RETIREMENT PLANS IN MEXICO DEVELOPMENT AND OPPORTUNITIES BY ACT. JUAN JOSE SOLORZANO AND ACT. MARCELA FLORES I PREFACE

|

|

|

- Benedict Paul

- 8 years ago

- Views:

Transcription

1 RETIREMENT PLANS IN MEXICO DEVELOPMENT AND OPPORTUNITIES BY ACT. JUAN JOSE SOLORZANO AND ACT. MARCELA FLORES I PREFACE The actual pension plans in Mexico have been considered in general not a real benefit for the companies, but.an option to replace old employees, when they reach a retiring age, that ranges between 55 to 65 years old. The Mexican Federal Labor Law stipulates that any company that desires- to dismiss an employee, must compensate him by giving him three months of his salary plus 20 days per year of service of the same sala,ry. This salary includes proportional part of christmas and holidays bonus. This payment is known as Legal Indemnity. tkoogh ~ven./retirement by age is not a real cause to dismiss an employee, most of the companies in Mexico consider the above mentioned items as the Legal Indemnity stipulated by law to retire an employee.

2 the Mexican companies have adopted the following: * Reviewer Notes: (1) quoted = contributed (2) salary quotation = covered salary (3) quotes = contributions.

quotes =")

3 b) ~ormal Plan.- Set up a pension plan for retirement concepts in order to yield periodic payments, which actuarial value at retirement age will be the total legal indemnity. In practice the employee receives the actuarial value in a lump sum. These plans are based upon.6x the average salary during last year. by seniority and The actuarial value of a pension with the above features, for life and at a 6.0% interest rate in the annuity calculation, will always be inferior to the three months salary plus 20 days per year as legal indemnity, and then the pension plan sets up that the actuarial value will not be lower to such amount. With this kind of pension plan, some companies add additional pensions to those employees with wages over 10 times the minirrlrlrrlsalary, in order to compensate them farthe low pension payment from the Social Security. SO this item of the retirement plans is what the employees with superior salaries consider a good fringe benefit.

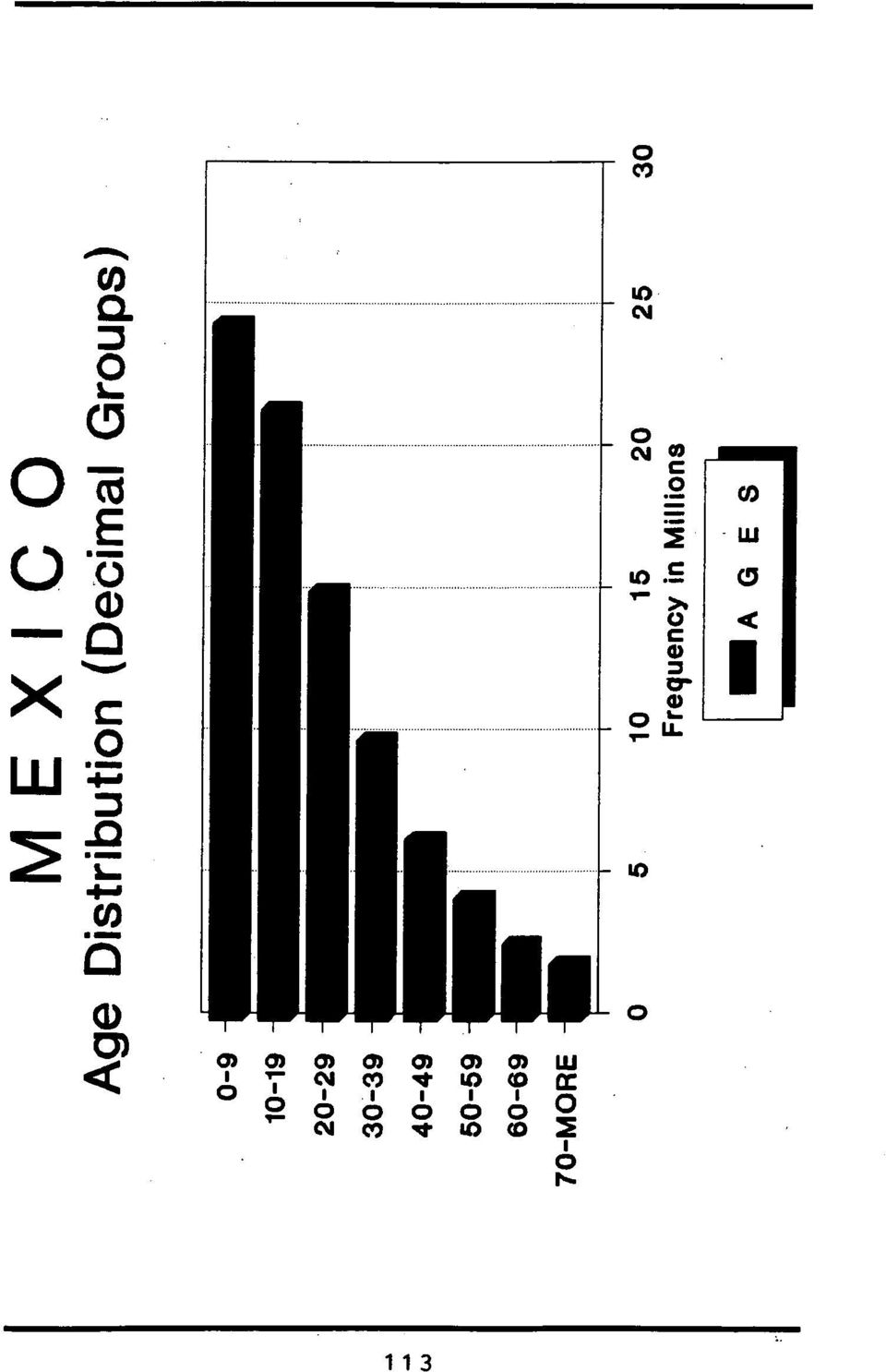

4 Other existing problem is that in general the employee who gets his retirement payment in a lump sum, it is usually not managed adequately and shortly he runs out of it counting, only with the Social Security resource. It is common that the companies with informal Pension plans or with out specific definition for the future of such payments, have not created any kind of fund or reserve, so when a person reaches the retirement age, the financial results of that accountant year are drastically affected. Only those companies with defined retirement plans, create funds, and/or trusts getting fiscal benefits for the contributions as for the interest generated from such funds, which are considered as not aggregate income for tax purposes. Companies with informal pension plans do not get any fiscal benefit until the payment is realized, so they can not record this liability when it is generated, but until it is required. One of the reasons why Mexican companies and their employees are not aware of retirement plans, is due that the number of retirement cases is pretty low* mainly because the country has a distribution of ages, according with the following figures in table one. I

5

6 Due to the above, workers affiliated to Mexican unions and employees prefer other kind of fringe benefit instead of the retirement plans, because they think it is a long term fringe benefit. Also in our country there is no culture in retirement matters and,with experience, the person who retires and was used to work his whole life, gets the feeling of becoming useless, and his life w i l l change drastically. 11. FISCAL BENEFITS 11.1 For the com~qpies. Contributions invested in an external fund for financing the liabilities, are income tax deductable and the interest generated from these funds is considered not aggregated income for tax purposes For the em~lo~ee. The compensation from an informal pension plan or the legal indemnity for an employee with 65 years old and 30 years of service, has a tax exemption of 36 million Mexican pesos ($11,650 dollars approx. ). Under a retirement plan, pensions paid during periodically terms are subject of tax deductions for the equivalent amount of 9 minimum salaries, 1.E. $ 3.6 million by month ($ 1,165 dollars approx.).

7 If the amount granted to an employee is paid through a retirement plan in one lump sum, the tax deduction is for $ 430 million pesos ($ 140,000 dollars approx. ), for a 65 years old employee with 30 years of service. So as it was shown above, tax exempt benefits are superior for those companies with established retirement plans MODIFICATIONS FOR Retirement matters. As of February 24, 1992 the Mexican Government improved the Social Security Law, adding to it a "Retirement Insurance", consisting in the following: (3) Employers are obliged to pay quotes of the 2% of the employees' salaries, through bank institutions, to be depositqd into individual accounts through a saving and retirement System under each employee name. The salary quotatiof'to be considered for this insurance will have a maximum limit of 25 minimum wage in force ($ 3,235 dollars approx.).

Employers are obliged to pay quotes of the 2%")

8 (3) Quotes received in the banks from the Social Security, must be deposited into an individual account in the Bank of Mexico, and it w i l l invest them in credits in charge of the Federal government. These credits w i l l be adjusted month by month according with inflation level officially published by the Bank of Mexico and w i l l generate interest rates no lower than 2% annuity monthly payable and reinvested in the same accounts. The puoteso)uill generate interest from the 4Th laborable- day received from the banks, which represents a minor effective interest rate for the employee. The employee could Withdraw the money from his account, when reaching the,retirement age, I.E. at 65 years old or before at 60 years old or in case of a 50% disability, or total disability. a) FOP buying a life annuity with tax exemption of 9 minimum wages in force ($ 1,165 dollars approx.), and paying taxes just for the exceeding amount.

uill generate interest from the 4Th laborable- day received from the banks, which represents a minor effective interest rate for the employee.")

9 b) The actuarial value of the pensions in a lump sum. In case of death the balance of the retirement individual account, will be delivered to the beneficiaries. EXAMPLE : For an employee wi'th $ 1,000,000 Mexican pesos ($ 324 dollars approx.) of monthly salary, considering a 2.0% of interest rate in his individual saving and retirement account. The amount that he could expect to have in his account over N years of savings, in months of salary will be as the following figure, TABLE 2 N SAVING YEARS FUND IN MONTHS OF SALARY

10 If we compare the above figures with indemnity: the legal TABLE 3 r N SENIORITY LEGAL INDEMNITY IN MONTHS OF SALARY As we show in the figures at retirement age the average that the individual accounts are going to Pay represents less than 50% of the legal indemnity. The 2% fund analized in a periodical pension way at a same rate of the 2.0% anually payable by month* for a person with 30 years of savings will give a Pension in salary percentage, as follows: INTEREST RATE YEARS OLD 5.2% 6.1% 65 YEARS OLD 9. 0% 10.2%

11 This percentage added to the Social Security one, per normal retirement or retirement in advance concepts, will reach pensions in average between 40% to 50% of the last salary, for employees with salaries lesser than 10 times the minirndnsalar~. So, since the social security does not guarantee increases, the pensions will lose buying Power. Due to this, it will be necessary for the companies to continue dismissing or paying indemnities In Accouuntina Matter, Actually, the obligation to register the contingent liabilities per seniority premium, pensions for retirement and compensations for dismissal concepts, exists through the D3 Bulletin since 1970, but neither the external auditors nor the accountants of the companies, follow it in a strict way. The transnational companies with branches in Mexico have the obligation to apply the FASB 87 bulletin to register the contingent liabilities. So, because of this reason and because year by year there are more retirements through legal indemnity that affect just one fiscal year in the accountant of the companies, the ~ccountant Institute made a new bulletin, D03, in order that the companies have a strict obligation to register the contingent liabilities.

12 Actually this bulletin is in process of approval by the members of the Institute. The purpose of this bulletin is to set UP the appropriaka features to register such liabilities already established, or for informal retirement plans. Through the application of this bulletin the companies will reflect in their financial statements the total cost of employment Per employees. IV. OPPORTUNITIES Due to the above mentioned items, from this Year on, the companies will have to do the followin&k: a) TO register the contingent liabilities for retirement concepts in their books, even if they count or not with formal or informal pension plans. b) TO pay an additional 2% over salaries, which will be reflected in their costs. In view of the two above mentioned issues, it is convenient for the companies to do the following: 1. For those companies with no specific pension plans:

TO register the contingent liabilities for retirement concepts in their books, even")

13 To establish a retirement pension plan to cover at least the equivalent legal indemnity, paid formerly through an informal plan, which will be considered as complement of the benefit granted by the Social Security, retirement insurance. The above will be in order to get the following benefit: a) The cost of -the 2% payroll established for the retirement insurance do not be considered as additional cost, but as complementary payment for retirement concept. In this way the companies could reduce the cost of the 2% of salaries established in the Social Security Law. b) In view that they must reflect in their books the cost of the contingent liabilities and if the reserve is constituted only in books, it will not be tax deductable it will be an advantage to create a fund in a bank or in an insurance company or in a stock house, and have the fiscal benefits over tax reductions. c) Grant to their employees higher benefits like a lump sum of a pension plan instead of the legal indemnity because of the higher exemption in taxes.

14 2. For the companies with established retirement plans : a) The cost of the 2% payroll for the retirement insurance do not be considered as additional cost, but complementary pa~ment for retirement concept. The cost is going to be just for the withdrawal, because they are changing part of the defined benefit plan by a defined contribution plan. b) Not to affect the cash flow of the company using the resources already established in the funds of the pension plans and trans* the corresponding amount to each individual account. C) TO improve the benefits with tendency to Pay pensions periodically and giving real benefits to their employees.

Not to affect the cash flow of the company using the resources already established in the funds of the pension plans and trans* the corresponding amount to")

Summary of Social Security and Private Employee Benefits MEXICO

Private Employee Benefits MEXICO 2013 Your Local Link to IGP in MEXICO: Seguros Monterrey New York Life, S.A. Seguros Monterrey, S.A., founded in 1940, is one of the leading life and health insurance companies

Private Employee Benefits MEXICO 2013 Your Local Link to IGP in MEXICO: Seguros Monterrey New York Life, S.A. Seguros Monterrey, S.A., founded in 1940, is one of the leading life and health insurance companies

Generic Local School District, Ohio Notes to the Basic Financial Statements For the Fiscal Year Ended June 30, 2015

Note 2 - Summary of Significant Accounting Policies Pensions For purposes of measuring the net pension liability, information about the fiduciary net position of the pension plans and additions to/deductions

Note 2 - Summary of Significant Accounting Policies Pensions For purposes of measuring the net pension liability, information about the fiduciary net position of the pension plans and additions to/deductions

How Can You Reduce Your Taxes?

RON GRAHAM AND ASSOCIATES LTD. 10585 111 Street NW, Edmonton, Alberta, T5M 0L7 Telephone (780) 429-6775 Facsimile (780) 424-0004 Email rgraham@rgafinancial.com How Can You Reduce Your Taxes? Tax Brackets.

RON GRAHAM AND ASSOCIATES LTD. 10585 111 Street NW, Edmonton, Alberta, T5M 0L7 Telephone (780) 429-6775 Facsimile (780) 424-0004 Email rgraham@rgafinancial.com How Can You Reduce Your Taxes? Tax Brackets.

STATE OF NEW JERSEY SUPPLEMENTAL ANNUITY COLLECTIVE TRUST. Financial Statements. June 30, 2014 and 2013. (With Independent Auditors Report Thereon)

") Financial Statements (With Independent Auditors Report Thereon) Financial Statements Table of Contents Independent Auditors Report 1 Management s Discussion and Analysis (Unaudited) 3 Basic Financial Statements:

Financial Statements (With Independent Auditors Report Thereon) Financial Statements Table of Contents Independent Auditors Report 1 Management s Discussion and Analysis (Unaudited) 3 Basic Financial Statements:

RETIREMENT FUND MEMBER INFORMATION

RETIREMENT FUND MEMBER INFORMATION OPTIONS ON RESIGNATION, RETRENCHMENT OR DISMISSAL If you resign, or are retrenched or dismissed, your membership of your retirement fund will come to an end. The fund

RETIREMENT FUND MEMBER INFORMATION OPTIONS ON RESIGNATION, RETRENCHMENT OR DISMISSAL If you resign, or are retrenched or dismissed, your membership of your retirement fund will come to an end. The fund

Options available to members on leaving their retirement fund

Options available to members on leaving their retirement fund Applicable to members leaving post March 2009 The contents of this document This document explains the different options you have available

Options available to members on leaving their retirement fund Applicable to members leaving post March 2009 The contents of this document This document explains the different options you have available

CONTRIBUTORY ANNUITY PLAN

CONTRIBUTORY ANNUITY PLAN FOR SALARIED EMPLOYES) INTERNATIONAL HARVESTER COMPANY AND AFFILIATED COMPANIES AS AMENDED AN IN EFFECT ON AND AFT JANUARY 1, 1944 lns'itu-.' OF INDUST',.IAL RELATIONS REil 4

CONTRIBUTORY ANNUITY PLAN FOR SALARIED EMPLOYES) INTERNATIONAL HARVESTER COMPANY AND AFFILIATED COMPANIES AS AMENDED AN IN EFFECT ON AND AFT JANUARY 1, 1944 lns'itu-.' OF INDUST',.IAL RELATIONS REil 4

IBN Glossary - Benefit Definitions. Accidental Death and Dismemberment

IBN Glossary - Benefit Definitions Accidental Death and Dismemberment Actuary - (Pension) Added Years Additional Voluntary Contributions (AVC) AVCs in house AVCs - FSAVCs AD&D provides coverage for death

IBN Glossary - Benefit Definitions Accidental Death and Dismemberment Actuary - (Pension) Added Years Additional Voluntary Contributions (AVC) AVCs in house AVCs - FSAVCs AD&D provides coverage for death

GENERAL INCOME TAX INFORMATION

NEW YORK STATE TEACHERS RETIREMENT SYSTEM GENERAL INCOME TAX INFORMATION TABLE OF CONTENTS Taxes on Loans from the Annuity Savings Fund 1 (Tier 1 and 2 Members Only) Taxes on the Withdrawal of the Annuity

NEW YORK STATE TEACHERS RETIREMENT SYSTEM GENERAL INCOME TAX INFORMATION TABLE OF CONTENTS Taxes on Loans from the Annuity Savings Fund 1 (Tier 1 and 2 Members Only) Taxes on the Withdrawal of the Annuity

Retirement planning with Group Superannuation. ICICI Prudential Group Superannuation Plan. Eligibility. Superannuation Benefits payable

Retirement planning with Group Superannuation After a valuable professional career with an organization, employees require the security of a regular income flow when they retire. Organizations help employees

Retirement planning with Group Superannuation After a valuable professional career with an organization, employees require the security of a regular income flow when they retire. Organizations help employees

Guide to Small Business Retirement Plans

Guide to Small Business Retirement Plans ADVANCED MARKETS All guarantees, including optional benefits, are backed by the claims paying ability of the issuing insurance company. Annuities issued by Transamerica

Guide to Small Business Retirement Plans ADVANCED MARKETS All guarantees, including optional benefits, are backed by the claims paying ability of the issuing insurance company. Annuities issued by Transamerica

Nonqualified Deferred Compensation Plans Why Administration Matters

Nonqualified Deferred Compensation Plans Why Administration Matters By: Howard D. Stern, FSA Vice President & Actuary The Pangburn Company HOWARD D. STERN, FSA is Vice President and Actuary with the Pangburn

Nonqualified Deferred Compensation Plans Why Administration Matters By: Howard D. Stern, FSA Vice President & Actuary The Pangburn Company HOWARD D. STERN, FSA is Vice President and Actuary with the Pangburn

This rule was filed as 13 NMAC 9.3. LIFE INSURANCE AND ANNUITIES VARIABLE ANNUITY CONTRACTS

This rule was filed as 13 NMAC 9.3. TITLE 13 CHAPTER 9 PART 3 INSURANCE LIFE INSURANCE AND ANNUITIES VARIABLE ANNUITY CONTRACTS 13.9.3.1 ISSUING AGENCY: New Mexico State Corporation Commission [Public

This rule was filed as 13 NMAC 9.3. TITLE 13 CHAPTER 9 PART 3 INSURANCE LIFE INSURANCE AND ANNUITIES VARIABLE ANNUITY CONTRACTS 13.9.3.1 ISSUING AGENCY: New Mexico State Corporation Commission [Public

BUYER S GUIDE TO FIXED DEFERRED ANNUITIES

BUYER S GUIDE TO FIXED DEFERRED ANNUITIES Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association of state insurance regulatory

BUYER S GUIDE TO FIXED DEFERRED ANNUITIES Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association of state insurance regulatory

Overview of Pension Plans in Latin America. with a focus on Brazil and Mexico

Overview of Pension Plans in Latin America with a focus on Brazil and Mexico Pension Practice in Latin America Three groups of countries are clearly identified Group I Mainly depending on State Social

Overview of Pension Plans in Latin America with a focus on Brazil and Mexico Pension Practice in Latin America Three groups of countries are clearly identified Group I Mainly depending on State Social

Side-by-Side Business Insurance Plan Comparisons

Side-by-Side Insurance Plan Comparisons Small Strategies & Solutions Protect and grow your business with proper planning The success of your business is based on your hard work and the efforts of key employees.

Side-by-Side Insurance Plan Comparisons Small Strategies & Solutions Protect and grow your business with proper planning The success of your business is based on your hard work and the efforts of key employees.

Mexico: 2014 Tax Reform Initiative

Mexico: 2014 Tax Reform Initiative October 2013 Summary The Mexican government recently published its plans for comprehensive economic reforms, which include the creation of a universal old age pension

Mexico: 2014 Tax Reform Initiative October 2013 Summary The Mexican government recently published its plans for comprehensive economic reforms, which include the creation of a universal old age pension

ACORN LIFE PERSONAL PENSION PLAN SINGLE CONTRIBUTION PROVISIONS

ACORN LIFE PERSONAL PENSION PLAN SINGLE CONTRIBUTION PROVISIONS 1. Summary (a) This Policy is a Single Contribution Personal Pension Plan issued by us, Acorn Life Limited (the Company ). The purpose of

ACORN LIFE PERSONAL PENSION PLAN SINGLE CONTRIBUTION PROVISIONS 1. Summary (a) This Policy is a Single Contribution Personal Pension Plan issued by us, Acorn Life Limited (the Company ). The purpose of

Annuity Principles and Concepts Session Five Lesson Two. Annuity (Benefit) Payment Options

Payment Options") Annuity Principles and Concepts Session Five Lesson Two Annuity (Benefit) Payment Options Life Contingency Options - How Income Payments Can Be Made To The Annuitant. Pure Life versus Life with Guaranteed

Annuity Principles and Concepts Session Five Lesson Two Annuity (Benefit) Payment Options Life Contingency Options - How Income Payments Can Be Made To The Annuitant. Pure Life versus Life with Guaranteed

WHO CAN CONTRIBUTE TO A ROTH IRA?

{ } ROTH IRAs 1 WHO CAN CONTRIBUTE TO A ROTH IRA? Any taxpayer who has compensation, regardless of age, can contribute to a ROTH IRA. Compensation is defined as wages, salaries, bonuses, commissions, tips,

{ } ROTH IRAs 1 WHO CAN CONTRIBUTE TO A ROTH IRA? Any taxpayer who has compensation, regardless of age, can contribute to a ROTH IRA. Compensation is defined as wages, salaries, bonuses, commissions, tips,

Funding income protection and trauma insurance via superannuation

TB 40 Funding income protection and trauma insurance via Issued on 16 June 2014. Summary The tax concessions available for certain contributions can make it tax effective to fund income protection (salary

TB 40 Funding income protection and trauma insurance via Issued on 16 June 2014. Summary The tax concessions available for certain contributions can make it tax effective to fund income protection (salary

Bank Owned Life Insurance. Kirk A. Pelikan 414-223-2529 kapelikan@michaelbest.com

Bank Owned Life Insurance Kirk A. Pelikan 414-223-2529 kapelikan@michaelbest.com BOLI: The Basics BOLI is a life insurance policy purchased by a bank to insure the life of a certain employee. Product has

Bank Owned Life Insurance Kirk A. Pelikan 414-223-2529 kapelikan@michaelbest.com BOLI: The Basics BOLI is a life insurance policy purchased by a bank to insure the life of a certain employee. Product has

Traditional IRA s Contribution rules-

A Traditional IRA is a retirement plan that allows you to save money for retirement. In the case of a traditional IRA, you may also be offered an immediate tax shelter for the contributions that you make

A Traditional IRA is a retirement plan that allows you to save money for retirement. In the case of a traditional IRA, you may also be offered an immediate tax shelter for the contributions that you make

Income for Life Annuity Program* Immediate Annuities for Retirement Income

Income for Life Annuity Program* Immediate Annuities for Retirement Income *ICMA-RC partners with select insurance companies that make annuities available through the Income for Life Annuity program. Participating

Income for Life Annuity Program* Immediate Annuities for Retirement Income *ICMA-RC partners with select insurance companies that make annuities available through the Income for Life Annuity program. Participating

CHAPTER 9 BUSINESS INSURANCE

CHAPTER 9 BUSINESS INSURANCE Just as individuals need insurance for protection so do businesses. Businesses need insurance to cover potential property losses and liability losses. Life insurance also is

CHAPTER 9 BUSINESS INSURANCE Just as individuals need insurance for protection so do businesses. Businesses need insurance to cover potential property losses and liability losses. Life insurance also is

This will depend upon three factors.

The basics: A SEP provides an employer with a simplified way to make contributions to an employee s individual retirement account or individual retirement annuity. Employer contributions are made directly

The basics: A SEP provides an employer with a simplified way to make contributions to an employee s individual retirement account or individual retirement annuity. Employer contributions are made directly

EITF ABSTRACTS. Title: Accounting for Deferred Compensation and Postretirement Benefit Aspects of Endorsement Split-Dollar Life Insurance Arrangements

EITF ABSTRACTS Issue No. 06-4 Title: Accounting for Deferred Compensation and Postretirement Benefit Aspects of Endorsement Split-Dollar Life Insurance Arrangements Dates Discussed: March 16, 2006; June

EITF ABSTRACTS Issue No. 06-4 Title: Accounting for Deferred Compensation and Postretirement Benefit Aspects of Endorsement Split-Dollar Life Insurance Arrangements Dates Discussed: March 16, 2006; June

PROTOTYPE SIMPLIFIED EMPLOYEE PROTOTYPE PLAN

PROTOTYPE SIMPLIFIED EMPLOYEE PROTOTYPE PLAN PROTOTYPE SIMPLIFIED EMPLOYEE PENSION PLAN AGREEMENT ARTICLE I Adoption and Purpose of Plan 1.01 Adoption of Plan: By completing and signing the Adoption Agreement,

PROTOTYPE SIMPLIFIED EMPLOYEE PROTOTYPE PLAN PROTOTYPE SIMPLIFIED EMPLOYEE PENSION PLAN AGREEMENT ARTICLE I Adoption and Purpose of Plan 1.01 Adoption of Plan: By completing and signing the Adoption Agreement,

Nonqualified benefits questionnaire

FOR LIFE Nonqualified benefits questionnaire The Lincoln National Life Insurance Company, Fort Wayne, IN Lincoln Life & Annuity Company of New York, Syracuse, NY 2065722 For Prepared by Date This questionnaire

FOR LIFE Nonqualified benefits questionnaire The Lincoln National Life Insurance Company, Fort Wayne, IN Lincoln Life & Annuity Company of New York, Syracuse, NY 2065722 For Prepared by Date This questionnaire

Organización Soriana S.A. de C.V. y Subsidiarias. Informe Anual AnnualReport. Estados Financieros. Financial Statements

Organización Soriana S.A. de C.V. y Subsidiarias Informe Anual AnnualReport 2 0 0 0 Estados Financieros Financial Statements 19 ÍNDICE INDEX Informe del Comisario Report of Shareholder Examiner 22 Informe

Organización Soriana S.A. de C.V. y Subsidiarias Informe Anual AnnualReport 2 0 0 0 Estados Financieros Financial Statements 19 ÍNDICE INDEX Informe del Comisario Report of Shareholder Examiner 22 Informe

FORCES NON-PUBLIC FUNDS EMPLOYEES PENSION PLAN

F I N A N C I A L S T A T E M E N T S For CANADIAN FORCES NON-PUBLIC FUNDS EMPLOYEES PENSION PLAN For year ended DECEMBER 31, 2009 AUDITORS' REPORT To the Chairperson and Members of the Employee Pension

F I N A N C I A L S T A T E M E N T S For CANADIAN FORCES NON-PUBLIC FUNDS EMPLOYEES PENSION PLAN For year ended DECEMBER 31, 2009 AUDITORS' REPORT To the Chairperson and Members of the Employee Pension

The Employee Stock Purchase Plan 1

The Employee Stock Purchase Plan 1 PLAN HIGHLIGHTS Through Stock Up! you invest in your future by owning a piece of USEC Inc. The Employee Stock Purchase Plan ( ESPP ) offers the following advantages:

The Employee Stock Purchase Plan 1 PLAN HIGHLIGHTS Through Stock Up! you invest in your future by owning a piece of USEC Inc. The Employee Stock Purchase Plan ( ESPP ) offers the following advantages:

Telegraph Investor SIPP Payment of Benefits Guidance Notes

Under the HMRC pension legislation you can take your benefits from age 55, or younger on ill health grounds (see section below). Please note that you do not have to leave employment to draw your benefits

Under the HMRC pension legislation you can take your benefits from age 55, or younger on ill health grounds (see section below). Please note that you do not have to leave employment to draw your benefits

Actuarial Speak 101 Terms and Definitions

Actuarial Speak 101 Terms and Definitions Introduction and Caveat: It is intended that all definitions and explanations are accurate. However, for purposes of understanding and clarity of key points, the

Actuarial Speak 101 Terms and Definitions Introduction and Caveat: It is intended that all definitions and explanations are accurate. However, for purposes of understanding and clarity of key points, the

INSURANCE DICTIONARY

INSURANCE DICTIONARY Actuary An actuary is a professional who uses statistical data to assess risk and calculate dividends, financial reserves, and insurance premiums for a business or insurer. Agent An

INSURANCE DICTIONARY Actuary An actuary is a professional who uses statistical data to assess risk and calculate dividends, financial reserves, and insurance premiums for a business or insurer. Agent An

Transactions & Savings Because managing your money should be easy.

Transactions & Savings Because managing your money should be easy. Your guide to how People s Choice Credit Union can help you with your everyday banking needs and achieve your saving and investment goals.

Transactions & Savings Because managing your money should be easy. Your guide to how People s Choice Credit Union can help you with your everyday banking needs and achieve your saving and investment goals.

Retirement Compensation Arrangement

tax efficient retirement planning tool business GUIDELINES Retirement Compensation Arrangement Supplement Retirement Income while providing Tax Deductible contributions RRSPs and Pension Plans provide

tax efficient retirement planning tool business GUIDELINES Retirement Compensation Arrangement Supplement Retirement Income while providing Tax Deductible contributions RRSPs and Pension Plans provide

SURRENDER REQUEST. 1. Copy of a cheque, or a cancelled cheque, or certification of account details from the bank (including full name and ID number)

") SURRENDER REQUEST The following documents must be attached: 1. Copy of a cheque, or a cancelled cheque, or certification of account details from the bank (including full name and ID number) 2. Legible

SURRENDER REQUEST The following documents must be attached: 1. Copy of a cheque, or a cancelled cheque, or certification of account details from the bank (including full name and ID number) 2. Legible

THE INSURANCE ORGANIZER

THE INSURANCE ORGANIZER SENIOR SOLUTIONS OF AMERICA, INC. www.todaysseniors.com COPYRIGHT 2007 SENIOR SOLUTIONS OF AMERICA, INC. ALL RIGHTS RESERVED. ORGANIZING YOUR INSURANCE POLICIES Your safe deposit

THE INSURANCE ORGANIZER SENIOR SOLUTIONS OF AMERICA, INC. www.todaysseniors.com COPYRIGHT 2007 SENIOR SOLUTIONS OF AMERICA, INC. ALL RIGHTS RESERVED. ORGANIZING YOUR INSURANCE POLICIES Your safe deposit

W3 Wealth Management, LLC Shelby Morgan 90 N. Miller Road Akron, OH 44313 330-836-3805 Shelby@W3wealth.com. Key Employee Insurance

W3 Wealth Management, LLC Shelby Morgan 90 N. Miller Road Akron, OH 44313 330-836-3805 Shelby@W3wealth.com Key Employee Insurance W3 Wealth Management, LLC Page 2 of 9 Table of Contents Life Insurance

W3 Wealth Management, LLC Shelby Morgan 90 N. Miller Road Akron, OH 44313 330-836-3805 Shelby@W3wealth.com Key Employee Insurance W3 Wealth Management, LLC Page 2 of 9 Table of Contents Life Insurance

Estate Planning. Insured Inheritance. Income Shelter. Insured Annuity. Capital Gains Protector

Estate Planning Insured Inheritance The Insured Inheritance concept demonstrates an opportunity to shelter a lump sum investment from income tax and to ensure that the maximum tax-free dollars become available

Estate Planning Insured Inheritance The Insured Inheritance concept demonstrates an opportunity to shelter a lump sum investment from income tax and to ensure that the maximum tax-free dollars become available

Retirement. This factsheet sets out the circumstances under which you may retire and receive a pension from USS.

RETIREMENT FINAL SALARY SECTION Retirement This factsheet sets out the circumstances under which you may retire and receive a pension from USS. From what age can I receive my retirement benefits from USS?

RETIREMENT FINAL SALARY SECTION Retirement This factsheet sets out the circumstances under which you may retire and receive a pension from USS. From what age can I receive my retirement benefits from USS?

Code means the Internal Revenue Code of 1986, as amended.

The American Funds Roth IRA Trust Agreement Pending IRS approval. Section 1 Definitions As used in this trust agreement ( Agreement ) and the related Application, the following terms shall have the meaning

The American Funds Roth IRA Trust Agreement Pending IRS approval. Section 1 Definitions As used in this trust agreement ( Agreement ) and the related Application, the following terms shall have the meaning

COUNTY EMPLOYEES' ANNUITY AND BENEFIT FUND OF COOK COUNTY ACTUARIAL VALUATION AS OF DECEMBER 31,2011

COUNTY EMPLOYEES' ANNUITY AND BENEFIT FUND OF COOK COUNTY ACTUARIAL VALUATION AS OF DECEMBER 31,2011 GOLDSTEIN & ASSOCIATES Actuaries and Consultants 29 SOUTH LaSALLE STREET CHICAGO, ILLINOIS 60603 PHONE

COUNTY EMPLOYEES' ANNUITY AND BENEFIT FUND OF COOK COUNTY ACTUARIAL VALUATION AS OF DECEMBER 31,2011 GOLDSTEIN & ASSOCIATES Actuaries and Consultants 29 SOUTH LaSALLE STREET CHICAGO, ILLINOIS 60603 PHONE

Fixed Deferred Annuities

Buyer s Guide to: Fixed Deferred Annuities National Association of Insurance Commissioners 2301 McGee St Suite 800 Kansas City, MO 64108-2604 (816) 842-3600 1999, 2007 National Association of Insurance

Buyer s Guide to: Fixed Deferred Annuities National Association of Insurance Commissioners 2301 McGee St Suite 800 Kansas City, MO 64108-2604 (816) 842-3600 1999, 2007 National Association of Insurance

Tax planning for retirement By Jenny Gordon, head: Retail Legal

Tax planning for retirement By Jenny Gordon, head: Retail Legal Agenda Tax deductions on contributions from 1 March 2015 Non-retirement funding income Tax during build up Tax on transfers Tax on lump sum

Tax planning for retirement By Jenny Gordon, head: Retail Legal Agenda Tax deductions on contributions from 1 March 2015 Non-retirement funding income Tax during build up Tax on transfers Tax on lump sum

BUYER S GUIDE TO FIXED DEFERRED ANNUITIES

BUYER S GUIDE TO FIXED DEFERRED ANNUITIES IT IS IMPORTANT that you understand the differences among various annuities so you can choose the kind that best fits your needs. This guide focuses on fixed deferred

BUYER S GUIDE TO FIXED DEFERRED ANNUITIES IT IS IMPORTANT that you understand the differences among various annuities so you can choose the kind that best fits your needs. This guide focuses on fixed deferred

your share incentive plan

your share incentive plan 1 Contents What is Match?... 4 Match... 4 How do I get shares under Match?... 5 Shares you buy: Partnership Shares... 5 Shares given to you by Matchtech Group: Match Shares...

your share incentive plan 1 Contents What is Match?... 4 Match... 4 How do I get shares under Match?... 5 Shares you buy: Partnership Shares... 5 Shares given to you by Matchtech Group: Match Shares...

DELUXE CORPORATION 401(k) AND PROFIT SHARING PLAN SUMMARY PLAN DESCRIPTION

AND PROFIT SHARING PLAN SUMMARY PLAN DESCRIPTION") DELUXE CORPORATION 401(k) AND PROFIT SHARING PLAN SUMMARY PLAN DESCRIPTION October 1, 2015 151027:0918 INFORMATION IN THIS SUMMARY INTRODUCTION... 1 WHY CONTRIBUTE TO THE PLAN?... 2 ELIGIBILITY... 2 Eligibility

DELUXE CORPORATION 401(k) AND PROFIT SHARING PLAN SUMMARY PLAN DESCRIPTION October 1, 2015 151027:0918 INFORMATION IN THIS SUMMARY INTRODUCTION... 1 WHY CONTRIBUTE TO THE PLAN?... 2 ELIGIBILITY... 2 Eligibility

500.4107 Separate account annual statement and other information to be submitted to commissioner.

THE INSURANCE CODE OF 1956 (EXCERPT) Act 218 of 1956 CHAPTER 41 MODIFIED GUARANTEED ANNUITIES 500.4101 Definitions. Sec. 4101. As used in this chapter: (a) Interest credits means all interest that is credited

THE INSURANCE CODE OF 1956 (EXCERPT) Act 218 of 1956 CHAPTER 41 MODIFIED GUARANTEED ANNUITIES 500.4101 Definitions. Sec. 4101. As used in this chapter: (a) Interest credits means all interest that is credited

Challenger Lifetime annuities

Challenger Lifetime annuities Regular and secure income for life Challenger Lifetime annuities A Challenger lifetime annuity is a secure investment that protects your savings and can provide an income

Challenger Lifetime annuities Regular and secure income for life Challenger Lifetime annuities A Challenger lifetime annuity is a secure investment that protects your savings and can provide an income

SIMPLIFIED EMPLOYEE PLAN

SIMPLIFIED EMPLOYEE PLAN SIMPLIFIED EMPLOYEE PENSION PLAN AGREEMENT ARTICLE I Adoption and Purpose of Plan 1.01 Adoption of Plan: By completing and signing the Adoption Agreement, the Employer adopts the

SIMPLIFIED EMPLOYEE PLAN SIMPLIFIED EMPLOYEE PENSION PLAN AGREEMENT ARTICLE I Adoption and Purpose of Plan 1.01 Adoption of Plan: By completing and signing the Adoption Agreement, the Employer adopts the

GN11A(ROI): CALCULATIONS REQUIRED UNDER THE FAMILY LAW ACT, 1995 OR THE FAMILY LAW (DIVORCE) ACT, 1996

: CALCULATIONS REQUIRED UNDER THE FAMILY LAW ACT, 1995 OR THE FAMILY LAW (DIVORCE) ACT, 1996") GN11A(ROI): CALCULATIONS REQUIRED UNDER THE FAMILY LAW ACT, 1995 OR THE FAMILY LAW (DIVORCE) ACT, 1996 Classification Practice Standard Legislation or Authority This Guidance Note must be read in conjunction

GN11A(ROI): CALCULATIONS REQUIRED UNDER THE FAMILY LAW ACT, 1995 OR THE FAMILY LAW (DIVORCE) ACT, 1996 Classification Practice Standard Legislation or Authority This Guidance Note must be read in conjunction

- on termination due to redundancy

The Increased Tax on Lump Sum Termination Payments By Ray Stevens (USA) INTRODUCTION In May, 1983, the Government announced increases in the taxation payable on lump sum superannuation benefits and on

The Increased Tax on Lump Sum Termination Payments By Ray Stevens (USA) INTRODUCTION In May, 1983, the Government announced increases in the taxation payable on lump sum superannuation benefits and on

CHAPTER 4 - TAX PREFERENCES FOR SUPERANNUATION AND LIFE INSURANCE SAVINGS

45 CHAPTER 4 - TAX PREFERENCES FOR SUPERANNUATION AND LIFE INSURANCE SAVINGS 4.1 Introduction In general, superannuation and life insurance have not been subject to the normal income tax treatment for

45 CHAPTER 4 - TAX PREFERENCES FOR SUPERANNUATION AND LIFE INSURANCE SAVINGS 4.1 Introduction In general, superannuation and life insurance have not been subject to the normal income tax treatment for

Voluntary Exit guidance for staff

Voluntary Exit guidance for staff This guide tells you about the compensation benefits available under the Civil Service Compensation Scheme 2010 if your employer runs a voluntary exit scheme. Who can

Voluntary Exit guidance for staff This guide tells you about the compensation benefits available under the Civil Service Compensation Scheme 2010 if your employer runs a voluntary exit scheme. Who can

Table of Contents. Participant Section

Table of Contents Participant Section Introduction...1 Planning Ahead...1 Distribution Making Your Choice...2 Other Considerations...5 Joint Life and Survivor Expectancy Table...7 Single Life Expectancy

Table of Contents Participant Section Introduction...1 Planning Ahead...1 Distribution Making Your Choice...2 Other Considerations...5 Joint Life and Survivor Expectancy Table...7 Single Life Expectancy

A compelling unbeatable package of guarantees and flexibility. Life insurance protection with optionality SM. CONSUMer Guide

CONSUMer Guide AG Secure Lifetime GUL with Lifestyle Income Solution SM Flexible premium, adjustable death benefit universal life insurance with secondary guarantee provisions Life insurance protection

CONSUMer Guide AG Secure Lifetime GUL with Lifestyle Income Solution SM Flexible premium, adjustable death benefit universal life insurance with secondary guarantee provisions Life insurance protection

Executive Summary of the Defined Benefit Plan Engineering Financial and Economic Security for Multiple Generations

Executive Summary of the Defined Benefit Plan Engineering Financial and Economic Security for Multiple Generations Benefit Focused vs. Lump Sum Focused Overview: What distinguishes a retirement plan which

Executive Summary of the Defined Benefit Plan Engineering Financial and Economic Security for Multiple Generations Benefit Focused vs. Lump Sum Focused Overview: What distinguishes a retirement plan which

CRS Report for Congress

Order Code RL30631 CRS Report for Congress Received through the CRS Web Retirement Benefits for Members of Congress Updated January 21, 2005 Patrick J. Purcell Specialist in Social Legislation Domestic

Order Code RL30631 CRS Report for Congress Received through the CRS Web Retirement Benefits for Members of Congress Updated January 21, 2005 Patrick J. Purcell Specialist in Social Legislation Domestic

Annuities. Introduction 2. What is an Annuity?... 2. How do they work?... 3. Types of Annuities... 4. Fixed vs. Variable annuities...

An Insider s Guide to Annuities Whatever your picture of retirement, the best way to get there and enjoy it once you ve arrived is with a focused, thoughtful plan. Introduction 2 What is an Annuity?...

An Insider s Guide to Annuities Whatever your picture of retirement, the best way to get there and enjoy it once you ve arrived is with a focused, thoughtful plan. Introduction 2 What is an Annuity?...

SACRAMENTO METROPOLITAN FIRE DISTRICT GOVERNMENTAL 457 DEFERRED COMPENSATION PLAN

SACRAMENTO METROPOLITAN FIRE DISTRICT GOVERNMENTAL 457 DEFERRED COMPENSATION PLAN DEEMED IRA ACCOUNTS DISCLOSURE STATEMENT This Disclosure Statement summarizes the provisions relating to the deemed IRA

SACRAMENTO METROPOLITAN FIRE DISTRICT GOVERNMENTAL 457 DEFERRED COMPENSATION PLAN DEEMED IRA ACCOUNTS DISCLOSURE STATEMENT This Disclosure Statement summarizes the provisions relating to the deemed IRA

GEORGIA CODE PROVISIONS PUBLIC RETIREMENT SYSTEMS INDEX

GEORGIA CODE PROVISIONS PUBLIC RETIREMENT SYSTEMS INDEX TITLE 47. RETIREMENT AND PENSIONS TITLE 47 NOTE CHAPTER 1. GENERAL PROVISIONS CHAPTER 2. EMPLOYEES' RETIREMENT SYSTEM OF GEORGIA CHAPTER 3. TEACHERS

GEORGIA CODE PROVISIONS PUBLIC RETIREMENT SYSTEMS INDEX TITLE 47. RETIREMENT AND PENSIONS TITLE 47 NOTE CHAPTER 1. GENERAL PROVISIONS CHAPTER 2. EMPLOYEES' RETIREMENT SYSTEM OF GEORGIA CHAPTER 3. TEACHERS

Actuarial Speak 101 Terms and Definitions

Actuarial Speak 101 Terms and Definitions Introduction and Caveat: It is intended that all definitions and explanations are accurate. However, for purposes of understanding and clarity of key points, the

Actuarial Speak 101 Terms and Definitions Introduction and Caveat: It is intended that all definitions and explanations are accurate. However, for purposes of understanding and clarity of key points, the

COMMUNITY ACTION PARTNERSHIP OF KERN DEFINED CONTRIBUTION PENSION PLAN FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR S REPORT

COMMUNITY ACTION PARTNERSHIP OF KERN DEFINED CONTRIBUTION PENSION PLAN FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR S REPORT FEBRUARY 28, 2014 AND 2013 COMMUNITY ACTION PARTNERSHIP OF KERN DEFINED CONTRIBUTION

COMMUNITY ACTION PARTNERSHIP OF KERN DEFINED CONTRIBUTION PENSION PLAN FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR S REPORT FEBRUARY 28, 2014 AND 2013 COMMUNITY ACTION PARTNERSHIP OF KERN DEFINED CONTRIBUTION

CHAPTER 26.1-35 STANDARD VALUATION LAW

CHAPTER 26.1-35 STANDARD VALUATION LAW 26.1-35-00.1. (Contingent effective date - See note) Definitions. In this chapter, the following definitions apply on or after the operative date of the valuation

CHAPTER 26.1-35 STANDARD VALUATION LAW 26.1-35-00.1. (Contingent effective date - See note) Definitions. In this chapter, the following definitions apply on or after the operative date of the valuation

Guide to Nondiscrimination Testing for Code Section 403(b) Plans. For Employers

Plans. For Employers") Guide to Nondiscrimination Testing for Code Section 403(b) Plans For Employers Table of contents PREFACE... III Question and Answers about Nondiscrimination Testing for Section 403(b) Tax-Sheltered Annuity

Guide to Nondiscrimination Testing for Code Section 403(b) Plans For Employers Table of contents PREFACE... III Question and Answers about Nondiscrimination Testing for Section 403(b) Tax-Sheltered Annuity

Employee: 9.75 % of gross monthly salary Employer: 12.25% of gross monthly salary depending on type of industry No salary ceiling.

Prepared by Mapfre Panama. I SUMMARY Social Security Eligibility Retirement Age Contributions Retirement Disability All private and public employees. 62M/57F Employee: 9.75 % of gross monthly salary Employer:

Prepared by Mapfre Panama. I SUMMARY Social Security Eligibility Retirement Age Contributions Retirement Disability All private and public employees. 62M/57F Employee: 9.75 % of gross monthly salary Employer:

Glossary of Qualified

Glossary of Qualified Retirement Plan Terms 401(k) Plan: A qualified profit sharing or stock bonus plan under which plan participants have an option to put money into the plan or receive the same amount

Glossary of Qualified Retirement Plan Terms 401(k) Plan: A qualified profit sharing or stock bonus plan under which plan participants have an option to put money into the plan or receive the same amount

v02979gl.doc PUBLIC EMPLOYEES RETIREMENT SYSTEM OF NEW JERSEY FORTY-EIGHTH ANNUAL REPORT OF THE ACTUARY PREPARED AS OF JULY 1, 2002

v02979gl.doc PUBLIC EMPLOYEES RETIREMENT SYSTEM OF NEW JERSEY FORTY-EIGHTH ANNUAL REPORT OF THE ACTUARY PREPARED AS OF JULY 1, 2002 March 12, 2003 Board of Trustees Public Employees Retirement System of

v02979gl.doc PUBLIC EMPLOYEES RETIREMENT SYSTEM OF NEW JERSEY FORTY-EIGHTH ANNUAL REPORT OF THE ACTUARY PREPARED AS OF JULY 1, 2002 March 12, 2003 Board of Trustees Public Employees Retirement System of

Smart strategies for maximising retirement income 2012/13

Smart strategies for maximising retirement income 2012/13 Why you need to create a life long income Australia has one of the highest life expectancies in the world and the average retirement length has

Smart strategies for maximising retirement income 2012/13 Why you need to create a life long income Australia has one of the highest life expectancies in the world and the average retirement length has

Voluntary Redundancy guidance for staff

Voluntary Redundancy guidance for staff This guide tells you about the compensation benefits available under the Research Councils Compensation Scheme 2010 if your employer is offering you voluntary redundancy.

Voluntary Redundancy guidance for staff This guide tells you about the compensation benefits available under the Research Councils Compensation Scheme 2010 if your employer is offering you voluntary redundancy.

Application for Retirement Allowance Public Employees' Retirement System Teachers' Pension and Annuity Fund

Application for Retirement Allowance Public Employees' Retirement System Teachers' Pension and Annuity Fund State of New Jersey Division of Pensions and Benefits PO Box 295 Trenton, New Jersey 08625-0295

Application for Retirement Allowance Public Employees' Retirement System Teachers' Pension and Annuity Fund State of New Jersey Division of Pensions and Benefits PO Box 295 Trenton, New Jersey 08625-0295

Allianz MasterDex 10 Plus Annuity

Allianz Life Insurance Company of North America Allianz MasterDex 10 SM Plus Annuity Start building today the life you want tomorrow CB51288-03 Page 1 of 16 Discover the MasterDex 10 Plus SM Annuity from

Allianz Life Insurance Company of North America Allianz MasterDex 10 SM Plus Annuity Start building today the life you want tomorrow CB51288-03 Page 1 of 16 Discover the MasterDex 10 Plus SM Annuity from

Basics of IRAs ING FINANCIAL SOLUTIONS. Your future. Made easier. SM

Basics of IRAs t FDIC/NCUA Insured t A Deposit Of A Bank t Bank Guaranteed May Lose Value t Insured By Any Federal Government Agency ING FINANCIAL SOLUTIONS Your future. Made easier. SM Traditional IRA

Basics of IRAs t FDIC/NCUA Insured t A Deposit Of A Bank t Bank Guaranteed May Lose Value t Insured By Any Federal Government Agency ING FINANCIAL SOLUTIONS Your future. Made easier. SM Traditional IRA

Buying a pension annuity

Buying a pension annuity Why do I need to think about buying a pension annuity? When you come to retire, you will have some important decisions to make. Probably most important of all is how you will generate

Buying a pension annuity Why do I need to think about buying a pension annuity? When you come to retire, you will have some important decisions to make. Probably most important of all is how you will generate

transamerica ADVANCED MARKETS Transamerica s guide to small business RETIREMENT PLANS

Transamerica s guide to small business RETIREMENT PLANS guide to small business RETIREMENT PLANS Once you decide to offer a retirement plan to your employees, one of the most important decisions you will

Transamerica s guide to small business RETIREMENT PLANS guide to small business RETIREMENT PLANS Once you decide to offer a retirement plan to your employees, one of the most important decisions you will

Randolph College Defined Contribution and Tax-Deferred Annuity Retirement Plan. Plan Document

Randolph College Defined Contribution and Tax-Deferred Annuity Retirement Plan Plan Document Amended and Restated Effective as of January 1, 2012 2 TABLE OF CONTENTS Page ARTICLE I: DEFINITIONS... 1 ARTICLE

Randolph College Defined Contribution and Tax-Deferred Annuity Retirement Plan Plan Document Amended and Restated Effective as of January 1, 2012 2 TABLE OF CONTENTS Page ARTICLE I: DEFINITIONS... 1 ARTICLE

An Adviser s Guide to Pensions

An Adviser s Guide to Pensions 1 An Adviser s Guide to Pensions Contents: Section 1: Personal Pensions 1.1 Eligibility 1.2 Maximum Benefits 1.3 Contributions & Tax Relief 1.4 Death Benefits 1.5 Retirement

An Adviser s Guide to Pensions 1 An Adviser s Guide to Pensions Contents: Section 1: Personal Pensions 1.1 Eligibility 1.2 Maximum Benefits 1.3 Contributions & Tax Relief 1.4 Death Benefits 1.5 Retirement

CANADA REVENUE AGENCY. INTERPRETATION BULLETIN - No: IT-85R2

CANADA REVENUE AGENCY INTERPRETATION BULLETIN - No: IT-85R2 DATE: July 31, 1986 SUBJECT: INCOME TAX ACT Health and Welfare Trusts for Employees REFERENCE: Paragraph 6(1)(a) and section 104 (also subsections

CANADA REVENUE AGENCY INTERPRETATION BULLETIN - No: IT-85R2 DATE: July 31, 1986 SUBJECT: INCOME TAX ACT Health and Welfare Trusts for Employees REFERENCE: Paragraph 6(1)(a) and section 104 (also subsections

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY 1. The simple interest per year is: $5,000.08 = $400 So after 10 years you will have: $400 10 = $4,000 in interest. The total balance will be

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY 1. The simple interest per year is: $5,000.08 = $400 So after 10 years you will have: $400 10 = $4,000 in interest. The total balance will be

Roth IRAs. Funding a Roth IRA

The Roth IRA differs from the traditional IRA in that contributions are never deductible and, if certain requirements are met, account distributions are free of federal income tax. Funding a Roth IRA Annual

The Roth IRA differs from the traditional IRA in that contributions are never deductible and, if certain requirements are met, account distributions are free of federal income tax. Funding a Roth IRA Annual

Thrift Savings Plan. Plan Overview. Investment Options. Contribution Limits. Withdrawal Options

Plan Overview Investment Options Contribution Limits Withdrawal Options (TSP) Contents Investment Options... Life Cycle Funds... TSP Contributions - Tax Treatment... Agency Contributions... Over 50 Catch-up

Plan Overview Investment Options Contribution Limits Withdrawal Options (TSP) Contents Investment Options... Life Cycle Funds... TSP Contributions - Tax Treatment... Agency Contributions... Over 50 Catch-up

THE ITC BUY OUT BOND BROCHURE. www.independent-trustee.com

THE ITC BUY OUT BOND BROCHURE www.independent-trustee.com If you were the member of an occupational pension scheme, leaving or have left employment, or your pension scheme is being wound up, it is time

THE ITC BUY OUT BOND BROCHURE www.independent-trustee.com If you were the member of an occupational pension scheme, leaving or have left employment, or your pension scheme is being wound up, it is time

58-58-50. Standard Valuation Law.

58-58-50. Standard Valuation Law. (a) This section shall be known as the Standard Valuation Law. (b) Each year the Commissioner shall value or cause to be valued the reserve liabilities ("reserves") for

58-58-50. Standard Valuation Law. (a) This section shall be known as the Standard Valuation Law. (b) Each year the Commissioner shall value or cause to be valued the reserve liabilities ("reserves") for

NORTHEAST INVESTORS TRUST. 125 High Street Boston, MA 02110 Telephone: 800-225-6704

NORTHEAST INVESTORS TRUST traditional IRA INVESTOR S KIT 125 High Street Boston, MA 02110 Telephone: 800-225-6704 Table of Contents NORTHEAST INVESTORS TRUST TRADITIONAL IRA DISCLOSURE STATEMENT...1 INTRODUCTION...1

NORTHEAST INVESTORS TRUST traditional IRA INVESTOR S KIT 125 High Street Boston, MA 02110 Telephone: 800-225-6704 Table of Contents NORTHEAST INVESTORS TRUST TRADITIONAL IRA DISCLOSURE STATEMENT...1 INTRODUCTION...1

YOUR GUIDE TO RETIREMENT

YOUR GUIDE TO RETIREMENT www.phoenixlife.co.uk CONTENTS Page Purpose of this guide 3 Your pension options - Buying your pension income (annuity) from us 4 Your pension options - Buying your pension income

YOUR GUIDE TO RETIREMENT www.phoenixlife.co.uk CONTENTS Page Purpose of this guide 3 Your pension options - Buying your pension income (annuity) from us 4 Your pension options - Buying your pension income

Your Investments and Other Assets

Your Investments and Other Assets 401(k) Plans Whose plan? Client Co-Client Current total value: $ Current Roth value: $ After-tax value (non-roth): $ Income Total income from this employer: $ Will this

Your Investments and Other Assets 401(k) Plans Whose plan? Client Co-Client Current total value: $ Current Roth value: $ After-tax value (non-roth): $ Income Total income from this employer: $ Will this

POWER SOLUTIONS INTERNATIONAL, INC. 70,000 SHARES OF COMMON STOCK TO BE ISSUED UNDER THE POWER GREAT LAKES, INC. EMPLOYEES 401(K) PROFIT SHARING PLAN

PROFIT SHARING PLAN") PROSPECTUS POWER SOLUTIONS INTERNATIONAL, INC. 70,000 SHARES OF COMMON STOCK TO BE ISSUED UNDER THE POWER GREAT LAKES, INC. EMPLOYEES 401(K) PROFIT SHARING PLAN This document relates to retirement benefits

PROSPECTUS POWER SOLUTIONS INTERNATIONAL, INC. 70,000 SHARES OF COMMON STOCK TO BE ISSUED UNDER THE POWER GREAT LAKES, INC. EMPLOYEES 401(K) PROFIT SHARING PLAN This document relates to retirement benefits

INSTITUTE OF ACTUARIES OF INDIA

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 17 th November 2011 Subject CT5 General Insurance, Life and Health Contingencies Time allowed: Three Hours (10.00 13.00 Hrs) Total Marks: 100 INSTRUCTIONS TO

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 17 th November 2011 Subject CT5 General Insurance, Life and Health Contingencies Time allowed: Three Hours (10.00 13.00 Hrs) Total Marks: 100 INSTRUCTIONS TO

UIL HOLDINGS CORPORATION 2012 NON-QUALIFIED EMPLOYEE STOCK PURCHASE PLAN

UIL HOLDINGS CORPORATION 2012 NON-QUALIFIED EMPLOYEE STOCK PURCHASE PLAN 1. Purpose The Employee Stock Purchase Plan (ESPP) is intended to provide Employees (as defined herein) of UIL Holdings Corporation

UIL HOLDINGS CORPORATION 2012 NON-QUALIFIED EMPLOYEE STOCK PURCHASE PLAN 1. Purpose The Employee Stock Purchase Plan (ESPP) is intended to provide Employees (as defined herein) of UIL Holdings Corporation

A GUIDE TO INVESTING IN ANNUITIES

A GUIDE TO INVESTING IN ANNUITIES What Benefits Do Annuities Offer in Planning for Retirement? Oppenheimer Life Agency, Ltd. Oppenheimer Life Agency, Ltd., a wholly owned subsidiary of Oppenheimer & Co.

A GUIDE TO INVESTING IN ANNUITIES What Benefits Do Annuities Offer in Planning for Retirement? Oppenheimer Life Agency, Ltd. Oppenheimer Life Agency, Ltd., a wholly owned subsidiary of Oppenheimer & Co.

TRUST AND AGENCY FUNDS

TRUST AND AGENCY FUNDS THE TRUST AND AGENCY FUND SECTION CONSISTS OF OVER 1,500 DIFFERENT FUNDS MAINTAINED IN THE COUNTY'S ACCOUNTING SYSTEM. THEY ARE GROUPED BELOW BY MAJOR CATEGORY FOR REPORTING PURPOSES.

TRUST AND AGENCY FUNDS THE TRUST AND AGENCY FUND SECTION CONSISTS OF OVER 1,500 DIFFERENT FUNDS MAINTAINED IN THE COUNTY'S ACCOUNTING SYSTEM. THEY ARE GROUPED BELOW BY MAJOR CATEGORY FOR REPORTING PURPOSES.

A registered corporate tax payer subject to insurance legislation. A registered corporate tax payer subject to insurance legislation.

International comparison omparison of insurance taxation Turkey General insurance overview verview Definition Definition of property and casualty insurance company A registered corporate tax payer subject

International comparison omparison of insurance taxation Turkey General insurance overview verview Definition Definition of property and casualty insurance company A registered corporate tax payer subject

Commercial Union Life Assurance Company Limited

Commercial Union Life Assurance Limited Registered office: St Helen s, 1 Undershaft, London, EC3P 3DQ Annual FSA Insurance Returns for the year ended 31st December 2002 Accounts and statements pursuant

Commercial Union Life Assurance Limited Registered office: St Helen s, 1 Undershaft, London, EC3P 3DQ Annual FSA Insurance Returns for the year ended 31st December 2002 Accounts and statements pursuant

401(k) Summary Plan Description

Summary Plan Description") 401(k) Summary Plan Description WELLSPAN 401(K) RETIREMENT SAVINGS PLAN SUMMARY PLAN DESCRIPTION I I PRIOR TO II III I TABLE OF TO YOUR PLAN What kind of Plan is this? 5 What information does this Summary

401(k) Summary Plan Description WELLSPAN 401(K) RETIREMENT SAVINGS PLAN SUMMARY PLAN DESCRIPTION I I PRIOR TO II III I TABLE OF TO YOUR PLAN What kind of Plan is this? 5 What information does this Summary

5. Defined Benefit and Defined Contribution Plans: Understanding the Differences

5. Defined Benefit and Defined Contribution Plans: Understanding the Differences Introduction Both defined benefit and defined contribution pension plans offer various advantages to employers and employees.

5. Defined Benefit and Defined Contribution Plans: Understanding the Differences Introduction Both defined benefit and defined contribution pension plans offer various advantages to employers and employees.

SEP IRA. For the self-employed and businesses with few employees

SEP IRA P L A N E S T A B L I S H M E N T G U I D E For the self-employed and businesses with few employees Features many of the same tax advantages as other plans Funded solely by Employer contributions

SEP IRA P L A N E S T A B L I S H M E N T G U I D E For the self-employed and businesses with few employees Features many of the same tax advantages as other plans Funded solely by Employer contributions

Key Person Insurance. Protect your business from the loss of a key person with life insurance payable to the business.

Key Person Insurance Protect your business from the loss of a key person with life insurance payable to the business. We offer you this concept piece to help you understand how life insurance can be used

Key Person Insurance Protect your business from the loss of a key person with life insurance payable to the business. We offer you this concept piece to help you understand how life insurance can be used