4. A Discount for Complexity: An Experiment

|

|

|

- Derrick Fox

- 1 years ago

- Views:

Transcription

1 A Discount for Complexity: An Experiment Company A Company B Operating Income $ 1 billion $ 1 billion Tax rate 40% 40% ROIC 10% 10% Expected Growth 5% 5% Cost of capital 8% 8% Business Mix Single Multiple Holdings Simple Complex Accounting Transparent Opaque Which firm would you value more highly? 240

2 241 Measuring Complexity: Volume of Data in Financial Statements Company Number of pages in last 10Q Number of pages in last 10K General Electric Microsoft Wal-mart Exxon Mobil Pfizer Citigroup Intel AIG Johnson & Johnson IBM

3 Measuring Complexity: A Complexity Score

4 Dealing with Complexity 243 In Discounted Cashflow Valuation The Aggressive Analyst: Trust the firm to tell the truth and value the firm based upon the firm s statements about their value. The Conservative Analyst: Don t value what you cannot see. The Compromise: Adjust the value for complexity n Adjust cash flows for complexity n Adjust the discount rate for complexity n Adjust the expected growth rate/ length of growth period n Value the firm and then discount value for complexity In relative valuation In a relative valuation, you may be able to assess the price that the market is charging for complexity: With the hundred largest market cap firms, for instance: PBV = ROE 0.55 Beta Expected growth rate # Pages in 10K 243

5 Be circumspect about defining debt for cost of capital purposes General Rule: Debt generally has the following characteristics: Commitment to make fixed payments in the future The fixed payments are tax deductible Failure to make the payments can lead to either default or loss of control of the firm to the party to whom payments are due. Defined as such, debt should include All interest bearing liabilities, short term as well as long term All leases, operating as well as capital Debt should not include Accounts payable or supplier credit Be wary of your conservative impulses which will tell you to count everything as debt. That will push up the debt ratio and lead you to understate your cost of capital. 244

6 Book Value or Market Value 245 You are valuing a distressed telecom company and have arrived at an estimate of $ 1 billion for the enterprise value (using a discounted cash flow valuation). The company has $ 1 billion in face value of debt outstanding but the debt is trading at 50% of face value (because of the distress). What is the value of the equity to you as an investor? a. The equity is worth nothing (EV minus Face Value of Debt) b. The equity is worth $ 500 million (EV minus Market Value of Debt) Would your answer be different if you were told that the liquidation value of the assets of the firm today is $1.2 billion and that you were planning to liquidate the firm today? 245

7 246 But you should consider other potential liabilities when getting to equity value If you have under funded pension fund or health care plans, you should consider the under funding at this stage in getting to the value of equity. If you do so, you should not double count by also including a cash flow line item reflecting cash you would need to set aside to meet the unfunded obligation. You should not be counting these items as debt in your cost of capital calculations. If you have contingent liabilities - for example, a potential liability from a lawsuit that has not been decided - you should consider the expected value of these contingent liabilities Value of contingent liability = Probability that the liability will occur * Expected value of liability 246

8 6. Equity to Employees: Effect on Value In recent years, firms have turned to giving employees (and especially top managers) equity option or restricted stock packages as part of compensation. If they are options, they usually are long term and on volatile stocks. If restricted stock, the restrictions are usually on trading. These equity compensation packages are clearly valuable and the question becomes how best to deal with them in valuation. Two key issues with employee options: How do options or restricted stock granted in the past affect equity value per share today? How do expected grants of either in the future affect equity value today? 247

9 The Easier Problem: Restricted Stock Grants Aswath Damodaran 248 When employee compensation takes the form of restricted stock grants, the solution is relatively simple. To account for restricted stock grants in the past, make sure that you count the restricted stock that have already been granted in shares outstanding today. That will reduce your value per share. To account for expected stock grants in the future, estimate the value of these grants as a percent of revenue and forecast that as expense as part of compensation expenses. That will reduce future income and cash flows. 248

10 The Bigger Challenge: Employee Options 249 It is true that options can increase the number of shares outstanding but dilution per se is not the problem. Options affect equity value at exercise because Shares are issued at below the prevailing market price. Options get exercised only when they are in the money. Alternatively, the company can use cashflows that would have been available to equity investors to buy back shares which are then used to meet option exercise. The lower cashflows reduce equity value. Options affect equity value before exercise because we have to build in the expectation that there is a probability of and a cost to exercise. 249

11 A simple example 250 XYZ company has $ 100 million in free cashflows to the firm, growing 3% a year in perpetuity and a cost of capital of 8%. It has 100 million shares outstanding and $ 1 billion in debt. Its value can be written as follows: Value of firm = 100 / ( ) = 2000 Debt = 1000 = Equity = 1000 Value per share = 1000/100 = $10 XYZ decides to give 10 million options at the money (with a strike price of $10) to its CEO. What effect will this have on the value of equity per share? a. None. The options are not in-the-money. b. Decrease by 10%, since the number of shares could increase by 10 million c. Decrease by less than 10%. The options will bring in cash into the firm but they have time value. 250

12 I. The Diluted Share Count Approach 251 The simplest way of dealing with options is to try to adjust the denominator for shares that will become outstanding if the options get exercised. In the example cited, this would imply the following: Value of firm = 100 / ( ) = 2000 Debt = 1000 = Equity = 1000 Number of diluted shares = 110 Value per share = 1000/110 = $9.09 The diluted approach fails to consider that exercising options will bring in cash into the firm. Consequently, they will overestimate the impact of options and understate the value of equity per share. 251

13 II. The Treasury Stock Approach 252 The treasury stock approach adds the proceeds from the exercise of options to the value of the equity before dividing by the diluted number of shares outstanding. In the example cited, this would imply the following: Value of firm = 100 / ( ) = 2000 Debt = 1000 = Equity = 1000 Number of diluted shares = 110 Proceeds from option exercise = 10 * 10 = 100 Value per share = ( )/110 = $ 10 The treasury stock approach fails to consider the time premium on the options. The treasury stock approach also has problems with out-of-themoney options. If considered, they can increase the value of equity per share. If ignored, they are treated as non-existent. 252

14 III. Option Value Drag 253 Step 1: Value the firm, using discounted cash flow or other valuation models. Step 2: Subtract out the value of the outstanding debt to arrive at the value of equity. Alternatively, skip step 1 and estimate the of equity directly. Step 3:Subtract out the market value (or estimated market value) of other equity claims: Value of Warrants = Market Price per Warrant * Number of Warrants : Alternatively estimate the value using option pricing model Value of Conversion Option = Market Value of Convertible Bonds - Value of Straight Debt Portion of Convertible Bonds Value of employee Options: Value using the average exercise price and maturity. Step 4:Divide the remaining value of equity by the number of shares outstanding to get value per share. 253

15 254 Valuing Equity Options issued by firms The Dilution Problem Option pricing models can be used to value employee options with four caveats Employee options are long term, making the assumptions about constant variance and constant dividend yields much shakier, Employee options result in stock dilution, and Employee options are often exercised before expiration, making it dangerous to use European option pricing models. Employee options cannot be exercised until the employee is vested. These problems can be partially alleviated by using an option pricing model, allowing for shifts in variance and early exercise, and factoring in the dilution effect. The resulting value can be adjusted for the probability that the employee will not be vested. 254

16 Valuing Employee Options 255 To value employee options, you need the following inputs into the option valuation model: Stock Price = $ 10, Adjusted for dilution = $9.58 Strike Price = $ 10 Maturity = 10 years (Can reduce to reflect early exercise) Standard deviation in stock price = 40% Riskless Rate = 4% Using a dilution-adjusted Black Scholes model, we arrive at the following inputs: N (d1) = N (d2) = Value per call = $ 9.58 (0.8199) - $10 e -(0.04) (10) (0.3624) = $

17 Value of Equity to Value of Equity per share 256 Using the value per call of $5.42, we can now estimate the value of equity per share after the option grant: Value of firm = 100 / ( ) = 2000 Debt = 1000 = Equity = 1000 Value of options granted = $ 54.2 = Value of Equity in stock = $945.8 / Number of shares outstanding / 100 = Value per share = $ 9.46 Note that this approach yields a higher value than the diluted share count approach (which ignores exercise proceeds) and a lower value than the treasury stock approach (which ignores the time premium on the options) 256

18 To tax adjust or not to tax adjust 257 In the example above, we have assumed that the options do not provide any tax advantages. To the extent that the exercise of the options creates tax advantages, the actual cost of the options will be lower by the tax savings. One simple adjustment is to multiply the value of the options by (1- tax rate) to get an after-tax option cost. 257

19 Option grants in the future 258 Assume now that this firm intends to continue granting options each year to its top management as part of compensation. These expected option grants will also affect value. The simplest mechanism for bringing in future option grants into the analysis is to do the following: Estimate the value of options granted each year over the last few years as a percent of revenues. Forecast out the value of option grants as a percent of revenues into future years, allowing for the fact that as revenues get larger, option grants as a percent of revenues will become smaller. Consider this line item as part of operating expenses each year. This will reduce the operating margin and cashflow each year. 258

20 When options affect equity value per share the most 259 Option grants affect value more The lower the strike price is set relative to the stock price The longer the term to maturity of the option The more volatile the stock price The effect on value will be magnified if companies are allowed to revisit option grants and reset the exercise price if the stock price moves down. 259

21 NARRATIVE AND NUMBERS: VALUATION AS A BRIDGE Tell me a story..

22 Valuation as a bridge Number Crunchers Story Tellers Favored Tools - Accounting statements - Excel spreadsheets - Statistical Measures - Pricing Data A Good Valuation Favored Tools - Anecdotes - Experience (own or others) - Behavioral evidence The Numbers People The Narrative People Illusions/Delusions 1. Precision: Data is precise 2. Objectivity: Data has no bias 3. Control: Data can control reality Illusions/Delusions 1. Creativity cannot be quantified 2. If the story is good, the investment will be. 3. Experience is the best teacher 261

23 Step 1: Survey the landscape Every valuation starts with a narrative, a story that you see unfolding for your company in the future. In developing this narrative, you will be making assessments of Your company (its products, its management and its history. The market or markets that you see it growing in. The competition it faces and will face. The macro environment in which it operates. 262

24

25 Step 2: Create a narrative for the future Every valuation starts with a narrative, a story that you see unfolding for your company in the future. In developing this narrative, you will be making assessments of your company (its products, its management), the market or markets that you see it growing in, the competition it faces and will face and the macro environment in which it operates. Rule 1: Keep it simple. Rule 2: Keep it focused. Rule 3: Stay grounded in reality. 264

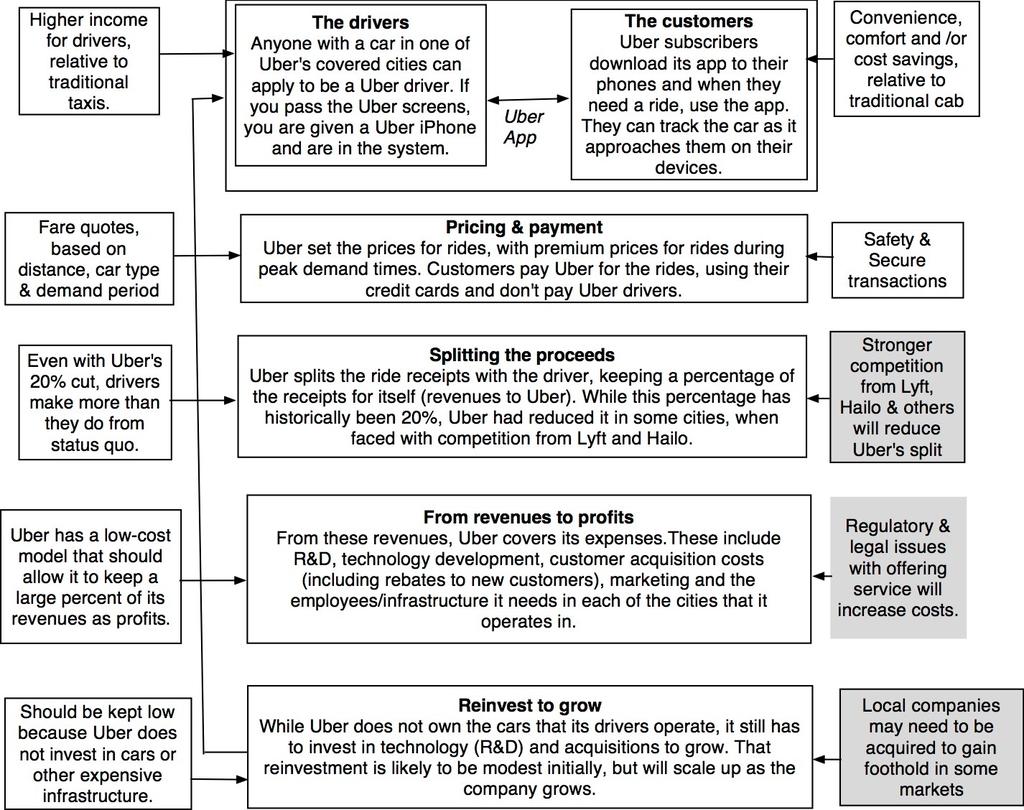

26 The Uber Narrative In June 2014, my initial narrative for Uber was that it would be 1. An urban car service business: I saw Uber primarily as a force in urban areas and only in the car service business. 2. Which would expand the business moderately (about 40% over ten years) by bringing in new users. 3. With local networking benefits: If Uber becomes large enough in any city, it will quickly become larger, but that will be of little help when it enters a new city. 4. Maintain its revenue sharing (20%) system due to strong competitive advantages (from being a first mover). 5. And its existing low-capital business model, with drivers as contractors and very little investment in infrastructure. 265

27 266 Step 3: Check the narrative against history, economic first principles & common sense 266

28 267 The Impossible, The Implausible and the Improbable 267

Employee Options, Restricted Stock and Value. Aswath Damodaran 1

Employee Options, Restricted Stock and Value 1 Basic Proposition on Options Any options issued by a firm, whether to management or employees or to investors (convertibles and warrants) create claims on

Employee Options, Restricted Stock and Value 1 Basic Proposition on Options Any options issued by a firm, whether to management or employees or to investors (convertibles and warrants) create claims on

Value of Equity and Per Share Value when there are options and warrants outstanding. Aswath Damodaran

Value of Equity and Per Share Value when there are options and warrants outstanding Aswath Damodaran 1 Equity Value and Per Share Value: A Test Assume that you have done an equity valuation of Microsoft.

Value of Equity and Per Share Value when there are options and warrants outstanding Aswath Damodaran 1 Equity Value and Per Share Value: A Test Assume that you have done an equity valuation of Microsoft.

Equity Value and Per Share Value: A Test

Equity Value and Per Share Value: A Test Assume that you have done an equity valuation of Microsoft. The total value for equity is estimated to be $ 400 billion and there are 5 billion shares outstanding.

Equity Value and Per Share Value: A Test Assume that you have done an equity valuation of Microsoft. The total value for equity is estimated to be $ 400 billion and there are 5 billion shares outstanding.

MANAGEMENT OPTIONS AND VALUE PER SHARE

1 MANAGEMENT OPTIONS AND VALUE PER SHARE Once you have valued the equity in a firm, it may appear to be a relatively simple exercise to estimate the value per share. All it seems you need to do is divide

1 MANAGEMENT OPTIONS AND VALUE PER SHARE Once you have valued the equity in a firm, it may appear to be a relatively simple exercise to estimate the value per share. All it seems you need to do is divide

Models of Risk and Return

Models of Risk and Return Aswath Damodaran Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

Models of Risk and Return Aswath Damodaran Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

CHAPTER 8. Problems and Questions

CHAPTER 8 Problems and Questions 1. Plastico, a manufacturer of consumer plastic products, is evaluating its capital structure. The balance sheet of the company is as follows (in millions): Assets Liabilities

CHAPTER 8 Problems and Questions 1. Plastico, a manufacturer of consumer plastic products, is evaluating its capital structure. The balance sheet of the company is as follows (in millions): Assets Liabilities

Discussion of Discounting in Oil and Gas Property Appraisal

Discussion of Discounting in Oil and Gas Property Appraisal Because investors prefer immediate cash returns over future cash returns, investors pay less for future cashflows; i.e., they "discount" them.

Discussion of Discounting in Oil and Gas Property Appraisal Because investors prefer immediate cash returns over future cash returns, investors pay less for future cashflows; i.e., they "discount" them.

NIKE Case Study Solutions

NIKE Case Study Solutions Professor Corwin This case study includes several problems related to the valuation of Nike. We will work through these problems throughout the course to demonstrate some of the

NIKE Case Study Solutions Professor Corwin This case study includes several problems related to the valuation of Nike. We will work through these problems throughout the course to demonstrate some of the

Finding the Right Financing Mix: The Capital Structure Decision. Aswath Damodaran 1

Finding the Right Financing Mix: The Capital Structure Decision Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate

Finding the Right Financing Mix: The Capital Structure Decision Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate

How To Calculate Financial Leverage Ratio

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

A Primer on Valuing Common Stock per IRS 409A and the Impact of FAS 157

A Primer on Valuing Common Stock per IRS 409A and the Impact of FAS 157 By Stanley Jay Feldman, Ph.D. Chairman and Chief Valuation Officer Axiom Valuation Solutions 201 Edgewater Drive, Suite 255 Wakefield,

A Primer on Valuing Common Stock per IRS 409A and the Impact of FAS 157 By Stanley Jay Feldman, Ph.D. Chairman and Chief Valuation Officer Axiom Valuation Solutions 201 Edgewater Drive, Suite 255 Wakefield,

Valuing Stock Appreciation Rights (SARs) in ESOP Sponsor Companies

in ESOP Sponsor Companies") ESOP Valuation Insights Valuing Stock Appreciation Rights (SARs) in ESOP Sponsor Companies Steve Whittington Stock appreciation rights (SARs) are used in conjunction with ESOP stock purchase transactions

ESOP Valuation Insights Valuing Stock Appreciation Rights (SARs) in ESOP Sponsor Companies Steve Whittington Stock appreciation rights (SARs) are used in conjunction with ESOP stock purchase transactions

II. Estimating Cash Flows

II. Estimating Cash Flows DCF Valuation Aswath Damodaran 61 Steps in Cash Flow Estimation Estimate the current earnings of the firm If looking at cash flows to equity, look at earnings after interest expenses

II. Estimating Cash Flows DCF Valuation Aswath Damodaran 61 Steps in Cash Flow Estimation Estimate the current earnings of the firm If looking at cash flows to equity, look at earnings after interest expenses

Option Pricing Applications in Valuation!

Option Pricing Applications in Valuation! Equity Value in Deeply Troubled Firms Value of Undeveloped Reserves for Natural Resource Firm Value of Patent/License 73 Option Pricing Applications in Equity

Option Pricing Applications in Valuation! Equity Value in Deeply Troubled Firms Value of Undeveloped Reserves for Natural Resource Firm Value of Patent/License 73 Option Pricing Applications in Equity

Estimating Risk free Rates. Aswath Damodaran. Stern School of Business. 44 West Fourth Street. New York, NY 10012. Adamodar@stern.nyu.

Estimating Risk free Rates Aswath Damodaran Stern School of Business 44 West Fourth Street New York, NY 10012 Adamodar@stern.nyu.edu Estimating Risk free Rates Models of risk and return in finance start

Estimating Risk free Rates Aswath Damodaran Stern School of Business 44 West Fourth Street New York, NY 10012 Adamodar@stern.nyu.edu Estimating Risk free Rates Models of risk and return in finance start

I. Estimating Discount Rates

I. Estimating Discount Rates DCF Valuation Aswath Damodaran 1 Estimating Inputs: Discount Rates Critical ingredient in discounted cashflow valuation. Errors in estimating the discount rate or mismatching

I. Estimating Discount Rates DCF Valuation Aswath Damodaran 1 Estimating Inputs: Discount Rates Critical ingredient in discounted cashflow valuation. Errors in estimating the discount rate or mismatching

Problem 1 Problem 2 Problem 3

Problem 1 (1) Book Value Debt/Equity Ratio = 2500/2500 = 100% Market Value of Equity = 50 million * $ 80 = $4,000 Market Value of Debt =.80 * 2500 = $2,000 Debt/Equity Ratio in market value terms = 2000/4000

Problem 1 (1) Book Value Debt/Equity Ratio = 2500/2500 = 100% Market Value of Equity = 50 million * $ 80 = $4,000 Market Value of Debt =.80 * 2500 = $2,000 Debt/Equity Ratio in market value terms = 2000/4000

Equity Value, Enterprise Value & Valuation Multiples: Why You Add and Subtract Different Items When Calculating Enterprise Value

Equity Value, Enterprise Value & Valuation Multiples: Why You Add and Subtract Different Items When Calculating Enterprise Value Hello and welcome to our next tutorial video here. In this lesson we're

Equity Value, Enterprise Value & Valuation Multiples: Why You Add and Subtract Different Items When Calculating Enterprise Value Hello and welcome to our next tutorial video here. In this lesson we're

Financial Statement Analysis!

Financial Statement Analysis! The raw data for investing Aswath Damodaran! 1! Questions we would like answered! Assets Liabilities What are the assets in place? How valuable are these assets? How risky

Financial Statement Analysis! The raw data for investing Aswath Damodaran! 1! Questions we would like answered! Assets Liabilities What are the assets in place? How valuable are these assets? How risky

FINANCIAL ANALYSIS GUIDE

MAN 4720 POLICY ANALYSIS AND FORMULATION FINANCIAL ANALYSIS GUIDE Revised -August 22, 2010 FINANCIAL ANALYSIS USING STRATEGIC PROFIT MODEL RATIOS Introduction Your policy course integrates information

MAN 4720 POLICY ANALYSIS AND FORMULATION FINANCIAL ANALYSIS GUIDE Revised -August 22, 2010 FINANCIAL ANALYSIS USING STRATEGIC PROFIT MODEL RATIOS Introduction Your policy course integrates information

Return on Equity has three ratio components. The three ratios that make up Return on Equity are:

Evaluating Financial Performance Chapter 1 Return on Equity Why Use Ratios? It has been said that you must measure what you expect to manage and accomplish. Without measurement, you have no reference to

Evaluating Financial Performance Chapter 1 Return on Equity Why Use Ratios? It has been said that you must measure what you expect to manage and accomplish. Without measurement, you have no reference to

Financial Statement and Cash Flow Analysis

Chapter 2 Financial Statement and Cash Flow Analysis Answers to Concept Review Questions 1. What role do the FASB and SEC play with regard to GAAP? The FASB is a nongovernmental, professional standards

Chapter 2 Financial Statement and Cash Flow Analysis Answers to Concept Review Questions 1. What role do the FASB and SEC play with regard to GAAP? The FASB is a nongovernmental, professional standards

Equity Research Methodology

Equity Research Methodology January 5, 2012 2012 Morningstar, Inc. All rights reserved. The information in this document is the property of Morningstar, Inc. Reproduction or transcription by any means,

Equity Research Methodology January 5, 2012 2012 Morningstar, Inc. All rights reserved. The information in this document is the property of Morningstar, Inc. Reproduction or transcription by any means,

Lecture 6. Forecasting Cash Flow Statement

Lecture 6 Forecasting Cash Flow Statement Takeaways from income statement and balance sheet forecasting Elias Rantapuska / Aalto BIZ Finance 2 Note on our discussion today Discussion today: Rather high-level

Lecture 6 Forecasting Cash Flow Statement Takeaways from income statement and balance sheet forecasting Elias Rantapuska / Aalto BIZ Finance 2 Note on our discussion today Discussion today: Rather high-level

Final Exam MØA 155 Financial Economics Fall 2009 Permitted Material: Calculator

University of Stavanger (UiS) Stavanger Masters Program Final Exam MØA 155 Financial Economics Fall 2009 Permitted Material: Calculator The number in brackets is the weight for each problem. The weights

University of Stavanger (UiS) Stavanger Masters Program Final Exam MØA 155 Financial Economics Fall 2009 Permitted Material: Calculator The number in brackets is the weight for each problem. The weights

Source of Finance and their Relative Costs F. COST OF CAPITAL

F. COST OF CAPITAL 1. Source of Finance and their Relative Costs 2. Estimating the Cost of Equity 3. Estimating the Cost of Debt and Other Capital Instruments 4. Estimating the Overall Cost of Capital

F. COST OF CAPITAL 1. Source of Finance and their Relative Costs 2. Estimating the Cost of Equity 3. Estimating the Cost of Debt and Other Capital Instruments 4. Estimating the Overall Cost of Capital

A Primer on Valuing Common Stock per IRS 409A and the Impact of Topic 820 (Formerly FAS 157)

") A Primer on Valuing Common Stock per IRS 409A and the Impact of Topic 820 (Formerly FAS 157) By Stanley Jay Feldman, Ph.D. Chairman and Chief Valuation Officer Axiom Valuation Solutions May 2010 201 Edgewater

A Primer on Valuing Common Stock per IRS 409A and the Impact of Topic 820 (Formerly FAS 157) By Stanley Jay Feldman, Ph.D. Chairman and Chief Valuation Officer Axiom Valuation Solutions May 2010 201 Edgewater

Financial ratio analysis

Financial ratio analysis A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction 2. Liquidity ratios 3. Profitability ratios and activity ratios 4. Financial leverage ratios 5. Shareholder

Financial ratio analysis A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction 2. Liquidity ratios 3. Profitability ratios and activity ratios 4. Financial leverage ratios 5. Shareholder

Estimating Beta. Aswath Damodaran

Estimating Beta The standard procedure for estimating betas is to regress stock returns (R j ) against market returns (R m ) - R j = a + b R m where a is the intercept and b is the slope of the regression.

Estimating Beta The standard procedure for estimating betas is to regress stock returns (R j ) against market returns (R m ) - R j = a + b R m where a is the intercept and b is the slope of the regression.

Discounted Cash Flow Valuation: Basics

Discounted Cash Flow Valuation: Basics Aswath Damodaran Aswath Damodaran 1 Discounted Cashflow Valuation: Basis for Approach Value = t=n CF t t =1(1+r) t where CF t is the cash flow in period t, r is the

Discounted Cash Flow Valuation: Basics Aswath Damodaran Aswath Damodaran 1 Discounted Cashflow Valuation: Basis for Approach Value = t=n CF t t =1(1+r) t where CF t is the cash flow in period t, r is the

Homework Solutions - Lecture 2

Homework Solutions - Lecture 2 1. The value of the S&P 500 index is 1286.12 and the treasury rate is 3.43%. In a typical year, stock repurchases increase the average payout ratio on S&P 500 stocks to over

Homework Solutions - Lecture 2 1. The value of the S&P 500 index is 1286.12 and the treasury rate is 3.43%. In a typical year, stock repurchases increase the average payout ratio on S&P 500 stocks to over

CHAPTER 16. Dilutive Securities and Earnings Per Share ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Concepts for Analysis

Concepts for Analysis") CHAPTER 16 Dilutive Securities and Earnings Per Share ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Convertible debt and preferred

CHAPTER 16 Dilutive Securities and Earnings Per Share ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Convertible debt and preferred

Measuring Investment Returns

Measuring Investment Returns Aswath Damodaran Stern School of Business Aswath Damodaran 156 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The

Measuring Investment Returns Aswath Damodaran Stern School of Business Aswath Damodaran 156 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The

INTERVIEWS - FINANCIAL MODELING

420 W. 118th Street, Room 420 New York, NY 10027 P: 212-854-4613 F: 212-854-6190 www.sipa.columbia.edu/ocs INTERVIEWS - FINANCIAL MODELING Basic valuation concepts are among the most popular technical

420 W. 118th Street, Room 420 New York, NY 10027 P: 212-854-4613 F: 212-854-6190 www.sipa.columbia.edu/ocs INTERVIEWS - FINANCIAL MODELING Basic valuation concepts are among the most popular technical

TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II + III

SOLUTIONS RE-EXAMS 2014 II + III") TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II III Instructions 1. Only one problem should be treated on each sheet of paper and only one side of the sheet should be used. 2. The solutions folder

TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II III Instructions 1. Only one problem should be treated on each sheet of paper and only one side of the sheet should be used. 2. The solutions folder

Course 1: Evaluating Financial Performance

Excellence in Financial Management Course 1: Evaluating Financial Performance Prepared by: Matt H. Evans, CPA, CMA, CFM This course provides a basic understanding of how to use ratio analysis for evaluating

Excellence in Financial Management Course 1: Evaluating Financial Performance Prepared by: Matt H. Evans, CPA, CMA, CFM This course provides a basic understanding of how to use ratio analysis for evaluating

Chapter 7: Capital Structure: An Overview of the Financing Decision

Chapter 7: Capital Structure: An Overview of the Financing Decision 1. Income bonds are similar to preferred stock in several ways. Payment of interest on income bonds depends on the availability of sufficient

Chapter 7: Capital Structure: An Overview of the Financing Decision 1. Income bonds are similar to preferred stock in several ways. Payment of interest on income bonds depends on the availability of sufficient

The Tangent or Efficient Portfolio

The Tangent or Efficient Portfolio 1 2 Identifying the Tangent Portfolio Sharpe Ratio: Measures the ratio of reward-to-volatility provided by a portfolio Sharpe Ratio Portfolio Excess Return E[ RP ] r

The Tangent or Efficient Portfolio 1 2 Identifying the Tangent Portfolio Sharpe Ratio: Measures the ratio of reward-to-volatility provided by a portfolio Sharpe Ratio Portfolio Excess Return E[ RP ] r

Untangling F9 terminology

Untangling F9 terminology Welcome! This is not a textbook and we are certainly not trying to replace yours! However, we do know that some students find some of the terminology used in F9 difficult to understand.

Untangling F9 terminology Welcome! This is not a textbook and we are certainly not trying to replace yours! However, we do know that some students find some of the terminology used in F9 difficult to understand.

CHAPTER FOUR Cash Accounting, Accrual Accounting, and Discounted Cash Flow Valuation

CHAPTER FOUR Cash Accounting, Accrual Accounting, and Discounted Cash Flow Valuation Concept Questions C4.1. There are difficulties in comparing multiples of earnings and book values - the old techniques

CHAPTER FOUR Cash Accounting, Accrual Accounting, and Discounted Cash Flow Valuation Concept Questions C4.1. There are difficulties in comparing multiples of earnings and book values - the old techniques

1 Pricing options using the Black Scholes formula

Lecture 9 Pricing options using the Black Scholes formula Exercise. Consider month options with exercise prices of K = 45. The variance of the underlying security is σ 2 = 0.20. The risk free interest

Lecture 9 Pricing options using the Black Scholes formula Exercise. Consider month options with exercise prices of K = 45. The variance of the underlying security is σ 2 = 0.20. The risk free interest

The Debt-Equity Trade Off: The Capital Structure Decision

The Debt-Equity Trade Off: The Capital Structure Decision Aswath Damodaran Stern School of Business Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable

The Debt-Equity Trade Off: The Capital Structure Decision Aswath Damodaran Stern School of Business Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable

CHAPTER 22 Options and Corporate Finance

CHAPTER 22 Options and Corporate Finance Multiple Choice Questions: I. DEFINITIONS OPTIONS a 1. A financial contract that gives its owner the right, but not the obligation, to buy or sell a specified asset

CHAPTER 22 Options and Corporate Finance Multiple Choice Questions: I. DEFINITIONS OPTIONS a 1. A financial contract that gives its owner the right, but not the obligation, to buy or sell a specified asset

Nature and Purpose of the Valuation of Business and Financial Assets

G. BUSINESS VALUATIONS 1. Nature and Purpose of the Valuation of Business and Financial Assets 2. Models for the Valuation of Shares 3. The Valuation of Debt and Other Financial Assets 4. Efficient Market

G. BUSINESS VALUATIONS 1. Nature and Purpose of the Valuation of Business and Financial Assets 2. Models for the Valuation of Shares 3. The Valuation of Debt and Other Financial Assets 4. Efficient Market

Claims on Equity: Voting and Liquidity Differentials, Cash flow Preferences and Financing Rights. Aswath Damodaran Stern School of Business

1 Claims on Equity: Voting and Liquidity Differentials, Cash flow Preferences and Financing Rights Aswath Damodaran Stern School of Business August 14, 2008 2 Claims on Equity: Voting Differentials, Cash

1 Claims on Equity: Voting and Liquidity Differentials, Cash flow Preferences and Financing Rights Aswath Damodaran Stern School of Business August 14, 2008 2 Claims on Equity: Voting Differentials, Cash

Chapter 7. . 1. component of the convertible can be estimated as 1100-796.15 = 303.85.

Chapter 7 7-1 Income bonds do share some characteristics with preferred stock. The primary difference is that interest paid on income bonds is tax deductible while preferred dividends are not. Income bondholders

Chapter 7 7-1 Income bonds do share some characteristics with preferred stock. The primary difference is that interest paid on income bonds is tax deductible while preferred dividends are not. Income bondholders

Investment Companies

Mutual Funds Mutual Funds Investment companies Financial intermediaries that collect funds form individual investors and invest those funds in a potentially wide rande of securities or other asstes Polling

Mutual Funds Mutual Funds Investment companies Financial intermediaries that collect funds form individual investors and invest those funds in a potentially wide rande of securities or other asstes Polling

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

Futures Price d,f $ 0.65 = (1.05) (1.04)

(1.04)") 24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

48 Share-based compensation plans

48 Share-based compensation plans Group Equity Incentive Plans The Group Equity Incentive Plans (GEI) of the support the orientation of senior management, in particular the Board of Management, to substainably

48 Share-based compensation plans Group Equity Incentive Plans The Group Equity Incentive Plans (GEI) of the support the orientation of senior management, in particular the Board of Management, to substainably

Basics of Discounted Cash Flow Valuation. Aswath Damodaran

Basics of Discounted Cash Flow Valuation Aswath Damodaran 1 Discounted Cashflow Valuation: Basis for Approach t = n CF Value = t t =1(1+ r) t where, n = Life of the asset CF t = Cashflow in period t r

Basics of Discounted Cash Flow Valuation Aswath Damodaran 1 Discounted Cashflow Valuation: Basis for Approach t = n CF Value = t t =1(1+ r) t where, n = Life of the asset CF t = Cashflow in period t r

Investing on hope? Small Cap and Growth Investing!

Investing on hope? Small Cap and Growth Investing! Aswath Damodaran Aswath Damodaran! 1! Who is a growth investor?! The Conventional definition: An investor who buys high price earnings ratio stocks or

Investing on hope? Small Cap and Growth Investing! Aswath Damodaran Aswath Damodaran! 1! Who is a growth investor?! The Conventional definition: An investor who buys high price earnings ratio stocks or

Financial Ratios and Quality Indicators

Financial Ratios and Quality Indicators From U.S. Small Business Administration Online Women's Business Center If you monitor the ratios on a regular basis you'll gain insight into how effectively you

Financial Ratios and Quality Indicators From U.S. Small Business Administration Online Women's Business Center If you monitor the ratios on a regular basis you'll gain insight into how effectively you

FAIR VALUE ACCOUNTING: VISIONARY THINKING OR OXYMORON? Aswath Damodaran

FAIR VALUE ACCOUNTING: VISIONARY THINKING OR OXYMORON? Aswath Damodaran Three big questions about fair value accounting Why fair value accounting? What is fair value? What are the first principles that

FAIR VALUE ACCOUNTING: VISIONARY THINKING OR OXYMORON? Aswath Damodaran Three big questions about fair value accounting Why fair value accounting? What is fair value? What are the first principles that

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 6 Introduction to Corporate Bonds

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 6 Introduction to Corporate Bonds Today: I. Equity is a call on firm value II. Senior Debt III. Junior Debt IV. Convertible Debt V. Variance

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 6 Introduction to Corporate Bonds Today: I. Equity is a call on firm value II. Senior Debt III. Junior Debt IV. Convertible Debt V. Variance

How Dilution Affects Option Value

How Dilution Affects Option Value If you buy a call option on an options exchange and then exercise it, you have no effect on the number of outstanding shares. The investor who sold the call simply hands

How Dilution Affects Option Value If you buy a call option on an options exchange and then exercise it, you have no effect on the number of outstanding shares. The investor who sold the call simply hands

Things to Absorb, Read, and Do

Things to Absorb, Read, and Do Things to absorb - Everything, plus remember some material from previous chapters. This chapter applies Chapter s 6, 7, and 12, Risk and Return concepts to the market value

Things to Absorb, Read, and Do Things to absorb - Everything, plus remember some material from previous chapters. This chapter applies Chapter s 6, 7, and 12, Risk and Return concepts to the market value

Camille Kerr and Corey Rosen, National Center for Employee Ownership

Camille Kerr and Corey Rosen, National Center for Employee Ownership Companies with 1,000 or fewer employees, almost all of which are closely held, provide almost 60% of all private sector jobs in the

Camille Kerr and Corey Rosen, National Center for Employee Ownership Companies with 1,000 or fewer employees, almost all of which are closely held, provide almost 60% of all private sector jobs in the

A Basic Introduction to the Methodology Used to Determine a Discount Rate

A Basic Introduction to the Methodology Used to Determine a Discount Rate By Dubravka Tosic, Ph.D. The term discount rate is one of the most fundamental, widely used terms in finance and economics. Whether

A Basic Introduction to the Methodology Used to Determine a Discount Rate By Dubravka Tosic, Ph.D. The term discount rate is one of the most fundamental, widely used terms in finance and economics. Whether

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions Chapter 3 Interpreting Financial Ratios Concept Check 3.1 1. What are the different motivations that

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions Chapter 3 Interpreting Financial Ratios Concept Check 3.1 1. What are the different motivations that

Bonds, Preferred Stock, and Common Stock

Bonds, Preferred Stock, and Common Stock I. Bonds 1. An investor has a required rate of return of 4% on a 1-year discount bond with a $100 face value. What is the most the investor would pay for 2. An

Bonds, Preferred Stock, and Common Stock I. Bonds 1. An investor has a required rate of return of 4% on a 1-year discount bond with a $100 face value. What is the most the investor would pay for 2. An

ENTREPRENEURIAL FINANCE: Strategy Valuation and Deal Structure

ENTREPRENEURIAL FINANCE: Strategy Valuation and Deal Structure Chapter 9 Valuation Questions and Problems 1. You are considering purchasing shares of DeltaCad Inc. for $40/share. Your analysis of the company

ENTREPRENEURIAL FINANCE: Strategy Valuation and Deal Structure Chapter 9 Valuation Questions and Problems 1. You are considering purchasing shares of DeltaCad Inc. for $40/share. Your analysis of the company

Stock Valuation: Gordon Growth Model. Week 2

Stock Valuation: Gordon Growth Model Week 2 Approaches to Valuation 1. Discounted Cash Flow Valuation The value of an asset is the sum of the discounted cash flows. 2. Contingent Claim Valuation A contingent

Stock Valuation: Gordon Growth Model Week 2 Approaches to Valuation 1. Discounted Cash Flow Valuation The value of an asset is the sum of the discounted cash flows. 2. Contingent Claim Valuation A contingent

What is Financial Planning

What is Financial Planning Firms must plan for both the short term and the long term. Short-term planning rarely looks further ahead than the next 12 months. It seeks to ensure that the firm has enough

What is Financial Planning Firms must plan for both the short term and the long term. Short-term planning rarely looks further ahead than the next 12 months. It seeks to ensure that the firm has enough

CHAPTER 5 OPTION PRICING THEORY AND MODELS

1 CHAPTER 5 OPTION PRICING THEORY AND MODELS In general, the value of any asset is the present value of the expected cash flows on that asset. In this section, we will consider an exception to that rule

1 CHAPTER 5 OPTION PRICING THEORY AND MODELS In general, the value of any asset is the present value of the expected cash flows on that asset. In this section, we will consider an exception to that rule

t = 1 2 3 1. Calculate the implied interest rates and graph the term structure of interest rates. t = 1 2 3 X t = 100 100 100 t = 1 2 3

MØA 155 PROBLEM SET: Summarizing Exercise 1. Present Value [3] You are given the following prices P t today for receiving risk free payments t periods from now. t = 1 2 3 P t = 0.95 0.9 0.85 1. Calculate

MØA 155 PROBLEM SET: Summarizing Exercise 1. Present Value [3] You are given the following prices P t today for receiving risk free payments t periods from now. t = 1 2 3 P t = 0.95 0.9 0.85 1. Calculate

Forecasting and Valuation of Enterprise Cash Flows 1. Dan Gode and James Ohlson

Forecasting and Valuation of Enterprise Cash Flows 1 1. Overview FORECASTING AND VALUATION OF ENTERPRISE CASH FLOWS Dan Gode and James Ohlson A decision to invest in a stock proceeds in two major steps

Forecasting and Valuation of Enterprise Cash Flows 1 1. Overview FORECASTING AND VALUATION OF ENTERPRISE CASH FLOWS Dan Gode and James Ohlson A decision to invest in a stock proceeds in two major steps

Determining the cost of equity

Determining the cost of equity Macroeconomic factors and the discount rate Baring Asset Management Limited 155 Bishopsgate London EC2M 3XY Tel: +44 (0)20 7628 6000 Fax: +44 (0)20 7638 7928 www.barings.com

Determining the cost of equity Macroeconomic factors and the discount rate Baring Asset Management Limited 155 Bishopsgate London EC2M 3XY Tel: +44 (0)20 7628 6000 Fax: +44 (0)20 7638 7928 www.barings.com

{What s it worth?} in privately owned companies. Valuation of equity compensation. Restricted Stock, Stock Options, Phantom Shares, and

plantemoran.com {What s it worth?} Valuation of equity compensation in privately owned companies Restricted Stock, Stock Options, Phantom Shares, and Other Forms of Equity Compensation The valuation of

plantemoran.com {What s it worth?} Valuation of equity compensation in privately owned companies Restricted Stock, Stock Options, Phantom Shares, and Other Forms of Equity Compensation The valuation of

MML SERIES INVESTMENT FUND

This Prospectus describes the following Funds. MML SERIES INVESTMENT FUND MML Money Market Fund seeks to maximize current income, preserve capital and maintain liquidity by investing in money market instruments.

This Prospectus describes the following Funds. MML SERIES INVESTMENT FUND MML Money Market Fund seeks to maximize current income, preserve capital and maintain liquidity by investing in money market instruments.

FOR IMMEDIATE RELEASE

FOR IMMEDIATE RELEASE For media inquiries, contact: Eric Armstrong, Citrix Systems, Inc. (954) 267-2977 or eric.armstrong@citrix.com For investor inquiries, contact: Eduardo Fleites, Citrix Systems, Inc.

FOR IMMEDIATE RELEASE For media inquiries, contact: Eric Armstrong, Citrix Systems, Inc. (954) 267-2977 or eric.armstrong@citrix.com For investor inquiries, contact: Eduardo Fleites, Citrix Systems, Inc.

5 Equity Plan Numbers You Need at Your Fingertips. Sean Kelly, CEP Morgan Stanley Lisa Klevence, CEP Plan Management Corp. CJ Napolitano Paradata

5 Equity Plan Numbers You Need at Your Fingertips Sean Kelly, CEP Morgan Stanley Lisa Klevence, CEP Plan Management Corp. CJ Napolitano Paradata Don t I just need numbers to complete my reporting requirements?

5 Equity Plan Numbers You Need at Your Fingertips Sean Kelly, CEP Morgan Stanley Lisa Klevence, CEP Plan Management Corp. CJ Napolitano Paradata Don t I just need numbers to complete my reporting requirements?

NorthCoast Investment Advisory Team 203.532.7000 info@northcoastam.com

NorthCoast Investment Advisory Team 203.532.7000 info@northcoastam.com NORTHCOAST ASSET MANAGEMENT An established leader in the field of tactical investment management, specializing in quantitative research

NorthCoast Investment Advisory Team 203.532.7000 info@northcoastam.com NORTHCOAST ASSET MANAGEMENT An established leader in the field of tactical investment management, specializing in quantitative research

Chapter 11 The Cost of Capital ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS

Chapter 11 The Cost of Capital ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 11-1 a. The weighted average cost of capital, WACC, is the weighted average of the after-tax component costs of capital -debt,

Chapter 11 The Cost of Capital ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 11-1 a. The weighted average cost of capital, WACC, is the weighted average of the after-tax component costs of capital -debt,

FRS 14 FINANCIAL REPORTING STANDARDS CONTENTS. Paragraph

ACCOUNTING STANDARDS BOARD OCTOBER 1998 CONTENTS SUMMARY Paragraph Objective 1 Definitions 2 Scope 3-8 Measurement: Basic earnings per share 9-26 Earnings basic 10-13 Number of shares basic 14-26 Bonus

ACCOUNTING STANDARDS BOARD OCTOBER 1998 CONTENTS SUMMARY Paragraph Objective 1 Definitions 2 Scope 3-8 Measurement: Basic earnings per share 9-26 Earnings basic 10-13 Number of shares basic 14-26 Bonus

CIS September 2012 Exam Diet. Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis

CIS September 2012 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Corporate Finance (1 13) 1. Assume a firm issues N1 billion in debt

CIS September 2012 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Corporate Finance (1 13) 1. Assume a firm issues N1 billion in debt

FSA Note: Summary of Financial Ratio Calculations

FSA Note: Summary of Financial Ratio Calculations This note contains a summary of the more common financial statement ratios. A few points should be noted: Calculations vary in practice; consistency and

FSA Note: Summary of Financial Ratio Calculations This note contains a summary of the more common financial statement ratios. A few points should be noted: Calculations vary in practice; consistency and

DUKE UNIVERSITY Fuqua School of Business. FINANCE 351 - CORPORATE FINANCE Problem Set #4 Prof. Simon Gervais Fall 2011 Term 2.

DUK UNIRSITY Fuqua School of Business FINANC 351 - CORPORAT FINANC Problem Set #4 Prof. Simon Gervais Fall 2011 Term 2 Questions 1. Suppose the corporate tax rate is 40%. Consider a firm that earns $1,000

DUK UNIRSITY Fuqua School of Business FINANC 351 - CORPORAT FINANC Problem Set #4 Prof. Simon Gervais Fall 2011 Term 2 Questions 1. Suppose the corporate tax rate is 40%. Consider a firm that earns $1,000

Referred to as the statement of financial position provides a snap shot of a company s assets, liabilities and equity at a particular point in time.

Glossary Aggressive investor Balance sheet Bear market Typically has a higher risk appetite. They are prepared or can afford to risk much more and for this they stand to reap the big rewards. Referred

Glossary Aggressive investor Balance sheet Bear market Typically has a higher risk appetite. They are prepared or can afford to risk much more and for this they stand to reap the big rewards. Referred

Discounted Cash Flow. Alessandro Macrì. Legal Counsel, GMAC Financial Services

Discounted Cash Flow Alessandro Macrì Legal Counsel, GMAC Financial Services History The idea that the value of an asset is the present value of the cash flows that you expect to generate by holding it

Discounted Cash Flow Alessandro Macrì Legal Counsel, GMAC Financial Services History The idea that the value of an asset is the present value of the cash flows that you expect to generate by holding it

Equity Analysis and Capital Structure. A New Venture s Perspective

Equity Analysis and Capital Structure A New Venture s Perspective 1 Venture s Capital Structure ASSETS Short- term Assets Cash A/R Inventories Long- term Assets Plant and Equipment Intellectual Property

Equity Analysis and Capital Structure A New Venture s Perspective 1 Venture s Capital Structure ASSETS Short- term Assets Cash A/R Inventories Long- term Assets Plant and Equipment Intellectual Property

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT PROBLEM SETS 1. In formulating a hedge position, a stock s beta and a bond s duration are used similarly to determine the expected percentage gain or loss

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT PROBLEM SETS 1. In formulating a hedge position, a stock s beta and a bond s duration are used similarly to determine the expected percentage gain or loss

Cost of Capital and Project Valuation

Cost of Capital and Project Valuation 1 Background Firm organization There are four types: sole proprietorships partnerships limited liability companies corporations Each organizational form has different

Cost of Capital and Project Valuation 1 Background Firm organization There are four types: sole proprietorships partnerships limited liability companies corporations Each organizational form has different

Chapter 9. The Valuation of Common Stock. 1.The Expected Return (Copied from Unit02, slide 36)

") Readings Chapters 9 and 10 Chapter 9. The Valuation of Common Stock 1. The investor s expected return 2. Valuation as the Present Value (PV) of dividends and the growth of dividends 3. The investor s required

Readings Chapters 9 and 10 Chapter 9. The Valuation of Common Stock 1. The investor s expected return 2. Valuation as the Present Value (PV) of dividends and the growth of dividends 3. The investor s required

TIP If you do not understand something,

Valuing common stocks Application of the DCF approach TIP If you do not understand something, ask me! The plan of the lecture Review what we have accomplished in the last lecture Some terms about stocks

Valuing common stocks Application of the DCF approach TIP If you do not understand something, ask me! The plan of the lecture Review what we have accomplished in the last lecture Some terms about stocks

Research and Development Expenses: Implications for Profitability Measurement and Valuation. Aswath Damodaran. Stern School of Business

Research and Development Expenses: Implications for Profitability Measurement and Valuation Aswath Damodaran Stern School of Business 44 West Fourth Street New York, NY 10012 adamodar@stern.nyu.edu Abstract

Research and Development Expenses: Implications for Profitability Measurement and Valuation Aswath Damodaran Stern School of Business 44 West Fourth Street New York, NY 10012 adamodar@stern.nyu.edu Abstract

Chapter 4: Liquor Store Business Valuation

Chapter 4: Liquor Store Business Valuation In this section, we will utilize three approaches to valuing a liquor store. These approaches are the: (1) cost (asset based), (2) market, and (3) income approach.

Chapter 4: Liquor Store Business Valuation In this section, we will utilize three approaches to valuing a liquor store. These approaches are the: (1) cost (asset based), (2) market, and (3) income approach.

Option Pricing Theory and Applications. Aswath Damodaran

Option Pricing Theory and Applications Aswath Damodaran What is an option? An option provides the holder with the right to buy or sell a specified quantity of an underlying asset at a fixed price (called

Option Pricing Theory and Applications Aswath Damodaran What is an option? An option provides the holder with the right to buy or sell a specified quantity of an underlying asset at a fixed price (called

Financial Markets And Financial Instruments - Part I

Financial Markets And Financial Instruments - Part I Financial Assets Real assets are things such as land, buildings, machinery, and knowledge that are used to produce goods and services. Financial assets

Financial Markets And Financial Instruments - Part I Financial Assets Real assets are things such as land, buildings, machinery, and knowledge that are used to produce goods and services. Financial assets

Today s Agenda. DFR1 and Quiz 3 recap. Net Capital Expenditures. Working Capital. Dividends. Estimating Cash Flows

Today s Agenda DFR1 and Quiz 3 recap Net Capital Expenditures Working Capital Dividends Estimating Cash Flows Net Capital expenditures Net capital expenditures = capital expenditures - depreciation Depreciation

Today s Agenda DFR1 and Quiz 3 recap Net Capital Expenditures Working Capital Dividends Estimating Cash Flows Net Capital expenditures Net capital expenditures = capital expenditures - depreciation Depreciation

Net Worth Calculation Worksheet

Net Worth Calculation Worksheet A form to help you assess your loved one s financial situation. Name: Date: A. ASSETS List everything your loved one owns that has cash value. 1. Liquid Assets a. Checking

Net Worth Calculation Worksheet A form to help you assess your loved one s financial situation. Name: Date: A. ASSETS List everything your loved one owns that has cash value. 1. Liquid Assets a. Checking

Course Outline. BUSN 6020/1-3 Corporate Finance (3,0,0)

") Course Outline Department of Accounting and Finance School of Business and Economics BUSN 6020/1-3 Corporate Finance (3,0,0) Calendar Description Students acquire the knowledge and skills required to effectively

Course Outline Department of Accounting and Finance School of Business and Economics BUSN 6020/1-3 Corporate Finance (3,0,0) Calendar Description Students acquire the knowledge and skills required to effectively

Trxade Group, Inc. (TCQB: TRXD): Record Revenues in Q3

: Record Revenues in Q3") Siddharth Rajeev, B.Tech, MBA, CFA Analyst November 5, 2015 Trxade Group, Inc. (TCQB: TRXD): Record Revenues in Q3 Sector/Industry: E-commerce Market Data (as of November 5, 2015) Current Price $1.15 Fair

Siddharth Rajeev, B.Tech, MBA, CFA Analyst November 5, 2015 Trxade Group, Inc. (TCQB: TRXD): Record Revenues in Q3 Sector/Industry: E-commerce Market Data (as of November 5, 2015) Current Price $1.15 Fair

New Venture Valuation

New Venture Valuation Antoinette Schoar MIT Sloan School of Management 15.431 Spring 2011 What is Different About Valuing New Ventures? Higher risks and higher uncertainty Potential rewards higher? Option

New Venture Valuation Antoinette Schoar MIT Sloan School of Management 15.431 Spring 2011 What is Different About Valuing New Ventures? Higher risks and higher uncertainty Potential rewards higher? Option

Module 1: Corporate Finance and the Role of Venture Capital Financing TABLE OF CONTENTS

1.0 ALTERNATIVE SOURCES OF FINANCE Module 1: Corporate Finance and the Role of Venture Capital Financing Alternative Sources of Finance TABLE OF CONTENTS 1.1 Short-Term Debt (Short-Term Loans, Line of

1.0 ALTERNATIVE SOURCES OF FINANCE Module 1: Corporate Finance and the Role of Venture Capital Financing Alternative Sources of Finance TABLE OF CONTENTS 1.1 Short-Term Debt (Short-Term Loans, Line of

A guide to investing in cash alternatives

A guide to investing in cash alternatives What you should know before you buy Wells Fargo Advisors wants to help you invest in cash alternative products that are suitable for you based on your investment

A guide to investing in cash alternatives What you should know before you buy Wells Fargo Advisors wants to help you invest in cash alternative products that are suitable for you based on your investment

Leveraged Buyout Model Quick Reference

Leveraged Buyout (LBO) Model Overview A leveraged buyout model shows what happens when a private equity firm acquires a company using a combination of equity (cash) and debt, and then sells it in 3-5 years.

Leveraged Buyout (LBO) Model Overview A leveraged buyout model shows what happens when a private equity firm acquires a company using a combination of equity (cash) and debt, and then sells it in 3-5 years.

Estimating Cash Flows

Estimating Cash Flows DCF Valuation 1 Steps in Cash Flow Estimation Estimate the current earnings of the firm If looking at cash flows to equity, look at earnings after interest expenses - i.e. net income

Estimating Cash Flows DCF Valuation 1 Steps in Cash Flow Estimation Estimate the current earnings of the firm If looking at cash flows to equity, look at earnings after interest expenses - i.e. net income

BASKET A collection of securities. The underlying securities within an ETF are often collectively referred to as a basket

Glossary: The ETF Portfolio Challenge Glossary is designed to help familiarize our participants with concepts and terminology closely associated with Exchange- Traded Products. For more educational offerings,

Glossary: The ETF Portfolio Challenge Glossary is designed to help familiarize our participants with concepts and terminology closely associated with Exchange- Traded Products. For more educational offerings,