CHAPTER 7. SALES TAXES, VEHICLE INVENTORY TAXES, AND STANDARD PRESUMPTIVE VALUE

|

|

|

- Priscilla May

- 9 years ago

- Views:

Transcription

1 CHAPTER 7. SALES TAXES, VEHICLE INVENTORY TAXES, AND STANDARD PRESUMPTIVE VALUE NOTE: This section is meant solely as an introduction and may not reflect the most recent law changes as Motor Vehicle Sales and Use Tax is regulated by the Texas Comptroller of Public Accounts. More detailed information may be obtained by calling or For Information regarding Vehicle Inventory Tax call For a complete list of motor vehicle sales and use tax forms, see forms.html. 7.1 Sales Tax. A sales tax, currently 6.25 percent, is levied on motor vehicle sales in the state of Texas. For sales tax purposes, the taxable total consideration of a motor vehicle is the sale price of the vehicle, less any trade-in allowance for a motor vehicle. It does not include documentary fees, inspection fees, finance charges or the title and registration fees. If the tax is submitted to the county tax assessor-collector more than 20 county working days after the sale, a penalty of 5 percent of the sales tax due is levied. If the tax is paid more than 30 calendar days after the date on which the tax was due, an additional 5 percent penalty is due. 7.2 Seller-financed Sales. If you are a dealer who offers consumers contracts to finance sales, you must be licensed by the Office of the Consumer Credit Commissioner. You must apply for and hold a permit from the Comptroller s Office. When the application for transfer of title is submitted, the dealer s seller-financed sales tax permit number from the Comptroller is placed on the application to defer the tax. Sales tax is paid on the receipts collected during each reporting period at the time of filing the seller-financed report. The tax is paid only on the amounts collected. Sales tax on a down payment would be due when the dealer files his seller-financed sales report to the Comptroller. The remaining taxes would then be collected on a straight-line basis for the remainder of the note amount. If payments stop and the vehicle is repossessed, sales tax must be paid only on the actual payments received by the dealer. This method is preferred by most dealers. In the event that sales tax is paid in full when the application for transfer of title is submitted or the sales tax is paid in full on the next seller-financed reporting period, then no refund is available if repossession occurs. This right to defer sales taxes is canceled in two situations. If the dealer does not transfer title within 60 days of the sale, all the sales tax is due in the period in which the failure to transfer the title occurs. Further, if the sales contract is sold to an unrelated third party or a nonqualifying related third party, the full sales tax amount is due in the period in which the note transfer occurs. The ability to defer sales tax on the transaction no longer exists. Page 7-1

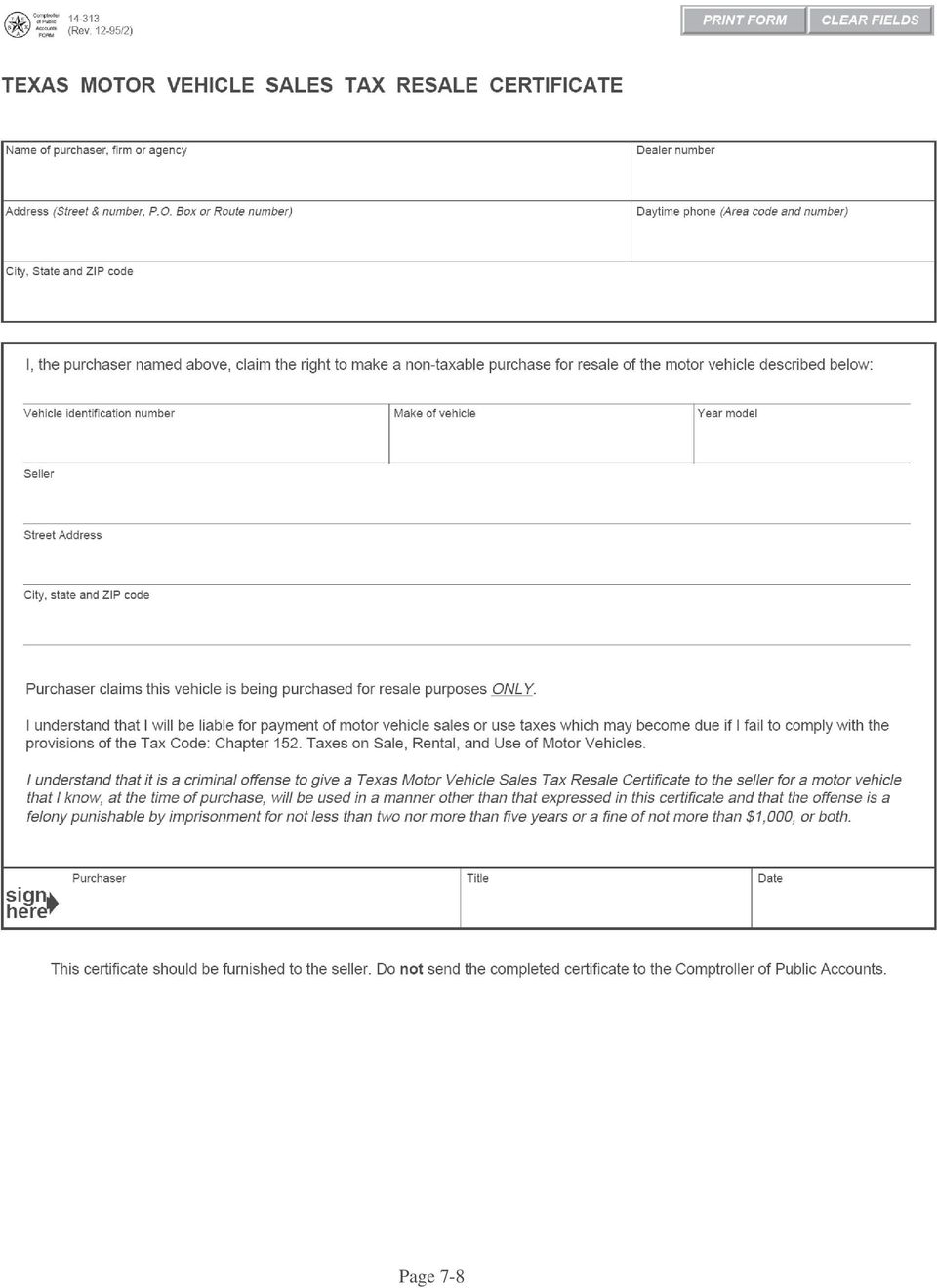

2 A seller-finance dealer may transfer a vehicle to a qualifying related finance company without accelerating and paying the tax. However, it only applies to qualifying transfers after a related finance company has registered with the Comptroller s office and paid a $600 registration fee. A qualifying related finance company is an entity that has at least 80 percent ownership identical to the ownership of the dealer. The application for a seller finance permit is Form AP-169 and the seller finance report is Form The application for a related finance company is Form AP Cash Sales and Third Party Finance Sales. The law requires the selling dealer in all cash sales (including bank-financed sales) to collect the sales tax from the customer and to pay it to the county tax office within 20 county working days. The failure to collect sales tax is not an excuse for failure to apply for transfer of title in a timely manner. The dealer may not give the title and transfer paperwork to the consumer and send the consumer to the tax office to apply for transfer of title. The dealer must handle the transaction. Even if no cash is received from a buyer, such as when a trade-in is used as the down payment on a replacement vehicle, the dealer must apply to transfer title in a timely manner and pay the applicable sales tax. To this day, tax offices statewide report dozens of dealers who do not collect the sales tax and rely on the buyer to handle the transfer themselves. These complaints result in warning letters and civil penalties assessed against the dealer by TxDMV. Failure to collect and pay tax may also result in actions by the Comptroller. 7.4 Exemption/Resale Certificates. a. Texas Motor Vehicle Sales Tax Exemption Certificate For Vehicles Taken Out of State. If the vehicle is to be transported immediately out of Texas for titling and registration, a motor vehicle sales tax exemption certificate Form may be completed and signed by the buyer. To be a valid exemption, there must be no use of the vehicle in Texas other than the immediate transportation of the vehicle out of the state. This certificate should be furnished to the buyer and retained by the seller. The seller must also send a copy to the Comptroller s office and then forward a copy of that correspondence to the purchaser. A copy of the form is available on page 7-7. The address to send the form to is: Texas Comptroller of Public Accounts Business Activity Research Team P. O. Box Austin, Texas b. Texas Motor Vehicle Sales Tax Resale Certificate -For Wholesale Sales. If the vehicle is sold wholesale to another Texas dealer who is purchasing it for resale only, no sales tax is due. Note that a new motor vehicle may be purchased for resale only by a dealer franchised to sell that type of new vehicle, while a used vehicle may be purchased for resale by any dealer holding a GDN. This form is not filed with any government agency. It is retained by the dealer as proof that the transaction qualifies for sales tax exemption. A blanket form of the certificate may be used if multiple sales are anticipated. See form on Page 7-8. Page 7-2

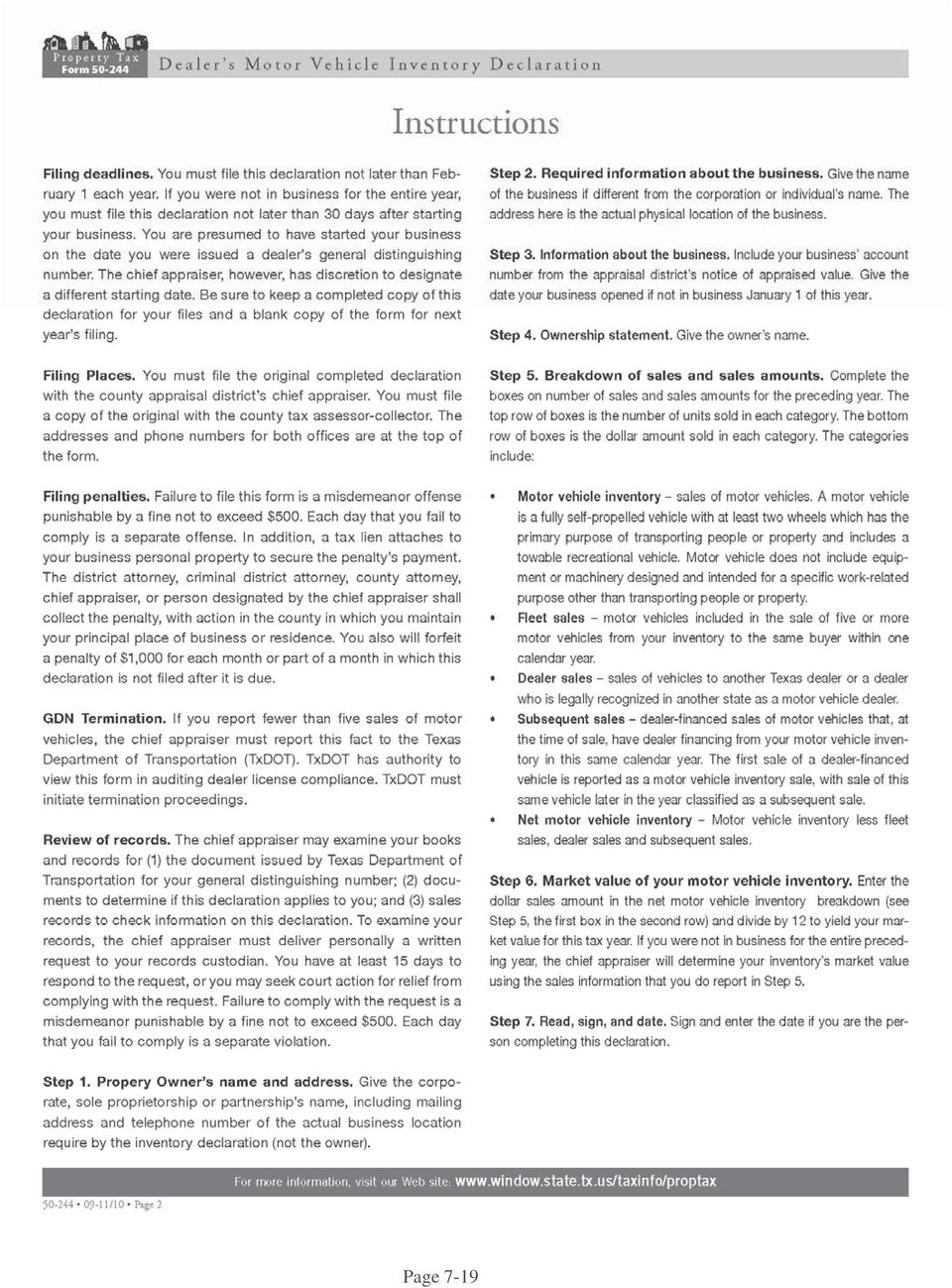

3 c. Orthopedic handicap exemption - A dealer selling a motor vehicle may not collect motor vehicle sales tax from a person claiming the orthopedic handicap exemption. Claim for the exemption must be on Form prescribed by the Comptroller, signed by the purchaser at the time of purchase and provided to the seller. See page 7-9 & 7-10 for a copy of this form. The Comptroller may require additional documentation by rule. The seller who obtains the required certificate is held harmless and has no responsibility to investigate. Other exemptions such as gift and religious organizations are claimed on the title application. 7.5 Motor Vehicle Inventory Taxes. Since 1994, all motor vehicle dealers except those selling trailers and those with wholesale licenses have had to report and pay motor vehicle inventory taxes (VIT). This is a property tax on dealers who were in business on January 1 of a particular year. A Dealer s Motor Vehicle Inventory Declaration (VIT Declaration) form must be filed upon the opening of a dealership and annually thereafter, as detailed below. Dealer s Motor Vehicle Inventory Tax Statements (VIT Statements) detailing the prior month's sales must be filed monthly. a. What to File. 1. Upon Becoming Licensed. In the dealer s first partial calendar year of business, he or she establishes a tax rate. This is done by filing a VIT Declaration with the county chief appraiser and sending a copy to the tax assessor-collector within 30 days of being licensed. The Declaration informs these offices that a new dealership has been established and a file must be started on the dealership. Thereafter, in the first partial calendar year of business, the dealer must complete and file monthly VIT Statements, filing the original with the county tax assessor-collector and a copy with the county appraisal district s chief appraiser. No VIT payments are due on these reports during the first calendar year. The monthly VIT Statements will be used to establish the tax rate for the following year. 2. VIT Declarations. The dealer s obligation to pay VIT payments begins on January 1 of the calendar year after the dealership is established. In January of each year, between January 1 and 31, the dealer must file an annual VIT Declaration, summarizing sales for the preceding calendar year. 3. VIT Statements. Each month in that first full calendar year of business the dealer must file a monthly VIT Statement and pay any VIT payments due. Monthly VIT Statements and annual Declarations are due whether or not any motor vehicles have been sold. A copy of the forms may be found in this Manual on pages 7-19 through b. When to Report. Every licensed motor vehicle dealer in the state of Texas, with the exception of those holding trailer dealer and wholesale licenses, is required to file the Dealer Motor Vehicle Inventory Declaration form, which lists the total value of the dealer s motor Page 7-3

4 vehicle inventory sold during the previous year. This form must be filed with the county appraisal district each year between January 1 and January 31. A copy must also be sent to the county tax assessor-collector s office. New dealers must file a Declaration form within 30 days of opening their business to report their name, address and TxDMV license information. Motor vehicle dealers must also file with the county tax assessor-collector s office the Dealer s Motor Vehicle Inventory Tax Statement, which lists the motor vehicles sold. A copy must also be sent to the county chief appraiser s office. The monthly VIT Statements and any VIT payments due are required to be filed by the 10 th day of each month, reporting the previous month s sales. c. Pay VIT Amounts Due. Multiply the total sales prices of taxable vehicles sold by the tax rate, called the Unit Property Tax Factor on the form, to calculate VIT due. Send the original monthly VIT Statement to your county tax assessor-collector, along with the tax payment. Send a copy of your monthly VIT Statement to your county appraisal district. 7.6 Penalties. a. TxDMV Administrative actions. Dealers who do not file timely annual VIT Declarations or dealers who report the sale of fewer than five vehicles in a calendar year are reported to the TxDMV by the chief appraiser and the tax assessor-collector offices. The law requires TxDMV to initiate termination proceedings against any dealer who fails to file a timely annual VIT Declaration, or who reports selling fewer than five vehicles in a calendar year. Further the tax assessor-collector offices and county appraisal districts may file administrative complaints with DMV for failure to timely file monthly VIT Statements. For failure to file VIT Statements and Declarations and pay VIT, administrative actions can range from warning letters to civil penalties of $500 or more, or license cancellation. Furthermore, dealers who falsify VIT Statements and Declarations are subject to serious penalties for falsification of government records. b. Failure to File a Monthly VIT Statement. In addition to the TxDMV penalties noted above, a dealer who does not file the monthly VIT Statement in a timely manner commits a misdemeanor punishable by a fine up to $100 per day until the VIT Statement is filed. A tax lien attaches to the dealer s business personal property to secure payment of the $100 penalty. A dealer forfeits an additional penalty of $500 for each month or portion of the months that the statement is not filed. Furthermore, a dealer who fails to remit the taxes due pays a 5 percent late fee, with another five percent if not paid within 10 days. c. Failure to File Annual VIT Declaration. In addition to the TxDMV penalties noted above, a dealer who does not file an annual VIT Declaration in a timely manner commits a misdemeanor punishable by a fine up to $500 per day until the VIT Declaration is filed. A tax lien attaches to the dealer s business personal property to secure payment of the penalty. A dealer forfeits an additional penalty of $1000 for each month or portion of month that is not filed. A very good form that explains the VIT procedure is attached to this section as an exhibit Page 7-4

5 starting on page Anyone wishing to download a personal copy can find the form on the Comptroller s website at: Standard Presumptive Value. The Standard Presumptive Value law (SPV) only applies to private-party sales. A private-party sale does not involve a licensed motor vehicle dealer. If a licensed motor vehicle dealer sells the used vehicle, tax is due based on the sales price. The county does not have to check the used vehicle s SPV if the seller is a licensed dealer. The selling dealer s signature on the title application is an acceptable record of the sales price. The county tax assessor-collector, at his or her option, may request the dealer s invoice or sales receipt from any purchaser. a. The law includes all motor vehicles with a few exceptions. The SPV law applies to all types of used motor vehicles. Basically, a motor vehicle is a self-propelled vehicle designed to transport persons or property, or a vehicle designed to carry property while being towed by another vehicle, on the public highways. Off-road vehicles, such as dirt bikes and all-terrain vehicles (ATVs), are not considered motor vehicles for motor vehicle sales tax purposes. They are not subject to the SPV calculation. b. The law excludes some sales transactions. SPV procedures are not used on these types of transactions: Salvage vehicles; Abandoned vehicles; Vehicles sold through storage or mechanic s liens; Vehicles eligible for classic car and classic truck license plates (whether or not the vehicles use those plates); Even trade of vehicles, which has a $5 motor vehicle tax, or The gift of a vehicle, which has a $10 motor vehicle tax; Governmental sales. c. Certified Appraisals by Dealers. A purchaser who pays less than 80 percent of the vehicle s SPV can realize a tax savings if a certified appraisal for the used vehicle reflects a lesser value. For example, a used vehicle may be worth less if it has substantial body damage or needs major mechanical work. The purchaser must present the appraisal to the county on a Comptroller form within 20 county working days from the purchase date or within 20 county working days after bringing the vehicle into Texas. There are two ways to get a certified appraisal: from a motor vehicle dealer licensed for that category of vehicle or from a licensed insurance adjuster. For example, a purchaser can request a car dealer to appraise a car, a motorcycle dealer to appraise a motorcycle or a trailer dealer to appraise a trailer. Dealer fees for appraisals are set by law and Comptroller rules. For most vehicles, a dealer can charge from $100 to no more than $300 for a certified appraisal. A dealer s certified appraisal of a motorcycle can cost from $40 to $300, and a dealer appraisal of a house trailer, travel trailer or a motor home can cost from $100 to $500. Page 7-5

6 The law allows licensed insurance adjusters to determine the fees they charge. Purchasers should realize that an appraisal fee may offset any tax savings. For example, tax on $1,600 of value is $100. In other words, a $100 appraisal must reduce the vehicle s SPV by more than $1,600 to save money. A $300 appraisal fee would require almost a $5,000 reduction in value to offset the appraisal cost. Comptroller Form , Used Motor Vehicle Certified Appraisal Form, is available on Window on State Government at Select Texas Taxes. The Comptroller s office provides this form to licensed motor vehicle dealers and insurance adjusters. A copy of this form in on page 7-11 and further instructions are on the back of the form which appear on page Gift tax. Effective September 1, 2009, transactions that qualify to be taxed as a gift ($10) are limited to those transactions where the vehicle is given to, or accepted from, a: parent or stepparent; grandparent or grandchild; child or stepchild; sibling; guardian; or Decedent s estate. A vehicle also qualifies to be taxed as a gift when it is donated to, or given by, a 501 (c)(3) nonprofit service organization. Otherwise, transactions without consideration are a sale and will be subject to tax calculated on the vehicle's standard presumptive value (industry book value). To document a gift, the donor and person receiving the vehicle must complete a joint notarized affidavit of fact describing the transaction and the relationship between the parties. Page 7-6

7 Page 7-7

8 Page 7-8

9 Page 7-9

10 Page 7-10

11 Page 7-11

12 Page 7-12

13 Page 7-13

14 Page 7-14

15 Page 7-15

16 Page 7-16

17 Page 7-17

18 Page 7-18

19 Page 7-19

20 Page 7-20

21 Page 7-21

22 Page 7-22

Motor Vehicle Sales, Use and Rental Tax

Motor Vehicle Sales, Use and Rental Tax Susan Combs, Texas Comptroller of Public Accounts March 2009 A 6.25 percent sales tax is imposed on the retail sales price (less trade-in allowance) of motor vehicles

Motor Vehicle Sales, Use and Rental Tax Susan Combs, Texas Comptroller of Public Accounts March 2009 A 6.25 percent sales tax is imposed on the retail sales price (less trade-in allowance) of motor vehicles

Title Ad Valorem Tax. O.C.G.A. Section 48-5C-1. Created by HB 386 (2012 Session) and Amended by HB 266 and HB 463 (2013 Session)

and Amended by HB 266 and HB 463 (2013 Session)") Title Ad Valorem Tax O.C.G.A. Section 48-5C-1 Created by HB 386 (2012 Session) and Amended by HB 266 and HB 463 (2013 Session) Tax reform legislation (HB 386) passed by the General Assembly in 2012 and

Title Ad Valorem Tax O.C.G.A. Section 48-5C-1 Created by HB 386 (2012 Session) and Amended by HB 266 and HB 463 (2013 Session) Tax reform legislation (HB 386) passed by the General Assembly in 2012 and

Heavy Equipment Dealers Special Inventory

Susan Combs Texas Comptroller of Public Accounts Heavy Equipment Dealers Special Inventory Instructions for Filing Forms and Paying Property Taxes January 2014 By publishing this manual, the Texas Comptroller

Susan Combs Texas Comptroller of Public Accounts Heavy Equipment Dealers Special Inventory Instructions for Filing Forms and Paying Property Taxes January 2014 By publishing this manual, the Texas Comptroller

Military Packet to Title and Register Your Vehicle

Military Packet to Title and Register Your Vehicle To transfer your vehicle to Texas follow the steps outlined below. Forms and instructions to follow: Step 1. Complete an enclosed VIN Self-Certification

Military Packet to Title and Register Your Vehicle To transfer your vehicle to Texas follow the steps outlined below. Forms and instructions to follow: Step 1. Complete an enclosed VIN Self-Certification

Title Office Reference Guides Setup

Title Office Reference Guides Setup For your convenience, we have inserted two methods of navigation for your use while referring to this resource: First We have inserted Adobe Reader Bookmarks. Click

Title Office Reference Guides Setup For your convenience, we have inserted two methods of navigation for your use while referring to this resource: First We have inserted Adobe Reader Bookmarks. Click

Ministry Of Finance VAT Department. VAT Guidance for on the Treatment of Motor Vehicles Version 4: November 1, 2015

Ministry Of Finance VAT Department VAT Guidance for on the Treatment of Motor Vehicles Version 4: November 1, 2015 Introduction This guide is intended to provide those selling or hiring vehicles by way

Ministry Of Finance VAT Department VAT Guidance for on the Treatment of Motor Vehicles Version 4: November 1, 2015 Introduction This guide is intended to provide those selling or hiring vehicles by way

Exempt Organizations: Sales and Purchases

Exempt Organizations: Sales and Purchases Susan Combs, Texas Comptroller of Public Accounts DECEMBER 2010 Organizations that have applied for and received a letter of exemption from sales tax don t have

Exempt Organizations: Sales and Purchases Susan Combs, Texas Comptroller of Public Accounts DECEMBER 2010 Organizations that have applied for and received a letter of exemption from sales tax don t have

The Connecticut Department of Motor Vehicles not the town.

WHAT IF MY VEHICLE WAS... SOLD? TOTALED? REGISTERED OUT OF STATE? STOLEN? TAXED IN WRONG TOWN? REPOSSESSED? DONATED? ASSESSMENT OFFICE Town Of Simsbury PO Box 495 Simsbury CT 06070 Office Hours 8:30 7:00

WHAT IF MY VEHICLE WAS... SOLD? TOTALED? REGISTERED OUT OF STATE? STOLEN? TAXED IN WRONG TOWN? REPOSSESSED? DONATED? ASSESSMENT OFFICE Town Of Simsbury PO Box 495 Simsbury CT 06070 Office Hours 8:30 7:00

VEHICLE DONATION PACKET

VEHICLE DONATION PACKET THANK YOU for donating your unwanted vehicle to Goodwill Central Texas. Your generous contribution will EMPOWER 100,000 CENTRAL TEXANS TO WORK! Please review the following instructions

VEHICLE DONATION PACKET THANK YOU for donating your unwanted vehicle to Goodwill Central Texas. Your generous contribution will EMPOWER 100,000 CENTRAL TEXANS TO WORK! Please review the following instructions

Motor Vehicle Sales and Purchases

www.revenue.state.mn.us Motor Vehicle Sales and Purchases 125 Sales Tax Fact Sheet What s New in 2013 Starting July 1, 2013: The tax on collector passenger vehicles and fire trucks is $150. The gift of

www.revenue.state.mn.us Motor Vehicle Sales and Purchases 125 Sales Tax Fact Sheet What s New in 2013 Starting July 1, 2013: The tax on collector passenger vehicles and fire trucks is $150. The gift of

Avoiding the 9 most common dealer violations. TIADA ANNUAL CONFERENCE August 11, 2015 San Antonio, Texas

Avoiding the 9 most common dealer violations TIADA ANNUAL CONFERENCE August 11, 2015 San Antonio, Texas Most Common Dealer Violations #1 Failure to Timely Transfer Title Texas Trans Code 501.0234 #2 Selling

Avoiding the 9 most common dealer violations TIADA ANNUAL CONFERENCE August 11, 2015 San Antonio, Texas Most Common Dealer Violations #1 Failure to Timely Transfer Title Texas Trans Code 501.0234 #2 Selling

How To Get A Title In Keso

Service Description Filing Fees Corrected or Updated KY Title Duplicate KY Title The following documents are required: Application for title/registration must be completed in the following sections: o

Service Description Filing Fees Corrected or Updated KY Title Duplicate KY Title The following documents are required: Application for title/registration must be completed in the following sections: o

MARYELLEN O SHAUGHNESSY

AUTO TITLE MANUAL Prepared and issued as a public service by the office of MARYELLEN O SHAUGHNESSY Franklin County Clerk of Courts revised 2/14 CLERK OF THE COURT OF COMMON PLEAS AUTO TITLE DIVISION MARYELLEN

AUTO TITLE MANUAL Prepared and issued as a public service by the office of MARYELLEN O SHAUGHNESSY Franklin County Clerk of Courts revised 2/14 CLERK OF THE COURT OF COMMON PLEAS AUTO TITLE DIVISION MARYELLEN

State of Colorado Motor Vehicle Dealer Board

State of Colorado Motor Vehicle Dealer Board Dealer - Wholesaler - Salesperson - Auction Dealer Mastery Examination Official Form Please Print Legibly Applicant Information - - First Name M.I. Last Name

State of Colorado Motor Vehicle Dealer Board Dealer - Wholesaler - Salesperson - Auction Dealer Mastery Examination Official Form Please Print Legibly Applicant Information - - First Name M.I. Last Name

OFF-ROAD VEHICLE AND BOAT DEALERS

BULLETIN NO. 013 Issued March 2003 Revised July 2013 THE RETAIL SALES TAX ACT OFF-ROAD VEHICLE AND BOAT DEALERS This bulletin provides information to help off-road vehicle and boat dealers apply the Retail

BULLETIN NO. 013 Issued March 2003 Revised July 2013 THE RETAIL SALES TAX ACT OFF-ROAD VEHICLE AND BOAT DEALERS This bulletin provides information to help off-road vehicle and boat dealers apply the Retail

PRIVATELY PURCHASED VEHICLES

BULLETIN NO. 054 Issued June 2010 Revised June 2015 THE RETAIL SALES TAX ACT PRIVATELY PURCHASED VEHICLES This bulletin provides information regarding the Retail Sales Tax (RST) application on privately

BULLETIN NO. 054 Issued June 2010 Revised June 2015 THE RETAIL SALES TAX ACT PRIVATELY PURCHASED VEHICLES This bulletin provides information regarding the Retail Sales Tax (RST) application on privately

APPLICATIONS APPLICATIONS TYPES VEHICLE TYPES

APPLICATIONS When a Title is Required... 4 Transferring Ownership... 6 Application Required within 60 Days of Date of Purchase... 8 Applying for Original Title Supporting Documents Required... 9 Making

APPLICATIONS When a Title is Required... 4 Transferring Ownership... 6 Application Required within 60 Days of Date of Purchase... 8 Applying for Original Title Supporting Documents Required... 9 Making

Chapter 8: Sales Tax Page 1

Chapter 8: Sales Tax Page 1 Chapter 8 Sales Tax Section 8-1 Requirement 8-1.1 Authorization. Section 205.52 of the General Sales Tax Act (MCL 205.52) authorizes the collection of sales tax on the purchase

Chapter 8: Sales Tax Page 1 Chapter 8 Sales Tax Section 8-1 Requirement 8-1.1 Authorization. Section 205.52 of the General Sales Tax Act (MCL 205.52) authorizes the collection of sales tax on the purchase

Dealer License Renewal Home Study Study Guide

Dealer License Renewal Home Study Study Guide Please remember if you paid for this course by credit card: LEGAL DISCLAIMER @ View this Disclaimer Online: http://www.gotplates.com/disclaimer.html Standard

Dealer License Renewal Home Study Study Guide Please remember if you paid for this course by credit card: LEGAL DISCLAIMER @ View this Disclaimer Online: http://www.gotplates.com/disclaimer.html Standard

What You Need to Do. What Happens Next

Dear Prospective Car Donor, Thank you for your interest in donating your vehicle to Wheels of Hope, a ministry whose primary focus is to provide affordable cars to those who need them most. How the Ministry

Dear Prospective Car Donor, Thank you for your interest in donating your vehicle to Wheels of Hope, a ministry whose primary focus is to provide affordable cars to those who need them most. How the Ministry

Salvage Dealer and Motor Vehicle Information

Salvage Dealer and Motor Vehicle Information TxDMV July 2011 We welcome your feedback! Send your comments to the following e-mail address: VTR_Title&[email protected] In the e-mail subject

Salvage Dealer and Motor Vehicle Information TxDMV July 2011 We welcome your feedback! Send your comments to the following e-mail address: VTR_Title&[email protected] In the e-mail subject

Motor Vehicle. Transfer Guide

Minnesota Department of Public Safety Driver and Vehicle Services 445 Minnesota Street Saint Paul, Minnesota 55101 Motor Vehicle General Information for Dealers Transfer Guide November 2012 TABLE OF CONTENTS

Minnesota Department of Public Safety Driver and Vehicle Services 445 Minnesota Street Saint Paul, Minnesota 55101 Motor Vehicle General Information for Dealers Transfer Guide November 2012 TABLE OF CONTENTS

The TxDMV s Role in Transportation Funding

The TxDMV s Role in Transportation Funding Testimony before the House Select Committee on Transportation Funding, Expenditures & Finance Jeremiah Kuntz Director, Government & Strategic Communications Texas

The TxDMV s Role in Transportation Funding Testimony before the House Select Committee on Transportation Funding, Expenditures & Finance Jeremiah Kuntz Director, Government & Strategic Communications Texas

Tax Commission. #14 motor vehicles. (Selling, Leasing & Renting) An Educational Guide to Sales Tax in the State of Idaho

An Educational Guide to Sales Tax in the State of Idaho") Tax Commission Idaho #14 motor vehicles (Selling, Leasing & Renting) An Educational Guide to Sales Tax in the State of Idaho This brochure is intended to help motor vehicle dealers, leasing companies,

Tax Commission Idaho #14 motor vehicles (Selling, Leasing & Renting) An Educational Guide to Sales Tax in the State of Idaho This brochure is intended to help motor vehicle dealers, leasing companies,

Florida Department of Highway Safety and Motor Vehicles Division of Motorist Services

PROCEDURE Florida Department of Highway Safety and Motor Vehicles DESCRIPTION AND USE: THIS PROCEDURE PROVIDES INFORMATION AND INSTRUCTIONS TO ASSIST TAX COLLECTOR EMPLOYEES, LICENSE PLATE AGENCY EMPLOYEES,

PROCEDURE Florida Department of Highway Safety and Motor Vehicles DESCRIPTION AND USE: THIS PROCEDURE PROVIDES INFORMATION AND INSTRUCTIONS TO ASSIST TAX COLLECTOR EMPLOYEES, LICENSE PLATE AGENCY EMPLOYEES,

General Instructions

Who must file Form RUT-50? You must file Form RUT-50, Private Party Vehicle Use Tax Transaction, if you purchased or acquired by gift or transfer a motor vehicle from a private party. If you purchased

Who must file Form RUT-50? You must file Form RUT-50, Private Party Vehicle Use Tax Transaction, if you purchased or acquired by gift or transfer a motor vehicle from a private party. If you purchased

Motor Vehicle Rental Tax Guidebook

Motor Vehicle Rental Tax Guidebook 2008 Susan Combs Texas Comptroller of Public Accounts Table of Contents Introduction 1 Definitions 2 Bad debt 2 Fair market value 2 Fair market value deduction 2 Farm

Motor Vehicle Rental Tax Guidebook 2008 Susan Combs Texas Comptroller of Public Accounts Table of Contents Introduction 1 Definitions 2 Bad debt 2 Fair market value 2 Fair market value deduction 2 Farm

MOTOR VEHICLE DEALER SALESPERSON STUDY GUIDE MATERIALS

MOTOR VEHICLE DEALER SALESPERSON STUDY GUIDE MATERIALS 2201 West Broad Street, Suite 104 Richmond, Virginia 23220 804-367-1100 www.mvdb.virginia.gov MVDB 35 REVISED 07/01/15 INTRODUCTION This study guide

MOTOR VEHICLE DEALER SALESPERSON STUDY GUIDE MATERIALS 2201 West Broad Street, Suite 104 Richmond, Virginia 23220 804-367-1100 www.mvdb.virginia.gov MVDB 35 REVISED 07/01/15 INTRODUCTION This study guide

Buying and Selling a Used Vehicle in Ontario

Buying and Selling a Used Vehicle in Ontario All information is available and taken from http://www.mto.gov.on.ca/english/dandv/vehicle/used.shtml By Ontario law, private sellers of most motor vehicles,

Buying and Selling a Used Vehicle in Ontario All information is available and taken from http://www.mto.gov.on.ca/english/dandv/vehicle/used.shtml By Ontario law, private sellers of most motor vehicles,

CHAPTER 4. COMPLIANCE & DEALER OPERATIONS

CHAPTER 4. COMPLIANCE & DEALER OPERATIONS 4.1 Codes and Rules. Codes are statutes or laws and are known as black letter law. Any changes to the codes require action by the Texas Legislature which meets

CHAPTER 4. COMPLIANCE & DEALER OPERATIONS 4.1 Codes and Rules. Codes are statutes or laws and are known as black letter law. Any changes to the codes require action by the Texas Legislature which meets

TITLE, REGISTRATION, AND SALES TAX SALES TAX SECTION UPDATES

TITLE, REGISTRATION, AND SALES TAX ADMINISTRATIVE MANUAL SALES TAX SECTION UPDATES Updated December 2009 Web Version SALES TAX SECTION: TABLE OF CONTENTS PAGE GENERAL INFORMATION ABOUT COLORADO STATE TAXES

TITLE, REGISTRATION, AND SALES TAX ADMINISTRATIVE MANUAL SALES TAX SECTION UPDATES Updated December 2009 Web Version SALES TAX SECTION: TABLE OF CONTENTS PAGE GENERAL INFORMATION ABOUT COLORADO STATE TAXES

VERMONT TITLE & TAX APPLICATION

VERMONT TITLE & TAX APPLICATION THIS IS NOT AN APPLICATION FOR REGISTRATION IF YOU WISH TO REGISTER YOUR VEHICLE, YOU MUST COMPLETE A VERMONT REGISTRATION, TAX & TITLE APPLICATION, TA-VD-119 Bennington

VERMONT TITLE & TAX APPLICATION THIS IS NOT AN APPLICATION FOR REGISTRATION IF YOU WISH TO REGISTER YOUR VEHICLE, YOU MUST COMPLETE A VERMONT REGISTRATION, TAX & TITLE APPLICATION, TA-VD-119 Bennington

South Carolina Department of Motor Vehicles

South Carolina Department of Motor Vehicles Form 400 Application for Certificate of Title and Registration for Motor Vehicle or Manufactured Home/Mobile Home SECTION A EXPEDITE (additional $20.00 fee)

South Carolina Department of Motor Vehicles Form 400 Application for Certificate of Title and Registration for Motor Vehicle or Manufactured Home/Mobile Home SECTION A EXPEDITE (additional $20.00 fee)

SALES AND USE TAX GUIDE FOR AUTOMOBILE AND TRUCK DEALERS

SALES AND USE TAX GUIDE FOR AUTOMOBILE AND TRUCK DEALERS 2016 EDITION (THROUGH THE 2015 SESSION OF THE GENERAL ASSEMBLY) SOUTH CAROLINA DEPARTMENT OF REVENUE OFFICE OF GENERAL COUNSEL/POLICY SECTION Nikki

SALES AND USE TAX GUIDE FOR AUTOMOBILE AND TRUCK DEALERS 2016 EDITION (THROUGH THE 2015 SESSION OF THE GENERAL ASSEMBLY) SOUTH CAROLINA DEPARTMENT OF REVENUE OFFICE OF GENERAL COUNSEL/POLICY SECTION Nikki

GEORGIA DEPARTMENT OF REVENUE TAX GUIDE

GEORGIA DEPARTMENT OF REVENUE TAX GUIDE FOR MOTOR VEHICLE DEALERS Department of Revenue - Motor Vehicle Division 4125 Welcome All Road Atlanta, Georgia 30349 Revised: January 31, 2013 EDITOR S NOTE The

GEORGIA DEPARTMENT OF REVENUE TAX GUIDE FOR MOTOR VEHICLE DEALERS Department of Revenue - Motor Vehicle Division 4125 Welcome All Road Atlanta, Georgia 30349 Revised: January 31, 2013 EDITOR S NOTE The

A BILL FOR AN ACT ENTITLED: "AN ACT GENERALLY REVISING MOTOR VEHICLE LAWS RELATED TO

SB0.0 SENATE BILL NO. INTRODUCED BY SONJU, ARNTZEN, HOLLENBAUGH, LAVIN A BILL FOR AN ACT ENTITLED: "AN ACT GENERALLY REVISING MOTOR VEHICLE LAWS RELATED TO THE USE OF AUTHORIZED AGENTS IN THE PROCESSING

SB0.0 SENATE BILL NO. INTRODUCED BY SONJU, ARNTZEN, HOLLENBAUGH, LAVIN A BILL FOR AN ACT ENTITLED: "AN ACT GENERALLY REVISING MOTOR VEHICLE LAWS RELATED TO THE USE OF AUTHORIZED AGENTS IN THE PROCESSING

PLEASE NOTE: Why was my vehicle impounded?

Ready to Protect, Proud to Serve Tucson Police Department 1310 W. Miracle Mile Tucson, AZ 85705 (520) 791-4285 Updated August 14, 2015 If your vehicle was impounded by an officer of the Tucson Police Department

Ready to Protect, Proud to Serve Tucson Police Department 1310 W. Miracle Mile Tucson, AZ 85705 (520) 791-4285 Updated August 14, 2015 If your vehicle was impounded by an officer of the Tucson Police Department

SALVAGE/NONREPAIRABLE MOTOR VEHICLE MANUAL

SALVAGE/NONREPAIRABLE MOTOR VEHICLE MANUAL TxDMV April 2014 We welcome your feedback! Send your comments and recommendations to the following e-mail address: [email protected] In the

SALVAGE/NONREPAIRABLE MOTOR VEHICLE MANUAL TxDMV April 2014 We welcome your feedback! Send your comments and recommendations to the following e-mail address: [email protected] In the

NUC-1 Illinois Business Registration

Illinois Department of Revenue NUC-1 Illinois Business Registration Read this information first You must read the instructions before completing this form. Be sure to complete all of the information that

Illinois Department of Revenue NUC-1 Illinois Business Registration Read this information first You must read the instructions before completing this form. Be sure to complete all of the information that

TAX COMPARISON 2014-2015

TAX COMPARISON 01-015 Between Caroline City of Fredericksburg King George Stafford Prepared by of Spotsylvania Department of Economic Development & Tourism 9019 Old Battlefield Boulevard, Suite 10 Spotsylvania,

TAX COMPARISON 01-015 Between Caroline City of Fredericksburg King George Stafford Prepared by of Spotsylvania Department of Economic Development & Tourism 9019 Old Battlefield Boulevard, Suite 10 Spotsylvania,

GEORGIA LEMON LAW SUMMARY

EXECUTIVE SUMMARY TIME PERIOD FOR FILING CLAIMS Although the lemon law does not provide a statute of limitations, a claim must allege at least one of the following: 1. A serious safety defect in the braking

EXECUTIVE SUMMARY TIME PERIOD FOR FILING CLAIMS Although the lemon law does not provide a statute of limitations, a claim must allege at least one of the following: 1. A serious safety defect in the braking

DEALER PROCEDURES MANUAL

STATE OF DELAWARE DIVISION OF MOTOR VEHICLES DEALER PROCEDURES MANUAL Revised September, 2015 1 Table of Contents Facilities... 4 Introduction... 4 Definitions... 5 Dealer Classifications... 6 Dealer Licensing

STATE OF DELAWARE DIVISION OF MOTOR VEHICLES DEALER PROCEDURES MANUAL Revised September, 2015 1 Table of Contents Facilities... 4 Introduction... 4 Definitions... 5 Dealer Classifications... 6 Dealer Licensing

How To Get A Car Title In Michigan

Chapter 3: Title and Registration Requirements Page 1 Chapter 3 Title and Registration Requirements Section 3-1 Titles 3-1.1 Authority. Section 235 of the Michigan Vehicle Code (MCL 257.235) requires a

Chapter 3: Title and Registration Requirements Page 1 Chapter 3 Title and Registration Requirements Section 3-1 Titles 3-1.1 Authority. Section 235 of the Michigan Vehicle Code (MCL 257.235) requires a

Figure: 7 TAC 84.809(b)

") Figure: 7 TAC 84.809(b) MOTOR VEHICLE RETAIL INSTALLMENT SALES CONTRACT (Optional: DATE ) BUYER SELLER/CREDITOR ADDRESS ADDRESS CITY STATE ZIP CITY STATE ZIP PHONE PHONE The Buyer is referred to as "I"

Figure: 7 TAC 84.809(b) MOTOR VEHICLE RETAIL INSTALLMENT SALES CONTRACT (Optional: DATE ) BUYER SELLER/CREDITOR ADDRESS ADDRESS CITY STATE ZIP CITY STATE ZIP PHONE PHONE The Buyer is referred to as "I"

Vehicle for Vets Program

Vehicle for Vets Program Serving Veterans and Their Families Across America 69 Grove Street, Worcester, MA 01605 Tel: (508) 791-1213 Fax: (508) 791-5296 (800) 482-2565 www.veteransinc.org Vehicles for

Vehicle for Vets Program Serving Veterans and Their Families Across America 69 Grove Street, Worcester, MA 01605 Tel: (508) 791-1213 Fax: (508) 791-5296 (800) 482-2565 www.veteransinc.org Vehicles for

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 1991 S 3. SENATE BILL 111 Finance Committee Substitute Adopted 4/22/91 Third Edition Engrossed 4/25/91

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION S SENATE BILL Finance Committee Substitute Adopted // Third Edition Engrossed // Short Title: Highway Use Tax Reductions. Sponsors: Referred to: (Public) February,

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION S SENATE BILL Finance Committee Substitute Adopted // Third Edition Engrossed // Short Title: Highway Use Tax Reductions. Sponsors: Referred to: (Public) February,

LAWS GOVERNING AUTO INDUSTRY

Automobile LAWS GOVERNING AUTO INDUSTRY Two of the main chapters of the Nevada Revised Statutes and Nevada Administrative Code discussed today are: Chapter 372: Sales and Use Taxes Chapter 482: Motor Vehicles

Automobile LAWS GOVERNING AUTO INDUSTRY Two of the main chapters of the Nevada Revised Statutes and Nevada Administrative Code discussed today are: Chapter 372: Sales and Use Taxes Chapter 482: Motor Vehicles

County Clerks Sales and Use Tax Guide for Automobile and Boat Transfers

County Clerks Sales and Use Tax Guide for Automobile and Boat Transfers August 2015 Dear County Clerks, This sales and use tax guide is intended as an informal reference for clerks who wish to gain a better

County Clerks Sales and Use Tax Guide for Automobile and Boat Transfers August 2015 Dear County Clerks, This sales and use tax guide is intended as an informal reference for clerks who wish to gain a better

CONSUMERS BE CAUTIOUS WHEN PURCHASING A MOTOR VEHICLE

SCOFFLAW NOTICE Effective October 1, 2010 the Cameron County Tax Assessor-Collector Motor Vehicle Division will deny the vehicle registration renewal of individuals who have outstanding traffic fines due

SCOFFLAW NOTICE Effective October 1, 2010 the Cameron County Tax Assessor-Collector Motor Vehicle Division will deny the vehicle registration renewal of individuals who have outstanding traffic fines due

The State Board of Equalization Welcomes You to the Basic Sales and Use Tax Seminar

The State Board of Equalization Welcomes You to the Basic Sales and Use Tax Seminar Welcome to the California State Board of Equalization s presentation on Basic Sales and Use Tax. 1 About This Presentation

The State Board of Equalization Welcomes You to the Basic Sales and Use Tax Seminar Welcome to the California State Board of Equalization s presentation on Basic Sales and Use Tax. 1 About This Presentation

MOTOR VEHICLE DEALER MANUAL 2014 EDITION

MOTOR VEHICLE DEALER MANUAL 2014 EDITION V1.0 PUBLISHED BY THE ENFORCEMENT DIVISION OF Copyright 2014 Texas Department of Motor Vehicles INTRODUCTION The purpose of this manual is to provide prospective

MOTOR VEHICLE DEALER MANUAL 2014 EDITION V1.0 PUBLISHED BY THE ENFORCEMENT DIVISION OF Copyright 2014 Texas Department of Motor Vehicles INTRODUCTION The purpose of this manual is to provide prospective

MISSISSIPPI LEGISLATURE REGULAR SESSION 2015

MISSISSIPPI LEGISLATURE REGULAR SESSION 2015 By: Representative Sullivan To: Ways and Means HOUSE BILL NO. 1000 (As Sent to Governor) 1 AN ACT TO AMEND SECTION 63-21-13, MISSISSIPPI CODE OF 1972, 2 TO

MISSISSIPPI LEGISLATURE REGULAR SESSION 2015 By: Representative Sullivan To: Ways and Means HOUSE BILL NO. 1000 (As Sent to Governor) 1 AN ACT TO AMEND SECTION 63-21-13, MISSISSIPPI CODE OF 1972, 2 TO

Filing Claims for Refund of Sales or Use Tax

State of Wisconsin Department of Revenue Important Change The football stadium district tax in Brown County ends on September 30, 2015. Filing Claims for Refund of Sales or Use Tax Includes information

State of Wisconsin Department of Revenue Important Change The football stadium district tax in Brown County ends on September 30, 2015. Filing Claims for Refund of Sales or Use Tax Includes information

INSURANCE LAWS OBJECTIVES FOR CLASS WHAT IS REQUIRED?

INSURANCE LAWS Frederick P. Garcia, Jr. Municipal Court Clerk City of San Antonio OBJECTIVES FOR CLASS Identify Statutory Authority Requirements for Establishment of Financial Responsibility ; Apply Coverage

INSURANCE LAWS Frederick P. Garcia, Jr. Municipal Court Clerk City of San Antonio OBJECTIVES FOR CLASS Identify Statutory Authority Requirements for Establishment of Financial Responsibility ; Apply Coverage

Dallas Central Appraisal District Frequently Asked Questions Business Personal Property (BPP)

") 1. How can I change my mailing address? Can you change my mailing address by phone? Please send us something in writing (or email us at [email protected]) indicating the correct mailing address for your property,

1. How can I change my mailing address? Can you change my mailing address by phone? Please send us something in writing (or email us at [email protected]) indicating the correct mailing address for your property,

Chapter 822. Regulation of Vehicle Related Businesses 2013 EDITION. Title 59 Page 461 (2013 Edition)

") Chapter 822 2013 EDITION Regulation of Vehicle Related Businesses VEHICLE DEALERS (Generally) 822.005 Acting as vehicle dealer without certificate; penalty 822.007 Injunction against person acting as vehicle

Chapter 822 2013 EDITION Regulation of Vehicle Related Businesses VEHICLE DEALERS (Generally) 822.005 Acting as vehicle dealer without certificate; penalty 822.007 Injunction against person acting as vehicle

Florida Department of Revenue. Motor Vehicle Dealer Standard Industry Guide

Florida Department of Revenue Standard Industry Guide PURPOSE This guide provides an auditor with information on the subject industry. This information will assist an auditor in recognizing areas to test

Florida Department of Revenue Standard Industry Guide PURPOSE This guide provides an auditor with information on the subject industry. This information will assist an auditor in recognizing areas to test

CHAPTER 3. LICENSING

CHAPTER 3. LICENSING 3.1 Who must be licensed. Any person who is engaged in the business of buying, selling or exchanging motor vehicles or otherwise engaging in business as a dealer, directly or indirectly,

CHAPTER 3. LICENSING 3.1 Who must be licensed. Any person who is engaged in the business of buying, selling or exchanging motor vehicles or otherwise engaging in business as a dealer, directly or indirectly,

New Cars Buying from a Licensed Dealer New Vehicle Warranty Florida s New Car Lemon Law

Buying a car is one of the most important and most expensive decisions most of us have to make. There is certainly no shortage of vehicles available, but buyers must know what to look for, what to ask

Buying a car is one of the most important and most expensive decisions most of us have to make. There is certainly no shortage of vehicles available, but buyers must know what to look for, what to ask

Comptroller of Public Accounts. Exempt Organizations, Texas Sales Tax and Fundraisers

Comptroller of Public Accounts Exempt Organizations, Texas Sales Tax and Fundraisers Sales Tax Nonprofit that sells taxable goods or services must obtain a sales tax permit and collect and remit the sales

Comptroller of Public Accounts Exempt Organizations, Texas Sales Tax and Fundraisers Sales Tax Nonprofit that sells taxable goods or services must obtain a sales tax permit and collect and remit the sales

Vehicle Title and Registration

Vehicle Title and Registration Motor Vehicle Division Vehicle Title and Registration Boats, Personal Watercraft and Motorized Pontoons Commercial & Heavy Vehicles Light Vehicles (cars, vans, pickups &

Vehicle Title and Registration Motor Vehicle Division Vehicle Title and Registration Boats, Personal Watercraft and Motorized Pontoons Commercial & Heavy Vehicles Light Vehicles (cars, vans, pickups &

FACT SHEET. Buying or Selling Your Vehicle in Pennsylvania

FACT SHEET Buying or Selling Your Vehicle in Pennsylvania PURPOSE The purpose of this fact sheet is to inform Pennsylvania residents of the proper procedures when buying or selling a vehicle in Pennsylvania

FACT SHEET Buying or Selling Your Vehicle in Pennsylvania PURPOSE The purpose of this fact sheet is to inform Pennsylvania residents of the proper procedures when buying or selling a vehicle in Pennsylvania

DEPARTMENT OF REVENUE. Division of Motor Vehicles Title and Registration Sections

DEPARTMENT OF REVENUE Division of Motor Vehicles Title and Registration Sections 1 CCR 204-10 Rule 48. COLORADO DEALER LICENSE PLATES Basis: The statutory bases for this regulation are sections 42-1-102(22),

DEPARTMENT OF REVENUE Division of Motor Vehicles Title and Registration Sections 1 CCR 204-10 Rule 48. COLORADO DEALER LICENSE PLATES Basis: The statutory bases for this regulation are sections 42-1-102(22),

Sales Tax On Dealer Owned Vehicles

Sales Tax On Dealer Owned Vehicles Minnesota Sales Tax Is A Retail Tax. In order to avoid multiple taxes, Minnesota law imposes sales tax once at the retail level. Sales tax is not due on wholesale transfers.

Sales Tax On Dealer Owned Vehicles Minnesota Sales Tax Is A Retail Tax. In order to avoid multiple taxes, Minnesota law imposes sales tax once at the retail level. Sales tax is not due on wholesale transfers.

- If I sell my house during the year, who gets the tax ticket and who is responsible for the taxes?

Real Estate Taxes - What is the Real Estate tax rate for Wythe County? - If I sell my house during the year, who gets the tax ticket and who is responsible for the taxes? - How and when will I be assessed

Real Estate Taxes - What is the Real Estate tax rate for Wythe County? - If I sell my house during the year, who gets the tax ticket and who is responsible for the taxes? - How and when will I be assessed

INFORMATION BULLETIN #28S SALES TAX APRIL 2012. (Replaces Information Bulletin #28S dated October 2011)

") INFORMATION BULLETIN #28S SALES TAX APRIL 2012 (Replaces Information Bulletin #28S dated October 2011) DISCLAIMER: SUBJECT: EFFECTIVE: Information bulletins are intended to provide nontechnical assistance

INFORMATION BULLETIN #28S SALES TAX APRIL 2012 (Replaces Information Bulletin #28S dated October 2011) DISCLAIMER: SUBJECT: EFFECTIVE: Information bulletins are intended to provide nontechnical assistance

MASSACHUSETTS LEMON LAW SUMMARY

EXECUTIVE SUMMARY TIME PERIOD FOR FILING CLAIMS ELIGIBLE VEHICLE 18 months from the date of the motor vehicle s original delivery to the consumer. Motor vehicles and motorcycles sold, leased, or replaced

EXECUTIVE SUMMARY TIME PERIOD FOR FILING CLAIMS ELIGIBLE VEHICLE 18 months from the date of the motor vehicle s original delivery to the consumer. Motor vehicles and motorcycles sold, leased, or replaced

GEORGIA DEPARTMENT OF REVENUE TAX GUIDE

GEORGIA DEPARTMENT OF REVENUE TAX GUIDE FOR MOTOR VEHICLE DEALERS Department of Revenue - Motor Vehicle Division 4125 Welcome All Road Atlanta, Georgia 30349 Revised: June 14, 2013 EDITOR S NOTE The purpose

GEORGIA DEPARTMENT OF REVENUE TAX GUIDE FOR MOTOR VEHICLE DEALERS Department of Revenue - Motor Vehicle Division 4125 Welcome All Road Atlanta, Georgia 30349 Revised: June 14, 2013 EDITOR S NOTE The purpose

Business tax tip #4 If You Make Purchases for Resale

Business tax tip #4 If You Make Purchases for Resale If you're a buyer... Does my sales and use tax license entitle me to make purchases without paying sales and use tax? No. Contrary to what many people

Business tax tip #4 If You Make Purchases for Resale If you're a buyer... Does my sales and use tax license entitle me to make purchases without paying sales and use tax? No. Contrary to what many people

STATE OF OKLAHOMA MANUFACTURED HOME QUICK REFERENCE GUIDE

STATE OF OKLAHOMA MANUFACTURED HOME QUICK REFERENCE GUIDE PUBLICATION NUMBER 10-05-MH-01 OKLAHOMA TAX COMMISSION AD VALOREM DIVISION August, 2010 TABLE OF CONTENTS Location of VIN Numbers...i New Manufactured

STATE OF OKLAHOMA MANUFACTURED HOME QUICK REFERENCE GUIDE PUBLICATION NUMBER 10-05-MH-01 OKLAHOMA TAX COMMISSION AD VALOREM DIVISION August, 2010 TABLE OF CONTENTS Location of VIN Numbers...i New Manufactured

STATE OF MAINE RULES RELATING TO THE SALE AND DELIVERY OF TOBACCO PRODUCTS IN MAINE

10-144 STATE OF MAINE RULES RELATING TO THE SALE AND DELIVERY OF TOBACCO PRODUCTS IN MAINE Chapter 203 DEPARTMENT OF HEALTH AND HUMAN SERVICES MAINE CENTER FOR DISEASE CONTROL AND PREVENTION DIVISION OF

10-144 STATE OF MAINE RULES RELATING TO THE SALE AND DELIVERY OF TOBACCO PRODUCTS IN MAINE Chapter 203 DEPARTMENT OF HEALTH AND HUMAN SERVICES MAINE CENTER FOR DISEASE CONTROL AND PREVENTION DIVISION OF

For more information, please contact the Treasury Management Division at (501) 371-4567.

371-4567.") If you are considering a move to Little Rock or have been a resident for a short time, you may have questions about Little Rock s tax rates. The following information includes a summary of various state

If you are considering a move to Little Rock or have been a resident for a short time, you may have questions about Little Rock s tax rates. The following information includes a summary of various state

Foreign Investment in Real Property Tax Act 1980 Buyer AND Seller Beware. By R. Scott Jones, Esq.

Foreign Investment in Real Property Tax Act 1980 Buyer AND Seller Beware By R. Scott Jones, Esq. This article summarizes the tax withholding rules imposed on a buyer and his/her agent when purchasing U.S.

Foreign Investment in Real Property Tax Act 1980 Buyer AND Seller Beware By R. Scott Jones, Esq. This article summarizes the tax withholding rules imposed on a buyer and his/her agent when purchasing U.S.

Instructions for City of Colorado Springs Sales and/or Use Tax Returns

Instructions for City of Colorado Springs Sales and/or Use Tax Returns Return MUST be filed even if there is NO tax due Make check payable to the City of Colorado Springs Retain returns and supporting

Instructions for City of Colorado Springs Sales and/or Use Tax Returns Return MUST be filed even if there is NO tax due Make check payable to the City of Colorado Springs Retain returns and supporting

TRANSFERS VEHICLE INDUSTRY REGISTRATION PROCEDURES

11 Title Page 11.000 Introduction 11-2 11.005 Basic Transfer Checklist: Title Smog Requirements for Transfers Use Tax Miscellaneous Transfer Requirements 11-2 11.010 Legal Owner/Lienholder Transfers 11-13

11 Title Page 11.000 Introduction 11-2 11.005 Basic Transfer Checklist: Title Smog Requirements for Transfers Use Tax Miscellaneous Transfer Requirements 11-2 11.010 Legal Owner/Lienholder Transfers 11-13

Property FAQs. Where do I pay my property tax? Generally speaking, property taxes are paid to local Tax Collectors where the property is located.

The following is intended to provide general information concerning a frequently asked question about taxes administered by the Mississippi Tax Commission. It is an informal interpretation of the tax law

The following is intended to provide general information concerning a frequently asked question about taxes administered by the Mississippi Tax Commission. It is an informal interpretation of the tax law

REAL ESTATE TAX CERTIFICATE LIENS (House Bill 371)

") REAL ESTATE TAX CERTIFICATE LIENS (House Bill 371) SUMMIT COUNTY FISCAL OFFICE BEGAN IMPLEMENTING THE NEW DELINQUENT PROPERTY TAX COLLECTION METHOD IN 1998 The information contained within will help explain

REAL ESTATE TAX CERTIFICATE LIENS (House Bill 371) SUMMIT COUNTY FISCAL OFFICE BEGAN IMPLEMENTING THE NEW DELINQUENT PROPERTY TAX COLLECTION METHOD IN 1998 The information contained within will help explain

2016 FR-400M. Motor Fuel Tax Forms and Instructions

Government of the District of Columbia Office of the Chief Financial Officer Office of Tax and Revenue 2016 FR-400M Motor Fuel Tax Forms and Instructions Effective October 1, 2013, the District shall levy

Government of the District of Columbia Office of the Chief Financial Officer Office of Tax and Revenue 2016 FR-400M Motor Fuel Tax Forms and Instructions Effective October 1, 2013, the District shall levy

COPYRIGHTED 2005-2006, DEALER TRAINING EXPERTS OF NORTHERN CALIFORNIA

40 Question Practice Test 1. When the odometer turns past 99,999 miles on a 5 digit odometer, a dealer must: a) File a Statement of Facts b) Reset the Odometer c) Call for Help d) Advise the Buyer and

40 Question Practice Test 1. When the odometer turns past 99,999 miles on a 5 digit odometer, a dealer must: a) File a Statement of Facts b) Reset the Odometer c) Call for Help d) Advise the Buyer and

ESSEX COUNTY REAL ESTATE TAX EXEMPTION TAX RELIEF FOR THE ELDERLY AND DISABLED TAX RELIEF FOR THE YEAR OF: 20

ESSEX COUNTY REAL ESTATE TAX EXEMPTION TAX RELIEF FOR THE ELDERLY AND DISABLED TAX RELIEF FOR THE YEAR OF: 20 Income can not exceed 27,500 Financial worth can not exceed 100,000 Maximum exemption granted

ESSEX COUNTY REAL ESTATE TAX EXEMPTION TAX RELIEF FOR THE ELDERLY AND DISABLED TAX RELIEF FOR THE YEAR OF: 20 Income can not exceed 27,500 Financial worth can not exceed 100,000 Maximum exemption granted

HOUSE BILL No. 2114 page 2

HOUSE BILL No. 2114 AN ACT concerning the vehicle dealers and manufacturers licensing act; relating to vehicle bonds; amending K.S.A. 2000 Supp. 8-2404 and repealing the existing section. Be it enacted

HOUSE BILL No. 2114 AN ACT concerning the vehicle dealers and manufacturers licensing act; relating to vehicle bonds; amending K.S.A. 2000 Supp. 8-2404 and repealing the existing section. Be it enacted

ARKANSAS STATE POLICE

ARKANSAS STATE POLICE Used Motor Vehicle Dealer License Application Form Act 490 Of 1993 As Amended ACA 23-112-601 Through 611 ASP-70 (Rev. 03/14) Information Section Any person who, for a commission or

ARKANSAS STATE POLICE Used Motor Vehicle Dealer License Application Form Act 490 Of 1993 As Amended ACA 23-112-601 Through 611 ASP-70 (Rev. 03/14) Information Section Any person who, for a commission or

FLORIDA LEMON LAW SUMMARY

EXECUTIVE SUMMARY TIME PERIOD FOR FILING CLAIMS ELIGIBLE VEHICLE ELIGIBLE CONSUMER For certified procedure, Lemon Law Rights Period (24 months from original delivery) plus 60 days. For state Board, Lemon

EXECUTIVE SUMMARY TIME PERIOD FOR FILING CLAIMS ELIGIBLE VEHICLE ELIGIBLE CONSUMER For certified procedure, Lemon Law Rights Period (24 months from original delivery) plus 60 days. For state Board, Lemon

Welcome to Mobile County How to register your vehicle in Mobile County, Alabama

Welcome to Mobile County How to register your vehicle in Mobile County, Alabama The Mobile County License Commissioner s office would like to welcome you to Mobile County. We are proud of our county s

Welcome to Mobile County How to register your vehicle in Mobile County, Alabama The Mobile County License Commissioner s office would like to welcome you to Mobile County. We are proud of our county s

ADMINISTRATION OF HOTEL OCCUPANCY TAX CITY OF SHERMAN I. HOTEL OCCUPANCY TAX REPORTING AND PAYMENT REQUIREMENTS

INTRODUCTION This information is provided to all hotels/motels/ bed & breakfast (hereinafter referred to as hotels ) in the City of Sherman to explain the rules for the administration of Hotel Occupancy

INTRODUCTION This information is provided to all hotels/motels/ bed & breakfast (hereinafter referred to as hotels ) in the City of Sherman to explain the rules for the administration of Hotel Occupancy

Form CT-706 NT Instructions Connecticut Estate Tax Return (for Nontaxable Estates)

") (Rev. 05/14) Form CT-706 NT Instructions Connecticut Estate Tax Return (for Nontaxable Estates) General Information For decedents dying during 2014, the Connecticut estate tax exemption amount is $2 million.

(Rev. 05/14) Form CT-706 NT Instructions Connecticut Estate Tax Return (for Nontaxable Estates) General Information For decedents dying during 2014, the Connecticut estate tax exemption amount is $2 million.

Sales and Use Tax Application for Refund. Sales and Use Tax. Application. Have Questions? Inside. Use the enclosed form to request a refund for:

Sales and Use Tax Application for Refund Have Questions? Call 850-617-8585 Inside Frequently Asked Questions... p. 2-3 For Information, Forms, and Online Filing...p. 3 Application Form...p. 4 Documentation

Sales and Use Tax Application for Refund Have Questions? Call 850-617-8585 Inside Frequently Asked Questions... p. 2-3 For Information, Forms, and Online Filing...p. 3 Application Form...p. 4 Documentation

Vehicle purchasing guide

Vehicle purchasing guide Buy from a licensed Wisconsin dealer and you are protected by Wisconsin's motor vehicle trade practice law. Dealers follow the law when they advertise, display, and sell vehicles.

Vehicle purchasing guide Buy from a licensed Wisconsin dealer and you are protected by Wisconsin's motor vehicle trade practice law. Dealers follow the law when they advertise, display, and sell vehicles.

ASSEMBLY BILL No. 335

AMENDED IN ASSEMBLY JANUARY 6, 2014 california legislature 2013 14 regular session ASSEMBLY BILL No. 335 Introduced by Assembly Member Brown February 13, 2013 An act to amend Section 14602.6 of the Vehicle

AMENDED IN ASSEMBLY JANUARY 6, 2014 california legislature 2013 14 regular session ASSEMBLY BILL No. 335 Introduced by Assembly Member Brown February 13, 2013 An act to amend Section 14602.6 of the Vehicle

How to Finalize a Private Used Car Sale

A page for each province! How to Finalize a Private Used Car Sale Everything you need to know about the steps involved with finalizing the sale of a used car - in every province. CARPROOF S SMART BUYERS

A page for each province! How to Finalize a Private Used Car Sale Everything you need to know about the steps involved with finalizing the sale of a used car - in every province. CARPROOF S SMART BUYERS

SALES AND USE TAX TECHNICAL BULLETINS SECTION 18

SECTION 18 - CERTAIN GOVERNMENTAL ENTITIES - THE STATE, COUNTIES, CITIES AND OTHER POLITICAL SUBDIVISIONS 18-1 PURCHASES AND SALES BY AND DONATIONS TO GOVERNMENTAL ENTITIES A. Purchases By Governmental

SECTION 18 - CERTAIN GOVERNMENTAL ENTITIES - THE STATE, COUNTIES, CITIES AND OTHER POLITICAL SUBDIVISIONS 18-1 PURCHASES AND SALES BY AND DONATIONS TO GOVERNMENTAL ENTITIES A. Purchases By Governmental