Credit Event Binary Options October 2007

|

|

|

- Elmer McDaniel

- 9 years ago

- Views:

Transcription

1 1

2 Agenda Credit Event Binary Options October 2007 The over-the-counter (OTC) credit derivatives environment Credit Default Swaps (CDS) Definition Cash Flows CDS Example CBOE s offerings within the credit derivatives space Advantages of trading credit derivatives on an exchange Defining Credit Event Binary Options (CEBOs) Single-Name CEBOs Basket CEBOs Contract Specifications CEBO Price History Trading Applications Theoretical Pricing Margin Requirements Quoting / Trading CEBOs on TWS 2

3 Credit Derivatives Dominated by the OTC market Credit Default Swaps (CDS) Notional value projected to reach $33 trillion by the end of 2008 CDS Notional Amounts in Trillions Sources: BIS and BBA $30 $25 $20 Single Nam e CDS 53% Multi Name CDS 47% BBA forecast for 2008 global credit market is $33 trillion 26 $15 $10 $5 $- 06/01/01 06/01/02 06/01/03 06/01/04 06/01/05 06/01/06 3

4 What is an OTC Credit Default Swap? A bilateral agreement between two counterparties to isolate the credit risk of a reference entity CDS are like insurance contracts on corporate debt Protection Buyer and Protection Seller Protection Buyer agrees to make periodic payments (quarterly) to the Protection Seller Payments expressed in basis points based on credit spreads Protection Seller collects premium and agrees to deliver par value of bonds upon confirmation of a credit event (e.g. bankruptcy, failure-topay, restructuring) 5 years is the standard length of a typical CDS CDS contracts written on single names and baskets Hedge funds, banks, and insurance companies are the major players ISDA master agreement required to trade CDS 4

5 CDS Cash Flows 5

6 CDS Example Credit Event Binary Options October 2007 Investor has a bullish view on the credit quality of XYZ Corp. Sell 5-year protection through CDS Why sell CDS if bullish on XYZ s credit quality? CDS will increase in value if the credit quality of XYZ decreases CDS will decrease in value if the credit quality of XYZ increases Dealer quotes 5-year protection on XYZ as 37 / 39 basis points Protection seller would receive 37 basis points per annum on the notional value of the contract for the life of the contract Protection buyer would pay 39 basis points per annum on the notional value of the contract for the life of the contract 6

7 CDS Example (continued) Investor wants to sell $1 million worth of protection Sells at 37 basis points = Receives $3,700 per year; 4 quarterly credits of $925 If there is no credit event before expiration, the Protection Seller simply keeps the premiums received Maximum gain to seller is $18,500 ($3,700 x 5 years) If there is a credit event prior to expiration: The value of XYZ s debt will fall significantly Recovery rate ~40% Protection Buyer delivers appropriate bonds (at their market value after the credit event) to the Protection Seller in exchange for the par value of the bonds Protection Buyer Receives Notional value of CDS * (1- Recovery Rate) $1 million * (1-0.40) = $600,000 7

to the Protection Seller in exchange for the par value of the bonds Protection Buyer Receives Notional value of CDS * (1- Recovery Rate) $1 million * (1-0.")

8 Exchange Traded Advantages Streamlined market place with easy access through securities accounts All investors, not just institutions, can now trade credit derivatives Transparent pricing and anonymous trading Reduced counterparty risk Cleared through AAA-rated Options Clearing Corporation Operational efficiency Standardization of contract terms Minimal documentation Immediate and unambiguous resolution of credit events Accessibility to other highly related CBOE products VIX Options / futures Equities (CBSX) Equity & Index options Consistent liquidity provided by Designated Primary Market Makers 8

Equity & Index options Consistent liquidity provided by Designated Primary")

9 What are CEBOs? Credit Event Binary Options (CEBOs) are the CBOE s translation of credit default swaps (CDS) to a regulated and centralized marketplace CEBOs pay a fixed amount if a credit event is confirmed in a reference entity. CEBOs expire worthless if no credit event is confirmed before expiration Credit Event : Bankruptcy Failure to pay Debt restructuring 9

10 CBOE s Credit Options Complex Single Name CEBOs Ford Motor Co. General Motors Corp. Hovnanian Enterprises Standard Pacific Corp Basket CEBOs Auto Sector Homebuilder Sector High-Yield Composite Each CEBO currently has two expirations September 2008 September 2012 More CEBOs with more expirations will be listed New products in the pipeline Credit spread options 10

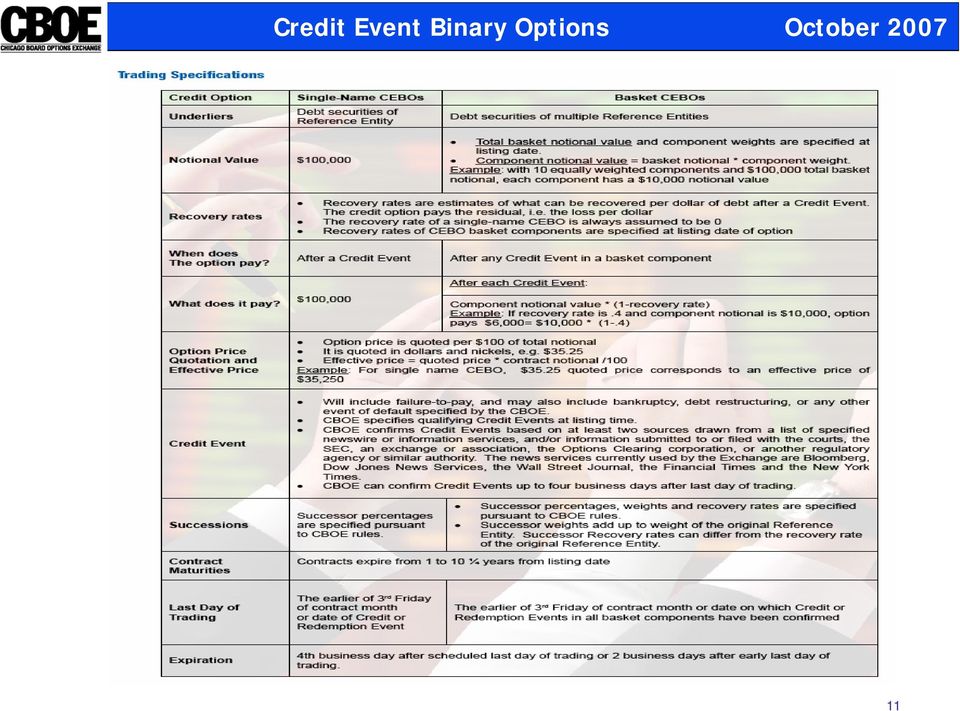

11 11

12 Ford Stock vs. Ford Sept CEBO FORD $20 $15 Ford Stock Ford Sep. '08 CEBO $16 $14 $12 $10 $10 $8 $6 $5 $- 10/8/ /2/2004 1/28/2005 3/21/2005 5/11/2005 6/30/2005 8/19/ /10/ /29/2005 1/23/2006 3/14/2006 5/3/2006 6/22/2006 8/11/ /3/ /22/2006 1/17/2007 3/8/2007 4/27/2007 6/18/2007 8/7/2007 Share Price CEBO Price $4 $2 $- 12

13 Homebuilder Sept. 08 CEBO price history CBOE Home Builders 1- Year CEBO Basket (BBR) Estimated Price $7.0 $6.0 $5.0 $4.0 $3.0 $2.0 $1.0 $0.0 10/16/ /1/ /16/ /4/2006 4/3/2007 4/17/2007 5/1/2007 5/15/2007 5/29/2007 6/12/2007 6/26/2007 7/10/2007 7/24/2007 8/7/2007 8/22/2007 9/6/

14 When a default occurs: 14

15 Basket CEBOs Credit Event Binary Options October 2007 Basket CEBOs pay-out a fixed cash amount each time there is a credit event in a basket component Basket components are weighted equally All multiple pay-out baskets 40% recovery rate assumed for each component When a credit event occurs in a component, the option pays out the fixed amount Basket continues to trade without that component until expiration or all components experience a credit event 3 baskets initially, with Sep. 08 & Sep. 12 expirations: Auto Sector Homebuilder Sector High-Yield Composite 15

16 Auto sector basket 16

17 Homebuilder sector basket 17

18 High Yield Composite 18

19 Trading Applications Single Name CEBOs Hedge corporate debt Hedge equities Speculate on the credit quality of corporate debt Basket CEBOs Hedge credit exposures to economic sectors, credit quality sectors or a cross-section of the market Adjust the sector or quality profile of a broadbased CDS index Hedge volatility exposures 19

20 Credit / Volatility Correlation 20

21 Single Name CEBO Quotes Equity Sep 2008 CEBO Sep 2012 CEBO Company Name Ticker Ticker 9/17/07 Midday Quotes Ticker 9/17/07 Mid-day Quotes General Motors Corp GM GCB 6.75B / 9.75A GCY 36.00B / 41.00A Ford Motor Company F FDE 7.50B / 10.50A FDW 37.00B / 42.00A Hovnanian Enterprises Inc HOV CKA 14.25B / 17.25A CKJ 57.00B / 62.00A Standard Pacific Corp SPF JSV 19.00B / 22.00A JSW 61.00B / 66.00A 21

22 Basket CEBO Quotes Equity Sep 2008 CEBO Sep 2012 CEBO Basket Name Ticker Ticker 9/17/07 Midday Quotes Ticker 9/17/07 Mid-day Quotes Auto Sector Homebuilder Sector High Yield Composite (ARM, AXL, F, GM, GT, TRW, VC) AFY 2.50B / 4.50A GCY 18.00B / 22.00A (KBH, HOV, SPF, CTX, LEN, PHM, TOL) BBR 5.00B / 7.00A FDW 21.00B / 25.00A 50 component s (e.g. F, GM, EP, CHK, NT, EK) HAU 1.50B / 6.50A HEU 16.00B / 19.00A 22

23 CEBO Theoretical Pricing -summation of discounted probabilities of a credit event occurring over the contract s life -estimated default probabilities can be found from Bloomberg, Moody s KMV, Reuters, RiskMetrics 23

24 Single-Name CEBO Margin Requirements Qualified Investor (>$5 million) Purchases = 20% * purchase amount E.g. - purchase amount = $10,000; margin required = $2,000 Sales the lesser of: Option proceeds + 20% of the cash settlement value The cash settlement value E.g. proceeds = $10,000; margin required = $30,000 ($10, % of $100,000) Non-qualified Investor Purchases option must be paid for in full Sales writers must maintain 100% of the cash settlement amount ($100,000 per contact) 24

25 Basket CEBO Margin Requirements Qualified Investor (>$5 million) Purchases = 15% * purchase amount E.g. - purchase amount = $10,000; margin required = $1,500 Sales the lesser of: Option proceeds + 15% of the cash settlement value The cash settlement value E.g. proceeds = $10,000; margin required = $22,000 ($10, % of $60,000) Non-qualified Investor Purchases option must be paid for in full Sales writers must maintain 100% of the cash settlement amount ($60,000 per contract) 25

26 CEBO Symbology on TWS Single-Name CEBOs GM = GCB Ford = FDE Hovnanian = CKA SPF = JSV Basket CEBOs Auto Sector = AYF Homebuilder Sector = BBR High-Yield Composite = HAU 26

27 CEBOs on TWS Credit Event Binary Options October

28 CEBOs from CBOE Matt McFarland, Director, Credit Derivatives (312) ; 28

Credit Default Swaps (CDS)

") Introduction to Credit Default Swaps (CDS) CDS Market CDS provide investors with the ability to easily and efficiently short credit Shorting allows positions to be taken in forward credit risk ik CDS allow

Introduction to Credit Default Swaps (CDS) CDS Market CDS provide investors with the ability to easily and efficiently short credit Shorting allows positions to be taken in forward credit risk ik CDS allow

ETF Options. Presented by The Options Industry Council 1-888-OPTIONS

ETF Options Presented by The Options Industry Council 1-888-OPTIONS ETF Options Options involve risks and are not suitable for everyone. Prior to buying or selling options, an investor must receive a copy

ETF Options Presented by The Options Industry Council 1-888-OPTIONS ETF Options Options involve risks and are not suitable for everyone. Prior to buying or selling options, an investor must receive a copy

An empirical analysis of the dynamic relationship between investment grade bonds and credit default swaps

An empirical analysis of the dynamic relationship between investment grade bonds and credit default swaps Roberto Blanco, Simon Brennan and Ian W. Marsh Credit derivatives Financial instruments that can

An empirical analysis of the dynamic relationship between investment grade bonds and credit default swaps Roberto Blanco, Simon Brennan and Ian W. Marsh Credit derivatives Financial instruments that can

Product Descriptions Credit Derivatives. Credit Derivatives Product Descriptions

Credit Derivatives Product Descriptions 1 Products Credit Derivatives Indices Credit Derivatives Tranches Credit Derivatives Options Product Specifications Credit Derivatives Indices A credit default swap

Credit Derivatives Product Descriptions 1 Products Credit Derivatives Indices Credit Derivatives Tranches Credit Derivatives Options Product Specifications Credit Derivatives Indices A credit default swap

Credit Derivatives. Southeastern Actuaries Conference. Fall Meeting. November 18, 2005. Credit Derivatives. What are they? How are they priced?

1 Credit Derivatives Southeastern Actuaries Conference Fall Meeting November 18, 2005 Credit Derivatives What are they? How are they priced? Applications in risk management Potential uses 2 2 Credit Derivatives

1 Credit Derivatives Southeastern Actuaries Conference Fall Meeting November 18, 2005 Credit Derivatives What are they? How are they priced? Applications in risk management Potential uses 2 2 Credit Derivatives

CDS IndexCo. LCDX Primer

LCDX Primer This document aims to outline the key characteristics of LCDX, and give investors the information they need to trade the index with confidence. What is LCDX? LCDX is a tradeable index with

LCDX Primer This document aims to outline the key characteristics of LCDX, and give investors the information they need to trade the index with confidence. What is LCDX? LCDX is a tradeable index with

Single Name Credit Derivatives:

Single ame Credit Derivatives: Products & Valuation Stephen M Schaefer London Business School Credit Risk Elective Summer 2012 Objectives To understand What single-name credit derivatives are How single

Single ame Credit Derivatives: Products & Valuation Stephen M Schaefer London Business School Credit Risk Elective Summer 2012 Objectives To understand What single-name credit derivatives are How single

How Securities Are Traded

How Securities Are Traded Chapter 3 Primary vs. Secondary Security Sales Primary new issue issuer receives the proceeds from the sale first-time issue: IPO = issuer sells stock for the first time seasoned

How Securities Are Traded Chapter 3 Primary vs. Secondary Security Sales Primary new issue issuer receives the proceeds from the sale first-time issue: IPO = issuer sells stock for the first time seasoned

Binary options. Giampaolo Gabbi

Binary options Giampaolo Gabbi Definition In finance, a binary option is a type of option where the payoff is either some fixed amount of some asset or nothing at all. The two main types of binary options

Binary options Giampaolo Gabbi Definition In finance, a binary option is a type of option where the payoff is either some fixed amount of some asset or nothing at all. The two main types of binary options

FREQUENTLY ASKED QUESTIONS BY INSURANCE PROFESSIONALS WHO ARE CONSIDERING FLEX OPTIONS

FREQUENTLY ASKED QUESTIONS BY INSURANCE PROFESSIONALS WHO ARE CONSIDERING FLEX OPTIONS WHAT ARE FLEX OPTIONS? FLEX options are customizable options where users define their own terms. They differ from

FREQUENTLY ASKED QUESTIONS BY INSURANCE PROFESSIONALS WHO ARE CONSIDERING FLEX OPTIONS WHAT ARE FLEX OPTIONS? FLEX options are customizable options where users define their own terms. They differ from

January 2011 Supplement to Characteristics and Risks of Standardized Options The February 1994 version of the booklet entitled Characteristics and Risks of Standardized Options (the Booklet ) is amended

January 2011 Supplement to Characteristics and Risks of Standardized Options The February 1994 version of the booklet entitled Characteristics and Risks of Standardized Options (the Booklet ) is amended

Introduction. Part IV: Option Fundamentals. Derivatives & Risk Management. The Nature of Derivatives. Definitions. Options. Main themes Options

Derivatives & Risk Management Main themes Options option pricing (microstructure & investments) hedging & real options (corporate) This & next weeks lectures Introduction Part IV: Option Fundamentals»

Derivatives & Risk Management Main themes Options option pricing (microstructure & investments) hedging & real options (corporate) This & next weeks lectures Introduction Part IV: Option Fundamentals»

www.optionseducation.org OIC Options on ETFs

www.optionseducation.org Options on ETFs 1 The Options Industry Council For the sake of simplicity, the examples that follow do not take into consideration commissions and other transaction fees, tax considerations,

www.optionseducation.org Options on ETFs 1 The Options Industry Council For the sake of simplicity, the examples that follow do not take into consideration commissions and other transaction fees, tax considerations,

Fixed Income ETFs: Navigating Today s Trading Environment

Fixed Income ETFs: Navigating Today s Trading Environment Karen Schenone, CFA Vice President, ishares Fixed Income Strategy Khoabane Phoofolo Vice President, ishares Capital Markets Today s Speakers Karen

Fixed Income ETFs: Navigating Today s Trading Environment Karen Schenone, CFA Vice President, ishares Fixed Income Strategy Khoabane Phoofolo Vice President, ishares Capital Markets Today s Speakers Karen

Trading in Treasury Bond Futures Contracts and Bonds in Australia

Trading in Treasury Bond Futures Contracts and Bonds in Australia Belinda Cheung* Treasury bond futures are a key financial product in Australia, with turnover in Treasury bond futures contracts significantly

Trading in Treasury Bond Futures Contracts and Bonds in Australia Belinda Cheung* Treasury bond futures are a key financial product in Australia, with turnover in Treasury bond futures contracts significantly

Credit Default Swaps (CDSs) and Systemic Risks

and Systemic Risks") Journal of Modern Accounting and Auditing, ISSN 1548-6583 June 2012, Vol. 8, No. 6, 880-890 D DAVID PUBLISHING Credit Default Swaps (CDSs) and Systemic Risks Eliana Angelini G. D Annunzio University of

Journal of Modern Accounting and Auditing, ISSN 1548-6583 June 2012, Vol. 8, No. 6, 880-890 D DAVID PUBLISHING Credit Default Swaps (CDSs) and Systemic Risks Eliana Angelini G. D Annunzio University of

The SPX Size Advantage

SPX (SM) vs. SPY Advantage Series- Part II The SPX Size Advantage September 18, 2013 Presented by Marty Kearney @MartyKearney Disclosures Options involve risks and are not suitable for all investors. Prior

SPX (SM) vs. SPY Advantage Series- Part II The SPX Size Advantage September 18, 2013 Presented by Marty Kearney @MartyKearney Disclosures Options involve risks and are not suitable for all investors. Prior

Credit Event Auction Primer

Credit Event Auction Primer This primer is provided for informational purposes only. Each auction is governed by the Auction Settlement Terms posted on www.isda.org/credit. For any questions about this

Credit Event Auction Primer This primer is provided for informational purposes only. Each auction is governed by the Auction Settlement Terms posted on www.isda.org/credit. For any questions about this

LOCKING IN TREASURY RATES WITH TREASURY LOCKS

LOCKING IN TREASURY RATES WITH TREASURY LOCKS Interest-rate sensitive financial decisions often involve a waiting period before they can be implemen-ted. This delay exposes institutions to the risk that

LOCKING IN TREASURY RATES WITH TREASURY LOCKS Interest-rate sensitive financial decisions often involve a waiting period before they can be implemen-ted. This delay exposes institutions to the risk that

How Securities Are Traded. Chapter 3

How Securities Are Traded Chapter 3 Primary vs. Secondary Security Sales Primary new issue issuer receives the proceeds from the sale first-time issue: IPO = issuer sells stock for the first time seasoned

How Securities Are Traded Chapter 3 Primary vs. Secondary Security Sales Primary new issue issuer receives the proceeds from the sale first-time issue: IPO = issuer sells stock for the first time seasoned

Insuring, Hedging and Trading Credit Risks in Financial Macroeconomics

Insuring, Hedging and Trading Credit Risks in Financial Macroeconomics Roxana Angela Calistru 1 + and Alexandru Trifu 1 1 Petre Andrei University of Iasi, Romania Abstract. The purpose of this paper is

Insuring, Hedging and Trading Credit Risks in Financial Macroeconomics Roxana Angela Calistru 1 + and Alexandru Trifu 1 1 Petre Andrei University of Iasi, Romania Abstract. The purpose of this paper is

Butterflies, Condors, and Jelly Rolls: Derivatives Explained

Butterflies, Condors, and Jelly Rolls: Derivatives Explained American Translators Association 47 th Annual Conference, New Orleans November 1, 2006 Ralf Lemster 1 Derivatives Explained What are derivatives?

Butterflies, Condors, and Jelly Rolls: Derivatives Explained American Translators Association 47 th Annual Conference, New Orleans November 1, 2006 Ralf Lemster 1 Derivatives Explained What are derivatives?

Variance swaps and CBOE S&P 500 variance futures

Variance swaps and CBOE S&P 500 variance futures by Lewis Biscamp and Tim Weithers, Chicago Trading Company, LLC Over the past several years, equity-index volatility products have emerged as an asset class

Variance swaps and CBOE S&P 500 variance futures by Lewis Biscamp and Tim Weithers, Chicago Trading Company, LLC Over the past several years, equity-index volatility products have emerged as an asset class

EXHIBIT A. Markit North America, Inc., or Markit Group Limited, or one of its subsidiaries or any successor sponsor according to each index.

EXHIBIT A CHAPTER 12: CREDIT CONTRACTS TERMS AND CONDITIONS Rule 1201. Scope (a) The rules in this chapter govern the trading of credit Contracts and Options on credit Contracts. The Clearing Organization(s)

EXHIBIT A CHAPTER 12: CREDIT CONTRACTS TERMS AND CONDITIONS Rule 1201. Scope (a) The rules in this chapter govern the trading of credit Contracts and Options on credit Contracts. The Clearing Organization(s)

Answers to Concepts in Review

Answers to Concepts in Review 1. Puts and calls are negotiable options issued in bearer form that allow the holder to sell (put) or buy (call) a stipulated amount of a specific security/financial asset,

Answers to Concepts in Review 1. Puts and calls are negotiable options issued in bearer form that allow the holder to sell (put) or buy (call) a stipulated amount of a specific security/financial asset,

Accounting for Derivatives. Rajan Chari Senior Manager [email protected]

Accounting for Derivatives Rajan Chari Senior Manager [email protected] October 3, 2005 Derivative Instruments to be Discussed Futures Forwards Options Swaps Copyright 2004 Deloitte Development LLC.

Accounting for Derivatives Rajan Chari Senior Manager [email protected] October 3, 2005 Derivative Instruments to be Discussed Futures Forwards Options Swaps Copyright 2004 Deloitte Development LLC.

Options Markets: Introduction

Options Markets: Introduction Chapter 20 Option Contracts call option = contract that gives the holder the right to purchase an asset at a specified price, on or before a certain date put option = contract

Options Markets: Introduction Chapter 20 Option Contracts call option = contract that gives the holder the right to purchase an asset at a specified price, on or before a certain date put option = contract

Introduction To Fixed Income Derivatives

Introduction To Fixed Income Derivatives Derivative instruments offer numerous benefits to investment managers and the clients they serve. The goal of this paper is to give a high level overview of derivatives

Introduction To Fixed Income Derivatives Derivative instruments offer numerous benefits to investment managers and the clients they serve. The goal of this paper is to give a high level overview of derivatives

Using Derivatives in the Fixed Income Markets

Using Derivatives in the Fixed Income Markets A White Paper by Manning & Napier www.manning-napier.com Unless otherwise noted, all figures are based in USD. 1 Introduction While derivatives may have a

Using Derivatives in the Fixed Income Markets A White Paper by Manning & Napier www.manning-napier.com Unless otherwise noted, all figures are based in USD. 1 Introduction While derivatives may have a

An Overview of the Use of Credit Spreads in Fair Valuation. Consultants in Treasury

Consultants in Treasury Written by: David W. Stowe, CFA Director Strategic Treasurer, Lead Financial Risk Management Reprinted from Treasury Update V o l u m e 4, I s s u e 1 SPRING / SUMMER 2010 1 Introduction

Consultants in Treasury Written by: David W. Stowe, CFA Director Strategic Treasurer, Lead Financial Risk Management Reprinted from Treasury Update V o l u m e 4, I s s u e 1 SPRING / SUMMER 2010 1 Introduction

A Short Introduction to Credit Default Swaps

A Short Introduction to Credit Default Swaps by Dr. Michail Anthropelos Spring 2010 1. Introduction The credit default swap (CDS) is the most common and widely used member of a large family of securities

A Short Introduction to Credit Default Swaps by Dr. Michail Anthropelos Spring 2010 1. Introduction The credit default swap (CDS) is the most common and widely used member of a large family of securities

Index Options. James Bittman. Unique Features & Strategies. Senior Instructor The Options Institute at CBOE

Index Options Unique Features & Strategies James Bittman Senior Instructor The Options Institute at CBOE Disclosures In order to simplify the computations, commissions have not been included in the examples

Index Options Unique Features & Strategies James Bittman Senior Instructor The Options Institute at CBOE Disclosures In order to simplify the computations, commissions have not been included in the examples

Complex Products. Non-Complex Products. General risks of trading

We offer a wide range of investments, each with their own risks and rewards. The following information provides you with a general description of the nature and risks of the investments that you can trade

We offer a wide range of investments, each with their own risks and rewards. The following information provides you with a general description of the nature and risks of the investments that you can trade

LEAPS LONG-TERM EQUITY ANTICIPATION SECURITIES

LEAPS LONG-TERM EQUITY ANTICIPATION SECURITIES The Options Industry Council (OIC) is a non-profit association created to educate the investing public and brokers about the benefits and risks of exchange-traded

LEAPS LONG-TERM EQUITY ANTICIPATION SECURITIES The Options Industry Council (OIC) is a non-profit association created to educate the investing public and brokers about the benefits and risks of exchange-traded

TW3421x - An Introduction to Credit Risk Management Credit Default Swaps and CDS Spreads! Dr. Pasquale Cirillo. Week 7 Lesson 1

TW3421x - An Introduction to Credit Risk Management Credit Default Swaps and CDS Spreads! Dr. Pasquale Cirillo Week 7 Lesson 1 Credit Default Swaps A Credit Default Swap (CDS) is an instrument providing

TW3421x - An Introduction to Credit Risk Management Credit Default Swaps and CDS Spreads! Dr. Pasquale Cirillo Week 7 Lesson 1 Credit Default Swaps A Credit Default Swap (CDS) is an instrument providing

BEAR: A person who believes that the price of a particular security or the market as a whole will go lower.

Trading Terms ARBITRAGE: The simultaneous purchase and sale of identical or equivalent financial instruments in order to benefit from a discrepancy in their price relationship. More generally, it refers

Trading Terms ARBITRAGE: The simultaneous purchase and sale of identical or equivalent financial instruments in order to benefit from a discrepancy in their price relationship. More generally, it refers

How To Understand Credit Default Swaps

The CDS market: A primer Including computational remarks on Default Probabilities online Roland Beck, Risk Analysis Group Folie 2 The CDS market: A primer Credit Default Swaps Short Introduction CDS are

The CDS market: A primer Including computational remarks on Default Probabilities online Roland Beck, Risk Analysis Group Folie 2 The CDS market: A primer Credit Default Swaps Short Introduction CDS are

Buying Equity Call Options

Buying Equity Call Options Presented by The Options Industry Council 1-888-OPTIONS Equity Call Options Options involve risks and are not suitable for everyone. Prior to buying or selling options, an investor

Buying Equity Call Options Presented by The Options Industry Council 1-888-OPTIONS Equity Call Options Options involve risks and are not suitable for everyone. Prior to buying or selling options, an investor

Introduction, Forwards and Futures

Introduction, Forwards and Futures Liuren Wu Zicklin School of Business, Baruch College Fall, 2007 (Hull chapters: 1,2,3,5) Liuren Wu Introduction, Forwards & Futures Option Pricing, Fall, 2007 1 / 35

Introduction, Forwards and Futures Liuren Wu Zicklin School of Business, Baruch College Fall, 2007 (Hull chapters: 1,2,3,5) Liuren Wu Introduction, Forwards & Futures Option Pricing, Fall, 2007 1 / 35

Market and Exercise Price Relationships. Option Terminology. Options Trading. CHAPTER 15 Options Markets 15.1 THE OPTION CONTRACT

CHAPTER 15 Options Markets 15.1 THE OPTION CONTRACT Option Terminology Buy - Long Sell - Short Call the right to buy Put the the right to sell Key Elements Exercise or Strike Price Premium or Price of

CHAPTER 15 Options Markets 15.1 THE OPTION CONTRACT Option Terminology Buy - Long Sell - Short Call the right to buy Put the the right to sell Key Elements Exercise or Strike Price Premium or Price of

Credit Default Swaps and the synthetic CDO

Credit Default Swaps and the synthetic CDO Bloomberg Seminar 20March 2003 Moorad Choudhry Journal of Bond Trading and Management www.yieldcurve.com Agenda o Credit derivatives and securitisation o Synthetic

Credit Default Swaps and the synthetic CDO Bloomberg Seminar 20March 2003 Moorad Choudhry Journal of Bond Trading and Management www.yieldcurve.com Agenda o Credit derivatives and securitisation o Synthetic

CHAPTER 20. Financial Options. Chapter Synopsis

CHAPTER 20 Financial Options Chapter Synopsis 20.1 Option Basics A financial option gives its owner the right, but not the obligation, to buy or sell a financial asset at a fixed price on or until a specified

CHAPTER 20 Financial Options Chapter Synopsis 20.1 Option Basics A financial option gives its owner the right, but not the obligation, to buy or sell a financial asset at a fixed price on or until a specified

The Single Name Corporate CDS Market. Alan White

The Single Name Corporate CDS Market Alan White CDS Structure Single Name DJ Index Products CDS Notional x [ ] bp p.a. Buyer Credit Risk of ABC Seller 125 Equally Weighted Names Buyer Delivery 10MM Principal

The Single Name Corporate CDS Market Alan White CDS Structure Single Name DJ Index Products CDS Notional x [ ] bp p.a. Buyer Credit Risk of ABC Seller 125 Equally Weighted Names Buyer Delivery 10MM Principal

Credit derivative products and their documentation: unfunded credit derivatives

Credit derivative products and their documentation: unfunded credit derivatives 1. Introduction The range of credit derivative products, their associated jargon and many acronyms dazzle: single name, basket,

Credit derivative products and their documentation: unfunded credit derivatives 1. Introduction The range of credit derivative products, their associated jargon and many acronyms dazzle: single name, basket,

Note 8: Derivative Instruments

Note 8: Derivative Instruments Derivative instruments are financial contracts that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity prices

Note 8: Derivative Instruments Derivative instruments are financial contracts that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity prices

Index, Interest Rate, and Currency Options

CHAPTER 3 Index, Interest Rate, and Currency Options INTRODUCTION In an effort to gauge the market s overall performance, industry participants developed indexes. Two of the most widely followed indexes

CHAPTER 3 Index, Interest Rate, and Currency Options INTRODUCTION In an effort to gauge the market s overall performance, industry participants developed indexes. Two of the most widely followed indexes

OPTIONS MARKETS AND VALUATIONS (CHAPTERS 16 & 17)

") OPTIONS MARKETS AND VALUATIONS (CHAPTERS 16 & 17) WHAT ARE OPTIONS? Derivative securities whose values are derived from the values of the underlying securities. Stock options quotations from WSJ. A call

OPTIONS MARKETS AND VALUATIONS (CHAPTERS 16 & 17) WHAT ARE OPTIONS? Derivative securities whose values are derived from the values of the underlying securities. Stock options quotations from WSJ. A call

CREDIT DEFAULT SWAPS AND CREDIT RISK PRICING MELİH SAZAK

CREDIT DEFAULT SWAPS AND CREDIT RISK PRICING MELİH SAZAK MSc Finance Cass Business School City University London 2012 1. Introduction Credit default swap (CDS), a type of over-the-counter derivative, is

CREDIT DEFAULT SWAPS AND CREDIT RISK PRICING MELİH SAZAK MSc Finance Cass Business School City University London 2012 1. Introduction Credit default swap (CDS), a type of over-the-counter derivative, is

Credit Derivatives Glossary

Credit Derivatives Glossary March 2009 Copyright 2009 Markit Group Limited Any reproduction, in full or in part, in any media without the prior written permission of Markit Group Limited will subject the

Credit Derivatives Glossary March 2009 Copyright 2009 Markit Group Limited Any reproduction, in full or in part, in any media without the prior written permission of Markit Group Limited will subject the

Risks of Investments explained

Risks of Investments explained Member of the London Stock Exchange .Introduction Killik & Co is committed to developing a clear and shared understanding of risk with its clients. The categories of risk

Risks of Investments explained Member of the London Stock Exchange .Introduction Killik & Co is committed to developing a clear and shared understanding of risk with its clients. The categories of risk

Currency Options. www.m-x.ca

Currency Options www.m-x.ca Table of Contents Introduction...3 How currencies are quoted in the spot market...4 How currency options work...6 Underlying currency...6 Trading unit...6 Option premiums...6

Currency Options www.m-x.ca Table of Contents Introduction...3 How currencies are quoted in the spot market...4 How currency options work...6 Underlying currency...6 Trading unit...6 Option premiums...6

Introduction to Fixed Income & Credit. Asset Management

Introduction to Fixed Income & Credit Asset Management Fixed Income explanation The Basis of Fixed Income is the need to purchase today with not enough cash available: ie. Mortgage or consumer loan You

Introduction to Fixed Income & Credit Asset Management Fixed Income explanation The Basis of Fixed Income is the need to purchase today with not enough cash available: ie. Mortgage or consumer loan You

COAL MARKET FREQUENTLY ASKED QUESTIONS

COAL MARKET FREQUENTLY ASKED QUESTIONS Over the course of the past decade, numerous issues have arisen in the U.S. coal trading arena. Bankruptcies, standardized trading contracts, and liquidity are a

COAL MARKET FREQUENTLY ASKED QUESTIONS Over the course of the past decade, numerous issues have arisen in the U.S. coal trading arena. Bankruptcies, standardized trading contracts, and liquidity are a

Note 10: Derivative Instruments

Note 10: Derivative Instruments Derivative instruments are financial contracts that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity

Note 10: Derivative Instruments Derivative instruments are financial contracts that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity

Options on. Dow Jones Industrial Average SM. the. DJX and DIA. Act on the Market You Know Best.

Options on the Dow Jones Industrial Average SM DJX and DIA Act on the Market You Know Best. A glossary of options definitions appears on page 21. The Chicago Board Options Exchange (CBOE) was founded in

Options on the Dow Jones Industrial Average SM DJX and DIA Act on the Market You Know Best. A glossary of options definitions appears on page 21. The Chicago Board Options Exchange (CBOE) was founded in

Reference Manual Currency Options

Reference Manual Currency Options TMX Group Equities Toronto Stock Exchange TSX Venture Exchange TMX Select Equicom Derivatives Montréal Exchange CDCC Montréal Climate Exchange Fixed Income Shorcan Energy

Reference Manual Currency Options TMX Group Equities Toronto Stock Exchange TSX Venture Exchange TMX Select Equicom Derivatives Montréal Exchange CDCC Montréal Climate Exchange Fixed Income Shorcan Energy

Interest Rate Hedging. November 2007

November 2007 ASSET = LEASE Deal Example LIABILITY = DEBT Airbus A320 cost $40m 85% floating rate debt : $34m Aircraft placed on lease for 7 years at fixed rental of $350k per month, priced at 5% Libor

November 2007 ASSET = LEASE Deal Example LIABILITY = DEBT Airbus A320 cost $40m 85% floating rate debt : $34m Aircraft placed on lease for 7 years at fixed rental of $350k per month, priced at 5% Libor

January 2001 UNDERSTANDING INDEX OPTIONS

January 2001 UNDERSTANDING INDEX OPTIONS Table of Contents Introduction 3 Benefits of Listed Index Options 5 What is an Index Option? 7 Equity vs. Index Options 9 Pricing Factors Underlying Instrument

January 2001 UNDERSTANDING INDEX OPTIONS Table of Contents Introduction 3 Benefits of Listed Index Options 5 What is an Index Option? 7 Equity vs. Index Options 9 Pricing Factors Underlying Instrument

Chicago Board Options Exchange. Margin Manual

Chicago Board Options Exchange Margin Manual April 2000 TABLE OF CONTENTS INTRODUCTION... 3 INITIAL AND MAINTENANCE MARGIN REQUIREMENTS Long Put or Long Call (9 months or less until expiration)... 4 Long

Chicago Board Options Exchange Margin Manual April 2000 TABLE OF CONTENTS INTRODUCTION... 3 INITIAL AND MAINTENANCE MARGIN REQUIREMENTS Long Put or Long Call (9 months or less until expiration)... 4 Long

A primer on Credit Default Swap (CDS)& RBI guidelines on CDS

& RBI guidelines on CDS") A primer on Credit Default Swap (CDS)& RBI guidelines on CDS Prof. Utkarsh Jain Assistant Professor,, Pune E-mail : [email protected] Prof. Kaustubh Medhekar Associate Professor,, Pune E-mail : [email protected]

A primer on Credit Default Swap (CDS)& RBI guidelines on CDS Prof. Utkarsh Jain Assistant Professor,, Pune E-mail : [email protected] Prof. Kaustubh Medhekar Associate Professor,, Pune E-mail : [email protected]

ODYSSEY RE HOLDINGS CORP. 10 Q Quarterly report pursuant to sections 13 or 15(d) Filed on 5/6/2010 Filed Period 3/31/2010

Filed on 5/6/2010 Filed Period 3/31/2010") ODYSSEY RE HOLDINGS CORP 10 Q Quarterly report pursuant to sections 13 or 15(d) Filed on 5/6/2010 Filed Period 3/31/2010 (Mark One) UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549

ODYSSEY RE HOLDINGS CORP 10 Q Quarterly report pursuant to sections 13 or 15(d) Filed on 5/6/2010 Filed Period 3/31/2010 (Mark One) UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549

36 South Breakfast. Profile of the U.S. Listed Equity Options Market. Zurich October 23, 2013

36 South Breakfast Profile of the U.S. Listed Equity Options Market Zurich October 23, 2013 The Options Industry Council (OIC) Gary Delany www.optionseducation.org Disclaimer Options involve risk and are

36 South Breakfast Profile of the U.S. Listed Equity Options Market Zurich October 23, 2013 The Options Industry Council (OIC) Gary Delany www.optionseducation.org Disclaimer Options involve risk and are

Learning Curve Forward Rate Agreements Anuk Teasdale

Learning Curve Forward Rate Agreements Anuk Teasdale YieldCurve.com 2004 Page 1 In this article we review the forward rate agreement. Money market derivatives are priced on the basis of the forward rate,

Learning Curve Forward Rate Agreements Anuk Teasdale YieldCurve.com 2004 Page 1 In this article we review the forward rate agreement. Money market derivatives are priced on the basis of the forward rate,

Interest Rate Options

Interest Rate Options A discussion of how investors can help control interest rate exposure and make the most of the interest rate market. The Chicago Board Options Exchange (CBOE) is the world s largest

Interest Rate Options A discussion of how investors can help control interest rate exposure and make the most of the interest rate market. The Chicago Board Options Exchange (CBOE) is the world s largest

CREDITEX BROKERAGE LLP BEST EXECUTION POLICY

CREDITEX BROKERAGE LLP BEST EXECUTION POLICY Version 1.1 The Execution Policy is applicable to broker services provided by Creditex Brokerage LLP ( CBL ). Introduction When providing brokerage services

CREDITEX BROKERAGE LLP BEST EXECUTION POLICY Version 1.1 The Execution Policy is applicable to broker services provided by Creditex Brokerage LLP ( CBL ). Introduction When providing brokerage services

Module 10 Foreign Exchange Contracts: Swaps and Options

Module 10 Foreign Exchange Contracts: Swaps and Options Developed by: Dr. Prabina Rajib Associate Professor (Finance & Accounts) Vinod Gupta School of Management IIT Kharagpur, 721 302 Email: [email protected]

Module 10 Foreign Exchange Contracts: Swaps and Options Developed by: Dr. Prabina Rajib Associate Professor (Finance & Accounts) Vinod Gupta School of Management IIT Kharagpur, 721 302 Email: [email protected]

Investments 320 Dr. Ahmed Y. Dashti Chapter 3 Interactive Qustions

Investments 320 Dr. Ahmed Y. Dashti Chapter 3 Interactive Qustions 3-1. A primary asset is an initial offering sold by a business, or government, to raise funds. A) True B) False 3-2. Money market instruments

Investments 320 Dr. Ahmed Y. Dashti Chapter 3 Interactive Qustions 3-1. A primary asset is an initial offering sold by a business, or government, to raise funds. A) True B) False 3-2. Money market instruments

UNDERSTANDING INDEX OPTIONS

UNDERSTANDING INDEX OPTIONS The Options Industry Council (OIC) is an industry cooperative created to educate the investing public and brokers about the benefits and risks of exchange-traded options. Options

UNDERSTANDING INDEX OPTIONS The Options Industry Council (OIC) is an industry cooperative created to educate the investing public and brokers about the benefits and risks of exchange-traded options. Options

Module I Financial derivatives an introduction Forward market and products

Module I 1. Financial derivatives an introduction 1.1 Derivative markets 1.1.1 Past and present 1.1.2 Difference between exchange traded and OTC derivatives 1.2 Derivative instruments 1.2.1 Concept and

Module I 1. Financial derivatives an introduction 1.1 Derivative markets 1.1.1 Past and present 1.1.2 Difference between exchange traded and OTC derivatives 1.2 Derivative instruments 1.2.1 Concept and

Using Currency Futures to Hedge Currency Risk

Using Currency Futures to Hedge Currency Risk By Sayee Srinivasan & Steven Youngren Product Research & Development Chicago Mercantile Exchange Inc. Introduction Investment professionals face a tough climate.

Using Currency Futures to Hedge Currency Risk By Sayee Srinivasan & Steven Youngren Product Research & Development Chicago Mercantile Exchange Inc. Introduction Investment professionals face a tough climate.

June 2008 Supplement to Characteristics and Risks of Standardized Options

June 2008 Supplement to Characteristics and Risks of Standardized Options This supplement supersedes and replaces the April 2008 Supplement to the booklet entitled Characteristics and Risks of Standardized

June 2008 Supplement to Characteristics and Risks of Standardized Options This supplement supersedes and replaces the April 2008 Supplement to the booklet entitled Characteristics and Risks of Standardized

11 Option. Payoffs and Option Strategies. Answers to Questions and Problems

11 Option Payoffs and Option Strategies Answers to Questions and Problems 1. Consider a call option with an exercise price of $80 and a cost of $5. Graph the profits and losses at expiration for various

11 Option Payoffs and Option Strategies Answers to Questions and Problems 1. Consider a call option with an exercise price of $80 and a cost of $5. Graph the profits and losses at expiration for various

XIV. Additional risk information on forward transactions in CFDs

XIV. Additional risk information on forward transactions in CFDs The following information is given in addition to the general risks associated with forward transactions. Please read the following information

XIV. Additional risk information on forward transactions in CFDs The following information is given in addition to the general risks associated with forward transactions. Please read the following information

Options CHAPTER 7 INTRODUCTION OPTION CLASSIFICATION

CHAPTER 7 Options INTRODUCTION An option is a contract between two parties that determines the time and price at which a stock may be bought or sold. The two parties to the contract are the buyer and the

CHAPTER 7 Options INTRODUCTION An option is a contract between two parties that determines the time and price at which a stock may be bought or sold. The two parties to the contract are the buyer and the

October 2003 UNDERSTANDING STOCK OPTIONS

October 2003 UNDERSTANDING STOCK OPTIONS Table of Contents Introduction 3 Benefits of Exchange-Traded Options 5 Orderly, Efficient, and Liquid Markets Flexibility Leverage Limited Risk for Buyer Guaranteed

October 2003 UNDERSTANDING STOCK OPTIONS Table of Contents Introduction 3 Benefits of Exchange-Traded Options 5 Orderly, Efficient, and Liquid Markets Flexibility Leverage Limited Risk for Buyer Guaranteed

Risks involved with futures trading

Appendix 1: Risks involved with futures trading Before executing any futures transaction, the client should obtain information on the risks involved. Note in particular the risks summarized in the following

Appendix 1: Risks involved with futures trading Before executing any futures transaction, the client should obtain information on the risks involved. Note in particular the risks summarized in the following

Brief Overview of Futures and Options in Risk Management

Brief Overview of Futures and Options in Risk Management Basic Definitions: Derivative Security: A security whose value depends on the worth of other basic underlying variables. E.G. Futures, Options,

Brief Overview of Futures and Options in Risk Management Basic Definitions: Derivative Security: A security whose value depends on the worth of other basic underlying variables. E.G. Futures, Options,

Hedging Oil and Gas Production: Issues and Considerations

View the online version at http://us.practicallaw.com/w-001-3415 Hedging Oil and Gas Production: Issues and Considerations DANIEL NOSSA, JESSE S. LOTAY AND PAUL E. VRANA, JACKSON WALKER LLP AND PRACTICAL

View the online version at http://us.practicallaw.com/w-001-3415 Hedging Oil and Gas Production: Issues and Considerations DANIEL NOSSA, JESSE S. LOTAY AND PAUL E. VRANA, JACKSON WALKER LLP AND PRACTICAL

Financial Markets And Financial Instruments - Part I

Financial Markets And Financial Instruments - Part I Financial Assets Real assets are things such as land, buildings, machinery, and knowledge that are used to produce goods and services. Financial assets

Financial Markets And Financial Instruments - Part I Financial Assets Real assets are things such as land, buildings, machinery, and knowledge that are used to produce goods and services. Financial assets

1 Regional Bank Regional banks specialize in consumer and commercial products within one region of a country, such as a state or within a group of states. A regional bank is smaller than a bank that operates

1 Regional Bank Regional banks specialize in consumer and commercial products within one region of a country, such as a state or within a group of states. A regional bank is smaller than a bank that operates

Risk Warning Notice. Introduction

First Equity Limited Salisbury House London Wall London EC2M 5QQ Tel 020 7374 2212 Fax 020 7374 2336 www.firstequity.ltd.uk Risk Warning Notice Introduction You should not invest in any investment product

First Equity Limited Salisbury House London Wall London EC2M 5QQ Tel 020 7374 2212 Fax 020 7374 2336 www.firstequity.ltd.uk Risk Warning Notice Introduction You should not invest in any investment product

OVERVIEW OF THE USE OF CROSS CURRENCY SWAPS

OVERVIEW OF THE USE OF CROSS CURRENCY SWAPS PRACTICAL CONSIDERATIONS IVAN LARIN CAPITAL MARKETS DEPARTMENT FABDM Webinar for Debt Managers Washington, D.C. 20 th January, 2016 AGENDA 1. BASICS 2. Pre-TRADE

OVERVIEW OF THE USE OF CROSS CURRENCY SWAPS PRACTICAL CONSIDERATIONS IVAN LARIN CAPITAL MARKETS DEPARTMENT FABDM Webinar for Debt Managers Washington, D.C. 20 th January, 2016 AGENDA 1. BASICS 2. Pre-TRADE

central Options www.888options.com By Marty Kearney

www.888options.com YOUR RESOURCE FOR OPTIONS EDUCATION SM Options central IN THIS S U M M E R 2 0 0 2 ISSUE: F E A T U R E : S E L L I N G P U T S O P T I O N S C E N T R A L M O V E S O N L I N E W H

www.888options.com YOUR RESOURCE FOR OPTIONS EDUCATION SM Options central IN THIS S U M M E R 2 0 0 2 ISSUE: F E A T U R E : S E L L I N G P U T S O P T I O N S C E N T R A L M O V E S O N L I N E W H

What Is an Option? the basics. Types of Options

the basics What Is an Option? An option is a contract to buy or sell a specific financial product officially known as the option s underlying instrument or underlying interest. For equity options, the

the basics What Is an Option? An option is a contract to buy or sell a specific financial product officially known as the option s underlying instrument or underlying interest. For equity options, the