Forensic Audit and Automated Oversight Federal Audit Executive Council September 24, 2009

|

|

|

- Peregrine Snow

- 10 years ago

- Views:

Transcription

1 Forensic Audit and Automated Oversight Federal Audit Executive Council September 24, 2009 Dr. Brett Baker, CPA, CISA Assistant Inspector General for Audit U.S. Department of Commerce OIG

2 Overview Forensic Audit and Automated Oversight Data Mining Techniques Equipment and Software Forensic Approach 2

3 Forensic Audit and Automated Oversight Definition of Forensic Audit Audit that specifically looks for financial misconduct, abusive or wasteful activity. Close coordination with investigators More than Computer Assisted Audit Techniques (CAATs) Forensic audit is growing in the Federal government GAO s Forensic Audit and Special Investigations (FSI) DoDIGData Mining Federal outlays are $2 trillion annually Approximately 11,000 OIG staff to provide oversight OMB estimates improper payments for Federal government at $72B (4%) GAGAS requires tests for fraud in audit work 100% review using automated business rules versus statistical sampling There is a place for both Automated Oversight Continuous monitoring Quick response 3

GAGAS requires tests for fraud in audit work 100% review using automated business rules versus statistical sampling There is a place for both Automated")

4 FY2008 Improper Payment Estimates

5 Data Versus Information An Endless Maze of Data... but No Information 5

6 What is Data Mining? Refers to the use of machine learning and statistical analysis for the purpose of finding patterns in data sets. If You Know Exactly What You Are Looking for, Use Structured Query Language (SQL). If You Know Only Vaguely What You Are Looking for, Turn to Data Mining. Most often used (up until recently) in marketing and customer analysis 6

.")

7 Different Levels of Knowledge Data Facts, numbers Information Summary Reports ACL, IDEA Knowledge Descriptive Analytics SAS, SPSS, ACL, IDEA Wisdom Predictive Analytics Clementine Intelligent Miner Enterprise Miner 7

8 Data Analysis Software - Fosters Creativity Can perform the tests wanted, instead of being limited to what technical staff can, or will, provide Not limited to just predetermined data formats and/or relationships Can create relationships, check calculations and perform comparisons Can examine all records, not just a sample Useful for identifying misappropriation of assets and fraudulent financial reporting Allows limitless number of analytical relationships to be assessed within large databases comparing large databases Identifies anomalies 8

9 Common Data Analysis Tests and Techniques Join Summarization Corrupt data (conversion) Blank fields (noteworthy if field is mandatory) Invalid dates Bounds testing Completeness Uniqueness Invalid codes Unreliable computed fields Illogical field relationships Trend analysis Duplicates 9

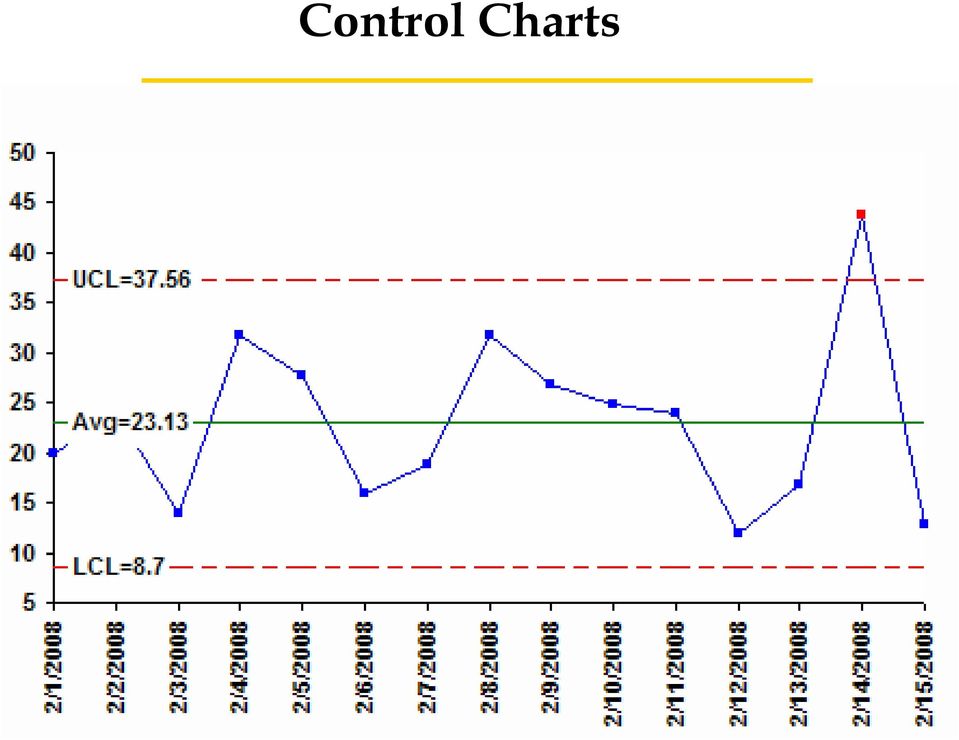

10 Control Charts

11 Frequency Distribution Anomalous Activity Normal Activity Anomalous Activity

12 Comparing Data Files (Three-Bucket Theory) Vendors Not Paid Yet Vendors Paid and In Vendor Table Vendors Paid but not In Vendor Table Vendor Table Disbursing Transactions

13 Hardware and Software Applications Hardware SQL servers Mainframe (QMF) Docking stations Terminal server Software Applications Data mining and predictive analytics, e.g., Clementine Data interrogation e.g., ACL, IDEA, MS Access, Excel Statistical analysis e.g., SPSS and SAS Link analysis I2 Lexis-Nexis Data conversion utilities (Monarch) Internet, open-source research Access to system query tools 13

Internet, open-source research Access to system query tools 13")

14 Forensic Audit Approach Audit objectives and audit universe Work with investigations Structured brainstorming Consider SME conference Identify indicators of potential fraud and ways to find in data Process to identify financial risks Map out the end-to-end process Identify systems and key processes Identify key controls Identify and obtain transaction-level data Record layout 1000 record dump ACL, IDEA, and Monarch can read virtually any data format Flat files, Delimited files, Dbase files, MS Access, Report files,. No file size limits Build targeted business rules and run against data Examine anomalies 14

15 End-to-End Payment Universe Forensic Audit Approach Personnel Systems Accounting Systems Contracting Systems Central Contractor Registry People Pay Entitlement Systems Commercial Pay Entitlement Systems Disbursing Systems $$ Treasury Check Federal Reserve System Commercial Bank Data Analysis 15

16 Growing a Forensic Audit Capability Developing an organization-wide capability All audit staff should have basic skill with ACL, IDEA, Access Forensic audit units perform more sophisticated analyses Phased development Staffing system savvy, critical thinking, analytical, business process knowledge Hardware and software Training.then immediate application to work Standard audit programs should include data analysis steps Include data analysis measures in staff performance plans Reporting Forensic Audit Results Tables Process flows.30,000 feet Forensic techniques used in audit can help improve process recommend them 16

17 DoD Joint Purchase Card Review (2002) Purpose Develop an automated oversight capability to identify anomalies in purchase card data that may indicate fraud or abuse Joint effort of all Defense audit and investigation organizations Transaction Universe 12 million purchase card transactions ($6.5B) 200,000 cardholders and 40,000 authorizing officials Data mining Results Developed 46 fraud indicators from SME conferences 6.5 million transactions (1+ indicator) 13,393 transactions (combinations of indicators) 2066 cardholders and 1604 approving officials in 752 locations 8243 transactions (researched by auditors ) 1250 questioned transactions (some level of misuse) Outcomes cases with adverse action and 75 investigations opened - Capability to embed data mining indicators in credit card company systems to promote continuous monitoring

13,393 transactions (combinations of indicators) 2066 cardholders and 1604 approving officials in 752 locations 8243 transactions (researched by auditors ) 1250")

18 Top Performing Combinations 97% Adult Internet sites, Weekend/Holidays 67% Purchases from 1 vendor, CH=AO 57% Adult Internet sites 57% Internet transactions, 3rd party billing 53% Interesting vendors, many transactions 43% Even dollars, near limit, same vendor, vendor business w/few CHs

19 Examples of Misuse and Abuse Splitting procurements Purchasing goods or services which, although for a valid governmental purpose, are prohibited on a purchase card Purchasing items for which there is no government need Engaging in fraudulent activity Invoices were being certified without being reviewed.

20

21 Way Ahead Set up working group to see where the OIG community is with forensic audit and automated oversight Offer assistance to OIGs on development and expansion of capabilities

Predictive Analysis Risk Analysis

Predictive Analysis Risk Analysis MARYLAND ASSOCIATION OF CPAS GOVERNMENT AND NOT-FOR-PROFIT CONFERENCE April 25, 2014 Overview Forensic Audit and Automated Oversight Data Analytics for Grant Oversight

Predictive Analysis Risk Analysis MARYLAND ASSOCIATION OF CPAS GOVERNMENT AND NOT-FOR-PROFIT CONFERENCE April 25, 2014 Overview Forensic Audit and Automated Oversight Data Analytics for Grant Oversight

Using Technology to Automate Fraud Detection Within Key Business Process Areas

Using Technology to Automate Fraud Detection Within Key Business Process Areas 2013 ACFE Canadian Fraud Conference September 10, 2013 John Verver, CA, CISA, CMA Vice President, Strategy ACL Services Ltd

Using Technology to Automate Fraud Detection Within Key Business Process Areas 2013 ACFE Canadian Fraud Conference September 10, 2013 John Verver, CA, CISA, CMA Vice President, Strategy ACL Services Ltd

The Federal Railroad Retirement Board (RRB) and Data Analytics

and Data Analytics") Exploring Innovation Leads to Data Analytics Phase I February 14, 2013 OFFICE OF INSPECTOR GENERAL RAILROAD RETIREMENT BOARD INTRODUCTION In response to the Federal government s mandate to become more

Exploring Innovation Leads to Data Analytics Phase I February 14, 2013 OFFICE OF INSPECTOR GENERAL RAILROAD RETIREMENT BOARD INTRODUCTION In response to the Federal government s mandate to become more

by: Scott Baranowski, CIA

Community Bank Auditors Group A/P, Procurement and Credit Card Internal Controls June 4, 2014 by: Scott Baranowski, CIA MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2013 Wolf

Community Bank Auditors Group A/P, Procurement and Credit Card Internal Controls June 4, 2014 by: Scott Baranowski, CIA MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2013 Wolf

AGA Kansas City Chapter Data Analytics & Continuous Monitoring

AGA Kansas City Chapter Data Analytics & Continuous Monitoring Agenda Market Overview & Drivers for Change Key challenges that organizations face Data Analytics What is data analytics and how can it help

AGA Kansas City Chapter Data Analytics & Continuous Monitoring Agenda Market Overview & Drivers for Change Key challenges that organizations face Data Analytics What is data analytics and how can it help

Why is Internal Audit so Hard?

Why is Internal Audit so Hard? 2 2014 Why is Internal Audit so Hard? 3 2014 Why is Internal Audit so Hard? Waste Abuse Fraud 4 2014 Waves of Change 1 st Wave Personal Computers Electronic Spreadsheets

Why is Internal Audit so Hard? 2 2014 Why is Internal Audit so Hard? 3 2014 Why is Internal Audit so Hard? Waste Abuse Fraud 4 2014 Waves of Change 1 st Wave Personal Computers Electronic Spreadsheets

Audit Readiness Essentials

Audit Readiness Essentials An Insider s Answers to Your Most Commonly Asked Questions www.pwc.com/publicsector Contents > 1 Introduction 2 Leadership Support 5 Audit Readiness Human Capital 9 Internal

Audit Readiness Essentials An Insider s Answers to Your Most Commonly Asked Questions www.pwc.com/publicsector Contents > 1 Introduction 2 Leadership Support 5 Audit Readiness Human Capital 9 Internal

Use of Data Extraction & Analysis Software In a Financial Statement Audit

Use of Data Extraction & Analysis Software In a Financial Statement Audit A Message from The Audit Wizard April 2008 Making Auditors Proficient, Inc. Phone: 352-750-9636 www.billallen.com E-mail: [email protected]

Use of Data Extraction & Analysis Software In a Financial Statement Audit A Message from The Audit Wizard April 2008 Making Auditors Proficient, Inc. Phone: 352-750-9636 www.billallen.com E-mail: [email protected]

Opening Statement of Senator Susan M. Collins Chairman, Committee on Homeland Security and Governmental Affairs

Opening Statement of Senator Susan M. Collins Chairman, Committee on Homeland Security and Governmental Affairs DHS Purchase Cards: Credit Without Accountability July 19, 2006 *** Today, the Committee

Opening Statement of Senator Susan M. Collins Chairman, Committee on Homeland Security and Governmental Affairs DHS Purchase Cards: Credit Without Accountability July 19, 2006 *** Today, the Committee

Fighting Fraud with Data Mining & Analysis

Fighting Fraud with Data Mining & Analysis Leonard W. Vona December 2008 Fraud Auditing, Inc. Phone: 518-784-2250 www.fraudauditing.net E-mail: [email protected] Copyright 2008 Leonard Vona and Fraud

Fighting Fraud with Data Mining & Analysis Leonard W. Vona December 2008 Fraud Auditing, Inc. Phone: 518-784-2250 www.fraudauditing.net E-mail: [email protected] Copyright 2008 Leonard Vona and Fraud

DISTRIBUTION: ASSISTANT G-1 FOR CIVILIAN PERSONNEL POLICY, DEPARTMENT OF THE ARMY DIRECTOR, PLANS, PROGRAMS, AND DIVERSITY, DEPARTMENT OF THE NAVY

DISTRIBUTION: ASSISTANT G-1 FOR CIVILIAN PERSONNEL POLICY, DEPARTMENT OF THE ARMY DIRECTOR, PLANS, PROGRAMS, AND DIVERSITY, DEPARTMENT OF THE NAVY DEPUTY DIRECTOR, PERSONNEL FORCE MANAGEMENT, DEPARTMENT

DISTRIBUTION: ASSISTANT G-1 FOR CIVILIAN PERSONNEL POLICY, DEPARTMENT OF THE ARMY DIRECTOR, PLANS, PROGRAMS, AND DIVERSITY, DEPARTMENT OF THE NAVY DEPUTY DIRECTOR, PERSONNEL FORCE MANAGEMENT, DEPARTMENT

Office of Investigations GEOFFREY CHERRINGTON, DEPUTY ASSISTANT INSPECTOR GENERAL FOR INVESTIGATIONS

Introduction to the GSA OIG Office of Investigations GEOFFREY CHERRINGTON, DEPUTY ASSISTANT INSPECTOR GENERAL FOR INVESTIGATIONS History of the Inspector General The Inspector General Act of 1978, as amended,

Introduction to the GSA OIG Office of Investigations GEOFFREY CHERRINGTON, DEPUTY ASSISTANT INSPECTOR GENERAL FOR INVESTIGATIONS History of the Inspector General The Inspector General Act of 1978, as amended,

ACL WHITEPAPER. Automating Fraud Detection: The Essential Guide. John Verver, CA, CISA, CMC, Vice President, Product Strategy & Alliances

ACL WHITEPAPER Automating Fraud Detection: The Essential Guide John Verver, CA, CISA, CMC, Vice President, Product Strategy & Alliances Contents EXECUTIVE SUMMARY..................................................................3

ACL WHITEPAPER Automating Fraud Detection: The Essential Guide John Verver, CA, CISA, CMC, Vice President, Product Strategy & Alliances Contents EXECUTIVE SUMMARY..................................................................3

Leveraging Big Data to Mitigate Health Care Fraud Risk

Leveraging Big Data to Mitigate Health Care Fraud Risk Jeremy Clopton, CPA, CFE, ACDA Senior Managing Consultant BKD, LLP Forensics & Valuation Services Introduction Health Care Is Victimized by Fraud

Leveraging Big Data to Mitigate Health Care Fraud Risk Jeremy Clopton, CPA, CFE, ACDA Senior Managing Consultant BKD, LLP Forensics & Valuation Services Introduction Health Care Is Victimized by Fraud

Procurement Fraud Identification & Role of Data Mining

The paper describes the known boundaries of Procurement Fraud and outlines the scope of data mining within the same. The paper also highlights some of the basic steps to be taken care of before the application

The paper describes the known boundaries of Procurement Fraud and outlines the scope of data mining within the same. The paper also highlights some of the basic steps to be taken care of before the application

Using CAAT in Compliance

Using CAAT in Compliance Auditing Suzann Hall, CPA, ACDA November 12, 2010 CHAN Founded in 1997 through the collaboration of Ascension Health and Catholic Health Initiatives, the two largest not-for-profit

Using CAAT in Compliance Auditing Suzann Hall, CPA, ACDA November 12, 2010 CHAN Founded in 1997 through the collaboration of Ascension Health and Catholic Health Initiatives, the two largest not-for-profit

DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs Need Improvement

Report No. DODIG-2015-068 I nspec tor Ge ne ral U.S. Department of Defense JA N UA RY 1 4, 2 0 1 5 DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs

Report No. DODIG-2015-068 I nspec tor Ge ne ral U.S. Department of Defense JA N UA RY 1 4, 2 0 1 5 DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs

OIG Hotline. Overview... 2. Examples of Allegations That Should Be Reported to the OIG Hotline... 3. Guidelines for Reporting Fraud...

OIG Hotline Overview... 2 Examples of Allegations That Should Be Reported to the OIG Hotline... 3 Guidelines for Reporting Fraud... 4 False Claims... 4 Embezzlement of Government Funds... 4 Contract Fraud...

OIG Hotline Overview... 2 Examples of Allegations That Should Be Reported to the OIG Hotline... 3 Guidelines for Reporting Fraud... 4 False Claims... 4 Embezzlement of Government Funds... 4 Contract Fraud...

Five-Year Strategic Plan

U.S. Department of Education Office of Inspector General Five-Year Strategic Plan Fiscal Years 2014 2018 Promoting the efficiency, effectiveness, and integrity of the Department s programs and operations

U.S. Department of Education Office of Inspector General Five-Year Strategic Plan Fiscal Years 2014 2018 Promoting the efficiency, effectiveness, and integrity of the Department s programs and operations

Internet Access to Information on Office of Inspector General Oversight of Agency Implementation of the American Recovery and Reinvestment Act of 2009

U.S. Department of Agriculture Office of Inspector General Immediate Office of Inspector General Internet Access to Information on Office of Inspector General Oversight of Agency Implementation of the

U.S. Department of Agriculture Office of Inspector General Immediate Office of Inspector General Internet Access to Information on Office of Inspector General Oversight of Agency Implementation of the

Microsoft Confidential

Brock Phillips, CPA, CFE, CCEP Forensic Accounting Sr. Manager Financial Integrity Unit Microsoft Audit Group Lou DeCola, CPA, CIA, CFE Forensic Accounting Sr. Manager Financial Integrity Unit Microsoft

Brock Phillips, CPA, CFE, CCEP Forensic Accounting Sr. Manager Financial Integrity Unit Microsoft Audit Group Lou DeCola, CPA, CIA, CFE Forensic Accounting Sr. Manager Financial Integrity Unit Microsoft

REPORT ON INDEPENDENT EVALUATION AND ASSESSMENT OF INTERNAL CONTROL FOR CONTRACT OVERSIGHT

REPORT ON INDEPENDENT EVALUATION AND ASSESSMENT OF INTERNAL CONTROL FOR CONTRACT OVERSIGHT SUBMITTED TO THE U.S. SECURITIES AND EXCHANGE COMMISSION OFFICE OF INSPECTOR GENERAL Cotton & Company LLP Auditors

REPORT ON INDEPENDENT EVALUATION AND ASSESSMENT OF INTERNAL CONTROL FOR CONTRACT OVERSIGHT SUBMITTED TO THE U.S. SECURITIES AND EXCHANGE COMMISSION OFFICE OF INSPECTOR GENERAL Cotton & Company LLP Auditors

GOVERNANCE: Enhanced Controls Needed To Avoid Duplicate Payments

GOVERNANCE: Enhanced Controls Needed To Avoid Duplicate Payments Audit Report OIG-A-2013-018 September 20, 2013 NATIONAL RAILROAD PASSENGER CORPORATION Office of Inspector General REPORT HIGHLIGHTS Why

GOVERNANCE: Enhanced Controls Needed To Avoid Duplicate Payments Audit Report OIG-A-2013-018 September 20, 2013 NATIONAL RAILROAD PASSENGER CORPORATION Office of Inspector General REPORT HIGHLIGHTS Why

AUDIT REPORT REPORT NUMBER 14 10. Information Technology Microsoft Software Licenses March 27, 2014

AUDIT REPORT REPORT NUMBER 14 10 Information Technology Microsoft Software Licenses March 27, 2014 Date March 27, 2014 To Chief Information Officer From Inspector General Subject Audit Report Information

AUDIT REPORT REPORT NUMBER 14 10 Information Technology Microsoft Software Licenses March 27, 2014 Date March 27, 2014 To Chief Information Officer From Inspector General Subject Audit Report Information

Keith Barger MFS, MCSE, CCE

Keith Barger MFS, MCSE, CCE Principal/Practice Leader Advisory Services Keith Barger is a Principal in the Advisory Services practice with Grant Thornton and the Practice Leader for Forensic Accounting

Keith Barger MFS, MCSE, CCE Principal/Practice Leader Advisory Services Keith Barger is a Principal in the Advisory Services practice with Grant Thornton and the Practice Leader for Forensic Accounting

Department of Homeland Security Office of Inspector General. Audit of Application Controls for FEMA's Individual Assistance Payment Application

Department of Homeland Security Office of Inspector General Audit of Application Controls for FEMA's Individual Assistance Payment Application OIG-09-104 September 2009 Table of Contents Objectives,

Department of Homeland Security Office of Inspector General Audit of Application Controls for FEMA's Individual Assistance Payment Application OIG-09-104 September 2009 Table of Contents Objectives,

Continuous Auditing with Data Analytics

Continuous Auditing with Data Analytics Brooke Miller, CPA, CIA, CPCU [email protected] Sean Scranton, CPCU, CISSP, CISM, CISA [email protected] Overview Understand embedding data analytics

Continuous Auditing with Data Analytics Brooke Miller, CPA, CIA, CPCU [email protected] Sean Scranton, CPCU, CISSP, CISM, CISA [email protected] Overview Understand embedding data analytics

Using Predictive Analytics to Detect Contract Fraud, Waste, and Abuse Case Study from U.S. Postal Service OIG

Using Predictive Analytics to Detect Contract Fraud, Waste, and Abuse Case Study from U.S. Postal Service OIG MACPA Government & Non Profit Conference April 26, 2013 Isaiah Goodall, Director of Business

Using Predictive Analytics to Detect Contract Fraud, Waste, and Abuse Case Study from U.S. Postal Service OIG MACPA Government & Non Profit Conference April 26, 2013 Isaiah Goodall, Director of Business

Implementation of the DoD Management Control Program for Navy Acquisition Category II and III Programs (D-2004-109)

") August 17, 2004 Acquisition Implementation of the DoD Management Control Program for Navy Acquisition Category II and III Programs (D-2004-109) Department of Defense Office of the Inspector General Quality

August 17, 2004 Acquisition Implementation of the DoD Management Control Program for Navy Acquisition Category II and III Programs (D-2004-109) Department of Defense Office of the Inspector General Quality

Department of Homeland Security Office of Inspector General

Department of Homeland Security Office of Inspector General Final Letter Report: Potential Duplicate Benefits Between FEMA s National Flood Insurance Program and Housing Assistance Programs OIG-09-102

Department of Homeland Security Office of Inspector General Final Letter Report: Potential Duplicate Benefits Between FEMA s National Flood Insurance Program and Housing Assistance Programs OIG-09-102

San Francisco Chapter. Jonathan Shipman, Ernst & Young David Morgan, Ernst & Young

Jonathan Shipman, Ernst & Young David Morgan, Ernst & Young Learning Objectives Understand how data analysis can impact/improve business Understand typical data analysis challenges Understand the various

Jonathan Shipman, Ernst & Young David Morgan, Ernst & Young Learning Objectives Understand how data analysis can impact/improve business Understand typical data analysis challenges Understand the various

LGMA Qld Governance and Corporate Planning Village Forum

www.pwc.com.au Fraud Risk Management Fraud Risk Assessments LGMA Qld Governance and Corporate Planning Village Forum March 2015 Agenda Introductions Fraud Risk Management Fraud Statistics s Global Economic

www.pwc.com.au Fraud Risk Management Fraud Risk Assessments LGMA Qld Governance and Corporate Planning Village Forum March 2015 Agenda Introductions Fraud Risk Management Fraud Statistics s Global Economic

Summary of DoD Office of the Inspector General Audits of DoD Financial Management Challenges

Inspector General U.S. Department of Defense Report No. DODIG-2015-144 JULY 7, 2015 Summary of DoD Office of the Inspector General Audits of DoD Financial Management Challenges INTEGRITY EFFICIENCY ACCOUNTABILITY

Inspector General U.S. Department of Defense Report No. DODIG-2015-144 JULY 7, 2015 Summary of DoD Office of the Inspector General Audits of DoD Financial Management Challenges INTEGRITY EFFICIENCY ACCOUNTABILITY

OFFICE OF INSPECTOR GENERAL

NATIONAL CREDIT UNION ADMINISTRATION OFFICE OF INSPECTOR GENERAL REVIEW OF NATIONAL CREDIT UNION ADMINISTRATION S PURCHASE AND TRAVEL CARD PROGRAMS Report #OIG-15-07 March 31, 2015 James W. Hagen Inspector

NATIONAL CREDIT UNION ADMINISTRATION OFFICE OF INSPECTOR GENERAL REVIEW OF NATIONAL CREDIT UNION ADMINISTRATION S PURCHASE AND TRAVEL CARD PROGRAMS Report #OIG-15-07 March 31, 2015 James W. Hagen Inspector

Fraud and Fraud Detection. A Data Analytics Approach + Website. Wiley Corporate F&A

Brochure More information from http://www.researchandmarkets.com/reports/2866056/ Fraud and Fraud Detection. A Data Analytics Approach + Website. Wiley Corporate F&A Description: Detect fraud faster no

Brochure More information from http://www.researchandmarkets.com/reports/2866056/ Fraud and Fraud Detection. A Data Analytics Approach + Website. Wiley Corporate F&A Description: Detect fraud faster no

Internal Control Review of the Government Purchase Card Program

Internal Control Review of the Government Purchase Card Program September 18, 2008 Report No. 440 UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 OFFICE OF INSPECTOR GENERAL September

Internal Control Review of the Government Purchase Card Program September 18, 2008 Report No. 440 UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 OFFICE OF INSPECTOR GENERAL September

Fraud Detection & Data Analytics

September 2008 Fraud Detection & Data Analytics How to Utilize CAATs to detect fraud AN INDEPENDENT MEMBER OF BAKER TILLY INTERNATIONAL 505 AFFILIATE OFFICES WORLDWIDE Course Topics Overview of Data Analytics

September 2008 Fraud Detection & Data Analytics How to Utilize CAATs to detect fraud AN INDEPENDENT MEMBER OF BAKER TILLY INTERNATIONAL 505 AFFILIATE OFFICES WORLDWIDE Course Topics Overview of Data Analytics

AUDIT REPORT 12-1 8. Audit of Controls over GPO s Fleet Credit Card Program. September 28, 2012

AUDIT REPORT 12-1 8 Audit of Controls over GPO s Fleet Credit Card Program September 28, 2012 Date September 28, 2012 To Director, Acquisition Services From Inspector General Subject Audit Report Audit

AUDIT REPORT 12-1 8 Audit of Controls over GPO s Fleet Credit Card Program September 28, 2012 Date September 28, 2012 To Director, Acquisition Services From Inspector General Subject Audit Report Audit

Information overload: How to make data analytics work for the internal audit function

Information overload: How to make data analytics work for the internal audit function Danny Miller, Scott Higgins and Michael Rose Contents 1 A value proposition for internal audit 2 Leveraging data analytics

Information overload: How to make data analytics work for the internal audit function Danny Miller, Scott Higgins and Michael Rose Contents 1 A value proposition for internal audit 2 Leveraging data analytics

Implementing a New Technology: FPS Successes, Challenges, and Best Practices

Implementing a New Technology: FPS Successes, Challenges, and Best Practices Centers for Medicare & Medicaid Services Raymond Wedgeworth Director, Data Analytics and Control Group Center for Program Integrity

Implementing a New Technology: FPS Successes, Challenges, and Best Practices Centers for Medicare & Medicaid Services Raymond Wedgeworth Director, Data Analytics and Control Group Center for Program Integrity

Current Uses and Trends in ACL and Data Mining

Current Uses and Trends in ACL and Data Mining Weaver and Tidwell, L.L.P. January 10, 2013 Marlon B Williams, CPA, ACDA Partner, Assurance Reema Parappilly, CISA Senior Manager, IT Advisory Objective Discuss

Current Uses and Trends in ACL and Data Mining Weaver and Tidwell, L.L.P. January 10, 2013 Marlon B Williams, CPA, ACDA Partner, Assurance Reema Parappilly, CISA Senior Manager, IT Advisory Objective Discuss

Funding Invoices to Expedite the Closure of Contracts Before Transitioning to a New DoD Payment System (D-2002-076)

") March 29, 2002 Financial Management Funding Invoices to Expedite the Closure of Contracts Before Transitioning to a New DoD Payment System (D-2002-076) Department of Defense Office of the Inspector General

March 29, 2002 Financial Management Funding Invoices to Expedite the Closure of Contracts Before Transitioning to a New DoD Payment System (D-2002-076) Department of Defense Office of the Inspector General

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL 400 MARYLAND AVENUE, S.W. WASHINGTON, DC 20202-1500.

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL 400 MARYLAND AVENUE, S.W. WASHINGTON, DC 20202-1500 February 1, 2006 Michell Clark, Designee Assistant Secretary for Management and Acting

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL 400 MARYLAND AVENUE, S.W. WASHINGTON, DC 20202-1500 February 1, 2006 Michell Clark, Designee Assistant Secretary for Management and Acting

Forensic Audit Building a World Class Program

Forensic Audit Building a World Class Program PAUL E. ZIKMUND DIRECTOR GLOBAL INTEGRITY AND FORENSIC AUDIT 1 2012 ACFE ANNUAL FRAUD CONFERENCE ORLANDO, FL Why the Need for Forensic Audit Program In response

Forensic Audit Building a World Class Program PAUL E. ZIKMUND DIRECTOR GLOBAL INTEGRITY AND FORENSIC AUDIT 1 2012 ACFE ANNUAL FRAUD CONFERENCE ORLANDO, FL Why the Need for Forensic Audit Program In response

INFORMATION TECHNOLOGY: Reservation System Infrastructure Updated, but Future System Sustainability Remains an Issue

INFORMATION TECHNOLOGY: Reservation System Infrastructure Updated, but Future System Audit Report OIG-A-2015-010 May 19, 2015 This page intentionally left blank. NATIONAL RAILROAD PASSENGER CORPORATION

INFORMATION TECHNOLOGY: Reservation System Infrastructure Updated, but Future System Audit Report OIG-A-2015-010 May 19, 2015 This page intentionally left blank. NATIONAL RAILROAD PASSENGER CORPORATION

NATIONAL OCEANIC AND ATMOSPHERIC ADMINISTRATION. Opportunities to Strengthen Internal Controls Over Improper Payments PUBLIC RELEASE

U.S. DEPARTMENT OF COMMERCE Office of Inspector General NATIONAL OCEANIC AND ATMOSPHERIC ADMINISTRATION Opportunities to Strengthen Internal Controls Over Improper Payments Final Report No.BSD-16186-0001/July

U.S. DEPARTMENT OF COMMERCE Office of Inspector General NATIONAL OCEANIC AND ATMOSPHERIC ADMINISTRATION Opportunities to Strengthen Internal Controls Over Improper Payments Final Report No.BSD-16186-0001/July

SYSTEMS AND CONTROLS. Management Assurances FEDERAL MANAGERS FINANCIAL INTEGRITY ACT (FMFIA) ASSURANCE STATEMENT FISCAL YEAR (FY) 2012

ASSURANCE STATEMENT FISCAL YEAR (FY) 2012") SYSTEMS AND CONTROLS Management Assurances FEDERAL MANAGERS FINANCIAL INTEGRITY ACT (FMFIA) ASSURANCE STATEMENT FISCAL YEAR (FY) 2012 Management is responsible for establishing and maintaining effective

SYSTEMS AND CONTROLS Management Assurances FEDERAL MANAGERS FINANCIAL INTEGRITY ACT (FMFIA) ASSURANCE STATEMENT FISCAL YEAR (FY) 2012 Management is responsible for establishing and maintaining effective

Strategies for Achieving Successful Audit Outcomes. Presented by: Noah Leiden, CPA Partner Patrick J. Fitzgerald, CPA Director

Strategies for Achieving Successful Audit Outcomes Presented by: Noah Leiden, CPA Partner Patrick J. Fitzgerald, CPA Director Agenda What is Success? Understanding and Impacting the Audit Process Strategies

Strategies for Achieving Successful Audit Outcomes Presented by: Noah Leiden, CPA Partner Patrick J. Fitzgerald, CPA Director Agenda What is Success? Understanding and Impacting the Audit Process Strategies

IBM QRadar Security Intelligence April 2013

IBM QRadar Security Intelligence April 2013 1 2012 IBM Corporation Today s Challenges 2 Organizations Need an Intelligent View into Their Security Posture 3 What is Security Intelligence? Security Intelligence

IBM QRadar Security Intelligence April 2013 1 2012 IBM Corporation Today s Challenges 2 Organizations Need an Intelligent View into Their Security Posture 3 What is Security Intelligence? Security Intelligence

DCAA New Tactics in Obtaining Contractor Internal audit reports

DCAA New Tactics in Obtaining Contractor Internal audit reports By Todd Bishop and David Eck, CPA In August 2012, the Defense Contract Audit Agency (DCAA) issued updates to its policy guidance and the

DCAA New Tactics in Obtaining Contractor Internal audit reports By Todd Bishop and David Eck, CPA In August 2012, the Defense Contract Audit Agency (DCAA) issued updates to its policy guidance and the

Unauthorized Use of the GPC Page 1 of 29 Welcome to Unauthorized Use of the GPC

Unauthorized Use of the GPC Page 1 of 29 Welcome to Unauthorized Use of the GPC In this topic you will be introduced to the many possible misuses of the Government Purchase Card (GPC), including the definition

Unauthorized Use of the GPC Page 1 of 29 Welcome to Unauthorized Use of the GPC In this topic you will be introduced to the many possible misuses of the Government Purchase Card (GPC), including the definition

Hexaware E-book on Predictive Analytics

Hexaware E-book on Predictive Analytics Business Intelligence & Analytics Actionable Intelligence Enabled Published on : Feb 7, 2012 Hexaware E-book on Predictive Analytics What is Data mining? Data mining,

Hexaware E-book on Predictive Analytics Business Intelligence & Analytics Actionable Intelligence Enabled Published on : Feb 7, 2012 Hexaware E-book on Predictive Analytics What is Data mining? Data mining,

ISOLATE AND ELIMINATE FRAUD THROUGH ADVANCED ANALYTICS. BENJAMIN CHIANG, CFE, CISA, CA Partner, Ernst and Young Advisory Singapore

With ever-increasing data volumes, more sophisticated fraud patterns, and a drive for strong corporate governance, how can organisations build a culture of integrity and compliance? Learn how data analytics

With ever-increasing data volumes, more sophisticated fraud patterns, and a drive for strong corporate governance, how can organisations build a culture of integrity and compliance? Learn how data analytics

Using Forensic Accounting to Detect Fraud in Public Service Organizations. Kevin M. Bronner, Ph.D. 1

Using Forensic Accounting to Detect Fraud in Public Service Organizations By Kevin M. Bronner, Ph.D. 1 Forensic accounting is a useful technique to detect fraud in public service organizations. This paper

Using Forensic Accounting to Detect Fraud in Public Service Organizations By Kevin M. Bronner, Ph.D. 1 Forensic accounting is a useful technique to detect fraud in public service organizations. This paper

Audit Report OFFICE OF INSPECTOR GENERAL. Farm Credit Administration s Purchase Card Program A-14-02. Auditor-in-Charge Sonya Cerne.

OFFICE OF INSPECTOR GENERAL Audit Report Farm Credit Administration s Purchase Card Program A-14-02 Auditor-in-Charge Sonya Cerne Issued September 5, 2014 FARM CREDIT ADMINISTRATION Farm Credit Administration

OFFICE OF INSPECTOR GENERAL Audit Report Farm Credit Administration s Purchase Card Program A-14-02 Auditor-in-Charge Sonya Cerne Issued September 5, 2014 FARM CREDIT ADMINISTRATION Farm Credit Administration

Data Mining: Unlocking the Intelligence in Your Data. Marlon B. Williams, CPA, ACDA Partner, IT Advisory Services Weaver

Data Mining: Unlocking the Intelligence in Your Data Marlon B. Williams, CPA, ACDA Partner, IT Advisory Services Weaver 0 Today s Agenda Big Data What is it? Data Mining at a Glance Why the Accounting

Data Mining: Unlocking the Intelligence in Your Data Marlon B. Williams, CPA, ACDA Partner, IT Advisory Services Weaver 0 Today s Agenda Big Data What is it? Data Mining at a Glance Why the Accounting

Standards of. Conduct. Important Phone Number for Reporting Violations

Standards of Conduct It is the policy of Security Health Plan that all its business be conducted honestly, ethically, and with integrity. Security Health Plan s relationships with members, hospitals, clinics,

Standards of Conduct It is the policy of Security Health Plan that all its business be conducted honestly, ethically, and with integrity. Security Health Plan s relationships with members, hospitals, clinics,

U S I N G D A T A A N A L Y S I S T O M E E T T H E R E Q U I R E M E N T S O F R I S K B A S E D A U D I T I N G S T A N D A R D S

U S I N G D A T A A N A L Y S I S T O M E E T T H E R E Q U I R E M E N T S O F R I S K B A S E D A U D I T I N G S T A N D A R D S A C a s e W a r e I D E A R e s e a r c h R e p o r t CaseWare IDEA Inc.

U S I N G D A T A A N A L Y S I S T O M E E T T H E R E Q U I R E M E N T S O F R I S K B A S E D A U D I T I N G S T A N D A R D S A C a s e W a r e I D E A R e s e a r c h R e p o r t CaseWare IDEA Inc.

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA PERFORMANCE AUDIT OFFICE OF INFORMATION TECHNOLOGY SERVICES STATE TERM CONTRACT FOR MICROCOMPUTERS AND PERIPHERALS JULY 2013 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE

STATE OF NORTH CAROLINA PERFORMANCE AUDIT OFFICE OF INFORMATION TECHNOLOGY SERVICES STATE TERM CONTRACT FOR MICROCOMPUTERS AND PERIPHERALS JULY 2013 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE

Sharon Kurek, CPA, CFE Director of Internal Audit

Sharon Kurek, CPA, CFE Director of Internal Audit What You Will Take Aware With You Definition of Internal Auditing Scope of Audit Activities Risk and Control Process Common Audit Topics Fraud Awareness

Sharon Kurek, CPA, CFE Director of Internal Audit What You Will Take Aware With You Definition of Internal Auditing Scope of Audit Activities Risk and Control Process Common Audit Topics Fraud Awareness

Acquisition. Controls for the DoD Aviation Into-Plane Reimbursement Card (D-2003-003) October 3, 2002

October 3, 2002") October 3, 2002 Acquisition Controls for the DoD Aviation Into-Plane Reimbursement Card (D-2003-003) Department of Defense Office of the Inspector General Quality Integrity Accountability Report Documentation

October 3, 2002 Acquisition Controls for the DoD Aviation Into-Plane Reimbursement Card (D-2003-003) Department of Defense Office of the Inspector General Quality Integrity Accountability Report Documentation

MICHIGAN AUDIT REPORT OFFICE OF THE AUDITOR GENERAL. Doug A. Ringler, C.P.A., C.I.A. AUDITOR GENERAL ENTERPRISE DATA WAREHOUSE

MICHIGAN OFFICE OF THE AUDITOR GENERAL AUDIT REPORT PERFORMANCE AUDIT OF THE ENTERPRISE DATA WAREHOUSE DEPARTMENT OF TECHNOLOGY, MANAGEMENT, AND BUDGET August 2014 Doug A. Ringler, C.P.A., C.I.A. AUDITOR

MICHIGAN OFFICE OF THE AUDITOR GENERAL AUDIT REPORT PERFORMANCE AUDIT OF THE ENTERPRISE DATA WAREHOUSE DEPARTMENT OF TECHNOLOGY, MANAGEMENT, AND BUDGET August 2014 Doug A. Ringler, C.P.A., C.I.A. AUDITOR

Security strategies to stay off the Børsen front page

Security strategies to stay off the Børsen front page Steve Durkin, Channel Director for Europe, Q1 Labs, an IBM Company 1 2012 IBM Corporation Given the dynamic nature of the challenge, measuring the

Security strategies to stay off the Børsen front page Steve Durkin, Channel Director for Europe, Q1 Labs, an IBM Company 1 2012 IBM Corporation Given the dynamic nature of the challenge, measuring the

Citibank Presents: Techniques for Establishing a Successful Audit Process

GSA SmartPay Conference Citibank Presents: Techniques for Establishing a Successful Audit Process David Ruda, Noak Smith (VA) Vice President, Public Sector Market Manager, Commercial Cards Citibank Presents:

GSA SmartPay Conference Citibank Presents: Techniques for Establishing a Successful Audit Process David Ruda, Noak Smith (VA) Vice President, Public Sector Market Manager, Commercial Cards Citibank Presents:

Data Analytics: Applying Data Analytics to a Continuous Controls Auditing / Monitoring Solution

Data Analytics: Applying Data Analytics to a Continuous Controls Auditing / Monitoring Solution December 10, 2014 Parm Lalli, CISA, ACDA Sunera Snapshot Professional consultancy with core competency in:

Data Analytics: Applying Data Analytics to a Continuous Controls Auditing / Monitoring Solution December 10, 2014 Parm Lalli, CISA, ACDA Sunera Snapshot Professional consultancy with core competency in:

AUDIT TIPS FOR MANAGING DISASTER-RELATED PROJECT COSTS

AUDIT TIPS FOR MANAGING DISASTER-RELATED PROJECT COSTS Department of Homeland Security Office of Inspector General September 2012 I. Introduction The Department of Homeland Security (DHS), Office of Inspector

AUDIT TIPS FOR MANAGING DISASTER-RELATED PROJECT COSTS Department of Homeland Security Office of Inspector General September 2012 I. Introduction The Department of Homeland Security (DHS), Office of Inspector

Status of Enterprise Resource Planning Systems Cost, Schedule, and Management Actions Taken to Address Prior Recommendations

Report No. DODIG-2013-111 I nspec tor Ge ne ral Department of Defense AUGUST 1, 2013 Status of Enterprise Resource Planning Systems Cost, Schedule, and Management Actions Taken to Address Prior s I N T

Report No. DODIG-2013-111 I nspec tor Ge ne ral Department of Defense AUGUST 1, 2013 Status of Enterprise Resource Planning Systems Cost, Schedule, and Management Actions Taken to Address Prior s I N T

Enterprise Forensics and ediscovery (EnCase) Privacy Impact Assessment

Privacy Impact Assessment") Enterprise Forensics and ediscovery (EnCase) Privacy Impact Assessment PIA Approval Date Mar. 14, 2011 System Overview The Enterprise Forensics and ediscovery (EnCase) solution is a major application that

Enterprise Forensics and ediscovery (EnCase) Privacy Impact Assessment PIA Approval Date Mar. 14, 2011 System Overview The Enterprise Forensics and ediscovery (EnCase) solution is a major application that

Audit of the Administrative and Loan Accounting Center, Austin, Texas

Department of Veterans Affairs Office of Inspector General Audit of the Administrative and Loan Accounting Center, Austin, Texas The Administrative and Loan Accounting Center needed to strengthen certain

Department of Veterans Affairs Office of Inspector General Audit of the Administrative and Loan Accounting Center, Austin, Texas The Administrative and Loan Accounting Center needed to strengthen certain