Item 4a July 23, 2014

|

|

|

- Horatio Wilkins

- 10 years ago

- Views:

Transcription

loan program?")

1 Item 4a July 23, 2014 Energy Commission ACTION CALENDAR July 23, 2014 To: From: Subject: Berkeley Energy Commission Neal De Snoo, Commission Secretary Property Assessed Clean Energy Loans ISSUE FOR CONSIDERATION Should the City Council authorize the HERO Property Assessed Clean Energy (PACE) loan program? FISCAL IMPACTS The financial impacts to the City would be relatively small and will be limited to existing staff time to post information about the program on the City s website and monitor uptake. CURRENT SITUATION AND ITS EFFECTS On May 1, 2014, the Federal Housing Finance Agency (FHFA) reiterated its 2010 position that PACE loans present a risk to mortgage lenders and its prohibition against Fannie Mac and Freddie Mae purchasing or refinancing mortgages with senior PACE loans. Fannie Mae and Freddie Mac underwrite conforming loans, i.e., non-jumbo loans. There are at least four residential PACE loan programs in California, including the CaliforniaFIRST program, which Council authorized in 2010 and the HERO program, which Council referred to staff to consider for authorization. No residential PACE loans have been issued in Berkeley since the FHFA stated its position on PACE loans in BACKGROUND PACE programs provide financing for renewable energy installations, energy and water efficiency improvements and electric vehicle charging infrastructure on private properties. Property owners repay the cost of the financing on their property tax bills. In 2010, the FHFA issued a statement directing Fannie Mae and Freddie Mac to take actions that would place restrictions on mortgages for properties with PACE loans. Fannie Mae and Freddie Mac are quasi-public entities that underwrite conforming residential mortgages. Such conforming loans range from $625,500 for a one unit building to $1,202,925 for a four-unit building. Loans in excess of this amount, i.e., jumbo loans, are not subject to Fannie Mae and Freddie Mac underwriting rules Milvia Street, Berkeley, CA Tel: (510) TDD: (510) Fax: (510) [email protected] Website:

reiterated its 2010 position that PACE loans present a risk to mortgage lenders and its prohibition against")

2 Property Assessed Clean Energy Loans Item 4a July 23, 2014 The actions that the FHFA directed include requiring PACE loans be paid off prior to sale or refinancing, requiring mortgage holders to obtain approval before assuming a PACE loan, and adjusting loan-to-value ratios and tightening debt-to-income ratios in jurisdictions that authorize PACE. The actions would have greater effects on affordable housing, which more commonly participate in conforming loans. The implications are summarized below. A PACE client could be required to pay off the PACE loan prior to refinancing. This is now in practice, but not always enforced. A mortgagee who obtained a PACE loan without approval from their mortgage company could be held in default of their loan and required to repay it immediately. There are no known instances of this happening. All conforming loans within a community that authorizes PACE loans would be subject to more restrictive terms the community could be redlined. There are no known instances of this happening. Staff is not aware of lenders calling an existing loan in default or of redlining a community because of PACE. To date, the only action taken by lenders has been to require that PACE loans be paid upon sale or refinancing existing mortgages and both the CaliforniaFIRST and HERO programs include disclosures to this effect. In an attempt to protect PACE borrowers and PACE communities, the State of California established the Property Assessed Clean Energy (PACE) Loss Reserve Program. The new reserve will underwrite residential loans from participating PACE providers with a.25% fee on new PACE loans. The Program would compensate first mortgage lenders for losses attributable to PACE loans. The establishment of the program resulted in a decision by the California Statewide Communities Development Authority (CSCDA) to reestablish the California FIRST residential PACE program, which is already authorized to serve Berkeley ( FHFA Secretary Mel Watt stated in a May 1, 2014 letter that the loss reserve program fails to offer loss protection to Fannie Mae and Freddie Mac and that the FHFA will continue to prohibit the Enterprises [Fannie Mae and Freddie Mac] from purchasing or refinancing mortgages that are encumbered with first-lien PACE loans. The letter did not reference the other sanctions mentioned in the 2010 statement. Similarly, in August 2013, the FHFA sent a letter to the City of San Diego stating that it had directed lenders not to purchase original loans or re-finance loans secured by properties that have a first lien PACE obligation attached. Again, the letter makes no reference to the other sanctions mentioned in the 2010 statement. Given the FHFA s recent communications, it appears that the agency is signaling that it would not impose sanctions other than requiring that PACE loans be repaid upon sale or refinancing.

3 Property Assessed Clean Energy Loans Item 4a July 23, 2014 Other PACE programs, including the HERO program, have been in operation since the FHFA s original statement was issued and have no plans to discontinue. HERO and CaliforniaFIRST are governed by joint powers authorities established by public agencies. There are other private companies offering PACE loans as well. ENVIRONMENTAL SUSTAINABILITY Participation in PACE programs directly supports the City s climate action goals by stimulating investments that will reduce carbon emissions and reduce water consumption. RATIONALE FOR RECOMMENDATION Current FHFA practices and recent FHFA communications lead to the conclusion that the risks to existing mortgage holders are known and manageable. Nevertheless, it is important to consider that the FHFA has the authority to impose more severe sanctions and that these risks would apply to lower value conforming loans and could disproportionately affect moderate and low-income households. The benefits, meanwhile are significant and could provide much needed capital for residential improvements, reduce community energy costs and greenhouse gas emissions and stimulate employment. ALTERNATIVE ACTIONS CONSIDERED The City could authorize the HERO program. The City could also authorize the privately administered PACE programs. However, unlike the California FIRST and HERO programs, there is no direct public oversight of these programs. Or, the existing CaliforniaPACE program could be deauthorized. Attachments: 1: FHFA Letter to Governor Brown, May 1, : FHFA Letter to the City of San Diego, July 24, : FHFA Statement on Certain Energy Retrofit Loans, July 6, 2010

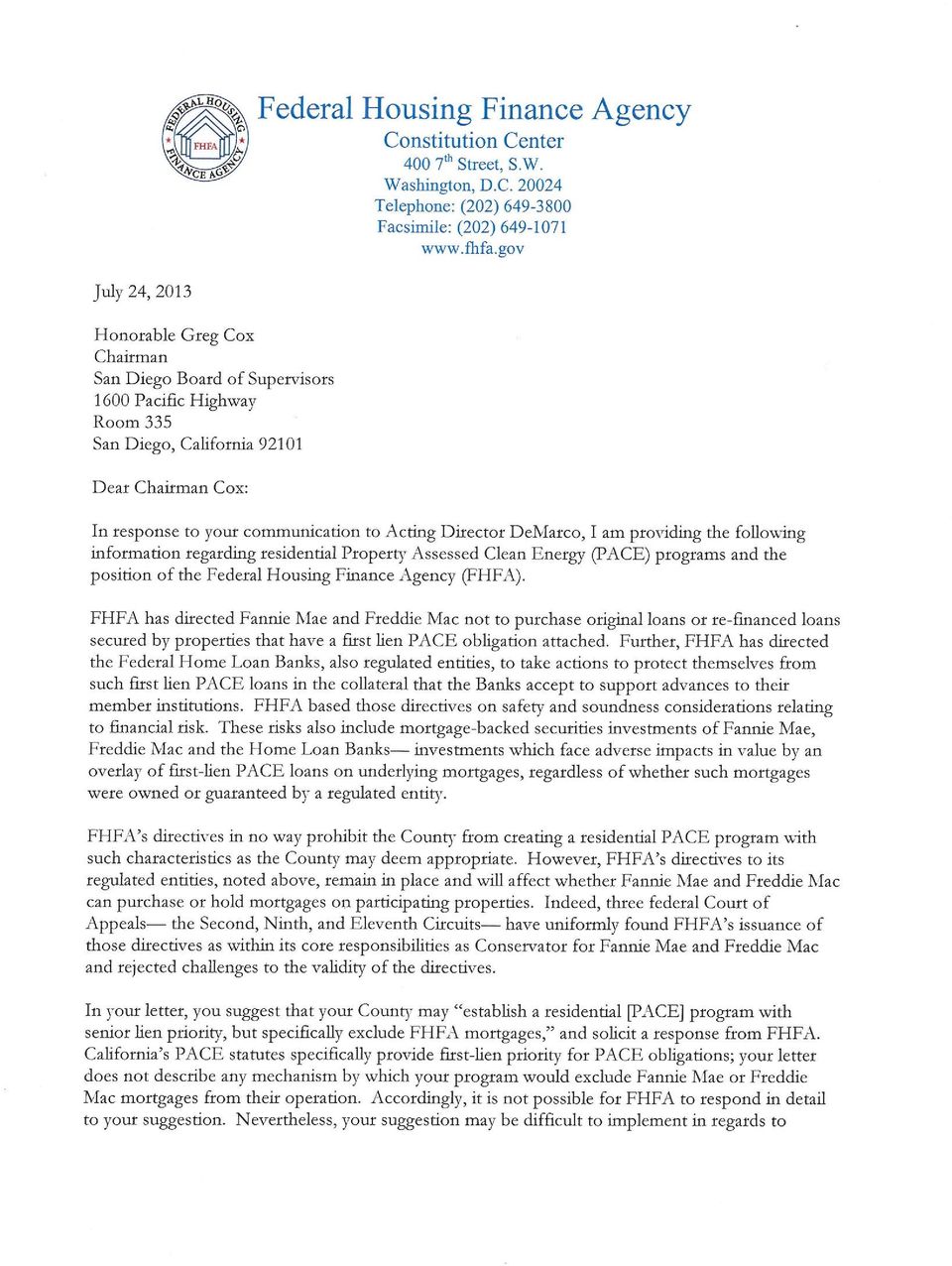

4 FEDERAL HOUSING FINANCE AGENCY Office of the Director May 1, 2014 The Honorable Edmund G. Brown Jr. Governor, State of California State Capitol Sacramento, CA RE: California Property Assessed Clean Energy Program Dear Governor Brown: Thank you for your letter of April 28,2014 about California's Property Assessed Clean Energy (PACE) program. The Federal Housing Finance Agency's (FHFA) General Counsel has been in touch with your staff, and I appreciate the time and materials they have provided concerning California's PACE program and intentions in creating the Reserve Fund. I am writing to inform you that FHFA is not prepared to change its position on California's first-lien PACE program and will continue to prohibit the Enterprises from purchasing or refinancing mortgages that are encumbered with first-lien PACE loans. California's PACE program would allow local governments to finance energy-related home improvement projects by placing an assessment on a homeowner's property in a first lien position, resulting in the subordination of an existing Enterprisebacked mortgage to a second lien position. The effect of this is to increase the risks and possibility of losses to the Enterprises. Additionally, because these loans run with the land, the ongoing monthly assessments for PACE loans are passed on to any subsequent property owners - including after a foreclosure or other distressed sale - unless fully paid off beforehand. In making this determination, FHFA has carefully reviewed the Reserve Fund created by the State of California and, while I appreciate that it is intended to mitigate these increased losses, it fails to offer full loss protection to the Enterprises. The Reserve Fund is not an adequate substitute for Enterprise mortgages maintaining a first lien position and FHFA also has concerns about the Reserve Fund's ongoing sustainability. Should you wish to discuss this matter further, I would be happy to discuss alternatives to first-lien PACE programs with you. Melvin L. Watt xc: The Honorable Barbara Boxer The Honorable Zoe Lofgren 400 7th Street, S.W., Washington, D.C (fax)

General Counsel has been in touch with your staff, and I appreciate the time and materials they have provided concerning California's PACE program and")

5

6

7 FEDERAL HOUSING FINANCE AGENCY STATEMENT For Immediate Release Contact: Corinne Russell (202) July 6, 2010 Stefanie Mullin (202) FHFA Statement on Certain Energy Retrofit Loan Programs After careful review and over a year of working with federal and state government agencies, the Federal Housing Finance Agency (FHFA) has determined that certain energy retrofit lending programs present significant safety and soundness concerns that must be addressed by Fannie Mae, Freddie Mac and the Federal Home Loan Banks. Specifically, programs denominated as Property Assessed Clean Energy (PACE) seek to foster lending for retrofits of residential or commercial properties through a county or city s tax assessment regime. Under most of these programs, such loans acquire a priority lien over existing mortgages, though certain states have chosen not to adopt such priority positions for their loans. First liens established by PACE loans are unlike routine tax assessments and pose unusual and difficult risk management challenges for lenders, servicers and mortgage securities investors. The size and duration of PACE loans exceed typical local tax programs and do not have the traditional community benefits associated with taxing initiatives. FHFA urged state and local governments to reconsider these programs and continues to call for a pause in such programs so concerns can be addressed. First liens for such loans represent a key alteration of traditional mortgage lending practice. They present significant risk to lenders and secondary market entities, may alter valuations for mortgage-backed securities and are not essential for successful programs to spur energy conservation. While the first lien position offered in most PACE programs minimizes credit risk for investors funding the programs, it alters traditional lending priorities. Underwriting for PACE programs results in collateral-based lending rather than lending based upon ability-to-pay, the absence of Truth-in-Lending Act and other consumer protections, and uncertainty as to whether the home improvements actually produce meaningful reductions in energy consumption. Efforts are just underway to develop underwriting and consumer protection standards as well as energy retrofit standards that are critical for homeowners and lenders to understand the risks and rewards of any energy retrofit lending program. However, first liens that disrupt a fragile housing finance market and long-standing lending priorities, the absence of robust underwriting standards to protect homeowners and the lack of energy retrofit standards to assist homeowners, appraisers, inspectors and lenders determine the value of retrofit products combine to raise safety and soundness concerns.

seek to foster lending for retrofits of residential or commercial properties through a county or city s tax assessment")

8 On May 5, 2010, Fannie Mae and Freddie Mac alerted their seller-servicers to gain an understanding of whether there are existing or prospective PACE or PACE-like programs in jurisdictions where they do business, to be aware that programs with first liens run contrary to the Fannie Mae-Freddie Mac Uniform Security Instrument and that the Enterprises would provide additional guidance should the programs move beyond the experimental stage. Those lender letters remain in effect. Today, FHFA is directing Fannie Mae, Freddie Mac and the Federal Home Loan Banks to undertake the following prudential actions: 1. For any homeowner who obtained a PACE or PACE-like loan with a priority first lien prior to this date, FHFA is directing Fannie Mae and Freddie Mac to waive their Uniform Security Instrument prohibitions against such senior liens. 2. In addressing PACE programs with first liens, Fannie Mae and Freddie Mac should undertake actions that protect their safe and sound operations. These include, but are not limited to: - Adjusting loan-to-value ratios to reflect the maximum permissible PACE loan amount available to borrowers in PACE jurisdictions; - Ensuring that loan covenants require approval/consent for any PACE loan; - Tightening borrower debt-to-income ratios to account for additional obligations associated with possible future PACE loans; - Ensuring that mortgages on properties in a jurisdiction offering PACE-like programs satisfy all applicable federal and state lending regulations and guidance. Fannie Mae and Freddie Mac should issue additional guidance as needed. 3. The Federal Home Loan Banks are directed to review their collateral policies in order to assure that pledged collateral is not adversely affected by energy retrofit programs that include first liens. Nothing in this Statement affects the normal underwriting programs of the regulated entities or their dealings with PACE programs that do not have a senior lien priority. Further, nothing in these directions to the regulated entities affects in any way underwriting related to traditional tax programs, but is focused solely on senior lien PACE lending initiatives. FHFA recognizes that PACE and PACE-like programs pose additional lending challenges, but also represent serious efforts to reduce energy consumption. FHFA remains committed to working with federal, state, and local government agencies to develop and implement energy retrofit lending programs with appropriate underwriting guidelines and consumer protection standards. FHFA will also continue to encourage the establishment of energy efficiency standards to support such programs. ### The Federal Housing Finance Agency regulates Fannie Mae, Freddie Mac and the 12 Federal Home Loan Banks. These government-sponsored enterprises provide more than $5.9 trillion in funding for the U.S. mortgage markets and financial institutions.

PACE and the Federal Housing Finance Agency (FHFA)

") MARCH 17, 2010 PACE and the Federal Housing Finance Agency (FHFA) By Mark Zimring and Merrian Fuller The FHFA regulates Fannie Mae, Freddie Mac, and the 12 Federal Home Loan Banks (the government-sponsored

MARCH 17, 2010 PACE and the Federal Housing Finance Agency (FHFA) By Mark Zimring and Merrian Fuller The FHFA regulates Fannie Mae, Freddie Mac, and the 12 Federal Home Loan Banks (the government-sponsored

Summary of the Housing and Economic Recovery Act of 2008

Summary of the Housing and Economic Recovery Act of 2008 On July 30, President Bush signed major housing legislation, HR 3221, the Housing and Economic Recovery Act of 2008. The bill restructures regulation

Summary of the Housing and Economic Recovery Act of 2008 On July 30, President Bush signed major housing legislation, HR 3221, the Housing and Economic Recovery Act of 2008. The bill restructures regulation

Chapter 13: Residential and Commercial Property Financing

Chapter 13 Outline / Page 1 Chapter 13: Residential and Commercial Property Financing Understanding the Mortgage Concept - secured vs. unsecured debt - mortgage pledge of property to secure a debt (See

Chapter 13 Outline / Page 1 Chapter 13: Residential and Commercial Property Financing Understanding the Mortgage Concept - secured vs. unsecured debt - mortgage pledge of property to secure a debt (See

S. 3085 Responsible Homeowner Refinancing Act of 2012

CONGRESSIONAL BUDGET OFFICE COST ESTIMATE August 24, 2012 S. 3085 Responsible Homeowner Refinancing Act of 2012 As introduced in the United States Senate on May 10, 2012 SUMMARY The Home Affordable Refinance

CONGRESSIONAL BUDGET OFFICE COST ESTIMATE August 24, 2012 S. 3085 Responsible Homeowner Refinancing Act of 2012 As introduced in the United States Senate on May 10, 2012 SUMMARY The Home Affordable Refinance

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Appendix A: Description of the Data

Appendix A: Description of the Data This data release presents information by year of origination on the dollar amounts, loan counts, and delinquency experience through year-end 2009 of single-family mortgages

Appendix A: Description of the Data This data release presents information by year of origination on the dollar amounts, loan counts, and delinquency experience through year-end 2009 of single-family mortgages

About Northwest Counseling Service

About Northwest Counseling Service Non Profit Agency No Cost Housing Counseling Services Any Service Related To A Home Specialize In Mortgage Delinquency 96% Rate In Keeping Residents In Homes HUD Certified/OHCD

About Northwest Counseling Service Non Profit Agency No Cost Housing Counseling Services Any Service Related To A Home Specialize In Mortgage Delinquency 96% Rate In Keeping Residents In Homes HUD Certified/OHCD

GLOSSARY COMMONLY USED REAL ESTATE TERMS

GLOSSARY COMMONLY USED REAL ESTATE TERMS Adjustable-Rate Mortgage (ARM): a mortgage loan with an interest rate that is subject to change and is not fixed at the same level for the life of the loan. These

GLOSSARY COMMONLY USED REAL ESTATE TERMS Adjustable-Rate Mortgage (ARM): a mortgage loan with an interest rate that is subject to change and is not fixed at the same level for the life of the loan. These

Homeowners Protection Act. I. Background

Homeowners Protection Act I. Background The Homeowners Protection Act of 1998 (the Act) was signed into law on July 29, 1998, and became effective on July 29, 1999. The Act was amended on December 27,

Homeowners Protection Act I. Background The Homeowners Protection Act of 1998 (the Act) was signed into law on July 29, 1998, and became effective on July 29, 1999. The Act was amended on December 27,

PACE LIENS AND SOLAR LEASES. PACE and Solar Liens. PACE-What is it 8/4/2015. Two Methods for Homeowners to Achieve Dual Goals

PACE LIENS AND SOLAR LEASES August 4, 2015 Sanjay Wagle, Senior Counsel Copyright 2015CALIFORNIAASSOCIATION OF REALTORS (C.A.R.). Permission is granted to C.A.R. members only to reproduce and use this

PACE LIENS AND SOLAR LEASES August 4, 2015 Sanjay Wagle, Senior Counsel Copyright 2015CALIFORNIAASSOCIATION OF REALTORS (C.A.R.). Permission is granted to C.A.R. members only to reproduce and use this

Financing Residential Real Estate

Financing Residential Real Estate Chapter 1: Finance and Investment Borrowing Money to Buy a Home Investments and Returns Types of Investments Ownership Investments Debt Investments Securities Investment

Financing Residential Real Estate Chapter 1: Finance and Investment Borrowing Money to Buy a Home Investments and Returns Types of Investments Ownership Investments Debt Investments Securities Investment

TITLE I-RESIDENTIAL MORTGAGE LOAN ORIGINATION STANDARDS

TITLE I-RESIDENTIAL MORTGAGE LOAN ORIGINATION STANDARDS Residential Mortgage Origination: Adds a number of new regulations and requirements to mortgage loan originators. The bill requires originators to

TITLE I-RESIDENTIAL MORTGAGE LOAN ORIGINATION STANDARDS Residential Mortgage Origination: Adds a number of new regulations and requirements to mortgage loan originators. The bill requires originators to

CALIFORNIA ALTERNATIVE ENERGY AND ADVANCED TRANSPORTATION FINANCING AUTHORITY Meeting Date: February 18, 2014

CALIFORNIA ALTERNATIVE ENERGY AND ADVANCED TRANSPORTATION FINANCING AUTHORITY Meeting Date: February 18, 2014 Request to Consider and Approve Emergency Regulations for the Property Assessed Clean Energy

CALIFORNIA ALTERNATIVE ENERGY AND ADVANCED TRANSPORTATION FINANCING AUTHORITY Meeting Date: February 18, 2014 Request to Consider and Approve Emergency Regulations for the Property Assessed Clean Energy

V 5.1. V. Lending HOPA. Homeowners Protection Act. Regulation Overview. Introduction

Homeowners Protection Act Introduction The Homeowners Protection Act of 1998 (the Act) was signed into law on July 29, 1998, and became effective on July 29, 1999. The Act was amended on December 27, 2000,

Homeowners Protection Act Introduction The Homeowners Protection Act of 1998 (the Act) was signed into law on July 29, 1998, and became effective on July 29, 1999. The Act was amended on December 27, 2000,

V600 Introduction to Mortgage Lending. Robin J Wybenga, CFO, TBA Credit Union [email protected] 231.946.7090

V600 Introduction to Mortgage Lending Robin J Wybenga, CFO, TBA Credit Union [email protected] 231.946.7090 Introduction Objectives 1. Identify the key benefits your CU gains by offering real estate lending

V600 Introduction to Mortgage Lending Robin J Wybenga, CFO, TBA Credit Union [email protected] 231.946.7090 Introduction Objectives 1. Identify the key benefits your CU gains by offering real estate lending

Title XIV - Mortgage Reform and Anti-Predatory Lending Act. Short title: "Mortgage Reform and Anti-Predatory Lending Act"

Title XIV - Mortgage Reform and Anti-Predatory Lending Act Short title: "Mortgage Reform and Anti-Predatory Lending Act" Subtitles A, B, C, and E are designated as Enumerated Consumer Law under the Bureau

Title XIV - Mortgage Reform and Anti-Predatory Lending Act Short title: "Mortgage Reform and Anti-Predatory Lending Act" Subtitles A, B, C, and E are designated as Enumerated Consumer Law under the Bureau

Section 1715z-20. Insurance of home equity conversion mortgages for elderly homeowners 1

Section 1715z-20. Insurance of home equity conversion mortgages for elderly homeowners 1 (a) Purpose The purpose of this section is to authorize the Secretary to carry out a program of mortgage insurance

Section 1715z-20. Insurance of home equity conversion mortgages for elderly homeowners 1 (a) Purpose The purpose of this section is to authorize the Secretary to carry out a program of mortgage insurance

Financing Residential Real Estate: SAFE Comprehensive 20 Hours

Financing Residential Real Estate: SAFE Comprehensive 20 Hours COURSE ORGANIZATION and DESIGN Roy L. Ponthier, Ph.D., Ed.D., CDEI, DREI Executive Director Module 1: Finance and Investment Mortgage loans

Financing Residential Real Estate: SAFE Comprehensive 20 Hours COURSE ORGANIZATION and DESIGN Roy L. Ponthier, Ph.D., Ed.D., CDEI, DREI Executive Director Module 1: Finance and Investment Mortgage loans

Lender Letter 07-2009 September 18, 2009. To: All Fannie Mae Single-Family Sellers and Servicers

Lender Letter 07-2009 September 18, 2009 To: All Fannie Mae Single-Family Sellers and Servicers Energy Loan Tax Assessment Programs Introduction Fannie Mae has recently received questions from lenders

Lender Letter 07-2009 September 18, 2009 To: All Fannie Mae Single-Family Sellers and Servicers Energy Loan Tax Assessment Programs Introduction Fannie Mae has recently received questions from lenders

Conventional Financing

Chapter 6 Conventional Financing 1 Chapter Objectives Identify the characteristics of a conventional loan. Define amortization. Identify different types of conventional loans. Discuss the use of private

Chapter 6 Conventional Financing 1 Chapter Objectives Identify the characteristics of a conventional loan. Define amortization. Identify different types of conventional loans. Discuss the use of private

Private Mortgage Insurance (PMI)

") Private Mortgage Insurance (PMI) Private Mortgage Insurance (PMI) New Law Requires Lenders to Cancel PMI If you are a homeowner, you will want to be aware of a new law that establishes rights for homeowners

Private Mortgage Insurance (PMI) Private Mortgage Insurance (PMI) New Law Requires Lenders to Cancel PMI If you are a homeowner, you will want to be aware of a new law that establishes rights for homeowners

Appraiser Independence Requirements Frequently Asked Questions (FAQs) November 2010

November 2010") Appraiser Independence Requirements Frequently Asked Questions (FAQs) November 2010 The Appraiser Independence Requirements (AIR) were developed by Fannie Mae, the Federal Housing Finance Agency (FHFA),

Appraiser Independence Requirements Frequently Asked Questions (FAQs) November 2010 The Appraiser Independence Requirements (AIR) were developed by Fannie Mae, the Federal Housing Finance Agency (FHFA),

Habitat for Humanity of Southern Brazoria County (HfHSBC) This policy defines the terms and conditions that are required in a Habitat mortgage.

This policy defines the terms and conditions that are required in a Habitat mortgage.") Habitat for Humanity of Southern Brazoria County (HfHSBC) HfHSBC Policy No. 24 - Mortgage Policy General Principles This policy defines the terms and conditions that are required in a Habitat mortgage.

Habitat for Humanity of Southern Brazoria County (HfHSBC) HfHSBC Policy No. 24 - Mortgage Policy General Principles This policy defines the terms and conditions that are required in a Habitat mortgage.

HARP 2.0. Home Affordable Refinance Program - 2012

HARP 2.0 Home Affordable Refinance Program - 2012 Home Affordable Refinance Program (HARP) On October 24, 2011,the Federal Housing Finance Agency (FHFA), with Fannie Mae and Freddie Mac, announced a series

HARP 2.0 Home Affordable Refinance Program - 2012 Home Affordable Refinance Program (HARP) On October 24, 2011,the Federal Housing Finance Agency (FHFA), with Fannie Mae and Freddie Mac, announced a series

FEDERAL HOUSING FINANCE AGENCY

FEDERAL HOUSING FINANCE AGENCY ADVISORY BULLETIN AB 2012-02 FRAMEWORK FOR ADVERSELY CLASSIFYING LOANS, OTHER REAL ESTATE OWNED, AND OTHER ASSETS AND LISTING ASSETS FOR SPECIAL MENTION Introduction This

FEDERAL HOUSING FINANCE AGENCY ADVISORY BULLETIN AB 2012-02 FRAMEWORK FOR ADVERSELY CLASSIFYING LOANS, OTHER REAL ESTATE OWNED, AND OTHER ASSETS AND LISTING ASSETS FOR SPECIAL MENTION Introduction This

Announcement 09-13 May 11, 2009. Home Affordable Refinance Updates and Clarifications to Announcement 09-04

Announcement 09-13 May 11, 2009 Amends these Guides: Selling Home Affordable Refinance Updates and Clarifications to Announcement 09-04 Introduction On March 4, 2009, Fannie Mae announced two new refinance

Announcement 09-13 May 11, 2009 Amends these Guides: Selling Home Affordable Refinance Updates and Clarifications to Announcement 09-04 Introduction On March 4, 2009, Fannie Mae announced two new refinance

Mortgage Glossary. Mortgage loans under which the interest rate is periodically adjusted based upon terms agreed to at the inception of the loan.

Adjustable Rate Mortgage (ARM): Alternative Documentation: Amortization: Annual Percentage Rate (APR): Appraisal: Appraisal Amount or Appraised Value: Appreciation: Balloon Mortgage: Bankruptcy: Cap: Cash-out

Adjustable Rate Mortgage (ARM): Alternative Documentation: Amortization: Annual Percentage Rate (APR): Appraisal: Appraisal Amount or Appraised Value: Appreciation: Balloon Mortgage: Bankruptcy: Cap: Cash-out

Homeowners Protection Act

Background The Homeowners Protection Act of 1998 became effective in July 1999. The act, also known as the PMI Cancellation Act, addresses the difficulties homeowners have experienced in canceling private

Background The Homeowners Protection Act of 1998 became effective in July 1999. The act, also known as the PMI Cancellation Act, addresses the difficulties homeowners have experienced in canceling private

A Consumer s Guide to. Buying a Co-op

A Consumer s Guide to Buying a Co-op A Consumer s Guide to Buying a Co-op In the United States, more than 1.2 million families of all income levels live in homes owned and operated through cooperative

A Consumer s Guide to Buying a Co-op A Consumer s Guide to Buying a Co-op In the United States, more than 1.2 million families of all income levels live in homes owned and operated through cooperative

Assumable mortgage: A mortgage that can be transferred from a seller to a buyer. The buyer then takes over payment of an existing loan.

MORTGAGE GLOSSARY Adjustable Rate Mortgage (ARM): A mortgage loan with payments usually lower than a fixed rate initially, but is subject to changes in interest rates. There are a variety of ARMs that

MORTGAGE GLOSSARY Adjustable Rate Mortgage (ARM): A mortgage loan with payments usually lower than a fixed rate initially, but is subject to changes in interest rates. There are a variety of ARMs that

Unique Opportunities in Property Assessed Clean Energy (PACE) Financing

Financing") Unique Opportunities in Property Assessed Clean Energy (PACE) Financing October 13, 2014 POSTED BY: Andrew J. Guzikowski & Dawn T. Lindsey & R. Lynn Parins The Wisconsin based Public Finance Authority

Unique Opportunities in Property Assessed Clean Energy (PACE) Financing October 13, 2014 POSTED BY: Andrew J. Guzikowski & Dawn T. Lindsey & R. Lynn Parins The Wisconsin based Public Finance Authority

ILLINOIS ASSOCIATION OF REALTORS HOUSING POLICY

ILLINOIS ASSOCIATION OF REALTORS HOUSING POLICY ILLINOIS ASSOCIATION OF REALTORS HOUSING POLICY As an Association, we reaffirm our commitment to the goal of decent housing and a suitable living environment

ILLINOIS ASSOCIATION OF REALTORS HOUSING POLICY ILLINOIS ASSOCIATION OF REALTORS HOUSING POLICY As an Association, we reaffirm our commitment to the goal of decent housing and a suitable living environment

Mortgages and Mortgage -Backed Securiti curi es ti Mortgage ort gage securitized mortgage- backed securities (MBSs) Primary Pri mary Mortgage Market

Primary Pri mary Mortgage Market") Mortgages and Mortgage-Backed Securities Mortgage Markets Mortgages are loans to individuals or businesses to purchase homes, land, or other real property Many mortgages are securitized Many mortgages

Mortgages and Mortgage-Backed Securities Mortgage Markets Mortgages are loans to individuals or businesses to purchase homes, land, or other real property Many mortgages are securitized Many mortgages

Adjustable Rate Mortgage (ARM) a mortgage with a variable interest rate, which adjusts monthly, biannually or annually.

a mortgage with a variable interest rate, which adjusts monthly, biannually or annually.") Glossary Adjustable Rate Mortgage (ARM) a mortgage with a variable interest rate, which adjusts monthly, biannually or annually. Amortization the way a loan is paid off over time in installments, detailing

Glossary Adjustable Rate Mortgage (ARM) a mortgage with a variable interest rate, which adjusts monthly, biannually or annually. Amortization the way a loan is paid off over time in installments, detailing

HOME BUYING101 TM %*'9 [[[ EPXEREJGY SVK i

HOME BUYING101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

HOME BUYING101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

Frequently Asked Questions About Trust Deed Investing and Sterling Pacific Financial

Frequently Asked Questions About Trust Deed Investing and Sterling Pacific Financial This document is presented in four categories: FAQs about Trust Deed Investments (this page) FAQs about investing with

Frequently Asked Questions About Trust Deed Investing and Sterling Pacific Financial This document is presented in four categories: FAQs about Trust Deed Investments (this page) FAQs about investing with

Subject: Compliance Bulletin: Private Mortgage Insurance Cancellation and Termination

CFPB Bulletin 2015-03 Date: August 4, 2015 Subject: Compliance Bulletin: Private Mortgage Insurance Cancellation and Termination The Bureau of Consumer Financial Protection (CFPB) is issuing this compliance

CFPB Bulletin 2015-03 Date: August 4, 2015 Subject: Compliance Bulletin: Private Mortgage Insurance Cancellation and Termination The Bureau of Consumer Financial Protection (CFPB) is issuing this compliance

The Consumer Financial Protection Bureau s Ability-to-Repay and Qualified Mortgage Rule

ADVISORY February 2013 The Consumer Financial Protection Bureau s Ability-to-Repay and Qualified Mortgage Rule On January 10, 2013, the Consumer Financial Protection Bureau ( CFPB ) issued its final Ability-to-Repay

ADVISORY February 2013 The Consumer Financial Protection Bureau s Ability-to-Repay and Qualified Mortgage Rule On January 10, 2013, the Consumer Financial Protection Bureau ( CFPB ) issued its final Ability-to-Repay

MORTGAGE DICTIONARY. Amortization - Amortization is a decrease in the value of assets with time, which is normally the useful life of tangible assets.

MORTGAGE DICTIONARY Adjustable-Rate Mortgage An adjustable-rate mortgage (ARM) is a product with a floating or variable rate that adjusts based on some index. Amortization - Amortization is a decrease

MORTGAGE DICTIONARY Adjustable-Rate Mortgage An adjustable-rate mortgage (ARM) is a product with a floating or variable rate that adjusts based on some index. Amortization - Amortization is a decrease

Financing Residential Real Estate. Lesson 12: VA-Guaranteed Loans

Financing Residential Real Estate Lesson 12: VA-Guaranteed Loans Introduction In this lesson we will cover: characteristics of VA loans, eligibility requirements, VA guaranty, VA loan amounts, and underwriting

Financing Residential Real Estate Lesson 12: VA-Guaranteed Loans Introduction In this lesson we will cover: characteristics of VA loans, eligibility requirements, VA guaranty, VA loan amounts, and underwriting

First Time Home Buyer Glossary

First Time Home Buyer Glossary For first time home buyers, knowing and understanding the following terms are very important when purchasing your first home. By understanding these terms, you will make

First Time Home Buyer Glossary For first time home buyers, knowing and understanding the following terms are very important when purchasing your first home. By understanding these terms, you will make

Contents. VA Credit Overlays

Contents... 1 Introduction... 3 Links... 3 Transaction Types... 3 Purchase Transactions... 3 Refinance Transaction Regular Refinance... 3 Refinance Transaction Interest Rate Reduction Refinance Loan/IRRRL...

Contents... 1 Introduction... 3 Links... 3 Transaction Types... 3 Purchase Transactions... 3 Refinance Transaction Regular Refinance... 3 Refinance Transaction Interest Rate Reduction Refinance Loan/IRRRL...

OPTIONS FOR MOBILIZING CLEAN ENERGY FINANCE

JUNE 2015 BUSINESS OPTIONS FOR MOBILIZING CLEAN ENERGY FINANCE Patrick Falwell, Center for Climate and Energy Solutions Clean energy and energy efficiency technologies are decreasing in cost and demonstrating

JUNE 2015 BUSINESS OPTIONS FOR MOBILIZING CLEAN ENERGY FINANCE Patrick Falwell, Center for Climate and Energy Solutions Clean energy and energy efficiency technologies are decreasing in cost and demonstrating

FOR IMMEDIATE RELEASE November 7, 2013 MEDIA CONTACT: Lisa Gagnon 703-903-3385 INVESTOR CONTACT: Robin Phillips 571-382-4732

FOR IMMEDIATE RELEASE MEDIA CONTACT: Lisa Gagnon 703-903-3385 INVESTOR CONTACT: Robin Phillips 571-382-4732 FREDDIE MAC REPORTS PRE-TAX INCOME OF $6.5 BILLION FOR THIRD QUARTER 2013 Release of Valuation

FOR IMMEDIATE RELEASE MEDIA CONTACT: Lisa Gagnon 703-903-3385 INVESTOR CONTACT: Robin Phillips 571-382-4732 FREDDIE MAC REPORTS PRE-TAX INCOME OF $6.5 BILLION FOR THIRD QUARTER 2013 Release of Valuation

ENERGY EFFICIENCY FINANCING IN THE COMMERCIAL SECTOR MUNICIPAL MODELS & OPPORTUNITIES

ENERGY EFFICIENCY FINANCING IN THE COMMERCIAL SECTOR MUNICIPAL MODELS & OPPORTUNITIES Greg Hale Natural Resources Defense Council Pew Center on Global Climate Change Carbon Markets Insights Americas 2010

ENERGY EFFICIENCY FINANCING IN THE COMMERCIAL SECTOR MUNICIPAL MODELS & OPPORTUNITIES Greg Hale Natural Resources Defense Council Pew Center on Global Climate Change Carbon Markets Insights Americas 2010

CFPB issues ability-to-repay and qualified mortgage rules

1 FEBRUARY 4, 2013 CFPB issues ability-to-repay and qualified mortgage rules By Raymond J. Gustini, Lloyd H. Spencer, Tiana M. Butcher, Courtney L. Lindsay II, and Pierce Han No standard is perfect, but

1 FEBRUARY 4, 2013 CFPB issues ability-to-repay and qualified mortgage rules By Raymond J. Gustini, Lloyd H. Spencer, Tiana M. Butcher, Courtney L. Lindsay II, and Pierce Han No standard is perfect, but

Frequently Asked Questions (FAQ) about Home Energy Savings Loans and Property Assessed Clean Energy (PACE) in Maine

about Home Energy Savings Loans and Property Assessed Clean Energy (PACE) in Maine") Frequently Asked Questions (FAQ) about Home Energy Savings Loans and Property Assessed Clean Energy (PACE) in Maine Efficiency Maine administers programs to improve comfort and lower energy costs for energy

Frequently Asked Questions (FAQ) about Home Energy Savings Loans and Property Assessed Clean Energy (PACE) in Maine Efficiency Maine administers programs to improve comfort and lower energy costs for energy

S. 720 Energy Savings and Industrial Competitiveness Act of 2015

CONGRESSIONAL BUDGET OFFICE COST ESTIMATE October 19, 2015 S. 720 Energy Savings and Industrial Competitiveness Act of 2015 As reported by the Senate Committee on Energy and Natural Resources on September

CONGRESSIONAL BUDGET OFFICE COST ESTIMATE October 19, 2015 S. 720 Energy Savings and Industrial Competitiveness Act of 2015 As reported by the Senate Committee on Energy and Natural Resources on September

Appraiser: a qualified individual who uses his or her experience and knowledge to prepare the appraisal estimate.

Mortgage Glossary 203(b): FHA program which provides mortgage insurance to protect lenders from default; used to finance the purchase of new or existing one- to four family housing; characterized by low

Mortgage Glossary 203(b): FHA program which provides mortgage insurance to protect lenders from default; used to finance the purchase of new or existing one- to four family housing; characterized by low

Re: HUD Office of Inspector General (OIG Phoenix Office) Audit - NOVA Home Loans/HFA Programs

Audit - NOVA Home Loans/HFA Programs") June 8, 2015 Ms. Kathleen Zadareky Deputy Assistant Secretary Office of Single Family Housing U.S. Department of Housing and Urban Development 451 7 th Street, S.W. Washington, DC 20410 Re: HUD Office

June 8, 2015 Ms. Kathleen Zadareky Deputy Assistant Secretary Office of Single Family Housing U.S. Department of Housing and Urban Development 451 7 th Street, S.W. Washington, DC 20410 Re: HUD Office

A PRIMER ON THE SECONDARY MORTGAGE MARKET

ONE FANEUIL HALL MARKETPLACE BOSTON, MA 02109 TEL. 617 367-4390 FAX 617 720-0918 WWW.CITYRESEARCH.COM A PRIMER ON THE SECONDARY MORTGAGE MARKET National Community Development Initiative Meetings New York,

ONE FANEUIL HALL MARKETPLACE BOSTON, MA 02109 TEL. 617 367-4390 FAX 617 720-0918 WWW.CITYRESEARCH.COM A PRIMER ON THE SECONDARY MORTGAGE MARKET National Community Development Initiative Meetings New York,

Adjustment Date - The date on which the interest rate changes for an adjustable-rate mortgage (ARM).

.") Glossary A Adjustable Rate Mortgage - An adjustable rate mortgage, commonly referred to as an ARM, is a loan type that allows the lender to adjust the interest rate during the term of the loan. Generally,

Glossary A Adjustable Rate Mortgage - An adjustable rate mortgage, commonly referred to as an ARM, is a loan type that allows the lender to adjust the interest rate during the term of the loan. Generally,

HUD s AFFORDABLE LENDING GOALS FOR FANNIE MAE AND FREDDIE MAC

Issue Brief HUD s AFFORDABLE LENDING GOALS FOR FANNIE MAE AND FREDDIE MAC Fannie Mae and Freddie Mac, government-sponsored enterprises (GSEs) in the secondary mortgage market, are the two largest sources

Issue Brief HUD s AFFORDABLE LENDING GOALS FOR FANNIE MAE AND FREDDIE MAC Fannie Mae and Freddie Mac, government-sponsored enterprises (GSEs) in the secondary mortgage market, are the two largest sources

HOME BUYING101. 701.255.0042 www.capcu.org i

HOME BUYING101 701.255.0042 www.capcu.org i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended,

HOME BUYING101 701.255.0042 www.capcu.org i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended,

A Presentation On the State of the Real Estate Crisis 1/30/2009

A Presentation On the State of the Real Estate Crisis 1/30/2009 Presented by Mike Anderson, CRMS President, Essential Mortgage, a Latter & Blum Realtors Company Immediate past president/legislative Chair

A Presentation On the State of the Real Estate Crisis 1/30/2009 Presented by Mike Anderson, CRMS President, Essential Mortgage, a Latter & Blum Realtors Company Immediate past president/legislative Chair

Structured Financial Products

Structured Products Structured Financial Products Bond products created through the SECURITIZATION Referred to the collection of Mortgage Backed Securities Asset Backed Securities Characteristics Assets

Structured Products Structured Financial Products Bond products created through the SECURITIZATION Referred to the collection of Mortgage Backed Securities Asset Backed Securities Characteristics Assets

Housing Opportunities for Native Americans & Alaska Natives NativeNatives

Housing Opportunities for Native Americans & Alaska Natives NativeNatives The Section 184 Indian Home Loan Guarantee program is a home loan product for federally recognized tribal members, tribes, and

Housing Opportunities for Native Americans & Alaska Natives NativeNatives The Section 184 Indian Home Loan Guarantee program is a home loan product for federally recognized tribal members, tribes, and

METHODOLOGY. Rating U.S. Property Assessed Clean Energy (PACE) Securitizations

Securitizations") J U LY 2 0 1 5 METHODOLOGY Rating U.S. Property Assessed Clean Energy (PACE) Securitizations Rating U.S. Property Assessed Clean Energy (PACE) Securitizations DBRS.COM 2 Related Research: Unified Interest

J U LY 2 0 1 5 METHODOLOGY Rating U.S. Property Assessed Clean Energy (PACE) Securitizations Rating U.S. Property Assessed Clean Energy (PACE) Securitizations DBRS.COM 2 Related Research: Unified Interest

CityLIFT Oakland/East Bay Program Overview Non-Approved Lender Participation Application

CityLIFT Oakland/East Bay Program Overview Non-Approved Lender Participation Application DUE BY: Monday, December 23, 2013, 5:00 pm. Dear Lender: The Unity Council Homeownership Center (TUC HOC) is administering

CityLIFT Oakland/East Bay Program Overview Non-Approved Lender Participation Application DUE BY: Monday, December 23, 2013, 5:00 pm. Dear Lender: The Unity Council Homeownership Center (TUC HOC) is administering

Introduction to Mortgage Insurance. Mexico City November 2003

Introduction to Mortgage Insurance Mexico City November 2003 Agenda United Guaranty Mortgage guaranty insurance Industry history Product structure and risk factors Advantages of mortgage insurance Process

Introduction to Mortgage Insurance Mexico City November 2003 Agenda United Guaranty Mortgage guaranty insurance Industry history Product structure and risk factors Advantages of mortgage insurance Process

ESCROW REQUIREMENTS UNDER TILA

Overview Escrow Requirements Reg. Z High Cost Mortgage and Counseling - Reg. Z & X Ability to Repay & Qualified Mortgages Reg. Z & X Mortgage Servicing Reg. Z & X Loan Originator Compensation Reg. Z Copies

Overview Escrow Requirements Reg. Z High Cost Mortgage and Counseling - Reg. Z & X Ability to Repay & Qualified Mortgages Reg. Z & X Mortgage Servicing Reg. Z & X Loan Originator Compensation Reg. Z Copies

A. Eligibility Requirements for a Loan Modification & Troubled Debt Restructure (TDRs)

") POLICY: L127 This policy governs any changes in original terms, on consumer and business loans including but not limited to real estate loans, that were agreed to at loan approval. Loan modifications and

POLICY: L127 This policy governs any changes in original terms, on consumer and business loans including but not limited to real estate loans, that were agreed to at loan approval. Loan modifications and

HOME AFFORDABLE MODIFICATION PROGRAM BASE NET PRESENT VALUE (NPV) MODEL SPECIFICATIONS

MODEL SPECIFICATIONS") Overview HOME AFFORDABLE MODIFICATION PROGRAM BASE NET PRESENT VALUE (NPV) MODEL SPECIFICATIONS As a part of the Making Home Affordable Program, we are providing standardized guidance and a base net present

Overview HOME AFFORDABLE MODIFICATION PROGRAM BASE NET PRESENT VALUE (NPV) MODEL SPECIFICATIONS As a part of the Making Home Affordable Program, we are providing standardized guidance and a base net present

Overview of Mortgage Lending

Chapter 1 Overview of Mortgage Lending 1 Chapter Objectives Identify historical events affecting today s mortgage industry. Contrast the primary mortgage market and secondary mortgage market. Identify

Chapter 1 Overview of Mortgage Lending 1 Chapter Objectives Identify historical events affecting today s mortgage industry. Contrast the primary mortgage market and secondary mortgage market. Identify

Recourse vs. Nonrecourse: Commercial Real Estate Financing Which One is Right for You?

Recourse vs. Nonrecourse: Commercial Real Estate Financing Which One is Right for You? Prepared by Bill White Director of Commercial Real Estate Lending In this white paper 1 Commercial real estate lenders

Recourse vs. Nonrecourse: Commercial Real Estate Financing Which One is Right for You? Prepared by Bill White Director of Commercial Real Estate Lending In this white paper 1 Commercial real estate lenders

House Committee on Financial Services. November 29, 2012

House Committee on Financial Services Joint Hearing Before the Subcommittee on Financial Institutions and Consumer Credit and the Subcommittee on Insurance, Housing and Community Opportunity Entitled Examining

House Committee on Financial Services Joint Hearing Before the Subcommittee on Financial Institutions and Consumer Credit and the Subcommittee on Insurance, Housing and Community Opportunity Entitled Examining

ReNew Grant Guidelines

Brooklyn Center ReNew Buyer Incentive Program Greater Metropolitan Housing Corporation Program Summary The Economic Development Authority (EDA) of Brooklyn Center, Minnesota (EDA) has partnered with the

Brooklyn Center ReNew Buyer Incentive Program Greater Metropolitan Housing Corporation Program Summary The Economic Development Authority (EDA) of Brooklyn Center, Minnesota (EDA) has partnered with the

Homeownership Preservation Policy for Residential Mortgage Assets. Section 110 of the Emergency Economic Stabilization Act (EESA)

") Homeownership Preservation Policy for Residential Mortgage Assets Section 110 of the Emergency Economic Stabilization Act (EESA) requires that each Federal property manager that holds, owns, or controls

Homeownership Preservation Policy for Residential Mortgage Assets Section 110 of the Emergency Economic Stabilization Act (EESA) requires that each Federal property manager that holds, owns, or controls

How To Understand The Mortgage Brokerage Industry

QCommission Sample Plans Mortgage Broker Industry Introduction The mortgage industry is primarily involved in providing loans to consumers. This industry is made up of many parts, governmental entities

QCommission Sample Plans Mortgage Broker Industry Introduction The mortgage industry is primarily involved in providing loans to consumers. This industry is made up of many parts, governmental entities

Citi U.S. Mortgage Lending Data and Servicing Foreclosure Prevention Efforts

Citi U.S. Mortgage Lending Data and Servicing Foreclosure Prevention Efforts Third Quarter 28 EXECUTIVE SUMMARY In February 28, we published our initial data report on Citi s U.S. mortgage lending businesses,

Citi U.S. Mortgage Lending Data and Servicing Foreclosure Prevention Efforts Third Quarter 28 EXECUTIVE SUMMARY In February 28, we published our initial data report on Citi s U.S. mortgage lending businesses,