Basel II. Tamer Bakiciol Nicolas Cojocaru-Durand Dongxu Lu

|

|

|

- Evelyn Nichols

- 8 years ago

- Views:

Transcription

1 Basel II Tamer Bakiciol Nicolas Cojocaru-Durand Dongxu Lu

2 Roadmap Background of Banking Regulation and Basel Accord Basel II: features and problems The Future of Banking regulations

3 Background of Banking Regulation and Basel Accord

4 Banking Supervision and Capital Regulation Purpose of banking supervision is to ensure that banks operate in a safe and sound manner. to ensure that banks "hold capital and reserves sufficient to support the risks that arise in their business". sound practices for banks' risk management Regulatory Capital list of the elements that count as capital for regulatory purposes the set of conditions these elements must comply with in order to be considered eligible. Risk-Weighted Assets all exposures after conversion into assets and after having received supervisory risk weights according to their degree of risk. A supervisory risk weight is a percentage used to convert the nominal amount of a credit exposure into an amount of 'exposure at risk'. Economic Capital: trade off between profitability and insolvency

5 Basel

6 What is the Basel Committee? Basel Committee on Banking Supervision was established by the central-bank governors of the G10 countries in 1974 Belgium, Canada, France, Germany, Italy, Japan, Luxemburg, Netherlands, Spain, Sweden, Switzerland, UK, US Meets at the Bank for International Settlements in Basel Its objective was to enhance understanding of key supervisory issues and improve the quality of banking supervision worldwide. Not a formal supranational supervisory authority and conclusions do not have legal force. Formulates broad supervisory standards and guidelines First major result was the 1988 Capital Accord 1997 developed a set of "Core Principles for Effective Banking Supervision ", which provides a comprehensive blueprint for an effective supervisory system.

7 Basel Capital Accords Chronology Basel I Capital Accord (1988) Amendment to the capital accord to incorporate market risks (1996) Basel II Capital Accord First Consultative Paper (1999) Second Consultative Paper (2001) Third Consultative Paper (2003) Final Document (2004) Basel II: International Convergence of Capital Measurement and Capital Standards: a Revised Framework Amendment (2005) The Application of Basel II to Trading Activities and the Treatment of Double Default Effects Final Version(2006) Basel II: International Convergence of Capital Measurement and Capital Standards: A Revised Framework - Comprehensive Version Proposed revisions to the Basel II market risk framework (2008)

8 Motives for Basel I Deregulation period after 1980 Increase in International presence of banks Decline in capital ratios of Banks just as increase in riskiness Risk posed to the stability of the global financial system by low capital levels of internationally active banks Competitive advantage accruing to banks subject to lower capital requirements Create a level of playing field

9 Motives and Objectives for Basel II Motives: Problems with Basel I Club-rule (being a member of OECD) is not meaningful in terms of riskiness Broad brush and lacks risk differentiation: One size fits all Divergence between Basel I risk weights and actual economic risks Regulatory arbitrage (Solved?) Inadequate recognition of advanced credit risk mitigation techniques(securitization and CDS) Objectives Eliminate regulatory arbitrage by getting risk weights right Align regulation with best practices in risk management Provide banks with incentives to enhance risk measurement and management capabilities. Basel II is not intended simply to ensure compliance with a new set of capital rules. Rather, it is intended to enhance the quality of risk management and supervision. Jaime Caruana Governor of the Banco de España Former Chairman of Basel Committee

10 Features and Problems of Basel II

11 3 Pillars of Basel II The second pillar supervisory review allows supervisors to evaluate a bank s assessment of its own risks and determine whether that assessment seems reasonable. It is not enough for a bank or its supervisors to rely on the calculation of minimum capital under the first pillar. Supervisors should provide an extra set of eyes to verify that the bank understands its risk profile and is sufficiently capitalized against its risks. The third pillar market discipline ensures that the market provides yet another set of eyes. The third pillar is intended to strengthen incentives for prudent risk management. Greater transparency in banks financial reporting should allow marketplace participants to better reward well-managed banks and penalize poorly-managed ones. Jaime Caruana

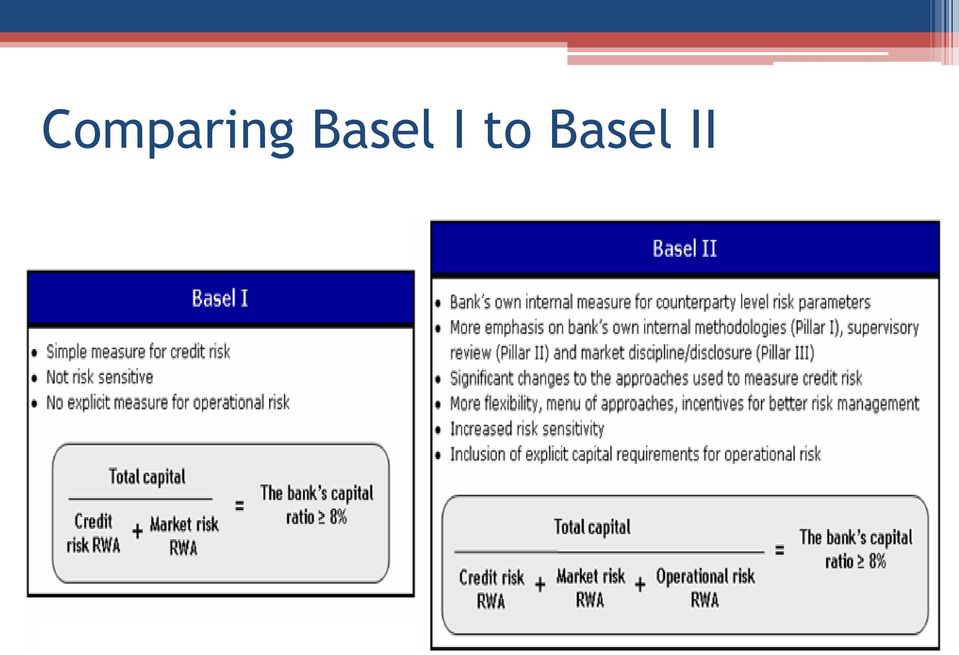

12 Comparing Basel I to Basel II

13 Pillar 1:Minimum Capital Requirements Pillar 1 Pillar 2 Pillar 3 Minimum Capital Requirements Supervisory Review Market Discipline Credit Risk Market Risk Operational Risk

14 Bank Capital Definition of regulatory bank capital established in 1988 under Basel I remains largely the same today and is also applicable under Basel II comprised of three levels (or 'tiers') of capital. An item may be classified under one of these tiers if it satisfies specific eligibility criteria. eligibility criteria for capital components ensure the similarity across all the countries. This has lead to greater comparability among banks, especially among those that are internationally active. criteria are: permanence, freedom (the ability to absorb losses on an ongoing basis), subordination to depositors and other creditors The extent to which capital instruments meet these broad criteria will determine the tier of capital in which they are categorized: Tier 1 or Tier 2

15 Tier 1 Capital Deemed to have highest capacity to absorbing losses in order to allow banks continue to operate on ongoing basis common shareholder equity Fully paid therefore available to absorb losses permanently Should losses occur, it is the common shareholders who bear such losses first Disclosed Reserves Published reserves derived from post-tax retained earnings and after dividend payments non-cumulative perpetual preferred stock

16 Tier 2 & Tier 3 Capital Tier 2 cannot exceed 100% of Tier 1 capital subordinated debt undisclosed reserves: availability is more uncertain general loan loss reserves hybrid debt equity capital instruments Tier 3 can be used to meet a proportion of the capital requirements of market risk Consist of subordinated debt with some limitations

17 Credit Risk Pillar 1 Pillar 2 Pillar 3 Minimum Capital Requirements Supervisory Review Market Discipline Credit Risk Market Risk Operational Risk

18 Credit Risk Standardized Approach Internal Ratings Based Approach (IRB) Foundation Advanced Credit risk mitigation CDS & Counterparty risk Securitization

19 Standardized Approach Based on external credit ratings Apply fixed risk weighting to assets based on: Type of entity (Sovereign, Commercial bank, Corporates, retail, etc.) Credit rating (AAA, Aaa,, Bbb)

20 Standardized Approach Pros: Simple Doesn t require extensive modeling Attractive for smaller banks with less experience Uniform across banks Cons: Less flexible and perhaps realistic Rests on credit ratings devised by external agencies (Moody s, S&P, Fitch)

21 Credit Ratings vs. Risk Weighted Assets

22 Credit Ratings: Sovereigns

23

24 Internal ratings based Based on internal loss models Two approaches Foundation: Bank produces own loss probability models (i.e. own credit ratings), but uses prescribed estimates of Loss Given Default (LGD) based on ratings Advanced: Bank uses own loss probability models and LGD models

25 IRB Example Correlation (R) = 0.12 (1 EXP(-50 PD)) / (1 EXP(-50)) [1 (1 EXP(-50 PD)) / (1 EXP(-50))] Maturity adjustment (b) = ( ln(pd))^2 Capital requirement (K) = [LGD N[(1 R)^-0.5 G(PD) + (R / (1 R))^0.5 G(0.999)] PD x LGD] x (1 1.5 x b)^-1 (1 + (M 2.5) b) Risk-weighted assets (RWA) = K x 12.5 x EAD

26

27 Internal Ratings Based Pros: More realistic Favored by larger banks, mandatory for large US banks Cons Similar to VaR: modeling rare events Large investment needed to put in place and maintain Large data requirement (5+ years) More discretion to banks as to how they value their risks

28 Standardized vs. IRB: by pd For small prob. of defaults large difference in risk weighting Source: Wikipedia, en.wikipedia.org/foundation_irb

29 Standardized vs. IRB: by credit

30 Adverse Selection

31 Securitization and credit protection Just like you can buy life insurance, banks can protect themselves against defaults by buying Credit Default Swaps (CDS) This exposes them to counterparty risk however They can also get rid of bad loans/risky exposure (even CDS) by repackaging assets in CDOs which are housed off balancesheet Loans SIV CDO tranches L1 L3 L5 L2 L4 B1 AAA B2 AA

32 CDO structure Using low-rated bonds, 2/3 of the new structure has higher rating If pd doubles (5% to 10%), the Senior tranche retains its rating, but not the rest

33 Regulatory arbitrage In hindsight, SIV s enabled banks to house risky assets outside the scope of Basel rules Because of the diversification coming from the pooling of risky assets, the tranches issued had higher credit ratings Limited provisions were made for the liquidity clause banks had with their SIV s especially if they issued short-term assets (ABCP) Combined, this reduced regulatory capital to be held and enabled more risk-taking

34 Market Risk Pillar 1 Pillar 2 Pillar 3 Minimum Capital Requirements Supervisory Review Market Discipline Credit Risk Market Risk Operational Risk Risk of losses of on- and off- balance sheet positions arising from movement in market price (interest rate, equity positions, foreign exchange and commodity risk)

35 Market Risk Market Risk General Market Risk Specific Risk VaR * Regulatory Coefficient Standardized Internal Model 10 day time horizon 99% confidence level May range from 3.0 to 4.0

36 Value at Risk For market risk the preferred approach is VaR (value at risk).

37 Problems with VaR Does not give the actual size of loss Fat tail Problem Created an incentive to take excessive but remote risks

38 Conditional VaR (CVaR) The CVaR at q% level" is the expected return on the portfolio in the worst q% of the cases.

39 Stress Testing and Scenario Analysis Test the portfolio under some stresses(e.g.): What happens if the market crashes by more than x% this year? What happens if interest rates go up by at least y%? What happens if oil prices rise by 200%?

40 Operational Risk Pillar 1 Pillar 2 Pillar 3 Minimum Capital Requirements Credit Risk Market Risk Operational Risk Supervisory Review Market Discipline Risk arising from execution of a company's business functions (e.g. legal risk)

41 Operational Risk Increasing sophistication Basic Indicator Approach Operational Risk Capital= α * Gross Revenue α is a percentage set by regulator Standardized Approach Operational Risk Capital= β * Gross Revenue per Business Line β is a percentage set by regulator Advanced Measurement Approach Operational Risk Capital= the risk measure generated by the bank s own operational risk measurement system

42 Pillar 2: Supervisory Review Pillar 1 Pillar 2 Pillar 3 Minimum Capital Requirements Supervisory Review Market Discipline Credit Risk Market Risk Operational Risk

43 Supervisory Review Principle 1: Banks should have a process for assessing their overall capital adequacy in relation to their risk profile and a strategy for maintaining their capital levels. Principle 2: Supervisors should review and evaluate banks internal capital adequacy assessments and strategies, as well as their ability to monitor and ensure their compliance with regulatory capital ratios. Supervisors should take appropriate supervisory action if they are not satisfied with the result of this process. Principle 3: Supervisors should expect banks to operate above the minimum regulatory capital ratios and should have the ability to require banks to hold capital in excess of the minimum. Principle 4: Supervisors should seek to intervene at an early stage to prevent capital from falling below the minimum levels required to support the risk characteristics of a particular bank and should require rapid remedial action if capital is not maintained or restored.

44 Pillar 3: Market Discipline Pillar 1 Pillar 2 Pillar 3 Minimum Capital Requirements Supervisory Review Market Discipline Credit Risk Market Risk Operational Risk

45 Market Discipline The third pillar greatly increases the disclosures that the bank must make. This is designed to allow the market to have a better picture of the overall risk position of the bank and to allow the counterparties of the bank to price and deal appropriately.

46 Beyond Basel II

47 Rethinking Basel II Even theoretically sound rules may be suboptimal because of compliance costs and supervisory limitations: Cost of Basel II? Basel 2 Risk rating will be determined by the assessments of external credit rating agencies. Debatable, after shortcomings exposed by subprime crisis Macroeconomic: Procyclicality More measures of system risk:covar

48 16 April 2008 Basel Committee announces steps to strengthen the resilience of the banking system The Committee reiterates the importance of implementing the Basel II Framework as it better reflects the types of risks banks face in an increasingly market-based credit intermediation process The committee acknowledged the deficiencies in the Framework. Further strengthening certain aspects of the Framework: higher capital requirements for certain complex structured credit products, such as so-called "resecuritisations" or CDOs of ABS, which have produced the majority of losses during the recent market turbulence. strengthen the capital treatment of liquidity facilities extended to support off-balance sheet vehicles such as ABCP conduits. strengthen the capital requirements in the trading book. Global banks' trading assets have grown at double digit rates in recent years, and the proportion of complex, less liquid credit products held in the trading book has likewise increased rapidly.

49 16 April 2008 Basel Committee announces steps to strengthen the resilience of the banking system The current value-at-risk based treatment for assessing capital for trading book risk does not capture extraordinary events that can affect many such exposures. Measures will be taken to include potential event risks in the trading book. The market turmoil has revealed significant risk management weaknesses at banking institutions. Issuance of Pillar 2 guidance in a number of areas to help strengthen risk management and supervisory practices: management of firm-wide risks banks' stress testing practices capital planning processes the management of off-balance sheet exposures and associated reputational risks risk management practices relating to securitization activities supervisory assessment of banks' valuation practices.

50 16 April 2008 Basel Committee announces steps to strengthen the resilience of the banking system Banks need to have strong liquidity cushions to weather prolonged periods of financial market stress and illiquidity Weaknesses in bank transparency and valuation practices for complex products have contributed to the build-up of concentrations in illiquid structured credit products and the undermining of confidence in the banking sector. The Committee will promote enhanced disclosures relating to complex securitization exposures, ABCP conduits and the sponsorship of off-balance sheet vehicles.

Bank Capital Adequacy under Basel III

Bank Capital Adequacy under Basel III Objectives The overall goal of this two-day workshop is to provide participants with an understanding of how capital is regulated under Basel II and III and appreciate

Bank Capital Adequacy under Basel III Objectives The overall goal of this two-day workshop is to provide participants with an understanding of how capital is regulated under Basel II and III and appreciate

Basel Committee on Banking Supervision

Basel Committee on Banking Supervision Reducing excessive variability in banks regulatory capital ratios A report to the G20 November 2014 This publication is available on the BIS website (www.bis.org).

Basel Committee on Banking Supervision Reducing excessive variability in banks regulatory capital ratios A report to the G20 November 2014 This publication is available on the BIS website (www.bis.org).

Commercial paper collateralized by a pool of loans, leases, receivables, or structured credit products. Asset-backed commercial paper (ABCP)

") GLOSSARY Asset-backed commercial paper (ABCP) Asset-backed security (ABS) Asset-backed securities index (ABX) Basel II Call (put) option Carry trade Collateralized debt obligation (CDO) Collateralized

GLOSSARY Asset-backed commercial paper (ABCP) Asset-backed security (ABS) Asset-backed securities index (ABX) Basel II Call (put) option Carry trade Collateralized debt obligation (CDO) Collateralized

Commercial paper collateralized by a pool of loans, leases, receivables, or structured credit products.

Asset-backed commercial paper (ABCP) Asset-backed security (ABS) Asset-backed securities index (ABX) Auction rate security Basel II Call (put) option Carry trade Commercial paper collateralized by a pool

Asset-backed commercial paper (ABCP) Asset-backed security (ABS) Asset-backed securities index (ABX) Auction rate security Basel II Call (put) option Carry trade Commercial paper collateralized by a pool

BASEL III PILLAR 3 CAPITAL ADEQUACY AND RISKS DISCLOSURES AS AT 30 SEPTEMBER 2015

BASEL III PILLAR 3 CAPITAL ADEQUACY AND RISKS DISCLOSURES AS AT 30 SEPTEMBER 2015 COMMONWEALTH BANK OF AUSTRALIA ACN 123 123 124 5 NOVEMBER 2015 This page has been intentionally left blank Introduction

BASEL III PILLAR 3 CAPITAL ADEQUACY AND RISKS DISCLOSURES AS AT 30 SEPTEMBER 2015 COMMONWEALTH BANK OF AUSTRALIA ACN 123 123 124 5 NOVEMBER 2015 This page has been intentionally left blank Introduction

Market Risk Capital Disclosures Report. For the Quarter Ended March 31, 2013

MARKET RISK CAPITAL DISCLOSURES REPORT For the quarter ended March 31, 2013 Table of Contents Section Page 1 Morgan Stanley... 1 2 Risk-based Capital Guidelines: Market Risk... 1 3 Market Risk... 1 3.1

MARKET RISK CAPITAL DISCLOSURES REPORT For the quarter ended March 31, 2013 Table of Contents Section Page 1 Morgan Stanley... 1 2 Risk-based Capital Guidelines: Market Risk... 1 3 Market Risk... 1 3.1

2. Banks must maintain a total capital ratio of at least 10% and a minimum Tier 1 ratio of 6%.

Chapter I Calculation of Minimum Capital Requirements INTRODUCTION 1. This section sets out the calculation of the total minimum capital requirements that Banks must meet for exposures to credit risk,

Chapter I Calculation of Minimum Capital Requirements INTRODUCTION 1. This section sets out the calculation of the total minimum capital requirements that Banks must meet for exposures to credit risk,

Stress testing and capital planning - the key to making the ICAAP forward looking PRMIA Greece Chapter Meeting Athens, 25 October 2007

Stress testing and capital planning - the key to making the ICAAP forward looking Athens, *connectedthinking Agenda Introduction on ICAAP requirements What is stress testing? Regulatory guidance on stress

Stress testing and capital planning - the key to making the ICAAP forward looking Athens, *connectedthinking Agenda Introduction on ICAAP requirements What is stress testing? Regulatory guidance on stress

1) What kind of risk on settlements is covered by 'Herstatt Risk' for which BCBS was formed?

What kind of risk on settlements is covered by 'Herstatt Risk' for which BCBS was formed?") 1) What kind of risk on settlements is covered by 'Herstatt Risk' for which BCBS was formed? a) Exchange rate risk b) Time difference risk c) Interest rate risk d) None 2) Which of the following is not

1) What kind of risk on settlements is covered by 'Herstatt Risk' for which BCBS was formed? a) Exchange rate risk b) Time difference risk c) Interest rate risk d) None 2) Which of the following is not

CANADIAN TIRE BANK. BASEL PILLAR 3 DISCLOSURES December 31, 2014 (unaudited)

") (unaudited) 1. SCOPE OF APPLICATION Basis of preparation This document represents the Basel Pillar 3 disclosures for Canadian Tire Bank ( the Bank ) and is unaudited. The Basel Pillar 3 disclosures included

(unaudited) 1. SCOPE OF APPLICATION Basis of preparation This document represents the Basel Pillar 3 disclosures for Canadian Tire Bank ( the Bank ) and is unaudited. The Basel Pillar 3 disclosures included

Risk & Capital Management under Basel III

www.pwc.com Risk & Capital Management under Basel III London, 15 Draft Agenda Basel III changes to capital rules - Definition of capital - Minimum capital ratios - Leverage ratio - Buffer requirements

www.pwc.com Risk & Capital Management under Basel III London, 15 Draft Agenda Basel III changes to capital rules - Definition of capital - Minimum capital ratios - Leverage ratio - Buffer requirements

LIQUIDITY RISK MANAGEMENT GUIDELINE

LIQUIDITY RISK MANAGEMENT GUIDELINE April 2009 Table of Contents Preamble... 3 Introduction... 4 Scope... 5 Coming into effect and updating... 6 1. Liquidity risk... 7 2. Sound and prudent liquidity risk

LIQUIDITY RISK MANAGEMENT GUIDELINE April 2009 Table of Contents Preamble... 3 Introduction... 4 Scope... 5 Coming into effect and updating... 6 1. Liquidity risk... 7 2. Sound and prudent liquidity risk

Capital adequacy ratios for banks - simplified explanation and

Page 1 of 9 Capital adequacy ratios for banks - simplified explanation and example of calculation Summary Capital adequacy ratios are a measure of the amount of a bank's capital expressed as a percentage

Page 1 of 9 Capital adequacy ratios for banks - simplified explanation and example of calculation Summary Capital adequacy ratios are a measure of the amount of a bank's capital expressed as a percentage

Securitized-Product Investment: Risk Management Perspectives *

- March 2008 Paper Series of Risk Management in Financial Institutions Securitized-Product Investment: Risk Management Perspectives * Financial Systems and Bank Examination Department Bank of Japan Please

- March 2008 Paper Series of Risk Management in Financial Institutions Securitized-Product Investment: Risk Management Perspectives * Financial Systems and Bank Examination Department Bank of Japan Please

Basel II, Pillar 3 Disclosure for Sun Life Financial Trust Inc.

Basel II, Pillar 3 Disclosure for Sun Life Financial Trust Inc. Introduction Basel II is an international framework on capital that applies to deposit taking institutions in many countries, including Canada.

Basel II, Pillar 3 Disclosure for Sun Life Financial Trust Inc. Introduction Basel II is an international framework on capital that applies to deposit taking institutions in many countries, including Canada.

TD Bank Financial Group Q4/08 Guide to Basel II

TD Bank Financial Group Q4/08 Guide to Basel II 1. OVERVIEW General Information on Basel can be found on the Canadian Bankers Association website at www.cba.ca. Choose Issues, Standards, Rules and Guidelines

TD Bank Financial Group Q4/08 Guide to Basel II 1. OVERVIEW General Information on Basel can be found on the Canadian Bankers Association website at www.cba.ca. Choose Issues, Standards, Rules and Guidelines

Basel III Pillar 3 CAPITAL ADEQUACY AND RISK DISCLOSURES AS AT 30 SEPTEMBER 2014

Basel III Pillar 3 CAPITAL ADEQUACY AND RISK DISCLOSURES AS AT 30 SEPTEMBER 2014 COMMONWEALTH BANK OF AUSTRALIA ACN 123 123 124 5 NOVEMBER 2014 1 Scope of Application The Commonwealth Bank of Australia

Basel III Pillar 3 CAPITAL ADEQUACY AND RISK DISCLOSURES AS AT 30 SEPTEMBER 2014 COMMONWEALTH BANK OF AUSTRALIA ACN 123 123 124 5 NOVEMBER 2014 1 Scope of Application The Commonwealth Bank of Australia

3/22/2010. Chapter 11. Eight Categories of Bank Regulation. Economic Analysis of. Regulation Lecture 1. Asymmetric Information and Bank Regulation

Chapter 11 Economic Analysis of Banking Regulation Lecture 1 Asymmetric Information and Bank Regulation Adverse Selection and Moral Hazard are the two concepts that underlie government regulation of the

Chapter 11 Economic Analysis of Banking Regulation Lecture 1 Asymmetric Information and Bank Regulation Adverse Selection and Moral Hazard are the two concepts that underlie government regulation of the

ZAG BANK BASEL II & III PILLAR 3 DISCLOSURES. December 31, 2014

ZAG BANK BASEL II & III PILLAR 3 DISCLOSURES December 31, 2014 Zag Bank (the Bank ) is required to make certain disclosures to meet the requirements of the Office of the Superintendent of Financial Institutions

ZAG BANK BASEL II & III PILLAR 3 DISCLOSURES December 31, 2014 Zag Bank (the Bank ) is required to make certain disclosures to meet the requirements of the Office of the Superintendent of Financial Institutions

Weaknesses in Regulatory Capital Models and Their Implications

Weaknesses in Regulatory Capital Models and Their Implications Amelia Ho, CA, CIA, CISA, CFE, ICBRR, PMP, MBA 2012 Enterprise Risk Management Symposium April 18-20, 2012 2012 Casualty Actuarial Society,

Weaknesses in Regulatory Capital Models and Their Implications Amelia Ho, CA, CIA, CISA, CFE, ICBRR, PMP, MBA 2012 Enterprise Risk Management Symposium April 18-20, 2012 2012 Casualty Actuarial Society,

The Ratio of Leverage. When you combine ignorance and leverage, you get some pretty interesting results. Warren Buffett

The Ratio of Leverage When you combine ignorance and leverage, you get some pretty interesting results. Warren Buffett 1 What is leverage? definition of leverage: debt to equity ratio Basel Commitee: One

The Ratio of Leverage When you combine ignorance and leverage, you get some pretty interesting results. Warren Buffett 1 What is leverage? definition of leverage: debt to equity ratio Basel Commitee: One

ICAAP Required Capital Assessment, Quantification & Allocation. Anand Borawake, VP, Risk Management, TD Bank anand.borawake@td.com

ICAAP Required Capital Assessment, Quantification & Allocation Anand Borawake, VP, Risk Management, TD Bank anand.borawake@td.com Table of Contents Key Takeaways - Value Add from the ICAAP The 3 Pillars

ICAAP Required Capital Assessment, Quantification & Allocation Anand Borawake, VP, Risk Management, TD Bank anand.borawake@td.com Table of Contents Key Takeaways - Value Add from the ICAAP The 3 Pillars

Regulatory Capital Disclosures

The Goldman Sachs Group, Inc. Regulatory Capital Disclosures For the period ended March 31, 2014 0 P age Introduction The Goldman Sachs Group, Inc. (Group Inc.) is a leading global investment banking,

The Goldman Sachs Group, Inc. Regulatory Capital Disclosures For the period ended March 31, 2014 0 P age Introduction The Goldman Sachs Group, Inc. (Group Inc.) is a leading global investment banking,

EASY FOREX TRADING LTD DISCLOSURE AND MARKET DISCIPLINE IN ACCORDANCE WITH CAPITAL ADEQUACY AND THE REQUIREMENTS ON RISK MANAGEMENT

EASY FOREX TRADING LTD DISCLOSURE AND MARKET DISCIPLINE IN ACCORDANCE WITH CAPITAL ADEQUACY AND THE REQUIREMENTS ON RISK MANAGEMENT 31 st December 2012 Introduction For the purposes of Directive DI144-2007-05

EASY FOREX TRADING LTD DISCLOSURE AND MARKET DISCIPLINE IN ACCORDANCE WITH CAPITAL ADEQUACY AND THE REQUIREMENTS ON RISK MANAGEMENT 31 st December 2012 Introduction For the purposes of Directive DI144-2007-05

An index of credit default swaps referencing 20 bonds collateralized by subprime mortgages.

ABX Asset-backed commercial paper (ABCP) Asset-backed security (ABS) Assets under management (AUM) Call (put) option Capital-to-risk-weighted assets ratio Carry trade Cash securitization CAT (catastrophe)

ABX Asset-backed commercial paper (ABCP) Asset-backed security (ABS) Assets under management (AUM) Call (put) option Capital-to-risk-weighted assets ratio Carry trade Cash securitization CAT (catastrophe)

For further information UBI Banca Investor Relations Tel.+ 39 0353922217 Email: investor.relations@ubibanca.it UBI Banca Press relations Tel.

- - - For further information UBI Banca Investor Relations Tel.+ 39 0353922217 Email: investor.relations@ubibanca.it UBI Banca Press relations Tel.+ 39 0302433591 +39 3358268310 Email: relesterne@ubibanca.it

- - - For further information UBI Banca Investor Relations Tel.+ 39 0353922217 Email: investor.relations@ubibanca.it UBI Banca Press relations Tel.+ 39 0302433591 +39 3358268310 Email: relesterne@ubibanca.it

Basel Committee on Banking Supervision. Capital requirements for banks equity investments in funds

Basel Committee on Banking Supervision Capital requirements for banks equity investments in funds December 2013 This publication is available on the BIS website (www.bis.org). Bank for International Settlements

Basel Committee on Banking Supervision Capital requirements for banks equity investments in funds December 2013 This publication is available on the BIS website (www.bis.org). Bank for International Settlements

More Transparency Needed For Bank Capital Relief Trades

OFFICE OF FINANCIAL RESEARCH BRIEF SERIES 15-4 June 11, 215 More Transparency Needed For Bank Capital Relief Trades By Jill Cetina, John McDonough, and Sriram Rajan1 Banks have significant incentives to

OFFICE OF FINANCIAL RESEARCH BRIEF SERIES 15-4 June 11, 215 More Transparency Needed For Bank Capital Relief Trades By Jill Cetina, John McDonough, and Sriram Rajan1 Banks have significant incentives to

Status of Capital Adequacy

Capital Adequacy Ratio Highlights 204 Status of Consolidated Capital Adequacy of Mizuho Financial Group, Inc. 206 Scope of Consolidation 206 Consolidated Capital Adequacy Ratio 208 Risk-Based Capital 210

Capital Adequacy Ratio Highlights 204 Status of Consolidated Capital Adequacy of Mizuho Financial Group, Inc. 206 Scope of Consolidation 206 Consolidated Capital Adequacy Ratio 208 Risk-Based Capital 210

ICAAP Report Q2 2015

ICAAP Report Q2 2015 Contents 1. INTRODUCTION... 3 1.1 THE THREE PILLARS FROM THE BASEL COMMITTEE... 3 1.2 BOARD OF MANAGEMENT APPROVAL OF THE ICAAP Q2 2015... 3 1.3 CAPITAL CALCULATION... 3 1.1.1 Use

ICAAP Report Q2 2015 Contents 1. INTRODUCTION... 3 1.1 THE THREE PILLARS FROM THE BASEL COMMITTEE... 3 1.2 BOARD OF MANAGEMENT APPROVAL OF THE ICAAP Q2 2015... 3 1.3 CAPITAL CALCULATION... 3 1.1.1 Use

Comments on the Basel Committee on Banking Supervision s Consultative Document: Supervisory framework for measuring and controlling large exposures

June 28, 2013 Comments on the Basel Committee on Banking Supervision s Consultative Document: Supervisory framework for measuring and controlling large exposures Japanese Bankers Association We, the Japanese

June 28, 2013 Comments on the Basel Committee on Banking Supervision s Consultative Document: Supervisory framework for measuring and controlling large exposures Japanese Bankers Association We, the Japanese

CITIGROUP INC. BASEL II.5 MARKET RISK DISCLOSURES AS OF AND FOR THE PERIOD ENDED MARCH 31, 2013

CITIGROUP INC. BASEL II.5 MARKET RISK DISCLOSURES AS OF AND FOR THE PERIOD ENDED MARCH 31, 2013 DATED AS OF MAY 15, 2013 Table of Contents Qualitative Disclosures Basis of Preparation and Review... 3 Risk

CITIGROUP INC. BASEL II.5 MARKET RISK DISCLOSURES AS OF AND FOR THE PERIOD ENDED MARCH 31, 2013 DATED AS OF MAY 15, 2013 Table of Contents Qualitative Disclosures Basis of Preparation and Review... 3 Risk

Mediterranean Guarantees

A newsletter on risk mitigation instruments for infrastructure investment in the Mediterranean Issue 2, October 2013 The Investment Security in the Mediterranean (ISMED) Support Programme seeks to increase

A newsletter on risk mitigation instruments for infrastructure investment in the Mediterranean Issue 2, October 2013 The Investment Security in the Mediterranean (ISMED) Support Programme seeks to increase

COMPUTERSHARE TRUST COMPANY OF CANADA BASEL III PILLAR 3 DISCLOSURES

COMPUTERSHARE TRUST COMPANY OF CANADA BASEL III PILLAR 3 DISCLOSURES December 31, 2013 Table of Contents Scope of Application... 3 Capital Structure... 3 Capital Adequacy... 3 Credit Risk... 4 Market Risk...

COMPUTERSHARE TRUST COMPANY OF CANADA BASEL III PILLAR 3 DISCLOSURES December 31, 2013 Table of Contents Scope of Application... 3 Capital Structure... 3 Capital Adequacy... 3 Credit Risk... 4 Market Risk...

Banking Regulation. Pros and Cons

Certificate in Social Banking Money and Society Banking Regulation Pros and Cons Professor Dr. Gregor Krämer Chair for Banking, Finance, and Accounting Alanus University of Arts and Social Sciences, Alfter,

Certificate in Social Banking Money and Society Banking Regulation Pros and Cons Professor Dr. Gregor Krämer Chair for Banking, Finance, and Accounting Alanus University of Arts and Social Sciences, Alfter,

TD Bank Financial Group Q1/08 Guide to Basel II

TD Bank Financial Group Q1/08 Guide to Basel II 1. OVERVIEW General Information on Basel can be found on the Canadian Bankers Association website at www.cba.ca. Choose Issues, Standards, Rules and Guidelines

TD Bank Financial Group Q1/08 Guide to Basel II 1. OVERVIEW General Information on Basel can be found on the Canadian Bankers Association website at www.cba.ca. Choose Issues, Standards, Rules and Guidelines

Date: June 4, 2012 To: Board of Governors From: Governor T arullo Initials Subject: Final Market Risk Capital Rule

B o a r d o f G o v e r n o r s o f t h e F e d e r a l R e s e r v e Sy s t e m Date: June 4, 2012 To: Board of Governors From: Governor T arullo Initials Subject: Final Market Risk Capital Rule Attached

B o a r d o f G o v e r n o r s o f t h e F e d e r a l R e s e r v e Sy s t e m Date: June 4, 2012 To: Board of Governors From: Governor T arullo Initials Subject: Final Market Risk Capital Rule Attached

Basel II. Questions and Answers FINANCIAL SERVICES

Basel II Questions and Answers FINANCIAL SERVICES Index Introduction 7 Basel II Accord 8 KPMG support regarding Basel II implementation 11 General questions on Basel II 13 1. What is the Bank for International

Basel II Questions and Answers FINANCIAL SERVICES Index Introduction 7 Basel II Accord 8 KPMG support regarding Basel II implementation 11 General questions on Basel II 13 1. What is the Bank for International

Bank of Queensland Limited

APRA 30 April 2012 The Basel II Capital Accord principles took effect in Australia on 1 January 2008. The framework for the application of Basel II in Australia is comprised of three pillars: Pillar 1:

APRA 30 April 2012 The Basel II Capital Accord principles took effect in Australia on 1 January 2008. The framework for the application of Basel II in Australia is comprised of three pillars: Pillar 1:

Basel 3: A new perspective on portfolio risk management. Tamar JOULIA-PARIS October 2011

Basel 3: A new perspective on portfolio risk management Tamar JOULIA-PARIS October 2011 1 Content 1. Basel 3 A complex regulatory framework With possible unintended consequences 2. Consequences on Main

Basel 3: A new perspective on portfolio risk management Tamar JOULIA-PARIS October 2011 1 Content 1. Basel 3 A complex regulatory framework With possible unintended consequences 2. Consequences on Main

Financial Stability Forum Recommends Actions to Enhance Market and Institutional Resilience

FINANCIAL STABILITY FORUM Press release Press enquiries: Washington +41 76 350 8430 Basel +41 76 350 8421 fsforum@bis.org Ref no: 7/2008E Financial Stability Forum Recommends Actions to Enhance Market

FINANCIAL STABILITY FORUM Press release Press enquiries: Washington +41 76 350 8430 Basel +41 76 350 8421 fsforum@bis.org Ref no: 7/2008E Financial Stability Forum Recommends Actions to Enhance Market

Capital Management Standard Banco Standard de Investimentos S/A

Capital Management Standard Banco Standard de Investimentos S/A Level: Entity Type: Capital Management Owner : Financial Director Approved by: Board of Directors and Brazilian Management Committee (Manco)

Capital Management Standard Banco Standard de Investimentos S/A Level: Entity Type: Capital Management Owner : Financial Director Approved by: Board of Directors and Brazilian Management Committee (Manco)

Arnout H. E. M. Wellink. President, De Nederlandsche Bank Chairman, Basel Committee on Banking Supervision

President, De Nederlandsche Bank Chairman, Basel Committee on Banking Supervision 118 27. Mai 2008 Banking Supervision in Europe: Developments and Challenges 1. The banking system has gone through major

President, De Nederlandsche Bank Chairman, Basel Committee on Banking Supervision 118 27. Mai 2008 Banking Supervision in Europe: Developments and Challenges 1. The banking system has gone through major

COMMERZBANK Capital Update - EU Wide Stress Test Results.

COMMERZBANK Capital Update - EU Wide Stress Test Results. COMMERZBANK was subject to the 2011 EU-wide stress test conducted by the European Banking Authority (EBA), in cooperation with the Bundesanstalt

COMMERZBANK Capital Update - EU Wide Stress Test Results. COMMERZBANK was subject to the 2011 EU-wide stress test conducted by the European Banking Authority (EBA), in cooperation with the Bundesanstalt

Conceptual Framework: What Does the Financial System Do? 1. Financial contracting: Get funds from savers to investors

Conceptual Framework: What Does the Financial System Do? 1. Financial contracting: Get funds from savers to investors Transactions costs Contracting costs (from asymmetric information) Adverse Selection

Conceptual Framework: What Does the Financial System Do? 1. Financial contracting: Get funds from savers to investors Transactions costs Contracting costs (from asymmetric information) Adverse Selection

The challenge of liquidity and collateral management in the new regulatory landscape

The challenge of liquidity and collateral management in the new regulatory landscape ICMA Professional Repo and Collateral Management Course 2012 Agenda 1. Background: The repo product under pressure 2.

The challenge of liquidity and collateral management in the new regulatory landscape ICMA Professional Repo and Collateral Management Course 2012 Agenda 1. Background: The repo product under pressure 2.

Key learning points I

Key learning points I What do banks do? Banks provide three core banking services Deposit collection Payment arrangement Underwrite loans Banks may also offer financial services such as cash, asset, and

Key learning points I What do banks do? Banks provide three core banking services Deposit collection Payment arrangement Underwrite loans Banks may also offer financial services such as cash, asset, and

Commercial Paper Conduritization Program

VII COMMERCIAL PAPER BACKED BY CREDIT CARD RECEIVABLES INTRODUCTION Asset-backed commercial paper (ABCP) conduits issue short-term notes backed by trade receivables, credit card receivables, or medium-term

VII COMMERCIAL PAPER BACKED BY CREDIT CARD RECEIVABLES INTRODUCTION Asset-backed commercial paper (ABCP) conduits issue short-term notes backed by trade receivables, credit card receivables, or medium-term

S t a n d a r d 4. 4 a. M a n a g e m e n t o f c r e d i t r i s k. Regulations and guidelines

S t a n d a r d 4. 4 a M a n a g e m e n t o f c r e d i t r i s k Regulations and guidelines THE FINANCIAL SUPERVISION AUTHORITY 4 Capital adequacy and risk management until further notice J. No. 1/120/2004

S t a n d a r d 4. 4 a M a n a g e m e n t o f c r e d i t r i s k Regulations and guidelines THE FINANCIAL SUPERVISION AUTHORITY 4 Capital adequacy and risk management until further notice J. No. 1/120/2004

Banco Sabadell Stress test results. 15 th July 2011

Banco Sabadell Stress test results 15 th July 2011 1 Disclaimer Banco Sabadell cautions that this presentation may contain forward looking statements with respect to the business. financial condition.

Banco Sabadell Stress test results 15 th July 2011 1 Disclaimer Banco Sabadell cautions that this presentation may contain forward looking statements with respect to the business. financial condition.

Bank Regulatory Capital Quick Reference. Very simply: to limit risk and reduce our potential, unexpected losses.

Bank Regulatory Capital: Why We Need It Very simply: to limit risk and reduce our potential, unexpected losses. Unlike normal companies, banks are in the business of issuing loans to individuals and businesses

Bank Regulatory Capital: Why We Need It Very simply: to limit risk and reduce our potential, unexpected losses. Unlike normal companies, banks are in the business of issuing loans to individuals and businesses

Checklist for Credit Risk Management

Checklist for Credit Risk Management I. Development and Establishment of Credit Risk Management System by Management Checkpoints - Credit risk is the risk that a financial institution will incur losses

Checklist for Credit Risk Management I. Development and Establishment of Credit Risk Management System by Management Checkpoints - Credit risk is the risk that a financial institution will incur losses

The Northern Trust Company, Canada Basel III Pillar lll Disclosure as at December 31, 2015

The Northern Trust Company, Canada Basel III Pillar lll Disclosure as at December 31, 2015 Subject to Board Approval Posting date: January 29, 2016 Contents NORTHERN TRUST OVERVIEW AND SCOPE OF APPPLICATION.

The Northern Trust Company, Canada Basel III Pillar lll Disclosure as at December 31, 2015 Subject to Board Approval Posting date: January 29, 2016 Contents NORTHERN TRUST OVERVIEW AND SCOPE OF APPPLICATION.

A Fundamental Review of Capital Charges Associated with Trading Activities

A Fundamental Review of Capital Charges Associated with Trading Activities Grahame Johnson Introduction Strengthening the capital that banks are required to hold to absorb losses from their trading and

A Fundamental Review of Capital Charges Associated with Trading Activities Grahame Johnson Introduction Strengthening the capital that banks are required to hold to absorb losses from their trading and

How To Understand The Concept Of Securitization

Asset Securitization 1 No securitization Mortgage borrowers Bank Investors 2 No securitization Consider a borrower that needs a bank loan to buy a house The bank lends the money in exchange of monthly

Asset Securitization 1 No securitization Mortgage borrowers Bank Investors 2 No securitization Consider a borrower that needs a bank loan to buy a house The bank lends the money in exchange of monthly

Prof Kevin Davis Melbourne Centre for Financial Studies. Managing Liquidity Risks. Session 5.1. Training Program ~ 8 12 December 2008 SHANGHAI, CHINA

Enhancing Risk Management and Governance in the Region s Banking System to Implement Basel II and to Meet Contemporary Risks and Challenges Arising from the Global Banking System Training Program ~ 8 12

Enhancing Risk Management and Governance in the Region s Banking System to Implement Basel II and to Meet Contemporary Risks and Challenges Arising from the Global Banking System Training Program ~ 8 12

Better capturing risks in the trading book

OLIVIER PRATO General Secretariat of the Commission bancaire General Surveillance of the Banking System Directorate International Affairs Division The 1996 Amendment to the Basel Capital Accord, which

OLIVIER PRATO General Secretariat of the Commission bancaire General Surveillance of the Banking System Directorate International Affairs Division The 1996 Amendment to the Basel Capital Accord, which

Risk Based Capital Guidelines; Market Risk. The Bank of New York Mellon Corporation Market Risk Disclosures. As of December 31, 2013

Risk Based Capital Guidelines; Market Risk The Bank of New York Mellon Corporation Market Risk Disclosures As of December 31, 2013 1 Basel II.5 Market Risk Annual Disclosure Introduction Since January

Risk Based Capital Guidelines; Market Risk The Bank of New York Mellon Corporation Market Risk Disclosures As of December 31, 2013 1 Basel II.5 Market Risk Annual Disclosure Introduction Since January

REMARKS ON THE BASEL CAPITAL FRAMEWORK AND TRADE FINANCE, 27 FEBRUARY 2014 SESSION 4. Mr. Andrew CORNFORD Research Fellow Financial Markets Center

REMARKS ON THE BASEL CAPITAL FRAMEWORK AND TRADE FINANCE, 27 FEBRUARY 2014 SESSION 4 Mr. Andrew CORNFORD Research Fellow Financial Markets Center 1 Webster2014.B3&TF Remarks on the Basel Capital Framework

REMARKS ON THE BASEL CAPITAL FRAMEWORK AND TRADE FINANCE, 27 FEBRUARY 2014 SESSION 4 Mr. Andrew CORNFORD Research Fellow Financial Markets Center 1 Webster2014.B3&TF Remarks on the Basel Capital Framework

Containing Systemic Risk: The Road to Reform. A. Introduction

SECTION II: STANDARDS FOR ACCOUNTING CONSOLIDATION A. Introduction It is widely recognized that a major contributing factor to the credit market crisis was the manner and extent to which risks associated

SECTION II: STANDARDS FOR ACCOUNTING CONSOLIDATION A. Introduction It is widely recognized that a major contributing factor to the credit market crisis was the manner and extent to which risks associated

Press release Press enquiries: +41 61 280 8188 press@bis.org www.bis.org

Press release Press enquiries: +41 61 280 8188 press@bis.org www.bis.org Ref no: 35/2010 12 September 2010 Group of Governors and Heads of Supervision announces higher global minimum capital standards

Press release Press enquiries: +41 61 280 8188 press@bis.org www.bis.org Ref no: 35/2010 12 September 2010 Group of Governors and Heads of Supervision announces higher global minimum capital standards

Equita SIM SpA publishes this Public Disclosure on its website www.equitasim.it

PUBLIC DISCLOSURE OF STATUS AS AT 31/12/2012 Introduction The Bank of Italy s Regulation concerning prudential supervision for securities brokerage companies [Italian legal entity acronym = SIM] (Title

PUBLIC DISCLOSURE OF STATUS AS AT 31/12/2012 Introduction The Bank of Italy s Regulation concerning prudential supervision for securities brokerage companies [Italian legal entity acronym = SIM] (Title

Nationwide Building Society Treasury Division One Threadneedle Street London UK EC2R 8AW. Tel: +44 1604 853008 andy.townsend@nationwide.co.

Nationwide Building Society Treasury Division One Threadneedle Street London UK EC2R 8AW Tel: +44 1604 853008 andy.townsend@nationwide.co.uk Uploaded via BCBS website 21 March 2014 Dear Sir or Madam BASEL

Nationwide Building Society Treasury Division One Threadneedle Street London UK EC2R 8AW Tel: +44 1604 853008 andy.townsend@nationwide.co.uk Uploaded via BCBS website 21 March 2014 Dear Sir or Madam BASEL

YEARENDED31DECEMBER2013 RISKMANAGEMENTDISCLOSURES

RISKMANAGEMENTDISCLOSURES 2015 YEARENDED31DECEMBER2013 ACCORDINGTOCHAPTER7(PAR.34-38)OFPARTCANDANNEXXIOFTHECYPRUSSECURITIES ANDEXCHANGECOMMISSIONDIRECTIVEDI144-2007-05FORTHECAPITALREQUIREMENTSOF INVESTMENTFIRMS

RISKMANAGEMENTDISCLOSURES 2015 YEARENDED31DECEMBER2013 ACCORDINGTOCHAPTER7(PAR.34-38)OFPARTCANDANNEXXIOFTHECYPRUSSECURITIES ANDEXCHANGECOMMISSIONDIRECTIVEDI144-2007-05FORTHECAPITALREQUIREMENTSOF INVESTMENTFIRMS

Basel Committee on Banking Supervision. Consultative Document. Standards. Capital floors: the design of a framework based on standardised approaches

Basel Committee on Banking Supervision Consultative Document Standards Capital floors: the design of a framework based on standardised approaches Issued for comment by 27 March 2015 December 2014 This

Basel Committee on Banking Supervision Consultative Document Standards Capital floors: the design of a framework based on standardised approaches Issued for comment by 27 March 2015 December 2014 This

Capital G Bank Limited. Interim Pillar 3 Disclosures 30th June, 2012

Capital G Bank Limited Interim Pillar 3 Disclosures 30th June, 2012 CONTENTS 1. CAUTIONARY STATEMENTS....1 2. INTRODUCTION...2 2.1 Background...2 2.2 Basis of Disclosure...3 2.3 Media and Location...3

Capital G Bank Limited Interim Pillar 3 Disclosures 30th June, 2012 CONTENTS 1. CAUTIONARY STATEMENTS....1 2. INTRODUCTION...2 2.1 Background...2 2.2 Basis of Disclosure...3 2.3 Media and Location...3

2014 EU-wide Stress Test

2014 EU-wide Stress Test Bank Name LEI Code DK - Sydbank GP5DT10VX1QRQUKVBK64 DK NUK_WL_NR_XX version 1809014 No restructuring 2014 EU-wide Stress Test 2014 EU-wide Stress Test Summary Adverse Scenario

2014 EU-wide Stress Test Bank Name LEI Code DK - Sydbank GP5DT10VX1QRQUKVBK64 DK NUK_WL_NR_XX version 1809014 No restructuring 2014 EU-wide Stress Test 2014 EU-wide Stress Test Summary Adverse Scenario

Fundamental Review of the Trading Book: A Revised Market Risk Framework Second Consultative Document by the Basel Committee on Banking Supervision

An Insight Paper by CRISIL GR&A ANALYSIS Fundamental Review of the Trading Book: A Revised Market Risk Framework Second Consultative Document by the Basel Committee on Banking Supervision The Basel Committee

An Insight Paper by CRISIL GR&A ANALYSIS Fundamental Review of the Trading Book: A Revised Market Risk Framework Second Consultative Document by the Basel Committee on Banking Supervision The Basel Committee

DECLARATION ON STRENGTHENING THE FINANCIAL SYSTEM LONDON SUMMIT, 2 APRIL 2009

DECLARATION ON STRENGTHENING THE FINANCIAL SYSTEM LONDON SUMMIT, 2 APRIL 2009 We, the Leaders of the G20, have taken, and will continue to take, action to strengthen regulation and supervision in line

DECLARATION ON STRENGTHENING THE FINANCIAL SYSTEM LONDON SUMMIT, 2 APRIL 2009 We, the Leaders of the G20, have taken, and will continue to take, action to strengthen regulation and supervision in line

Jupiter Asset Management Ltd Pillar 3 Disclosures as at 31 December 2014

Jupiter Asset Management Ltd Pillar 3 Disclosures CONTENTS Overview 2 Risk management framework 3 Own funds 7 Capital requirements 8 Credit risk 9 Interest rate risk in non-trading book 11 Non-trading

Jupiter Asset Management Ltd Pillar 3 Disclosures CONTENTS Overview 2 Risk management framework 3 Own funds 7 Capital requirements 8 Credit risk 9 Interest rate risk in non-trading book 11 Non-trading

Capital Market Services UK Limited Pillar 3 Disclosure

February 2013 Capital Market Services UK Limited Pillar 3 Disclosure Contents 1.0 Overview 2.0 Frequency and location of disclosure 3.0 Verification 4.0 Scope of application 5.1 Risk Management objectives

February 2013 Capital Market Services UK Limited Pillar 3 Disclosure Contents 1.0 Overview 2.0 Frequency and location of disclosure 3.0 Verification 4.0 Scope of application 5.1 Risk Management objectives

Disclosure 17 OffV (Credit Risk Mitigation Techniques)

") Disclosure 17 OffV (Credit Risk Mitigation Techniques) The Austrian Financial Market Authority (FMA) and the Oesterreichsiche Nationalbank (OeNB) have assessed UniCredit Bank Austria AG for the use of

Disclosure 17 OffV (Credit Risk Mitigation Techniques) The Austrian Financial Market Authority (FMA) and the Oesterreichsiche Nationalbank (OeNB) have assessed UniCredit Bank Austria AG for the use of

RISK MANAGEMENT REPORT (for the Financial Year Ended 31 March 2012)

") RISK MANAGEMENT REPORT (for the Financial Year Ended 31 March 2012) Integrated Risk Management Framework The Group s Integrated Risk Management Framework (IRMF) sets the fundamental elements to manage

RISK MANAGEMENT REPORT (for the Financial Year Ended 31 March 2012) Integrated Risk Management Framework The Group s Integrated Risk Management Framework (IRMF) sets the fundamental elements to manage

CREDIT RISK MANAGEMENT

GLOBAL ASSOCIATION OF RISK PROFESSIONALS The GARP Risk Series CREDIT RISK MANAGEMENT Chapter 1 Credit Risk Assessment Chapter Focus Distinguishing credit risk from market risk Credit policy and credit

GLOBAL ASSOCIATION OF RISK PROFESSIONALS The GARP Risk Series CREDIT RISK MANAGEMENT Chapter 1 Credit Risk Assessment Chapter Focus Distinguishing credit risk from market risk Credit policy and credit

China International Capital Corporation (UK) Limited Pillar 3 Disclosure

Limited Pillar 3 Disclosure") 1. Overview Pillar 3 Disclosure March 2014 China International Capital Corporation (UK) Limited Pillar 3 Disclosure The European Union s Capital Requirements Directive ( CRD ) came into effect on 1 January

1. Overview Pillar 3 Disclosure March 2014 China International Capital Corporation (UK) Limited Pillar 3 Disclosure The European Union s Capital Requirements Directive ( CRD ) came into effect on 1 January

Basel Committee on Banking Supervision. Basel III definition of capital - Frequently asked questions

Basel Committee on Banking Supervision Basel III definition of capital - Frequently asked questions July 2011 Copies of publications are available from: Bank for International Settlements Communications

Basel Committee on Banking Supervision Basel III definition of capital - Frequently asked questions July 2011 Copies of publications are available from: Bank for International Settlements Communications

Standard Chartered Bank (Thai) PCL & its Financial Business Group Pillar 3 Disclosures 30 June 2015

PCL & its Financial Business Group Pillar 3 Disclosures 30 June 2015") Standard Chartered Bank (Thai) PCL & its Financial Business Group Registered Office: 90 North Sathorn Road, Silom Bangkok, 10500, Thailand Overview During 2013, the Bank of Thailand ( BOT ) published the

Standard Chartered Bank (Thai) PCL & its Financial Business Group Registered Office: 90 North Sathorn Road, Silom Bangkok, 10500, Thailand Overview During 2013, the Bank of Thailand ( BOT ) published the

HOCH CAPITAL LTD PILLAR 3 DISCLOSURES As at 1 February 2015

HOCH CAPITAL LTD PILLAR 3 DISCLOSURES As at 1 February 2015 TABLE OF CONTENTS 1. Overview / Background 1.1 Introduction 1.2 Frequency of disclosure 1.3 Location and verification of disclosure 1.4 Scope

HOCH CAPITAL LTD PILLAR 3 DISCLOSURES As at 1 February 2015 TABLE OF CONTENTS 1. Overview / Background 1.1 Introduction 1.2 Frequency of disclosure 1.3 Location and verification of disclosure 1.4 Scope

Capital Adequacy: Asset Risk Charge

Prudential Standard LPS 114 Capital Adequacy: Asset Risk Charge Objective and key requirements of this Prudential Standard This Prudential Standard requires a life company to maintain adequate capital

Prudential Standard LPS 114 Capital Adequacy: Asset Risk Charge Objective and key requirements of this Prudential Standard This Prudential Standard requires a life company to maintain adequate capital

EXTRACT FROM. Common shares issued by the bank For an instrument to be included in CET1 capital it must meet all of the criteria that follow.

EXTRACT FROM BASEL III: A GLOBAL REGULATORY FRAMEWORK FOR MORE RESILIENT BANKS AND BANKING SYSTEMS DEFINITIONS OF COMMON EQUITY TIER 1, ADDITIONAL TIER I AND TIER II CAPITAL I. Common Equity Tier 1 (CET1)

EXTRACT FROM BASEL III: A GLOBAL REGULATORY FRAMEWORK FOR MORE RESILIENT BANKS AND BANKING SYSTEMS DEFINITIONS OF COMMON EQUITY TIER 1, ADDITIONAL TIER I AND TIER II CAPITAL I. Common Equity Tier 1 (CET1)

Risk Management Programme Guidelines

Risk Management Programme Guidelines Submissions are invited on these draft Reserve Bank risk management programme guidelines for non-bank deposit takers. Submissions should be made by 29 June 2009 and

Risk Management Programme Guidelines Submissions are invited on these draft Reserve Bank risk management programme guidelines for non-bank deposit takers. Submissions should be made by 29 June 2009 and

Year end results. Basel II Pillar 3 Disclosures 2010

Year end results Basel II Pillar 3 Disclosures 2010 Notes about this report Overview of Basel II and Pillar 3 Barclays has applied the Basel II framework since 2008. The Basel accord is made up of three

Year end results Basel II Pillar 3 Disclosures 2010 Notes about this report Overview of Basel II and Pillar 3 Barclays has applied the Basel II framework since 2008. The Basel accord is made up of three

The Goldman Sachs Group, Inc. and Goldman Sachs Bank USA. 2015 Annual Dodd-Frank Act Stress Test Disclosure

The Goldman Sachs Group, Inc. and Goldman Sachs Bank USA 2015 Annual Dodd-Frank Act Stress Test Disclosure March 2015 2015 Annual Dodd-Frank Act Stress Test Disclosure for The Goldman Sachs Group, Inc.

The Goldman Sachs Group, Inc. and Goldman Sachs Bank USA 2015 Annual Dodd-Frank Act Stress Test Disclosure March 2015 2015 Annual Dodd-Frank Act Stress Test Disclosure for The Goldman Sachs Group, Inc.

Recognised Investment Exchanges. Chapter 2. Recognition requirements

Recognised Investment Exchanges Chapter Recognition REC : Recognition Section.3 : Financial resources.3 Financial resources.3.1 UK Schedule to the Recognition Requirements Regulations, Paragraph 1 (1)

Recognised Investment Exchanges Chapter Recognition REC : Recognition Section.3 : Financial resources.3 Financial resources.3.1 UK Schedule to the Recognition Requirements Regulations, Paragraph 1 (1)

POLICY POSITION PAPER ON THE PRUDENTIAL TREATMENT OF CAPITALISED EXPENSES

POLICY POSITION PAPER ON THE PRUDENTIAL TREATMENT OF CAPITALISED EXPENSES RESULTS OF A SURVEY OF AUTHORISED DEPOSIT-TAKING INSTITIONS, UNDERTAKEN BY THE AUSTRALIAN PRUDENTIAL REGULATION AUTHORITY June

POLICY POSITION PAPER ON THE PRUDENTIAL TREATMENT OF CAPITALISED EXPENSES RESULTS OF A SURVEY OF AUTHORISED DEPOSIT-TAKING INSTITIONS, UNDERTAKEN BY THE AUSTRALIAN PRUDENTIAL REGULATION AUTHORITY June

2016 Comprehensive Capital Analysis and Review

BMO Financial Corp. and BMO Harris Bank N.A. 206 Comprehensive Capital Analysis and Review Dodd-Frank Act Company-Run Stress Test Supervisory Severely Adverse Scenario Results Disclosure June 23, 206 Overview

BMO Financial Corp. and BMO Harris Bank N.A. 206 Comprehensive Capital Analysis and Review Dodd-Frank Act Company-Run Stress Test Supervisory Severely Adverse Scenario Results Disclosure June 23, 206 Overview

Risk Management Structure

Commitment to Risk Management Basic Approach Progress in financial deregulation and internationalization has led to growth in the diversity and complexity of banking operations, exposing financial institutions

Commitment to Risk Management Basic Approach Progress in financial deregulation and internationalization has led to growth in the diversity and complexity of banking operations, exposing financial institutions

Credit Risk Management: Trends and Opportunities

Risk & Compliance the way we see it Credit Risk Management: Trends and Opportunities The Current State of Credit Risk Management 1 Overview The crisis exposed the shortcomings of existing risk management

Risk & Compliance the way we see it Credit Risk Management: Trends and Opportunities The Current State of Credit Risk Management 1 Overview The crisis exposed the shortcomings of existing risk management

Strengthening the banking union and the regulatory treatment of banks sovereign exposures Informal ECOFIN, April 22, 2016 Presidency note

Strengthening the banking union and the regulatory treatment of banks sovereign exposures Informal ECOFIN, April 22, 2016 Presidency note Introduction One of the key priorities of the Dutch Presidency

Strengthening the banking union and the regulatory treatment of banks sovereign exposures Informal ECOFIN, April 22, 2016 Presidency note Introduction One of the key priorities of the Dutch Presidency

Division 9 Specific requirements for certain portfolios of exposures

L. S. NO. 2 TO GAZETTE NO. 43/2006 L.N. 228 of 2006 B3157 Division 9 Specific requirements for certain portfolios of exposures 197. Purchased receivables An authorized institution shall classify its purchased

L. S. NO. 2 TO GAZETTE NO. 43/2006 L.N. 228 of 2006 B3157 Division 9 Specific requirements for certain portfolios of exposures 197. Purchased receivables An authorized institution shall classify its purchased

79 8.1. Capital requirement under Pillar I 81 8.2. ICAAP 81 8.2.1. Capital requirement under Pillar II 82 8.2.2. Internal assessment of capital

8. Capital management 79 8.1. Capital requirement under Pillar I 81 8.2. ICAAP 81 8.2.1. Capital requirement under Pillar II 82 8.2.2. Internal assessment of capital needed on the basis of economic capital

8. Capital management 79 8.1. Capital requirement under Pillar I 81 8.2. ICAAP 81 8.2.1. Capital requirement under Pillar II 82 8.2.2. Internal assessment of capital needed on the basis of economic capital

Interview with Gabriel Bernardino, Chairman of EIOPA, conducted by Anke Dembowski, Institutional Money (Germany)

") 1 Interview with Gabriel Bernardino, Chairman of EIOPA, conducted by Anke Dembowski, Institutional Money (Germany) 1. Insurance companies vs. Occupational Retirement Provision (IORPs) EIOPA has submitted

1 Interview with Gabriel Bernardino, Chairman of EIOPA, conducted by Anke Dembowski, Institutional Money (Germany) 1. Insurance companies vs. Occupational Retirement Provision (IORPs) EIOPA has submitted

FINANCIAL STABILITY FORUM. Report of the Financial Stability Forum on Enhancing Market and Institutional Resilience

Report of the Financial Stability Forum on Enhancing Market and Institutional Resilience 7 April 2008 Report of the Financial Stability Forum on Enhancing Market and Institutional Resilience Table of

Report of the Financial Stability Forum on Enhancing Market and Institutional Resilience 7 April 2008 Report of the Financial Stability Forum on Enhancing Market and Institutional Resilience Table of

Richard Rosen Federal Reserve Bank of Chicago

Richard Rosen Federal Reserve Bank of Chicago The views expressed here are my own and may not represent those of the Federal Reserve Bank of Chicago or the Federal Reserve System. Why was this crisis different

Richard Rosen Federal Reserve Bank of Chicago The views expressed here are my own and may not represent those of the Federal Reserve Bank of Chicago or the Federal Reserve System. Why was this crisis different

Glossary & Definitions

Glossary & Definitions SEB Glossary & Definitions December 2014 Asset quality... 3 Credit loss level... 3 Gross level of impaired loans... 3 Net level of impaired loans... 3 Specific reserve ratio for

Glossary & Definitions SEB Glossary & Definitions December 2014 Asset quality... 3 Credit loss level... 3 Gross level of impaired loans... 3 Net level of impaired loans... 3 Specific reserve ratio for

Citigroup Inc. Basel II.5 Market Risk Disclosures As of and For the Period Ended March 31, 2014

Citigroup Inc. Basel II.5 Market Risk Disclosures and For the Period Ended TABLE OF CONTENTS OVERVIEW 3 Organization 3 Capital Adequacy 3 Basel II.5 Covered Positions 3 Valuation and Accounting Policies

Citigroup Inc. Basel II.5 Market Risk Disclosures and For the Period Ended TABLE OF CONTENTS OVERVIEW 3 Organization 3 Capital Adequacy 3 Basel II.5 Covered Positions 3 Valuation and Accounting Policies

Chart I.1. Difference between Primary Surplus (PS) and Bond Yield Spreads in Selected EU 1 Countries

and Bond Yield Spreads in Selected EU 1 Countries") LIST OF CHARTS Chart I.1. Difference between Primary Surplus (PS) and Bond Yield Spreads in Selected EU 1 Countries Chart I.2. Gross Debt Stock and Budget Deficits of Selected Countries as of 2010 1 Chart

LIST OF CHARTS Chart I.1. Difference between Primary Surplus (PS) and Bond Yield Spreads in Selected EU 1 Countries Chart I.2. Gross Debt Stock and Budget Deficits of Selected Countries as of 2010 1 Chart

The Western Hemisphere Credit & Loan Reporting Initiative (WHCRI)

") The Western Hemisphere Credit & Loan Reporting Initiative (WHCRI) Public Credit Registries as a Tool for Bank Regulation and Supervision Matías Gutierrez Girault & Jane Hwang III Evaluation Workshop Mexico

The Western Hemisphere Credit & Loan Reporting Initiative (WHCRI) Public Credit Registries as a Tool for Bank Regulation and Supervision Matías Gutierrez Girault & Jane Hwang III Evaluation Workshop Mexico

INCREASING GLOBAL FINANCIAL INTEGRITY: THE ROLES OF MARKET DISCIPLINE, REGULATION, AND SUPERVISION

INCREASING GLOBAL FINANCIAL INTEGRITY: THE ROLES OF MARKET DISCIPLINE, REGULATION, AND SUPERVISION Laurence H. Meyer Recent developments, both at home and abroad, have reinforced the importance of efforts

INCREASING GLOBAL FINANCIAL INTEGRITY: THE ROLES OF MARKET DISCIPLINE, REGULATION, AND SUPERVISION Laurence H. Meyer Recent developments, both at home and abroad, have reinforced the importance of efforts

Portfolio Management for Banks

Enterprise Risk Solutions Portfolio Management for Banks RiskFrontier, our industry-leading economic capital and credit portfolio risk management solution, along with our expert Portfolio Advisory Services

Enterprise Risk Solutions Portfolio Management for Banks RiskFrontier, our industry-leading economic capital and credit portfolio risk management solution, along with our expert Portfolio Advisory Services