ARIZONA TRANSACTION PRIVILEGE TAX AND USE TAX

|

|

|

- Agnes Harris

- 9 years ago

- Views:

Transcription

1 ARIZONA TRANSACTION PRIVILEGE TAX AND USE TAX

2 DEFINITION TRANSACTION PRIVILEGE TAX Commonly referred to as sales tax, TPT is tax on the retail sale of tangible personal property and certain services. Retail Sale Sale to end user End user Each state defines it differently Special case in AZ, a MRRA contractor is an end user Tangible can be touched, felt, tasted Special case in AZ, downloadable software is tangible personal property Personal Property Property that is not land or a building or anything attached to land and a building Special case counters in a bank

3 THE GENERAL RULES The University of Arizona is not a non-profit organization and is not exempt from sales/use tax. Sales to a non-profit organization Generally not exempt Sales by a non-profit organization Generally exempt Goods Generally taxable unless specifically exempt Services Generally exempt unless specifically taxable Examples of taxable services include: transportation, utilities, telecommunications, photographer s services, and amusements

4 SALES TAX RATES For transactions involving retail, restaurants, utilities, communications, job printing, publication, rent of personal property, amusements, etc AZ State 5.6% Pima County 0.5% Tucson 0% when UA is seller UA is exempt from collecting Tucson tax from its customers, but: Tucson 2-4% when UA is buyer UA pays 2% to vendors retail, restaurants, communications, job printing, publication, rent of personal property and amusements UA pays 4% to vendors public utilities

5 SALES TAX RATES - SUMMARY Description Tax % (when selling) Tax % (when buying) AZ State 5.60% 5.60% Pima County* 0.50% 0.50% Tucson City 0% 2-4% Total 6.10% 8.10%-10.10% *This may change when selling/buying from different counties

6 DEFINITION USE TAX Self-assessed tax on the use, storage, or consumption of tangible personal property Sales tax was not levied by the vendor The purchase is otherwise taxable in Arizona Example: Purchase from an out of state vendor who does not have an Arizona TPT license

7 USE TAX RATE AZ State 5.60% Counties generally do not impose use tax The University of Arizona is not subject to city tax

8 SALES OR USE TAX? So, how do you know if it s sales tax or use tax? Does it make a difference? Sales and use tax are complementary Pay only sales tax or use tax Vendors charge sales tax Use tax is self-assessed

9 WHAT IS NEXUS? Nexus means connection, or linkage. Factors that can create nexus: Renting or owning property Business presence in the state Trade shows (except Nevada/Florida) Presence of agents/contractors/employees Consequence of having nexus Register as a retailer in that state Collect taxes File returns Remit payment to the state

10 NON-TAXABLE TRANSACTIONS Professional/personal services, unless: They are specifically taxable, such as: Transportation, utilities, telecommunications, and photographer s services Repair/maintenance and installation services, unless: Taxable if not separately disclosed on invoice Taxable if installation is to be attached to real property Shipping services/freight charges, unless: Taxable if handling is included Warranty services/service contracts Be careful, if related to software, it MAY be taxable Conference registration fees

11 MORE NON-TAXABLE TRANSACTIONS Professional membership dues Textbooks/required course materials Printed and other media materials (available to the public) by UA Libraries Unprepared food for home (human) consumption Medically prescribed drugs, equipment or devices Purchase for resale Others as set forth in statutes such as ARS or ARS

12 MACHINERY & EQUIPMENT USED FOR RESEARCH Machinery or equipment used for research Tax exempt Must be 100% research use Dollar amount is not a factor Machinery or equipment does not include: Expendable materials and supplies Office equipment, furniture and supplies Hand tools Janitorial equipment Licensed motor vehicles Shops, buildings, depots A repair or replacement part of tax-exempt research equipment is also exempt Leases and rentals of tax-exempt research equipment are exempt

(14) to claim exemption from sales tax Use exemption ARS 42-5159(B)(14) to claim exemption")

13 MACHINERY & EQUIPMENT USED FOR RESEARCH Research does not include: Social sciences Psychology Routine consumer product testing Computer software development Non-technological activities or technical services PCs, laptops and portable devices are almost never tax exempt Computers used in research of computer software Not tax exempt Use exemption ARS (B)(14) to claim exemption from sales tax Use exemption ARS (B)(14) to claim exemption from use tax

(14) to claim exemption from sales tax Use exemption ARS 42-5159(B)(14) to claim exemption")

14 CHEMICALS USED FOR RESEARCH Chemicals used directly in research are tax exempt Exempt chemicals cannot be used or consumed in: Packaging Storage Transportation Researcher who orders the item must determine whether it is chemical Use exemption ARS (A)(38) to claim exemption from sales tax Use exemption ARS (A)(35) to claim exemption from use tax

(35) to claim exemption from")

and")

15 COMPUTER HARDWARE & SOFTWARE Purchase of hardware and standard, pre-written or canned software: Almost never* exempt Purchase of tangible, regardless of delivery *Purchase of customized software: Designed exclusively to the specifications of a UA unique application Modification of standard software at installation does not make it custom Not taxable Purchase of services *Purchase (by a community college or university) of remote software applications that either: Are designed to assess or test student learning, or Promote curriculum design and enhancement Not taxable ARS (53) and ARS (50)

and")

16 HARDWARE & SOFTWARE SERVICES Computer services such as analysis, design, repair, and support engineering: Not taxable Maintenance and warranty agreement for hardware and software: Generally not taxable if: Sold as a separate item, and The price is stated separately Software agreement including updates, upgrades, modification or revisions to a standard software: Taxable

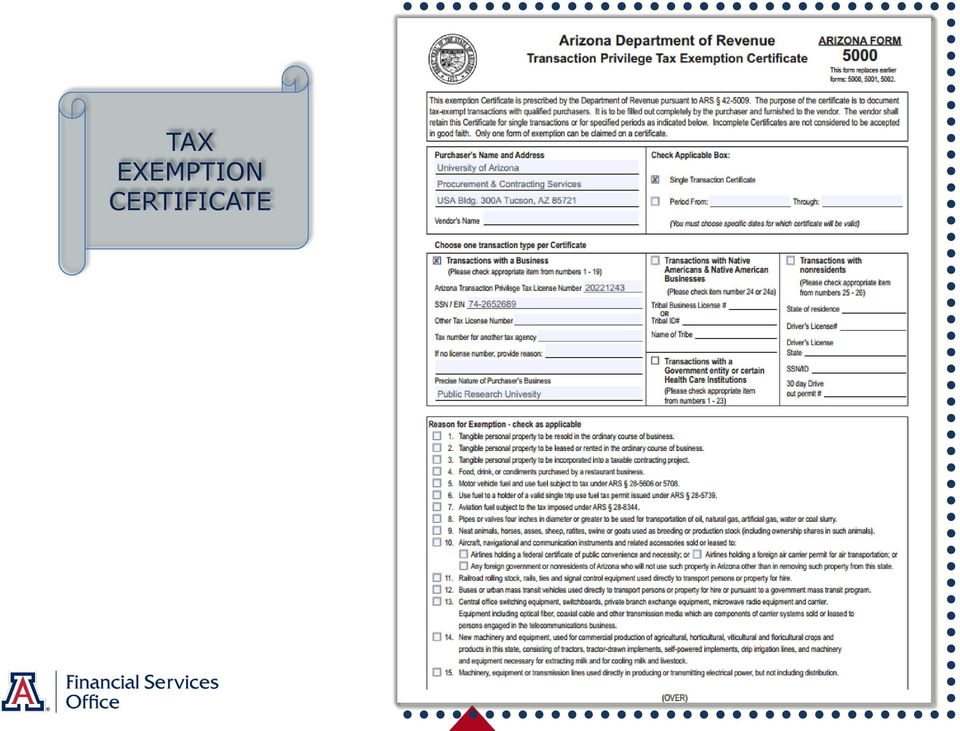

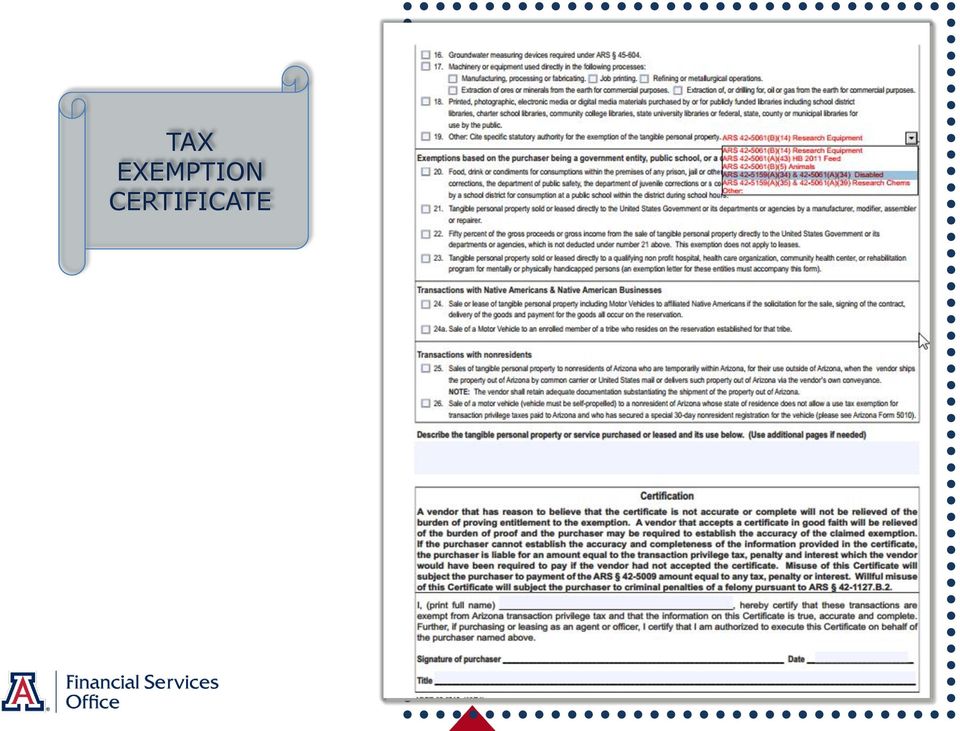

17 CLAIMING THE TAX EXEMPTION FROM A VENDOR Vendors must document tax exempt transactions: Tax exemption certificate (Arizona Form 5000) is required and provides: University s Federal Tax ID ( ), AZ TPT License Number ( ), Reason for exemption, and The signature of the individual authorizing the purchase Arizona Form 5000 for a PCard purchase: Provided to the vendor (prior to transaction) by the department Signed by the departmental individual who authorizes the purchase Certificate is located on E-Forms and on the Financial Services Office Tax Services webpage:

18 TAX EXEMPTION CERTIFICATE

19 TAX EXEMPTION CERTIFICATE

20 PCARD USE TAX EXEMPTION PCard reconcilers avoid erroneous assessment of use tax by: Entering the sales tax amount in the Enter Sales Tax field when sales tax is charged by the vendor, or Checking the Tax Exempt Indicator box in UAccess Financials when the transaction is tax exempt, or Checking the Tax Exempt Indicator box in UAccess Financials when sales tax is charged but amount cannot be identified Taxes are always included in the total price for the following: Airline tickets Telecommunication charges (Verizon/ AT&T / Sprint, etc.) Use tax is not automatically assessed on the following object codes: 3820, 3870, 5520, 5540, 5560, 5810, 5830, 5850, 7810, 7820, 7830, and 9175

Taxable vs.")

21 UNIVERSITY AS A SELLER We work together to properly collect and remit TPT Department s responsibilities: Identify taxable sales for Arizona customers Collect the correct tax Use proper object codes (refer to Financial Services Manual 8.11) Taxable vs. non-taxable Deposit revenue and tax in University accounts Maintain detailed records of sales activities FSO s responsibilities: Prepare TPT return Remit tax receipts to the State of Arizona Provide guidance to Departments

published in AZ Publisher is liable for sales tax even if the customer subscribes from")

22 COMMON ISSUE: PUBLICATION Publication (e.g. newspapers, magazines, journals) published in AZ Publisher is liable for sales tax even if the customer subscribes from out-of-state, except for: Tourist magazines that promote tourism and travel in Arizona

23 GENERAL ERROR CORRECTION FOR USE TAX Step 1 Review transactions where use tax was wrongly charged UAccess Analytics >General Financial Management >Transactions>Include relevant account/org information>doc Type (PCDO) Change the report format Detailed by Fund Group by Account and Object code Export data to excel where it can be sorted to see if use tax was charged and whether it needs correction If use tax has been wrongly charged, see step 2

24 GENERAL ERROR CORRECTION FOR USE TAX Step 2 GEC Main menu>transactions>general Error Correction Click on GEC

25 GENERAL ERROR CORRECTION FOR USE TAX Step 2 continued Description Reversal of use tax Explanation Brief explanation why All entries would be in the From section Reducing expense and liability from the account Chart UA Reducing expenses Account # - Account # in which the expense was charged Object code Object code in which the expense was charged Reference Origin Code 01 Reference Number Original doc # where the expense was charged Line Description Reversal of use tax Amount Use tax charged Click Add

26 GENERAL ERROR CORRECTION FOR USE TAX Step 2 continued Reducing liability Account # Object code 9190 Reference Origin Code 01 Reference Number Original doc # where the expense was charged Line Description Reversal of use tax Amount Use tax charged Click Add Notes and Attachments - Include detailed explanation why the transaction is not taxable Optional if details are included in Explanation box Submit Please note Use tax can be reversed only for prior periods in the current fiscal year

27 EXAMPLE OF A COMPLETED GEC

28 IN REVIEW: THE GENERAL RULES Purchase and sale of tangible property is generally taxable, unless specifically exempt Purchase and sale of services is generally exempt, unless specifically taxed If taxable goods are purchased from an out of state vendor without Arizona nexus, self-assess use tax If an item does not fit into machinery or equipment used in research or chemical used in research, it generally DOES NOT qualify for tax exemption

29 UNIVERSITY AS A BUYER

30 UNIVERSITY AS A SELLER

31 RESOURCES AND CONTACT INFORMATION Tax Services Arizona Sales and Use Tax page: For assistance to determine the taxability of a purchase/sale: [email protected] FSO-Tax Compliance: For assistance to record the purchase, sales and related tax, or correction of use tax: FSO-Financial Management: or

32 QUESTIONS?

Sales and Use Taxes: Texas

Jay M. Chadha, Fulbright & Jaworski LLP A Q&A guide to sales and use tax law in Texas. This Q&A addresses key areas of sales and use tax law such as tax scope, multi-state transactions and collecting taxes

Jay M. Chadha, Fulbright & Jaworski LLP A Q&A guide to sales and use tax law in Texas. This Q&A addresses key areas of sales and use tax law such as tax scope, multi-state transactions and collecting taxes

TENNESSEE DEPARTMENT OF REVENUE REVENUE RULING # 07-05 WARNING

TENNESSEE DEPARTMENT OF REVENUE REVENUE RULING # 07-05 WARNING Revenue rulings are not binding on the Department. This presentation of the ruling in a redacted form is information only. Rulings are made

TENNESSEE DEPARTMENT OF REVENUE REVENUE RULING # 07-05 WARNING Revenue rulings are not binding on the Department. This presentation of the ruling in a redacted form is information only. Rulings are made

Section 1: Georgia Sales and Use Tax Principles Presented by Ned A. Lenhart, CMI, CPA

Page 1 of 9 Section 1: Georgia Sales and Use Tax Principles Presented by Ned A. Lenhart, CMI, CPA The objective of this section is to introduce and review some of the foundational components of Georgia

Page 1 of 9 Section 1: Georgia Sales and Use Tax Principles Presented by Ned A. Lenhart, CMI, CPA The objective of this section is to introduce and review some of the foundational components of Georgia

SENATE BILL No. 372 page 2

SENATE BILL No. 372 AN ACT relating to sales taxation; concerning the sourcing of mobile telecommunications services; amending K.S.A. 2001 Supp. 79-3603 and repealing the existing section; also repealing

SENATE BILL No. 372 AN ACT relating to sales taxation; concerning the sourcing of mobile telecommunications services; amending K.S.A. 2001 Supp. 79-3603 and repealing the existing section; also repealing

IOWA SALES / USE TAX BASICS. Terry O Neill Taxpayer Service Specialist

IOWA SALES / USE TAX BASICS Terry O Neill Taxpayer Service Specialist Agenda Sales tax and use tax what s the difference? What is taxable? What rate of tax do I charge? What is local option sales tax?

IOWA SALES / USE TAX BASICS Terry O Neill Taxpayer Service Specialist Agenda Sales tax and use tax what s the difference? What is taxable? What rate of tax do I charge? What is local option sales tax?

State, Local Tax Structure Base State, Local Tax Structure, the State of Ohio

, Structure Base, Structure, the of Income / LLC; S-Corporation; General es $150, plus 0.26% on excess receipts over $1.0 million. All out-of-state sales are exempt NOTE: The following organizations are

, Structure Base, Structure, the of Income / LLC; S-Corporation; General es $150, plus 0.26% on excess receipts over $1.0 million. All out-of-state sales are exempt NOTE: The following organizations are

BUSINESS BASICS A GUIDE TO TAXES FOR ARIZONA BUSINESSES

This publication is designed to help Arizona businesses comply with the state s basic tax and licensing requirements. In case of inconsistency or omission in this publication, the language of the Arizona

This publication is designed to help Arizona businesses comply with the state s basic tax and licensing requirements. In case of inconsistency or omission in this publication, the language of the Arizona

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING # 10-24 WARNING

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING # 10-24 WARNING Letter rulings are binding on the Department only with respect to the individual taxpayer being addressed in the ruling. This presentation

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING # 10-24 WARNING Letter rulings are binding on the Department only with respect to the individual taxpayer being addressed in the ruling. This presentation

ST-1 Instructions. General Information

Illinois Department of Revenue ST-1 Instructions Who must file Form ST-1? You must file Form ST-1, Sales and Use Tax and E911 Surcharge Return, if you are making retail sales of any of the following in

Illinois Department of Revenue ST-1 Instructions Who must file Form ST-1? You must file Form ST-1, Sales and Use Tax and E911 Surcharge Return, if you are making retail sales of any of the following in

BEFORE THE TAX COMMISSION OF THE STATE OF IDAHO ) ) ) ) ) ) On June 13, 2008, the staff of the Sales Tax Audit Bureau (Bureau) of the Idaho State

) ) ) ) ) On June 13, 2008, the staff of the Sales Tax Audit Bureau (Bureau) of the Idaho State") BEFORE THE TAX COMMISSION OF THE STATE OF IDAHO In the Matter of the Protest of, Petitioner. DOCKET NO. 21395 DECISION On June 13, 2008, the staff of the Sales Tax Audit Bureau (Bureau of the Idaho State

BEFORE THE TAX COMMISSION OF THE STATE OF IDAHO In the Matter of the Protest of, Petitioner. DOCKET NO. 21395 DECISION On June 13, 2008, the staff of the Sales Tax Audit Bureau (Bureau of the Idaho State

This letter concerns tangible personal property transferred incident to sales of service. See 86 Ill. Adm. Code 140.01. (This is a GIL.

ST 08-0176-GIL 12/10/2008 SERVICE OCCUPATION TAX This letter concerns tangible personal property transferred incident to sales of service. See 86 Ill. Adm. Code 140.01. (This is a GIL.) December 10, 2008

ST 08-0176-GIL 12/10/2008 SERVICE OCCUPATION TAX This letter concerns tangible personal property transferred incident to sales of service. See 86 Ill. Adm. Code 140.01. (This is a GIL.) December 10, 2008

STATE OF ARIZONA Department of Revenue

STATE OF ARIZONA Department of Revenue Janice K. Brewer Governor PRIVATE TAXPAYER RULING LR13-002 John A. Greene Director The Department issues this private taxpayer ruling in response to your letters

STATE OF ARIZONA Department of Revenue Janice K. Brewer Governor PRIVATE TAXPAYER RULING LR13-002 John A. Greene Director The Department issues this private taxpayer ruling in response to your letters

SALES AND USE TAX TECHNICAL BULLETINS SECTION 18

SECTION 18 - CERTAIN GOVERNMENTAL ENTITIES - THE STATE, COUNTIES, CITIES AND OTHER POLITICAL SUBDIVISIONS 18-1 PURCHASES AND SALES BY AND DONATIONS TO GOVERNMENTAL ENTITIES A. Purchases By Governmental

SECTION 18 - CERTAIN GOVERNMENTAL ENTITIES - THE STATE, COUNTIES, CITIES AND OTHER POLITICAL SUBDIVISIONS 18-1 PURCHASES AND SALES BY AND DONATIONS TO GOVERNMENTAL ENTITIES A. Purchases By Governmental

ENGROSSED HOUSE By: Deutschendorf of the House. ( revenue and taxation amending 68 O.S., Section. 1352 definitions - Sales Tax Code effective

ENGROSSED HOUSE BILL NO. 2736 By: Deutschendorf of the House and Robinson of the Senate ( revenue and taxation amending 68 O.S., Section 1352 definitions - Sales Tax Code effective date emergency ) BE

ENGROSSED HOUSE BILL NO. 2736 By: Deutschendorf of the House and Robinson of the Senate ( revenue and taxation amending 68 O.S., Section 1352 definitions - Sales Tax Code effective date emergency ) BE

Changes in Arkansas Sales and Use Tax Law Effective January 1, 2008

STATE OF ARKANSAS Department of Finance and Administration http://www.arkansas.gov/dfa SALES & USE TAX SECTION P. O. BOX 1272 LITTLE ROCK, AR 72203-1272 PHONE: (501) 682-7104 FAX: (501) 682-7904 [email protected]

STATE OF ARKANSAS Department of Finance and Administration http://www.arkansas.gov/dfa SALES & USE TAX SECTION P. O. BOX 1272 LITTLE ROCK, AR 72203-1272 PHONE: (501) 682-7104 FAX: (501) 682-7904 [email protected]

STATE OF ARIZONA Department of Revenue Office of the Director (602) 716-6090

716-6090") STATE OF ARIZONA Department of Revenue Office of the Director (602) 716-6090 Janet Napolitano Governor CERTIFIED MAIL Gale Garriott Director The Director's Review of the Decision ) O R D E R of the Administrative

STATE OF ARIZONA Department of Revenue Office of the Director (602) 716-6090 Janet Napolitano Governor CERTIFIED MAIL Gale Garriott Director The Director's Review of the Decision ) O R D E R of the Administrative

BULK SALES - BUYING AND SELLING BUSINESS ASSETS

BULLETIN NO. TAMTA 002 Issued October 2010 THE TAX ADMINISTRATION AND MISCELLANEOUS TAXES ACT BULK SALES - BUYING AND SELLING BUSINESS ASSETS This bulletin explains the seller s and buyer s requirements

BULLETIN NO. TAMTA 002 Issued October 2010 THE TAX ADMINISTRATION AND MISCELLANEOUS TAXES ACT BULK SALES - BUYING AND SELLING BUSINESS ASSETS This bulletin explains the seller s and buyer s requirements

ACCOUNTING FOR SALES TAX PROFESSIONALS

ACCOUNTING FOR IPT ANNUAL CONFERENCE SALES TAX PROFESSIONALS Suzanne Wilson Jeff McGhehey, CMI Sr. Mgr. Transaction Tax Sr. Mgr. Indirect Tax American Airlines The Home Depot Phoenix, AZ Atlanta, GA [email protected]

ACCOUNTING FOR IPT ANNUAL CONFERENCE SALES TAX PROFESSIONALS Suzanne Wilson Jeff McGhehey, CMI Sr. Mgr. Transaction Tax Sr. Mgr. Indirect Tax American Airlines The Home Depot Phoenix, AZ Atlanta, GA [email protected]

SC PRIVATE LETTER RULING #07-7. Sales of Photograph Prints via an Internet Website (Sales and Use Tax)

") State of South Carolina Department of Revenue 301 Gervais Street, P.O. Box 125, Columbia, South Carolina 29214 Website Address: http://www.sctax.org SC PRIVATE LETTER RULING #07-7 SUBJECT: Sales of Photograph

State of South Carolina Department of Revenue 301 Gervais Street, P.O. Box 125, Columbia, South Carolina 29214 Website Address: http://www.sctax.org SC PRIVATE LETTER RULING #07-7 SUBJECT: Sales of Photograph

SALES AND USE TAX TECHNICAL BULLETINS SECTION 7 PRINTERS, NEWSPAPER OR MAGAZINE PUBLISHERS AND BOOKBINDERS

SECTION 7 - PRINTERS, NEWSPAPER OR MAGAZINE PUBLISHERS AND BOOKBINDERS 7-1 COMMERCIAL PRINTERS AND PUBLISHERS A. All retail sales of tangible personal property by commercial printers or publishers are

SECTION 7 - PRINTERS, NEWSPAPER OR MAGAZINE PUBLISHERS AND BOOKBINDERS 7-1 COMMERCIAL PRINTERS AND PUBLISHERS A. All retail sales of tangible personal property by commercial printers or publishers are

Sales and Use Tax on Construction, Improvements, Installations and Repairs

Sales and Use Tax on Construction, Improvements, Installations and Repairs GT-800067 R.09/14 In Florida, the taxing of property improvements, installation, and repairs varies according to the exact nature

Sales and Use Tax on Construction, Improvements, Installations and Repairs GT-800067 R.09/14 In Florida, the taxing of property improvements, installation, and repairs varies according to the exact nature

INFORMATION BULLETIN #28WC SALES TAX AUGUST 2008. (replaces Information Bulletin #28WC, dated May, 2007)

") INFORMATION BULLETIN #28WC SALES TAX AUGUST 2008 (replaces Information Bulletin #28WC, dated May, 2007) DISCLAIMER: SUBJECT: Informational bulletins are intended to provide nontechnical assistance to the

INFORMATION BULLETIN #28WC SALES TAX AUGUST 2008 (replaces Information Bulletin #28WC, dated May, 2007) DISCLAIMER: SUBJECT: Informational bulletins are intended to provide nontechnical assistance to the

SALES AND USE TAX TECHNICAL BULLETINS SECTION 17

SECTION 17 - NONPROFIT ENTITIES - HOSPITALS, EDUCATIONAL INSTITUTIONS, CHURCHES, ORPHANAGES AND OTHER CHARITABLE OR RELIGIOUS INSTITUTIONS AND ORGANIZATIONS AND QUALIFIED RETIREMENT FACILITIES WHOSE PROPERTY

SECTION 17 - NONPROFIT ENTITIES - HOSPITALS, EDUCATIONAL INSTITUTIONS, CHURCHES, ORPHANAGES AND OTHER CHARITABLE OR RELIGIOUS INSTITUTIONS AND ORGANIZATIONS AND QUALIFIED RETIREMENT FACILITIES WHOSE PROPERTY

Exempt Organizations: Sales and Purchases

Exempt Organizations: Sales and Purchases Susan Combs, Texas Comptroller of Public Accounts DECEMBER 2010 Organizations that have applied for and received a letter of exemption from sales tax don t have

Exempt Organizations: Sales and Purchases Susan Combs, Texas Comptroller of Public Accounts DECEMBER 2010 Organizations that have applied for and received a letter of exemption from sales tax don t have

Frequently Asked Questions: The New Computer and Software Services Tax Effective 7/31/13

Frequently Asked Questions: The New Computer and Software Services Tax Effective 7/31/13 The Department has received a number of questions about the new sales and use tax applicable to computer system

Frequently Asked Questions: The New Computer and Software Services Tax Effective 7/31/13 The Department has received a number of questions about the new sales and use tax applicable to computer system

PST-5 Issued: June 1984 Revised: August 2015 GENERAL INFORMATION

Information Bulletin PST-5 Issued: June 1984 Revised: August 2015 Was this bulletin useful? THE PROVINCIAL SALES TAX ACT GENERAL INFORMATION Click here to complete our short READER SURVEY This bulletin

Information Bulletin PST-5 Issued: June 1984 Revised: August 2015 Was this bulletin useful? THE PROVINCIAL SALES TAX ACT GENERAL INFORMATION Click here to complete our short READER SURVEY This bulletin

SALES AND USE TAX TECHNICAL BULLETINS SECTION 20

SECTION 20 - RADIO, TELEVISION AND CABLE TELEVISION STATIONS, MOTION PICTURE THEATRES, VIDEO PROGRAMMING PROVIDERS, AND SATELLITE DIGITAL AUDIO RADIO SERVICE PROVIDERS 20-1 RECEIPTS FROM VIDEO PROGRAMMING

SECTION 20 - RADIO, TELEVISION AND CABLE TELEVISION STATIONS, MOTION PICTURE THEATRES, VIDEO PROGRAMMING PROVIDERS, AND SATELLITE DIGITAL AUDIO RADIO SERVICE PROVIDERS 20-1 RECEIPTS FROM VIDEO PROGRAMMING

COLORADO DEPARTMENT OF REVENUE GUIDE TO THE MANAGED AUDIT PROGRAM FOR SALES AND USE TAXES

GUIDE TO THE FOR SALES AND USE TAXES AS OF June 29, 2007 Contents Preface Introduction to the Managed Audit Program............... 3 Reviewing your sales.................................... 5 Reviewing

GUIDE TO THE FOR SALES AND USE TAXES AS OF June 29, 2007 Contents Preface Introduction to the Managed Audit Program............... 3 Reviewing your sales.................................... 5 Reviewing

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING # 11-29 WARNING

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING # 11-29 WARNING Letter rulings are binding on the Department only with respect to the individual taxpayer being addressed in the ruling. This presentation

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING # 11-29 WARNING Letter rulings are binding on the Department only with respect to the individual taxpayer being addressed in the ruling. This presentation

CHAPTER 57-39.2 SALES TAX

CHAPTER 57-39.2 SALES TAX 57-39.2-01. (Effective for taxable events occurring through June 30, 2017) Definitions. The following words, terms, and phrases, when used in this chapter, have the meaning ascribed

CHAPTER 57-39.2 SALES TAX 57-39.2-01. (Effective for taxable events occurring through June 30, 2017) Definitions. The following words, terms, and phrases, when used in this chapter, have the meaning ascribed

DR-15. Instructions for. Sales and Use Tax Returns. www.myflorida.com/dor. Use the correct tax return for each reporting period.

Instructions for DR-15 Sales and Use Tax Returns DR-15N R. 01/15 Rule 12A-1.097 Florida Administrative Code Effective 01/15 Use the correct tax return for each reporting period. To receive a collection

Instructions for DR-15 Sales and Use Tax Returns DR-15N R. 01/15 Rule 12A-1.097 Florida Administrative Code Effective 01/15 Use the correct tax return for each reporting period. To receive a collection

State Tax Chart Results

Tax Chart Results Tax Type: Sales/Use Advertising Services This chart shows whether or not the state taxes advertising services. Advertising MI Not taxable When an advertising agency goes beyond the rendering

Tax Chart Results Tax Type: Sales/Use Advertising Services This chart shows whether or not the state taxes advertising services. Advertising MI Not taxable When an advertising agency goes beyond the rendering

TENNESSEE DEPARTMENT OF REVENUE REVENUE RULING # 04-20 WARNING

TENNESSEE DEPARTMENT OF REVENUE REVENUE RULING # 04-20 WARNING Revenue rulings are not binding on the Department. This presentation of the ruling in a redacted form is information only. Rulings are made

TENNESSEE DEPARTMENT OF REVENUE REVENUE RULING # 04-20 WARNING Revenue rulings are not binding on the Department. This presentation of the ruling in a redacted form is information only. Rulings are made

How To Pay For A Computer In Wisconsin

32 Wisconsin Tax Bulletin 152 July 2007 Wisconsin Department of Revenue Frequently Asked Questions Sales and Use Tax Treatment Computer Hardware, Software, Services 1. What computer hardware, software,

32 Wisconsin Tax Bulletin 152 July 2007 Wisconsin Department of Revenue Frequently Asked Questions Sales and Use Tax Treatment Computer Hardware, Software, Services 1. What computer hardware, software,

Title 61 REVENUE AND TAXATION Part I. Taxes Collected and Administered by the Secretary of Revenue * * *

RULE Department of Revenue Policy Services Division Definition of Tangible Personal Property (LAC 61:I.4301) Under the authority of R.S. 47:301 and R.S. 47:1511 and in accordance with the provisions of

RULE Department of Revenue Policy Services Division Definition of Tangible Personal Property (LAC 61:I.4301) Under the authority of R.S. 47:301 and R.S. 47:1511 and in accordance with the provisions of

Article Tax General. In this title the following words have the meanings indicated. (1) acquires tangible personal property in a sale; or

acquires tangible personal property in a sale; or") Article Tax General [Previous][Next] 11 101. (a) (b) In this title the following words have the meanings indicated. Buyer means a person who: (1) acquires tangible personal property in a sale; or (2) obtains

Article Tax General [Previous][Next] 11 101. (a) (b) In this title the following words have the meanings indicated. Buyer means a person who: (1) acquires tangible personal property in a sale; or (2) obtains

General Transitional Rules for the Re-implementation of the Provincial Sales Tax Provincial Sales Tax Act

Provincial Sales Tax (PST) Notice Notice 2012-010 Issued: October 15, 2012 Revised: February 18, 2013 General Transitional Rules for the Re-implementation of the Provincial Sales Tax Provincial Sales Tax

Provincial Sales Tax (PST) Notice Notice 2012-010 Issued: October 15, 2012 Revised: February 18, 2013 General Transitional Rules for the Re-implementation of the Provincial Sales Tax Provincial Sales Tax

Georgia Sales and Use Tax Issues For Nonprofits Organizations. April 14, 2009

Georgia Sales and Use Tax Issues For Nonprofits Organizations April 14, 2009 Overview Application of Sales/Use Taxes to Nonprofits Scope of Sales/Use Taxes in General Potential Exemptions/Exclusions From

Georgia Sales and Use Tax Issues For Nonprofits Organizations April 14, 2009 Overview Application of Sales/Use Taxes to Nonprofits Scope of Sales/Use Taxes in General Potential Exemptions/Exclusions From

November 26, 2013. 1. COMPANY 1 (The Company) sells Software as follows:

sells Software as follows:") ST 13-0076-GIL 11/26/2013 COMPUTER SOFTWARE If transactions for the licensing of computer software meet all of the criteria provided in subsection (a)(1) of Section 130.1935, neither the transfer of the

ST 13-0076-GIL 11/26/2013 COMPUTER SOFTWARE If transactions for the licensing of computer software meet all of the criteria provided in subsection (a)(1) of Section 130.1935, neither the transfer of the

Tax Commission. #14 motor vehicles. (Selling, Leasing & Renting) An Educational Guide to Sales Tax in the State of Idaho

An Educational Guide to Sales Tax in the State of Idaho") Tax Commission Idaho #14 motor vehicles (Selling, Leasing & Renting) An Educational Guide to Sales Tax in the State of Idaho This brochure is intended to help motor vehicle dealers, leasing companies,

Tax Commission Idaho #14 motor vehicles (Selling, Leasing & Renting) An Educational Guide to Sales Tax in the State of Idaho This brochure is intended to help motor vehicle dealers, leasing companies,

TAX COMPARISON 2014-2015

TAX COMPARISON 01-015 Between Caroline City of Fredericksburg King George Stafford Prepared by of Spotsylvania Department of Economic Development & Tourism 9019 Old Battlefield Boulevard, Suite 10 Spotsylvania,

TAX COMPARISON 01-015 Between Caroline City of Fredericksburg King George Stafford Prepared by of Spotsylvania Department of Economic Development & Tourism 9019 Old Battlefield Boulevard, Suite 10 Spotsylvania,

INFORMATION BULLETIN #8 SALES TAX NOVEMBER 2011. (Replaces Bulletin #8 dated May 2002)

") INFORMATION BULLETIN #8 SALES TAX NOVEMBER 2011 (Replaces Bulletin #8 dated May 2002) DISCLAIMER: SUBJECT: Information bulletins are intended to provide nontechnical assistance to the general public. Every

INFORMATION BULLETIN #8 SALES TAX NOVEMBER 2011 (Replaces Bulletin #8 dated May 2002) DISCLAIMER: SUBJECT: Information bulletins are intended to provide nontechnical assistance to the general public. Every

Instructions for City of Colorado Springs Sales and/or Use Tax Returns

Instructions for City of Colorado Springs Sales and/or Use Tax Returns Return MUST be filed even if there is NO tax due Make check payable to the City of Colorado Springs Retain returns and supporting

Instructions for City of Colorado Springs Sales and/or Use Tax Returns Return MUST be filed even if there is NO tax due Make check payable to the City of Colorado Springs Retain returns and supporting

MAINE REVENUE SERVICES SALES, FUEL & SPECIAL TAX DIVISION INSTRUCTIONAL BULLETIN NO. 3

MAINE REVENUE SERVICES SALES, FUEL & SPECIAL TAX DIVISION INSTRUCTIONAL BULLETIN NO. 3 PHOTOGRAPHERS AND PHOTOFINISHERS This bulletin is intended solely as advice to assist persons in determining, exercising

MAINE REVENUE SERVICES SALES, FUEL & SPECIAL TAX DIVISION INSTRUCTIONAL BULLETIN NO. 3 PHOTOGRAPHERS AND PHOTOFINISHERS This bulletin is intended solely as advice to assist persons in determining, exercising

Computer Data Center Program (Established under A.R.S. 41-1519) INSTRUCTIONS FOR APPLICATION FOR CDC CERTIFICATION 1

INSTRUCTIONS FOR APPLICATION FOR CDC CERTIFICATION 1") A. Background Computer Data Center Program (Established under A.R.S. 41-1519) INSTRUCTIONS FOR APPLICATION FOR CDC CERTIFICATION 1 The Arizona Legislature in 2013 established the Computer Data Center program

A. Background Computer Data Center Program (Established under A.R.S. 41-1519) INSTRUCTIONS FOR APPLICATION FOR CDC CERTIFICATION 1 The Arizona Legislature in 2013 established the Computer Data Center program

City and County of Denver. General Tax Information Booklet

City and County of Denver General Tax Information Booklet Table of Contents INTRODUCTION... 4 TYPES OF TAX... 5 DENVER SALES TAX... 5 DENVER USE TAX... 5 DENVER OCCUPATIONAL PRIVILEGE TAX (OPT)... 7 LODGER

City and County of Denver General Tax Information Booklet Table of Contents INTRODUCTION... 4 TYPES OF TAX... 5 DENVER SALES TAX... 5 DENVER USE TAX... 5 DENVER OCCUPATIONAL PRIVILEGE TAX (OPT)... 7 LODGER

October 18, 2013. Dear Xxxxx:

ST-13-0058-GIL 10/18/13 SERVICE OCCUPATION TAX If no tangible personal property is transferred to the customer, then no Illinois Retailers Occupation Tax or Service Occupation Tax would apply. See 86 Ill.

ST-13-0058-GIL 10/18/13 SERVICE OCCUPATION TAX If no tangible personal property is transferred to the customer, then no Illinois Retailers Occupation Tax or Service Occupation Tax would apply. See 86 Ill.

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO.S980428A On April

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO.S980428A On April

Sales and Use Tax Fundamentals for Construction Companies

Sales and Use Tax Fundamentals for Construction Companies July 24, 2014 Presented by: Michael L. Colavito, Jr., JD Michael P. Corcoran, CPA 2014 All Rights Reserved 805 King Farm Boulevard Suite 300 Rockville,

Sales and Use Tax Fundamentals for Construction Companies July 24, 2014 Presented by: Michael L. Colavito, Jr., JD Michael P. Corcoran, CPA 2014 All Rights Reserved 805 King Farm Boulevard Suite 300 Rockville,

Miami University Purchasing Card Policy & Procedure

Miami University Purchasing Card Policy & Procedure MAY 22, 2015 1 Table of Contents Program Purpose... 3 Overview... 3 Advantages... 4 Getting Started- Card Application & Activation... 4 Capabilities,

Miami University Purchasing Card Policy & Procedure MAY 22, 2015 1 Table of Contents Program Purpose... 3 Overview... 3 Advantages... 4 Getting Started- Card Application & Activation... 4 Capabilities,

Filing Claims for Refund of Sales or Use Tax

State of Wisconsin Department of Revenue Important Change The football stadium district tax in Brown County ends on September 30, 2015. Filing Claims for Refund of Sales or Use Tax Includes information

State of Wisconsin Department of Revenue Important Change The football stadium district tax in Brown County ends on September 30, 2015. Filing Claims for Refund of Sales or Use Tax Includes information

OPIC. Business Purchases. General Information

New Jersey Division of Taxation TAX OPIC Business Purchases Bulletin S&U-9 Introduction This bulletin provides information on the taxability of business purchases of various goods and services. It explains

New Jersey Division of Taxation TAX OPIC Business Purchases Bulletin S&U-9 Introduction This bulletin provides information on the taxability of business purchases of various goods and services. It explains

Isolated and Occasional Sales

www.revenue.state.mn.us Isolated and Occasional Sales 132 Sales Tax Fact Sheet When a business or trade sells tangible personal property (goods or equipment), the sale is usually subject to Minnesota sales

www.revenue.state.mn.us Isolated and Occasional Sales 132 Sales Tax Fact Sheet When a business or trade sells tangible personal property (goods or equipment), the sale is usually subject to Minnesota sales

IDAHO. #4 retailers An Educational Guide to Sales Tax in the State of Idaho. Who is a retailer? Do I need a seller s permit?

Tax Commission IDAHO #4 retailers An Educational Guide to Sales Tax in the State of Idaho This brochure is intended to help retailers understand the sales tax laws that apply to their business. This information

Tax Commission IDAHO #4 retailers An Educational Guide to Sales Tax in the State of Idaho This brochure is intended to help retailers understand the sales tax laws that apply to their business. This information

NEW JERSEY DIVISION OF TAXATION REGULATORY SERVICES BRANCH TECHNICAL BULLETIN

NEW JERSEY DIVISION OF TAXATION REGULATORY SERVICES BRANCH TECHNICAL BULLETIN TB - 72 ISSUED: 7-3-13 TAX: TOPIC: SALES AND USE TAX CLOUD COMPUTING (SaaS, PaaS, IaaS) This Technical Bulletin addresses the

NEW JERSEY DIVISION OF TAXATION REGULATORY SERVICES BRANCH TECHNICAL BULLETIN TB - 72 ISSUED: 7-3-13 TAX: TOPIC: SALES AND USE TAX CLOUD COMPUTING (SaaS, PaaS, IaaS) This Technical Bulletin addresses the

FOR INFORMATION PURPOSES ONLY.

Form AS 2915.1 A Rev. Aug 11 14 COMMONWEALTH OF PUERTO RICO DEPARTMENT OF THE TREASURY SALES AND USE TAX MONTHLY RETURN (Electronically Filed) MERCHANT S REGISTRATION NUMBER PERIOD (MONTH/YEAR) MONTH YEAR

Form AS 2915.1 A Rev. Aug 11 14 COMMONWEALTH OF PUERTO RICO DEPARTMENT OF THE TREASURY SALES AND USE TAX MONTHLY RETURN (Electronically Filed) MERCHANT S REGISTRATION NUMBER PERIOD (MONTH/YEAR) MONTH YEAR

REVENUE ADMINISTRATIVE BULLETIN 2002-15. Approved: June 10, 2002 SALES AND USE TAX EXEMPTIONS AND REQUIREMENTS

JOHN ENGLER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING DOUGLAS B. ROBERTS STATE TREASURER REVENUE ADMINISTRATIVE BULLETIN 2002-15 Approved: June 10, 2002 SALES AND USE TAX EXEMPTIONS AND

JOHN ENGLER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING DOUGLAS B. ROBERTS STATE TREASURER REVENUE ADMINISTRATIVE BULLETIN 2002-15 Approved: June 10, 2002 SALES AND USE TAX EXEMPTIONS AND

The State Board of Equalization Welcomes You to the Basic Sales and Use Tax Seminar

The State Board of Equalization Welcomes You to the Basic Sales and Use Tax Seminar Welcome to the California State Board of Equalization s presentation on Basic Sales and Use Tax. 1 About This Presentation

The State Board of Equalization Welcomes You to the Basic Sales and Use Tax Seminar Welcome to the California State Board of Equalization s presentation on Basic Sales and Use Tax. 1 About This Presentation

IDAHO #2 USE TAX An Educational Guide to Sales Tax in the State of Idaho

Tax Commission IDAHO #2 USE TAX An Educational Guide to Sales Tax in the State of Idaho This brochure is intended to help businesses, organizations, and individuals understand how use tax applies to them.

Tax Commission IDAHO #2 USE TAX An Educational Guide to Sales Tax in the State of Idaho This brochure is intended to help businesses, organizations, and individuals understand how use tax applies to them.

ILLINOIS REGISTER DEPARTMENT OF REVENUE NOTICE OF PROPOSED AMENDMENT TITLE 86: REVENUE CHAPTER I: DEPARTMENT OF REVENUE

TITLE 86: REVENUE CHAPTER I: PART 320 REGIONAL TRANSPORTATION AUTHORITY RETAILERS' OCCUPATION TAX Section 320.101 Nature of the Regional Transportation Authority Retailers' Occupation Tax 320.105 Registration

TITLE 86: REVENUE CHAPTER I: PART 320 REGIONAL TRANSPORTATION AUTHORITY RETAILERS' OCCUPATION TAX Section 320.101 Nature of the Regional Transportation Authority Retailers' Occupation Tax 320.105 Registration

CHAPTER 174 HOUSE BILL 2546 AN ACT

Senate Engrossed House Bill State of Arizona House of Representatives Fifty-first Legislature Second Regular Session CHAPTER HOUSE BILL AN ACT AMENDING SECTION -.0, ARIZONA REVISED STATUTES; AMENDING SECTION

Senate Engrossed House Bill State of Arizona House of Representatives Fifty-first Legislature Second Regular Session CHAPTER HOUSE BILL AN ACT AMENDING SECTION -.0, ARIZONA REVISED STATUTES; AMENDING SECTION

Individual income tax

International Tax Puerto Rico Tax Alert 12 June 2015 Tax reform enacted Contacts Francisco A. Castillo [email protected] Ricardo Villate [email protected] Michelle Corretjer [email protected]

International Tax Puerto Rico Tax Alert 12 June 2015 Tax reform enacted Contacts Francisco A. Castillo [email protected] Ricardo Villate [email protected] Michelle Corretjer [email protected]

S&U-8 Alarm Systems. Rev. 8/99

S&U-8 Alarm Systems Introduction Sales and installations of alarm and security systems such as burglar and fire alarms are generally taxable in New Jersey. However, the sales tax requirements differ based

S&U-8 Alarm Systems Introduction Sales and installations of alarm and security systems such as burglar and fire alarms are generally taxable in New Jersey. However, the sales tax requirements differ based

CONSTRUCTION CONTRACTORS, OWNER BUILDERS AND SPECULATIVE BUILDERS

CONSTRUCTION CONTRACTORS, OWNER BUILDERS AND SPECULATIVE BUILDERS This publication is for general information about the Transaction Privilege (Sales) Tax on contracting activities. It contains excerpts

CONSTRUCTION CONTRACTORS, OWNER BUILDERS AND SPECULATIVE BUILDERS This publication is for general information about the Transaction Privilege (Sales) Tax on contracting activities. It contains excerpts

Telecommunication Services

South Dakota Department of Revenue 445 East Capitol Avenue Pierre, South Dakota 57501 Telecommunication Services A p r i l 2 0 1 2 This Tax Facts is designed to explain how sales and use tax applies to

South Dakota Department of Revenue 445 East Capitol Avenue Pierre, South Dakota 57501 Telecommunication Services A p r i l 2 0 1 2 This Tax Facts is designed to explain how sales and use tax applies to

Business tax tip #4 If You Make Purchases for Resale

Business tax tip #4 If You Make Purchases for Resale If you're a buyer... Does my sales and use tax license entitle me to make purchases without paying sales and use tax? No. Contrary to what many people

Business tax tip #4 If You Make Purchases for Resale If you're a buyer... Does my sales and use tax license entitle me to make purchases without paying sales and use tax? No. Contrary to what many people

Florida Annual Resale Certificate for Sales Tax

Florida Annual Resale Certificate for Sales Tax GT-800060 R. 07/15 What s New for 2015 Florida Annual Resale Certificates for Sales Tax Florida Annual Resale Certificates for Sales Tax are available for

Florida Annual Resale Certificate for Sales Tax GT-800060 R. 07/15 What s New for 2015 Florida Annual Resale Certificates for Sales Tax Florida Annual Resale Certificates for Sales Tax are available for

Provincial Sales Tax (PST) Bulletin. Vehicle Services and Parts Provincial Sales Tax Act. Table of Contents. Overview

Bulletin. Vehicle Services and Parts Provincial Sales Tax Act. Table of Contents. Overview") Provincial Sales Tax (PST) Bulletin Bulletin PST 118 Issued: November 2013 Vehicle Services and Parts Provincial Sales Tax Act This bulletin provides information on how the provincial sales tax (PST) applies

Provincial Sales Tax (PST) Bulletin Bulletin PST 118 Issued: November 2013 Vehicle Services and Parts Provincial Sales Tax Act This bulletin provides information on how the provincial sales tax (PST) applies

LAWS GOVERNING AUTO INDUSTRY

Automobile LAWS GOVERNING AUTO INDUSTRY Two of the main chapters of the Nevada Revised Statutes and Nevada Administrative Code discussed today are: Chapter 372: Sales and Use Taxes Chapter 482: Motor Vehicles

Automobile LAWS GOVERNING AUTO INDUSTRY Two of the main chapters of the Nevada Revised Statutes and Nevada Administrative Code discussed today are: Chapter 372: Sales and Use Taxes Chapter 482: Motor Vehicles

Title 35 Mississippi State Tax Commission. Part IV Sales & Use. Sub Part 13 General

1 Title 35 Mississippi State Tax Commission Part IV Sales & Use Sub Part 13 General Chapter 02 Sales Made By and To Schools and Colleges and Universities Junior Colleges, Community Colleges, Colleges and

1 Title 35 Mississippi State Tax Commission Part IV Sales & Use Sub Part 13 General Chapter 02 Sales Made By and To Schools and Colleges and Universities Junior Colleges, Community Colleges, Colleges and

Sales and Use Tax on Building Contractors

Sales and Use Tax on Building Contractors GT-800007 R. 03/15 Definitions Fabrication Cost The cost to a real property contractor to fabricate an item. This cost includes direct materials, labor, and other

Sales and Use Tax on Building Contractors GT-800007 R. 03/15 Definitions Fabrication Cost The cost to a real property contractor to fabricate an item. This cost includes direct materials, labor, and other

Sales and Use Taxes: New Jersey

Page 1 of 21 Sales and Use Taxes: New Jersey Resource type: Article: know-how Status: Law stated as at 18-May-2012 Jurisdiction: New Jersey A Q&A guide to sales and use tax in New Jersey. This Q&A addresses

Page 1 of 21 Sales and Use Taxes: New Jersey Resource type: Article: know-how Status: Law stated as at 18-May-2012 Jurisdiction: New Jersey A Q&A guide to sales and use tax in New Jersey. This Q&A addresses

Chapter Four Taxable Services and Contractors

GR-9. Taxable Services Service of, addition to or the service of alteration, cleaning, refinishing, replacement and repair of the following items of tangible personal property are subject to the tax. 1.

GR-9. Taxable Services Service of, addition to or the service of alteration, cleaning, refinishing, replacement and repair of the following items of tangible personal property are subject to the tax. 1.

Frequently Asked Questions

23 Frequently Asked Questions Chapter 23 Frequently Asked Questions The following are some Frequently Asked Questions concerning the sales and use tax law. These questions are listed under the following

23 Frequently Asked Questions Chapter 23 Frequently Asked Questions The following are some Frequently Asked Questions concerning the sales and use tax law. These questions are listed under the following