Making Retirement Work

|

|

|

- Brittany McDaniel

- 8 years ago

- Views:

Transcription

1 Making Retirement Work Francis J. Sennott March 12, 2013 ROPES & GRAY LLP

2 Agenda Planning for Retirement Saving for retirement Qualified retirement plans Other personal savings Investment planning Social Security Asset draw down Other retirement planning considerations 2

3 Planning for Retirement 3

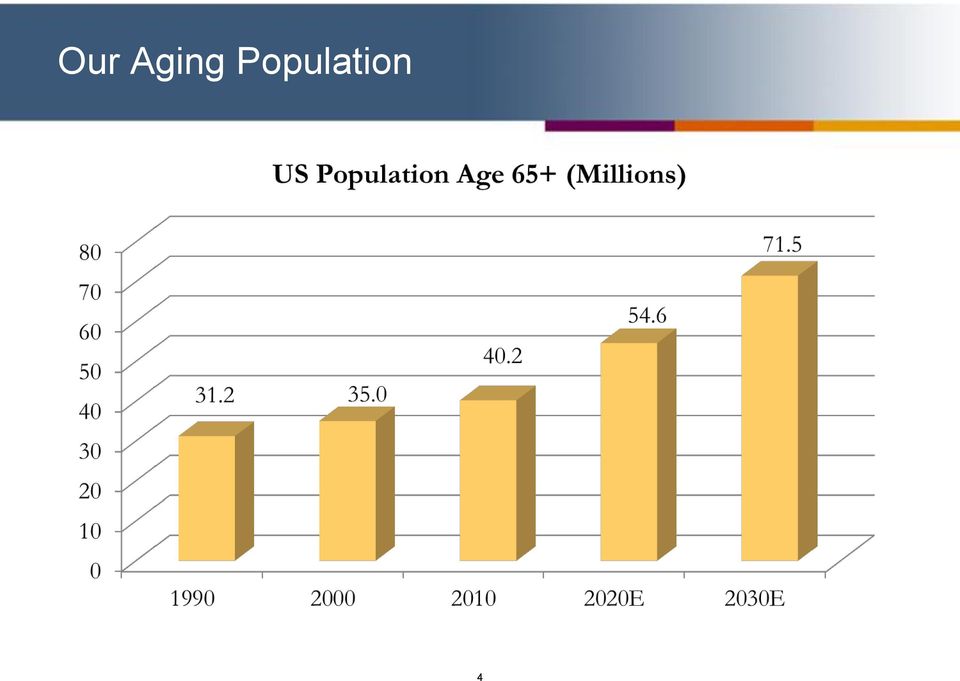

4 Our Aging Population 4

5 What is Retirement Planning? Lifestyle planning Cash flow planning Income tax planning Debt management College funding Investment planning Benefits planning Distribution planning Life insurance planning Estate planning 5

6 Where Will Your Retirement Income Come From? Traditional Sources Employer sponsored retirement savings plans Personal savings Social Security Other Sources Price trade-down in personal residence Reverse mortgage Inheritance Life insurance proceeds on death of family member 6

7 Retirement Planning Tools The Boston College Center for Retirement Research provides data on many retirement planning issues The Center for Retirement Research also provides interactive retirement planning tools 7

8 Savings for Retirement 8

9 Start Saving Early Twin Sisters: Janet Joan Invests $2,000 per year Invests $2,000 per year for 10 years for 35 years from age 21 to 30 from age 31 to 65 Earns a 7% Earns a 7% annual return annual return At age 65 $316,000 $296,000 9

10 Set Your Savings Goals Pre-tax Savings As a Percentage of Salary to Achieve a 70% Retirement Income Replacement Ratio at Age 65* Pre-tax Investment Return Age 4% 5% 6% 7% 8% 9% 10% 25 32% 23% 16% 12% 8% 6% 4% 30 37% 27% 20% 15% 11% 8% 6% 35 45% 34% 26% 19% 15% 11% 9% 40 55% 43% 33% 26% 20% 16% 13% 45 70% 56% 45% 36% 29% 24% 20% 50 76% 79% 65% 54% 45% 38% 32% % 124% 105% 89% 77% 66% 57% % 261% 226% 197% 174% 154% 137% Assumes 3% average salary increases over career, 2% cost of living increases, $0 starting balance, age 95 life expectancy. Adjust for employer matching contributions. 10

11 Saving for Retirement Tax Favored Investing Employer sponsored retirement plans 401(k) plans 403(b) plans 457(b) plans Self-employed plans Traditional individual retirement accounts (IRAs) Roth IRAs Nonqualified annuities Personal Savings Bank accounts Mutual Funds & ETFs Brokerage and investment accounts Separately managed accounts 11

12 401(k)/403(b) Plans Qualified employer-sponsored retirement plan Traditional Roth Assets grow free of income tax Participants may contribute Up to $17,500 in 2013 Participants age 50 or older may make a $5,500 catch-up contribution bringing total to $23,000 for 2013 Required minimum distributions begin at later of retirement under the plan or attainment of age 70 ½ Distributions are based on life expectancy The required minimum distributions increase as the participant ages Plan assets may be rolled into an IRA at retirement 12

13 Traditional vs. Roth 401(k)/403(b) Traditional 401(k)/403(b) Contributions are pre-tax Distributions taxed at ordinary income rates Required minimum distributions commence at the later of retirement, or attaining age 70 ½ 10% Penalty tax on distributions before age 59 ½ Certain exceptions apply Roth 401(k)/403(b) Contributions are after tax Distributions are free of tax if Funds in plan for at least five years and The distribution is Made after age 59 ½ Made after a disability Payable to a beneficiary at death $10,000 or less and used to help purchase your first home Required minimum distributions from Roth 401(k)/403(b), but not from rollover Roth IRA 13

14 Roth Income Tax Considerations Traditional Roth Roth 401(k) 401(k) Advantage 2012 Contribution $15,000 $15,000 Held Back to Pay Tax (33%) $0 ($5,000) Final Contribution $15,000 $10,000 Growth After 10 Years 2x 2x (7.18%/Yr) (7.18%/Yr) Balance After 10 Years $30,000 $20,000 Tax Due on Liquidation Case 1. 25% Rate ($7,500) $0 Case 2. 33% Rate ($10,000) $0 Case 3. 40% Rate ($12,000) $0 Liquidation Value Case 1. 25% Rate $22,500 $20,000 ($2,500) Case 2. 33% Rate $20,000 $20,000 ($0) Case 3. 40% Rate $18,000 $20,000 $2,000 14

$0 Case 3. 40% Rate ($12,000) $0 Liquidation Value Case 1. 25% Rate $22,500 $20,000 ($2,500) Case 2.")

($5,000) Balance $15,000 $5,000 $15,000 $0 Growth After 10 Years 2x 1.7x 2x (7.18%/Yr) (5.45%) (7.18%) Balance After 10 Years $30,000 $8,500 $30,000 Tax Due on Liquidation Case 1.")

15 Source of Funds to Pay Tax Liability Traditional Taxable Roth Taxable Roth 401(k) Side Fund 401(k) Side Fund Advantage 2012 Contribution $15,000 $5,000 $15,000 $5,000 Liquidated to Pay Tax (33%) $0 $0 ($0) ($5,000) Balance $15,000 $5,000 $15,000 $0 Growth After 10 Years 2x 1.7x 2x (7.18%/Yr) (5.45%) (7.18%) Balance After 10 Years $30,000 $8,500 $30,000 Tax Due on Liquidation Case 1. 25% Rate ($7,500) $0 $0 Case 2. 33% Rate ($10,000) $0 $0 Case 3. 40% Rate ($12,000) $0 $0 Liquidation Value Case 1. 25% Rate $22,500 $8,500 $30,000 Case 2. 33% Rate $20,000 $8,500 $30,000 Case 3. 40% Rate $18,000 $8,500 $30,000 Total Liquidation Value Case 1. 25% Rate $31,000 $30,000 ($1,000) Case 2. 33% Rate $28,500 $30,000 $1,500 Case 3. 40% Rate $26,500 $30,000 $3,500 15

$0 $0 Liquidation Value Case 1. 25% Rate $22,500 $8,500 $30,000 Case 2. 33% Rate $20,000 $8,500 $30,000 Case 3.")

16 Personal Savings - Individual Retirement Accounts Traditional IRA $5,500 annual contribution limit (plus $1,000 catch-up contributions) Spousal IRAs may be established Contributions fully tax deductible if Not covered by employer-sponsored plan If covered by employer plan, phase-out of contribution deduction as income increases Modified adjusted gross income (MAGI) between $59,000 and $69,000 for a single person MAGI of $95,000 to $115,000 for a married couple If only one spouse is covered by an employer sponsored plan, joint MAGI of $178,000 to $188,000 for the non-covered spouse Permitted investments include mutual funds and self-directed brokerage accounts Investment income is tax deferred Required minimum distributions upon attaining age 70 ½ Distributions subject to income tax at ordinary rates after recovery of after-tax balance over taxpayer s life expectancy 10% Excise tax on distributions prior to age 59 ½. Certain exceptions apply 16

17 Personal Savings - Individual Retirement Accounts Roth IRA Similar to traditional IRA with tax free earnings Distributions are free of tax if Funds in plan for at least five years and The distribution is Made after age 59 ½ Made after a disability Payable to a beneficiary at death $10,000 or less and used to help purchase your first home Contributions are not deductible Contribution limits integrated with traditional IRA contribution limits Phase-out of contribution limit as income increases Modified adjusted gross income (MAGI) between $110,000 and $125,000 for a single person MAGI of $178,000 to $188,000 for a married couple Conversion to Roth IRA permissible with no income limits Cannot cherry-pick IRA to be converted No required minimum distributions 17

18 Nonqualified Annuities A financial vehicle offered by life insurance companies Invest funds in annuity policy Earn an investment return Pay expenses associated with the annuity policy Eventually take distributions over a period of time based on the accumulated cash value There are no contribution limits Contributions are not tax deductible outside of a qualified plan or IRA Earnings grow free of tax Distributions are subject to income tax Cost basis is recovered over life expectancy of annuitant, so portion of benefit is tax free. 18

19 Nonqualified Annuities Investment Options Fixed annuities The insurance company controls the investment of the policy cash value. The cash is usually invested in a mixture of bonds and mortgages. The insurance company usually guarantees a minimum investment return, typically 2% to 3%. Once the contract is annuitized, benefit payments are fixed. Variable annuities The insurance company provides the policy owner a series of mutual fund investment options and the owner may decided how to allocate the cash value across the funds. Earnings are credited to the contract in accordance with the investment performance of the underlying funds. Once the contract is annuitized, benefit payments will vary with investment performance. 19

20 Selected Annuity Income Options Straight life income Life with period certain Joint and survivor Term certain 20

21 Rules for Saving - Retirement Plans Maximize income tax favored vehicles Contribute to Roth 401(k) if cash flow permits Contribute the maximum, including catch-up contributions Contribute to Roth IRA if cash flow still permits If your adjusted gross income (AGI) is over the limit ($127,000 for a single individual, $188,000 for a married couple) consider contributing to a traditional IRA and then converting to a Roth IRA Cannot cherry pick IRA to convert; must aggregate all IRA balances and after tax contributions and allocate to amount converted If Roth option not available, contribute to regular 401(k) If cash flow doesn t permit a Roth IRA contribution, and AGI is below limits, consider a tax deductible IRA contribution. 21

22 Rules for Savings Retirement Plans (Cont.) Non-deductible IRA contributions May not be worthwhile for an equity investor under the current income tax regime for capital gains and dividends The IRA converts tax favored capital gains and dividends to ordinary income 20% 40% in Massachusetts 25% 45% in top tax bracket $5,500 non-deductible IRA contribution: At 6% annual return, balance grows to $17,639 after 20 years If liquidated, ordinary income tax due on $12,139 ($17,639 - $5,500) After 40% tax, balance is $12,783 After tax annual return of 4.31% Reduction due to income taxes is 6% % = 1.69%, or 28% of total An equity investor would expect a lower effective tax rate than 28% Results could be different for a fixed income investor 2013 Income tax changes may affect results: 39.6% top federal tax rate 3.8% Medicare tax on investment income 22

23 Rules for Savings - Annuities Annuities are tax favored, but this may not be the right time for them For fixed annuities, interest rates are very low and the contracts usually carry a 1.25% mortality and expense (M & E) fee, leaving a modest net return For equity investors in variable annuities The result is similar to that for non-deductible traditional IRAs with capital gains and dividend income converted to ordinary income, and there is still the 1.25% M & E fee. Annuities may still be appropriate for someone with real concerns about outliving their assets. 23

24 Annuity Returns * Single Premium Immediate Annuity Net Gross Cost Tax After Tax Year Age Outlay Benefit Recovery at 33% Benefit IRR ,000 6,072 5,000 (354) 5, % ,072 5,000 (354) 5, % ,072 5,000 (354) 5, % ,072 5,000 (354) 5, % ,072 5,000 (354) 5, % ,072 5,000 (354) 5, % ,072 5,000 (354) 5, % ,072 5,000 (354) 5, % ,072 5,000 (354) 5, % ,072 5,000 (354) 5, % ,072 5,000 (354) 5, % ,072 5,000 (354) 5, % ,072 5,000 (354) 5, % ,072 5,000 (354) 5, % ,072 5,000 (354) 5, % Single Premium Immediate Annuity Straight life annuity 65 Year old female $100,000 Investment 20 Year life expectancy 33% Income tax rate ,072 5,000 (354) 5, % ,072 5,000 (354) 5, % ,072 5,000 (354) 5, % ,072 5,000 (354) 5, % ,072 5,000 (354) 5, % ,072 - (2,004) 4, % ,072 - (2,004) 4, % ,072 - (2,004) 4, % ,072 - (2,004) 4, % ,072 - (2,004) 4, % ,072 - (2,004) 4, % ,072 - (2,004) 4, % ,072 - (2,004) 4, % ,072 - (2,004) 4, % ,072 - (2,004) 4, % Benefit figures from 24

25 Personal Savings - Investment Vehicles Mutual funds Diversification Reasonable fees Fees are usually expressed as a percentage of the assets under management ( AUM ) (i.e., 0.50% %, aka 50 basis points to 150 basis points ) Note share classes (i.e., A, B, I, R) Active vs. passive management Open vs. closed-end funds Exchange Traded Funds ( ETFs) Diversification Modest fees Passive management May be slightly more income tax efficient than a passive mutual fund Individually owned securities For those with some investment expertise and the time to manage their own assets 25

26 Personal Savings - Investment Platforms Mutual fund families i.e., Vanguard, Fidelity, T. Rowe Price Discount brokers i.e., Schwab, Fidelity, E-Trade, TD Ameritrade Access to mutual funds from numerous fund families, ETFs and individual securities at low cost Access to research material, but otherwise limited investment advice Full service brokers i.e., Merrill Lynch, Morgan Stanley, UBS Access to mutual funds, ETFs and individual securities Access to research and financial planning tools Typically offer a wrap program that offers advice and asset management for a percentage of the assets under management (1% - 3%). May be best option for investors with accounts less than $500,000 26

27 Personal Savings - Investment Platforms (Cont.) Separately Managed Accounts ( SMAs ) Manager with expertise in a single asset class (i.e., large cap U.S. equities, municipal bonds) Charge a fee based on assets under management 0.30% % for a fixed income portfolio 0.80% % for an equity portfolio Large minimum investments ($500,000 - $5,000,000) A full service broker may access SMAs for clients at lower minimums and fees Greater ability to be income tax efficient Investment Advisors Manager of Managers May use a combination of SMAs and mutual funds Recommend asset allocation Prepare consolidated statements and investment reports Charge a fee on top of mutual fund and SMA fees 0.50% % depending on level of service Typically have relationship minimums of $500,

28 Savings Rules of Thumb As excess cash flow permits fund: Down payment for first home 6 Month supply of liquid assets Pay down high interest debt Regular 401(k)/403(b) Roth 401(k)/403(b) Tax deductible IRA Roth IRA Taxable investment accounts Consider non-deductible IRAs and annuities depending upon tax rules and interest rate environment As family situation changes fund: Life insurance for survivor income protection 529 Plans for child s college costs Long term care insurance Gifts to heirs and charities 28

29 Investment Planning 29

30 Asset Allocation Historical Review of Market Leadership 30

31 Sample Asset Allocation Models Income/ Aggressive Conservative Moderate Growth Balanced Growth Growth Cash Money Markets 5% 4.0% 3% 2.5% 1.5% Fixed Income U.S. Investment Grade - Taxable/Tax Exempt 51% 41.0% 31% 21.5% 13.5% High Yield Bonds 2% 2.5% 3% 3.0% 2.5% Emerging Market Debt 2% 2.5% 3% 3.0% 2.5% Equity U.S. Large Cap 14% 17.5% 21.0% 23.5% 26.0% U.S. Mid/Small Cap 5% 6.0% 7.5% 10.0% 12.0% Non-U.S. Developed 10% 12.5% 16.5% 20.5% 24.5% Non-U.S. Emerging 3% 4.0% 5.0% 6.0% 7.0% Long-Short 2% 2.0% 2.0% 1.5% 1.5% Equity Income 3% 4.0% 4.0% 4.0% 4.0% Commodity Funds 3% 4.0% 4.0% 4.5% 5.0% Total 100% 100% 100% 100% 100% 31

32 Target Retirement Date Funds JP Morgan Retirement Target Date Funds See BC Center for Retirement Research: 32

33 Social Security 33

34 Social Security Normal Retirement Age Year of Birth Full Retirement Age and 2 months and 4 months and 6 months and 8 months and 10 months 1960 or later 67 34

35 Social Security Full Benefit at Normal Retirement Age The maximum monthly benefit for 2013 is $2,533 May collect a reduced benefit as early as age 62 5/9 th of 1% per month for first 36 months 5/12ths of 1% per month for each additional month May delay receipt of benefits until age 70 8% per year increase for those born 1943 or later See BC s Center for Retirement Research: 35

36 Social Security Reduction for Continued Earnings If you collect a benefit before your normal retirement age, the benefit is reduced by $1 for every $2 in earnings above an annual limit. The 2013 limit is $15,120 In the year you reach normal retirement age, the benefit is reduced by $1 for every $3$ of earnings above the limit until the month you reach normal retirement age. There is no reduction in benefits once you reach normal retirement age. Example: A worker starts collecting Social Security at age 62 in 2013; the benefit is $1,000/mo or $12,000 per year Normal retirement age is 66 The worker earns $25,120 in wages, $10,000 over the limit The Social Security benefit will be reduced by $5,000 for the year 36

37 Social Security Spousal Benefit At retirement, a spouse may collect the greater of his or her own Social Security benefit or 50% of the other spouse s benefit. Spousal benefits are reduced for early retirement or increased for delayed retirement in the same manner as with the primary benefit. When the spouse earning the primary benefit dies, the surviving spouse may step up to the primary benefit. 37

38 Social Security In general, don t collect benefits if they ll be reduced by continued earnings in excess of the annual limit Wait until normal retirement age (NRA) if you believe you ll live into your early 80s. Wait until age 70 if you believe you ll live into your mid 80s. At your NRA, your spouse may collect the spousal benefit even if you have elected to suspend your own benefits until age 70. If you have reached NRA, you can claim a spousal benefit and then switch to your own record at a later date. H & W are both age 66 and at NRA When to Collect Benefits? H s benefit is $1,400 per month while W s is $1,000 H files for benefits, but defers to age 70. W can receive $700/month (50% of H s benefit) until age 70 and then switch to her own higher benefit of 132% of the NRA benefit (8% per year for 4 years), or $1,320/mo before COLAs 38

39 Social Security Benefit Analysis* Pre-tax After Tax Pre-tax After Tax Pre-tax After Tax Maximum Starting Age Benefit Benefit 4% Benefit Benefit 4% Benefit Benefit 4% PV Age 62 21,277 15,852 15, , ,703 16,169 31, , ,137 16,492 46, , ,580 16,822 61, , ,031 17,158 76, , ,492 17,501 90,652 33,560 25,002 20, , ,962 17, ,760 34,231 25,502 40, , ,441 18, ,597 34,915 26,012 60, , ,930 18, ,168 35,614 26,532 79,858 44,161 32,900 24, , ,428 18, ,478 36,326 27,063 98,872 45,044 33,558 47, , ,937 19, ,532 37,053 27, ,521 45,945 34,229 70, , ,456 19, ,335 37,794 28, ,810 46,864 34,914 93, , ,985 20, ,891 38,549 28, ,748 47,801 35, , , ,524 20, ,206 39,320 29, ,341 48,757 36, , , ,075 20, ,285 40,107 29, ,596 49,733 37, , , ,636 21, ,131 40,909 30, ,519 50,727 37, , , ,209 21, ,749 41,727 31, ,117 51,742 38, , , ,793 22, ,144 42,562 31, ,395 52,777 39, , , ,389 22, ,319 43,413 32, ,360 53,832 40, , , ,997 23, ,280 44,281 32, ,018 54,909 40, , , ,617 23, ,030 45,167 33, ,375 56,007 41, , , ,249 24, ,573 46,070 34, ,437 57,127 42, , , ,894 24, ,914 46,992 35, ,209 58,270 43, , , ,552 24, ,055 47,931 35, ,697 59,435 44, , , ,223 25, ,002 48,890 36, ,907 60,624 45, , , ,908 26, ,757 49,868 37, ,843 61,836 46, , , ,606 26, ,325 50,865 37, ,511 63,073 46, , , ,318 27, ,709 51,883 38, ,916 64,334 47, , , ,044 27, ,912 52,920 39, ,064 65,621 48, , , ,785 28, ,938 53,979 40, ,959 66,933 49, , , * NRA age 67, 2% inflation, 30% income tax rate on 85% of benefit, 4% discount rate, normal benefit of $2,533 39

40 Asset Draw Down 40

41 Draw Down Rates Extensive research has been done on safe draw down rates in retirement 2.1% Inflation Assumption 4% Inflation Assumption Graphs taken from: Breaking Free from the Safe Withdrawal Rate Paradigm: Extending the Efficient Frontier for Retirement Income by Wade Pfau, AdvisorPerspectives.com. 41

42 Draw Down Rates It s too late for me now; I have what I have. How much can I spend? Safe Draw Down Rate in Perpetuity In theory, your funds should never run out and your spending should keep up with inflation if you withdraw no more than: the gross investment return minus the inflation rate For example: If your gross investment return is 6% and inflation is 2%, you can withdraw 4% of your balance (6% - 2%). Income taxes on the 6% investment return must be paid from the funds withdrawn. 42

43 Safe Draw Down of $100,000* 6% Gross investment return, 4% annual draw down ($4,000) 43

44 Draw Down Rates When Spending Principal * I put my kinds through college and they ll get my house. I don t care if I leave them anything else. Pre-tax Investment Return Yrs. in Ret. 4% 5% 6% 7% 8% 9% 10% 10 11% 11% 12% 12% 13% 13% 14% 15 8% 8% 9% 9% 10% 10% 11% 20 6% 6% 7% 8% 8% 9% 9% 25 5% 6% 6% 7% 7% 8% 9% 30 4% 5% 6% 6% 7% 7% 8% 35 4% 4% 5% 6% 6% 7% 8% 40 4% 4% 5% 5% 6% 7% 8% 45 3% 4% 5% 5% 6% 7% 8% Assumes 2% cost of living increases. 44

45 Draw Down on $100,000 When Spending Principal * Retire age 65, 30 year life expectancy, 8% investment return, 2% cost of living increases, 6.78% draw down rate ($6,780). 45

46 Problems with Formulaic Draw Down Rates You cannot know in advance what investment returns and inflation rates will be. What if the inflation rate exceeds the gross return? What if your portfolio loses money? Is your only option to invest in completely safe investments that is likely produce little return? i.e., short term U.S. government bonds What if something unexpected happens? An unusual expense? You live too long? A prolonged market decline? No draw down formula is safe indefinitely You must periodically update your retirement plan 46

47 Monte Carlo Sensitivity Analysis * 90 th % 10 th % 50 th % Assumes 8% investment return, 11.84% volatility, initial 6.78% draw down, 2% cost of living increases, 30-year draw down period. 47

48 Rules of Thumb for Draw Downs Maximize income tax deferral In general, spend already taxed assets first upon retirement Postpone distributions from IRAs and qualified plans for as long as possible Required minimum distributions (RMDs) from regular IRAs and qualified plans begin at age 70 ½ RMDs from a qualified plan may be postponed if the participant is still employed by the sponsoring employer and not considered retired under the terms of the plan. Participant may elect to postpone first RMD into the next tax year and take two distributions that year. Decision depends upon tax rate differential in the two calendar years Take only RMDs unless more is required. Reconsider if income tax rates are expected to increase significantly in the future and the participant is already taking large distributions Spend Roth assets last There are no required distributions from a Roth IRA, but there are RMDs from a Roth 401(k) Roll your Roth 401(k) into a Roth IRA upon termination or retirement 48

49 Other Retirement Planning Considerations Medicare supplement insurance Long term care insurance Change of domicile Defined benefit pension distribution options 49

50 IRS Circular 230 Disclosure To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. tax advice contained herein is not intended or written to be used, and cannot be used by any taxpayer, for the purpose of avoiding U.S. tax penalties. 50

! There are currently two types of IRAs.

An IRA can be established and funded at any time from January 1 of the current year and up to and including the date an individual s income tax return is due (generally, April 1 of the following year),

An IRA can be established and funded at any time from January 1 of the current year and up to and including the date an individual s income tax return is due (generally, April 1 of the following year),

Can Deduction Be Taken Prior to Investing the Funds?

Deadline to Establish and Fund an IRA An IRA can be established and funded at any time from January of the current year and up to and including the date an individual s income tax return is due (generally,

Deadline to Establish and Fund an IRA An IRA can be established and funded at any time from January of the current year and up to and including the date an individual s income tax return is due (generally,

IRA opportunities at UBS

IRA opportunities at UBS IRAs are highly popular and effective retirement savings vehicles that give your investment earnings the benefit of tax-favored treatment and provide an ideal supplement to employer-sponsored

IRA opportunities at UBS IRAs are highly popular and effective retirement savings vehicles that give your investment earnings the benefit of tax-favored treatment and provide an ideal supplement to employer-sponsored

Traditional and Roth IRAs

october 2012 Understanding Traditional and Roth IRAs summary An Individual Retirement Account (IRA) is a powerful savings vehicle that can help you meet your financial goals. As shown in the chart on page

october 2012 Understanding Traditional and Roth IRAs summary An Individual Retirement Account (IRA) is a powerful savings vehicle that can help you meet your financial goals. As shown in the chart on page

Chapter 14. Agenda. Individual Annuities. Annuities and Individual Retirement Accounts

Chapter 14 Annuities and Individual Retirement Accounts Agenda 2 Individual Annuities Types of Annuities Taxation of Individual Annuities Individual Retirement Accounts Individual Annuities 3 An annuity

Chapter 14 Annuities and Individual Retirement Accounts Agenda 2 Individual Annuities Types of Annuities Taxation of Individual Annuities Individual Retirement Accounts Individual Annuities 3 An annuity

EXPLORING YOUR IRA OPTIONS. Whichever you choose traditional or Roth investing in an IRA is a good step toward saving for retirement.

EXPLORING YOUR IRA OPTIONS Whichever you choose traditional or Roth investing in an IRA is a good step toward saving for retirement. 2 EXPLORING YOUR IRA OPTIONS Planning for retirement can be a challenging

EXPLORING YOUR IRA OPTIONS Whichever you choose traditional or Roth investing in an IRA is a good step toward saving for retirement. 2 EXPLORING YOUR IRA OPTIONS Planning for retirement can be a challenging

Table of contents. 2 Federal income tax rates. 12 Required minimum distributions. 4 Child credits. 13 Roths. 5 Taxes: estates, gifts, Social Security

2015 Tax Guide Table of contents 2 Federal income tax rates 4 Child credits 5 Taxes: estates, gifts, Social Security 6 Rules on retirement plans 8 Saver s credit 12 Required minimum distributions 13 Roths

2015 Tax Guide Table of contents 2 Federal income tax rates 4 Child credits 5 Taxes: estates, gifts, Social Security 6 Rules on retirement plans 8 Saver s credit 12 Required minimum distributions 13 Roths

An IRA can put you in control of your retirement, whether you

IRAs: Powering Your Retirement One of the most effective ways to build and manage funds to help you meet your financial goals is through an Individual Retirement Account (IRA). An IRA can put you in control

IRAs: Powering Your Retirement One of the most effective ways to build and manage funds to help you meet your financial goals is through an Individual Retirement Account (IRA). An IRA can put you in control

1040 Review Guide: MARKETS ADVANCED. Using Your Clients 1040 to Identify Planning Opportunities

1040 Review Guide: Using Your Clients 1040 to Identify Planning Opportunities ADVANCED MARKETS Producers Guide to a 1040 Review At Transamerica, we re committed to providing you and your clients with the

1040 Review Guide: Using Your Clients 1040 to Identify Planning Opportunities ADVANCED MARKETS Producers Guide to a 1040 Review At Transamerica, we re committed to providing you and your clients with the

chart retirement plans 8 Retirement plans available to self-employed individuals include:

retirement plans Contributing to retirement plans can provide you with financial security as well as reducing and/or deferring your taxes. However, there are complex rules that govern the type of plans

retirement plans Contributing to retirement plans can provide you with financial security as well as reducing and/or deferring your taxes. However, there are complex rules that govern the type of plans

KEY FACTORS WHEN CONSIDERING A ROTH IRA CONVERSION

KEY FACTORS WHEN CONSIDERING A ROTH IRA CONVERSION PERTINENT INFORMATION Mr. Kugler has accumulated $1,000,000 in a traditional IRA. Mrs. Kugler is the designated beneficiary (DB) and their daughter is

KEY FACTORS WHEN CONSIDERING A ROTH IRA CONVERSION PERTINENT INFORMATION Mr. Kugler has accumulated $1,000,000 in a traditional IRA. Mrs. Kugler is the designated beneficiary (DB) and their daughter is

Tax-smart ways to save and invest. TIAA-CREF Financial Essentials

Tax-smart ways to save and invest TIAA-CREF Financial Essentials Today s agenda: 1. Finding funds for saving 2. Tax law provisions promoting saving 3. TIAA-CREF savings opportunities 4. TIAA-CREF can help

Tax-smart ways to save and invest TIAA-CREF Financial Essentials Today s agenda: 1. Finding funds for saving 2. Tax law provisions promoting saving 3. TIAA-CREF savings opportunities 4. TIAA-CREF can help

WHICH TYPE OF IRA MAKES THE MOST SENSE FOR YOU?

WHICH TYPE OF IRA MAKES THE MOST SENSE FOR YOU? In 1974, when IRAs were first created, they were rather simple and straightforward. Now, 35 years later, it s challenging to know the best way to save more

WHICH TYPE OF IRA MAKES THE MOST SENSE FOR YOU? In 1974, when IRAs were first created, they were rather simple and straightforward. Now, 35 years later, it s challenging to know the best way to save more

BMO Funds State Street Bank and Trust Company Universal Individual Retirement Account Disclosure Statement. Part One: Description of Traditional IRAs

BMO Funds State Street Bank and Trust Company Universal Individual Retirement Account Disclosure Statement Part One: Description of Traditional IRAs Part One of the Disclosure Statement describes the rules

BMO Funds State Street Bank and Trust Company Universal Individual Retirement Account Disclosure Statement Part One: Description of Traditional IRAs Part One of the Disclosure Statement describes the rules

TRADITIONAL IRA DISCLOSURE STATEMENT

TRADITIONAL IRA DISCLOSURE STATEMENT TABLE OF CONTENTS REVOCATION OF ACCOUNT... 1 STATUTORY REQUIREMENTS... 1 (1) Qualification Requirements... 1 (2) Required Distribution Rules... 1 (3) Approved Form....

TRADITIONAL IRA DISCLOSURE STATEMENT TABLE OF CONTENTS REVOCATION OF ACCOUNT... 1 STATUTORY REQUIREMENTS... 1 (1) Qualification Requirements... 1 (2) Required Distribution Rules... 1 (3) Approved Form....

Traditional and Roth IRAs

Traditional and Roth IRAs Information Kit, Disclosure Statement and Custodial Agreement NOT FDIC INSURED \ NO BANK GUARANTEE \ MAY LOSE VALUE FRM-IRADISC(1/11) State Street Bank and Trust Company Universal

Traditional and Roth IRAs Information Kit, Disclosure Statement and Custodial Agreement NOT FDIC INSURED \ NO BANK GUARANTEE \ MAY LOSE VALUE FRM-IRADISC(1/11) State Street Bank and Trust Company Universal

Traditional and Roth IRAs. Invest for retirement with tax-advantaged accounts

Traditional and s Invest for retirement with tax-advantaged accounts Your Retirement It is your ultimate reward for a lifetime of hard work and dedication. It is a time when you should have the financial

Traditional and s Invest for retirement with tax-advantaged accounts Your Retirement It is your ultimate reward for a lifetime of hard work and dedication. It is a time when you should have the financial

Taxes and Transitions

Taxes and Transitions THE NEW FRONTIER FOR RETIREMENT PLANNING Wealthy individuals have been hit with their first major tax increase in more than 20 years, with tax hikes on ordinary income, dividends

Taxes and Transitions THE NEW FRONTIER FOR RETIREMENT PLANNING Wealthy individuals have been hit with their first major tax increase in more than 20 years, with tax hikes on ordinary income, dividends

Supplement to IRA Custodial Agreements

Supplement to IRA Custodial Agreements Effective December 31, 2014, the update below will be made to the American Century Custodial agreements for the following retirement accounts: Traditional IRAs, Roth

Supplement to IRA Custodial Agreements Effective December 31, 2014, the update below will be made to the American Century Custodial agreements for the following retirement accounts: Traditional IRAs, Roth

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE. Tax-advantaged IRAs. Invest in your retirement savings while reducing taxes

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Taxadvantaged IRAs Invest in your retirement savings while reducing taxes Find the answers inside Why invest for retirement? p. 1 Discover three good reasons

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Taxadvantaged IRAs Invest in your retirement savings while reducing taxes Find the answers inside Why invest for retirement? p. 1 Discover three good reasons

Tax Alpha. Robert S. Keebler, CPA, M.S.T., AEP. Keebler & Associates, LLP 420 South Washington Street Green Bay, WI 54301.

Tax Alpha Presented by Robert S. Keebler, CPA, M.S.T., AEP Keebler & Associates, LLP 420 South Washington Street Green Bay, WI 54301 Agenda 1. Five Dimensional Tax System Ordinary Income Rates Capital

Tax Alpha Presented by Robert S. Keebler, CPA, M.S.T., AEP Keebler & Associates, LLP 420 South Washington Street Green Bay, WI 54301 Agenda 1. Five Dimensional Tax System Ordinary Income Rates Capital

Preparing for Your Retirement: An IRA Review

Preparing for Your Retirement: An IRA Review How much of your earning power will be available for your use when you retire? What will happen to your standard of living when your income ceases at retirement?

Preparing for Your Retirement: An IRA Review How much of your earning power will be available for your use when you retire? What will happen to your standard of living when your income ceases at retirement?

Federal Tax and Capital Gains: Rates Over Time

Preparing for a World of Higher Taxes Are You Ready? Presented by: Matt Sommer, CFP, CPWA, AIF Director and Senior Retirement Specialist, Retirement Strategy Group C-0610-114 4-30-11 Federal Tax and Capital

Preparing for a World of Higher Taxes Are You Ready? Presented by: Matt Sommer, CFP, CPWA, AIF Director and Senior Retirement Specialist, Retirement Strategy Group C-0610-114 4-30-11 Federal Tax and Capital

2008-2012 $5,000 2013-2015 $5,500 Future years Increased by cost-of-living adjustments (in $500 increments)

") Part One of the Disclosure Statement describes the rules applicable to Traditional IRAs. IRAs described in these pages are called Traditional IRAs to distinguish them from the Roth IRAs, which are described

Part One of the Disclosure Statement describes the rules applicable to Traditional IRAs. IRAs described in these pages are called Traditional IRAs to distinguish them from the Roth IRAs, which are described

Q & A s about IRAs. Your promotional imprint here and/or back cover.

P l a n n i n g Y o u r R e t i r e m e n t Q & A s about IRAs Your promotional imprint here and/or back cover. ABC Company 123 Main Street Anywhere, USA 12345 www.sampleabccompany.com 1-800-123-4567 The

P l a n n i n g Y o u r R e t i r e m e n t Q & A s about IRAs Your promotional imprint here and/or back cover. ABC Company 123 Main Street Anywhere, USA 12345 www.sampleabccompany.com 1-800-123-4567 The

Distributions and Rollovers from

Page 1 of 6 Frequently Asked Questions about Distributions and Rollovers from Retirement Accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one

Page 1 of 6 Frequently Asked Questions about Distributions and Rollovers from Retirement Accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one

SHENANDOAH LIFE ANNUITIES

ANNUITIES AGENT GUIDE SHENANDOAH LIFE ANNUITIES FOR AGENT USE ONLY This piece is not intended to create public interest in an insurance product, an insurer, or an agent. SHENANDOAH LIFE ANNUITIES For

ANNUITIES AGENT GUIDE SHENANDOAH LIFE ANNUITIES FOR AGENT USE ONLY This piece is not intended to create public interest in an insurance product, an insurer, or an agent. SHENANDOAH LIFE ANNUITIES For

Roth IRAs and Conversions

Roth IRAs and Conversions When the law that created Roth IRAs was originally enacted there were two eligibility limits placed on them. The first affected an individual s ability to contribute to the Roth-

Roth IRAs and Conversions When the law that created Roth IRAs was originally enacted there were two eligibility limits placed on them. The first affected an individual s ability to contribute to the Roth-

NORTHEAST INVESTORS TRUST. 125 High Street Boston, MA 02110 Telephone: 800-225-6704

NORTHEAST INVESTORS TRUST traditional IRA INVESTOR S KIT 125 High Street Boston, MA 02110 Telephone: 800-225-6704 Table of Contents NORTHEAST INVESTORS TRUST TRADITIONAL IRA DISCLOSURE STATEMENT...1 INTRODUCTION...1

NORTHEAST INVESTORS TRUST traditional IRA INVESTOR S KIT 125 High Street Boston, MA 02110 Telephone: 800-225-6704 Table of Contents NORTHEAST INVESTORS TRUST TRADITIONAL IRA DISCLOSURE STATEMENT...1 INTRODUCTION...1

Caution: Special rules apply to certain distributions to reservists and national guardsmen called to active duty after September 11, 2001.

Thorsen Clark Tracey Wealth Management 301 East Pine Street Suite 1100 Orlando, FL 32801 407-246-8888 407-897-4427 thorsenclarktraceywealthmanagement@raymondjames.com tctwealthmanagement.com Roth IRAs

Thorsen Clark Tracey Wealth Management 301 East Pine Street Suite 1100 Orlando, FL 32801 407-246-8888 407-897-4427 thorsenclarktraceywealthmanagement@raymondjames.com tctwealthmanagement.com Roth IRAs

Retirement Plan Distributions Choices & Opportunities

Retirement Plan Distributions Choices & Opportunities Leaving Your Job: Things to Think About» What you want to do next Work full time? Part time? Retire? How much will your lifestyle cost?» Continuing

Retirement Plan Distributions Choices & Opportunities Leaving Your Job: Things to Think About» What you want to do next Work full time? Part time? Retire? How much will your lifestyle cost?» Continuing

Frequently asked questions

Page 1 of 6 Frequently asked questions Distributions and rollovers from retirement accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one of several

Page 1 of 6 Frequently asked questions Distributions and rollovers from retirement accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one of several

Questions and Answers about the Roth 401(k)

") THE RETIREMENT GROUP AT MERRILL LYNCH Q A Questions and Answers about the Roth 401(k) How the Roth 401(k) Works Q. What is the Roth 401(k) contribution option? A. The Roth 401(k) contribution option allows

THE RETIREMENT GROUP AT MERRILL LYNCH Q A Questions and Answers about the Roth 401(k) How the Roth 401(k) Works Q. What is the Roth 401(k) contribution option? A. The Roth 401(k) contribution option allows

Disclosure Statement and Custodial Agreement for Traditional or Roth Individual Retirement Accounts

ab Disclosure Statement and Custodial Agreement for Traditional or Roth Individual Retirement Accounts This booklet contains disclosures required by federal law. a Please keep this information for future

ab Disclosure Statement and Custodial Agreement for Traditional or Roth Individual Retirement Accounts This booklet contains disclosures required by federal law. a Please keep this information for future

Wealth Strategies. www.rfawealth.com. Saving For Retirement: Tax Deductible vs Roth Contributions. www.rfawealth.com

www.rfawealth.com Wealth Strategies Saving For Retirement: Tax Deductible vs Roth Contributions Part 2 of 12 Your Guide to Saving for Retirement WEALTH STRATEGIES Page 1 Saving For Retirement: Tax Deductible

www.rfawealth.com Wealth Strategies Saving For Retirement: Tax Deductible vs Roth Contributions Part 2 of 12 Your Guide to Saving for Retirement WEALTH STRATEGIES Page 1 Saving For Retirement: Tax Deductible

How much can I deduct if I am an active participant in a qualified plan?... 2

Table of Contents What is an Individual Retirement Account (IRA)?...................................... 1 Who may establish a Traditional IRA?............................................... 1 How much

Table of Contents What is an Individual Retirement Account (IRA)?...................................... 1 Who may establish a Traditional IRA?............................................... 1 How much

How Can a Traditional IRA Help Me Save For Retirement?

Learn About IRAs Traditional IRAs How can a Traditional IRA help me save for retirement? Who may contribute, and how much? What is a spousal contribution? What is a SEP Contribution? What is an IRA catch-up

Learn About IRAs Traditional IRAs How can a Traditional IRA help me save for retirement? Who may contribute, and how much? What is a spousal contribution? What is a SEP Contribution? What is an IRA catch-up

Part VII Individual Retirement Accounts

Part VII are a retirement planning tool that virtually everyone should consider. The new IRA options also have made selecting an IRA a bit more complicated. IRA Basics The Traditional IRA is an Individual

Part VII are a retirement planning tool that virtually everyone should consider. The new IRA options also have made selecting an IRA a bit more complicated. IRA Basics The Traditional IRA is an Individual

RETIREMENT ACCOUNTS. Alternative Retirement Financial Plans and Their Features

RETIREMENT ACCOUNTS The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial tax advantages that will typically have the

RETIREMENT ACCOUNTS The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial tax advantages that will typically have the

State Street Bank and Trust Company Universal Individual Retirement Account Information Kit

State Street Bank and Trust Company Universal Individual Retirement Account Information Kit The Federated Funds State Street Bank and Trust Company Universal Individual Retirement Custodial Account Instructions

State Street Bank and Trust Company Universal Individual Retirement Account Information Kit The Federated Funds State Street Bank and Trust Company Universal Individual Retirement Custodial Account Instructions

Leaving your employer? Options for your retirement plan

Leaving your employer? Options for your retirement plan Contents Evaluating your options 1 The benefits of tax-deferred investing 4 Flexibility offered by an IRA rollover 6 How to get started 9 Evaluating

Leaving your employer? Options for your retirement plan Contents Evaluating your options 1 The benefits of tax-deferred investing 4 Flexibility offered by an IRA rollover 6 How to get started 9 Evaluating

Important Information Morgan Stanley SIMPLE IRA Summary

SIMPLE IRA Summary September 2013 Important Information Morgan Stanley SIMPLE IRA Summary The following is intended to provide you with basic information on the roles and services that Morgan Stanley Smith

SIMPLE IRA Summary September 2013 Important Information Morgan Stanley SIMPLE IRA Summary The following is intended to provide you with basic information on the roles and services that Morgan Stanley Smith

Annuities. Introduction 2. What is an Annuity?... 2. How do they work?... 3. Types of Annuities... 4. Fixed vs. Variable annuities...

An Insider s Guide to Annuities Whatever your picture of retirement, the best way to get there and enjoy it once you ve arrived is with a focused, thoughtful plan. Introduction 2 What is an Annuity?...

An Insider s Guide to Annuities Whatever your picture of retirement, the best way to get there and enjoy it once you ve arrived is with a focused, thoughtful plan. Introduction 2 What is an Annuity?...

DISCLOSURE STATEMENT

DISCLOSURE STATEMENT for Individual Retirement Annuities Home Office: Wilmington, Delaware Administrative Office: P.O. Box 19032 Greenville, SC 29602-9032 Telephone 866-262-1161 The following information

DISCLOSURE STATEMENT for Individual Retirement Annuities Home Office: Wilmington, Delaware Administrative Office: P.O. Box 19032 Greenville, SC 29602-9032 Telephone 866-262-1161 The following information

Preparing Your Savings for Retirement

Preparing Your Savings for Retirement The Retirement Income Series Part 1: Preparing Your Savings for Retirement Identify sources of income, including Social Security Assess the impact of future health

Preparing Your Savings for Retirement The Retirement Income Series Part 1: Preparing Your Savings for Retirement Identify sources of income, including Social Security Assess the impact of future health

10 common IRA mistakes

10 common mistakes Help protect your valuable retirement assets Not FDIC Insured May Lose Value No Bank Guarantee Not Insured by Any Government Agency You ve worked hard to build your retirement assets......

10 common mistakes Help protect your valuable retirement assets Not FDIC Insured May Lose Value No Bank Guarantee Not Insured by Any Government Agency You ve worked hard to build your retirement assets......

Retirement Plans Guide Facts at a glance

Retirement Plans Guide Facts at a glance Contents 1 What s Your Plan? 2 Small Business/Employer Retirement Plans 4 IRAs 5 Retirement Plan Distributions 7 Rollovers and Transfers 8 Federal Tax Rates and

Retirement Plans Guide Facts at a glance Contents 1 What s Your Plan? 2 Small Business/Employer Retirement Plans 4 IRAs 5 Retirement Plan Distributions 7 Rollovers and Transfers 8 Federal Tax Rates and

A guide for managing your IRA inheritance. Maximize your inherited IRA and enhance your financial security.

A guide for managing your IRA inheritance Maximize your inherited IRA and enhance your financial security. Make the most of your inheritance by taking advantage of continued tax-deferred growth potential.

A guide for managing your IRA inheritance Maximize your inherited IRA and enhance your financial security. Make the most of your inheritance by taking advantage of continued tax-deferred growth potential.

IRA Opportunities. Traditional IRA vs. Roth IRA: Which is right for you? What kind of retirement funding vehicle is right for you?

IRA Opportunities. Traditional IRA vs. Roth IRA: Which is right for you? What kind of retirement funding vehicle is right for you? Now more than ever, an Individual Retirement Account (IRA) may help provide

IRA Opportunities. Traditional IRA vs. Roth IRA: Which is right for you? What kind of retirement funding vehicle is right for you? Now more than ever, an Individual Retirement Account (IRA) may help provide

Guide to Individual Retirement Accounts. Make a secure retirement yours

Guide to Individual Retirement Accounts Make a secure retirement yours Retirement means something different to everyone. Some dream of stopping employment completely and some want to continue working.

Guide to Individual Retirement Accounts Make a secure retirement yours Retirement means something different to everyone. Some dream of stopping employment completely and some want to continue working.

Making Retirement Assets Last a Lifetime PART 1

Making Retirement Assets Last a Lifetime PART 1 The importance of a solid exit strategy During the working years, accumulating assets for retirement is one of the primary goals of the investing population.

Making Retirement Assets Last a Lifetime PART 1 The importance of a solid exit strategy During the working years, accumulating assets for retirement is one of the primary goals of the investing population.

The Basics of Annuities: Income Beyond the Paycheck

The Basics of Annuities: PLANNING FOR INCOME NEEDS TABLE OF CONTENTS Income Beyond the Paycheck...1 The Facts of Retirement...2 What Is an Annuity?...2 What Type of Annuity Is Right for Me?...2 Payment

The Basics of Annuities: PLANNING FOR INCOME NEEDS TABLE OF CONTENTS Income Beyond the Paycheck...1 The Facts of Retirement...2 What Is an Annuity?...2 What Type of Annuity Is Right for Me?...2 Payment

The Basics of Annuities: Planning for Income Needs

March 2013 The Basics of Annuities: Planning for Income Needs summary the facts of retirement Earning income once your paychecks stop that is, after your retirement requires preparing for what s to come

March 2013 The Basics of Annuities: Planning for Income Needs summary the facts of retirement Earning income once your paychecks stop that is, after your retirement requires preparing for what s to come

Sample. Table of Contents. Introduction... 1. What is the difference between a regular 401(k) deferral (pre-tax) and a Roth 401(k) deferral?...

deferral (pre-tax) and a Roth 401(k) deferral?...") Table of Contents Introduction... 1 What is the difference between a regular 401(k) deferral (pre-tax) and a Roth 401(k) deferral?... 2 Who is eligible to make a Roth 401(k) deferral?... 3 Roth IRAs have

Table of Contents Introduction... 1 What is the difference between a regular 401(k) deferral (pre-tax) and a Roth 401(k) deferral?... 2 Who is eligible to make a Roth 401(k) deferral?... 3 Roth IRAs have

ROTH IRA REQUIREMENTS

Regarding Roth Individual Retirement Annuity (IRA) Plans Described in Section 408A of the Internal Revenue Code This Disclosure Statement ( Disclosure ) presents a general overview of the federal laws

Regarding Roth Individual Retirement Annuity (IRA) Plans Described in Section 408A of the Internal Revenue Code This Disclosure Statement ( Disclosure ) presents a general overview of the federal laws

RETIREMENT ACCOUNTS (c) Gary R. Evans, 2006-2011, September 24, 2011. Alternative Retirement Financial Plans and Their Features

Gary R. Evans, 2006-2011, September 24, 2011. Alternative Retirement Financial Plans and Their Features") RETIREMENT ACCOUNTS (c) Gary R. Evans, 2006-2011, September 24, 2011. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

RETIREMENT ACCOUNTS (c) Gary R. Evans, 2006-2011, September 24, 2011. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

Annual contributions: Conversion of a traditional IRA account: Rollovers from a qualified plan:

The Roth IRA differs from the traditional IRA in that contributions are never deductible and, if certain requirements are met, account distributions are free of federal income tax. 1 Annual contributions:

The Roth IRA differs from the traditional IRA in that contributions are never deductible and, if certain requirements are met, account distributions are free of federal income tax. 1 Annual contributions:

Retirement. A Guide to Roth IRAs

Retirement A Guide to Roth IRAs A Roth IRA is an individual retirement account named for the late Senate Finance Committee Chairman, William Roth, Jr. who championed the creation of this new type of IRA.

Retirement A Guide to Roth IRAs A Roth IRA is an individual retirement account named for the late Senate Finance Committee Chairman, William Roth, Jr. who championed the creation of this new type of IRA.

PERSONAL FINANCE. individual retirement accounts (IRAs)

") PERSONAL FINANCE individual retirement accounts (IRAs) 1 our mission To lead and inspire actions that improve financial readiness for the military and local community. table of contents The Basics Of IRAs...

PERSONAL FINANCE individual retirement accounts (IRAs) 1 our mission To lead and inspire actions that improve financial readiness for the military and local community. table of contents The Basics Of IRAs...

IRAs Traditional Individual Retirement Accounts. 2008 and 2009. Questions & Answers

IRAs Traditional Individual Retirement Accounts 2008 and 2009 Questions & Answers What is the purpose of this brochure? It summarizes the primary laws which govern traditional IRAs for 2008 and 2009. What

IRAs Traditional Individual Retirement Accounts 2008 and 2009 Questions & Answers What is the purpose of this brochure? It summarizes the primary laws which govern traditional IRAs for 2008 and 2009. What

Your Guide to Fixed Annuities

Your Guide to Fixed Annuities A Smart Choice for Safety Conscious Individuals Seeking Financial Security Protect Your Future Whether you re preparing for retirement or already enjoying retirement, a fixed

Your Guide to Fixed Annuities A Smart Choice for Safety Conscious Individuals Seeking Financial Security Protect Your Future Whether you re preparing for retirement or already enjoying retirement, a fixed

Roth IRAs. Funding a Roth IRA

The Roth IRA differs from the traditional IRA in that contributions are never deductible and, if certain requirements are met, account distributions are free of federal income tax. Funding a Roth IRA Annual

The Roth IRA differs from the traditional IRA in that contributions are never deductible and, if certain requirements are met, account distributions are free of federal income tax. Funding a Roth IRA Annual

Alternative Retirement Financial Plans and Their Features

RETIREMENT ACCOUNTS Gary R. Evans, 2006-2013, November 20, 2013. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

RETIREMENT ACCOUNTS Gary R. Evans, 2006-2013, November 20, 2013. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

2014 tax planning tables

2014 tax planning tables 2014 important deadlines Last day to January 15 Pay fourth-quarter 2013 federal individual estimated income tax January 27 Buy in to close a short-against-the-box position (regular-way

2014 tax planning tables 2014 important deadlines Last day to January 15 Pay fourth-quarter 2013 federal individual estimated income tax January 27 Buy in to close a short-against-the-box position (regular-way

8 Years Later, Same Old Questions: Evaluating Roth IRAs

8 Years Later, Same Old Questions: Evaluating Roth IRAs By Mark H. Gaudet, CPA, CFP The Taxpayer Relief Act of 1997 introduced a new type of IRA for taxpayers and investors the Roth IRA. Eight years have

8 Years Later, Same Old Questions: Evaluating Roth IRAs By Mark H. Gaudet, CPA, CFP The Taxpayer Relief Act of 1997 introduced a new type of IRA for taxpayers and investors the Roth IRA. Eight years have

How To Convert An Ira To A Roth Ira

Roth Conversion Frequently Asked Questions Brian Dobbis QPA, QKA, QPFC Retirement Analyst, Private Wealth Group 888-522-2388 A Roth individual retirement account (IRA) is a tax-deferred and potentially

Roth Conversion Frequently Asked Questions Brian Dobbis QPA, QKA, QPFC Retirement Analyst, Private Wealth Group 888-522-2388 A Roth individual retirement account (IRA) is a tax-deferred and potentially

ROTH IRA REQUIREMENTS

Regarding Roth Individual Retirement Annuity (IRA) Plans Described in Section 408A of the Internal Revenue Code This Disclosure Statement ( Disclosure ) presents a general overview of the federal laws

Regarding Roth Individual Retirement Annuity (IRA) Plans Described in Section 408A of the Internal Revenue Code This Disclosure Statement ( Disclosure ) presents a general overview of the federal laws

Preparing for Your Retirement: A Tax-Deferred Annuity (TDA) Review

Review") Preparing for Your Retirement: A Tax-Deferred Annuity (TDA) Review How much of your earning power will be available for your use when you retire? What will happen to your standard of living when your income

Preparing for Your Retirement: A Tax-Deferred Annuity (TDA) Review How much of your earning power will be available for your use when you retire? What will happen to your standard of living when your income

ira individual retirement accounts Traditional IRA

ira individual retirement accounts Traditional IRA Grow dollars for tomorrow, save on taxes today. A traditional IRA may provide you significant immediate tax savings, and due to the deferral of all taxes

ira individual retirement accounts Traditional IRA Grow dollars for tomorrow, save on taxes today. A traditional IRA may provide you significant immediate tax savings, and due to the deferral of all taxes

What You Need to Know About Roth IRA Conversions in 2010

What You Need to Know About Roth IRA Conversions in 2010 Your Guide to THE 2010 IRA Tax Law Changes From the editors at SmartMoney Custom Solutions Dear Reader, The year 2010 offers you an unprecedented

What You Need to Know About Roth IRA Conversions in 2010 Your Guide to THE 2010 IRA Tax Law Changes From the editors at SmartMoney Custom Solutions Dear Reader, The year 2010 offers you an unprecedented

Tax Strategies From a Financial Planning Perspective

Tax Strategies From a Financial Planning Perspective Spectrum Advisors Don Goerner offers securities through Purshe Kaplan Sterling Investments Member FINRA/ SIPC Headquartered at 18 Corporate Woods Blvd.,

Tax Strategies From a Financial Planning Perspective Spectrum Advisors Don Goerner offers securities through Purshe Kaplan Sterling Investments Member FINRA/ SIPC Headquartered at 18 Corporate Woods Blvd.,

Roth 401(k) Analyzer SM

Analyzer SM") Roth 401(k) Analyzer SM Supplemental Information Report Pre-tax or Roth 401(k)? Background Information Starting January 1, 2006, employers may add a new feature called a Roth 401(k) to their new or existing

Roth 401(k) Analyzer SM Supplemental Information Report Pre-tax or Roth 401(k)? Background Information Starting January 1, 2006, employers may add a new feature called a Roth 401(k) to their new or existing

Traditional and Roth IRAs. Invest for retirement with tax-advantaged accounts

Traditional and Roth IRAs Invest for retirement with tax-advantaged accounts Your Retirement It is your ultimate reward for a lifetime of hard work and dedication. It is a time when you should have the

Traditional and Roth IRAs Invest for retirement with tax-advantaged accounts Your Retirement It is your ultimate reward for a lifetime of hard work and dedication. It is a time when you should have the

TO ROTH OR NOT TO ROTH, THAT IS THE QUESTION

TO ROTH OR NOT TO ROTH, THAT IS THE QUESTION J. Scott Dillon Carruthers & Roth, P.A. 235 N. Edgeworth Street Greensboro, NC 27401 336.478.1119 jsd@crlaw.com OVERVIEW The Rules Roth IRA Roth 401(k) Roth

TO ROTH OR NOT TO ROTH, THAT IS THE QUESTION J. Scott Dillon Carruthers & Roth, P.A. 235 N. Edgeworth Street Greensboro, NC 27401 336.478.1119 jsd@crlaw.com OVERVIEW The Rules Roth IRA Roth 401(k) Roth

PRIVACY POLICIES, DISCLOSURES, INSTRUCTIONS & AGREEMENTS FOR: INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA

TRADITIONAL IRA SEP IRA ROTH IRA") Fairholme Funds Inc. PRIVACY POLICIES, DISCLOSURES, INSTRUCTIONS & AGREEMENTS FOR: INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA FAIRHOLME FUNDS, INC. INDIVIDUAL RETIREMENT ACCOUNT

Fairholme Funds Inc. PRIVACY POLICIES, DISCLOSURES, INSTRUCTIONS & AGREEMENTS FOR: INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA FAIRHOLME FUNDS, INC. INDIVIDUAL RETIREMENT ACCOUNT

Beginning in 2010, the Tax Increase Prevention and ROTH IRA CONVERSION

ROTH IRA CONVERSION Assessing Suitability of the Strategy for Individuals and their Heirs Executive Summary A Roth IRA conversion may benefit individuals during their retirement years by potentially reducing

ROTH IRA CONVERSION Assessing Suitability of the Strategy for Individuals and their Heirs Executive Summary A Roth IRA conversion may benefit individuals during their retirement years by potentially reducing

Maximize Retirement Income and Preserve Accumulated Wealth

Maximize Retirement Income and Preserve Accumulated Wealth Welcome! Steven M. Dalton, CFP 40 South River Road, Unit 15 Bedford, NH 03110 603-668-2303 Securities offered through Comprehensive Asset Management

Maximize Retirement Income and Preserve Accumulated Wealth Welcome! Steven M. Dalton, CFP 40 South River Road, Unit 15 Bedford, NH 03110 603-668-2303 Securities offered through Comprehensive Asset Management

AN ANALYSIS OF ROTH CONVERSIONS 1

AN ANALYSIS OF ROTH CONVERSIONS In 1997, Congress introduced the Roth IRA, giving investors a new product for retirement savings. The Roth IRA is essentially a mirror image of the Traditional IRA, but

AN ANALYSIS OF ROTH CONVERSIONS In 1997, Congress introduced the Roth IRA, giving investors a new product for retirement savings. The Roth IRA is essentially a mirror image of the Traditional IRA, but

IRAs. AKD Consultants Adam Dworkin CPA 188 Whiting Street Suite 10 Hingham, MA 02043 781-556-5554 Adam@AKDConsultants.com

AKD Consultants Adam Dworkin CPA 188 Whiting Street Suite 10 Hingham, MA 02043 781-556-5554 Adam@AKDConsultants.com IRAs October 01, 2013 Page 1 of 8, see disclaimer on final page Both traditional and

AKD Consultants Adam Dworkin CPA 188 Whiting Street Suite 10 Hingham, MA 02043 781-556-5554 Adam@AKDConsultants.com IRAs October 01, 2013 Page 1 of 8, see disclaimer on final page Both traditional and

Understanding annuities

ab Wealth Management Americas Understanding annuities Rethinking the role they play in retirement income planning Protecting your retirement income security from life s uncertainties. The retirement landscape

ab Wealth Management Americas Understanding annuities Rethinking the role they play in retirement income planning Protecting your retirement income security from life s uncertainties. The retirement landscape

IRAs Traditional Individual Retirement Accounts. 2014 and 2015. Questions & Answers

IRAs Traditional Individual Retirement Accounts 2014 and 2015 Questions & Answers What is the purpose of this brochure? It summarizes the primary laws governing traditional IRAs for 2014 and 2015. What

IRAs Traditional Individual Retirement Accounts 2014 and 2015 Questions & Answers What is the purpose of this brochure? It summarizes the primary laws governing traditional IRAs for 2014 and 2015. What

IRAs Traditional Individual Retirement Accounts. 2013 and 2014. Questions & Answers

IRAs Traditional Individual Retirement Accounts 2013 and 2014 Questions & Answers What is the purpose of this brochure? It summarizes the primary laws governing traditional IRAs for 2013 and 2014. What

IRAs Traditional Individual Retirement Accounts 2013 and 2014 Questions & Answers What is the purpose of this brochure? It summarizes the primary laws governing traditional IRAs for 2013 and 2014. What

IRAs: Four Facts You Should Know

IRAs: Four Facts You Should Know Overview: The decision between contributing to a traditional 2007 IRA and a Roth IRA depends on many factors. The following discusses some of the key concepts to consider

IRAs: Four Facts You Should Know Overview: The decision between contributing to a traditional 2007 IRA and a Roth IRA depends on many factors. The following discusses some of the key concepts to consider

16. Individual Retirement Accounts

16. Individual Retirement Accounts Introduction Through enactment of the Employee Retirement Income Security Act of 1974 (ERISA), Congress established individual retirement accounts (IRAs) to provide workers

16. Individual Retirement Accounts Introduction Through enactment of the Employee Retirement Income Security Act of 1974 (ERISA), Congress established individual retirement accounts (IRAs) to provide workers

2016 Tax Planning & Reference Guide

2016 Tax Planning & Reference Guide The 2016 Tax Planning & Reference Guide is designed as a reference and is not intended to function as tax advice. Please consult your professional accounting advisor

2016 Tax Planning & Reference Guide The 2016 Tax Planning & Reference Guide is designed as a reference and is not intended to function as tax advice. Please consult your professional accounting advisor

Retirement Savings Vehicles

Retirement Savings Retirement Savings If you ask yourself why it s important to invest, one of the answers may well be a comfortable retirement. To ensure your retirement matches or comes close to the

Retirement Savings Retirement Savings If you ask yourself why it s important to invest, one of the answers may well be a comfortable retirement. To ensure your retirement matches or comes close to the

the t. rowe price Guide for IRA and 403(b) Account Beneficiaries

Account Beneficiaries") the t. rowe price Guide for IRA and 403(b) Account Beneficiaries who should use this guide T. Rowe Price retirement specialists have designed this guide for: 1 : Individuals who are beneficiaries of the

the t. rowe price Guide for IRA and 403(b) Account Beneficiaries who should use this guide T. Rowe Price retirement specialists have designed this guide for: 1 : Individuals who are beneficiaries of the

December 2014. Tax-Efficient Investing Through Asset Location. John Wyckoff, CPA/PFS, CFP

John Wyckoff, CPA/PFS, CFP Your investment priorities are likely to evolve over time, but one goal will remain constant: to maximize your investment returns. Not all returns are created equal, however.

John Wyckoff, CPA/PFS, CFP Your investment priorities are likely to evolve over time, but one goal will remain constant: to maximize your investment returns. Not all returns are created equal, however.

SCHNEIDER FUNDS INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA

TRADITIONAL IRA SEP IRA ROTH IRA") SCHNEIDER FUNDS INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA)

SCHNEIDER FUNDS INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA)

Variable Annuities. Reno J. Frazzitta Investment Advisor Representative 877-909-7233 www.thesmartmoneyguy.com

Reno J. Frazzitta Investment Advisor Representative 877-909-7233 www.thesmartmoneyguy.com Variable Annuities Page 1 of 8, see disclaimer on final page Variable Annuities What is a variable annuity? Investor

Reno J. Frazzitta Investment Advisor Representative 877-909-7233 www.thesmartmoneyguy.com Variable Annuities Page 1 of 8, see disclaimer on final page Variable Annuities What is a variable annuity? Investor

Understanding Annuities: A Lesson in Annuities

Understanding Annuities: A Lesson in Annuities Did you know that an annuity can be used to systematically accumulate money for retirement purposes, as well as to guarantee a retirement income that you

Understanding Annuities: A Lesson in Annuities Did you know that an annuity can be used to systematically accumulate money for retirement purposes, as well as to guarantee a retirement income that you

OPTION SELECT ROTH IRA DISCLOSURE STATEMENT

OPTION SELECT ROTH IRA DISCLOSURE STATEMENT Group Policy Form No. 01-1115-98 Group Certificate Form No. 01-1115C-98 and state variations thereof. Not for use in Florida. Regarding Roth Individual Retirement

OPTION SELECT ROTH IRA DISCLOSURE STATEMENT Group Policy Form No. 01-1115-98 Group Certificate Form No. 01-1115C-98 and state variations thereof. Not for use in Florida. Regarding Roth Individual Retirement

Howard 457 Deemed IRA Participation Agreement for Deferred Compensation Plan

Howard 457 Deemed IRA Participation Agreement for Deferred Compensation Plan DC-4803 (09/2015) For help, please call 1-877-677-3678 www.howard457.com 1 2 DC-4803 (09/2015) For help, please call 1-877-677-3678

Howard 457 Deemed IRA Participation Agreement for Deferred Compensation Plan DC-4803 (09/2015) For help, please call 1-877-677-3678 www.howard457.com 1 2 DC-4803 (09/2015) For help, please call 1-877-677-3678

Retirement: Time to Enjoy Your Rewards

Retirement: Time to Enjoy Your Rewards New York Life Guaranteed Lifetime Income Annuity The Company You Keep Some people generate retirement income by withdrawing money from their savings as they need

Retirement: Time to Enjoy Your Rewards New York Life Guaranteed Lifetime Income Annuity The Company You Keep Some people generate retirement income by withdrawing money from their savings as they need

IMPORTANT INFORMATION ABOUT ROTH CONTRIBUTIONS

IMPORTANT INFORMATION ABOUT ROTH CONTRIBUTIONS What is a Roth 401(k)? Is it a new type of plan? No, it is not a new type of plan. Designated Roth contributions are a type of contribution that new or existing

IMPORTANT INFORMATION ABOUT ROTH CONTRIBUTIONS What is a Roth 401(k)? Is it a new type of plan? No, it is not a new type of plan. Designated Roth contributions are a type of contribution that new or existing

The Roth IRA. An IRA with a difference. Is it right for you?

The Roth IRA An IRA with a difference Is it right for you? The Roth IRA An IRA with a difference The original IRA was designed to help individuals plan for their retirement by enabling them to make tax-deductible

The Roth IRA An IRA with a difference Is it right for you? The Roth IRA An IRA with a difference The original IRA was designed to help individuals plan for their retirement by enabling them to make tax-deductible

G U A R A N T E E D I N C O M E S O L U T I O N S NEW YORK LIFE LIFETIME INCOME ANNUITY

G U A R A N T E E D I N C O M E S O L U T I O N S NEW YORK LIFE LIFETIME INCOME ANNUITY NEW YORK LIFE: BUILT FOR TIMES LIKE THESE New York Life Insurance Company, the parent company of New York Life Insurance

G U A R A N T E E D I N C O M E S O L U T I O N S NEW YORK LIFE LIFETIME INCOME ANNUITY NEW YORK LIFE: BUILT FOR TIMES LIKE THESE New York Life Insurance Company, the parent company of New York Life Insurance

The IBM 401(k) Plus Plan. Invest today for what you hope to accomplish tomorrow

Plus Plan. Invest today for what you hope to accomplish tomorrow") The IBM 401(k) Plus Plan Invest today for what you hope to accomplish tomorrow The IBM 401(k) Plus Plan Dollar-for-dollar company match, automatic company contributions, broad range of investment options

The IBM 401(k) Plus Plan Invest today for what you hope to accomplish tomorrow The IBM 401(k) Plus Plan Dollar-for-dollar company match, automatic company contributions, broad range of investment options

Overview. Retirement Plan

Overview Retirement Plan Retirement Plan 74 Regardless of your age, the time for thinking about retirement is now. With careful planning, you can help make your retirement years a more comfortable and

Overview Retirement Plan Retirement Plan 74 Regardless of your age, the time for thinking about retirement is now. With careful planning, you can help make your retirement years a more comfortable and

Traditional IRA and Roth IRA

Traditional IRA and Roth IRA Plan Today for a Secure Tomorrow lord abbett retirement services Bring an Unwavering Commitment to Your Retirement Plan Founded in 1929, Lord Abbett is an independent, privately

Traditional IRA and Roth IRA Plan Today for a Secure Tomorrow lord abbett retirement services Bring an Unwavering Commitment to Your Retirement Plan Founded in 1929, Lord Abbett is an independent, privately