Central Bank Deleveraging and Financial Sector Regulation. Perry Mehrling Minsky Conference, DC April 15, 2015

|

|

|

- Coral Chambers

- 8 years ago

- Views:

Transcription

1 Central Bank Deleveraging and Financial Sector Regulation Perry Mehrling Minsky Conference, DC April 15, 2015

2 Why is central banking difficult? Essential hybridity Inherent hierarchy Inherent instability Financial globalization

3 Essential hybridity Bankers bank Private sector, peace time, private profit Backstop for money market funding (flow) Backstop for capital market lending (stock) Government bank Public sector, war time, public purpose Backstop for war debt issuance (flow) Backstop for government debt market (stock) Contradictions/Dynamics of Hybridity

Backstop for government debt market (stock)")

4 Inherent Hierarchy World Reserve Currency Central Bank Currency Bank Deposits Domestic Credit Dollar C6 Swap Line Bilateral Swaps, Regional Pooling, IMF National Money National Credit

5 Inherent Instability of Credit Credit anticipates uncertain future Mistakes are inevitable; externalities and herding Money doesn t manage itself Older Versions Hawtrey, trade credit Keynes/Minsky, business investment and credit New Market Based Credit Household mortgage credit, not business Capital market securitization, not bank lending Global money market funding, not domestic deposits

6 Financial Globalization an effective, smoothly functioning international capital market is itself an instrument of world economic growth, not a nuisance which can be disposed of and the functioning of which can be transferred to new or extended inter-governmental institutions. the main requirement of international monetary reform is to preserve and improve the efficiency of the private capital market while building protection against its performing in a destabilizing fashion. (Depres, Kindleberger, Salant 1966)

7 Economics not much help Technocratic domestic management focus Business cycle stabilization Inflation targeting Keynesian versus Monetarists frame Fiscal policy versus Monetary Policy IS/LM versus MV=PY, no central bank qua bank Active Management versus Laissez Faire Discretion versus Rules New Synthesis and Great Moderation DSGE and Taylor Rule

8 A Bagehot Moment

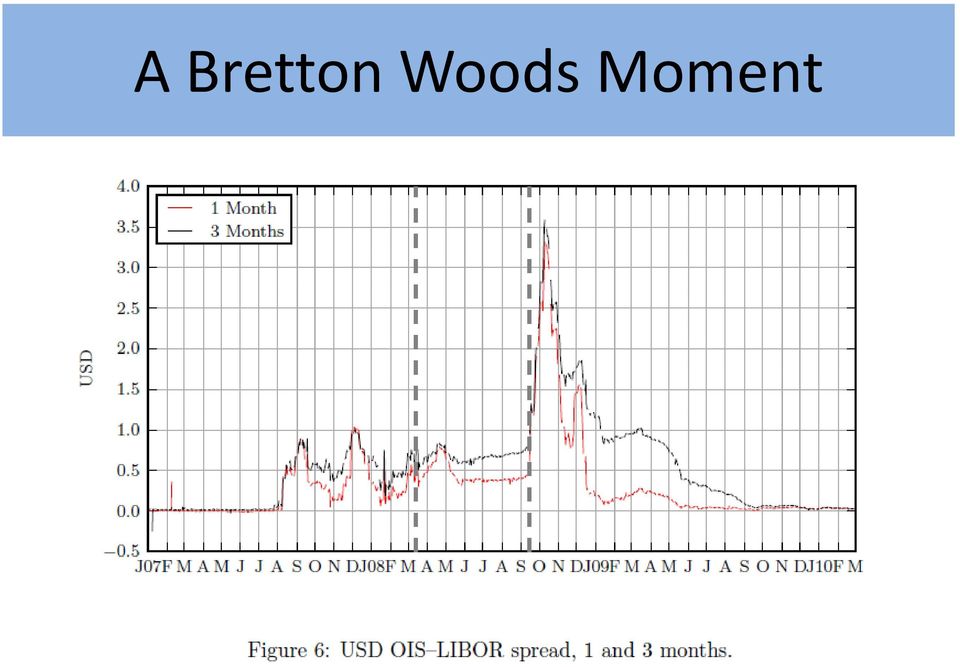

9 A Bretton Woods Moment

10 Transformation of Fed Balance Sheet Stage I: Dealer of Last Resort Collapsing private money market; expanding central bank counterparty Collapsing shadow banking ; expanding central bank good bank Stage II: Monetary Stimulus (QE 1,2,3) Deliberate distortion of private asset prices Deliberate expansion of central bank balance sheet

11 What is leverage? April 8, 2015 April 8, 2015 (restated) Assets Liabilities Assets Liabilities Tbonds 2.5 MBS Currency.3 RRP 2.8 Deposits TBills 4.4 TBonds 4.4 MBS Money 4.4 TBills 1.9 TBonds Assets = 4.48 Liabilities = 4.42 Capital =.06 OIS = 4.4 IRS = 4.4 CDS = 1.9

12 Shadow Banking and Central Banking Capital Funding Bank Global Money Dealer Asset Manager Assets Liabilities Assets Liabilities Assets Liabilities RMBS CDS IRS FXS MM funding MM funding Reserves Liquidity put deposits Capital Derivative Dealer deposits Capital CDS IRS FXS Assets CDS IRS FXS Reserves Liquidity Put Liabilities CDS IRS FXS Capital

13 Backstopping Market-making, Last Resort Global Money Dealer Derivative Dealer Central Bank (or C6) Assets MM funding Reserves Liquidity put Assets CDS IRS FXS Reserves Liquidity put Assets Reserves Liabilities deposits Liabilities CDS IRS FXS Liabilities Liquidity put GMD Liquidity put DD

14 What would Exit mean? Fed makes Outside spread Stabilization not stimulus motive Tapering, to allow normalization of capital market prices Reverse repo, to allow normalization of money market funding price Private dealer system makes Inside spread Private profit not Fed gaming motive Short term volatility inevitable, indeed necessary incentive for revival of private market making

15 Emerging Market Structure Matched Book (e.g. central clearing counterparty) Global Liquidity Backstop Private first resort, Public last resort Speculative Book (e.g. market-making) Local Capital Backstop Private first resort, Public last resort Fraught politics of stabilization Liquidity crisis moves prices, causes insolvency Global vs. Local responsibility

Local Capital Backstop Private first resort, Public last resort Fraught")

16 Emerging Monetary Policy Framework Monetary Policy transmission From O/N to asset prices through market-makers Money market funding (e.g. 3 month) Capital market lending (e.g. 10 year) Managing balance, Discipline versus elasticity International differentiation/management Private finance, dollar and C6, (e.g. FX) Public finance, (e.g. development bank)

Capital market lending (e.g. 10 year) Managing balance, Discipline versus")

17 Bottom Line 1. No public deleveraging [sic] until global dealer system prepared to replace with private leveraging [sic] Money dealers Derivative dealers 2. Financial Sector Regulation is about growing a robust infrastructure for market-based credit CCP and speculative dealer system, first resort Central Bank backstop, last resort 3. Exit = Transition to Markets Including market prices, both money and capital

![[sic] Money dealers Derivative dealers 2.](/docs-images/42/11262518/images/page_17.jpg "Financial Sector Regulation is about growing a robust infrastructure for market-based credit CCP and")

18 Why is Central Banking Difficult? Technocratic veil obscures institutional reality Theory: Monetary Walrasianism to DSGE Policy: Large-scale econometric models What is missing? Essential hybridity Inherent hierarchy Inherent instability Financial globalization

19 New Economic Thinking Needed Capitalism is essentially a financial system (Minsky 1967) Banking as Payments System Banking as Marketmaking System

20 Further Reading Bagehot was a Shadow Banker: Shadow Banking, Central Banking, and the Future of Global Finance China s Engagement with an Evolving International Monetary System: a Payments Perspective Why Central Banking Should be Re-Imagined Essential Hybridity: a Money View of FX

The Inherent Hierarchy of Money

0 The Inherent Hierarchy of Money by Perry Mehrling January 25, 2012 Prepared for Duncan Foley festschrift volume, and conference April 20-21, 2012. 1 Always and everywhere, monetary systems are hierarchical.

0 The Inherent Hierarchy of Money by Perry Mehrling January 25, 2012 Prepared for Duncan Foley festschrift volume, and conference April 20-21, 2012. 1 Always and everywhere, monetary systems are hierarchical.

THE IMPORTANCE OF RISK MANAGEMENT

THE IMPORTANCE OF RISK MANAGEMENT Andrew L. T. Sheng* I have a terribly difficult task, because I have very little to add after such excellent presentations by three wise men, Stanley Fischer, whom I worked

THE IMPORTANCE OF RISK MANAGEMENT Andrew L. T. Sheng* I have a terribly difficult task, because I have very little to add after such excellent presentations by three wise men, Stanley Fischer, whom I worked

CENTRAL BANKS DIVERGE

GLOBAL OUTLOOK CENTRAL BANKS DIVERGE MAY 21, 2015 MACROECONOMICS OF POLICY DIVERGENCE WHAT S AHEAD Global Overview: Roots of Divergence Federal Reserve Preparing for Liftoff QE in the U.S. Versus the Euro-Zone

GLOBAL OUTLOOK CENTRAL BANKS DIVERGE MAY 21, 2015 MACROECONOMICS OF POLICY DIVERGENCE WHAT S AHEAD Global Overview: Roots of Divergence Federal Reserve Preparing for Liftoff QE in the U.S. Versus the Euro-Zone

Chapter 17. Fixed Exchange Rates and Foreign Exchange Intervention. Copyright 2003 Pearson Education, Inc.

Chapter 17 Fixed Exchange Rates and Foreign Exchange Intervention Slide 17-1 Chapter 17 Learning Goals How a central bank must manage monetary policy so as to fix its currency's value in the foreign exchange

Chapter 17 Fixed Exchange Rates and Foreign Exchange Intervention Slide 17-1 Chapter 17 Learning Goals How a central bank must manage monetary policy so as to fix its currency's value in the foreign exchange

Toward Further Development of the Tokyo Financial Market: Issues on Repo Market Reform

May 13, 2015 Bank of Japan Toward Further Development of the Tokyo Financial Market: Issues on Repo Market Reform Keynote Speech at the Futures Industry Association Japan (FIA Japan) Financial Market Conference

May 13, 2015 Bank of Japan Toward Further Development of the Tokyo Financial Market: Issues on Repo Market Reform Keynote Speech at the Futures Industry Association Japan (FIA Japan) Financial Market Conference

Understanding Central Banking in Light of the Credit Turmoil

Understanding Central Banking in Light of the Credit Turmoil Marvin Goodfriend Tepper School Carnegie Mellon University Implementing Monetary Policy Post-Crisis: What Have We Learned? What Do We Need to

Understanding Central Banking in Light of the Credit Turmoil Marvin Goodfriend Tepper School Carnegie Mellon University Implementing Monetary Policy Post-Crisis: What Have We Learned? What Do We Need to

KBW Mortgage Finance Conference. June 2, 2015

KBW Mortgage Finance Conference June 2, 2015 Forward Looking Statements This presentation contains forward looking statements within the meaning of the safe harbor provisions of the Private Securities

KBW Mortgage Finance Conference June 2, 2015 Forward Looking Statements This presentation contains forward looking statements within the meaning of the safe harbor provisions of the Private Securities

Conceptual Framework: What Does the Financial System Do? 1. Financial contracting: Get funds from savers to investors

Conceptual Framework: What Does the Financial System Do? 1. Financial contracting: Get funds from savers to investors Transactions costs Contracting costs (from asymmetric information) Adverse Selection

Conceptual Framework: What Does the Financial System Do? 1. Financial contracting: Get funds from savers to investors Transactions costs Contracting costs (from asymmetric information) Adverse Selection

Forecasting Chinese Economy for the Years 2013-2014

Forecasting Chinese Economy for the Years 2013-2014 Xuesong Li Professor of Economics Deputy Director of Institute of Quantitative & Technical Economics Chinese Academy of Social Sciences Email: xsli@cass.org.cn

Forecasting Chinese Economy for the Years 2013-2014 Xuesong Li Professor of Economics Deputy Director of Institute of Quantitative & Technical Economics Chinese Academy of Social Sciences Email: xsli@cass.org.cn

The challenge of liquidity and collateral management in the new regulatory landscape

The challenge of liquidity and collateral management in the new regulatory landscape ICMA Professional Repo and Collateral Management Course 2012 Agenda 1. Background: The repo product under pressure 2.

The challenge of liquidity and collateral management in the new regulatory landscape ICMA Professional Repo and Collateral Management Course 2012 Agenda 1. Background: The repo product under pressure 2.

Development of Money Markets

Development of Money Markets Mats Filipsson International Monetary Fund Monetary and Exchange Affairs Department Workshop on Developing Government Bond Markets in APEC Economies Shanghai, November 12 15,

Development of Money Markets Mats Filipsson International Monetary Fund Monetary and Exchange Affairs Department Workshop on Developing Government Bond Markets in APEC Economies Shanghai, November 12 15,

Collateral Management Best Practices for Broker-Dealers

Banking & Securities Collateral Management Best Practices for Broker-Dealers Jeff Penney Collateral Management Best Practices for Broker-Dealers 1 col lat er al (noun) something pledged as security for

Banking & Securities Collateral Management Best Practices for Broker-Dealers Jeff Penney Collateral Management Best Practices for Broker-Dealers 1 col lat er al (noun) something pledged as security for

Phoenix Management Services Lending Climate in America Survey

Phoenix Management Services Lending Climate in America Survey 4th Quarter 2010 Summary, Trends and Implications PHOENIX LENDING CLIMATE IN AMERICA QUARTERLY SURVEY SUMMARY, TRENDS AND IMPLICATIONS 1. Existing

Phoenix Management Services Lending Climate in America Survey 4th Quarter 2010 Summary, Trends and Implications PHOENIX LENDING CLIMATE IN AMERICA QUARTERLY SURVEY SUMMARY, TRENDS AND IMPLICATIONS 1. Existing

Chart I.1. Difference between Primary Surplus (PS) and Bond Yield Spreads in Selected EU 1 Countries

and Bond Yield Spreads in Selected EU 1 Countries") LIST OF CHARTS Chart I.1. Difference between Primary Surplus (PS) and Bond Yield Spreads in Selected EU 1 Countries Chart I.2. Gross Debt Stock and Budget Deficits of Selected Countries as of 2010 1 Chart

LIST OF CHARTS Chart I.1. Difference between Primary Surplus (PS) and Bond Yield Spreads in Selected EU 1 Countries Chart I.2. Gross Debt Stock and Budget Deficits of Selected Countries as of 2010 1 Chart

The Primary Dealer System. Counterparty Management, Markets Group

The Primary Dealer System Counterparty Management, Markets Group Central Banking Seminar September 2015 Overview Primary Dealers serve, first and foremost, as trading counterparties of the FRBNY in its

The Primary Dealer System Counterparty Management, Markets Group Central Banking Seminar September 2015 Overview Primary Dealers serve, first and foremost, as trading counterparties of the FRBNY in its

Debt Overhang and Capital Regulation

Debt Overhang and Capital Regulation Anat Admati INET in Berlin: Rethinking Economics and Politics The Challenge of Deleveraging and Overhangs of Debt II: The Politics and Economics of Restructuring April

Debt Overhang and Capital Regulation Anat Admati INET in Berlin: Rethinking Economics and Politics The Challenge of Deleveraging and Overhangs of Debt II: The Politics and Economics of Restructuring April

Globalization and Monetary Policy

Globalization and Monetary Policy John B. Taylor Stanford University Fifteenth Cycle of Economic Lectures Banco de Guatemala 22 June 2006 Outline: Three Themes Increased Need for Systematic Strategies

Globalization and Monetary Policy John B. Taylor Stanford University Fifteenth Cycle of Economic Lectures Banco de Guatemala 22 June 2006 Outline: Three Themes Increased Need for Systematic Strategies

i T-bill (dy) = $10,000 - $9,765 360 = 6.768% $10,000 125

= $10,000 - $9,765 360 = 6.768% $10,000 125") Answers to Chapter 5 Questions 1. First, money market instruments are generally sold in large denominations (often in units of $1 million to $10 million). Most money market participants want or need to

Answers to Chapter 5 Questions 1. First, money market instruments are generally sold in large denominations (often in units of $1 million to $10 million). Most money market participants want or need to

Lecture 4: The Aftermath of the Crisis

Lecture 4: The Aftermath of the Crisis 2 The Fed s Efforts to Restore Financial Stability A financial panic in fall 2008 threatened the stability of the global financial system. In its lender-of-last-resort

Lecture 4: The Aftermath of the Crisis 2 The Fed s Efforts to Restore Financial Stability A financial panic in fall 2008 threatened the stability of the global financial system. In its lender-of-last-resort

Lecture 16: Financial Crisis

Lecture 16: Financial Crisis What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows in financial markets, with the result that financial

Lecture 16: Financial Crisis What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows in financial markets, with the result that financial

DEVELOPMENTS IN 1990 s

MACROECONOMIC MANAGEMENT WITH OPEN CAPITAL ACCOUNTS: THE TURKISH CASE FAIK OZTRAK Director TUSIAD-Koc University, Economic Research Forum HIGH LEVEL SEMINAR ON CRISIS PREVENTION, SINGAPORE, JULY 1, 26

MACROECONOMIC MANAGEMENT WITH OPEN CAPITAL ACCOUNTS: THE TURKISH CASE FAIK OZTRAK Director TUSIAD-Koc University, Economic Research Forum HIGH LEVEL SEMINAR ON CRISIS PREVENTION, SINGAPORE, JULY 1, 26

Monetary Operations: Liquidity Insurance

Monetary Operations: Liquidity Insurance Garreth Rule Operationalising Financial Stability CEMLA 25 29 November 2013 The Bank of England does not accept any liability for misleading or inaccurate information

Monetary Operations: Liquidity Insurance Garreth Rule Operationalising Financial Stability CEMLA 25 29 November 2013 The Bank of England does not accept any liability for misleading or inaccurate information

Markets, Investments, and Financial Management FIFTEENTH EDITION

INTRODUCTION TO FINANCE Markets, Investments, and Financial Management FIFTEENTH EDITION Ronald W. Melicher Professor of Finance University of Colorado at Boulder Edgar A. Norton Professor of Finance Illinois

INTRODUCTION TO FINANCE Markets, Investments, and Financial Management FIFTEENTH EDITION Ronald W. Melicher Professor of Finance University of Colorado at Boulder Edgar A. Norton Professor of Finance Illinois

Session 39 PD, Inflation or Default? Potential Impacts on the Life Insurance Industry. Moderator: John R. Skar, FSA

Session 39 PD, Inflation or Default? Potential Impacts on the Life Insurance Industry Moderator: John R. Skar, FSA Presenters: John R. Skar, FSA Walker Todd Inflation or Default? Which way out of the U.S.

Session 39 PD, Inflation or Default? Potential Impacts on the Life Insurance Industry Moderator: John R. Skar, FSA Presenters: John R. Skar, FSA Walker Todd Inflation or Default? Which way out of the U.S.

Econ 336 - Spring 2007 Homework 5

Econ 336 - Spring 2007 Homework 5 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The real exchange rate, q, is defined as A) E times P B)

Econ 336 - Spring 2007 Homework 5 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The real exchange rate, q, is defined as A) E times P B)

EC 341 Monetary and Banking Institutions, Boston University Summer 2, 2012 Homework 3 Due date: Tuesday, July 31, 6:00 PM.

EC 341 Monetary and Banking Institutions, Boston University Summer 2, 2012 Homework 3 Due date: Tuesday, July 31, 6:00 PM. Problem 1 Questions 1, 4, 6, 8, 12, 13, 16, 18, 22, and 23 from Chapter 8. Solutions:

EC 341 Monetary and Banking Institutions, Boston University Summer 2, 2012 Homework 3 Due date: Tuesday, July 31, 6:00 PM. Problem 1 Questions 1, 4, 6, 8, 12, 13, 16, 18, 22, and 23 from Chapter 8. Solutions:

Managing Stop-Go Capital Flows in EM Asia: So Far, So Good

Managing Stop-Go Capital Flows in EM Asia: So Far, So Good Andrew Filardo Bank for International Settlements Prepared for the Central Banks of Finland and Austria Joint Conference on European Economic

Managing Stop-Go Capital Flows in EM Asia: So Far, So Good Andrew Filardo Bank for International Settlements Prepared for the Central Banks of Finland and Austria Joint Conference on European Economic

Lecture 10: International banking

Lecture 10: International banking The sessions so far have focused on banking in a domestic context. In this lecture we are going to look at the issues which arise from the internationalisation of banking,

Lecture 10: International banking The sessions so far have focused on banking in a domestic context. In this lecture we are going to look at the issues which arise from the internationalisation of banking,

GOVERNMENT DEBT MANAGEMENT AT THE ZERO LOWER BOUND

GOVERNMENT DEBT MANAGEMENT AT THE ZERO LOWER BOUND ROBIN GREENWOOD SAMUEL G. HANSON JOSHUA S. RUDOLPH LAWRENCE H. SUMMERS OUR PAPER I. Quantify Fed vs. Treasury conflict in QE era II. Fed vs. Treasury

GOVERNMENT DEBT MANAGEMENT AT THE ZERO LOWER BOUND ROBIN GREENWOOD SAMUEL G. HANSON JOSHUA S. RUDOLPH LAWRENCE H. SUMMERS OUR PAPER I. Quantify Fed vs. Treasury conflict in QE era II. Fed vs. Treasury

Challenges to Central Banking from Globalized Financial Systems. Discussant s comments by Michael Reddell Reserve Bank of New Zealand 1 On

Challenges to Central Banking from Globalized Financial Systems Conference at the IMF in Washington, D.C., September 16 17, 2002 Discussant s comments by Michael Reddell Reserve Bank of New Zealand 1 On

Challenges to Central Banking from Globalized Financial Systems Conference at the IMF in Washington, D.C., September 16 17, 2002 Discussant s comments by Michael Reddell Reserve Bank of New Zealand 1 On

Macroprudential Policies in Korea

1 IMF-Riksbank Conference Stockholm, November 13~14, 2014 Macroprudential Policies in Korea Tae Soo Kang Disclaimer This presentation represents the views of the author and not necessarily those of the

1 IMF-Riksbank Conference Stockholm, November 13~14, 2014 Macroprudential Policies in Korea Tae Soo Kang Disclaimer This presentation represents the views of the author and not necessarily those of the

Use of currencies In international trade by Marc Auboin, Counsellor

Use of currencies In international trade by Marc Auboin, Counsellor 3 basic realities and 2 questions Trade finance: systemic to trade. Little trade paid cash - 70-80% of world trade relies on trade credit/guarantees.

Use of currencies In international trade by Marc Auboin, Counsellor 3 basic realities and 2 questions Trade finance: systemic to trade. Little trade paid cash - 70-80% of world trade relies on trade credit/guarantees.

Monetary Policy in the Post Crisis Period: The Turkish Perspective

Monetary Policy in the Post Crisis Period: The Turkish Perspective Hakan Kara Economic Research Forum Conference İstanbul April 19, 2013 Outline 1. Motivation of the New Policy Framework 2. New Instruments

Monetary Policy in the Post Crisis Period: The Turkish Perspective Hakan Kara Economic Research Forum Conference İstanbul April 19, 2013 Outline 1. Motivation of the New Policy Framework 2. New Instruments

Financial Status, Operating Results and Risk Management

Financial Status, Operating Results and Risk Management 87 Financial Status 88 89 90 90 90 95 95 Operating Results Cash Flow Effects of Major Capital Expenditures in the Most Recent Fiscal Year on Financial

Financial Status, Operating Results and Risk Management 87 Financial Status 88 89 90 90 90 95 95 Operating Results Cash Flow Effects of Major Capital Expenditures in the Most Recent Fiscal Year on Financial

Fixed Exchange Rates and Exchange Market Intervention. Chapter 18

Fixed Exchange Rates and Exchange Market Intervention Chapter 18 1. Central bank intervention in the foreign exchange market 2. Stabilization under xed exchange rates 3. Exchange rate crises 4. Sterilized

Fixed Exchange Rates and Exchange Market Intervention Chapter 18 1. Central bank intervention in the foreign exchange market 2. Stabilization under xed exchange rates 3. Exchange rate crises 4. Sterilized

Comments on the Basel Committee on Banking Supervision s Consultative Document: Supervisory framework for measuring and controlling large exposures

June 28, 2013 Comments on the Basel Committee on Banking Supervision s Consultative Document: Supervisory framework for measuring and controlling large exposures Japanese Bankers Association We, the Japanese

June 28, 2013 Comments on the Basel Committee on Banking Supervision s Consultative Document: Supervisory framework for measuring and controlling large exposures Japanese Bankers Association We, the Japanese

Discussion of Government and Central Bank Balance Sheets, Inflation and Monetary Policy by Christopher A. Sims

Discussion of Government and Central Bank Balance Sheets, Inflation and Monetary Policy by Christopher A. Sims Timothy Cogley May 16, 2009 Questions about the Fed s Balance Sheet Does the vast expansion

Discussion of Government and Central Bank Balance Sheets, Inflation and Monetary Policy by Christopher A. Sims Timothy Cogley May 16, 2009 Questions about the Fed s Balance Sheet Does the vast expansion

René Garcia Professor of finance

Liquidity Risk: What is it? How to Measure it? René Garcia Professor of finance EDHEC Business School, CIRANO Cirano, Montreal, January 7, 2009 The financial and economic environment We are living through

Liquidity Risk: What is it? How to Measure it? René Garcia Professor of finance EDHEC Business School, CIRANO Cirano, Montreal, January 7, 2009 The financial and economic environment We are living through

Financial-Institutions Management. Solutions 5. Chapter 18: Liability and Liquidity Management Reserve Requirements

Solutions 5 Chapter 18: Liability and Liquidity Management Reserve Requirements 8. City Bank has estimated that its average daily demand deposit balance over the recent 14- day reserve computation period

Solutions 5 Chapter 18: Liability and Liquidity Management Reserve Requirements 8. City Bank has estimated that its average daily demand deposit balance over the recent 14- day reserve computation period

New York University Courant Institute of Mathematical Sciences. Syllabus

New York University Courant Institute of Mathematical Sciences Syllabus Mathematical Finance Seminar Course: A Practical Approach to Risk Assessment of Mortgage-Backed Securities September 8, 2010 December

New York University Courant Institute of Mathematical Sciences Syllabus Mathematical Finance Seminar Course: A Practical Approach to Risk Assessment of Mortgage-Backed Securities September 8, 2010 December

Monetary policy, fiscal policy and public debt management

Monetary policy, fiscal policy and public debt management People s Bank of China Abstract This paper touches on the interaction between monetary policy, fiscal policy and public debt management. The first

Monetary policy, fiscal policy and public debt management People s Bank of China Abstract This paper touches on the interaction between monetary policy, fiscal policy and public debt management. The first

FREQUENTLY ASKED QUESTIONS ON TREASURY S PROGRAM TO SELL MBS

FREQUENTLY ASKED QUESTIONS ON TREASURY S PROGRAM TO SELL MBS The following frequently asked questions provide further information regarding Treasury s program to wind down its $142 billion portfolio of

FREQUENTLY ASKED QUESTIONS ON TREASURY S PROGRAM TO SELL MBS The following frequently asked questions provide further information regarding Treasury s program to wind down its $142 billion portfolio of

Ignazio Visco: Rebalancing trade and capital flows

Ignazio Visco: Rebalancing trade and capital flows Remarks by Mr Ignazio Visco, Deputy Director General of the Bank of Italy, at the Global Economic Symposium 2010, Istanbul, 29 September 2010. * * * 1.

Ignazio Visco: Rebalancing trade and capital flows Remarks by Mr Ignazio Visco, Deputy Director General of the Bank of Italy, at the Global Economic Symposium 2010, Istanbul, 29 September 2010. * * * 1.

Inside and outside liquidity provision

Inside and outside liquidity provision James McAndrews, FRBNY, ECB Workshop on Excess Liquidity and Money Market Functioning, 19/20 November, 2012 The views expressed in this presentation are those of

Inside and outside liquidity provision James McAndrews, FRBNY, ECB Workshop on Excess Liquidity and Money Market Functioning, 19/20 November, 2012 The views expressed in this presentation are those of

Financial Intermediation and Credit Policy in Business Cycle Analysis. Mark Gertler and Nobuhiro Kiyotaki NYU and Princeton

Financial Intermediation and Credit Policy in Business Cycle Analysis Mark Gertler and Nobuhiro Kiyotaki NYU and Princeton Motivation Present a canonical framework to think about the current - nancial

Financial Intermediation and Credit Policy in Business Cycle Analysis Mark Gertler and Nobuhiro Kiyotaki NYU and Princeton Motivation Present a canonical framework to think about the current - nancial

Switzerland 2013 Article for Consultation Preliminary Conclusions Bern, March 18, 2013

Switzerland 2013 Article for Consultation Preliminary Conclusions Bern, March 18, 2013 With the exchange rate floor in place for over a year, the Swiss economy remains stable, though inflation remains

Switzerland 2013 Article for Consultation Preliminary Conclusions Bern, March 18, 2013 With the exchange rate floor in place for over a year, the Swiss economy remains stable, though inflation remains

MASTER OF SCIENCE FINANCIAL ECONOMICS ABAC SCHOOL OF MANAGEMENT ASSUMPTION UNIVERSITY OF THAILAND

MASTER OF SCIENCE FINANCIAL ECONOMICS ABAC SCHOOL OF MANAGEMENT ASSUMPTION UNIVERSITY OF THAILAND ECO 5001 Mathematics for Finance and Economics The uses of mathematical argument in extending the range,

MASTER OF SCIENCE FINANCIAL ECONOMICS ABAC SCHOOL OF MANAGEMENT ASSUMPTION UNIVERSITY OF THAILAND ECO 5001 Mathematics for Finance and Economics The uses of mathematical argument in extending the range,

Special Drawing Rights A Way out of Global Imbalances?

Special Drawing Rights A Way out of Global Imbalances? Stefan Bender Special Drawing Rights Definition Special Drawing Rights (SDR) are the monetary unit of the reserve assets of the International Monetary

Special Drawing Rights A Way out of Global Imbalances? Stefan Bender Special Drawing Rights Definition Special Drawing Rights (SDR) are the monetary unit of the reserve assets of the International Monetary

FX / XCCY Swap market overview. Frankfurt, 9 th of September 2014 Patrick Chauvet, BNPParibas Fixed Income

FX / XCCY Swap market overview Frankfurt, 9 th of September 2014 Patrick Chauvet, BNPParibas Fixed Income Introduction 3 products allow market players to trade Forex swaps, or in fact Cross currency basis

FX / XCCY Swap market overview Frankfurt, 9 th of September 2014 Patrick Chauvet, BNPParibas Fixed Income Introduction 3 products allow market players to trade Forex swaps, or in fact Cross currency basis

Observations on Financial Innovation and Finance Science

Observations on Financial Innovation and Finance Science Robert C. Merton MIT Sloan School of Management Symposium CALTECH + FINANCE May 1, 2015 Overview of my remarks Well-functioning financial system

Observations on Financial Innovation and Finance Science Robert C. Merton MIT Sloan School of Management Symposium CALTECH + FINANCE May 1, 2015 Overview of my remarks Well-functioning financial system

MACROECONOMICS. The Monetary System: What It Is and How It Works. N. Gregory Mankiw. PowerPoint Slides by Ron Cronovich

4 : What It Is and How It Works MACROECONOMICS N. Gregory Mankiw Modified for EC 204 by Bob Murphy PowerPoint Slides by Ron Cronovich 2013 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL

4 : What It Is and How It Works MACROECONOMICS N. Gregory Mankiw Modified for EC 204 by Bob Murphy PowerPoint Slides by Ron Cronovich 2013 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL

6. Federal Funds: Final Settlement

6. Federal Funds: Final Settlement Stigum (p. 507) says The primary job of the manager of a bank s fed funds desk is to ensure (1) that the bank settles with the Fed and (2) that in doing so, it hold no

6. Federal Funds: Final Settlement Stigum (p. 507) says The primary job of the manager of a bank s fed funds desk is to ensure (1) that the bank settles with the Fed and (2) that in doing so, it hold no

THE RETURN OF CAPITAL EXPENDITURE OR CAPEX CYCLE IN MALAYSIA

PUBLIC BANK BERHAD ECONOMICS DIVISION MENARA PUBLIC BANK 146 JALAN AMPANG 50450 KUALA LUMPUR TEL : 03 2176 6000/666 FAX : 03 2163 9929 Public Bank Economic Review is published bi monthly by Economics Division,

PUBLIC BANK BERHAD ECONOMICS DIVISION MENARA PUBLIC BANK 146 JALAN AMPANG 50450 KUALA LUMPUR TEL : 03 2176 6000/666 FAX : 03 2163 9929 Public Bank Economic Review is published bi monthly by Economics Division,

Letter from the President

Letter from the President 1 FEDERAL RESERVE BANK OF NEW YORK 2013 ANNUAL REPORT LETTER FROM THE PRESIDENT The year 2013 marked the centennial of the Federal Reserve System. During the year, the Federal

Letter from the President 1 FEDERAL RESERVE BANK OF NEW YORK 2013 ANNUAL REPORT LETTER FROM THE PRESIDENT The year 2013 marked the centennial of the Federal Reserve System. During the year, the Federal

Richard Rosen Federal Reserve Bank of Chicago

Richard Rosen Federal Reserve Bank of Chicago The views expressed here are my own and may not represent those of the Federal Reserve Bank of Chicago or the Federal Reserve System. Why was this crisis different

Richard Rosen Federal Reserve Bank of Chicago The views expressed here are my own and may not represent those of the Federal Reserve Bank of Chicago or the Federal Reserve System. Why was this crisis different

Prof Kevin Davis Melbourne Centre for Financial Studies. Managing Liquidity Risks. Session 5.1. Training Program ~ 8 12 December 2008 SHANGHAI, CHINA

Enhancing Risk Management and Governance in the Region s Banking System to Implement Basel II and to Meet Contemporary Risks and Challenges Arising from the Global Banking System Training Program ~ 8 12

Enhancing Risk Management and Governance in the Region s Banking System to Implement Basel II and to Meet Contemporary Risks and Challenges Arising from the Global Banking System Training Program ~ 8 12

The U.S. Financial Crisis: Lessons From Sweden

Order Code RS22962 September 29, 2008 The U.S. Financial Crisis: Lessons From Sweden Summary James K. Jackson Specialist in International Trade and Finance Foreign Affairs, Defense, and Trade Division

Order Code RS22962 September 29, 2008 The U.S. Financial Crisis: Lessons From Sweden Summary James K. Jackson Specialist in International Trade and Finance Foreign Affairs, Defense, and Trade Division

Leverage OTC Clearing & Interdealer Risk Management

OTC Clearing, Volcker Rule and Transaction Strategy: Changing market dynamics & liquidity for Corporate Treasurers Presented by Larry Tabb (Founder & CEO) PRMIA Global Risk Conference New York, NY May

OTC Clearing, Volcker Rule and Transaction Strategy: Changing market dynamics & liquidity for Corporate Treasurers Presented by Larry Tabb (Founder & CEO) PRMIA Global Risk Conference New York, NY May

Money: Definition. Money: Functions. Money: Types 2/13/2014. ECON 3010 Intermediate Macroeconomics

Money: Definition ECON 3010 Intermediate Macroeconomics Chapter 4 The Monetary System: What It Is and How It Works Money is the stock of assets that can be readily used to make transactions. Money: Functions

Money: Definition ECON 3010 Intermediate Macroeconomics Chapter 4 The Monetary System: What It Is and How It Works Money is the stock of assets that can be readily used to make transactions. Money: Functions

The Ratio of Leverage. When you combine ignorance and leverage, you get some pretty interesting results. Warren Buffett

The Ratio of Leverage When you combine ignorance and leverage, you get some pretty interesting results. Warren Buffett 1 What is leverage? definition of leverage: debt to equity ratio Basel Commitee: One

The Ratio of Leverage When you combine ignorance and leverage, you get some pretty interesting results. Warren Buffett 1 What is leverage? definition of leverage: debt to equity ratio Basel Commitee: One

The Debt Challenge in Europe. Alan Ahearne and Guntram Wolff October 2011

The Debt Challenge in Europe Alan Ahearne and Guntram Wolff October 2011 Outline The challenge: debt overhang and price adjustment. Large increase in private debt prior to the crisis. Balance-sheet adjustments

The Debt Challenge in Europe Alan Ahearne and Guntram Wolff October 2011 Outline The challenge: debt overhang and price adjustment. Large increase in private debt prior to the crisis. Balance-sheet adjustments

Basel Committee on Banking Supervision. Frequently Asked Questions on Basel III s January 2013 Liquidity Coverage Ratio framework

Basel Committee on Banking Supervision Frequently Asked Questions on Basel III s January 2013 Liquidity Coverage Ratio framework April 2014 This publication is available on the BIS website (www.bis.org).

Basel Committee on Banking Supervision Frequently Asked Questions on Basel III s January 2013 Liquidity Coverage Ratio framework April 2014 This publication is available on the BIS website (www.bis.org).

Minsky, Financial Governance, Banking, and Financial Instability in Brazil

Minsky, Financial Governance, Banking, and Financial Instability in Brazil FELIPE REZENDE, PH.D., Research Scholar, NY, USA Remarks Prepared For The Conference: Financial Governance After The Crisis cosponsored

Minsky, Financial Governance, Banking, and Financial Instability in Brazil FELIPE REZENDE, PH.D., Research Scholar, NY, USA Remarks Prepared For The Conference: Financial Governance After The Crisis cosponsored

Regulating Shadow Banking. Patrick Bolton Columbia University

Regulating Shadow Banking Patrick Bolton Columbia University Outline 1. Maturity Mismatch & Financial Crises: a classic story Low interest rates and lax monetary policy Real estate boom 2. New twist in

Regulating Shadow Banking Patrick Bolton Columbia University Outline 1. Maturity Mismatch & Financial Crises: a classic story Low interest rates and lax monetary policy Real estate boom 2. New twist in

Zurich, 13 December 2007. Introductory remarks by Philipp Hildebrand

abcdefg News conference Zurich, 13 December 2007 Introductory remarks by Philipp Hildebrand Six months ago, when our Financial Stability Report was published, I stated that "the global financial system

abcdefg News conference Zurich, 13 December 2007 Introductory remarks by Philipp Hildebrand Six months ago, when our Financial Stability Report was published, I stated that "the global financial system

Convention Seychelles Interbank Foreign Exchange Market (SIFXM)

") Convention Seychelles Interbank Foreign Exchange Market (SIFXM) A. The Market The Central Bank of Seychelles (CBS) is developing an interbank market for the trading of foreign exchange as part of its ongoing

Convention Seychelles Interbank Foreign Exchange Market (SIFXM) A. The Market The Central Bank of Seychelles (CBS) is developing an interbank market for the trading of foreign exchange as part of its ongoing

1 October 2015. Statement of Policy Governing the Acquisition and Management of Financial Assets for the Bank of Canada s Balance Sheet

1 October 2015 Statement of Policy Governing the Acquisition and Management of Financial Assets for the Bank of Canada s Balance Sheet Table of Contents 1. Purpose of Policy 2. Objectives of Holding Financial

1 October 2015 Statement of Policy Governing the Acquisition and Management of Financial Assets for the Bank of Canada s Balance Sheet Table of Contents 1. Purpose of Policy 2. Objectives of Holding Financial

Economic Outlook 2009/2010

Economic Outlook 29/21 s Twenty-Eighth Annual Forecast Luncheon Paul R. Portney Dean, Professor of Economics, and Halle Chair in Leadership Marshall J. Vest Director Economic and Business Research Center

Economic Outlook 29/21 s Twenty-Eighth Annual Forecast Luncheon Paul R. Portney Dean, Professor of Economics, and Halle Chair in Leadership Marshall J. Vest Director Economic and Business Research Center

Development of the Client-Focused, Capital-Efficient Business Model

Development of the Client-Focused, Capital-Efficient Business Model David Mathers, Chief Operating Officer, Investment Bank at the Goldman Sachs European Financials Conference, Madrid, June 10, 2010 Cautionary

Development of the Client-Focused, Capital-Efficient Business Model David Mathers, Chief Operating Officer, Investment Bank at the Goldman Sachs European Financials Conference, Madrid, June 10, 2010 Cautionary

Assessing the Risks of Mortgage REITs. By Sabrina R. Pellerin, David A. Price, Steven J. Sabol, and John R. Walter

Economic Brief November 2013, EB13-11 Assessing the Risks of Mortgage REITs By Sabrina R. Pellerin, David A. Price, Steven J. Sabol, and John R. Walter Regulators have expressed concern about the growth

Economic Brief November 2013, EB13-11 Assessing the Risks of Mortgage REITs By Sabrina R. Pellerin, David A. Price, Steven J. Sabol, and John R. Walter Regulators have expressed concern about the growth

Jane D Arista, Political Economy Research Institute (PERI) ECONOMISTS' COMMITTEE FOR STABLE, ACCOUNTABLE, FAIR AND EFFICIENT FINANCIAL REFORM

ECONOMISTS' COMMITTEE FOR STABLE, ACCOUNTABLE, FAIR AND EFFICIENT FINANCIAL REFORM") policy brief #1 Leverage, Proprietary Trading and Funding Activities Jane D Arista, Political Economy Research Institute (PERI) October 7, 2009 SAFER A PROJECT OF THE POLITICAL ECONOMY RESEARCH INSTITUTE

policy brief #1 Leverage, Proprietary Trading and Funding Activities Jane D Arista, Political Economy Research Institute (PERI) October 7, 2009 SAFER A PROJECT OF THE POLITICAL ECONOMY RESEARCH INSTITUTE

Market Linked Certificates of Deposit

Market Linked Certificates of Deposit This material was prepared by Wells Fargo Securities, LLC, a registered brokerdealer and separate non-bank affiliate of Wells Fargo & Company. This material is not

Market Linked Certificates of Deposit This material was prepared by Wells Fargo Securities, LLC, a registered brokerdealer and separate non-bank affiliate of Wells Fargo & Company. This material is not

The Global Credit Crisis: Implications for Systemic Risk. Raghuram G. Rajan University of Chicago and NBER

The Global Credit Crisis: Implications for Systemic Risk Identification and Monitoring Raghuram G. Rajan University of Chicago and NBER What caused the crisis? Inadequate global demand. Chronically surplus

The Global Credit Crisis: Implications for Systemic Risk Identification and Monitoring Raghuram G. Rajan University of Chicago and NBER What caused the crisis? Inadequate global demand. Chronically surplus

Malayan Banking Berhad, New York Branch Resolution Plan

Malayan Banking Berhad, New York Branch Resolution Plan Section 1: PUBLIC SECTION December 2013 Humanizing Banking Services Introduction Malayan Banking Berhad, New York ( MBBNY ) is pleased to present

Malayan Banking Berhad, New York Branch Resolution Plan Section 1: PUBLIC SECTION December 2013 Humanizing Banking Services Introduction Malayan Banking Berhad, New York ( MBBNY ) is pleased to present

The History of Crisis. Background Information: The Financial Crisis and Fair Value

The History of Crisis What is going on? Privatisation of money supply Financialisation: commodification of money and debt (linked to accounting) Deregulated global flow of capital (but not labour) (linked

The History of Crisis What is going on? Privatisation of money supply Financialisation: commodification of money and debt (linked to accounting) Deregulated global flow of capital (but not labour) (linked

Sixteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington D.C., December 1 5, 2003

BOPCOM-03/13 Sixteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington D.C., December 1 5, 2003 Developments in Market Clearing and Settlement Arrangements: Some Balance Sheet

BOPCOM-03/13 Sixteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington D.C., December 1 5, 2003 Developments in Market Clearing and Settlement Arrangements: Some Balance Sheet

Time Matters: Capital Markets. Peter Diamond November 9 2011

Time Matters: Capital Markets Peter Diamond November 9 2011 Bank Regulation Old Monetary policy Inflation, unemployment Safety and soundness of banks Microprudential regulation Deposit insurance Consumer

Time Matters: Capital Markets Peter Diamond November 9 2011 Bank Regulation Old Monetary policy Inflation, unemployment Safety and soundness of banks Microprudential regulation Deposit insurance Consumer

Money and Capital in an OLG Model

Money and Capital in an OLG Model D. Andolfatto June 2011 Environment Time is discrete and the horizon is infinite ( =1 2 ) At the beginning of time, there is an initial old population that lives (participates)

Money and Capital in an OLG Model D. Andolfatto June 2011 Environment Time is discrete and the horizon is infinite ( =1 2 ) At the beginning of time, there is an initial old population that lives (participates)

Notes on the Feasibility and Impact of a general Financial Transactions Tax. Civil society consultation with the IMF on 28 January 2010

Notes on the Feasibility and Impact of a general Financial Transactions Tax Civil society consultation with the IMF on 28 January 2010 Rodney Schmidt Principal Researcher The North-South Institute rschmidt@nsi-ins.ca

Notes on the Feasibility and Impact of a general Financial Transactions Tax Civil society consultation with the IMF on 28 January 2010 Rodney Schmidt Principal Researcher The North-South Institute rschmidt@nsi-ins.ca

Introduction to Fixed Income (IFI) Course Syllabus

Course Syllabus") Introduction to Fixed Income (IFI) Course Syllabus 1. Fixed income markets 1.1 Understand the function of fixed income markets 1.2 Know the main fixed income market products: Loans Bonds Money market instruments

Introduction to Fixed Income (IFI) Course Syllabus 1. Fixed income markets 1.1 Understand the function of fixed income markets 1.2 Know the main fixed income market products: Loans Bonds Money market instruments

Cash Flow Forecasting and Cash Balance Management DPI 10

Cash Flow Forecasting and Cash Balance Management DPI 10 Cash forecasting and cash management - Background 1 What is cash management? The strategy and associated processes for managing cost-effective the

Cash Flow Forecasting and Cash Balance Management DPI 10 Cash forecasting and cash management - Background 1 What is cash management? The strategy and associated processes for managing cost-effective the

Verðtryggð Lán. Dr. Jacky Mallett jacky@iiim.is

Verðtryggð Lán Dr. Jacky Mallett jacky@iiim.is Mortgage Lending Rates in 2012 Iceland 9%+ 4% + Inflation rate on principal, 25-40 years Structured as negative amortization loans United States ~4.5% Fixed

Verðtryggð Lán Dr. Jacky Mallett jacky@iiim.is Mortgage Lending Rates in 2012 Iceland 9%+ 4% + Inflation rate on principal, 25-40 years Structured as negative amortization loans United States ~4.5% Fixed

The Relationship between Capital, Liquidity and Risk in Commercial Banks. by Tamara Kochubey and Dorota Kowalczyk. Comments by Ricardo Lago

The Relationship between Capital, Liquidity and Risk in Commercial Banks by Tamara Kochubey and Dorota Kowalczyk Comments by Ricardo Lago I- Motivation and Method U.S. commercial banks : decision making

The Relationship between Capital, Liquidity and Risk in Commercial Banks by Tamara Kochubey and Dorota Kowalczyk Comments by Ricardo Lago I- Motivation and Method U.S. commercial banks : decision making

FIN 684 Fixed-Income Analysis From Repos to Monetary Policy. Funding Positions

FIN 684 Fixed-Income Analysis From Repos to Monetary Policy Professor Robert B.H. Hauswald Kogod School of Business, AU Funding Positions Short-term funding: repos and money markets funding trading positions

FIN 684 Fixed-Income Analysis From Repos to Monetary Policy Professor Robert B.H. Hauswald Kogod School of Business, AU Funding Positions Short-term funding: repos and money markets funding trading positions

The Case for a Custom Fixed Income Benchmark. ssga.com/definedcontribution REFINING THE AGG

The Case for a Custom Fixed Income Benchmark ssga.com/definedcontribution REFINING THE AGG For decades, the Barclays US Aggregate Index (the Agg ) has been a popular benchmark for core bond investment

The Case for a Custom Fixed Income Benchmark ssga.com/definedcontribution REFINING THE AGG For decades, the Barclays US Aggregate Index (the Agg ) has been a popular benchmark for core bond investment

Seminar. Global Foreign Exchange Markets Chapter 9. Copyright 2013 Pearson Education. 20 Kasım 13 Çarşamba

Seminar Global Foreign Exchange Markets Chapter 9 9- Learning Objectives To learn the fundamentals of foreign exchange To identify the major characteristics of the foreign-exchange market and how governments

Seminar Global Foreign Exchange Markets Chapter 9 9- Learning Objectives To learn the fundamentals of foreign exchange To identify the major characteristics of the foreign-exchange market and how governments

CALVERT UNCONSTRAINED BOND FUND A More Expansive Approach to Fixed-Income Investing

CALVERT UNCONSTRAINED BOND FUND A More Expansive Approach to Fixed-Income Investing A Challenging Environment for Investors MOVING BEYOND TRADITIONAL FIXED-INCOME INVESTING ALONE For many advisors and

CALVERT UNCONSTRAINED BOND FUND A More Expansive Approach to Fixed-Income Investing A Challenging Environment for Investors MOVING BEYOND TRADITIONAL FIXED-INCOME INVESTING ALONE For many advisors and

Chapter 16: Financial Risk Management

Chapter 16: Financial Risk Management Introduction Overview of Financial Risk Management in Treasury Interest Rate Risk Foreign Exchange (FX) Risk Commodity Price Risk Managing Financial Risk The Benefits

Chapter 16: Financial Risk Management Introduction Overview of Financial Risk Management in Treasury Interest Rate Risk Foreign Exchange (FX) Risk Commodity Price Risk Managing Financial Risk The Benefits

Lecture 10-1. The Twin Deficits

Lecture 10-1 The Twin Deficits The IS-LM model of the previous lectures endogenised the interest rate while assuming that the portion (NX 0 ) of net exports not dependent on income was exogenously fixed.

Lecture 10-1 The Twin Deficits The IS-LM model of the previous lectures endogenised the interest rate while assuming that the portion (NX 0 ) of net exports not dependent on income was exogenously fixed.

BNP Paribas Official Institutions Programme of events 2015I 1. WELCOME to the BNP Paribas Official Institutions Training and Conference agenda

BNP Paribas Official Institutions Programme of events 2015I 1 WELCOME to the BNP Paribas Official Institutions Training and Conference agenda 2015 BNP Paribas Official Institutions Programme of events

BNP Paribas Official Institutions Programme of events 2015I 1 WELCOME to the BNP Paribas Official Institutions Training and Conference agenda 2015 BNP Paribas Official Institutions Programme of events

Clearing and settlement of exchange traded derivatives

Clearing and settlement of exchange traded derivatives by John W. McPartland, consultant, Financial Markets Group Derivatives are a class of financial instruments that derive their value from some underlying

Clearing and settlement of exchange traded derivatives by John W. McPartland, consultant, Financial Markets Group Derivatives are a class of financial instruments that derive their value from some underlying

China s Economic Reforms and Growth Prospects. Nicholas Lardy. Anthony M Solomon Senior Fellow. Peterson Institute for International Economics

China s Economic Reforms and Growth Prospects Nicholas Lardy Anthony M Solomon Senior Fellow Peterson Institute for International Economics Paper Prepared for the CF-40 PIIE 2014 Conference Beijing May

China s Economic Reforms and Growth Prospects Nicholas Lardy Anthony M Solomon Senior Fellow Peterson Institute for International Economics Paper Prepared for the CF-40 PIIE 2014 Conference Beijing May

Keynote Speech, EIB/IMF Meeting, 23 October, Brussels

Keynote Speech, EIB/IMF Meeting, 23 October, Brussels Governor Carlos Costa Six years since the onset of the financial crisis in 2008, output levels in the EU are below those observed before the crisis.

Keynote Speech, EIB/IMF Meeting, 23 October, Brussels Governor Carlos Costa Six years since the onset of the financial crisis in 2008, output levels in the EU are below those observed before the crisis.

Managing liquidity in a post crisis world

Managing liquidity in a post crisis world Goldman Sachs European Financials Conference Money market current environment and expected development Market observation Euribor-Eonia Spread Credit spreads /

Managing liquidity in a post crisis world Goldman Sachs European Financials Conference Money market current environment and expected development Market observation Euribor-Eonia Spread Credit spreads /

RISK DISCLOSURE STATEMENT

RISK DISCLOSURE STATEMENT You should note that there are significant risks inherent in investing in certain financial instruments and in certain markets. Investment in derivatives, futures, options and

RISK DISCLOSURE STATEMENT You should note that there are significant risks inherent in investing in certain financial instruments and in certain markets. Investment in derivatives, futures, options and

8. Eurodollars: Parallel Settlement

8. Eurodollars: Parallel Settlement Eurodollars are dollar balances held by banks or bank branches outside the country, which banks hold no reserves at the Fed and consequently have no direct access to

8. Eurodollars: Parallel Settlement Eurodollars are dollar balances held by banks or bank branches outside the country, which banks hold no reserves at the Fed and consequently have no direct access to

How To Be Cheerful About 2012

2012: Deeper into crisis or the long road to recovery? Bart Van Craeynest Hoofdeconoom Petercam Bart.vancraeynest@petercam.be 1 2012: crises looking for answers Global slowdown No 2008-0909 rerun Crises

2012: Deeper into crisis or the long road to recovery? Bart Van Craeynest Hoofdeconoom Petercam Bart.vancraeynest@petercam.be 1 2012: crises looking for answers Global slowdown No 2008-0909 rerun Crises

Omgeo Asset Class Coverage

Equity Ownership interest in a corporation in the form of common stock or preferred stock. Common Stock American Depositary Receipts (ADR) Global Depositary Receipts (GDR) Exchange Traded Funds (ETF) As

Equity Ownership interest in a corporation in the form of common stock or preferred stock. Common Stock American Depositary Receipts (ADR) Global Depositary Receipts (GDR) Exchange Traded Funds (ETF) As

Introduction to Health Care Accounting. What Is Financial Management?

Chapter 1 Introduction to Health Care Accounting and Financial Management Do I Really Need to Understand Accounting to Be an Effective Health Care Manager? Today s health care system, with its many types

Chapter 1 Introduction to Health Care Accounting and Financial Management Do I Really Need to Understand Accounting to Be an Effective Health Care Manager? Today s health care system, with its many types

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Study Questions 5 (Money) MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The functions of money are 1) A) medium of exchange, unit of account,

Study Questions 5 (Money) MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The functions of money are 1) A) medium of exchange, unit of account,