Merchant Best Practices & Guidelines

|

|

|

- Solomon Ross

- 9 years ago

- Views:

Transcription

1 National Bank of Abu Dhabi Merchant Best Practices & Guidelines Merchant Advice Version 1.0 January 24, 2016

2 Table of Content 1. Guidelines to reduce Merchant Risks Card Present Transactions Card Not Present Transactions Goods Delivery Refunds Third Party Processing Chargeback Important Information to Remember Secure the Terminal Public Page 2 of 16

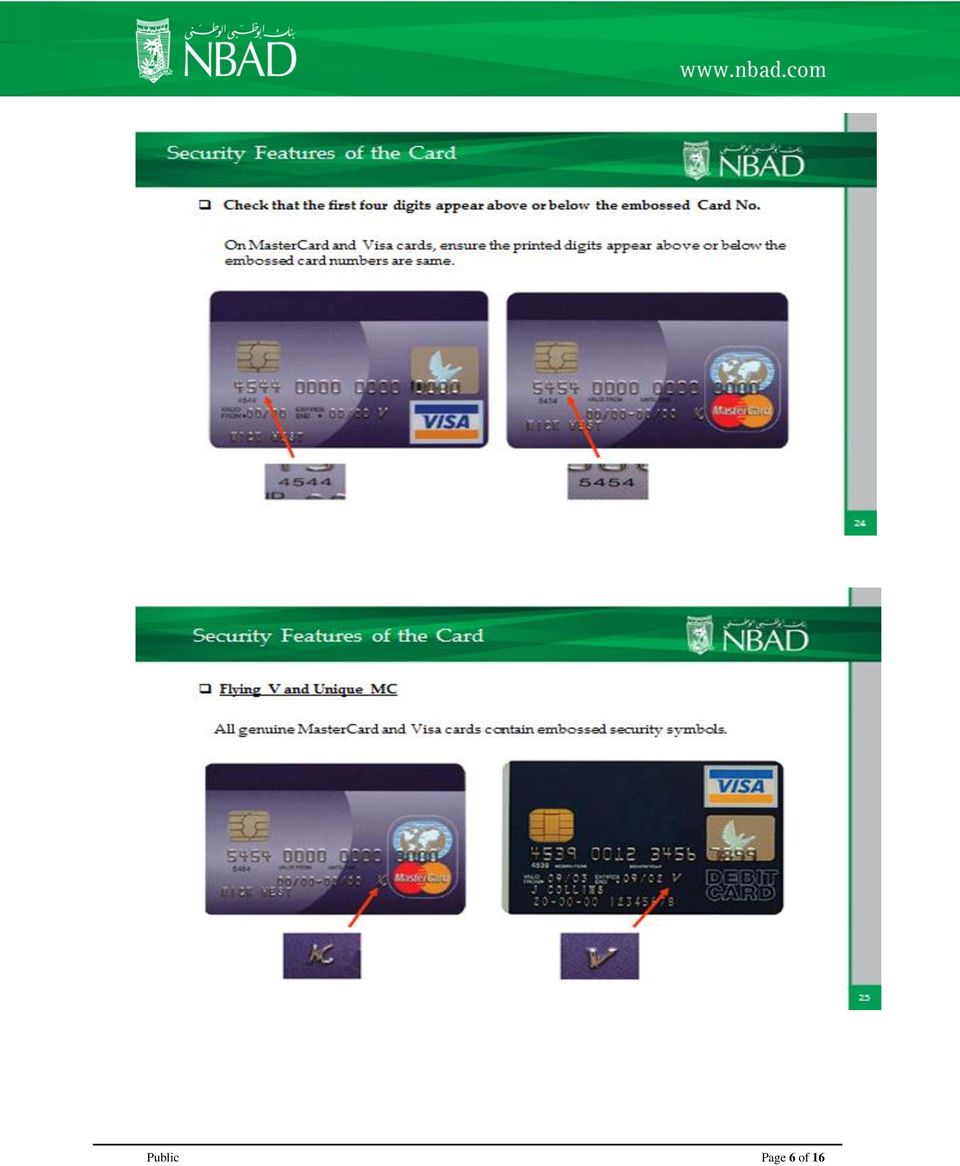

3 1. Guidelines to reduce Merchant Risks 1.1 Card Present Transactions When the card is present at the point of sale, take a good look at the card to ensure that it is genuine. Ensure that you maintain possession of the card until the transaction has been completed. Review the Payment Card Does the card appear genuine? Is the embossing clear and even and does the printing look professional? Embossing - the card numbers should be raised, clear and straight Visa and MasterCard have the first four card numbers printed under the embossing Note - The numbers are often mismatched or altered on counterfeit cards Check the front and back to ensure the card contains: - Card Issuer s logo - Cardholder name - Card number - Expiry date - Signature - CVV2/CVC2 The 3 digit value located on or near the signature panel of the credit card. - Holograms should appear three-dimensional and change color when tilted, look for the Visa Dove or MasterCard Worldwide Map Check the cardholder s signature on the receipt against the actual credit card. Signature Panel - the words `MasterCard` or `Visa` are printed repeatedly at a 45 degree angle - the panel is designed to reveal tampering Check expiration dates on all credit cards. Never accept an expired credit card. Ensure the number embossed on the front of the card matches the truncated number on the receipt. Does the name match the customer? Does the gender of the presenter match the name printed on the card? Ask for photo id to confirm details if suspicious. Always swipe or dip the payment card Never manually enter the credit card number. Take extra caution if the customer requests you to manually key a transaction Terminal Location and PIN Chip card processing Chip cards are MasterCard and Visa (credit and debit) cards that are embedded with a security chip that provides further protection to assist in decreasing the risk of fraudulent transactions and chargeback disputes. Look at the card and if there is a chip, always insert the card into the chip reader at the first instance. As with any other transaction, a degree of caution must also be exhibited when processing chip card transactions. If, Public Page 3 of 16

4 The terminal displays Insert Chip when the card is swiped through the terminal and the card in question does not have a chip on it, do not proceed with the transaction The terminal displays Insert Chip and the chip when inserted cannot be read by the terminal, do not proceed with the transaction What to look out for Being vigilant about unusual credit card spending can help you avoid becoming a victim of a potential fraud attack. Look out for: Customers who appear nervous or anxious, or hurry you at closing time. Customers who seem to not care about the item they are purchasing. For example, those who do not check the size or the price of an item, grab several items quickly, or do not worry about the warranty. Customers who request immediate delivery, that is, they want to take large and expensive items immediately. Customers who request you to manually key the card number. Multiple cards presented. Be wary of customers who give you more than two card numbers, or try to split the order. Do not Double swipe at the terminal Double swiping refers to the act of a merchant completing a second swipe of a card at the terminal after the card has already been swiped and the transaction is being processed. Double-swiping has been identified as the root cause in several large data compromise events globally. Merchants may be subjected to fines and other recovery fees by NBAD if they are found to be conducting this type of activity. Further instructions Do not accept declined transactions. Do not split a declined transaction into smaller amounts. Be on the alert for counterfeit cards. Check the chip on the card to ensure that it is embedded in the card and not protruding on the surface. You can conduct a simple test by running your finger across the surface of the chip. Customers who present a card not in their name and when questioned advise that it is their partner s or friend s card. If the customer does not cooperate or the details do not match, do not proceed with the transaction and ask for another form of payment. In the event that a customer or transaction appears suspicious, before deciding whether or not to proceed with the transaction, the staff member should contact NBAD Card Center. Public Page 4 of 16

5 Common Card Designs: Front view: Back view: Public Page 5 of 16

6 Public Page 6 of 16

7 Public Page 7 of 16

8 Public Page 8 of 16

9 1.2 Card Not Present Transactions Card not present transactions are those where neither the card nor the cardholder are present at the point of sale, such as internet or mail order/ telephone order purchases. Merchants who accept card not present transactions face a higher risk of becoming victims of fraud as the anonymity of card not present transactions make them appealing targets for fraudsters. The following tips may help reduce the possibility of fraudulent card not present transactions: Obtain as much information as possible: the credit card number, name of bank, full name, address, expiry date, CVV2/CVC2 and contact telephone number (including landline). If processing the transaction via a terminal ensure you enter the card details correctly as per the operating guides for MOTO transactions. Use some form of additional validations, such as the electronic white pages to cross check details provided. Call the customer on the quoted contact telephone number to confirm details of the order, especially for large and/or suspicious orders. Request further identification such as a photocopy of the front and back of the card. This will ensure the person has the card in their possession. Ensure it is a genuine photocopy, not a photo shopped image. If you take payments via a website, contact your gateway provider and see if they have any fraud prevention software which you can utilize. Keep all copies of correspondence including invoices, s, quotations, faxes, proof of delivery etc. Always obtain authorization for all card not present transactions, regardless of value, and for the full amount of the transaction. Remember, an authorization only confirms that funds are available at the time of the call and that the card has not been reported lost or stolen. It does not guarantee that the person quoting the card number is the owner of the card or is entitled to use the card. What to look out for Items ordered of an unusual quantity or multiple orders of the same item. Big ticket items or orders that are larger than normal for your business. Orders requested as urgent or for overnight delivery. When orders are cancelled and customer is requesting a transfer of money to a card or method other than back to the original credit card. (e.g. Money order, money transfer). This is not permitted. Different cards are provided (including different cardholder names) but same delivery address given. Multiple cards presented. Public Page 9 of 16

10 If they do give you multiple card numbers look at the actual numbers, are the first 12 digits the same then they change the last four? For example you have been given three cards: , , Notice that the card numbers only vary by the last four digits. Be wary of internet orders using generic internet addresses using free services. messages written in poor or childlike English. Multiple transactions charged to one card over a short period of time. Further instructions Take note of varying delivery addresses for repeat customers Be mindful of your states crime hotspots and delivery of goods to these hotspots Exercise caution when taking foreign orders, such as orders from Asia, the Middle East and Africa which may present a higher risk. Remember, the liability for all card not present transactions rests with the merchant. Therefore the more information you gather to satisfy yourself that the transaction is valid the more chance you have of identifying fraud and reducing the chargeback risk. Secure your customers data At NBAD, we are committed to providing our merchants assistance to help protect their business, and their customers, from the growing threat posed by online fraudsters. Without a doubt this is one of the biggest challenges faced by business today. If you are a merchant who has access to, or stores credit card details in any format, or if you use a service provider who does, it is your responsibility to ensure that your customers payment details remain secure. It is important that you understand the measures which need to be taken to ensure the security of highly sensitive personal financial information. Website requirements All merchants using an Internet Merchant Facility must comply with NBAD s website standards. NBAD reserves the right to decline, deactivate access or terminate merchants who do not comply with these requirements for the duration of the facility. Your website must satisfy all of the following criteria: The trading name and the URL must not have any substantial differences in wording. This will maintain consistency and reduce any potential cardholder confusion. Public Page 10 of 16

11 A clear description of the goods and services offered for sale. Contact information trading name, trade license number, and address. Telephone number and fax number where available. A clear explanation of shipping practices and delivery policy/timeframe. Transaction currency: NBAD merchants can process AED amount only, unless enrolled for dynamic currency services and may settle into AED accounts only. Total cost of the goods or services purchased, inclusive of all shipping charges. Card scheme brand marks are displayed wherever payment options are presented. Export restrictions (if any) countries to which the merchant does not ship. A clear refund/return policy. Consumer data privacy policy advises what you plan to do with information collected from your customers. Security capabilities and policy for transmission of payment card details. Each merchant domain name must utilize separate payment pages. It is necessary to check that website links do not go to another domain name from which payments can be made in relation to goods or services offered through the first website. All information must be accurate in all respects. Your website must not: Contain anything that constitutes or encourages a violation of any applicable law or regulations, including but not limited to the sale of illegal goods or the violation of export controls, obscenity laws or gambling laws. Contain any adult or pornographic content. Offer for sale goods or services, or use to display materials, which may be considered by a reasonable person to be obscene, vulgar, offensive, dangerous, or are otherwise inappropriate. Use unaccredited payment pages. Fail to use digital certificates to establish a secure browser session. For further information on data security standards please refer to following website 3D Secure - online authentication tool 3D Secure is an online service designed to make online shopping transactions safer by authenticating a cardholder s identity at the time of purchase. This service is known as Verified by Visa and MasterCard SecureCode. A transaction using Verified by Visa/SecureCode will redirect cardholders to the website of their card issuing bank. The cardholder may then be requested by their bank to enter a Public Page 11 of 16

12 password to be authenticated. If a customer is not registered with 3D Secure then they are still able to make a purchase from your website. Following confirmation, the window disappears and the cardholder is returned to the checkout screen. If the cardholder is not confirmed, the transaction will be declined. Participating merchants are protected by their merchant bank from receiving certain fraud-related chargebacks. For further information about Verified by Visa and MasterCard SecureCode, please contact NBAD Card Center. Note: If you are operating via a third party online Payment Service Provider (PSP), it is your responsibility to ensure that the correct risk management rules are applied to your payment facility. 2. Goods Delivery A common point of fraudulent transactions is allowing someone, particularly a third party, to pick up the goods from your store after a telephone order has been placed without the credit card being presented, a card imprint taken or signature obtained. Deliveries should always be made by your carrier or by a reputable courier engaged by you, not by your customer. For deliveries the following procedures are recommended: Ensure the person making the delivery delivers the goods to a person inside the premises, not someone waiting outside. The deliverer should always obtain the signature of the person taking the delivery. Never deliver to car parks or parks. Try to deliver only to physical addresses, take extra caution when delivering to hotels and PO BOX addresses. Be wary of orders going overseas, recent fraud trends have indicated Africa and Asia fraudsters targeting UAE merchants with stolen credit card numbers. Site the card wherever possible upon delivery of the goods. Check internet maps and street views to verify business. 3. Refunds You are not permitted to: Refund a transaction back to a card other than the one used to make the original purchase. Public Page 12 of 16

13 Send the refunded amount to the customer via the Internet, money order or international money transfer. It is also beneficial to monitor all refunds processed. An increasingly common form of fraud involves employees using your EFTPOS solution to process refunds to their own cards. Ensure only authorized staff have access to process refunds and be aware of your refund limits. Regularly change your refund password. Do not use a generic password such as Third Party Processing Third party processing is forbidden. Third party processing is where you process a transaction on behalf of another company or person. If any transactions are deemed as fraudulent, you will be responsible for the chargeback of that transaction. Here are some typical scenarios of third party processing: If you process these transactions I will give you 15% of the total sales. My terminal is broken and the bank can t fix it till later this week, can you please process this transaction for me as I will lose the sale? 5. Chargeback A chargeback is a reversal of a credit card transaction and usually occurs when a customer raises a dispute with their financial institution (also known as the Issuer) in relation to a purchase made on their credit card. A chargeback may cause the amount of the original sale and a commission / discount amount to be deducted from the merchant s account. The reasons why chargebacks arise vary greatly but are generally the result of a customer or issuer bank being dissatisfied with their purchase or due to illegal or fraudulent activity/use of their card. Common chargeback: Transaction not recognized by the cardholder Transaction not authorized by the cardholder Duplicated transactions Cancelled recurring/direct debit transactions Goods/services not received or faulty Goods/services not as described Declined Authorization Fraudulent multiple transactions Legal proceedings Public Page 13 of 16

14 Point-of-Sale errors Delayed Charges Invalid / Incorrect Card / Account number used Late Presentment / Expired Card The Chargeback process a. Transaction is disputed. Cardholder raises problem with their financial institution (known as the Issuer) or the Issuer discovers a breach of the card scheme rules. b. Issuer advises NBAD Merchant Services via schemes. c. NBAD Merchant Services may request documentation from the merchant to verify the transaction. The merchant has a set timeframe to respond to retrieval requests, usually 10 days. d. If the dispute is invalid, NBAD Merchant Services will decline the chargeback and return it to the Issuer. e. If the chargeback is valid, the chargeback amount is debited from the merchant s account and written notification is provided to the merchant. A commission / discount amount may also be charged to the merchants account. 6. Important Information to Remember If you are suspicious, contact the NBAD Card Center- Risk & Fraud team prior to the processing and dispatching of the goods. Always obtain authorization, especially for online transactions, regardless of value and for the full transaction amount. Look at the decline codes on the POS terminal when a transaction rejects, does the code indicate the card is lost or stolen? If so retain the card. Is the card number valid? If not do not proceed with the transaction or accept another card. Do not lower the amounts, split sales or accept card after card. Be mindful of overseas orders. Never conduct third party processing. Store your customer s information securely. Ensure all your computer systems are password protected and data maintained on databases should be encrypted. Ensure all paper records are securely stored with restricted access. Never store the CVV2/CVC2 or full card track data. Report all security incidents. Train your staff. Ensure your staffs are aware and vigilant of potential fraudsters. Be aware of what your staffs are processing. Staff has been found to be involved in fraudulent activity. Look out for staff refunding to their own credit cards or storing unnecessary customer information. Be extra cautious on high risk transactions including: card not present, manually keyed, no authorization obtained or fallback transactions. Public Page 14 of 16

15 Adopting these suggestions may help reduce fraud but will not guarantee that you will not be a victim of credit card fraud. It is your responsibility to confirm that the purchaser is the genuine cardholder, as you may be liable for the transaction in the case of a chargeback under your merchant agreement terms and conditions. Merchants should be aware of their responsibilities under their NBAD Merchant Terms & Conditions. 7. Secure the Terminal Fraud and misuse of credit or debit card information is a growing problem for many merchants globally. The loss of customer card data and subsequent misuse may undermine customer confidence and potentially reduce card usage at your business. As part of NBAD s ongoing commitment to providing the most up to date information on terminal and cardholder data security, we have outlined a list of best practices for protecting your terminals and your customer s information. Your NBAD merchant terminal is equipped with a number of in-built security features which are designed to protect your customers information. By implementing the recommended best practices below, you can protect your business, your customers and your reputation from credit and debit card fraud or misuse. Recommended best practices Always ensure that terminals are secure and under supervision during operating hours (including any spare or replacement terminals you have) Secure your equipment do not leave terminals unattended. Ensure that only authorized employees have access to your terminals and are fully trained on their use when closing your store or kiosk, always ensure that your terminals are securely locked and not exposed to unauthorized access. Never allow your terminal to be maintained, swapped or removed without advance notice from NBAD. Be aware of unannounced terminal service visits. Only allow authorized NBAD personnel to maintain, swap or remove your terminal, and always ensure that security identification is provided. Inspect your terminals on a regular basis, to ensure that the terminal casing is whole with external security stickers remaining unbroken and of a high print quality. Ensure that there are no additional cables running from your terminal Make sure that any CCTV or other security cameras located near your terminal(s) can t observe Cardholders entering details. It is important to notify NBAD Cards Center immediately if: a. Your terminal is missing Public Page 15 of 16

16 b. You, or any member of your staff, is approached to perform maintenance, swap or remove your terminal without prior notification from NBAD and/or security identification is not provided c. Your terminal prints incorrect receipts or has incorrect details d. Your terminal is damaged or appears to be tampered with. Public Page 16 of 16

BWA Merchant Services. Credit Card Fraud Protection User Guide

1 BWA Merchant Services Credit Card Fraud Protection User Guide 2 Contents: 1. How to reduce the risk of card present fraud... 3 2. How to reduce the risk of card not present fraud... 5 3. Delivering the

1 BWA Merchant Services Credit Card Fraud Protection User Guide 2 Contents: 1. How to reduce the risk of card present fraud... 3 2. How to reduce the risk of card not present fraud... 5 3. Delivering the

Merchant Business Solutions. Protecting business against credit card fraud.

Merchant Business Solutions. Protecting business against credit card fraud. Version 4.0 May 2011 Contents Protect your business 3 Authorisation 4 Chargebacks 5 Verification of Purchaser 6 Types of goods

Merchant Business Solutions. Protecting business against credit card fraud. Version 4.0 May 2011 Contents Protect your business 3 Authorisation 4 Chargebacks 5 Verification of Purchaser 6 Types of goods

Fraud Minimisation Guide ANZ Merchant Business Solutions

Fraud Minimisation Guide ANZ Merchant Business Solutions INTRODUCTION Fraud can occur in and is a risk for any business that accepts credit cards and it can have a significant financial impact on your

Fraud Minimisation Guide ANZ Merchant Business Solutions INTRODUCTION Fraud can occur in and is a risk for any business that accepts credit cards and it can have a significant financial impact on your

Fraud Minimisation, Data Security and Chargeback Guide SECURING YOUR BUSINESS

Fraud Minimisation, Data Security and Chargeback Guide SECURING YOUR BUSINESS Fraud Minimisation and Chargeback Guide Fraud is a problem for many merchants and can have a substantial financial impact

Fraud Minimisation, Data Security and Chargeback Guide SECURING YOUR BUSINESS Fraud Minimisation and Chargeback Guide Fraud is a problem for many merchants and can have a substantial financial impact

CREDIT CARD FRAUD PROTECTION. how to protect your business and your customers

CREDIT CARD FRAUD PROTECTION how to protect your business and your customers INTRODUCTION It is an unfortunate fact that many businesses will encounter a customer who presents a credit card or a credit

CREDIT CARD FRAUD PROTECTION how to protect your business and your customers INTRODUCTION It is an unfortunate fact that many businesses will encounter a customer who presents a credit card or a credit

FREQUENTLY ASKED QUESTIONS - CHARGEBACKS

FREQUENTLY ASKED QUESTIONS - CHARGEBACKS # Questions Answer 1 What is a Chargeback? A Chargeback is the term used by Banks for debiting a merchant s bank account due to successful return of a transaction

FREQUENTLY ASKED QUESTIONS - CHARGEBACKS # Questions Answer 1 What is a Chargeback? A Chargeback is the term used by Banks for debiting a merchant s bank account due to successful return of a transaction

PROTECT YOUR BUSINESS FROM LOSSES WHILE ACCEPTING CREDIT CARDS

PROTECT YOUR BUSINESS FROM LOSSES WHILE ACCEPTING CREDIT CARDS TABLE OF CONTENTS Introduction...1 Preventing Fraud in a Card-Present Environment...2 How to Reduce Chargebacks in a Card-Present Environment...4

PROTECT YOUR BUSINESS FROM LOSSES WHILE ACCEPTING CREDIT CARDS TABLE OF CONTENTS Introduction...1 Preventing Fraud in a Card-Present Environment...2 How to Reduce Chargebacks in a Card-Present Environment...4

How To Spot & Prevent Fraudulent Credit Card Activity

Datalink Bankcard Services How To Spot & Prevent Fraudulent Credit Card Activity White Paper 2013 According to statistics from the U.S. Department of Justice and the Consumer Sentinel Network, credit card

Datalink Bankcard Services How To Spot & Prevent Fraudulent Credit Card Activity White Paper 2013 According to statistics from the U.S. Department of Justice and the Consumer Sentinel Network, credit card

YOUR GUIDE TO SAFER, SMARTER CREDIT CARD PAYMENTS. What you need to know about chargebacks and fraud on mail, telephone, IVR and Internet orders

YOUR GUIDE TO SAFER, SMARTER CREDIT CARD PAYMENTS What you need to know about chargebacks and fraud on mail, telephone, IVR and Internet orders Contents HELPING YOU PROTECT YOUR BUSINESS AND YOUR PROFITS

YOUR GUIDE TO SAFER, SMARTER CREDIT CARD PAYMENTS What you need to know about chargebacks and fraud on mail, telephone, IVR and Internet orders Contents HELPING YOU PROTECT YOUR BUSINESS AND YOUR PROFITS

Integrated EFTPOS User Guide

business Integrated EFTPOS User Guide www.bendigobank.com.au Table of contents Keypad layout....3 Debit card purchase...4 Credit and charge card purchase...5 Processing a tip (restaurants only)...6 Pre-authorisation

business Integrated EFTPOS User Guide www.bendigobank.com.au Table of contents Keypad layout....3 Debit card purchase...4 Credit and charge card purchase...5 Processing a tip (restaurants only)...6 Pre-authorisation

Avoiding Fraud. Learn to recognize the warning signs for fraud and follow these card acceptance guidelines to reduce your risk.

Avoiding Fraud Learn to recognize the warning signs for fraud and follow these card acceptance guidelines to reduce your risk. Intoduction Fraud comes in many forms and hurts merchants of all sizes. Whether

Avoiding Fraud Learn to recognize the warning signs for fraud and follow these card acceptance guidelines to reduce your risk. Intoduction Fraud comes in many forms and hurts merchants of all sizes. Whether

ipayu TM Prepaid MasterCard FREQUENTLY ASKED QUESTIONS

ipayu TM Prepaid MasterCard FREQUENTLY ASKED QUESTIONS What is the ipayu Prepaid The ipayu Prepaid MasterCard provides parents with a convenient, safe way to send money to their students. Students can

ipayu TM Prepaid MasterCard FREQUENTLY ASKED QUESTIONS What is the ipayu Prepaid The ipayu Prepaid MasterCard provides parents with a convenient, safe way to send money to their students. Students can

Credit/Debit Card Processing Requirements and Best Practices. Adele Honeyman Oregon State Treasury Training Specialist

Credit/Debit Card Processing Requirements and Best Practices Adele Honeyman Oregon State Treasury Training Specialist 1 What? What do I need to know about excepting credit cards? Who s involved, how it

Credit/Debit Card Processing Requirements and Best Practices Adele Honeyman Oregon State Treasury Training Specialist 1 What? What do I need to know about excepting credit cards? Who s involved, how it

Card and Account Security. Important information about your card and account.

Card and Account Security. Important information about your card and account. 2 Card and Account Security 1. Peace of mind As a Bendigo Bank customer you can bank with confidence knowing that, if you take

Card and Account Security. Important information about your card and account. 2 Card and Account Security 1. Peace of mind As a Bendigo Bank customer you can bank with confidence knowing that, if you take

Merchant Payment Card Processing Guidelines

Merchant Payment Card Processing Guidelines The following is intended to provide guidance that departments or units can use to help develop specific procedures for their department or unit. If you have

Merchant Payment Card Processing Guidelines The following is intended to provide guidance that departments or units can use to help develop specific procedures for their department or unit. If you have

Guide to credit card security

Contents Click on a title below to jump straight to that section. What is credit card fraud? Types of credit card fraud Current scams Keeping your card and card details safe Banking and shopping securely

Contents Click on a title below to jump straight to that section. What is credit card fraud? Types of credit card fraud Current scams Keeping your card and card details safe Banking and shopping securely

A multi-layered approach to payment card security.

A multi-layered approach to payment card security. CARD-NOT-PRESENT 1 A recent research study revealed that Visa cards are the most widely used payment method at Canadian websites, on the phone, or through

A multi-layered approach to payment card security. CARD-NOT-PRESENT 1 A recent research study revealed that Visa cards are the most widely used payment method at Canadian websites, on the phone, or through

When checking the status of the Cardholder's Card (card status check) a so-called "zero value authorisation" shall always be used.

a so-called zero value authorisation shall always be used.") REGULATIONS FOR SALES PAID BY CARD REMOTE TRADING (Card Not Present) (May 2015) These regulations, the "Remote Trading Regulations", apply to sales paid by Card in Remote Trading. "Remote Trading" refers

REGULATIONS FOR SALES PAID BY CARD REMOTE TRADING (Card Not Present) (May 2015) These regulations, the "Remote Trading Regulations", apply to sales paid by Card in Remote Trading. "Remote Trading" refers

Dear Valued Merchant,

Dear Valued Merchant, Welcome to Central Payment thank you for becoming our client. We are committed to providing our merchants with outstanding customer service and superior products. It is our company

Dear Valued Merchant, Welcome to Central Payment thank you for becoming our client. We are committed to providing our merchants with outstanding customer service and superior products. It is our company

Clark Brands Payment Methods Manual. First Data Locations

Clark Brands Payment Methods Manual First Data Locations Table of Contents Introduction... 3 Valid Card Types... 3 Authorization Numbers, Merchant ID Numbers and Request for Copy Fax Numbers... 4 Other

Clark Brands Payment Methods Manual First Data Locations Table of Contents Introduction... 3 Valid Card Types... 3 Authorization Numbers, Merchant ID Numbers and Request for Copy Fax Numbers... 4 Other

Retrieval & Chargeback Best Practices

Retrieval & Chargeback Best Practices A Merchant User s Guide to Help Manage Disputes Version Three November, 2010 www.firstdata.com THIS PAGE INTENTIONALLY LEFT BLANK. Developed by: First Data Payment

Retrieval & Chargeback Best Practices A Merchant User s Guide to Help Manage Disputes Version Three November, 2010 www.firstdata.com THIS PAGE INTENTIONALLY LEFT BLANK. Developed by: First Data Payment

Righting wrongs. How Westpac helps you resolve credit and debit card transaction disputes.

Righting wrongs. How Westpac helps you resolve credit and debit card transaction disputes. Although at Westpac we do everything we can to prevent it, sometimes problems arise with credit and debit card

Righting wrongs. How Westpac helps you resolve credit and debit card transaction disputes. Although at Westpac we do everything we can to prevent it, sometimes problems arise with credit and debit card

CRM4M Accounting Set Up and Miscellaneous Accounting Guide Rev. 10/17/2008 rb

CRM4M Accounting Set Up and Miscellaneous Accounting Guide Rev. 10/17/2008 rb Topic Page Chart of Accounts 3 Creating a Batch Manually 8 Closing a Batch Manually 11 Cancellation Fees 17 Check Refunds 19

CRM4M Accounting Set Up and Miscellaneous Accounting Guide Rev. 10/17/2008 rb Topic Page Chart of Accounts 3 Creating a Batch Manually 8 Closing a Batch Manually 11 Cancellation Fees 17 Check Refunds 19

Merchant Operating Guide

PB 1 Merchant Operating Guide ANZ FastPay MOBILE PAYMENT SOLUTION Contents 1. Welcome 4 1.1 Merchant Agreement 4 1.2 Contact Details 4 1.3 How to get started 4 1.4 Authorisation 4 1.4.1 Authorisation Declined

PB 1 Merchant Operating Guide ANZ FastPay MOBILE PAYMENT SOLUTION Contents 1. Welcome 4 1.1 Merchant Agreement 4 1.2 Contact Details 4 1.3 How to get started 4 1.4 Authorisation 4 1.4.1 Authorisation Declined

AIB Merchant Services AIB Merchant Services Quick Reference Guide Ingenico

AIB Merchant Services AIB Merchant Services Quick Reference Guide Ingenico AIB Merchant Services AIBMS Quick Reference Guide This quick reference guide has been designed to answer the most common queries

AIB Merchant Services AIB Merchant Services Quick Reference Guide Ingenico AIB Merchant Services AIBMS Quick Reference Guide This quick reference guide has been designed to answer the most common queries

Your Guide. to doing business with American Express

Your Guide to doing business with American Express Contact Information Internet General Information Point-of-Purchase Materials Online Merchant Services Marketing Opportunities americanexpress.co.uk/ondisplay

Your Guide to doing business with American Express Contact Information Internet General Information Point-of-Purchase Materials Online Merchant Services Marketing Opportunities americanexpress.co.uk/ondisplay

Visa Merchant Best Practice Guide for Cardholder Not Present Transactions

Visa Merchant Best Practice Guide for Cardholder Not Present Transactions Table of Contents Section 1 About This Guide 03 Section 2 Merchant Procedures 05 Section 3 Authorisation 07 Authorisation Procedures

Visa Merchant Best Practice Guide for Cardholder Not Present Transactions Table of Contents Section 1 About This Guide 03 Section 2 Merchant Procedures 05 Section 3 Authorisation 07 Authorisation Procedures

Merchant Operating Guide.

Merchant Operating Guide. Card acceptance by business MERCHANT BUSINESS SOLUTIONS Postal Address Merchant Business Solutions GPO Box 18 Sydney NSW 2001 Westpac Merchant Business Solutions Help Desk: Sales

Merchant Operating Guide. Card acceptance by business MERCHANT BUSINESS SOLUTIONS Postal Address Merchant Business Solutions GPO Box 18 Sydney NSW 2001 Westpac Merchant Business Solutions Help Desk: Sales

Chargeback Reason Code List - U.S.

AL Airline Transaction Dispute AP Automatic Payment AW Altered Amount CA Cash Advance Dispute CD Credit Posted as Card Sale CR Cancelled Reservation This chargeback occurs because of a dispute on an Airline

AL Airline Transaction Dispute AP Automatic Payment AW Altered Amount CA Cash Advance Dispute CD Credit Posted as Card Sale CR Cancelled Reservation This chargeback occurs because of a dispute on an Airline

ING Vysya Bank Forex Travel Card is a pre-paid foreign currency chip card that offers you a safe, secure and

Forex Travel Card FAQs: What is ING Vysya Bank Forex Travel Card? ING Vysya Bank Forex Travel Card is a pre-paid foreign currency chip card that offers you a safe, secure and convenient way to meet all

Forex Travel Card FAQs: What is ING Vysya Bank Forex Travel Card? ING Vysya Bank Forex Travel Card is a pre-paid foreign currency chip card that offers you a safe, secure and convenient way to meet all

Your Guide. to doing business with American Express

Your Guide to doing business with American Express Contact Information Internet General Information Point-of-Purchase Materials Online Merchant Services Marketing Opportunities americanexpress.co.uk/signage

Your Guide to doing business with American Express Contact Information Internet General Information Point-of-Purchase Materials Online Merchant Services Marketing Opportunities americanexpress.co.uk/signage

Merchant Operating Guide

Merchant Trading Name: Merchant Identification Number: Terminal Identification Number: PB 1 Merchant Operating Guide ANZ POS PLUS INTEGRATED EFTPOS SOLUTIONS Contents 1. Welcome 4 1.1 Merchant Agreement

Merchant Trading Name: Merchant Identification Number: Terminal Identification Number: PB 1 Merchant Operating Guide ANZ POS PLUS INTEGRATED EFTPOS SOLUTIONS Contents 1. Welcome 4 1.1 Merchant Agreement

Actorcard Prepaid Visa Card Terms & Conditions

Actorcard Prepaid Visa Card Terms & Conditions These Terms & Conditions apply to your Actorcard prepaid Visa debit card. Please read them carefully. In these Terms & Conditions: "Account" means the prepaid

Actorcard Prepaid Visa Card Terms & Conditions These Terms & Conditions apply to your Actorcard prepaid Visa debit card. Please read them carefully. In these Terms & Conditions: "Account" means the prepaid

Reloadable Visa Debit Card. These are your Reloadable Visa Debit Card Terms and Conditions.

Reloadable Visa Debit Card These are your Reloadable Visa Debit Card Terms and Conditions. "Agreement" means these Visa Prepaid Card Terms and Conditions."We" "us" and "our" refer to Del Norte Credit Union.

Reloadable Visa Debit Card These are your Reloadable Visa Debit Card Terms and Conditions. "Agreement" means these Visa Prepaid Card Terms and Conditions."We" "us" and "our" refer to Del Norte Credit Union.

ONPOINT COMMUNITY CREDIT UNION International Prepaid Card Terms and Conditions

ONPOINT COMMUNITY CREDIT UNION International Prepaid Card Terms and Conditions International Prepaid Card These are your International Prepaid Card Terms and Conditions. "Agreement" means these VISA Prepaid

ONPOINT COMMUNITY CREDIT UNION International Prepaid Card Terms and Conditions International Prepaid Card These are your International Prepaid Card Terms and Conditions. "Agreement" means these VISA Prepaid

Merchant Services. How to help protect your business

Please immediately report any suspicious activity involving credit card or debit card use to TD Merchant Services at 1-800-6-116 For more information, visit www.tdmerchantservices.com Merchant Services

Please immediately report any suspicious activity involving credit card or debit card use to TD Merchant Services at 1-800-6-116 For more information, visit www.tdmerchantservices.com Merchant Services

EFTPOS Merchant Facilities Quick Reference Guide

EFTPOS Merchant Facilities Quick Reference Guide How to Use this Guide This handy Quick Reference Guide has been designed to give you step-by-step, easy-to-follow instructions on how to correctly use your

EFTPOS Merchant Facilities Quick Reference Guide How to Use this Guide This handy Quick Reference Guide has been designed to give you step-by-step, easy-to-follow instructions on how to correctly use your

Ti ps. Merchant. for Credit Card Transactions. Processing Tips CARD ONE INTERNATIONAL INC

Merchant Processing Tips Ti ps for Credit Card Transactions CARD ONE INTERNATIONAL INC Card One International Inc - Merchant Processing Tips for Card Transactions Page 1 of 11 Merchant Processing Tips

Merchant Processing Tips Ti ps for Credit Card Transactions CARD ONE INTERNATIONAL INC Card One International Inc - Merchant Processing Tips for Card Transactions Page 1 of 11 Merchant Processing Tips

Visa Student Card Terms and Conditions. These are your Student Card Terms and Conditions.

Visa Student Card Terms and Conditions These are your Student Card Terms and Conditions. "Agreement" means these Visa Student Card Terms and Conditions. "We" "us" and "our" refer to Bank-Fund Staff Federal

Visa Student Card Terms and Conditions These are your Student Card Terms and Conditions. "Agreement" means these Visa Student Card Terms and Conditions. "We" "us" and "our" refer to Bank-Fund Staff Federal

Merchant Guide to the Visa Address Verification Service

Merchant Guide to the Visa Address Verification Service Merchant Guide to the Visa Address Verification Service TABLE OF CONTENTS Table of Contents Merchant Guide to the Visa Address Verification Service

Merchant Guide to the Visa Address Verification Service Merchant Guide to the Visa Address Verification Service TABLE OF CONTENTS Table of Contents Merchant Guide to the Visa Address Verification Service

BNZ Advantage Credit Card Terms and Conditions.

BNZ Advantage Credit Card Terms and Conditions. 1 May 2015 This document contains the terms and conditions that apply to BNZ Advantage credit card accounts operated by you, including the terms and conditions

BNZ Advantage Credit Card Terms and Conditions. 1 May 2015 This document contains the terms and conditions that apply to BNZ Advantage credit card accounts operated by you, including the terms and conditions

Debit MasterCard. Conditions of Use. These are the conditions of use that apply to your Rabobank Debit MasterCard. You must read and retain them.

Debit MasterCard Conditions of Use These are the conditions of use that apply to your Rabobank Debit MasterCard. You must read and retain them. May 2013 Contents 1. Signing your card... 3 2. Ownership

Debit MasterCard Conditions of Use These are the conditions of use that apply to your Rabobank Debit MasterCard. You must read and retain them. May 2013 Contents 1. Signing your card... 3 2. Ownership

Credit Cards CARD TRANSACTIONS AND YOU. Credit Cards. A consumer education programme by:

Credit Cards CARD TRANSACTIONS AND YOU Credit Cards A consumer education programme by: CONTENTS 1 Introduction 2 What is a credit card and how it works Applying for a credit card 3 Application process

Credit Cards CARD TRANSACTIONS AND YOU Credit Cards A consumer education programme by: CONTENTS 1 Introduction 2 What is a credit card and how it works Applying for a credit card 3 Application process

Visa Tips for Restaurant Staff

Visa Tips for Restaurant Staff Helpful Information and Best Practices for Handling Visa Transactions For U.S. Only When it comes to restaurants, most customers are looking for the same basic things...

Visa Tips for Restaurant Staff Helpful Information and Best Practices for Handling Visa Transactions For U.S. Only When it comes to restaurants, most customers are looking for the same basic things...

Suncorp Bank EFTPOS. Terms and Conditions for a Suncorp Merchant Facility

Suncorp Bank EFTPOS Terms and Conditions for a Suncorp Merchant Facility Contents 1 Introduction...3 9 Recurring Transactions...12 1.1 Welcome...3 10 Hotel/Motel Merchants - Transaction Processing Requirements...12

Suncorp Bank EFTPOS Terms and Conditions for a Suncorp Merchant Facility Contents 1 Introduction...3 9 Recurring Transactions...12 1.1 Welcome...3 10 Hotel/Motel Merchants - Transaction Processing Requirements...12

Merchant Card Processing Best Practices

Merchant Card Processing Best Practices Background: The major credit card companies (VISA, MasterCard, Discover, and American Express) have published a uniform set of data security standards that ALL merchants

Merchant Card Processing Best Practices Background: The major credit card companies (VISA, MasterCard, Discover, and American Express) have published a uniform set of data security standards that ALL merchants

With the Target breach on everyone s mind, you may find these Customer Service Q & A s helpful.

With the Target breach on everyone s mind, you may find these Customer Service Q & A s helpful. Breach Overview Q: Media reports are stating that Target experienced a data breach. Can you provide more

With the Target breach on everyone s mind, you may find these Customer Service Q & A s helpful. Breach Overview Q: Media reports are stating that Target experienced a data breach. Can you provide more

How does the EMV Travel Prepaid Card work?

How does the EMV Travel Prepaid Card work? The EMV Travel Prepaid Card is a reloadable prepaid Visa Reloadable EMV Travel Prepaid Card, which means you can spend up to the value placed on the card anywhere

How does the EMV Travel Prepaid Card work? The EMV Travel Prepaid Card is a reloadable prepaid Visa Reloadable EMV Travel Prepaid Card, which means you can spend up to the value placed on the card anywhere

Getting Started. Quick Reference Guide for Payment Processing

Getting Started Quick Reference Guide for Payment Processing In today s competitive landscape, you have many choices when it comes to selecting your payments provider, and we appreciate your business.

Getting Started Quick Reference Guide for Payment Processing In today s competitive landscape, you have many choices when it comes to selecting your payments provider, and we appreciate your business.

Chargebacks & Retrievals. Expand Your Knowledge

Chargebacks & Retrievals Expand Your Knowledge Agenda The Philosophy Dispute Process Overview and Timeline Retrieval Request Overview and Recent Changes/Trends Chargeback Overview and Recent Changes/Trends

Chargebacks & Retrievals Expand Your Knowledge Agenda The Philosophy Dispute Process Overview and Timeline Retrieval Request Overview and Recent Changes/Trends Chargeback Overview and Recent Changes/Trends

360 Federal Credit Union Reloadable Prepaid Card Terms and Conditions

360 Federal Credit Union Reloadable Prepaid Card Terms and Conditions These are your Prepaid Card Terms and Conditions: "Agreement" means these Visa Prepaid Card Terms and Conditions. "We" "us" and "our"

360 Federal Credit Union Reloadable Prepaid Card Terms and Conditions These are your Prepaid Card Terms and Conditions: "Agreement" means these Visa Prepaid Card Terms and Conditions. "We" "us" and "our"

Eagle POS Procedure Guide For Epicor Bankcard Processing

Eagle POS Procedure Guide For Epicor Bankcard Processing Table of Contents Introduction... 3 1 Transactions using a Swiped Bankcard... 3 Basic Swiped Credit Card Sale & Return transaction... 3 Sales &

Eagle POS Procedure Guide For Epicor Bankcard Processing Table of Contents Introduction... 3 1 Transactions using a Swiped Bankcard... 3 Basic Swiped Credit Card Sale & Return transaction... 3 Sales &

Arab Bank Cards User Guide

Arab Bank Cards User Guide 4600900 arabbank.jo A card to suit every lifestyle Coming to you from the largest Arab banking network, Arab Bank Cards entitle you to a host of benefits designed to offer you

Arab Bank Cards User Guide 4600900 arabbank.jo A card to suit every lifestyle Coming to you from the largest Arab banking network, Arab Bank Cards entitle you to a host of benefits designed to offer you

Credit cards explained

Credit cards explained What is a credit card? As its name suggests, a credit card lets you buy things on credit meaning that you don t need to have the money upfront to pay for your purchases. If large,

Credit cards explained What is a credit card? As its name suggests, a credit card lets you buy things on credit meaning that you don t need to have the money upfront to pay for your purchases. If large,

EMV EMV TABLE OF CONTENTS

2 TABLE OF CONTENTS Intro... 2 Are You Ready?... 3 What Is?... 4 Why?... 5 What Does Mean To Your Business?... 6 Checklist... 8 3 U.S. Merchants 60% are expected to convert to -enabled devices by 2015.

2 TABLE OF CONTENTS Intro... 2 Are You Ready?... 3 What Is?... 4 Why?... 5 What Does Mean To Your Business?... 6 Checklist... 8 3 U.S. Merchants 60% are expected to convert to -enabled devices by 2015.

Cardholder Bank Disputed Transactions

Cardholder Bank Disputed Transactions Merchant Card Services Office of Business and Financial Services Welcome! Table of Contents: Introduction Types of Disputed Transactions Bank Transaction Processing

Cardholder Bank Disputed Transactions Merchant Card Services Office of Business and Financial Services Welcome! Table of Contents: Introduction Types of Disputed Transactions Bank Transaction Processing

Understanding and Preventing Chargebacks and Retrievals

Understanding and Preventing Chargebacks and Retrievals Table of Contents Introduction... 2 The Purpose of This Guide.... 2 Retrieval Requests.. 3 What Is a Retrieval Request?... 3 Life Cycle of a Retrieval

Understanding and Preventing Chargebacks and Retrievals Table of Contents Introduction... 2 The Purpose of This Guide.... 2 Retrieval Requests.. 3 What Is a Retrieval Request?... 3 Life Cycle of a Retrieval

CardLink Merchant Services

CardLink Merchant Services w w w. b u t t e r f i e l d b a n k. k y C a r d L i n k M e r c h a n t S e r v i c e s S t a c k i n g t h e c a r d s i n y o u r f a v o u r Butterfield Bank's all-inclusive

CardLink Merchant Services w w w. b u t t e r f i e l d b a n k. k y C a r d L i n k M e r c h a n t S e r v i c e s S t a c k i n g t h e c a r d s i n y o u r f a v o u r Butterfield Bank's all-inclusive

Credit Card Acceptance & Chargeback Prevention

Credit Card Acceptance & Chargeback Prevention Tips for Travel Agents July 2010 About this Guidebook... 3 Credit Card Acceptance... 4 Fraud Prevention Tips... 7 Credit Card Chargebacks Tips...11 Payment

Credit Card Acceptance & Chargeback Prevention Tips for Travel Agents July 2010 About this Guidebook... 3 Credit Card Acceptance... 4 Fraud Prevention Tips... 7 Credit Card Chargebacks Tips...11 Payment

Card Not Present Fraud Webinar Transcript

Card Not Present Fraud Webinar Transcript All right let s go ahead and get things started, and to do that, I d like to turn it over to Fae Ghormley. Fae? Thank you for giving us this opportunity to share

Card Not Present Fraud Webinar Transcript All right let s go ahead and get things started, and to do that, I d like to turn it over to Fae Ghormley. Fae? Thank you for giving us this opportunity to share

Credit Card Conditions of Use. Credit Guide.

Credit Card Conditions of Use. Credit Guide. Effective Date: 20 May 2016 This document does not contain all the terms of this agreement or all of the information we are required by law to give you before

Credit Card Conditions of Use. Credit Guide. Effective Date: 20 May 2016 This document does not contain all the terms of this agreement or all of the information we are required by law to give you before

FREQUENTLY ASKED QUESTIONS

FREQUENTLY ASKED QUESTIONS 1. What is the YES BANK MasterCard SecureCode? The MasterCard SecureCode is a service offered by YES BANK in partnership with MasterCard. This authentication is basically a password

FREQUENTLY ASKED QUESTIONS 1. What is the YES BANK MasterCard SecureCode? The MasterCard SecureCode is a service offered by YES BANK in partnership with MasterCard. This authentication is basically a password

Merchant Agreement for MasterCard, Maestro, Visa, Visa Electron, V PAY, JCB, China UnionPay and American Express. Business Procedures

Merchant Agreement for MasterCard, Maestro, Visa, Visa Electron, V PAY, JCB, China UnionPay and American Express Business Procedures Table of Contents 1. Introduction...2 2. Face-to-Face Transactions...2

Merchant Agreement for MasterCard, Maestro, Visa, Visa Electron, V PAY, JCB, China UnionPay and American Express Business Procedures Table of Contents 1. Introduction...2 2. Face-to-Face Transactions...2

New Account Reference Guide

New Account Reference Guide Welcome to BBVA Compass Merchant Services Thank you for choosing BBVA Compass as your Merchant Services provider. BBVA Compass is dedicated to providing your business with the

New Account Reference Guide Welcome to BBVA Compass Merchant Services Thank you for choosing BBVA Compass as your Merchant Services provider. BBVA Compass is dedicated to providing your business with the

Procedure guide. For a smoother operation

Procedure guide For a smoother operation Welcome to Barclaycard Global Payment Acceptance About this document This procedure guide along with the Terms and Conditions and Additional Service Conditions

Procedure guide For a smoother operation Welcome to Barclaycard Global Payment Acceptance About this document This procedure guide along with the Terms and Conditions and Additional Service Conditions

Procedure guide. For a smoother operation

Procedure guide For a smoother operation Welcome to Barclaycard Global Payment Acceptance About this document This procedure guide along with the Terms and Conditions and Additional Service Conditions

Procedure guide For a smoother operation Welcome to Barclaycard Global Payment Acceptance About this document This procedure guide along with the Terms and Conditions and Additional Service Conditions

Payment System Forum and Exhibition 2014 Sasana Kijang, Kuala Lumpur

Payment System Forum and Exhibition 2014 Sasana Kijang, Kuala Lumpur Enabling Payment Card Acceptance at Small and Medium Enterprises (SMEs) and Microenterprises Part 1: Payment Card Acceptance Infrastructure

Payment System Forum and Exhibition 2014 Sasana Kijang, Kuala Lumpur Enabling Payment Card Acceptance at Small and Medium Enterprises (SMEs) and Microenterprises Part 1: Payment Card Acceptance Infrastructure

NAB EFTPOS User Guide. for Countertop & Mobile Terminals

NAB EFTPOS User Guide for Countertop & Mobile Terminals About your NAB EFTPOS Terminal NAB EFTPOS Mobile NAB EFTPOS Countertoptop Table of Contents Getting to know your NAB EFTPOS VeriFone terminal...5

NAB EFTPOS User Guide for Countertop & Mobile Terminals About your NAB EFTPOS Terminal NAB EFTPOS Mobile NAB EFTPOS Countertoptop Table of Contents Getting to know your NAB EFTPOS VeriFone terminal...5

ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE PERSONAL CHECK and/or ATM CARD

ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE PERSONAL CHECK and/or ATM CARD This agreement and disclosure applies to payment orders and funds transfers governed by the Electronic Fund Transfer Act.

ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE PERSONAL CHECK and/or ATM CARD This agreement and disclosure applies to payment orders and funds transfers governed by the Electronic Fund Transfer Act.

For Card Not Present (CNP) Merchants. Card Acceptance Operating Guide

Merchants. Card Acceptance Operating Guide") For Card Not Present (CNP) Merchants Card Acceptance Operating Guide Card Acceptance Operating Guide For Card Not Present (CNP) Merchants With EMS, mail, telephone and Internet card acceptance is a simple

For Card Not Present (CNP) Merchants Card Acceptance Operating Guide Card Acceptance Operating Guide For Card Not Present (CNP) Merchants With EMS, mail, telephone and Internet card acceptance is a simple

Acceptance to Minimize Fraud

Best Practices for Credit Card Acceptance to Minimize Fraud By implementing best practices in credit card processing, you decrease the likelihood of fraudulent transactions and chargebacks. In general,

Best Practices for Credit Card Acceptance to Minimize Fraud By implementing best practices in credit card processing, you decrease the likelihood of fraudulent transactions and chargebacks. In general,

Payment Card Security Elements and Card Acceptance. Instruction

Payment Card Security Elements and Card Acceptance Instruction Content Internetbank. General requirements.... Use of Card in payment terminal.... Transaction cancellation.... Personal identification....

Payment Card Security Elements and Card Acceptance Instruction Content Internetbank. General requirements.... Use of Card in payment terminal.... Transaction cancellation.... Personal identification....

April 12, 2004. To: Verified by Visa Merchants Verified by Visa Acquirers Verified by Visa Merchant Service Providers

April 12, 2004 To: Verified by Visa Merchants Verified by Visa Acquirers Verified by Visa Merchant Service Providers The year 2003 was an active one for the Verified by Visa program, and 2004 promises

April 12, 2004 To: Verified by Visa Merchants Verified by Visa Acquirers Verified by Visa Merchant Service Providers The year 2003 was an active one for the Verified by Visa program, and 2004 promises

ANZ Credit Cards CONDITIONS OF USE

ANZ Credit Cards CONDITIONS OF USE EFFECTIVE 5 OCTOBER 2015 ANZ Credit Cards Conditions of Use These Conditions of Use (as amended from time to time) govern the use of your ANZ Visa card, ANZ Visa Gold

ANZ Credit Cards CONDITIONS OF USE EFFECTIVE 5 OCTOBER 2015 ANZ Credit Cards Conditions of Use These Conditions of Use (as amended from time to time) govern the use of your ANZ Visa card, ANZ Visa Gold

Using Your Terminal for UnionPay Cards (05/15)

") Using Your Terminal for UnionPay Cards (05/15) Contents IMPORTANT: READ FIRST... 2 UnionPay overview... 3 How to identify UnionPay cards... 4 Card entry and card verification methods... 5 Processing UnionPay

Using Your Terminal for UnionPay Cards (05/15) Contents IMPORTANT: READ FIRST... 2 UnionPay overview... 3 How to identify UnionPay cards... 4 Card entry and card verification methods... 5 Processing UnionPay

Yes, your card will expire at a given date, which is printed on the front of your card.

What is the Debenhams Prepaid Card? Debenhams Prepaid Card works in a similar way to a pay as you go mobile phone. You top up what you need, when you need it. You top the card up with money which can be

What is the Debenhams Prepaid Card? Debenhams Prepaid Card works in a similar way to a pay as you go mobile phone. You top up what you need, when you need it. You top the card up with money which can be

Payment Card Industry Data Security Standard PCI DSS

Payment Card Industry Data Security Standard PCI DSS What is PCI DSS? Requirements developed by the five card brands: VISA, Mastercard, AMEX, JCB and Discover. Their aim was to put together a common set

Payment Card Industry Data Security Standard PCI DSS What is PCI DSS? Requirements developed by the five card brands: VISA, Mastercard, AMEX, JCB and Discover. Their aim was to put together a common set

ELAVON OG UK/IRE January 2013. Operating Guide

Operating Guide Table of Contents Section 1 Introduction... 3 Section 2 Authorisation... 3 Section 3 Electronic Processing... 7 Section 4 Statements... 8 Section 5 Fraudulent Transactions... 11 Section

Operating Guide Table of Contents Section 1 Introduction... 3 Section 2 Authorisation... 3 Section 3 Electronic Processing... 7 Section 4 Statements... 8 Section 5 Fraudulent Transactions... 11 Section

FIGHTING FRAUD: IMPROVING INFORMATION SECURITY TESTIMONY OF JOHN J. BRADY VICE PRESIDENT, MERCHANT FRAUD CONTROL MASTERCARD INTERNATIONAL

FIGHTING FRAUD: IMPROVING INFORMATION SECURITY TESTIMONY OF JOHN J. BRADY VICE PRESIDENT, MERCHANT FRAUD CONTROL MASTERCARD INTERNATIONAL Before the Subcommittee on Financial Institutions and Consumer

FIGHTING FRAUD: IMPROVING INFORMATION SECURITY TESTIMONY OF JOHN J. BRADY VICE PRESIDENT, MERCHANT FRAUD CONTROL MASTERCARD INTERNATIONAL Before the Subcommittee on Financial Institutions and Consumer

FUNDS TRANSFER AGREEMENT AND DISCLOSURES

REG E DISCLOSURE This disclosure contains information about terms, fees, and interest rates for some of the accounts we offer. ELECTRONIC FUNDS TRANSFER AGREEMENT AND DISCLOSURES This form complies with

REG E DISCLOSURE This disclosure contains information about terms, fees, and interest rates for some of the accounts we offer. ELECTRONIC FUNDS TRANSFER AGREEMENT AND DISCLOSURES This form complies with

ANZ Merchant Business Solutions MERCHANT OPERATING GUIDE

ANZ Merchant Business Solutions MERCHANT OPERATING GUIDE Contents Getting Started Welcome to ANZ 2 How to Contact Us 2 Your Key Responsibilities 3 Which Cards Should you Accept? 4 Security Checks to Validate

ANZ Merchant Business Solutions MERCHANT OPERATING GUIDE Contents Getting Started Welcome to ANZ 2 How to Contact Us 2 Your Key Responsibilities 3 Which Cards Should you Accept? 4 Security Checks to Validate

SUBMITTER MERCHANT AGREEMENT PAYMENT PROCESSING INSTRUCTIONS AND GUIDELINES

SUBMITTER MERCHANT AGREEMENT PAYMENT PROCESSING INSTRUCTIONS AND GUIDELINES Paymentech, L.P. ( Paymentech or we, us or our and the like) and ( ) are excited about the opportunity to provide you with state-of-the-art

SUBMITTER MERCHANT AGREEMENT PAYMENT PROCESSING INSTRUCTIONS AND GUIDELINES Paymentech, L.P. ( Paymentech or we, us or our and the like) and ( ) are excited about the opportunity to provide you with state-of-the-art

Credit Card Conditions of Use. Credit Guide.

Credit Card Conditions of Use Credit Guide. Effective Date: September 2015 This document contains the terms and conditions that apply to St.George Bank Business Visa Debit Card cardholders and to all transactions

Credit Card Conditions of Use Credit Guide. Effective Date: September 2015 This document contains the terms and conditions that apply to St.George Bank Business Visa Debit Card cardholders and to all transactions

Online Payment Processing Definitions From Credit Research Foundation (http://www.crfonline.org/)

") Online Payment Processing Definitions From Credit Research Foundation (http://www.crfonline.org/) The following glossary represents definitions for commonly-used terms in online payment processing. Address

Online Payment Processing Definitions From Credit Research Foundation (http://www.crfonline.org/) The following glossary represents definitions for commonly-used terms in online payment processing. Address

Internet Authentication Procedure Guide

Internet Authentication Procedure Guide Authenticating cardholders successfully V10.0 Released May 2012 Software Version: Internet Authentication Protocol COPYRIGHT NOTICE No part of this publication may

Internet Authentication Procedure Guide Authenticating cardholders successfully V10.0 Released May 2012 Software Version: Internet Authentication Protocol COPYRIGHT NOTICE No part of this publication may

Expect to know where you stand with your Visa Debit Card

Expect to know where you stand with your Visa Debit Card VISA DEBIT CONDITIONS OF USE Acceptance of Conditions of Use 1.1 By using your Debit Card, you agree that these Conditions of Use are binding on:

Expect to know where you stand with your Visa Debit Card VISA DEBIT CONDITIONS OF USE Acceptance of Conditions of Use 1.1 By using your Debit Card, you agree that these Conditions of Use are binding on:

Merchant Facility Terms and Conditions 4. 1 Introduction 4. 1.1 Purpose of these Terms and Conditions 4. 2 Merchant Services 4. 2.1 Our obligations 4

Table of Contents Merchant Facility Terms and Conditions 4 1 Introduction 4 1.1 Purpose of these Terms and Conditions 4 2 Merchant Services 4 2.1 Our obligations 4 3 Your obligations 5 3.1 General obligations

Table of Contents Merchant Facility Terms and Conditions 4 1 Introduction 4 1.1 Purpose of these Terms and Conditions 4 2 Merchant Services 4 2.1 Our obligations 4 3 Your obligations 5 3.1 General obligations

credit card Conditions of Use

VISA credit card Conditions of Use EFFECTIVE FROM 20 MARCH 2013 a refreshing attitude to banking QUEENSLAND COUNTRY CREDIT UNION VISA CREDIT CARD 1 Contents 1. Introduction 3 2. Additional Cards 3 3. Application

VISA credit card Conditions of Use EFFECTIVE FROM 20 MARCH 2013 a refreshing attitude to banking QUEENSLAND COUNTRY CREDIT UNION VISA CREDIT CARD 1 Contents 1. Introduction 3 2. Additional Cards 3 3. Application

2 Scroll button 8 Power button

PAX User Guide. 1 Table of contents. Keypad layout 3 Debit card purchase 4 Credit and charge card purchase 5 Processing a purchase when tipping is enabled 6 Processing a purchase with cash out when tipping

PAX User Guide. 1 Table of contents. Keypad layout 3 Debit card purchase 4 Credit and charge card purchase 5 Processing a purchase when tipping is enabled 6 Processing a purchase with cash out when tipping

Contents. HSBC Merchant Services

Contents Section Page Welcome 1 HSBC Merchant Services 1 About This Document 1 An Introduction To Card Processing 3 Risk Awareness 4 Card Present Transactions 8 Checking Cards 8 Accepting Cards Using An

Contents Section Page Welcome 1 HSBC Merchant Services 1 About This Document 1 An Introduction To Card Processing 3 Risk Awareness 4 Card Present Transactions 8 Checking Cards 8 Accepting Cards Using An

www.fpcu.org RELOADABLE PREPAID CARD

www.fpcu.org RELOADABLE PREPAID CARD terms AND CONDITIONS Effective 5.1.12 The following are your Financial Partners Credit Union MASTERCARD Reloadable Prepaid Card Terms and Conditions. Except as the

www.fpcu.org RELOADABLE PREPAID CARD terms AND CONDITIONS Effective 5.1.12 The following are your Financial Partners Credit Union MASTERCARD Reloadable Prepaid Card Terms and Conditions. Except as the

MasterCard Special Edition

2015 An Empower Federal Credit Union publication. MasterCard Special Edition Important details about our MasterCard conversion. Message From The President John Wakefield President/CEO Why MasterCard? For

2015 An Empower Federal Credit Union publication. MasterCard Special Edition Important details about our MasterCard conversion. Message From The President John Wakefield President/CEO Why MasterCard? For

increase your resistance How card not present gaming companies can minimise the risk of losing money through chargebacks

increase your resistance How card not present gaming companies can minimise the risk of losing money through chargebacks payment acceptance protect yourself We know that receiving a chargeback can cause

increase your resistance How card not present gaming companies can minimise the risk of losing money through chargebacks payment acceptance protect yourself We know that receiving a chargeback can cause