Internal Controls and Fraud Detection & Prevention. Harold Monk and Jennifer Christensen

|

|

|

- Diana King

- 10 years ago

- Views:

Transcription

1 Internal Controls and Fraud Detection & Prevention Harold Monk and Jennifer Christensen 1

2 Common Fraud Statements Everyone in government has an honest and charitable heart. It may happen other places, but not here. Our employees have been here forever! There is no way they would steal. We trust them, and anyway, we would have found it by now. We are just a small department with only a few employees. We can t really have controls set up to prevent and detect fraud. 2

3 Data From the ACFE The following slides are from the Association of Certified Fraud Examiners Report to the Nation 2014 (Used With Permission) 3

4 Initial Detection of Occupational Frauds 4

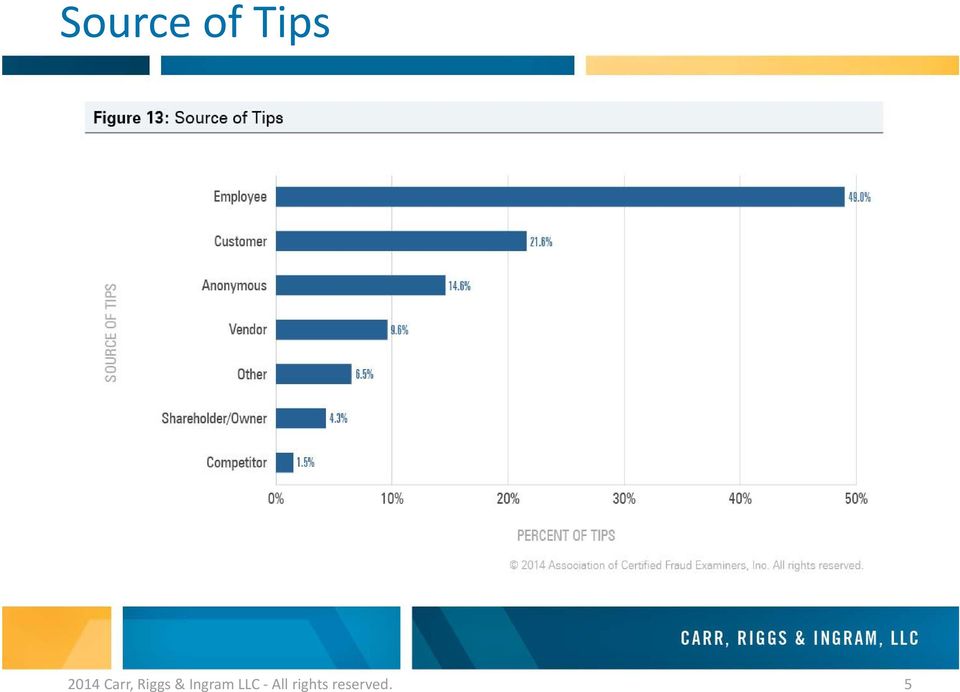

5 Source of Tips 5

6 Impact of Hotlines 6

7 Type of Victim Organization 7

8 Type of Victim Organization 8

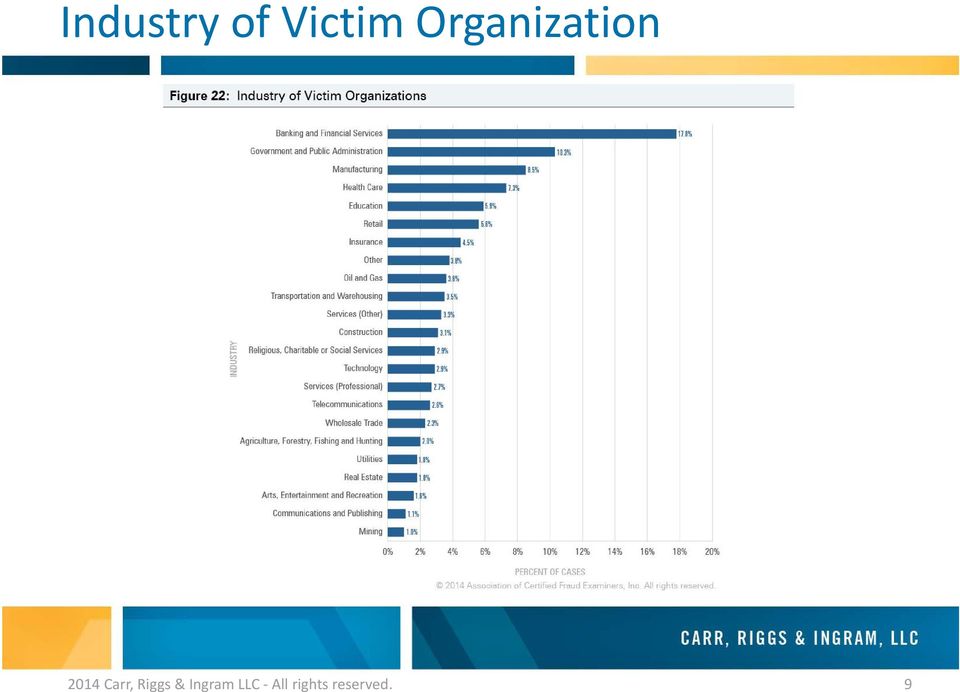

9 Industry of Victim Organization 9

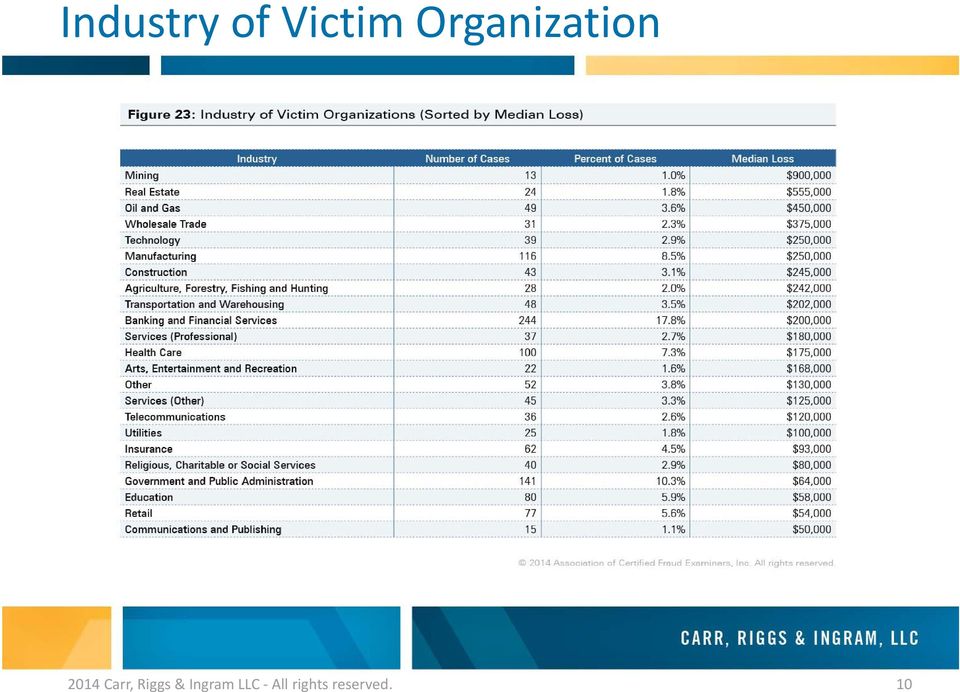

10 Industry of Victim Organization 10

11 Anti Fraud Controls by Region 11

12 Control Weaknesses That Contributed to Fraud 12

13 Perpetrator s Age 13

14 Perpetrator s Age 14

15 Behavioral Red Flags Displayed by Perpetrators 15

16 Types of Government Fraud Skimming Funds are diverted before they are ever recorded in the books. Purchase Card Abuse Use of organization issued cards for personal use or misuse of credit card and identity information. Fictitious Vendors Perpetrators set up a company and submit fake/altered invoices for payments. Conflicts of Interest School Board or upper level management have financial interest from or with vendors. Payroll Fictitious employees, continued payment of terminated employees, fraudulent timekeeping. 16

17 Examples of Fraud Internal Accounts Cash vs. checks received consider check log or breaking out cash and checks on deposit records Signature stamps used on checks send unopened bank statements to principal to review check payees and amounts Fundraisers held and not deposited hard to discover Tickets sales inventory ticket series, control acquisition of ticket rolls, require two people to sell tickets 17

18 Examples of Fraud Budget Accounts Cafeteria food inventory or sales likely small amounts, perform analytics such as cost per sales Capital asset misappropriation or personal use perform physical observation, keep secure, include policy on personal use, track certain high risk assets below capitalization threshold (Note new OMB requirement for computing devices being classified as supplies) 18

19 Examples of Fraud Budget Accounts Construction costs monitoring costs and performance against contract Grants new OMB Super Circular to streamline process and reduce waste and fraud, recipient may be held more accountable. 19

20 What Happens to Fraudsters? 51% are Prosecuted 98% Prosecuted are Convicted 31% of Those Convicted Are Sent to Jail 72% Sent to Jail Go For More Than 1 Year SO HOW MANY IDENTIFIED PERPETRATORS SPEND MORE THAN 1 YEAR IN JAIL? 20

21 More Than 1 Year in Jail 11% 21

22 Fraud Prevention Intellectuals solve problems. Geniuses prevent them. Albert Einstein 22

23 ACFE Statistics Approximately 40% of fraud cases are due to a simple lack of internal controls. Following a fraud, approximately 80% of organizations modify internal controls. People account for more than 60% of fraud perpetrators. Approximately 90% of perpetrators have been on the job at least one year. 50% have been for six or more years. More than 85% have never been charged/convicted of fraud. More than 82% have never been punished or terminated during their employment. 23

24 Results of Fraud Financial loss Additional costs of investigation and possibly prosecution Time spent on insurance claims and investigations, and possibly prosecution Negative publicity 24

25 Fraud Triangle 25

26 Key Fraudster Characteristics Tenured Trusted Trusted Educated Least Suspected Fraudsters do not look like crooks! 26

27 Components of Internal Control COSO Report 2013 Control Environment Risk Assessment Control Activities Communication Monitoring 27

28 Components of Internal Control COSO Report 2013 Control Environment tone at the top Integrity and ethical values standard code of conduct School Board need to demonstrate independence and oversight Accountability what happens when rules are broken? 28

29 Components of Internal Control COSO Report 2013 Risk Assessment Specifying suitable objectives Identifying risks Risk analysis to determine how to manage risks 29

30 Components of Internal Control COSO Report 2013 Control Activities actions established through policies and procedures to help ensure that management directives to mitigate risks to the achievement of objectives are carried out Policies to establish what should be done Procedures that implement the policy 30

31 Components of Internal Control COSO Report 2013 Communication Internal communications communications with School Board, employees, offering a whistleblower hotline External communications communications with public, vendors, regulators, offering a whistleblower hotline 31

32 Components of Internal Control COSO Report 2013 Monitoring Evaluate internal controls Evaluate internal control deficiencies 32

33 IT Controls Understand the significance of applications to financial reporting or to safeguarding assets Factors to consider when analyzing complexity/risks: Number of users Number of interfaces with other applications Length of time in service On mainframe, server, or in cloud/web based Necessary to include in disaster plan 33

34 Limitations of Internal Control COSO Report 2013 Judgment Breakdowns Management override Collusion Cost vs. Benefits 34

35 Fraud Prevention Prevention Techniques Deterrence Techniques Detection Techniques 35

36 Top 10 Fraud Prevention Actions Partner with employees to create an anti fraud culture. Know employees beyond technical skills. Train team to be aware of signs of fraud and recognize fraudulent activities. Create an easy and comfortable method for employees to report suspicious activities or observations. 36

37 Top 10 Fraud Prevention Actions Implement an anti fraud program and increase the perception of being caught. Begin with a formal fraud policy. Find one or more controls to increase perception of detection. Closely monitor the policy and diligently seek compliance. Respond appropriately to any discovered fraud. Use reliable access controls, such as strong passwords, which increase traceability of actions. 37

38 Top 10 Fraud Prevention Actions Become involved in the financials with a focus on anomalies. Compare financial statements against the budget and investigate unexpected variances. Review bank statements, ledgers, and journals on a regular basis and look for unusual items. Open and read financial mail. Understand line items on your financial statement. 38

39 Top 10 Fraud Prevention Actions Be careful with checks, which are essentially cash. Sign your own checks and avoid signature stamps. Check for altered payees and amounts. Periodically compare cancelled checks to invoices. Review the front and back of cancelled checks with each bank statement. 39

40 Top 10 Fraud Prevention Actions Establish policies for credit purchases. Implement credit purchase contracts for employees outlining utilization responsibilities and rules. Restrict accounts with spending limits and merchant accounting codes. 40

41 Top 10 Fraud Prevention Actions Pay attention to signs of a fraud. Recognize it can occur within your business. Observe sudden and unusual lifestyle changes of key employees. Pay attention to abrupt changes in financial losses, ratios, and performance. Use an internal audit function as part of the anti fraud program. 41

42 Top 10 Fraud Prevention Actions Assess anti fraud controls and improve them. Learn the most effective anti fraud controls. Apply these professional recommendations and encourage employees to identify additional opportunities. Accountability for key personnel, coupled with employee involvement, decrease the opportunity for fraudulent activity. 42

43 Top 10 Fraud Prevention Actions Assess anti fraud controls and improve them. Prevention examples: Segregation or rotation of duties Credit card policies and procedures Dual signatures required Access controls for computers Background checks for key hires 43

44 Top 10 Fraud Prevention Actions Assess anti fraud controls and improve them. Detection examples: Effective Tips and complaints system and/or whistleblower system Management review (journals, bank records, etc.) Internal/Fraud audits External audits 44

45 Top 10 Fraud Prevention Actions Understand the profile of a fraudster. Fraudster is often tenured. Holds a key position along the cash trail. Usually educated, trustworthy, and often with a great personality. 45

46 Top 10 Fraud Prevention Actions Implement an effectual anonymous tips and complaints system. Establish an independent, easy system for reporting tips and complaints regarding possible fraud. Allow employees, vendors, and customers to report suspicions. Regularly promote the system. 46

47 Top 10 Fraud Prevention Actions Request a professional fraud assessment. Your auditors are trained to identify weaknesses in internal controls related to fraud prevention and detection. Basic checks and balances may often be implemented with a minimal cost. Consider a regular fraud audit or fraud review about every 3 years or less if an internal audit function is not present. 47

48 48

49 Harold Monk Jennifer Christensen 49

Steven Boyer Vice-President, Gallagher Bassett Services Inc.

Employee Dishonesty and Fraud Motive, Rationale & Opportunity Steven Boyer Vice-President, Gallagher Bassett Services Inc. Randall Wilson, CPA/CFF, CFE, Cr.FA Partner, National Practice Director Fraud

Employee Dishonesty and Fraud Motive, Rationale & Opportunity Steven Boyer Vice-President, Gallagher Bassett Services Inc. Randall Wilson, CPA/CFF, CFE, Cr.FA Partner, National Practice Director Fraud

Fraud Awareness Training

UT System Administration General Compliance Training Fall 2014 This training will take approximately 20 minutes to complete Objectives What is occupational fraud Common myths about fraud Conditions for

UT System Administration General Compliance Training Fall 2014 This training will take approximately 20 minutes to complete Objectives What is occupational fraud Common myths about fraud Conditions for

Financial Services Group

Fraud Detection and Prevention Presented by: Carrie Kennedy, CPA, Partner Anthony Porter, CPA, Manager 1 The material appearing in this presentation is for informational purposes only and should not be

Fraud Detection and Prevention Presented by: Carrie Kennedy, CPA, Partner Anthony Porter, CPA, Manager 1 The material appearing in this presentation is for informational purposes only and should not be

FRAUD PREVENTION STRATEGIES FOR HEALTH CARE A FORENSIC ACCOUNTANT S PERSPECTIVE

FRAUD PREVENTION STRATEGIES FOR HEALTH CARE A FORENSIC ACCOUNTANT S PERSPECTIVE CPAs & ADVISORS experience reach // S. Todd Burchett, CPA, ABV, ASA, CFF, CFE Partner [email protected] 210.268.1932 AGENDA

FRAUD PREVENTION STRATEGIES FOR HEALTH CARE A FORENSIC ACCOUNTANT S PERSPECTIVE CPAs & ADVISORS experience reach // S. Todd Burchett, CPA, ABV, ASA, CFF, CFE Partner [email protected] 210.268.1932 AGENDA

Avoiding Theft in Your Nonprofit Ohio Attorney General Mike DeWine

Avoiding Theft in Your Nonprofit Ohio Attorney General Mike DeWine 1 Dear Nonprofit Leader, The single greatest asset of a nonprofit is arguably its reputation. When theft or misappropriation of assets

Avoiding Theft in Your Nonprofit Ohio Attorney General Mike DeWine 1 Dear Nonprofit Leader, The single greatest asset of a nonprofit is arguably its reputation. When theft or misappropriation of assets

Fraud Prevention and Deterrence

Fraud Prevention and Deterrence Fraud Risk Assessment 2016 Association of Certified Fraud Examiners, Inc. What Is Fraud Risk? The vulnerability that an organization faces from individuals capable of combining

Fraud Prevention and Deterrence Fraud Risk Assessment 2016 Association of Certified Fraud Examiners, Inc. What Is Fraud Risk? The vulnerability that an organization faces from individuals capable of combining

5 Important Controls to Mitigate Employee Fraud

5 Important Controls to Mitigate Employee Fraud LMCIT WEBINAR : FEBRUARY 10, 2015 IN PARTNERSHIP WITH EIDE BAILLY Presenter: Jason Olson, MBA, CPA/CFF, CFE, CFI Presentation Disclaimer These seminar materials

5 Important Controls to Mitigate Employee Fraud LMCIT WEBINAR : FEBRUARY 10, 2015 IN PARTNERSHIP WITH EIDE BAILLY Presenter: Jason Olson, MBA, CPA/CFF, CFE, CFI Presentation Disclaimer These seminar materials

September 28, 2011. Audit s Role in Governance, Risk Management and Internal Control

September 28, 2011 Internal Audit Overview Audit s Role in Governance, Risk Management and Internal Control Mission Provide independent, objective assurance and advisory services designed to add value

September 28, 2011 Internal Audit Overview Audit s Role in Governance, Risk Management and Internal Control Mission Provide independent, objective assurance and advisory services designed to add value

Office of the Inspector General

Office of the Inspector General Commonwealth of Massachusetts Gregory W. Sullivan Inspector General Guide to Developing and Implementing Fraud Prevention Programs April 2005 Dear Public Officials: April

Office of the Inspector General Commonwealth of Massachusetts Gregory W. Sullivan Inspector General Guide to Developing and Implementing Fraud Prevention Programs April 2005 Dear Public Officials: April

RED FLAGS OF FRAUD MAY 13, 2014 IIA AUSTIN CHAPTER

MAY 13, 2014 IIA AUSTIN CHAPTER 2014 by the Association of Certified Fraud Examiners, Inc. Revised: 3/26/14 No portion of this work may be reproduced or transmitted in any form or by any means electronic

MAY 13, 2014 IIA AUSTIN CHAPTER 2014 by the Association of Certified Fraud Examiners, Inc. Revised: 3/26/14 No portion of this work may be reproduced or transmitted in any form or by any means electronic

Sharon Kurek, CPA, CFE Director of Internal Audit

Sharon Kurek, CPA, CFE Director of Internal Audit What You Will Take Aware With You Definition of Internal Auditing Scope of Audit Activities Risk and Control Process Common Audit Topics Fraud Awareness

Sharon Kurek, CPA, CFE Director of Internal Audit What You Will Take Aware With You Definition of Internal Auditing Scope of Audit Activities Risk and Control Process Common Audit Topics Fraud Awareness

Fraud Prevention: The Prevention and Detection of Fraud Begins with You

Fraud Prevention: The Prevention and Detection of Fraud Begins with You Takeaways What is fraud? Definition Facts Four factors Fraud risk assessment Four evaluation criteria Common fraud schemes Case studies

Fraud Prevention: The Prevention and Detection of Fraud Begins with You Takeaways What is fraud? Definition Facts Four factors Fraud risk assessment Four evaluation criteria Common fraud schemes Case studies

Is There Anyway to Prevent Fraud? Bill Gady, CGA CPA Partner

Is There Anyway to Prevent Fraud? Bill Gady, CGA CPA Partner Learning Objectives: Understand how fraud can occur Learn procedures you can implement to prevent fraud Learn how to detect fraud Common Situations

Is There Anyway to Prevent Fraud? Bill Gady, CGA CPA Partner Learning Objectives: Understand how fraud can occur Learn procedures you can implement to prevent fraud Learn how to detect fraud Common Situations

Fraud Control Theory

13 Fraud Control Theory Using a variation of a saying from the 1960s, fraud happens. Like all costs of doing business, fraud must be managed. Management must recognize that people commit fraudulent acts

13 Fraud Control Theory Using a variation of a saying from the 1960s, fraud happens. Like all costs of doing business, fraud must be managed. Management must recognize that people commit fraudulent acts

Making Your Fraud Vision 20 / 20. Thomas R. Strause, CIA, CFE, CBA, CISA, CFSA, CICA Partner FOS tstrause@fosaudit.

Making Your Fraud Vision 20 / 20 Thomas R. Strause, CIA, CFE, CBA, CISA, CFSA, CICA Partner [email protected] 610-603-5603 Topics to be Covered + Summary of Fraud Statistics ACFE 2014 Report + Current

Making Your Fraud Vision 20 / 20 Thomas R. Strause, CIA, CFE, CBA, CISA, CFSA, CICA Partner [email protected] 610-603-5603 Topics to be Covered + Summary of Fraud Statistics ACFE 2014 Report + Current

INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 240 THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS

240 THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS") INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 240 Introduction THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial statements for

INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 240 Introduction THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial statements for

INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS CONTENTS") INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS CONTENTS Paragraphs Introduction... 1-3 Characteristics of Fraud...

INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS CONTENTS Paragraphs Introduction... 1-3 Characteristics of Fraud...

Antifraud program and controls assessment grid*

Advisory Services Antifraud program and * Fraud risks & controls February 2008 *connectedthinking 2008 PricewaterhouseCoopers LLP. All rights reserved. PricewaterhouseCoopers refers to PricewaterhouseCoopers

Advisory Services Antifraud program and * Fraud risks & controls February 2008 *connectedthinking 2008 PricewaterhouseCoopers LLP. All rights reserved. PricewaterhouseCoopers refers to PricewaterhouseCoopers

Fraud Prevention Training

Fraud Prevention Training Kim Turner, Chief Audit Executive Emily Knopp, Audit Director Fraud Prevention: WHAT YOU WILL LEARN & FRAUD FACTS What you will take away with you: Glossary of Fraud Terms Details

Fraud Prevention Training Kim Turner, Chief Audit Executive Emily Knopp, Audit Director Fraud Prevention: WHAT YOU WILL LEARN & FRAUD FACTS What you will take away with you: Glossary of Fraud Terms Details

Fraud and Role of Information Technology. September 2008

Fraud and Role of Information Technology September 2008 Agenda IT Value Proposition Slide 2 Prior Interpretations of Internal Control Structure Have Addressed Three Separate Parts Which Were Audited Somewhat

Fraud and Role of Information Technology September 2008 Agenda IT Value Proposition Slide 2 Prior Interpretations of Internal Control Structure Have Addressed Three Separate Parts Which Were Audited Somewhat

Types of Fraud and Recent Cases. Developing an Effective Anti-fraud Program from the Top Down

Types of and Recent Cases Developing an Effective Anti-fraud Program from the Top Down 1 Types of and Recent Cases Chris Grippa (404-817-5945) FIDS Senior Manager with Ernst & Young LLP Works with clients

Types of and Recent Cases Developing an Effective Anti-fraud Program from the Top Down 1 Types of and Recent Cases Chris Grippa (404-817-5945) FIDS Senior Manager with Ernst & Young LLP Works with clients

Fundamentals of Computer and Internet Fraud WORLD HEADQUARTERS THE GREGOR BUILDING 716 WEST AVE AUSTIN, TX 78701-2727 USA

Fundamentals of Computer and Internet Fraud WORLD HEADQUARTERS THE GREGOR BUILDING 716 WEST AVE AUSTIN, TX 78701-2727 USA II. THE USE OF COMPUTERS IN OCCUPATIONAL FRAUD Occupational fraud refers to the

Fundamentals of Computer and Internet Fraud WORLD HEADQUARTERS THE GREGOR BUILDING 716 WEST AVE AUSTIN, TX 78701-2727 USA II. THE USE OF COMPUTERS IN OCCUPATIONAL FRAUD Occupational fraud refers to the

Fraud: Real Stories, Real People, Real Impact

Fraud: Real Stories, Real People, Real Impact Chris Harper, CPA, MBA Senior Manager Types of Fraud Asset misappropriation Fraudulent financial reporting Identity theft Detection Skills The Fraud Triangle

Fraud: Real Stories, Real People, Real Impact Chris Harper, CPA, MBA Senior Manager Types of Fraud Asset misappropriation Fraudulent financial reporting Identity theft Detection Skills The Fraud Triangle

Accounts Payable Best Practices

Accounts Payable Best Practices Presented by: Eddy Castaneda, CPA, MBA Accounts Payable Best Practices Top Practices AP Top Practices Document your current AP procedures Can identify overlapping work Can

Accounts Payable Best Practices Presented by: Eddy Castaneda, CPA, MBA Accounts Payable Best Practices Top Practices AP Top Practices Document your current AP procedures Can identify overlapping work Can

7/22/2014. From Treadway To the Cube (1987 2014) So, Who is COSO? What Does COSO Do?

So, Who is COSO? What Does COSO Do?") From Treadway To the Cube (1987 2014) National Society of Accountants for Cooperatives (NSAC) CLAconnect.com Instructor: Ron Durkin, CPA/CFF, CFE, CIRA National Principal in Charge Fraud & Misconduct Investigations

From Treadway To the Cube (1987 2014) National Society of Accountants for Cooperatives (NSAC) CLAconnect.com Instructor: Ron Durkin, CPA/CFF, CFE, CIRA National Principal in Charge Fraud & Misconduct Investigations

Employee Embezzlement and Fraud. Defending Against Insider Threats

Employee Embezzlement and Fraud Defending Against Insider Threats Today s Approach An open dialogue and sharing of information regarding a common threat of internal losses. There is no guarantee that any

Employee Embezzlement and Fraud Defending Against Insider Threats Today s Approach An open dialogue and sharing of information regarding a common threat of internal losses. There is no guarantee that any

Proactive Fraud Detection with Data Mining Fear not the computer You play ball with it and it will play ball with you

3/27/2012 Proactive Fraud Detection with Data Mining Fear not the computer You play ball with it and it will play ball with you Executive Summary The time to test fraud controls is before you have a fraud

3/27/2012 Proactive Fraud Detection with Data Mining Fear not the computer You play ball with it and it will play ball with you Executive Summary The time to test fraud controls is before you have a fraud

Fraud Prevention, Detection and Response. Dean Bunch, Ernst & Young Fraud Investigation & Dispute Services

Fraud Prevention, Detection and Response. Dean Bunch, Ernst & Young Fraud Investigation & Dispute Services Agenda Fraud Overview Fraud Prevention Fraud Detection Fraud Response Questions Page 2 Fraud Overview

Fraud Prevention, Detection and Response. Dean Bunch, Ernst & Young Fraud Investigation & Dispute Services Agenda Fraud Overview Fraud Prevention Fraud Detection Fraud Response Questions Page 2 Fraud Overview

The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements

ISA 240 February 2008 International Standard on Auditing The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements INTERNATIONAL STANDARD ON AUDITING 240 The Auditor s Responsibilities

ISA 240 February 2008 International Standard on Auditing The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements INTERNATIONAL STANDARD ON AUDITING 240 The Auditor s Responsibilities

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

INTERNATIONAL STANDARD ON 240 THE AUDITOR S RESPONSIBILITIES RELATING TO (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction

INTERNATIONAL STANDARD ON 240 THE AUDITOR S RESPONSIBILITIES RELATING TO (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction

by: Scott Baranowski, CIA

Community Bank Auditors Group A/P, Procurement and Credit Card Internal Controls June 4, 2014 by: Scott Baranowski, CIA MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2013 Wolf

Community Bank Auditors Group A/P, Procurement and Credit Card Internal Controls June 4, 2014 by: Scott Baranowski, CIA MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2013 Wolf

716 West Ave Austin, TX 78701-2727 USA

Fundamentals of Computer and Internet Fraud GLOBAL Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA II. THE USE OF COMPUTERS IN OCCUPATIONAL FRAUD Occupational fraud refers to the

Fundamentals of Computer and Internet Fraud GLOBAL Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA II. THE USE OF COMPUTERS IN OCCUPATIONAL FRAUD Occupational fraud refers to the

1/17/2013 FRAUD RISK MANAGEMENT PROGRAM SESSION OBJECTIVE AND OUTLINE

FRAUD RISK MANAGEMENT PROGRAM SHERYL VACCA SENIOR VICE PRESIDENT AND CHIEF COMPLIANCE AND AUDIT OFFICER MIKE JENSON UCR AUDIT DIRECTOR SESSION OBJECTIVE AND OUTLINE Assist campus managers in the development

FRAUD RISK MANAGEMENT PROGRAM SHERYL VACCA SENIOR VICE PRESIDENT AND CHIEF COMPLIANCE AND AUDIT OFFICER MIKE JENSON UCR AUDIT DIRECTOR SESSION OBJECTIVE AND OUTLINE Assist campus managers in the development

AGA Kansas City Chapter Data Analytics & Continuous Monitoring

AGA Kansas City Chapter Data Analytics & Continuous Monitoring Agenda Market Overview & Drivers for Change Key challenges that organizations face Data Analytics What is data analytics and how can it help

AGA Kansas City Chapter Data Analytics & Continuous Monitoring Agenda Market Overview & Drivers for Change Key challenges that organizations face Data Analytics What is data analytics and how can it help

Fraud and internal controls, Part 3: Internal fraud schemes

Fraud and internal controls, Part 3: Internal fraud schemes By EVERETT COLBY, CFE, FCGA This is the third and final article in a series by Mr. Colby on Fraud and internal controls to be carried on PD Net.

Fraud and internal controls, Part 3: Internal fraud schemes By EVERETT COLBY, CFE, FCGA This is the third and final article in a series by Mr. Colby on Fraud and internal controls to be carried on PD Net.

MEMORANDUM INTERNAL CONTROL REQUIREMENTS FOR NON-PROFITS

DIVISION OF CHILD CARE AND EARLY CHILDHOOD EDUCATION HEALTH AND NUTRITION UNIT P O BOX 1437, SLOT S 155 501-320-8982 FAX: 501-682-2334 TDD: 501-682-1550 TO: NON-PROFIT INSTITUTIONS FROM: HEALTH AND NUTRITION

DIVISION OF CHILD CARE AND EARLY CHILDHOOD EDUCATION HEALTH AND NUTRITION UNIT P O BOX 1437, SLOT S 155 501-320-8982 FAX: 501-682-2334 TDD: 501-682-1550 TO: NON-PROFIT INSTITUTIONS FROM: HEALTH AND NUTRITION

How To Prevent Fraud On A Credit Card

Fraud Detection and Prevention Financial Management Advisory Council August 28, 2014 Sarah Mahugh, CPA, MBA Financial Audit Audit Manager Overview Fraud trends Fraud Risks and internal controls Case Studies

Fraud Detection and Prevention Financial Management Advisory Council August 28, 2014 Sarah Mahugh, CPA, MBA Financial Audit Audit Manager Overview Fraud trends Fraud Risks and internal controls Case Studies

Tips to Prevent and Detect Workplace Fraud

40 Tips to Prevent and Detect Workplace Fraud an E-book developed for you by: Table of Contents preventive controls detective controls 1. culture of ethics 2. free of moral hazards 3. risk management policy

40 Tips to Prevent and Detect Workplace Fraud an E-book developed for you by: Table of Contents preventive controls detective controls 1. culture of ethics 2. free of moral hazards 3. risk management policy

INTRODUCTION TO FRAUD EXAMINATION

INTRODUCTION TO FRAUD EXAMINATION GLOBAL HEADQUARTERS THE GREGOR BUILDING 716 WEST AVE AUSTIN, TX 78701-2727 USA VII. FRAUDULENT FINANCIAL TRANSACTIONS: FRAUD SCHEMES Introduction Fraud can be committed

INTRODUCTION TO FRAUD EXAMINATION GLOBAL HEADQUARTERS THE GREGOR BUILDING 716 WEST AVE AUSTIN, TX 78701-2727 USA VII. FRAUDULENT FINANCIAL TRANSACTIONS: FRAUD SCHEMES Introduction Fraud can be committed

ACE elite fraudprotector

ACE elite fraudprotector Commercial Crime Insurance Policy ACE elite fraudprotector Insurance Policy (ed. AU 09/10) It wouldn t happen to us ACE elite fraudprotector Insurance Policy Fraud is a major threat

ACE elite fraudprotector Commercial Crime Insurance Policy ACE elite fraudprotector Insurance Policy (ed. AU 09/10) It wouldn t happen to us ACE elite fraudprotector Insurance Policy Fraud is a major threat

Fraud Risk Management Procedures

Fraud Risk Management Procedures 1. Introduction KCE Electronics Public Company Limited ( KCE or the Company ) is committed to achieving the highest levels of business integrity, morals and transparency

Fraud Risk Management Procedures 1. Introduction KCE Electronics Public Company Limited ( KCE or the Company ) is committed to achieving the highest levels of business integrity, morals and transparency

Presented by: Donald F. Conway, CPA Mercadien, P.C., Certified Public Accountants. Forensic Accounting, Political Corruption & White Collar Offenses

Presented by: Donald F. Conway, CPA Mercadien, P.C., Certified Public Accountants Forensic Accounting, Political Corruption & White Collar Offenses Defining Fraud The dictionary defines fraud as a deception

Presented by: Donald F. Conway, CPA Mercadien, P.C., Certified Public Accountants Forensic Accounting, Political Corruption & White Collar Offenses Defining Fraud The dictionary defines fraud as a deception

Fraud Awareness and Prevention Program Report

Internal Audit Department Fraud Awareness and Prevention Program Report Project 2009-263 A Review of Fraud Awareness, Prevention, Detection and Risk Mitigation Practices in Landfill Operations, Central

Internal Audit Department Fraud Awareness and Prevention Program Report Project 2009-263 A Review of Fraud Awareness, Prevention, Detection and Risk Mitigation Practices in Landfill Operations, Central

UNDERSTANDING INTERNAL CONTROLS. A Reference Guide for Managing University Business Practices

UNDERSTANDING INTERNAL CONTROLS A Reference Guide for Managing University Business Practices Table of Contents INTRODUCTION...1 OBJECTIVES...1 SCOPE...2 RESPONSIBILITY...2 BALANCING RISK AND CONTROL...3

UNDERSTANDING INTERNAL CONTROLS A Reference Guide for Managing University Business Practices Table of Contents INTRODUCTION...1 OBJECTIVES...1 SCOPE...2 RESPONSIBILITY...2 BALANCING RISK AND CONTROL...3

Chapter 15 Auditing the Expenditure Cycle

Chapter 15 Auditing the Expenditure Cycle Expenditure cycle consists of activities related to the acquisition of and payment for plant assets and goods and services. Two major transaction classes: 1 purchases

Chapter 15 Auditing the Expenditure Cycle Expenditure cycle consists of activities related to the acquisition of and payment for plant assets and goods and services. Two major transaction classes: 1 purchases

AN AUDIT OF INTERNAL CONTROL OVER FINANCIAL REPORTING THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL STATEMENTS:

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STAFF VIEWS AN AUDIT OF INTERNAL CONTROL OVER FINANCIAL REPORTING THAT IS INTEGRATED WITH AN

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STAFF VIEWS AN AUDIT OF INTERNAL CONTROL OVER FINANCIAL REPORTING THAT IS INTEGRATED WITH AN

How To Prevent Fraud In The United States

Fraud Detection & Prevention for Accounts Payable! Presented by Larry Holmes! Accounts Payable With Fraud! Paying for goods and services that were not received! Paying inflated prices for goods and services!

Fraud Detection & Prevention for Accounts Payable! Presented by Larry Holmes! Accounts Payable With Fraud! Paying for goods and services that were not received! Paying inflated prices for goods and services!

The auditors responsibility to consider fraud in an audit of financial statements

The auditors responsibility to consider fraud in an audit of financial statements Audit in a nutshell Reality Picture (= financial statements) Balance sheet Assets Liabilities Equity Process Detection

The auditors responsibility to consider fraud in an audit of financial statements Audit in a nutshell Reality Picture (= financial statements) Balance sheet Assets Liabilities Equity Process Detection

TITLE: Fraud Prevention and Detection Program IDENTIFIER: S-FW-LD-1008 APPROVED: Executive Cabinet (Pending)

") PAGE 1 of 5 TITLE: Fraud Prevention and Detection Program IDENTIFIER: S-FW-LD-1008 APPROVED: Executive Cabinet (Pending) ORIGINAL: 11/03 REVISED: 10/07, 09/10, 04/13 REVIEWED: EFFECTIVE DATE Acute Care

PAGE 1 of 5 TITLE: Fraud Prevention and Detection Program IDENTIFIER: S-FW-LD-1008 APPROVED: Executive Cabinet (Pending) ORIGINAL: 11/03 REVISED: 10/07, 09/10, 04/13 REVIEWED: EFFECTIVE DATE Acute Care

Guide to Internal Control Over Financial Reporting

Guide to Internal Control Over Financial Reporting The Center for Audit Quality prepared this Guide to provide an overview for the general public of internal control over financial reporting ( ICFR ).

Guide to Internal Control Over Financial Reporting The Center for Audit Quality prepared this Guide to provide an overview for the general public of internal control over financial reporting ( ICFR ).

Checklist. Internal financial controls for charities. Contents. 1. Self-assessment checklist

1 of 9 Internal financial controls for charities Checklist Contents 1. Self-assessment checklist 1 2. Some key issues, monitoring arrangements and risk of fraud 2 3. Income 3 4. Purchases and payments

1 of 9 Internal financial controls for charities Checklist Contents 1. Self-assessment checklist 1 2. Some key issues, monitoring arrangements and risk of fraud 2 3. Income 3 4. Purchases and payments

Table of Contents: Chapter 2 Internal Control

Table of Contents: Chapter 2 Chapter 2... 2 2.1 Establishing an Effective System... 2 2.1.1 Sample Plan Elements... 5 2.1.2 Limitations of... 7 2.2 Approvals... 7 2.3 PCard... 7 2.4 Payroll... 7 2.5 Reconciliation

Table of Contents: Chapter 2 Chapter 2... 2 2.1 Establishing an Effective System... 2 2.1.1 Sample Plan Elements... 5 2.1.2 Limitations of... 7 2.2 Approvals... 7 2.3 PCard... 7 2.4 Payroll... 7 2.5 Reconciliation

Centre for Corporate Governance. Sample listing of fraud schemes

Centre for Corporate Governance Sample listing of fraud schemes Sample listing of fraud schemes The following listing of possible fraud schemes can be utilized by management and auditors to assist in identifying

Centre for Corporate Governance Sample listing of fraud schemes Sample listing of fraud schemes The following listing of possible fraud schemes can be utilized by management and auditors to assist in identifying

Internal Controls for Small Organizations. Jen Parker, CPA Director of Accounting & Finance US Youth Soccer

Internal Controls for Small Organizations Jen Parker, CPA Director of Accounting & Finance US Youth Soccer Fraud Statistics: The following statistics about fraud and white collar crime are from the Association

Internal Controls for Small Organizations Jen Parker, CPA Director of Accounting & Finance US Youth Soccer Fraud Statistics: The following statistics about fraud and white collar crime are from the Association

IPPF Practice Guide. Internal Auditing and Fraud

IPPF Practice Guide Internal Auditing and Fraud December 2009 IPPF Practice Guide Table of Contents Introduction... 1 Executive Summary... 2 Definition of Fraud... 4 Fraud Awareness... 5 A. Reasons for

IPPF Practice Guide Internal Auditing and Fraud December 2009 IPPF Practice Guide Table of Contents Introduction... 1 Executive Summary... 2 Definition of Fraud... 4 Fraud Awareness... 5 A. Reasons for

ACCOUNTING AND FINANCIAL REPORTING REGULATION MANUAL

ACCOUNTING AND FINANCIAL REPORTING REGULATION MANUAL STATE BOARD OF ACCOUNTS 302 West Washington Street Room E418 Indianapolis, Indiana 46204-2769 Issued January 2011 Revised April 2012 TABLE OF CONTENTS

ACCOUNTING AND FINANCIAL REPORTING REGULATION MANUAL STATE BOARD OF ACCOUNTS 302 West Washington Street Room E418 Indianapolis, Indiana 46204-2769 Issued January 2011 Revised April 2012 TABLE OF CONTENTS

Fraud Prevention Checklist for Small Businesses

Fraud Prevention Checklist for Small Businesses 11 Ways to Minimize the Risk and Impact PAYMENT SOLUTIONS Fraud can have a devastating impact on small businesses. Prevention and mitigation strategies can

Fraud Prevention Checklist for Small Businesses 11 Ways to Minimize the Risk and Impact PAYMENT SOLUTIONS Fraud can have a devastating impact on small businesses. Prevention and mitigation strategies can

Standard Procedures and Controls for the Title Industry. Prepared by the ALTA Internal Auditing Committee ALTA

Standard Procedures and Controls for the Title Industry Prepared by the ALTA Internal Auditing Committee ALTA The American Land Title Association, founded in 1907, is the national trade association and

Standard Procedures and Controls for the Title Industry Prepared by the ALTA Internal Auditing Committee ALTA The American Land Title Association, founded in 1907, is the national trade association and

Conversion. Concealment methods. Example #1: Skimming. Example #2: Skimming. 2015 GASBO Conference. Thomas Buckhoff, Ph.D.

Top Five Employee Fraud Schemes Forensic Solutions, LLC Forensic accounting and litigation support services Presented by: Thomas Buckhoff, Ph.D., CPA/CFF, CFE Fraudsters love cash! Cash is the asset most

Top Five Employee Fraud Schemes Forensic Solutions, LLC Forensic accounting and litigation support services Presented by: Thomas Buckhoff, Ph.D., CPA/CFF, CFE Fraudsters love cash! Cash is the asset most

Consideration of Fraud in a Financial Statement Audit

Consideration of Fraud in a Financial Statement Audit 151 AU-C Section 240 Consideration of Fraud in a Financial Statement Audit Source: SAS No. 122; SAS No. 128. Effective for audits of financial statements

Consideration of Fraud in a Financial Statement Audit 151 AU-C Section 240 Consideration of Fraud in a Financial Statement Audit Source: SAS No. 122; SAS No. 128. Effective for audits of financial statements

ACL EBOOK. Detecting and Preventing Fraud with Data Analytics

ACL EBOOK Detecting and Preventing Fraud with Data Analytics Contents Why use data analysis for fraud?... 4 Internal control systems, while good, are not good enough... 5 Purpose-built data analytics is

ACL EBOOK Detecting and Preventing Fraud with Data Analytics Contents Why use data analysis for fraud?... 4 Internal control systems, while good, are not good enough... 5 Purpose-built data analytics is

ACL WHITEPAPER. Automating Fraud Detection: The Essential Guide. John Verver, CA, CISA, CMC, Vice President, Product Strategy & Alliances

ACL WHITEPAPER Automating Fraud Detection: The Essential Guide John Verver, CA, CISA, CMC, Vice President, Product Strategy & Alliances Contents EXECUTIVE SUMMARY..................................................................3

ACL WHITEPAPER Automating Fraud Detection: The Essential Guide John Verver, CA, CISA, CMC, Vice President, Product Strategy & Alliances Contents EXECUTIVE SUMMARY..................................................................3

Using Technology to Automate Fraud Detection Within Key Business Process Areas

Using Technology to Automate Fraud Detection Within Key Business Process Areas 2013 ACFE Canadian Fraud Conference September 10, 2013 John Verver, CA, CISA, CMA Vice President, Strategy ACL Services Ltd

Using Technology to Automate Fraud Detection Within Key Business Process Areas 2013 ACFE Canadian Fraud Conference September 10, 2013 John Verver, CA, CISA, CMA Vice President, Strategy ACL Services Ltd

PREVENTING AND DETECTING FRAUD IN NOT-FOR-PROFIT ORGANIZATIONS UPDATED EDITION

PREVENTING AND DETECTING FRAUD IN NOT-FOR-PROFIT ORGANIZATIONS UPDATED EDITION Preventing and Detecting Fraud in Not-For-Profit Organizations Table of Contents Page I. An Overview of Fraud in the United

PREVENTING AND DETECTING FRAUD IN NOT-FOR-PROFIT ORGANIZATIONS UPDATED EDITION Preventing and Detecting Fraud in Not-For-Profit Organizations Table of Contents Page I. An Overview of Fraud in the United

Asset Misappropriation Research White Paper for the Institute for Fraud Prevention

Asset Misappropriation Research White Paper for the Institute for Fraud Prevention by Chad Albrecht, Mary-Jo Kranacher & Steve Albrecht Abstract In this paper we provide a general overview of asset misappropriation.

Asset Misappropriation Research White Paper for the Institute for Fraud Prevention by Chad Albrecht, Mary-Jo Kranacher & Steve Albrecht Abstract In this paper we provide a general overview of asset misappropriation.

SUBSIDIARY LEDGER MANAGEMENT AND INTERNAL CONTROLS

SUBSIDIARY LEDGER MANAGEMENT AND INTERNAL CONTROLS Introduction: A critical component of the University s internal control environment over financial transactions is the departmental subsidiary ledger

SUBSIDIARY LEDGER MANAGEMENT AND INTERNAL CONTROLS Introduction: A critical component of the University s internal control environment over financial transactions is the departmental subsidiary ledger

Auditing Standard ASA 240 The Auditor's Responsibilities Relating to Fraud in an Audit of a Financial Report

Compiled Auditing Standard ASA 240 (November 2013) Auditing Standard ASA 240 The Auditor's Responsibilities Relating to Fraud in an Audit of a Financial Report This compilation was prepared on 11 November

Compiled Auditing Standard ASA 240 (November 2013) Auditing Standard ASA 240 The Auditor's Responsibilities Relating to Fraud in an Audit of a Financial Report This compilation was prepared on 11 November

MCPHS IDENTITY THEFT POLICY

SECTION 1: BACKGROUND MCPHS IDENTITY THEFT POLICY The risk to the College, its employees and students from data loss and identity theft is of significant concern to the College and can be reduced only

SECTION 1: BACKGROUND MCPHS IDENTITY THEFT POLICY The risk to the College, its employees and students from data loss and identity theft is of significant concern to the College and can be reduced only

ANTI-FRAUD POLICY Adopted August 13, 2015

ANTI-FRAUD POLICY Adopted August 13, 2015 Introduction The Board of Commissioners of the Housing Authority of the City of Muskogee (MHA) has established an anti-fraud policy to enforce controls and to

ANTI-FRAUD POLICY Adopted August 13, 2015 Introduction The Board of Commissioners of the Housing Authority of the City of Muskogee (MHA) has established an anti-fraud policy to enforce controls and to

Red Flag Identity Theft Financial Policy 1.10

Issued: 05/16/2014 Revised: Policy and College ( Seminary ) developed this Identity Theft Prevention Program ("Program") pursuant to the Federal Trade Commission's ( FTC ) Red Flags Rule, which implements

Issued: 05/16/2014 Revised: Policy and College ( Seminary ) developed this Identity Theft Prevention Program ("Program") pursuant to the Federal Trade Commission's ( FTC ) Red Flags Rule, which implements

Audit Guide for Audit Committees of Small Nonprofit Organizations

Audit Guide for Audit Committees of Small Nonprofit Organizations A free resource provided by the Virginia Society of Certified Public Accountants Audit Guide for Small Nonprofit Organizations A free resource

Audit Guide for Audit Committees of Small Nonprofit Organizations A free resource provided by the Virginia Society of Certified Public Accountants Audit Guide for Small Nonprofit Organizations A free resource

COMPONENTS OF INTERNAL CONTROL. ACCT430, Notes, Chapter 7, Internal Controls

ACCT430, Notes, Chapter 7, Internal Controls DEFINITION OF INTERNAL CONTROLS (COSO) (Note: COSO is the acronym for the Committee of Sponsoring Organizations, which includes American Accounting Association,

ACCT430, Notes, Chapter 7, Internal Controls DEFINITION OF INTERNAL CONTROLS (COSO) (Note: COSO is the acronym for the Committee of Sponsoring Organizations, which includes American Accounting Association,

GOVERNANCE, RISK AND COMPLIANCE. Internal Audit. Assessing Fraud Vulnerabilities. kpmg.com/in

GOVERNANCE, RISK AND COMPLIANCE Internal Audit Assessing Fraud Vulnerabilities kpmg.com/in 1 Internal Audit Assessing Fraud Vulnerabilities Introduction Globalization has increased the scale and complexity

GOVERNANCE, RISK AND COMPLIANCE Internal Audit Assessing Fraud Vulnerabilities kpmg.com/in 1 Internal Audit Assessing Fraud Vulnerabilities Introduction Globalization has increased the scale and complexity

Internal Controls for Small Businesses to Reduce the Risk of Fraud

Internal Controls for Small Businesses to Reduce the Risk of Fraud Copyright Copyright 2009 Intuit, Inc. All rights reserved. Intuit, Inc. 5601 Headquarters Drive Plano, TX 75024 Trademarks Intuit, the

Internal Controls for Small Businesses to Reduce the Risk of Fraud Copyright Copyright 2009 Intuit, Inc. All rights reserved. Intuit, Inc. 5601 Headquarters Drive Plano, TX 75024 Trademarks Intuit, the

Student Fraud Project: Forensic Analysis of Personal and Corporate Bank Statements

Student Fraud Project: Forensic Analysis of Personal and Corporate Bank Statements Economic Crime and the Online World 22 nd Annual ECI Conference November 2, 2011 Moderator: Bernard Hyman Jr., Esq. (315)

Student Fraud Project: Forensic Analysis of Personal and Corporate Bank Statements Economic Crime and the Online World 22 nd Annual ECI Conference November 2, 2011 Moderator: Bernard Hyman Jr., Esq. (315)

Introduction to Fraud Examination. World Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA

Introduction to Fraud Examination World Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA VII. FRAUDULENT FINANCIAL TRANSACTIONS: FRAUD SCHEMES Introduction Fraud can be committed

Introduction to Fraud Examination World Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA VII. FRAUDULENT FINANCIAL TRANSACTIONS: FRAUD SCHEMES Introduction Fraud can be committed

Forensic Audit Building a World Class Program

Forensic Audit Building a World Class Program PAUL E. ZIKMUND DIRECTOR GLOBAL INTEGRITY AND FORENSIC AUDIT 1 2012 ACFE ANNUAL FRAUD CONFERENCE ORLANDO, FL Why the Need for Forensic Audit Program In response

Forensic Audit Building a World Class Program PAUL E. ZIKMUND DIRECTOR GLOBAL INTEGRITY AND FORENSIC AUDIT 1 2012 ACFE ANNUAL FRAUD CONFERENCE ORLANDO, FL Why the Need for Forensic Audit Program In response

ACCOUNTING RECORDS: HOW THEY ARE USED TO CONCEAL FRAUD. ROSANNE TERHART, CFE, CA Senior Manager BDO Canada LLP Vancouver, British Columbia Canada

Once an employee commits fraud, he has limited time to conceal the financial transaction in the accounting records. Learn how employees hide these fraudulent transactions and what to look for when reviewing

Once an employee commits fraud, he has limited time to conceal the financial transaction in the accounting records. Learn how employees hide these fraudulent transactions and what to look for when reviewing

KEYS TO AN EFFECTIVE DIRECTOR CORPORATE COMPLIANCE AND INTERNAL AUDIT MULTICARE HEALTH SYSTEM TACOMA, WA

KEYS TO AN EFFECTIVE ANTI-FRAUD PROGRAM WAYNE PURVES DIRECTOR CORPORATE COMPLIANCE AND INTERNAL AUDIT MULTICARE HEALTH SYSTEM TACOMA, WA AHIA 32 nd Annual Conference August 25-28, 2013 Chicago, Illinois

KEYS TO AN EFFECTIVE ANTI-FRAUD PROGRAM WAYNE PURVES DIRECTOR CORPORATE COMPLIANCE AND INTERNAL AUDIT MULTICARE HEALTH SYSTEM TACOMA, WA AHIA 32 nd Annual Conference August 25-28, 2013 Chicago, Illinois

ATTACHMENT L. 2012/13 Internal Control Questionnaire for Workforce Organizations/Programs

ATTACHMENT L 2012/13 Internal Control Questionnaire for Workforce Organizations/Programs Prepared by: Financial Monitoring and Accountability Section Date: August 10, 2012 Introduction and Purpose The

ATTACHMENT L 2012/13 Internal Control Questionnaire for Workforce Organizations/Programs Prepared by: Financial Monitoring and Accountability Section Date: August 10, 2012 Introduction and Purpose The

Fraud Prevention Policy

FRAUD PREVENTION POLICY 1. Purpose 1.1. This policy sets out the general principles and minimum requirements for managing fraud risks across the Amcor Group and all its member and affiliated companies

FRAUD PREVENTION POLICY 1. Purpose 1.1. This policy sets out the general principles and minimum requirements for managing fraud risks across the Amcor Group and all its member and affiliated companies

Preventing Fraud: The Importance of Internal Controls

Preventing Fraud: The Importance of Internal Controls Presented by: Scott Gold, CPA,BKD, LLP @ BKDForensics Today s Agenda Faces of fraud Real life examples: The latest schemes Lifestyles of the Rich and

Preventing Fraud: The Importance of Internal Controls Presented by: Scott Gold, CPA,BKD, LLP @ BKDForensics Today s Agenda Faces of fraud Real life examples: The latest schemes Lifestyles of the Rich and