Standards for Determining Monthly Debt and Income Appendix Q

|

|

|

- Geraldine Booth

- 8 years ago

- Views:

Transcription

1 Standards for Determining Monthly Debt and Income Appendix Q October Genworth Financial, Inc. All rights reserved. Agenda What we will cover General Income Requirements Documentation Requirements Genworth Website Helpful tools 1 1

2 The Rule CFPB s Ability-to-Repay (ATR) Rule Final CFPB rule, effective January 10, 2014, requires mortgage lenders to consider consumers ability to repay loans before extending credit Excludes open-end credit, timeshare plans, reverse mortgages and certain temporary loans 2 Ability-to-Repay (ATR) Rule Key concepts of the new rule: The creditor must make a reasonable and good faith determination that the consumer has the ability to repay the loan. Mortgage borrowers must provide ample financial documentation; lenders must verify the documents. In order to be approved for a particular home loan, the borrower must have sufficient income and assets to repay the loan. 3 2

3 Ability-to-Repay (ATR) Rule At minimum, creditors must consider: 1. Current or reasonably expected income or assets 2. Current employment status 3. Monthly payment on the covered transaction 4. Monthly payment on any simultaneous loan 5. Monthly payment for mortgage-related obligations 6. Current debt obligations, alimony, and child support 7. Monthly debt-to-income ratio or residual income 8. Credit history Creditors must verify the information using reliable third party records Appendix Q contains the standards for determining monthly debt and income. 4 Qualified Mortgages (QM) Appendix Q Provides guidance for determining Monthly Debt and Income 5 3

4 Amendments to Appendix Q 6 Qualified Mortgages (QM) Generally, a QM loan has: (i) substantially equal monthly payments, (ii) a loan term <= 30 years, (iii) points and fees that do not exceed 3%, (iv) been underwritten using the maximum interest rate that may apply during the first 5 years (and with amortizing monthly payments), 7 4

5 Qualified Mortgages (QM) (v) the creditor considers and verifies the borrower s income, assets and debts in accordance with Appendix Q, and (vi) a DTI that does not exceed 43%. However, for loans that are eligible for purchase by Fannie or Freddie, FHA, VA, USDA, Rural Housing Service, a mortgage is a QM loan if it meets conditions (i)-(iii) above. Note the loan only needs to be eligible for purchase; actual sale to Fannie/Freddie isn t required. 8 Income Requirements Appendix Q gives guidance on determining the Stability and Eligibility of a consumers income. This guidance may differ from your current investors such as: Fannie Mae, Freddie Mac, FHA, VA Please also be aware that your internal guidelines may also currently differ. Effective income is: Verifiable Steady, Stable or increasing Likely to continue into the future Only Effective Income May Be Used In Qualifying 9 5

6 Verifying Employment History Two year history is required on the 1003 for all applicants All Gaps Of Employment Must Be Addressed By The Applicant And Reviewed By The Creditor 10 Verifying Employment History Consumers must: Explain any gaps in employment that span one or more months, and Indicate if he/she was in school or the military for the recent two full years, providing evidence supporting this claim, such as college transcripts, or discharge papers. Allowances Can Be Made For Seasonal Employment If Documented By The Creditor 11 6

13")

7 Verifying Employment History Examine probability of continued employment: The consumer s past employment record Qualifications for the position Previous training and education; and The employer s confirmation of continued employment Income Stability Takes Precedence Over Job Stability 12 Verification of Employment (VOE) 13 7

8 Verifying Employment History If consumer is returning to work after an extended absence, income can be considered if: Applicant is employed in the current job for six months or longer; and A two year work history prior to an absence from employment has been documented using: Traditional employment verifications; and/or Copies of IRS Form W-2s or pay stubs. Extended Absence Is Defined As Six Months 14 Verifying Employment/Income History Salary and Wage Earnings: The income of each consumer who will be obligated for the mortgage debt must be analyzed to determine whether his/her income level can be reasonably expected to continue through at least the first three years of the mortgage loan Effective income for consumers planning to retire during the first three-year period must include the amount of: a. Documented retirement benefits; b. Social Security payments; or c. Other payments expected to be received in retirement. Creditors Must Not Ask The Consumer About Possible, Future Maternity Leave 15 8

9 Verifying Employment/Income History Overtime and Bonus Income can be considered: If the consumer has received this income for the past two years, and it will likely continue The creditor must develop an average of bonus or overtime income for the past two years. If either type of income shows a continual decline, the creditor must document in writing a sound rationalization for including the income when qualifying the consumer A Period Of More Than Two Years Must Be Used In Calculating The Average Overtime And Bonus Income If The Income Varies Significantly From Year To Year 16 Verifying Employment/Income History Part Time and Seasonal Income: Part-time and seasonal income can be considered in qualifying the consumer if the creditor documents that the consumer has worked the part-time job uninterrupted for the past two years, and plans to continue Seasonal income is considered uninterrupted, and may be used to qualify the consumer, if the creditor documents that the consumer: Has worked the same job for the past two years, and Expects to be rehired the next season. Part-time Income Refers To Employment Taken To Supplement The Consumer s Income From Regular Employment; Par-time Employment Is Not A Primary Job And It Is Worked Less Than 40 Hours 17 9

10 Verifying Income History Income: Commission Commission income must be averaged over the previous two years Must be stable and likely to continue To qualify commission income, the consumer must provide: Copies of signed tax returns for the last two years; and The most recent pay stub Unreimbursed Business Expenses Must Be Subtracted From Gross Income 18 Verifying Income History Income: Other Retirement income must be verified from the former employer, or from Federal tax returns If any retirement income, such as employer pensions or 401(k) s, will cease within the first full three years of the mortgage loan, such income may not be used in qualifying Social Security income must be verified by the Social Security Administration If any benefits expire within the first full three years of the loan, the income source may not be used in qualifying The creditor must obtain a complete copy of the current awards letter. Not all Social Security income is for retirement-aged recipients; therefore, documented continuation is required. Some portion of Social Security income may be grossed up if deemed nontaxable by the IRS

11 Does your borrower own 25% or more of a business? 20 Verifying Employment/Income History Self Employed: Income from self-employment is considered stable, and effective, if the consumer has been self-employed for two or more years Review for declining income trends Self-employed consumers must provide the following documentation: Signed, dated individual tax returns, with all applicable tax schedules for the most recent two years; For a corporation, S corporation, or partnership, signed copies of Federal business income tax returns for the last two years, with all applicable tax schedules; Year to date profit and loss (P&L) statement and balance sheet; and Consumers With 25% Or Greater Ownership Interest In A Business Are Considered Self-Employed 21 11

12 Verifying Employment/Income History Self Employed Continued: Establishing a Consumer s Earnings Trends Establish the consumer s earnings trend from the previous two years using the consumer s tax returns. Documentation from the Consumer Quarterly tax returns, the income analysis may include income through the period covered by the tax filings, or P&L statement may be included in the analysis, provided the income stream based on the P&L is consistent with the previous years earnings. If the P&L statements show an income stream considerably greater income, the creditor must base the income analysis solely on the income verified through the tax returns. If the earnings trend is downward and the most recent tax return or P&L is less than the prior year s tax return, the consumer s most recent year s tax return or P&L must be used to calculate his/her income. The creditor may need to determine the likelihood of the income continuing on a downward trend. 22 Verifying Employment/Income History Self Employed Continued: Analyzing the Business Financial Strength Review the Source of the business income; Annual earnings that are stable or increasing are acceptable, while businesses that show a significant decline in income over the analysis period are not acceptable

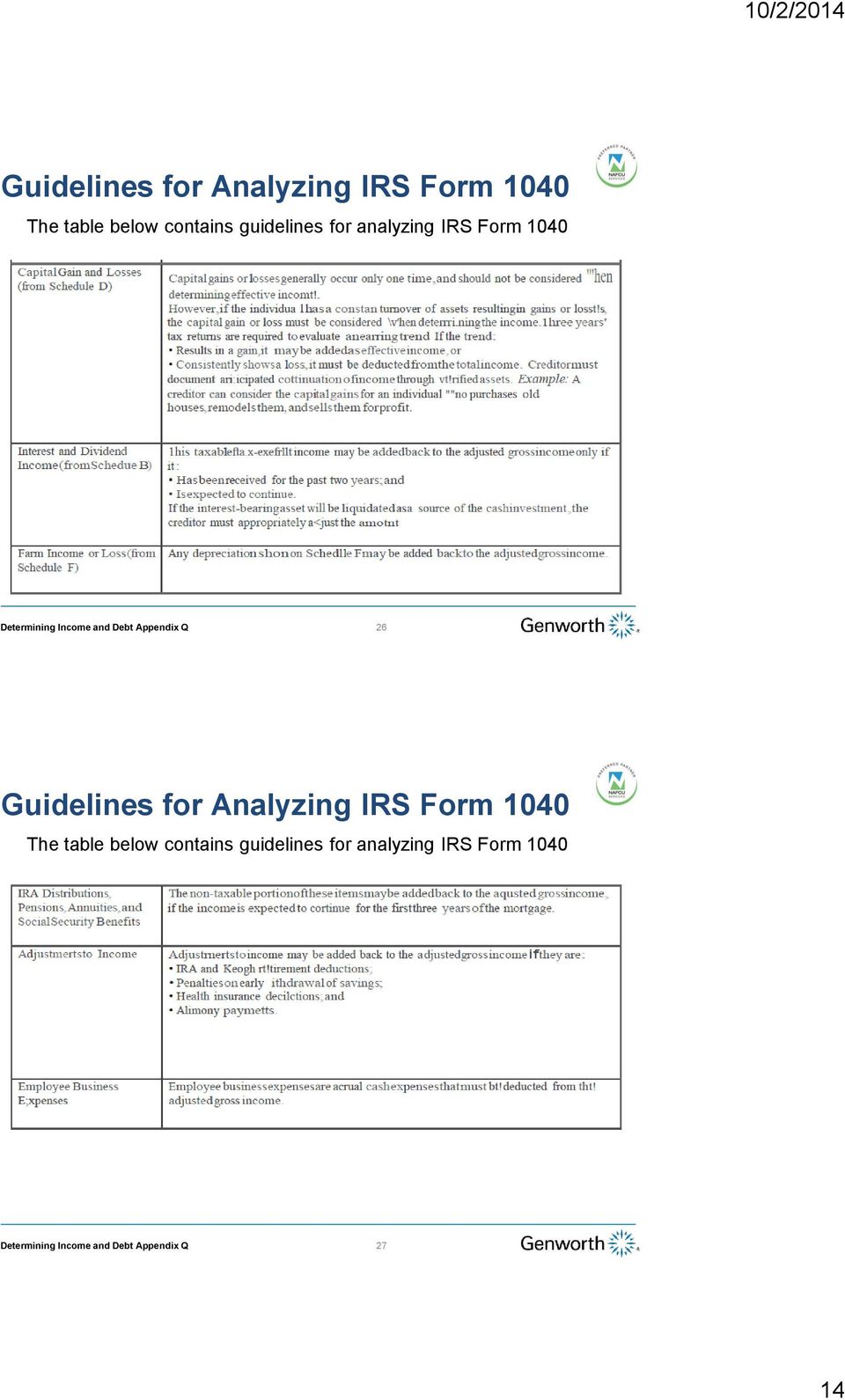

13 Verifying Income History Income Analysis: Individual Tax Returns (IRS Form 1040): Analyzing the Individual 1040 General Policy on Adjusting Income Based on a Review of IRS Form The amount shown on a consumer s IRS Form 1040 as adjusted gross income must either be increased or decreased based on the creditor s analysis of the individual tax return and any related tax schedules. 24 Guidelines for Analyzing IRS Form 1040 The table below contains guidelines for analyzing IRS Form

14 Guidelines for Analyzing IRS Form 1040 The table below contains guidelines for analyzing IRS Form Guidelines for Analyzing IRS Form 1040 The table below contains guidelines for analyzing IRS Form

15 Verifying Income History Self Employed Continued: Corporate Tax Returns (IRS Form 1120) Obtain Consumer Percentage of Ownership Information Analyzing Corporate Tax Returns: To determine a consumer s self-employed income from a corporation the adjusted business income must: Be determined; and Multiplied by the consumer s percentage of ownership in the business The table on the next slide describes the items found on IRS Form 1120 for which an adjustment must be made in order to determine adjusted business income A Corporation Is A State-Chartered Business Owned By Its Stockholders 28 IRS Form 1120 Adjustment Chart 29 15

16 Verifying Employment/Income History Self Employed Continued: S Corp Tax Returns (IRS Form 1120S) An S corporation is generally a small, start-up business, with gains and losses passed to stockholders in proportion to each stockholder s percentage of business ownership Income for owners of S corporations comes from IRS Form W-2 wages, and is taxed at the individual rate. The IRS Form 1120S, Compensation of Officers line item is transferred to the consumer s individual IRS Form 1040 S corporation depreciation and depletion may be added back to income in proportion to the consumer s share of the corporation s income. Income must also be reduced proportionately by the total obligations payable by the corporation in less than one year A Consumer s Withdrawal Of Cash From The Corporation May Have A Severe Negative Impact On The Corporation s Ability To Continue Operating, And Must Be Considered 30 Verifying Employment/Income History Self Employed Continued: Partnership Tax Returns (IRS Form 1065) A partnership is formed when two or more individuals form a business, and share in profits, losses, and responsibility for running the company Each partner pays taxes on his/her proportionate share of the partnership s net income; partnership depreciation and depletion may be added back to income in proportion to the consumer s share of the partnership s income The Consumer s Withdrawal Of Cash From The Corporation May Have A Severe Negative Impact On The Corporation s Ability To Continue Operating, And Must Be Considered 31 16

17 Verifying Employment/Income History Self Employed Continued: Partnership Tax Returns (IRS Form 1065) General and limited partnerships report income on IRS Form 1065, and the partners share of income is carried over to Schedule E of IRS Form Review IRS Form 1065 to assess the viability of the business. Both depreciation and depletion may be added back to the income in proportion to the consumer s share of income. Income must also be reduced proportionately by the total obligations payable by the partnership in less than one year A Consumer s Withdrawal Of Cash From The Corporation May Have A Severe Negative Impact On The Corporation s Ability To Continue Operating, And Must Be Considered 32 IRS Form 4506-t IRS 4506-t or similar forms Allows lenders to obtain transcripts of the tax returns for borrowers for free. Once signed and dated by applicant the form is good for 120 days or 8821 may also be used in lieu of the 4506-t but these forms typically cost to execute. Fannie Mae and Freddie Mac both have policies in place regarding the use of the form during processing

18 Verifying Employment/Income Business: Employed by Family Owned Income Documentation Requirement. In addition to normal employment verification, a consumer employed by a family owned business is required to provide evidence that he/she is not an owner of the business, which may include: Copies of signed personal tax returns, or A signed copy of the corporate tax return showing ownership percentage 34 Verifying Non-Employment Income INCOME: NON-EMPLOYMENT RELATED CONSUMER Alimony,, Alimony Child Support, and Maintenance Income Criteria. child support, or maintenance income may be considered effective, if: Payments are likely to be received consistently for the first three years of the mortgage The consumer provides the required documentation, which includes a copy of the: Final divorce decree; Legal separation agreement; A Court order; or Voluntary payment agreement; and A The consumer can provide acceptable evidence that payments have been received during the last 12 months, such as: Cancelled checks; Deposit slips; Tax returns; or Court records Child Support May Be Grossed Up Under The Same Provisions As Non-taxable Income Sources 35 18

19 Verifying Non-Employment Income NON-EMPLOYMENT RELATED CONSUMER INCOME: Investment and Trust Income Interest and dividend income may be used as long as tax returns or account statements support a two-year receipt history This income must be averaged over the two years. A Subtract any funds that are derived from these sources, and are required for the cash investment before calculating projected income Income from trusts may be used if guaranteed, constant payments will continue for at least the first three years of the mortgage term Required trust income documentation includes a copy of the Trust Agreement or other trustee statement, confirming the: Amount of the trust; Frequency of distribution; and Duration of payments. Trust account funds may be used for the required cash investment if the consumer provides adequate documentation that the withdrawal of funds will not negatively affect income. 36 Verifying Non-Employment Income NON-EMPLOYMENT RELATED CONSUMER INCOME: Eligible Investment Properties (Subject of your transaction) Follow the steps in the table below to calculate an investment property s income or loss if the property to be subject to a mortgage is an eligible investment property

20 Verifying Non-Employment Income NON-EMPLOYMENT RELATED CONSUMER INCOME: Rental Income (Other owned properties) Rent received for properties owned by the consumer is acceptable as long as the creditor can document the stability of the rental income through: A current lease; An agreement to lease, or A rental history over the previous 24 months that is free of unexplained gaps greater than three months (such gaps could be explained by student, seasonal, or military renters, or property rehabilitation). The underwriting analysis may not consider rental income from any property being vacated by the consumer, except under the circumstances described on the next slides. Rental Income From Any Property Being Vacated By The Consumer May Not Typically Be Considered 38 Verifying Non-Employment Income When a consumer vacates a principal residence in favor of another principal residence, the rental income, reduced by the appropriate vacancy factor, may be considered in the underwriting analysis under the circumstances listed in the table below. Exception Regarding The Exclusion Of Rental Income From A Principal Residence Being Vacated By A Consumer 39 20

21 Verifying Non-Employment Income When a consumer vacates a principal residence in favor of another principal residence, the rental income, reduced by the appropriate vacancy factor, may be considered in the underwriting analysis under the circumstances listed in the table below. Exception Regarding The Exclusion Of Rental Income From A Principal Residence Being Vacated By A Consumer 40 Verifying Non-Employment Income NON-EMPLOYMENT RELATED CONSUMER INCOME: Rental Income from Consumer Occupied Properties (Multi-family) The rent for multiple unit property where the consumer resides in one or more units and charges rent to tenants of other units may be used for qualifying purposes Projected rent for the tenant-occupied units only may: Be considered gross income, only after deducting vacancy and maintenance factors, and Not be used as a direct offset to the mortgage payment. Reduce The Gross Rental Amount By 25 Percent For Vacancies And Maintenance 41 21

22 Verifying Non-Employment Income Verifying Rental Income: IRS Form 1040 Schedule E and Current leases/rental agreements are required to verify all consumer rental income Analyzing IRS Form 1040 Schedule E: The IRS Form 1040 Schedule E is required to verify all rental income. Depreciation shown on Schedule E may be added back to the net income or loss. Income Positive rental income is considered gross income for qualifying purposes, while negative income must be treated as a recurring liability. The Creditor Must Confirm That The Consumer Still Owns Each Property Listed, By Comparing Schedule E With The REO Section Of The URLA 42 Verifying Non-Employment Income Verifying Rental Income: IRS Form 1040 Schedule E and Current leases/rental agreements are required to verify all consumer rental income. Using Current Leases To Analyze Rental Income Review the current signed lease or other rental agreement for a property that was acquired since the last income tax filing, and is not shown on Schedule E. Reduce the gross rental amount by 25 percent for vacancies and maintenance; Subtract PITI and any homeowners association dues; and apply the net if positive, or recurring debts, if negative 43 22

23 Verifying Non-Employment Income INCOME: NON-EMPLOYMENT RELATED CONSUMER Other See Appendix Q for guidance on other types of income such as: Military Income VA Benefits MCC s Notes Receivable Government Assistance Programs Homeownership Subsidies Income from Roommates Conversion of current Primary Residence Non Taxable and Projected Income 44 Consumer Liabilities: Recurring Obligations : Obligation Types of Recurring Recurring obligations include: loans;. a All installment accounts;. b Revolving charge loans;. c Real estate Alimony;. d. e Child support; and. f Other continuing obligations 45 23

24 Consumer Liabilities: Recurring Obligations Debt to Income Ratio Computation for Recurring Obligations The creditor must include the following when computing the debt to income ratios for recurring obligations: Monthly housing expense; and Additional recurring charges extending ten months or more, such as a. Payments on installment accounts; b. Child support or separate maintenance payments; c. Revolving accounts; (if no payment is listed on the credit report and a balance is listed use the greater of 5% or $10. A payment from a current statement may also be used) and d. Alimony (creditor may choose to treat as a reduction of income) e. Contingent liabilities (unless exempt) Debts Lasting Less Than Ten Months Must Be Included If The Amount Of The Debt Affects The Consumer s Ability To Pay 46 Additional Resources GENWORTH RESOURCES ActionCenter : Your Local Genworth Underwriting Manager Your Genworth Account Executive or Manager 47 24

25 Disclaimer Genworth Mortgage Insurance is happy to provide you with these training materials. While we strive for accuracy, we also know that any discussion of laws and their application to particular facts is subject to individual interpretation, change, and other uncertainties. Our training is not intended as legal advice, and is not a substitute for advice of counsel. Your legal counsel should be consulted regarding the requirements and applicability of Dodd-Frank and the CFPB Rules. GENWORTH EXPRESSLY DISCLAIMS ANY AND ALL WARRANTIES, EXPRESS OR IMPLIED, INCLUDING WITHOUT LIMITATION WARRANTIES OF MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE, WITH RESPECT TO THESE MATERIALS AND THE RELATED TRAINING. IN NO EVENT SHALL GENWORTH BE LIABLE FOR ANY DIRECT, INDIRECT, INCIDENTAL, PUNITIVE, OR CONSEQUENTIAL DAMAGES OF ANY KIND WHATSOEVER WITH RESPECT TO THE TRAINING AND THE MATERIALS. 48 Thank you! Genworth Financial is the NAFCU Services Preferred Partner for Private Mortgage Insurance. More educational resources are available at Talk to you next year! That MI Guy!

CASH FLOW ANALYSIS (FORM 1084)

") CASH FLOW ANALYSIS (FORM 1084) Form 1040 Individual Income Tax Return Line 1 - Total Income: Begin with Total Income, which represents the borrower's gross income before adjustments. Line 2 Wages, Salaries,

CASH FLOW ANALYSIS (FORM 1084) Form 1040 Individual Income Tax Return Line 1 - Total Income: Begin with Total Income, which represents the borrower's gross income before adjustments. Line 2 Wages, Salaries,

FNMA Self-Employed Income Calculations

FNMA Self-Employed Income Calculations FNMA considers any individual that has a 25% or more ownership interest in a business to be self-employed. BUSINESS STRUCTURES Knowledge of the structure of the business

FNMA Self-Employed Income Calculations FNMA considers any individual that has a 25% or more ownership interest in a business to be self-employed. BUSINESS STRUCTURES Knowledge of the structure of the business

U.S. Department of Housing and Urban Development Office of Public and Indian Housing

U.S. Department of Housing and Urban Development Office of Public and Indian Housing Special Attention of: Notice PIH-2014-22 All Section 184 Approved Mortgagees, Effective: September 16, 2014 Indian Housing

U.S. Department of Housing and Urban Development Office of Public and Indian Housing Special Attention of: Notice PIH-2014-22 All Section 184 Approved Mortgagees, Effective: September 16, 2014 Indian Housing

The FHLBI may, in its discretion, allow applicants to follow the income guidelines of other funding sources where differences exist.

Attachment D Income Guidelines For all FHLBI Affordable Housing Program (AHP) projects (including competitive AHP and the Homeownership Set-aside Programs) sponsors and members are required to use the

Attachment D Income Guidelines For all FHLBI Affordable Housing Program (AHP) projects (including competitive AHP and the Homeownership Set-aside Programs) sponsors and members are required to use the

Income. 3.4-A General. Section 3.4: Income

Income 3.4-A General Employment and income are essential ingredients to successful home ownership. Qualifying income should be stable, predictable, and likely to continue. The Underwriter must determine

Income 3.4-A General Employment and income are essential ingredients to successful home ownership. Qualifying income should be stable, predictable, and likely to continue. The Underwriter must determine

PURCHASE AND RATE TERM REFINANCE 1. Occupancy Units FICO LTV/CLTV Loan Amount

EXPRESS JUMBO FIXED RATE AND ARM PROGRAM MATRIX: PURCHASE AND RATE TERM REFINANCE 1 Occupancy Units FICO LTV/CLTV Loan Amount 80/80 $1,500,000 Primary Residence 1 720 75/75 $1,750,000 70/70 $2,000,000

EXPRESS JUMBO FIXED RATE AND ARM PROGRAM MATRIX: PURCHASE AND RATE TERM REFINANCE 1 Occupancy Units FICO LTV/CLTV Loan Amount 80/80 $1,500,000 Primary Residence 1 720 75/75 $1,750,000 70/70 $2,000,000

Analyzing Business Tax Returns. Partnership Corporation S-Corporation LLC

Analyzing Business Tax Returns Partnership Corporation S-Corporation LLC 1 Partnership Definition: A partnership is formed when two or more individuals form a business and share in the profits, losses

Analyzing Business Tax Returns Partnership Corporation S-Corporation LLC 1 Partnership Definition: A partnership is formed when two or more individuals form a business and share in the profits, losses

FHA Guideline Changes Effective for Case Numbers Assigned On or After Sept 14, 2015

Topic Current FHA Guideline New FHA Guideline Assets Gift Funds as Reserves Manual Underwriting: Not allowed as reserves Manual underwriting: Not allowed as reserves TOTAL Scorecard: Not allowed as reserves

Topic Current FHA Guideline New FHA Guideline Assets Gift Funds as Reserves Manual Underwriting: Not allowed as reserves Manual underwriting: Not allowed as reserves TOTAL Scorecard: Not allowed as reserves

Loan Prospector Documentation Matrix

Use the following information as a reference for documenting your Loan Prospector loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie Mac Single-

Use the following information as a reference for documenting your Loan Prospector loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie Mac Single-

11.1 INTRODUCTION 11.2 THE RATIOS

0BCHAPTER 11: RATIO ANALYSIS 11.1 INTRODUCTION Ratios are used to determine whether the borrower s repayment income can reasonably be expected to meet the anticipated monthly housing expense and total

0BCHAPTER 11: RATIO ANALYSIS 11.1 INTRODUCTION Ratios are used to determine whether the borrower s repayment income can reasonably be expected to meet the anticipated monthly housing expense and total

Section 1.37a Income Analysis

Section 1.37a Income Analysis In This Section This section contains the following topics. Overview... 2 General... 2 Introduction... 2 Related Bulletins... 3 Qualifying Income... 4 Stability of Income...

Section 1.37a Income Analysis In This Section This section contains the following topics. Overview... 2 General... 2 Introduction... 2 Related Bulletins... 3 Qualifying Income... 4 Stability of Income...

Single Family Housing Guaranteed Loan Program Underwriting and Loan Closing Documentation Matrix

Single Family Housing Guaranteed Loan Program Underwriting and Loan Closing Matrix Origination Matrix (January 2013) Table of Contents Matrix Origination... 1 Underwriting... 1 Credit... 7 Employment/Income...

Single Family Housing Guaranteed Loan Program Underwriting and Loan Closing Matrix Origination Matrix (January 2013) Table of Contents Matrix Origination... 1 Underwriting... 1 Credit... 7 Employment/Income...

The CFPB s Ability-to-Repay Regulation Z Rules: (12 CFR 1026.43)

") The CFPB s Ability-to-Repay Regulation Z Rules: (12 CFR 1026.43) This has been updated to include changes from the CFPB final rule issued on September 13, 2013. In addition, this CompNOTES only covers

The CFPB s Ability-to-Repay Regulation Z Rules: (12 CFR 1026.43) This has been updated to include changes from the CFPB final rule issued on September 13, 2013. In addition, this CompNOTES only covers

CFPB s Final Mortgage Regulations:

CFPB s Final Mortgage Regulations: Ability-to-Repay and Qualified Mortgage Rules November 4, 2013 E. Andrew Keeney, Esq. Kaufman & Canoles, P.C. Ability-to-Repay and Qualified Mortgage Rules E. Andrew

CFPB s Final Mortgage Regulations: Ability-to-Repay and Qualified Mortgage Rules November 4, 2013 E. Andrew Keeney, Esq. Kaufman & Canoles, P.C. Ability-to-Repay and Qualified Mortgage Rules E. Andrew

CALHOME MORTGAGE ASSISTANCE PROGRAM GUIDELINES

PLANNING AND DEVELOPMENT DEPARTMENT HOUSING AND COMMUNITY DEVELOPMENT DIVISION CALHOME MORTGAGE ASSISTANCE PROGRAM GUIDELINES PROGRAM OVERVIEW The CalHome Mortgage Assistance Program is a program funded

PLANNING AND DEVELOPMENT DEPARTMENT HOUSING AND COMMUNITY DEVELOPMENT DIVISION CALHOME MORTGAGE ASSISTANCE PROGRAM GUIDELINES PROGRAM OVERVIEW The CalHome Mortgage Assistance Program is a program funded

Ability to Repay/Qualified Mortgage Rule

Ability to Repay/Qualified Mortgage Rule Note: This document was used in support of a live discussion. As such, it does not necessarily express the entirety of that discussion nor the relative emphasis

Ability to Repay/Qualified Mortgage Rule Note: This document was used in support of a live discussion. As such, it does not necessarily express the entirety of that discussion nor the relative emphasis

Exhibit 101 Income Calculation Guidelines for Alternative to Foreclosure Options

The required documentation to verify income from sources disclosed by the Borrower(s) on Form 710, Uniform Borrower Assistance Form, and the corresponding methods to calculate the income from each source

The required documentation to verify income from sources disclosed by the Borrower(s) on Form 710, Uniform Borrower Assistance Form, and the corresponding methods to calculate the income from each source

The CFPB s Qualified Mortgage Requirements from the ATR/QM Final Rule (12 CFR 1026.43)

") The CFPB s Qualified Mortgage Requirements from the ATR/QM Final Rule (12 CFR 1026.43) This has been updated to include changes from the CFPB final rule issued on September 13, 2013. In addition, this

The CFPB s Qualified Mortgage Requirements from the ATR/QM Final Rule (12 CFR 1026.43) This has been updated to include changes from the CFPB final rule issued on September 13, 2013. In addition, this

Cash Flow Analysis (Form 1084)

") Cash Flow Analysis (Form 1084) Borrower Name: Business Name (optional): This worksheet may be used to prepare a written evaluation of the analysis of income related to self-employment. The purpose of this

Cash Flow Analysis (Form 1084) Borrower Name: Business Name (optional): This worksheet may be used to prepare a written evaluation of the analysis of income related to self-employment. The purpose of this

USDA Rural Development/Special Loan Servicing

Guidance Lender (Loan Holder/Loan Servicer) Borrowers USDA Rural Development/Special Loan Servicing The Lender must be a Section 502 Single Family Housing Guaranteed Loan Program approved Lender. The current

Guidance Lender (Loan Holder/Loan Servicer) Borrowers USDA Rural Development/Special Loan Servicing The Lender must be a Section 502 Single Family Housing Guaranteed Loan Program approved Lender. The current

CFPB issues ability-to-repay and qualified mortgage rules

1 FEBRUARY 4, 2013 CFPB issues ability-to-repay and qualified mortgage rules By Raymond J. Gustini, Lloyd H. Spencer, Tiana M. Butcher, Courtney L. Lindsay II, and Pierce Han No standard is perfect, but

1 FEBRUARY 4, 2013 CFPB issues ability-to-repay and qualified mortgage rules By Raymond J. Gustini, Lloyd H. Spencer, Tiana M. Butcher, Courtney L. Lindsay II, and Pierce Han No standard is perfect, but

Section 1026.43. Ability-to-Repay (ATR) 1026.43(c)(1) and Qualified Mortgage (QM) 1026.43(e), (f)

1026.43(c)(1) and Qualified Mortgage (QM) 1026.43(e), (f)") Section 1026.43 Ability-to-Repay (ATR) 1026.43(c)(1) and Qualified Mortgage (QM) 1026.43(e), (f) Effective January 10, 2014 As of 10/15/2013- By Venessa Snell This section applies to any consumer credit

Section 1026.43 Ability-to-Repay (ATR) 1026.43(c)(1) and Qualified Mortgage (QM) 1026.43(e), (f) Effective January 10, 2014 As of 10/15/2013- By Venessa Snell This section applies to any consumer credit

Federal Home Loan Bank of Boston Affordable Housing and Equity Builder Program Income Calculation Guidelines

Federal Home Loan Bank of Boston Affordable Housing and Equity Builder Program I. Introduction: The Federal Home Loan Bank of Boston (Bank) is using the following guidelines to verify household income

Federal Home Loan Bank of Boston Affordable Housing and Equity Builder Program I. Introduction: The Federal Home Loan Bank of Boston (Bank) is using the following guidelines to verify household income

Advertising, Consumer protection, Mortgages, Reporting and recordkeeping

List of Subjects in 12 CFR Part 1026 Advertising, Consumer protection, Mortgages, Reporting and recordkeeping requirements, Truth in Lending. Authority and Issuance For the reasons set forth in the preamble,

List of Subjects in 12 CFR Part 1026 Advertising, Consumer protection, Mortgages, Reporting and recordkeeping requirements, Truth in Lending. Authority and Issuance For the reasons set forth in the preamble,

El Paso County, Colorado!

El Paso County, Colorado ADMINISTRATOR S GUIDELINES PUBLISHED 7-16 14 Updates are shown on Page 3 El Paso County, Colorado MCC Program Page 2 TABLE OF CONTENTS PROGRAM UPDATES 3 THE ORIGINATION TEAM 4

El Paso County, Colorado ADMINISTRATOR S GUIDELINES PUBLISHED 7-16 14 Updates are shown on Page 3 El Paso County, Colorado MCC Program Page 2 TABLE OF CONTENTS PROGRAM UPDATES 3 THE ORIGINATION TEAM 4

FHA Changes 4000.1 Effective With Case Numbers assigned on or after 9/14/15. Skyline / New Leaf

FHA Changes 4000.1 Effective With Case Numbers assigned on or after 9/14/15 Skyline / New Leaf Manual downgrade regardless of a Total Scorecard Approval When the date of the Borrower s bankruptcy discharge

FHA Changes 4000.1 Effective With Case Numbers assigned on or after 9/14/15 Skyline / New Leaf Manual downgrade regardless of a Total Scorecard Approval When the date of the Borrower s bankruptcy discharge

FHA Underwriting Changes

FHA Underwriting Changes Effective for case numbers issued on and after September 14, 2015 Same Day Turn Times, Everyday Housekeeping All attendees are in listen only mode This seminar is being recorded

FHA Underwriting Changes Effective for case numbers issued on and after September 14, 2015 Same Day Turn Times, Everyday Housekeeping All attendees are in listen only mode This seminar is being recorded

HARP DU REFI PLUS Training

HARP DU REFI PLUS Training Offered by FIRST MORTGAGE CORPORATION JUNE 14, 2013 Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie Mac. This

HARP DU REFI PLUS Training Offered by FIRST MORTGAGE CORPORATION JUNE 14, 2013 Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie Mac. This

VA Product Guidelines

July 16, 2015 VA Product Guidelines Purchase Occupancy Units LTV CLTV Minimum Credit Score Primary 1-4 100 100 620 Rate/Term Refinance Occupancy Units LTV CLTV Minimum Credit Score Primary 1-4 90 90 620

July 16, 2015 VA Product Guidelines Purchase Occupancy Units LTV CLTV Minimum Credit Score Primary 1-4 100 100 620 Rate/Term Refinance Occupancy Units LTV CLTV Minimum Credit Score Primary 1-4 90 90 620

Conventional DU Refi Plus

Endeavor America Loan Services Conventional DU Refi Plus Guidelines Conventional Guidelines... 3 Matrix... 3 Overview... 3 Program Expiration... 3 Loan Purpose... 4 Maximum LTV, CLTV, and HCLTV Ratios

Endeavor America Loan Services Conventional DU Refi Plus Guidelines Conventional Guidelines... 3 Matrix... 3 Overview... 3 Program Expiration... 3 Loan Purpose... 4 Maximum LTV, CLTV, and HCLTV Ratios

The Impact of the CFPB s New Mortgage Rules on the Closing Process

The Impact of the CFPB s New Mortgage Rules on the Closing Process March 11, 2014 Banking & Finance Practice Escrow Account Rule 4 Escrow Account Rule Effective June 1, 2013. Extends current rule from

The Impact of the CFPB s New Mortgage Rules on the Closing Process March 11, 2014 Banking & Finance Practice Escrow Account Rule 4 Escrow Account Rule Effective June 1, 2013. Extends current rule from

Section C. Borrower Credit Analysis Overview

Section C. Borrower Credit Analysis Overview In This Section This section contains the topics listed in the table below. Topic Topic Name See Page 1 General Guidelines for Analyzing Borrower 4-C-2 Credit

Section C. Borrower Credit Analysis Overview In This Section This section contains the topics listed in the table below. Topic Topic Name See Page 1 General Guidelines for Analyzing Borrower 4-C-2 Credit

FHA STREAMLINE REFINANCE PRODUCT PROFILE

Terms 30 Year Terms 15 Year Terms Maximum LTV/CLTV LTV/CLTV Score LTV/CLTV Score Non-Credit Qualifying N/A N/A Credit Qualifying 97.75% 97.75% Applies to Case Numbers assigned on or after January 26, 2015

Terms 30 Year Terms 15 Year Terms Maximum LTV/CLTV LTV/CLTV Score LTV/CLTV Score Non-Credit Qualifying N/A N/A Credit Qualifying 97.75% 97.75% Applies to Case Numbers assigned on or after January 26, 2015

Federal Home Loan Bank of Chicago Community Investment. DPP Income Calculation Guidelines

Federal Home Loan Bank of Chicago Community Investment DPP Income Calculation Guidelines TABLE OF CONTENTS I. Income Eligibility Requirements II. Basis for Income Eligibility A. Determining Household Size

Federal Home Loan Bank of Chicago Community Investment DPP Income Calculation Guidelines TABLE OF CONTENTS I. Income Eligibility Requirements II. Basis for Income Eligibility A. Determining Household Size

Minimum mortgage amount $50,000. Stated Income: $750,000 Metro Toronto, Metro Calgary, Metro Vancouver; $600,000 rest of Canada.

Product Features Insurer Programs: CMHC & Genworth Loan Purpose Property Type Standard, Rental, Business for Self Stated and Income Qualified, New to Canada, Purchase Plus, Second Home, Flex Down. Purchase

Product Features Insurer Programs: CMHC & Genworth Loan Purpose Property Type Standard, Rental, Business for Self Stated and Income Qualified, New to Canada, Purchase Plus, Second Home, Flex Down. Purchase

NEIGHBORHOOD STABILIZATION PROGRAM (NSP) APPLICATION FOR NSP LOAN. Program Guidelines

APPLICATION FOR NSP LOAN. Program Guidelines") APPLICATION FOR NSP LOAN Income limits per household Program Guidelines Maximum Income 1 48,150 2 55,000 3 61,900 4 68,750 5 74,250 6 79,750 7 85,250 8 90,750 Homebuyer Requirements Home Education Minimum

APPLICATION FOR NSP LOAN Income limits per household Program Guidelines Maximum Income 1 48,150 2 55,000 3 61,900 4 68,750 5 74,250 6 79,750 7 85,250 8 90,750 Homebuyer Requirements Home Education Minimum

Document source of funds if amount exceeds 1% of sales price OR appears excessive based on borrower's savings history.

ASSETS Earnest Money Document source of funds if amount exceeds 2% of sales price OR appears excessive based on borrower's savings history. Document source of funds if amount exceeds 1% of sales price

ASSETS Earnest Money Document source of funds if amount exceeds 2% of sales price OR appears excessive based on borrower's savings history. Document source of funds if amount exceeds 1% of sales price

ATR/QM FAQs. Table of Contents. General

Table of Contents General... 1 Ability to Repay (ATR)/Qualified Mortgage (QM)... 2 ATR Eligibility... 2 Qualifying Ratios... 3 Employment/Income... 4 Verifying Employment History (Employment Gaps)... 4

Table of Contents General... 1 Ability to Repay (ATR)/Qualified Mortgage (QM)... 2 ATR Eligibility... 2 Qualifying Ratios... 3 Employment/Income... 4 Verifying Employment History (Employment Gaps)... 4

Early Summary of Ability to Repay and Qualified Mortgage Rules under Dodd-Frank Wall Street Reform and Consumer Protection Act.

Early Summary of Ability to Repay and Qualified Mortgage Rules under Dodd-Frank Wall Street Reform and Consumer Protection Act January 11, 2013 OVERVIEW - On January 10, 2013, the Consumer Financial Protection

Early Summary of Ability to Repay and Qualified Mortgage Rules under Dodd-Frank Wall Street Reform and Consumer Protection Act January 11, 2013 OVERVIEW - On January 10, 2013, the Consumer Financial Protection

FEDERAL HOME LOAN BANK OF DES MOINES COMMUNITY INVESTMENT. Homeownership AHP and Down Payment Products (DP) Income Calculation Guidelines

Income Calculation Guidelines") FEDERAL HOME LOAN BANK OF DES MOINES COMMUNITY INVESTMENT Homeownership AHP and Down Payment Products (DP) Income Calculation Guidelines TABLE OF CONTENTS I. Income Eligibility Requirements (3) II. Basis

FEDERAL HOME LOAN BANK OF DES MOINES COMMUNITY INVESTMENT Homeownership AHP and Down Payment Products (DP) Income Calculation Guidelines TABLE OF CONTENTS I. Income Eligibility Requirements (3) II. Basis

Revolving Debt & Other Agency Guideline Revisions Note: SunTrust specific overlays are underlined.

Assets Section 2.04 DU Refi Plus Loan Program DU Refi Plus STM to STM Transactions Asset Documentation Requirements Assets must be documented in accordance with DU Refi Plus eligible DU Findings report.

Assets Section 2.04 DU Refi Plus Loan Program DU Refi Plus STM to STM Transactions Asset Documentation Requirements Assets must be documented in accordance with DU Refi Plus eligible DU Findings report.

The Chase Guaranteed Rural Housing Refinance Program Features

PROGRAM ELIGIBILITY Borrower Eligibility In order to be eligible for a Rural Development guaranteed loan, the Borrowers adjusted household income cannot exceed the maximum allowable income limit set forth

PROGRAM ELIGIBILITY Borrower Eligibility In order to be eligible for a Rural Development guaranteed loan, the Borrowers adjusted household income cannot exceed the maximum allowable income limit set forth

Income Calculation Guidelines Competitive Affordable Housing Program (Attachment D)

") Income Calculation Guidelines Competitive Affordable Housing Program (Attachment D) This document sets forth the income guidelines for the Competitive Program of the Affordable Housing Program (AHP) of

Income Calculation Guidelines Competitive Affordable Housing Program (Attachment D) This document sets forth the income guidelines for the Competitive Program of the Affordable Housing Program (AHP) of

Exhibit A. Unemployment Mortgage Assistance Program (UMAP)

") History Exhibit A In January 2010, US Treasury (Treasury) created the Housing Finance Agency (HFA) Innovation Fund for the Hardest-Hit Housing Markets (HFA Hardest-Hit Fund) and allocated funds under the

History Exhibit A In January 2010, US Treasury (Treasury) created the Housing Finance Agency (HFA) Innovation Fund for the Hardest-Hit Housing Markets (HFA Hardest-Hit Fund) and allocated funds under the

Contents. VA Credit Overlays

Contents... 1 Introduction... 3 Links... 3 Transaction Types... 3 Purchase Transactions... 3 Refinance Transaction Regular Refinance... 3 Refinance Transaction Interest Rate Reduction Refinance Loan/IRRRL...

Contents... 1 Introduction... 3 Links... 3 Transaction Types... 3 Purchase Transactions... 3 Refinance Transaction Regular Refinance... 3 Refinance Transaction Interest Rate Reduction Refinance Loan/IRRRL...

Fifth Third Home Buying Guide. A Guide to Residential Home Buying.

Fifth Third Home Buying Guide A Guide to Residential Home Buying. Important Contacts and Numbers. Use this page to record important information as you move through the homebuying process. Realtor/Builder

Fifth Third Home Buying Guide A Guide to Residential Home Buying. Important Contacts and Numbers. Use this page to record important information as you move through the homebuying process. Realtor/Builder

QM - Qualified Mortgages. Internal Training Use only July 1, 2014 #T014

QM - Qualified Mortgages Internal Training Use only July 1, 2014 #T014 Rules & Terms to Know QM ATR HPML High Cost Rebuttable Presumption Safe Harbor Excludable Discount Pts History of QM & ATR Rules The

QM - Qualified Mortgages Internal Training Use only July 1, 2014 #T014 Rules & Terms to Know QM ATR HPML High Cost Rebuttable Presumption Safe Harbor Excludable Discount Pts History of QM & ATR Rules The

To see if you qualify for this program, send the items listed below to Northwest Savings Bank.

COMPLETE YOUR CHECKLIST We need this information to help you modify your mortgage payment. To see if you qualify for this program, send the items listed below to Northwest Savings Bank. 1. The enclosed

COMPLETE YOUR CHECKLIST We need this information to help you modify your mortgage payment. To see if you qualify for this program, send the items listed below to Northwest Savings Bank. 1. The enclosed

CFPB Regulations on Ability to Repay and Qualified Mortgages. MDDCCUA Training

CFPB Regulations on Ability to Repay and Qualified Mortgages MDDCCUA Training October 30, 2013 E. Andrew Keeney, Esq. Kaufman & Canoles, P.C. Ability-to-Repay and Qualified Mortgage Rules E. Andrew Keeney,

CFPB Regulations on Ability to Repay and Qualified Mortgages MDDCCUA Training October 30, 2013 E. Andrew Keeney, Esq. Kaufman & Canoles, P.C. Ability-to-Repay and Qualified Mortgage Rules E. Andrew Keeney,

Regulatory Practice Letter July 2013 RPL 13-17

Regulatory Practice Letter July 2013 RPL 13-17 CPFB Finalizes Additional Amendments to Rules Governing Ability-to Repay and Mortgage Servicing Standards Executive Summary The Bureau of Consumer Financial

Regulatory Practice Letter July 2013 RPL 13-17 CPFB Finalizes Additional Amendments to Rules Governing Ability-to Repay and Mortgage Servicing Standards Executive Summary The Bureau of Consumer Financial

Ability to Repay & QM Regulations

Ability to Repay & QM Regulations 2013 Rushmore Loan Management Services LLC. All Rights Reserved. This is intended as educational material only. It does not provide legal advice. Revised December 2013

Ability to Repay & QM Regulations 2013 Rushmore Loan Management Services LLC. All Rights Reserved. This is intended as educational material only. It does not provide legal advice. Revised December 2013

Section 1: Loan Characteristics

Home Flex Quick Reference: Program Summary The following is an outline of the underwriting and closing requirements of New Hampshire Housing Home Flex program, which is available to lenders who have signed

Home Flex Quick Reference: Program Summary The following is an outline of the underwriting and closing requirements of New Hampshire Housing Home Flex program, which is available to lenders who have signed

Bank of America Home Affordable Foreclosure Alternative (HAFA) Matrix

Matrix") Bank of America Home Affordable Foreclosure Alternative (HAFA) Matrix If you do not qualify for the Home Affordable Modification Program (HAMP) or other modification programs that we offer, you will be

Bank of America Home Affordable Foreclosure Alternative (HAFA) Matrix If you do not qualify for the Home Affordable Modification Program (HAMP) or other modification programs that we offer, you will be

This chapter introduces you to the many roles played by the

3 C h a p t e r 3 The Mortgage Lending Process In This Chapter This chapter introduces you to the many roles played by the mortgage professional. It then walks you through the loan process and discusses

3 C h a p t e r 3 The Mortgage Lending Process In This Chapter This chapter introduces you to the many roles played by the mortgage professional. It then walks you through the loan process and discusses

FHA Advantage Underwriting Guide

FHA Advantage Underwriting Guide Page left blank intentionally. WHEDA Introduction 1 Last Revised Date: September 25, 2015 Table of Contents 1.00 Introduction... 6 2.00 Underwriting Philosophy... 7 3.00

FHA Advantage Underwriting Guide Page left blank intentionally. WHEDA Introduction 1 Last Revised Date: September 25, 2015 Table of Contents 1.00 Introduction... 6 2.00 Underwriting Philosophy... 7 3.00

Borrower Response Package Directions Mortgage Assistance Request Form Follows

Borrower Response Package Directions Mortgage Assistance Request Form Follows If you are experiencing a temporary or long-term hardship and need help, you must complete and submit this form along with

Borrower Response Package Directions Mortgage Assistance Request Form Follows If you are experiencing a temporary or long-term hardship and need help, you must complete and submit this form along with

PROCEDURAL MANUAL ALABAMA HOUSING FINANCE AUTHORITY

PROCEDURAL MANUAL ALABAMA HOUSING FINANCE AUTHORITY CONTENTS INTRODUCTION SECTION I DEFINITIONS... 4 SECTION II MORTGAGOR ELIGIBILITY EVALUATION... 6 A. Income Restrictions... 6 B. Occupancy... 6 C. Residence

PROCEDURAL MANUAL ALABAMA HOUSING FINANCE AUTHORITY CONTENTS INTRODUCTION SECTION I DEFINITIONS... 4 SECTION II MORTGAGOR ELIGIBILITY EVALUATION... 6 A. Income Restrictions... 6 B. Occupancy... 6 C. Residence

CFPB FINAL RULES SUN WEST IMPLEMENTATION GUIDE

CFPB FINAL RULES SUN WEST IMPLEMENTATION GUIDE January 02, 2015 In case of any queries regarding the information available in this guide, please reach us at qmteam@swmc.com. Sun West Mortgage Company,

CFPB FINAL RULES SUN WEST IMPLEMENTATION GUIDE January 02, 2015 In case of any queries regarding the information available in this guide, please reach us at qmteam@swmc.com. Sun West Mortgage Company,

VA Product Guidelines

August 10, 2015 VA Product Guidelines Purchase Occupancy Units LTV CLTV Primary 1-4 100 100 620 Rate/Term Refinance Occupancy Units LTV CLTV Primary 1-4 100 100 620 IRRRL Occupancy Units LTV CLTV Primary

August 10, 2015 VA Product Guidelines Purchase Occupancy Units LTV CLTV Primary 1-4 100 100 620 Rate/Term Refinance Occupancy Units LTV CLTV Primary 1-4 100 100 620 IRRRL Occupancy Units LTV CLTV Primary

Chapter 4: Credit Underwriting

Chapter 4: Credit Underwriting Chapter 4 Credit Underwriting Overview In this Chapter This chapter contains the following topics. Topic See Page 4.01 How to Underwrite a VA Guaranteed Loan 4-2 4.02 Income

Chapter 4: Credit Underwriting Chapter 4 Credit Underwriting Overview In this Chapter This chapter contains the following topics. Topic See Page 4.01 How to Underwrite a VA Guaranteed Loan 4-2 4.02 Income

Home Start Homebuyer Tax Credit New Hampshire Housing s Mortgage Credit Certificate (MCC) Program with a New Hampshire Housing Mortgage

Program with a New Hampshire Housing Mortgage") with a New Hampshire Housing Mortgage MCC Reservation #: Applicant: Lender: Lender Email: : _ Co-Applicant: Lender Contact: Lender Phone: Checklist The following items are required for issuance of a Mortgage

with a New Hampshire Housing Mortgage MCC Reservation #: Applicant: Lender: Lender Email: : _ Co-Applicant: Lender Contact: Lender Phone: Checklist The following items are required for issuance of a Mortgage

HECM FINANCIAL ASSESSMENT AND PROPERTY CHARGE GUIDE

Attachment 2 HECM FINANCIAL ASSESSMENT AND PROPERTY CHARGE GUIDE EFFECTIVE FOR HECM CASE NUMBERS ISSUED ON OR AFTER March 2, 2015 November 10, 2014 Page 1 Table of Contents Financial Assessment Overview...

Attachment 2 HECM FINANCIAL ASSESSMENT AND PROPERTY CHARGE GUIDE EFFECTIVE FOR HECM CASE NUMBERS ISSUED ON OR AFTER March 2, 2015 November 10, 2014 Page 1 Table of Contents Financial Assessment Overview...

EFFECTIVE SEP 14, 2015. FHA Rule Changes. www.greenpathfunding.com

EFFECTIVE SEP 14, 2015 FHA Rule Changes www.greenpathfunding.com FHA Changes: Assets 2015 1 Any single deposit that exceeds 25% of the total monthly qualifying income on the loan. Additionally, any questionable

EFFECTIVE SEP 14, 2015 FHA Rule Changes www.greenpathfunding.com FHA Changes: Assets 2015 1 Any single deposit that exceeds 25% of the total monthly qualifying income on the loan. Additionally, any questionable

Understanding Loan Prospector s Determination of Total Monthly Debt for FHA and VA Loans

Understanding s Determination of Total Monthly Debt for FHA and Effective for new submissions on and after the October 19, 2014 Implementation The accuracy of the total monthly debt-to-income (DTI) ratio

Understanding s Determination of Total Monthly Debt for FHA and Effective for new submissions on and after the October 19, 2014 Implementation The accuracy of the total monthly debt-to-income (DTI) ratio

Section 1.37 Income Validation Guidelines

Section 1.37 Income Validation lines In This Section This section contains the following topics. Income Validation Requirements... 2 Overview... 2 Related Bulletins... 2 IRS Form 4506-T Requirement...

Section 1.37 Income Validation lines In This Section This section contains the following topics. Income Validation Requirements... 2 Overview... 2 Related Bulletins... 2 IRS Form 4506-T Requirement...

E MORTGAGE MANAGEMENT LLC 303 DU REFI PLUS

E MORTGAGE MANAGEMENT LLC 303 DU REFI PLUS PRODUCT GUIDELINES 12/8/2014 MORTGAGE ELIGIBILITY Product Description and Product Codes Code Short Description Long Description CF30RP 30 YR REFI PLUS CF30RP

E MORTGAGE MANAGEMENT LLC 303 DU REFI PLUS PRODUCT GUIDELINES 12/8/2014 MORTGAGE ELIGIBILITY Product Description and Product Codes Code Short Description Long Description CF30RP 30 YR REFI PLUS CF30RP

Ability-to-Repay and Qualified Mortgage Rule

APRIL 10, 2013 Ability-to-Repay and Qualified Mortgage Rule SMALL ENTITY COMPLIANCE GUIDE 1 Please refer to our concurrent proposal about the changes we have proposed to this rule. This notice proposes

APRIL 10, 2013 Ability-to-Repay and Qualified Mortgage Rule SMALL ENTITY COMPLIANCE GUIDE 1 Please refer to our concurrent proposal about the changes we have proposed to this rule. This notice proposes

WHEDA Advantage Conventional Underwriting Guide

WHEDA Advantage Conventional Underwriting Guide Page left blank intentionally. WHEDA Introduction 1 Last Revised Date: October 30, 2015 Table of Contents 1.00 Introduction... 6 2.00 Underwriting Philosophy...

WHEDA Advantage Conventional Underwriting Guide Page left blank intentionally. WHEDA Introduction 1 Last Revised Date: October 30, 2015 Table of Contents 1.00 Introduction... 6 2.00 Underwriting Philosophy...

VA Loan Guaranty Program Serve the mortgage lending needs of borrowers who serve our country

VA Loan Guaranty Program Serve the mortgage lending needs of borrowers who serve our country Jaime A Garcia 626.768.0700 NMLS 290316 DRE 01148553 Desktop Underwriter is a registered trademark of Fannie

VA Loan Guaranty Program Serve the mortgage lending needs of borrowers who serve our country Jaime A Garcia 626.768.0700 NMLS 290316 DRE 01148553 Desktop Underwriter is a registered trademark of Fannie

QUICK MORTGAGE GUIDE

QUICK MORTGAGE GUIDE TABLE OF CONTENTS FNMA CONVENTIONAL LOANS - Page 3 FHA LOANS - Page 7 VA LOANS - Page 11 ADJUSTABLE RATE MORTGAGES - Page 15 CONTACT INFORMATION - Page 16 FNMA CONVENTIONAL LOANS The

QUICK MORTGAGE GUIDE TABLE OF CONTENTS FNMA CONVENTIONAL LOANS - Page 3 FHA LOANS - Page 7 VA LOANS - Page 11 ADJUSTABLE RATE MORTGAGES - Page 15 CONTACT INFORMATION - Page 16 FNMA CONVENTIONAL LOANS The

Uniform Residential Loan Application 1003

Uniform Residential Loan Application 1003 Purpose Mortgage Loan Application The loan application is your introduction to the borrower. Analysis of the form helps you to develop an image of the borrower

Uniform Residential Loan Application 1003 Purpose Mortgage Loan Application The loan application is your introduction to the borrower. Analysis of the form helps you to develop an image of the borrower

Magnolia Bank VA Refinance Options

Interest Rate Reduction Refinance Loans (IRRRLS) Eligibility Cash Out Refinance 1. ELIGIBLE PRODUCTS VA Fixed Rate Product VA Hybrid ARMs VA High Balance Products VA Fixed Rate Product VA Hybrid ARMs VA

Interest Rate Reduction Refinance Loans (IRRRLS) Eligibility Cash Out Refinance 1. ELIGIBLE PRODUCTS VA Fixed Rate Product VA Hybrid ARMs VA High Balance Products VA Fixed Rate Product VA Hybrid ARMs VA

CHAPTER 9: INCOME ANALYSIS 7 CFR 3555.152

CHAPTER 9: INCOME ANALYSIS 7 CFR 3555.152 9.1 INTRODUCTION The lender is responsible for ensuring that applicants meet eligibility criteria for the SFHGLP. One very important criterion is income eligibility.

CHAPTER 9: INCOME ANALYSIS 7 CFR 3555.152 9.1 INTRODUCTION The lender is responsible for ensuring that applicants meet eligibility criteria for the SFHGLP. One very important criterion is income eligibility.

ATR and QM Effective Date

The Consumer Financial Protection Bureau (CFPB) has issued the final regulations to implement the Ability to Repay (ATR) and Qualified Mortgage (QM) provisions under the Dodd-Frank Act. Greenbox Loans

The Consumer Financial Protection Bureau (CFPB) has issued the final regulations to implement the Ability to Repay (ATR) and Qualified Mortgage (QM) provisions under the Dodd-Frank Act. Greenbox Loans

Break Out Session: Mortgage Loan Underwriting and Pricing

Break Out Session: Mortgage Loan Underwriting and Pricing Agenda Ability to Repay (ATR)/Qualified Mortgages (QMs) Effective Date: Applications received on or after January 10, 2014 2013 Home Ownership

Break Out Session: Mortgage Loan Underwriting and Pricing Agenda Ability to Repay (ATR)/Qualified Mortgages (QMs) Effective Date: Applications received on or after January 10, 2014 2013 Home Ownership

A Simplified Overview of FHA Loan Origination

Introduction to FHA Origination A Simplified Overview of FHA Loan Origination Topics of Discussion Introduction to FHA Fundamentals of Loan Origination FHA Loan Limits Borrower Eligibility Property Eligibility

Introduction to FHA Origination A Simplified Overview of FHA Loan Origination Topics of Discussion Introduction to FHA Fundamentals of Loan Origination FHA Loan Limits Borrower Eligibility Property Eligibility

MSHDA's Down Payment Assistance and Mortgage Credit Certificate. May 21, 2010 (3:30 5:00 p.m.) Facilitated by: Carol Brito (MSHDA) Sponsored by:

Facilitated by: Carol Brito (MSHDA) Sponsored by:") MSHDA's Down Payment Assistance and Mortgage Credit Certificate May 21, 2010 (3:30 5:00 p.m.) Facilitated by: Carol Brito (MSHDA) Sponsored by: CREDIT UNIONS A DRIVING FORCE OF COMMUNITIES MSHDA Overview

MSHDA's Down Payment Assistance and Mortgage Credit Certificate May 21, 2010 (3:30 5:00 p.m.) Facilitated by: Carol Brito (MSHDA) Sponsored by: CREDIT UNIONS A DRIVING FORCE OF COMMUNITIES MSHDA Overview

CFPB Issues Much Anticipated Final Rules: Ability to Repay, Qualified Mortgages, Escrow Requirements and Homeownership Counseling

CFPB Issues Much Anticipated Final Rules: Ability to Repay, Qualified Mortgages, Escrow Requirements and Homeownership Counseling The Consumer Financial Protection Bureau ( CFPB ) issued their much anticipated

CFPB Issues Much Anticipated Final Rules: Ability to Repay, Qualified Mortgages, Escrow Requirements and Homeownership Counseling The Consumer Financial Protection Bureau ( CFPB ) issued their much anticipated

VA IRRL 2. CURRENT FIRST MORTGAGE ELIGIBILITY

1. PRODUCT DESCRIPTION VA Fixed Rate and ARM Mortgages for Refinance Transactions Fixed Rate Mortgage 10 to 30 years in 5 year increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans are

1. PRODUCT DESCRIPTION VA Fixed Rate and ARM Mortgages for Refinance Transactions Fixed Rate Mortgage 10 to 30 years in 5 year increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans are

Underwriting Guidelines

Underwriting Guidelines The requirements in this section apply to all Loans submitted to ALC for purchase or funding. However, agency eligible conforming Loans must meet applicable Fannie Mae and Freddie

Underwriting Guidelines The requirements in this section apply to all Loans submitted to ALC for purchase or funding. However, agency eligible conforming Loans must meet applicable Fannie Mae and Freddie

Section 2.04 - DU Refi Plus Loan Program

Section 2.04 - DU Refi Plus Loan Program In This Product Description This product description contains the following topics: Overview... 2 Related Bulletins... 5 Existing Mortgage Eligibility Requirements...

Section 2.04 - DU Refi Plus Loan Program In This Product Description This product description contains the following topics: Overview... 2 Related Bulletins... 5 Existing Mortgage Eligibility Requirements...

CLIENT AND FRIENDS BANKING UPDATE SILVER, FREEDMAN & TAFF, L.L.P. 3299 K STREET, N.W., SUITE 100, WASHINGTON, D.C.

CLIENT AND FRIENDS BANKING UPDATE SILVER, FREEDMAN & TAFF, L.L.P. 3299 K STREET, N.W., SUITE 100, WASHINGTON, D.C. 20007 (202) 295-4500 (202) 337-5502 www.sftlaw.com A DETAILED SUMMARY OF THE CFPB S FINAL

CLIENT AND FRIENDS BANKING UPDATE SILVER, FREEDMAN & TAFF, L.L.P. 3299 K STREET, N.W., SUITE 100, WASHINGTON, D.C. 20007 (202) 295-4500 (202) 337-5502 www.sftlaw.com A DETAILED SUMMARY OF THE CFPB S FINAL

Summary of 2013 Mortgage Rules Issued by the Consumer Financial Protection Bureau

Summary of 2013 Mortgage Rules Issued by the Consumer Financial Protection Bureau Promontory Financial Group, LLC 801 17th Street, NW, Suite 1100 Washington, DC 20006 +1 202 384 1200 promontory.com Contents

Summary of 2013 Mortgage Rules Issued by the Consumer Financial Protection Bureau Promontory Financial Group, LLC 801 17th Street, NW, Suite 1100 Washington, DC 20006 +1 202 384 1200 promontory.com Contents

Arkansas Development Finance Authority

Arkansas Development Finance Authority ADFA S MORTGAGE BOND PROGRAM Arkansas Development Finance Authority P.O. Box 8023 Little Rock, AR 72203 www.arkansas.gov/adfa Home ToOwn Staff Murray Harding-Manager

Arkansas Development Finance Authority ADFA S MORTGAGE BOND PROGRAM Arkansas Development Finance Authority P.O. Box 8023 Little Rock, AR 72203 www.arkansas.gov/adfa Home ToOwn Staff Murray Harding-Manager

Brooklyn Park Economic Development Authority

Brooklyn Park Economic Development Authority Neighborhood Stabilization Program NSP HOMEBUYER ASSISTANCE PROGRAM FOR CITY/PARTNER ACQUISITION AND REHAB Program Description & Guidelines July 2011 TABLE

Brooklyn Park Economic Development Authority Neighborhood Stabilization Program NSP HOMEBUYER ASSISTANCE PROGRAM FOR CITY/PARTNER ACQUISITION AND REHAB Program Description & Guidelines July 2011 TABLE

DOCUMENTS. Document Requirements for Your Home Loan

DOCUMENTS Document Requirements for Your Home Loan Copyright 2016 Platinum Home Mortgage Corporation All Rights Reserved Feel free to email, tweet, blog, and pass this ebook around the web, but please

DOCUMENTS Document Requirements for Your Home Loan Copyright 2016 Platinum Home Mortgage Corporation All Rights Reserved Feel free to email, tweet, blog, and pass this ebook around the web, but please

ACTION ITEM REVISIONS AND MODIFICATIONS TO UNIVERSITY OF CALIFORNIA LOAN PROGRAM POLICIES AND PROCEDURES EXECUTIVE SUMMARY

F9 Office of the President TO MEMBERS OF THE COMMITTEE ON FINANCE: For Meeting of November 14, 2013 ACTION ITEM REVISIONS AND MODIFICATIONS TO UNIVERSITY OF CALIFORNIA LOAN PROGRAM POLICIES AND PROCEDURES

F9 Office of the President TO MEMBERS OF THE COMMITTEE ON FINANCE: For Meeting of November 14, 2013 ACTION ITEM REVISIONS AND MODIFICATIONS TO UNIVERSITY OF CALIFORNIA LOAN PROGRAM POLICIES AND PROCEDURES

Quick Reference Program Summary. The following is an outline of the underwriting and closing requirements of New Hampshire Housing.

Quick Reference Program Summary The following is an outline of the underwriting and closing requirements of New Hampshire Housing. Specific Program Rules are attached to this reference. A reservation cannot

Quick Reference Program Summary The following is an outline of the underwriting and closing requirements of New Hampshire Housing. Specific Program Rules are attached to this reference. A reservation cannot

CITY OF MURFREESBORO AFFORDABLE HOUSING ASSISTANCE PROGRAM POLICIES AND PROCEDURES

CITY OF MURFREESBORO AFFORDABLE HOUSING ASSISTANCE PROGRAM POLICIES AND PROCEDURES 100. Purpose The Murfreesboro Affordable Housing Assistance Program (the Program) encourages homeownership for low-income,

CITY OF MURFREESBORO AFFORDABLE HOUSING ASSISTANCE PROGRAM POLICIES AND PROCEDURES 100. Purpose The Murfreesboro Affordable Housing Assistance Program (the Program) encourages homeownership for low-income,

7/2013 PHFA FORM 3. I/We [print name(s)]: do hereby attest that I/we and the property being purchased meet the following program requirements:

![7/2013 PHFA FORM 3. I/We [print name(s)]: do hereby attest that I/we and the property being purchased meet the following program requirements:](/thumbs/25/5267993.jpg "7/2013 PHFA FORM 3. I/We [print name(s)]: do hereby attest that I/we and the property being purchased meet the following program requirements:") PENNSYLVANIA HOUSING FINANCE AGENCY MORTGAGOR S AFFIDAVIT OF ELIGIBILITY AND ACKNOWLEDGMENT OF PROGRAM REQUIREMENTS FOR KEYSTONE HOME LOAN, HOMESTEAD AND MORTGAGE CREDIT CERTIFICATE PROGRAMS To be completed

PENNSYLVANIA HOUSING FINANCE AGENCY MORTGAGOR S AFFIDAVIT OF ELIGIBILITY AND ACKNOWLEDGMENT OF PROGRAM REQUIREMENTS FOR KEYSTONE HOME LOAN, HOMESTEAD AND MORTGAGE CREDIT CERTIFICATE PROGRAMS To be completed

Supporting documentation and verification guide. For NAB Homeplus and NAB Peak Performance

Supporting documentation and verification guide For NAB Homeplus and NAB Peak Performance Contents Income verification 2 Full time and part time employment (PAYG)2 2 Casual employment2 2 Return to work

Supporting documentation and verification guide For NAB Homeplus and NAB Peak Performance Contents Income verification 2 Full time and part time employment (PAYG)2 2 Casual employment2 2 Return to work

The Consumer Financial Protection Bureau s Ability-to-Repay and Qualified Mortgage Rule

ADVISORY February 2013 The Consumer Financial Protection Bureau s Ability-to-Repay and Qualified Mortgage Rule On January 10, 2013, the Consumer Financial Protection Bureau ( CFPB ) issued its final Ability-to-Repay

ADVISORY February 2013 The Consumer Financial Protection Bureau s Ability-to-Repay and Qualified Mortgage Rule On January 10, 2013, the Consumer Financial Protection Bureau ( CFPB ) issued its final Ability-to-Repay

Ability-to-Repay and Qualified Mortgage Rule

OCTOBER 17, 2013 Ability-to-Repay and Qualified Mortgage Rule SMALL ENTITY COMPLIANCE GUIDE 1 The Bureau recently finalized changes to this rule. The June 2013 ATR/QM Concurrent Final Rule, July 2013 Final

OCTOBER 17, 2013 Ability-to-Repay and Qualified Mortgage Rule SMALL ENTITY COMPLIANCE GUIDE 1 The Bureau recently finalized changes to this rule. The June 2013 ATR/QM Concurrent Final Rule, July 2013 Final

Dr. Debra Sherrill Central Piedmont Community College

Dr. Debra Sherrill Central Piedmont Community College 1 2 Describe the benefits and pitfalls of renting versus owning a home. List the steps required to obtain a mortgage loan. Identify mortgage options

Dr. Debra Sherrill Central Piedmont Community College 1 2 Describe the benefits and pitfalls of renting versus owning a home. List the steps required to obtain a mortgage loan. Identify mortgage options

LOSS MITIGATION APPLICATION

Loan Number: {1} LOSS MITIGATION APPLICATION COMPLETE ALL PAGES OF THIS FORM See Instructions corresponding with numbers in brackets {} on form BORROWER {3} CO BORROWER {4} Borrower s Name Co Borrower

Loan Number: {1} LOSS MITIGATION APPLICATION COMPLETE ALL PAGES OF THIS FORM See Instructions corresponding with numbers in brackets {} on form BORROWER {3} CO BORROWER {4} Borrower s Name Co Borrower

Uniform Residential Loan Application

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable.

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable.

The New Mortgage Servicing Rules. FMS East Coast Regional Conference September 17, 2013

The New Mortgage Servicing Rules FMS East Coast Regional Conference September 17, 2013 What are the new Mortgage Servicing Rules? Ability to Repay/Qualified Mortgage Rule 2013 HOEPA Rule Loan Originator

The New Mortgage Servicing Rules FMS East Coast Regional Conference September 17, 2013 What are the new Mortgage Servicing Rules? Ability to Repay/Qualified Mortgage Rule 2013 HOEPA Rule Loan Originator

Compromise Application

Compromise Application Before we will consider accepting less than the full amount due, we must receive all of the information requested below. Your documentation will be reviewed and verified. A Revenue

Compromise Application Before we will consider accepting less than the full amount due, we must receive all of the information requested below. Your documentation will be reviewed and verified. A Revenue

Allowable Transaction Types:

Allowable Transaction Types: LIFT PRODUCT GUIDELINES Purchases Existing home (with or without property renovation) Short sales (see Restrictions and Commitment Period sections) New construction (must be

Allowable Transaction Types: LIFT PRODUCT GUIDELINES Purchases Existing home (with or without property renovation) Short sales (see Restrictions and Commitment Period sections) New construction (must be

UNDERWRITING GUIDELINES (Applicant and Income Requirements)

") (Applicant and Income Requirements) Applicant Eligibility Have the ability to personally occupy the dwelling Be a citizen of the United States or be admitted for permanent residency Non-occupant co-borrowers

(Applicant and Income Requirements) Applicant Eligibility Have the ability to personally occupy the dwelling Be a citizen of the United States or be admitted for permanent residency Non-occupant co-borrowers