DNB Liquidity Pillar 2 Supervision. Seminar Das neue SREP Konzept der Aufsicht Clemens Bonner (c.bonner@dnb.nl)

|

|

|

- Darrell Owen

- 7 years ago

- Views:

Transcription

1 DNB Liquidity Pillar 2 Supervision Seminar Das neue SREP Konzept der Aufsicht Clemens Bonner (c.bonner@dnb.nl)

2 Legal framework Act on Financial Supervision (Wft) Decree on Prudential Rules pursuant to the Wft 2011 Liquidity regulation pursuant to the Wft LCR like monthly reporting since 2003 (adjusted as of May 1st 2011) 2011 Liquidity policy rule pursuant to the Wft Introduction of the ILAAP requirement as of July 1st

3 Overview- ILAAP & Pillar 2 Timeline September 2008: Publication of the BCBS Principles for Sound Liquidity Risk Management and Supervision June 2011: Introduction of Dutch Internal Liquidity Adequacy Assessment Process (ILAAP) From November 2011: quarterly data submissions by banks allowing DNB to carry out a quantitative Pillar 2 assessment and annual submissions of banks qualitative and quantitative risk management information 2012: Formal implementation of funding assessment framework 2013: Formal implementation of top-down liquidity stress test Main purpose of Liquidity Pillar 2 Encourage firms to develop and use better risk management techniques in monitoring and managing their risks Ensure that firms hold internal capital and liquidity buffers that are consistent with their risk profiles and strategies

4 ILAAP and ICAAP Joint but different Risk profile based on FOCUS assessment Qualitative assessment of the controls (EBA principles) ILAAP received from Bank Quantitative assessment ICAAP received from Bank SREP assessment of capital and liquidity buffers Stresstesting

5 The Liquidity SREP process Identification of themes Identification of Themes Banks prepare ILAAP and data submissions Assessment and benchmark sessions DNB Panel and decision making Communication to banks Identification of themes: points of attention which can be specific (i.e. asset encumbrance) but also more general (i.e. funding risks) Assessment and benchmark sessions: Initially split in qualitative and quantitative workstreams, which later come to a joint assessment per bank (includes several meetings with the banks). In the benchmark sessions, outcomes for the individual banks are compared and discussed to ensure a level playing field. DNB Panel and decision making: Panel members are managers of Supervision, Supervision Policy and Financial Stability divisions (to cover both micro and macro). In the panel session, proposed feedback to the bank is discussed and formally approved. Communication to banks: Each SREP round ends with a formal letter communicating the results of the assessment as well as potential measures

but also more general (i.e. funding risks) Assessment and benchmark sessions: Initially split in qualitative and quantitative")

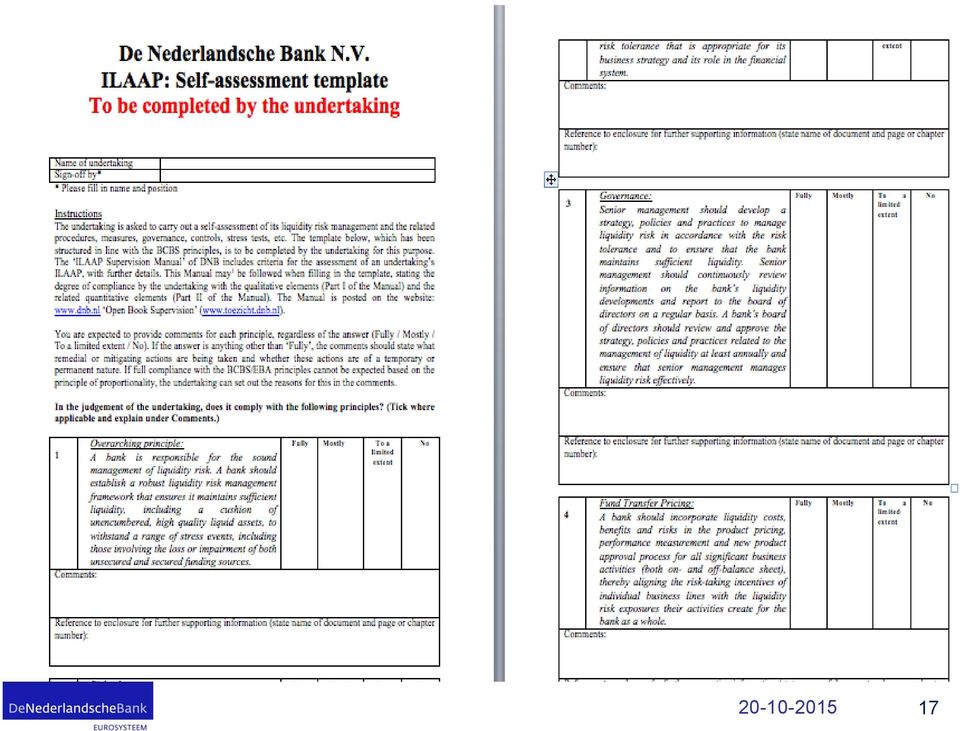

6 Main elements of an ILAAP package Sign off by (a member of) the board of directors Readers manual Overview of the group structure including intra-group (or intra-company for branches) cash flows Documents along the lines of the BCBS Sound Principles, such as: Stress testing Funds Transfer Pricing Risk tolerance and strategy, etc. Completed ILAAP self-assessment template Completed ILAAP Data Template: Balance sheet in 3 major currencies, behavioural and contractual maturity calendar, breakdown of liquidity buffer, funding plan, asset encumbrance, stress testing Explanatory note with details on interpretations made regarding the data template or with details when instructions were not followed as well as explanation on the scope (group / solo) of the report; An ILAAP-process description, including the governance of the ILAAP; An overview of relevant findings by the Internal Audit Department;

7 Building blocks and assessment Short-term liquidity risk Pillar 1 requirement LCR and NSFR Liquidity Stress Testing Long-term funding risk Concentration of funding Asset encumbrance Long term maturity mismatch Currency mismatch Market access External factors Assessment of liquidity and funding risk Mitigating actions required from the bank Strength of governance Risk management Quality of risk management Self assessment Audit

8 Building blocks and assessment Short-term liquidity risk Pillar 1 requirement LCR and NSFR Liquidity Stress Testing Concentration of funding Long-term funding risk Asset encumbrance Long term maturity mismatch Currency mismatch Market access External factors Assessment of liquidity and funding risk Mitigating actions required from the bank Strength of governance Risk management Quality of risk management Self assessment Audit

9 Short-term liquidity risk Dutch Pillar 1 liquidity requirement Compares expected outflows under severe stress with possibilities to generate liquidity Similar to Basel III LCR; more strict on outflow assumptions, more lenient on collateral recognition 1 week & 1 month requirement LCR and NSFR Although not a formal requirement yet, important part of assessment Especially banks migration plans receive attention Stress test Top-down and bottom-up with stress horizons up to 5 years Top-down is used to challenge and benchmark banks internal stress test results Idiosyncratic, marktet-wide as well as combinations Takes into account banks capital and funding position as well as quality of risk management Compliance with Pillar 1 requirement during stress is tested Functions as binding component

10 Building blocks and assessment Short-term liquidity risk Pillar 1 requirement LCR and NSFR Liquidity Stress Testing Long-term funding risk Concentration of funding Asset encumbrance Long term maturity mismatch Currency mismatch Market access External factors Assessment of liquidity and funding risk Mitigating actions required from the bank Strength of governance Risk management Quality of risk management Self assessment Audit

11 Long-term Funding risk 1. The bank s funding sources are well diversified 2. The characteristics of assets and liabilities match 3. No excessive asset encumbrance 4. The bank is active in important funding markets 5. The bank s liquidity buffers are sufficient to withstand prolonged periods of stress 6. The bank s reputation is not at stake (external drivers) Overall assessment of sustainability of funding model Assessment of structural soundness of banks funding models Longer horizon than LCR and stress tests View on market access during times of stress Limits set during ILAAP evaluation but not a minimum requirement Higher risk of unsustainable funding model leads to increased liquidity or capital requirements

12 Building blocks and assessment Short-term liquidity risk Pillar 1 requirement LCR and NSFR Liquidity Stress Testing Long-term funding risk Concentration of funding Asset encumbrance Long term maturity mismatch Currency mismatch Market access External factors Assessment of liquidity and funding risk Mitigating actions required from the bank Strength of governance Risk management Quality of risk management Self assessment Audit

13 Quality of risk management General Liquidity risk management: General Principles Governance Public disclosure Liquidity focused Liquidity risk tolerance and risk appetite Identification and measurement Contingency Funding Plan (CFP) Intraday liquidity risk management Internal stress testing frameworks Collateral management Funding focused Intra-group relationship and currency risks Funding Strategy and market access Fund Transfer Pricing

14 Quality of risk management Contingency Funding Plan (CFP) Internal stress testing frameworks

15 Stress testing Many banks see stress tests as academic exercises to fulfil supervisory expectations However, they should be based on realistic assessments of what can go wrong Important types: Idiosyncratic Market-wide Combined Reverse stress testing Periods: 3 to 12 months Documentation is very important: the regulator should be able to replicate the stress test and understand underlying assumptions

16 Stress testing Scenario assumptions: Complete dry-up of unsecured interbank markets Secured funding is more stable but maturities will shorten Especially complex products will suffer very high haircuts Retail deposits also entail liquidity risk (especially in idiosyncratic stress) Margin calls associated with derivatives increase in the volatility of the underlying asset. Legal impediments on the transfer of liquidity can cause major issues It is difficult to stop lending (roll-over) to retail and corporates Some run-off rates for idiosyncratic stress: Retail: 10% to 15% Unsecured: 100% Corporate: 40% to 60% Committed facilities to SME/corporates (20%) and to banks (100%) Haircuts (depending on rating) Government bonds (5% to 25%) Covered bonds (15% to 70%) ABS (20% to 70%) Equities (25% to 60%)

and to banks (100%) Haircuts (depending on rating) Government bonds (5% to 25%) Covered bonds (15% to 70%) ABS")

17 Contingency Funding Plans If liquidity suddenly evaporates, managers have a very limited amount of time on their hands to act. A plan helps in such a situation Some key questions: Which assets can be more easily sold? What is the estimated price of these sales? Which emergency funding sources may be available? At which cost? What should be done first? Who are the key contacts? Key elements: Roles and responsibilities (procedures, responsibilities and lines of authority to be activated) Early warning indicators (definition of liquidity events and triggers for applying contingency funding plans) Measures (escalation levels and action plans to enhance liquidity management) Communication (procedures for enhancing internal and external communications) Reviews and tests Important: CFP should be practicable with a clear link to liquidity stress tests

Early warning indicators (definition of liquidity events and triggers for applying")

18 Other points of attention Funding Strategy Funds Transfer Pricing Intraday liquidity risk management Data quality

19 ILAAP: linking the principles Bank Business Model Basic Questions: Does the risk appetite correspond with the business model? Has the risk appetite statement been implemented in the risk appetite framework? Are there limits in place that correspond to the risk tolerance? Have stress tests been used to establish limits and buffers? Is the CFP a good fit and are there clear triggers and actions? (linked to stress test)

20

21 How to determine adequacy? Green / 1 = all principles fulfilled Yellow / 2 = Improvement Requirement Orange / 3 = Non Compliance Red / 4 = Non compliance, and risk requires Immediate intervention Overall Assessment 2 Qualitative Criteria Risk Appetite Management Fund pricing Measurement Data integrity Trend analysis Balance sheet Maturity calendar Consolidatie Funding Intraday Collateral Limits Buffer Stress test Forecasts Stress test Contingency plan Liquid assets Publication Assessment of Liquidity Adequacy 2 Quality of ILAAP package 1 Quantitative Criteria Risk Control Risk Position

22 Potential Supervisory Measures Outcome of SREP can refer to both qualitative and quantitative deficiencies In case of deficiencies in risk management, quantitative measures are used as short-term measures and incentives Potential quantitative measures: Higher buffer requirement (increased liquidity requirement) Minimum excess liquidity buffer on top of 100% requirement Limits on concentration of less liquid assets in the buffer Limit on maturity mismatches, foreign currency funding, asset encumbrance Potential qualitative measures: Revision of specific parts of ILAAP (i.e. connect CFP to stress testing results) Broader changes to the banks governance structure

23 Thank You

Liquidity Coverage Ratio

Liquidity Coverage Ratio Aims to ensure banks maintain adequate levels of unencumbered high quality assets (numerator) against net cash outflows (denominator) over a 30 day significant stress period. High

Liquidity Coverage Ratio Aims to ensure banks maintain adequate levels of unencumbered high quality assets (numerator) against net cash outflows (denominator) over a 30 day significant stress period. High

Basel Committee on Banking Supervision

Basel Committee on Banking Supervision Liquidity coverage ratio disclosure standards January 2014 (rev. March 2014) This publication is available on the BIS website (www.bis.org). Bank for International

Basel Committee on Banking Supervision Liquidity coverage ratio disclosure standards January 2014 (rev. March 2014) This publication is available on the BIS website (www.bis.org). Bank for International

NATIONAL BANK OF ROMANIA

NATIONAL BANK OF ROMANIA Regulation No. 18/2009 on governance arrangements of the credit institutions, internal capital adequacy assessment process and the conditions for outsourcing their activities,

NATIONAL BANK OF ROMANIA Regulation No. 18/2009 on governance arrangements of the credit institutions, internal capital adequacy assessment process and the conditions for outsourcing their activities,

Consultation Paper on Liquidity Coverage Ratio Disclosure Requirements

CONSULTATION PAPER P018-2015 Consultation Paper on Disclosure Requirements October 2015 i TABLE OF CONTENTS TABLE OF CONTENTS... ii 1 Preface... 1 2 Specific Areas for Comment... 3 2.1 Scope of Application...

CONSULTATION PAPER P018-2015 Consultation Paper on Disclosure Requirements October 2015 i TABLE OF CONTENTS TABLE OF CONTENTS... ii 1 Preface... 1 2 Specific Areas for Comment... 3 2.1 Scope of Application...

Net Stable Funding Ratio

Net Stable Funding Ratio Aims to establish a minimum acceptable amount of stable funding based on the liquidity characteristics of an institution s assets and activities over a one year horizon. The amount

Net Stable Funding Ratio Aims to establish a minimum acceptable amount of stable funding based on the liquidity characteristics of an institution s assets and activities over a one year horizon. The amount

The PRA s approach to supervising liquidity and funding risks

Supervisory Statement SS24/15 The PRA s approach to supervising liquidity and funding risks June 2015 Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation Authority, registered

Supervisory Statement SS24/15 The PRA s approach to supervising liquidity and funding risks June 2015 Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation Authority, registered

Risk Management Programme Guidelines

Risk Management Programme Guidelines Submissions are invited on these draft Reserve Bank risk management programme guidelines for non-bank deposit takers. Submissions should be made by 29 June 2009 and

Risk Management Programme Guidelines Submissions are invited on these draft Reserve Bank risk management programme guidelines for non-bank deposit takers. Submissions should be made by 29 June 2009 and

Prof Kevin Davis Melbourne Centre for Financial Studies. Managing Liquidity Risks. Session 5.1. Training Program ~ 8 12 December 2008 SHANGHAI, CHINA

Enhancing Risk Management and Governance in the Region s Banking System to Implement Basel II and to Meet Contemporary Risks and Challenges Arising from the Global Banking System Training Program ~ 8 12

Enhancing Risk Management and Governance in the Region s Banking System to Implement Basel II and to Meet Contemporary Risks and Challenges Arising from the Global Banking System Training Program ~ 8 12

Key matters in examining Liquidity Risk Management at Large Complex Financial Groups

Key matters in examining Liquidity Risk Management at Large Complex Financial Groups (1) Governance of liquidity risk management Senior management of a large complex financial group (hereinafter referred

Key matters in examining Liquidity Risk Management at Large Complex Financial Groups (1) Governance of liquidity risk management Senior management of a large complex financial group (hereinafter referred

ICAAP Report Q2 2015

ICAAP Report Q2 2015 Contents 1. INTRODUCTION... 3 1.1 THE THREE PILLARS FROM THE BASEL COMMITTEE... 3 1.2 BOARD OF MANAGEMENT APPROVAL OF THE ICAAP Q2 2015... 3 1.3 CAPITAL CALCULATION... 3 1.1.1 Use

ICAAP Report Q2 2015 Contents 1. INTRODUCTION... 3 1.1 THE THREE PILLARS FROM THE BASEL COMMITTEE... 3 1.2 BOARD OF MANAGEMENT APPROVAL OF THE ICAAP Q2 2015... 3 1.3 CAPITAL CALCULATION... 3 1.1.1 Use

Liquidity Stress Testing

Liquidity Stress Testing Scenario modelling in a globally operating bank APRA Liquidity Risk Management Conference Sydney, 3-4 May 2007 Andrew Martin Head of Funding & Liquidity Risk Management, Asia/Pacific

Liquidity Stress Testing Scenario modelling in a globally operating bank APRA Liquidity Risk Management Conference Sydney, 3-4 May 2007 Andrew Martin Head of Funding & Liquidity Risk Management, Asia/Pacific

Impact assessment of the new liquidity rules on Luxembourg banks

Impact assessment of the new liquidity rules on Luxembourg Abstract of the presentation held at the ABBL conference Basel III New Liquidity Rules: Which Impacts for Luxembourg? 1 Context A local Quantitative

Impact assessment of the new liquidity rules on Luxembourg Abstract of the presentation held at the ABBL conference Basel III New Liquidity Rules: Which Impacts for Luxembourg? 1 Context A local Quantitative

Risk & Capital Management under Basel III

www.pwc.com Risk & Capital Management under Basel III London, 15 Draft Agenda Basel III changes to capital rules - Definition of capital - Minimum capital ratios - Leverage ratio - Buffer requirements

www.pwc.com Risk & Capital Management under Basel III London, 15 Draft Agenda Basel III changes to capital rules - Definition of capital - Minimum capital ratios - Leverage ratio - Buffer requirements

NOVEMBER 2010 (REVISED)

") CENTRAL BANK OF CYPRUS BANKING SUPERVISION AND REGULATION DIVISION DIRECTIVE TO BANKS ON THE COMPUTATION OF PRUDENTIAL LIQUIDITY IN ALL CURRENCIES NOVEMBER 2010 (REVISED) DIRECTIVE TO BANKS ON THE COMPUTATION

CENTRAL BANK OF CYPRUS BANKING SUPERVISION AND REGULATION DIVISION DIRECTIVE TO BANKS ON THE COMPUTATION OF PRUDENTIAL LIQUIDITY IN ALL CURRENCIES NOVEMBER 2010 (REVISED) DIRECTIVE TO BANKS ON THE COMPUTATION

LIQUIDITY RISK MANAGEMENT GUIDELINE

LIQUIDITY RISK MANAGEMENT GUIDELINE April 2009 Table of Contents Preamble... 3 Introduction... 4 Scope... 5 Coming into effect and updating... 6 1. Liquidity risk... 7 2. Sound and prudent liquidity risk

LIQUIDITY RISK MANAGEMENT GUIDELINE April 2009 Table of Contents Preamble... 3 Introduction... 4 Scope... 5 Coming into effect and updating... 6 1. Liquidity risk... 7 2. Sound and prudent liquidity risk

FOREX Bank AB. Annual information about capital adequacy and risk management 1

2011 Annual information about capital adequacy and risk management Annual information about capital adequacy and risk management 1 Introduction FOREX BANK AB, 516406-0104, is the parent company of the

2011 Annual information about capital adequacy and risk management Annual information about capital adequacy and risk management 1 Introduction FOREX BANK AB, 516406-0104, is the parent company of the

Basel Committee on Banking Supervision. Net Stable Funding Ratio disclosure standards

Basel Committee on Banking Supervision Net Stable Funding Ratio disclosure standards June 2015 This publication is available on the BIS website (www.bis.org). Bank for International Settlements 2015. All

Basel Committee on Banking Supervision Net Stable Funding Ratio disclosure standards June 2015 This publication is available on the BIS website (www.bis.org). Bank for International Settlements 2015. All

Policy on the Management of Country Risk by Credit Institutions

2013 Policy on the Management of Country Risk by Credit Institutions 1 Policy on the Management of Country Risk by Credit Institutions Contents 1. Introduction and Application 2 1.1 Application of this

2013 Policy on the Management of Country Risk by Credit Institutions 1 Policy on the Management of Country Risk by Credit Institutions Contents 1. Introduction and Application 2 1.1 Application of this

Basel Committee on Banking Supervision. Principles for Sound Liquidity Risk Management and Supervision. June 2008 DRAFT FOR CONSULTATION

Basel Committee on Banking Supervision Principles for Sound Liquidity Risk Management and Supervision June 2008 DRAFT FOR CONSULTATION Requests for copies of publications, or for additions/changes to

Basel Committee on Banking Supervision Principles for Sound Liquidity Risk Management and Supervision June 2008 DRAFT FOR CONSULTATION Requests for copies of publications, or for additions/changes to

Basel Committee on Banking Supervision. Consultative Document. Net Stable Funding Ratio disclosure standards. Issued for comment by 6 March 2015

Basel Committee on Banking Supervision Consultative Document Net Stable Funding Ratio disclosure standards Issued for comment by 6 March 2015 December 2014 This publication is available on the BIS website

Basel Committee on Banking Supervision Consultative Document Net Stable Funding Ratio disclosure standards Issued for comment by 6 March 2015 December 2014 This publication is available on the BIS website

Liquidity Cash Flow Planning and Stress Testing Model. User s Guide. Version 2.1

Liquidity Cash Flow Planning and Stress Testing Model User s Guide Version 2.1 Table of Contents INTRODUCTION...1 MODEL STRUCTURE...2 BASE CASE ASSUMPTIONS...3 KEY LIQUIDITY VARIABLES...3 WORKSHEET MAINTENANCE...3

Liquidity Cash Flow Planning and Stress Testing Model User s Guide Version 2.1 Table of Contents INTRODUCTION...1 MODEL STRUCTURE...2 BASE CASE ASSUMPTIONS...3 KEY LIQUIDITY VARIABLES...3 WORKSHEET MAINTENANCE...3

Basel Committee on Banking Supervision. Principles for Sound Liquidity Risk Management and Supervision

Basel Committee on Banking Supervision Principles for Sound Liquidity Risk Management and Supervision September 2008 Requests for copies of publications, or for additions/changes to the mailing list,

Basel Committee on Banking Supervision Principles for Sound Liquidity Risk Management and Supervision September 2008 Requests for copies of publications, or for additions/changes to the mailing list,

The Internal Capital Adequacy Assessment Process (ICAAP) and the Supervisory Review and Evaluation Process (SREP)

and the Supervisory Review and Evaluation Process (SREP)") Supervisory Statement SS5/13 The Internal Capital Adequacy Assessment Process (ICAAP) and the Supervisory Review and Evaluation Process (SREP) December 2013 Prudential Regulation Authority 20 Moorgate

Supervisory Statement SS5/13 The Internal Capital Adequacy Assessment Process (ICAAP) and the Supervisory Review and Evaluation Process (SREP) December 2013 Prudential Regulation Authority 20 Moorgate

Economic Commentaries

n Economic Commentaries In its Financial Stability Report 214:1, the Riksbank recommended that a requirement for the Liquidity Coverage Ratio (LCR) in Swedish kronor be introduced. The background to this

n Economic Commentaries In its Financial Stability Report 214:1, the Riksbank recommended that a requirement for the Liquidity Coverage Ratio (LCR) in Swedish kronor be introduced. The background to this

Decision on recovery plans of credit institutions. Subject matter Article 1

Pursuant to Article 101, paragraph (2), item (8) and Article 154, paragraph (2) of the Credit Institutions Act (Official Gazette 159/2013) and Article 43, paragraph (2), item (9) of the Act on the Croatian

Pursuant to Article 101, paragraph (2), item (8) and Article 154, paragraph (2) of the Credit Institutions Act (Official Gazette 159/2013) and Article 43, paragraph (2), item (9) of the Act on the Croatian

Close Brothers Group plc

Close Brothers Group plc Pillar 3 disclosures for the year ended 31 July 2008 Close Brothers Group plc Pillar 3 disclosures for the year ended 31 July 2008 Contents 1. Overview 2. Risk management objectives

Close Brothers Group plc Pillar 3 disclosures for the year ended 31 July 2008 Close Brothers Group plc Pillar 3 disclosures for the year ended 31 July 2008 Contents 1. Overview 2. Risk management objectives

Prudential Standard APS 210 Liquidity

Prudential Standard APS 210 Liquidity Objectives and key requirements of this Prudential Standard This Prudential Standard aims to ensure that an authorised deposit-taking institution adopts prudent practices

Prudential Standard APS 210 Liquidity Objectives and key requirements of this Prudential Standard This Prudential Standard aims to ensure that an authorised deposit-taking institution adopts prudent practices

Basel 3: A new perspective on portfolio risk management. Tamar JOULIA-PARIS October 2011

Basel 3: A new perspective on portfolio risk management Tamar JOULIA-PARIS October 2011 1 Content 1. Basel 3 A complex regulatory framework With possible unintended consequences 2. Consequences on Main

Basel 3: A new perspective on portfolio risk management Tamar JOULIA-PARIS October 2011 1 Content 1. Basel 3 A complex regulatory framework With possible unintended consequences 2. Consequences on Main

Asset and liability management: suggestions for greater effectiveness

Supervisory Statement LSS1/13 Asset and liability management: suggestions for greater effectiveness April 2013 Supervisory Statement LSS1/13 Asset and liability management: suggestions for greater effectiveness

Supervisory Statement LSS1/13 Asset and liability management: suggestions for greater effectiveness April 2013 Supervisory Statement LSS1/13 Asset and liability management: suggestions for greater effectiveness

Guideline. No: B-6 Date: February 2012

Guideline Subject: No: B-6 Date: February 2012 This Guideline sets out prudential considerations relating to the liquidity risk management programs of federally regulated deposit-taking institutions and

Guideline Subject: No: B-6 Date: February 2012 This Guideline sets out prudential considerations relating to the liquidity risk management programs of federally regulated deposit-taking institutions and

Best Practices for Liquidity Regulatory Reporting According to FSA PS09/16 Moody's Analytics Liquidity Risk and FSA Reporting Webinar Series

Best Practices for Liquidity Regulatory Reporting According to FSA PS09/16 Moody's Analytics Liquidity Risk and FSA Reporting Webinar Series XAVIER PERNOT, ANTOINE SPINELLI January, 19th 2010 Agenda 1.

Best Practices for Liquidity Regulatory Reporting According to FSA PS09/16 Moody's Analytics Liquidity Risk and FSA Reporting Webinar Series XAVIER PERNOT, ANTOINE SPINELLI January, 19th 2010 Agenda 1.

Basel Committee on Banking Supervision. Frequently Asked Questions on Basel III s January 2013 Liquidity Coverage Ratio framework

Basel Committee on Banking Supervision Frequently Asked Questions on Basel III s January 2013 Liquidity Coverage Ratio framework April 2014 This publication is available on the BIS website (www.bis.org).

Basel Committee on Banking Supervision Frequently Asked Questions on Basel III s January 2013 Liquidity Coverage Ratio framework April 2014 This publication is available on the BIS website (www.bis.org).

ILAS overview for UK branches of foreign banks

ILAS overview for UK branches of foreign banks Draft version 0.6 Revised June 2010 Page 1 of 8 Katalysys Table of Contents 1 Introduction... 3 2 Overview of the new liquidity framework... 3 3 Scope...

ILAS overview for UK branches of foreign banks Draft version 0.6 Revised June 2010 Page 1 of 8 Katalysys Table of Contents 1 Introduction... 3 2 Overview of the new liquidity framework... 3 3 Scope...

Bank Capital Adequacy under Basel III

Bank Capital Adequacy under Basel III Objectives The overall goal of this two-day workshop is to provide participants with an understanding of how capital is regulated under Basel II and III and appreciate

Bank Capital Adequacy under Basel III Objectives The overall goal of this two-day workshop is to provide participants with an understanding of how capital is regulated under Basel II and III and appreciate

Basel Committee on Banking Supervision. Basel III framework for liquidity - Frequently asked questions

Basel Committee on Banking Supervision Basel III framework for liquidity - Frequently asked questions July 2011 Copies of publications are available from: Bank for International Settlements Communications

Basel Committee on Banking Supervision Basel III framework for liquidity - Frequently asked questions July 2011 Copies of publications are available from: Bank for International Settlements Communications

Standard Chartered Bank (Thai) PCL & its Financial Business Group Pillar 3 Disclosures 30 June 2015

PCL & its Financial Business Group Pillar 3 Disclosures 30 June 2015") Standard Chartered Bank (Thai) PCL & its Financial Business Group Registered Office: 90 North Sathorn Road, Silom Bangkok, 10500, Thailand Overview During 2013, the Bank of Thailand ( BOT ) published the

Standard Chartered Bank (Thai) PCL & its Financial Business Group Registered Office: 90 North Sathorn Road, Silom Bangkok, 10500, Thailand Overview During 2013, the Bank of Thailand ( BOT ) published the

Disclosure 17 OffV (Credit Risk Mitigation Techniques)

") Disclosure 17 OffV (Credit Risk Mitigation Techniques) The Austrian Financial Market Authority (FMA) and the Oesterreichsiche Nationalbank (OeNB) have assessed UniCredit Bank Austria AG for the use of

Disclosure 17 OffV (Credit Risk Mitigation Techniques) The Austrian Financial Market Authority (FMA) and the Oesterreichsiche Nationalbank (OeNB) have assessed UniCredit Bank Austria AG for the use of

Regulatory Practice Letter November 2014 RPL 14-20

Regulatory Practice Letter November 2014 RPL 14-20 BCBS Issues Final Net Stable Funding Ratio Standard Executive Summary The Basel Committee on Banking Supervision ( BCBS or Basel Committee ) issued its

Regulatory Practice Letter November 2014 RPL 14-20 BCBS Issues Final Net Stable Funding Ratio Standard Executive Summary The Basel Committee on Banking Supervision ( BCBS or Basel Committee ) issued its

S t a n d a r d 4. 4 c. M a n a g e m e n t o f m a r k e t r i s k. Regulations and guidelines

S t a n d a r d 4. 4 c M a n a g e m e n t o f m a r k e t r i s k Regulations and guidelines H o w t o r e a d a s t a n d a r d A standard is a collection of subject-specific regulations and guidelines

S t a n d a r d 4. 4 c M a n a g e m e n t o f m a r k e t r i s k Regulations and guidelines H o w t o r e a d a s t a n d a r d A standard is a collection of subject-specific regulations and guidelines

DG FISMA CONSULTATION PAPER ON FURTHER CONSIDERATIONS FOR THE IMPLEMENTATION OF THE NSFR IN THE EU

EUROPEAN COMMISSION Directorate-General for Financial Stability, Financial Services and Capital Markets Union DG FISMA CONSULTATION PAPER ON FURTHER CONSIDERATIONS FOR THE IMPLEMENTATION OF THE NSFR IN

EUROPEAN COMMISSION Directorate-General for Financial Stability, Financial Services and Capital Markets Union DG FISMA CONSULTATION PAPER ON FURTHER CONSIDERATIONS FOR THE IMPLEMENTATION OF THE NSFR IN

PART B INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS (ICAAP)

") Framework (Basel II) Internal Capital Adequacy Assessment PART A OVERVIEW...2 1. Introduction...2 2. Applicability...3 3. Legal Provision...3 4. Effective Date of Implementation...3 5. Level of Application...3

Framework (Basel II) Internal Capital Adequacy Assessment PART A OVERVIEW...2 1. Introduction...2 2. Applicability...3 3. Legal Provision...3 4. Effective Date of Implementation...3 5. Level of Application...3

Supervisory Statement SS18/13. Recovery planning. December 2013. (Last updated 16 January 2015)

") Supervisory Statement SS18/13 Recovery planning December 2013 (Last updated 16 January 2015) Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation Authority, registered office:

Supervisory Statement SS18/13 Recovery planning December 2013 (Last updated 16 January 2015) Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation Authority, registered office:

Interagency Guidance on Funds Transfer Pricing Related to Funding and Contingent Liquidity Risks. March 1, 2016

Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of the Comptroller of the Currency Interagency Guidance on Funds Transfer Pricing Related to Funding and Contingent

Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of the Comptroller of the Currency Interagency Guidance on Funds Transfer Pricing Related to Funding and Contingent

Policy Statement PS11/15. CRD IV: Liquidity. June 2015

Policy Statement PS11/15 CRD IV: Liquidity June 2015 Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation Authority, registered office: 8 Lothbury, London EC2R 7HH. Registered

Policy Statement PS11/15 CRD IV: Liquidity June 2015 Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation Authority, registered office: 8 Lothbury, London EC2R 7HH. Registered

The challenge of liquidity and collateral management in the new regulatory landscape

The challenge of liquidity and collateral management in the new regulatory landscape ICMA Professional Repo and Collateral Management Course 2012 Agenda 1. Background: The repo product under pressure 2.

The challenge of liquidity and collateral management in the new regulatory landscape ICMA Professional Repo and Collateral Management Course 2012 Agenda 1. Background: The repo product under pressure 2.

FS Regulatory Brief. Basel III liquidity regime More practical but not yet workable. January 2013. Key LCR changes

Basel III liquidity regime More practical but not yet workable January 2013 On January 7 th, the Basel Committee on Banking Supervision ( BCBS ) issued a finalized standard ( Standard ) on the Liquidity

Basel III liquidity regime More practical but not yet workable January 2013 On January 7 th, the Basel Committee on Banking Supervision ( BCBS ) issued a finalized standard ( Standard ) on the Liquidity

Basel Committee on Banking Supervision. Frequently asked. monitoring

Basel Committee on Banking Supervision Frequently asked questions on Basel III monitoring REVISED September 2012 Requests for copies of publications, or for additions/changes to the mailing list, should

Basel Committee on Banking Supervision Frequently asked questions on Basel III monitoring REVISED September 2012 Requests for copies of publications, or for additions/changes to the mailing list, should

Solutions for Balance Sheet Management

ENTERPRISE RISK SOLUTIONS Solutions for Balance Sheet Management Moody s Analytics offers a powerful combination of software and advisory services for essential balance sheet and liquidity risk management.

ENTERPRISE RISK SOLUTIONS Solutions for Balance Sheet Management Moody s Analytics offers a powerful combination of software and advisory services for essential balance sheet and liquidity risk management.

Prudential Standard APS 210 Liquidity

Prudential Standard APS 210 Liquidity Objectives and key requirements of this Prudential Standard This Prudential Standard requires an authorised deposit-taking institution to adopt prudent practices in

Prudential Standard APS 210 Liquidity Objectives and key requirements of this Prudential Standard This Prudential Standard requires an authorised deposit-taking institution to adopt prudent practices in

Basel III Liquidity Risk Monitoring and IT Infrastructure impacts

RISK MANAGEMENT Basel III Liquidity Risk Monitoring and IT Infrastructure impacts Richard Filippi Headstrong This paper will delve into some of the issues surrounding Basel III Liquidity Risk Measurements

RISK MANAGEMENT Basel III Liquidity Risk Monitoring and IT Infrastructure impacts Richard Filippi Headstrong This paper will delve into some of the issues surrounding Basel III Liquidity Risk Measurements

Comments on the Basel Committee on Banking Supervision s Consultative Document: Monitoring indicators for intraday liquidity management

September 14, 2012 Comments on the Basel Committee on Banking Supervision s Consultative Document: Monitoring indicators for intraday liquidity management Japanese Bankers Association We, the Japanese

September 14, 2012 Comments on the Basel Committee on Banking Supervision s Consultative Document: Monitoring indicators for intraday liquidity management Japanese Bankers Association We, the Japanese

Basel Committee on Banking Supervision. Consultative Document. Basel III: The Net Stable Funding Ratio. Issued for comment by 11 April 2014

Basel Committee on Banking Supervision Consultative Document Basel III: The Net Stable Funding Ratio Issued for comment by 11 April 2014 January 2014 This publication is available on the BIS website (www.bis.org).

Basel Committee on Banking Supervision Consultative Document Basel III: The Net Stable Funding Ratio Issued for comment by 11 April 2014 January 2014 This publication is available on the BIS website (www.bis.org).

Basel Committee on Banking Supervision. Basel III: the net stable funding ratio

Basel Committee on Banking Supervision Basel III: the net stable funding ratio October 2014 This publication is available on the BIS website (www.bis.org). Bank for International Settlements 2014. All

Basel Committee on Banking Supervision Basel III: the net stable funding ratio October 2014 This publication is available on the BIS website (www.bis.org). Bank for International Settlements 2014. All

RISK MANAGEMENT REPORT (for the Financial Year Ended 31 March 2012)

") RISK MANAGEMENT REPORT (for the Financial Year Ended 31 March 2012) Integrated Risk Management Framework The Group s Integrated Risk Management Framework (IRMF) sets the fundamental elements to manage

RISK MANAGEMENT REPORT (for the Financial Year Ended 31 March 2012) Integrated Risk Management Framework The Group s Integrated Risk Management Framework (IRMF) sets the fundamental elements to manage

Basel Committee on Banking Supervision. Standards. Interest rate risk in the banking book

Basel Committee on Banking Supervision Standards Interest rate risk in the banking book April 2016 This publication is available on the BIS website (www.bis.org). Bank for International Settlements 2016.

Basel Committee on Banking Supervision Standards Interest rate risk in the banking book April 2016 This publication is available on the BIS website (www.bis.org). Bank for International Settlements 2016.

PART A: OVERVIEW...1 1. Introduction...1. 2. Applicability...2. 3. Legal Provisions...2. 4. Effective Date...2

PART A: OVERVIEW...1 1. Introduction...1 2. Applicability...2 3. Legal Provisions...2 4. Effective Date...2 PART B: INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS...3 5. Overview of ICAAP...3 6. Board and

PART A: OVERVIEW...1 1. Introduction...1 2. Applicability...2 3. Legal Provisions...2 4. Effective Date...2 PART B: INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS...3 5. Overview of ICAAP...3 6. Board and

NUCSOFT. Asset Liability Management

NUCSOFT Asset Liability Management ALM Overview Forecasting, Budgeting & Planning Tool for Advanced Liquidity Management & ALM Analysis & Monitoring of Liquidity Buffers, Key Regulatory Ratios such as

NUCSOFT Asset Liability Management ALM Overview Forecasting, Budgeting & Planning Tool for Advanced Liquidity Management & ALM Analysis & Monitoring of Liquidity Buffers, Key Regulatory Ratios such as

Santander Views on Basel s Liquidity Framework

Santander Views on Basel s Liquidity Framework Presentation Santander welcomes the effort made by the Basel Committee to safeguard financial market stability and to preserve the system from a renewed liquidity

Santander Views on Basel s Liquidity Framework Presentation Santander welcomes the effort made by the Basel Committee to safeguard financial market stability and to preserve the system from a renewed liquidity

ZAG BANK BASEL II & III PILLAR 3 DISCLOSURES. December 31, 2014

ZAG BANK BASEL II & III PILLAR 3 DISCLOSURES December 31, 2014 Zag Bank (the Bank ) is required to make certain disclosures to meet the requirements of the Office of the Superintendent of Financial Institutions

ZAG BANK BASEL II & III PILLAR 3 DISCLOSURES December 31, 2014 Zag Bank (the Bank ) is required to make certain disclosures to meet the requirements of the Office of the Superintendent of Financial Institutions

Information on Capital Structure, Liquidity and Leverage Ratios as per Basel III Framework. as at March 31, 2015 PUBLIC

Information on Capital Structure, Liquidity and Leverage Ratios as per Basel III Framework as at Table of Contents Capital Structure Page Statement of Financial Position - Step 1 (Table 2(b)) 3 Statement

Information on Capital Structure, Liquidity and Leverage Ratios as per Basel III Framework as at Table of Contents Capital Structure Page Statement of Financial Position - Step 1 (Table 2(b)) 3 Statement

Basel Committee on Banking Supervision. Frequently asked questions on Basel III monitoring. February 2013 BANK FOR INTERNATIONAL SETTLEMENTS

Basel Committee on Banking Supervision Frequently asked questions on Basel III monitoring February 2013 BANK FOR INTERNATIONAL SETTLEMENTS This publication is available on the BIS website (www.bis.org).

Basel Committee on Banking Supervision Frequently asked questions on Basel III monitoring February 2013 BANK FOR INTERNATIONAL SETTLEMENTS This publication is available on the BIS website (www.bis.org).

INTERNAL CAPITAL ADEQUACY ASSESSMENT

INTERNAL CAPITAL ADEQUACY ASSESSMENT 30 june 2011 Contents Page 1. Introduction... 3 2. Process for determining the solvency need... 4 2.1. The basis for capital management... 4 2.2. Risk identification...

INTERNAL CAPITAL ADEQUACY ASSESSMENT 30 june 2011 Contents Page 1. Introduction... 3 2. Process for determining the solvency need... 4 2.1. The basis for capital management... 4 2.2. Risk identification...

Liquidity: A bigger challenge than capital

FINANCIAL SERVICES Liquidity: A bigger challenge than capital May 2012 kpmg.com 2 LIQUIDITY: A BIGGER CHALLENGE THAN CAPITAL Liquidity: A bigger challenge than capital The Basel Committee on Banking Supervision

FINANCIAL SERVICES Liquidity: A bigger challenge than capital May 2012 kpmg.com 2 LIQUIDITY: A BIGGER CHALLENGE THAN CAPITAL Liquidity: A bigger challenge than capital The Basel Committee on Banking Supervision

EBA-GL-2015-02. 23 July 2015. Guidelines. on the minimum list of qualitative and quantitative recovery plan indicators

EBA-GL-2015-02 23 July 2015 Guidelines on the minimum list of qualitative and quantitative recovery plan indicators Contents EBA Guidelines on the minimum list of qualitative and quantitative recovery

EBA-GL-2015-02 23 July 2015 Guidelines on the minimum list of qualitative and quantitative recovery plan indicators Contents EBA Guidelines on the minimum list of qualitative and quantitative recovery

1. Introduction... 3. 2. Process for determining the solvency need... 4. 3. Definitions of main risk types... 9

Contents Page 1. Introduction... 3 2. Process for determining the solvency need... 4 2.1 The basis for capital management...4 2.2 Risk identification...5 2.3 Danske Bank s internal assessment of its solvency

Contents Page 1. Introduction... 3 2. Process for determining the solvency need... 4 2.1 The basis for capital management...4 2.2 Risk identification...5 2.3 Danske Bank s internal assessment of its solvency

Guidance Note: Stress Testing Class 2 Credit Unions. November, 2013. Ce document est également disponible en français

Guidance Note: Stress Testing Class 2 Credit Unions November, 2013 Ce document est également disponible en français This Guidance Note is for use by all Class 2 credit unions with assets in excess of $1

Guidance Note: Stress Testing Class 2 Credit Unions November, 2013 Ce document est également disponible en français This Guidance Note is for use by all Class 2 credit unions with assets in excess of $1

Basel III: Liquidity Rules

February 2011 Basel III: Liquidity Rules 1 Introduction and timing On 16 December 2010 the Basel Committee on Banking Supervision (the Committee ) published the final form of a set of reforms to strengthen

February 2011 Basel III: Liquidity Rules 1 Introduction and timing On 16 December 2010 the Basel Committee on Banking Supervision (the Committee ) published the final form of a set of reforms to strengthen

ORSA - The heart of Solvency II

ORSA - The heart of Solvency II Groupe Consultatif Summer School Gabriel Bernardino, EIOPA Lisbon, 25 May 2011 ORSA - The heart of Solvency II Developing the regulatory framework for Solvency II ORSA it

ORSA - The heart of Solvency II Groupe Consultatif Summer School Gabriel Bernardino, EIOPA Lisbon, 25 May 2011 ORSA - The heart of Solvency II Developing the regulatory framework for Solvency II ORSA it

Consultation Paper. Draft regulatory technical standards

EBA/CP/2013/39 22.10.2013 Consultation Paper Draft regulatory technical standards On derogations for currencies with constraints on the availability of liquid assets under Article 419(5) of Regulation

EBA/CP/2013/39 22.10.2013 Consultation Paper Draft regulatory technical standards On derogations for currencies with constraints on the availability of liquid assets under Article 419(5) of Regulation

An Oracle White Paper October 2012. Liquidity Risk: Thinking Beyond Compliance

An Oracle White Paper October 2012 Liquidity Risk: Thinking Beyond Compliance Executive Overview... 2 Introduction... 2 Competing Challenges... 3 A Costly Proposition... 4 Looking Long-Term... 6 Conclusion...

An Oracle White Paper October 2012 Liquidity Risk: Thinking Beyond Compliance Executive Overview... 2 Introduction... 2 Competing Challenges... 3 A Costly Proposition... 4 Looking Long-Term... 6 Conclusion...

GUIDELINES ON CORPORATE GOVERNANCE FOR LABUAN BANKS

GUIDELINES ON CORPORATE GOVERNANCE FOR LABUAN BANKS 1.0 Introduction 1.1 Good corporate governance practice improves safety and soundness through effective risk management and creates the ability to execute

GUIDELINES ON CORPORATE GOVERNANCE FOR LABUAN BANKS 1.0 Introduction 1.1 Good corporate governance practice improves safety and soundness through effective risk management and creates the ability to execute

Information on Capital Structure, Liquidity Coverage and Leverage Ratios as per Basel-III Framework as at March 31, 2016

Information on Capital Structure, Liquidity Coverage and Leverage Ratios as per Basel-III Framework as at March 31, 2016 Table of Contents Capital Structure Statement of Financial Position - Step 1 ( Table

Information on Capital Structure, Liquidity Coverage and Leverage Ratios as per Basel-III Framework as at March 31, 2016 Table of Contents Capital Structure Statement of Financial Position - Step 1 ( Table

Liquidity Risk Stress Testing

Liquidity Risk Stress Testing White Paper Liquidity Risk Stress Testing In this White Paper A financial world under transformation...4 Characteristics of liquidity risk management...5 New regulation and

Liquidity Risk Stress Testing White Paper Liquidity Risk Stress Testing In this White Paper A financial world under transformation...4 Characteristics of liquidity risk management...5 New regulation and

Capital Requirements Directive IV Framework Liquidity Requirements. Allen & Overy Client Briefing Paper 15 January 2014. www.allenovery.

Capital Requirements Directive IV Framework Liquidity Requirements Allen & Overy Client Briefing Paper 15 January 2014 2 CRD IV Framework: Liquidity Requirements January 2014 CRD IV Framework: Liquidity

Capital Requirements Directive IV Framework Liquidity Requirements Allen & Overy Client Briefing Paper 15 January 2014 2 CRD IV Framework: Liquidity Requirements January 2014 CRD IV Framework: Liquidity

U.S. regulatory capital: Basel III liquidity coverage ratio final rule

U.S. regulatory capital: Basel III liquidity coverage ratio final rule Overview and key highlights November 2014 DRAFT - For Discussion Purposes Only Contents U.S. Basel III Liquidity Coverage Ratio (LCR)

U.S. regulatory capital: Basel III liquidity coverage ratio final rule Overview and key highlights November 2014 DRAFT - For Discussion Purposes Only Contents U.S. Basel III Liquidity Coverage Ratio (LCR)

Securitization Perspectives: Final U.S. Liquidity Coverage Ratio. September 10, 2014

Securitization Perspectives: Final U.S. Liquidity Coverage Ratio September 10, 2014 Introduction! On September 3rd, the Agencies adopted regulations implementing a liquidity coverage ratio (LCR) requirement

Securitization Perspectives: Final U.S. Liquidity Coverage Ratio September 10, 2014 Introduction! On September 3rd, the Agencies adopted regulations implementing a liquidity coverage ratio (LCR) requirement

Society of Actuaries in Ireland

Society of Actuaries in Ireland Information and Assistance Note LA-1: Actuaries involved in the Own Risk & Solvency Assessment (ORSA) under Solvency II Life Assurance and Life Reinsurance Business Issued

Society of Actuaries in Ireland Information and Assistance Note LA-1: Actuaries involved in the Own Risk & Solvency Assessment (ORSA) under Solvency II Life Assurance and Life Reinsurance Business Issued

ICAAP Required Capital Assessment, Quantification & Allocation. Anand Borawake, VP, Risk Management, TD Bank anand.borawake@td.com

ICAAP Required Capital Assessment, Quantification & Allocation Anand Borawake, VP, Risk Management, TD Bank anand.borawake@td.com Table of Contents Key Takeaways - Value Add from the ICAAP The 3 Pillars

ICAAP Required Capital Assessment, Quantification & Allocation Anand Borawake, VP, Risk Management, TD Bank anand.borawake@td.com Table of Contents Key Takeaways - Value Add from the ICAAP The 3 Pillars

Regional workshop BCCL-METAC Operational functioning of supervisory Colleges BEYROUTH, April 25 th, 2012

Regional workshop BCCL-METAC Operational functioning of supervisory Colleges BEYROUTH, April 25 th, 2012 INTRODUCTION SUPERVISORY COLLEGES ARE A FUNDAMENTAL TOOL OF COOPERATION : At the light of the crisis,

Regional workshop BCCL-METAC Operational functioning of supervisory Colleges BEYROUTH, April 25 th, 2012 INTRODUCTION SUPERVISORY COLLEGES ARE A FUNDAMENTAL TOOL OF COOPERATION : At the light of the crisis,

DISCLOSURE ON CAPITAL ADEQUACY & MARKET DISCIPLINE (CAMD)

") DISCLOSURE ON CAPITAL ADEQUACY & MARKET DISCIPLINE (CAMD) A) Scope of Application : (a) This guidelines applies to Delta Brac Housing Finance Corporation Ltd. (b) (c) DBH has no subsidiary companies. Not

DISCLOSURE ON CAPITAL ADEQUACY & MARKET DISCIPLINE (CAMD) A) Scope of Application : (a) This guidelines applies to Delta Brac Housing Finance Corporation Ltd. (b) (c) DBH has no subsidiary companies. Not

MISSION VALUES. The guide has been printed by:

www.cudgc.sk.ca MISSION We instill public confidence in Saskatchewan credit unions by guaranteeing deposits. As the primary prudential and solvency regulator, we promote responsible governance by credit

www.cudgc.sk.ca MISSION We instill public confidence in Saskatchewan credit unions by guaranteeing deposits. As the primary prudential and solvency regulator, we promote responsible governance by credit

Rogers Bank Basel III Pillar 3 Disclosures

Basel III Pillar 3 Disclosures As at June 30, 2014 Table of Contents 1. Scope of Application... 2 Reporting Entity... 2 Risk Management Framework... 2 2-3. Capital Structure and Adequacy... 3 Regulatory

Basel III Pillar 3 Disclosures As at June 30, 2014 Table of Contents 1. Scope of Application... 2 Reporting Entity... 2 Risk Management Framework... 2 2-3. Capital Structure and Adequacy... 3 Regulatory

Risk Management. Risk Management Overview. Credit Risk

Risk Management Risk Management Overview Risk management is a cornerstone of prudent banking practice. A strong enterprise-wide risk management culture provides the foundation for the Bank s risk management

Risk Management Risk Management Overview Risk management is a cornerstone of prudent banking practice. A strong enterprise-wide risk management culture provides the foundation for the Bank s risk management

EBA final draft Regulatory Technical Standards

EBA/RTS/2014/11 18 July 2014 EBA final draft Regulatory Technical Standards on the content of recovery plans under Article 5(10) of Directive 2014/59/EU establishing a framework for the recovery and resolution

EBA/RTS/2014/11 18 July 2014 EBA final draft Regulatory Technical Standards on the content of recovery plans under Article 5(10) of Directive 2014/59/EU establishing a framework for the recovery and resolution

The Northern Trust Company, Canada Basel III Pillar lll Disclosure as at December 31, 2015

The Northern Trust Company, Canada Basel III Pillar lll Disclosure as at December 31, 2015 Subject to Board Approval Posting date: January 29, 2016 Contents NORTHERN TRUST OVERVIEW AND SCOPE OF APPPLICATION.

The Northern Trust Company, Canada Basel III Pillar lll Disclosure as at December 31, 2015 Subject to Board Approval Posting date: January 29, 2016 Contents NORTHERN TRUST OVERVIEW AND SCOPE OF APPPLICATION.

Consultation Paper. Draft Guidelines on credit institutions credit risk management practices and accounting for expected credit losses EBA/CP/2016/10

EBA/CP/2016/10 26 July 2016 Consultation Paper Draft Guidelines on credit institutions credit risk management practices and accounting for expected credit losses Contents 1. Responding to this consultation

EBA/CP/2016/10 26 July 2016 Consultation Paper Draft Guidelines on credit institutions credit risk management practices and accounting for expected credit losses Contents 1. Responding to this consultation

CMC Markets Pillar 3 Disclosures

CMC Markets Pillar 3 Disclosures 2011 Table of Contents 1. Overview... 3 2. Scope of application... 4 3. Risk management objectives and policies... 5 4. Capital resources... 7 4.1 Tier 1 Capital... 7 4.2

CMC Markets Pillar 3 Disclosures 2011 Table of Contents 1. Overview... 3 2. Scope of application... 4 3. Risk management objectives and policies... 5 4. Capital resources... 7 4.1 Tier 1 Capital... 7 4.2

Part II Prudential regulatory requirements

List of references to the Basel frameworks The questionnaire is aimed at assessing equivalence with respect to the provisions Capital Requirements Regulations () and the Capital Requirements Directive

List of references to the Basel frameworks The questionnaire is aimed at assessing equivalence with respect to the provisions Capital Requirements Regulations () and the Capital Requirements Directive

Email: Stefan.ingves@bis.org 11 April 2014

Pinners Hall 105-108 Old Broad Street London EC2N 1EX tel: + 44 (0)20 7216 8947 fax: + 44 (2)20 7216 8928 web: www.ibfed.org Mr Stefan Ingves Chairman Basel Committee on Banking Supervision Centralbahnplatz

Pinners Hall 105-108 Old Broad Street London EC2N 1EX tel: + 44 (0)20 7216 8947 fax: + 44 (2)20 7216 8928 web: www.ibfed.org Mr Stefan Ingves Chairman Basel Committee on Banking Supervision Centralbahnplatz

Solvency II for Beginners 16.05.2013

Solvency II for Beginners 16.05.2013 Agenda Why has Solvency II been created? Structure of Solvency II The Solvency II Balance Sheet Pillar II & III Aspects Where are we now? Solvency II & Actuaries Why

Solvency II for Beginners 16.05.2013 Agenda Why has Solvency II been created? Structure of Solvency II The Solvency II Balance Sheet Pillar II & III Aspects Where are we now? Solvency II & Actuaries Why

EACB Comments On the BCBS Consultative Document on Net Stable Funding Ratio

EACB Comments On the BCBS Consultative Document on Net Stable Funding Ratio Brussels, 10 th April 2014 Contact: For further information or questions on this paper, please contact: a. Mr. Volker Heegemann,

EACB Comments On the BCBS Consultative Document on Net Stable Funding Ratio Brussels, 10 th April 2014 Contact: For further information or questions on this paper, please contact: a. Mr. Volker Heegemann,

High level principles for risk management

16 February 2010 High level principles for risk management Background and introduction 1. In their declaration of 15 November 2008, the G-20 leaders stated that regulators should develop enhanced guidance

16 February 2010 High level principles for risk management Background and introduction 1. In their declaration of 15 November 2008, the G-20 leaders stated that regulators should develop enhanced guidance

Proposed regulatory framework for haircuts on securities financing transactions

Proposed regulatory framework for haircuts on securities financing transactions Instructions for the Quantitative Impact Study (QIS2) for Regulated Financial Intermediaries (Banks and Broker-Dealers) 5

Proposed regulatory framework for haircuts on securities financing transactions Instructions for the Quantitative Impact Study (QIS2) for Regulated Financial Intermediaries (Banks and Broker-Dealers) 5

Capital Requirements Directive Pillar 3 Disclosure. Western Asset Management Company Limited December 2008

Capital Requirements Directive Pillar 3 Disclosure Western Asset Management Company Limited December 2008 Background Under the 2006 Capital Requirements Directive ( CRD ), a revised regulatory framework

Capital Requirements Directive Pillar 3 Disclosure Western Asset Management Company Limited December 2008 Background Under the 2006 Capital Requirements Directive ( CRD ), a revised regulatory framework

Asset Liability Management

e-learning and reference solutions for the global finance professional Asset Liability Management A comprehensive e-learning product covering Global Best Practices, Strategic, Operational and Analytical

e-learning and reference solutions for the global finance professional Asset Liability Management A comprehensive e-learning product covering Global Best Practices, Strategic, Operational and Analytical

EIOPA-CP-11/008 7 November 2011. Consultation Paper On the Proposal for Guidelines on Own Risk and Solvency Assessment

EIOPA-CP-11/008 7 November 2011 Consultation Paper On the Proposal for Guidelines on Own Risk and Solvency Assessment EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel. + 49 69-951119-20;

EIOPA-CP-11/008 7 November 2011 Consultation Paper On the Proposal for Guidelines on Own Risk and Solvency Assessment EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel. + 49 69-951119-20;

Final Report on Public Consultation No. 14/017 on Guidelines on own risk and solvency assessment

EIOPA-BoS-14/259 28 January 2015 Final Report on Public Consultation No. 14/017 on Guidelines on own risk and solvency assessment EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel.

EIOPA-BoS-14/259 28 January 2015 Final Report on Public Consultation No. 14/017 on Guidelines on own risk and solvency assessment EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel.

The Liquidity Coverage Ratio and Potential Implications for (Small) Business Financing in an Austrian Context Executive Summary (July 2012)

Business Financing in an Austrian Context Executive Summary (July 2012)") The Liquidity Coverage Ratio and Potential Implications for (Small) Business Financing in an Austrian Context Executive Summary (July 2012) A study by IHS (Bernhard Felderer, Ines Fortin) and LBMS (Luise

The Liquidity Coverage Ratio and Potential Implications for (Small) Business Financing in an Austrian Context Executive Summary (July 2012) A study by IHS (Bernhard Felderer, Ines Fortin) and LBMS (Luise

Guidance on the management of interest rate risk arising from nontrading

Guidance on the management of interest rate risk arising from nontrading activities Introduction 1. These Guidelines refer to the application of the Supervisory Review Process under Pillar 2 to a structured

Guidance on the management of interest rate risk arising from nontrading activities Introduction 1. These Guidelines refer to the application of the Supervisory Review Process under Pillar 2 to a structured

Basel Committee on Banking Supervision. Consultative Document. International framework for liquidity risk measurement, standards and monitoring

Basel Committee on Banking Supervision Consultative Document International framework for liquidity risk measurement, standards and monitoring Issued for comment by 16 April 2010 December 2009 Requests

Basel Committee on Banking Supervision Consultative Document International framework for liquidity risk measurement, standards and monitoring Issued for comment by 16 April 2010 December 2009 Requests