How To Get A Mortgage On A House For $249,000

|

|

|

- Emma Wheeler

- 3 years ago

- Views:

Transcription

1 Section 11.5 Buying a House with a Mortgage

2 INB Table of Contents Date Topic Page # February 19, 2014 Section 11.5 Examples 36 February 19, 2014 Section 11.5 Notes

3 What You Will Learn Homeowner s Mortgage Conventional Loans Adjustable-Rate Mortgages 3

4 Homeowner s Mortgage A homeowner s mortgage is a longterm loan in which the property is pledged as a security payment of the difference between the down payment and the sale price. 4

5 Homeowner s Mortgage The two types are the conventional loan and the adjustable-rate loan (or the variable-rate loan). The major difference between the two is that the interest rate for a conventional loan is fixed for the duration of the loan, where as the interest rate for the variable-rate loan may change every period, as specified in the loan. 5

6 Homeowner s Mortgage Lending institutions may require the buyer to pay one or more points for a loan at the time of the closing (the final step in the sale process). According to the Internal Revenue Service, points are interest prepaid by the buyer and may be used to reduce the stated interest rate the lender charges. One point is equal to 1% of the loan amount. 6

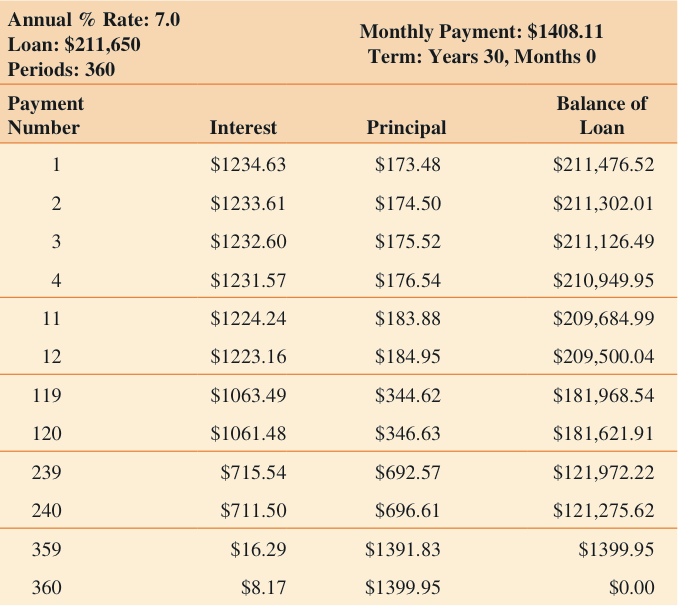

7 Example 1: Down Payment and Points Patricia and Marshall Martin wish to purchase a house selling for $249,000. They plan to obtain a loan from their bank. The bank requires a 15% down payment, payable to the seller, and a payment of 2 points, payable to the bank, at the time of closing. a) Determine the Martin s down payment. b) Determine the amount of the Martin s mortgage. c) Determine the cost of the 2 points paid by the Martins on their mortgage. 7

8 Qualifying for a Mortgage Banks use a formula to determine the maximum monthly payment that they believe is within the purchaser s ability to pay. They calculate the adjusted monthly income which equals the gross monthly income minus any fixed monthly payments (with more than 10 payments remaining). They multiply that result by 28%. This is the maximum monthly payment the lending institution believes the purchaser can afford. This includes: principal, interest, tax, insurance. 11

9 Principal and Interest Payment Formula m is principal and interest payment p is the amount of the mortgage m p r n 1 1 r n n t r is the interest rate as a decimal n is the number of payments per year t is the time in years 13

10 Example 3: Using the Principal and Interest Payment Formula Use the principal and interest payment formula to calculate the Martin s monthly principal and interest payment. Recall that the Martins are seeking a 30-year, $211,650 mortgage with an interest rate of 7%. 14

11 Amortization Schedule By repeatedly using the simple interest formula month to month on the unpaid balance, you could calculate the principal and the interest for all the payments, which is a tedious task. However, a list containing the payment number, payment on the interest, payment on the principal, and balance of the loan can be prepared using a computer. Such a list is called a loan amortization schedule. 18

12 Amortization Schedule 19

13 Adjustable Rate Mortgages Also, called ARMs or variable-rate mortgages. The monthly mortgage payment rate remains the same for a 1, 2, or 5-year period, even though the interest rate of a mortgage may change every 3 or 6 months or some other predetermined period. 20

14 Adjustable Rate Mortgages The monthly payment is readjusted after the time period so the loan will be paid off in the set amount of time or the bank may extend the time period of the loan beyond the predetermined years to make the payment affordable. 21

15 Example 5: An Adjustable-Rate Mortgage Tony and Keisha Torrence purchased a house for $115,000 with a down payment of $23,100. They obtained a 30-year adjustable-rate mortgage with the following terms. The interest rate is based on a 6-month Treasury bill. The interest rate charged is 3% above the interest rate of the 6-month Treasury bill (3% is the add on rate). The interest rate is adjusted every 6 months on the date of adjustment. The interest rate will not change more than 1% (up or down) when it is adjusted. The maximum interest rate for the duration of the loan is 12%. There is no lower limit on the interest rate. The initial mortgage interest rate is 5.5%, and the monthly payments (including principal and interest) are adjusted every 5 years. a) Determine the initial monthly payment. b) Determine the adjusted interest rate in 6 months if the interest rate on the Treasury bill at that time is 2%. 22

16 Table

17 Rate Caps To prevent rapid increases in interest rates, some banks have a rate cap. A rate cap limits the maximum amount the interest rate may change. A periodic rate cap limits the amount the interest rate may increase in any one period. 28

18 Rate Caps An aggregate rate cap limits the interest rate increase and decrease over the entire life of the loan. A payment cap limits the amount the monthly payment may change but does not limit changes in interest rates. 29

19 Other Types of Mortgages FHA Mortgage VA Mortgage Graduated Payment Mortgage (GPM) Balloon-Payment Mortgage (BPM) Home Equity Loans Also, see 30

11.5 Buying a House with a Mortgage FILLED IN.notebook February 17, 2015

11.5 Buying a House with a Mortgage 1 DOWN PAYMENT The amount of cash the buyer must pay the seller before the lending institution will grant the buyer a mortgage for the remaining amount of the home price

11.5 Buying a House with a Mortgage 1 DOWN PAYMENT The amount of cash the buyer must pay the seller before the lending institution will grant the buyer a mortgage for the remaining amount of the home price

RESIDENTIAL MORTGAGE PRODUCT INFORMATION DISCLOSURE

RESIDENTIAL MORTGAGE PRODUCT INFORMATION DISCLOSURE Whether you are buying a house or refinancing an existing mortgage, this information can help you decide what type of mortgage is right for you. You

RESIDENTIAL MORTGAGE PRODUCT INFORMATION DISCLOSURE Whether you are buying a house or refinancing an existing mortgage, this information can help you decide what type of mortgage is right for you. You

Paragon 5. Financial Calculators User Guide

Paragon 5 Financial Calculators User Guide Table of Contents Financial Calculators... 3 Use of Calculators... 3 Mortgage Calculators... 4 15 Yr vs. 30 Year... 4 Adjustable Rate Amortizer... 4 Affordability...

Paragon 5 Financial Calculators User Guide Table of Contents Financial Calculators... 3 Use of Calculators... 3 Mortgage Calculators... 4 15 Yr vs. 30 Year... 4 Adjustable Rate Amortizer... 4 Affordability...

Fifth Third Home Buying Guide. A Guide to Residential Home Buying.

Fifth Third Home Buying Guide A Guide to Residential Home Buying. Important Contacts and Numbers. Use this page to record important information as you move through the homebuying process. Realtor/Builder

Fifth Third Home Buying Guide A Guide to Residential Home Buying. Important Contacts and Numbers. Use this page to record important information as you move through the homebuying process. Realtor/Builder

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

HOME BUYING MADE EASY. Live the dream of owning your own home.

HOME BUYING MADE EASY Live the dream of owning your own home. sm Getting started For most of us, buying our first home is a dream come true. It s also a lengthy process where potential and sometimes very

HOME BUYING MADE EASY Live the dream of owning your own home. sm Getting started For most of us, buying our first home is a dream come true. It s also a lengthy process where potential and sometimes very

Estimated Purchaser Cost Form

Buyer s Cost 1 Estimated Purchaser Cost Form When to use the form: 1. before showing property; 2. at the time of an offer and/or counteroffer; and, 3. prior to the closing. 2 Estimated Purchaser Cost Form

Buyer s Cost 1 Estimated Purchaser Cost Form When to use the form: 1. before showing property; 2. at the time of an offer and/or counteroffer; and, 3. prior to the closing. 2 Estimated Purchaser Cost Form

Welcome to the. Harvard Faculty Real Estate Services. Home Buying and Financing Seminar

Welcome to the Harvard Faculty Real Estate Services Home Buying and Financing Seminar Our Goals Outline the services offered through the Harvard University Real Estate Advantage Program, administered through

Welcome to the Harvard Faculty Real Estate Services Home Buying and Financing Seminar Our Goals Outline the services offered through the Harvard University Real Estate Advantage Program, administered through

HOME BUYING MADE EASY. Know what you need to get it right.

HOME BUYING MADE EASY Know what you need to get it right. HOME BUYING MADE EASY PNC, PNC AgentView and Home Insight are registered service marks of The PNC Financial Services Group, Inc. ( PNC ). PNC has

HOME BUYING MADE EASY Know what you need to get it right. HOME BUYING MADE EASY PNC, PNC AgentView and Home Insight are registered service marks of The PNC Financial Services Group, Inc. ( PNC ). PNC has

Chapter 11 Note Packet 11.1 Percents

Chapter 11 Note Packet Name: 11.1 Percents Example 1: A Yahoo! Question of the Week asked, "At what age do you consider someone old?" Out of the 3496 respondents, 1017 said that age 80 is old. What percent

Chapter 11 Note Packet Name: 11.1 Percents Example 1: A Yahoo! Question of the Week asked, "At what age do you consider someone old?" Out of the 3496 respondents, 1017 said that age 80 is old. What percent

HOME BUYING MADE EASY. Live the dream of owning your own home.

HOME BUYING MADE EASY Live the dream of owning your own home. HOME buying Made Easy PNC, PNC AgentView and Home Insight are registered service marks of The PNC Financial Services Group, Inc. ( PNC ). PNC

HOME BUYING MADE EASY Live the dream of owning your own home. HOME buying Made Easy PNC, PNC AgentView and Home Insight are registered service marks of The PNC Financial Services Group, Inc. ( PNC ). PNC

Consolidated by Commercial Bank Schedule D Loans Origination

6/30/2015 (a) First mortgage FHA-15 yrs 138 $ 13,642 $ 9 $ 11 3.36 (b) First mortgage VA-15 yrs 25 3,422 1 5 3.30 (c) First mortgage conventional conforming 15 yrs 508 57,084 344 164 3.06 (d) First mortgage

6/30/2015 (a) First mortgage FHA-15 yrs 138 $ 13,642 $ 9 $ 11 3.36 (b) First mortgage VA-15 yrs 25 3,422 1 5 3.30 (c) First mortgage conventional conforming 15 yrs 508 57,084 344 164 3.06 (d) First mortgage

NATIONAL INTERACTIVE STUDY GROUP UNIT 8 QUESTIONS

NATIONAL INTERACTIVE STUDY GROUP UNIT 8 QUESTIONS National Interactive Study Group 2 SESSION 8 JOHN MATHIS Notes for Tonight 1. To MUTE your phone line use *6 2. To UNMUTE your phone line use #6 3. Chat

NATIONAL INTERACTIVE STUDY GROUP UNIT 8 QUESTIONS National Interactive Study Group 2 SESSION 8 JOHN MATHIS Notes for Tonight 1. To MUTE your phone line use *6 2. To UNMUTE your phone line use #6 3. Chat

Different Types of Loans

Different Types of Loans All loans, no matter what they are, are either secured or unsecured. Knowing the difference can better help you understand how they work and what to expect when applying for one.

Different Types of Loans All loans, no matter what they are, are either secured or unsecured. Knowing the difference can better help you understand how they work and what to expect when applying for one.

The Adjustable Rate Loan, the Graduated Payment Loan, and Other Loan Arrangements

Chapter 43 The Adjustable Rate Loan, the Graduated Payment Loan, and Other Loan Arrangements INTRODUCTION When interest rates are generally stable from year to year, the fixed-rate amortized loan works

Chapter 43 The Adjustable Rate Loan, the Graduated Payment Loan, and Other Loan Arrangements INTRODUCTION When interest rates are generally stable from year to year, the fixed-rate amortized loan works

T14-1 REVIEW EXERCISES CHAPTER 14 SECTION I. Using Table 14-1 as needed, calculate the required information for the following. mortgages: 8.78 9.

T- REVIEW EXERCISES CHAPTER SECTION I Using Table - as needed, calculate the required information for the following mortgages: Amount Interest Term of Number of $,000s Table Monthly Total Financed Rate

T- REVIEW EXERCISES CHAPTER SECTION I Using Table - as needed, calculate the required information for the following mortgages: Amount Interest Term of Number of $,000s Table Monthly Total Financed Rate

Broker. Financing Real Estate. Chapter 12. Copyright Gold Coast Schools 1

Broker Chapter 12 Financing Real Estate Copyright Gold Coast Schools 1 Learning Objectives Describe the difference between a note and a mortgage Explain the benefits of having the first recorded lien on

Broker Chapter 12 Financing Real Estate Copyright Gold Coast Schools 1 Learning Objectives Describe the difference between a note and a mortgage Explain the benefits of having the first recorded lien on

SHOPPING FOR A MORTGAGE

SHOPPING FOR A MORTGAGE The Traditional Fixed-Rate Mortgage Key characteristics: Level payments, fixed interest rate, fixed term. This mortgage is the one which most of us know, and it is still the loan

SHOPPING FOR A MORTGAGE The Traditional Fixed-Rate Mortgage Key characteristics: Level payments, fixed interest rate, fixed term. This mortgage is the one which most of us know, and it is still the loan

Obtain Information from Several Lenders

ESPAÑOL Shopping around for a home loan or mortgage will help you to get the best financing deal. A mortgage--whether it s a home purchase, a refinancing, or a home equity loan--is a product, just like

ESPAÑOL Shopping around for a home loan or mortgage will help you to get the best financing deal. A mortgage--whether it s a home purchase, a refinancing, or a home equity loan--is a product, just like

Obtain Information from Several Lenders

Shopping around for a home loan or mortgage will help you to get the best financing deal. A mortgage--whether it s a home purchase, a refinancing, or a home equity loan--is a product, just like a car,

Shopping around for a home loan or mortgage will help you to get the best financing deal. A mortgage--whether it s a home purchase, a refinancing, or a home equity loan--is a product, just like a car,

Preparing for homeownership

Preparing for homeownership What we ll cover 1. Getting ready for homeownership 2. Mortgage basics 3. What you need to buy a home 4. Finding the right home 5. Resources 2 Getting ready for homeownership

Preparing for homeownership What we ll cover 1. Getting ready for homeownership 2. Mortgage basics 3. What you need to buy a home 4. Finding the right home 5. Resources 2 Getting ready for homeownership

Homeownership. Your First Steps toward. Getting Started. Know Your Finances. Which Mortgage Is Right for You?

Your First Steps toward Homeownership Identify the type of mortgage that meets your specific financial needs Getting Started Many people don t consider buying a home because they re afraid they can t afford

Your First Steps toward Homeownership Identify the type of mortgage that meets your specific financial needs Getting Started Many people don t consider buying a home because they re afraid they can t afford

MORTGAGE BANKING TERMS

MORTGAGE BANKING TERMS Acquisition cost: Add-on interest: In a HUD/FHA transaction, the price the borrower paid for the property plus any of the following costs: closing, repairs, or financing (except

MORTGAGE BANKING TERMS Acquisition cost: Add-on interest: In a HUD/FHA transaction, the price the borrower paid for the property plus any of the following costs: closing, repairs, or financing (except

HOME BUYING101. 701.255.0042 www.capcu.org i

HOME BUYING101 701.255.0042 www.capcu.org i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended,

HOME BUYING101 701.255.0042 www.capcu.org i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended,

Interest-Only Mortgage Payments and Payment-Option ARMs Are They for You?

Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation National Credit Union Administration Office of the Comptroller of the Currency Office of Thrift Supervision Interest-Only

Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation National Credit Union Administration Office of the Comptroller of the Currency Office of Thrift Supervision Interest-Only

Lesson 13: Applying for a Mortgage Loan

1 Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 2 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit unions

1 Real Estate Principles of Georgia Lesson 13: Applying for a Mortgage Loan 2 Choosing a Lender Types of lenders Types of lenders include: savings and loans commercial banks savings banks credit unions

Homebuyer Education: What You Need to Know

Homebuyer Education: What You Need to Know Today s Objectives Prepare your finances for home ownership Steps to mortgage prequalification Shopping for a home- who are the major players? Choosing the correct

Homebuyer Education: What You Need to Know Today s Objectives Prepare your finances for home ownership Steps to mortgage prequalification Shopping for a home- who are the major players? Choosing the correct

Consumer Handbook on Adjustable Rate Mortgages

Consumer Handbook on Adjustable Rate Mortgages Federal Reserve Board Office of Thrift supervision EQUAL HOUSING OPPORTUNITY This booklet was prepared in consultation with the following organizations: American

Consumer Handbook on Adjustable Rate Mortgages Federal Reserve Board Office of Thrift supervision EQUAL HOUSING OPPORTUNITY This booklet was prepared in consultation with the following organizations: American

CONSUMER HANDBOOK ON ADJUSTABLE RATE MORTGAGES Federal Reserve Board Office of Thrift Supervision

CONSUMER HANDBOOK ON ADJUSTABLE RATE MORTGAGES Federal Reserve Board Office of Thrift Supervision This booklet was prepared in consultation with the following organizations: American Bankers Association

CONSUMER HANDBOOK ON ADJUSTABLE RATE MORTGAGES Federal Reserve Board Office of Thrift Supervision This booklet was prepared in consultation with the following organizations: American Bankers Association

Guide to Purchasing a Home

Your journey to homeownership starts at your credit union. Purchasing your first home is a big decision, and it may even seem overwhelming. Rest assured Beacon Credit Union is here to assist you in understanding

Your journey to homeownership starts at your credit union. Purchasing your first home is a big decision, and it may even seem overwhelming. Rest assured Beacon Credit Union is here to assist you in understanding

Consumer Handbook on Adjustable Rate Mortgages Published by: Federal Reserve Board Office of Thrift Supervision EQUAL HOUSING OPPORTUNITY This

Consumer Handbook on Adjustable Rate Mortgages Published by: Federal Reserve Board Office of Thrift Supervision EQUAL HOUSING OPPORTUNITY This booklet was prepared in consultation with the following organizations:

Consumer Handbook on Adjustable Rate Mortgages Published by: Federal Reserve Board Office of Thrift Supervision EQUAL HOUSING OPPORTUNITY This booklet was prepared in consultation with the following organizations:

Adjustable Rate Mortgage (ARM) a mortgage with a variable interest rate, which adjusts monthly, biannually or annually.

a mortgage with a variable interest rate, which adjusts monthly, biannually or annually.") Glossary Adjustable Rate Mortgage (ARM) a mortgage with a variable interest rate, which adjusts monthly, biannually or annually. Amortization the way a loan is paid off over time in installments, detailing

Glossary Adjustable Rate Mortgage (ARM) a mortgage with a variable interest rate, which adjusts monthly, biannually or annually. Amortization the way a loan is paid off over time in installments, detailing

CONSUMER HANDBOOK ON ADJUSTABLE RATE MORTGAGES

CONSUMER HANDBOOK ON ADJUSTABLE RATE MORTGAGES This booklet was originally prepared by the Federal Reserve Board and the Office of Thrift Supervision in consultation with the following organizations: American

CONSUMER HANDBOOK ON ADJUSTABLE RATE MORTGAGES This booklet was originally prepared by the Federal Reserve Board and the Office of Thrift Supervision in consultation with the following organizations: American

Mortgage Terms. Appraisal An estimate of the value of property, made by a qualified professional called an "appraiser".

Mortgage Terms Acceleration The right of the mortgagee (lender) to demand the immediate repayment of the mortgage loan balance upon the default of the mortgagor (borrower), or by using the right vested

Mortgage Terms Acceleration The right of the mortgagee (lender) to demand the immediate repayment of the mortgage loan balance upon the default of the mortgagor (borrower), or by using the right vested

GLOSSARY COMMONLY USED REAL ESTATE TERMS

GLOSSARY COMMONLY USED REAL ESTATE TERMS Adjustable-Rate Mortgage (ARM): a mortgage loan with an interest rate that is subject to change and is not fixed at the same level for the life of the loan. These

GLOSSARY COMMONLY USED REAL ESTATE TERMS Adjustable-Rate Mortgage (ARM): a mortgage loan with an interest rate that is subject to change and is not fixed at the same level for the life of the loan. These

MORTGAGE TERMINOLOGY DEFINED

MORTGAGE TERMINOLOGY DEFINED 1-year Adjustable Rate Mortgage Mortgage where the annual rate changes yearly. The rate is usually based on movements of a published index plus a specified margin, chosen by

MORTGAGE TERMINOLOGY DEFINED 1-year Adjustable Rate Mortgage Mortgage where the annual rate changes yearly. The rate is usually based on movements of a published index plus a specified margin, chosen by

Purchasing and Financing a Home

Purchasing and Financing a Home C H A P T E R 9 degree, the Stockwells discovered that both of them could pursue their careers right where they were. For the first year, their rent was $550 per month.

Purchasing and Financing a Home C H A P T E R 9 degree, the Stockwells discovered that both of them could pursue their careers right where they were. For the first year, their rent was $550 per month.

Bokern Realty serving St. Louis since 1901. Home Buying Educational Seminar The WU Employer Assisted Housing Program

Home Buying Educational Seminar The WU Employer Assisted Housing Program Agenda WU Employer Assisted Housing Program Program highlights Neighborhoods Home Financing Benefits of homeownership Preparation

Home Buying Educational Seminar The WU Employer Assisted Housing Program Agenda WU Employer Assisted Housing Program Program highlights Neighborhoods Home Financing Benefits of homeownership Preparation

Understanding Consumer and Mortgage Loans

Personal Finance: Another Perspective Classroom Slides: Understanding Consumer and Mortgage Loans Updated 2014-02-04 1 Objectives A. Understand how consumer loans can keep you from your goals B. Understand

Personal Finance: Another Perspective Classroom Slides: Understanding Consumer and Mortgage Loans Updated 2014-02-04 1 Objectives A. Understand how consumer loans can keep you from your goals B. Understand

CONSUMER HANDBOOK ON ADJUSTABLE RATE MORTGAGES

CONSUMER HANDBOOK ON ADJUSTABLE RATE MORTGAGES Federal Reserve Board Office of Thrift Supervision This booklet was originally prepared in consultation with the following organizations: American Bankers

CONSUMER HANDBOOK ON ADJUSTABLE RATE MORTGAGES Federal Reserve Board Office of Thrift Supervision This booklet was originally prepared in consultation with the following organizations: American Bankers

Participant Guide Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum

Your Own Home Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page To Rent or Own 1 Steps Involved in Buying a Home 2 Am I Ready to Buy a Home? 3 Patricia

Your Own Home Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page To Rent or Own 1 Steps Involved in Buying a Home 2 Am I Ready to Buy a Home? 3 Patricia

Your Guide To Home Financing

Your Guide To Home Financing You re buying your first home. We have an easy mortgage solution. When buying a home, the world of mortgages can be intimidating and overwhelming. The key to feeling good about

Your Guide To Home Financing You re buying your first home. We have an easy mortgage solution. When buying a home, the world of mortgages can be intimidating and overwhelming. The key to feeling good about

Homebuyer s Handbook

Homebuyer s Handbook Understanding the home buying process Buying a home is one of life s most exciting events and is still one of the smartest investments you can make. But the process of finding, buying

Homebuyer s Handbook Understanding the home buying process Buying a home is one of life s most exciting events and is still one of the smartest investments you can make. But the process of finding, buying

Appendix B: Cash Flow Analysis. I. Introduction

I. Introduction The calculation of the economic value of the MMI Fund involves the estimation of the present value of future cash flows generated by the existing portfolio. This requires the projection

I. Introduction The calculation of the economic value of the MMI Fund involves the estimation of the present value of future cash flows generated by the existing portfolio. This requires the projection

HOME BUYING101 TM %*'9 [[[ EPXEREJGY SVK i

HOME BUYING101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

HOME BUYING101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

Appreciation is one way that the the difference between the market value of property and the amount owed on it increases.

Chapter 22 Buying a Home 22.1 Why Buy a Home? Vocab Market value appraised value assessed value Equity conventional loan FHA loan Trust deed escrow account discount points Loan origination fee closing

Chapter 22 Buying a Home 22.1 Why Buy a Home? Vocab Market value appraised value assessed value Equity conventional loan FHA loan Trust deed escrow account discount points Loan origination fee closing

Looking for the Best Mortgage?

Looking for the Best Mortgage? Shop, Compare, Negotiate Shopping around for a home loan or mortgage will help you to get the best financing deal. A mortgage whether it s a home purchase, a refinancing,

Looking for the Best Mortgage? Shop, Compare, Negotiate Shopping around for a home loan or mortgage will help you to get the best financing deal. A mortgage whether it s a home purchase, a refinancing,

Homebuyers Dictionary

2935 Breezewood Avenue Suite 100 Fayetteville, NC 28303 www.fayhba.org Homebuyers Dictionary ARM? GPM? PITI? You d have to be a cryptologist to figure out some of the terms buyers encounter during the

2935 Breezewood Avenue Suite 100 Fayetteville, NC 28303 www.fayhba.org Homebuyers Dictionary ARM? GPM? PITI? You d have to be a cryptologist to figure out some of the terms buyers encounter during the

BUYING A HOME BUILDING A HOME REFINANCING

Guide to Mortgages BUYING A HOME BUILDING A HOME REFINANCING Trust People First For Your Mortgage Needs People First is committed to providing our members with quality mortgage products that are both competitive

Guide to Mortgages BUYING A HOME BUILDING A HOME REFINANCING Trust People First For Your Mortgage Needs People First is committed to providing our members with quality mortgage products that are both competitive

Case Study 1: Adjustable-Rate Home Mortgage Loan Concepts illustrated: Time value of money, equivalence calculation, and loan analysis. Required readings: Chapters 4 and 5. 1 Background Buying a home today

Case Study 1: Adjustable-Rate Home Mortgage Loan Concepts illustrated: Time value of money, equivalence calculation, and loan analysis. Required readings: Chapters 4 and 5. 1 Background Buying a home today

Federal Housing Administration [FHA] and Veterans Administration [VA] Loan Programs A. LOAN PROGRAMS OF THE FEDERAL HOUSING ADMINISTRATION (FHA)

![Federal Housing Administration [FHA] and Veterans Administration [VA] Loan Programs A. LOAN PROGRAMS OF THE FEDERAL HOUSING ADMINISTRATION (FHA)](/thumbs/25/5268134.jpg "Federal Housing Administration [FHA] and Veterans Administration [VA] Loan Programs A. LOAN PROGRAMS OF THE FEDERAL HOUSING ADMINISTRATION (FHA)") Chapter 42 Federal Housing Administration [FHA] and Veterans Administration [VA] Loan Programs A. LOAN PROGRAMS OF THE FEDERAL HOUSING ADMINISTRATION (FHA) INTRODUCTION Besides conventional loans discussed

Chapter 42 Federal Housing Administration [FHA] and Veterans Administration [VA] Loan Programs A. LOAN PROGRAMS OF THE FEDERAL HOUSING ADMINISTRATION (FHA) INTRODUCTION Besides conventional loans discussed

Chapter 15 Questions Real Estate Financing: Practice

Chapter 15 Questions Real Estate Financing: Practice 1. Kahlid has been making periodic payments of principal and interest on a loan, but the final payment will be larger than the others. This is a(n)

Chapter 15 Questions Real Estate Financing: Practice 1. Kahlid has been making periodic payments of principal and interest on a loan, but the final payment will be larger than the others. This is a(n)

Fin 4713 Chapter 6. Interest Rate Risk. Interest Rate Risk. Alternative Mortgage Instruments. Interest Rate Risk. Alternative Mortgage Instruments

Fin 4713 Chapter 6 Chapter 6 Learning Objectives Understand alternative mortgage instruments Understand how the characteristics of various AMIs solve the problems of a fixed-rate mortgage Alternative Mortgage

Fin 4713 Chapter 6 Chapter 6 Learning Objectives Understand alternative mortgage instruments Understand how the characteristics of various AMIs solve the problems of a fixed-rate mortgage Alternative Mortgage

Settlement Disclosure

Settlement Disclosure This form is a statement of final loan terms and actual closing costs. Settlement information Date 12/13/2011 Agent Martha Jones Location ABC Settlement 54321 Random Blvd, Ste 405

Settlement Disclosure This form is a statement of final loan terms and actual closing costs. Settlement information Date 12/13/2011 Agent Martha Jones Location ABC Settlement 54321 Random Blvd, Ste 405

Home Mortgage Search Process By Geoff Wells

Home Mortgage Search Process By Geoff Wells 2013 1 Introduction The purpose of document is to provide home mortgage shopping information for new home buyers and existing home buyers looking to refinance.

Home Mortgage Search Process By Geoff Wells 2013 1 Introduction The purpose of document is to provide home mortgage shopping information for new home buyers and existing home buyers looking to refinance.

Homebuyer s Guide. Brought to you by:

Homebuyer s Guide Brought to you by: AmeriSouth Mortgage Company NMLS ID: 67050 Phone: (704) 845-9400 info@amerisouth.com www.amerisouth.com The basics What is a mortgage? A mortgage is a loan secured

Homebuyer s Guide Brought to you by: AmeriSouth Mortgage Company NMLS ID: 67050 Phone: (704) 845-9400 info@amerisouth.com www.amerisouth.com The basics What is a mortgage? A mortgage is a loan secured

MORTGAGE DICTIONARY. Amortization - Amortization is a decrease in the value of assets with time, which is normally the useful life of tangible assets.

MORTGAGE DICTIONARY Adjustable-Rate Mortgage An adjustable-rate mortgage (ARM) is a product with a floating or variable rate that adjusts based on some index. Amortization - Amortization is a decrease

MORTGAGE DICTIONARY Adjustable-Rate Mortgage An adjustable-rate mortgage (ARM) is a product with a floating or variable rate that adjusts based on some index. Amortization - Amortization is a decrease

Arkansas Development Finance Authority

Arkansas Development Finance Authority ADFA S MORTGAGE BOND PROGRAM Arkansas Development Finance Authority P.O. Box 8023 Little Rock, AR 72203 www.arkansas.gov/adfa Home ToOwn Staff Murray Harding-Manager

Arkansas Development Finance Authority ADFA S MORTGAGE BOND PROGRAM Arkansas Development Finance Authority P.O. Box 8023 Little Rock, AR 72203 www.arkansas.gov/adfa Home ToOwn Staff Murray Harding-Manager

GLOSSARY OF TERMS. Adjustment Date: The date that the interest rate changes on an adjustable-rate mortgage.

GLOSSARY OF TERMS A Acceleration: The right of the mortgagee (lender) to demand the immediate repayment of the mortgage loan balance upon the default of the mortgager (borrower), or by using the right

GLOSSARY OF TERMS A Acceleration: The right of the mortgagee (lender) to demand the immediate repayment of the mortgage loan balance upon the default of the mortgager (borrower), or by using the right

presents Understanding VA Hybrid ARM Loans NMLS #1109426

presents Understanding VA Hybrid ARM Loans NMLS #1109426 Decide if a Hybrid ARM is right for you... This guide is a start-to-finish explanation of the VA Hybrid ARM program. We ll begin by discussing what

presents Understanding VA Hybrid ARM Loans NMLS #1109426 Decide if a Hybrid ARM is right for you... This guide is a start-to-finish explanation of the VA Hybrid ARM program. We ll begin by discussing what

Shopping for your home loan. Settlement cost booklet

Shopping for your home loan Settlement cost booklet January 2014 This booklet was initially prepared by the U.S. Department of Housing and Urban Development. The Consumer Financial Protection Bureau (CFPB)

Shopping for your home loan Settlement cost booklet January 2014 This booklet was initially prepared by the U.S. Department of Housing and Urban Development. The Consumer Financial Protection Bureau (CFPB)

Choosing the Best Mortgage

A HOME FOR YOUR FAMILY 12 Choosing the Best Mortgage Distributed in furtherance of the Acts of Congress of May 8 and June 30, 1914. Employment and program opportunities are offered to all people regardless

A HOME FOR YOUR FAMILY 12 Choosing the Best Mortgage Distributed in furtherance of the Acts of Congress of May 8 and June 30, 1914. Employment and program opportunities are offered to all people regardless

The Mortgage Market. Concepts and Buzzwords. Readings. Tuckman, chapter 21.

The Mortgage Market Concepts and Buzzwords The Mortgage Market The Basic Fixed Rate Mortgage Prepayments mortgagor, mortgagee, PTI and LTV ratios, fixed-rate, GPM, ARM, balloon, GNMA, FNMA, FHLMC, Private

The Mortgage Market Concepts and Buzzwords The Mortgage Market The Basic Fixed Rate Mortgage Prepayments mortgagor, mortgagee, PTI and LTV ratios, fixed-rate, GPM, ARM, balloon, GNMA, FNMA, FHLMC, Private

7. Consumer and Mortgage Loans

7. Consumer and Mortgage Loans Introduction For many years, inspired religious leaders have urged their followers to get out of debt and live within their means. Gordon B. Hinckley spoke directly to members

7. Consumer and Mortgage Loans Introduction For many years, inspired religious leaders have urged their followers to get out of debt and live within their means. Gordon B. Hinckley spoke directly to members

Is now a good time to refinance?

Is now a good time to refinance? Our Business Is The American Dream At Fannie Mae, we are in the American Dream business. Our Mission is to tear down barriers, lower costs, and increase the opportunities

Is now a good time to refinance? Our Business Is The American Dream At Fannie Mae, we are in the American Dream business. Our Mission is to tear down barriers, lower costs, and increase the opportunities

Insert Realtor/ Builder logo. Insert affiliate Bank logo

Insert affiliate Bank logo 1 Insert Realtor/ Builder logo Your Step-By-Step Guide HOME BUYERS HANDBOOK Purchasing a home is one of the most important decisions you will ever make. A home can be an excellent

Insert affiliate Bank logo 1 Insert Realtor/ Builder logo Your Step-By-Step Guide HOME BUYERS HANDBOOK Purchasing a home is one of the most important decisions you will ever make. A home can be an excellent

Non Depository/Mortgage Institutions Schedule D Loans Origination

6/30/2015 Total Number Amount Discount Weighted (1) First mortgage FHA-15 yrs 24 $ 2,165 $0 $ 15 3.95 (2) First mortgage VA-15 yrs 12 2,428 15 13 3.61 (3) First mortgage conventional conforming 15 yrs

6/30/2015 Total Number Amount Discount Weighted (1) First mortgage FHA-15 yrs 24 $ 2,165 $0 $ 15 3.95 (2) First mortgage VA-15 yrs 12 2,428 15 13 3.61 (3) First mortgage conventional conforming 15 yrs

Definitions. In some cases a survey rather than an ILC is required.

Definitions 1. What is the closing? The closing is a formal meeting at which both the buyer and seller meet to sign all the final documentation required for the buyer's mortgage loan. Once the closing

Definitions 1. What is the closing? The closing is a formal meeting at which both the buyer and seller meet to sign all the final documentation required for the buyer's mortgage loan. Once the closing

Conventional Financing

Chapter 6 Conventional Financing 1 Chapter Objectives Identify the characteristics of a conventional loan. Define amortization. Identify different types of conventional loans. Discuss the use of private

Chapter 6 Conventional Financing 1 Chapter Objectives Identify the characteristics of a conventional loan. Define amortization. Identify different types of conventional loans. Discuss the use of private

Mortgages and Mortgage -Backed Securiti curi es ti Mortgage ort gage securitized mortgage- backed securities (MBSs) Primary Pri mary Mortgage Market

Primary Pri mary Mortgage Market") Mortgages and Mortgage-Backed Securities Mortgage Markets Mortgages are loans to individuals or businesses to purchase homes, land, or other real property Many mortgages are securitized Many mortgages

Mortgages and Mortgage-Backed Securities Mortgage Markets Mortgages are loans to individuals or businesses to purchase homes, land, or other real property Many mortgages are securitized Many mortgages

Program Overview For MRED

Program Overview For MRED 1 How searching for a new home has changed: Over 90% of homebuyers begin their search and view property listings online Over 72% of these homebuyers then EXIT the listing to search

Program Overview For MRED 1 How searching for a new home has changed: Over 90% of homebuyers begin their search and view property listings online Over 72% of these homebuyers then EXIT the listing to search

The Pr o f e s s i o n a l La n d l o r d Ho w To

The Pr o f e s s i o n a l La n d l o r d Ho w To Providing Property Management Solutions for Over 25 Years Setting up a Loan What follows is one possible way to record a loan and payments of that loan.

The Pr o f e s s i o n a l La n d l o r d Ho w To Providing Property Management Solutions for Over 25 Years Setting up a Loan What follows is one possible way to record a loan and payments of that loan.

5+ Key Components To Most Adjustable Rate Mortgages

5+ Key Components To Most Adjustable Rate Mortgages 1. Index rate The rate to which the interest rate on an adjustable rate loan is tied. One of the more popular indexes used is the 1-year U.S. Treasury

5+ Key Components To Most Adjustable Rate Mortgages 1. Index rate The rate to which the interest rate on an adjustable rate loan is tied. One of the more popular indexes used is the 1-year U.S. Treasury

SELLER S NET & BUYER S COST

SELLER S NET & BUYER S COST Closing Day The day of closing is the responsibility of the seller with the exception of prepaid interest on a new loan and a new insurance policy. Taxes nsurance nterest New

SELLER S NET & BUYER S COST Closing Day The day of closing is the responsibility of the seller with the exception of prepaid interest on a new loan and a new insurance policy. Taxes nsurance nterest New

OPENING DOORS WITH OUR RESIDENTIAL LENDING

OPENING DOORS WITH OUR RESIDENTIAL LENDING We offer a wide range of options for homebuyers and homeowners looking to refinance. OPENING DOORS WITH OUR RESIDENTIAL LENDING THE FINANCING SOLUTION YOU SEEK.

OPENING DOORS WITH OUR RESIDENTIAL LENDING We offer a wide range of options for homebuyers and homeowners looking to refinance. OPENING DOORS WITH OUR RESIDENTIAL LENDING THE FINANCING SOLUTION YOU SEEK.

Glossary of Terms. Here are some helpful definitions to common terms.

Glossary of Terms Here are some helpful definitions to common terms. 1003 Loan application 4506 IRS form requesting copy of tax return Abstract of title A historical summary provided by a title insurance

Glossary of Terms Here are some helpful definitions to common terms. 1003 Loan application 4506 IRS form requesting copy of tax return Abstract of title A historical summary provided by a title insurance

Reverse Mortgage Glossary of Terms

Reverse Mortgage Glossary of Terms Acceleration Clause Adjustable Rate Annuity Appraisal Appreciation Available Principle Limit Change of Circumstance Closing Condemnation Correspondent Cost to Cure Credit

Reverse Mortgage Glossary of Terms Acceleration Clause Adjustable Rate Annuity Appraisal Appreciation Available Principle Limit Change of Circumstance Closing Condemnation Correspondent Cost to Cure Credit

Good Faith Estimate (GFE)

") OMB Approval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Originator Address Borrower Property Address Originator Phone Number Originator Email Date of GFE Purpose Shopping for your loan

OMB Approval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Originator Address Borrower Property Address Originator Phone Number Originator Email Date of GFE Purpose Shopping for your loan

lesson three buying a home overheads

lesson three buying a home overheads the home-buying process phase 1: determine home ownership needs What type of housing should I (we) buy? How much can I (we) afford to spend? phase 2: locate and evaluate

lesson three buying a home overheads the home-buying process phase 1: determine home ownership needs What type of housing should I (we) buy? How much can I (we) afford to spend? phase 2: locate and evaluate

Mortgage Terms. Accrued interest Interest that is earned but not paid, adding to the amount owed.

Mortgage Terms Accrued interest Interest that is earned but not paid, adding to the amount owed. Negative amortization A rise in the loan balance when the mortgage payment is less than the interest due.

Mortgage Terms Accrued interest Interest that is earned but not paid, adding to the amount owed. Negative amortization A rise in the loan balance when the mortgage payment is less than the interest due.

Dr. Debra Sherrill Central Piedmont Community College

Dr. Debra Sherrill Central Piedmont Community College 1 2 Describe the benefits and pitfalls of renting versus owning a home. List the steps required to obtain a mortgage loan. Identify mortgage options

Dr. Debra Sherrill Central Piedmont Community College 1 2 Describe the benefits and pitfalls of renting versus owning a home. List the steps required to obtain a mortgage loan. Identify mortgage options

CITY AND COUNTY OF DENVER, COLORADO 2015 MORTGAGE CREDIT CERTIFICATE (MCC) PROGRAM PROGRAM SUMMARY AND GUIDELINES. January 1, 2015

PROGRAM PROGRAM SUMMARY AND GUIDELINES. January 1, 2015") CITY AND COUNTY OF DENVER, COLORADO 2015 MORTGAGE CREDIT CERTIFICATE (MCC) PROGRAM PROGRAM SUMMARY AND GUIDELINES January 1, 2015 PURPOSE The purposes of the MCC Program are to: Provide a first-time homebuyer

CITY AND COUNTY OF DENVER, COLORADO 2015 MORTGAGE CREDIT CERTIFICATE (MCC) PROGRAM PROGRAM SUMMARY AND GUIDELINES January 1, 2015 PURPOSE The purposes of the MCC Program are to: Provide a first-time homebuyer

PURCHASE MORTGAGE. Mortgage loan types

PURCHASE MORTGAGE Mortgage loan types There are many types of mortgages used worldwide, but several factors broadly define the characteristics of the mortgage. All of these may be subject to local regulation

PURCHASE MORTGAGE Mortgage loan types There are many types of mortgages used worldwide, but several factors broadly define the characteristics of the mortgage. All of these may be subject to local regulation

Mortgage Lending Basics

Welcome to PMI s On Demand Training Bootcamp Mortgage Lending Basics PRESENTED BY PMI MORTGAGE INSURANCE CO. Introduction to Mortgage Lending Course Overview Mortgage Lending Basics Origination Process

Welcome to PMI s On Demand Training Bootcamp Mortgage Lending Basics PRESENTED BY PMI MORTGAGE INSURANCE CO. Introduction to Mortgage Lending Course Overview Mortgage Lending Basics Origination Process

Title Insurance Glossary

Title Insurance Glossary Abstract of Title A condensed history or summary of all transactions affecting a particular tract of land. Adjustable Rate Mortgages Mortgages with an interest rate that may change

Title Insurance Glossary Abstract of Title A condensed history or summary of all transactions affecting a particular tract of land. Adjustable Rate Mortgages Mortgages with an interest rate that may change

A mortgage is a loan that is used to finance the purchase of your home. It consists of 5 parts: collateral, principal, interest, taxes, and insurance.

A mortgage is a loan that is used to finance the purchase of your home. It consists of 5 parts: collateral, principal, interest, taxes, and insurance. When you agree to a mortgage, you enter into a legal

A mortgage is a loan that is used to finance the purchase of your home. It consists of 5 parts: collateral, principal, interest, taxes, and insurance. When you agree to a mortgage, you enter into a legal

Accounts payable Money which you owe to an individual or business for goods or services that have been received but not yet paid for.

A Account A record of a business transaction. A contract arrangement, written or unwritten, to purchase and take delivery with payment to be made later as arranged. Accounts payable Money which you owe

A Account A record of a business transaction. A contract arrangement, written or unwritten, to purchase and take delivery with payment to be made later as arranged. Accounts payable Money which you owe

If P = principal, r = annual interest rate, and t = time (in years), then the simple interest I is given by I = P rt.

, then the simple interest I is given by I = P rt.") 13 Consumer Mathematics 13.1 The Time Value of Money Start with some Definitions: Definition 1. The amount of a loan or a deposit is called the principal. Definition 2. The amount a loan or a deposit increases

13 Consumer Mathematics 13.1 The Time Value of Money Start with some Definitions: Definition 1. The amount of a loan or a deposit is called the principal. Definition 2. The amount a loan or a deposit increases

MORTGAGE TERMS. Assignment of Mortgage A document used to transfer ownership of a mortgage from one party to another.

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

VA financing- Serving the homeownership needs of those who serve our country

VA financing- Serving the homeownership needs of those who serve our country Paul M. Carter Home Mortgage Consultant NMLSR ID 49022 Warwick City Hall Warwick, RI September 12, 2012 Agenda Current industry

VA financing- Serving the homeownership needs of those who serve our country Paul M. Carter Home Mortgage Consultant NMLSR ID 49022 Warwick City Hall Warwick, RI September 12, 2012 Agenda Current industry

HOMEBUYER S MORTGAGE GUIDE

WWW.WINTRUSTMORTGAGE.COM WINTRUST.COM/MYHOME HOMEBUYER S MORTGAGE GUIDE HELPFUL INFORMATION ABOUT THE MORTGAGE PROCESS TO GUIDE YOU AS YOU PURCHASE YOUR NEW HOME. www.wintrust.com/myhome WHY WINTRUST?

WWW.WINTRUSTMORTGAGE.COM WINTRUST.COM/MYHOME HOMEBUYER S MORTGAGE GUIDE HELPFUL INFORMATION ABOUT THE MORTGAGE PROCESS TO GUIDE YOU AS YOU PURCHASE YOUR NEW HOME. www.wintrust.com/myhome WHY WINTRUST?

Instructor Guide Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum

Your Own Home Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Module Overview 1 Purpose 1 Objectives 1 Time 1 Materials and Equipment Needed to Present

Your Own Home Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Module Overview 1 Purpose 1 Objectives 1 Time 1 Materials and Equipment Needed to Present

MSHDA's Down Payment Assistance and Mortgage Credit Certificate. May 21, 2010 (3:30 5:00 p.m.) Facilitated by: Carol Brito (MSHDA) Sponsored by:

Facilitated by: Carol Brito (MSHDA) Sponsored by:") MSHDA's Down Payment Assistance and Mortgage Credit Certificate May 21, 2010 (3:30 5:00 p.m.) Facilitated by: Carol Brito (MSHDA) Sponsored by: CREDIT UNIONS A DRIVING FORCE OF COMMUNITIES MSHDA Overview

MSHDA's Down Payment Assistance and Mortgage Credit Certificate May 21, 2010 (3:30 5:00 p.m.) Facilitated by: Carol Brito (MSHDA) Sponsored by: CREDIT UNIONS A DRIVING FORCE OF COMMUNITIES MSHDA Overview

Home Buyers. from application to closing. Derek Haley, Senior Loan Officer SunTrust Mortgage, Inc. 919.426.5023 Derek.Haley@SunTrust.

Information for First-time Home Buyers An overview of the mortgage process, from application to closing. Derek Haley, Senior Loan Officer SunTrust Mortgage, Inc. 919.426.5023 Derek.Haley@SunTrust.com NMLSR#

Information for First-time Home Buyers An overview of the mortgage process, from application to closing. Derek Haley, Senior Loan Officer SunTrust Mortgage, Inc. 919.426.5023 Derek.Haley@SunTrust.com NMLSR#

Appendix B: Cash Flow Analysis. I. Introduction

I. Introduction The calculation of the economic value of the MMI Fund involves the estimation of the present value of future cash flows generated by the existing portfolio and future books of business.

I. Introduction The calculation of the economic value of the MMI Fund involves the estimation of the present value of future cash flows generated by the existing portfolio and future books of business.

Finance 197. Simple One-time Interest

Finance 197 Finance We have to work with money every day. While balancing your checkbook or calculating your monthly expenditures on espresso requires only arithmetic, when we start saving, planning for

Finance 197 Finance We have to work with money every day. While balancing your checkbook or calculating your monthly expenditures on espresso requires only arithmetic, when we start saving, planning for

How To Get A Home Equity Line Of Credit

A GUIDE TO HOME EQUITY LINES OF CREDIT Call or visit one of our offices today to see what products in this guide we have to offer you! TABLE OF CONTENTS Introduction What is a home equity line of credit

A GUIDE TO HOME EQUITY LINES OF CREDIT Call or visit one of our offices today to see what products in this guide we have to offer you! TABLE OF CONTENTS Introduction What is a home equity line of credit

Teacher's Guide. Lesson Five. Buying a Home 04/09

Teacher's Guide $ Lesson Five Buying a Home 04/09 buying a home websites Buying a Home is a major life milestone that requires some thoughtful planning and know-how. Students need to understand all aspects

Teacher's Guide $ Lesson Five Buying a Home 04/09 buying a home websites Buying a Home is a major life milestone that requires some thoughtful planning and know-how. Students need to understand all aspects

Chapter 4: Managing Your Money Lecture notes Math 1030 Section D

Section D.1: Loan Basics Definition of loan principal For any loan, the principal is the amount of money owed at any particular time. Interest is charged on the loan principal. To pay off a loan, you must

Section D.1: Loan Basics Definition of loan principal For any loan, the principal is the amount of money owed at any particular time. Interest is charged on the loan principal. To pay off a loan, you must

HOMEOWNERSHIP: Understanding What You Can Afford, Mortgages, and Closing Costs. Illinois Association of REALTORS. Springfield, IL 62701

Illinois Association of REALTORS 522 S. Fifth Street Springfield, IL 62701 www.illinoisrealtor.org www.yourillinoishome.com HOMEOWNERSHIP: Understanding What You Can Afford, Mortgages, and Closing Costs

Illinois Association of REALTORS 522 S. Fifth Street Springfield, IL 62701 www.illinoisrealtor.org www.yourillinoishome.com HOMEOWNERSHIP: Understanding What You Can Afford, Mortgages, and Closing Costs