DEBT COLLECTION AGENCIES: REPORT OF WORKING PARTY

|

|

|

- Douglas Gaines

- 9 years ago

- Views:

Transcription

1 STATES OF JERSEY DEBT COLLECTION AGENCIES: REPORT OF WORKING PARTY Presented to the States on 20th March 2012 by the Minister for Economic Development STATES GREFFE 2012 Price code: B R.36

2 2 REPORT Background This Report follows the proposition lodged by Deputy M. Tadier of St. Brelade on 6th June 2011 (P.102/2011) to request the Minister (a) (b) (c) to establish a Working Party to examine the current operation of debt collection agencies in Jersey and to consider the creation of a code of practice for such agencies to ensure that they operate according to best practice; to appoint at least 2 States members as members of the Working Party and to take the necessary steps to appoint other members with relevant skills and experience, including representatives of the debt collection industry and representatives of groups representing the interests of consumers; to present the report of the Working Party to the States once the Working Party has concluded its work. The Minister fully supported the proposition and chaired the first meeting of the Working Party in September Composition of the Working Party Deputy M. Tadier of St. Brelade and Senator F. du H. Le Gresley were appointed as the 2 States members. The meeting was very well attended by representatives from 5 Debt Collection Agencies, as well as representation from the Citizens Advice Bureau and Trading Standards. The Manager of the Citizens Advice Bureau agreed to chair future meetings and oversee the work of the group. Working Party Membership Deputy M. Tadier of St. Brelade Senator F. du H. Le Gresley Working Party Chairman Mr. M. Ferey, Citizens Advice Bureau Miss A. de Bourcier, Trading Standards Service Mr. M. Williams, Collect Services Limited Mr. P. Boots, Cashback Limited Mr. S. De Mouilpied, Resolve C.I. Ltd. Ms. E. Atkinson, Chancellors Debt Recovery Limited Mr. S. Hill, Hillbury Collection Services

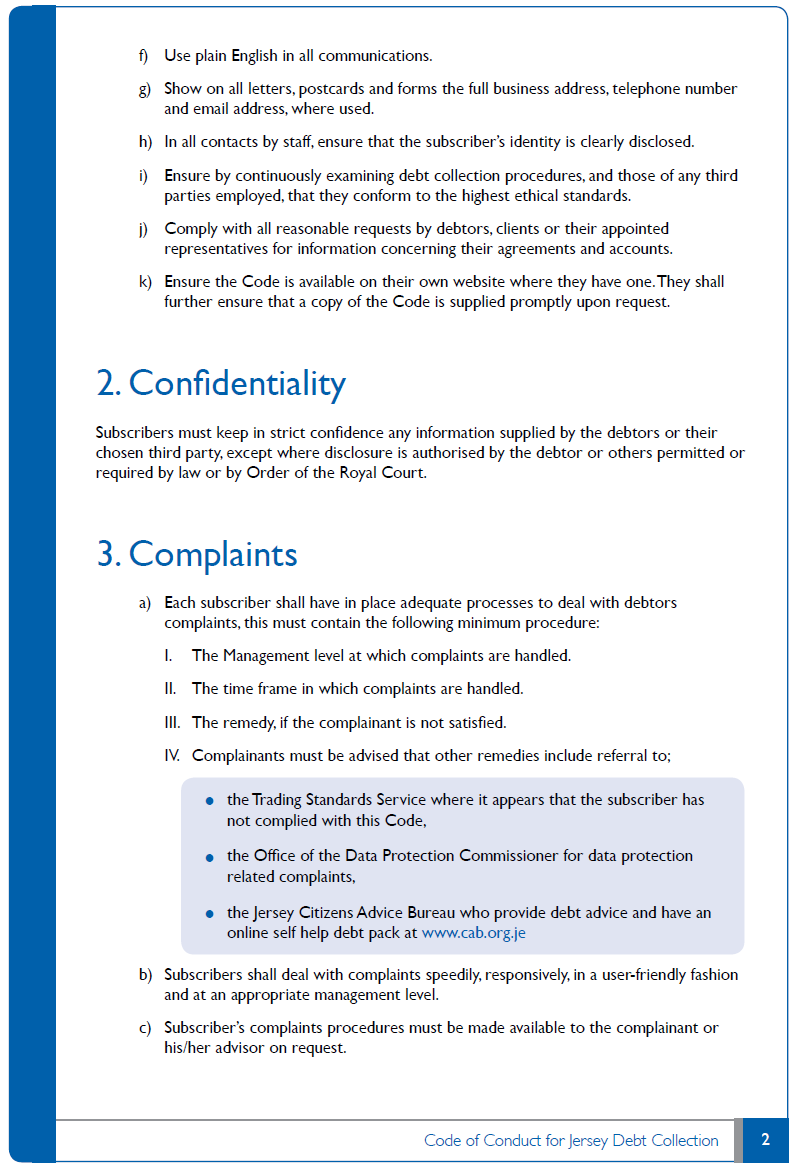

3 3 The basis for a Code of Conduct In 2011, the Minister for Economic Development published a Consultation Green Paper on the introduction of a new consumer protection Law. This followed the introduction in the United Kingdom (UK) of the Consumer Protection from Unfair Trading Regulations in 2008, which was a legal obligation flowing from the implementation of the Unfair Commercial Practices Directive. With this work in train and mindful that any future legislation would regulate some aspects of debt collection, the group were keen to expedite a voluntary Code of Conduct. This document would then form a useful guide and reference in determining professional diligence under the proposed new Law. The Code is modelled around the debt collection guidelines issued by the UK Office of Fair Trading and the UK Credit Services Association Code of Practice. Five Debt Collection Agencies in Jersey have already agreed to subscribe to the Jersey Code from 1st March The scope is sufficiently wide to allow other organisations who are involved in their own debt collection activities to consider subscribing. Overview of the Code The code contains 7 sections dealing with different aspects of debt collection activities. In summary, these are 1. General Code of Conduct To ensure subscribers act responsibly and with integrity in the day-to-day conduct of its business. 2. Confidentiality To ensure subscribers keep information in the strictest of confidence and adhere to the Law and fundamental principles of Data Protection. 3. Complaints Have an adequate complaints procedure and advise complainants of all of the other remedies available including referral to the Trading Standards Service where it appears that the subscriber has not complied with this Code; the Office of the Data Protection Commissioner for data protection related complaints; the Jersey Citizens Advice Bureau who provide debt advice and have an online self-help debt pack at

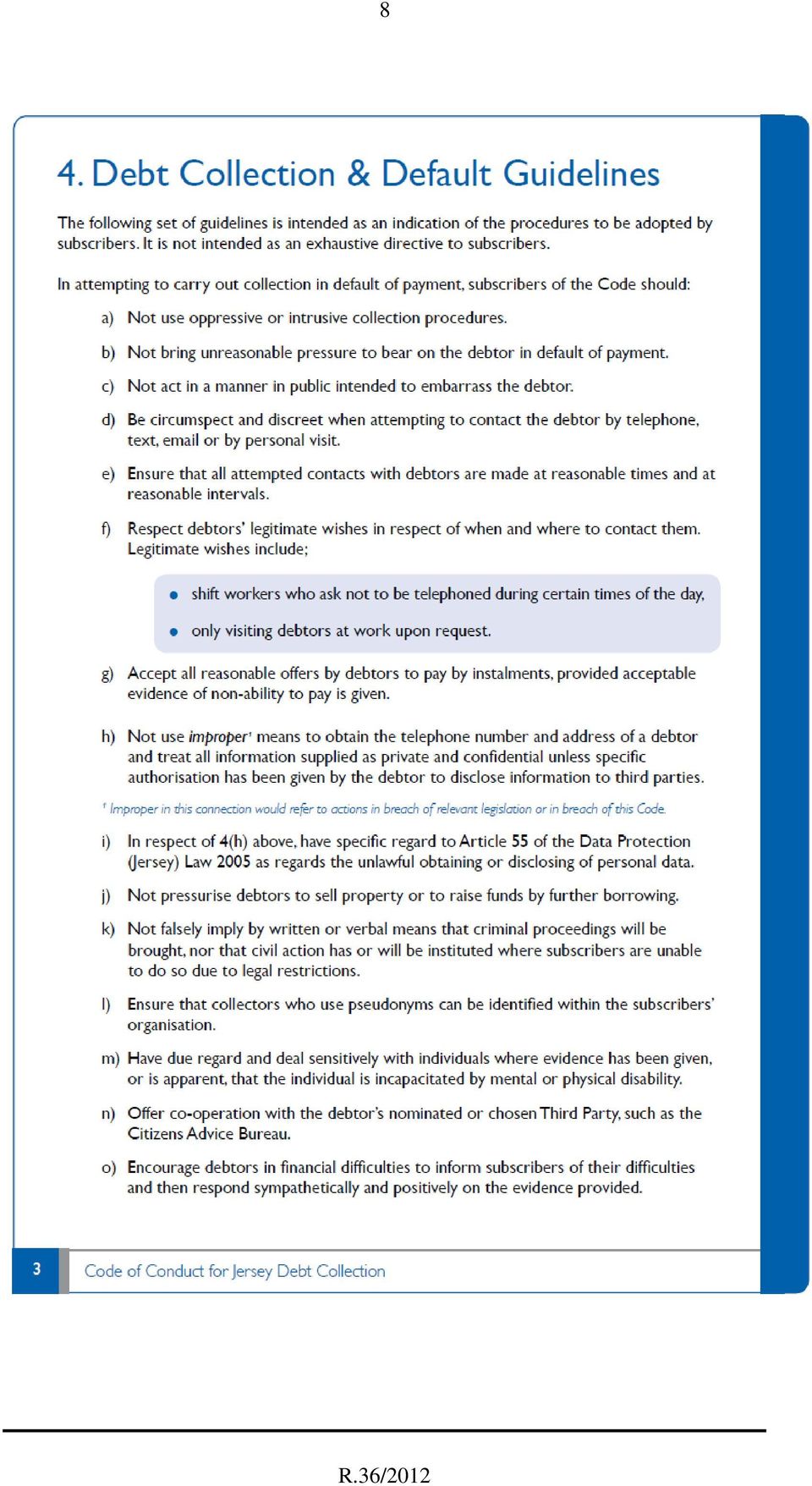

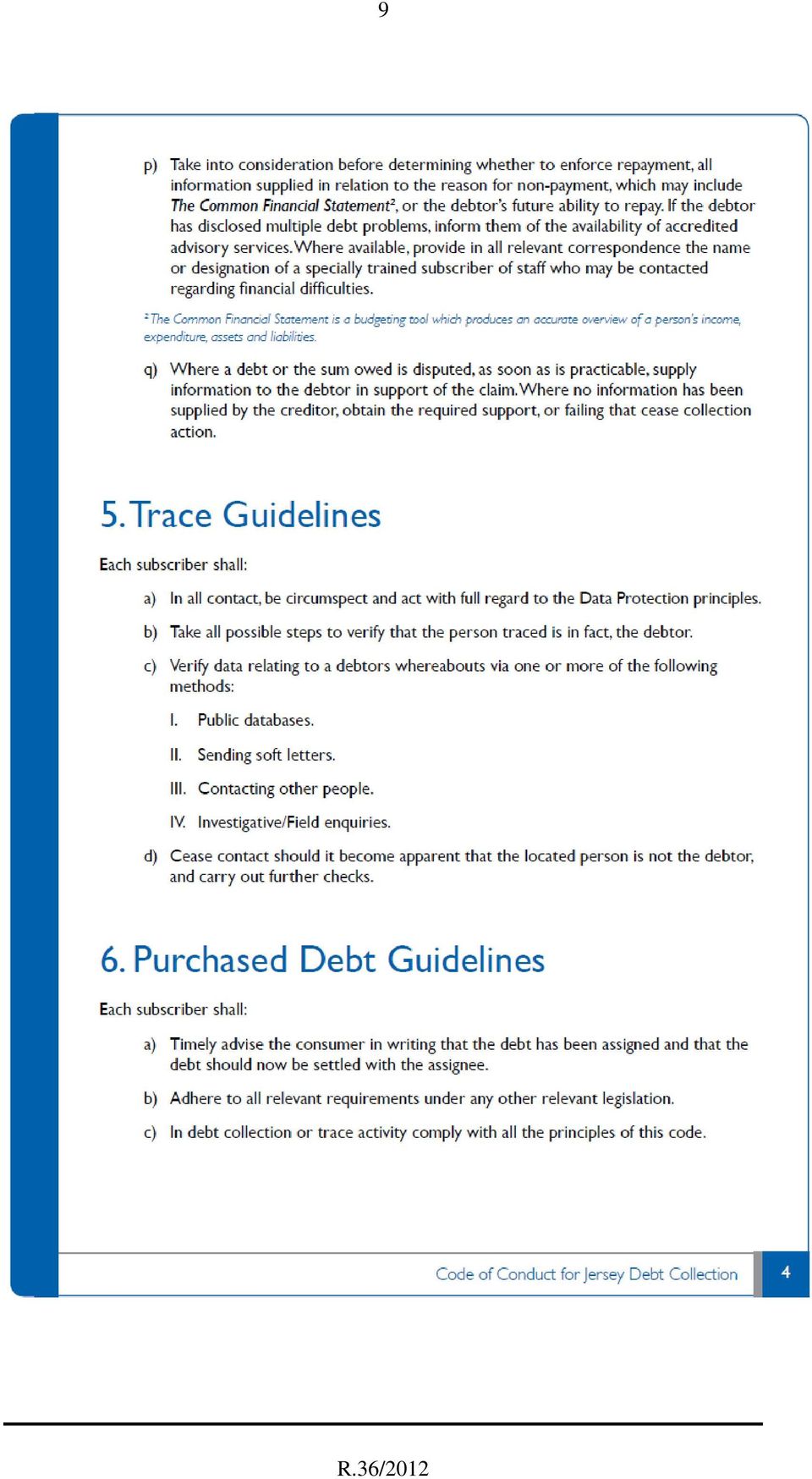

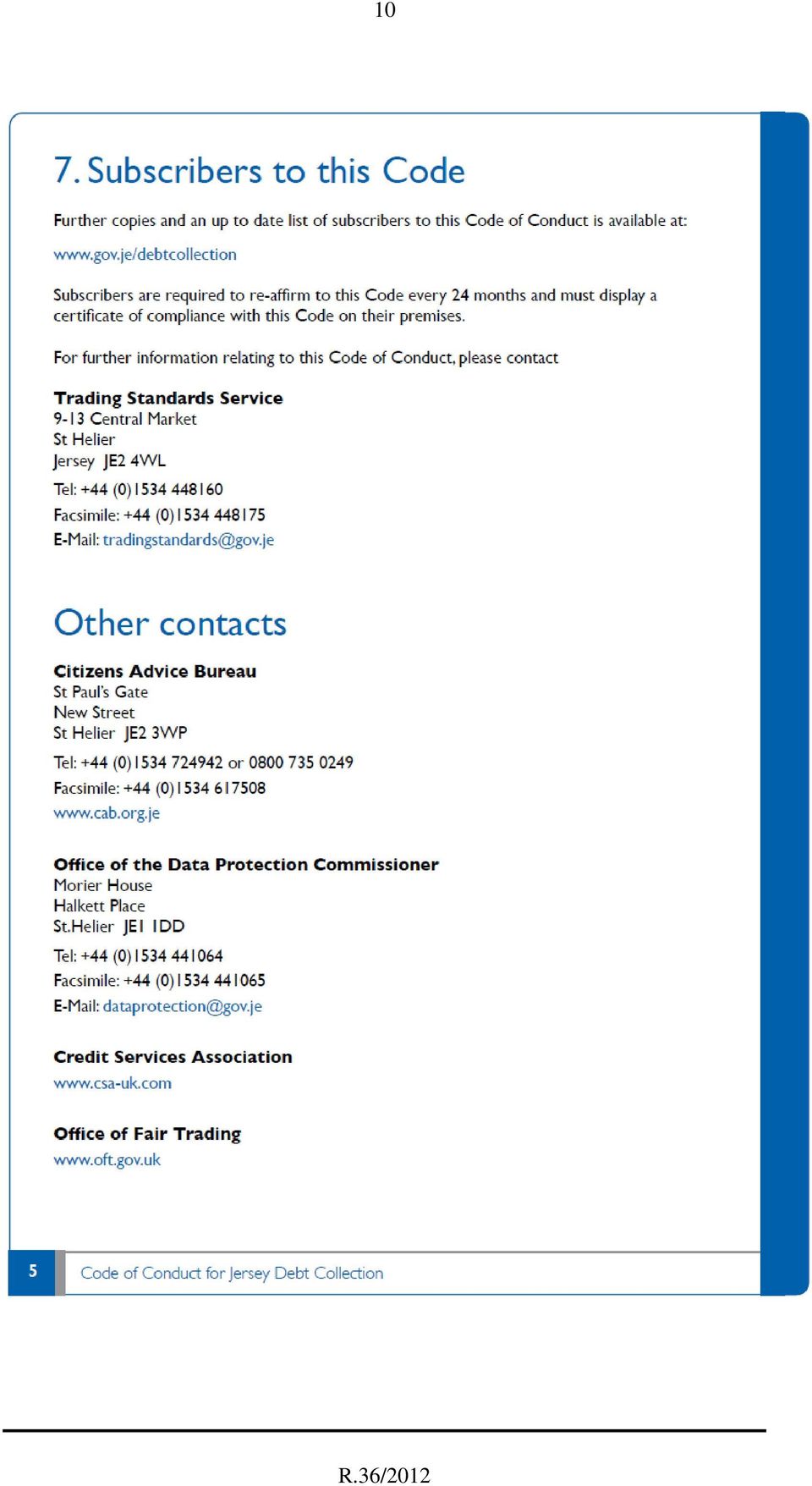

4 4 4. Default Guidelines Follow clear industry standards in attempting to carry out collection in default of payment. 5. Trace Guidelines Ensure subscribers are circumspect and take all steps to verify that the person traced is in fact the debtor. 6. Purchased Debt Guidelines Timely advise consumers when debt has been assigned and to whom. 7. Subscribing to this Code Reconfirm to the Code every 24 months and display a certificate of compliance. Monitor and Review Subscription will be managed by the Trading Standards Service in the same way that they manage subscribers to the Code of Practice for Consumer Lending. Subscribers must ensure they make the Code available on their own website and provide a copy to debtors promptly on request. It will also be available on the States of Jersey website. Complaints relating to non-compliance will be directed to the Trading Standards Service for investigation. The Working Party has agreed to review the Code from time to time to ensure it reflects current best practice. A copy of the Code of Conduct for Jersey Debt Collection is attached at the Appendix to this Report.

5 5 APPENDIX

6 6

7 7

8 8

9 9

10 10

Health Care Insurance Ltd Complaints Handling Policy

Health Care Insurance Ltd Complaints Handling Policy Purpose The purpose of this document is to outline the procedure that Health Care Insurance Ltd (HCI) will adopt in the process of resolving complaints

Health Care Insurance Ltd Complaints Handling Policy Purpose The purpose of this document is to outline the procedure that Health Care Insurance Ltd (HCI) will adopt in the process of resolving complaints

CODE GOVERNANCE COMMITTEE CHARTER. 1 Functions and responsibilities of the Code Governance Committee

CODE GOVERNANCE COMMITTEE CHARTER 1 Functions and responsibilities of the Code Governance Committee 1.1 Consistent with the Code and the Constitution, the Code Governance Committee shall be responsible

CODE GOVERNANCE COMMITTEE CHARTER 1 Functions and responsibilities of the Code Governance Committee 1.1 Consistent with the Code and the Constitution, the Code Governance Committee shall be responsible

Table of Contents... 1. Chapter 1 Introduction... 5. 1.1 Goals & Objectives... 5 1.2 Required Review... 5 1.3 Applicability...

... 1 Chapter 1 Introduction... 5 1.1 Goals & Objectives... 5 1.2 Required Review... 5 1.3 Applicability... 5 Chapter 2 Company Culture... 6 Chapter 3 Risk Management Governance... 7 3.1 Board of Directors...

... 1 Chapter 1 Introduction... 5 1.1 Goals & Objectives... 5 1.2 Required Review... 5 1.3 Applicability... 5 Chapter 2 Company Culture... 6 Chapter 3 Risk Management Governance... 7 3.1 Board of Directors...

Information Governance Framework

Information Governance Framework March 2014 CONTENT Page 1 Introduction 1 2 Strategic Aim 2 3 Purpose, Values and Principles 2 4 Scope 3 5 Roles and Responsibilities 3 6 Review 5 Appendix 1 - Information

Information Governance Framework March 2014 CONTENT Page 1 Introduction 1 2 Strategic Aim 2 3 Purpose, Values and Principles 2 4 Scope 3 5 Roles and Responsibilities 3 6 Review 5 Appendix 1 - Information

STATES OF JERSEY STATES OF JERSEY COMPLAINTS PANEL: RENEWAL OF MEMBERSHIP STATES GREFFE

STATES OF JERSEY STATES OF JERSEY COMPLAINTS PANEL: RENEWAL OF MEMBERSHIP Lodged au Greffe on 9th July 2015 by the Privileges and Procedures Committee STATES GREFFE 2015 Price code: B P.71 PROPOSITION

STATES OF JERSEY STATES OF JERSEY COMPLAINTS PANEL: RENEWAL OF MEMBERSHIP Lodged au Greffe on 9th July 2015 by the Privileges and Procedures Committee STATES GREFFE 2015 Price code: B P.71 PROPOSITION

AUDIT COMMITTEE TERMS OF REFERENCE

AUDIT COMMITTEE TERMS OF REFERENCE 1. Purpose The Audit Committee will assist the Board of Directors (the "Board") in fulfilling its oversight responsibilities. The Audit Committee will review the financial

AUDIT COMMITTEE TERMS OF REFERENCE 1. Purpose The Audit Committee will assist the Board of Directors (the "Board") in fulfilling its oversight responsibilities. The Audit Committee will review the financial

UNITED KINGDOM DEBT MANAGEMENT OFFICE. Executive Agency Framework Document

UNITED KINGDOM DEBT MANAGEMENT OFFICE Executive Agency Framework Document April 2005 UNITED KINGDOM DEBT MANAGEMENT OFFICE Executive Agency Framework Document April 2005 FOREWORD BY THE FINANCIAL SECRETARY

UNITED KINGDOM DEBT MANAGEMENT OFFICE Executive Agency Framework Document April 2005 UNITED KINGDOM DEBT MANAGEMENT OFFICE Executive Agency Framework Document April 2005 FOREWORD BY THE FINANCIAL SECRETARY

BRACKNELL FOREST COUNCIL ADULT SOCIAL CARE & HEALTH DEBT RECOVERY POLICY & PROCEDURES

BRACKNELL FOREST COUNCIL ADULT SOCIAL CARE & HEALTH DEBT RECOVERY POLICY & PROCEDURES POLICY DOCUMENT Table of Contents 1. Definitions and Abbreviations... 3 2. Legal Status... 4 3. Principles for Debt

BRACKNELL FOREST COUNCIL ADULT SOCIAL CARE & HEALTH DEBT RECOVERY POLICY & PROCEDURES POLICY DOCUMENT Table of Contents 1. Definitions and Abbreviations... 3 2. Legal Status... 4 3. Principles for Debt

Align Technology. Data Protection Binding Corporate Rules Processor Policy. 2014 Align Technology, Inc. All rights reserved.

Align Technology Data Protection Binding Corporate Rules Processor Policy Confidential Contents INTRODUCTION TO THIS POLICY 3 PART I: BACKGROUND AND ACTIONS 4 PART II: PROCESSOR OBLIGATIONS 6 PART III:

Align Technology Data Protection Binding Corporate Rules Processor Policy Confidential Contents INTRODUCTION TO THIS POLICY 3 PART I: BACKGROUND AND ACTIONS 4 PART II: PROCESSOR OBLIGATIONS 6 PART III:

Principles for the Reporting of Arrears, Arrangements and Defaults at Credit Reference Agencies

Principles for the Reporting of Arrears, Arrangements and Defaults at Credit Reference Agencies Foreword by the Information Commissioner s Office The Information Commissioner s Office (ICO) published Data

Principles for the Reporting of Arrears, Arrangements and Defaults at Credit Reference Agencies Foreword by the Information Commissioner s Office The Information Commissioner s Office (ICO) published Data

HIGHFIELD RESOURCES LIMITED AUDIT, BUSINESS RISK & COMPLIANCE COMMITTEE CHARTER

HIGHFIELD RESOURCES LIMITED AUDIT, BUSINESS RISK & COMPLIANCE COMMITTEE CHARTER HIGHFIELD RESOURCES LTD AUDIT, BUSINESS RISK & COMPLIANCE COMMITTEE CHARTER PART 1 - PRELIMINARY 1. Introduction 1.1 The

HIGHFIELD RESOURCES LIMITED AUDIT, BUSINESS RISK & COMPLIANCE COMMITTEE CHARTER HIGHFIELD RESOURCES LTD AUDIT, BUSINESS RISK & COMPLIANCE COMMITTEE CHARTER PART 1 - PRELIMINARY 1. Introduction 1.1 The

COMPLAINTS PROCEDURE ENGLAND BEAUFORT ROAD SURGERY INTRODUCTION

COMPLAINTS PROCEDURE ENGLAND BEAUFORT ROAD SURGERY INTRODUCTION This procedure sets out the Practice s approach to the handling of complaints and is intended as an internal guide who should be made readily

COMPLAINTS PROCEDURE ENGLAND BEAUFORT ROAD SURGERY INTRODUCTION This procedure sets out the Practice s approach to the handling of complaints and is intended as an internal guide who should be made readily

STATES OF JERSEY JERSEY FINANCIAL SERVICES COMMISSION: APPOINTMENT OF COMMISSIONERS

STATES OF JERSEY r JERSEY FINANCIAL SERVICES COMMISSION: APPOINTMENT OF COMMISSIONERS Lodged au Greffe on 30th August 2005 by the Economic Development Committee STATES GREFFE PROPOSITION THE STATES are

STATES OF JERSEY r JERSEY FINANCIAL SERVICES COMMISSION: APPOINTMENT OF COMMISSIONERS Lodged au Greffe on 30th August 2005 by the Economic Development Committee STATES GREFFE PROPOSITION THE STATES are

PRIVATE HEALTH INSURANCE INTERMEDIARIES. DOCUMENT 1: Self-Audit Guide for All Members of PHIIA JUNE 2015 VERSION 2

PRIVATE HEALTH INSURANCE INTERMEDIARIES DOCUMENT 1: Self-Audit Guide for All Members of PHIIA JUNE 2015 VERSION 2 9 For All Members of PHIIA Code Compliance Committee Private Health Insurance Intermediaries

PRIVATE HEALTH INSURANCE INTERMEDIARIES DOCUMENT 1: Self-Audit Guide for All Members of PHIIA JUNE 2015 VERSION 2 9 For All Members of PHIIA Code Compliance Committee Private Health Insurance Intermediaries

Information, Triage & the Receptionist's Role

Information, Triage & the Receptionist's Role The Receptionist s Role In most advice services, the receptionist is the first person a client meets when s/he is seeking advice. The receptionist is the public

Information, Triage & the Receptionist's Role The Receptionist s Role In most advice services, the receptionist is the first person a client meets when s/he is seeking advice. The receptionist is the public

Key to Disclosures Corporate Governance Council Principles and Recommendations

Rules 4.7.3 and 4.10.3 1 Appendix 4G Name of entity Key to Disclosures Corporate Governance Council Principles and Recommendations WHITE ROCK MINERALS LTD ABN/ARBN Financial year ended 64 142 809 970 30/06/2015

Rules 4.7.3 and 4.10.3 1 Appendix 4G Name of entity Key to Disclosures Corporate Governance Council Principles and Recommendations WHITE ROCK MINERALS LTD ABN/ARBN Financial year ended 64 142 809 970 30/06/2015

to the practitioner any improper debt recovery actions taken by the debt-collection company.

Circular Circular No. 08-04 (CR) Practitioners must enter into a debt-collection-company appointment agreement Practitioners must monitor the performance of the debt-collection companies Using Debt-Collection

Circular Circular No. 08-04 (CR) Practitioners must enter into a debt-collection-company appointment agreement Practitioners must monitor the performance of the debt-collection companies Using Debt-Collection

Assessment and Collection of Selected Penalties. Workers Compensation Board

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Assessment and Collection of Selected Penalties Workers Compensation Board Report 2011-S-3

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Assessment and Collection of Selected Penalties Workers Compensation Board Report 2011-S-3

Annex A CITY OF YORK COUNCIL CORPORATE DEBT POLICY

Annex A CITY OF YORK COUNCIL CORPORATE DEBT POLICY Contents Paragraph Introduction 1-3 Policy Objectives 4-5 Policy Purpose 6-9 Governance 10 Delivering the Service to the Customer 11 13 Communicating

Annex A CITY OF YORK COUNCIL CORPORATE DEBT POLICY Contents Paragraph Introduction 1-3 Policy Objectives 4-5 Policy Purpose 6-9 Governance 10 Delivering the Service to the Customer 11 13 Communicating

STATES OF JERSEY DRAFT HEALTH INSURANCE FUND (MISCELLANEOUS PROVISIONS) (AMENDMENT) (JERSEY) LAW 201- STATES GREFFE

(AMENDMENT) (JERSEY) LAW 201- STATES GREFFE") STATES OF JERSEY r DRAFT HEALTH INSURANCE FUND (MISCELLANEOUS PROVISIONS) (AMENDMENT) (JERSEY) LAW 201- Lodged au Greffe on 25th September 2012 by the Minister for Social Security STATES GREFFE 2012 Price

STATES OF JERSEY r DRAFT HEALTH INSURANCE FUND (MISCELLANEOUS PROVISIONS) (AMENDMENT) (JERSEY) LAW 201- Lodged au Greffe on 25th September 2012 by the Minister for Social Security STATES GREFFE 2012 Price

Property Management (Factoring) Policy. Approval date July 2014 Review date July 2017 Approved by Link Group Board. www.linkhousing.org.

Policy. Approval date July 2014 Review date July 2017 Approved by Link Group Board. www.linkhousing.org.") Property Management (Factoring) Policy Approval date July 2014 Review date July 2017 Approved by Link Group Board 1. INTRODUCTION This policy has been devised to show how Link operates property management

Property Management (Factoring) Policy Approval date July 2014 Review date July 2017 Approved by Link Group Board 1. INTRODUCTION This policy has been devised to show how Link operates property management

COMPLIANCE MANAGEMENT SYSTEM

COMPLIANCE MANAGEMENT SYSTEM INTRODUCTION Financial institutions operate in a dynamic environment influenced by industry consolidation, convergence of financial services, emerging technology, and market

COMPLIANCE MANAGEMENT SYSTEM INTRODUCTION Financial institutions operate in a dynamic environment influenced by industry consolidation, convergence of financial services, emerging technology, and market

Quality Assurance and Safeguards Working Arrangements for the Launch of the NDIS in Victoria

Quality Assurance and Safeguards Working Arrangements for the Launch of the NDIS in Victoria As agreed between the Commonwealth of Australia and Victoria As at 6 May 2013 1 Contents 1. Background... 3

Quality Assurance and Safeguards Working Arrangements for the Launch of the NDIS in Victoria As agreed between the Commonwealth of Australia and Victoria As at 6 May 2013 1 Contents 1. Background... 3

Bridgewater Housing Association Ltd Policy

Bridgewater Housing Association Ltd Policy Approved committee on by 5 August 1998 31 March 1999 26 April 2000 25 September 2002 30 November 2005 17 December 2008 Review Date: 16 December 2011 Ref: Arrears

Bridgewater Housing Association Ltd Policy Approved committee on by 5 August 1998 31 March 1999 26 April 2000 25 September 2002 30 November 2005 17 December 2008 Review Date: 16 December 2011 Ref: Arrears

PRIVATE HEALTH INSURANCE INTERMEDIARIES CODE OF CONDUCT JUNE 2015 VERSION 2

PRIVATE HEALTH INSURANCE INTERMEDIARIES CODE OF CONDUCT JUNE 2015 VERSION 2 CONTENTS PART A - Page 4 GENERAL 1. INTRODUCTION 2. OUR COMMITMENT UNDER THE CODE 3. PRIVATE HEALTH INSURANCE ENVIRONMENT PART

PRIVATE HEALTH INSURANCE INTERMEDIARIES CODE OF CONDUCT JUNE 2015 VERSION 2 CONTENTS PART A - Page 4 GENERAL 1. INTRODUCTION 2. OUR COMMITMENT UNDER THE CODE 3. PRIVATE HEALTH INSURANCE ENVIRONMENT PART

Privacy Policy Statement

Privacy Policy Statement Our Commitment While information is the foundation for providing you with superior service, protecting the privacy of your personal information is of the highest importance to

Privacy Policy Statement Our Commitment While information is the foundation for providing you with superior service, protecting the privacy of your personal information is of the highest importance to

Santander Corporate & Commercial Intermediary registration and information renewal form

INTERMEDIARIES & BROKERS ONLY: NOT FOR PUBLIC DISTRIBUTION Santander Corporate & Commercial Intermediary registration and information renewal form Please fill in the form using BLOCK CAPITALS and black

INTERMEDIARIES & BROKERS ONLY: NOT FOR PUBLIC DISTRIBUTION Santander Corporate & Commercial Intermediary registration and information renewal form Please fill in the form using BLOCK CAPITALS and black

APPLICATION OF THE KING III REPORT ON CORPORATE GOVERNANCE PRINCIPLES

APPLICATION OF THE KING III REPORT ON CORPORATE GOVERNANCE PRINCIPLES Ethical Leadership and Corporate Citizenship The board should provide effective leadership based on ethical foundation. that the company

APPLICATION OF THE KING III REPORT ON CORPORATE GOVERNANCE PRINCIPLES Ethical Leadership and Corporate Citizenship The board should provide effective leadership based on ethical foundation. that the company

Client Complaints Management Policy Summary

Client Complaints Management Policy Summary Purpose The purpose of this Policy is to: Provide an avenue for client communication and feedback; Recognise, promote and protect the client s rights, including

Client Complaints Management Policy Summary Purpose The purpose of this Policy is to: Provide an avenue for client communication and feedback; Recognise, promote and protect the client s rights, including

CREDIT REPAIR AUSTRALIA Pty Ltd ( CRA ) A.C.N 103 959 502 CODE OF CONDUCT IN RELATION TO CREDIT RESTORATION SERVICES

A.C.N 103 959 502 CODE OF CONDUCT IN RELATION TO CREDIT RESTORATION SERVICES") CREDIT REPAIR AUSTRALIA Pty Ltd ( CRA ) A.C.N 103 959 502 CODE OF CONDUCT IN RELATION TO CREDIT RESTORATION SERVICES 1. SHORT TITLE 1. Short title. 2. Background & Purposes. 3. Definitions. 4. Prohibited

CREDIT REPAIR AUSTRALIA Pty Ltd ( CRA ) A.C.N 103 959 502 CODE OF CONDUCT IN RELATION TO CREDIT RESTORATION SERVICES 1. SHORT TITLE 1. Short title. 2. Background & Purposes. 3. Definitions. 4. Prohibited

INSURANCE ACT 2008 CORPORATE GOVERNANCE CODE OF PRACTICE FOR REGULATED INSURANCE ENTITIES

SD 0880/10 INSURANCE ACT 2008 CORPORATE GOVERNANCE CODE OF PRACTICE FOR REGULATED INSURANCE ENTITIES Laid before Tynwald 16 November 2010 Coming into operation 1 October 2010 The Supervisor, after consulting

SD 0880/10 INSURANCE ACT 2008 CORPORATE GOVERNANCE CODE OF PRACTICE FOR REGULATED INSURANCE ENTITIES Laid before Tynwald 16 November 2010 Coming into operation 1 October 2010 The Supervisor, after consulting

LEEDS CITY COUNCIL CORPORATE DEBT POLICY

LEEDS CITY COUNCIL CORPORATE DEBT POLICY ( Draft Version 5 ) Summary of policy : This policy details the principles to be adopted by the Council when undertaking the collection of debt in the City of Leeds

LEEDS CITY COUNCIL CORPORATE DEBT POLICY ( Draft Version 5 ) Summary of policy : This policy details the principles to be adopted by the Council when undertaking the collection of debt in the City of Leeds

Policy document Strategic/Governance SG 13

Rates and Charges Debt Collection and Recovery Head of Power Sections 132-134 of the Local Government Regulation 2012 sets the parameters for Local Government s management of overdue rates and charges.

Rates and Charges Debt Collection and Recovery Head of Power Sections 132-134 of the Local Government Regulation 2012 sets the parameters for Local Government s management of overdue rates and charges.

Code of Conduct for Indirect Access Providers

Code of Conduct for Indirect Access Providers Version 1.0 (interim) August 2015 Contents 1 Introduction. 3 1.1 Background to the Code... 3 1.2 About the Code... 3 1.3 In-Scope Payment Systems... 4 1.4

Code of Conduct for Indirect Access Providers Version 1.0 (interim) August 2015 Contents 1 Introduction. 3 1.1 Background to the Code... 3 1.2 About the Code... 3 1.3 In-Scope Payment Systems... 4 1.4

BRITISH COUNCIL DATA PROTECTION CODE FOR PARTNERS AND SUPPLIERS

BRITISH COUNCIL DATA PROTECTION CODE FOR PARTNERS AND SUPPLIERS Mat Wright www.britishcouncil.org CONTENTS Purpose of the code 1 Scope of the code 1 The British Council s data protection commitment and

BRITISH COUNCIL DATA PROTECTION CODE FOR PARTNERS AND SUPPLIERS Mat Wright www.britishcouncil.org CONTENTS Purpose of the code 1 Scope of the code 1 The British Council s data protection commitment and

Enterprise bargaining

Enterprise bargaining Australia s new workplace relations system From 1 July 2009, most Australian workplaces are governed by a new system created by the Fair Work Act 2009. The Fair Work Ombudsman helps

Enterprise bargaining Australia s new workplace relations system From 1 July 2009, most Australian workplaces are governed by a new system created by the Fair Work Act 2009. The Fair Work Ombudsman helps

STATES OF JERSEY JERSEY FINANCIAL SERVICES COMMISSION: APPOINTMENT OF COMMISSIONER

STATES OF JERSEY r JERSEY FINANCIAL SERVICES COMMISSION: APPOINTMENT OF COMMISSIONER Lodged au Greffe on 1st June 2006 by the Minister for Economic Development STATES GREFFE PROPOSITION THE STATES are

STATES OF JERSEY r JERSEY FINANCIAL SERVICES COMMISSION: APPOINTMENT OF COMMISSIONER Lodged au Greffe on 1st June 2006 by the Minister for Economic Development STATES GREFFE PROPOSITION THE STATES are

Registration must be carried out by a top executive or a number of executives having the power to commit the whole company in the EU.

Questions and answers 1- What is the purpose of The Initiative? Why are we doing this? The purpose of the Supply Chain Initiative is to promote fair business practices in the food supply chain as a basis

Questions and answers 1- What is the purpose of The Initiative? Why are we doing this? The purpose of the Supply Chain Initiative is to promote fair business practices in the food supply chain as a basis

T&Cs for GUARANTOR Instalment & Bond Loans

T&Cs for GUARANTOR Instalment & Bond Loans 1. INTERPRETATION TERMS AND CONDITIONS 1.1. In these Terms and Conditions, the words "you'" and "your" refer to the Debtors who have entered into this Loan Agreement.

T&Cs for GUARANTOR Instalment & Bond Loans 1. INTERPRETATION TERMS AND CONDITIONS 1.1. In these Terms and Conditions, the words "you'" and "your" refer to the Debtors who have entered into this Loan Agreement.

Explanation where the company has partially applied or not applied King III principles

King Code of Corporate Governance for South Africa, 2009 (King III) checklist The Board of Directors (the Board) of Famous Brands Limited (Famous Brands or the company) is fully committed to business integrity,

King Code of Corporate Governance for South Africa, 2009 (King III) checklist The Board of Directors (the Board) of Famous Brands Limited (Famous Brands or the company) is fully committed to business integrity,

Relate. Personal Insolvency Bill 2012. August 2012. New arrangements for dealing with debt. Contents

August 2012 Volume 39: Issue 8 ISSN 0790-4290 Contents Relate The journal of developments in social services, policy and legislation in Ireland Page No. 1 Personal Insolvency Bill 2012 This issue deals

August 2012 Volume 39: Issue 8 ISSN 0790-4290 Contents Relate The journal of developments in social services, policy and legislation in Ireland Page No. 1 Personal Insolvency Bill 2012 This issue deals

Guide to making a complaint about an NHS service

Guide to making a complaint about an NHS service February 2014 Healthwatch Coventry www.healthwatchcoventry.org.uk Contents 1. About this guide page 3 2. The NHS complaints procedure page 3 3. About the

Guide to making a complaint about an NHS service February 2014 Healthwatch Coventry www.healthwatchcoventry.org.uk Contents 1. About this guide page 3 2. The NHS complaints procedure page 3 3. About the

The business now helps customers Australia wide. We assist customers with Residential, Business, Commercial and Chattel Mortgages, and also Leasing.

Priority Home Loans was established in 2001 by Bryan and Lorraine Coleman. Priority Home Loans has helped many people into new and established homes over that time. Our aim is to provide you with a professional

Priority Home Loans was established in 2001 by Bryan and Lorraine Coleman. Priority Home Loans has helped many people into new and established homes over that time. Our aim is to provide you with a professional

Application of the Framework is relevant to clinical networks, units and health service teams within each service or organisation.

NSW Health Performance Framework The NSW Health Performance Framework, encompassing Service Agreements, Service Compacts Performance Review meetings and associated processes, is now well accepted across

NSW Health Performance Framework The NSW Health Performance Framework, encompassing Service Agreements, Service Compacts Performance Review meetings and associated processes, is now well accepted across

Ayrshire and Arran NHS Board

Paper 17 Ayrshire and Arran NHS Board Monday 19 May 2014 Information Governance Annual Report Author: Mrs Jillian Neilson Head of Information Governance Sponsoring Director: Dr Alison Graham Medical Director

Paper 17 Ayrshire and Arran NHS Board Monday 19 May 2014 Information Governance Annual Report Author: Mrs Jillian Neilson Head of Information Governance Sponsoring Director: Dr Alison Graham Medical Director

THE CLAIMS MANAGEMENT CODE ( the Code )

") THE CLAIMS MANAGEMENT CODE ( the Code ) CONTENTS 1 Introduction 2 Principles 3 Publishing the Code 4 Training and Competence 5 Advertising, Marketing and Promotional Activities 6 Charges 7 Information

THE CLAIMS MANAGEMENT CODE ( the Code ) CONTENTS 1 Introduction 2 Principles 3 Publishing the Code 4 Training and Competence 5 Advertising, Marketing and Promotional Activities 6 Charges 7 Information

Customer Feedback Management Policy

Customer Feedback Management Policy Version 2.0 Table of Contents 1 Document Control... 3 1.1 Document Information... 3 1.2 Document History... 3 1.3 Scheduled amendments... 3 1.4 Document Approvals...

Customer Feedback Management Policy Version 2.0 Table of Contents 1 Document Control... 3 1.1 Document Information... 3 1.2 Document History... 3 1.3 Scheduled amendments... 3 1.4 Document Approvals...

Memorandum of Understanding

Memorandum of Understanding between Department for Business, Innovation and Skills and United Kingdom Accreditation Service Page 1 of 13 Contents 1 Purpose... 3 2 Background... 3 3 Scope of activity...

Memorandum of Understanding between Department for Business, Innovation and Skills and United Kingdom Accreditation Service Page 1 of 13 Contents 1 Purpose... 3 2 Background... 3 3 Scope of activity...

Align Technology. Data Protection Binding Corporate Rules Controller Policy. 2014 Align Technology, Inc. All rights reserved.

Align Technology Data Protection Binding Corporate Rules Controller Policy Contents INTRODUCTION 3 PART I: BACKGROUND AND ACTIONS 4 PART II: CONTROLLER OBLIGATIONS 6 PART III: APPENDICES 13 2 P a g e INTRODUCTION

Align Technology Data Protection Binding Corporate Rules Controller Policy Contents INTRODUCTION 3 PART I: BACKGROUND AND ACTIONS 4 PART II: CONTROLLER OBLIGATIONS 6 PART III: APPENDICES 13 2 P a g e INTRODUCTION

Private Health Insurance Code of Conduct

Private Health Insurance Code of Conduct July 2014: Version 5 CONTENTS PART A: GENERAL 1 1. INTRODUCTION 1 1.1 Introduction 1 1.2 Compliance 1 2. OUR COMMITMENT UNDER THE CODE 2 3. PRIVATE HEALTH INSURANCE

Private Health Insurance Code of Conduct July 2014: Version 5 CONTENTS PART A: GENERAL 1 1. INTRODUCTION 1 1.1 Introduction 1 1.2 Compliance 1 2. OUR COMMITMENT UNDER THE CODE 2 3. PRIVATE HEALTH INSURANCE

PRIVACY POLICY NEXT BUSINESS ENERGY PTY LIMITED ABN 91 167 937 555

PRIVACY POLICY NEXT BUSINESS ENERGY PTY LIMITED ABN 91 167 937 555 TABLE OF CONTENTS 1. INTRODUCTION 3 2. HOW WE COLLECT YOUR PERSONAL INFORMATION 3 3. TYPES OF INFORMATION WE COLLECT 4 4. HOW WE USE THE

PRIVACY POLICY NEXT BUSINESS ENERGY PTY LIMITED ABN 91 167 937 555 TABLE OF CONTENTS 1. INTRODUCTION 3 2. HOW WE COLLECT YOUR PERSONAL INFORMATION 3 3. TYPES OF INFORMATION WE COLLECT 4 4. HOW WE USE THE

Review of the effectiveness of an online database for small amount lenders

CONSULTATION PAPER 198 Review of the effectiveness of an online database for small amount lenders January 2013 About this paper This consultation paper explains the background and scope of ASIC s review

CONSULTATION PAPER 198 Review of the effectiveness of an online database for small amount lenders January 2013 About this paper This consultation paper explains the background and scope of ASIC s review

Residential mortgages general information

Residential mortgages general information Residential mortgages general information 2 Contents Who we are and what we do 2 Forms of security 2 Representative Example 2 Indication of possible further costs

Residential mortgages general information Residential mortgages general information 2 Contents Who we are and what we do 2 Forms of security 2 Representative Example 2 Indication of possible further costs

LEEDS BECKETT UNIVERSITY. Information Security Policy. 1.0 Introduction

LEEDS BECKETT UNIVERSITY Information Security Policy 1.0 Introduction 1.1 Information in all of its forms is crucial to the effective functioning and good governance of our University. We are committed

LEEDS BECKETT UNIVERSITY Information Security Policy 1.0 Introduction 1.1 Information in all of its forms is crucial to the effective functioning and good governance of our University. We are committed

STATES OF JERSEY DRAFT COLLECTIVE INVESTMENT FUNDS (RECOGNIZED FUNDS) (ACTIONS FOR DAMAGES) (JERSEY) REGULATIONS 200-

(ACTIONS FOR DAMAGES) (JERSEY) REGULATIONS 200-") STATES OF JERSEY r DRAFT COLLECTIVE INVESTMENT FUNDS (RECOGNIZED FUNDS) (ACTIONS FOR DAMAGES) (JERSEY) REGULATIONS 200- Lodged au Greffe on 8th October 2008 by the Minister for Economic Development STATES

STATES OF JERSEY r DRAFT COLLECTIVE INVESTMENT FUNDS (RECOGNIZED FUNDS) (ACTIONS FOR DAMAGES) (JERSEY) REGULATIONS 200- Lodged au Greffe on 8th October 2008 by the Minister for Economic Development STATES

Public Sector Pension Investment Board

Public Sector Pension Investment Board Office of the Auditor General of Canada Bureau du vérificateur général du Canada Ce document est également publié en français. Her Majesty the Queen in Right of Canada,

Public Sector Pension Investment Board Office of the Auditor General of Canada Bureau du vérificateur général du Canada Ce document est également publié en français. Her Majesty the Queen in Right of Canada,

Fair Debt. Policy. Why Have A Fair Debt Policy?

Fair Debt Policy A policy to assist customers who owe money to the council. Why Have A Fair Debt Policy? Wyre Borough Council is required to collect monies from both its residents (Council Tax) and businesses

Fair Debt Policy A policy to assist customers who owe money to the council. Why Have A Fair Debt Policy? Wyre Borough Council is required to collect monies from both its residents (Council Tax) and businesses

High Oak Surgery Complaints Policy Document Description Lead Author(s) Change History Document complies with the Equality Act 2010

Change History Document complies with the Equality Act 2010") High Oak Surgery Complaints Policy Document Description Document Type CQC Standard 7 Service Application Version 2 Ratification Date Target Group All staff Last Reviewed October 2012 Next Review Date October

High Oak Surgery Complaints Policy Document Description Document Type CQC Standard 7 Service Application Version 2 Ratification Date Target Group All staff Last Reviewed October 2012 Next Review Date October

Information Paper for the Legislative Council Panel on Financial Affairs. Protection of Consumer Credit Data

LC Paper No. CB(1)691/03-04(01) Information Paper for the Legislative Council Panel on Financial Affairs Protection of Consumer Credit Data Purpose Pursuant to the request by the Panel vide the Clerk to

LC Paper No. CB(1)691/03-04(01) Information Paper for the Legislative Council Panel on Financial Affairs Protection of Consumer Credit Data Purpose Pursuant to the request by the Panel vide the Clerk to

PRIVATE HEALTH INSURANCE INTERMEDIARIES PRACTICE CODES JUNE 2015 VERSION 2

PRIVATE HEALTH INSURANCE INTERMEDIARIES PRACTICE CODES JUNE 2015 VERSION 2 CONTENTS PART A - Pages 3-4 INTRODUCTION 1. ACCEPTANCE OF CODES 2. CODE COMPLIANCE 2.1 CODE COMPLIANCE COMMITTEE 3. REVIEW AND

PRIVATE HEALTH INSURANCE INTERMEDIARIES PRACTICE CODES JUNE 2015 VERSION 2 CONTENTS PART A - Pages 3-4 INTRODUCTION 1. ACCEPTANCE OF CODES 2. CODE COMPLIANCE 2.1 CODE COMPLIANCE COMMITTEE 3. REVIEW AND

II. Compliance Examinations - Compliance Management System. Compliance Management System. Introduction. Board of Directors and Management Oversight

Compliance Management System Introduction Financial institutions operate in a dynamic environment influenced by industry consolidation, convergence of financial services, emerging technology, and market

Compliance Management System Introduction Financial institutions operate in a dynamic environment influenced by industry consolidation, convergence of financial services, emerging technology, and market

Complaints that are not required to be considered under the arrangements

Under the provisions of the National Health Service (Pharmaceutical Services) Regulations 2005 pharmacy contractors are required to have in place arrangements, for the handling and consideration of complaints

Under the provisions of the National Health Service (Pharmaceutical Services) Regulations 2005 pharmacy contractors are required to have in place arrangements, for the handling and consideration of complaints

British Institute of Technology and E-commerce. Constitution, Governance and accreditation arrangements

British Institute of Technology and E-commerce Constitution, Governance and accreditation arrangements 1. BITE s constitution The British Institute of Technology and E-commerce is registered as a private

British Institute of Technology and E-commerce Constitution, Governance and accreditation arrangements 1. BITE s constitution The British Institute of Technology and E-commerce is registered as a private

Financial Regulation: An overview of the FCA s proposal of the new Consumer Credit regime October 2013

Financial Regulation: An overview of the FCA s proposal of the new Consumer Credit regime October 2013 Consultation Paper 13/10: Detailed Proposals for the FCA regime for Consumer Credit In early October

Financial Regulation: An overview of the FCA s proposal of the new Consumer Credit regime October 2013 Consultation Paper 13/10: Detailed Proposals for the FCA regime for Consumer Credit In early October

Information Governance Policy

Information Governance Policy 1 Introduction Healthwatch Rutland (HWR) needs to collect and use certain types of information about the Data Subjects who come into contact with it in order to carry on its

Information Governance Policy 1 Introduction Healthwatch Rutland (HWR) needs to collect and use certain types of information about the Data Subjects who come into contact with it in order to carry on its

ACCC/ASIC 'Debt collection guideline for collectors and creditors' publication review

1 November 2012 Mr Richard Weksler Assistant Director Compliance Strategies Branch Australian Competition & Consumer Commission Level 35 360 Elizabeth Street MELBOURNE VIC 3000 By email: [email protected]

1 November 2012 Mr Richard Weksler Assistant Director Compliance Strategies Branch Australian Competition & Consumer Commission Level 35 360 Elizabeth Street MELBOURNE VIC 3000 By email: [email protected]

South East Water Corporation Finance Audit and Risk Management Committee Charter. October 2012

South East Water Corporation Finance Audit and Risk Management Committee Charter October 2012 Version: 1.0 Page 1 of 6 DOCUMENT NUMBER BS 2359 1. Purpose The South East Water Corporation Board's Finance

South East Water Corporation Finance Audit and Risk Management Committee Charter October 2012 Version: 1.0 Page 1 of 6 DOCUMENT NUMBER BS 2359 1. Purpose The South East Water Corporation Board's Finance

DATA PROTECTION (JERSEY) LAW 2005 NO CREDIT? CREDIT EXPLAINED

LAW 2005 NO CREDIT? CREDIT EXPLAINED") DATA PROTECTION (JERSEY) LAW 2005 NO CREDIT? CREDIT EXPLAINED GD11 2 DATA PROTECTION (JERSEY) LAW 2005: NO CREDIT? Credit explained Contents Section 1 How do lenders decide if they will offer me credit?

DATA PROTECTION (JERSEY) LAW 2005 NO CREDIT? CREDIT EXPLAINED GD11 2 DATA PROTECTION (JERSEY) LAW 2005: NO CREDIT? Credit explained Contents Section 1 How do lenders decide if they will offer me credit?

TERMS OF BUSINESS. Our commitment to you MCCAMBRIDGE DUFFY INSOLVENCY PRACTITIONERS

TERMS OF BUSINESS Our commitment to you MCCAMBRIDGE DUFFY INSOLVENCY PRACTITIONERS The agreement between you & us is made on the following terms Definition of terms We/Us/Our You Creditors Insolvency Advice

TERMS OF BUSINESS Our commitment to you MCCAMBRIDGE DUFFY INSOLVENCY PRACTITIONERS The agreement between you & us is made on the following terms Definition of terms We/Us/Our You Creditors Insolvency Advice

APPLICATION OF KING III CORPORATE GOVERNANCE PRINCIPLES 2014

WOOLWORTHS HOLDINGS LIMITED CORPORATE GOVERNANCE PRINCIPLES 2014 CORPORATE GOVERNANCE PRINCIPLES 2014 CORPORATE GOVERNANCE PRINCIPLES 2014 This table is a useful reference to each of the King III principles

WOOLWORTHS HOLDINGS LIMITED CORPORATE GOVERNANCE PRINCIPLES 2014 CORPORATE GOVERNANCE PRINCIPLES 2014 CORPORATE GOVERNANCE PRINCIPLES 2014 This table is a useful reference to each of the King III principles

Report by Executive Director of Financial Services. Contact: Lynn Brown Ext: 73837 COPORATE DEBT POLICY

1 Glasgow City Council Executive Committee ITEM 4 24 th August 2007 Report by Executive Director of Financial Services Contact: Lynn Brown Ext: 73837 COPORATE DEBT POLICY Purpose of Report: The purpose

1 Glasgow City Council Executive Committee ITEM 4 24 th August 2007 Report by Executive Director of Financial Services Contact: Lynn Brown Ext: 73837 COPORATE DEBT POLICY Purpose of Report: The purpose

POLICIES, RULES AND GUIDELINES

APEC CROSS-BORDER PRIVACY RULES SYSTEM POLICIES, RULES AND GUIDELINES The purpose of this document is to describe the APEC Cross Border Privacy Rules (CBPR) System, its core elements, governance structure

APEC CROSS-BORDER PRIVACY RULES SYSTEM POLICIES, RULES AND GUIDELINES The purpose of this document is to describe the APEC Cross Border Privacy Rules (CBPR) System, its core elements, governance structure

Code of Professional and Ethical Conduct for Telecare Services Association of New Zealand (TSANZ)

") Code of Professional and Ethical Conduct for Telecare Services Association of New Zealand (TSANZ) The members of the Telecare Services are committed to the highest standards of professional and ethical

Code of Professional and Ethical Conduct for Telecare Services Association of New Zealand (TSANZ) The members of the Telecare Services are committed to the highest standards of professional and ethical

The NHS Foundation Trust Code of Governance

The NHS Foundation Trust Code of Governance www.monitor-nhsft.gov.uk The NHS Foundation Trust Code of Governance 1 Contents 1 Introduction 4 1.1 Why is there a code of governance for NHS foundation trusts?

The NHS Foundation Trust Code of Governance www.monitor-nhsft.gov.uk The NHS Foundation Trust Code of Governance 1 Contents 1 Introduction 4 1.1 Why is there a code of governance for NHS foundation trusts?

COUNTY OF ORANGE DEPARTMENT OF HEALTH. Corporate Compliance Plan

COUNTY OF ORANGE DEPARTMENT OF HEALTH Corporate Compliance Plan COUNTY OF ORANGE DEPARTMENT OF HEALTH CORPORATE COMPLIANCE PLAN I. Corporate Compliance Plan It is the policy of the Orange County Department

COUNTY OF ORANGE DEPARTMENT OF HEALTH Corporate Compliance Plan COUNTY OF ORANGE DEPARTMENT OF HEALTH CORPORATE COMPLIANCE PLAN I. Corporate Compliance Plan It is the policy of the Orange County Department

GOOD BANKING PRACTICE

GOOD BANKING PRACTICE 2015 1 GOOD BANKING PRACTICE GOOD BANKING PRACTICE Good banking practice fosters trust, performance and transparency. The principles of good banking apply to a bank s customer relationships

GOOD BANKING PRACTICE 2015 1 GOOD BANKING PRACTICE GOOD BANKING PRACTICE Good banking practice fosters trust, performance and transparency. The principles of good banking apply to a bank s customer relationships

Submission in response to the Life Insurance and Advice Working Group Interim Report on Retail Life Insurance

30 January 2015 Mr John Trowbridge Chairman Life Insurance and Advice Working Group Email: [email protected] Dear Mr Trowbridge, Submission in response to the Life Insurance and Advice Working

30 January 2015 Mr John Trowbridge Chairman Life Insurance and Advice Working Group Email: [email protected] Dear Mr Trowbridge, Submission in response to the Life Insurance and Advice Working