How To Calculate Net Present Value In Excel 113

|

|

|

- Bertina Carpenter

- 5 years ago

- Views:

Transcription

1 11. Introduction to Discounted Cash Flow Analysis and Financial Functions in Excel John Herbohn and Steve Harrison The financial and economic analysis of investment projects is typically carried out using the technique of discounted cash flow (DCF) analysis. This module introduces concepts of discounting and DCF analysis for the derivation of project performance criteria such as net present value (NPV), internal rate of return (IRR) and benefit to cost (B/C) ratios. These concepts and criteria are introduced with respect to a simple example, for which calculations using MicroSoft Excel are demonstrated CASH FLOWS, COMPOUNDING AND DISCOUNTING Discounted Cash Flow (DCF) analysis is the technique used to derive economic and financial performance criteria for investment projects. It is important to review some of the basic concepts of DCF analysis before proceeding to topics such as cost0benefit analysis (CBA), financial analysis (FA), linear programming and the estimation of non-market benefits. Cash flow analysis is simply the process of identifying and categories of cash flows associated with a project or proposed course of action, and making estimates of their values. For example, when considering establishment of a forestry plantation, this would involve identifying and making estimates of the cash outflows associated with establishing the trees (e.g. the cost of buying or leasing the land, purchasing seedlings, and planting the seedlings), maintaining the plantation (such as cost of fertilizer, labour, pruning and thinning) and harvesting. As well, it would be necessary to estimate the cash inflows from the plantation through sales of thinnings and timber at final harvest. Discounted cash flow analysis is an extension of simple cash flow analysis and takes into account the time value of money and the risks of investing in a project. A number of criteria are used in DCF to estimate project performance including Net Present Value (NPV), Internal Rate of Return (IRR) and Benefit-Cost (B/C) ratios. Before discussing criteria to measure project performance, it is necessary to introduce some concepts and procedures with respect to compounding and discounting. Let us begin with the concepts of simple and compound interest. For the moment, consider the interest rate as the cost of capital for the project. Suppose a person has to choose between receiving $1000 now, or a guaranteed $1000 in 12 months time. A rational person will naturally choose the former, because during the intervening period he or she could use the $1000 for profitable investment (e.g. earning interest in the bank) or desired consumption. If the $1000 were invested at an annual interest rate of 8%, then over the year it would earn $80 in interest. That is, a principal of $1000 invested for one year at an interest rate of 8% would have a future value of $1000 (1.08) or $1080. The $1000 may be invested for a second year, in which case it will earn further interest. If the interest again accrues on the principal of $1000 only, it is known as simple interest. In this case the future value after two years will be $1160. On the other hand, if interest in the second year accrues on the whole $1080, known as compound interest, the future value will be $1080 (1.08) or $ Most investment and borrowing situations involve compound interest, although the timing of interest payments may be such that all interest is paid before further interest accrues. The future value of the $1000 after two years may also be derived as $1000 (1.08) 2 = $

ratios. These concepts and criteria are introduced with respect to a simple example, for which calculations using MicroSoft Excel are demonstrated. 109 1.")

2 110 Socio-economic Research Methods in Forestry In general, the future value of an amount $a, invested for n years at an interest rate of i, is $a (1+i) n, where it it to be noted that the interest rate i is expressed as a decimal (e.g and not 8 for an 8% rate). The reverse of compounding finding the present-day equivalent to a future sum is known as discounting. Because $1000 invested for one year at an interest rate of 8% would have a value of $1080 in one year, the present value of $1080 one year from now, when the interest rate is 8%, is $1080/1.08 = $1000. Similarly, the present value of $1000 to be received one year from now, when the interest rate is 8%, is $1000/1.08 = $ In general, if an amount $a is to be received after n years, and the annual interest rate is i, then the present value is $a / (1+i) n The above discussion has been in terms of amounts in a single year. Investments usually incur costs and generate income in each of a number of years. Suppose the amount of $1000 is to be received at the end of each of the next four years. If not discounted, the sum of these amounts would be $4000. But suppose the interest rate is 8%. What is the present value of this stream of amounts? This is obtained by discounting the amount at the end of each year by the appropriate discount factor then summing: $1000/ $1000/ $1000/ $1000/ = $1000/ $1000/ $1000/ $1000/ = $ $ $ $ = $ The discount factors 1/1.08 t for t = 1 to 4 may be calculated for each year or read from published tables. It is to be noted that the present value of the annual amounts is progressively reduced for each year further into the future (from $ after one year to $ after four years), and the sum is approximately $700 less than if no discounting (a zero discount rate) had been applied. 2. DEFINITION OF ANNUAL NET CASH FLOWS DCF analysis is applied to the evaluation of investment projects. Such a project may involve creation of a terminating asset (such as a forestry plantation), infrastructure (such as a road or plywood plant) or research (including scientific and socioeconomic research). Any project may be regarded as generating cash flows. The term cash flow refers to any movement of money to or away from an investor (an individual, firm, industry or government). Projects require payments in the form of capital outlays and annual operating costs, referred to as cash outflows. They give rise to receipts or revenues, referred to as project benefits or cash inflows. For each year, the difference between project benefits and capital plus operating costs is known as the net cash flow for that year. The net cash flow in any year may be defined as a t = b t - (k t + c t ) where b t are project benefits in year t k t are capital outlays in year t c t are operating costs in year t. It is to be noted that when determining these net cash flows, expenditure items and income items are timed for the point at which the transactions takes place, rather than the time at which they are used. Thus for example expenditure on purchase of an item of machinery rather than annual allowances for depreciation would enter the cash flows. It is to be further noted that cash flows should not include interest payments. The discounting procedure in a sense simulates interest payments, so to include these in the operating costs would be to double-count them. Example 1 A project involves an immediate outlay of $25,000, with annual expenditures in each of three years of $4000, and generates revenue in each of three years of $15,000. These cash flows data may be set out, and annual net cash flows derived, as in Table 1.

3 Introduction to Discounted Cash Flow Analysis and Financial Functions in Excel 111 Table 1. Annual cash flows for a hypothetical project Year Project Capital Operating Net cash benefits outlays costs flow ($) ($) ($) ($) Two points may be noted about these cash flows. First, the capital outlay is timed for Year 0. By convention this is the beginning of the first year (i.e. right now). On the other hand, only half of the first year s operating costs are scheduled for the Year 0 (the beginning of the first year). The remaining half of the first year s operating costs plus the first half of the second year s operating costs are scheduled for the end of the first year (or, equivalently, the beginning of the second year). In this way, operating costs are spread equally between the beginning and the end of each year. (The final half of the third year s operating costs are scheduled for the end of Year 3.) In the case of project benefits, these are assumed to accrue at the end of each year, which would be consistent with lags in production or payments. These within-year timing issues are unlikely to make a large difference to overall project profitability, but it is useful to make these timing assumptions clear. A second point to note about Table 1 is that net cash flows (second column less third plus fourth column) are at first negative, but then become positive and increase over time. This is a typical pattern of wellbehaved cash flows, for which performance criteria can usually be derived without computational difficulties. 3. PROJECT PERFORMANCE CRITERIA Let us now consider a number of project performance criteria which can be obtained by discounted cash flow analysis. These criteria will be defined, then derived for the cash flow data of Example 1. Net present value The net present value (NPV) is the sum of the discounted annual cash flows. For the example, taking an interest rate of 8%, this is NPV = a 0 + a 1 /(1+i) + a 2 /(1+i) 2 + a 3 /(1+i) 3 A project is regarded as economically desirable if the NPV is positive. The project can then bear the cost of capital (the interest rate) and still leave a surplus or profit. For the example, NPV = /(1.08) /(1.08) /(1.08) 3 = / / / = $ The interpretation of this figure is that the project can suppport an 8% interest rate and still generate a surplus of benefits over costs, after allowing for timing differences in these, of approximately $3000. Net future value An alternative to the net present value is the net future value (NFV), for which annual cash flows are compounded forward to their value at the end of the project s life. Once the NPV is known, the NFV may be obtained indirectly by compounding forward the NPV by the number of years of the project life. For Example 1, the net future value is NFV = NPV (1.08) 3 = $ x = Internal rate of return The internal rate of return (IRR) is the interest rate such that the discounted sum

.")

4 112 Socio-economic Research Methods in Forestry of net cash flows is zero. If the interest rate were equal to the IRR, the net present value would be exactly zero. The IRR cannot be determined by an algebraic formula, but rather has to be approximated by trial and error methods. For the above example, we know that the IRR is somewhere above 8%. Deriving the NPV with a range of discount rates would reveal that the IRR falls between 13% and 14%, but closer to the latter. In practice, a financial function can be called up to perform the trial-and-error calculations. It would be found in this case that the IRR is about 13.8%. 1 The IRR is the highest interest rate which the project can support and still break even. A project is judged to be worthwhile in economic terms if the internal rate of return is greater than the cost of capital. If this is the case, the project could have supported a higher rate of interest than was actually experienced, and still made a positive payoff. In the above case, the project would be profitable provided the cost of capital was less than 13.8%. The IRR as a criterion of project profitability suffers from a number of theoretical and practical limitations. On the theoretical side, it assumes that the same rate of return is appropriate when the project is in surplus and when it is in deficit. However, the cost of borrowed funds may be quite different to the earning rate of the firm. It could be more appropriate to use two rates when determining the IRR. The actual cost of capital could be used when the project is in deficit, and the earning rate (unknown, to be determined by trial-and-error) could be applied when the project is in surplus. This would give a better indication of the earning rate of the project to the firm or government. From a practical viewpoint, the IRR may not exist or it may not be unique. This problem may be examined in terms of the NPV profile, a graph of NPV versus the rate of interest. When the IRR is well behaved, this profile takes the form as in Figure 1. As the 1 Calculation of internal rate of return in fact involves solving a polynomial equation, and efficient solution methods such as Newton s approximation are used in computer packages. interest rate increases the NPV falls, being zero where the NPV curve crosses the interest rate axis; the IRR corresponds with this discount rate. Consider a project for which the net cash flow in each year (including Year 0) is positive. Regardless of the interest rate, the NPV will never be zero, so it will not be possible to determine an IRR. Similarly, a project with a large initial capital outlay and for which future benefits are relatively small or negative may not have a positive NPV regardless of the interest rate, so again the curve for the NPV profile may never cross the interest rate axis. If a project generates runs of positive and negative net cash flows, the NPV profile may take the form of a roller-coaster curve, crossing the interest rate axis in several places. 2 This indicates multiple internal rates of return, one at each interest rate where NPV is zero. It is then by no means clear which if any of the rates we should choose to call the IRR. Further, for some sections of the NPV profile (those that are upward sloping), the NPV is increasing as the interest rate increases. This implies that the greater the cost of capital the more profitable the project. Clearly, multiple internal rates of return and perverse relationships between the NPV and the discount rate are not very satisfactory. Benefit-to-cost ratios A number of benefit-cost ratio concepts have been developed. For simplicity, we will consider only two concepts, referred to as the gross and net B/C ratio and defined respectively as Gross B/C ratio = PV of benefits/(pv of capital costs + PV of operating costs) Net B/C ratio = (PV of benefits PV of operating costs)/pv of capital costs 2 Mathematically, the polynomial equation defining the NPV can have up as many roots or solutions as there are turning points in NPV values (changes from positive to negative or negative to positive). A project which has alternating runs of positive and negative cash flows is a candidate for problems with estimation of the IRR.

5 Introduction to Discounted Cash Flow Analysis and Financial Functions in Excel 113 For the above project, the present value of capital outlays is $25,000, since outlays are made immediately and as a single amount. The present values of project benefits and operating costs are: PV of benefits = $15000/ $15000/ $15000/ = $ PV of operating costs = $ $4000/ $4000/ $2000/ = $ Hence the benefit-to-cost ratios are 38, gross B/C ratio = = , , net B/C ratio = = ,000 A project is judged to be worthwhile in economic terms if it has a B/C ratio is greater than unity, i.e. if the present value of benefits exceeds the present value of costs (in gross or net terms). If one of the above ratios is greater than unity, then the other will be greater than unity also. In the above example, the ratios are greater than unity, indicating that the project is worthwhile on economic grounds. It is not clear on logical grounds which of the ratios is the most useful. Net present value Internal rate of return 0 Interest rate Figure 1. The NPV profile for a project The payback period The payback period (PP) is the number of years for the projects to break even, i.e. the number of years for which discounted annual net cash flows must be summed before the sum becomes positive (and remains positive for the remainder of the project s life). The payback period for a project with the above net cash flows can be determined as in the following table. From this table, it is apparent that the sum of discounted net cash flows does not become positive until Year 3, so the payback period is three years. The payback period indicates the number of years until the investment in a project is recovered. It is a useful criterion for a firm with a short planning horizon, but does not take account of all the information available, i.e. the net cash flows for years beyond the payback period. The peak deficit This is a measure of the greatest amount that the project owes the firm or government, i.e. the furtherest in the red it goes. In the above table, the largest negative value is -$27,000, so this is the peak deficit. Peak deficit is a useful measure in terms of financing a project, since it indicates the total amount of finance that will be required.

.")

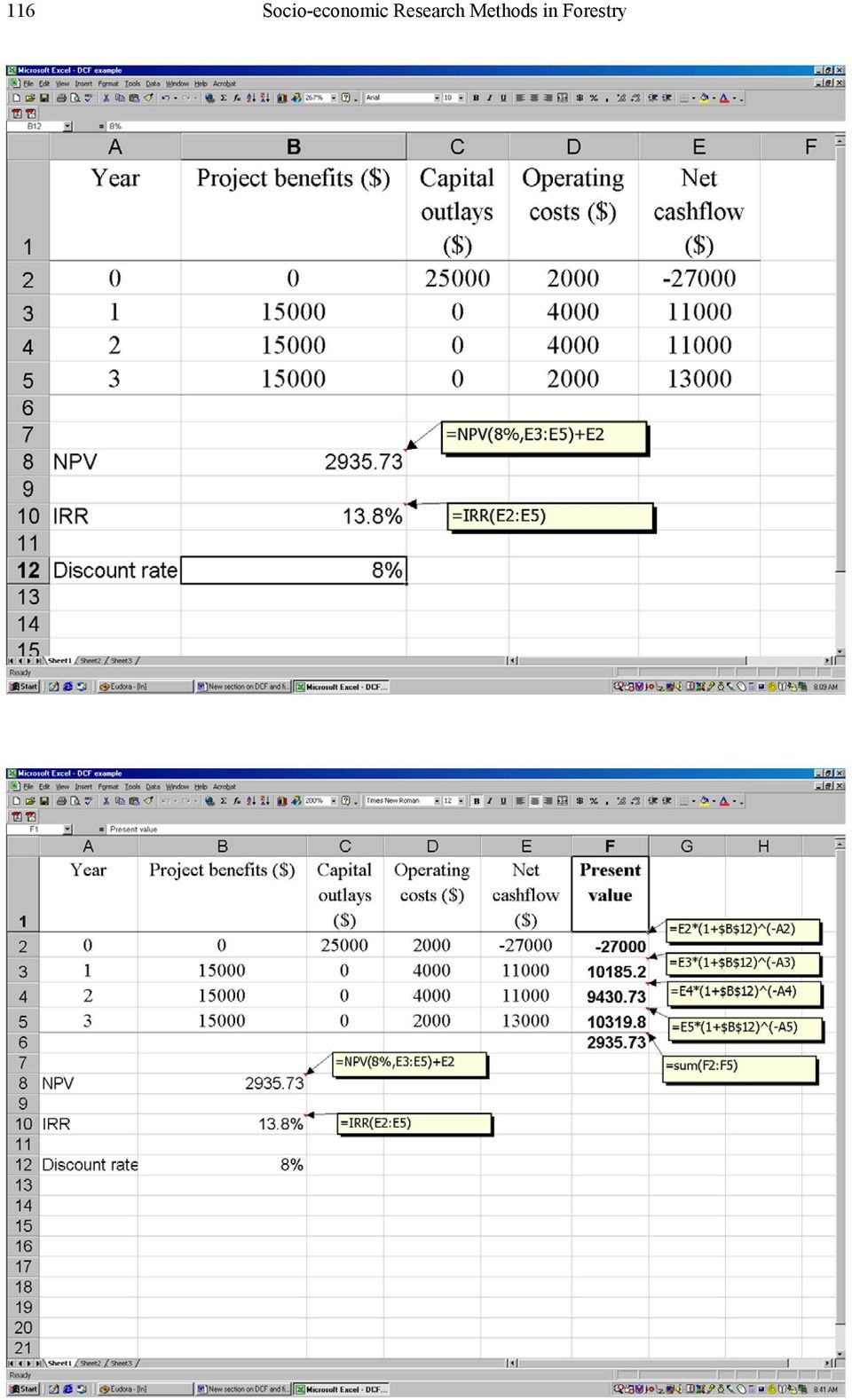

6 114 Socio-economic Research Methods in Forestry Table 2. Derivation of project balances and payback period Year Net cash PV of net Cumulative PV of net cash flow cash flow flow (or project balance) ($) ($) ($) = = = Review of DCF performance criteria The most commonly used discounted cash flow performance criteria NPV, IRR, B/C ratios and payback period may be summarised as in Table 3. The various criteria are closely related, but measure slightly different things. In this respect, they tend to complement one another, so that it is common to estimate and report more than one of the measures. Perhaps the most useful measure, and the one most often reported, is the net present value. This tells the total payoff from a project. A limitation of the NPV is that it is not related to the size of the project. If one project has a slightly lower NPV than another, but the capital outlays required are much lower, then the second project will probably be the preferred one. In this sense, a rate of return measure such as the IRR is also useful. The payback period and peak deficit are useful supplementary project information for decision-makers. They have greater relevance for private sector investments, for firms which cannot afford long delays in recouping expenditure, and where careful attention must be paid to the total amount of funds that will need to be committed to the project to remain solvent. Table 3. Summary of definitions of main DFC performance criteria Net present value (NPV) Internal rate of return (IRR) Benefit to cost ratio (B/C) Payback period p a t / (1+i) t, where t is time, c t is the annual net cash flow, t=1 i is the discount rate p is the planning horizon p The value of r such that a t / (1+r) t = 0 t=1 Present value of project benefits / present value of project costs Number of periods until NPV becomes (and remains) positive 4. USING EXCEL FINANCIAL FUNCTIONS It is common to use a spreadsheet program such as Excel to undertake financial and cost benefit analyses. Excel has a range of financial functions that can be useful (as listed in Apppendix 1). Two of the most useful and commonly used financial functions in Excel are those to calculate Net Present Value ( NPV ) and Internal Rate of Return ( IRR ). This section illustrates the use of two of the NPV and IRR functions, applied to the data in Example 1, in an Excel worksheet: Using the NPV and IRR functions The NPV function calculates the net present value of an investment (i.e. series of cash flows) by using a discount rate and a series of future payments (negative

7 Introduction to Discounted Cash Flow Analysis and Financial Functions in Excel 115 values) and income (positive values). The syntax for this function is: NPV(discount rate, value1, value2.) It is important to remember that the NPV calculation is for cashflows starting at the end of period 1. If the first cash flow occurs at the beginning of period 1 (i.e. period 0), the first value must be added to the NPV result, not included in the value arguments of the function. Thus to value the NPV for example 1, the following formula would be inserted into a spreadsheet cell: =NPV(8%, 11000, 11000, 13000) Note that the cashflow sequence used in the NPV calculation is for years 1 to 3. The value for year 0 (-$27000) is added to the NPV result. An alternative means of calculating NPV and IRR in the above example would be to replace the string of values with cell references to where the values are located within the workbook. This is illustrated in the worksheet below. This approach has the advantage of allowing changes to the made to the cashflows (in Column E) which then automatically flow through to the calculation of the NPV. This is particularly useful when it is desired to investigate how changes in cash flows affect NPV. Similarly, the discount rate given in the formula (in this case 8%) could be replaced with a cell reference. In this case the effects of a change in discount rate on NPV could be observed simply changing the cell value rather than the formula. In the worksheet below, the 8% in the formula for NPV in cell B8 would be replaced by a reference to cell B12. The new formula would be =NPV(B12, E3:E5)+E2. Another approach to calculating NPV is to simply calculate the present value of cash flows for each year using the discounting formula given in Equation 1 and then simply add these individual figures. This approach has a number of advantages in more complex applications particularly those involved complex financial models with variable periods of cash flows and where discount rates change over the life of a project. This is illustrated in the workbook below:

is added to the NPV result.")

8 116 Socio-economic Research Methods in Forestry

9 Introduction to Discounted Cash Flow Analysis and Financial Functions in Excel 117 The formula in Cells F2, F3, F4 and F5 calculate the present value of the net cash flow in each of the years 0 through to 3 using the formula given in Equation 1. These present values for each of the years are then summed in cell F6 to give the Net Present Value of the series of cash flows associated with the project. The resulting NPV in cell F6 is identical to the NPV calculated in cell B8. Note that an absolute cell address for the discount rate has been used ($B$12) using $. This allows the formula in cell F2 to be simply copied into cells F3, F4 and F5. APPENDIX 1: FINANCIAL FUNCTIONS IN EXCEL ACCRINT Returns the accrued interest for a security that pays periodic interest ACCRINTM Returns the accrued interest for a security that pays interest at maturity AMORDEGRC Returns the depreciation for each accounting period AMORLINC Returns the depreciation for each accounting period COUPDAYBS Returns the number of days from the beginning of the coupon period to the settlement date COUPDAYS Returns the number of days in the coupon period that contains the settlement date COUPDAYSNC Returns the number of days from the settlement date to the next coupon date COUPNCD Returns the next coupon date after the settlement date COUPNUM Returns the number of coupons payable between the settlement date and maturity date COUPPCD Returns the previous coupon date before the settlement date CUMIPMT Returns the cumulative interest paid between two periods CUMPRINC Returns the cumulative principal paid on a loan between two periods DB Returns the depreciation of an asset for a specified period using the fixeddeclining balance method DDB Returns the depreciation of an asset for a specified period using the doubledeclining balance method or some other depreciation method DISC Returns the discount rate for a security DOLLARDE Converts a dollar price, expressed as a fraction, into a dollar price, expressed as a decimal number DOLLARFR Converts a dollar price, expressed as a decimal number, into a dollar price, expressed as a fraction DURATION Returns the annual duration of a security with periodic interest payments EFFECT Returns the effective annual interest rate FV Returns the future value of an investment FVSCHEDULE Returns the future value of an initial principal after applying a series of compound interest rates INTRATE Returns the interest rate for a fully invested security IPMT Returns the interest payment for an investment for a given period IRR Returns the internal rate of return for a series of cash flows ISPMT Calculates the interest paid during a specific period of an investment. MDURATION Returns the Macauley modified duration for a security with an assumed par value of $100 MIRR Returns the internal rate of return where positive and negative cash flows are financed at different rates NOMINAL Returns the annual nominal interest rate NPER Returns the number of periods for an investment NPV Returns the net present value of an investment based on a series of periodic cash flows and a discount rate ODDFPRICE Returns the price per $100 face value of a security with an odd first period ODDFYIELD Returns the yield of a security with an odd first period ODDLPRICE Returns the price per $100 face value of a security with an odd last period ODDLYIELD Returns the yield of a security with an odd last period PMT Returns the periodic payment for an annuity PPMT Returns the payment on the principal for an investment for a given period PRICE Returns the price per $100 face value of a security that pays periodic interest PRICEDISC Returns the price per $100 face value of a discounted security

using $.")

10 118 Socio-economic Research Methods in Forestry PRICEMAT Returns the price per $100 face value of a security that pays interest at maturity PV Returns the present value of an investment RATE Returns the interest rate per period of an annuity RECEIVED Returns the amount received at maturity for a fully invested security SLN Returns the straight-line depreciation of an asset for one period SYD Returns the sum-of-years' digits depreciation of an asset for a specified period TBILLEQ Returns the bond-equivalent yield for a Treasury bill TBILLPRICE Returns the price per $100 face value for a Treasury bill TBILLYIELD Returns the yield for a Treasury bill VDB Returns the depreciation of an asset for a specified or partial period using a declining balance method XIRR Returns the internal rate of return for a schedule of cash flows that is not necessarily periodic XNPV Returns the net present value for a schedule of cash flows that is not necessarily periodic YIELD Returns the yield on a security that pays periodic interest YIELDDISC Returns the annual yield for a discounted security. For example, a Treasury bill YIELDMAT Returns the annual yield of a security that pays interest at maturity

EXCEL FUNCTIONS MOST COMMON

EXCEL FUNCTIONS MOST COMMON This is a list of the most common Functions in Excel with a description. To see the syntax and a more in depth description, the function is a link to the Microsoft Excel site.

EXCEL FUNCTIONS MOST COMMON This is a list of the most common Functions in Excel with a description. To see the syntax and a more in depth description, the function is a link to the Microsoft Excel site.

Excel 2010 Formulas & Functions

Excel is the world s premier spreadsheet software. You can use Excel to analyze numbers, keep track of data, and graphically represent your information. With Excel 2010, you can manage more data than ever,

Excel is the world s premier spreadsheet software. You can use Excel to analyze numbers, keep track of data, and graphically represent your information. With Excel 2010, you can manage more data than ever,

9-17a Tutorial 9 Practice Review Assignment

9-17a Tutorial 9 Practice Review Assignment Data File needed for the Review Assignments: Restaurant.xlsx Sylvia has some new figures for the business plan for Jerel's. She has received slightly better

9-17a Tutorial 9 Practice Review Assignment Data File needed for the Review Assignments: Restaurant.xlsx Sylvia has some new figures for the business plan for Jerel's. She has received slightly better

NOTE: All of the information contained in this file has been collected from the various HELP files found in Excel for each of these functions.

NOTE: All of the information contained in this file has been collected from the various HELP files found in Excel for each of these functions. PV Returns the present value of an investment. The present

NOTE: All of the information contained in this file has been collected from the various HELP files found in Excel for each of these functions. PV Returns the present value of an investment. The present

COMPUTER APPLICATIONS IN BANKING & FINANCE. Salih KATIRCIOGLU

COMPUTER APPLICATIONS IN BANKING & FINANCE Salih KATIRCIOGLU Eastern Mediterranean University Faculty of Business and Economics Department of Banking and Finance Famagusta, Turkish Republic of Northern

COMPUTER APPLICATIONS IN BANKING & FINANCE Salih KATIRCIOGLU Eastern Mediterranean University Faculty of Business and Economics Department of Banking and Finance Famagusta, Turkish Republic of Northern

PMT. 0 or omitted At the end of the period 1 At the beginning of the period

PMT Calculates the payment for a loan based on constant payments and a constant interest rate. PMT(rate,nper,pv,fv,type) For a more complete description of the arguments in PMT, see the PV function. Rate

PMT Calculates the payment for a loan based on constant payments and a constant interest rate. PMT(rate,nper,pv,fv,type) For a more complete description of the arguments in PMT, see the PV function. Rate

6: Financial Calculations

: Financial Calculations The Time Value of Money Growth of Money I Growth of Money II The FV Function Amortisation of a Loan Annuity Calculation Comparing Investments Worked examples Other Financial Functions

: Financial Calculations The Time Value of Money Growth of Money I Growth of Money II The FV Function Amortisation of a Loan Annuity Calculation Comparing Investments Worked examples Other Financial Functions

REVIEW MATERIALS FOR REAL ESTATE ANALYSIS

REVIEW MATERIALS FOR REAL ESTATE ANALYSIS 1997, Roy T. Black REAE 5311, Fall 2005 University of Texas at Arlington J. Andrew Hansz, Ph.D., CFA CONTENTS ITEM ANNUAL COMPOUND INTEREST TABLES AT 10% MATERIALS

REVIEW MATERIALS FOR REAL ESTATE ANALYSIS 1997, Roy T. Black REAE 5311, Fall 2005 University of Texas at Arlington J. Andrew Hansz, Ph.D., CFA CONTENTS ITEM ANNUAL COMPOUND INTEREST TABLES AT 10% MATERIALS

Chapter 7 SOLUTIONS TO END-OF-CHAPTER PROBLEMS

Chapter 7 SOLUTIONS TO END-OF-CHAPTER PROBLEMS 7-1 0 1 2 3 4 5 10% PV 10,000 FV 5? FV 5 $10,000(1.10) 5 $10,000(FVIF 10%, 5 ) $10,000(1.6105) $16,105. Alternatively, with a financial calculator enter the

Chapter 7 SOLUTIONS TO END-OF-CHAPTER PROBLEMS 7-1 0 1 2 3 4 5 10% PV 10,000 FV 5? FV 5 $10,000(1.10) 5 $10,000(FVIF 10%, 5 ) $10,000(1.6105) $16,105. Alternatively, with a financial calculator enter the

CE Entrepreneurship. Investment decision making

CE Entrepreneurship Investment decision making Cash Flow For projects where there is a need to spend money to develop a product or establish a service which results in cash coming into the business in

CE Entrepreneurship Investment decision making Cash Flow For projects where there is a need to spend money to develop a product or establish a service which results in cash coming into the business in

10.SHORT-TERM DECISIONS & CAPITAL INVESTMENT APPRAISAL

INDUSTRIAL UNIVERSITY OF HO CHI MINH CITY AUDITING ACCOUNTING FACULTY 10.SHORT-TERM DECISIONS & CAPITAL INVESTMENT APPRAISAL 4 Topic List INDUSTRIAL UNIVERSITY OF HO CHI MINH CITY AUDITING ACCOUNTING FACULTY

INDUSTRIAL UNIVERSITY OF HO CHI MINH CITY AUDITING ACCOUNTING FACULTY 10.SHORT-TERM DECISIONS & CAPITAL INVESTMENT APPRAISAL 4 Topic List INDUSTRIAL UNIVERSITY OF HO CHI MINH CITY AUDITING ACCOUNTING FACULTY

Dick Schwanke Finite Math 111 Harford Community College Fall 2013

Annuities and Amortization Finite Mathematics 111 Dick Schwanke Session #3 1 In the Previous Two Sessions Calculating Simple Interest Finding the Amount Owed Computing Discounted Loans Quick Review of

Annuities and Amortization Finite Mathematics 111 Dick Schwanke Session #3 1 In the Previous Two Sessions Calculating Simple Interest Finding the Amount Owed Computing Discounted Loans Quick Review of

Module 5: Interest concepts of future and present value

Page 1 of 23 Module 5: Interest concepts of future and present value Overview In this module, you learn about the fundamental concepts of interest and present and future values, as well as ordinary annuities

Page 1 of 23 Module 5: Interest concepts of future and present value Overview In this module, you learn about the fundamental concepts of interest and present and future values, as well as ordinary annuities

Module 5: Interest concepts of future and present value

file:///f /Courses/2010-11/CGA/FA2/06course/m05intro.htm Module 5: Interest concepts of future and present value Overview In this module, you learn about the fundamental concepts of interest and present

file:///f /Courses/2010-11/CGA/FA2/06course/m05intro.htm Module 5: Interest concepts of future and present value Overview In this module, you learn about the fundamental concepts of interest and present

BENEFIT-COST ANALYSIS Financial and Economic Appraisal using Spreadsheets

BENEFIT-COST ANALYSIS Financial and Economic Appraisal using Spreadsheets Ch. 3: Decision Rules Harry Campbell & Richard Brown School of Economics The University of Queensland Applied Investment Appraisal

BENEFIT-COST ANALYSIS Financial and Economic Appraisal using Spreadsheets Ch. 3: Decision Rules Harry Campbell & Richard Brown School of Economics The University of Queensland Applied Investment Appraisal

CALCULATOR TUTORIAL. Because most students that use Understanding Healthcare Financial Management will be conducting time

CALCULATOR TUTORIAL INTRODUCTION Because most students that use Understanding Healthcare Financial Management will be conducting time value analyses on spreadsheets, most of the text discussion focuses

CALCULATOR TUTORIAL INTRODUCTION Because most students that use Understanding Healthcare Financial Management will be conducting time value analyses on spreadsheets, most of the text discussion focuses

Excel Financial Functions

Excel Financial Functions PV() Effect() Nominal() FV() PMT() Payment Amortization Table Payment Array Table NPer() Rate() NPV() IRR() MIRR() Yield() Price() Accrint() Future Value How much will your money

Excel Financial Functions PV() Effect() Nominal() FV() PMT() Payment Amortization Table Payment Array Table NPer() Rate() NPV() IRR() MIRR() Yield() Price() Accrint() Future Value How much will your money

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions Chapter 8 Capital Budgeting Concept Check 8.1 1. What is the difference between independent and mutually

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions Chapter 8 Capital Budgeting Concept Check 8.1 1. What is the difference between independent and mutually

How To Calculate Discounted Cash Flow

Chapter 1 The Overall Process Capital Expenditures Whenever we make an expenditure that generates a cash flow benefit for more than one year, this is a capital expenditure. Examples include the purchase

Chapter 1 The Overall Process Capital Expenditures Whenever we make an expenditure that generates a cash flow benefit for more than one year, this is a capital expenditure. Examples include the purchase

In this chapter we will learn about. Treasury Notes and Bonds, Treasury Inflation Protected Securities,

2 Treasury Securities In this chapter we will learn about Treasury Bills, Treasury Notes and Bonds, Strips, Treasury Inflation Protected Securities, and a few other products including Eurodollar deposits.

2 Treasury Securities In this chapter we will learn about Treasury Bills, Treasury Notes and Bonds, Strips, Treasury Inflation Protected Securities, and a few other products including Eurodollar deposits.

CHAPTER 7: NPV AND CAPITAL BUDGETING

CHAPTER 7: NPV AND CAPITAL BUDGETING I. Introduction Assigned problems are 3, 7, 34, 36, and 41. Read Appendix A. The key to analyzing a new project is to think incrementally. We calculate the incremental

CHAPTER 7: NPV AND CAPITAL BUDGETING I. Introduction Assigned problems are 3, 7, 34, 36, and 41. Read Appendix A. The key to analyzing a new project is to think incrementally. We calculate the incremental

ICASL - Business School Programme

ICASL - Business School Programme Quantitative Techniques for Business (Module 3) Financial Mathematics TUTORIAL 2A This chapter deals with problems related to investing money or capital in a business

ICASL - Business School Programme Quantitative Techniques for Business (Module 3) Financial Mathematics TUTORIAL 2A This chapter deals with problems related to investing money or capital in a business

CHAPTER 6 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA

CHAPTER 6 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Answers to Concepts Review and Critical Thinking Questions 1. Assuming conventional cash flows, a payback period less than the project s life means

CHAPTER 6 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Answers to Concepts Review and Critical Thinking Questions 1. Assuming conventional cash flows, a payback period less than the project s life means

The Reinvestment Assumption Dallas Brozik, Marshall University

The Reinvestment Assumption Dallas Brozik, Marshall University Every field of study has its little odd bits, and one of the odd bits in finance is the reinvestment assumption. It is an artifact of the

The Reinvestment Assumption Dallas Brozik, Marshall University Every field of study has its little odd bits, and one of the odd bits in finance is the reinvestment assumption. It is an artifact of the

Cost Benefits analysis

Cost Benefits analysis One of the key items in any business case is an analysis of the costs of a project that includes some consideration of both the cost and the payback (be it in monetary or other terms).

Cost Benefits analysis One of the key items in any business case is an analysis of the costs of a project that includes some consideration of both the cost and the payback (be it in monetary or other terms).

Module 10: Assessing the Business Case

Module 10: Assessing the Business Case Learning Objectives After completing this section, you will be able to: Do preliminary assessment of proposed energy management investments. The measures recommended

Module 10: Assessing the Business Case Learning Objectives After completing this section, you will be able to: Do preliminary assessment of proposed energy management investments. The measures recommended

MODULE 2. Capital Budgeting

MODULE 2 Capital Budgeting Capital Budgeting is a project selection exercise performed by the business enterprise. Capital budgeting uses the concept of present value to select the projects. Capital budgeting

MODULE 2 Capital Budgeting Capital Budgeting is a project selection exercise performed by the business enterprise. Capital budgeting uses the concept of present value to select the projects. Capital budgeting

$1,300 + 1,500 + 1,900 = $4,700. in cash flows. The project still needs to create another: $5,500 4,700 = $800

1. To calculate the payback period, we need to find the time that the project has recovered its initial investment. After three years, the project has created: $1,300 + 1,500 + 1,900 = $4,700 in cash flows.

1. To calculate the payback period, we need to find the time that the project has recovered its initial investment. After three years, the project has created: $1,300 + 1,500 + 1,900 = $4,700 in cash flows.

Performing Net Present Value (NPV) Calculations

Calculations") Strategies and Mechanisms For Promoting Cleaner Production Investments In Developing Countries Profiting From Cleaner Production Performing Net Present Value (NPV) Calculations Cleaner Production Profiting

Strategies and Mechanisms For Promoting Cleaner Production Investments In Developing Countries Profiting From Cleaner Production Performing Net Present Value (NPV) Calculations Cleaner Production Profiting

Integrated Case. 5-42 First National Bank Time Value of Money Analysis

Integrated Case 5-42 First National Bank Time Value of Money Analysis You have applied for a job with a local bank. As part of its evaluation process, you must take an examination on time value of money

Integrated Case 5-42 First National Bank Time Value of Money Analysis You have applied for a job with a local bank. As part of its evaluation process, you must take an examination on time value of money

Net Present Value (NPV)

") Investment Criteria 208 Net Present Value (NPV) What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value and

Investment Criteria 208 Net Present Value (NPV) What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value and

PV Tutorial Using Excel

EYK 15-3 PV Tutorial Using Excel TABLE OF CONTENTS Introduction Exercise 1: Exercise 2: Exercise 3: Exercise 4: Exercise 5: Exercise 6: Exercise 7: Exercise 8: Exercise 9: Exercise 10: Exercise 11: Exercise

EYK 15-3 PV Tutorial Using Excel TABLE OF CONTENTS Introduction Exercise 1: Exercise 2: Exercise 3: Exercise 4: Exercise 5: Exercise 6: Exercise 7: Exercise 8: Exercise 9: Exercise 10: Exercise 11: Exercise

rate nper pmt pv Interest Number of Payment Present Future Rate Periods Amount Value Value 12.00% 1 0 $100.00 $112.00

In Excel language, if the initial cash flow is an inflow (positive), then the future value must be an outflow (negative). Therefore you must add a negative sign before the FV (and PV) function. The inputs

In Excel language, if the initial cash flow is an inflow (positive), then the future value must be an outflow (negative). Therefore you must add a negative sign before the FV (and PV) function. The inputs

How To Use A Speech Applications Builder

IP Telephony Contact Centers Mobility Services WHITE PAPER Avaya Speech Applications Builder Overview of Rapid Application Development and Deployment for Avaya Speech Self Service Version 1.3 May 2005

IP Telephony Contact Centers Mobility Services WHITE PAPER Avaya Speech Applications Builder Overview of Rapid Application Development and Deployment for Avaya Speech Self Service Version 1.3 May 2005

Investment Decision Analysis

Lecture: IV 1 Investment Decision Analysis The investment decision process: Generate cash flow forecasts for the projects, Determine the appropriate opportunity cost of capital, Use the cash flows and

Lecture: IV 1 Investment Decision Analysis The investment decision process: Generate cash flow forecasts for the projects, Determine the appropriate opportunity cost of capital, Use the cash flows and

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Answers to Concepts Review and Critical Thinking Questions 1. A payback period less than the project s life means that the NPV is positive for

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Answers to Concepts Review and Critical Thinking Questions 1. A payback period less than the project s life means that the NPV is positive for

Calculating Loan Payments

IN THIS CHAPTER Calculating Loan Payments...............1 Calculating Principal Payments...........4 Working with Future Value...............7 Using the Present Value Function..........9 Calculating Interest

IN THIS CHAPTER Calculating Loan Payments...............1 Calculating Principal Payments...........4 Working with Future Value...............7 Using the Present Value Function..........9 Calculating Interest

Course 3: Capital Budgeting Analysis

Excellence in Financial Management Course 3: Capital Budgeting Analysis Prepared by: Matt H. Evans, CPA, CMA, CFM This course provides a concise overview of capital budgeting analysis. This course is recommended

Excellence in Financial Management Course 3: Capital Budgeting Analysis Prepared by: Matt H. Evans, CPA, CMA, CFM This course provides a concise overview of capital budgeting analysis. This course is recommended

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Solutions to Questions and Problems NOTE: All-end-of chapter problems were solved using a spreadsheet. Many problems require multiple steps. Due to space and readability

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Solutions to Questions and Problems NOTE: All-end-of chapter problems were solved using a spreadsheet. Many problems require multiple steps. Due to space and readability

Bond valuation. Present value of a bond = present value of interest payments + present value of maturity value

Bond valuation A reading prepared by Pamela Peterson Drake O U T L I N E 1. Valuation of long-term debt securities 2. Issues 3. Summary 1. Valuation of long-term debt securities Debt securities are obligations

Bond valuation A reading prepared by Pamela Peterson Drake O U T L I N E 1. Valuation of long-term debt securities 2. Issues 3. Summary 1. Valuation of long-term debt securities Debt securities are obligations

Present Value Concepts

Present Value Concepts Present value concepts are widely used by accountants in the preparation of financial statements. In fact, under International Financial Reporting Standards (IFRS), these concepts

Present Value Concepts Present value concepts are widely used by accountants in the preparation of financial statements. In fact, under International Financial Reporting Standards (IFRS), these concepts

( ) ( )( ) ( ) 2 ( ) 3. n n = 100 000 1+ 0.10 = 100 000 1.331 = 133100

( )( ) ( ) 2 ( ) 3. n n = 100 000 1+ 0.10 = 100 000 1.331 = 133100") Mariusz Próchniak Chair of Economics II Warsaw School of Economics CAPITAL BUDGETING Managerial Economics 1 2 1 Future value (FV) r annual interest rate B the amount of money held today Interest is compounded

Mariusz Próchniak Chair of Economics II Warsaw School of Economics CAPITAL BUDGETING Managerial Economics 1 2 1 Future value (FV) r annual interest rate B the amount of money held today Interest is compounded

Part 610 Natural Resource Economics Handbook

Part 610 Natural Resource Economics Handbook 610.20 Introduction Subpart C Discounted Cash Flow Analysis A. Benefits and costs of conservation practices do not necessarily occur at the same time. Certain

Part 610 Natural Resource Economics Handbook 610.20 Introduction Subpart C Discounted Cash Flow Analysis A. Benefits and costs of conservation practices do not necessarily occur at the same time. Certain

HO-23: METHODS OF INVESTMENT APPRAISAL

HO-23: METHODS OF INVESTMENT APPRAISAL After completing this exercise you will be able to: Calculate and compare the different returns on an investment using the ROI, NPV, IRR functions. Investments: Discounting,

HO-23: METHODS OF INVESTMENT APPRAISAL After completing this exercise you will be able to: Calculate and compare the different returns on an investment using the ROI, NPV, IRR functions. Investments: Discounting,

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Basic 1. To calculate the payback period, we need to find the time that the project has recovered its initial investment. After two years, the

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Basic 1. To calculate the payback period, we need to find the time that the project has recovered its initial investment. After two years, the

e C P M 1 0 5 : P o r t f o l i o M a n a g e m e n t f o r P r i m a v e r a P 6 W e b A c c e s s

e C P M 1 5 : P o r t f o l i o M a n a g e m e n t f o r P r i m a v e r a P 6 W e b A c c e s s Capital Budgeting C o l l a b o r a t i v e P r o j e c t M a n a g e m e n t e C P M 1 5 C a p i t a l

e C P M 1 5 : P o r t f o l i o M a n a g e m e n t f o r P r i m a v e r a P 6 W e b A c c e s s Capital Budgeting C o l l a b o r a t i v e P r o j e c t M a n a g e m e n t e C P M 1 5 C a p i t a l

Chapter 09 - Using Discounted Cash-Flow Analysis to Make Investment Decisions

Solutions to Chapter 9 Using Discounted Cash-Flow Analysis to Make Investment Decisions 1. Net income = ($74 $42 $10) [0.35 ($74 $42 $10)] = $22 $7.7 = $14.3 million Revenues cash expenses taxes paid =

Solutions to Chapter 9 Using Discounted Cash-Flow Analysis to Make Investment Decisions 1. Net income = ($74 $42 $10) [0.35 ($74 $42 $10)] = $22 $7.7 = $14.3 million Revenues cash expenses taxes paid =

Solutions to Chapter 8. Net Present Value and Other Investment Criteria

Solutions to Chapter 8 Net Present Value and Other Investment Criteria. NPV A = $00 + [$80 annuity factor (%, periods)] = $00 $80 $8. 0 0. 0. (.) NPV B = $00 + [$00 annuity factor (%, periods)] = $00 $00

Solutions to Chapter 8 Net Present Value and Other Investment Criteria. NPV A = $00 + [$80 annuity factor (%, periods)] = $00 $80 $8. 0 0. 0. (.) NPV B = $00 + [$00 annuity factor (%, periods)] = $00 $00

CARNEGIE MELLON UNIVERSITY CIO INSTITUTE

CARNEGIE MELLON UNIVERSITY CIO INSTITUTE CAPITAL BUDGETING BASICS Contact Information: Lynne Pastor Email: [email protected] RELATED LEARNGING OBJECTIVES 7.2 LO 3: Compare and contrast the implications

CARNEGIE MELLON UNIVERSITY CIO INSTITUTE CAPITAL BUDGETING BASICS Contact Information: Lynne Pastor Email: [email protected] RELATED LEARNGING OBJECTIVES 7.2 LO 3: Compare and contrast the implications

Prepared by: Dalia A. Marafi Version 2.0

Kuwait University College of Business Administration Department of Finance and Financial Institutions Using )Casio FC-200V( for Fundamentals of Financial Management (220) Prepared by: Dalia A. Marafi Version

Kuwait University College of Business Administration Department of Finance and Financial Institutions Using )Casio FC-200V( for Fundamentals of Financial Management (220) Prepared by: Dalia A. Marafi Version

Capital Investment Analysis and Project Assessment

PURDUE EXTENSION EC-731 Capital Investment Analysis and Project Assessment Michael Boehlje and Cole Ehmke Department of Agricultural Economics Capital investment decisions that involve the purchase of

PURDUE EXTENSION EC-731 Capital Investment Analysis and Project Assessment Michael Boehlje and Cole Ehmke Department of Agricultural Economics Capital investment decisions that involve the purchase of

CHAPTER 4. The Time Value of Money. Chapter Synopsis

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

UNDERSTANDING HEALTHCARE FINANCIAL MANAGEMENT, 5ed. Time Value Analysis

This is a sample of the instructor resources for Understanding Healthcare Financial Management, Fifth Edition, by Louis Gapenski. This sample contains the chapter models, end-of-chapter problems, and end-of-chapter

This is a sample of the instructor resources for Understanding Healthcare Financial Management, Fifth Edition, by Louis Gapenski. This sample contains the chapter models, end-of-chapter problems, and end-of-chapter

Chapter 6. Discounted Cash Flow Valuation. Key Concepts and Skills. Multiple Cash Flows Future Value Example 6.1. Answer 6.1

Chapter 6 Key Concepts and Skills Be able to compute: the future value of multiple cash flows the present value of multiple cash flows the future and present value of annuities Discounted Cash Flow Valuation

Chapter 6 Key Concepts and Skills Be able to compute: the future value of multiple cash flows the present value of multiple cash flows the future and present value of annuities Discounted Cash Flow Valuation

Chapter 4 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS

Chapter 4 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS 4-1 a. PV (present value) is the value today of a future payment, or stream of payments, discounted at the appropriate rate of interest.

Chapter 4 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS 4-1 a. PV (present value) is the value today of a future payment, or stream of payments, discounted at the appropriate rate of interest.

Course FM / Exam 2. Calculator advice

Course FM / Exam 2 Introduction It wasn t very long ago that the square root key was the most advanced function of the only calculator approved by the SOA/CAS for use during an actuarial exam. Now students

Course FM / Exam 2 Introduction It wasn t very long ago that the square root key was the most advanced function of the only calculator approved by the SOA/CAS for use during an actuarial exam. Now students

Numbers 101: Cost and Value Over Time

The Anderson School at UCLA POL 2000-09 Numbers 101: Cost and Value Over Time Copyright 2000 by Richard P. Rumelt. We use the tool called discounting to compare money amounts received or paid at different

The Anderson School at UCLA POL 2000-09 Numbers 101: Cost and Value Over Time Copyright 2000 by Richard P. Rumelt. We use the tool called discounting to compare money amounts received or paid at different

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES

Chapter - The Term Structure of Interest Rates CHAPTER : THE TERM STRUCTURE OF INTEREST RATES PROBLEM SETS.. In general, the forward rate can be viewed as the sum of the market s expectation of the future

Chapter - The Term Structure of Interest Rates CHAPTER : THE TERM STRUCTURE OF INTEREST RATES PROBLEM SETS.. In general, the forward rate can be viewed as the sum of the market s expectation of the future

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES

CHAPTER : THE TERM STRUCTURE OF INTEREST RATES CHAPTER : THE TERM STRUCTURE OF INTEREST RATES PROBLEM SETS.. In general, the forward rate can be viewed as the sum of the market s expectation of the future

CHAPTER : THE TERM STRUCTURE OF INTEREST RATES CHAPTER : THE TERM STRUCTURE OF INTEREST RATES PROBLEM SETS.. In general, the forward rate can be viewed as the sum of the market s expectation of the future

Financial Math on Spreadsheet and Calculator Version 4.0

Financial Math on Spreadsheet and Calculator Version 4.0 2002 Kent L. Womack and Andrew Brownell Tuck School of Business Dartmouth College Table of Contents INTRODUCTION...1 PERFORMING TVM CALCULATIONS

Financial Math on Spreadsheet and Calculator Version 4.0 2002 Kent L. Womack and Andrew Brownell Tuck School of Business Dartmouth College Table of Contents INTRODUCTION...1 PERFORMING TVM CALCULATIONS

Chapter 10. What is capital budgeting? Topics. The Basics of Capital Budgeting: Evaluating Cash Flows

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows 1 Topics Overview and vocabulary Methods NPV IRR, MIRR Profitability Index Payback, discounted payback Unequal lives Economic life 2 What

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows 1 Topics Overview and vocabulary Methods NPV IRR, MIRR Profitability Index Payback, discounted payback Unequal lives Economic life 2 What

This is Time Value of Money: Multiple Flows, chapter 7 from the book Finance for Managers (index.html) (v. 0.1).

(v. 0.1).") This is Time Value of Money: Multiple Flows, chapter 7 from the book Finance for Managers (index.html) (v. 0.1). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

This is Time Value of Money: Multiple Flows, chapter 7 from the book Finance for Managers (index.html) (v. 0.1). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

DUKE UNIVERSITY Fuqua School of Business. FINANCE 351 - CORPORATE FINANCE Problem Set #1 Prof. Simon Gervais Fall 2011 Term 2.

DUKE UNIVERSITY Fuqua School of Business FINANCE 351 - CORPORATE FINANCE Problem Set #1 Prof. Simon Gervais Fall 2011 Term 2 Questions 1. Two years ago, you put $20,000 dollars in a savings account earning

DUKE UNIVERSITY Fuqua School of Business FINANCE 351 - CORPORATE FINANCE Problem Set #1 Prof. Simon Gervais Fall 2011 Term 2 Questions 1. Two years ago, you put $20,000 dollars in a savings account earning

Fixed Income: Practice Problems with Solutions

Fixed Income: Practice Problems with Solutions Directions: Unless otherwise stated, assume semi-annual payment on bonds.. A 6.0 percent bond matures in exactly 8 years and has a par value of 000 dollars.

Fixed Income: Practice Problems with Solutions Directions: Unless otherwise stated, assume semi-annual payment on bonds.. A 6.0 percent bond matures in exactly 8 years and has a par value of 000 dollars.

Time Value of Money 1

Time Value of Money 1 This topic introduces you to the analysis of trade-offs over time. Financial decisions involve costs and benefits that are spread over time. Financial decision makers in households

Time Value of Money 1 This topic introduces you to the analysis of trade-offs over time. Financial decisions involve costs and benefits that are spread over time. Financial decision makers in households

Financial and Cash Flow Analysis Methods. www.project-finance.com

Financial and Cash Flow Analysis Methods Financial analysis Historic analysis (BS, ratios, CF analysis, management strategy) Current position (environment, industry, products, management) Future (competitiveness,

Financial and Cash Flow Analysis Methods Financial analysis Historic analysis (BS, ratios, CF analysis, management strategy) Current position (environment, industry, products, management) Future (competitiveness,

HP 12C Calculations. 2. If you are given the following set of cash flows and discount rates, can you calculate the PV? (pg.

HP 12C Calculations This handout has examples for calculations on the HP12C: 1. Present Value (PV) 2. Present Value with cash flows and discount rate constant over time 3. Present Value with uneven cash

HP 12C Calculations This handout has examples for calculations on the HP12C: 1. Present Value (PV) 2. Present Value with cash flows and discount rate constant over time 3. Present Value with uneven cash

Basic Financial Tools: A Review. 3 n 1 n. PV FV 1 FV 2 FV 3 FV n 1 FV n 1 (1 i)

") Chapter 28 Basic Financial Tools: A Review The building blocks of finance include the time value of money, risk and its relationship with rates of return, and stock and bond valuation models. These topics

Chapter 28 Basic Financial Tools: A Review The building blocks of finance include the time value of money, risk and its relationship with rates of return, and stock and bond valuation models. These topics

Dick Schwanke Finite Math 111 Harford Community College Fall 2015

Using Technology to Assist in Financial Calculations Calculators: TI-83 and HP-12C Software: Microsoft Excel 2007/2010 Session #4 of Finite Mathematics 1 TI-83 / 84 Graphing Calculator Section 5.5 of textbook

Using Technology to Assist in Financial Calculations Calculators: TI-83 and HP-12C Software: Microsoft Excel 2007/2010 Session #4 of Finite Mathematics 1 TI-83 / 84 Graphing Calculator Section 5.5 of textbook

Statistical Models for Forecasting and Planning

Part 5 Statistical Models for Forecasting and Planning Chapter 16 Financial Calculations: Interest, Annuities and NPV chapter 16 Financial Calculations: Interest, Annuities and NPV Outcomes Financial information

Part 5 Statistical Models for Forecasting and Planning Chapter 16 Financial Calculations: Interest, Annuities and NPV chapter 16 Financial Calculations: Interest, Annuities and NPV Outcomes Financial information

Chapter 6. Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams

Chapter 6 Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams 1. Distinguish between an ordinary annuity and an annuity due, and calculate present

Chapter 6 Learning Objectives Principles Used in This Chapter 1. Annuities 2. Perpetuities 3. Complex Cash Flow Streams 1. Distinguish between an ordinary annuity and an annuity due, and calculate present

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA 1. To calculate the payback period, we need to find the time that the project has recovered its initial investment. After three years, the project

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA 1. To calculate the payback period, we need to find the time that the project has recovered its initial investment. After three years, the project

5. Time value of money

1 Simple interest 2 5. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

1 Simple interest 2 5. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

Vilnius University. Faculty of Mathematics and Informatics. Gintautas Bareikis

Vilnius University Faculty of Mathematics and Informatics Gintautas Bareikis CONTENT Chapter 1. SIMPLE AND COMPOUND INTEREST 1.1 Simple interest......................................................................

Vilnius University Faculty of Mathematics and Informatics Gintautas Bareikis CONTENT Chapter 1. SIMPLE AND COMPOUND INTEREST 1.1 Simple interest......................................................................

PowerPoint. to accompany. Chapter 5. Interest Rates

PowerPoint to accompany Chapter 5 Interest Rates 5.1 Interest Rate Quotes and Adjustments To understand interest rates, it s important to think of interest rates as a price the price of using money. When

PowerPoint to accompany Chapter 5 Interest Rates 5.1 Interest Rate Quotes and Adjustments To understand interest rates, it s important to think of interest rates as a price the price of using money. When

The Cost of Capital, and a Note on Capitalization

The Cost of Capital, and a Note on Capitalization Prepared by Kerry Krutilla 8all rights reserved Introduction Often in class we have presented a diagram like this: Table 1 B B1 B2 B3 C -Co This kind of

The Cost of Capital, and a Note on Capitalization Prepared by Kerry Krutilla 8all rights reserved Introduction Often in class we have presented a diagram like this: Table 1 B B1 B2 B3 C -Co This kind of

Capital Budgeting OVERVIEW

WSG12 7/7/03 4:25 PM Page 191 12 Capital Budgeting OVERVIEW This chapter concentrates on the long-term, strategic considerations and focuses primarily on the firm s investment opportunities. The discussions

WSG12 7/7/03 4:25 PM Page 191 12 Capital Budgeting OVERVIEW This chapter concentrates on the long-term, strategic considerations and focuses primarily on the firm s investment opportunities. The discussions

Investments. 1.1 Future value and present value. What you must be able to explain:

Investments What you must be able to explain: Future value Present value Annual effective interest rate Net present value (NPV ) and opportunity cost of capital Internal rate of return (IRR) Payback rule

Investments What you must be able to explain: Future value Present value Annual effective interest rate Net present value (NPV ) and opportunity cost of capital Internal rate of return (IRR) Payback rule

Investment Appraisal INTRODUCTION

8 Investment Appraisal INTRODUCTION After reading the chapter, you should: understand what is meant by the time value of money; be able to carry out a discounted cash flow analysis to assess the viability

8 Investment Appraisal INTRODUCTION After reading the chapter, you should: understand what is meant by the time value of money; be able to carry out a discounted cash flow analysis to assess the viability

Bond Price Arithmetic

1 Bond Price Arithmetic The purpose of this chapter is: To review the basics of the time value of money. This involves reviewing discounting guaranteed future cash flows at annual, semiannual and continuously

1 Bond Price Arithmetic The purpose of this chapter is: To review the basics of the time value of money. This involves reviewing discounting guaranteed future cash flows at annual, semiannual and continuously

PRESENT DISCOUNTED VALUE

THE BOND MARKET Bond a fixed (nominal) income asset which has a: -face value (stated value of the bond) - coupon interest rate (stated interest rate) - maturity date (length of time for fixed income payments)

THE BOND MARKET Bond a fixed (nominal) income asset which has a: -face value (stated value of the bond) - coupon interest rate (stated interest rate) - maturity date (length of time for fixed income payments)

CHAPTER 6 DISCOUNTED CASH FLOW VALUATION

CHAPTER 6 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. The four pieces are the present value (PV), the periodic cash flow (C), the discount rate (r), and

CHAPTER 6 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. The four pieces are the present value (PV), the periodic cash flow (C), the discount rate (r), and

Answers to Review Questions

Answers to Review Questions 1. The real rate of interest is the rate that creates an equilibrium between the supply of savings and demand for investment funds. The nominal rate of interest is the actual

Answers to Review Questions 1. The real rate of interest is the rate that creates an equilibrium between the supply of savings and demand for investment funds. The nominal rate of interest is the actual

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO END-OF-CHAPTER QUESTIONS

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether they should

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether they should

VALUATION OF DEBT CONTRACTS AND THEIR PRICE VOLATILITY CHARACTERISTICS QUESTIONS See answers below

VALUATION OF DEBT CONTRACTS AND THEIR PRICE VOLATILITY CHARACTERISTICS QUESTIONS See answers below 1. Determine the value of the following risk-free debt instrument, which promises to make the respective

VALUATION OF DEBT CONTRACTS AND THEIR PRICE VOLATILITY CHARACTERISTICS QUESTIONS See answers below 1. Determine the value of the following risk-free debt instrument, which promises to make the respective

CHAPTER 5. Interest Rates. Chapter Synopsis

CHAPTER 5 Interest Rates Chapter Synopsis 5.1 Interest Rate Quotes and Adjustments Interest rates can compound more than once per year, such as monthly or semiannually. An annual percentage rate (APR)

CHAPTER 5 Interest Rates Chapter Synopsis 5.1 Interest Rate Quotes and Adjustments Interest rates can compound more than once per year, such as monthly or semiannually. An annual percentage rate (APR)

FI 302, Business Finance Exam 2, Fall 2000 versions 1 & 8 KEYKEYKEYKEYKEYKEYKEYKEYKEYKEYKEYKEYKEY

FI 302, Business Finance Exam 2, Fall 2000 versions 1 & 8 KEYKEYKEYKEYKEYKEYKEYKEYKEYKEYKEYKEYKEY 1. (3 points) BS16 What is a 401k plan Most U.S. households single largest lifetime source of savings is

FI 302, Business Finance Exam 2, Fall 2000 versions 1 & 8 KEYKEYKEYKEYKEYKEYKEYKEYKEYKEYKEYKEYKEY 1. (3 points) BS16 What is a 401k plan Most U.S. households single largest lifetime source of savings is

The Time Value of Money

The Time Value of Money Future Value - Amount to which an investment will grow after earning interest. Compound Interest - Interest earned on interest. Simple Interest - Interest earned only on the original

The Time Value of Money Future Value - Amount to which an investment will grow after earning interest. Compound Interest - Interest earned on interest. Simple Interest - Interest earned only on the original

Introduction to the Hewlett-Packard (HP) 10BII Calculator and Review of Mortgage Finance Calculations

10BII Calculator and Review of Mortgage Finance Calculations") Introduction to the Hewlett-Packard (HP) 10BII Calculator and Review of Mortgage Finance Calculations Real Estate Division Sauder School of Business University of British Columbia Introduction to the Hewlett-Packard

Introduction to the Hewlett-Packard (HP) 10BII Calculator and Review of Mortgage Finance Calculations Real Estate Division Sauder School of Business University of British Columbia Introduction to the Hewlett-Packard

EXAM 2 OVERVIEW. Binay Adhikari

EXAM 2 OVERVIEW Binay Adhikari FEDERAL RESERVE & MARKET ACTIVITY (BS38) Definition 4.1 Discount Rate The discount rate is the periodic percentage return subtracted from the future cash flow for computing

EXAM 2 OVERVIEW Binay Adhikari FEDERAL RESERVE & MARKET ACTIVITY (BS38) Definition 4.1 Discount Rate The discount rate is the periodic percentage return subtracted from the future cash flow for computing

Time Value of Money. Nature of Interest. appendix. study objectives

2918T_appC_C01-C20.qxd 8/28/08 9:57 PM Page C-1 appendix C Time Value of Money study objectives After studying this appendix, you should be able to: 1 Distinguish between simple and compound interest.

2918T_appC_C01-C20.qxd 8/28/08 9:57 PM Page C-1 appendix C Time Value of Money study objectives After studying this appendix, you should be able to: 1 Distinguish between simple and compound interest.

Investment Appraisal

Investment Appraisal Article relevant to F1 Business Mathematics and Quantitative Methods Author: Pat McGillion, current Examiner. Questions 1 and 6 often relate to Investment Appraisal, which is underpinned

Investment Appraisal Article relevant to F1 Business Mathematics and Quantitative Methods Author: Pat McGillion, current Examiner. Questions 1 and 6 often relate to Investment Appraisal, which is underpinned

An Appraisal Tool for Valuing Forest Lands

An Appraisal Tool for Valuing Forest Lands By Thomas J. Straka and Steven H. Bullard Abstract Forest and natural resources valuation can present challenging analysis and appraisal problems. Calculations

An Appraisal Tool for Valuing Forest Lands By Thomas J. Straka and Steven H. Bullard Abstract Forest and natural resources valuation can present challenging analysis and appraisal problems. Calculations

CHAPTER 9 Time Value Analysis

Copyright 2008 by the Foundation of the American College of Healthcare Executives 6/11/07 Version 9-1 CHAPTER 9 Time Value Analysis Future and present values Lump sums Annuities Uneven cash flow streams

Copyright 2008 by the Foundation of the American College of Healthcare Executives 6/11/07 Version 9-1 CHAPTER 9 Time Value Analysis Future and present values Lump sums Annuities Uneven cash flow streams

Introduction. Turning the Calculator On and Off

Texas Instruments BAII PLUS Calculator Tutorial to accompany Cyr, et. al. Contemporary Financial Management, 1 st Canadian Edition, 2004 Version #6, May 5, 2004 By William F. Rentz and Alfred L. Kahl Introduction

Texas Instruments BAII PLUS Calculator Tutorial to accompany Cyr, et. al. Contemporary Financial Management, 1 st Canadian Edition, 2004 Version #6, May 5, 2004 By William F. Rentz and Alfred L. Kahl Introduction

If I offered to give you $100, you would probably

File C5-96 June 2013 www.extension.iastate.edu/agdm Understanding the Time Value of Money If I offered to give you $100, you would probably say yes. Then, if I asked you if you wanted the $100 today or

File C5-96 June 2013 www.extension.iastate.edu/agdm Understanding the Time Value of Money If I offered to give you $100, you would probably say yes. Then, if I asked you if you wanted the $100 today or

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES 1. Expectations hypothesis. The yields on long-term bonds are geometric averages of present and expected future short rates. An upward sloping curve is

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES 1. Expectations hypothesis. The yields on long-term bonds are geometric averages of present and expected future short rates. An upward sloping curve is

FINANCIAL AND RISK ANALYSIS WITH RETSCREEN SOFTWARE. SLIDE 1: Financial and Risk Analysis with RETScreen Software

Training Module SPEAKER S NOTES FINANCIAL AND RISK ANALYSIS WITH RETSCREEN SOFTWARE CLEAN ENERGY PROJECT ANALYSIS COURSE This document provides a transcription of the oral presentation (Voice & Slides)

Training Module SPEAKER S NOTES FINANCIAL AND RISK ANALYSIS WITH RETSCREEN SOFTWARE CLEAN ENERGY PROJECT ANALYSIS COURSE This document provides a transcription of the oral presentation (Voice & Slides)

Hewlett-Packard 10BII Tutorial

This tutorial has been developed to be used in conjunction with Brigham and Houston s Fundamentals of Financial Management 11 th edition and Fundamentals of Financial Management: Concise Edition. In particular,

This tutorial has been developed to be used in conjunction with Brigham and Houston s Fundamentals of Financial Management 11 th edition and Fundamentals of Financial Management: Concise Edition. In particular,