between Unrestricted

FY14 ANNUAL FINANCIAL STATEMENTS Financial Statements for the Years Ended June 30, 2014 and 2013 and Independent Auditor s Report. Including Schedule

FY14 ANNUAL FINANCIAL STATEMENTS Financial Statements for the Years Ended June 30, 2014 and 2013 and Independent Auditor s Report. Including Schedule of Expenditures of Federal Awards and Single Audit

FY14 ANNUAL FINANCIAL STATEMENTS Financial Statements for the Years Ended June 30, 2014 and 2013 and Independent Auditor s Report. Including Schedule of Expenditures of Federal Awards and Single Audit

REPORT NO. 2014-174 MARCH 2014 NEW COLLEGE OF FLORIDA. Financial Audit

REPORT NO. 2014-174 MARCH 2014 Financial Audit For the Fiscal Year Ended June 30, 2013 BOARD OF TRUSTEES AND PRESIDENT Members of the Board of Trustees and President who served during the 2012-13 fiscal

REPORT NO. 2014-174 MARCH 2014 Financial Audit For the Fiscal Year Ended June 30, 2013 BOARD OF TRUSTEES AND PRESIDENT Members of the Board of Trustees and President who served during the 2012-13 fiscal

XIV. Accounting for Gifts, Endowment Earnings and Other Projects

XIV. Accounting for Gifts, Endowment Earnings and Other Projects A. Overview: RIT receives gifts and other income to support the operations of the University. Gifts that are restricted for use by the donor

XIV. Accounting for Gifts, Endowment Earnings and Other Projects A. Overview: RIT receives gifts and other income to support the operations of the University. Gifts that are restricted for use by the donor

Programmatic Facilities projects that benefit a specific program or function.

The Colorado School of Mines capital budget is impacted by several factors including the implementation of a new strategic plan, the growth in enrollment and research, and the availability of state funds

The Colorado School of Mines capital budget is impacted by several factors including the implementation of a new strategic plan, the growth in enrollment and research, and the availability of state funds

USING HYPERION PROFITABILITY & COST MANAGEMENT WITH HYPERION PLANNING FOR RCM SESSION 35090 MARCH 8, 2016

USING HYPERION PROFITABILITY & COST MANAGEMENT WITH HYPERION PLANNING FOR RCM SESSION 35090 MARCH 8, 2016 PRESENTERS Andy Rosenau AVP Budget & Administration Rutgers University arosenau@rutgers.edu Andy

USING HYPERION PROFITABILITY & COST MANAGEMENT WITH HYPERION PLANNING FOR RCM SESSION 35090 MARCH 8, 2016 PRESENTERS Andy Rosenau AVP Budget & Administration Rutgers University arosenau@rutgers.edu Andy

TCS Online Data Dictionary

TCS Online Data Dictionary Label Definition Report Academic year The period of time generally extending from September to June; usually equated to 2 semesters or trimesters, 3 Report Filters quarters,

TCS Online Data Dictionary Label Definition Report Academic year The period of time generally extending from September to June; usually equated to 2 semesters or trimesters, 3 Report Filters quarters,

Children and Families Commission of Orange County

Agenda Item No. 4 December 7, 2011 Meeting DATE: November 21, 2011 TO: FROM: SUBJECT: Children and Families Commission of Orange County Michael M. Ruane, Executive Director Commission Workshop on Strategic

Agenda Item No. 4 December 7, 2011 Meeting DATE: November 21, 2011 TO: FROM: SUBJECT: Children and Families Commission of Orange County Michael M. Ruane, Executive Director Commission Workshop on Strategic

REVENUE AND EXPENDITURE/EXPENSE ANALYSIS

THE UNIVERSITY OF TEXAS SYSTEM OFFICE OF THE CONTROLLER REVENUE AND EXPENDITURE/EXPENSE ANALYSIS 1999 2008 2009 Update 201 Seventh Street, ASH 5 th Floor Austin, Texas 78701 512.499.4527 www.utsystem.edu/cont

THE UNIVERSITY OF TEXAS SYSTEM OFFICE OF THE CONTROLLER REVENUE AND EXPENDITURE/EXPENSE ANALYSIS 1999 2008 2009 Update 201 Seventh Street, ASH 5 th Floor Austin, Texas 78701 512.499.4527 www.utsystem.edu/cont

JD EDWARDS ENTERPRISEONE ADVANCED REAL ESTATE FORECASTING

JD EDWARDS ENTERPRISEONE ADVANCED REAL ESTATE FORECASTING Increase accuracy of budget, forecast, and valuations Improve data integrity and staff productivity The Issue: Disparate Real Estate Budgeting,

JD EDWARDS ENTERPRISEONE ADVANCED REAL ESTATE FORECASTING Increase accuracy of budget, forecast, and valuations Improve data integrity and staff productivity The Issue: Disparate Real Estate Budgeting,

DEPARTMENT OF FINANCE AND ADMINISTRATION-POLICY 03

DEPARTMENT OF FINANCE AND ADMINISTRATION-POLICY 03 Policy 3-Uniform Reporting Requirements and Cost Allocation Plans for Subrecipients of Federal and State Grant Monies (Revised 12/97) Introduction to

DEPARTMENT OF FINANCE AND ADMINISTRATION-POLICY 03 Policy 3-Uniform Reporting Requirements and Cost Allocation Plans for Subrecipients of Federal and State Grant Monies (Revised 12/97) Introduction to

WORKING PAPER, V3 Revised January 2012

WORKING PAPER, V3 Revised January 2012 Incentive-Based Budget Model Undergraduate Tuition Allocation *New or revised material is indicated by an asterisk. The following information is intended to provide

WORKING PAPER, V3 Revised January 2012 Incentive-Based Budget Model Undergraduate Tuition Allocation *New or revised material is indicated by an asterisk. The following information is intended to provide

Case Western Reserve University Consolidated Financial Statements for the Year Ending June 30, 2001

Contents Report of Independent Accountants 1 Part 1 Consolidated Financial Statements Consolidated Balance Sheet 2 Consolidated Statement of Activities 3 Consolidated Statement of Cash Flows 4 Part 2 Summary

Contents Report of Independent Accountants 1 Part 1 Consolidated Financial Statements Consolidated Balance Sheet 2 Consolidated Statement of Activities 3 Consolidated Statement of Cash Flows 4 Part 2 Summary

Budget and Financial Planning at UMass Boston. Presentation to: Faculty Council February 7, 2011

Budget and Financial Planning at UMass Boston Presentation to: Faculty Council February 7, 2011 Three Year Investment Scenario Investments in UMass Boston: New Resources in Recent Operating Budgets Through

Budget and Financial Planning at UMass Boston Presentation to: Faculty Council February 7, 2011 Three Year Investment Scenario Investments in UMass Boston: New Resources in Recent Operating Budgets Through

BUDGET APPROVED ON JULY 17, 2014 PROPOSED BUDGET

BUDGET APPROVED ON JULY 17, 2014 PROPOSED BUDGET FY2015 PROPOSED BUDGET FISCAL YEAR 2014-15 Budget Methodology: Temple University is implementing a decentralized budget model in fiscal year 2014-15. This

BUDGET APPROVED ON JULY 17, 2014 PROPOSED BUDGET FY2015 PROPOSED BUDGET FISCAL YEAR 2014-15 Budget Methodology: Temple University is implementing a decentralized budget model in fiscal year 2014-15. This

ST. MARY SEMINARY AND GRADUATE SCHOOL OF THEOLOGY (OUR LADY OF THE LAKE) FINANCIAL REPORT. JUNE 30, 2015 and 2014

FINANCIAL REPORT. JUNE 30, 2015 and 2014") ST. MARY SEMINARY AND GRADUATE SCHOOL OF THEOLOGY FINANCIAL REPORT JUNE 30, 2015 and 2014 CONTENTS Page INDEPENDENT AUDITORS' REPORT ON THE FINANCIAL STATEMENTS 1 FINANCIAL STATEMENTS Statements of financial

ST. MARY SEMINARY AND GRADUATE SCHOOL OF THEOLOGY FINANCIAL REPORT JUNE 30, 2015 and 2014 CONTENTS Page INDEPENDENT AUDITORS' REPORT ON THE FINANCIAL STATEMENTS 1 FINANCIAL STATEMENTS Statements of financial

University of Missouri System Accounting Policies and Procedures

University of Missouri System Accounting Policies and Procedures Policy Number: APM 65.10 Policy Name: Allowance and Write-off for Uncollectible Student Loans General Policy and Procedure Overview: In

University of Missouri System Accounting Policies and Procedures Policy Number: APM 65.10 Policy Name: Allowance and Write-off for Uncollectible Student Loans General Policy and Procedure Overview: In

Each year, millions of Californians pursue degrees and certificates or enroll in courses

Higher Education Each year, millions of Californians pursue degrees and certificates or enroll in courses to improve their knowledge and skills at the state s higher education institutions. More are connected

Higher Education Each year, millions of Californians pursue degrees and certificates or enroll in courses to improve their knowledge and skills at the state s higher education institutions. More are connected

4 b) Where to Record Revenue. 4 5 c) When to Record Revenue. 6-11 Recognition of Unrestricted Revenue Recognition of Restricted Revenue Sources

Where to Record Revenue. 4 5 c) When to Record Revenue. 6-11 Recognition of Unrestricted Revenue Recognition of Restricted Revenue Sources") Revenue Recognition Policy Guidelines These guidelines are organized within the following sections: Pages I. Purpose 1 II. Responsibilities 1 III. Definitions 2-3 IV. Major Sources of Revenue and Normal

Revenue Recognition Policy Guidelines These guidelines are organized within the following sections: Pages I. Purpose 1 II. Responsibilities 1 III. Definitions 2-3 IV. Major Sources of Revenue and Normal

West Virginia Council for Community and Technical College Education

West Virginia Council for Community and Technical College Education Combined Financial Statements Years Ended June 30, 2013 and 2012 and Independent Auditor s Reports TABLE OF CONTENTS INDEPENDENT AUDITOR

West Virginia Council for Community and Technical College Education Combined Financial Statements Years Ended June 30, 2013 and 2012 and Independent Auditor s Reports TABLE OF CONTENTS INDEPENDENT AUDITOR

MAKE-A-WISH FOUNDATION OF MASSACHUSETTS AND RHODE ISLAND, INC. Financial Statements. August 31, 2014. (With Independent Auditors Report Thereon)

") MAKE-A-WISH FOUNDATION OF MASSACHUSETTS Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Statement of Financial Position 3 Statement

MAKE-A-WISH FOUNDATION OF MASSACHUSETTS Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Statement of Financial Position 3 Statement

Pensacola Habitat For Humanity, Inc. Pensacola, Florida. Audited Financial Statements. With Supplementary Information

Pensacola, Florida Audited Financial Statements With Supplementary Information June 30, 2014 Pensacola, Florida Audited Financial Statements With Supplementary Information June 30, 2014 CONTENTS PAGE Independent

Pensacola, Florida Audited Financial Statements With Supplementary Information June 30, 2014 Pensacola, Florida Audited Financial Statements With Supplementary Information June 30, 2014 CONTENTS PAGE Independent

The Application of International Accounting Standards in the Financial Statements of Tearfund Partners

The Application of International Accounting Standards in the Financial Statements of Tearfund Partners Context: International Accounting Standards (IAS) have been developed primarily to bring consistency

The Application of International Accounting Standards in the Financial Statements of Tearfund Partners Context: International Accounting Standards (IAS) have been developed primarily to bring consistency

REPORT NO. 2014-121 MARCH 2014 MIAMI DADE COLLEGE. Financial Audit. For the Fiscal Year Ended June 30, 2013

77 REPORT NO. 2014-121 MARCH 2014 Financial Audit For the Fiscal Year Ended June 30, 2013 BOARD OF TRUSTEES AND PRESIDENT Members of the Board of Trustees and President who served during the 2012-13 fiscal

77 REPORT NO. 2014-121 MARCH 2014 Financial Audit For the Fiscal Year Ended June 30, 2013 BOARD OF TRUSTEES AND PRESIDENT Members of the Board of Trustees and President who served during the 2012-13 fiscal

REPORT NO. 2011-108 FEBRUARY 2011 SEMINOLE STATE COLLEGE OF FLORIDA. Financial Audit

REPORT NO. 2011-108 FEBRUARY 2011 SEMINOLE STATE COLLEGE OF FLORIDA Financial Audit For the Fiscal Year Ended June 30, 2010 BOARD OF TRUSTEES AND PRESIDENT Members of the Board of Trustees and President

REPORT NO. 2011-108 FEBRUARY 2011 SEMINOLE STATE COLLEGE OF FLORIDA Financial Audit For the Fiscal Year Ended June 30, 2010 BOARD OF TRUSTEES AND PRESIDENT Members of the Board of Trustees and President

MINNESOTA STATE COLLEGES AND UNIVERSITIES BOARD OF TRUSTEES Agenda Item Summary Sheet

MINNESOTA STATE COLLEGES AND UNIVERSITIES BOARD OF TRUSTEES Agenda Item Summary Sheet Name: Finance and Facilities Committee Date: June 17, 2015 Title: FY2016 Operating Budget (Second Reading) Purpose

MINNESOTA STATE COLLEGES AND UNIVERSITIES BOARD OF TRUSTEES Agenda Item Summary Sheet Name: Finance and Facilities Committee Date: June 17, 2015 Title: FY2016 Operating Budget (Second Reading) Purpose

Celebration Church of Jacksonville, Inc.

Financial Statements and Independent Auditor s Report Contents Page Independent Auditor s Report...3 Financial Statements Statement of Financial Position...4 Statement of Activities...5 Statement of Cash

Financial Statements and Independent Auditor s Report Contents Page Independent Auditor s Report...3 Financial Statements Statement of Financial Position...4 Statement of Activities...5 Statement of Cash

Budget Policies and Procedures Manual

Office of Budget and Planning Budget Policies and Procedures Manual Revised 3/02/15 Office of Budget and Planning Budget Policies and Procedures Manual Contents Introduction 1 Preparation and Approval

Office of Budget and Planning Budget Policies and Procedures Manual Revised 3/02/15 Office of Budget and Planning Budget Policies and Procedures Manual Contents Introduction 1 Preparation and Approval

The Large Public University

By Kenneth A. Jessell PhD. CFO Perspectives Additional Perspectives CFO Perspectives: The Large Public University is one in a series of white papers that looks at the role of the CFO within different institutional

By Kenneth A. Jessell PhD. CFO Perspectives Additional Perspectives CFO Perspectives: The Large Public University is one in a series of white papers that looks at the role of the CFO within different institutional

SUPPORTING DATA FOR FISCAL YEAR 2014 ILLINOIS COMMUNITY COLLEGE SYSTEM, ADULT EDUCATION, AND POSTSECONDARY CAREER AND TECHNICAL EDUCATION

SUPPORTING DATA FOR FISCAL YEAR 2014 ILLINOIS COMMUNITY COLLEGE SYSTEM, ADULT EDUCATION, AND POSTSECONDARY CAREER AND TECHNICAL EDUCATION 1) Copy of the Operating Budget Appropriation and Supporting Technical

SUPPORTING DATA FOR FISCAL YEAR 2014 ILLINOIS COMMUNITY COLLEGE SYSTEM, ADULT EDUCATION, AND POSTSECONDARY CAREER AND TECHNICAL EDUCATION 1) Copy of the Operating Budget Appropriation and Supporting Technical