CITY OF SACRAMENTO INTERNAL AUDIT. Inventory Processes & Inventory Reports, Department of Utilities Report Number

|

|

|

- Paul Ward

- 7 years ago

- Views:

Transcription

1 CITY OF SACRAMENTO INTERNAL AUDIT Inventory Processes & Inventory Reports, Department of Utilities Report Number

2

3 Table of Contents Inventory Processes and Inventory Reports, Department of Utilities Report Number EXECUTIVE SUMMARY OF FINDINGS & RECOMMENDATIONS iii PRELIMINARY SECTION Introduction 1 Objective & Scope 1 Citywide Ramifications 1 CONCLUSIONS FINDINGS Summary of Audit Findings 1. Beginning Inventory Correction of $486,706 FY 2007 Errors 3 1A. Reversal of an Incorrect, FY 2007, $400,620 Inventory Write-off 3 1B. Correction of $82,086 of FY 2007 Inventory Pricing Errors 3 2. Correction of $69,058 of Net Errors in FY 2008 Receipts and Disbursements Inventory Reports 3 3. FY 2008 Physical Count of Ending Inventory Understated by $457, Other Concerns 4 Approximately $600 thousand of fixed assets not recorded on the fixed asset report Approximately $200 thousand of inventory improperly expensed at purchase, instead of recording in inventory as required APPENDIX 5 ii

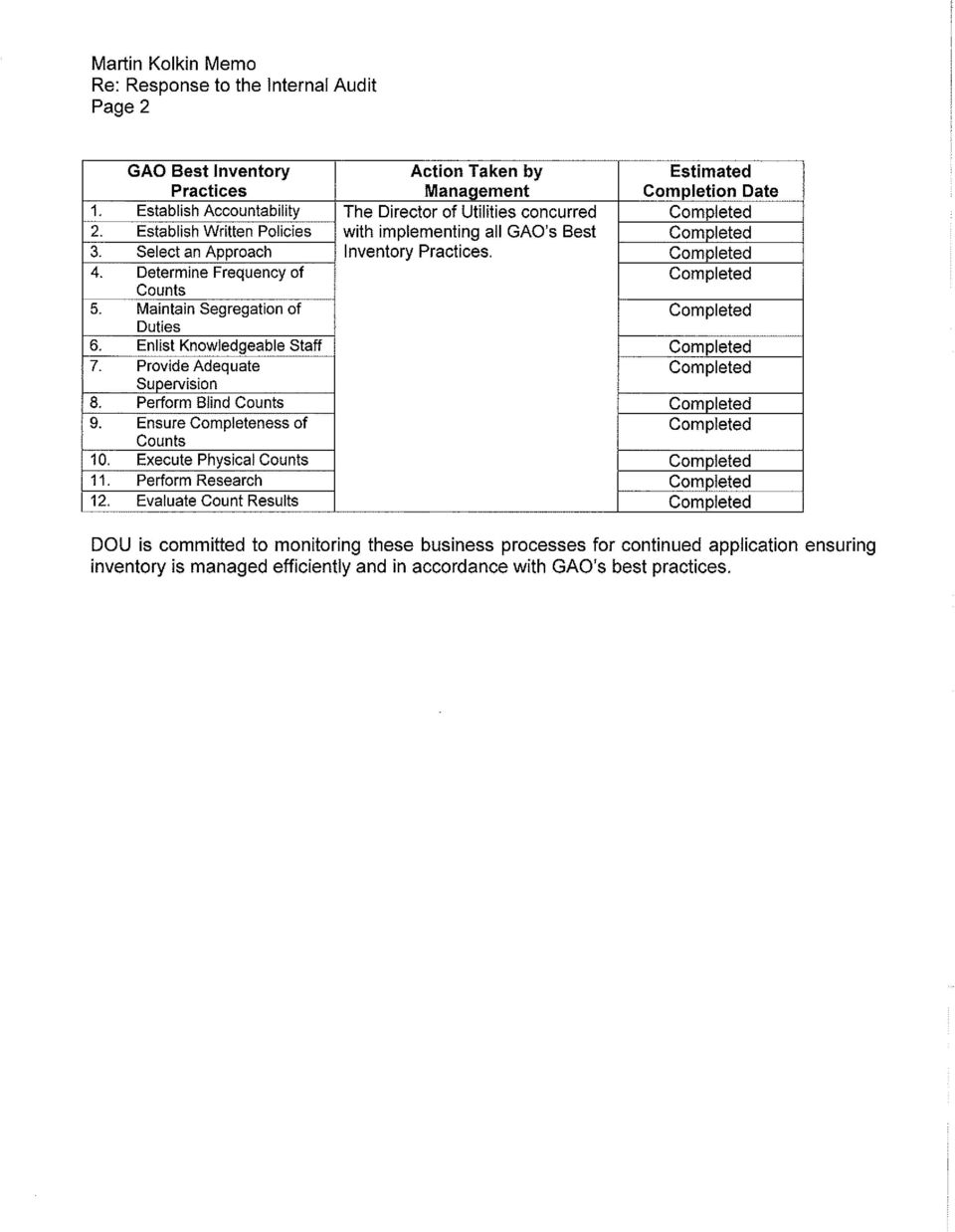

4 Executive Summary of Findings & Recommendations Inventory Processes and Inventory Reports, Department of Utilities Report Number Material deficiencies in departmental inventory controls were cited in the City of Sacramento s internal audit report Management Controls: Inventory & Debit Card Usage for the Department of Utilities, dated May 16, Further internal audit review of the Department of Utilities ( DOU ) was performed at the request of the new DOU Department Director and at the direction of the City Manager, the Mayor, and City Council. Based upon the work performed, the City Auditor concluded that systematic and material deficiencies existed in the Water, Sewer, and Storm Drainage Funds inventory processes and reports. However, Department of Utilities representatives were supportive of recommended improvements and made substantial progress in resolving cited deficiencies. The City Auditor recommended adjustments to DOU s inventory system and financial statement that resulted in approximately $871 thousand of net increases for FY The Director of Utilities concurred and appropriate corrections were made to the City s financial system. The City Auditor recommends that the Director of Utilities or his representatives implement industry best practices as cited in Best Practices in Achieving Consistent, Accurate Physical Counts of Inventory and Related Property, released by the Government Accountability Office ( GAO ) in March GAO Best Inventory Practices Action Taken by Management Estimated Completion Date 1. Establish Accountability The Director of Utilities concurred 2. Establish Written Policies with implementing all GAO s Best 3. Select an Approach Inventory Practices. 4. Determine Frequency of Counts 5. Maintain Segregation of Duties 6. Enlist Knowledgeable Staff 7. Provide Adequate Supervision 8. Perform Blind Counts 9. Ensure Completeness of Counts 10. Execute Physical Counts 11. Perform Research 12. Evaluate Count Results iii

5 Preliminary Section Inventory Processes and Inventory Reports, Department of Utilities Report Number INTRODUCTION The City Auditor completed a limited scope examination of the inventory processes and reports for the Water, Sewer, and Storm Drainage Funds. The Solid Waste Fund did not reflect an inventory and accordingly was not included in this audit. OBJECTIVE & SCOPE This report provides the Mayor, City Council, and the City Manager with an objective evaluation of the Department of Utilities inventory processes and inventory reporting tools for the Water, Sewer, and Storm Drainage Funds. The objectives of this internal audit report also include providing recommendations for best practices in achieving accurate inventory counts and inventory reports. Records Examined The audit included, but was not limited to the following: Physical observations of internal controls, operations, and practices; Analytical examinations of financial data; Examination and verification of general ledger data; Review of inventory reports and programming; Interviews and discussions with personnel from the Department of Utilities, the Finance Department, the City Attorney s Office, and the City Manager s Office; and Review of best practices for inventory. The audit report is intended for the information and use of the Mayor, City Council, City Manager, and City Management. CITYWIDE RAMIFICATIONS This report focused solely upon the inventory for DOU. Conclusions regarding other City Departments are beyond the scope of this audit. However, audit recommendations have relevance for numerous City Departments that maintain inventory. 1

6 Conclusions and Findings Inventory Processes and Inventory Reports, Department of Utilities Report Number The City Auditor determined that systematic and material deficiencies existed in the Water, Sewer, and Storm Drainage Funds inventory processes and reports. Deficiencies located included flawed and inadequately designed inventory reports, insufficient internal controls, pricing input errors, quantity input errors, inadequate separation of duties, inaccurate physical inventory counts, and the absence of internal process to report deficiencies to management. Summary of Audit Findings Finding Findings Dollar Value 1 Correction of FY 2007 Beginning Inventory $482,706 2 Errors in FY 2008 Inventory Reports < 69,058> 3 FY 2008 Physical Count Understatement 457,433 Additionally, $161,381 of tools was misclassified as DOU s inventory within the City s financial system. DEPARTMENT DIRECTOR S ACTION Department Director Marty Hanneman immediately committed resources to resolve located deficiencies. The status of the corrective actions is noted throughout this report. FINDINGS DOU s inventory processes and reports required corrections to all aspects of the inventory process; 1) Beginning Inventory; 2) Receipts and Disbursements Inventory Reports, 3) Physical Counts and 4) Other Concerns. Table of Inventory Adjustments Total Findings $871,081 Per Inventory Reports Adjustment Needed Per Audit Beginning Inventory, 7/1/07 $1,884,518* $ 482,706 $2,367,224 Net Receipts & Disbursements 916,621 <69,058> 847,563 Ending Inventory, 6/30/08 $2,801,139* $ 413,648 $3,214,787 Short and Over <56,873> 43,785 <13,088> Physical Count $2,744,266 $ 457,433 $3,201,699 * - Beginning and Ending Inventory were decreased by $161,381 for the reclassification of tools incorrectly included in inventory. 2

7 1. Beginning Inventory Correction of $482,706 FY 2007 Errors The City of Sacramento s internal audit report Management Controls: Inventory & Debit Card Usage for the Department of Utilities dated May 16, 2008, cited material errors in the FY 2007 inventory report used as the basis for a $400,620 inventory write-off. The Audit Report recommended taking steps to accurately compute the value of the ending inventory. 1A. Reversal of an Incorrect, FY 2007, $400,620 Inventory Write-off The City Auditor recommends that the $400,620 inventory write-off entry for FY 2007 be reversed in FY 2008 and the correct beginning inventory value determined. The Director of Utilities concurred and this entry was reversed in FY B. Correction of $82,086 of FY 2007 Inventory Pricing Errors The City Auditor recommends that the beginning inventory of FY 2008 be increased by $82,086 to correct for pricing errors, incomplete data, and computational errors. The Director of Utilities concurred and this entry was made in FY Correction of $69,058 of Net Errors in FY 2008 Receipts and Disbursement Inventory Reports DOU representatives acknowledged during the audit that pricing errors in their receipts and disbursement reports were so prevalent that no reliance could be placed on unit costs information within that system. Additionally, employees were permitted unrestricted access, without training, to correct pricing per unit and number of units purchased. Lastly, no internal procedures existed for reporting deficiencies to DOU management. Table of Total Receipts & Disbursements Per Inventory Reports Adjustment Needed Per Audit Total Receipts $5,515,573 $<2,411,067> $3,104,507 Total Disbursements 4,598,952 <2,342,009> 2,256,944 Net Receipts and Disbursements $ 916,621 <$69,058> $847,563 The Director of Utilities concurred. DOU representatives corrected design flaws in inventory reports, developed sufficient internal controls, provided controls for adequate separation of duties, provided ongoing training, and developed internal procedures for reporting deficiencies to DOU management. 3. FY 2008 Physical Count of Ending Inventory Understated by $457,433 As previously noted, DOU representatives acknowledged during the audit that pricing errors in their inventory system were so prevalent that no reliance could be placed on unit costs information within that system. As a result, DOU s FY 2008 inventory valuations for the City s financial statements were recalculated based upon replacement costs 1 and the physical count of the ending inventory, conducted by DOU, was understated by $457, The City Auditor noted that this inventory methodology was not in accordance with Generally Accepted Account Principles ( GAAP ). However, if fully disclosed, it is the City Auditor s opinion that this inventory valuation was one of the more practical methodologies available to DOU representatives. 3

8 According to DOU representatives, unit cost corrections within DOU s inventory system are scheduled to be completed in January The Director of Utilities concurred and this entry was posted in FY OTHER CONCERNS According to Plant Services Division representatives no fixed asset listing existed and inventory on hand was immediately expensed. Plant Services Division representatives estimated the dollar value of these items as approximately: A. $600 thousand of fixed assets not on the fixed asset report; and B. $200 thousand of inventory improperly expensed at purchase, instead of recording in inventory as required. DOU representatives noted that fixed assets had been inventoried, as recommended by the City Auditor. DOU representatives also stated that new procedures were implemented to ensure that inventory is recorded in a consistent and well documented manner. 4

9 APPENDIX Management Response 5

10

11

Table of Contents The Revenue Division s Cash Controls Report Number 2007-01

i Table of Contents The Revenue Division s Cash Controls Report Number 2007-01 EXECUTIVE SUMMARY iii PRELIMINARY Introduction 1 Objective 1 Audit Scope 1 Citywide Ramification 2 CONCLUSIONS 1. REVENUE

i Table of Contents The Revenue Division s Cash Controls Report Number 2007-01 EXECUTIVE SUMMARY iii PRELIMINARY Introduction 1 Objective 1 Audit Scope 1 Citywide Ramification 2 CONCLUSIONS 1. REVENUE

WEEK 6. Objective 1: Sales Transaction Cycle Risks

WEEK 6 CSA ch4 & GS ch10: pp457-488 Objective 1: Sales Transaction Cycle Risks The major assertions of interest to the auditor in ST of balances for account receivable are existence and valuation and allocation.

WEEK 6 CSA ch4 & GS ch10: pp457-488 Objective 1: Sales Transaction Cycle Risks The major assertions of interest to the auditor in ST of balances for account receivable are existence and valuation and allocation.

Chapter 15: Accounts Payable and Purchases

Accounting Research Manager - Audit Private Accounting Research Manager Miller Interpretations and Other Resources Knowledge-Based Audit Procedures Chapter 15: Accounts Payable and Purchases Chapter 15:

Accounting Research Manager - Audit Private Accounting Research Manager Miller Interpretations and Other Resources Knowledge-Based Audit Procedures Chapter 15: Accounts Payable and Purchases Chapter 15:

Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained

Performing Audit Procedures in Response to Assessed Risks 1781 AU Section 318 Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained (Supersedes SAS No. 55.)

Performing Audit Procedures in Response to Assessed Risks 1781 AU Section 318 Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained (Supersedes SAS No. 55.)

ACCOUNTING FOR AND AUDIT OF INVENTORIES

ACCOUNTING FOR AND AUDIT OF INVENTORIES PRESENTED BY MICHEAL AGHWANA MANAGER: PEAK PROFESSIONAL SERVICES IN HOUSE SEMINAR SERIES NO 3 PEAK PROFESSIONAL SERVICES (CHARTERED ACCOUNTANTS) NIGERIA A member

ACCOUNTING FOR AND AUDIT OF INVENTORIES PRESENTED BY MICHEAL AGHWANA MANAGER: PEAK PROFESSIONAL SERVICES IN HOUSE SEMINAR SERIES NO 3 PEAK PROFESSIONAL SERVICES (CHARTERED ACCOUNTANTS) NIGERIA A member

The audit of inventories

The audit of inventories Why is it important? Easiest assets to manipulate Misstatement affect reported profit: misstatement of inventory balances has a direct effect on reported profit. Inventories identification:

The audit of inventories Why is it important? Easiest assets to manipulate Misstatement affect reported profit: misstatement of inventory balances has a direct effect on reported profit. Inventories identification:

LEGAL SERVICES CORPORATION OFFICE OF INSPECTOR GENERAL FINAL REPORT ON SELECTED INTERNAL CONTROLS RHODE ISLAND LEGAL SERVICES, INC.

LEGAL SERVICES CORPORATION OFFICE OF INSPECTOR GENERAL FINAL REPORT ON SELECTED INTERNAL CONTROLS RHODE ISLAND LEGAL SERVICES, INC. RNO 140000 Report No. AU 16-05 March 2016 www.oig.lsc.gov TABLE OF CONTENTS

LEGAL SERVICES CORPORATION OFFICE OF INSPECTOR GENERAL FINAL REPORT ON SELECTED INTERNAL CONTROLS RHODE ISLAND LEGAL SERVICES, INC. RNO 140000 Report No. AU 16-05 March 2016 www.oig.lsc.gov TABLE OF CONTENTS

Department of Developmental Disabilities Accounts ReceivableAudit

Department of Developmental Disabilities Accounts Receivable Period: September 2015 through December 2015 Results Summary: Objective Accounts Receivable Creation Receipt of Payment Monitoring of Past Due

Department of Developmental Disabilities Accounts Receivable Period: September 2015 through December 2015 Results Summary: Objective Accounts Receivable Creation Receipt of Payment Monitoring of Past Due

Ken Wade, Jeff Bryson, Eileen Fitzgerald and Michael Forster. From: Frederick Udochi cc: Zewdneh Shiferaw. Date: May 14, 2009

To: Ken Wade, Jeff Bryson, Eileen Fitzgerald and Michael Forster From: Frederick Udochi cc: Zewdneh Shiferaw Date: May 14, 2009 Subject: Review of Accounts Payable/ ACH Wire Transfers Process Enclosed

To: Ken Wade, Jeff Bryson, Eileen Fitzgerald and Michael Forster From: Frederick Udochi cc: Zewdneh Shiferaw Date: May 14, 2009 Subject: Review of Accounts Payable/ ACH Wire Transfers Process Enclosed

Accounting 408 Test 3b Section Row

Accounting 408 Test 3b Name Section Row Multiple Choice. (2 points each) Read the following questions carefully and indicate the one best answer to each question by placing an X (do not circle) over the

Accounting 408 Test 3b Name Section Row Multiple Choice. (2 points each) Read the following questions carefully and indicate the one best answer to each question by placing an X (do not circle) over the

City of Amsterdam. Records and Reports. Report of Examination. Thomas P. DiNapoli. Period Covered: June 1, 2011 March 31, 2013 2013M-266

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY City of Amsterdam Records and Reports Report of Examination Period Covered: June 1, 2011 March 31, 2013 2013M-266

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY City of Amsterdam Records and Reports Report of Examination Period Covered: June 1, 2011 March 31, 2013 2013M-266

KANSAS CITY, MISSOURI RESPONSES TO THE FISCAL YEAR 2013 AUDIT MANAGEMENT LETTER

KANSAS CITY, MISSOURI RESPONSES TO THE FISCAL YEAR 2013 AUDIT MANAGEMENT LETTER Material Weaknesses (0) No material weaknesses were reported for FY 2013. Significant Deficiencies (1) Grant Receivable Accounting

KANSAS CITY, MISSOURI RESPONSES TO THE FISCAL YEAR 2013 AUDIT MANAGEMENT LETTER Material Weaknesses (0) No material weaknesses were reported for FY 2013. Significant Deficiencies (1) Grant Receivable Accounting

Audit Sampling. AU Section 350 AU 350.05

Audit Sampling 2067 AU Section 350 Audit Sampling (Supersedes SAS No. 1, sections 320A and 320B.) Source: SAS No. 39; SAS No. 43; SAS No. 45; SAS No. 111. See section 9350 for interpretations of this section.

Audit Sampling 2067 AU Section 350 Audit Sampling (Supersedes SAS No. 1, sections 320A and 320B.) Source: SAS No. 39; SAS No. 43; SAS No. 45; SAS No. 111. See section 9350 for interpretations of this section.

City of Richmond Department of Finance Fixed Assets

REPORT # 2012-07 AUDIT Of the City of Richmond Department of Finance Fixed Assets January 2012 TABLE OF CONTENTS Executive Summary..... i Comprehensive List of Recommendations iv Introduction...........

REPORT # 2012-07 AUDIT Of the City of Richmond Department of Finance Fixed Assets January 2012 TABLE OF CONTENTS Executive Summary..... i Comprehensive List of Recommendations iv Introduction...........

Innovation and Technology Department

PERFORMANCE AUDIT Innovation and Technology Department IT Inventory Asset Management January 11, 2016 Office of the City Manager Internal Audit Division Cheryl Johannes, Internal Audit Manager PERFORMANCE

PERFORMANCE AUDIT Innovation and Technology Department IT Inventory Asset Management January 11, 2016 Office of the City Manager Internal Audit Division Cheryl Johannes, Internal Audit Manager PERFORMANCE

Water and Wastewater Services Inventory Process Review

Water and Wastewater Services Inventory Process Review May 30, 2006 Report No. 06-15 Evan A. Lukic, CPA County Auditor Executive Summary This report summarizes our review of central warehouse inventory

Water and Wastewater Services Inventory Process Review May 30, 2006 Report No. 06-15 Evan A. Lukic, CPA County Auditor Executive Summary This report summarizes our review of central warehouse inventory

OFFICE OF THE CITY AUDITOR

OFFICE OF THE CITY AUDITOR PERFORMANCE AUDIT OF FUEL SERVICE CARDS Paul T. Garner Assistant City Auditor Prepared by: Theresa Hampden, CPA Audit Manager Regina Cannon Auditor October 29, 2004 Memorandum

OFFICE OF THE CITY AUDITOR PERFORMANCE AUDIT OF FUEL SERVICE CARDS Paul T. Garner Assistant City Auditor Prepared by: Theresa Hampden, CPA Audit Manager Regina Cannon Auditor October 29, 2004 Memorandum

Performance Audit Resolution Region H-Mid-Missouri Solid Waste Management District December 31, 2009, 201 0 and 2011

Performance Audit Resolution Region H-Mid-Missouri Solid Waste Management District December 31, 2009, 201 0 and 2011 1. Sunshine Law Policy Not Provided We recommend the District adopt a written Sunshine

Performance Audit Resolution Region H-Mid-Missouri Solid Waste Management District December 31, 2009, 201 0 and 2011 1. Sunshine Law Policy Not Provided We recommend the District adopt a written Sunshine

AUDIT REPORT 12-1 8. Audit of Controls over GPO s Fleet Credit Card Program. September 28, 2012

AUDIT REPORT 12-1 8 Audit of Controls over GPO s Fleet Credit Card Program September 28, 2012 Date September 28, 2012 To Director, Acquisition Services From Inspector General Subject Audit Report Audit

AUDIT REPORT 12-1 8 Audit of Controls over GPO s Fleet Credit Card Program September 28, 2012 Date September 28, 2012 To Director, Acquisition Services From Inspector General Subject Audit Report Audit

The Use of Spreadsheets: Considerations for Section 404 of the Sarbanes-Oxley Act*

The Use of Spreadsheets: Considerations for Section 404 of the Sarbanes-Oxley Act* July 2004 *connectedthinking The Use of Spreadsheets: Considerations for Section 404 of the Sarbanes-Oxley Act Introduction

The Use of Spreadsheets: Considerations for Section 404 of the Sarbanes-Oxley Act* July 2004 *connectedthinking The Use of Spreadsheets: Considerations for Section 404 of the Sarbanes-Oxley Act Introduction

Workers Compensation Commission

Audit Report Workers Compensation Commission March 2009 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related follow-up correspondence are

Audit Report Workers Compensation Commission March 2009 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related follow-up correspondence are

Audit of Financial Reporting Controls

Audit of Financial Reporting Controls WESTERN ECONOMIC DIVERSIFICATION CANADA Audit & Evaluation Branch February 2012 Table of Contents 1.0 Executive Summary 1 2.0 Statement of Assurance 1 3.0 Introduction

Audit of Financial Reporting Controls WESTERN ECONOMIC DIVERSIFICATION CANADA Audit & Evaluation Branch February 2012 Table of Contents 1.0 Executive Summary 1 2.0 Statement of Assurance 1 3.0 Introduction

REVENUE AND FINANCE DEPARTMENT ACCOUNTS RECEIVABLE/BILLING DIVISION CITY-WIDE ACCOUNTS RECEIVABLE AUDIT 11-10 JUNE 28, 2012

REVENUE AND FINANCE DEPARTMENT ACCOUNTS RECEIVABLE/BILLING DIVISION CITY-WIDE ACCOUNTS RECEIVABLE AUDIT 11-10 JUNE 28, 2012 CITY OF TAMPA Bob Buckhorn, Mayor Internal Audit Department Roger Strout, Internal

REVENUE AND FINANCE DEPARTMENT ACCOUNTS RECEIVABLE/BILLING DIVISION CITY-WIDE ACCOUNTS RECEIVABLE AUDIT 11-10 JUNE 28, 2012 CITY OF TAMPA Bob Buckhorn, Mayor Internal Audit Department Roger Strout, Internal

DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs Need Improvement

Report No. DODIG-2015-068 I nspec tor Ge ne ral U.S. Department of Defense JA N UA RY 1 4, 2 0 1 5 DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs

Report No. DODIG-2015-068 I nspec tor Ge ne ral U.S. Department of Defense JA N UA RY 1 4, 2 0 1 5 DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs

Internal Audit. Audit of the Inventory Control Framework

Internal Audit Audit of the Inventory Control Framework June 2010 Table of Contents EXECUTIVE SUMMARY...4 1. INTRODUCTION...7 1.1 BACKGROUND...7 1.2 OBJECTIVES...7 1.3 SCOPE OF THE AUDIT...7 1.4 METHODOLOGY...8

Internal Audit Audit of the Inventory Control Framework June 2010 Table of Contents EXECUTIVE SUMMARY...4 1. INTRODUCTION...7 1.1 BACKGROUND...7 1.2 OBJECTIVES...7 1.3 SCOPE OF THE AUDIT...7 1.4 METHODOLOGY...8

Audit Report on Inventory Controls Over Noncontrolled Drugs at Coney Island Hospital MG07-111A

Audit Report on Inventory Controls Over Noncontrolled Drugs at Coney Island Hospital MG07-111A June 25, 2009 THE CITY OF NEW YORK OFFICE OF THE COMPTROLLER 1 CENTRE STREET NEW YORK, N.Y. 10007-2341 WILLIAM

Audit Report on Inventory Controls Over Noncontrolled Drugs at Coney Island Hospital MG07-111A June 25, 2009 THE CITY OF NEW YORK OFFICE OF THE COMPTROLLER 1 CENTRE STREET NEW YORK, N.Y. 10007-2341 WILLIAM

CHAPTER 13 AUDITING DEBT OBLIGATIONS AND STOCKHOLDERS EQUITY TRANSACTIONS

A U D I T I N G A RISK-BASED APPROACH TO CONDUCTING A QUALITY AUDIT 9 th Edition Karla M. Johnstone Audrey A. Gramling Larry E. Rittenberg CHAPTER 13 AUDITING DEBT OBLIGATIONS AND STOCKHOLDERS EQUITY TRANSACTIONS

A U D I T I N G A RISK-BASED APPROACH TO CONDUCTING A QUALITY AUDIT 9 th Edition Karla M. Johnstone Audrey A. Gramling Larry E. Rittenberg CHAPTER 13 AUDITING DEBT OBLIGATIONS AND STOCKHOLDERS EQUITY TRANSACTIONS

AUDITOR GENERAL WILLIAM O. MONROE, CPA

AUDITOR GENERAL WILLIAM O. MONROE, CPA HILLSBOROUGH COUNTY DISTRICT SCHOOL BOARD LAWSON FINANCIALS MODULE Information Technology Audit SUMMARY To support its financial management needs, the Hillsborough

AUDITOR GENERAL WILLIAM O. MONROE, CPA HILLSBOROUGH COUNTY DISTRICT SCHOOL BOARD LAWSON FINANCIALS MODULE Information Technology Audit SUMMARY To support its financial management needs, the Hillsborough

CITY OF PALO ALTO OFFICE OF THE CITY AUDITOR

CITY OF PALO ALTO OFFICE OF THE CITY AUDITOR The Honorable City Council Attention: Finance Committee Palo Alto, California February 18, 2014 Inventory Management Audit In accordance with the Fiscal Year

CITY OF PALO ALTO OFFICE OF THE CITY AUDITOR The Honorable City Council Attention: Finance Committee Palo Alto, California February 18, 2014 Inventory Management Audit In accordance with the Fiscal Year

Inspection Observations Related to PCAOB "Risk Assessment" Auditing Standards (No. 8 through No.15)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org Inspection Observations Related to PCAOB "Risk Assessment" Auditing Standards (No. 8 through

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org Inspection Observations Related to PCAOB "Risk Assessment" Auditing Standards (No. 8 through

CITY OF SAN ANTONIO OFFICE OF THE CITY AUDITOR. Audit of Transportation and Capital Improvements. On-Call Contracts. Project No.

CITY OF SAN ANTONIO OFFICE OF THE CITY AUDITOR Audit of Transportation and Capital Improvements On-Call Contracts Project No. AU14-005 August 18, 2015 Kevin W. Barthold, CPA, CIA, CISA City Auditor Executive

CITY OF SAN ANTONIO OFFICE OF THE CITY AUDITOR Audit of Transportation and Capital Improvements On-Call Contracts Project No. AU14-005 August 18, 2015 Kevin W. Barthold, CPA, CIA, CISA City Auditor Executive

BACKGROUND, OBJECTIVES & METHODOLOGY

Page 2 of 10 Background BACKGROUND, OBJECTIVES & METHODOLOGY In accordance with the Office of the Controller s City Services Auditor Division (CSA) fiscal year 2011-12 work plan, CSA audited the warehouse

Page 2 of 10 Background BACKGROUND, OBJECTIVES & METHODOLOGY In accordance with the Office of the Controller s City Services Auditor Division (CSA) fiscal year 2011-12 work plan, CSA audited the warehouse

Annual Risk Assessment and Audit Plan Fiscal Year 2015/2016

Annual Risk Assessment and Audit Plan Fiscal Year 2015/2016 Office of the Internal Auditor May 2015 Table of Contents Introduction... 3 Risk Assessment Process... 3 Interpreting Risk Assessment Results...

Annual Risk Assessment and Audit Plan Fiscal Year 2015/2016 Office of the Internal Auditor May 2015 Table of Contents Introduction... 3 Risk Assessment Process... 3 Interpreting Risk Assessment Results...

Report on. 2009 Inspection of PricewaterhouseCoopers LLP. Public Company Accounting Oversight Board

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2009 (Headquartered in New York, New York) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2009 (Headquartered in New York, New York) Issued by the Public Company Accounting

Communicating Internal Control Related Matters Identified in an Audit

Communicating Internal Control 1843 AU Section 325 Communicating Internal Control Related Matters Identified in an Audit (Supersedes SAS No. 112.) Source: SAS No. 115. Effective for audits of financial

Communicating Internal Control 1843 AU Section 325 Communicating Internal Control Related Matters Identified in an Audit (Supersedes SAS No. 112.) Source: SAS No. 115. Effective for audits of financial

Social Services Contract Monitoring Audit

City of Austin AUDIT REPORT A Report to the Austin City Council Mayor Lee Leffingwell Mayor Pro Tem Sheryl Cole Social Services Contract Monitoring Audit October 2011 Council Members Chris Riley Mike Martinez

City of Austin AUDIT REPORT A Report to the Austin City Council Mayor Lee Leffingwell Mayor Pro Tem Sheryl Cole Social Services Contract Monitoring Audit October 2011 Council Members Chris Riley Mike Martinez

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/073

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/073 Audit of maintenance and building services provided by the Office of Central Support Services at Headquarters Overall results relating to the Office of Central

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/073 Audit of maintenance and building services provided by the Office of Central Support Services at Headquarters Overall results relating to the Office of Central

REPORT 2016/061 INTERNAL AUDIT DIVISION. Audit of inventory management in the United Nations Interim Force in Lebanon

INTERNAL AUDIT DIVISION REPORT 2016/061 Audit of inventory management in the United Nations Interim Force in Lebanon Overall results relating to the effective management of inventory were initially assessed

INTERNAL AUDIT DIVISION REPORT 2016/061 Audit of inventory management in the United Nations Interim Force in Lebanon Overall results relating to the effective management of inventory were initially assessed

Or download and view an electronic copy by visiting: www.sarasotagov.com

You can obtain copies of this report by contacting us at: Office of the City Auditor and Clerk 1565 1 st Street Sarasota, FL 34236 (941) 954-4135 Or download and view an electronic copy by visiting: www.sarasotagov.com

You can obtain copies of this report by contacting us at: Office of the City Auditor and Clerk 1565 1 st Street Sarasota, FL 34236 (941) 954-4135 Or download and view an electronic copy by visiting: www.sarasotagov.com

COMPTROLLER FINANCIAL AUDIT

City of New York OFFICE OF THE COMPTROLLER Scott M. Stringer COMPTROLLER FINANCIAL AUDIT Marjorie Landa Deputy Comptroller for Audit Audit Report on the Department of Education's Oversight of Computer

City of New York OFFICE OF THE COMPTROLLER Scott M. Stringer COMPTROLLER FINANCIAL AUDIT Marjorie Landa Deputy Comptroller for Audit Audit Report on the Department of Education's Oversight of Computer

Audit of Controls Over Contract Payments FINAL AUDIT REPORT

Audit of Controls Over Contract Payments FINAL AUDIT REPORT ED-OIG/A07-A0015 March 2001 Our mission is to promote the efficient U.S. Department of Education and effective use of taxpayer dollars Office

Audit of Controls Over Contract Payments FINAL AUDIT REPORT ED-OIG/A07-A0015 March 2001 Our mission is to promote the efficient U.S. Department of Education and effective use of taxpayer dollars Office

U.S. Department of Agriculture Office of Inspector General Financial and IT Operations Audit Report

U.S. Department of Agriculture Office of Inspector General Financial and IT Operations Audit Report FISCAL YEAR 2000 NATIONAL FINANCE CENTER REVIEW OF INTERNAL CONTROLS NAT Report No. 11401-7-FM June 2001

U.S. Department of Agriculture Office of Inspector General Financial and IT Operations Audit Report FISCAL YEAR 2000 NATIONAL FINANCE CENTER REVIEW OF INTERNAL CONTROLS NAT Report No. 11401-7-FM June 2001

OFFICE OF THE STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT SERVICES

OFFICE OF THE STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT SERVICES AND ECONOMIC DEVELOPMENT TECHNICAL ASSISTANCE Comptroller OFFICE OF THE STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT SERVICES & ECONOMIC

OFFICE OF THE STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT SERVICES AND ECONOMIC DEVELOPMENT TECHNICAL ASSISTANCE Comptroller OFFICE OF THE STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT SERVICES & ECONOMIC

Office of the City Auditor. Audit Report. AUDIT OF MONTHLY BANK RECONCILIATIONS (Report No. A08-014) May 16, 2008. City Auditor. Craig D.

May 16, 2008. City Auditor. Craig D.") CITY OF DALLAS Dallas City Council Office of the City Auditor Audit Report Mayor Tom Leppert Mayor Pro Tem Dr. Elba Garcia AUDIT OF MONTHLY BANK RECONCILIATIONS (Report No. A08-014) Deputy Mayor Pro Tem

CITY OF DALLAS Dallas City Council Office of the City Auditor Audit Report Mayor Tom Leppert Mayor Pro Tem Dr. Elba Garcia AUDIT OF MONTHLY BANK RECONCILIATIONS (Report No. A08-014) Deputy Mayor Pro Tem

KPMG LLP Suite 12000 1801 K Street, NW Washington, DC 20006 Independent Auditors Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements

KPMG LLP Suite 12000 1801 K Street, NW Washington, DC 20006 Independent Auditors Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements

Navy s Contract/Vendor Pay Process Was Not Auditable

Inspector General U.S. Department of Defense Report No. DODIG-2015-142 JULY 1, 2015 Navy s Contract/Vendor Pay Process Was Not Auditable INTEGRITY EFFICIENCY ACCOUNTABILITY EXCELLENCE INTEGRITY EFFICIENCY

Inspector General U.S. Department of Defense Report No. DODIG-2015-142 JULY 1, 2015 Navy s Contract/Vendor Pay Process Was Not Auditable INTEGRITY EFFICIENCY ACCOUNTABILITY EXCELLENCE INTEGRITY EFFICIENCY

AUDIT REPORT FACILITIES INFORMATION MANAGEMENT SYSTEM DOE/IG-0468 APRIL 2000

DOE/IG-0468 AUDIT REPORT FACILITIES INFORMATION MANAGEMENT SYSTEM APRIL 2000 U.S. DEPARTMENT OF ENERGY OFFICE OF INSPECTOR GENERAL OFFICE OF AUDIT SERVICES April 26, 2000 MEMORANDUM FOR THE SECRETARY FROM:

DOE/IG-0468 AUDIT REPORT FACILITIES INFORMATION MANAGEMENT SYSTEM APRIL 2000 U.S. DEPARTMENT OF ENERGY OFFICE OF INSPECTOR GENERAL OFFICE OF AUDIT SERVICES April 26, 2000 MEMORANDUM FOR THE SECRETARY FROM:

RELEVANT TO FOUNDATION LEVEL PAPER FAU / ACCA QUALIFICATION PAPER F8

RELEVANT TO FOUNDATION LEVEL PAPER FAU / ACCA QUALIFICATION PAPER F8 Audit procedures Audit procedures are an important area of the syllabus, though candidates often use inappropriate audit procedures

RELEVANT TO FOUNDATION LEVEL PAPER FAU / ACCA QUALIFICATION PAPER F8 Audit procedures Audit procedures are an important area of the syllabus, though candidates often use inappropriate audit procedures

Webinar: PCAOB Inspections of Small Firm Broker-Dealer Auditors. January 15, 2015

Webinar: PCAOB Inspections of Small Firm Broker-Dealer Auditors January 15, 2015 Introductory Remarks Mary Sjoquist, Director Office of Outreach and Small Business Liaison Caveat The views we express today

Webinar: PCAOB Inspections of Small Firm Broker-Dealer Auditors January 15, 2015 Introductory Remarks Mary Sjoquist, Director Office of Outreach and Small Business Liaison Caveat The views we express today

AUDIT REPORT REPORT NUMBER 14 10. Information Technology Microsoft Software Licenses March 27, 2014

AUDIT REPORT REPORT NUMBER 14 10 Information Technology Microsoft Software Licenses March 27, 2014 Date March 27, 2014 To Chief Information Officer From Inspector General Subject Audit Report Information

AUDIT REPORT REPORT NUMBER 14 10 Information Technology Microsoft Software Licenses March 27, 2014 Date March 27, 2014 To Chief Information Officer From Inspector General Subject Audit Report Information

AUDIT REPORT. Materials System Inventory Management Practices at Washington River Protection Solutions

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections AUDIT REPORT Materials System Inventory Management Practices at Washington River Protection Solutions OAS-M-15-01

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections AUDIT REPORT Materials System Inventory Management Practices at Washington River Protection Solutions OAS-M-15-01

AU14-F02 Financial Services Department Utilities Business Office Audit Follow-up Report

AU4-F0 Financial Services Department Utilities Business Office Audit Follow-up Report City Auditor s Office Arlena Sones, CPA, CIA, CGAP City Auditor September 3, 05 Executive Summary As part of our annual

AU4-F0 Financial Services Department Utilities Business Office Audit Follow-up Report City Auditor s Office Arlena Sones, CPA, CIA, CGAP City Auditor September 3, 05 Executive Summary As part of our annual

Chapter 7: Solutions. Multiple Choice Questions From CPA Examinations. 7-27 a. (2) b. (1) c. (4) d. (4) 7-28 a. (3) b. (3) c. (4) d.

b. (1) c. (4) d. (4) 7-28 a. (3) b. (3) c. (4) d.") Chapter 7: Solutions Multiple Choice Questions From CPA Examinations 7-27 a. (2) b. (1) c. (4) d. (4) 7-28 a. (3) b. (3) c. (4) d. (4) Discussion Questions And Problems 7-29 a. 1. External 7. Internal

Chapter 7: Solutions Multiple Choice Questions From CPA Examinations 7-27 a. (2) b. (1) c. (4) d. (4) 7-28 a. (3) b. (3) c. (4) d. (4) Discussion Questions And Problems 7-29 a. 1. External 7. Internal

Assessing Credit Risk

Assessing Credit Risk Objectives Discuss the following: Inherent Risk Quality of Risk Management Residual or Composite Risk Risk Trend 2 Inherent Risk Define the risk Identify sources of risk Quantify

Assessing Credit Risk Objectives Discuss the following: Inherent Risk Quality of Risk Management Residual or Composite Risk Risk Trend 2 Inherent Risk Define the risk Identify sources of risk Quantify

In Brief. Smithsonian Institution Office of the Inspector General

Smithsonian Institution Office of the Inspector General In Brief Oversight of Contractors at Smithsonian Business Ventures Report Number A-07-05, February 25, 2008 Why We Did This Audit This audit is the

Smithsonian Institution Office of the Inspector General In Brief Oversight of Contractors at Smithsonian Business Ventures Report Number A-07-05, February 25, 2008 Why We Did This Audit This audit is the

Independent Auditor s Report on the Export Import Bank s Data Reliability

OFFICE OF INSPECTOR GENERAL EXPORT IMPORT BANK of the UNITED STATES Independent Auditor s Report on the Export Import Bank s Data Reliability September 28, 2015 OIG AR 15 07. I NSPECTOR G ENERAL EXPORT-IMPORT

OFFICE OF INSPECTOR GENERAL EXPORT IMPORT BANK of the UNITED STATES Independent Auditor s Report on the Export Import Bank s Data Reliability September 28, 2015 OIG AR 15 07. I NSPECTOR G ENERAL EXPORT-IMPORT

Examiner s report F8 Audit & Assurance September 2015

Examiner s report F8 Audit & Assurance September 2015 General Comments There were two sections to the examination paper and all the questions were compulsory. Section A consisted of 12 multiple-choice

Examiner s report F8 Audit & Assurance September 2015 General Comments There were two sections to the examination paper and all the questions were compulsory. Section A consisted of 12 multiple-choice

Prince George s County Public Schools

Financial Management Practices Audit Report Prince George s County Public Schools February 2014 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and

Financial Management Practices Audit Report Prince George s County Public Schools February 2014 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and

INTERNAL CONTROL MATRIX FOR AUDIT OF ESTIMATING SYSTEM CONTROLS Version No. 3.2 June 2006. 31-d Page 1 of 7

INTERNAL CONTROL MATRIX FOR AUDIT OF ESTIMATING SYSTEM CONTROLS Version No. 3.2 June 2006 Control Objectives Example Control Activities Audit Procedures 1. INTERNAL AUDITS Management should periodically

INTERNAL CONTROL MATRIX FOR AUDIT OF ESTIMATING SYSTEM CONTROLS Version No. 3.2 June 2006 Control Objectives Example Control Activities Audit Procedures 1. INTERNAL AUDITS Management should periodically

Office of the City Auditor. Audit of the Department of Public Works and Public Utilities Inventory/Storerooms

Audit of the Department of Public Works and Public Utilities Report Date: March 21, 2016 Office of the City Auditor 2401 Courthouse Drive, Room 344 Virginia Beach, Virginia 23456 757.385.5870 Promoting

Audit of the Department of Public Works and Public Utilities Report Date: March 21, 2016 Office of the City Auditor 2401 Courthouse Drive, Room 344 Virginia Beach, Virginia 23456 757.385.5870 Promoting

Chapter 14 Completing the Tests in the Sales and Collection Cycle: Accounts Receivable

Chapter 14 Completing the Tests in the Sales and Collection Cycle: Accounts Receivable Review Questions 14-1 Tests of details of financial balances are designed to determine the reasonableness of the balances

Chapter 14 Completing the Tests in the Sales and Collection Cycle: Accounts Receivable Review Questions 14-1 Tests of details of financial balances are designed to determine the reasonableness of the balances

Fundamentals Level Skills Module, Paper F8 (INT)

") Answers Fundamentals Level Skills Module, Paper F8 (INT) Audit and Assurance (International) December 2013 Answers 1 (a) Audit risk and its components Audit risk is the risk that the auditor expresses

Answers Fundamentals Level Skills Module, Paper F8 (INT) Audit and Assurance (International) December 2013 Answers 1 (a) Audit risk and its components Audit risk is the risk that the auditor expresses

AUDIT OF SBA S COMPLIANCE WITH JOINT FINANCIAL MANAGEMENT IMPROVEMENT PROGRAM PROPERTY MANAGEMENT SYSTEM REQUIREMENTS AUDIT REPORT NUMBER 3-34

AUDIT OF SBA S COMPLIANCE WITH JOINT FINANCIAL MANAGEMENT IMPROVEMENT PROGRAM PROPERTY MANAGEMENT SYSTEM REQUIREMENTS AUDIT REPORT NUMBER 3-34 JULY 23, 2003 This report may contain proprietary information

AUDIT OF SBA S COMPLIANCE WITH JOINT FINANCIAL MANAGEMENT IMPROVEMENT PROGRAM PROPERTY MANAGEMENT SYSTEM REQUIREMENTS AUDIT REPORT NUMBER 3-34 JULY 23, 2003 This report may contain proprietary information

AUDIT OF CASH REGISTER, IMPREST FUNDS, AND PETTY CASH TRANSACTIONS JULY 01, 2004 THROUGH JUNE 30, 2005 TABLE OF CONTENTS

AUDIT OF CASH REGISTER, IMPREST FUNDS, AND PETTY CASH TRANSACTIONS JULY 01, 2004 THROUGH JUNE 30, 2005 TABLE OF CONTENTS INTRODUCTION... 1 SCOPE AND OBJECTIVES... 2 METHODOLOGY... 3 SUMMARY OF AUDIT FINDINGS...

AUDIT OF CASH REGISTER, IMPREST FUNDS, AND PETTY CASH TRANSACTIONS JULY 01, 2004 THROUGH JUNE 30, 2005 TABLE OF CONTENTS INTRODUCTION... 1 SCOPE AND OBJECTIVES... 2 METHODOLOGY... 3 SUMMARY OF AUDIT FINDINGS...

Communicating Internal Control Related Matters Identified in an Audit

Communicating Internal Control Related Matters 227 AU-C Section 265 Communicating Internal Control Related Matters Identified in an Audit Source: SAS No. 122; SAS No. 125; SAS No. 128. See section 9265

Communicating Internal Control Related Matters 227 AU-C Section 265 Communicating Internal Control Related Matters Identified in an Audit Source: SAS No. 122; SAS No. 125; SAS No. 128. See section 9265

Examiner s report F8 Audit & Assurance December 2014

Examiner s report F8 Audit & Assurance December 2014 General Comments The examination consisted of twelve objective test questions in Section A, worth 20 marks and six questions in Section B worth 80 marks.

Examiner s report F8 Audit & Assurance December 2014 General Comments The examination consisted of twelve objective test questions in Section A, worth 20 marks and six questions in Section B worth 80 marks.

Department of Transportation Financial Management Information System Centralized Operations

Audit Report Department of Transportation Financial Management Information System Centralized Operations July 2001 This report and any related follow-up correspondence are available to the public and may

Audit Report Department of Transportation Financial Management Information System Centralized Operations July 2001 This report and any related follow-up correspondence are available to the public and may

Report on. 2015 Inspection of Deloitte AS (Headquartered in Oslo, Kingdom of Norway) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Oslo, Kingdom of Norway) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Oslo, Kingdom of Norway) Issued by the Public Company Accounting

AUDIT REPORT. The Energy Information Administration s Information Technology Program

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections AUDIT REPORT The Energy Information Administration s Information Technology Program DOE-OIG-16-04 November 2015 Department

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections AUDIT REPORT The Energy Information Administration s Information Technology Program DOE-OIG-16-04 November 2015 Department

U S I N G D A T A A N A L Y S I S T O M E E T T H E R E Q U I R E M E N T S O F R I S K B A S E D A U D I T I N G S T A N D A R D S

U S I N G D A T A A N A L Y S I S T O M E E T T H E R E Q U I R E M E N T S O F R I S K B A S E D A U D I T I N G S T A N D A R D S A C a s e W a r e I D E A R e s e a r c h R e p o r t CaseWare IDEA Inc.

U S I N G D A T A A N A L Y S I S T O M E E T T H E R E Q U I R E M E N T S O F R I S K B A S E D A U D I T I N G S T A N D A R D S A C a s e W a r e I D E A R e s e a r c h R e p o r t CaseWare IDEA Inc.

Lebanese Association of Certified Public Accountants - AUDIT December Exam 2014

MULTIPLE CHOICE QUESTIONS (40%) 1) When qualifying an opinion because of an insufficiency of audit evidence, an auditor should refer to the situation in the Opinion (introductory) Scope paragraph paragraph

MULTIPLE CHOICE QUESTIONS (40%) 1) When qualifying an opinion because of an insufficiency of audit evidence, an auditor should refer to the situation in the Opinion (introductory) Scope paragraph paragraph

2012 AICPA Newly Released Questions Auditing

Following are multiple choice questions recently released by the AICPA. These questions were released by the AICPA with letter answers only. Our editorial board has provided the accompanying explanation.

Following are multiple choice questions recently released by the AICPA. These questions were released by the AICPA with letter answers only. Our editorial board has provided the accompanying explanation.

What are substantive tests?

Session Overview Test 3 topics Tut letter 104: Substantive procedures: My approach to this session General principles, when it comes to substantive procedures Developing frameworks for answering substantive

Session Overview Test 3 topics Tut letter 104: Substantive procedures: My approach to this session General principles, when it comes to substantive procedures Developing frameworks for answering substantive

AUDIT REPORT INTERNAL AUDIT DIVISION. Audit of non-expendable property at Headquarters

INTERNAL AUDIT DIVISION AUDIT REPORT Audit of non-expendable property at Headquarters Overall results relating to the effective management of property records and inventory control were initially assessed

INTERNAL AUDIT DIVISION AUDIT REPORT Audit of non-expendable property at Headquarters Overall results relating to the effective management of property records and inventory control were initially assessed

Transmittal Letter... 1. Objectives and Scope... 2. Approach... 3-7. Financial System... 8. Permitting Application... 9

Internal Audit Committee of Information Technology Risk Assessment Public Report Prepared By: Internal Auditors of Brevard County September 30, 2009 Table of Contents Transmittal Letter... 1 Objectives

Internal Audit Committee of Information Technology Risk Assessment Public Report Prepared By: Internal Auditors of Brevard County September 30, 2009 Table of Contents Transmittal Letter... 1 Objectives

Follow-up Audit Golf Course Retail Inventory Controls

Follow-up Audit Golf Course Retail Inventory Controls October 2000 City Auditor s Office City of Kansas City, Missouri 32-2000 October 31, 2000 Honorable Mayor, Members of the City Council, and Members

Follow-up Audit Golf Course Retail Inventory Controls October 2000 City Auditor s Office City of Kansas City, Missouri 32-2000 October 31, 2000 Honorable Mayor, Members of the City Council, and Members

Public Safety Vehicle Repair Audit

City of Austin AUDIT REPORT A Report to the Austin City Council Mayor Lee Leffingwell Public Safety Vehicle Repair Audit October 2013 Mayor Pro Tem Sheryl Cole Council Members Chris Riley Mike Martinez

City of Austin AUDIT REPORT A Report to the Austin City Council Mayor Lee Leffingwell Public Safety Vehicle Repair Audit October 2013 Mayor Pro Tem Sheryl Cole Council Members Chris Riley Mike Martinez

Appendix C: Examples of Common Accounting and Bookkeeping Procedures

Appendix C: Examples of Common Accounting and Bookkeeping Procedures In this Appendix the use of the term monthly means on a regular cycle, based on the needs of your district. Some of the sample accounting

Appendix C: Examples of Common Accounting and Bookkeeping Procedures In this Appendix the use of the term monthly means on a regular cycle, based on the needs of your district. Some of the sample accounting

Internal Audit Committee of Brevard County, Florida Internal Audit of Timekeeping and Payroll Process

Internal Audit Committee of Brevard County, Florida Internal Audit of Timekeeping and Payroll Process May 31, 2011 Prepared By: Table of Contents Transmittal Letter... 1 Executive Summary... 2-4 Background...

Internal Audit Committee of Brevard County, Florida Internal Audit of Timekeeping and Payroll Process May 31, 2011 Prepared By: Table of Contents Transmittal Letter... 1 Executive Summary... 2-4 Background...

Community Ambulance Service District

STATUTORY AUDIT Community Ambulance Service District For the year ended June 30, 2014 Oklahoma State Auditor & Inspector Gary A. Jones, CPA, CFE This publication, issued by the Oklahoma State Auditor and

STATUTORY AUDIT Community Ambulance Service District For the year ended June 30, 2014 Oklahoma State Auditor & Inspector Gary A. Jones, CPA, CFE This publication, issued by the Oklahoma State Auditor and

How To Audit A Company

INTERNATIONAL STANDARD ON AUDITING 315 IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT (Effective for audits of financial statements for

INTERNATIONAL STANDARD ON AUDITING 315 IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT (Effective for audits of financial statements for

OPERATIONAL AND CONSUMABLE INVENTORY POLICY

OPERATIONAL AND CONSUMABLE INVENTORY POLICY PURPOSE The purpose of this policy is to establish guidelines for the management of inventory as a key institutional resource. This policy lays the foundation

OPERATIONAL AND CONSUMABLE INVENTORY POLICY PURPOSE The purpose of this policy is to establish guidelines for the management of inventory as a key institutional resource. This policy lays the foundation

AUDITOR GENERAL DAVID W. MARTIN, CPA

AUDITOR GENERAL DAVID W. MARTIN, CPA AGENCY FOR HEALTH CARE ADMINISTRATION ADMINISTRATIVE ACTIVITIES Operational Audit SUMMARY This operational audit of the Agency for Health Care Administration (Agency)

AUDITOR GENERAL DAVID W. MARTIN, CPA AGENCY FOR HEALTH CARE ADMINISTRATION ADMINISTRATIVE ACTIVITIES Operational Audit SUMMARY This operational audit of the Agency for Health Care Administration (Agency)

NASA Financial Management

Before the Government Reform Subcommittee on Government Efficiency and Financial Management U.S. House of Representatives For Release on Delivery expected at 2:00 p.m. EDT Wednesday May 19, 2004 NASA Financial

Before the Government Reform Subcommittee on Government Efficiency and Financial Management U.S. House of Representatives For Release on Delivery expected at 2:00 p.m. EDT Wednesday May 19, 2004 NASA Financial

INTUIT PROFESSIONAL EDUCATION. QuickBooks Files: Sharing, Managing, and Maintaining Data Integrity

INTUIT PROFESSIONAL EDUCATION QuickBooks Files: Sharing, Managing, and Maintaining Data Integrity Copyright Copyright 2008 Intuit Inc. All rights reserved. Intuit Inc. 5601 Headquarters Drive Plano, TX

INTUIT PROFESSIONAL EDUCATION QuickBooks Files: Sharing, Managing, and Maintaining Data Integrity Copyright Copyright 2008 Intuit Inc. All rights reserved. Intuit Inc. 5601 Headquarters Drive Plano, TX

OFFICE OF INSPECTOR GENERAL. Audit Report

OFFICE OF INSPECTOR GENERAL Audit Report Audit of Internal Control Over Accounts Payable Report No. 09-03 March 31, 2009 RAILROAD RETIREMENT BOARD INTRODUCTION This report presents the results of the Office

OFFICE OF INSPECTOR GENERAL Audit Report Audit of Internal Control Over Accounts Payable Report No. 09-03 March 31, 2009 RAILROAD RETIREMENT BOARD INTRODUCTION This report presents the results of the Office

10-1. Auditing Business Process. Objectives Understand the Auditing of the Enteties Business. Process

10-1 Auditing Business Process Auditing Business Process Objectives Understand the Auditing of the Enteties Business Process Identify the types of transactions in different Business Process Asses Control

10-1 Auditing Business Process Auditing Business Process Objectives Understand the Auditing of the Enteties Business Process Identify the types of transactions in different Business Process Asses Control

Basic Concepts of Accounting Subsidiary Subsidiary Special Special Inform Infor a m tion Ledgers Ledger Journals Jour Systems

COMPUTERIZED ACCOUNTING SYSTEMS Basic Concepts of Accounting Information Systems Subsidiary Ledgers Special Journals Computerized accounting systems Manual accounting systems Example Advantages Sales journal

COMPUTERIZED ACCOUNTING SYSTEMS Basic Concepts of Accounting Information Systems Subsidiary Ledgers Special Journals Computerized accounting systems Manual accounting systems Example Advantages Sales journal

INTERNATIONAL STANDARD ON AUDITING 530 AUDIT SAMPLING AND OTHER MEANS OF TESTING CONTENTS

INTERNATIONAL STANDARD ON AUDITING 530 AUDIT SAMPLING AND OTHER MEANS OF TESTING (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction...

INTERNATIONAL STANDARD ON AUDITING 530 AUDIT SAMPLING AND OTHER MEANS OF TESTING (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction...

FOR PUBLIC RELEASE. Office of the Secretary. Commerce Should Strengthen Accountability and Internal Controls in Its Motor Pool Operations

U.S. DEPARTMENT OF COMMERCE Office of the Secretary Commerce Should Strengthen Accountability and Internal Controls in Its Motor Pool Operations FOR PUBLIC RELEASE Office of Audit and Evaluation UNITED

U.S. DEPARTMENT OF COMMERCE Office of the Secretary Commerce Should Strengthen Accountability and Internal Controls in Its Motor Pool Operations FOR PUBLIC RELEASE Office of Audit and Evaluation UNITED

Substantive Tests of Transactions and Balances

10 CHAPTER Substantive Tests of Transactions and Balances LEARNING OBJECTIVES After studying this chapter you should be able to: 1 2 identify and distinguish between tests of controls and substantive tests

10 CHAPTER Substantive Tests of Transactions and Balances LEARNING OBJECTIVES After studying this chapter you should be able to: 1 2 identify and distinguish between tests of controls and substantive tests

Missouri State Auditor March 2014 http://auditor.mo.gov Report No. 2014-016

Thomas A. Schweich Missouri State Auditor FOLLOW-UP REPORT ON AUDIT FINDINGS City of Marshfield March 2014 Report No. 2014-016 http://auditor.mo.gov Follow-Up Report on Audit Findings Table of Contents

Thomas A. Schweich Missouri State Auditor FOLLOW-UP REPORT ON AUDIT FINDINGS City of Marshfield March 2014 Report No. 2014-016 http://auditor.mo.gov Follow-Up Report on Audit Findings Table of Contents

FLORIDA DEPARTMENT OF ENVIRONMENTAL PROTECTION LOAN NO. WW67006P

FLORIDA DEPARTMENT OF ENVIRONMENTAL PROTECTION LOAN NO. WW67006P SPECIAL PURPOSE FINANCIAL STATEMENT AND INDEPENDENT AUDITORS REPORTS AUGUST 2007 (DATE OF LOAN INCEPTION) THROUGH SEPTEMBER 2011 CITY OF

FLORIDA DEPARTMENT OF ENVIRONMENTAL PROTECTION LOAN NO. WW67006P SPECIAL PURPOSE FINANCIAL STATEMENT AND INDEPENDENT AUDITORS REPORTS AUGUST 2007 (DATE OF LOAN INCEPTION) THROUGH SEPTEMBER 2011 CITY OF

EPA Needs to Improve Its. Information Technology. Audit Follow-Up Processes

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Information Technology EPA Needs to Improve Its Information Technology Audit Follow-Up Processes Report No. 16-P-0100 March 10, 2016 Report

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Information Technology EPA Needs to Improve Its Information Technology Audit Follow-Up Processes Report No. 16-P-0100 March 10, 2016 Report

Report 7 Appendix 1d Final Internal Audit Report Sundry Income and Debtors (inc. Fees and Charges) Greater London Authority February 2010

Greater London Authority February 2010") Report 7 Appendix 1d Final Internal Audit Report Sundry Income and Debtors (inc. Fees and Charges) Greater London Authority February 2010 This report has been prepared on the basis of the limitations set

Report 7 Appendix 1d Final Internal Audit Report Sundry Income and Debtors (inc. Fees and Charges) Greater London Authority February 2010 This report has been prepared on the basis of the limitations set

Office of the Inspector General Department of Defense

ACCOUNTING ENTRIES MADE IN COMPILING THE FY 2000 FINANCIAL STATEMENTS FOR THE WORKING CAPITAL FUNDS OF THE AIR FORCE AND OTHER DEFENSE ORGANIZATIONS Report No. D-2001-163 July 26, 2001 Office of the Inspector

ACCOUNTING ENTRIES MADE IN COMPILING THE FY 2000 FINANCIAL STATEMENTS FOR THE WORKING CAPITAL FUNDS OF THE AIR FORCE AND OTHER DEFENSE ORGANIZATIONS Report No. D-2001-163 July 26, 2001 Office of the Inspector

Division of Insurance Internal Control Questionnaire For the period July 1, 2013 through June 30, 2014

Official Audit Report Issued March 6, 2015 Internal Control Questionnaire For the period July 1, 2013 through June 30, 2014 State House Room 230 Boston, MA 02133 auditor@sao.state.ma.us www.mass.gov/auditor

Official Audit Report Issued March 6, 2015 Internal Control Questionnaire For the period July 1, 2013 through June 30, 2014 State House Room 230 Boston, MA 02133 auditor@sao.state.ma.us www.mass.gov/auditor

INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 315

315") INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 315 IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT (Effective for audits of financial

INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 315 IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT (Effective for audits of financial

Appendix E: Business Process Characteristics How This Resolves Current Deficiencies

Appendix E: Business Process Characteristics How This Resolves Current Deficiencies The BPR working group identified major deficiencies in the As-Is environment, and developed business processes, rules,

Appendix E: Business Process Characteristics How This Resolves Current Deficiencies The BPR working group identified major deficiencies in the As-Is environment, and developed business processes, rules,

Reporting Capital Equipment: An Auditor's Perspective

Reporting Capital Equipment: An Auditor's Perspective Brian Mikel CHAN HEALTHCARE Overview Internal audit background Capital equipment sources and requirements Audit perspective and definitions Depreciation

Reporting Capital Equipment: An Auditor's Perspective Brian Mikel CHAN HEALTHCARE Overview Internal audit background Capital equipment sources and requirements Audit perspective and definitions Depreciation