Life Insurance Demand and Financial Inclusion Evidence from Italian households

|

|

|

- Pauline Brianne Hart

- 8 years ago

- Views:

Transcription

1 Life Insurance Demand and Financial Inclusion Evidence from Italian households Elisa Luciano* Joint work with Mariacristina Rossi *University of Turin, CeRP-CCA and Netspar Summer School on Gender, Economics and Society

2 Introduction We look into the demand for life insurance products by focusing on: life insurance and death assurance products, by looking at the propensity to buy and the intensity of the demand (premium) We use the Bank of Italy dataset SHIW (survey household, income, wealth) Our findings show that financial inclusion acts as a main driver of life insurance demand. Inclusion is either having stocks, a mortgage or being financially literate.

3 LI can be of two types: i) pure life insurance, which guarantees a lump sum (pure endowment) or an annuity upon survival of the subscriber and ii) term insurance, which guarantees to beneficiaries a payment if death occurs to the subscriber. While the first type represents pure savings, the second reveals the intention to bequeath. Pure life insurance often covers the whole life type: it consists of an accumulation plan which pays a lump sum (or annuity) if the subscriber is alive, whenever she decides to stop the contract, and pays a lump sum to the heirs (whose amount is precisely known in advance) in case of subscribers death.

if the subscriber is alive,")

4 LI as saving tool: annuities Life Insurance (LI) can be very effective in planning efficiently saving patterns. LI can represent a vehicle for savings and building up annuities. It could be of particular interest to those who are exposed to little annuitisation in Italy workers will receive their pension as an annuity (mandatory) - risk of over-annuitisation? (Brown and Nijman 2011) However, people who have discontinous career or are not in the labour market are at risk of under-annuitisation This makes it particuarly interesting for women, who are far from the labour markets and more vulnerable to little annuitization

5 Annuity puzzle and bequest intention Death assurance captures the saving intention for the next generation- post mortem utility life insurance responds to an intertemporal planning, both within the life cycle and within an intergenerational dimension Annuity puzzle total (Yaari, 1965) or partial annuities with bequest motives (Davidoff et al., 2005) are optimal Yet few buy them. Preferences for bequest could explain lack of annuities, particularly for the wealthiest (Lockwood, 2012)

are optimal Yet few buy them.")

6 Our paper aims at investigating whether the traditional drivers of insurance demand work on the Italian data. The main determinants of life insurance have been traditionally detected in: household income, tax treatment, education, life expectancy, young dependents ratio, risk aversion, financial vulnerability, age and bequest intention. we take them all into account by adding closeness to financial market and focusing on women, who are less financially literate, usually more risk averse, participate lee to the labour market.

7 Research drivers On gender, little has been studied w.r.t. insurance. Exception is Gandolfi and Miners (1986). They focus on within couples behavior, finding a strong discrepancy within the couple in the demand for insurance, with wives having much lower life insurance than their husbands. Much more has been studied w.r.t. financial literacy. Wsj, june 14: women, especially, are failing financial literacy. Lack of knowledge is more costly if you live more (women do) and does not depend on social status (wealth, education). 22 and self-confidence in financial matters, which is lower for women (more prone to learn) J

and does not depend on social status (wealth, education).")

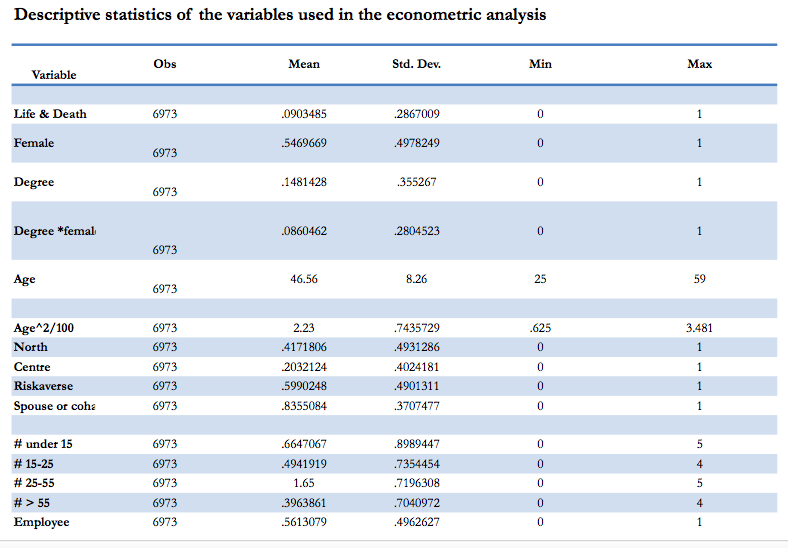

8 Data We use the SHIW data 2012 Our sample consists of individuals aged between 24 and 60 they are either a household head or the spouse, where the head is self-stated. We exclude other relatives and children living in the household so as to focus on the couple (or single) decisions. Our final sample consists of 6,973 individual-observations.

decisions.")

9 Gender Life&Death insurance Life Insurance Male 12.0% 7.4% Female 6.6% 4.7% Total Gender Traditional Life&death Insurance Male 9.9% Female 5.4% Total 7.40

10 Descriptive Statistics Life&Death insurance Total Life Insurance Total Age Male Female Male Female over Traditional Life & death Insurance Total Age Male Female below 34 years over

11

12

13 Table: Financial Knowledge and Life Insurance Financial literacy (highest scores) Total (%) Sex No Yes Male Female Total

14 Endogeneity of Stock Holding Instrumented via father or mother with managerial skills - parents with managerial job at the age of the respondent The main respondent is asked what was the occupation of your mother and father at your age?. We consider managers, freelancers and entrepreneurs as managerial occupations so as to build up the instrument. The rationale relies on the reasoning that having a parent with higher education or managerial job increases the likelihood of having a higher cognitive ability and financial knowledge (see Calcagno and Urzi, 2014) Note: Financial Literacy is based on three questions assessing the respondents knowledge of the concepts of variable versus fixed interest-rate mortgage, inflation rate and portfolio risk and diversification.

Note: Financial Literacy is based on three questions assessing the respondents knowledge of the concepts of variable versus fixed interest-rate mortgage, inflation rate")

15 Strategy We look at three different models The propensity to buy any insurance (probit) Life insurance and death assurance as a joint decision (biprobit) The amount of premia (tobit) Focus on gender, participation to the financial and real estate market, occupational stutus and measures of risk

16 Table: Insurance Holding Any Insurance Holding (1) (2) (3) (4) female *** *** *** ** Log hh income *** *** *** Individual income/family income 4.32e-07*** 4.33e-07*** 8.34e-07*** 1.54e-06** Under *** *** *** Over *** *** *** Employee Self-employed *** *** Income/Wealth ** ** * Medium city * Large city *** *** *** Mega city *** *** *** *** Bequest * Homeownership * Stock holding *** Financial literacy *** 0.256**

17 Table: Life Insurance Life Insurance (1) (2) (3) (4) female ** ** * * Log hh income *** *** *** Individual income/family income 1.43e-07** 1.33e-07** 2.52e-07* 7.68e-07 Under ** ** ** *** ** *** ** Over *** *** ** * Employee Self-employed *** *** * Income/Wealth ** ** Homeownership Stock holding *** Financial literacy ** 0.102

18 Table: Term Insurance Term Insurance (1) (2) (3) (4) female *** *** *** *** Log hh income *** *** *** Individual income/family income 3.37e-07*** 3.36e-07*** 6.10e-07*** 1.21e-06** Under * ** * *** *** *** Over *** *** ** Employee Self-employed *** *** Income/Wealth ** ** * * Homeownership * Stock holding *** Financial literacy *** 0.245**

19 Table: Tobit Premia. Life Life Life Term Term Term female * *** *** *** Log hh income 1,636*** 1,692*** 1,105* 1,254*** 1,332*** Individual/hh income ** ** * *** *** ** Income/wealth Homeown Stock holding 1,513** 1,438** Financial Literacy 264.6** ** 3,209

20 Discussion Income is significant, though tiny effect. Both as household income as well as individual over hh income risk aversion is not. we know however that risk aversion is self declared Holding stocks is one of the main determinants, while home ownership is not significant Financial market participation (proxied by stock market participation)generates a strong effect on insurance demand, suggesting that when families are close to the financial system they diversify in all possible forms

generates a strong effect on")

21 Policy implication To study policy implications, we first produce a prediction of the probabilities to have one form of insurance (life or death) given that the respondent already has the other. We do this separately for men and women, given that their demands are significantly different We then study the (unconditional) probabilities of having either life or death insurance, under the true and under shocked values of some relevant variables, such as income, education and stock ownership. This is like asking which manoeuvres are likely to increase insurance demand for intermediaries, be them banks or insurance companies..

22

23

24 Policy implications in a nutshell By increasing financial knowledge (one additional correct answer, life insurance would increase by 2 percentage points, to 10 % for men) the effect would be stronger for term insurance by increasing to 15 % participation of men (to 11% the overall participation)

25 Extensions We extend the analysis to allow for the panel dimension of the analysis by running a fixed effect estimate

26 Table: Life Insurance (D) Selected Regressors (1) (2) (3) (4) (5) OLS - FinLit OLS - Stock FE - All FE - Male FE - Female Female ** ** (0.0070) (0.0070) Living together ** * * (0.0363) (0.0363) (0.0859) (0.1523) (0.0870) Married ** * (0.0341) (0.0340) (0.0733) (0.1415) (0.0865) Inactive *** *** * (0.0203) (0.0204) (0.0308) (0.0336) (0.0145) Self-Employed *** *** (0.0114) (0.0114) (0.0274) (0.0377) (0.0371) Female*Inactive *** (0.0235) (0.0235) (0.0344) Home-owner *** *** (0.0074) (0.0074) (0.0229) (0.0300) (0.0302) Risk Adverse ** ** (0.0070) (0.0070) (0.0092) (0.0126) (0.0115) Financial literacy *** (0.0071) Hold stocks ** ** *** (0.0161) (0.0230) (0.0313) (0.0274) Time dummies No No Yes Yes Yes Observations

27 Conclusions Life and Death Insurance seem to go hand in hand Income and asset are shaping demand insurance Financial market inclusion measured by stock holding participation and financial knowledge act as principal driver Death assurance, which should proxy bequest intention, seem to be less appealing to women (both as participation and premia) Financial Literacy is particularly a strong determinant of term insurance

Life Insurance Demand. Evidence from Italian households with a gender twist

Life Insurance Demand. Evidence from Italian households with a gender twist Elisa Luciano Federico Petri Mariacristina Rossi University of Turin and CeRP-CCA CINTIA International Conference, Turin, Italy

Life Insurance Demand. Evidence from Italian households with a gender twist Elisa Luciano Federico Petri Mariacristina Rossi University of Turin and CeRP-CCA CINTIA International Conference, Turin, Italy

How To Find Out What Determines The Demand For Insurance

ISSN 2279-9362 Life Insurance Demand and Financial Inclusion; Evidence from Italian households Elisa Luciano Mariacristina Rossi No. 398 December 2014 www.carloalberto.org/research/working-papers 2014

ISSN 2279-9362 Life Insurance Demand and Financial Inclusion; Evidence from Italian households Elisa Luciano Mariacristina Rossi No. 398 December 2014 www.carloalberto.org/research/working-papers 2014

Financial inclusion and life insurance demand: Evidence from Italian households

Financial inclusion and life insurance demand: Evidence from Italian households Discussion Hazel Bateman UNSW Business School UNSW, Sydney, Australia Outline Paper Summary Comments Discussion Paper Summary

Financial inclusion and life insurance demand: Evidence from Italian households Discussion Hazel Bateman UNSW Business School UNSW, Sydney, Australia Outline Paper Summary Comments Discussion Paper Summary

What determines annuity demand at retirement?

What determines annuity demand at retirement? Giuseppe Cappelletti Giovanni Guazzarotti Pietro Tommasino Banca d Italia International Pension Workshop - Netspar 2011 Cappelletti, Guazzarotti, Tommasino

What determines annuity demand at retirement? Giuseppe Cappelletti Giovanni Guazzarotti Pietro Tommasino Banca d Italia International Pension Workshop - Netspar 2011 Cappelletti, Guazzarotti, Tommasino

Explaining why, right or wrong, (Italian) households do not like Reverse Mortgages

households do not like Reverse Mortgages") Explaining why, right or wrong, (Italian) households do not like Reverse Mortgages Elsa Fornero Mariacristina Rossi Maria Cesira Urzì Brancati Save PHF Conference on Demographic Trends, Saving and Retirement

Explaining why, right or wrong, (Italian) households do not like Reverse Mortgages Elsa Fornero Mariacristina Rossi Maria Cesira Urzì Brancati Save PHF Conference on Demographic Trends, Saving and Retirement

ESTATE PLANNING INFORMATION

ESTATE PLANNING INFORMATION I PERSONAL AND FAMILY DATA A. Husband Husband's Name: (First) (Middle) (Last) Social Security Number Home Phone Employer Business Address Business Phone Place of Birth: U.S.

ESTATE PLANNING INFORMATION I PERSONAL AND FAMILY DATA A. Husband Husband's Name: (First) (Middle) (Last) Social Security Number Home Phone Employer Business Address Business Phone Place of Birth: U.S.

The Effect of Social and Demographic Factors on Life Insurance Demand in Croatia

International Journal of Business and Social Science Vol. 4 No. 9; August 2013 The Effect of Social and Demographic Factors on Life Insurance Demand in Croatia MARIJANA ĆURAK Associate Professor Department

International Journal of Business and Social Science Vol. 4 No. 9; August 2013 The Effect of Social and Demographic Factors on Life Insurance Demand in Croatia MARIJANA ĆURAK Associate Professor Department

Complexity as a Barrier to Annuitization

Complexity as a Barrier to Annuitization 1 Jeffrey R. Brown, Illinois & NBER Erzo F.P. Luttmer, Dartmouth & NBER Arie Kapteyn, USC & NBER Olivia S. Mitchell, Wharton & NBER GWU/FRB Financial Literacy Seminar

Complexity as a Barrier to Annuitization 1 Jeffrey R. Brown, Illinois & NBER Erzo F.P. Luttmer, Dartmouth & NBER Arie Kapteyn, USC & NBER Olivia S. Mitchell, Wharton & NBER GWU/FRB Financial Literacy Seminar

Annuity Principles and Concepts Session Five Lesson Two. Annuity (Benefit) Payment Options

Payment Options") Annuity Principles and Concepts Session Five Lesson Two Annuity (Benefit) Payment Options Life Contingency Options - How Income Payments Can Be Made To The Annuitant. Pure Life versus Life with Guaranteed

Annuity Principles and Concepts Session Five Lesson Two Annuity (Benefit) Payment Options Life Contingency Options - How Income Payments Can Be Made To The Annuitant. Pure Life versus Life with Guaranteed

READING 14: LIFETIME FINANCIAL ADVICE: HUMAN CAPITAL, ASSET ALLOCATION, AND INSURANCE

READING 14: LIFETIME FINANCIAL ADVICE: HUMAN CAPITAL, ASSET ALLOCATION, AND INSURANCE Introduction (optional) The education and skills that we build over this first stage of our lives not only determine

READING 14: LIFETIME FINANCIAL ADVICE: HUMAN CAPITAL, ASSET ALLOCATION, AND INSURANCE Introduction (optional) The education and skills that we build over this first stage of our lives not only determine

How To Use A Massmutual Whole Life Insurance Policy

An Educational Guide for Individuals Unlocking the value of whole life Whole life insurance as a financial asset Insurance Strategies Contents 3 Whole life insurance: A versatile financial asset 4 Providing

An Educational Guide for Individuals Unlocking the value of whole life Whole life insurance as a financial asset Insurance Strategies Contents 3 Whole life insurance: A versatile financial asset 4 Providing

Efficient Retirement Life Insurance - The Bernheimian Case Study

INTRODUCTION It is well established in the economics literature that annuities ought to be of substantial value to life-cycle consumers who face an uncertain date of death. Yaari (1965) proved that a life-cycle

INTRODUCTION It is well established in the economics literature that annuities ought to be of substantial value to life-cycle consumers who face an uncertain date of death. Yaari (1965) proved that a life-cycle

Maximizing your Pension with Life Insurance

American Brokerage Services, Inc. 805 E Willow Grove Ave. Suite 2-B Wyndmoor, PA 1-888-227-3131 500 annuities1@absgo.com www.absgo.com Maximizing your Pension with Life Insurance Page 2 of 6 Maximizing

American Brokerage Services, Inc. 805 E Willow Grove Ave. Suite 2-B Wyndmoor, PA 1-888-227-3131 500 annuities1@absgo.com www.absgo.com Maximizing your Pension with Life Insurance Page 2 of 6 Maximizing

Life Insurance and Household Consumption

Life Insurance and Household Consumption Jay Hong José-Víctor Ríos-Rull Torino, April 13, 15 Life Insurance and Household Consumption April 13, 15 1/41 Introduction: A few questions How do preferences

Life Insurance and Household Consumption Jay Hong José-Víctor Ríos-Rull Torino, April 13, 15 Life Insurance and Household Consumption April 13, 15 1/41 Introduction: A few questions How do preferences

Maximizing Your Pension with Life Insurance

Maximizing Your Pension with Life Insurance Introduction If you participate in a traditional pension plan (known as a defined benefit plan) with your employer, you may receive monthly benefits from the

Maximizing Your Pension with Life Insurance Introduction If you participate in a traditional pension plan (known as a defined benefit plan) with your employer, you may receive monthly benefits from the

THE RESPONSIBILITY TO SAVE AND CONTRIBUTE TO

PREPARING FOR RETIREMENT: THE IMPORTANCE OF PLANNING COSTS Annamaria Lusardi, Dartmouth College* THE RESPONSIBILITY TO SAVE AND CONTRIBUTE TO a pension is increasingly left to the individual worker. For

PREPARING FOR RETIREMENT: THE IMPORTANCE OF PLANNING COSTS Annamaria Lusardi, Dartmouth College* THE RESPONSIBILITY TO SAVE AND CONTRIBUTE TO a pension is increasingly left to the individual worker. For

Optimal portfolio choice with health contingent income products: The value of life care annuities

Optimal portfolio choice with health contingent income products: The value of life care annuities Shang Wu CEPAR and School of Risk and Actuarial Studies UNSW Australia Joint work with Ralph Stevens and

Optimal portfolio choice with health contingent income products: The value of life care annuities Shang Wu CEPAR and School of Risk and Actuarial Studies UNSW Australia Joint work with Ralph Stevens and

How To Understand The Economic And Social Costs Of Living In Australia

Australia s retirement provision: the decumulation challenge John Piggott Director CEPAR Outline of talk Introduction to Australian retirement policy Issues in Longevity Current retirement products in

Australia s retirement provision: the decumulation challenge John Piggott Director CEPAR Outline of talk Introduction to Australian retirement policy Issues in Longevity Current retirement products in

Police Pensions Scheme FAQ s. Q. What is the level of my contribution each month?

Police Pensions Scheme FAQ s Q. What is the level of my contribution each month? A. The current contribution rates at 12.25% with parity of contributions for both men and women. It is possible that the

Police Pensions Scheme FAQ s Q. What is the level of my contribution each month? A. The current contribution rates at 12.25% with parity of contributions for both men and women. It is possible that the

Why Do Rich People Buy Life Insurance? By Lisa L. Verdon College of Wooster. January 2012. Abstract

Why Do Rich People Buy Life Insurance? By Lisa L. Verdon College of Wooster January 2012 Abstract Life insurance can be thought of as insurance against a loss of income or as an investment. Those with

Why Do Rich People Buy Life Insurance? By Lisa L. Verdon College of Wooster January 2012 Abstract Life insurance can be thought of as insurance against a loss of income or as an investment. Those with

The psychology and economics of reverse mortgage attitudes: evidence from the Netherlands

The psychology and economics of reverse mortgage attitudes: evidence from the Netherlands Rik Dillingh *, Henriette Prast**, Mariacristina Rossi***, Cesira Urzì Brancati*** *University of Tilburg, Ministry

The psychology and economics of reverse mortgage attitudes: evidence from the Netherlands Rik Dillingh *, Henriette Prast**, Mariacristina Rossi***, Cesira Urzì Brancati*** *University of Tilburg, Ministry

On average, young retirees are not

How Financially Secure Are Young Retirees and Older Workers? FIGURE 1 Financial Status of People Age 51 to 59, by Work Status THOUSS OF DOLLARS 14 1 8 6 $82 RETIREES WORKERS $99 4 $41 $24 MEDIAN MEDIAN

How Financially Secure Are Young Retirees and Older Workers? FIGURE 1 Financial Status of People Age 51 to 59, by Work Status THOUSS OF DOLLARS 14 1 8 6 $82 RETIREES WORKERS $99 4 $41 $24 MEDIAN MEDIAN

Note: The paid up value would be payable only on due maturity of the policy.

Section II Question 6 The earning member of a family aged 35 years expects to earn till next 25 years. He expects an annual growth of 8% in his existing net income of Rs. 5 lakh p.a. If he considers an

Section II Question 6 The earning member of a family aged 35 years expects to earn till next 25 years. He expects an annual growth of 8% in his existing net income of Rs. 5 lakh p.a. If he considers an

NTA s and the annuity puzzle

NTA s and the annuity puzzle David McCarthy NTA workshop Honolulu, 15 th June 2010 hello Today s lecture Was billed as Pension Economics But I teach a 70-hour course on pension economics and finance at

NTA s and the annuity puzzle David McCarthy NTA workshop Honolulu, 15 th June 2010 hello Today s lecture Was billed as Pension Economics But I teach a 70-hour course on pension economics and finance at

LIFE INSURANCE AND PENSIONS by Peter Tryfos York University

LIFE INSURANCE AND PENSIONS by Peter Tryfos York University Introduction Life insurance is the business of insuring human life: in return for a premium payable in one sum or installments, an insurance

LIFE INSURANCE AND PENSIONS by Peter Tryfos York University Introduction Life insurance is the business of insuring human life: in return for a premium payable in one sum or installments, an insurance

Working Paper 135/13 THE PSYCHOLOGY AND ECONOMICS OF REVERSE MORTGAGE ATTITUDES: EVIDENCE FROM THE NETHERLANDS

Working Paper 135/13 THE PSYCHOLOGY AND ECONOMICS OF REVERSE MORTGAGE ATTITUDES: EVIDENCE FROM THE NETHERLANDS Rik Dillingh Henriette Prast Mariacristina Rossi Cesira Urzì Brancati The psychology and economics

Working Paper 135/13 THE PSYCHOLOGY AND ECONOMICS OF REVERSE MORTGAGE ATTITUDES: EVIDENCE FROM THE NETHERLANDS Rik Dillingh Henriette Prast Mariacristina Rossi Cesira Urzì Brancati The psychology and economics

CHAPTER 10 ANNUITIES

CHAPTER 10 ANNUITIES are contracts sold by life insurance companies that pay monthly, quarterly, semiannual, or annual income benefits for the life of a person (the annuitant), for the lives of two or

CHAPTER 10 ANNUITIES are contracts sold by life insurance companies that pay monthly, quarterly, semiannual, or annual income benefits for the life of a person (the annuitant), for the lives of two or

RE 7: Second Level Regulatory Examination: Long Term Insurance Category B, Long Term Insurance Category C And Retail Pension Funds

COMPLIANCE MONITORING SYSTEMS CC RE 7: Second Level Regulatory Examination: Long Term Insurance Category B, Long Term Insurance Category C And Retail Pension Funds Alan Holton December 2009 All representatives

COMPLIANCE MONITORING SYSTEMS CC RE 7: Second Level Regulatory Examination: Long Term Insurance Category B, Long Term Insurance Category C And Retail Pension Funds Alan Holton December 2009 All representatives

2) You must then determine how much of the risk you are willing to assume.

You must then determine how much of the risk you are willing to assume.") CHAPTER 4 Life Insurance Structure, Concepts, and Planning Strategies Where can you make a Simpler living as a needs financial planner? 1) Wealthy clients have a much higher profit margin. The challenge

CHAPTER 4 Life Insurance Structure, Concepts, and Planning Strategies Where can you make a Simpler living as a needs financial planner? 1) Wealthy clients have a much higher profit margin. The challenge

Why Advisors Should Use Deferred-Income Annuities

Why Advisors Should Use Deferred-Income Annuities November 24, 2015 by Michael Finke Retirement income planning is a mathematical problem in which an investor begins with a lump sum of wealth and withdraws

Why Advisors Should Use Deferred-Income Annuities November 24, 2015 by Michael Finke Retirement income planning is a mathematical problem in which an investor begins with a lump sum of wealth and withdraws

Responses to Inquiries RFP 14-01 Annuity Services Provider

Responses to Inquiries RFP 14-01 Annuity Services Provider 1. Is there a reason for the apparent drop off in the level of plan annuitizations in the 4 th quarter of 2013? Answer. INPRS cannot speculate

Responses to Inquiries RFP 14-01 Annuity Services Provider 1. Is there a reason for the apparent drop off in the level of plan annuitizations in the 4 th quarter of 2013? Answer. INPRS cannot speculate

Developments in Pension and Annuity Markets. Ian Tonks

Developments in Pension and Annuity Markets Ian Tonks Outline Pensions policy and annuity markets in an ageing world DC pensions: auto-enrolment in UK from 2012 Structure of annuity markets in UK Types

Developments in Pension and Annuity Markets Ian Tonks Outline Pensions policy and annuity markets in an ageing world DC pensions: auto-enrolment in UK from 2012 Structure of annuity markets in UK Types

The 2015 Self-Assessment Guide For Long Term Care Insurance

The 2015 Self-Assessment Guide For Long Term Care Insurance A JOINT PUBLICATION BY: SHIP State Health Insurance Assistance Program And Indiana Partnership Long Term Care Insurance Program Both of the Indiana

The 2015 Self-Assessment Guide For Long Term Care Insurance A JOINT PUBLICATION BY: SHIP State Health Insurance Assistance Program And Indiana Partnership Long Term Care Insurance Program Both of the Indiana

Health and Mortality Delta: Assessing the Welfare Cost of Household Insurance Choice

Health and Mortality Delta: Assessing the Welfare Cost of Household Insurance Choice Ralph S. J. Koijen Stijn Van Nieuwerburgh Motohiro Yogo University of Chicago and NBER New York University, NBER, and

Health and Mortality Delta: Assessing the Welfare Cost of Household Insurance Choice Ralph S. J. Koijen Stijn Van Nieuwerburgh Motohiro Yogo University of Chicago and NBER New York University, NBER, and

Lifetime Income Benefit Rider

for a secure Retirement Lifetime Income Benefit Rider (LIBR-2010)* Included automatically on most Fixed Indexed Annuities** for use with Fixed Indexed Annuities *May vary by state. Not available in all

for a secure Retirement Lifetime Income Benefit Rider (LIBR-2010)* Included automatically on most Fixed Indexed Annuities** for use with Fixed Indexed Annuities *May vary by state. Not available in all

Initial Data Gathering Workbook

Initial Data Gathering Workbook Client Name: Date returned from client: / / Version 06.10 1 Overview This worksheet is designed to help you gather the required information for your customized financial

Initial Data Gathering Workbook Client Name: Date returned from client: / / Version 06.10 1 Overview This worksheet is designed to help you gather the required information for your customized financial

Caution: Withdrawals made prior to age 59 ½ may be subject to a 10 percent federal penalty tax.

Annuity Distributions What are annuity distributions? How are annuity distributions made? How are your annuity payouts computed if you elect to annuitize? Who are the parties to an annuity contract? How

Annuity Distributions What are annuity distributions? How are annuity distributions made? How are your annuity payouts computed if you elect to annuitize? Who are the parties to an annuity contract? How

Options available to members on leaving their retirement fund

Options available to members on leaving their retirement fund Applicable to members leaving post March 2009 The contents of this document This document explains the different options you have available

Options available to members on leaving their retirement fund Applicable to members leaving post March 2009 The contents of this document This document explains the different options you have available

Life events that may derail a financial plan

Life events that may derail a financial plan The BMO Institute provides insights and strategies around wealth planning and financial decisions to better prepare you for a confident financial future. bmoharris.com

Life events that may derail a financial plan The BMO Institute provides insights and strategies around wealth planning and financial decisions to better prepare you for a confident financial future. bmoharris.com

Guide to Pension Annuities

Guide to Pension Annuities Having successfully built up a pension fund during your working life, there will come a time when you will need to make some important decisions about how to use this fund. These

Guide to Pension Annuities Having successfully built up a pension fund during your working life, there will come a time when you will need to make some important decisions about how to use this fund. These

Immediate Annuity Quotation

Immediate Annuity Quotation Personalized for: Prepared by: Ivon T Hughes Tel: 514-842-9001 Email: info@trustco.ca Fax: 514-842-1085 Reference #: 186078.1 Date Prepared: November 1, 2012 Date Prepared:

Immediate Annuity Quotation Personalized for: Prepared by: Ivon T Hughes Tel: 514-842-9001 Email: info@trustco.ca Fax: 514-842-1085 Reference #: 186078.1 Date Prepared: November 1, 2012 Date Prepared:

Understanding Annuities: A Lesson in Annuities

Understanding Annuities: A Lesson in Annuities Did you know that an annuity can be used to systematically accumulate money for retirement purposes, as well as to guarantee a retirement income that you

Understanding Annuities: A Lesson in Annuities Did you know that an annuity can be used to systematically accumulate money for retirement purposes, as well as to guarantee a retirement income that you

Maximize Your Pension with Life Insurance

Maximize Your Pension with Life Insurance How Death Benefit Protection Can Help You Get the Most Out of Your Pension Benefits Client Brochure Achieve financial protection while maximizing your pension

Maximize Your Pension with Life Insurance How Death Benefit Protection Can Help You Get the Most Out of Your Pension Benefits Client Brochure Achieve financial protection while maximizing your pension

HOW MUCH WILL MY PENSION BE?

HOW MUCH WILL MY PENSION BE? The monthly pension you receive will depend on: How much of retirement benefit you decide to use for a pension benefit In the case of a life annuity the provision you make

HOW MUCH WILL MY PENSION BE? The monthly pension you receive will depend on: How much of retirement benefit you decide to use for a pension benefit In the case of a life annuity the provision you make

Guaranteeing an Income for Life: An Immediate Income Annuity Review

Guaranteeing an Income for Life: An Immediate Income Annuity Review The biggest financial risk that anyone faces during retirement is the risk that savings will be depleted...the risk that income will

Guaranteeing an Income for Life: An Immediate Income Annuity Review The biggest financial risk that anyone faces during retirement is the risk that savings will be depleted...the risk that income will

personal financial planning interview questionnaire

name: name: Financial advisor s name: Tony Novak, Freedom Benefits, 800-609-0683 Date of interview: Documents reviewed: Tax returns Liability insurance policies Medical insurance policies Life insurance

name: name: Financial advisor s name: Tony Novak, Freedom Benefits, 800-609-0683 Date of interview: Documents reviewed: Tax returns Liability insurance policies Medical insurance policies Life insurance

Complimentary Financial Planner

Complimentary Financial Planner Creating Wealth Since 1922 PERSONAL INFORMATION Name Social Security Number Date of Birth Home Street Address You Your Spouse City, State, Zip Home Telephone Marital Status

Complimentary Financial Planner Creating Wealth Since 1922 PERSONAL INFORMATION Name Social Security Number Date of Birth Home Street Address You Your Spouse City, State, Zip Home Telephone Marital Status

Retirement Income Investment Strategy by Andrew J. Krosnowski

Retirement Income Investment Strategy by Andrew J. Krosnowski Step 1- Income Needs-When formulating a successful strategy to generate income during retirement we feel that it is important to start by identifying

Retirement Income Investment Strategy by Andrew J. Krosnowski Step 1- Income Needs-When formulating a successful strategy to generate income during retirement we feel that it is important to start by identifying

3158 Des Plaines Avenue, Suite 209 Voice: (847) 296-8890 Des Plaines, IL 60018-4222 Fax: (847) 296-8871 Toll Free: (888) 658-SSCG

296-8890 Des Plaines, IL 60018-4222 Fax: (847) 296-8871 Toll Free: (888) 658-SSCG") SSCG Actuarial Solutions & Software Innovations 3158 Des Plaines Avenue, Suite 209 Voice: (847) 296-8890 Des Plaines, IL 60018-4222 Fax: (847) 296-8871 Toll Free: (888) 658-SSCG Doris J. Bloom, FLMI web

SSCG Actuarial Solutions & Software Innovations 3158 Des Plaines Avenue, Suite 209 Voice: (847) 296-8890 Des Plaines, IL 60018-4222 Fax: (847) 296-8871 Toll Free: (888) 658-SSCG Doris J. Bloom, FLMI web

Challenger Guaranteed Annuity (Liquid Lifetime)

") Challenger Guaranteed Annuity (Liquid Lifetime) Product Disclosure Statement (PDS) Dated 27 October 2014 Challenger Guaranteed Annuity (SPIN CHG0005AU) Issuer Challenger Life Company Limited (ABN 44 072

Challenger Guaranteed Annuity (Liquid Lifetime) Product Disclosure Statement (PDS) Dated 27 October 2014 Challenger Guaranteed Annuity (SPIN CHG0005AU) Issuer Challenger Life Company Limited (ABN 44 072

The choice between an annuity and a lump sum: Results from Swiss pension funds

Journal of Public Economics 91 (2007) 1944 1966 www.elsevier.com/locate/econbase The choice between an annuity and a lump sum: Results from Swiss pension funds Monika Bütler a,, Federica Teppa b a FEW-HSG

Journal of Public Economics 91 (2007) 1944 1966 www.elsevier.com/locate/econbase The choice between an annuity and a lump sum: Results from Swiss pension funds Monika Bütler a,, Federica Teppa b a FEW-HSG

2 Voluntary retirement module specification

2 Voluntary retirement module specification As part of its research on Superannuation Policy for Post-Retirement the Commission has developed a model referred to as the Productivity Commission Retirement

2 Voluntary retirement module specification As part of its research on Superannuation Policy for Post-Retirement the Commission has developed a model referred to as the Productivity Commission Retirement

YOUR PRACTICE AND POSITIONING FOR STRATEGIC ADVANTAGE LEADERS PARTNERS, INC. 100 S. WYNSTONE PARK DRIVE NORTH BARRINGTON, IL 60010 847.304.

YOUR PRACTICE AND LEADERS PARTNERS POSITIONING FOR STRATEGIC ADVANTAGE ASSET LEVERAGE STRATEGIES INTRINSIC STOCK VALUE LOCK IN STRATEGY We all have our favorite stocks which most likely have taken a hit

YOUR PRACTICE AND LEADERS PARTNERS POSITIONING FOR STRATEGIC ADVANTAGE ASSET LEVERAGE STRATEGIES INTRINSIC STOCK VALUE LOCK IN STRATEGY We all have our favorite stocks which most likely have taken a hit

Using Life Insurance for Pension Maximization

Using Life Insurance for Pension Maximization Help your clients capitalize on their pension plans Agent Guide For agent use only. Not to be used for consumer solicitation purposes. Help Your Clients Obtain

Using Life Insurance for Pension Maximization Help your clients capitalize on their pension plans Agent Guide For agent use only. Not to be used for consumer solicitation purposes. Help Your Clients Obtain

Alternative Retirement Financial Plans and Their Features

RETIREMENT ACCOUNTS Gary R. Evans, 2006-2013, November 20, 2013. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

RETIREMENT ACCOUNTS Gary R. Evans, 2006-2013, November 20, 2013. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

Private pensions. Quality of life can be planned/

Private pensions Quality of life can be planned/ Is your future firmly resting on three pillars?/ A worthwhile financial future rests securely on three pillars. That's why a life insurance policy is always

Private pensions Quality of life can be planned/ Is your future firmly resting on three pillars?/ A worthwhile financial future rests securely on three pillars. That's why a life insurance policy is always

Household Life Cycle Protection: Life Insurance Holdings, Financial Vulnerability and Portfolio Implications

Household Life Cycle Protection: Life Insurance Holdings, Financial Vulnerability and Portfolio Implications August 28, 2006 Yijia Lin * Department of Accounting & Finance Youngstown State University ylin@ysu.edu

Household Life Cycle Protection: Life Insurance Holdings, Financial Vulnerability and Portfolio Implications August 28, 2006 Yijia Lin * Department of Accounting & Finance Youngstown State University ylin@ysu.edu

Your pension benefit options

2 Your pension benefit options Traditional pension plans generally provide the option of a lump-sum payment or a fixed monthly payment for life through an annuity. The fixed monthly payment amount is usually

2 Your pension benefit options Traditional pension plans generally provide the option of a lump-sum payment or a fixed monthly payment for life through an annuity. The fixed monthly payment amount is usually

How Credit Affects Revealed Risk Preferences

Evidence from Home Equity Loans and Voluntary Unemployment Insurance Kristoffer Markwardt Alessandro Martinello László Sándor + SFI and University of Copenhagen + Harvard University Liquidity and risk

Evidence from Home Equity Loans and Voluntary Unemployment Insurance Kristoffer Markwardt Alessandro Martinello László Sándor + SFI and University of Copenhagen + Harvard University Liquidity and risk

Financial Planning Questionnaire

Form No. (To be filled in by FPSB India) Financial Planning Questionnaire Candidate s Name FPSBI No. / NCFM No. Candidate s Signatures Mode of Registration Education Provider Name of the Education Provider

Form No. (To be filled in by FPSB India) Financial Planning Questionnaire Candidate s Name FPSBI No. / NCFM No. Candidate s Signatures Mode of Registration Education Provider Name of the Education Provider

RETIREMENT ACCOUNTS. Alternative Retirement Financial Plans and Their Features

RETIREMENT ACCOUNTS The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial tax advantages that will typically have the

RETIREMENT ACCOUNTS The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial tax advantages that will typically have the

PERCEPTION OF SENIOR CITIZEN RESPONDENTS AS TO REVERSE MORTGAGE SCHEME

CHAPTER- V PERCEPTION OF SENIOR CITIZEN RESPONDENTS AS TO REVERSE MORTGAGE SCHEME 5.1 Introduction The present study intended to investigate the senior citizen s retirement planning and their perception

CHAPTER- V PERCEPTION OF SENIOR CITIZEN RESPONDENTS AS TO REVERSE MORTGAGE SCHEME 5.1 Introduction The present study intended to investigate the senior citizen s retirement planning and their perception

PENSION PLAN DISTRIBUTIONS: THE IMPORTANCE OF FINANCIAL LITERACY. Robert L. Clark, Melinda Sandler Morrill, Steven G. Allen

PENSION PLAN DISTRIBUTIONS: THE IMPORTANCE OF FINANCIAL LITERACY Robert L. Clark, Melinda Sandler Morrill, Steven G. Allen ABSTRACT This chapter examines workers plans to take lump sum distributions versus

PENSION PLAN DISTRIBUTIONS: THE IMPORTANCE OF FINANCIAL LITERACY Robert L. Clark, Melinda Sandler Morrill, Steven G. Allen ABSTRACT This chapter examines workers plans to take lump sum distributions versus

Life Cycle Asset Allocation A Suitable Approach for Defined Contribution Pension Plans

Life Cycle Asset Allocation A Suitable Approach for Defined Contribution Pension Plans Challenges for defined contribution plans While Eastern Europe is a prominent example of the importance of defined

Life Cycle Asset Allocation A Suitable Approach for Defined Contribution Pension Plans Challenges for defined contribution plans While Eastern Europe is a prominent example of the importance of defined

the annuity y(p (pension) maze

maze") the annuity y(p (pension) maze Bruce Cameron Editor: Personal Finance the annuity maze warning!! no annuity will make up for a shortfall in retirement savings increasing your investment risk is not a solution

the annuity y(p (pension) maze Bruce Cameron Editor: Personal Finance the annuity maze warning!! no annuity will make up for a shortfall in retirement savings increasing your investment risk is not a solution

Enhanced Annuities. Contact us at info@justretirement.co.za 1

This brochure gives a brief explanation of Just Retirement Enhanced Annuities, all of which provide a guaranteed income for life. It explains who may qualify for a higher retirement income from this product

This brochure gives a brief explanation of Just Retirement Enhanced Annuities, all of which provide a guaranteed income for life. It explains who may qualify for a higher retirement income from this product

Life Insurance and Annuity Buyer s Guide

Life Insurance and Annuity Buyer s Guide Published by the Kentucky Office of Insurance Introduction The Kentucky Office of Insurance is pleased to offer this Life Insurance and Annuity Buyer s Guide as

Life Insurance and Annuity Buyer s Guide Published by the Kentucky Office of Insurance Introduction The Kentucky Office of Insurance is pleased to offer this Life Insurance and Annuity Buyer s Guide as

ECONOMICS AND FINANCE OF PENSIONS Lecture 8

ECONOMICS AND FINANCE OF PENSIONS Lecture 8 ANNUITIES MARKETS Dr David McCarthy Today s lecture Why study annuities? Annuity demand Theoretical demand for annuities The demand puzzle Asymmetric information

ECONOMICS AND FINANCE OF PENSIONS Lecture 8 ANNUITIES MARKETS Dr David McCarthy Today s lecture Why study annuities? Annuity demand Theoretical demand for annuities The demand puzzle Asymmetric information

Discussion by Paula Lopes

Trading Death: The Implications of Annuity Replication for the Annuity Puzzle, Arbitrage, Speculation and Portfolios Charles Sutcliffe Discussion by Paula Lopes Motivation Annuities are largely viewed

Trading Death: The Implications of Annuity Replication for the Annuity Puzzle, Arbitrage, Speculation and Portfolios Charles Sutcliffe Discussion by Paula Lopes Motivation Annuities are largely viewed

ESTATE PLANNING WORKSHEET

ESTATE PLANNING WORKSHEET Please complete the following worksheet and mail it to my office prior to our initial meeting, or e-mail it, or bring it with you. At the end of the worksheet is a list of documents

ESTATE PLANNING WORKSHEET Please complete the following worksheet and mail it to my office prior to our initial meeting, or e-mail it, or bring it with you. At the end of the worksheet is a list of documents

Financial Fact Finder

Financial Fact Finder Strategic Wealth Management Group Ltd. Chief Centre, Suite 100 455 Valley Brook Road McMurray, PA 15317 www.swmgroup.com Phone: 724.969.1180 Toll Free: 800.693.2200 Fax: 724.969.0321

Financial Fact Finder Strategic Wealth Management Group Ltd. Chief Centre, Suite 100 455 Valley Brook Road McMurray, PA 15317 www.swmgroup.com Phone: 724.969.1180 Toll Free: 800.693.2200 Fax: 724.969.0321

Uptake of Micro Life Insurance in Rural Ghana

Uptake of Micro Life Insurance in Rural Ghana Lena Giesbert (GIGA Hamburg & Humboldt University of Berlin) CPRC 2010 Conference Ten Years of War against Poverty : What have we learned since 2000 and what

Uptake of Micro Life Insurance in Rural Ghana Lena Giesbert (GIGA Hamburg & Humboldt University of Berlin) CPRC 2010 Conference Ten Years of War against Poverty : What have we learned since 2000 and what

LIVE NEWARK DEPARTMENT OF ECOMONIC AND HOUSING DEVELOPMENT DIVISION OF HOUSING AND REAL ESTATE HOME FACADE PROGRAM (HFP) APPLICATION

APPLICATION") LIVE NEWARK DEPARTMENT OF ECOMONIC AND HOUSING DEVELOPMENT DIVISION OF HOUSING AND REAL ESTATE HOME FACADE PROGRAM (HFP) APPLICATION Please PRINT and complete ALL pages of this application in its entirety

LIVE NEWARK DEPARTMENT OF ECOMONIC AND HOUSING DEVELOPMENT DIVISION OF HOUSING AND REAL ESTATE HOME FACADE PROGRAM (HFP) APPLICATION Please PRINT and complete ALL pages of this application in its entirety

Should I Buy an Income Annuity?

Prepared For: Valued Client Prepared By: CPS The purchase of any financial product involves a trade off. For example when saving for retirement, you are often faced with making a trade off between how

Prepared For: Valued Client Prepared By: CPS The purchase of any financial product involves a trade off. For example when saving for retirement, you are often faced with making a trade off between how

Trends in Household Wealth Dynamics, 2005-2007

Technical Series Paper #09-03 Trends in Household Wealth Dynamics, 2005-2007 Elena Gouskova and Frank Stafford Survey Research Center - Institute for Social Research University of Michigan September, 2009

Technical Series Paper #09-03 Trends in Household Wealth Dynamics, 2005-2007 Elena Gouskova and Frank Stafford Survey Research Center - Institute for Social Research University of Michigan September, 2009

Life Insurance and Annuity Buyer s Guide Introduction

Life Insurance and Annuity Buyer s Guide Introduction The Kentucky Office of Insurance is pleased to offer this Life Insurance and Annuity Buyer s Guide as an aid to assist you in determining your insurance

Life Insurance and Annuity Buyer s Guide Introduction The Kentucky Office of Insurance is pleased to offer this Life Insurance and Annuity Buyer s Guide as an aid to assist you in determining your insurance

Do You Have the Right Life Insurance?

Do You Have the Right Life Insurance? Having adequate life insurance should be an important part of your financial planning. The type(s) you choose will depend on your needs and goals. Life insurance was

Do You Have the Right Life Insurance? Having adequate life insurance should be an important part of your financial planning. The type(s) you choose will depend on your needs and goals. Life insurance was

Basic Annuity Basics

Basic Annuity Basics For broker use only; Securities and Investment Advisory Services offered through Woodbury Financial Services, Inc. Member FINRA, SIPC and Registered Investment Adviser. P O Box 64284

Basic Annuity Basics For broker use only; Securities and Investment Advisory Services offered through Woodbury Financial Services, Inc. Member FINRA, SIPC and Registered Investment Adviser. P O Box 64284

Contents: What is an Annuity?

Contents: What is an Annuity? When might I need an annuity policy? Types of annuities Pension annuities Annuity income options Enhanced and Lifestyle annuities Impaired Life annuities Annuity rates FAQs

Contents: What is an Annuity? When might I need an annuity policy? Types of annuities Pension annuities Annuity income options Enhanced and Lifestyle annuities Impaired Life annuities Annuity rates FAQs

A Guide to Life Insurance Cover Creating your success through Financial Planning

& Guidance A Guide to Life Insurance Cover A Guide to Life Insurance Cover Financial Broker Contents How can I protect my family financially if I die? 02 What is life insurance? 03 What is a Financial

& Guidance A Guide to Life Insurance Cover A Guide to Life Insurance Cover Financial Broker Contents How can I protect my family financially if I die? 02 What is life insurance? 03 What is a Financial

Working Beyond Retirement-Age

Working Beyond Retirement-Age Kelly A. Holder and Sandra L. Clark U.S. Census Bureau Housing and Household Economics Division Labor Force Statistics Branch Presented at the American Sociological Association

Working Beyond Retirement-Age Kelly A. Holder and Sandra L. Clark U.S. Census Bureau Housing and Household Economics Division Labor Force Statistics Branch Presented at the American Sociological Association

A Guide to Life Insurance Cover Creating your success through Financial Planning

& Guidance A Guide to Life Insurance Cover Contents How can I protect my family financially if I die? 02 What is life insurance? 03 What is a Financial Broker? 06 Why would I need to use a Financial Broker?

& Guidance A Guide to Life Insurance Cover Contents How can I protect my family financially if I die? 02 What is life insurance? 03 What is a Financial Broker? 06 Why would I need to use a Financial Broker?

FINANCIAL ANALYSIS ****** UPDATED FOR 55% BENEFIT ****** ****** FOR ALL SURVIVORS ******

FINANCIAL ANALYSIS ****** UPDATED FOR 55% BENEFIT ****** ****** FOR ALL SURVIVORS ****** This fact sheet is designed to supplement the Department of Defense brochure: SBP SURVIVOR BENEFIT PLAN FOR THE

FINANCIAL ANALYSIS ****** UPDATED FOR 55% BENEFIT ****** ****** FOR ALL SURVIVORS ****** This fact sheet is designed to supplement the Department of Defense brochure: SBP SURVIVOR BENEFIT PLAN FOR THE

How much do means-tested benefits reduce the demand for annuities?

How much do means-tested benefits reduce the demand for annuities? MONIKA BÜTLER SEW HSG Universität St. Gallen, CESIfo & Netspar KIM PEIJNENBURG Bocconi University, IGIER, & Netspar STEFAN STAUBLI University

How much do means-tested benefits reduce the demand for annuities? MONIKA BÜTLER SEW HSG Universität St. Gallen, CESIfo & Netspar KIM PEIJNENBURG Bocconi University, IGIER, & Netspar STEFAN STAUBLI University

TABLE OF CONTENTS: PART A: EXAMPLES

TABLE OF CONTENTS: PART A: EXAMPLES Compound interest calculations Example 1: Determine the future value of a single payment (lump sum)... 3 Example 2: Determine the annual rate of interest earned by an

TABLE OF CONTENTS: PART A: EXAMPLES Compound interest calculations Example 1: Determine the future value of a single payment (lump sum)... 3 Example 2: Determine the annual rate of interest earned by an

WOMEN AND RISK MADE SIMPLE

WOMEN AND RISK MADE SIMPLE Working with the profession to simplify the language of insurance UNDERSTANDING WOMEN AND RISK Risk is part of life. At home, at work, on the road, on holiday, you re at risk

WOMEN AND RISK MADE SIMPLE Working with the profession to simplify the language of insurance UNDERSTANDING WOMEN AND RISK Risk is part of life. At home, at work, on the road, on holiday, you re at risk

Income for Life Annuity Program* Immediate Annuities for Retirement Income

Income for Life Annuity Program* Immediate Annuities for Retirement Income *ICMA-RC partners with select insurance companies that make annuities available through the Income for Life Annuity program. Participating

Income for Life Annuity Program* Immediate Annuities for Retirement Income *ICMA-RC partners with select insurance companies that make annuities available through the Income for Life Annuity program. Participating

What to Consider When Faced With the Pension Election Decision

PENSION ELECTION Key Information About Your Pension (Optional Forms of Benefits) Pension Math and Factors to Consider Pension Maximization What Happens if Your Company Files for Bankruptcy and Your Company

PENSION ELECTION Key Information About Your Pension (Optional Forms of Benefits) Pension Math and Factors to Consider Pension Maximization What Happens if Your Company Files for Bankruptcy and Your Company

Chapter URL: http://www.nber.org/chapters/c10322

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Themes in the Economics of Aging Volume Author/Editor: David A. Wise, editor Volume Publisher:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Themes in the Economics of Aging Volume Author/Editor: David A. Wise, editor Volume Publisher:

Choosing the right investment strategy is not as complicated as it seems. This questionnaire will provide us guidance on the type of investor you

Choosing the right investment strategy is not as complicated as it seems. This questionnaire will provide us guidance on the type of investor you might be and also assist us in selecting the best suited

Choosing the right investment strategy is not as complicated as it seems. This questionnaire will provide us guidance on the type of investor you might be and also assist us in selecting the best suited

Notes - Gruber, Public Finance Chapter 13 - Social Security Social Security started in 1935 in Great Depression. Asset values had fallen drastically,

Notes - Gruber, Public Finance Chapter 13 - Social Security Social Security started in 1935 in Great Depression. Asset values had fallen drastically, many elderly lost their lifetime savings. Workers pay

Notes - Gruber, Public Finance Chapter 13 - Social Security Social Security started in 1935 in Great Depression. Asset values had fallen drastically, many elderly lost their lifetime savings. Workers pay

China s Middle Market for Life Insurance

China s Middle Market for Life Insurance May 2014 Sponsored by: SOA International Section SOA Marketing & Distribution Section SOA Research Expanding Boundaries Pool The opinions expressed and conclusions

China s Middle Market for Life Insurance May 2014 Sponsored by: SOA International Section SOA Marketing & Distribution Section SOA Research Expanding Boundaries Pool The opinions expressed and conclusions

THE TRUSTEES RECOMMEND THAT YOU ASK FOR THESE QUOTES TO BETTER UNDERSTAND YOUR OPTIONS. THERE IS NO OBLIGATION TO ACCEPT THE QUOTES.

Annexure 1- Detailed Guide CAPE PENINSULA UNIVERSITY OF TECHNOLOGY RETIREMENT FUND COMMISSION FREE PENSION QUOTATIONS When you reach retirement, you will face a difficult decision as to what pension to

Annexure 1- Detailed Guide CAPE PENINSULA UNIVERSITY OF TECHNOLOGY RETIREMENT FUND COMMISSION FREE PENSION QUOTATIONS When you reach retirement, you will face a difficult decision as to what pension to

The Kreager Law Firm 7373 Broadway, Suite 500 San Antonio, Texas 78209 (210) 829-7722. Estate Planning Information

829-7722. Estate Planning Information") Estate Planning Information Please complete this questionnaire and bring it with you for your initial consultation with us. Of course, this information will be kept in strictest confidence. A. Husband

Estate Planning Information Please complete this questionnaire and bring it with you for your initial consultation with us. Of course, this information will be kept in strictest confidence. A. Husband

The Demand Analysis of Life Insurance for Ethnic Regions in Gansu Province in China

www.sciedu.ca/ijba International Journal of Business Administration Vol. 5, o. 4; 2014 The Demand Analysis of Life for Ethnic Regions in Gansu Province in China Jianshen Zhang 1 1 School of Economics,

www.sciedu.ca/ijba International Journal of Business Administration Vol. 5, o. 4; 2014 The Demand Analysis of Life for Ethnic Regions in Gansu Province in China Jianshen Zhang 1 1 School of Economics,

Should I Buy an Income Annuity?

Prepared For: Fred & Wilma FLINT Prepared By: Don Maycock The purchase of any financial product involves a trade off. For example when saving for retirement, you are often faced with making a trade off

Prepared For: Fred & Wilma FLINT Prepared By: Don Maycock The purchase of any financial product involves a trade off. For example when saving for retirement, you are often faced with making a trade off

Viliam Páleník. Kristína Petríková. Institute of Economic Research SAS European Economic and Social Committee. Institute of Economic Research SAS

Viliam Páleník Institute of Economic Research SAS European Economic and Social Committee Kristína Petríková Institute of Economic Research SAS Motivation Introduction Context Financial Services Equity

Viliam Páleník Institute of Economic Research SAS European Economic and Social Committee Kristína Petríková Institute of Economic Research SAS Motivation Introduction Context Financial Services Equity

Protect your heirs by selecting the right structure for your Vanguard Variable Annuity

Protect your heirs by selecting the right structure for your Vanguard Variable Annuity 5074 (04/11) Make the right choices when structuring your annuity When you buy a Vanguard Variable Annuity, you have

Protect your heirs by selecting the right structure for your Vanguard Variable Annuity 5074 (04/11) Make the right choices when structuring your annuity When you buy a Vanguard Variable Annuity, you have