Deposit Insurance. Seminar for Sr. Bank Supervisors. F. Montes-Negret, Sector Manager, LCSFF The World Bank, Oct. 24, 2002

|

|

|

- Hugo Walsh

- 8 years ago

- Views:

Transcription

1 Deposit Insurance Seminar for Sr. Bank Supervisors F. Montes-Negret, Sector Manager, LCSFF The World Bank, Oct. 24, 2002

2 Agenda A. Introduction B. The Theory: Deposit Insurance & Risk Objectives Pros and Cons Size of the Insurance Fund Measuring Risk Pricing Loss-sharing C. The Mexican Case: FOBAPROA vs. IPAB D. Conclusions Bibliography 2

3 A. Introduction Regulators recognize the inherent instability of the banking system due to the fact that: (1) liquid liabilities exceed by far liquid assets; (2) the nature of the deposit insurance contract; and (3) the high leverage of banks (D/A). Then the need for a safety net. Demand deposits are characterized by two features: (1) Claims are redeemed on a first come, first served basis (sequentially); and (2) Full pay or no pay method. 3

Claims are redeemed on a first come, first served basis")

4 Introduction (cont.) Banks respond to deposit losses by drawing down their cash, selling liquid assets and borrowing short-term. Beyond that they hit a liquidity crisis and if they must continue to sell fast assets at fire-sell prices, then they might become insolvent. Then a deposit insurance fund provides another defense to prevent depositors from over-reacting. The key issue is how to develop incentive-compatible deposit insurance systems. 4

5 Introduction (Cont.) Deposit insurance is only one of the components of the financial safety net: Sound legal regime; Stable macroeconomic environment; Compliance with recognized accounting & auditing standards; Adequate Chartering Function (licensing); Strong Prudential Supervision Function; Strict Termination Authority (de-licensing); Incentive-compatible Deposit Insurance System; Adequate Lender of Last Resort Function; Effective Disclosure Regime. 5

; Strong Prudential Supervision Function; Strict Termination Authority (de-licensing);")

6 Introduction (Cont.) The Rediscount window is no substitute for a deposit insurance fund because: (1) to borrow from the discount window the bank needs high quality liquid assets to pledge; (2) Borrowing is not automatic but discretionary; and (3) Central ban loans are meant to provide temporary liquidity to solvent banks. Incentive-compatible deposit insurance should increase: (1) shareholders discipline; (2) depositors discipline; and (3) Regulatory discipline. 6

7 Introduction (cont.) Key attributes of an effective Deposit Insurance System: Explicitly defined benefits (coverage & limits); Mandatory bank participation; Clear mandates and responsibilities for the deposit insurer; Close coordination among the agencies involved; Well-defined funding mechanism for the deposit insurer; Public information campaign. 7

8 Introduction (cont.) Spectrum of Deposit Insurance Systems: Paybox: pays claims of depositors after a bank is closed; Risk-minimization systems: control entry/exit into the system, assess and monitor risks, conduct examinations of banks, provision of financial assistance and intervention powers, resolving bank failures and finding least cost solutions. I will focus on the latter, although not all functions might be performed by the deposit insurer. 8

9 B. Deposit Insurance: Objectives To prevent bank runs and enhance the stability of the financial system (remember banks are highly leveraged institutions with a high share of illiquid assets compared to the maturity of their liabilitieshigh term-transformation risk); To overcome the asymmetry of information in the banking system (i.e.; the bank knows more about the riskiness of its activities than its depositors); To protect small depositors; To facilitate banks orderly exit. 9

; To protect small depositors; To facilitate banks orderly")

10 The Pros and Cons Cons Moral hazard: depositors have less interest in monitoring banks and banks have more incentives to increase their risks. Weaker market discipline. Generous deposit insurance might have negative effects on bank stability. Pros Create a safety net to prevent bank panics. Protect the smaller, less informed, depositors. 10

11 Size of the Fund US (200): 8,571 banks with $6.5 trillion in total assets and $2.5 trillion of insured deposits (38.5%) were contributing to the FDIC Insurance Fund, which at the time had accumulated $32 billion to cover this exposure. Was that enough? Which criteria should be used to answer that question? 11

12 Risk-Based Premium System The Deposit Insurance Fund is like an insurance company, with a portfolio of contingent credit exposures to insured banks. However, present approaches (flat premium schedule) set the desired reserve ratio as a fix percentage independent of the fund s actual loss profile. One innovative approach is to estimate a cumulative loss distribution and calculate potential losses against the reserves of the insurance fund (i.e., linking the desired level of capitalization with the desired credit rating). 12

13 Measuring Risk:Definitions Probability of default (PD i ):the probability that the counterparty (i) will fail to service its obligations Frequency Distribution of losses (number of loss events per year); Expected Loss (EL): mean of the loss distribution; Unexpected Loss( UL) : standard deviation of the loss distribution; Loss Given Default: the extent of the loss incurred in the event the counterparty defaults (% of Insured Deposits X) Severity Distribution (S, value of a loss event); Default Correlations: the degree to which the default risk of the counterparties are correlated. 13

Severity Distribution (S, value of a loss event); Default Correlations: the degree to which the default risk of the counterparties are")

14 Measuring Risk: Formulas ELi = PDi. Xi. Si Because default is a Bernoulli random variable, its standard deviation is PDi ( 1 PDi ), and if we assume no correlation between PD, S and X, then: UL i = ( PDi PDi ) µ s X i + PDiX i σ s i i Where Si ~ f (µ s, s s ) and if s s = 0 then simplify. 14

µ s X i + PDiX i σ s i i Where Si ~ f (µ")

15 Measuring Risk:Conclusion The exposure to individual banks can be added to get a cumulative loss distribution, reflecting the expected loss of individual banks, the size of individual exposures and the correlation of losses in the portfolio. The distribution will be skewed with lumpiness reflecting the contribution of large banks. The risk at the portfolio level then will be a weighted average of Elp= S EL i. The ULp is more complex since it must consider the correlation between individual losses r ij. 15

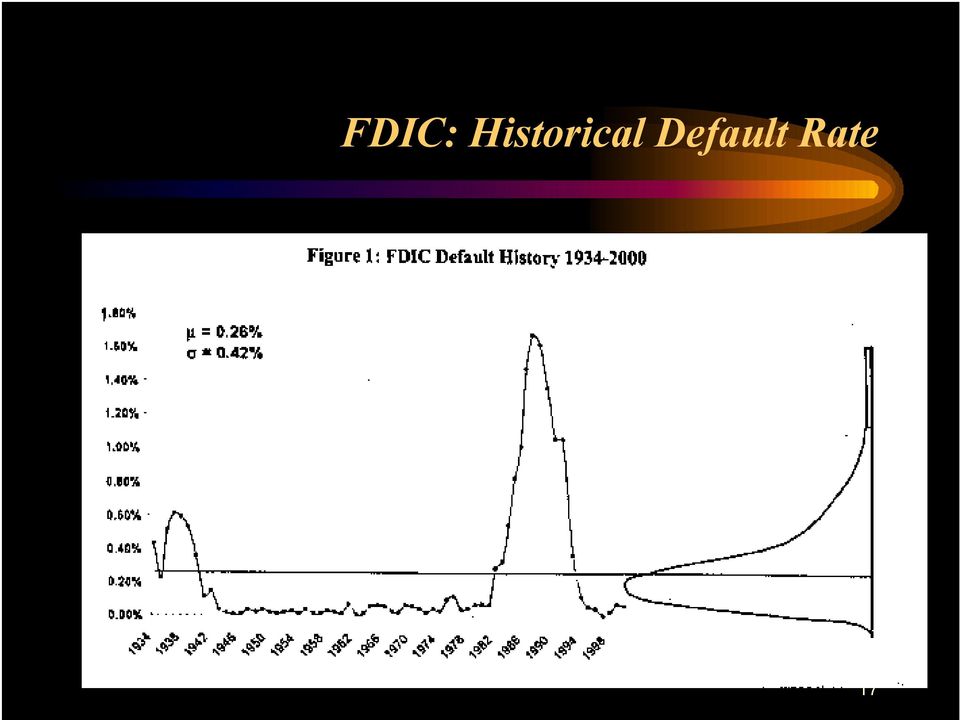

16 Probability of Default Three main approaches to estimating default frequencies: Historical default rate (for the FDIC the average default rate was 0.26% of assets per year between , see graph 1); Credit Scoring Models; Risk Ratings (S&P) --> PD 16

; Credit")

17 FDIC: Historical Default Rate 17

18 Severity (Loss given default) Approaches: Fixed or stochastic FDIC losses between were 30% of insured assets, 1/3 of this were expenses (administrative + legal costs) and 2/3 bad assets. Pay-off to depositors of failed banks (less than 1/4 of cases); Purchase and assumption transactions. 18

; Purchase")

19 Pricing: Insurance Fees Uniform fees Could be de-stabilizing Risk-based pricing Expected loss penalizes riskier banks but also smaller ones. Unexpected loss contribution based pricing penalizes larger banks. Ex-ante and Ex-post pricing; Ex-post rebates. Pro-cyclicality Designated Reserve Ratio drops when banks are weak, while the fund requires higher premiums when banks can least afford them. Fairness. 19

20 FDIC Pricing: Insurance Fees US: average 23 basis points, with a target level of reserves under the FDIC Improvement Act (FIDICIA) of 1.25% of insured deposits ( Designated Reserve Ratio ), plus a US$30 billion line of credit from the Treasury. After 1999, 97% of insured deposits had a de facto zero fee and the remaining 3% was differentiated by risk in 5 buckets with fees going from 3 to 27 bps (minimal risk differentiation for 8,000 insured banks with large differences in risk profiles and size). 20

21 Risk-based Pricing At a minimum premiums should cover expected losses: Making the fund self-financing through time; Relieving moral hazard; However,leads to under-pricing of very large exposures. To correct contributory risk affecting loss distribution should be included (Unexpected Loss Contribution). P i = El i + h ULC i 21

22 Risk-Sharing Splitting of loss-distribution in to two zones (see graph): Zone A: smaller losses cover by reserves; Zone B: catastrophic losses cover by loss reinsurance This structure mirrors the loss distribution for banks: Losses are covered by the bank shareholders up to the capitalization level; Beyond that, losses are borne by the deposit insurance fund and uninsured creditors. Risks are held by: government, banks themselves (mutual insurance), private capital or reinsurance market. 22

23 Risk-sharing: Zone A and B 23

24 Government System Mandatory Government assumes both parts of the risk distribution: Zone A losses -->Reserve Fund Zone B losses --> Treasury Deposit Premium = Expected loss <pricing by private sector (public good). Death spiral effect : Deterrence effect of insurance premiums might be insufficient if risk-taking is U- shaped (does not deter well capitalized banks or severely under-capitalized banks ==> need to complement it with other tools (PCA). 24

25 Private System Losses to be shared between banks and the capital and reinsurance market. Banks mutually insured losses in Zone A but reinsure or transfer Zone B losses. Practical problem: Fund s reserves well below insured deposits of largest bank. If so solvency standard difficult to reach. Higher price than in the closed government system. Large banks will be charged proportionately more because they impose a much greater need to hold incremental economic capital. 25

26 Private system (cont.) Cyclical behavior: during expansion system accumulates reserves beyond target solvency standard. If they result from: risks in Zone A --> rebates to banks; risks in Zone B --> profits to reinsurers. When reserves fall below the solvency standard there will be a need to recapitalize the fund. This is problematic since additional capital will be required at the trough of the business cycle. Although in theory a private system might lead to efficient pricing and correct incentives, in practice it might be unworkable (size of insured deposits vs. size of K and insurance markets). 26

27 Hybrid Deposit Insurance System Banks might mutually insure Zone A losses, while Government reinsures Zone B losses. The risk sharing determines how the risks are split. This leads to a dual pricing system, but government should chage banks for the expected loss for the excess of loss reinsurance. The latter would be very small if government insures extreme catastrophe losses. The price for insuring small banks in Zone A will depend on the sharing point. Expected losses plus economic charge for loss volatility up to the risk sharing point. If Zone A is small, prices will be close to expected losses. 27

28 C. The Mexican case Severe banking crisis (December, 1994); Universal deposit coverage to prevent bank runs (blanket guarantee including inter-bank deposits); Shock Denial Least cash but not least cost solution (FOBAPROA bonds) Creation of IPAB (1998) Towards resolution of banking problems Recapitalizations privatizations, liquidations and sale of NPLs. Cost of the crisis about 20% of GDP. Transitioning to a limited-coverage deposit insurance system. 28

29 D. Conclusions The risk management problem faced by a deposit insurance fund is directly related to the riskiness of the insured individual banks in the portfolio. Modern risk analysis theory should be used to estimate the cumulative loss distribution. Loss distributions should be broken down into two zones: Zone A losses covered by reserves (funded or collable) and Zone B excess losses covered by reinsurance. It must be decided who bears the risk in each zone of the loss distribution and how does the partition point influence pricing. Heterogeneity of banks complicates matters. 29

30 Conclusions (cont.) Arguably, the most practical and lowest cost solution is for the government to own both parts of the loss distribution. This can be viewed as a mandatory insurance contract between the government and the banks. Pricing should be risk-based on expected losses. This greatly mitigates banks moral hazard and ensures self financing over time. Countries with explicit deposit insurance are more attractive to international non-bank depositors, as well as those with coinsurance, low premiums and private managed systems. 30

31 Conclusions (cont.) Differential deposit insurance in each country offers the possibility of international regulatory competition. The EU Directive on deposit insurance imposes minimum standards but it is silent on the level of the premium. Unanswered questions: Cost to taxpayers for providing insurance provision. Only as a backstop providing catastrophic insurance?. How does this affect the probability of systemic risk?. 31

32 Bibliography Deposit Insurance and Risk Management of the U.S. Banking System: How Much?, How safe?, Who Pays?, by A. Kuritzkes, T. Schuermann and S. Weiner, The Wharton School, Financial Institutions Center, U. of Pennsylvania, 02/02-B, April 29, Guidance for Developing Effective Deposit Insurance Systems, Financial Stability Forum, September, Deposit Insurance Around the Globe: Where does it work?, E. Kane and A. Demirguc-Kunt, NBER, WP 8493, September, Deposit Insurance and International bank Deposits, H. Huizinga and G. Nicodeme, Economic Papers, Economic Commission, Directorate General for Economic and Financial Affairs, Number 164, February,

Deposit Insurance Pricing. Luc Laeven World Bank Global Dialogue 2002

Deposit Insurance Pricing Luc Laeven World Bank Global Dialogue 2002 1 Introduction Explicit deposit insurance should not be adopted in countries with a weak institutional environment Political economy

Deposit Insurance Pricing Luc Laeven World Bank Global Dialogue 2002 1 Introduction Explicit deposit insurance should not be adopted in countries with a weak institutional environment Political economy

3/22/2010. Chapter 11. Eight Categories of Bank Regulation. Economic Analysis of. Regulation Lecture 1. Asymmetric Information and Bank Regulation

Chapter 11 Economic Analysis of Banking Regulation Lecture 1 Asymmetric Information and Bank Regulation Adverse Selection and Moral Hazard are the two concepts that underlie government regulation of the

Chapter 11 Economic Analysis of Banking Regulation Lecture 1 Asymmetric Information and Bank Regulation Adverse Selection and Moral Hazard are the two concepts that underlie government regulation of the

Financial-Institutions Management. Solutions 5. Chapter 18: Liability and Liquidity Management Reserve Requirements

Solutions 5 Chapter 18: Liability and Liquidity Management Reserve Requirements 8. City Bank has estimated that its average daily demand deposit balance over the recent 14- day reserve computation period

Solutions 5 Chapter 18: Liability and Liquidity Management Reserve Requirements 8. City Bank has estimated that its average daily demand deposit balance over the recent 14- day reserve computation period

Ch 19 Deposit Insurance Overview

Ch 19 Deposit Insurance Overview The focus of this chapter is the mechanisms designed to protect FIs from liquidity crises. Deposit Insurance Funds Securities Investors Protection Corporation Pension Benefit

Ch 19 Deposit Insurance Overview The focus of this chapter is the mechanisms designed to protect FIs from liquidity crises. Deposit Insurance Funds Securities Investors Protection Corporation Pension Benefit

Homework Assignment #5: Answer Key

Homework Assignment #5: Answer Key Write out solutions to the following problems from your textbook. Be sure to show your work on an math and use figures or graphs where appropriate. Chapter 11: #1 Describe

Homework Assignment #5: Answer Key Write out solutions to the following problems from your textbook. Be sure to show your work on an math and use figures or graphs where appropriate. Chapter 11: #1 Describe

Enhanced Guidance for Effective Deposit Insurance Systems: Mitigating Moral Hazard. Guidance Paper. Prepared by the Research and Guidance Committee

May 2013 Enhanced Guidance for Effective Deposit Insurance Systems: Mitigating Moral Hazard Guidance Paper Prepared by the Research and Guidance Committee International Association of Deposit Insurers

May 2013 Enhanced Guidance for Effective Deposit Insurance Systems: Mitigating Moral Hazard Guidance Paper Prepared by the Research and Guidance Committee International Association of Deposit Insurers

The role of capital for non-bank actors. Denis Duverne

The role of capital for non-bank actors Denis Duverne Key messages for today 1 The balance sheet structure of insurance companies is fundamentally different from that of banks The business model of insurance

The role of capital for non-bank actors Denis Duverne Key messages for today 1 The balance sheet structure of insurance companies is fundamentally different from that of banks The business model of insurance

What is new in Basel 3:

Camera dei Deputati 17 Indagine conoscitiva 4 ALLEGATO What is new in Basel 3: How it will influence market participants Krishnan Ramadurai Managing Director Camera dei Deputati 18 Indagine conoscitiva

Camera dei Deputati 17 Indagine conoscitiva 4 ALLEGATO What is new in Basel 3: How it will influence market participants Krishnan Ramadurai Managing Director Camera dei Deputati 18 Indagine conoscitiva

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective Paul Thornton International Actuarial Association Presentation to OECD Insurance and Pensions Committee June 2010

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective Paul Thornton International Actuarial Association Presentation to OECD Insurance and Pensions Committee June 2010

FINANCIAL DOMINANCE MARKUS K. BRUNNERMEIER & YULIY SANNIKOV

Based on: The I Theory of Money - Redistributive Monetary Policy CFS Symposium: Banking, Liquidity, and Monetary Policy 26 September 2013, Frankfurt am Main 2013 FINANCIAL DOMINANCE MARKUS K. BRUNNERMEIER

Based on: The I Theory of Money - Redistributive Monetary Policy CFS Symposium: Banking, Liquidity, and Monetary Policy 26 September 2013, Frankfurt am Main 2013 FINANCIAL DOMINANCE MARKUS K. BRUNNERMEIER

Inside and outside liquidity provision

Inside and outside liquidity provision James McAndrews, FRBNY, ECB Workshop on Excess Liquidity and Money Market Functioning, 19/20 November, 2012 The views expressed in this presentation are those of

Inside and outside liquidity provision James McAndrews, FRBNY, ECB Workshop on Excess Liquidity and Money Market Functioning, 19/20 November, 2012 The views expressed in this presentation are those of

Designing the funding side of the Single Resolution Mechanism (SRM): A proposal for a layered scheme with limited joint liability

: A proposal for a layered scheme with limited joint liability") Jan Pieter Krahnen - Jörg Rocholl Designing the funding side of the Single Resolution Mechanism (SRM): A proposal for a layered scheme with limited joint liability White Paper Series No. 10 Designing the

Jan Pieter Krahnen - Jörg Rocholl Designing the funding side of the Single Resolution Mechanism (SRM): A proposal for a layered scheme with limited joint liability White Paper Series No. 10 Designing the

CONSULTATION PAPER P016-2006 October 2006. Proposed Regulatory Framework on Mortgage Insurance Business

CONSULTATION PAPER P016-2006 October 2006 Proposed Regulatory Framework on Mortgage Insurance Business PREFACE 1 Mortgage insurance protects residential mortgage lenders against losses on mortgage loans

CONSULTATION PAPER P016-2006 October 2006 Proposed Regulatory Framework on Mortgage Insurance Business PREFACE 1 Mortgage insurance protects residential mortgage lenders against losses on mortgage loans

FIN 683 Financial Institutions Management Liquidity Management and Deposit Insurance

FIN 683 Financial Institutions Management Liquidity Management and Deposit Insurance Professor Robert B.H. Hauswald Kogod School of Business, AU Bank Runs Can arise due to concern about: Bank solvency

FIN 683 Financial Institutions Management Liquidity Management and Deposit Insurance Professor Robert B.H. Hauswald Kogod School of Business, AU Bank Runs Can arise due to concern about: Bank solvency

DSF POLICY BRIEFS No. 1/ February 2011

DSF POLICY BRIEFS No. 1/ February 2011 Risk Based Deposit Insurance for the Netherlands Dirk Schoenmaker* Summary: During the recent financial crisis, deposit insurance cover was increased across the world.

DSF POLICY BRIEFS No. 1/ February 2011 Risk Based Deposit Insurance for the Netherlands Dirk Schoenmaker* Summary: During the recent financial crisis, deposit insurance cover was increased across the world.

Information as of 10/19/08. FDIC Temporary Liquidity Guarantee Program What is It and What Does It Mean to Community Banks?

Information as of 10/19/08 FDIC Temporary Liquidity Guarantee Program What is It and What Does It Mean to Community Banks? Introduction The Liquidity Guarantee Program The FDIC has created a temporary

Information as of 10/19/08 FDIC Temporary Liquidity Guarantee Program What is It and What Does It Mean to Community Banks? Introduction The Liquidity Guarantee Program The FDIC has created a temporary

Banks, Liquidity Management, and Monetary Policy

Discussion of Banks, Liquidity Management, and Monetary Policy by Javier Bianchi and Saki Bigio Itamar Drechsler NYU Stern and NBER Bu/Boston Fed Conference on Macro-Finance Linkages 2013 Objectives 1.

Discussion of Banks, Liquidity Management, and Monetary Policy by Javier Bianchi and Saki Bigio Itamar Drechsler NYU Stern and NBER Bu/Boston Fed Conference on Macro-Finance Linkages 2013 Objectives 1.

Systemic Risk and the Insurance Industry

Systemic Risk and the Insurance Industry J. David Cummins, Temple University The Brookings Institution Conference on Regulating Non-Bank SIFIs May 9, 2013 Copyright J. David Cummins, 2013, all rights reserved.

Systemic Risk and the Insurance Industry J. David Cummins, Temple University The Brookings Institution Conference on Regulating Non-Bank SIFIs May 9, 2013 Copyright J. David Cummins, 2013, all rights reserved.

a. If the risk premium for a given customer is 2.5 percent, what is the simple promised interest return on the loan?

Selected Questions and Exercises Chapter 11 2. Differentiate between a secured and an unsecured loan. Who bears most of the risk in a fixed-rate loan? Why would bankers prefer to charge floating rates,

Selected Questions and Exercises Chapter 11 2. Differentiate between a secured and an unsecured loan. Who bears most of the risk in a fixed-rate loan? Why would bankers prefer to charge floating rates,

Chapter 11. Economic Analysis of Banking Regulation

Chapter 11 Economic Analysis of Banking Regulation How Asymmetric Information Explains Banking Regulation 1.Government safety net and deposit insurance prevents bank runs due to asymmetric information

Chapter 11 Economic Analysis of Banking Regulation How Asymmetric Information Explains Banking Regulation 1.Government safety net and deposit insurance prevents bank runs due to asymmetric information

Deposit Insurance and Risk Management of the U.S. Banking System: How Much? How Safe? Who Pays? Financial Institutions Center

Financial Institutions Center Deposit Insurance and Risk Management of the U.S. Banking System: How Much? How Safe? Who Pays? by Andrew Kuritzkes Til Schuermann Scott Weiner 02-02-B The Wharton Financial

Financial Institutions Center Deposit Insurance and Risk Management of the U.S. Banking System: How Much? How Safe? Who Pays? by Andrew Kuritzkes Til Schuermann Scott Weiner 02-02-B The Wharton Financial

LIQUIDITY RISK MANAGEMENT GUIDELINE

LIQUIDITY RISK MANAGEMENT GUIDELINE April 2009 Table of Contents Preamble... 3 Introduction... 4 Scope... 5 Coming into effect and updating... 6 1. Liquidity risk... 7 2. Sound and prudent liquidity risk

LIQUIDITY RISK MANAGEMENT GUIDELINE April 2009 Table of Contents Preamble... 3 Introduction... 4 Scope... 5 Coming into effect and updating... 6 1. Liquidity risk... 7 2. Sound and prudent liquidity risk

Dumfries Mutual Insurance Company Financial Statements For the year ended December 31, 2010

Dumfries Mutual Insurance Company Financial Statements For the year ended December 31, 2010 Contents Independent Auditors' Report 2 Financial Statements Balance Sheet 3 Statement of Operations and Unappropriated

Dumfries Mutual Insurance Company Financial Statements For the year ended December 31, 2010 Contents Independent Auditors' Report 2 Financial Statements Balance Sheet 3 Statement of Operations and Unappropriated

STATEMENT OF DIANE ELLIS DIRECTOR DIVISION OF INSURANCE AND RESEARCH FEDERAL DEPOSIT INSURANCE CORPORATION

STATEMENT OF DIANE ELLIS DIRECTOR DIVISION OF INSURANCE AND RESEARCH FEDERAL DEPOSIT INSURANCE CORPORATION on HOUSING FINANCE REFORM: POWERS AND STRUCTURE OF A STRONG REGULATOR COMMITTEE ON BANKING, HOUSING,

STATEMENT OF DIANE ELLIS DIRECTOR DIVISION OF INSURANCE AND RESEARCH FEDERAL DEPOSIT INSURANCE CORPORATION on HOUSING FINANCE REFORM: POWERS AND STRUCTURE OF A STRONG REGULATOR COMMITTEE ON BANKING, HOUSING,

Capital adequacy ratios for banks - simplified explanation and

Page 1 of 9 Capital adequacy ratios for banks - simplified explanation and example of calculation Summary Capital adequacy ratios are a measure of the amount of a bank's capital expressed as a percentage

Page 1 of 9 Capital adequacy ratios for banks - simplified explanation and example of calculation Summary Capital adequacy ratios are a measure of the amount of a bank's capital expressed as a percentage

FSB/IOSCO Consultative Document - Assessment Methodologies for Identifying Non-Bank Non-Insurer Global Systemically Important Financial Institutions

CAPITAL GROUP'" The Capital Group Companies, Inc. 333 South Hope Street Los Angeles, California 90071-1406 Secretariat of the Financial Stability Board c/o Bank for International Settlements CH -4002 Basel,

CAPITAL GROUP'" The Capital Group Companies, Inc. 333 South Hope Street Los Angeles, California 90071-1406 Secretariat of the Financial Stability Board c/o Bank for International Settlements CH -4002 Basel,

FSB launches peer review on deposit insurance systems and invites feedback from stakeholders

Press release Press enquiries: Basel +41 61 280 8037 Press.service@bis.org Ref no: 26/2011 1 July 2011 FSB launches peer review on deposit insurance systems and invites feedback from stakeholders The Financial

Press release Press enquiries: Basel +41 61 280 8037 Press.service@bis.org Ref no: 26/2011 1 July 2011 FSB launches peer review on deposit insurance systems and invites feedback from stakeholders The Financial

PROPERTY/CASUALTY INSURANCE AND SYSTEMIC RISK

PROPERTY/CASUALTY INSURANCE AND SYSTEMIC RISK Steven N. Weisbart, Ph.D., CLU Chief Economist President April 2011 INTRODUCTION To prevent another financial meltdown like the one that affected the world

PROPERTY/CASUALTY INSURANCE AND SYSTEMIC RISK Steven N. Weisbart, Ph.D., CLU Chief Economist President April 2011 INTRODUCTION To prevent another financial meltdown like the one that affected the world

The Financial Crises of the 21st Century

The Financial Crises of the 21st Century Workshop of the Austrian Research Association (Österreichische Forschungsgemeinschaft) 18. - 19. 10. 2012 Towards a Unified European Banking Market Univ.Prof. Dr.

The Financial Crises of the 21st Century Workshop of the Austrian Research Association (Österreichische Forschungsgemeinschaft) 18. - 19. 10. 2012 Towards a Unified European Banking Market Univ.Prof. Dr.

Conceptual Framework: What Does the Financial System Do? 1. Financial contracting: Get funds from savers to investors

Conceptual Framework: What Does the Financial System Do? 1. Financial contracting: Get funds from savers to investors Transactions costs Contracting costs (from asymmetric information) Adverse Selection

Conceptual Framework: What Does the Financial System Do? 1. Financial contracting: Get funds from savers to investors Transactions costs Contracting costs (from asymmetric information) Adverse Selection

A FRAMEWORK FOR MACROPRUDENTIAL BANKING REGULATION 1

A FRAMEWORK FOR MACROPRUDENTIAL BANKING REGULATION 1 JEAN-CHARLES ROCHET 2 March 2005 Abstract: We offer a framework for macroprudential banking regulation, with a particular emphasis on Latin American

A FRAMEWORK FOR MACROPRUDENTIAL BANKING REGULATION 1 JEAN-CHARLES ROCHET 2 March 2005 Abstract: We offer a framework for macroprudential banking regulation, with a particular emphasis on Latin American

Re: Advance Notice of Proposed Rulemaking Regarding Authority to Require Supervision and Regulation of Certain Nonbank Financial Companies

JAMES D. MACPHEE Chairman SALVATORE MARRANCA Chairman-Elect JEFFREY L. GERHART Vice Chairman JACK A. HARTINGS Treasurer WAYNE A. COTTLE Secretary R. MICHAEL MENZIES SR. Immediate Past Chairman November

JAMES D. MACPHEE Chairman SALVATORE MARRANCA Chairman-Elect JEFFREY L. GERHART Vice Chairman JACK A. HARTINGS Treasurer WAYNE A. COTTLE Secretary R. MICHAEL MENZIES SR. Immediate Past Chairman November

DEPOSIT INSURANCE FUNDING: ASSURING CONFIDENCE November 2013

FEDERAL DEPOSIT INSURANCE CORPORATION STAFF PAPER DEPOSIT INSURANCE FUNDING: ASSURING CONFIDENCE November 2013 Diane Ellis* Director, Division of Insurance and Research Federal Deposit Insurance Corporation

FEDERAL DEPOSIT INSURANCE CORPORATION STAFF PAPER DEPOSIT INSURANCE FUNDING: ASSURING CONFIDENCE November 2013 Diane Ellis* Director, Division of Insurance and Research Federal Deposit Insurance Corporation

FSI-IADI Seminar on Bank Resolution, Crisis Management and Deposit Insurance Issues. Coordination of safety net players: Role of DIA.

FSI-IADI Seminar on Bank Resolution, Crisis Management and Deposit Insurance Issues Coordination of safety net players: Role of DIA Jerzy Pruski IADI President and Chair of the Executive Council President

FSI-IADI Seminar on Bank Resolution, Crisis Management and Deposit Insurance Issues Coordination of safety net players: Role of DIA Jerzy Pruski IADI President and Chair of the Executive Council President

Unlimited deposit insurance is unnecessary

October 13, 2010 Mr. Robert Feldman Executive Secretary Attn: Comments Federal Deposit Insurance Corporation 550 17 th Street, NW Washington, DC 20429 Re: RIN # 3064-AD37 Dear Secretary Feldman: Treasury

October 13, 2010 Mr. Robert Feldman Executive Secretary Attn: Comments Federal Deposit Insurance Corporation 550 17 th Street, NW Washington, DC 20429 Re: RIN # 3064-AD37 Dear Secretary Feldman: Treasury

Deposit Insurance Reserve Fund Strategy

Deposit Insurance Reserve Fund Strategy September 2013 Table of Contents Executive Summary... 2 Introduction... 3 Background... 4 Purpose of the Reserve Fund... 5 Current State... 5 Increasing Size and

Deposit Insurance Reserve Fund Strategy September 2013 Table of Contents Executive Summary... 2 Introduction... 3 Background... 4 Purpose of the Reserve Fund... 5 Current State... 5 Increasing Size and

Market Value Based Accounting and Capital Framework

Market Value Based Accounting and Capital Framework Presented by: Erik Anderson, FSA, MAAA New York Life Insurance Company Prannoy Chaudhury, FSA, MAAA Milliman 2014 ASNY Meeting November 5, 2014 1 07

Market Value Based Accounting and Capital Framework Presented by: Erik Anderson, FSA, MAAA New York Life Insurance Company Prannoy Chaudhury, FSA, MAAA Milliman 2014 ASNY Meeting November 5, 2014 1 07

Compensation and Risk Incentives in Banking

Compensation and Risk Incentives in Banking By Jian Cai, Kent Cherny, and Todd Milbourn Abstract In this Economic Commentary, we review why executive compensation contracts are often structured the way

Compensation and Risk Incentives in Banking By Jian Cai, Kent Cherny, and Todd Milbourn Abstract In this Economic Commentary, we review why executive compensation contracts are often structured the way

1 Introduction. 1.1 Three pillar approach

1 Introduction 1.1 Three pillar approach The recent years have shown that (financial) companies need to have a good management, a good business strategy, a good financial strength and a sound risk management

1 Introduction 1.1 Three pillar approach The recent years have shown that (financial) companies need to have a good management, a good business strategy, a good financial strength and a sound risk management

Managing Systemic Banking Crises. David S. Hoelscher Assistant Director Money and Credit Markets Department

Managing Systemic Banking Crises David S. Hoelscher Assistant Director Money and Credit Markets Department 2 Introduction Systemic banking crises of unprecedented scale: Argentina, East Asia, Ecuador,

Managing Systemic Banking Crises David S. Hoelscher Assistant Director Money and Credit Markets Department 2 Introduction Systemic banking crises of unprecedented scale: Argentina, East Asia, Ecuador,

A Bail-In or a Bail-Out? New Risks on the Horizon in the Banking Sector

The US banking sector is currently characterized by good credit fundamentals and supportive technicals. A key risk offsetting this credit strength is the prospect of a new bank resolution regime (Orderly

The US banking sector is currently characterized by good credit fundamentals and supportive technicals. A key risk offsetting this credit strength is the prospect of a new bank resolution regime (Orderly

GAO DEPOSIT INSURANCE 1. Analysis of Insurance Premium Disparity Between Banks and Thrifts. ? FiJNDS. lhrsday

i GAO United States General Accounting Office Testimony Before the Subcommittee on Financial Institutions and Consumer Credit, Committee on Banking and Financial Services, House of Representatives For

i GAO United States General Accounting Office Testimony Before the Subcommittee on Financial Institutions and Consumer Credit, Committee on Banking and Financial Services, House of Representatives For

Guiding principles on the temporary funding needed to support the orderly resolution of a global systemically important bank ( G-SIB )

") Guiding principles on the temporary funding needed to support the orderly resolution of a global systemically important bank ( G-SIB ) Consultative Document 3 November 2015 ii The Financial Stability Board

Guiding principles on the temporary funding needed to support the orderly resolution of a global systemically important bank ( G-SIB ) Consultative Document 3 November 2015 ii The Financial Stability Board

René Garcia Professor of finance

Liquidity Risk: What is it? How to Measure it? René Garcia Professor of finance EDHEC Business School, CIRANO Cirano, Montreal, January 7, 2009 The financial and economic environment We are living through

Liquidity Risk: What is it? How to Measure it? René Garcia Professor of finance EDHEC Business School, CIRANO Cirano, Montreal, January 7, 2009 The financial and economic environment We are living through

Insurance as Operational Risk Management Tool

DOI: 10.7763/IPEDR. 2012. V54. 7 Insurance as Operational Risk Management Tool Milan Rippel 1, Lucie Suchankova 2 1 Charles University in Prague, Czech Republic 2 Charles University in Prague, Czech Republic

DOI: 10.7763/IPEDR. 2012. V54. 7 Insurance as Operational Risk Management Tool Milan Rippel 1, Lucie Suchankova 2 1 Charles University in Prague, Czech Republic 2 Charles University in Prague, Czech Republic

Debt Overhang and Capital Regulation

Debt Overhang and Capital Regulation Anat Admati INET in Berlin: Rethinking Economics and Politics The Challenge of Deleveraging and Overhangs of Debt II: The Politics and Economics of Restructuring April

Debt Overhang and Capital Regulation Anat Admati INET in Berlin: Rethinking Economics and Politics The Challenge of Deleveraging and Overhangs of Debt II: The Politics and Economics of Restructuring April

The Deutsche Bundesbank s Prudential Database (BAKIS)

") Schmollers Jahrbuch 128 (2008), 321 328 Duncker & Humblot, Berlin The Deutsche Bundesbank s Prudential Database (BAKIS) By Christoph Memmel and Ingrid Stein* Introduction Analyses and empirical studies

Schmollers Jahrbuch 128 (2008), 321 328 Duncker & Humblot, Berlin The Deutsche Bundesbank s Prudential Database (BAKIS) By Christoph Memmel and Ingrid Stein* Introduction Analyses and empirical studies

GUIDELINES ON RISK MANAGEMENT AND INTERNAL CONTROLS FOR INSURANCE AND REINSURANCE COMPANIES

20 th February, 2013 To Insurance Companies Reinsurance Companies GUIDELINES ON RISK MANAGEMENT AND INTERNAL CONTROLS FOR INSURANCE AND REINSURANCE COMPANIES These guidelines on Risk Management and Internal

20 th February, 2013 To Insurance Companies Reinsurance Companies GUIDELINES ON RISK MANAGEMENT AND INTERNAL CONTROLS FOR INSURANCE AND REINSURANCE COMPANIES These guidelines on Risk Management and Internal

RISK-BASED SUPERVISORY FRAMEWORK TEMPLATE FOR INSURANCE COMPANIES

RISK-BASED SUPERVISORY FRAMEWORK TEMPLATE FOR INSURANCE COMPANIES JUNE 26, 2006 This publication was produced for review by the United States Agency for International Development. It was prepared by Stephen

RISK-BASED SUPERVISORY FRAMEWORK TEMPLATE FOR INSURANCE COMPANIES JUNE 26, 2006 This publication was produced for review by the United States Agency for International Development. It was prepared by Stephen

Banking Union and Nexus between Banks and Sovereigns Jan Frait Executive Director Financial Stability Department

Banking Union and Nexus between Banks and Sovereigns Jan Frait Executive Director Financial Stability Department Presentation for the workshop Eurozone and the Banking Union Institute for International

Banking Union and Nexus between Banks and Sovereigns Jan Frait Executive Director Financial Stability Department Presentation for the workshop Eurozone and the Banking Union Institute for International

Understanding Two Different Industries

The Business of and Banking Understanding Two Different Industries Banks bipartisanpolicy.org @BPC_Bipartisan facebook.com/bipartisanpolicycenter @BPC_Bipartisan Introduction Immediately after the enactment

The Business of and Banking Understanding Two Different Industries Banks bipartisanpolicy.org @BPC_Bipartisan facebook.com/bipartisanpolicycenter @BPC_Bipartisan Introduction Immediately after the enactment

The International Certificate in Banking Risk and Regulation (ICBRR)

") The International Certificate in Banking Risk and Regulation (ICBRR) The ICBRR fosters financial risk awareness through thought leadership. To develop best practices in financial Risk Management, the authors

The International Certificate in Banking Risk and Regulation (ICBRR) The ICBRR fosters financial risk awareness through thought leadership. To develop best practices in financial Risk Management, the authors

The consequences of a low interest rate environment from a supervisory perspective

Annual Press Conference on 26 March 2013 Dr Patrick Raaflaub CEO The consequences of a low interest rate environment from a supervisory perspective Even if the news headlines had calmed down for a while,

Annual Press Conference on 26 March 2013 Dr Patrick Raaflaub CEO The consequences of a low interest rate environment from a supervisory perspective Even if the news headlines had calmed down for a while,

Monetary Operations: Liquidity Insurance

Monetary Operations: Liquidity Insurance Garreth Rule Operationalising Financial Stability CEMLA 25 29 November 2013 The Bank of England does not accept any liability for misleading or inaccurate information

Monetary Operations: Liquidity Insurance Garreth Rule Operationalising Financial Stability CEMLA 25 29 November 2013 The Bank of England does not accept any liability for misleading or inaccurate information

the actions of the party who is insured. These actions cannot be fully observed or verified by the insurance (hidden action).

.") Moral Hazard Definition: Moral hazard is a situation in which one agent decides on how much risk to take, while another agent bears (parts of) the negative consequences of risky choices. Typical case:

Moral Hazard Definition: Moral hazard is a situation in which one agent decides on how much risk to take, while another agent bears (parts of) the negative consequences of risky choices. Typical case:

Understanding Leverage in Closed-End Funds

Closed-End Funds Understanding Leverage in Closed-End Funds The concept of leverage seems simple: borrowing money at a low cost and using it to seek higher returns on an investment. Leverage as it applies

Closed-End Funds Understanding Leverage in Closed-End Funds The concept of leverage seems simple: borrowing money at a low cost and using it to seek higher returns on an investment. Leverage as it applies

Basel Committee on Banking Supervision. International Association of Deposit Insurers. Consultative Document

Basel Committee on Banking Supervision International Association of Deposit Insurers Consultative Document Core Principles for Effective Deposit Insurance Systems Issued for comment by 15 May 2009 March

Basel Committee on Banking Supervision International Association of Deposit Insurers Consultative Document Core Principles for Effective Deposit Insurance Systems Issued for comment by 15 May 2009 March

Insurance Europe response to FSB consultation on a policy framework for addressing shadow banking risks

Position Paper Insurance Europe response to FSB consultation on a policy framework for addressing shadow banking risks Our reference: ECO-INV-13-002 Date: 4 January 2013 Referring to: FSB Consultation

Position Paper Insurance Europe response to FSB consultation on a policy framework for addressing shadow banking risks Our reference: ECO-INV-13-002 Date: 4 January 2013 Referring to: FSB Consultation

Capital Adequacy: Asset Risk Charge

Prudential Standard LPS 114 Capital Adequacy: Asset Risk Charge Objective and key requirements of this Prudential Standard This Prudential Standard requires a life company to maintain adequate capital

Prudential Standard LPS 114 Capital Adequacy: Asset Risk Charge Objective and key requirements of this Prudential Standard This Prudential Standard requires a life company to maintain adequate capital

Subnational Borrowing Framework Lili Liu Lead Economist Economic Policy and Debt Department

International Seminar on Building New Countryside and Promoting Balanced Regional Development for a Harmonious Society Haikou, China 2006 年 8 月 21-26 日 Subnational Borrowing Framework Lili Liu Lead Economist

International Seminar on Building New Countryside and Promoting Balanced Regional Development for a Harmonious Society Haikou, China 2006 年 8 月 21-26 日 Subnational Borrowing Framework Lili Liu Lead Economist

BOARD OF GOVERNORS FEDERAL RESERVE SYSTEM

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D.C. 20551 DIVISION OF BANKING SUPERVISION AND REGULATION DIVISION OF CONSUMER AND COMMUNITY AFFAIRS SR 12-17 CA 12-14 December 17, 2012 TO

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D.C. 20551 DIVISION OF BANKING SUPERVISION AND REGULATION DIVISION OF CONSUMER AND COMMUNITY AFFAIRS SR 12-17 CA 12-14 December 17, 2012 TO

Subordinated Debt and the Quality of Market Discipline in Banking by Mark Levonian Federal Reserve Bank of San Francisco

Subordinated Debt and the Quality of Market Discipline in Banking by Mark Levonian Federal Reserve Bank of San Francisco Comments by Gerald A. Hanweck Federal Deposit Insurance Corporation Visiting Scholar,

Subordinated Debt and the Quality of Market Discipline in Banking by Mark Levonian Federal Reserve Bank of San Francisco Comments by Gerald A. Hanweck Federal Deposit Insurance Corporation Visiting Scholar,

Central Bank of Iraq. Press Communiqué

Central Bank of Iraq Press Communiqué New Central Bank policy instruments Summary At its August 26 meeting, the Board of the Central Bank of Iraq (CBI) adopted a new Reserve Requirement regulation and

Central Bank of Iraq Press Communiqué New Central Bank policy instruments Summary At its August 26 meeting, the Board of the Central Bank of Iraq (CBI) adopted a new Reserve Requirement regulation and

Net Stable Funding Ratio

Net Stable Funding Ratio Aims to establish a minimum acceptable amount of stable funding based on the liquidity characteristics of an institution s assets and activities over a one year horizon. The amount

Net Stable Funding Ratio Aims to establish a minimum acceptable amount of stable funding based on the liquidity characteristics of an institution s assets and activities over a one year horizon. The amount

The Empire Life Insurance Company

The Empire Life Insurance Company Condensed Interim Consolidated Financial Statements For the six months ended June 30, 2015 Unaudited Issue Date: August 7, 2015 DRAFT NOTICE OF NO AUDITOR REVIEW OF CONDENSED

The Empire Life Insurance Company Condensed Interim Consolidated Financial Statements For the six months ended June 30, 2015 Unaudited Issue Date: August 7, 2015 DRAFT NOTICE OF NO AUDITOR REVIEW OF CONDENSED

What s on a bank s balance sheet?

The Capital Markets Initiative January 2014 TO: Interested Parties FROM: David Hollingsworth and Lauren Oppenheimer RE: Capital Requirements and Bank Balance Sheets: Reviewing the Basics What s on a bank

The Capital Markets Initiative January 2014 TO: Interested Parties FROM: David Hollingsworth and Lauren Oppenheimer RE: Capital Requirements and Bank Balance Sheets: Reviewing the Basics What s on a bank

Should Banks Trade Equity Derivatives to Manage Credit Risk? Kevin Davis 9/4/1991

Should Banks Trade Equity Derivatives to Manage Credit Risk? Kevin Davis 9/4/1991 Banks incur a variety of risks and utilise different techniques to manage the exposures so created. Some of those techniques

Should Banks Trade Equity Derivatives to Manage Credit Risk? Kevin Davis 9/4/1991 Banks incur a variety of risks and utilise different techniques to manage the exposures so created. Some of those techniques

INCREASING GLOBAL FINANCIAL INTEGRITY: THE ROLES OF MARKET DISCIPLINE, REGULATION, AND SUPERVISION

INCREASING GLOBAL FINANCIAL INTEGRITY: THE ROLES OF MARKET DISCIPLINE, REGULATION, AND SUPERVISION Laurence H. Meyer Recent developments, both at home and abroad, have reinforced the importance of efforts

INCREASING GLOBAL FINANCIAL INTEGRITY: THE ROLES OF MARKET DISCIPLINE, REGULATION, AND SUPERVISION Laurence H. Meyer Recent developments, both at home and abroad, have reinforced the importance of efforts

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

Bank Capital Adequacy under Basel III

Bank Capital Adequacy under Basel III Objectives The overall goal of this two-day workshop is to provide participants with an understanding of how capital is regulated under Basel II and III and appreciate

Bank Capital Adequacy under Basel III Objectives The overall goal of this two-day workshop is to provide participants with an understanding of how capital is regulated under Basel II and III and appreciate

FINANCIAL STABILITY FORUM Working Group on Deposit Insurance

June 2000 International Guidance on Deposit Insurance A Consultative Process Background In November 1999, the Financial Stability Forum (FSF) - a forum convened by the G7 Finance Ministers and Central

June 2000 International Guidance on Deposit Insurance A Consultative Process Background In November 1999, the Financial Stability Forum (FSF) - a forum convened by the G7 Finance Ministers and Central

AN EMPIRICAL EXAMINATION OF DEPOSIT INSURANCE DECISIONS. Ei-Run Dga - Intro. University of Nebraska, 1984

AN EMPIRICAL EXAMINATION OF DEPOSIT INSURANCE DECISIONS Ei-Run Dga - Intro University of Nebraska, 1984 Advisers: Manferd O. Peterson and Robin Grieves Deposit insurance is implicitly or explicitly compulsory

AN EMPIRICAL EXAMINATION OF DEPOSIT INSURANCE DECISIONS Ei-Run Dga - Intro University of Nebraska, 1984 Advisers: Manferd O. Peterson and Robin Grieves Deposit insurance is implicitly or explicitly compulsory

http://angel.bfwpub.com/section/content/default.asp?wci=pgt...

Hmwk 14 1. Let's find out what counts as money. In this chapter, we used a typical definition of money: A widely accepted means of payment. Under this definition, which people are using money in the following

Hmwk 14 1. Let's find out what counts as money. In this chapter, we used a typical definition of money: A widely accepted means of payment. Under this definition, which people are using money in the following

SINGLE-FAMILY CREDIT RISK TRANSFER PROGRESS REPORT June 2016. Page Footer. Division of Housing Mission and Goals

SINGLE-FAMILY CREDIT RISK TRANSFER PROGRESS REPORT June 2016 Page Footer Division of Housing Mission and Goals Table of Contents Table of Contents... i Introduction... 1 Enterprise Efforts to Share Credit

SINGLE-FAMILY CREDIT RISK TRANSFER PROGRESS REPORT June 2016 Page Footer Division of Housing Mission and Goals Table of Contents Table of Contents... i Introduction... 1 Enterprise Efforts to Share Credit

Prof Kevin Davis Melbourne Centre for Financial Studies. Managing Liquidity Risks. Session 5.1. Training Program ~ 8 12 December 2008 SHANGHAI, CHINA

Enhancing Risk Management and Governance in the Region s Banking System to Implement Basel II and to Meet Contemporary Risks and Challenges Arising from the Global Banking System Training Program ~ 8 12

Enhancing Risk Management and Governance in the Region s Banking System to Implement Basel II and to Meet Contemporary Risks and Challenges Arising from the Global Banking System Training Program ~ 8 12

The Risk Free Investment Options Are Changing: A Guide for Plan Sponsors

The Risk Free Investment Options Are Changing: A Guide for Plan Sponsors Benjamin J. Smith, CFA Principal, Chief Investment Officer Contents Overview. Money Market Mutual Funds. A New Alternative to Money

The Risk Free Investment Options Are Changing: A Guide for Plan Sponsors Benjamin J. Smith, CFA Principal, Chief Investment Officer Contents Overview. Money Market Mutual Funds. A New Alternative to Money

The package of measures to avoid artificial volatility and pro-cyclicality

The package of measures to avoid artificial volatility and pro-cyclicality Explanation of the measures and the need to include them in the Solvency II framework Contents 1. Key messages 2. Why the package

The package of measures to avoid artificial volatility and pro-cyclicality Explanation of the measures and the need to include them in the Solvency II framework Contents 1. Key messages 2. Why the package

Bankruptcy law, bank liquidations and the case of Brazil. Aloisio Araujo IMPA, FGV Banco Central do Brasil May 6 th, 2013

Bankruptcy law, bank liquidations and the case of Brazil Aloisio Araujo IMPA, FGV Banco Central do Brasil May 6 th, 2013 Description of the talk A. Corporate bankruptcy law reform in Brazil How bad is

Bankruptcy law, bank liquidations and the case of Brazil Aloisio Araujo IMPA, FGV Banco Central do Brasil May 6 th, 2013 Description of the talk A. Corporate bankruptcy law reform in Brazil How bad is

Weaknesses in Regulatory Capital Models and Their Implications

Weaknesses in Regulatory Capital Models and Their Implications Amelia Ho, CA, CIA, CISA, CFE, ICBRR, PMP, MBA 2012 Enterprise Risk Management Symposium April 18-20, 2012 2012 Casualty Actuarial Society,

Weaknesses in Regulatory Capital Models and Their Implications Amelia Ho, CA, CIA, CISA, CFE, ICBRR, PMP, MBA 2012 Enterprise Risk Management Symposium April 18-20, 2012 2012 Casualty Actuarial Society,

Chapter 12 Practice Problems

Chapter 12 Practice Problems 1. Bankers hold more liquid assets than most business firms. Why? The liabilities of business firms (money owed to others) is very rarely callable (meaning that it is required

Chapter 12 Practice Problems 1. Bankers hold more liquid assets than most business firms. Why? The liabilities of business firms (money owed to others) is very rarely callable (meaning that it is required

Santander Views on Basel s Liquidity Framework

Santander Views on Basel s Liquidity Framework Presentation Santander welcomes the effort made by the Basel Committee to safeguard financial market stability and to preserve the system from a renewed liquidity

Santander Views on Basel s Liquidity Framework Presentation Santander welcomes the effort made by the Basel Committee to safeguard financial market stability and to preserve the system from a renewed liquidity

Basel II. Tamer Bakiciol Nicolas Cojocaru-Durand Dongxu Lu

Basel II Tamer Bakiciol Nicolas Cojocaru-Durand Dongxu Lu Roadmap Background of Banking Regulation and Basel Accord Basel II: features and problems The Future of Banking regulations Background of Banking

Basel II Tamer Bakiciol Nicolas Cojocaru-Durand Dongxu Lu Roadmap Background of Banking Regulation and Basel Accord Basel II: features and problems The Future of Banking regulations Background of Banking

Credit Guarantees for Small Business Lending

Credit Guarantees for Small Business Lending -Experiences of a small business credit guarantee company Contents Importance of SMEs in the Chinese economy SMEs current access to finance Current status of

Credit Guarantees for Small Business Lending -Experiences of a small business credit guarantee company Contents Importance of SMEs in the Chinese economy SMEs current access to finance Current status of

PNB Life Insurance Inc. Risk Management Framework

1. Capital Management and Management of Insurance and Financial Risks Although life insurance companies are in the business of taking risks, the Company limits its risk exposure only to measurable and

1. Capital Management and Management of Insurance and Financial Risks Although life insurance companies are in the business of taking risks, the Company limits its risk exposure only to measurable and

How To Calculate Financial Leverage Ratio

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

Understanding Central Banking in Light of the Credit Turmoil

Understanding Central Banking in Light of the Credit Turmoil Marvin Goodfriend Tepper School Carnegie Mellon University Implementing Monetary Policy Post-Crisis: What Have We Learned? What Do We Need to

Understanding Central Banking in Light of the Credit Turmoil Marvin Goodfriend Tepper School Carnegie Mellon University Implementing Monetary Policy Post-Crisis: What Have We Learned? What Do We Need to

Deposit Insurance Establishment (Financed by the People s Republic of China Regional Cooperation and Poverty Reduction Fund)

") Technical Assistance Report Project Number: 43074 Regional Policy and Advisory Technical Assistance (R-PATA) August 2009 Deposit Insurance Establishment (Financed by the People s Republic of China Regional

Technical Assistance Report Project Number: 43074 Regional Policy and Advisory Technical Assistance (R-PATA) August 2009 Deposit Insurance Establishment (Financed by the People s Republic of China Regional

IndyMac. John F. Bovenzi Deputy to the Chairman and Chief Operating Officer, Federal Deposit Insurance Corporation April 3, 2009

IndyMac Federal Bank FSB John F. Bovenzi Deputy to the Chairman and Chief Operating Officer, Federal Deposit Insurance Corporation April 3, 2009 FDIC s Resolution Strategies Open Bank Assistance Financial

IndyMac Federal Bank FSB John F. Bovenzi Deputy to the Chairman and Chief Operating Officer, Federal Deposit Insurance Corporation April 3, 2009 FDIC s Resolution Strategies Open Bank Assistance Financial

Does Deposit Insurance Increase Banking System Stability? An Empirical Investigation. Aslı Demirgüç-Kunt and Enrica Detragiache

Does Deposit Insurance Increase Banking System Stability? An Empirical Investigation Aslı Demirgüç-Kunt and Enrica Detragiache Objective Does deposit insurance affect bank stability? Do differences in

Does Deposit Insurance Increase Banking System Stability? An Empirical Investigation Aslı Demirgüç-Kunt and Enrica Detragiache Objective Does deposit insurance affect bank stability? Do differences in

International Accounting Standard 32 Financial Instruments: Presentation

EC staff consolidated version as of 21 June 2012, EN EU IAS 32 FOR INFORMATION PURPOSES ONLY International Accounting Standard 32 Financial Instruments: Presentation Objective 1 [Deleted] 2 The objective

EC staff consolidated version as of 21 June 2012, EN EU IAS 32 FOR INFORMATION PURPOSES ONLY International Accounting Standard 32 Financial Instruments: Presentation Objective 1 [Deleted] 2 The objective

2. The European insurance sector 1

2. The European insurance sector 1 The life sector faces new growth opportunities with the aging of populations worldwide, while the non-life sector may look for new innovative products. Structural budget

2. The European insurance sector 1 The life sector faces new growth opportunities with the aging of populations worldwide, while the non-life sector may look for new innovative products. Structural budget

Basel II, Pillar 3 Disclosure for Sun Life Financial Trust Inc.

Basel II, Pillar 3 Disclosure for Sun Life Financial Trust Inc. Introduction Basel II is an international framework on capital that applies to deposit taking institutions in many countries, including Canada.

Basel II, Pillar 3 Disclosure for Sun Life Financial Trust Inc. Introduction Basel II is an international framework on capital that applies to deposit taking institutions in many countries, including Canada.

Basel Committee on Banking Supervision. International Association of Deposit Insurers. Core Principles for Effective Deposit Insurance Systems

Basel Committee on Banking Supervision International Association of Deposit Insurers Core Principles for Effective Deposit Insurance Systems A methodology for compliance assessment December 2010 Copies

Basel Committee on Banking Supervision International Association of Deposit Insurers Core Principles for Effective Deposit Insurance Systems A methodology for compliance assessment December 2010 Copies

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014

Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014") Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial year from 1 January 2014 to 31 December 2014

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial year from 1 January 2014 to 31 December 2014

Measures for Ensuring the Stability of the Payment and Settlement Functions of Financial Institutions (Executive Summary)

") (Provisional translation) Report of the Financial System Council Measures for Ensuring the Stability of the Payment and Settlement Functions of Financial Institutions (Executive Summary) 1. Preface It

(Provisional translation) Report of the Financial System Council Measures for Ensuring the Stability of the Payment and Settlement Functions of Financial Institutions (Executive Summary) 1. Preface It

STATEMENT OF THE FEDERAL DEPOSIT INSURANCE CORPORATION LEGISLATIVE PROPOSALS TO CREATE A COVERED BOND MARKET IN THE UNITED STATES

STATEMENT OF THE FEDERAL DEPOSIT INSURANCE CORPORATION on LEGISLATIVE PROPOSALS TO CREATE A COVERED BOND MARKET IN THE UNITED STATES SUBCOMMITTEE ON CAPITAL MARKETS AND GOVERNMENT- SPONSORED ENTERPRISES

STATEMENT OF THE FEDERAL DEPOSIT INSURANCE CORPORATION on LEGISLATIVE PROPOSALS TO CREATE A COVERED BOND MARKET IN THE UNITED STATES SUBCOMMITTEE ON CAPITAL MARKETS AND GOVERNMENT- SPONSORED ENTERPRISES

Life Insurance risk management in the Insurance company : CSOB case studies

Life Insurance risk management in the Insurance company : CSOB case studies Content Topics : case study Life Insurance risk management, 1. Life Insurance 2. Case study what is life insurance product and

Life Insurance risk management in the Insurance company : CSOB case studies Content Topics : case study Life Insurance risk management, 1. Life Insurance 2. Case study what is life insurance product and

RBC Money Market Funds Prospectus

RBC Money Market Funds Prospectus November 25, 2015 Prime Money Market Fund RBC Institutional Class 1: RBC Institutional Class 2: RBC Select Class: RBC Reserve Class: RBC Investor Class: TPNXX TKIXX TKSXX

RBC Money Market Funds Prospectus November 25, 2015 Prime Money Market Fund RBC Institutional Class 1: RBC Institutional Class 2: RBC Select Class: RBC Reserve Class: RBC Investor Class: TPNXX TKIXX TKSXX

Financial Status, Operating Results and Risk Management

Financial Status, Operating Results and Risk Management 87 Financial Status 88 89 90 90 90 95 95 Operating Results Cash Flow Effects of Major Capital Expenditures in the Most Recent Fiscal Year on Financial

Financial Status, Operating Results and Risk Management 87 Financial Status 88 89 90 90 90 95 95 Operating Results Cash Flow Effects of Major Capital Expenditures in the Most Recent Fiscal Year on Financial