Maryland Insurance Administration Report on the Effect of Competitive Rating on the Insurance Markets in Maryland

|

|

|

- Philip Stanley

- 8 years ago

- Views:

Transcription

1 Maryland Insurance Administration 2009 Report on the Effect of Competitive Rating on the Insurance Markets in Maryland January, 2010

2 Maryland Insurance Administration 2009 Report on the Effect of Competitive Rating on the Insurance Markets in Maryland Table of Contents I. Preface 1 II. Competitive Rating 1 III. Evaluating the Competitive Market 2 IV. Private Passenger Automobile Insurance 2 V. Homeowner's Insurance 5 VI. Conclusions 7 VII. Exhibits 8

3 I. Preface Each year, the Insurance Commissioner is required to report to the Governor and the General Assembly on the effect of competitive rating on the insurance markets in the State. (See of the Insurance Article.) This report summarizes Maryland s competitive rating law and provides information on the competitiveness of the market in two of the most important insurance markets for consumers, private passenger automobile insurance and homeowners insurance for calendar year II. Competitive Rating The Insurance Reform Act of 1995 (HB 923, Competitive Rating) authorized insurers to use rates for certain lines of property and casualty insurance without the prior approval of the Commissioner. Each authorized insurer and each rating organization designated by an insurer for the filing of rates must file with the Commissioner all rates and supplementary rate information as well as any changes to rates or supplementary rate information on or before the date they become effective. (See of the Insurance Article.) In accordance with ratemaking principles, rates may not be excessive, inadequate, or unfairly discriminatory. Under competitive rating, the Commissioner may only find a rate to be excessive if it is unreasonably high for the insurance provided and the Commissioner has issued a ruling that a reasonable degree of competition does not exist in the market to which the rate is applicable. (See of the Insurance Article.) States moved from prior approval of rates to competitive rating to allow insurers to react quickly to business cycles. When claims experience is favorable, it is anticipated that insurers 1

4 will generally act to decrease rates and/or relax underwriting restrictions to increase their market share. When claims experience deteriorates, it is anticipated that insurers will generally act to increase rates and/or tighten their underwriting standards to accept less risk. Proponents of competitive rating maintain that competition between insurers prevents excessive rating even during a downturn in the business cycle because no insurer is willing to raise rates to the point where it will lose significant market share to one or more of its competitors. Moreover, competition encourages insurers to accept more risks, making insurance widely available to consumers. III. Evaluating the Competitive Market In determining the competitiveness of a market, the Commissioner must consider all relevant factors including: The number of insurers providing coverage in the market; The concentration of market share of those insurers; Changes in market share of the insurers; and Ease of entry for new insurers/products. (See of the Insurance Article.) The subsequent sections of this report examine the number of insurers providing coverage and the market share for these insurers in two insurance lines, private passenger automobile insurance and homeowners insurance, for calendar year IV. Private Passenger Automobile Insurance During calendar year 2008, there were 148 companies actively providing private passenger automobile insurance and related products in the State of Maryland. Many of these 2

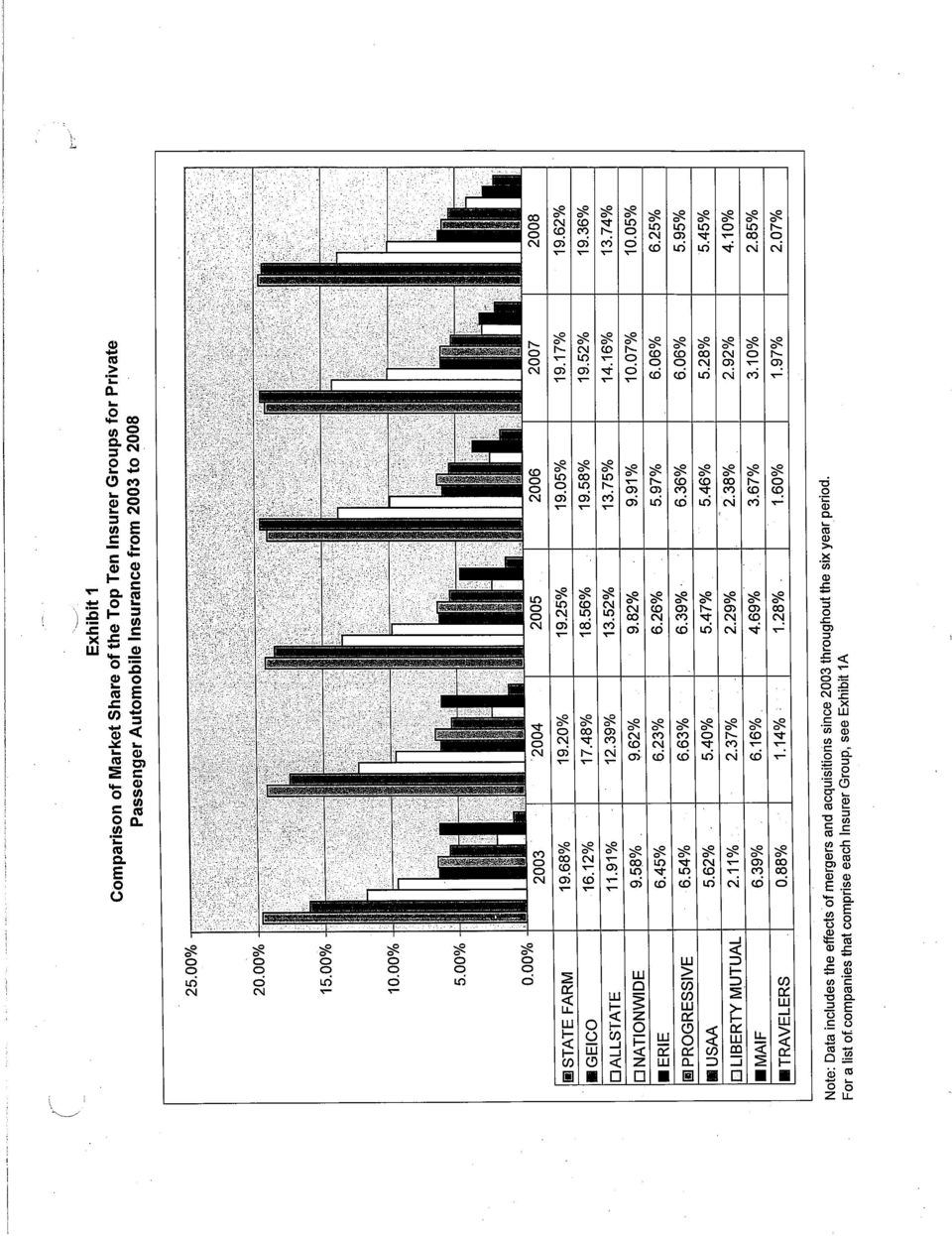

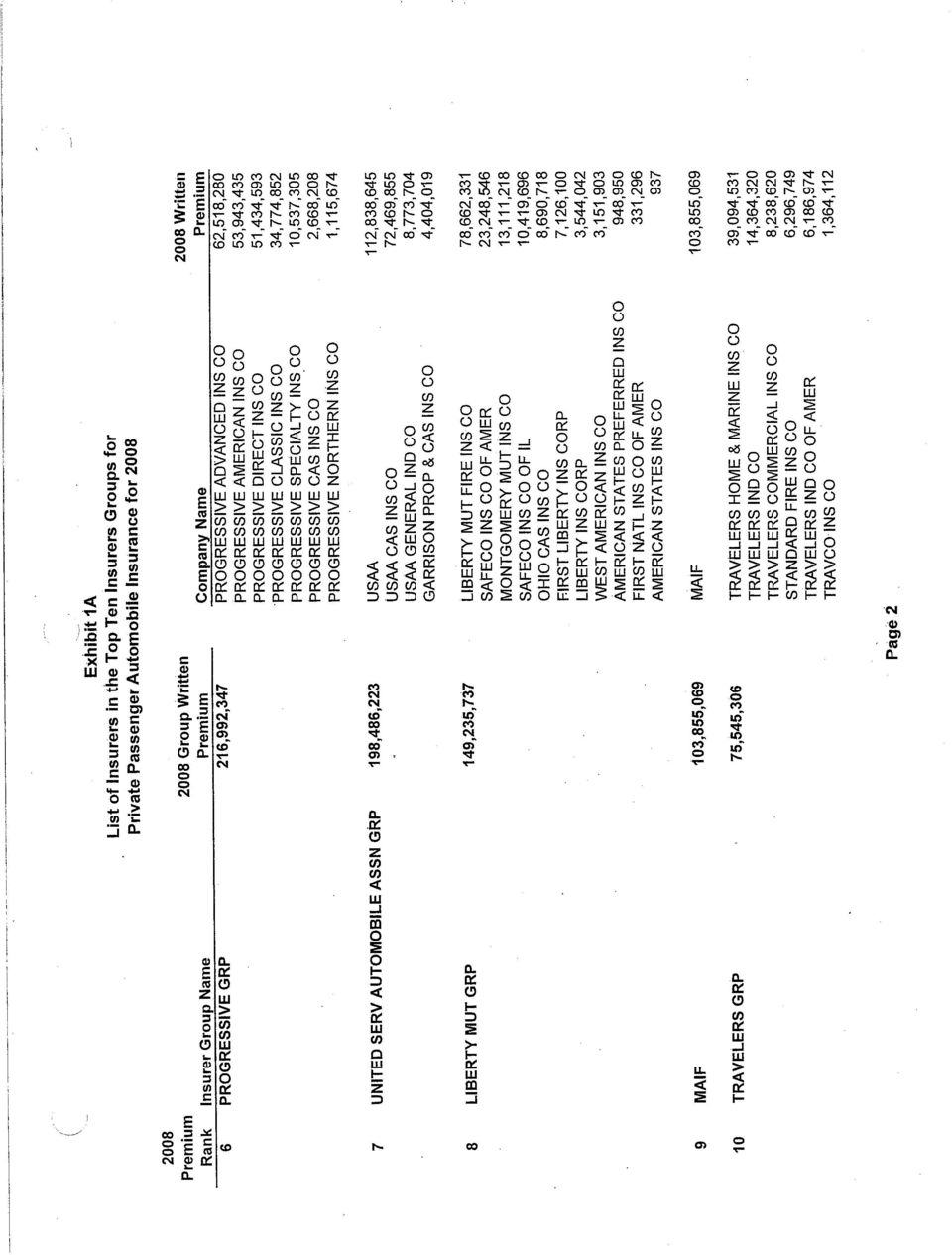

5 companies are owned by the same holding company (hereinafter insurer group ). 1 Exhibit 1A identifies the top ten insurer groups, the individual companies comprising each insurer group and the 2008 written premium for the insurer group as well as each individual company. Of the 148 companies writing private passenger automobile insurance, 55 are a part of the top ten insurer groups. The market share for the top ten insurer groups has remained relatively stable between 2003 and (See Exhibit 1.) In 2003, these top ten insurer groups accounted for about 85 percent of the private passenger automobile insurance market increasing to just over 89 percent by Over this six year period, the market share for GEICO, Allstate, Liberty Mutual and Travelers has increased and the market share for State Farm, Nationwide, Erie, Progressive, and USAA has fluctuated somewhat, but have basically remained stable, while Maryland Automobile Insurance Fund s (MAIF) market share has decreased significantly. A commonly accepted measure of market concentration is the Herfindahl-Hirschman Index (HHI). 3 Markets in which HHI is between 1000 and 1800 points are considered to be moderately concentrated and those in which the HHI is in excess of 1800 points are considered to be concentrated. Using the market share for each of the top ten insurers for Maryland 2008, the HHI for Maryland is 1183 up from 1044 for 2003, suggesting a minimally concentrated market. 4 1 Insurer groups are being used in this report as opposed to individual companies as this provides a consistent comparison of data over the years due to individual company mergers and acquisitions. 2 According to the National Association of Insurance Commissioners, the top ten insurer groups accounted for 66.6 percent of the direct premiums written countrywide in 2008 for private passenger automobile insurance. 3 This is calculated by squaring the market share of each firm competing in the market and then summing the resulting numbers. The HHI takes into account the relative size and distribution of the firms in a market and approaches zero when a market consists of a large number of firms of relatively equal size. The HHI increases both as the number of firms in the market decreases and as the disparity in size between those firms increases. 4 Using market share for the top ten insurer groups for 2008 from the National Association of Insurance Commissioners, the HHI for the nation as a whole is 642, an indication of a competitive national market. 3

6 In the private passenger automobile insurance market, individuals with risk characteristics that private passenger auto insurers are unwilling to accept are able to obtain coverage from MAIF. In 2003, MAIF had 6.39 percent of the private passenger auto insurance market. This decreased by about 55 percent in 2008 to 2.85 percent. Over this six year period, private passenger auto insurers appear to have competed for greater market share by accepting more risk, a sign of a competitive market. In a competitive market, rates are responsive to changing conditions. Table 1 below shows the average premium expenditure representing the average premium paid per vehicle -- for automobile liability and physical damage (comprehensive and collision combined) for years 2003 through During this time period, coverage expenditures have been rather stable with the exception of an increase in the rate of growth for 2004, which may be attributable to a major winter storm in Year Table 1: Maryland Statewide Average Automobile Premium Expenditures: Auto Liability Expenditure % Change Year Auto Physical Damage Expenditure % % % Change % % % % % % % % % % 5 Combined coverage expenditure information is not available. 4

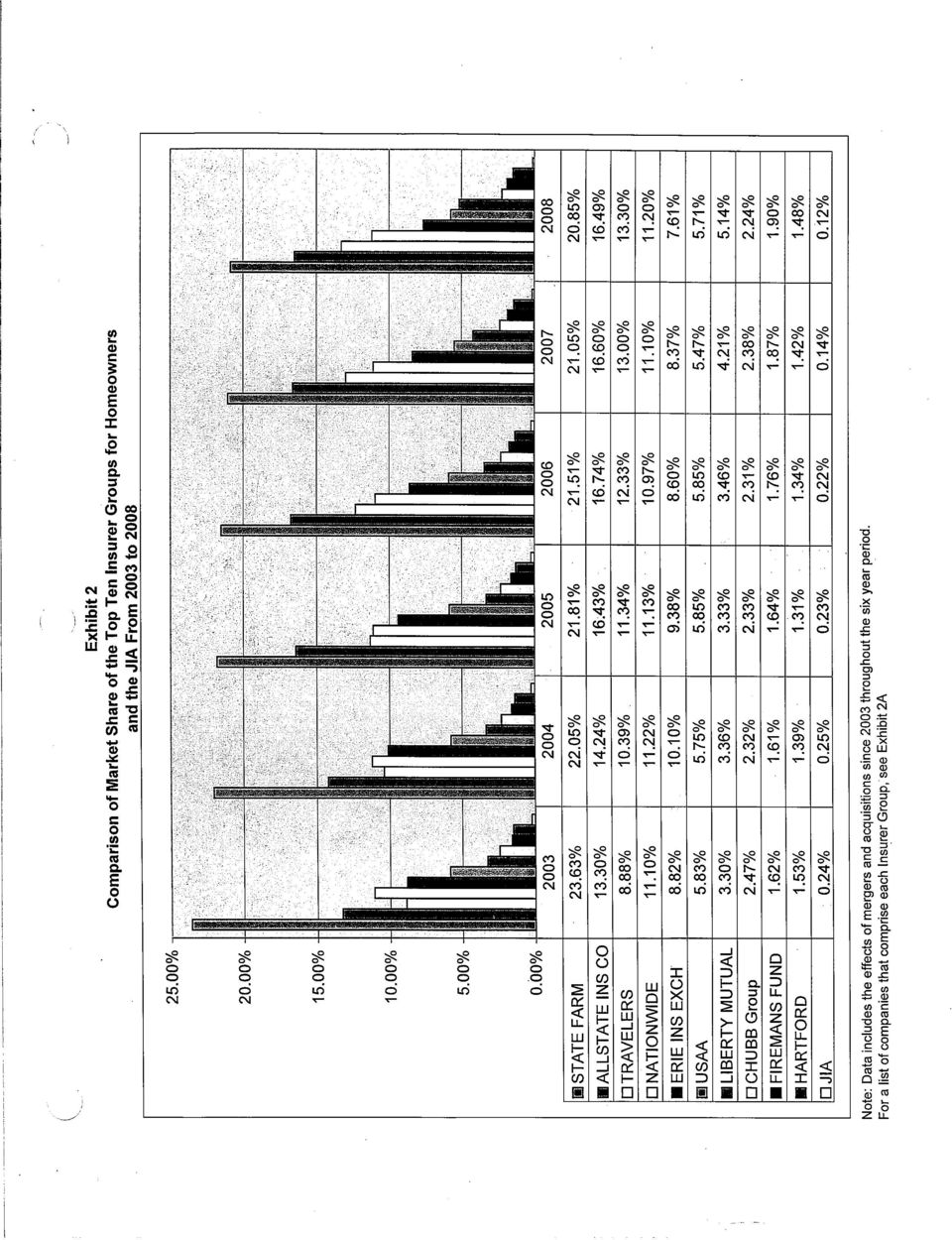

7 Maryland s private passenger automobile insurance market appears to be moderately concentrated. The drop in MAIF s market share combined with premium changes responsive to market conditions provides evidence that this minimally concentrated market remains competitive. The Maryland Insurance Administration will continue to monitor the market to look for any signs of a concentrated market. V. Homeowner s Insurance During calendar year 2008, there were 117 companies actively providing homeowners insurance in Maryland. 6 Of the 117 actively writing homeowners insurance, 44 are a part of the top ten insurer groups. Exhibit 2A identifies the top ten insurer groups, the individual companies comprising each insurer group and the 2008 written premium for the insurer group as well as each individual company. The market share for the top ten insurer groups increased between 2003 and In 2003, these top ten insurer groups accounted for about 80 percent of the homeowner s insurance market increasing to about 86 percent by Over this six year period, the market share for Allstate, Travelers, Liberty Mutual, and Fireman s Fund increased and the market share for Nationwide, Erie, USAA, Chubb, and Zurich has fluctuated somewhat, but have basically remained stable, while State Farm and the Joint Insurance Association s ( JIA s ) market share decreased. Using the market share for each of the top ten insurers for Maryland 2008, the HHI for Maryland is 1137 up from 1065 for 2003, suggesting a minimally concentrated market. Another measure of competition is the percentage of business held by the Joint Insurance Association ( JIA ), the State s residual property insurer. In 2003, JIA had about 0.24 percent of the homeowner s insurance market. This decreased by about 50 percent by 2008 to about

8 percent. Over this six year period, homeowner s insurers appear to have competed for greater market share by accepting more risk. A potential sign of a concentrated homeowner s insurance market is the unwillingness of some insurers to write business in certain portions of the State, notably the Eastern Shore and Southern Maryland. During the 2007 Legislative Session, a Task Force to study the availability and affordability of property insurance in coastal areas was created. The Task Force held three meetings during the month of October and received testimony from producers, insurers, builders, catastrophe modelers, financial rating organizations and others to investigate the availability and affordability of property insurance in the coastal areas of the State and to learn of possible reasons for the decreasing competition as well as receive suggestions on the best way to maintain the affordability and availability of property insurance products for consumers in Maryland s coastal areas. As a direct result of those meetings and the subsequent report issued by the Task Force, the legislature enacted the Omnibus Coastal Property Reform Act (HB 1353). It is anticipated that this legislation will be of great benefit to Maryland consumers in the future; however, it is still too soon to assess its impact at this point in time. Unfortunately, it is no longer possible for the MIA to determine the extent to which average homeowner s insurance premiums change over time in response to market conditions. The amendments adopted in 1999 to through of the Insurance Article abrogated on June 30, This abrogated amendment was the authority the MIA relied upon to collect the homeowners data used to calculate the average premium that was then placed in this report. 6

9 The homeowner s insurance market appears to be moderately concentrated and may be concentrated in certain geographic areas. The Maryland Insurance Administration will continue to monitor the market to determine if it becomes concentrated. VI. Conclusions When healthy competition exists in the private passenger automobile insurance and homeowner s insurance markets, Maryland insurance consumers have a variety of choices with respect to insurers, products and pricing. The MIA, in evaluating the competitiveness of the marketplace, takes into consideration the number of insurers in the marketplace, the concentration of the market shares of those insurers, and the changes in market share that occur over time. The market share information for 2008 suggests Maryland s private passenger auto insurance and homeowner s insurance markets are minimally concentrated. For private passenger auto insurance, the declining market share for MAIF and premium changes responsive to the market suggest this moderately concentrated market is competitive. For homeowner s insurance, the small market share for the residual market is an indication of a competitive market. However, the unwillingness of some insurers to write homeowner s insurance in certain portions of the state may be a sign that this market could become concentrated. The MIA will continue to monitor both markets for changes in market concentration, competitiveness and availability. 7

10 VII. Exhibits Exhibit 1: Comparison of Market Share of the Top Ten Insurer Groups for Private Passenger Automobile Insurance from 2003 to 2008 Exhibit 1A: List of Insurers in the Top Ten Insurer Groups for Private Passenger Automobile Insurance for 2008 Exhibit 2: Comparison of Market Share of the Top Ten Insurer Groups for Homeowners and the JIA from 2003 to 2008 Exhibit 2A: List of Insurers in the Top Ten Insurer Groups for Homeowners Insurance for

11

12

13

14

15

16

INSURANCE, ADMINISTRATION. 2013 Report on the Effect of Competitive Rating on the Insurance Markets in Maryland

INSURANCE, ADMINISTRATION 2013 Report on the Effect of Competitive Rating on the Insurance Markets in Maryland. October 15, 2013 Maryland Insurance Administration 2013 Report on the Effect of Competitive

INSURANCE, ADMINISTRATION 2013 Report on the Effect of Competitive Rating on the Insurance Markets in Maryland. October 15, 2013 Maryland Insurance Administration 2013 Report on the Effect of Competitive

Massachusetts Insurance Federation Two Center Plaza 8 th Floor Boston, MA 02108

Massachusetts Insurance Federation Two Center Plaza 8 th Floor Boston, MA 02108 (617) 557-5538 STATEMENT OF THE MASSACHUSETTS INSURANCE FEDERATION TO THE DIVISION OF INSURANCE IN CONNECTION WITH ITS INFORMATIONAL

Massachusetts Insurance Federation Two Center Plaza 8 th Floor Boston, MA 02108 (617) 557-5538 STATEMENT OF THE MASSACHUSETTS INSURANCE FEDERATION TO THE DIVISION OF INSURANCE IN CONNECTION WITH ITS INFORMATIONAL

The Maryland Automobile Insurance Fund and the Private Insurance Market

The Maryland Automobile Insurance Fund and the Private Insurance Market January 2004 Section I Topics discussed in this section: Who created MAIF and why was it created? Was MAIF created to compete with

The Maryland Automobile Insurance Fund and the Private Insurance Market January 2004 Section I Topics discussed in this section: Who created MAIF and why was it created? Was MAIF created to compete with

Complaint Ratio Index Report of Maryland's Top 20 Auto Insurers for 1998

1 Complaint Ratio Index Report of Maryland's Top 20 Auto Insurers for 1998 A resource for consumers provided by the Maryland Insurance Administration 525 St. Paul Place Baltimore, MD 21202 1-800-492-6116

1 Complaint Ratio Index Report of Maryland's Top 20 Auto Insurers for 1998 A resource for consumers provided by the Maryland Insurance Administration 525 St. Paul Place Baltimore, MD 21202 1-800-492-6116

State of Maryland OFFICE OF THE ATTORNEY ANNUAL REPORT OF THE PEOPLE'S INSURANCE COUNSEL DIVISION. Fiscal Year 2013

State of Maryland OFFICE OF THE ATTORNEY GENERAL ANNUAL REPORT OF THE PEOPLE'S INSURANCE COUNSEL DIVISION Fiscal Year 2013 Submitted to the Governor and General Assembly I. INTRODUCTION The People's Insurance

State of Maryland OFFICE OF THE ATTORNEY GENERAL ANNUAL REPORT OF THE PEOPLE'S INSURANCE COUNSEL DIVISION Fiscal Year 2013 Submitted to the Governor and General Assembly I. INTRODUCTION The People's Insurance

Credit-based Insurance Score Homeowners Insurance P044804. Comments of the Center for Economic Justice on

on Model Section 6(b) Order for Data from Insurance Companies for Use in FACT Act Section 215 Study of Insurance Scoring June 18, 2008 The Center for Economic Justice (CEJ) supports the Commissioners resolution

on Model Section 6(b) Order for Data from Insurance Companies for Use in FACT Act Section 215 Study of Insurance Scoring June 18, 2008 The Center for Economic Justice (CEJ) supports the Commissioners resolution

ANNUAL STUDY OF MEDICAL MALPRACTICE INSURANCE MARKET IN ARKANSAS

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE INSURANCE

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE INSURANCE

Auto Insurance Sample Premium Tables 2014/15

Auto Insurance Sample Premium Tables 2014/15 Prepared by Commonwealth of State Corporation Commission Bureau of Insurance P.O. Box 1157 Richmond, 23218 (804) 371-9185 (877) 310-6560 Website: www.scc.virginia.gov/boi

Auto Insurance Sample Premium Tables 2014/15 Prepared by Commonwealth of State Corporation Commission Bureau of Insurance P.O. Box 1157 Richmond, 23218 (804) 371-9185 (877) 310-6560 Website: www.scc.virginia.gov/boi

Consumer policies such as homeowners and auto insurance. Business policies such as business interruption insurance.

The information in the report cards is as of October 18, 2013. It covers the insurers who make up the majority of the insurance market in areas affected by Storm Sandy, including: Consumer policies such

The information in the report cards is as of October 18, 2013. It covers the insurers who make up the majority of the insurance market in areas affected by Storm Sandy, including: Consumer policies such

Uninsured and Underinsured Motorist Coverage in Ohio Report Required by Senate Bill 97 Prepared as of October 31, 2003

Report Required by Senate Bill 97 Prepared as of October 31, 2003 Executive Summary The following report summarizes the recent history of uninsured and underinsured motorist ( UM/UIM ) coverage in Ohio,

Report Required by Senate Bill 97 Prepared as of October 31, 2003 Executive Summary The following report summarizes the recent history of uninsured and underinsured motorist ( UM/UIM ) coverage in Ohio,

Maryland Insurance Administration s 2005 Report on the Availability and Affordability of Health Care Medical Professional Liability Insurance in

Maryland Insurance Administration s 2005 Report on the Availability and Affordability of Health Care Medical Professional Liability Insurance in Maryland November, 2005 Maryland Insurance Administration's

Maryland Insurance Administration s 2005 Report on the Availability and Affordability of Health Care Medical Professional Liability Insurance in Maryland November, 2005 Maryland Insurance Administration's

Maryland Insurance Administration s 2006 Report on the Availability and Affordability of Health Care Medical Professional Liability Insurance in

Maryland Insurance Administration s 2006 Report on the Availability and Affordability of Health Care Professional Liability Insurance in Maryland September 5, 2006 Maryland Insurance Administration's 2006

Maryland Insurance Administration s 2006 Report on the Availability and Affordability of Health Care Professional Liability Insurance in Maryland September 5, 2006 Maryland Insurance Administration's 2006

2014 Report on Availability and Affordability of Health Care Medical Professional Liability Insurance in Maryland

2014 Report on Availability and Affordability of Health Care Medical Professional Liability Insurance in Maryland July 2014 MSAR 2976 Table of Contents Executive Summary...1 Introduction...2 Medical Malpractice

2014 Report on Availability and Affordability of Health Care Medical Professional Liability Insurance in Maryland July 2014 MSAR 2976 Table of Contents Executive Summary...1 Introduction...2 Medical Malpractice

My name is Steven Lehmann. I am a Principal with Pinnacle Actuarial Resources, Inc., an actuarial consulting

Insurer Use of Education and Occupation Data National Conference of Insurance Legislators Special Property-Casualty Insurance Meeting February 28, 2009 My name is Steven Lehmann. I am a Principal with

Insurer Use of Education and Occupation Data National Conference of Insurance Legislators Special Property-Casualty Insurance Meeting February 28, 2009 My name is Steven Lehmann. I am a Principal with

62nd Legislature AN ACT ALLOWING SPECIAL RISK CLASSIFICATIONS FOR PRIVATE PASSENGER AND COMMERCIAL

62nd Legislature SB0352 AN ACT ALLOWING SPECIAL RISK CLASSIFICATIONS FOR PRIVATE PASSENGER AND COMMERCIAL AUTOMOBILE POLICIES TO BE BASED ON FAVORABLE AND ADVERSE INFORMATION CONTAINED IN AN EXPERIENCE

62nd Legislature SB0352 AN ACT ALLOWING SPECIAL RISK CLASSIFICATIONS FOR PRIVATE PASSENGER AND COMMERCIAL AUTOMOBILE POLICIES TO BE BASED ON FAVORABLE AND ADVERSE INFORMATION CONTAINED IN AN EXPERIENCE

The Competitiveness and Premium Excessiveness of the Home and Auto Insurance Industries in the State of Michigan

JENNIFER M. GRANHOLM GOVERNOR STATE OF MICHIGAN OFFICE OF FINANCIAL AND INSURANCE SERVICES DEPARTMENT OF LABOR & ECONOMIC GROWTH DAVID C. HOLLISTER, DIRECTOR LINDA A. WATTERS COMMISSIONER The and Premium

JENNIFER M. GRANHOLM GOVERNOR STATE OF MICHIGAN OFFICE OF FINANCIAL AND INSURANCE SERVICES DEPARTMENT OF LABOR & ECONOMIC GROWTH DAVID C. HOLLISTER, DIRECTOR LINDA A. WATTERS COMMISSIONER The and Premium

ANNUAL STUDY OF MEDICAL MALPRACTICE INSURANCE MARKET IN ARKANSAS

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE

ANNUAL STUDY OF MEDICAL MALPRACTICE INSURANCE MARKET IN ARKANSAS

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE

USE AND IMPACT OF CREDIT IN PERSONAL LINES INSURANCE PREMIUMS PURSUANT TO ARK. CODE ANN. 23-67-415

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1452 OF 2003) USE AND IMPACT OF CREDIT IN PERSONAL

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1452 OF 2003) USE AND IMPACT OF CREDIT IN PERSONAL

Fact Checker. A Check of the Facts in the Michigan Automobile and Home Insurance Consumer Advocate Report to the Governor, 2009

Fact Checker A Check of the Facts in the Michigan Automobile and Home Insurance Consumer Advocate Report to the Governor, 2009 Published by the Insurance Institute of Michigan 334 Townsend, Lansing, MI

Fact Checker A Check of the Facts in the Michigan Automobile and Home Insurance Consumer Advocate Report to the Governor, 2009 Published by the Insurance Institute of Michigan 334 Townsend, Lansing, MI

Don t Make Main Street Insurance Consumers Subsidize Wall Street

Don t Make Main Street Insurance Consumers Subsidize Wall Street To address the economic turmoil caused by the collapse of several major Wall Street firms, Congress now faces the difficult charge of crafting

Don t Make Main Street Insurance Consumers Subsidize Wall Street To address the economic turmoil caused by the collapse of several major Wall Street firms, Congress now faces the difficult charge of crafting

ANNUAL STUDY OF MEDICAL MALPRACTICE INSURANCE MARKET IN ARKANSAS

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE

The Use of Education and Occupation as Underwriting Factors in Determining Policyholder Premiums for Private Passenger Auto Insurance

The Use of Education and Occupation as Underwriting Factors in Determining Policyholder Premiums for Private Passenger Auto Insurance Written Testimony of Robert P. Hartwig, Ph.D., CPCU President & Chief

The Use of Education and Occupation as Underwriting Factors in Determining Policyholder Premiums for Private Passenger Auto Insurance Written Testimony of Robert P. Hartwig, Ph.D., CPCU President & Chief

Private Passenger Automobile Tort Reform Rate Reductions: Fact versus Fiction

Private Passenger Automobile Tort Reform Rate Reductions: Fact versus Fiction 1. Executive Summary Insurers Reap Windfall Auto Insurance Profits As Insurance Department Fails to Meet Legislative Intent

Private Passenger Automobile Tort Reform Rate Reductions: Fact versus Fiction 1. Executive Summary Insurers Reap Windfall Auto Insurance Profits As Insurance Department Fails to Meet Legislative Intent

2011 Report on the Availability and Affordability of Health Care Medical Professional Liability Insurance in Maryland

2011 Report on the Availability and Affordability of Health Care Medical Professional Liability Insurance in Maryland August 2011 Table of Contents Executive Summary.1 Introduction..2 Malpractice Insurance

2011 Report on the Availability and Affordability of Health Care Medical Professional Liability Insurance in Maryland August 2011 Table of Contents Executive Summary.1 Introduction..2 Malpractice Insurance

HOUSE OF REPRESENTATIVES STAFF ANALYSIS REFERENCE ACTION ANALYST STAFF DIRECTOR SUMMARY ANALYSIS

HOUSE OF REPRESENTATIVES STAFF ANALYSIS BILL #: CS/HB 1267 Property Insurance SPONSOR(S): Jobs & Entrepreneurship Council; Robaina and others TIED BILLS: IDEN./SIM. BILLS: SB 2498 REFERENCE ACTION ANALYST

HOUSE OF REPRESENTATIVES STAFF ANALYSIS BILL #: CS/HB 1267 Property Insurance SPONSOR(S): Jobs & Entrepreneurship Council; Robaina and others TIED BILLS: IDEN./SIM. BILLS: SB 2498 REFERENCE ACTION ANALYST

Arkansas Insurance Department

Arkansas Insurance Department Mike Beebe Governor Jay Bradford Commissioner August 15, 2011 Via E-Mail and Messenger Mr. David Ferguson Director Bureau of Legislative Research State Capitol, Room 315 Little

Arkansas Insurance Department Mike Beebe Governor Jay Bradford Commissioner August 15, 2011 Via E-Mail and Messenger Mr. David Ferguson Director Bureau of Legislative Research State Capitol, Room 315 Little

2003 Complaint Statistics of Insurance Companies Showing 10 or More Complaints for Coverage Type - Private Passenger Automobile

for Coverage Type - Private Passenger Automobile AFFIRMATIVE INSURANCE COMPANY 223 83,921,675 20 1 202 0 ALLSTATE INSURANCE COMPANY 226 415,822,885 25 2 190 9 ALLSTATE PROPERTY AND CASUALTY INSURANCE COMPANY

for Coverage Type - Private Passenger Automobile AFFIRMATIVE INSURANCE COMPANY 223 83,921,675 20 1 202 0 ALLSTATE INSURANCE COMPANY 226 415,822,885 25 2 190 9 ALLSTATE PROPERTY AND CASUALTY INSURANCE COMPANY

2013 Annual Private Passenger Automobile & Homeowners Insurance Comparison Tables

State of Utah Insurance Department Todd E. Kiser Commissioner 2013 As required by law, the Utah Insurance Department has prepared this guide to auto and homeowners insurance. This annual guide provides

State of Utah Insurance Department Todd E. Kiser Commissioner 2013 As required by law, the Utah Insurance Department has prepared this guide to auto and homeowners insurance. This annual guide provides

Automobile Insurance: The Road Ahead

Automobile Insurance: The Road Ahead An Executive Summary of the Attorney General on the Status of Insurance Deregulation Commonwealth of Massachusetts Office of Attorney General Martha Coakley December

Automobile Insurance: The Road Ahead An Executive Summary of the Attorney General on the Status of Insurance Deregulation Commonwealth of Massachusetts Office of Attorney General Martha Coakley December

Texas Private Passenger Automobile Insurance Profitability, 1990 to 1998. A Report by the Center for Economic Justice. April 1999

Texas Private Passenger Automobile Insurance Profitability, 1990 to 1998 This report reviews the loss ratio experience of Texas private passenger automobile insurers from 1990 through 1998 and with particular

Texas Private Passenger Automobile Insurance Profitability, 1990 to 1998 This report reviews the loss ratio experience of Texas private passenger automobile insurers from 1990 through 1998 and with particular

Homeowners Insurance in the States

Testimony to the Senate Business and Commerce Committee Senator John J. Carona, Chair Texas Legislature Tuesday, July 10, 2012 Heather Morton National Conference of State Legislatures Denver, Colorado

Testimony to the Senate Business and Commerce Committee Senator John J. Carona, Chair Texas Legislature Tuesday, July 10, 2012 Heather Morton National Conference of State Legislatures Denver, Colorado

Residual Markets. Residual Markets in which insurers participate to make coverage available to those unable to obtain coverage in Standard Market

Residual Markets David C. Marlett, PhD, CPCU Chair, Department of Finance, Banking and Insurance Appalachian State University marlettdc@appstate.edu 828.262.2849 http://insurance.appstate.edu/ Residual

Residual Markets David C. Marlett, PhD, CPCU Chair, Department of Finance, Banking and Insurance Appalachian State University marlettdc@appstate.edu 828.262.2849 http://insurance.appstate.edu/ Residual

Supplemental Handout TNC Insurance Compromise Model Bill Updated March 26

Supplemental Handout TNC Insurance Compromise Model Bill Updated March 26 2015 National Association of Insurance Commissioners SUGGESTED KEY MESSAGES FOR TNC INSURANCE COMPROMISE MODEL BILL SUPPORTERS:

Supplemental Handout TNC Insurance Compromise Model Bill Updated March 26 2015 National Association of Insurance Commissioners SUGGESTED KEY MESSAGES FOR TNC INSURANCE COMPROMISE MODEL BILL SUPPORTERS:

AGENCY: Federal Insurance Office, Departmental Offices, Treasury.

This document is scheduled to be published in the Federal Register on 07/02/2015 and available online at http://federalregister.gov/a/2015-16333, and on FDsys.gov Billing Code 4810-25-P DEPARTMENT OF THE

This document is scheduled to be published in the Federal Register on 07/02/2015 and available online at http://federalregister.gov/a/2015-16333, and on FDsys.gov Billing Code 4810-25-P DEPARTMENT OF THE

NEWS RELEASE. Total pages: 5 plus attachment. Thursday, April 3, 2014 Andy Morrison (646) 408-3735

408-3735") NEWS RELEASE Total pages: 5 plus attachment For immediate release: For more information: Thursday, April 3, 2014 Andy Morrison (646) 408-3735 Top NY Auto Insurers Charge Higher Rates to HS Grads and Blue

NEWS RELEASE Total pages: 5 plus attachment For immediate release: For more information: Thursday, April 3, 2014 Andy Morrison (646) 408-3735 Top NY Auto Insurers Charge Higher Rates to HS Grads and Blue

2012 Annual Private Passenger Automobile & Homeowners Insurance Comparison Tables

State of Utah Insurance Department Neal T. Gooch Commissioner 2012 As required by law, the Utah Insurance Department has prepared this guide to auto and homeowners insurance. This annual guide provides

State of Utah Insurance Department Neal T. Gooch Commissioner 2012 As required by law, the Utah Insurance Department has prepared this guide to auto and homeowners insurance. This annual guide provides

A) FLEX RATING A FAILURE

FLEX RATING A FAILURE") STATEMENT OF J. ROBERT HUNTER, DIRECTOR OF INSURANCE BEFORE THE ASSEMBLY STANDING COMMITTEE ON INSURANCE REGARDING THE AUTOMOBILE INSURANCE MARKET IN NEW YORK STATE ALBANY, NEW YORK APRIL 10, 2014 Mr.

STATEMENT OF J. ROBERT HUNTER, DIRECTOR OF INSURANCE BEFORE THE ASSEMBLY STANDING COMMITTEE ON INSURANCE REGARDING THE AUTOMOBILE INSURANCE MARKET IN NEW YORK STATE ALBANY, NEW YORK APRIL 10, 2014 Mr.

VERMONT DEPARTMENT OF BANKING, INSURANCE, SECURITIES, AND HEALTH CARE ADMINISTRATION

VERMONT DEPARTMENT OF BANKING, INSURANCE, SECURITIES, AND HEALTH CARE ADMINISTRATION TECHNIQUES TO STABILIZE VERMONT WORKERS COMPENSATION PREMIUM COSTS AND MINIMIZE THE IMPACT OF LARGE CLAIMS Prepared

VERMONT DEPARTMENT OF BANKING, INSURANCE, SECURITIES, AND HEALTH CARE ADMINISTRATION TECHNIQUES TO STABILIZE VERMONT WORKERS COMPENSATION PREMIUM COSTS AND MINIMIZE THE IMPACT OF LARGE CLAIMS Prepared

MAJOR AUTO INSURERS CHARGE HIGHER RATES TO HIGH SCHOOL GRADUATES AND BLUE COLLAR WORKERS

Immediate Release: Contact: July 22, 2013 Peter Kitchen (202) 737-0766 Tom Feltner (202) 618-0310 MAJOR AUTO INSURERS CHARGE HIGHER RATES TO HIGH SCHOOL GRADUATES AND BLUE COLLAR WORKERS National Consumer

Immediate Release: Contact: July 22, 2013 Peter Kitchen (202) 737-0766 Tom Feltner (202) 618-0310 MAJOR AUTO INSURERS CHARGE HIGHER RATES TO HIGH SCHOOL GRADUATES AND BLUE COLLAR WORKERS National Consumer

The Use of Credit Scores by Auto Insurers: Adverse Impacts on Low- and Moderate-Income Drivers

The Use of Credit Scores by Auto Insurers: Adverse Impacts on Low- and Moderate-Income Drivers December 2013 Stephen Brobeck Executive Director J. Robert Hunter Director of Insurance Tom Feltner Director

The Use of Credit Scores by Auto Insurers: Adverse Impacts on Low- and Moderate-Income Drivers December 2013 Stephen Brobeck Executive Director J. Robert Hunter Director of Insurance Tom Feltner Director

Measuring Crash Avoidance System Effectiveness with Insurance Data

www.iihs.org Measuring Crash Avoidance System Effectiveness with Insurance Data 2013 Government/Industry Meeting Washington, DC January 30, 2013 Matthew Moore, Vice President, HLDI The Insurance Institute

www.iihs.org Measuring Crash Avoidance System Effectiveness with Insurance Data 2013 Government/Industry Meeting Washington, DC January 30, 2013 Matthew Moore, Vice President, HLDI The Insurance Institute

ANNUAL STUDY OF MEDICAL MALPRACTICE INSURANCE MARKET IN ARKANSAS

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE

Bulletin 15-04. Date: January 23, 2015. All P&C Insurance Companies, The Maryland Automobile Insurance Fund and The Joint Insurance Association

LAWRENCE J. HOGAN, JR. Governor BOYD K. RUTHERFORD Lt. Governor AL REDMER, JR. Commissioner NANCY GRODIN Deputy Commissioner JOY HATCHETTE Associate Commissioner Consumer Education and Advocacy Date: January

LAWRENCE J. HOGAN, JR. Governor BOYD K. RUTHERFORD Lt. Governor AL REDMER, JR. Commissioner NANCY GRODIN Deputy Commissioner JOY HATCHETTE Associate Commissioner Consumer Education and Advocacy Date: January

2012 Minnesota Homeowners Report

2012 Minnesota Homeowners Report Minnesota Department of Commerce 2012 Homeowners Insurance Report Page 1 2012 Minnesota Homeowners Report The Minnesota Homeowners Report is completed annually by the Minnesota

2012 Minnesota Homeowners Report Minnesota Department of Commerce 2012 Homeowners Insurance Report Page 1 2012 Minnesota Homeowners Report The Minnesota Homeowners Report is completed annually by the Minnesota

REFERENCE ACTION ANALYST STAFF DIRECTOR or BUDGET/POLICY CHIEF SUMMARY ANALYSIS

HOUSE OF REPRESENTATIVES STAFF ANALYSIS BILL #: CS/HB 929 Peril of Flood SPONSOR(S): Insurance & Banking; Ahern TIED BILLS: IDEN./SIM. BILLS: CS/SB 584 REFERENCE ACTION ANALYST STAFF DIRECTOR or BUDGET/POLICY

HOUSE OF REPRESENTATIVES STAFF ANALYSIS BILL #: CS/HB 929 Peril of Flood SPONSOR(S): Insurance & Banking; Ahern TIED BILLS: IDEN./SIM. BILLS: CS/SB 584 REFERENCE ACTION ANALYST STAFF DIRECTOR or BUDGET/POLICY

Good morning Mr. Chairman and distinguished members of the Committee. My name is

STATEMENT OF JOHN MARCHIONI VICE CHAIRMAN, COALITION FOR AUTO INSURNCE COMPETITION TO THE U.S. HOUSE COMMITTEE ON FINANCIAL SERVICES SUBCOMMITTEE ON CAPITAL MARKETS APRIL 10, 2003 Good morning Mr. Chairman

STATEMENT OF JOHN MARCHIONI VICE CHAIRMAN, COALITION FOR AUTO INSURNCE COMPETITION TO THE U.S. HOUSE COMMITTEE ON FINANCIAL SERVICES SUBCOMMITTEE ON CAPITAL MARKETS APRIL 10, 2003 Good morning Mr. Chairman

Department of Legislative Services Maryland General Assembly 2011 Session

House Bill 959 Economic Matters Department of Legislative Services Maryland General Assembly 2011 Session FISCAL AND POLICY NOTE Revised (Delegate Davis) Insurance - Surplus Lines HB 959 Finance This bill

House Bill 959 Economic Matters Department of Legislative Services Maryland General Assembly 2011 Session FISCAL AND POLICY NOTE Revised (Delegate Davis) Insurance - Surplus Lines HB 959 Finance This bill

Companies Filing on Property/Casualty Blank Homeowners multiple peril Business in Mississippi for Year Ended 12/31/2008

Companies Filing on Property/Casualty Blank Homeowners multiple peril Business in Mississippi for Year Ended 12/31/28 Premiums Market Losses Premiums Losses Paid Earned State Farm Fire and Casualty Company

Companies Filing on Property/Casualty Blank Homeowners multiple peril Business in Mississippi for Year Ended 12/31/28 Premiums Market Losses Premiums Losses Paid Earned State Farm Fire and Casualty Company

2008 Annual Ranking of Automobile Insurance Complaints

New York State Insurance Department 2008 Annual Ranking of Automobile Insurance Complaints David A. Paterson Governor Eric R. Dinallo Superintendent This Annual Ranking of Automobile Insurance Complaints

New York State Insurance Department 2008 Annual Ranking of Automobile Insurance Complaints David A. Paterson Governor Eric R. Dinallo Superintendent This Annual Ranking of Automobile Insurance Complaints

CONFERENCE COMMITTEE REPORT BRIEF HOUSE BILL NO. 2446

SESSION OF 2016 CONFERENCE COMMITTEE REPORT BRIEF HOUSE BILL NO. 2446 As Agreed to March 24, 2016 Brief* HB 2446 would amend the Kansas Automobile Injury Reparations Act to increase the minimum motor vehicle

SESSION OF 2016 CONFERENCE COMMITTEE REPORT BRIEF HOUSE BILL NO. 2446 As Agreed to March 24, 2016 Brief* HB 2446 would amend the Kansas Automobile Injury Reparations Act to increase the minimum motor vehicle

Texas Department of Insurance Use of Credit Information Private Passenger Auto

The companies listed below indicated the use of credit information for the purpose of underwriting and/or rating private passenger auto insurance. The underwriting process is used to determine whether

The companies listed below indicated the use of credit information for the purpose of underwriting and/or rating private passenger auto insurance. The underwriting process is used to determine whether

Ohio Medical Malpractice Commission. Statement of James Hurley, ACAS, MAAA Chairperson, Medical Malpractice Subcommittee American Academy of Actuaries

Ohio Medical Malpractice Commission Statement of James Hurley, ACAS, MAAA Chairperson, Medical Malpractice Subcommittee American Academy of Actuaries June 11, 2003 The American Academy of Actuaries is

Ohio Medical Malpractice Commission Statement of James Hurley, ACAS, MAAA Chairperson, Medical Malpractice Subcommittee American Academy of Actuaries June 11, 2003 The American Academy of Actuaries is

How To Support Independent Insurance Agents Of Texas

what is IIAT? The Independent Insurance Agents of Texas (IIAT) is the nation s largest state association of independent insurance agencies, representing nearly 1,800 agencies employing 15,000 agents and

what is IIAT? The Independent Insurance Agents of Texas (IIAT) is the nation s largest state association of independent insurance agencies, representing nearly 1,800 agencies employing 15,000 agents and

U.S. Homeowners Market

U.S. Homeowners Market Casualty Actuarial Society Spring Meeting Kelleen Arquette, FCAS, MAAA May 2013 2013 Towers Watson. All rights reserved. AGENDA Agenda Market Overview Market Definition Direct Written

U.S. Homeowners Market Casualty Actuarial Society Spring Meeting Kelleen Arquette, FCAS, MAAA May 2013 2013 Towers Watson. All rights reserved. AGENDA Agenda Market Overview Market Definition Direct Written

Louisiana Department of Insurance. State. Insurance. 10 years post-katrina. James J. Donelon, Commissioner

Louisiana Department of Insurance State Of Insurance 10 years post-katrina James J. Donelon, Commissioner Message from Insurance Commissioner Jim Donelon It s hard to imagine and it s not something we

Louisiana Department of Insurance State Of Insurance 10 years post-katrina James J. Donelon, Commissioner Message from Insurance Commissioner Jim Donelon It s hard to imagine and it s not something we

Low-Income Drivers and the Need for Affordable Auto Insurance 1

Low-Income Drivers and the Need for Affordable Auto Insurance 1 Summary of the Issue The automobile insurance Maryland law requires is often out of reach for low-income individuals. Auto insurance providers

Low-Income Drivers and the Need for Affordable Auto Insurance 1 Summary of the Issue The automobile insurance Maryland law requires is often out of reach for low-income individuals. Auto insurance providers

Percent change. Rank Most expensive states Average expenditure Rank Least expensive states Average expenditure

Page 1 of 7 Auto Insurance AAA s 2010 Your Driving Costs study found that the average cost to own and operate a sedan rose by 4.8 percent to $8,487 per year, compared with the previous year. Rising fuel,

Page 1 of 7 Auto Insurance AAA s 2010 Your Driving Costs study found that the average cost to own and operate a sedan rose by 4.8 percent to $8,487 per year, compared with the previous year. Rising fuel,

2014 Alabama Insurance Market Analysis Ted A. Kinney, CIC CPCU ARM AU AAM AAI AINS CPIA CRIS AIIA Director of Education and Technical Affairs

2014 Alabama Insurance Market Analysis Ted A. Kinney, CIC CPCU ARM AU AAM AAI AINS CPIA CRIS AIIA Director of Education and Technical Affairs The 2014 Edition of the Property/Casualty State/Line Report

2014 Alabama Insurance Market Analysis Ted A. Kinney, CIC CPCU ARM AU AAM AAI AINS CPIA CRIS AIIA Director of Education and Technical Affairs The 2014 Edition of the Property/Casualty State/Line Report

States offer Insurance Assistance for Hurricane Evacuees

FOR IMMEDIATE RELEASE George Dale, Commissioner of Insurance/State Fire Marshal Mississippi Insurance Department Jackson, Mississippi Friday, September 2, 2005 For additional information, please contact

FOR IMMEDIATE RELEASE George Dale, Commissioner of Insurance/State Fire Marshal Mississippi Insurance Department Jackson, Mississippi Friday, September 2, 2005 For additional information, please contact

J.D. Power Reports: Gen Y Least Satisfied among Generational Segments with Homeowners and Renters Insurance

J.D. Power Reports: Gen Y Least Satisfied among Generational Segments with Homeowners and Renters Insurance Amica Mutual Ranks Highest in Homeowners Insurance Customer Satisfaction; GEICO Ranks Highest

J.D. Power Reports: Gen Y Least Satisfied among Generational Segments with Homeowners and Renters Insurance Amica Mutual Ranks Highest in Homeowners Insurance Customer Satisfaction; GEICO Ranks Highest

How To Get A Home Insurance Policy On The Gulf Coast

INSURANCE IN MISSISSIPPI 10 YEARS AFTER KATRINA Mike Chaney, Commissioner A publication of the Mississippi Insurance Department August 2015 Message from Commissioner of Insurance Mike Chaney One of the

INSURANCE IN MISSISSIPPI 10 YEARS AFTER KATRINA Mike Chaney, Commissioner A publication of the Mississippi Insurance Department August 2015 Message from Commissioner of Insurance Mike Chaney One of the

Presentation to the LRC Automobile Insurance Modernization Committee

Presentation to the LRC Automobile Insurance Modernization Committee Rose Vaughn Williams December 6, 2011 In North Carolina, as in all states but a few, anyone who wants to drive on our roads is required

Presentation to the LRC Automobile Insurance Modernization Committee Rose Vaughn Williams December 6, 2011 In North Carolina, as in all states but a few, anyone who wants to drive on our roads is required

Price Optimization and Regulation Las Vegas Ratemaking & Product Management Seminar March 2009

Price Optimization and Regulation Las Vegas Ratemaking & Product Management Seminar March 2009 Arthur J. Schwartz, MAAA, FCAS Associate P&C Actuary North Carolina Department of Insurance Raleigh, NC What

Price Optimization and Regulation Las Vegas Ratemaking & Product Management Seminar March 2009 Arthur J. Schwartz, MAAA, FCAS Associate P&C Actuary North Carolina Department of Insurance Raleigh, NC What

GG.00 Injured Workers Insurance Fund. ($ in Thousands) CY 2000 CY 2001 CY 2002 % Change Actual Budget Budget Change Prior Year

CY 2000 CY 2001 CY 2002 % Change Actual Budget Budget Change Prior Year") GG.00 Injured Workers Insurance Fund Operating Budget Data ($ in Thousands) CY 2000 CY 2001 CY 2002 % Change Actual Budget Budget Change Prior Year Nonbudgeted Fund $28,674 $38,281 $36,546 ($1,735) -4.53%

GG.00 Injured Workers Insurance Fund Operating Budget Data ($ in Thousands) CY 2000 CY 2001 CY 2002 % Change Actual Budget Budget Change Prior Year Nonbudgeted Fund $28,674 $38,281 $36,546 ($1,735) -4.53%

HOUSE BILL 924. P1, J1, J2 1lr1413 A BILL ENTITLED. Commission on State Administered Medical Malpractice Liability Insurance

HOUSE BILL P, J, J lr By: Delegate Mizeur Introduced and read first time: February, Assigned to: Economic Matters A BILL ENTITLED AN ACT concerning Commission on State Administered Medical Malpractice

HOUSE BILL P, J, J lr By: Delegate Mizeur Introduced and read first time: February, Assigned to: Economic Matters A BILL ENTITLED AN ACT concerning Commission on State Administered Medical Malpractice

The Impact of First-Party Bad Faith Legislation on Homeowners Insurance Claim Trends in Washington State

April 2, 2009 The Impact of First-Party Bad Faith Legislation on Homeowners Insurance Claim Trends in Washington State INTERIM FINDINGS In 2007, the Washington State Legislature enacted the Insurance Fair

April 2, 2009 The Impact of First-Party Bad Faith Legislation on Homeowners Insurance Claim Trends in Washington State INTERIM FINDINGS In 2007, the Washington State Legislature enacted the Insurance Fair

Territorial Rating System for Automobile Insurance

Sec. 38a-686 page 1 (5-12) TABLE OF CONTENTS Territorial Rating System for Automobile Insurance Definitions. 38a-686-1 Private passenger nonfleet automobile insurance rate filings. 38a-686-2 Private passenger

Sec. 38a-686 page 1 (5-12) TABLE OF CONTENTS Territorial Rating System for Automobile Insurance Definitions. 38a-686-1 Private passenger nonfleet automobile insurance rate filings. 38a-686-2 Private passenger

Louisiana Department of Insurance

Louisiana Department of Insurance This public document was published at a total cost of $ 1,818.58 Thirty-two copies of this public document were published in this first printing at a cost of $ 39.19.

Louisiana Department of Insurance This public document was published at a total cost of $ 1,818.58 Thirty-two copies of this public document were published in this first printing at a cost of $ 39.19.

Private Passenger Automobile Insurance Coverages

Private Passenger Automobile Insurance Coverages An Actuarial Study of the Frequency and Cost of Claims for the State of Michigan by EPIC Consulting, LLC Principal Authors: Michael J. Miller, FCAS, MAAA

Private Passenger Automobile Insurance Coverages An Actuarial Study of the Frequency and Cost of Claims for the State of Michigan by EPIC Consulting, LLC Principal Authors: Michael J. Miller, FCAS, MAAA

2012 Market Share. Insurers. The 2012 Texas premium and. in Texas. for

By David Surles, CPCU, RPLU, AAI Contributing Author Insurers for Regina Anderson in Texas IIAT Manager of Technical Services The Texas premium and loss information tells a story of rising premiums and

By David Surles, CPCU, RPLU, AAI Contributing Author Insurers for Regina Anderson in Texas IIAT Manager of Technical Services The Texas premium and loss information tells a story of rising premiums and

Florida Residential Property Exposure

Florida Office of Insurance Regulation Presentation for the: Florida Chamber of Commerce Annual Insurance Summit Orlando, Florida January 2010 The materials presented here were compiled by the OIR and

Florida Office of Insurance Regulation Presentation for the: Florida Chamber of Commerce Annual Insurance Summit Orlando, Florida January 2010 The materials presented here were compiled by the OIR and

The State of Competition in the Workers' Compensation Market 2015

Maine State Library Maine State Documents Insurance Documents Professional and Financial Regulation 12-30-2015 The State of Competition in the Workers' Compensation Market 2015 Maine Bureau of Insurance

Maine State Library Maine State Documents Insurance Documents Professional and Financial Regulation 12-30-2015 The State of Competition in the Workers' Compensation Market 2015 Maine Bureau of Insurance

If you have questions regarding personal automobile insurance, please contact our Consumer Services Division at 1-888-TRY-WVIC, or visit our website

If you have questions regarding personal automobile insurance, please contact our Consumer Services Division at 1-888-TRY-WVIC, or visit our website at www.wvinsurance.gov Table of Contents Introduction...

If you have questions regarding personal automobile insurance, please contact our Consumer Services Division at 1-888-TRY-WVIC, or visit our website at www.wvinsurance.gov Table of Contents Introduction...

CHAPTER 2016-197. Committee Substitute for Committee Substitute for Senate Bill No. 1274

CHAPTER 2016-197 Committee Substitute for Committee Substitute for Senate Bill No. 1274 An act relating to limited sinkhole coverage insurance; amending s. 624.407, F.S.; specifying the amount of surplus

CHAPTER 2016-197 Committee Substitute for Committee Substitute for Senate Bill No. 1274 An act relating to limited sinkhole coverage insurance; amending s. 624.407, F.S.; specifying the amount of surplus

Florida Senate - 2016 SB 1274

By Senator Latvala 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 A bill to be entitled An act relating to sinkhole insurance; amending s. 624.407, F.S.; specifying

By Senator Latvala 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 A bill to be entitled An act relating to sinkhole insurance; amending s. 624.407, F.S.; specifying

About the Office of Insurance Regulation. About the Insurance Commissioner

About the Office of Insurance Regulation The Florida Office of Insurance Regulation (Office) has primary responsibility for regulation, compliance and enforcement of statutes relating to the business of

About the Office of Insurance Regulation The Florida Office of Insurance Regulation (Office) has primary responsibility for regulation, compliance and enforcement of statutes relating to the business of

Transportation Network Companies: Insurance Industry Advocacy Toolkit

Transportation Network Companies: Insurance Industry Advocacy Toolkit This toolkit, developed by an insurance industry working group, is intended to provide guidance and resources for insurance industry

Transportation Network Companies: Insurance Industry Advocacy Toolkit This toolkit, developed by an insurance industry working group, is intended to provide guidance and resources for insurance industry

PROPOSITION 103 S IMPACT ON AUTO INSURANCE PREMIUMS IN CALIFORNIA 15 YEARS OF INSURANCE REFORM: 1989-2004

PROPOSITION 103 S IMPACT ON AUTO INSURANCE PREMIUMS IN CALIFORNIA 15 YEARS OF INSURANCE REFORM: 1989-2004 In a voter revolt against massive increases in the price of auto, homeowner and business insurance,

PROPOSITION 103 S IMPACT ON AUTO INSURANCE PREMIUMS IN CALIFORNIA 15 YEARS OF INSURANCE REFORM: 1989-2004 In a voter revolt against massive increases in the price of auto, homeowner and business insurance,

CONFERENCE COMMITTEE REPORT BRIEF HOUSE BILL NO. 2352

SESSION OF 2015 CONFERENCE COMMITTEE REPORT BRIEF HOUSE BILL NO. 2352 As Agreed to May 20, 2015 Brief* HB 2352 would make several amendments to the Insurance Code. Among the amendments, the bill would

SESSION OF 2015 CONFERENCE COMMITTEE REPORT BRIEF HOUSE BILL NO. 2352 As Agreed to May 20, 2015 Brief* HB 2352 would make several amendments to the Insurance Code. Among the amendments, the bill would

April 10, 2003 10:00 a.m. Ernst N. Csiszar Director of Insurance State of South Carolina

Outline of Testimony Before the Congress of the United States of America House of Representatives Committee on Financial Services Subcommittee on Capital Markets, Insurance, and Government Sponsored Enterprises

Outline of Testimony Before the Congress of the United States of America House of Representatives Committee on Financial Services Subcommittee on Capital Markets, Insurance, and Government Sponsored Enterprises

Part I. Texas Department of Insurance Page 1 of 15 Chapter 5. Property and Casualty Insurance.

Part I. Texas Department of Insurance Page 1 of 15 SUBCHAPTER H. CANCELLATION, DENIAL, AND NONRENEWAL OF CERTAIN PROPERTY AND CASUALTY INSURANCE COVERAGE 28 TAC 5.7001, 5.7002, AND 5.7009 1. INTRODUCTION.

Part I. Texas Department of Insurance Page 1 of 15 SUBCHAPTER H. CANCELLATION, DENIAL, AND NONRENEWAL OF CERTAIN PROPERTY AND CASUALTY INSURANCE COVERAGE 28 TAC 5.7001, 5.7002, AND 5.7009 1. INTRODUCTION.

Medical Malpractice Liability Insurers - Biennial Reporting of Rate Modifiers

INSURANCE DEPARTMENT OF BANKING AND INSURANCE OFFICE OF PROPERTY AND CASUALTY Medical Malpractice Liability Insurers - Biennial Reporting of Rate Modifiers Proposed New Rules: N.J.A.C. 11:27-13 Authorized

INSURANCE DEPARTMENT OF BANKING AND INSURANCE OFFICE OF PROPERTY AND CASUALTY Medical Malpractice Liability Insurers - Biennial Reporting of Rate Modifiers Proposed New Rules: N.J.A.C. 11:27-13 Authorized

CALIFORNIA EARTHQUAKE AUTHORITY. Financial Statements. December 31, 2001 and 2000. (With Independent Auditors Report Thereon)

") Financial Statements (With Independent Auditors Report Thereon) Three Embarcadero Center San Francisco, CA 94111 Independent Auditors Report The Board of Directors California Earthquake Authority: We have

Financial Statements (With Independent Auditors Report Thereon) Three Embarcadero Center San Francisco, CA 94111 Independent Auditors Report The Board of Directors California Earthquake Authority: We have

LARGEST AUTO INSURERS FREQUENTLY CHARGE HIGHER PREMIUMS TO SAFE DRIVERS THAN TO THOSE RESPONSIBLE FOR ACCIDENTS

FOR IMMEDIATE RELEASE Contact: Bob Hunter, CFA, (703) 528-0062 January 28, 2013 LARGEST AUTO INSURERS FREQUENTLY CHARGE HIGHER PREMIUMS TO SAFE DRIVERS THAN TO THOSE RESPONSIBLE FOR ACCIDENTS 12-City Survey

FOR IMMEDIATE RELEASE Contact: Bob Hunter, CFA, (703) 528-0062 January 28, 2013 LARGEST AUTO INSURERS FREQUENTLY CHARGE HIGHER PREMIUMS TO SAFE DRIVERS THAN TO THOSE RESPONSIBLE FOR ACCIDENTS 12-City Survey

Louisiana Department of Insurance

Louisiana Department of Insurance This public document was published at a total cost of $ 1,382.06. Thirty-two copies of this public document were published in this first printing at a cost of $ 41.64.

Louisiana Department of Insurance This public document was published at a total cost of $ 1,382.06. Thirty-two copies of this public document were published in this first printing at a cost of $ 41.64.

Session 25 L, Introduction to General Insurance Ratemaking & Reserving: An Integrated Look. Moderator: W. Scott Lennox, FSA, FCAS, FCIA

Session 25 L, Introduction to General Insurance Ratemaking & Reserving: An Integrated Look Moderator: W. Scott Lennox, FSA, FCAS, FCIA Presenter: Houston Cheng, FCAS, FCIA Society of Actuaries 2013 Annual

Session 25 L, Introduction to General Insurance Ratemaking & Reserving: An Integrated Look Moderator: W. Scott Lennox, FSA, FCAS, FCIA Presenter: Houston Cheng, FCAS, FCIA Society of Actuaries 2013 Annual

2013 Complaint Ratio per $1 Million of Direct Premiums

2013 Complaint Ratio per $1 Million of Direct Premiums Property and Liability Companies Showing 0 or More Complaints Having Premium Dollars of at Least $1 For Coverage Type: Private Auto - All Company

2013 Complaint Ratio per $1 Million of Direct Premiums Property and Liability Companies Showing 0 or More Complaints Having Premium Dollars of at Least $1 For Coverage Type: Private Auto - All Company

Esurance Insurance, an Internet-based provider, opening for business March 29;

Executive Summary Three years ago, the New Jersey automobile insurance market was imploding. With more than 40 carriers leaving New Jersey during the previous 10 years, and major carriers threatening to

Executive Summary Three years ago, the New Jersey automobile insurance market was imploding. With more than 40 carriers leaving New Jersey during the previous 10 years, and major carriers threatening to

CHAPTER 10 - PROPERTY AND CASUALTY DIVISION SECTION.0100 - GENERAL PROVISIONS

CHAPTER 10 - PROPERTY AND CASUALTY DIVISION SECTION.0100 - GENERAL PROVISIONS 11 NCAC 10.0101 PURPOSE OF DIVISION 11 NCAC 10.0102 DEPUTY COMMISSIONER 11 NCAC 10.0103 DIVISION PERSONNEL History Note: Authority

CHAPTER 10 - PROPERTY AND CASUALTY DIVISION SECTION.0100 - GENERAL PROVISIONS 11 NCAC 10.0101 PURPOSE OF DIVISION 11 NCAC 10.0102 DEPUTY COMMISSIONER 11 NCAC 10.0103 DIVISION PERSONNEL History Note: Authority

Office of Insurance Regulation

Talking Points Update PIP/No-Fault House Insurance Committee October 18, 2005 Mr. Chairman, members, thank you for the opportunity to provide you with some comments today. Mr. Chairman your staff did an

Talking Points Update PIP/No-Fault House Insurance Committee October 18, 2005 Mr. Chairman, members, thank you for the opportunity to provide you with some comments today. Mr. Chairman your staff did an

Major Auto Insurers Charge Higher Rates to High School Graduates and Low Income Workers

Major Auto Insurers Charge Higher Rates to High School Graduates and Low Income Workers In Buffalo and across the State of New York Low Income Workers are Paying More for Auto Insurance as a result of

Major Auto Insurers Charge Higher Rates to High School Graduates and Low Income Workers In Buffalo and across the State of New York Low Income Workers are Paying More for Auto Insurance as a result of

Report on Availability and Affordability of Personal and Commercial Property and Casualty Insurance in Coastal Areas in Maryland

Report on Availability and Affordability of Personal and Commercial Property and Casualty Insurance in Coastal Areas in Maryland Therese M. Goldsmith Commissioner October 2012 List of Figures and Tables

Report on Availability and Affordability of Personal and Commercial Property and Casualty Insurance in Coastal Areas in Maryland Therese M. Goldsmith Commissioner October 2012 List of Figures and Tables

Illinois Department of Insurance

Illinois Department of Insurance PAT QUINN Governor ANDREW BORON Director To the Honorable Members of the General Assembly: The Illinois Insurance Cost Containment Act requires the Director of Insurance

Illinois Department of Insurance PAT QUINN Governor ANDREW BORON Director To the Honorable Members of the General Assembly: The Illinois Insurance Cost Containment Act requires the Director of Insurance

S-4504.1 SUBSTITUTE SENATE BILL 6252. State of Washington 61st Legislature 2010 Regular Session

S-4504.1 SUBSTITUTE SENATE BILL 6252 State of Washington 61st Legislature 2010 Regular Session By Senate Labor, Commerce & Consumer Protection (originally sponsored by Senators Kohl-Welles, Kline, and

S-4504.1 SUBSTITUTE SENATE BILL 6252 State of Washington 61st Legislature 2010 Regular Session By Senate Labor, Commerce & Consumer Protection (originally sponsored by Senators Kohl-Welles, Kline, and

The Florida Senate POTENTIAL IMPACT OF MANDATING BODILY INJURY LIABILITY INSURANCE FOR MOTOR VEHICLES. Interim Project Summary 98-03 November 1998

The Florida Senate Interim Project Summary 98-03 November 1998 Committee on Banking and Insurance Senator Mario Diaz-Balart, Chairman POTENTIAL IMPACT OF MANDATING BODILY INJURY LIABILITY INSURANCE FOR

The Florida Senate Interim Project Summary 98-03 November 1998 Committee on Banking and Insurance Senator Mario Diaz-Balart, Chairman POTENTIAL IMPACT OF MANDATING BODILY INJURY LIABILITY INSURANCE FOR

Maryland Insurance Administration s 2005 Report on Workers Compensation Insurance

Maryland Insurance Administration s 2005 Report on Workers Compensation Insurance December 2005 Table of Contents Topic Page I Preface 3 II Overview 4 III Market Concentration 6 IV NCCI s Rate Filings

Maryland Insurance Administration s 2005 Report on Workers Compensation Insurance December 2005 Table of Contents Topic Page I Preface 3 II Overview 4 III Market Concentration 6 IV NCCI s Rate Filings

HOMEOWNERS INSURANCE ACT OF 2010

HOMEOWNERS INSURANCE ACT OF 2010 The purpose of the Act is to promote the public welfare by regulating Property Casualty Rates to the end that they not be excessive, inadequate or unfairly discriminatory;

HOMEOWNERS INSURANCE ACT OF 2010 The purpose of the Act is to promote the public welfare by regulating Property Casualty Rates to the end that they not be excessive, inadequate or unfairly discriminatory;

Hurricane Hotline Contact Numbers, August 15, 2007

Hurricane Hotline Contact Numbers, August 15, 2007 Insurance Industry Provides "Hotline" Contact Numbers To Ease With Claims Process Contact: Sam Miller, 850.386.6668 x 223 Gary Landry, 850.386.6668 x

Hurricane Hotline Contact Numbers, August 15, 2007 Insurance Industry Provides "Hotline" Contact Numbers To Ease With Claims Process Contact: Sam Miller, 850.386.6668 x 223 Gary Landry, 850.386.6668 x

Please see Section IX. for Additional Information:

BILL: CS/SB 916 The Florida Senate BILL ANALYSIS AND FISCAL IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) Prepared By: The

BILL: CS/SB 916 The Florida Senate BILL ANALYSIS AND FISCAL IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) Prepared By: The