Financial Intermediation and Credit Policy in Business Cycle Analysis

|

|

|

- Matilda Clemence Roberts

- 10 years ago

- Views:

Transcription

1 Financial Intermediation and Credit Policy in Business Cycle Analysis 06/2011

2 Introduction Motivation Environment Model Household Banks Non Financial firms Equillibrium Policies Calibration and Simulation Results

3 Motivation Current crisis has been characterised by disruptions in financial intermediation and FED used unconventional MP to handle the crisis. Most of the previous literature focussed on models with frictionless capital markets or frictions on non financial firms. In this paper K&G focus on a real business cycle model with some frictions (financial intermediation and liquidity risk). How credit market frictions may affect real activity? How various credit policies may work given crisis scenario?

.")

4 Continuum of households, Continuum of firms, Continuum of bank (continuum of islands) Goods and Capital goods producers Goverment/Central Bank Two type of island: Investing and Non investing Capital is homogeneous ψ t+1 capital quality shock(markov process), π investment opportunity arrival (i.i.d.)

, π investment opportunity arrival (i.")

5

6 Household Each household has 1 - f workers and f bankers. Bankers exits next period with i.i.d prob 1 σ,the retained earnings is tranfered to the household. Same number of bankers (as exiting) are born out of worker force. Bank pays dividends only when it exits and becomes a worker

7 Household Household chooses consumption, labor supply, and riskless debt (C t, L t, D ht+1 ) to maximize expected discounted utility Complete Consumption insurance: Workers and firms belong to the big group in household Workers and bankers return their wages and earnings, respectively, to the household

8 Banks Agency problem:banker may divert a fraction,θ of the total assts back to its family. The net worth of banks evolve as per the capital quality shock and fluctuation in the return of assets (magnified given high leverage ratio)

9 Banks It can be shown that the value function is linear: Case I:Frictionless interbank mkt: At aggregate level, Q t S t = φ t N t, where φ t is the leverage ratio. Case II:Frictional interbank mkt: At aggregate level, Q h t S h t φ h t N h t.

10 Non Financial firms Goods producers:crs(cobb-douglas)with mobile labour, aggregate productivity A t is markov process,objective to maximise profits Capital goods producers:aggregate production function is DRS in the SR, as are subjected to adjustment cost and is CRS in the LR. Goods producer borrows from the bank and buys new capital,at the price,q i t Lump sum distribution of profits(capital good producers) to the households

11 Equillibrium Households,Banks and Non financial firms maximise utility and profits,respectively. Markets clear in both type of islands (Securities, Labor, Goods, Interbank loans, riskless govt. bonds) If ω indexes (inversly) the relative degree of frictions in interbank market. ω = 1,Frictionless economy: Banks do not face any idiosyncratic liquidity risk (aggregate bank lending is constrained by the aggregate bank capital). ω = 0,Frictional economy:banks constrained balance sheet disrupts credit flows and thus depresses real activity

12 The central bank is not balance sheet constrained. Govt budget const: G t + Q t S t = T t + R t S t 1 3 possible credit policies(s t ) Direct Lending (DL): Expansion of the supply of funds in the market at no subsidised rate. Direct window lending (liquidity facility) (DWL): Expands total level of assets intermediated by banks on investing islands (CB can enforce repayment) Equity injection (EI):Expands value of asset intermediated 1-1 High efficiency cost(evaluation and monitoring). Lump sum taxes(distortionary) and net earning/profits through participation.

(DWL): Expands total level of assets intermediated by banks on investing islands (CB can enforce")

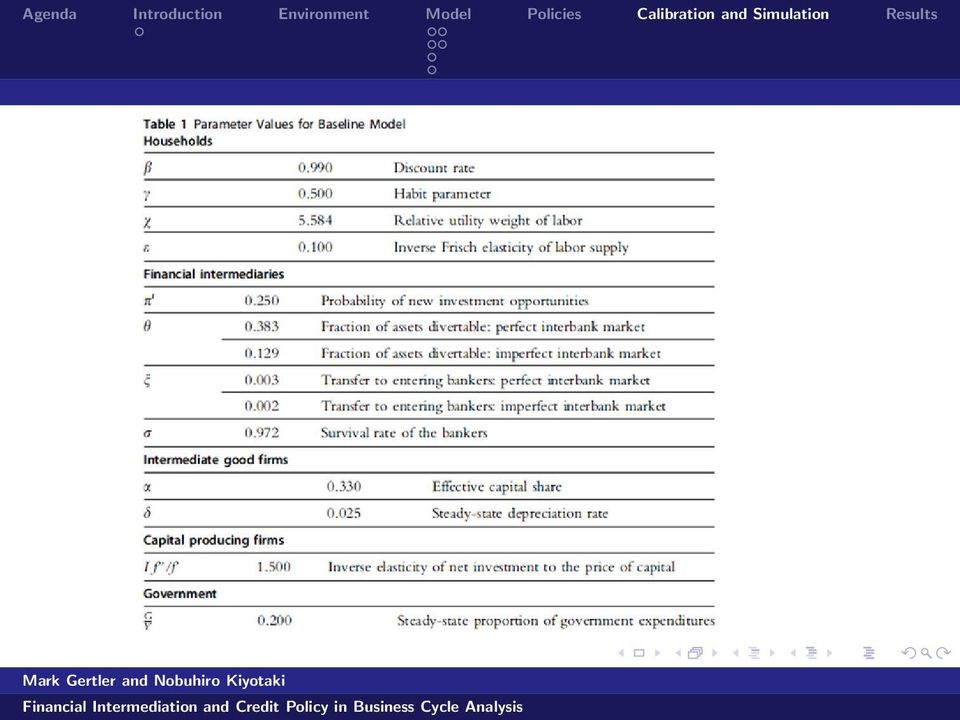

13 Calibration Total 11 parameters (7 are standard preference and technology parameters:β, γ, χ, ɛ, α, δ, η) They consider both ω = 0 and ω = 1 case Crisis simulation Initiation of crisis: Deterioration in value of intermediary portfolios.a 5% unanticipated decline in capital quality with an autoregressive factor of Magnification: Leverage ratio, decline in asset value and net worth,asset prices, balance sheet tightens

14

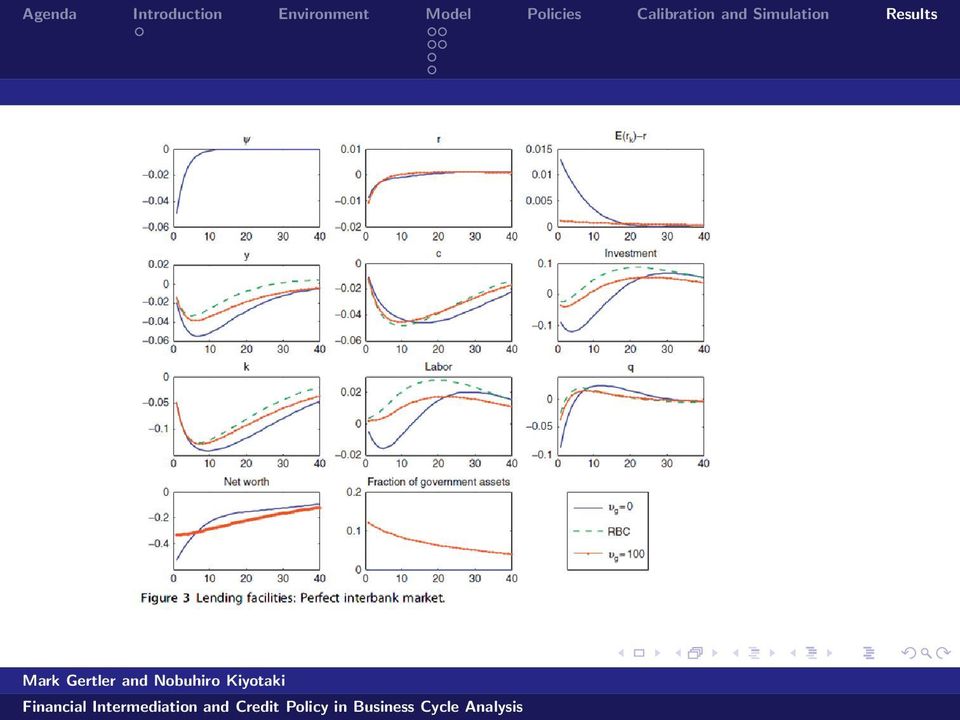

15 With no credit policy: RBC economy: Modest downturn in output and consumption, and high return to capital induces increase in investment and employment Frictionless interbank: Output,investment and employment decline more than in the RBC case. Frictional interbank: Overall deterioration is further magnified. Sharp rise in credit spread. With credit policy (DL): Frictionless interbank: Dampening of overall decline in output,investment and rise in spread. Frictional interbank: Policy effectively dampens the overall deterioration and is in fact much more effective as compared to the previous case

: Frictionless interbank: Dampening of overall decline in output,investment and rise in spread.")

16

17

18

19

Financial Intermediation and Credit Policy in Business Cycle Analysis. Mark Gertler and Nobuhiro Kiyotaki NYU and Princeton

Financial Intermediation and Credit Policy in Business Cycle Analysis Mark Gertler and Nobuhiro Kiyotaki NYU and Princeton Motivation Present a canonical framework to think about the current - nancial

Financial Intermediation and Credit Policy in Business Cycle Analysis Mark Gertler and Nobuhiro Kiyotaki NYU and Princeton Motivation Present a canonical framework to think about the current - nancial

Discussion of Gertler and Kiyotaki: Financial intermediation and credit policy in business cycle analysis

Discussion of Gertler and Kiyotaki: Financial intermediation and credit policy in business cycle analysis Harris Dellas Department of Economics University of Bern June 10, 2010 Figure: Ramon s reaction

Discussion of Gertler and Kiyotaki: Financial intermediation and credit policy in business cycle analysis Harris Dellas Department of Economics University of Bern June 10, 2010 Figure: Ramon s reaction

Financial Intermediation and Credit Policy. Business Cycle Analysis

Financial Intermediation and Credit Policy In Business Cycle Analysis Mark Gertler and Nobuhiro Kiyotaki NYU and Princeton October 29 Old Motivation (for BGG 1999) Great Depression Emerging market crises

Financial Intermediation and Credit Policy In Business Cycle Analysis Mark Gertler and Nobuhiro Kiyotaki NYU and Princeton October 29 Old Motivation (for BGG 1999) Great Depression Emerging market crises

How To Understand How A Crisis In Financial Intermediation Can Be Resolved

Financial Intermediation and Credit Policy in Business Cycle Analysis Mark Gertler and Nobuhiro Kiyotaki N.Y.U. and Princeton October 29 This version: March 21 Abstract We develop a canonical framework

Financial Intermediation and Credit Policy in Business Cycle Analysis Mark Gertler and Nobuhiro Kiyotaki N.Y.U. and Princeton October 29 This version: March 21 Abstract We develop a canonical framework

Discussion of Capital Injection, Monetary Policy, and Financial Accelerators

Discussion of Capital Injection, Monetary Policy, and Financial Accelerators Karl Walentin Sveriges Riksbank 1. Background This paper is part of the large literature that takes as its starting point the

Discussion of Capital Injection, Monetary Policy, and Financial Accelerators Karl Walentin Sveriges Riksbank 1. Background This paper is part of the large literature that takes as its starting point the

MACROECONOMICS. The Monetary System: What It Is and How It Works. N. Gregory Mankiw. PowerPoint Slides by Ron Cronovich

4 : What It Is and How It Works MACROECONOMICS N. Gregory Mankiw Modified for EC 204 by Bob Murphy PowerPoint Slides by Ron Cronovich 2013 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL

4 : What It Is and How It Works MACROECONOMICS N. Gregory Mankiw Modified for EC 204 by Bob Murphy PowerPoint Slides by Ron Cronovich 2013 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL

René Garcia Professor of finance

Liquidity Risk: What is it? How to Measure it? René Garcia Professor of finance EDHEC Business School, CIRANO Cirano, Montreal, January 7, 2009 The financial and economic environment We are living through

Liquidity Risk: What is it? How to Measure it? René Garcia Professor of finance EDHEC Business School, CIRANO Cirano, Montreal, January 7, 2009 The financial and economic environment We are living through

QUIZ IV Version 1. March 24, 2004. 4:35 p.m. 5:40 p.m. BA 2-210

NAME: Student ID: College of Business Administration Department of Economics Principles of Macroeconomics O. Mikhail ECO 2013-0008 Spring 2004 QUIZ IV Version 1 This closed book QUIZ is worth 100 points.

NAME: Student ID: College of Business Administration Department of Economics Principles of Macroeconomics O. Mikhail ECO 2013-0008 Spring 2004 QUIZ IV Version 1 This closed book QUIZ is worth 100 points.

MACROECONOMIC AND INDUSTRY ANALYSIS VALUATION PROCESS

MACROECONOMIC AND INDUSTRY ANALYSIS VALUATION PROCESS BUSINESS ANALYSIS INTRODUCTION To determine a proper price for a firm s stock, security analyst must forecast the dividend & earnings that can be expected

MACROECONOMIC AND INDUSTRY ANALYSIS VALUATION PROCESS BUSINESS ANALYSIS INTRODUCTION To determine a proper price for a firm s stock, security analyst must forecast the dividend & earnings that can be expected

4. The minimum amount of owners' equity in a bank mandated by regulators is called a requirement. A) reserve B) margin C) liquidity D) capital

reserve B) margin C) liquidity D) capital") Chapter 4 - Sample Questions 1. Quantitative easing is most closely akin to: A) discount lending. B) open-market operations. C) fractional-reserve banking. D) capital requirements. 2. Money market mutual

Chapter 4 - Sample Questions 1. Quantitative easing is most closely akin to: A) discount lending. B) open-market operations. C) fractional-reserve banking. D) capital requirements. 2. Money market mutual

Money: Definition. Money: Functions. Money: Types 2/13/2014. ECON 3010 Intermediate Macroeconomics

Money: Definition ECON 3010 Intermediate Macroeconomics Chapter 4 The Monetary System: What It Is and How It Works Money is the stock of assets that can be readily used to make transactions. Money: Functions

Money: Definition ECON 3010 Intermediate Macroeconomics Chapter 4 The Monetary System: What It Is and How It Works Money is the stock of assets that can be readily used to make transactions. Money: Functions

. In this case the leakage effect of tax increases is mitigated because some of the reduction in disposable income would have otherwise been saved.

Chapter 4 Review Questions. Explain how an increase in government spending and an equal increase in lump sum taxes can generate an increase in equilibrium output. Under what conditions will a balanced

Chapter 4 Review Questions. Explain how an increase in government spending and an equal increase in lump sum taxes can generate an increase in equilibrium output. Under what conditions will a balanced

How Bankers Think. Build a sound financial base to support your company for future growth

How Bankers Think Build a sound financial base to support your company for future growth Presented by: Lisa Chapman Business Planning, Social Media Marketing & SEO 615-477-8412 Questions to Consider First

How Bankers Think Build a sound financial base to support your company for future growth Presented by: Lisa Chapman Business Planning, Social Media Marketing & SEO 615-477-8412 Questions to Consider First

The Banking System and the Money Supply. 2003 South-Western/Thomson Learning

The Banking System and the Money Supply 2003 South-Western/Thomson Learning What Counts as Money MONEY Anything that is widely accepted as a means of payment What Counts as Money MONEY Anything that is

The Banking System and the Money Supply 2003 South-Western/Thomson Learning What Counts as Money MONEY Anything that is widely accepted as a means of payment What Counts as Money MONEY Anything that is

ASB Securities. ASB Margin Lending

ASB Securities ASB Margin Lending 2 Contents 01 ASB Margin Lending Widen your investment portfolio How does it work? 02 Why use Margin Lending? 03 The ASB Securities Margin Lending Service 04 The risk/reward

ASB Securities ASB Margin Lending 2 Contents 01 ASB Margin Lending Widen your investment portfolio How does it work? 02 Why use Margin Lending? 03 The ASB Securities Margin Lending Service 04 The risk/reward

Chapter 13 Money and Banking

Chapter 13 Money and Banking After reading Chapter 13, MONEY AND BANKING, you should be able to: Explain the three functions of money: Medium of Exchange, Unit of Account, Store of Value. Understand the

Chapter 13 Money and Banking After reading Chapter 13, MONEY AND BANKING, you should be able to: Explain the three functions of money: Medium of Exchange, Unit of Account, Store of Value. Understand the

Prof Kevin Davis Melbourne Centre for Financial Studies. Current Issues in Bank Capital Planning. Session 4.4

Enhancing Risk Management and Governance in the Region s Banking System to Implement Basel II and to Meet Contemporary Risks and Challenges Arising from the Global Banking System Training Program ~ 8 12

Enhancing Risk Management and Governance in the Region s Banking System to Implement Basel II and to Meet Contemporary Risks and Challenges Arising from the Global Banking System Training Program ~ 8 12

EC 341 Monetary and Banking Institutions, Boston University Summer 2, 2012 Homework 3 Due date: Tuesday, July 31, 6:00 PM.

EC 341 Monetary and Banking Institutions, Boston University Summer 2, 2012 Homework 3 Due date: Tuesday, July 31, 6:00 PM. Problem 1 Questions 1, 4, 6, 8, 12, 13, 16, 18, 22, and 23 from Chapter 8. Solutions:

EC 341 Monetary and Banking Institutions, Boston University Summer 2, 2012 Homework 3 Due date: Tuesday, July 31, 6:00 PM. Problem 1 Questions 1, 4, 6, 8, 12, 13, 16, 18, 22, and 23 from Chapter 8. Solutions:

Net Stable Funding Ratio

Net Stable Funding Ratio Aims to establish a minimum acceptable amount of stable funding based on the liquidity characteristics of an institution s assets and activities over a one year horizon. The amount

Net Stable Funding Ratio Aims to establish a minimum acceptable amount of stable funding based on the liquidity characteristics of an institution s assets and activities over a one year horizon. The amount

Human Capital Risk, Contract Enforcement, and the Macroeconomy

Human Capital Risk, Contract Enforcement, and the Macroeconomy Tom Krebs University of Mannheim Moritz Kuhn University of Bonn Mark Wright UCLA and Chicago Fed General Issue: For many households (the young),

Human Capital Risk, Contract Enforcement, and the Macroeconomy Tom Krebs University of Mannheim Moritz Kuhn University of Bonn Mark Wright UCLA and Chicago Fed General Issue: For many households (the young),

General guidelines for the completion of the bank lending survey questionnaire

General guidelines for the completion of the bank lending survey questionnaire This document includes the general guidelines for the completion of the questionnaire and the terminology used in the survey.

General guidelines for the completion of the bank lending survey questionnaire This document includes the general guidelines for the completion of the questionnaire and the terminology used in the survey.

A Model of Financial Crises

A Model of Financial Crises Coordination Failure due to Bad Assets Keiichiro Kobayashi Research Institute of Economy, Trade and Industry (RIETI) Canon Institute for Global Studies (CIGS) Septempber 16,

A Model of Financial Crises Coordination Failure due to Bad Assets Keiichiro Kobayashi Research Institute of Economy, Trade and Industry (RIETI) Canon Institute for Global Studies (CIGS) Septempber 16,

PRESENT DISCOUNTED VALUE

THE BOND MARKET Bond a fixed (nominal) income asset which has a: -face value (stated value of the bond) - coupon interest rate (stated interest rate) - maturity date (length of time for fixed income payments)

THE BOND MARKET Bond a fixed (nominal) income asset which has a: -face value (stated value of the bond) - coupon interest rate (stated interest rate) - maturity date (length of time for fixed income payments)

Econ 202 Section 2 Final Exam

Douglas, Fall 2009 December 17, 2009 A: Special Code 0000 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 202 Section 2 Final Exam 1. The present value

Douglas, Fall 2009 December 17, 2009 A: Special Code 0000 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 202 Section 2 Final Exam 1. The present value

Chapter 2. Practice Problems. MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 2 Practice Problems MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Assume that you borrow $2000 at 10% annual interest to finance a new

Chapter 2 Practice Problems MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Assume that you borrow $2000 at 10% annual interest to finance a new

Director s Guide to Credit

Federal Reserve Bank of Atlanta Director s Guide to Credit This guide was created by the Supervision and Regulation Division of the Federal Reserve Bank of Atlanta, 1000 Peachtree Street NE, Atlanta,

Federal Reserve Bank of Atlanta Director s Guide to Credit This guide was created by the Supervision and Regulation Division of the Federal Reserve Bank of Atlanta, 1000 Peachtree Street NE, Atlanta,

Macroprudential Policies in Korea

1 IMF-Riksbank Conference Stockholm, November 13~14, 2014 Macroprudential Policies in Korea Tae Soo Kang Disclaimer This presentation represents the views of the author and not necessarily those of the

1 IMF-Riksbank Conference Stockholm, November 13~14, 2014 Macroprudential Policies in Korea Tae Soo Kang Disclaimer This presentation represents the views of the author and not necessarily those of the

FRBSF ECONOMIC LETTER

FRBSF ECONOMIC LETTER 2009-27 August 31, 2009 Credit Market Conditions and the Use of Bank Lines of Credit BY CHRISTOPHER M. JAMES Many credit line agreements contain restrictive covenants and other contingencies

FRBSF ECONOMIC LETTER 2009-27 August 31, 2009 Credit Market Conditions and the Use of Bank Lines of Credit BY CHRISTOPHER M. JAMES Many credit line agreements contain restrictive covenants and other contingencies

Financial Development and Macroeconomic Stability

Financial Development and Macroeconomic Stability Vincenzo Quadrini University of Southern California Urban Jermann Wharton School of the University of Pennsylvania January 31, 2005 VERY PRELIMINARY AND

Financial Development and Macroeconomic Stability Vincenzo Quadrini University of Southern California Urban Jermann Wharton School of the University of Pennsylvania January 31, 2005 VERY PRELIMINARY AND

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Survey of Macroeconomics, MBA 641 Fall 2006, Quiz 4 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The central bank for the United States

Survey of Macroeconomics, MBA 641 Fall 2006, Quiz 4 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The central bank for the United States

- 168 - Chapter Seven. Specification of Financial Soundness Indicators for Other Sectors

- 168 - Chapter Seven Specification of Financial Soundness Indicators for Other Sectors Introduction 7.1 Drawing on the definitions and concepts set out in Part I of the Guide, this chapter explains how

- 168 - Chapter Seven Specification of Financial Soundness Indicators for Other Sectors Introduction 7.1 Drawing on the definitions and concepts set out in Part I of the Guide, this chapter explains how

the actions of the party who is insured. These actions cannot be fully observed or verified by the insurance (hidden action).

.") Moral Hazard Definition: Moral hazard is a situation in which one agent decides on how much risk to take, while another agent bears (parts of) the negative consequences of risky choices. Typical case:

Moral Hazard Definition: Moral hazard is a situation in which one agent decides on how much risk to take, while another agent bears (parts of) the negative consequences of risky choices. Typical case:

ECON 4110: Money, Banking and the Macroeconomy Midterm Exam 2

ECON 4110: Money, Banking and the Macroeconomy Midterm Exam 2 Name: SID: MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following

ECON 4110: Money, Banking and the Macroeconomy Midterm Exam 2 Name: SID: MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following

HAS FINANCE BECOME TOO EXPENSIVE? AN ESTIMATION OF THE UNIT COST OF FINANCIAL INTERMEDIATION IN EUROPE 1951-2007

HAS FINANCE BECOME TOO EXPENSIVE? AN ESTIMATION OF THE UNIT COST OF FINANCIAL INTERMEDIATION IN EUROPE 1951-2007 IPP Policy Briefs n 10 June 2014 Guillaume Bazot www.ipp.eu Summary Finance played an increasing

HAS FINANCE BECOME TOO EXPENSIVE? AN ESTIMATION OF THE UNIT COST OF FINANCIAL INTERMEDIATION IN EUROPE 1951-2007 IPP Policy Briefs n 10 June 2014 Guillaume Bazot www.ipp.eu Summary Finance played an increasing

Lecture 1. Financial Market Frictions and Real Activity: Basic Concepts

Lecture 1 Financial Market Frictions and Real Activity: Basic Concepts Mark Gertler NYU June 2009 0 First Some Background Motivation... 1 Old Macro Analyzes pre versus post 1984:Q4. 1 New Macro Analyzes

Lecture 1 Financial Market Frictions and Real Activity: Basic Concepts Mark Gertler NYU June 2009 0 First Some Background Motivation... 1 Old Macro Analyzes pre versus post 1984:Q4. 1 New Macro Analyzes

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following is the primary source of external funds used by American businesses

Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following is the primary source of external funds used by American businesses

What three main functions do they have? Reducing transaction costs, reducing financial risk, providing liquidity

Unit 4 Test Review KEY Savings, Investment and the Financial System 1. What is a financial intermediary? Explain how each of the following fulfills that role: Financial Intermediary: Transforms funds into

Unit 4 Test Review KEY Savings, Investment and the Financial System 1. What is a financial intermediary? Explain how each of the following fulfills that role: Financial Intermediary: Transforms funds into

Investment insight. Fixed income the what, when, where, why and how TABLE 1: DIFFERENT TYPES OF FIXED INCOME SECURITIES. What is fixed income?

Fixed income investments make up a large proportion of the investment universe and can form a significant part of a diversified portfolio but investors are often much less familiar with how fixed income

Fixed income investments make up a large proportion of the investment universe and can form a significant part of a diversified portfolio but investors are often much less familiar with how fixed income

Finding the Right Financing Mix: The Capital Structure Decision. Aswath Damodaran 1

Finding the Right Financing Mix: The Capital Structure Decision Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate

Finding the Right Financing Mix: The Capital Structure Decision Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate

In ation Tax and In ation Subsidies: Working Capital in a Cash-in-advance model

In ation Tax and In ation Subsidies: Working Capital in a Cash-in-advance model George T. McCandless March 3, 006 Abstract This paper studies the nature of monetary policy with nancial intermediaries that

In ation Tax and In ation Subsidies: Working Capital in a Cash-in-advance model George T. McCandless March 3, 006 Abstract This paper studies the nature of monetary policy with nancial intermediaries that

Debt Overhang and Capital Regulation

Debt Overhang and Capital Regulation Anat Admati INET in Berlin: Rethinking Economics and Politics The Challenge of Deleveraging and Overhangs of Debt II: The Politics and Economics of Restructuring April

Debt Overhang and Capital Regulation Anat Admati INET in Berlin: Rethinking Economics and Politics The Challenge of Deleveraging and Overhangs of Debt II: The Politics and Economics of Restructuring April

Bank and Sovereign Debt Risk Connection

Bank and Sovereign Debt Risk Connection Matthieu Darraq Paries European Central Bank Diego Rodriguez Palenzuela European Central Bank Ester Faia Frankfurt University and CFS First draft: December 212.

Bank and Sovereign Debt Risk Connection Matthieu Darraq Paries European Central Bank Diego Rodriguez Palenzuela European Central Bank Ester Faia Frankfurt University and CFS First draft: December 212.

Banks, Liquidity Management, and Monetary Policy

Discussion of Banks, Liquidity Management, and Monetary Policy by Javier Bianchi and Saki Bigio Itamar Drechsler NYU Stern and NBER Bu/Boston Fed Conference on Macro-Finance Linkages 2013 Objectives 1.

Discussion of Banks, Liquidity Management, and Monetary Policy by Javier Bianchi and Saki Bigio Itamar Drechsler NYU Stern and NBER Bu/Boston Fed Conference on Macro-Finance Linkages 2013 Objectives 1.

Current Accounts in Open Economies Obstfeld and Rogoff, Chapter 2

Current Accounts in Open Economies Obstfeld and Rogoff, Chapter 2 1 Consumption with many periods 1.1 Finite horizon of T Optimization problem maximize U t = u (c t ) + β (c t+1 ) + β 2 u (c t+2 ) +...

Current Accounts in Open Economies Obstfeld and Rogoff, Chapter 2 1 Consumption with many periods 1.1 Finite horizon of T Optimization problem maximize U t = u (c t ) + β (c t+1 ) + β 2 u (c t+2 ) +...

College of Business Administration Savannah State University Personal Finance (BUSA 3000) Quiz 1 Fall 2011 Dr. William A. Dowling.

Quiz 1 Fall 2011 Dr. William A. Dowling.") College of Business Administration Savannah State University Personal Finance (BUSA 3000) Quiz 1 Fall 2011 Dr. William A. Dowling Exam Key Instructions: You are to answer each of the following. If the

College of Business Administration Savannah State University Personal Finance (BUSA 3000) Quiz 1 Fall 2011 Dr. William A. Dowling Exam Key Instructions: You are to answer each of the following. If the

Lecture 16: Financial Crisis

Lecture 16: Financial Crisis What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows in financial markets, with the result that financial

Lecture 16: Financial Crisis What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to information flows in financial markets, with the result that financial

Conceptual Framework: What Does the Financial System Do? 1. Financial contracting: Get funds from savers to investors

Conceptual Framework: What Does the Financial System Do? 1. Financial contracting: Get funds from savers to investors Transactions costs Contracting costs (from asymmetric information) Adverse Selection

Conceptual Framework: What Does the Financial System Do? 1. Financial contracting: Get funds from savers to investors Transactions costs Contracting costs (from asymmetric information) Adverse Selection

Econ 202 Section 4 Final Exam

Douglas, Fall 2009 December 15, 2009 A: Special Code 00004 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 202 Section 4 Final Exam 1. Oceania buys $40

Douglas, Fall 2009 December 15, 2009 A: Special Code 00004 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 202 Section 4 Final Exam 1. Oceania buys $40

Chapter 12 Practice Problems

Chapter 12 Practice Problems 1. Bankers hold more liquid assets than most business firms. Why? The liabilities of business firms (money owed to others) is very rarely callable (meaning that it is required

Chapter 12 Practice Problems 1. Bankers hold more liquid assets than most business firms. Why? The liabilities of business firms (money owed to others) is very rarely callable (meaning that it is required

Reading the balance of payments accounts

Reading the balance of payments accounts The balance of payments refers to both: All the various payments between a country and the rest of the world The particular system of accounting we use to keep

Reading the balance of payments accounts The balance of payments refers to both: All the various payments between a country and the rest of the world The particular system of accounting we use to keep

The Current Crisis in the Subprime Mortgage Market. Jason Vinar GMAC ResCap

The Current Crisis in the Subprime Mortgage Market Jason Vinar GMAC ResCap Overview Merrill s Market Economist, August 2006 Morgan Stanley s Mortgage Finance, March 2007 Citigroup s Housing Monitor, March

The Current Crisis in the Subprime Mortgage Market Jason Vinar GMAC ResCap Overview Merrill s Market Economist, August 2006 Morgan Stanley s Mortgage Finance, March 2007 Citigroup s Housing Monitor, March

Money and Capital in an OLG Model

Money and Capital in an OLG Model D. Andolfatto June 2011 Environment Time is discrete and the horizon is infinite ( =1 2 ) At the beginning of time, there is an initial old population that lives (participates)

Money and Capital in an OLG Model D. Andolfatto June 2011 Environment Time is discrete and the horizon is infinite ( =1 2 ) At the beginning of time, there is an initial old population that lives (participates)

Loan Disclosure Statement

ab Loan Disclosure Statement Risk Factors You Should Consider Before Using Margin or Other Loans Secured by Your Securities Accounts This brochure is only a summary of certain risk factors you should consider

ab Loan Disclosure Statement Risk Factors You Should Consider Before Using Margin or Other Loans Secured by Your Securities Accounts This brochure is only a summary of certain risk factors you should consider

Corporate Credit Analysis. Arnold Ziegel Mountain Mentors Associates

Corporate Credit Analysis Arnold Ziegel Mountain Mentors Associates I. Introduction The Goals and Nature of Credit Analysis II. Capital Structure and the Suppliers of Capital January, 2008 2008 Arnold

Corporate Credit Analysis Arnold Ziegel Mountain Mentors Associates I. Introduction The Goals and Nature of Credit Analysis II. Capital Structure and the Suppliers of Capital January, 2008 2008 Arnold

SMALL BUSINESS DEVELOPMENT CENTER RM. 032

SMALL BUSINESS DEVELOPMENT CENTER RM. 032 FINANCING THROUGH COMMERCIAL BANKS Revised January, 2013 Adapted from: National Federation of Independent Business report Steps to Small Business Financing Jeffrey

SMALL BUSINESS DEVELOPMENT CENTER RM. 032 FINANCING THROUGH COMMERCIAL BANKS Revised January, 2013 Adapted from: National Federation of Independent Business report Steps to Small Business Financing Jeffrey

Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market

Communications P.O. Box, CH-8022 Zurich Telephone +41 44 631 31 11 Fax +41 44 631 39 10 Zurich, 13 September 2007 Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market The

Communications P.O. Box, CH-8022 Zurich Telephone +41 44 631 31 11 Fax +41 44 631 39 10 Zurich, 13 September 2007 Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market The

VI. Real Business Cycles Models

VI. Real Business Cycles Models Introduction Business cycle research studies the causes and consequences of the recurrent expansions and contractions in aggregate economic activity that occur in most industrialized

VI. Real Business Cycles Models Introduction Business cycle research studies the causes and consequences of the recurrent expansions and contractions in aggregate economic activity that occur in most industrialized

Topic 2. Incorporating Financial Frictions in DSGE Models

Topic 2 Incorporating Financial Frictions in DSGE Models Mark Gertler NYU April 2009 0 Overview Conventional Model with Perfect Capital Markets: 1. Arbitrage between return to capital and riskless rate

Topic 2 Incorporating Financial Frictions in DSGE Models Mark Gertler NYU April 2009 0 Overview Conventional Model with Perfect Capital Markets: 1. Arbitrage between return to capital and riskless rate

Company Financial Plan

Financial Modeling Templates http://spreadsheetml.com/finance/companyfinancialplan.shtml Copyright (c) 2009-2014, ConnectCode All Rights Reserved. ConnectCode accepts no responsibility for any adverse

Financial Modeling Templates http://spreadsheetml.com/finance/companyfinancialplan.shtml Copyright (c) 2009-2014, ConnectCode All Rights Reserved. ConnectCode accepts no responsibility for any adverse

ECONOMIC AND MONETARY DEVELOPMENTS

Box 6 SMALL AND MEDIUM-SIZED ENTERPRISES IN THE EURO AREA: ECONOMIC IMPORTANCE AND FINANCING CONDITIONS This box reviews the key role played by small and medium-sized enterprises (SMEs) in the euro area

Box 6 SMALL AND MEDIUM-SIZED ENTERPRISES IN THE EURO AREA: ECONOMIC IMPORTANCE AND FINANCING CONDITIONS This box reviews the key role played by small and medium-sized enterprises (SMEs) in the euro area

real r = nominal r inflation rate (25)

") 3 The price of Loanable Funds Definition 19 INTEREST RATE:(r) Charge per dollar per period that borrowers pay or lenders receive. What affects the interest rate: inflation. risk. taxes. The real interest

3 The price of Loanable Funds Definition 19 INTEREST RATE:(r) Charge per dollar per period that borrowers pay or lenders receive. What affects the interest rate: inflation. risk. taxes. The real interest

Financial Stability Report 2015/2016

Financial Stability Report 2015/2016 Press Conference Presentation Miroslav Singer Governor Prague, 14 June 2016 Structure of presentation I. Overall assessment of risks and setting of countercyclical

Financial Stability Report 2015/2016 Press Conference Presentation Miroslav Singer Governor Prague, 14 June 2016 Structure of presentation I. Overall assessment of risks and setting of countercyclical

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

ECON 4110: Sample Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Economists define risk as A) the difference between the return on common

ECON 4110: Sample Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Economists define risk as A) the difference between the return on common

How Securities Are Traded. Chapter 3

How Securities Are Traded Chapter 3 Primary vs. Secondary Security Sales Primary new issue issuer receives the proceeds from the sale first-time issue: IPO = issuer sells stock for the first time seasoned

How Securities Are Traded Chapter 3 Primary vs. Secondary Security Sales Primary new issue issuer receives the proceeds from the sale first-time issue: IPO = issuer sells stock for the first time seasoned

BANKERS GUIDE TO SECURE LENDING

BANKERS GUIDE TO SECURE LENDING WAREHOUSE RECEIPTS, ORDER OR STRAIGHT BILLS OF LADING, OTHER NEGOTIABLE AND NON-NEGOTIABLE DOCUMENTS OF TITLE, INCLUDING WAREHOUSE AND BAILEE OR DOCK RECEIPTS Lending Rationale

BANKERS GUIDE TO SECURE LENDING WAREHOUSE RECEIPTS, ORDER OR STRAIGHT BILLS OF LADING, OTHER NEGOTIABLE AND NON-NEGOTIABLE DOCUMENTS OF TITLE, INCLUDING WAREHOUSE AND BAILEE OR DOCK RECEIPTS Lending Rationale

Key Points to Borrowing Money

Key Points to Borrowing Money Borrowing money is one of the most common sources of funding for a small business, but obtaining a loan isn't always easy. Before you approach your banker for a loan, it is

Key Points to Borrowing Money Borrowing money is one of the most common sources of funding for a small business, but obtaining a loan isn't always easy. Before you approach your banker for a loan, it is

Business Studies - Financial Planning and Management Study Notes. Financial Planning and Management Study Notes:

Business Studies - Financial Planning and Management Study Notes Financial Planning and Management Study Notes: The Role of Financial Planning: The strategic role of financial management: Organisational

Business Studies - Financial Planning and Management Study Notes Financial Planning and Management Study Notes: The Role of Financial Planning: The strategic role of financial management: Organisational

Copyright 2009 Pearson Education Canada

The consequence of failing to adjust the discount rate for the risk implicit in projects is that the firm will accept high-risk projects, which usually have higher IRR due to their high-risk nature, and

The consequence of failing to adjust the discount rate for the risk implicit in projects is that the firm will accept high-risk projects, which usually have higher IRR due to their high-risk nature, and

Project LINK Meeting New York, 20-22 October 2010. Country Report: Australia

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

Discussion of Bacchetta, Benhima and Poilly : Corporate Cash and Employment

Summary Discussion of Bacchetta, Benhima and Poilly : Corporate Cash and Employment Vivien Lewis (KU Leuven) "New Developments in Business Cycle Analysis : The Role of Labor Markets and International Linkages"

Summary Discussion of Bacchetta, Benhima and Poilly : Corporate Cash and Employment Vivien Lewis (KU Leuven) "New Developments in Business Cycle Analysis : The Role of Labor Markets and International Linkages"

CHAPTER 22: FUTURES MARKETS

CHAPTER 22: FUTURES MARKETS PROBLEM SETS 1. There is little hedging or speculative demand for cement futures, since cement prices are fairly stable and predictable. The trading activity necessary to support

CHAPTER 22: FUTURES MARKETS PROBLEM SETS 1. There is little hedging or speculative demand for cement futures, since cement prices are fairly stable and predictable. The trading activity necessary to support

SPDR S&P 400 Mid Cap Value ETF

SPDR S&P 400 Mid Cap Value ETF Summary Prospectus-October 31, 2015 Before you invest in the SPDR S&P 400 Mid Cap Value ETF (the Fund ), you may want to review the Fund's prospectus and statement of additional

SPDR S&P 400 Mid Cap Value ETF Summary Prospectus-October 31, 2015 Before you invest in the SPDR S&P 400 Mid Cap Value ETF (the Fund ), you may want to review the Fund's prospectus and statement of additional

QE Equivalence to Interest Rate Policy: Implications for Exit

QE Equivalence to Interest Rate Policy: Implications for Exit Samuel Reynard Preliminary Draft - January 13, 2015 Abstract A negative policy interest rate of about 4 percentage points equivalent to the

QE Equivalence to Interest Rate Policy: Implications for Exit Samuel Reynard Preliminary Draft - January 13, 2015 Abstract A negative policy interest rate of about 4 percentage points equivalent to the

THE MEANING OF MONEY. The Functions of Money. Money has three functions in the economy: The Functions of Money. The Functions of Money

In this chapter, look for the answers to these questions: What assets are considered money? What are the functions of money? The types of money? 11 What is the Federal Reserve? What role do banks play

In this chapter, look for the answers to these questions: What assets are considered money? What are the functions of money? The types of money? 11 What is the Federal Reserve? What role do banks play

Lecture Notes on MONEY, BANKING, AND FINANCIAL MARKETS. Peter N. Ireland Department of Economics Boston College. [email protected]

Lecture Notes on MONEY, BANKING, AND FINANCIAL MARKETS Peter N. Ireland Department of Economics Boston College [email protected] http://www2.bc.edu/~irelandp/ec261.html Chapter 9: Banking and the Management

Lecture Notes on MONEY, BANKING, AND FINANCIAL MARKETS Peter N. Ireland Department of Economics Boston College [email protected] http://www2.bc.edu/~irelandp/ec261.html Chapter 9: Banking and the Management

Saving and Investing. Chapter 11 Section Main Menu

Saving and Investing How does investing contribute to the free enterprise system? How does the financial system bring together savers and borrowers? How do financial intermediaries link savers and borrowers?

Saving and Investing How does investing contribute to the free enterprise system? How does the financial system bring together savers and borrowers? How do financial intermediaries link savers and borrowers?

Lending Solutions. Leverage-based products to complement investment strategies. Your Business Without Limits

Lending Solutions Leverage-based products to complement investment strategies Your Business Without Limits Let Pershing Help You Set Yourself Apart Your clients count on you to manage their assets. But

Lending Solutions Leverage-based products to complement investment strategies Your Business Without Limits Let Pershing Help You Set Yourself Apart Your clients count on you to manage their assets. But

4. Only one asset that can be used for production, and is available in xed supply in the aggregate (call it land).

.") Chapter 3 Credit and Business Cycles Here I present a model of the interaction between credit and business cycles. In representative agent models, remember, no lending takes place! The literature on the

Chapter 3 Credit and Business Cycles Here I present a model of the interaction between credit and business cycles. In representative agent models, remember, no lending takes place! The literature on the

FINANCIAL SERVICES BOARD COLLECTIVE INVESTMENT SCHEMES

FINANCIAL SERVICES BOARD COLLECTIVE INVESTMENT SCHEMES INTRODUCTION This booklet will provide you with information on the importance of understanding ways in which Collective Investment Schemes ( CIS )

FINANCIAL SERVICES BOARD COLLECTIVE INVESTMENT SCHEMES INTRODUCTION This booklet will provide you with information on the importance of understanding ways in which Collective Investment Schemes ( CIS )

Long Term Business Financing Strategy For A Pakistan Business. Byco Petroleum Pakistan Limited

Long Term Business Financing Strategy For A Pakistan Business Byco Petroleum Pakistan Limited Contents Why We Need Financing Strategy 3 How Financing Strategies are driven? 4 Financing Prerequisite for

Long Term Business Financing Strategy For A Pakistan Business Byco Petroleum Pakistan Limited Contents Why We Need Financing Strategy 3 How Financing Strategies are driven? 4 Financing Prerequisite for

Chapter 7. . 1. component of the convertible can be estimated as 1100-796.15 = 303.85.

Chapter 7 7-1 Income bonds do share some characteristics with preferred stock. The primary difference is that interest paid on income bonds is tax deductible while preferred dividends are not. Income bondholders

Chapter 7 7-1 Income bonds do share some characteristics with preferred stock. The primary difference is that interest paid on income bonds is tax deductible while preferred dividends are not. Income bondholders

How Do I Qualify for a loan?

How Do I Qualify for a loan? Borrowing money is one of the most common sources of funding for a small business, but obtaining a loan isn't always easy. Before you approach your banker for a loan, it is

How Do I Qualify for a loan? Borrowing money is one of the most common sources of funding for a small business, but obtaining a loan isn't always easy. Before you approach your banker for a loan, it is

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Suvey of Macroeconomics, MBA 641 Fall 2006, Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Modern macroeconomics emerged from

Suvey of Macroeconomics, MBA 641 Fall 2006, Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Modern macroeconomics emerged from

WHAT IS PREMIUM HOW DOES PREMIUM FINANCING? FINANCING WORK?

Life Insurance Premium Financing 1 of 5 WHAT IS PREMIUM FINANCING? Premium financing allows individuals who have a life insurance need to defer using their liquid assets to fund a life insurance policy.

Life Insurance Premium Financing 1 of 5 WHAT IS PREMIUM FINANCING? Premium financing allows individuals who have a life insurance need to defer using their liquid assets to fund a life insurance policy.