Italian RMBS Index Report Q4 2011: Credit Performance Deteriorated, But Stayed Within Our Expectations

|

|

|

- Georgiana Ford

- 10 years ago

- Views:

Transcription

1 February 17, 2012 Italian RMBS Index Report Q4 2011: Credit Performance Deteriorated, But Stayed Within Our Expectations Primary Credit Analyst: Benedetta Avesani, Milan (39) ; Secondary Contact: Andrew M Bowyer, CFA, London (44) ; [email protected] Data Analyst: Shilpi Purkayastha, Data Analyst, London (44) ; [email protected] Table Of Contents Related Criteria And Research 1

20-7176-3940; shilpi_purkayastha@standardandpoors.")

2 Italian RMBS Index Report Q4 2011: Credit Performance Deteriorated, But Stayed Within Our Expectations Table 1 Performance Indicators (%) Q Q Q Q Q Q Q Q Q Q Q Q Index changes Total delinquencies day delinquencies Prepayments Economic data Unemployment rate* N/A N/A N/A N/A N/A Real GDP growth* N/A N/A N/A N/A N/A N/A N/A *Istat (Istituto Nazionale di Statistica). N/A--Not available. The performance of Italian residential mortgage-backed securities (RMBS) transactions slightly worsened in Q However, the deterioration was in line with Standard & Poor's Ratings Services' expectations. Delinquencies and defaults rose slightly after stabilizing in the first half of Total delinquencies have risen slightly, to 3.09% in Q4 2011, from 2.88% in Q1 that year. Severe delinquencies (over 90 days) increased to 1.53% from 1.42% in Q We believe the weaker collateral performance reflects the weakening economies of Italy and the European Economic and Monetary Union (EMU or eurozone). However 1.53% is still lower than the peak of 1.94% recorded by the 90 plus days arrears in Q4 2009, when Italy was in recession. The prepayment rate also increased slightly to 5.58%, from 5.52% in Q the lowest level we have seen over the past five years. Overview The performance of Italian RMBS transactions slightly worsened in Q4 2011, compared with the previous quarter, with severe delinquencies increasing to 1.53% from 1.42%. Total delinquencies have slightly increased over the past year, to 3.09% in Q from 2.88% in Q The weaker collateral performance reflects the weakening economies of Italy and the eurozone, in our view. Downside risks in the eurozone's economic outlook have increased, in our view. Recent economic indicators, such as the purchasing managers indices, show that economic activity contracted in most countries during Q4 2011, and that the first quarter of 2012 is likely to be no different. In our opinion, a prolonged recession would have a particularly hard impact on countries like Spain, Portugal, and Italy. We now project flat GDP growth for the eurozone as a whole in 2012 and 1.0% growth in 2013, compared with our earlier projection of 0.4% growth in 2012 (see "Economic Research: Assessing The Severity Of The Eurozone Standard & Poors RatingsDirect on the Global Credit Portal February 17,

. N/A--Not available.")

3 Recession Is A Close Call" published on Jan. 31, 2012). We've also further lowered our Italian GDP growth forecast for this year to minus 1.0% from 0.5% as of October 2011 in the baseline forecast of a mild recession. In our alternative forecast of a true double dip, which would have a particularly adverse effect on Italy, we would expect GDP to fall to minus 3.0% this year. We currently assign a 60% probability to our baseline forecast, versus 40% for our alternative forecast of a true double dip. The weakening of the Italian economy is also demonstrated in the unemployment rate, which increased to 8.9% in Q from 8.3% in Q3 that year. The latest figure is higher than recorded a year earlier (8.1%) and represents the peak since 2002, when unemployment reached 8.6% before falling to 6.1% in We believe that the slight increase in severe delinquencies seen in the quarter reflects flagging economic conditions, but it is still in line with our expectations. The Italian housing market's decline, which began in 2006, began to stabilize during the first half of However, it started to stumble again in the second half, with residential real estate sales dropping by 2.7% in Q and 4.1% in Q year-on-year. According to the latest quarterly report from the Ministry of Economy and Finance's "Agenzia del Territorio," after four consecutive quarters of real estate market deterioration, in Q the number of residential real estate sales was slightly up again in relative terms by 1.4% year-on-year. However, they were even lower in Q3 than they were at the same point in 2009, when the market dropped by 11% year-on-year by number of transactions. The Bank of Italy's latest survey of the real estate market in October 2011 also pointed to increasing pressure on house prices and an increasing number of outstanding listings with real estate agents. According to the Bank of Italy's latest publication, the volume of new residential mortgage loans granted to Italian families dropped by about 16% in Q3 2011, compared with the same quarter in This, in our opinion, was due to the banks' requirement of higher spreads, and the weak economy. The Italian housing market has been volatile over the past two years, but it has generally declined overall. However, the drop in the number of transactions and the pressure on housing prices has been limited, in comparison with other European countries. We do not expect the Italian housing market's decline to negatively affect Italian RMBS transactions for a number of reasons, such as: Limited decline in the property prices; Low loan-to-value ratios and fairly high seasoning generally shown by Italian portfolios backing the transactions; and The fact that our ratings have proven to be stable under moderate stress conditions, after applying haircuts to the underlying properties' valuations of up to 10%. The renegotiation scheme ("Piano Famiglie") launched in 2009 by the Association of Italian Banks (ABI) allows participating banks to grant periods when payments do not need to be made (a "payment holiday") to mortgage loan borrowers that meet certain conditions. This scheme was due to stop in January 2012, but ABI has since extended it until July According to ABI, as of Nov. 30, 2011, banks have conceded payment holidays to 7 billion worth of mortgages granted to individuals. This means that about 2.1% of loans have benefited from the renegotiation scheme, demonstrating the financial resilience of the Italian families affected and the negligible impact 3

4 of this scheme on the RMBS transactions that we have rated. We are monitoring any evolution of the takeover ratio. We rated two new transactions in Q4: Voba N. 3 S.r.l., which closed on Nov. 23, 2011, and was originated by Banca Popolare dell'alto Adige S.C.p.A. (see "New Issue: Voba N. 3 S.r.l."); and Fanes S.r.l. (Series ), which closed on Dec. 2, 2011, and was originated by Cassa di Risparmio di Bolzano SpA (see "New Issue: Fanes S.r.l."). On Dec. 21, 2011, we placed our ratings on 26 tranches in 19 Italian RMBS transactions on CreditWatch negative, following recent rating actions that involved several European banks (see "Ratings On 305 Tranches In 120 European RMBS Transactions Placed On CreditWatch Negative After Bank Rating Actions," published on Dec. 21, 2011). We consider the ratings on the Italian RMBS tranches affected to be directly linked to the ratings on the banks acting as counterparties in these transactions, as per our 2010 counterparty criteria (see "Counterparty and Supporting Obligations Methodology and Assumptions," published on Dec. 2, 2010). On Jan. 13, 2012, we lowered our unsolicited long-term rating on the Republic of Italy to 'BBB+' from 'A' (see "Italy's Unsolicited Ratings Lowered To 'BBB+/A-2'; Outlook Negative"). As a result, on Jan. 23, 2012, we lowered all of our 'AAA (sf)' ratings on Italian structured finance securities to 'AA+ (sf)'. According to our EMU criteria, six notches is the maximum permissible uplift between the unsolicited rating on the Republic of Italy and those specific structured finance transaction ratings (see "Nonsovereign Ratings That Exceed EMU Sovereign Ratings: Methodology And Assumptions," published on June 14, 2011, and "Various Rating Actions Taken On 340 European Structured Finance Tranches After Eurozone Sovereign Rating Actions," published on Jan. 23, 2012). We do not anticipate any downward rating actions driven by performance reasons in the coming months. Even though the performance of Italian RMBS transactions slightly worsened in Q compared with Q3, the deterioration has been in line with our expectations. Likewise, the decline in the housing market is limited and still within our tested assumptions. We will monitor the weakening collateral performance and the decline of the Italian housing market in our surveillance process of Italian RMBS transactions. Once we have reviewed the affected transactions, we will resolve the Italian RMBS CreditWatch placements of Dec. 21, Table 2 Italian RMBS Transactions To Which We Assigned A Second Rating In 2011 Rating date Originator Issuer Size (mil. ) Ratings on all classes at issuance Feb 23, 2011 Veneto Banca SpA and Banca Popolare di Intra SpA Claris Finance 2008 S.r.l A (AA-), B (NR), C1 (NR), C2 (NR) Feb 11, 2011 Banca Apulia SpA Apulia Finance N. 4 S.r.l. (series ) Feb 11, 2011 Banca Apulia SpA Apulia Finance N. 4 S.r.l. (series ) A (AA-), B (NR) A (AA), B (NR) Feb 16, 2011 Banca Nazionale del Lavoro SpA Vela Mortgages S.r.l. (series 1) 5, A (AAA), B (AA), C (A), D (NR) Feb 16, 2011 Banca Nazionale del Lavoro SpA Vela Mortgages S.r.l. (series 2) 2, A (AAA), B (AAA), C (AA+), D (NR) Mar 21, 2011 Cassa di Risparmio di Parma e Piacenza SpA MondoMutui Cariparma S.r.l. 4, A (AAA), J (NR) Standard & Poors RatingsDirect on the Global Credit Portal February 17,

, B (NR), C (NR) May 17, 2011 Banca Sella SpA Mars 2600 S.r.l. (series 2) 224.7 A (AAA), B (AA), C (AA-), D (NR) May 31, 2011 Banca Sella SpA Mars 2600 (series 3) 212.")

5 Table 2 Italian RMBS Transactions To Which We Assigned A Second Rating In 2011 (cont.) Feb 23, 2011 Banca Padovana Credito Cooperativo S.C. Alta Padovana Finance S.r.l. (series ) A (AAA), B (NR), C (NR) May 17, 2011 Banca Sella SpA Mars 2600 S.r.l. (series 2) A (AAA), B (AA), C (AA-), D (NR) May 31, 2011 Banca Sella SpA Mars 2600 (series 3) A (AAA), B (AA), C (A-), D (NR) Mar 11, 2011 Banca Popolare dell'alto Adige ScpA Voba Finance N. 2 S.r.l A (AA), B (NR), C (NR) Feb 11, 2011 Cassa di Risparmio di Bolzano SpA Fanes S.r.l. (series ) A (AAA), B (NR) Apr 22, 2011 NR--Not rated. Chart 1 Cassa di Risparmio di Ravenna and Banca di Imola Argentario Finance S.r.l A1 (AA), A2 (AA), B1 (NR), B2 (NR), C (NR) 5

, B (NR) Apr 22, 2011 NR--Not rated. Chart 1 Cassa di Risparmio di Ravenna and Banca di Imola Argentario Finance S.r.l. 451.7 A1 (AA), A2 (AA), B1 (NR), B2 (NR), C (NR) www.standardandpoors.")

6 Chart 2 Standard & Poors RatingsDirect on the Global Credit Portal February 17,

7 Chart 3 7

8 Chart 4 Standard & Poors RatingsDirect on the Global Credit Portal February 17,

9 Chart 5 Table 3 Italian RMBS Transactions Included In Indices Issue date Originator Transaction Short name Mar 20, Banca Popolare di Vicenza Scarl Berica MBS S.r.l. Berica May 24, 2001 Sept 27, 2001 Feb 21, 2002 Mar 20, 2002 Jul 27, 2002 Mar 25, 2003 Dec 5, 2002 Dec 20, 2002 Jan 23, 2003 Banca Apulia SpA Apulia Finance S.r.l. Apulia Finance 1 Five Italian banks belonging to the co-operative credit ("credito cooperativo") system Credico Finance SpA Credico 1 Banca Popolare di Vicenza Scarl Berica 2 MBS S.r.l. Berica 2 Banche Popolari Unite Orio Finance No. 3 PLC Orio 3 Veneto Banca Scrl Claris Finance S.r.l. Claris Finance Fineco Banca ICQ SpA Heliconus S.r.l. Heliconus Banca CR Firenze SpA CR Firenze Mutui S.r.l. CR Firenze Banca Popolare di Intra Scparl Intra Mortgage Finance 1 S.r.l. Intra Barclays Bank PLC, Italian branch (formerly Banca Woolwich SpA) Mercurio Mortgage Finance S.r.l. (Series ) Mercurio 1 9

Mercurio Mortgage Finance S.r.l. (Series 2003-1) Mercurio 1 www.standardandpoors.com/ratingsdirect 9")

10 Table 3 Italian RMBS Transactions Included In Indices (cont.) Feb 17, 2003 Feb 27, 2003 Feb 28, 2003 Mar 13, 2003 Mar 14, 2003 Mar 28, 2003 Apr 28, 2003 Apr 30, 2003 June 26, 2003 Aug 6, 2003 Nov 28, 2003 Dec 3, 2003 Dec 22, 2003 Jan 26, 2004 Mar 12, 2004 Apr 16, 2004 Apr 16, 2004 Jun 22, 2004 Oct 21, 2004 Dec 4, 2004 Banca Popolare di Vicenza Scarl Berica 3 MBS S.r.l. Berica 3 Banca Intesa SpA IntesaBci Sec. 2 S.r.l. Intesa BCI 2 Banca Antoniana Popolare Veneta SpA Giotto Finance 2 SpA Giotto 2 Banche Popolari Unite and Centrobanca SpA Sintonia Finance S.r.l. Sintonia Banca Agricola Mantovana SpA Mantegna Finance II S.r.l. Mantegna Finance II Banca delle 'Mar.e SpA Mar.e Mutui Societa per la Cartolarizzazione Mar.e Mutui Unibanca SpA Romagna Finance S.r.l. Romagna Banca Nazionale del Lavoro SpA Vela Home S.r.l. Vela Home 1 Barclays Bank PLC, Italian branch (formerly Banca Woolwich SpA) Mercurio Mortgage Finance S.r.l. (Series ) Mercurio 2 Banca Apulia SpA Apulia Finance No. 2 S.r.l. Apulia Finance 2 Fin-Eco Banca ICQ SpA F-E Mortgages S.r.l. F-E Mortgages Banca Meridiana SpA and Veneto Banca Scrl Claris Finance 2003 S.r.l. Claris Finance 2003 Meliorbanca SpA Sestante Finance S.r.l. Sestante Finance Banca Monte dei Paschi di Siena SpA Siena Mortgages 03-4 S.r.l. Siena 03-4 Banca Popolare di Vicenza Scarl and Cariprato - Cassa di Risparmio di Prato SpA Berica Residential MBS 1 S.r.l. Berica 4 Banca Poplare di Spoleto SpA Spoleto Mortgages S.r.l. Spoleto Banca Nazionale del Lavoro SpA Vela Home S.r.l. Vela 2 12 Italian banks belonging to the co-operative credit ("credito cooperativo") system Credico Finance 3 S.r.l. Credico 3 Banca Apulia SpA Apulia Mortgages Finance N. 3 S.r.l. Apulia 3 Meliorbanca SpA Sestante Finance S.r.l. Sestante 2 Feb 3, 2005 Banca Popolare di Puglia e Basilcata S.c.a.r.l. Media Finance S.r.l Media Apr 8, 2005 FinecoBank SpA F-E Mortgages S.r.l. series 2005 F-E Mortgages 2005 May 6, 2005 Jul 12, 2005 Jan 21, 2005 Nov 3, 2005 Dec 16, 2005 Unicredit Banca SpA Cordusio RMBS S.r.l. Cordusio 1 Banca di Bergamo SpA and Veneto Banca SCPA Claris Finance 2005 S.r.l. Claris 2005 Banca Popolare di Vicenza Scarl, Cariprato - Cassa di Risparmio di Prato SpA, and Banca Nuova SpA Berica 5 Residential MBS S.r.l. Berica 5 Banca Nazionale del Lavoro Vela Home S.r.l. Series 3 Vela 3 Meliorbanca SpA Sestante Finance S.r.l. Series 3 Sestante 3 Standard & Poors RatingsDirect on the Global Credit Portal February 17,

11 Table 3 Italian RMBS Transactions Included In Indices (cont.) Dec 21, 2005 Feb 16, 2006 Feb 21, 2006 Jul 12, 2006 Cassa di Risparmio di Asti SpA Asti Finance S.r.l. Asti Banca Nazionale del Lavoro SpA Vela ABS S.r.l. Vela ABS Banca Nuova SpA, Cariprato - Cassa di Risparmio di Prato SpA, Banca Popolare di Vicenza ScpA Berica 6 Residential MBS S.r.l. Berica 6 Unicredit Banca SpA Cordusio RMBS 2 S.r.l. Cordusio 2 Jul 4, 2006 Banca Popolare di Milano BPM Securitisation 2 S.r.l. BPM 2 Oct 2, 2006 Banca Nazionale del Lavoro Vela Home S.r.l. Series 4 Vela 4 Oct 27, 2006 Nov 23, 2006 Dec 19, 2006 Mar 5, 2007 Feb 15, 2007 Mar 15, 2007 Mar 15, 2007 May 5, 2007 Jul 15, 2007 Jul 15, 2007 Dec 14, 2007 Dec 17, 2007 Dec 19, 2007 May 21, 2008 May 23, 2008 Jun 06, 2008 Jun 16, 2008 Jun 30, 2008 Jul 02, 2008 Aug 4, 2008 Jul 30, 2009 Banca delle 'Mar.e SpA Mar.e Mutui 2 Societa per la Cartolarizzazione a.r.l. Mar.e 2 Unicredit Banca per la Casa SpA Cordusio RMBS 3 - UBCasa 1 S.r.l. Cordusio 3 UBC-1 Meliorbanca SpA Sestante Finance S.r.l. Series 4 Sestante 4 Intesa Sanpaolo SpA Intesa Sec. 3 S.r.l. Intesa Sec 3 Banca Meridiana SpA, Banca di Bergamo SpA, and Veneto Banca Holdings S.C.P.A. Claris Finance 2007 S.r.l. Claris 2007 Banco Popolare Societa Cooperativa SCRL BP Mortgages S.r.l. BP Mortgages Banca di Roma SpA Capital Mortgage S.r.l. Capital Mortgage UniCredit Banca SpA Cordusio RMBS Securitisation S.r.l. Cordusio 4 Credito Bergamasco and Banco Popolare Societa Cooperativa SCRL BP Mortgages S.r.l. series 2 BP Mortgages BHW Bausparkasse AG, Hameln PB Domicilio Ltd. PB Domicilio Deutsche Bank Mutui SpA Eurohome (Italy) Mortgages S.r.l. Eurohome (Italy) Mortgages S.r.l. Banca Popolare di Crema SpA Banca Popolare di Cremona SpA, Banca Popolare di Lodi SpA, and Cassa di Risparmio di Lucca Pisa e Livorno SpA BPL Mortgages S.r.l. BPL Mortgages Bipop Carire SpA Capital Mortgage S.r.l. BIPCA Cordusio RMBS Unipol Banca SpA Grecale ABS S.r.l. Grecale ABS Cassa di Risparmio di Asti SpA Asti Finance S.r.l. Asti 2008 Cassa di Risparmio della Provincia di Teramo SpA Adriatico Finance RMBS S.r.l. Adriatico Finance Meliorbanca SpA Sestante Finance S.r.l. Series 5 Sestante 5 Barclays Bank PLC Mercurio Mortgage Finance S.r.l. Mercurio Banca Popolare di Puglia e Basilicata Scpa Media Finance S.r.l Media 2 Intesa Sanpaolo SpA Adriano Finance S.r.l. Adriano Finance Banca Popolare di Bari S.c.p.a. Popolari Bari Mortgages S.r.l. Popolare Bari 11

12 Table 3 Italian RMBS Transactions Included In Indices (cont.) Nov 18, 2008 Nov 17, 2008 Aug 7, 2009 Cassa di Risparmio di Cento SpA Guercino Solutions S.r.l. Guercino Solutions Banca Popolare di Vicenza ScpA, Cariprato - Cassa di Risparmio di Prato SpA, and Banca Nuova SpA Berica 7 Residential MBS S.r.l. Berica 7 Banca popolare dell'emilia Romagna S.C. Estense Finance S.r.l. Estense *The indices also include data from the following fully repaid transactions: Upgrade SpA, BPM Securitisation S.r.l., Bononia Funding S.r.l., Palazzo Finance 2 SpA., Grecale S.r.l., Siena Mortgages 00-1 SpA, Siena Mortgages 01-2 SpA, BPV Mortgages S.r.l., Garda Securitisation S.r.l., Velites S.r.l., Orio Finance No. 1 PLC and Orio Finance No. 2 PLC.,Mosaico Finance S.r.l.,Seashell II S.r.l., Siena Mortgages 02-3 SpA, BPL Mortgages S.r.l. Table 4 Italian RMBS Transactions Closed In 2011* Issue date Originator Issuer Size (mil. ) Apr 12, Banca Popolare di Puglia e Basilicata ScpA (BPPB) Media Finance S.r.l. (series ) Jun 21, 2011 Jul 22, 2011 Jul 25, 2011 Nov 23, 2011 Ratings on all classes at issuance A1 (AAA), A2 (AAA), B (NR) Cassa di Risparmio di Ferrara SpA Giovecca Mortgages S.r.l A1 (AAA), J (NR) Banca Santo Stefano Credito Cooperativo Martellago Venezia Società Cooperativa Cassa di Risparmio di Bra (CR Bra), Banca di Credito Cooperativo di Pianfei e Rocca de'baldi (Bcc Pianfei), and Banca Alpi Marittime (Alpi Marittime) BSS Securitisation 1 S.r.l A1 (AAA), A2 (AAA), B (BBB), C (NR) Dedalo Finance S.r.l A (AAA), B (NR) Banca Popolare dell'alto Adige S.C.p.A. VOBA N. 3 S.r.l A1 (AAA), A2 (AAA), J (NR) Dec 2, 2011 Cassa di Risparmio di Bolzano SpA Fanes S.r.l. (Series ) A (AAA), B (NR) *Rated by Standard & Poor's. NR--Not rated. Standard & Poors RatingsDirect on the Global Credit Portal February 17,

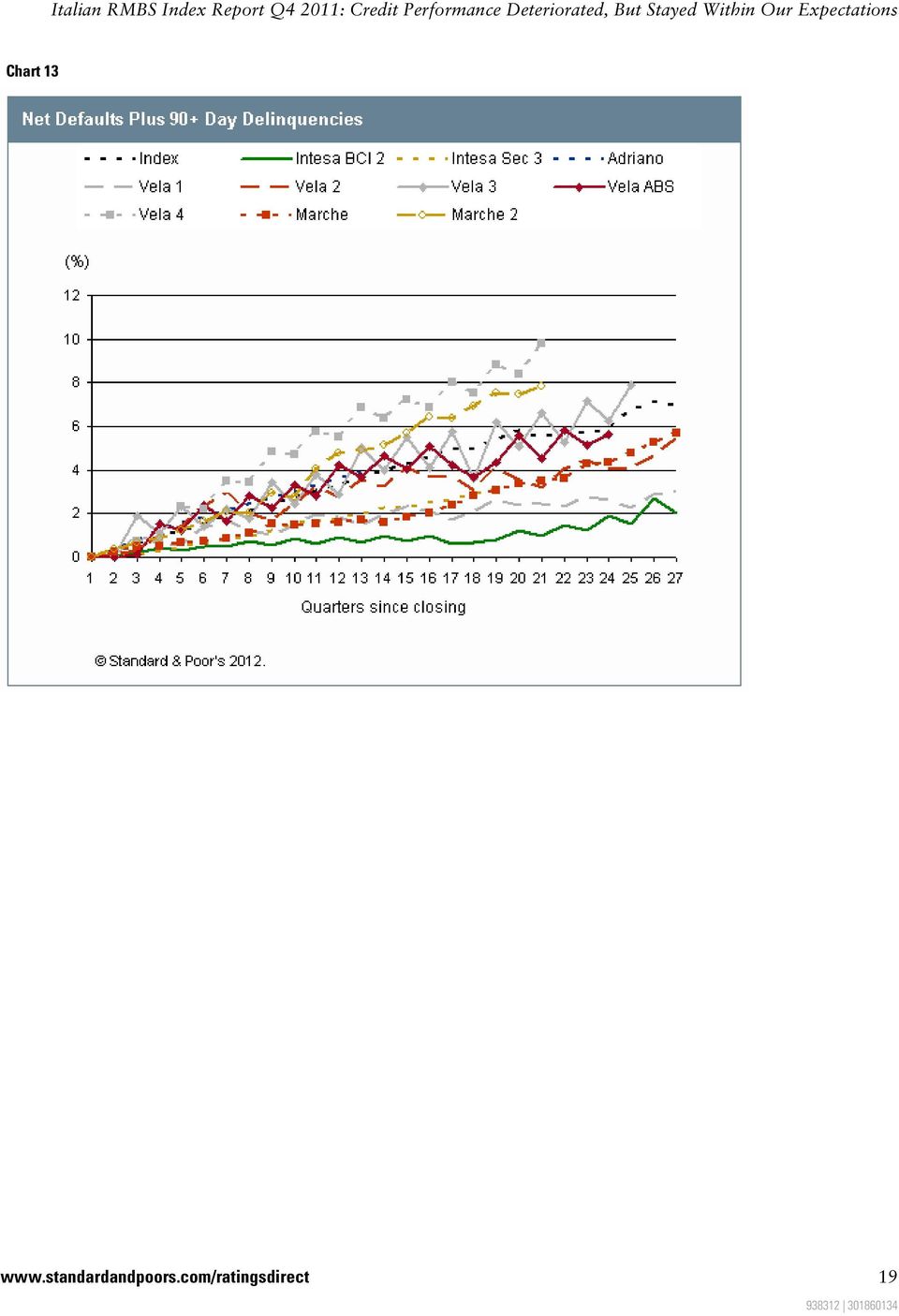

13 Chart

14 Chart 7 Standard & Poors RatingsDirect on the Global Credit Portal February 17,

15 Chart

16 Chart 10 Standard & Poors RatingsDirect on the Global Credit Portal February 17,

17 Chart

18 Chart 12 Standard & Poors RatingsDirect on the Global Credit Portal February 17,

19 Chart

20 Chart 14 Standard & Poors RatingsDirect on the Global Credit Portal February 17,

21 Chart

22 Chart 16 Standard & Poors RatingsDirect on the Global Credit Portal February 17,

23 Chart

24 Chart 18 Standard & Poors RatingsDirect on the Global Credit Portal February 17,

25 Chart

26 Chart 20 Standard & Poors RatingsDirect on the Global Credit Portal February 17,

27 Chart

28 Chart 22 Standard & Poors RatingsDirect on the Global Credit Portal February 17,

29 Chart

30 Chart 24 Standard & Poors RatingsDirect on the Global Credit Portal February 17,

31 Chart

32 Chart 26 Related Criteria And Research Economic Research: Assessing The Severity Of The Eurozone Recession Is A Close Call, Jan. 31, 2012 Various Rating Actions Taken On 340 European Structured Finance Tranches After Eurozone Sovereign Rating Actions, Jan. 23, 2012 Italy's Unsolicited Ratings Lowered To 'BBB+/A-2'; Outlook Negative, Jan. 13, 2012 Ratings On 305 Tranches In 120 European RMBS Transactions Placed On CreditWatch Negative After Bank Rating Actions, Dec. 21, 2011 Economic Research: The Specter Of A Double Dip In Europe Looms Larger, Oct. 4, 2011 Nonsovereign Ratings That Exceed EMU Sovereign Ratings: Methodology And Assumptions, June 14, 2011, Counterparty And Supporting Obligations Update, Jan. 13, 2011 Counterparty and Supporting Obligations Methodology and Assumptions, Dec. 6, 2010 Update To The Cash Flow Criteria For European RMBS Transactions, Jan. 6, 2009 Update To The Criteria For Rating Italian Residential Mortgage-Backed Securities, Jan. 6, 2009 Revised Italian RMBS High Constant Payment Rate Assumption, Oct. 14, 2008 Keeping Up With The Diversity: Navigating The Multifarious Italian RMBS Market, May 11, 2006 Additional Contact: Structured Finance Europe; [email protected] Standard & Poors RatingsDirect on the Global Credit Portal February 17,

33 Copyright 2012 by Standard & Poor's Financial Services LLC. All rights reserved. No content (including ratings, credit-related analyses and data, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is provided on an "as is" basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING WILL BE UNINTERRUPTED, OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility of such damages. Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. S&P's opinions, analyses, and rating acknowledgment decisions (described below) are not recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives. To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P reserves the right to assign, withdraw, or suspend such acknowledgement at any time and in its sole discretion. S&P Parties disclaim any duty whatsoever arising out of the assignment, withdrawal, or suspension of an acknowledgment as well as any liability for any damage alleged to have been suffered on account thereof. S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain nonpublic information received in connection with each analytical process. S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites, (free of charge), and and (subscription), and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available at

UBI Banca Ratings Lowered To 'BBB-/A-3' On Heightened Economic And Industry Risks In Italy; Outlook Negative

Research Update: UBI Banca Ratings Lowered To 'BBB-/A-3' On Heightened Economic And Industry Risks In Italy; Outlook Negative Analytical Group Contact: Financial Institutions Ratings Europe; [email protected]

Research Update: UBI Banca Ratings Lowered To 'BBB-/A-3' On Heightened Economic And Industry Risks In Italy; Outlook Negative Analytical Group Contact: Financial Institutions Ratings Europe; [email protected]

Spanish Multi-Cedulas Rating Actions As Of Aug. 2, 2012

Spanish Multi-Cedulas Rating Actions As Of Aug. 2, 2012 Covered Bonds Frankfurt: Karlo S Fuchs, Analytical Manager, Frankfurt (49) 69-33-999-156; [email protected] Covered Bonds London:

Spanish Multi-Cedulas Rating Actions As Of Aug. 2, 2012 Covered Bonds Frankfurt: Karlo S Fuchs, Analytical Manager, Frankfurt (49) 69-33-999-156; [email protected] Covered Bonds London:

Four Ratings Raised From GreatAmerica Leasing Receivables Funding L.L.C.; 10 Ratings Affirmed

Four s Raised From GreatAmerica Leasing Receivables Funding L.L.C.; 10 s Affirmed Primary Credit Analyst: Srabani C Chandra-Lal, New York (1) 212-438-5036; [email protected] Secondary

Four s Raised From GreatAmerica Leasing Receivables Funding L.L.C.; 10 s Affirmed Primary Credit Analyst: Srabani C Chandra-Lal, New York (1) 212-438-5036; [email protected] Secondary

Pohjola Non-Life Insurance Downgraded To 'A+' After Government Support Review Of Pohjola Bank; Outlook Remains Negative

Research Update: Pohjola Non-Life Insurance Downgraded To 'A+' After Government Support Review Of Pohjola Bank; Outlook Remains Negative Primary Credit Analyst: Anna Glennmar, Stockholm (46) 8-440-5922;

Research Update: Pohjola Non-Life Insurance Downgraded To 'A+' After Government Support Review Of Pohjola Bank; Outlook Remains Negative Primary Credit Analyst: Anna Glennmar, Stockholm (46) 8-440-5922;

Gemini Securitization Corp., LLC (As Of May 2014)

") ABCP Portfolio Data: Gemini Securitization Corp., LLC (As Of May 2014) Primary Credit Analyst: Thomas G Dunn, New York (1) 212-438-1623; [email protected] Surveillance Credit Analyst: Marc

ABCP Portfolio Data: Gemini Securitization Corp., LLC (As Of May 2014) Primary Credit Analyst: Thomas G Dunn, New York (1) 212-438-1623; [email protected] Surveillance Credit Analyst: Marc

AEG Power Solutions Downgraded To 'CCC-' On Heightened Risk Of Missing An Interest Payment; Outlook Negative

Research Update: AEG Power Solutions Downgraded To 'CCC-' On Heightened Risk Of Missing An Interest Payment; Outlook Negative Primary Credit Analyst: Abigail Klimovich, CFA, London (44) 20-7176-3554; [email protected]

Research Update: AEG Power Solutions Downgraded To 'CCC-' On Heightened Risk Of Missing An Interest Payment; Outlook Negative Primary Credit Analyst: Abigail Klimovich, CFA, London (44) 20-7176-3554; [email protected]

Research Update: Danish Mortgage Bank DLR Kredit A/S Assigned 'BBB+/A-2' Ratings. Table Of Contents

May 31, 2012 Research Update: Danish Mortgage Bank DLR Kredit A/S Assigned 'BBB+/A-2' Ratings Primary Credit Analyst: Per Tornqvist, Stockholm (46) 8-440-5904;[email protected] Secondary

May 31, 2012 Research Update: Danish Mortgage Bank DLR Kredit A/S Assigned 'BBB+/A-2' Ratings Primary Credit Analyst: Per Tornqvist, Stockholm (46) 8-440-5904;[email protected] Secondary

AEG Power Solutions Downgraded To 'CCC+' On Weak Earnings And Delays In Customer Payments; Outlook Negative

Research Update: AEG Power Solutions Downgraded To 'CCC+' On Weak Earnings And Delays In Customer Payments; Outlook Negative Primary Credit Analyst: Abigail Klimovich, CFA, London (44) 20-7176-3554; [email protected]

Research Update: AEG Power Solutions Downgraded To 'CCC+' On Weak Earnings And Delays In Customer Payments; Outlook Negative Primary Credit Analyst: Abigail Klimovich, CFA, London (44) 20-7176-3554; [email protected]

RBS Citizens Financial Group Ratings Affirmed; Outlook Remains Negative; Stand-Alone Credit Profile Lowered To 'a-'

Research Update: RBS Citizens Financial Group Ratings Affirmed; Outlook Remains Negative; Stand-Alone Credit Profile Lowered To 'a-' Primary Credit Analyst: Barbara Duberstein, New York (1) 212-438-5656;

Research Update: RBS Citizens Financial Group Ratings Affirmed; Outlook Remains Negative; Stand-Alone Credit Profile Lowered To 'a-' Primary Credit Analyst: Barbara Duberstein, New York (1) 212-438-5656;

Residential Real Estate Company Deutsche Wohnen 'BBB+' Ratings Placed On CreditWatch Negative On Conwert Takeover Offer

Research Update: Residential Real Estate Company Deutsche Wohnen 'BBB+' Ratings Placed On CreditWatch Negative On Conwert Takeover Offer Primary Credit Analyst: Marie-Aude Vialle, London (44) 20-7176-3655;

Research Update: Residential Real Estate Company Deutsche Wohnen 'BBB+' Ratings Placed On CreditWatch Negative On Conwert Takeover Offer Primary Credit Analyst: Marie-Aude Vialle, London (44) 20-7176-3655;

Kuwait Projects Co. (Holding) Affirmed At 'BBB-/A-3'; Outlook Stable

Affirmed At 'BBB-/A-3'; Outlook Stable") Research Update: Kuwait Projects Co. (Holding) Affirmed At 'BBB-/A-3'; Outlook Stable Primary Credit Analyst: Per Karlsson, Stockholm (46) 8-440-5927; [email protected] Secondary Contact:

Research Update: Kuwait Projects Co. (Holding) Affirmed At 'BBB-/A-3'; Outlook Stable Primary Credit Analyst: Per Karlsson, Stockholm (46) 8-440-5927; [email protected] Secondary Contact:

Spain-Based IT Service Provider Amadeus IT Holding Rating Raised To 'BBB/A-2' On Strong Financials, Outlook Stable

Research Update: Spain-Based IT Service Provider Amadeus IT Holding Rating Raised To 'BBB/A-2' On Strong Financials, Outlook Stable Primary Credit Analyst: Stefan Kirschner, Frankfurt (49) 69-33-999-281;

Research Update: Spain-Based IT Service Provider Amadeus IT Holding Rating Raised To 'BBB/A-2' On Strong Financials, Outlook Stable Primary Credit Analyst: Stefan Kirschner, Frankfurt (49) 69-33-999-281;

Lake Oswego, Oregon; Water/Sewer

Summary: Lake Oswego, Oregon; Water/Sewer Primary Credit Analyst: Aaron Lee, San Francisco (1) 415-371-5066; [email protected] Secondary Contact: Tim Tung, San Francisco (415) 371-5041; [email protected]

Summary: Lake Oswego, Oregon; Water/Sewer Primary Credit Analyst: Aaron Lee, San Francisco (1) 415-371-5066; [email protected] Secondary Contact: Tim Tung, San Francisco (415) 371-5041; [email protected]

Danish Bank DLR Kredit Affirmed At 'BBB+/A-2'; Junior Subordinated Debt Downgraded To 'BB'; Outlook Remains Stable

Research Update: Danish Bank DLR Kredit Affirmed At 'BBB+/A-2'; Junior Subordinated Debt Downgraded To 'BB'; Outlook Remains Stable Primary Credit Analyst: Sean Cotten, Stockholm (46) 8-440-5928; [email protected]

Research Update: Danish Bank DLR Kredit Affirmed At 'BBB+/A-2'; Junior Subordinated Debt Downgraded To 'BB'; Outlook Remains Stable Primary Credit Analyst: Sean Cotten, Stockholm (46) 8-440-5928; [email protected]

Volkswagen Bank Ratings Lowered To 'A-/A-2'; Outlook Negative

Research Update: Volkswagen Bank Ratings Lowered To 'A-/A-2'; Outlook Negative Primary Credit Analyst: Salla von Steinaecker, Frankfurt (49) 69-33-999-164; [email protected] Secondary

Research Update: Volkswagen Bank Ratings Lowered To 'A-/A-2'; Outlook Negative Primary Credit Analyst: Salla von Steinaecker, Frankfurt (49) 69-33-999-164; [email protected] Secondary

Electricity Transmission System Operator TenneT's Hybrid Equity Content Revised To Intermediate; 'A-' Ratings Affirmed

Research Update: Electricity Transmission System Operator TenneT's Hybrid Equity Content Revised To Intermediate; 'A-' Ratings Affirmed Primary Credit Analyst: Beatrice de Taisne, CFA, London (44) 20-7176-3938;

Research Update: Electricity Transmission System Operator TenneT's Hybrid Equity Content Revised To Intermediate; 'A-' Ratings Affirmed Primary Credit Analyst: Beatrice de Taisne, CFA, London (44) 20-7176-3938;

Lloyds Banking Group Life Insurance Operations 'A' Ratings Affirmed And Removed From CreditWatch; Outlook Stable

Research Update: Lloyds Banking Group Life Insurance Operations 'A' Ratings Affirmed And Removed From CreditWatch; Outlook Stable Primary Credit Analyst: Oluwatosin S Adesiyan, London (44) 20-7176-3279;

Research Update: Lloyds Banking Group Life Insurance Operations 'A' Ratings Affirmed And Removed From CreditWatch; Outlook Stable Primary Credit Analyst: Oluwatosin S Adesiyan, London (44) 20-7176-3279;

Standard & Poor's Puts Ratings On Eurozone Sovereigns On CreditWatch With Negative Implications

December 5, 2011 Standard & Poor's Puts Ratings On Eurozone Sovereigns On CreditWatch With Negative Implications Primary Credit Analysts: Moritz Kraemer, Frankfurt (49) 69-33-99-9249; [email protected]

December 5, 2011 Standard & Poor's Puts Ratings On Eurozone Sovereigns On CreditWatch With Negative Implications Primary Credit Analysts: Moritz Kraemer, Frankfurt (49) 69-33-99-9249; [email protected]

Market Data Analysis - Pacific Life

Research Update: 'A+', Pacific LifeCorp 'BBB+' Ratings Affirmed; Outlook Stable; New Senior Notes Rated 'BBB+' Primary Credit Analyst: Carmi Margalit, CFA, New York (1) 212-438-1000; [email protected]

Research Update: 'A+', Pacific LifeCorp 'BBB+' Ratings Affirmed; Outlook Stable; New Senior Notes Rated 'BBB+' Primary Credit Analyst: Carmi Margalit, CFA, New York (1) 212-438-1000; [email protected]

R.V.I. Guaranty Co. Ltd. And Subsidiaries 'BBB' Ratings Affirmed After Insurance Criteria Change; The Outlook Is Stable

Research Update: R.V.I. Guaranty Co. Ltd. And Subsidiaries 'BBB' Ratings Affirmed After Insurance Criteria Change; The Outlook Is Stable Primary Credit Analyst: David S Veno, New York (1) 212-438-2108;

Research Update: R.V.I. Guaranty Co. Ltd. And Subsidiaries 'BBB' Ratings Affirmed After Insurance Criteria Change; The Outlook Is Stable Primary Credit Analyst: David S Veno, New York (1) 212-438-2108;

Research Update: Ratings Lowered On Netherlands-Based SNS REAAL N.V. Group And Core Subs On Slower Recovery Prospects; Outlook Stable

March 1, 2012 Research Update: Ratings Lowered On Netherlands-Based SNS REAAL N.V. Group And Core Subs On Slower Recovery Prospects; Outlook Stable Primary Credit Analysts: Alexandre Birry, London 44 (0)

March 1, 2012 Research Update: Ratings Lowered On Netherlands-Based SNS REAAL N.V. Group And Core Subs On Slower Recovery Prospects; Outlook Stable Primary Credit Analysts: Alexandre Birry, London 44 (0)

Turkey-Based Appliance Manufacturer Vestel Outlook Revised To Positive; 'B-' Rating Affirmed

Research Update: Turkey-Based Appliance Manufacturer Vestel Outlook Revised To Positive; 'B-' Rating Affirmed Primary Credit Analyst: Alexander Griaznov, Moscow (7) 495-783-4109; [email protected]

Research Update: Turkey-Based Appliance Manufacturer Vestel Outlook Revised To Positive; 'B-' Rating Affirmed Primary Credit Analyst: Alexander Griaznov, Moscow (7) 495-783-4109; [email protected]

Swedbank Outlook Revised To Stable From Negative On Improved Business Position; Ratings Affirmed At 'A+/A-1'

Research Update: Swedbank Outlook Revised To Stable From Negative On Improved Business Position; Ratings Primary Credit Analyst: Alexander Ekbom, Stockholm (46) 8-440-5911; [email protected]

Research Update: Swedbank Outlook Revised To Stable From Negative On Improved Business Position; Ratings Primary Credit Analyst: Alexander Ekbom, Stockholm (46) 8-440-5911; [email protected]

S&P Takes Rating Actions On Section 15 Bonds Issued By Various Danish Mortgage Banks

S&P Takes Rating Actions On Section 15 Bonds Issued By Various Danish Mortgage Banks Primary Credit Analyst: Casper R Andersen, London (44) 20-7176-6757; [email protected] Secondary

S&P Takes Rating Actions On Section 15 Bonds Issued By Various Danish Mortgage Banks Primary Credit Analyst: Casper R Andersen, London (44) 20-7176-6757; [email protected] Secondary

Six Russian Real Estate Companies On CreditWatch Amid Higher Interest Rates, Weakening Demand, Sharp Ruble Depreciation

Research Update: Six Russian Real Estate Companies On CreditWatch Amid Higher Interest Rates, Weakening Demand, Sharp Ruble Depreciation Primary Credit Analyst: Anton Geyze, Moscow (7) 495-783-4134; [email protected]

Research Update: Six Russian Real Estate Companies On CreditWatch Amid Higher Interest Rates, Weakening Demand, Sharp Ruble Depreciation Primary Credit Analyst: Anton Geyze, Moscow (7) 495-783-4134; [email protected]

German Utility RWE Downgraded To 'BBB-/A-3'; Outlook Negative

Research Update: German Utility RWE Downgraded To 'BBB-/A-3'; Outlook Negative Primary Credit Analyst: Vittoria Ferraris, Milan (39) 02-72111-207; [email protected] Secondary Contact: Tobias

Research Update: German Utility RWE Downgraded To 'BBB-/A-3'; Outlook Negative Primary Credit Analyst: Vittoria Ferraris, Milan (39) 02-72111-207; [email protected] Secondary Contact: Tobias

Research Update: Banco Monex S.A. Rated Global Scale 'BB+/B', National Scale 'mxa+/mxa-1' Rating Affirmed. Table Of Contents

May 17, 2012 Research Update: Banco Monex S.A. Rated Global Scale 'BB+/B', National Scale 'mxa+/mxa-1' Rating Affirmed Primary Credit Analyst: Arturo Sanchez, Mexico City (52) 55-5081-4468;[email protected]

May 17, 2012 Research Update: Banco Monex S.A. Rated Global Scale 'BB+/B', National Scale 'mxa+/mxa-1' Rating Affirmed Primary Credit Analyst: Arturo Sanchez, Mexico City (52) 55-5081-4468;[email protected]

Bertelsmann SE & Co. KGaA's Hybrid Equity Content Revised To "Intermediate"; 'BBB+/A-2' Ratings Affirmed

Research Update: Bertelsmann SE & Co. KGaA's Hybrid Equity Content Revised To "Intermediate"; 'BBB+/A-2' Ratings Affirmed Primary Credit Analyst: Florence Devevey, Madrid (34) 91-788-7236; [email protected]

Research Update: Bertelsmann SE & Co. KGaA's Hybrid Equity Content Revised To "Intermediate"; 'BBB+/A-2' Ratings Affirmed Primary Credit Analyst: Florence Devevey, Madrid (34) 91-788-7236; [email protected]

Guardian Life Insurance, Core Operating Subsidiaries 'AA+' Ratings Affirmed On Criteria Review, Outlook Negative

Research Update: Guardian Life Insurance, Core Operating Subsidiaries 'AA+' Ratings Affirmed On Criteria Review, Outlook Negative Primary Credit Analyst: Neal I Freedman, New York (1) 212-438-1274; [email protected]

Research Update: Guardian Life Insurance, Core Operating Subsidiaries 'AA+' Ratings Affirmed On Criteria Review, Outlook Negative Primary Credit Analyst: Neal I Freedman, New York (1) 212-438-1274; [email protected]

Italian Veneto Banca 'BB/B' Ratings Affirmed And Removed From CreditWatch Negative Following Review; Outlook Negative

Research Update: Italian Veneto Banca 'BB/B' Ratings Affirmed And Removed From CreditWatch Negative Following Review; Outlook Negative Table Of Contents Overview Rating Action Rationale Outlook Ratings

Research Update: Italian Veneto Banca 'BB/B' Ratings Affirmed And Removed From CreditWatch Negative Following Review; Outlook Negative Table Of Contents Overview Rating Action Rationale Outlook Ratings

Interactive Brokers LLC

Summary: Interactive Brokers LLC Primary Credit Analyst: Clayton D Montgomery, New York (1) 212-438-5079; [email protected] Secondary Contact: Robert B Hoban, New York (1) 212-438-7385;

Summary: Interactive Brokers LLC Primary Credit Analyst: Clayton D Montgomery, New York (1) 212-438-5079; [email protected] Secondary Contact: Robert B Hoban, New York (1) 212-438-7385;

A Financial Analysis of Energies and Gas Pipelines

Research Update: Interconexion Electrica S.A. E.S.P. (ISA) 'BBB' Credit Rating Affirmed, Outlook Remains Stable Primary Credit Analyst: Maria del Sol S Gonzalez, CFA, New York (1) 212-438-4443; [email protected]

Research Update: Interconexion Electrica S.A. E.S.P. (ISA) 'BBB' Credit Rating Affirmed, Outlook Remains Stable Primary Credit Analyst: Maria del Sol S Gonzalez, CFA, New York (1) 212-438-4443; [email protected]

Constellium Holdco B.V. Recovery Rating Profile

Recovery Report: Constellium Holdco B.V. Recovery Rating Profile Recovery Analyst: Franck Rizzoli, London (44) 20-7176-3934; [email protected] Primary Credit Analyst: Tatjana Lescova,

Recovery Report: Constellium Holdco B.V. Recovery Rating Profile Recovery Analyst: Franck Rizzoli, London (44) 20-7176-3934; [email protected] Primary Credit Analyst: Tatjana Lescova,

New York Life Insurance Co. 'AA+/A-1+' Rating Affirmed On Criteria Review; Outlook Stable

Research Update: New York Life Insurance Co. 'AA+/A-1+' Rating Affirmed On Criteria Review; Outlook Stable Primary Credit Analyst: Michael E Gross, San Francisco (1) 415-371-5003; [email protected]

Research Update: New York Life Insurance Co. 'AA+/A-1+' Rating Affirmed On Criteria Review; Outlook Stable Primary Credit Analyst: Michael E Gross, San Francisco (1) 415-371-5003; [email protected]

Dogus Holding 'BB/B' Ratings Affirmed On Sustained Investments And Expected Completion Of Garanti Sale; Outlook Negative

Research Update: Dogus Holding 'BB/B' Ratings Affirmed On Sustained Investments And Expected Completion Of Garanti Sale; Outlook Negative Primary Credit Analyst: Renato Panichi, Milan (39) 02-72111-215;

Research Update: Dogus Holding 'BB/B' Ratings Affirmed On Sustained Investments And Expected Completion Of Garanti Sale; Outlook Negative Primary Credit Analyst: Renato Panichi, Milan (39) 02-72111-215;

Central Texas Regional Mobility Authority; Toll Roads Bridges

Summary: Central Texas Regional Mobility Authority; Toll Roads Bridges Primary Credit Analyst: Todd R Spence, Dallas (1) 214-871-1424; [email protected] Secondary Contact: Peter V Murphy,

Summary: Central Texas Regional Mobility Authority; Toll Roads Bridges Primary Credit Analyst: Todd R Spence, Dallas (1) 214-871-1424; [email protected] Secondary Contact: Peter V Murphy,

Healthcare Support (North Staffs) Finance Outlook Revised To Stable On Operating Risk; 'BBB-' Issue Ratings Affirmed

Finance Outlook Revised To Stable On Operating Risk; 'BBB-' Issue Ratings Affirmed") Research Update: Healthcare Support (North Staffs) Finance Outlook Revised To Stable On Operating Risk; 'BBB-' Issue Ratings Affirmed Primary Credit Analyst: Manuel Dusina, London (44) 20-7176-5530; [email protected]

Research Update: Healthcare Support (North Staffs) Finance Outlook Revised To Stable On Operating Risk; 'BBB-' Issue Ratings Affirmed Primary Credit Analyst: Manuel Dusina, London (44) 20-7176-5530; [email protected]

Mounting Student Debt Is Reshaping The U.S. Student Loan Market

STRUCTURED FINANCE RESEARCH Mounting Student Debt Is Reshaping The U.S. Student Loan Market Primary Credit Analyst: Erkan Erturk, PhD, New York (1) 212-438-2450; [email protected] Business

STRUCTURED FINANCE RESEARCH Mounting Student Debt Is Reshaping The U.S. Student Loan Market Primary Credit Analyst: Erkan Erturk, PhD, New York (1) 212-438-2450; [email protected] Business

Sirius International Group Outlook Revised To Stable On Plans To Retain Its Strategy Post Acquisition; Ratings Affirmed

Research Update: Sirius International Group Outlook Revised To Stable On Plans To Retain Its Strategy Post Acquisition; Ratings Affirmed Primary Credit Analyst: Anvar Gabidullin, CFA, London (44) 20-7176-7047;

Research Update: Sirius International Group Outlook Revised To Stable On Plans To Retain Its Strategy Post Acquisition; Ratings Affirmed Primary Credit Analyst: Anvar Gabidullin, CFA, London (44) 20-7176-7047;

Millenniumbcp Ageas Core Non-Life Insurance Entity 'BB' Ratings On CreditWatch Positive On Announced Ownership Change

Research Update: Millenniumbcp Ageas Core Non-Life Insurance Entity 'BB' Ratings On CreditWatch Positive On Announced Ownership Change Primary Credit Analyst: Gwenaelle Gibert, Paris (33) 1-4420-6693;

Research Update: Millenniumbcp Ageas Core Non-Life Insurance Entity 'BB' Ratings On CreditWatch Positive On Announced Ownership Change Primary Credit Analyst: Gwenaelle Gibert, Paris (33) 1-4420-6693;

Centennial Water and Sanitation District, Colorado; Water/Sewer

Summary: Centennial Water and Sanitation District, Colorado; Water/Sewer Primary Credit Analyst: Scott D Garrigan, Chicago (1) 312-233-7014; [email protected] Secondary Contact: Tim Tung,

Summary: Centennial Water and Sanitation District, Colorado; Water/Sewer Primary Credit Analyst: Scott D Garrigan, Chicago (1) 312-233-7014; [email protected] Secondary Contact: Tim Tung,

Codelco Rating Outlook Revised To Negative On Lower Copper Prices, 'AA-' Rating Affirmed

Research Update: Codelco Rating Outlook Revised To Negative On Lower Copper Prices, 'AA-' Rating Affirmed Primary Credit Analyst: Diego H Ocampo, Sao Paulo (55) 11-3039-9769; [email protected]

Research Update: Codelco Rating Outlook Revised To Negative On Lower Copper Prices, 'AA-' Rating Affirmed Primary Credit Analyst: Diego H Ocampo, Sao Paulo (55) 11-3039-9769; [email protected]

China Life Insurance Co. Ltd.

Primary Credit Analyst: Connie Wong, Singapore (65) 6239-6353; [email protected] Secondary Contact: Philip P Chung, CFA, Singapore (65) 6239-6343; [email protected] Table

Primary Credit Analyst: Connie Wong, Singapore (65) 6239-6353; [email protected] Secondary Contact: Philip P Chung, CFA, Singapore (65) 6239-6343; [email protected] Table

Islamic Development Bank 'AAA/A-1+' Ratings Affirmed On Criteria Revision; Outlook Stable

Research Update: Islamic Development Bank 'AAA/A-1+' Ratings Affirmed On Criteria Revision; Outlook Stable Primary Credit Analyst: Dima B Jardaneh, Dubai (971) 4-372-7154; [email protected]

Research Update: Islamic Development Bank 'AAA/A-1+' Ratings Affirmed On Criteria Revision; Outlook Stable Primary Credit Analyst: Dima B Jardaneh, Dubai (971) 4-372-7154; [email protected]

Ten Japanese Insurers Downgraded; Outlooks On Two Other Insurers Revised Down To Stable Following Downgrade Of Japan

Ten Japanese Insurers Downgraded; Outlooks On Two Other Insurers Revised Down To Stable Following Primary Credit Analyst: Reina Tanaka, Tokyo (81) 3-4550-8587; [email protected] Secondary

Ten Japanese Insurers Downgraded; Outlooks On Two Other Insurers Revised Down To Stable Following Primary Credit Analyst: Reina Tanaka, Tokyo (81) 3-4550-8587; [email protected] Secondary

Evaluating Insurers Enterprise Risk Management Practice

Evaluating Insurers Enterprise Risk Management Practice Li Cheng, CFA, FRM, FSA Director Financial Services Ratings October 3, 2013 Permission to reprint or distribute any content from this presentation

Evaluating Insurers Enterprise Risk Management Practice Li Cheng, CFA, FRM, FSA Director Financial Services Ratings October 3, 2013 Permission to reprint or distribute any content from this presentation

GCC Infrastructure Credit Quality

GCC Infrastructure Credit Quality Karim Nassif Associate Director Corporate and Infrastructure Ratings 18 February 2014 Permission to reprint or distribute any content from this presentation requires the

GCC Infrastructure Credit Quality Karim Nassif Associate Director Corporate and Infrastructure Ratings 18 February 2014 Permission to reprint or distribute any content from this presentation requires the

Workshop B: Credit Spread Trends In The Energy Sector

Workshop B: Credit Spread Trends In The Energy Sector James West Director, FIOTC Product Management 26 November, 2014 Permission to reprint or distribute any content from this presentation requires the

Workshop B: Credit Spread Trends In The Energy Sector James West Director, FIOTC Product Management 26 November, 2014 Permission to reprint or distribute any content from this presentation requires the

Vienna Insurance Group AG Wiener Versicherung Gruppe

Summary: Vienna Insurance Group AG Wiener Versicherung Gruppe Primary Credit Analyst: Johannes Bender, Frankfurt (49) 69-33-999-196; [email protected] Secondary Contact: Ralf Bender,

Summary: Vienna Insurance Group AG Wiener Versicherung Gruppe Primary Credit Analyst: Johannes Bender, Frankfurt (49) 69-33-999-196; [email protected] Secondary Contact: Ralf Bender,

U.K. Broadcaster ITV Upgraded To 'BBB-/A-3' On Expected Solid Credit Metrics, Moderate Financial Policy; Outlook Stable

Research Update: U.K. Broadcaster ITV Upgraded To 'BBB-/A-3' On Expected Solid Credit Metrics, Moderate Financial Policy; Outlook Stable Primary Credit Analyst: Patrizia D'Amico, Milan (39) 02-72111-206;

Research Update: U.K. Broadcaster ITV Upgraded To 'BBB-/A-3' On Expected Solid Credit Metrics, Moderate Financial Policy; Outlook Stable Primary Credit Analyst: Patrizia D'Amico, Milan (39) 02-72111-206;

Stand-Alone Credit Profiles: One Component Of A Rating

General Criteria: Stand-Alone Credit Profiles: One Component Of A Rating Criteria Officer, EMEA Corporates: Emmanuel Dubois-Pelerin, Paris (33) 1-4420-6673; [email protected]

General Criteria: Stand-Alone Credit Profiles: One Component Of A Rating Criteria Officer, EMEA Corporates: Emmanuel Dubois-Pelerin, Paris (33) 1-4420-6673; [email protected]

Lloyds Banking Group Life Insurance Operations 'A' Ratings Affirmed; Outlook Negative

Research Update: Lloyds Banking Group Life Insurance Operations 'A' Ratings Affirmed; Outlook Negative Primary Credit Analyst: Oliver Herbert, London (44) 20-7176-7054; [email protected]

Research Update: Lloyds Banking Group Life Insurance Operations 'A' Ratings Affirmed; Outlook Negative Primary Credit Analyst: Oliver Herbert, London (44) 20-7176-7054; [email protected]

Lear Corp.'s Recovery Rating Profile

Recovery Report: Lear Corp.'s Recovery Rating Profile Primary Credit Analyst: Lawrence Orlowski, CFA, New York (1) 212-438-1000; [email protected] Recovery Analyst: Greg Maddock, New

Recovery Report: Lear Corp.'s Recovery Rating Profile Primary Credit Analyst: Lawrence Orlowski, CFA, New York (1) 212-438-1000; [email protected] Recovery Analyst: Greg Maddock, New

FWD Life Insurance Co. (Bermuda) Ltd. Assigned 'A-' And 'cnaa' Ratings; Outlook Stable

Ltd. Assigned 'A-' And 'cnaa' Ratings; Outlook Stable") Research Update: FWD Life Insurance Co. (Bermuda) Ltd. Assigned 'A-' And 'cnaa' Ratings; Outlook Stable Primary Credit Analyst: Anna Kong, FSA, FRM, Hong Kong (852) 2533-3571; [email protected]

Research Update: FWD Life Insurance Co. (Bermuda) Ltd. Assigned 'A-' And 'cnaa' Ratings; Outlook Stable Primary Credit Analyst: Anna Kong, FSA, FRM, Hong Kong (852) 2533-3571; [email protected]

International Finance Corp. 'AAA/A-1+' Rating Affirmed; Outlook Remains Stable

Research Update: International Finance Corp. 'AAA/A-1+' Rating Affirmed; Outlook Remains Stable Primary Credit Analyst: Elie Heriard Dubreuil, London (44) 207-176-7302; [email protected]

Research Update: International Finance Corp. 'AAA/A-1+' Rating Affirmed; Outlook Remains Stable Primary Credit Analyst: Elie Heriard Dubreuil, London (44) 207-176-7302; [email protected]

Methodology: Business Risk/Financial Risk Matrix Expanded

Criteria Corporates General: Methodology: Business Risk/Financial Risk Matrix Expanded Criteria Officer: Mark Puccia, Managing Director, New York (1) 212-438-7233; [email protected] Table

Criteria Corporates General: Methodology: Business Risk/Financial Risk Matrix Expanded Criteria Officer: Mark Puccia, Managing Director, New York (1) 212-438-7233; [email protected] Table