Collateralization, Bank Loan Rates and Monitoring

|

|

|

- Marilyn Palmer

- 10 years ago

- Views:

Transcription

1 Collateralization, Bank Loan Rates and Monitoring Geraldo Cerqueiro Universidade ecatólica a Portuguesa Steven Ongena University of Zurich, SFI and CEPR Kasper Roszbach Sveriges Riksbank and University of Groningen Day Ahead Conference, Federal Reserve Bank of Philadelphia January 2, 2014 The views expressed in this paper are solely the responsibility of the authors and should not be interpreted as reflecting the views of the Executive Board of Sveriges Riksbank.

2 This paper: attempts to take a step forward in identifying the role that collateral plays in debt contracts, for credit availability and for bank monitoring; uses a unique dataset from a large bank containing frequently updated internal assessments of collateral values, and finds that, in response to a legal reform that exogenously reduced collateral values, the bank increased interest rates, tightened credit limits, and reduced the intensity of its monitoring of both borrowers and collateral This spurred delinquency on tax payments by borrowers, documenting the economic importance of (i) collateral for borrowers and (ii) lender seniority for banks 2

collateral for borrowers and (ii) lender seniority for")

3 We find that An exogenous reduction in the collateral coverage ratio (collateral/ loan exposure, mean = 47%) of 6 percentage points was followed by Changes in contract features Increase in the loan spread by 20 bps (mean spread = 4.1%, mean rate = 6.6%) 11 percent reduction in borrower s lending limit in the bank A drop in monitoring activity 2.3 months extra between collateral reviews (mean = 10.3 months) 0.8 months (25 days) extra between borrower reviews (mean = 12.2 months) An increase in borrower delinquencies 12 percentage points rise of firms with delayed tax payments (mean = 7%) 3

0.8 months (25 days) extra between borrower reviews (mean = 12.")

4 Motivation Collateral is used all over the world to facilitate lending by alleviating information asymmetries Collateral can have aggregate implications Fluctuations in collateral values can generate credit cycles: Bernanke Gertler (1989), Kiyotaki Moore (1997) Affects dbt debt capacity and investment: t Gan (2007); Vig (2011); Chaney et al. 2009) However: still know more about theoretical motivations for using collateral than about its empirical workings Partly due to data limitations partly due to simultaneity issues involving debt contract parameters 4

However: still know more about theoretical motivations for using collateral than about its empirical workings Partly due to data")

5 This paper deals with role of collateral at micro level How does pledged ld dcollateral l influence loan rates and the availability of credit? An ex ante sorting device or means to influence ex post borrower behavior? [Bester, 1985; Chan Thakor, 1987; Boot Thakor, 1994] Empirical evidence: Ex post concerns dominate [Berger Frame Ioanniddou, 2010)] positive relation between collateral and loan rates [Brick Palia, 2007); Bharath et al. 2007] But: difficult to address simultaneity of rates and collateral posting How does collateral affect bank monitoring? Substitutes for screening [Manove Padilla Pagano, 2001] Affects bank monitoring [Berglöf Von Thadden, 1994, Rajan Winton, 1995, Longhofer Santos, 2000] Empirical evidence: Collateralized claims are better monitored [Ono Uesugui, 2009; Argentiero, 2009] 5

![[Bester, 1985; Chan Thakor, 1987; Boot Thakor, 1994] Empirical evidence: Ex post concerns dominate [Berger Frame Ioanniddou, 2010)] positive relation between collateral and loan rates [Brick Palia,](/docs-images/55/9065023/images/page_5.jpg "2007); Bharath et al. 2007] But: difficult to address simultaneity of rates and collateral posting How does collateral affect bank monitoring?")

6 What are floating liens A special collateral right Compares to US FL; UK (floating charge), AUS (chattel pledge) Typically constitutes a prioritized collateral claim on personal (i.e., moveable) as opposed to real property related to a business Assets can be called not only in case of bankruptcy but when other creditor seizes assets Pool of underlying assets can vary over time, assets remain available for operations of business In Sweden, some classes of assets were excluded from the FL such as: cash, money in bank accounts and assets that that can be mortgaged in other ways (typically real estate and financial assets like stock and bonds) 6

as opposed to real property related to a business Assets can be called not only in case of bankruptcy but when other creditor seizes assets Pool of")

7 Exploit an experimental setting A change in the law in Sweden altered the value of floating liens (FL), a common collateral type in Sweden. As of 1 January 2004: Special priority rights of old and new floating liens (FL) were weakened and converted into normal priority rights: Assets can now only be claimed in case of bankruptcy Share of assets that could serve as FL collateral restricted to 55% of their total, but types of assets slightly widened. Purpose to reduce the value of FL collateral Official i records of the Parliamentary Committee on Civil il Law: Give stronger incentives for banks in credit granting decisions to analyze profitability, do ongoing monitoring and weaken incentives to secure collateral. [and] avoid inefficient liquidations and improve opportunities for temporarily troubled but essentially e pofia profitable businesses ui e to re emerge. e e 7

8 Data All Swedish corporate accounts of a large Nordic Baltic commercial bank All loan files kept by bank for each borrower between 2002:04 and 2005:09, monthly frequency Focus on business loans (those with a pre determined quarterly repayment schedule) not secured by standardized collateral such as cars, real estate, etc. but may be secured by floating lien Loan rates on business loans are adjustable at quarterly basis only contract term that is adjustable (!) Matched with official i register it of pledged ld dfloating liens maintained i dby Swedish Companies Registration Office 8

9 9

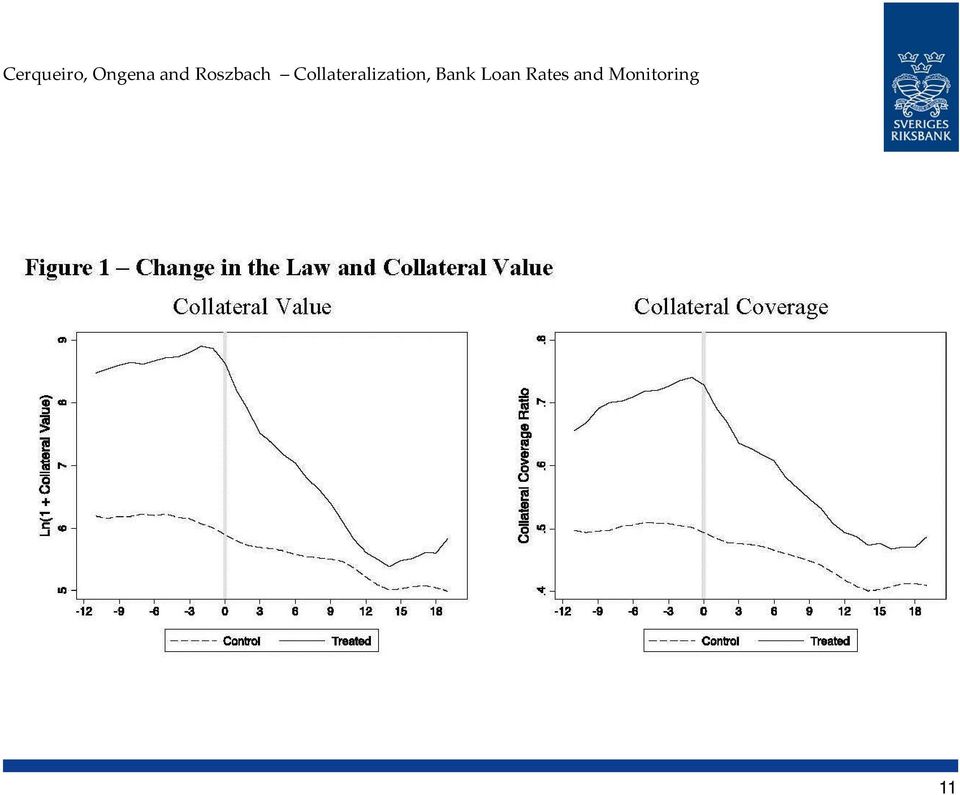

10 Result #1 There is a deterioration in the value of the floating lien as assessed by the bank 10

11 11

12 Mean collateral ratio = % Standard deviation: % Treated = % 12

13 Result #2 The drop in collateral values results in: A tightening of the adjustable terms of the outstanding collateralized loans, A reduced willingness of the bank to lend (credit supply) to the firm. 13

to")

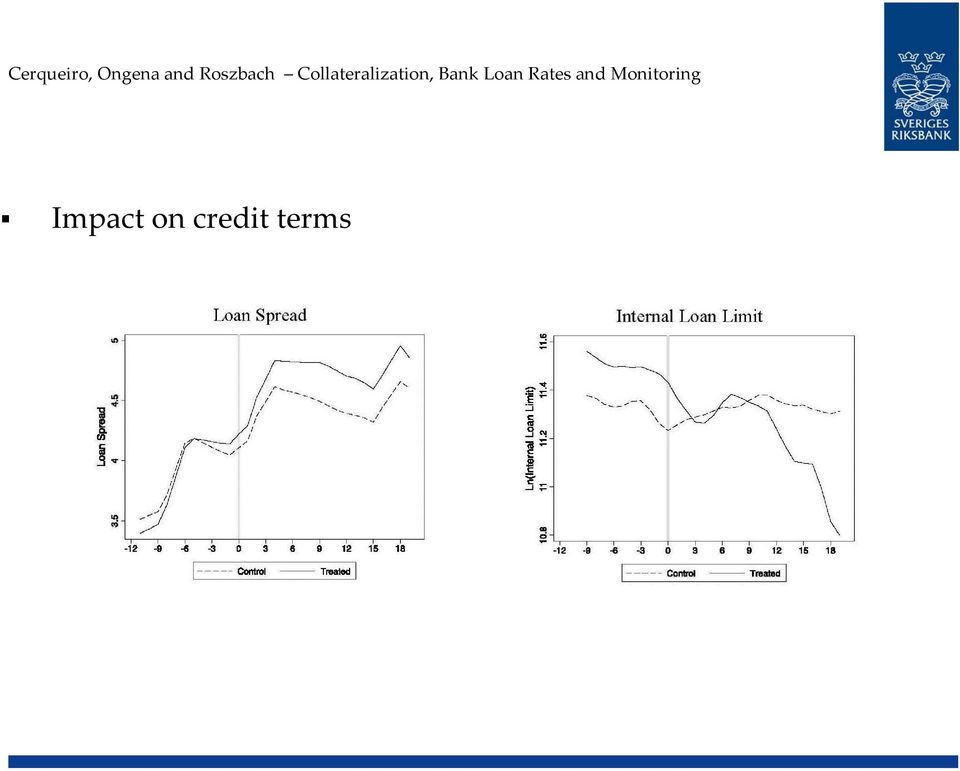

14 Impact on credit terms

15 Mean loan spread = 4.28 % Standard deviation: 0.11 % Mean internal limit= EUR 177,080 Standard deviation: EUR 2,616, = 4.68 % Exp(ln(177,080) 0.11) = EUR 158,634 15

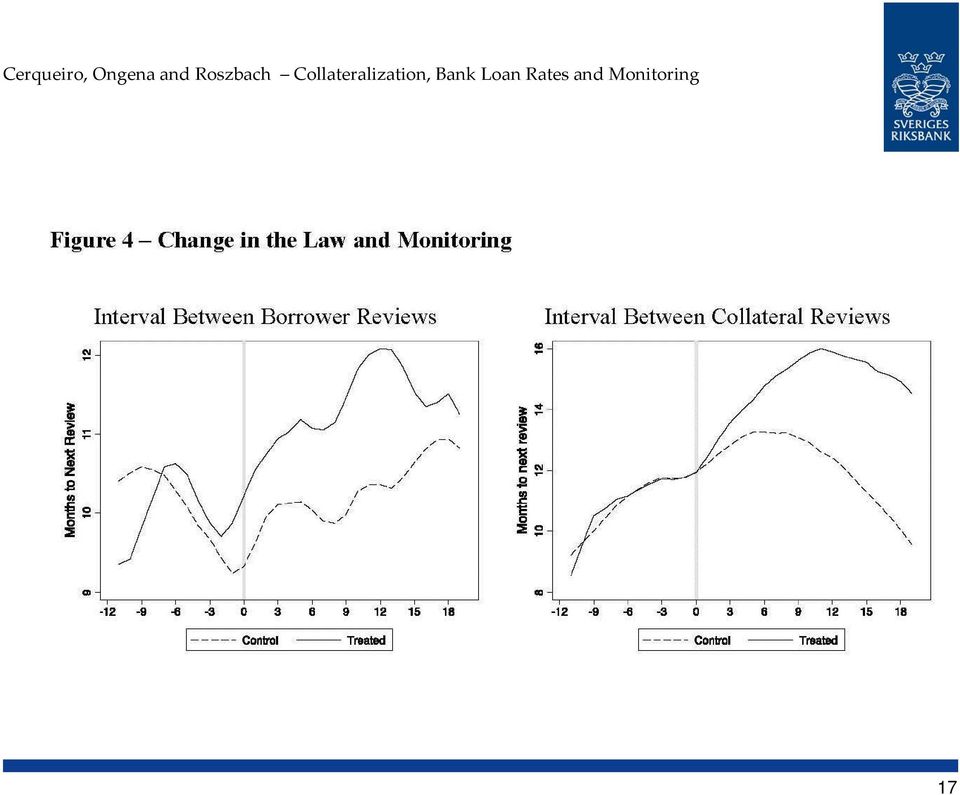

16 Result #3 The loss of collateral also results in: A decrease in the monitoring of this collateral by the bank : Rajan and Winton (JF 1995): collateral can improve lendersʹ incentives to monitor when the value of the assets pledged is risky An ambiguous effect on the monitoring by the bank of the borrower given that the decrease in monitoring of this collateral may be more than offset by increased monitoring of borrower operations and cash flows Hence net effect may be negative or positive, but possibly smaller? 16

17 17

18 Mean time = months Standard deviation: 4.33 months 25 days increase = months Mean time = months Standard deviation: 9.08 months = months

19 Robustness and symmetry y Placebo test: redo for lease contracts as control group Differential trends (before and after) Non linear effect over time of treatment After treatment period restricted to December 31 st, 2004 Treated Winners : borrowers that pledged a floating lien to any other creditor than our bank before 2004 Find similar opposite effects for collateral coverage, loan rates and collateral monitoring 19

20 Result #4 Delinquencies on tax payments to the tax authorities increase significantly ifi (VAT payments, employers taxes, court injunctions) 20

21 Change in the Law and Borrower Delinquency on Tax Payments Fraction of fi.1.05 firms with remarks Control Treated 21

22 Change in the Law and Borrower Delinquency Treated 0.12*** Dependent variable: Post - Pre Difference of Borrower Missed a Tax Payment (5.06) Constant 0.03*** (4.73) Observations 2,580 R-squared

23 Conclusion When we use a change in law in Sweden that exogenously reduced the value of floating liens, we find that: Collateral is important for both lender and borrower The exogenous decrease in collateral values led to: An increase in lending rates A reduction in credit supply A reduction in bank monitoring frequency Our findings suggest that while pledging high quality collateral enables borrowers to pay lower loan rates and benefit from increased credit availability, it also preserves banks incentives to monitor the borrower. 23

24 How do our findings relate to recent empirical work? Findings are consistent with: Haselmann, Pistor and Vig (2010): Strengthening legal rules designed to protect creditors claims outside bankruptcy increased bank klending in transition ii countries Berger, Frame & Ioannidou (2010): Document that collateral serves primarily as a contractual device to solve moral hazard problems. Our findings complement: Vig (2011): Reform that improved ability of lenders to access the collateral of the firm reduced corporate secured debt, debt maturity, and asset growth in India. Introduced a liquidation bias and firms alter their debt structures to contract around it Rodano, Serrano Velarde & Tarantino (2011): Reforms of Italian bankruptcy law strengthening firms rights to renegotiate outstanding deals with creditors increased funding cost for SME; But law simplifying liquidation procedure decreased funding cost Benmelech et al. (2008, 2009, 2011); (Gavazza, 2010): examine the effects of liquidation value on financial contracts using the redeployability of assets 24

25 THANK YOU 25

26 Extra slide How this paper complements literature on liquidation values and financial contracts Has access to precise collateral values as assessed by the creditor. Analyzes a separate determinant of liquidation value: an exogenous decrease in the value of a special priority right claim Also analyze the role of the priority structure of claims: provide an estimate of the value of creditor seniority. Although the priority structure of creditors is key in corporate finance theory, direct empirical evidence on the actual value of debt seniority is scant. 26

FEDERAL HOUSING FINANCE AGENCY

FEDERAL HOUSING FINANCE AGENCY ADVISORY BULLETIN AB 2012-02 FRAMEWORK FOR ADVERSELY CLASSIFYING LOANS, OTHER REAL ESTATE OWNED, AND OTHER ASSETS AND LISTING ASSETS FOR SPECIAL MENTION Introduction This

FEDERAL HOUSING FINANCE AGENCY ADVISORY BULLETIN AB 2012-02 FRAMEWORK FOR ADVERSELY CLASSIFYING LOANS, OTHER REAL ESTATE OWNED, AND OTHER ASSETS AND LISTING ASSETS FOR SPECIAL MENTION Introduction This

Small Business Borrowing and the Owner Manager Agency Costs: Evidence on Finnish Data. Jyrki Niskanen Mervi Niskanen 10.11.2005

Small Business Borrowing and the Owner Manager Agency Costs: Evidence on Finnish Data Jyrki Niskanen Mervi Niskanen 10.11.2005 Abstract. This study investigates the impact that managerial ownership has

Small Business Borrowing and the Owner Manager Agency Costs: Evidence on Finnish Data Jyrki Niskanen Mervi Niskanen 10.11.2005 Abstract. This study investigates the impact that managerial ownership has

Financial-Institutions Management. Solutions 6

Solutions 6 Chapter 25: Loan Sales 2. A bank has made a three-year $10 million loan that pays annual interest of 8 percent. The principal is due at the end of the third year. a. The bank is willing to

Solutions 6 Chapter 25: Loan Sales 2. A bank has made a three-year $10 million loan that pays annual interest of 8 percent. The principal is due at the end of the third year. a. The bank is willing to

Discussion of Capital Injection, Monetary Policy, and Financial Accelerators

Discussion of Capital Injection, Monetary Policy, and Financial Accelerators Karl Walentin Sveriges Riksbank 1. Background This paper is part of the large literature that takes as its starting point the

Discussion of Capital Injection, Monetary Policy, and Financial Accelerators Karl Walentin Sveriges Riksbank 1. Background This paper is part of the large literature that takes as its starting point the

Economic Commentaries

n Economic Commentaries In its Financial Stability Report 214:1, the Riksbank recommended that a requirement for the Liquidity Coverage Ratio (LCR) in Swedish kronor be introduced. The background to this

n Economic Commentaries In its Financial Stability Report 214:1, the Riksbank recommended that a requirement for the Liquidity Coverage Ratio (LCR) in Swedish kronor be introduced. The background to this

WHAT IS BUSINESS CREDIT?

1 WHAT IS BUSINESS CREDIT? Why Do I Need Credit? Establishing a good credit rating is an important financial priority for every business. Having good business credit means that owners of businesses can

1 WHAT IS BUSINESS CREDIT? Why Do I Need Credit? Establishing a good credit rating is an important financial priority for every business. Having good business credit means that owners of businesses can

INTERNET APPENDIX TIME FOR A CHANGE : LOAN CONDITIONS AND BANK BEHAVIOR WHEN FIRMS SWITCH BANKS. This appendix contains additional material:

INTERNET APPENDIX TO TIME FOR A CHANGE : LOAN CONDITIONS AND BANK BEHAVIOR WHEN FIRMS SWITCH BANKS This appendix contains additional material: I. Assumptions II. Simulations III. Static Results IV. Dynamic

INTERNET APPENDIX TO TIME FOR A CHANGE : LOAN CONDITIONS AND BANK BEHAVIOR WHEN FIRMS SWITCH BANKS This appendix contains additional material: I. Assumptions II. Simulations III. Static Results IV. Dynamic

Chapter 14. Understanding Financial Contracts. Learning Objectives. Introduction

Chapter 14 Understanding Financial Contracts Learning Objectives Differentiate among the different mechanisms of external financing of firms Explain why mechanisms of external financing depend upon firm

Chapter 14 Understanding Financial Contracts Learning Objectives Differentiate among the different mechanisms of external financing of firms Explain why mechanisms of external financing depend upon firm

An Empirical Analysis of Insider Rates vs. Outsider Rates in Bank Lending

An Empirical Analysis of Insider Rates vs. Outsider Rates in Bank Lending Lamont Black* Indiana University Federal Reserve Board of Governors November 2006 ABSTRACT: This paper analyzes empirically the

An Empirical Analysis of Insider Rates vs. Outsider Rates in Bank Lending Lamont Black* Indiana University Federal Reserve Board of Governors November 2006 ABSTRACT: This paper analyzes empirically the

So You Want to Borrow Money to Start a Business?

So You Want to Borrow Money to Start a Business? M any small business owners cannot understand why a lending institution would refuse to lend them money. Others have no trouble getting money, but they

So You Want to Borrow Money to Start a Business? M any small business owners cannot understand why a lending institution would refuse to lend them money. Others have no trouble getting money, but they

CORPORATE INTERROGATORIES IN AID OF EXECUTION

LIST 1. Copies of all income tax returns filed by the corporation for the past three calendar years. 2. The original of all certificates of stock owned or beneficially held by the corporation, either alone

LIST 1. Copies of all income tax returns filed by the corporation for the past three calendar years. 2. The original of all certificates of stock owned or beneficially held by the corporation, either alone

Leveraged Bank Loans. Prudential Investment Management-Fixed Income. Leveraged Loans: Capturing Investor Attention August 2005

Prudential Investment Management-Fixed Income Leveraged Loans: Capturing Investor Attention August 2005 Ross Smead Head of US Bank Loan Team, Prudential Investment Management-Fixed Income Success in today

Prudential Investment Management-Fixed Income Leveraged Loans: Capturing Investor Attention August 2005 Ross Smead Head of US Bank Loan Team, Prudential Investment Management-Fixed Income Success in today

Real Estate & Mortgage Investment Specialists

Your Real Estate & Mortgage Investment Specialists Private Lending FAQ s 1. Why Should I Invest In A Mortgage? A mortgage is a loan in which real estate or property is used as collateral. When an individual

Your Real Estate & Mortgage Investment Specialists Private Lending FAQ s 1. Why Should I Invest In A Mortgage? A mortgage is a loan in which real estate or property is used as collateral. When an individual

Selecting sources of finance for business

Selecting sources of finance for business by Steve Jay 08 Sep 2003 This article considers the practical issues facing a business when selecting appropriate sources of finance. It does not consider the

Selecting sources of finance for business by Steve Jay 08 Sep 2003 This article considers the practical issues facing a business when selecting appropriate sources of finance. It does not consider the

Lending 101 The Basics

Lending 101 The Basics Overview Loan categories Credit types Different loan types Interest rate Applying for a loan Credit & credit reports Simple loan tips Test Loan Categories Secured loan - a loan that

Lending 101 The Basics Overview Loan categories Credit types Different loan types Interest rate Applying for a loan Credit & credit reports Simple loan tips Test Loan Categories Secured loan - a loan that

Collateral, Type of Lender and Relationship Banking as Determinants of Credit Risk

Collateral, Type of Lender and Relationship Banking as Determinants of Credit Risk Gabriel Jiménez Jesús Saurina Bank of Spain. Directorate-General of Banking Regulation May 2003 Abstract This paper analyses

Collateral, Type of Lender and Relationship Banking as Determinants of Credit Risk Gabriel Jiménez Jesús Saurina Bank of Spain. Directorate-General of Banking Regulation May 2003 Abstract This paper analyses

Economic Factors Affecting Small Business Lending and Loan Guarantees

Order Code RL34400 Economic Factors Affecting Small Business Lending and Loan Guarantees February 28, 2008 N. Eric Weiss Analyst in Financial Economics Government & Finance Division Economic Factors Affecting

Order Code RL34400 Economic Factors Affecting Small Business Lending and Loan Guarantees February 28, 2008 N. Eric Weiss Analyst in Financial Economics Government & Finance Division Economic Factors Affecting

Aggregate Risk and the Choice Between Cash and Lines of Credit

Aggregate Risk and the Choice Between Cash and Lines of Credit Viral Acharya NYU Stern School of Business, CEPR, NBER Heitor Almeida University of Illinois at Urbana Champaign, NBER Murillo Campello Cornell

Aggregate Risk and the Choice Between Cash and Lines of Credit Viral Acharya NYU Stern School of Business, CEPR, NBER Heitor Almeida University of Illinois at Urbana Champaign, NBER Murillo Campello Cornell

Accounts Receivable and Inventory Financing

Accounts Receivable and Inventory Financing Glossary Accounts Payable - A current liability representing the amount owed by an individual or a business to a creditor for merchandise or services purchased

Accounts Receivable and Inventory Financing Glossary Accounts Payable - A current liability representing the amount owed by an individual or a business to a creditor for merchandise or services purchased

Use this section to learn more about business loans and specific financial products that might be right for your company.

Types of Financing Use this section to learn more about business loans and specific financial products that might be right for your company. Revolving Line Of Credit Revolving lines of credit are the most

Types of Financing Use this section to learn more about business loans and specific financial products that might be right for your company. Revolving Line Of Credit Revolving lines of credit are the most

Basel III: The Net Stable Funding Ratio

POSITION PAPER Our reference: 2014/00010 1 (10) 11/04/2014 Basel Committee on Banking Supervision Consultative Document Basel III: The Net Stable Funding Ratio Key suggestions to the current NSFR proposal

POSITION PAPER Our reference: 2014/00010 1 (10) 11/04/2014 Basel Committee on Banking Supervision Consultative Document Basel III: The Net Stable Funding Ratio Key suggestions to the current NSFR proposal

State Small Business Credit Initiative

State Small Business Credit Initiative Collateral Enhancement Program Ohio Capital Access Program Targeted Investment Program The State of Ohio is an Equal Opportunity Employer and Provider of ADA Services.

State Small Business Credit Initiative Collateral Enhancement Program Ohio Capital Access Program Targeted Investment Program The State of Ohio is an Equal Opportunity Employer and Provider of ADA Services.

Loan Disclosure Statement

ab Loan Disclosure Statement Risk Factors You Should Consider Before Using Margin or Other Loans Secured by Your Securities Accounts This brochure is only a summary of certain risk factors you should consider

ab Loan Disclosure Statement Risk Factors You Should Consider Before Using Margin or Other Loans Secured by Your Securities Accounts This brochure is only a summary of certain risk factors you should consider

Static Pool Analysis: Evaluation of Loan Data and Projections of Performance March 2006

Static Pool Analysis: Evaluation of Loan Data and Projections of Performance March 2006 Introduction This whitepaper provides examiners with a discussion on measuring and predicting the effect of vehicle

Static Pool Analysis: Evaluation of Loan Data and Projections of Performance March 2006 Introduction This whitepaper provides examiners with a discussion on measuring and predicting the effect of vehicle

Quarterly Credit Conditions Survey Report

Quarterly Credit Conditions Survey Report Contents March 2014 Quarter Prepared by the Monetary Analysis & Programming Department Research & Economic Programming Division List of Tables and Charts 2 Background

Quarterly Credit Conditions Survey Report Contents March 2014 Quarter Prepared by the Monetary Analysis & Programming Department Research & Economic Programming Division List of Tables and Charts 2 Background

ABL Step 1 An Introduction. How SIPPA can change the Lending Environment and Access to Credit

ABL Step 1 An Introduction How SIPPA can change the Lending Environment and Access to Credit Traditional Bank vs ABL Bank Focused on Credit Status Over reliance on Real Estate Vulnerable to Economic Cycles

ABL Step 1 An Introduction How SIPPA can change the Lending Environment and Access to Credit Traditional Bank vs ABL Bank Focused on Credit Status Over reliance on Real Estate Vulnerable to Economic Cycles

Topic Overview. Strategies and Management E4: Resources Management Sources of Financing

Resources for the TEKLA curriculum at Junior Secondary Topic 7 Sources of Financing Strategies and Management Extension Learning Element Module E4 Resources Management Topic Level Duration Topic Overview

Resources for the TEKLA curriculum at Junior Secondary Topic 7 Sources of Financing Strategies and Management Extension Learning Element Module E4 Resources Management Topic Level Duration Topic Overview

I. Introduction. II. Financial Markets (Direct Finance) A. How the Financial Market Works. B. The Debt Market (Bond Market)

A. How the Financial Market Works. B. The Debt Market (Bond Market)") University of California, Merced EC 121-Money and Banking Chapter 2 Lecture otes Professor Jason Lee I. Introduction In economics, investment is defined as an increase in the capital stock. This is important

University of California, Merced EC 121-Money and Banking Chapter 2 Lecture otes Professor Jason Lee I. Introduction In economics, investment is defined as an increase in the capital stock. This is important

Considerations for Troubled Debt Restructuring Identification of Loans August 2011

Considerations for Troubled Debt Restructuring Identification of Loans August 2011 Introduction This document is intended to provide examiners with a general overview of the judgments required by an institution

Considerations for Troubled Debt Restructuring Identification of Loans August 2011 Introduction This document is intended to provide examiners with a general overview of the judgments required by an institution

Remember the Interest

STUDENT MODULE 7.1 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. Remember the Interest Mom, it is not fair. If Bill can

STUDENT MODULE 7.1 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. Remember the Interest Mom, it is not fair. If Bill can

TERMS OF LENDING FOR SMALL BUSINESS LINES OF CREDIT: THE ROLE OF LOAN GUARANTEES

The International Journal of Business and Finance Research Volume 5 Number 1 2011 TERMS OF LENDING FOR SMALL BUSINESS LINES OF CREDIT: THE ROLE OF LOAN GUARANTEES Raymond Posey, Mount Union College Alan

The International Journal of Business and Finance Research Volume 5 Number 1 2011 TERMS OF LENDING FOR SMALL BUSINESS LINES OF CREDIT: THE ROLE OF LOAN GUARANTEES Raymond Posey, Mount Union College Alan

Why Do Borrowers Pledge Collateral? New Empirical Evidence on the Role of Asymmetric Information

Why Do Borrowers Pledge Collateral? New Empirical Evidence on the Role of Asymmetric Information Allen N. Berger Board of Governors of the Federal Reserve System Wharton Financial Institutions Center [email protected]

Why Do Borrowers Pledge Collateral? New Empirical Evidence on the Role of Asymmetric Information Allen N. Berger Board of Governors of the Federal Reserve System Wharton Financial Institutions Center [email protected]

GLOSSARY COMMONLY USED REAL ESTATE TERMS

GLOSSARY COMMONLY USED REAL ESTATE TERMS Adjustable-Rate Mortgage (ARM): a mortgage loan with an interest rate that is subject to change and is not fixed at the same level for the life of the loan. These

GLOSSARY COMMONLY USED REAL ESTATE TERMS Adjustable-Rate Mortgage (ARM): a mortgage loan with an interest rate that is subject to change and is not fixed at the same level for the life of the loan. These

Trouble Debt Restructuring & OREO Accounting

Session Objectives Trouble Debt Restructuring & OREO Accounting Chris Vallez, CPA, CICA, MBA, Partner Ellen Vargo, CPA, CFE, FCPA, NCCO Partner Nearman, Maynard, Vallez, CPA s Identify accounting guidance

Session Objectives Trouble Debt Restructuring & OREO Accounting Chris Vallez, CPA, CICA, MBA, Partner Ellen Vargo, CPA, CFE, FCPA, NCCO Partner Nearman, Maynard, Vallez, CPA s Identify accounting guidance

5.3.2015 г. OC = AAI + ACP

D. Dimov Working capital (or short-term financial) management is the management of current assets and current liabilities: Current assets include inventory, accounts receivable, marketable securities,

D. Dimov Working capital (or short-term financial) management is the management of current assets and current liabilities: Current assets include inventory, accounts receivable, marketable securities,

Table of Contents. Interest Expense and Income 185.32 Why do financing accounts borrow from Treasury? 185.33 Why do financing accounts earn interest?

SECTION 185 FEDERAL CREDIT Table of Contents General Information 185.1 Does this section apply to me? 185.2 What background information must I know? 185.3 What special terms must I know? 185.4 Are there

SECTION 185 FEDERAL CREDIT Table of Contents General Information 185.1 Does this section apply to me? 185.2 What background information must I know? 185.3 What special terms must I know? 185.4 Are there

Small Business Finance Thinking Strategically

Small Business Finance Thinking Strategically Copyright 2007 by AbdulJaami, PLLC. All Rights Reserved. This publication is intended as a general guide only. It does not contain a general legal analysis

Small Business Finance Thinking Strategically Copyright 2007 by AbdulJaami, PLLC. All Rights Reserved. This publication is intended as a general guide only. It does not contain a general legal analysis

General guidelines for the completion of the bank lending survey questionnaire

General guidelines for the completion of the bank lending survey questionnaire This document includes the general guidelines for the completion of the questionnaire and the terminology used in the survey.

General guidelines for the completion of the bank lending survey questionnaire This document includes the general guidelines for the completion of the questionnaire and the terminology used in the survey.

Use of Consumer Credit Data for Statistical Purposes: Korean Experience

Use of Consumer Credit Data for Statistical Purposes: Korean Experience Byong-ki Min October 2014 Abstract For some time, the Bank of Korea has sought to obtain micro data that can help us to analyze our

Use of Consumer Credit Data for Statistical Purposes: Korean Experience Byong-ki Min October 2014 Abstract For some time, the Bank of Korea has sought to obtain micro data that can help us to analyze our

About Us. Est. Glynn Parker. Peter Hirst. Parker Shop Equipment. Rapiscan

01823 663737 About Us Leasing Programmes Limited lends money to businesses looking to acquire equipment. We offer leasing, hire purchase and loan facilities. We can also arrange factoring and invoice discounting.

01823 663737 About Us Leasing Programmes Limited lends money to businesses looking to acquire equipment. We offer leasing, hire purchase and loan facilities. We can also arrange factoring and invoice discounting.

Understanding Regulation U

Understanding Regulation U What every deal lawyer needs to know about the margin regulations November 17, 2011 Craig Unterberg David Aman Federal Margin Regulations Background Authorized under Section

Understanding Regulation U What every deal lawyer needs to know about the margin regulations November 17, 2011 Craig Unterberg David Aman Federal Margin Regulations Background Authorized under Section

Chapter 13: Residential and Commercial Property Financing

Chapter 13 Outline / Page 1 Chapter 13: Residential and Commercial Property Financing Understanding the Mortgage Concept - secured vs. unsecured debt - mortgage pledge of property to secure a debt (See

Chapter 13 Outline / Page 1 Chapter 13: Residential and Commercial Property Financing Understanding the Mortgage Concept - secured vs. unsecured debt - mortgage pledge of property to secure a debt (See

Saudi mortgage laws A formula for a wellfunctioning

Saudi mortgage laws A formula for a wellfunctioning market? Introduction and background Over the last five years the Government of Saudi Arabia has continued to invest considerable amounts of oil revenue

Saudi mortgage laws A formula for a wellfunctioning market? Introduction and background Over the last five years the Government of Saudi Arabia has continued to invest considerable amounts of oil revenue

An Alternative Way to Diversify an Income Strategy

Senior Secured Loans An Alternative Way to Diversify an Income Strategy Alternative Thinking Series There is no shortage of uncertainty and risk facing today s investor. From high unemployment and depressed

Senior Secured Loans An Alternative Way to Diversify an Income Strategy Alternative Thinking Series There is no shortage of uncertainty and risk facing today s investor. From high unemployment and depressed

Understanding Loans and Other Programs Available for Certified Minority Business Enterprises

Understanding Loans and Other Programs Available for Certified Minority Business Enterprises Presented by Allen McConnell, Manager Minority Business Development Division Slide 1 Access to Financial Assistance

Understanding Loans and Other Programs Available for Certified Minority Business Enterprises Presented by Allen McConnell, Manager Minority Business Development Division Slide 1 Access to Financial Assistance

Aurora Capital. $50,000 maximum (this amount is subject to the availability of funds) Five year balloon with a 20-year amortization schedule.

Five year balloon with a 20-year amortization schedule.") Aurora Capital Summary: Aurora Capital will be used to finance the rehabilitation and construction of commercial real estate in downtown Elkhart. The objective of the loan pool will be to stimulate physical

Aurora Capital Summary: Aurora Capital will be used to finance the rehabilitation and construction of commercial real estate in downtown Elkhart. The objective of the loan pool will be to stimulate physical

St. Vincent and the Grenadines International Financial Services Authority Statement of Guidance No. 3

St. Vincent and the Grenadines International Financial Services Authority Statement of Guidance No. 3 Loan Classification Criteria Provisioning Guidelines Treatment of Interest on Loans Write off Procedures

St. Vincent and the Grenadines International Financial Services Authority Statement of Guidance No. 3 Loan Classification Criteria Provisioning Guidelines Treatment of Interest on Loans Write off Procedures

Danish mortgage bonds provide attractive yields and low risk

JANUARY 2015 Danish mortgage bonds provide attractive yields and low risk New European Union legislation favours Danish mortgage bonds KEY CONCEPTS New legislation favours Danish mortgage bonds Attractive

JANUARY 2015 Danish mortgage bonds provide attractive yields and low risk New European Union legislation favours Danish mortgage bonds KEY CONCEPTS New legislation favours Danish mortgage bonds Attractive

A. Eligibility Requirements for a Loan Modification & Troubled Debt Restructure (TDRs)

") POLICY: L127 This policy governs any changes in original terms, on consumer and business loans including but not limited to real estate loans, that were agreed to at loan approval. Loan modifications and

POLICY: L127 This policy governs any changes in original terms, on consumer and business loans including but not limited to real estate loans, that were agreed to at loan approval. Loan modifications and

EC 341 Monetary and Banking Institutions, Boston University Summer 2, 2012 Homework 3 Due date: Tuesday, July 31, 6:00 PM.

EC 341 Monetary and Banking Institutions, Boston University Summer 2, 2012 Homework 3 Due date: Tuesday, July 31, 6:00 PM. Problem 1 Questions 1, 4, 6, 8, 12, 13, 16, 18, 22, and 23 from Chapter 8. Solutions:

EC 341 Monetary and Banking Institutions, Boston University Summer 2, 2012 Homework 3 Due date: Tuesday, July 31, 6:00 PM. Problem 1 Questions 1, 4, 6, 8, 12, 13, 16, 18, 22, and 23 from Chapter 8. Solutions:

The Debt-Equity Trade Off: The Capital Structure Decision

The Debt-Equity Trade Off: The Capital Structure Decision Aswath Damodaran Stern School of Business Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable

The Debt-Equity Trade Off: The Capital Structure Decision Aswath Damodaran Stern School of Business Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable

BUSINESS LOAN APPLICATION

BUSINESS LOAN APPLICATION Thank you for your decision in obtaining a commercial loan from our business service division. Please complete the following information as accurately as possible so we may better

BUSINESS LOAN APPLICATION Thank you for your decision in obtaining a commercial loan from our business service division. Please complete the following information as accurately as possible so we may better

City of Avon, MN Revolving Loan (RLF) Application

Application") City of Avon, MN Revolving Loan (RLF) Application LARGE LOAN APPLICATION 140 Stratford Street East INSTRUCTIONS: This application is for loans greater than or equal to 8,001. Please read the Revolving

City of Avon, MN Revolving Loan (RLF) Application LARGE LOAN APPLICATION 140 Stratford Street East INSTRUCTIONS: This application is for loans greater than or equal to 8,001. Please read the Revolving

Minority Business Development Division Allen McConnell, Manger (614) 752-4833 [email protected] www.development.ohio.

752-4833 Allen.McConnell@development.ohio.gov www.development.ohio.") Minority Business Development Division Allen McConnell, Manger (614) 752-4833 [email protected] www.development.ohio.gov The State of Ohio is an Equal Opportunity Employer and Provider

Minority Business Development Division Allen McConnell, Manger (614) 752-4833 [email protected] www.development.ohio.gov The State of Ohio is an Equal Opportunity Employer and Provider

COMMERCIAL LENDING POLICY DEVELOPMENT GUIDE Minimum Expectations

Additional Tools: COMMERCIAL LENDING POLICY DEVELOPMENT GUIDE Minimum Expectations Class 2 Institutions February 2014 Ce document est également disponible en français. COMMERCIAL LENDING POLICY DEVELOPMENT

Additional Tools: COMMERCIAL LENDING POLICY DEVELOPMENT GUIDE Minimum Expectations Class 2 Institutions February 2014 Ce document est également disponible en français. COMMERCIAL LENDING POLICY DEVELOPMENT

Chapter 9 Bonds and Their Valuation ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS

Chapter 9 Bonds and Their Valuation ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 9-1 a. A bond is a promissory note issued by a business or a governmental unit. Treasury bonds, sometimes referred to as

Chapter 9 Bonds and Their Valuation ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 9-1 a. A bond is a promissory note issued by a business or a governmental unit. Treasury bonds, sometimes referred to as

The Determinants of Collateral: a Decision Tree Analysis of SME Loans

The Determinants of Collateral: a Decision Tree Analysis of SME Loans Tensie Steijvers 1, Wim Voordeckers 2, Koen Vanhoof 3 Hasselt University, Belgium Summary Previous empirical research has devoted little

The Determinants of Collateral: a Decision Tree Analysis of SME Loans Tensie Steijvers 1, Wim Voordeckers 2, Koen Vanhoof 3 Hasselt University, Belgium Summary Previous empirical research has devoted little

THE ABC S OF BORROWING

THE ABC S OF BORROWING All businesses, no matter what size, need to raise money at some time. Small business owners may be able to dip into their personal savings or borrow money from friends. More likely,

THE ABC S OF BORROWING All businesses, no matter what size, need to raise money at some time. Small business owners may be able to dip into their personal savings or borrow money from friends. More likely,

A Proposal to Resolve the Distress of Large and Complex Financial Institutions

A Proposal to Resolve the Distress of Large and Complex Financial Institutions Viral V Acharya, Barry Adler and Matthew Richardson 1 Due to the difficulty in resolving bankruptcies of large multinational

A Proposal to Resolve the Distress of Large and Complex Financial Institutions Viral V Acharya, Barry Adler and Matthew Richardson 1 Due to the difficulty in resolving bankruptcies of large multinational

CREDIT RISK MANAGEMENT IN INDIAN COMMERCIAL BANKS

CREDIT RISK MANAGEMENT IN INDIAN COMMERCIAL BANKS MS. ASHA SINGH RESEARCH SCHOLAR, MEWAR UNIVERSITY, CHITTORGARH, RAJASTHAN. ABSTRACT Risk is inherent part of bank s business. Effective risk management

CREDIT RISK MANAGEMENT IN INDIAN COMMERCIAL BANKS MS. ASHA SINGH RESEARCH SCHOLAR, MEWAR UNIVERSITY, CHITTORGARH, RAJASTHAN. ABSTRACT Risk is inherent part of bank s business. Effective risk management

www.development.ohio.gov

Minority Business Development Division Joseph Brooks (614) 466-5065 [email protected] www.development.ohio.gov The State of Ohio is an Equal Opportunity Employer and Provider of ADA Services

Minority Business Development Division Joseph Brooks (614) 466-5065 [email protected] www.development.ohio.gov The State of Ohio is an Equal Opportunity Employer and Provider of ADA Services

Quarterly Credit Conditions Survey Report

Quarterly Credit Conditions Survey Report Contents List of Charts 2 List of Tables 3 Background 4 Overview 5 Credit Market Conditions 8 Personal Lending 10 Micro Business Lending 13 Small Business Lending

Quarterly Credit Conditions Survey Report Contents List of Charts 2 List of Tables 3 Background 4 Overview 5 Credit Market Conditions 8 Personal Lending 10 Micro Business Lending 13 Small Business Lending

Accounts payable Money which you owe to an individual or business for goods or services that have been received but not yet paid for.

A Account A record of a business transaction. A contract arrangement, written or unwritten, to purchase and take delivery with payment to be made later as arranged. Accounts payable Money which you owe

A Account A record of a business transaction. A contract arrangement, written or unwritten, to purchase and take delivery with payment to be made later as arranged. Accounts payable Money which you owe

Appraisal A written analysis prepared by a qualified appraiser and estimating the value of a property

REAL ESTATE BASICS Affordability Analysis An analysis of a buyer s ability to afford the purchase of a home, reviews income, liabilities, and available funds, and considers the type of mortgage a buyer

REAL ESTATE BASICS Affordability Analysis An analysis of a buyer s ability to afford the purchase of a home, reviews income, liabilities, and available funds, and considers the type of mortgage a buyer

Working Capital and Contract Caplines Program. Caplines 2.0: New and Improved

Working Capital and Contract Caplines Program Caplines 2.0: New and Improved Topics for Today s Discussion Structural Changes Key Features for Working Capital Caplines Key Features for Contract Caplines

Working Capital and Contract Caplines Program Caplines 2.0: New and Improved Topics for Today s Discussion Structural Changes Key Features for Working Capital Caplines Key Features for Contract Caplines

3/22/2010. Chapter 11. Eight Categories of Bank Regulation. Economic Analysis of. Regulation Lecture 1. Asymmetric Information and Bank Regulation

Chapter 11 Economic Analysis of Banking Regulation Lecture 1 Asymmetric Information and Bank Regulation Adverse Selection and Moral Hazard are the two concepts that underlie government regulation of the

Chapter 11 Economic Analysis of Banking Regulation Lecture 1 Asymmetric Information and Bank Regulation Adverse Selection and Moral Hazard are the two concepts that underlie government regulation of the

3. How does a spot loan differ from a loan commitment? What are the advantages and disadvantages of borrowing through a loan commitment?

Solutions for End-of-Chapter Questions and Problems 1. Why is credit risk analysis an important component of FI risk management? What recent activities by FIs have made the task of credit risk assessment

Solutions for End-of-Chapter Questions and Problems 1. Why is credit risk analysis an important component of FI risk management? What recent activities by FIs have made the task of credit risk assessment

International School of Economics at Tbilisi State University. Does a collateralized loan have a higher probability to default?

International School of Economics at Tbilisi State University Does a collateralized loan have a higher probability to default? Irakli Ninua Supervisor: Frédéric Laurin June 2008 Introduction My research

International School of Economics at Tbilisi State University Does a collateralized loan have a higher probability to default? Irakli Ninua Supervisor: Frédéric Laurin June 2008 Introduction My research

CDFI Bond Guarantee Program Secondary Loan Requirements

CDFI Bond Guarantee Program Secondary Loan Requirements In order for an Eligible CDFI to make a Secondary Loan through the CDFI Bond Guarantee Program, it must ensure that the Secondary Loan is made in

CDFI Bond Guarantee Program Secondary Loan Requirements In order for an Eligible CDFI to make a Secondary Loan through the CDFI Bond Guarantee Program, it must ensure that the Secondary Loan is made in

COMMERCIAL LENDING POLICY DEVELOPMENT GUIDE Minimum Considerations

DRAFT FOR COMMENT Additional Tools: COMMERCIAL LENDING POLICY DEVELOPMENT GUIDE Minimum Considerations Class 2 Institutions April 2013 This document is also available in French. COMMERCIAL CREDIT POLICY

DRAFT FOR COMMENT Additional Tools: COMMERCIAL LENDING POLICY DEVELOPMENT GUIDE Minimum Considerations Class 2 Institutions April 2013 This document is also available in French. COMMERCIAL CREDIT POLICY

HOME AFFORDABLE MODIFICATION PROGRAM BASE NET PRESENT VALUE (NPV) MODEL SPECIFICATIONS

MODEL SPECIFICATIONS") Overview HOME AFFORDABLE MODIFICATION PROGRAM BASE NET PRESENT VALUE (NPV) MODEL SPECIFICATIONS As a part of the Making Home Affordable Program, we are providing standardized guidance and a base net present

Overview HOME AFFORDABLE MODIFICATION PROGRAM BASE NET PRESENT VALUE (NPV) MODEL SPECIFICATIONS As a part of the Making Home Affordable Program, we are providing standardized guidance and a base net present