Presentation of Simplified Method for Preparing the Facilities and Administrative Cost Rate Proposal. Jason Guilbeault, Senior Consultant

|

|

|

- Roberta Lee

- 8 years ago

- Views:

Transcription

1 Presentation of Simplified Method for Preparing the Facilities and Administrative Cost Rate Proposal Jason Guilbeault, Senior Consultant MAXIMUS, 2014

2 Agenda 1. What is the Facilities and Administrative cost proposal? 2. Why do one? 3. What are its components? 4. How do you prepare one? 5. Common target areas during rate negotiation. 6. Short Form vs. Long Form considerations.

3 What is the F&A cost proposal? The F&A cost proposal helps the school to recover the cost of institutional expenses related to research and other, externally-funded direct activities. The federal government mandates that schools submit the F&A cost proposal to their cognizant agency, either DHHS-DCA or ONR-DCAA. Title 2 CFR Part 220 (Formerly Circular A-21) prescribes what can or cannot be included in the F&A cost categories. The F&A cost proposal is subject to Federal audit, based on Part 220 requirements.

4 Why do one? The institution can be reimbursed for overhead / indirect costs on certain federal awards. Granting agencies include the National Institutes of Health, the National Science Foundation, Department of Defense, and the Department of Education. Provides a critical source of revenue at a time when budgets are tight. If completed in the appropriate manner, e.g., follows Part 220 requirements, federal audit is not lengthy.

5 Who Can Use the Simplified Method? 2 CFR Part 220, Subsection H: Where the total direct cost of work covered by Part 220 at an institution does not exceed $10 million in a fiscal year, the use of the simplified procedure described in subsections H2 or 3, may be used in determining allowable F&A costs. New Uniform Guidance (2 CFR 200): Effective 12/26/13 (uniform implementation 12/26/14 applicable to new awards and incremental funding awarded on or after 12/26/14), but for F&A costing purposes, we anticipate this goes into effect starting with FY16 base years. Subpart F (Audits) of the Guidance is effective for the first fiscal year beginning after 12/26/14. Institutions that have never received a negotiated rate may elect to charge a de minimis rate of 10% of MTDC, which may be used indefinitely. It is recommended you weigh the cost to benefit of using the 10% rate. Typical negotiated rates are much higher than 10%.

: Effective 12/26/13 (uniform implementation 12/26/14 applicable to new awards and incremental funding awarded on or after 12/26/14), but for F&A costing purposes, we")

6 What is the F&A rate? Total FY14 F&A Costs Total FY14 Direct Activity Costs* =? % * Includes instruction, sponsored research awards, public service awards, auxiliary enterprises, student services, and other direct costs (unallowable activities)

7 There are two components to F&A costs: Facilities Utilities Interest on buildings/equip/cap improvements Building Depreciation* Equipment Depreciation* Physical Plant Administration Campus Security Library * Grant-funded assets are not included.

8 Administration Grant Administration and Compliance (Office of Sponsored Projects) University Administration (Human Resources, Finance, Budget, President s Office) Department Administration, including Department Chair and Support Staff For Short Form method, computed as 20 percent of the salaries and expenses of deans, heads of departments, and their administrative assistants.

9 Steps In The Cost Proposal Process 1. Procure Financial and Asset Data 2. Reconcile To Financial Statement 3. Reclassify Costs To 2 CFR Part 220 Cost Categories 4. Exclusion Of Costs 5. Adjustments for Interest / SWCAP / Depreciation / O&M 6. Calculate Rate 7. Submit Final Package

10 Procuring Financial and Asset Data 1. Pertains to a single fiscal year, known in the F&A world as your base year. 2. Expenditure data needs to have the following data elements: Account or Chart String Expenditure Transactions At The Object / Expense Code Department Financial Statement Code/Function

11 Asset Data - Depreciation 1. 2 CFR Part 220, Section F2 2. Gather asset records to identify buildings and equipment. 3. Reconcile depreciation to amount recorded in Financial Statements. 4. Determine allowable depreciation for Short Form F&A cost proposal. Usually determined by space data

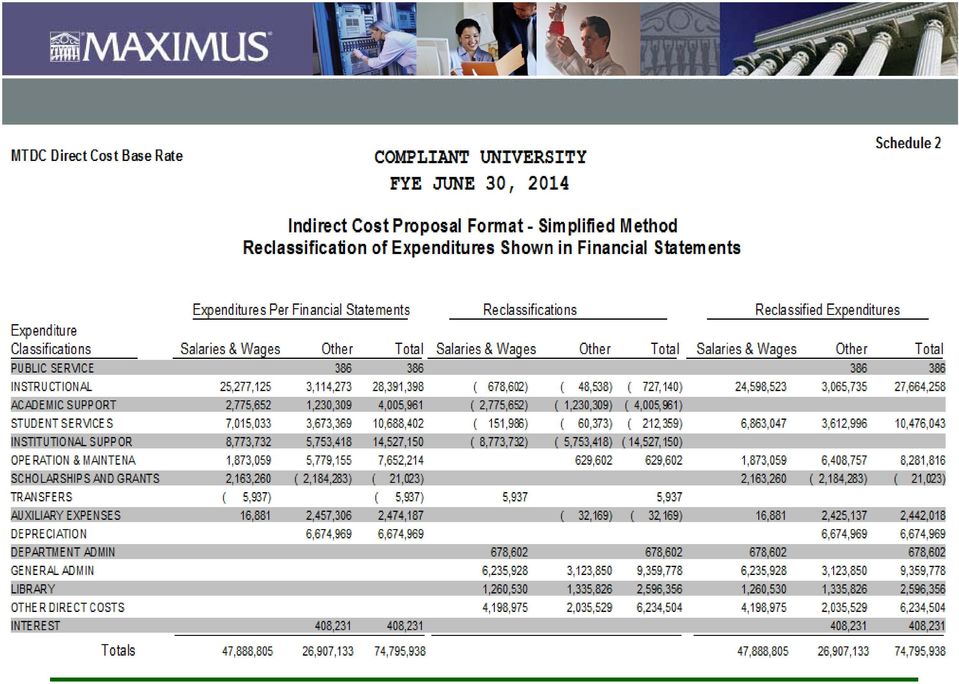

12 Reconcile Financial Data to Financial Statements (Schedule 1)

13 Reclassify Costs to 2 CFR Part 220 Categories 1. Part 220, Sections F4 (O&M), F5 (GA) and F8 (Library). 2. Expenditure data needs to be scrutinized at the account and department level. Facilities Cost Examples Library costs may be classified as Academic Support function for the Financial Statements, but they are defined as a Facilities costs by Part 220. Move to Library Function in the indirect cost pool. Campus Security is often classified as Institutional Support for the Financial Statements, but should be in the O&M function in the indirect cost pool.

14 Reclassify Costs to Part 220 Categories Administrative Cost Examples Institutional Support is typically defined as General Administration (scrub for OIA). Department Administration costs are those of Department Chairs, College Deans and Clerical Support (20% for Short Form Method). Requires salary and fringe benefit expenses, by title code and employee. Costs are re-classified from Instruction direct base to DA function of the indirect cost pool.

. Requires salary and fringe benefit expenses, by title code and employee.")

15 Reclassify Costs to Part 220 Categories Unallowable Costs Part 220, Section J Costs such as Alumni Relations and Fundraising need to be classified as Other Direct Costs. Financial data needs to be scrutinized at the Object / Expense Code level for: Entertainment expenses Certain legal costs Lobbying costs

16

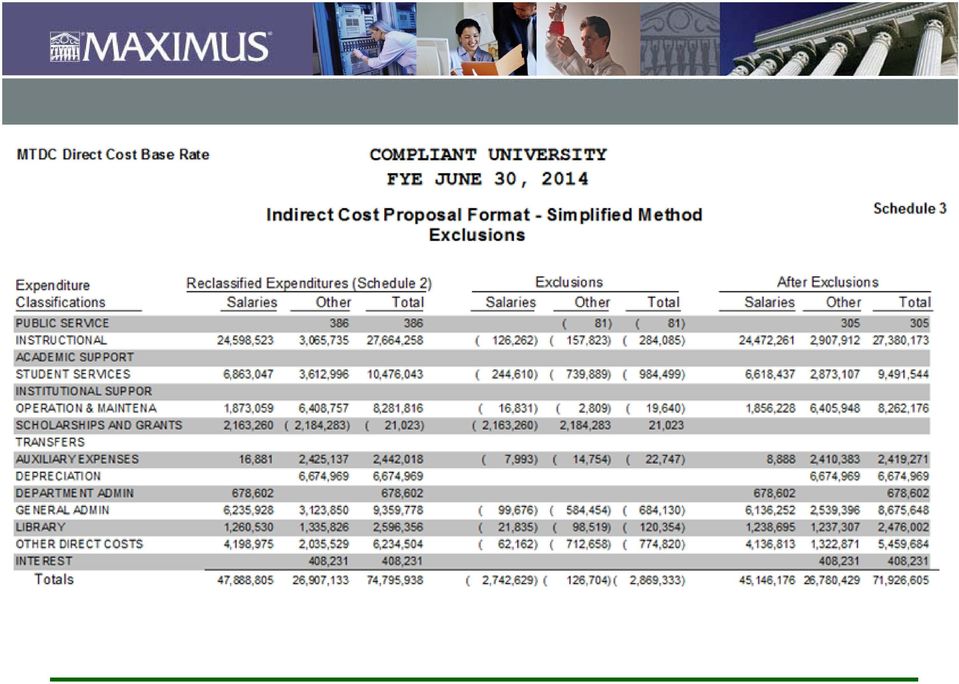

17 Exclusion of Costs Part 220, Section G2 Prescribes Expenditure Eliminations Patient care & tuition remission Scholarships and fellowships Participant Support Subcontract expenditures above $25,000 Sponsor paid facilities rental costs Capital Assets F&A Cost Recovery

18 Exclusion of Costs (cont.) Exclude unallowable expenses DCA Best Practices Manual Appendix E: The treatment of unallowable activities differs from the treatment of other unallowable costs (e.g. bad debt expense) in that the former includes the salaries of personnel which must be included in the salary and wage distribution base in the computation of the indirect cost rate, while the latter are excluded from the rate computation entirely.

in that the former includes the salaries of personnel which must be included in the salary")

19

20 Adjustments for O&M / Interest / Depreciation / SWCAP Part 220, Section F3 allows for inclusion of interest costs on capitalized debt. Administrative costs paid on behalf of the state are also eligible for inclusion. Your state must have an approved SWCAP through DCA. Building and equipment depreciation are shown as an adjustment on Schedule 4. Part 220 also says you need to adjust the costs of O&M, depreciation, and capital interest related to Auxiliaries/OIA.

21

22 Great! All costs are aligned to Part 220! You must now determine which rate base to use. Part 220 allows three different bases: Salaries and Wages Salaries and Wages + Benefits Salaries and Wages + Benefits + Other Expenses (MTDC) S&W provides the highest rate due to the lower base, while MTDC provides the lowest rate due to the larger base, but the latter may provide more F&A recovery. You need to review your grant stream to determine which base to use.

23 Quick Case Study University has the following research expenses projected for FY2014: Salaries and Wages - $3,000,000 Fringes - $1,000,000 Other - $2,000,000 (not including non-f&a expenses) Recovery with 65% S&W base = $1,950,000 Recovery with 55% S&W&F base = $2,200,000 Recovery with 45% MTDC base = $2,700,000 In this scenario, using an MTDC base for the F&A rate provides the best recovery.

24

25 The Final Package 1. Print out final Schedules 1-4, Rate Schedule 2. You will need to footnote Reclassifications, Eliminations and Adjustments (see next slide) 3. Part 220 requires that disclosures/certifications be signed by someone in upper management. 4. A checklist is also required by DCA San Francisco (we include it on all F&A Cost Rate Proposals). 5. Now, you are ready to send the package to the Division of Cost Allocation, a unit of the Department of Health and Human Services.

26

27

28

29

30

31 The Rate Negotiation 1. DCA will audit the cost proposal and will respond with requests for additional data. 2. Then, the institution will negotiate a rate with DCA. 3. The final rate is usually lower than the proposed rate. 4. Institutions may be able to establish a four-year agreement with DCA. 5. If this is the first go-around, DCA may only grant a one-year rate.

32 The Rate Negotiation Risk Areas 1. Make sure unallowable activities are mapped to Other Direct Costs, or some other function that is in the denominator. Unallowable expenses (i.e., bad debt, alcohol) should be taken out of the calculation altogether % DA calculation Review the title codes. DCA will review these and make sure you are not including non-da personnel (i.e., dean of students). 3. Fringe Benefits If you are using a fringe benefit rate, it should be a federally negotiated fringe benefit rate. 4. Space data The more accurate your data, the easier it is to defend. Preferably use Part 220 classifications for your space functionality.

33 Converting from Short to Long Form Weigh the cost to benefit: Long Form may yield a higher rate. Long Form requires more administrative work. Once you go to Long Form you cannot go back to Short Form. Must use MTDC for base, which could be good or bad depending on your grant portfolio.

34 Converting from Short to Long Form Extra administrative work (if you don t do this already): Need departmental space survey data on a room by room basis, classified by Part 220 categories. Need equipment inventory by room, building, or department (room is best). Need building interest broken down by building. Chart of Accounts/Accounting system must be able to properly identify unallowable costs.

35 Converting from Short to Long Form Extra administrative work (continued): Need building depreciation by building. Need equipment depreciation by asset, and be able to differentiate between federally, state, private, or institutionally-funded equipment. Be able to identify employees by class (ex: faculty and professional, administrative, and general support)

36 Questions / Comments Thanks! Jason Guilbeault, Senior Consultant: (847) / JasonRGuilbeault@maximus.com

COLLEGE AND UNIVERSITY COST IDENTIFICATION AND ALLOCATION

NATIONAL ASSOCIATION OF COLLEGE AND UNIVERSITY BUSINESS OFFICERS COLLEGE AND UNIVERSITY COST IDENTIFICATION AND ALLOCATION INTRODUCTION... 2 FINANCIAL / FUND ACCOUNTING...2 WHY FUND ACCOUNTING?... 2 WHAT

NATIONAL ASSOCIATION OF COLLEGE AND UNIVERSITY BUSINESS OFFICERS COLLEGE AND UNIVERSITY COST IDENTIFICATION AND ALLOCATION INTRODUCTION... 2 FINANCIAL / FUND ACCOUNTING...2 WHY FUND ACCOUNTING?... 2 WHAT

Overview of Federal Cost Allocation & Indirect Cost Rates (2 CFR Part 200) for The State of Washington

for The State of Washington") Overview of Federal Cost Allocation & Indirect Cost Rates (2 CFR Part 200) for The State of Washington Presented by: MGT of America, Inc. Bret Schlyer, Director bschlyer@mgtamer.com 316-214-3163 Cost Principles

Overview of Federal Cost Allocation & Indirect Cost Rates (2 CFR Part 200) for The State of Washington Presented by: MGT of America, Inc. Bret Schlyer, Director bschlyer@mgtamer.com 316-214-3163 Cost Principles

1.1.0 Description of Your Cost Accounting System

1.1.0 Description of Your Cost Accounting System The University of California s cost accounting system incorporates data accumulated and recorded in the financial accounting system. The financial statements

1.1.0 Description of Your Cost Accounting System The University of California s cost accounting system incorporates data accumulated and recorded in the financial accounting system. The financial statements

Program Policy Guidance OSHC-2011-06

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT Office of Sustainable Housing and Communities WASHINGTON, DC 20410-0050 Date: April 13, 2011 Program Policy Guidance OSHC-2011-06 Subject: Indirect Cost

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT Office of Sustainable Housing and Communities WASHINGTON, DC 20410-0050 Date: April 13, 2011 Program Policy Guidance OSHC-2011-06 Subject: Indirect Cost

REVIEW GUIDE FOR NON PROFIT ORGANIZATION S INDIRECT COST PROPOSALS

REVIEW GUIDE FOR NON PROFIT ORGANIZATION S INDIRECT COST PROPOSALS U.S. DEPARTMENT OF HEALTH AND HUMAN SERVICES PROGRAM SUPPORT CENTER DIVISION OF COST ALLOCATION 2003 TABLE OF CONTENTS PAGE I. Introduction...

REVIEW GUIDE FOR NON PROFIT ORGANIZATION S INDIRECT COST PROPOSALS U.S. DEPARTMENT OF HEALTH AND HUMAN SERVICES PROGRAM SUPPORT CENTER DIVISION OF COST ALLOCATION 2003 TABLE OF CONTENTS PAGE I. Introduction...

Frequently Asked Questions (FAQ s)

") Questions about Cognizance: Frequently Asked Questions (FAQ s) 1. How can I determine who is my cognizant agency responsible to establish my indirect cost rate(s)? For commercial, for-profit companies

Questions about Cognizance: Frequently Asked Questions (FAQ s) 1. How can I determine who is my cognizant agency responsible to establish my indirect cost rate(s)? For commercial, for-profit companies

Deans, Directors, Department Heads, Business Administrators, Faculty, Finance Personnel, and Sponsored Project Personnel

Northwestern University Title: Applicable to: Calculation of Recharge Center Rates (Step-by-Step Guidance) Deans, Directors, Department Heads, Business Administrators, Faculty, Finance Personnel, and Sponsored

Northwestern University Title: Applicable to: Calculation of Recharge Center Rates (Step-by-Step Guidance) Deans, Directors, Department Heads, Business Administrators, Faculty, Finance Personnel, and Sponsored

The University of Georgia Service Center Policy

TABLE OF CONTENTS The University of Georgia Service Center Policy 1. INTRODUCTION... 4 2. SCOPE... 4 2.1. Recharge Activities... 4 2.2. Service Centers... 4 2.3. Specialized Service Centers... 4 3. INTENT....

TABLE OF CONTENTS The University of Georgia Service Center Policy 1. INTRODUCTION... 4 2. SCOPE... 4 2.1. Recharge Activities... 4 2.2. Service Centers... 4 2.3. Specialized Service Centers... 4 3. INTENT....

SAMPLE INDIRECT COST PROPOSAL FORMAT FOR NONPROFIT ORGANIZATIONS

SAMPLE INDIRECT COST PROPOSAL FORMAT FOR NONPROFIT ORGANIZATIONS A. INTRODUCTION Name of Organization (nonprofit) is a nonprofit located in Anytown, USA. The nonprofit administers a variety of programs

SAMPLE INDIRECT COST PROPOSAL FORMAT FOR NONPROFIT ORGANIZATIONS A. INTRODUCTION Name of Organization (nonprofit) is a nonprofit located in Anytown, USA. The nonprofit administers a variety of programs

DIVISION OF RESEARCH RECHARGE FACILITIES OPERATING PROCEDURES. August 2012. 11200 SW 8th Street MARC 430 Miami, FL 33199 http://research.fiu.

DIVISION OF RESEARCH RECHARGE FACILITIES OPERATING PROCEDURES August 2012 11200 SW 8th Street MARC 430 Miami, FL 33199 http://research.fiu.edu Table of Contents Recharge Service Facility Operating Procedures

DIVISION OF RESEARCH RECHARGE FACILITIES OPERATING PROCEDURES August 2012 11200 SW 8th Street MARC 430 Miami, FL 33199 http://research.fiu.edu Table of Contents Recharge Service Facility Operating Procedures

UNIVERSITY OF OKLAHOMA/NORMAN CAMPUS OFFICE OF RESEARCH SERVICES Procedures Guide. Recharge Center Operations

UNIVERSITY OF OKLAHOMA/NORMAN CAMPUS OFFICE OF RESEARCH SERVICES Procedures Guide Recharge Center Operations Overview 3 Establishing a Recharge Center 3 Information that Will Need to be Determined 3 Rate

UNIVERSITY OF OKLAHOMA/NORMAN CAMPUS OFFICE OF RESEARCH SERVICES Procedures Guide Recharge Center Operations Overview 3 Establishing a Recharge Center 3 Information that Will Need to be Determined 3 Rate

Preparing a Budget for a Research Grant Proposal. Office of Sponsored Projects Faculty Education Working Group http://www.dartmouth.

Preparing a Budget for a Research Grant Proposal Office of Sponsored Projects Faculty Education Working Group http://www.dartmouth.edu/~osp Table of Contents 1. SOLICITATIONS 2. THE PURPOSE & IMPORTANCE

Preparing a Budget for a Research Grant Proposal Office of Sponsored Projects Faculty Education Working Group http://www.dartmouth.edu/~osp Table of Contents 1. SOLICITATIONS 2. THE PURPOSE & IMPORTANCE

U.S. Fish and Wildlife Service Financial Assistance Business Process Indirect Costs and Negotiated Indirect Cost Rate Agreements

U.S. Fish and Wildlife Service Financial Assistance Business Process Indirect Costs and Negotiated Indirect Cost Rate Agreements Definitions Term Cognizant agency for indirect costs Direct costs Indirect

U.S. Fish and Wildlife Service Financial Assistance Business Process Indirect Costs and Negotiated Indirect Cost Rate Agreements Definitions Term Cognizant agency for indirect costs Direct costs Indirect

ILLINOIS DEPARTMENT OF HUMAN SERVICES INSTRUCTIONS FOR GRANT REPORT

ILLINOIS DEPARTMENT OF HUMAN SERVICES INSTRUCTIONS FOR GRANT REPORT Page 1 of 2: Grant Report for the period July 1 ST through June 30 TH Enter the agency name and FEIN (Federal Employment Identification

ILLINOIS DEPARTMENT OF HUMAN SERVICES INSTRUCTIONS FOR GRANT REPORT Page 1 of 2: Grant Report for the period July 1 ST through June 30 TH Enter the agency name and FEIN (Federal Employment Identification

under Federal Grants/Cooperative Agreements and Cost Reimbursement Contracts (Rev. 7/15/14)

") CHARGING OF DIRECT and INDIRECT COSTS under Federal Grants/Cooperative Agreements and Cost Reimbursement Contracts (Rev. 7/15/14) Direct Costs are those costs which are allowed to be reimbursed under federal

CHARGING OF DIRECT and INDIRECT COSTS under Federal Grants/Cooperative Agreements and Cost Reimbursement Contracts (Rev. 7/15/14) Direct Costs are those costs which are allowed to be reimbursed under federal

Cost Accounting Standards Board. Disclosure Statement for Educational Institutions CASB DS-2. University of Central Florida Resubmission No.

Cost Accounting Standards Board Disclosure Statement for Educational Institutions CASB DS-2 Resubmission No. 3 Effective July 1, 2005 FORM APPROVED OMB NUMBER 0348-0055 COST ACCOUNTING STANDARDS BOARD

Cost Accounting Standards Board Disclosure Statement for Educational Institutions CASB DS-2 Resubmission No. 3 Effective July 1, 2005 FORM APPROVED OMB NUMBER 0348-0055 COST ACCOUNTING STANDARDS BOARD

Unrelated Business Income Taxes (UBIT), Weill Cornell Medical College - Qatar

, Weill Cornell Medical College - Qatar") INTERIM Issued: June 4, 2004 CORNELL UNIVERSITY POLICY LIBRARY Unrelated Business Income Taxes (UBIT), Weill Cornell Medical College - Qatar POLICY 3.15.2 Responsible Executive: Dean, POLICY STATEMENT

INTERIM Issued: June 4, 2004 CORNELL UNIVERSITY POLICY LIBRARY Unrelated Business Income Taxes (UBIT), Weill Cornell Medical College - Qatar POLICY 3.15.2 Responsible Executive: Dean, POLICY STATEMENT

Research Administration at the University of Maryland

Research Administration at the University of Maryland Anne S. Geronimo, M.S. Director, Research Development Division of Research University of Maryland June 2007 Tokyo, Japan University of Maryland Profile

Research Administration at the University of Maryland Anne S. Geronimo, M.S. Director, Research Development Division of Research University of Maryland June 2007 Tokyo, Japan University of Maryland Profile

10/30/2015. Uniform Guidance: Cost Principles. Why This Session Is Needed. Lesson Overview & Module Objectives. Changes to many Cost Principles and

Uniform Guidance: Cost Principles Uniform Guidance: Cost Principles 1 Why This Session Is Needed Changes to many Cost Principles and Selected Items of Cost Impact of changes on current operations Required

Uniform Guidance: Cost Principles Uniform Guidance: Cost Principles 1 Why This Session Is Needed Changes to many Cost Principles and Selected Items of Cost Impact of changes on current operations Required

2015 NEROAC Session # 27, May 5, 2015 10:15 am San Diego, California Indirect Costs

2015 NEROAC Session # 27, May 5, 2015 10:15 am San Diego, California Indirect Costs Edward Nwaba, MBA, CPA Director, Awards Management Division Office of Grants and Financial Management, NIFA/USDA Agenda

2015 NEROAC Session # 27, May 5, 2015 10:15 am San Diego, California Indirect Costs Edward Nwaba, MBA, CPA Director, Awards Management Division Office of Grants and Financial Management, NIFA/USDA Agenda

Charging of Direct Costs to Sponsored Projects: Policy

Charging of Direct Costs to Sponsored Projects: Policy Policy Sections Policy Statement Reason for Policy Who Should Know This Policy Contacts Applicable WMC Policies Applicable Federal Regulations & Criteria

Charging of Direct Costs to Sponsored Projects: Policy Policy Sections Policy Statement Reason for Policy Who Should Know This Policy Contacts Applicable WMC Policies Applicable Federal Regulations & Criteria

Syracuse University Interdepartmental Recharge Centers

Syracuse University Interdepartmental Recharge Centers Policy Implementation Recharge Centers Recharge centers are departments or functional units that provide goods and services primarily for the benefit

Syracuse University Interdepartmental Recharge Centers Policy Implementation Recharge Centers Recharge centers are departments or functional units that provide goods and services primarily for the benefit

Core Research Facilities & Service Centers for the New Administrator

Core Research Facilities & Service Centers for the New Administrator David Ngo, University of Texas Southwestern Medical Center at Dallas Zach Belton, Huron Consulting Group Agenda Service center basics

Core Research Facilities & Service Centers for the New Administrator David Ngo, University of Texas Southwestern Medical Center at Dallas Zach Belton, Huron Consulting Group Agenda Service center basics

COST ACCOUNTING STANDARDS BOARD DISCLOSURE STATEMENT FOR EDUCATIONAL INSTITUTIONS CASB DS-2

FOR CASB DS-2 Revision Number 3 Effective Date July 01, 2004 INDEX GENERAL INSTRUCTIONS -- Continuation Sheet...(i) COVER SHEET AND CERTIFICATION... C-1 PART I General Information... I-1 PART II PART III

FOR CASB DS-2 Revision Number 3 Effective Date July 01, 2004 INDEX GENERAL INSTRUCTIONS -- Continuation Sheet...(i) COVER SHEET AND CERTIFICATION... C-1 PART I General Information... I-1 PART II PART III

U.S. universities, U.S. community colleges

Indirect Cost Policy for Project Grants and Contracts for Applicant Organizations Definition The Bill & Melinda Gates Foundation defines indirect costs as: Overhead expenses or ongoing operational costs

Indirect Cost Policy for Project Grants and Contracts for Applicant Organizations Definition The Bill & Melinda Gates Foundation defines indirect costs as: Overhead expenses or ongoing operational costs

Unallowable Cost Categories (in alphabetical order)

") Unallowable Cost Definitions Unallowable costs are those costs that cannot be charged to the Federal Government or included in the Facilities and Administrative (indirect) cost rate. Overview The Office

Unallowable Cost Definitions Unallowable costs are those costs that cannot be charged to the Federal Government or included in the Facilities and Administrative (indirect) cost rate. Overview The Office

GRANTS PROCEDURES MANUAL. Office of Grants and Foundation Relations April 2016. Rev 4/5/16

GRANTS PROCEDURES MANUAL Office of Grants and Foundation Relations April 2016 Rev 4/5/16 The Whitman College Office of Grants & Foundation Relations, in collaboration with the Business Office, has developed

GRANTS PROCEDURES MANUAL Office of Grants and Foundation Relations April 2016 Rev 4/5/16 The Whitman College Office of Grants & Foundation Relations, in collaboration with the Business Office, has developed

How To Audit An Educational Institution

March 26, 2015 13(1) CHAPTER 13 Table of Contents Paragraph Page 13-000 Audits at Educational Institutions, Nonprofit Organizations, and Federally Funded Research and Development Centers (FFRDCs) 13-001

March 26, 2015 13(1) CHAPTER 13 Table of Contents Paragraph Page 13-000 Audits at Educational Institutions, Nonprofit Organizations, and Federally Funded Research and Development Centers (FFRDCs) 13-001

GRANTS PROCEDURES MANUAL

GRANTS PROCEDURES MANUAL Office of Sponsored Programs Office of Foundation & Corporate Relations April 2013 Grants Procedures Manual The Whitman College Office of Sponsored Programs, in collaboration with

GRANTS PROCEDURES MANUAL Office of Sponsored Programs Office of Foundation & Corporate Relations April 2013 Grants Procedures Manual The Whitman College Office of Sponsored Programs, in collaboration with

The President s Emergency Plan for AIDS Relief. How to Manage USG Grants

The President s Emergency Plan for AIDS Relief How to Manage USG Grants Code of Federal Regulations (CFR) OMB Circulars A - 133 A - 122 (or A - 21) A - 110 / 22 CFR 226 (or other agency version) Automated

The President s Emergency Plan for AIDS Relief How to Manage USG Grants Code of Federal Regulations (CFR) OMB Circulars A - 133 A - 122 (or A - 21) A - 110 / 22 CFR 226 (or other agency version) Automated

SLIPPERY ROCK UNIVERSITY. OFFICE OF GRANTS AND SPONSORED RESEARCH Cost Sharing on Externally Sponsored Projects

SLIPPERY ROCK UNIVERSITY A. Purpose & Scope OFFICE OF GRANTS AND SPONSORED RESEARCH Cost Sharing on Externally Sponsored Projects This policy sets forth the guidelines for committing cost share or matching

SLIPPERY ROCK UNIVERSITY A. Purpose & Scope OFFICE OF GRANTS AND SPONSORED RESEARCH Cost Sharing on Externally Sponsored Projects This policy sets forth the guidelines for committing cost share or matching

OMB. Uniform Guidance

2014 OMB Uniform Guidance Assessing the OMB Uniform Guidance: Major Changes and Impacts The Office of Management and Budget (OMB) consolidated the federal government s guidance on Uniform Administrative

2014 OMB Uniform Guidance Assessing the OMB Uniform Guidance: Major Changes and Impacts The Office of Management and Budget (OMB) consolidated the federal government s guidance on Uniform Administrative

The Cost of College Project

The Cost of College Project Instructions for Data Completion National Association of College and University Business Officers 2501 M Street, N.W., Suite 400 Washington, DC 20037-1308 Table of Contents

The Cost of College Project Instructions for Data Completion National Association of College and University Business Officers 2501 M Street, N.W., Suite 400 Washington, DC 20037-1308 Table of Contents

Account Groups. Table of Contents. VII. 32 accounts - Loan Funds Purpose, Source of Funds, Typical Expenditures, Transfers, Restrictions

Account Groups Table of Contents I. 14 accounts - Education and General Funds Purpose, Source of funds, Typical Expenditures, Transfers, Restrictions, Travel, Balance II. 18 accounts - Service Center Revolving

Account Groups Table of Contents I. 14 accounts - Education and General Funds Purpose, Source of funds, Typical Expenditures, Transfers, Restrictions, Travel, Balance II. 18 accounts - Service Center Revolving

Effective Date: 27 June 2013 Presidents Council Approval: 29 April 2013 Board Approval: 27 June 2013. 1. Purpose

Davis Applied Technology College: A Utah College of Applied Technology Campus Restricted Fund Accounting Sponsored Project Contracts, Custom Fit, & Grants 1. Purpose Effective Date: 27 June 2013 Presidents

Davis Applied Technology College: A Utah College of Applied Technology Campus Restricted Fund Accounting Sponsored Project Contracts, Custom Fit, & Grants 1. Purpose Effective Date: 27 June 2013 Presidents

Operations and Maintenance (O&M)

") Operations and Maintenance (O&M) Uniform Guidance, Appendix III, B. 4. Expenses incurred for administration, supervision, operation, maintenance, preservation and protection of the institution s physical

Operations and Maintenance (O&M) Uniform Guidance, Appendix III, B. 4. Expenses incurred for administration, supervision, operation, maintenance, preservation and protection of the institution s physical

SECTION III. Examples of Exhibits to Support Indirect Cost Rate Proposals

SECTION III Examples of Exhibits to Support Indirect Cost Rate Proposals SECTION III Examples of Exhibits to Support Indirect Cost Rate Proposals Index Exhibits Description Page Numbers Exhibit A Personnel

SECTION III Examples of Exhibits to Support Indirect Cost Rate Proposals SECTION III Examples of Exhibits to Support Indirect Cost Rate Proposals Index Exhibits Description Page Numbers Exhibit A Personnel

I. BACKGROUND INFORMATION

TO: FROM: Board of Trustees Kirsten M. Volpi Executive Vice President for Finance and Administration DATE: May 18, 2015 SUBJECT: FY 2016 Budget I. BACKGROUND INFORMATION As we approach fiscal year 2016

TO: FROM: Board of Trustees Kirsten M. Volpi Executive Vice President for Finance and Administration DATE: May 18, 2015 SUBJECT: FY 2016 Budget I. BACKGROUND INFORMATION As we approach fiscal year 2016

A Guide for Indirect Cost Rate Determination

A Guide for Indirect Cost Rate Determination Based on the Cost Principles and Procedures Required by OMB Circular A-122 (2 CFR Part 230) for Non-profit Organizations and by the Federal Acquisition Regulation

A Guide for Indirect Cost Rate Determination Based on the Cost Principles and Procedures Required by OMB Circular A-122 (2 CFR Part 230) for Non-profit Organizations and by the Federal Acquisition Regulation

services, or disposal of surplus equipment.

Accounting 1 II B 18 Allowable N/A CPRIT awards - indirect costs Advertising 2 II B 18 Allowable Allowable only for recruitment of Unallowable-(1) All advertising and public relations personnel, the procurement

Accounting 1 II B 18 Allowable N/A CPRIT awards - indirect costs Advertising 2 II B 18 Allowable Allowable only for recruitment of Unallowable-(1) All advertising and public relations personnel, the procurement

Research Administration at The University of Chicago

Research Administration at The University of Chicago Mary Ellen Sheridan, Ph.D. Associate Vice President for Research University Research Administration University of Chicago Outline of JST Seminar Facts

Research Administration at The University of Chicago Mary Ellen Sheridan, Ph.D. Associate Vice President for Research University Research Administration University of Chicago Outline of JST Seminar Facts

Budget and Financial Planning at UMass Boston. Presentation to: Faculty Council February 7, 2011

Budget and Financial Planning at UMass Boston Presentation to: Faculty Council February 7, 2011 Three Year Investment Scenario Investments in UMass Boston: New Resources in Recent Operating Budgets Through

Budget and Financial Planning at UMass Boston Presentation to: Faculty Council February 7, 2011 Three Year Investment Scenario Investments in UMass Boston: New Resources in Recent Operating Budgets Through

General Information. the ratio between the total indirect expenses and some direct cost base.

These guidelines include information related to: General Information A. Definition of Indirect Costs B. Types of Indirect Rates C. Determination of Indirect Cost Rates and Cost Allocation D. Submissions

These guidelines include information related to: General Information A. Definition of Indirect Costs B. Types of Indirect Rates C. Determination of Indirect Cost Rates and Cost Allocation D. Submissions

New Jersey Department of Transportation Bureau of Research Guidelines for Preparing and Reviewing Budgets and Invoices for Fixed-Price Agreements

New Jersey Department of Transportation Bureau of Research Guidelines for Preparing and Reviewing Budgets and Invoices for Fixed-Price Agreements INTRODUCTION This Guide is intended as a general resource

New Jersey Department of Transportation Bureau of Research Guidelines for Preparing and Reviewing Budgets and Invoices for Fixed-Price Agreements INTRODUCTION This Guide is intended as a general resource

Capital Area Council of Governments FY 2015 Cost Allocation Plan

Capital Area Council of Governments FY 2015 Cost Allocation Plan The Capital Area Council of Governments uses the cost allocation method prescribed in OMB Circular A 87, Department of Health and Human

Capital Area Council of Governments FY 2015 Cost Allocation Plan The Capital Area Council of Governments uses the cost allocation method prescribed in OMB Circular A 87, Department of Health and Human

Presenting the Numbers: Accounting Systems for Government Contractors

Presenting the Numbers: Accounting Systems for Government Contractors William D. Craven, CPA Senior Cost/Price Analyst CH2M HILL Plateau Remediation Company William D. Craven, CPA, CMA, CIA Cost/Price

Presenting the Numbers: Accounting Systems for Government Contractors William D. Craven, CPA Senior Cost/Price Analyst CH2M HILL Plateau Remediation Company William D. Craven, CPA, CMA, CIA Cost/Price

CIRCULAR NO. A-122 Revised May 10, 2004

TO THE HEADS OF EXECUTIVE DEPARTMENTS AND ESTABLISHMENTS SUBJECT: Cost Principles for Non-Profit Organizations CIRCULAR NO. A-122 Revised May 10, 2004 1. Purpose. This Circular establishes principles for

TO THE HEADS OF EXECUTIVE DEPARTMENTS AND ESTABLISHMENTS SUBJECT: Cost Principles for Non-Profit Organizations CIRCULAR NO. A-122 Revised May 10, 2004 1. Purpose. This Circular establishes principles for

Office of the President Phone: 774.455.7710 333 South Street, Suite 400 Fax: 774-455-7730

Office of the President Phone: 774.455.7710 333 South Street, Suite 400 Fax: 774-455-7730 Shrewsbury, Massachusetts 01545 www.massachusetts.edu As part of the Commonwealth s budget process, the University

Office of the President Phone: 774.455.7710 333 South Street, Suite 400 Fax: 774-455-7730 Shrewsbury, Massachusetts 01545 www.massachusetts.edu As part of the Commonwealth s budget process, the University

Newark Grants Office FAQ's

Newark Grants Office FAQ's 1. What is a grant? 2. What is a contract? 3. What is the difference between the Newark Grants Office (NGO) and the Post Award Department? 4. What are the responsibilities of

Newark Grants Office FAQ's 1. What is a grant? 2. What is a contract? 3. What is the difference between the Newark Grants Office (NGO) and the Post Award Department? 4. What are the responsibilities of

University of Illinois at Urbana-Champaign FY16 Provisional Facilities/Administrative (F&A), Tuition Remission, and Fringe Benefit Rates

, Tuition Remission, and Fringe Benefit Rates") Updated 7/29/15 University of Illinois at Urbana-Champaign FY16 Provisional Facilities/Administrative (F&A), Tuition Remission, and Fringe Benefit Rates FACILITIES AND ADMINISTRATION (F&A) RATES On-Campus

Updated 7/29/15 University of Illinois at Urbana-Champaign FY16 Provisional Facilities/Administrative (F&A), Tuition Remission, and Fringe Benefit Rates FACILITIES AND ADMINISTRATION (F&A) RATES On-Campus

Budgets and Financial Monitoring Tools and Tips. January 21, 2014

Budgets and Financial Monitoring Tools and Tips January 21, 2014 Overview Setting the stage with regulatory framework Circulars and general ideas and principles behind them Changes to OMB with the recently

Budgets and Financial Monitoring Tools and Tips January 21, 2014 Overview Setting the stage with regulatory framework Circulars and general ideas and principles behind them Changes to OMB with the recently

VANDERBILT UNIVERSITY SERVICE CENTER POLICY

VANDERBILT UNIVERSITY SERVICE CENTER POLICY EFFECTIVE DATE: JULY 1, 2008 I. POLICY STATEMENT Vanderbilt University operating units that charge internal users for goods and services are required to document

VANDERBILT UNIVERSITY SERVICE CENTER POLICY EFFECTIVE DATE: JULY 1, 2008 I. POLICY STATEMENT Vanderbilt University operating units that charge internal users for goods and services are required to document

Procedures and Guidelines for External Grants and Sponsored Programs

Definitions: Procedures and Guidelines for External Grants and Sponsored Programs 1. Grant and Contract Financial Administration Office (Grants Office): The office within the Accounting Operations Area

Definitions: Procedures and Guidelines for External Grants and Sponsored Programs 1. Grant and Contract Financial Administration Office (Grants Office): The office within the Accounting Operations Area

A Guide for Indirect Cost Rate Determination

A Guide for Indirect Cost Rate Determination Based on the Cost Principles and Procedures Required by OMB Circular A-122 (2 CFR Part 230) for Non-profit Organizations and by the Federal Acquisition Regulation

A Guide for Indirect Cost Rate Determination Based on the Cost Principles and Procedures Required by OMB Circular A-122 (2 CFR Part 230) for Non-profit Organizations and by the Federal Acquisition Regulation

ALLOCATION AND CHARGING OF DIRECT AND INDIRECT COSTS AT THE UNIVERSITY OF ROCHESTER

ALLOCATION AND CHARGING OF DIRECT AND INDIRECT COSTS AT THE UNIVERSITY OF ROCHESTER OVERVIEW Federal regulation mandates that universities establish consistent practices for defining and charging costs

ALLOCATION AND CHARGING OF DIRECT AND INDIRECT COSTS AT THE UNIVERSITY OF ROCHESTER OVERVIEW Federal regulation mandates that universities establish consistent practices for defining and charging costs

200.110 Effective/applicability date

Administrative Changes Kris Rhodes, Director 200.110 Effective/applicability date Final rule issued 12/26/2013 Federal agencies submit drafts implementing regulations to OMB by June 2014 Uniform implementation

Administrative Changes Kris Rhodes, Director 200.110 Effective/applicability date Final rule issued 12/26/2013 Federal agencies submit drafts implementing regulations to OMB by June 2014 Uniform implementation

Advisory Report 2010-1

Advisory Report 2010-1 National Association of College and University Business Officers www.nacubo.org Public Institutions: Methodologies for Allocating Depreciation, Operation and Maintenance of Plant,

Advisory Report 2010-1 National Association of College and University Business Officers www.nacubo.org Public Institutions: Methodologies for Allocating Depreciation, Operation and Maintenance of Plant,

You've successfully subscribed to this feed! Updated content can be viewed in Internet Explorer and other programs that use the Common Feed List.

Page 1 of 5 You've successfully subscribed to this feed! Updated content can be viewed in Internet Explorer and other programs that use the Common Feed List. View my feeds DCAA News Thursday, May 28, 2009,

Page 1 of 5 You've successfully subscribed to this feed! Updated content can be viewed in Internet Explorer and other programs that use the Common Feed List. View my feeds DCAA News Thursday, May 28, 2009,

Wisconsin Partnership Program Policy on Allowable and Non-Allowable Grant Expenses

Wisconsin Partnership Program Policy on Allowable and Non-Allowable Grant Expenses Revised 9/19/2014 The Wisconsin Partnership Program (WPP) has specific policies on allowable and non-allowable expenses

Wisconsin Partnership Program Policy on Allowable and Non-Allowable Grant Expenses Revised 9/19/2014 The Wisconsin Partnership Program (WPP) has specific policies on allowable and non-allowable expenses

ELECTRONIC CODE OF FEDERAL REGULATIONS

About GPO Newsroom/Media Congressional Relations Inspector General Careers Contact askgpo Help Home Customers Vendors Libraries FDsys: GPO's Federal Digital System About FDsys Search Government Publications

About GPO Newsroom/Media Congressional Relations Inspector General Careers Contact askgpo Help Home Customers Vendors Libraries FDsys: GPO's Federal Digital System About FDsys Search Government Publications

Federal Register / Vol. 70, No. 168 / Wednesday, August 31, 2005 / Rules and Regulations 51927

Federal Register / Vol. 70, No. 168 / Wednesday, August 31, 2005 / Rules and Regulations 51927 occurs, the governmental unit should be guided by the requirements in Appendix C to this part relating to

Federal Register / Vol. 70, No. 168 / Wednesday, August 31, 2005 / Rules and Regulations 51927 occurs, the governmental unit should be guided by the requirements in Appendix C to this part relating to

Provisional Billing Rates. Beth Citeroni Acquisition Cost/Price Analyst

Provisional Billing Rates Beth Citeroni Acquisition Cost/Price Analyst Definition FAR 42.701 Provisional rate or billing rate is an established temporary indirect rate applicable to a specified period

Provisional Billing Rates Beth Citeroni Acquisition Cost/Price Analyst Definition FAR 42.701 Provisional rate or billing rate is an established temporary indirect rate applicable to a specified period

Office of Sponsored Research

UG QUICK GUIDE (Vol. 1) MAJOR CHANGES IN THE UNIFORM GUIDANCE AFFECTING PROPOSAL BUDGETS AND CHARGING OF DIRECT COSTS The Office of Management and Budget (OMB) has combined many of the federal circulars

UG QUICK GUIDE (Vol. 1) MAJOR CHANGES IN THE UNIFORM GUIDANCE AFFECTING PROPOSAL BUDGETS AND CHARGING OF DIRECT COSTS The Office of Management and Budget (OMB) has combined many of the federal circulars

Is is Direct? Is it Indirect?

Attachment 19 Cost Principles Applicable to Grants and Contracts with State and Local Governments (0MB Circular A-87) Exercise 3 Is it Allowable? Is it Unallowable? Is is Direct? Is it Indirect? 1 The

Attachment 19 Cost Principles Applicable to Grants and Contracts with State and Local Governments (0MB Circular A-87) Exercise 3 Is it Allowable? Is it Unallowable? Is is Direct? Is it Indirect? 1 The

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AT 2 CFR 200

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AT 2 CFR 200 November 11, 2014 WHAT S CHANGING AND WHEN? Grants Reform Office of Management and Budget Circulars

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AT 2 CFR 200 November 11, 2014 WHAT S CHANGING AND WHEN? Grants Reform Office of Management and Budget Circulars

Service Centers Reference Manual

Service Centers Reference Manual The Nuts and Bolts of Service Centers FY 2010 SOM Division of Finance and Office of Research Compliance and Integrity University of Pennsylvania School of Medicine Table

Service Centers Reference Manual The Nuts and Bolts of Service Centers FY 2010 SOM Division of Finance and Office of Research Compliance and Integrity University of Pennsylvania School of Medicine Table

2014 Higher Education Accounting Forum

2014 Higher Education Accounting Forum The Accounting of RCM April 28, 2014 Conference Session Speakers Name Title Organization Andrew L. Laws Managing Director (session facilitator) Huron Consulting Group

2014 Higher Education Accounting Forum The Accounting of RCM April 28, 2014 Conference Session Speakers Name Title Organization Andrew L. Laws Managing Director (session facilitator) Huron Consulting Group

University of California, Berkeley MANAGEMENT S DISCUSSION AND ANALYSIS (UNAUDITED)

") The objective of Management s Discussion & Analysis (MD&A) is to help readers of the financial statements of the University of California, Berkeley (Berkeley) better understand the financial position and

The objective of Management s Discussion & Analysis (MD&A) is to help readers of the financial statements of the University of California, Berkeley (Berkeley) better understand the financial position and

Office of Financial Services March 2003

Business Expense Guidelines Page 1 California Institute of Technology BUSINESS EXPENSE GUIDELINES Office of Financial Services March 2003 Revision date: 9/12/05 Business Expense Guidelines Page 2 Contents

Business Expense Guidelines Page 1 California Institute of Technology BUSINESS EXPENSE GUIDELINES Office of Financial Services March 2003 Revision date: 9/12/05 Business Expense Guidelines Page 2 Contents

Allowable and Unallowable Costs Reference Guide Description Allowable Unallowable

1 Advertizing and Public Relations 200.421 Advertizing and Public relations costs for: Advertizing and Public relations costs for: The term advertising costs means the costs of advertising media and corollary

1 Advertizing and Public Relations 200.421 Advertizing and Public relations costs for: Advertizing and Public relations costs for: The term advertising costs means the costs of advertising media and corollary

REVENUE AND EXPENDITURE/EXPENSE ANALYSIS

THE UNIVERSITY OF TEXAS SYSTEM OFFICE OF THE CONTROLLER REVENUE AND EXPENDITURE/EXPENSE ANALYSIS 1999 2008 2009 Update 201 Seventh Street, ASH 5 th Floor Austin, Texas 78701 512.499.4527 www.utsystem.edu/cont

THE UNIVERSITY OF TEXAS SYSTEM OFFICE OF THE CONTROLLER REVENUE AND EXPENDITURE/EXPENSE ANALYSIS 1999 2008 2009 Update 201 Seventh Street, ASH 5 th Floor Austin, Texas 78701 512.499.4527 www.utsystem.edu/cont

Emory Research A-to-Z

Emory Research A-to-Z May 16, 2013 OSP OGCA OTT ORC COI EHSO IRB OCR IACUC DAR Reminders: NEXT MEETING: July 18, 2013 9:30 am to 11:00 am Woodruff Health Sciences Administration Building Auditorium, 1440

Emory Research A-to-Z May 16, 2013 OSP OGCA OTT ORC COI EHSO IRB OCR IACUC DAR Reminders: NEXT MEETING: July 18, 2013 9:30 am to 11:00 am Woodruff Health Sciences Administration Building Auditorium, 1440

Kirsten Volpi Senior Vice President for Finance and Administration

TO: FROM: Board of Trustees Kirsten Volpi Senior Vice President for Finance and Administration DATE: May 23, 2011 SUBJECT: FY 2012 Budget I. BACKGROUND INFORMATION Fiscal Year 2012 Operating Budget Summary

TO: FROM: Board of Trustees Kirsten Volpi Senior Vice President for Finance and Administration DATE: May 23, 2011 SUBJECT: FY 2012 Budget I. BACKGROUND INFORMATION Fiscal Year 2012 Operating Budget Summary

Timekeeping Case Study #1 [OIG Audit Report No. 11 15]

![Timekeeping Case Study #1 [OIG Audit Report No. 11 15]](/thumbs/27/10491628.jpg "Timekeeping Case Study #1 [OIG Audit Report No. 11 15]") Timekeeping Case Study #1 [OIG Audit Report No. 11 15] Finding: 1. This local government grantee claimed $8,940 of site supervisor salaries in January 2009 for work performed in December 2008. It provided

Timekeeping Case Study #1 [OIG Audit Report No. 11 15] Finding: 1. This local government grantee claimed $8,940 of site supervisor salaries in January 2009 for work performed in December 2008. It provided

Northern Marianas College Fiscal Year 2013 Operations Budget and Financial Plan

Northern Marianas College Fiscal Year 2013 Operations Budget and Financial Plan General Information The Northern Marianas College (NMC) has been no stranger to financial struggles during the turbulent

Northern Marianas College Fiscal Year 2013 Operations Budget and Financial Plan General Information The Northern Marianas College (NMC) has been no stranger to financial struggles during the turbulent

Frequently Asked Questions Updated: September 2015

Frequently Asked Questions Updated: September 2015 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200

Frequently Asked Questions Updated: September 2015 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200

Indirect Cost Rate Agreement Guide for Non-Profit Organizations

U.S. Department of Veterans Affairs Homeless Providers Grant and Per Diem Program Indirect Cost Rate Agreement Guide for Non-Profit Organizations Based on the Cost Principles and Procedures Required under

U.S. Department of Veterans Affairs Homeless Providers Grant and Per Diem Program Indirect Cost Rate Agreement Guide for Non-Profit Organizations Based on the Cost Principles and Procedures Required under

University of Alaska Facilities and Administrative Cost Guidelines FY02 FY04

University of Alaska Facilities and Administrative Cost Guidelines FY02 FY04 A. General The purpose and intent of this document is to establish the basis and methodology for developing the university's

University of Alaska Facilities and Administrative Cost Guidelines FY02 FY04 A. General The purpose and intent of this document is to establish the basis and methodology for developing the university's

COST ACCOUNTING STANDARDS BOARD DISCLOSURE STATEMENT FOR EDUCATIONAL INSTITUTIONS CASB DS-2

FOR CASB DS-2 INDEX GENERAL INSTRUCTIONS -- Continuation Sheet...(i) COVER SHEET AND CERTIFICATION...C-1 PART I General Information... I-1 PART II PART III PART IV PART V PART VI PART VII Direct Costs...II-1

FOR CASB DS-2 INDEX GENERAL INSTRUCTIONS -- Continuation Sheet...(i) COVER SHEET AND CERTIFICATION...C-1 PART I General Information... I-1 PART II PART III PART IV PART V PART VI PART VII Direct Costs...II-1

TABLE OF CONTENTS CHAPTER 9

TABLE OF CONTENTS CHAPTER 9 Purpose...1 Balance Sheet Accounts...1 Assets...1 Cash...1 Accounts Receivable...2 Accounts Receivable Allowances...4 Loans and Notes Receivable...4 Loans and Notes Allowances...5

TABLE OF CONTENTS CHAPTER 9 Purpose...1 Balance Sheet Accounts...1 Assets...1 Cash...1 Accounts Receivable...2 Accounts Receivable Allowances...4 Loans and Notes Receivable...4 Loans and Notes Allowances...5

Accounting Overview Training. Revised on 4-24-14

Accounting Overview Training Revised on 4-24-14 Purpose of Accounting Overview Training To provide University Business Managers and Financial Administrators with 1. A basic understanding of the authoritative

Accounting Overview Training Revised on 4-24-14 Purpose of Accounting Overview Training To provide University Business Managers and Financial Administrators with 1. A basic understanding of the authoritative

The Large Public University

By Kenneth A. Jessell PhD. CFO Perspectives Additional Perspectives CFO Perspectives: The Large Public University is one in a series of white papers that looks at the role of the CFO within different institutional

By Kenneth A. Jessell PhD. CFO Perspectives Additional Perspectives CFO Perspectives: The Large Public University is one in a series of white papers that looks at the role of the CFO within different institutional

EXECUTIVE SUMMARY BACKGROUND

EXECUTIVE SUMMARY BACKGROUND Title XIX of the Social Security Act (the Act) established the Medicaid program to pay for the medical assistance costs of certain individuals and families with limited incomes

EXECUTIVE SUMMARY BACKGROUND Title XIX of the Social Security Act (the Act) established the Medicaid program to pay for the medical assistance costs of certain individuals and families with limited incomes

The Colleges of the Seneca Financial Statements May 31, 2007 and 2006

Financial Statements PricewaterhouseCoopers LLP 1100 Bausch & Lomb Place Rochester NY 14604-2705 Telephone (585) 232 4000 Facsimile (585) 454 6594 Report of Independent Auditors To the Board of Trustees

Financial Statements PricewaterhouseCoopers LLP 1100 Bausch & Lomb Place Rochester NY 14604-2705 Telephone (585) 232 4000 Facsimile (585) 454 6594 Report of Independent Auditors To the Board of Trustees

FOUR TESTS OF ALLOWABILITY: An allowable cost must pass all four tests, otherwise it is unallowable.

COST POLICY A critical responsibility in the post award administration of sponsored projects is to ensure that all costs charged are ALLOWABLE, ALLOCABLE and REASONABLE under the approved budget and the

COST POLICY A critical responsibility in the post award administration of sponsored projects is to ensure that all costs charged are ALLOWABLE, ALLOCABLE and REASONABLE under the approved budget and the

PROFESSIONAL MASTERS

PROFESSIONAL MASTERS PROGRAM GUIDELINES West Lafayette Campus August 2012 Definition of Professional Masters Program The characteristics of a Professional Masters program at Purdue as outlined below provide

PROFESSIONAL MASTERS PROGRAM GUIDELINES West Lafayette Campus August 2012 Definition of Professional Masters Program The characteristics of a Professional Masters program at Purdue as outlined below provide

UNIVERSITY OF CALIFORNIA SANTA CRUZ RECHARGE RATE POLICIES

RECHARGE DEFINITION: A recharge is defined as "the cost charged to a University department for specific goods or services provided by another University department". Recharges move funding/expenses from

RECHARGE DEFINITION: A recharge is defined as "the cost charged to a University department for specific goods or services provided by another University department". Recharges move funding/expenses from

Cost Allocation Cost Pooling & Time Distribution

Cost Allocation Cost Pooling & Time Distribution Objectives Cost Allocation Cost Pooling Cost Allocation Plans Time Distribution Common Compliance Findings The process used to distribute costs to a final

Cost Allocation Cost Pooling & Time Distribution Objectives Cost Allocation Cost Pooling Cost Allocation Plans Time Distribution Common Compliance Findings The process used to distribute costs to a final

CALIFORNIA STATE UNIVERSITY, SAN MARCOS. Financial Statements. June 30, 2005 and 2004. (With Independent Auditors Report Thereon)

") Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Management s Discussion and Analysis 3 Financial Statements: Statements of Net Assets

Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Management s Discussion and Analysis 3 Financial Statements: Statements of Net Assets

The University of Financial Plan - A Summary

Multi-Year Financial Plan Academic Division FY2015-16 through FY2021-22 1 Multi-Year Financial Plan The accompanying projection has been prepared for the use of the Board of Visitors and administration

Multi-Year Financial Plan Academic Division FY2015-16 through FY2021-22 1 Multi-Year Financial Plan The accompanying projection has been prepared for the use of the Board of Visitors and administration

Contract Compliance and the Federal Acquisition Regulation (FAR)

") Contract Compliance and the Federal Acquisition Regulation (FAR) ORA CERTIFICATE PROGRAM (MODULE 11) 27 MAY 2015 Learning Objectives Participants will learn about the history of the Federal Acquisition

Contract Compliance and the Federal Acquisition Regulation (FAR) ORA CERTIFICATE PROGRAM (MODULE 11) 27 MAY 2015 Learning Objectives Participants will learn about the history of the Federal Acquisition

Staff Timesheets: Requirements and Issues

Staff Timesheets: Requirements and Issues 1 You need to know... The information in this session is based on CNCS and Federal laws, rules, and regulations; CNCS grant terms and provisions; and generally

Staff Timesheets: Requirements and Issues 1 You need to know... The information in this session is based on CNCS and Federal laws, rules, and regulations; CNCS grant terms and provisions; and generally

Clinical Faculty Remuneration Policy. Date: January 27, 2015 Policy ID: 1.630 Status: Final

Clinical Faculty Remuneration Policy Date: Policy ID: 1.630 Status: Final Contact Office: Controller Dean s Office, School of Medicine PO Box 800796 Charlottesville, VA 22908 phone: 434-924-8412 fax: 434-924-8173

Clinical Faculty Remuneration Policy Date: Policy ID: 1.630 Status: Final Contact Office: Controller Dean s Office, School of Medicine PO Box 800796 Charlottesville, VA 22908 phone: 434-924-8412 fax: 434-924-8173

Budget Policies and Procedures Manual

Office of Budget and Planning Budget Policies and Procedures Manual Revised 3/02/15 Office of Budget and Planning Budget Policies and Procedures Manual Contents Introduction 1 Preparation and Approval

Office of Budget and Planning Budget Policies and Procedures Manual Revised 3/02/15 Office of Budget and Planning Budget Policies and Procedures Manual Contents Introduction 1 Preparation and Approval

BUDGET ADVISORY COMMITTEE FINAL BUDGET

BUDGET ADVISORY COMMITTEE FINAL BUDGET 2012 2013 PROPOSED BUDGET Following are the budget parameters for the proposed 2012-2013 budget: Proposed 2011/2012 2012/2013 Budgeted Enrollment (10 students = $263,000)

BUDGET ADVISORY COMMITTEE FINAL BUDGET 2012 2013 PROPOSED BUDGET Following are the budget parameters for the proposed 2012-2013 budget: Proposed 2011/2012 2012/2013 Budgeted Enrollment (10 students = $263,000)

Multi Year Financial Plan Academic Division FY2016-17 through FY2022-23

Multi Year Financial Plan Academic Division FY2016-17 through FY2022-23 Multi Year Financial Plan The Multi-Year Financial Plan was developed in concert with the Finance Committee and approved by the Board

Multi Year Financial Plan Academic Division FY2016-17 through FY2022-23 Multi Year Financial Plan The Multi-Year Financial Plan was developed in concert with the Finance Committee and approved by the Board

The Graduate School. Goals & Challenges

The Graduate School Goals & Challenges University s Goals (paraphrased) Earn national/international recognition Recruitment and retention of high quality students Delivery of high quality, innovative graduate

The Graduate School Goals & Challenges University s Goals (paraphrased) Earn national/international recognition Recruitment and retention of high quality students Delivery of high quality, innovative graduate

How To Determine The Cost Of A Project

51880 Federal Register / Vol. 70, No. 168 / Wednesday, August 31, 2005 / Rules and Regulations E.O.s 12549 (3 CFR, 1986 Comp., p. 189) and 12689 (3 CFR, 1989 Comp., p. 235), Debarment and Suspension. The

51880 Federal Register / Vol. 70, No. 168 / Wednesday, August 31, 2005 / Rules and Regulations E.O.s 12549 (3 CFR, 1986 Comp., p. 189) and 12689 (3 CFR, 1989 Comp., p. 235), Debarment and Suspension. The

ALAMO COLLEGES FOUNDATION, INC. (A Texas nonprofit Foundation) AUDITED FINANCIAL STATEMENTS. Year Ended December 31, 2012

AUDITED FINANCIAL STATEMENTS. Year Ended December 31, 2012") R. D. Harrison, CPA Certified Public Accountant Member American Institute of Certified Public Accountants Registered with the Public Company Accounting Oversight Board ALAMO COLLEGES FOUNDATION, INC. AUDITED

R. D. Harrison, CPA Certified Public Accountant Member American Institute of Certified Public Accountants Registered with the Public Company Accounting Oversight Board ALAMO COLLEGES FOUNDATION, INC. AUDITED

Uniform Guidance Training #1 Implementation at VCU

Uniform Guidance Training #1 Implementation at VCU Annie Publow, CRA, MFA Director of Sponsored Programs, Government/NonProfit Support Mark Roberts Director of Grants & Contracts Accounting Uniform Guidance

Uniform Guidance Training #1 Implementation at VCU Annie Publow, CRA, MFA Director of Sponsored Programs, Government/NonProfit Support Mark Roberts Director of Grants & Contracts Accounting Uniform Guidance