ACCOUNTING POLICY AND PROCEDURES (APP) MANUAL. TOPIC: Section 11 Institution Accounting 2.1 EFFECTIVE DATE: 06/01/1983

|

|

|

- August Cole

- 8 years ago

- Views:

Transcription

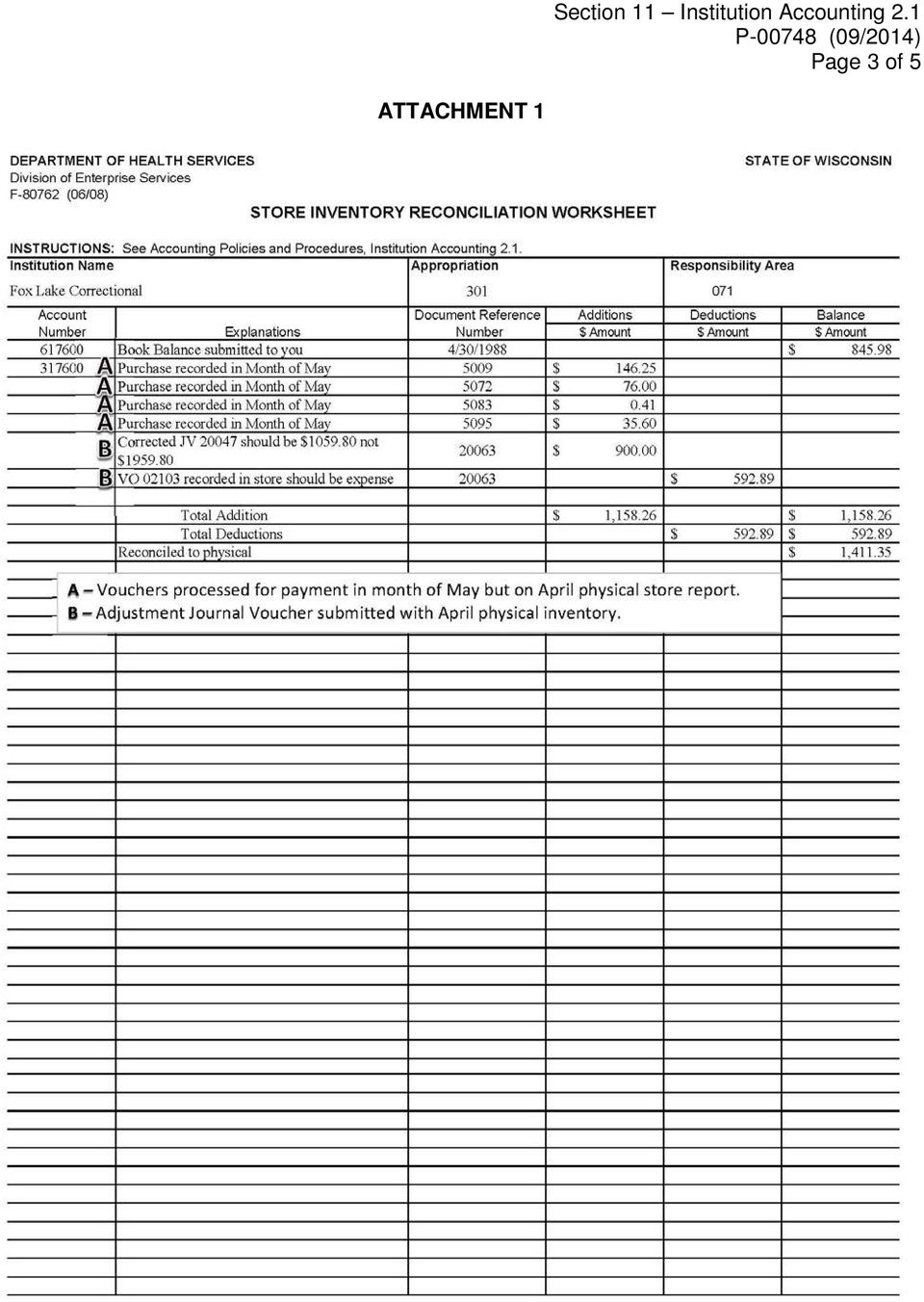

1 STATE OF WISCONSIN DEPARTMENT OF HEALTH SERVICES DIVISION OF ENTERPRISE SERVICES BUREAU OF FISCAL SERVICES ACCOUNTING POLICY AND PROCEDURES (APP) MANUAL TOPIC: EFFECTIVE DATE: 06/01/1983 TITLE: Store Inventory Reconciliation REVISION DATE: 01/21/2015 AUTHORIZED BY: Deputy Director, Bureau of Fiscal Services BACKGROUND The annual store accounts reconciliation will be based on a April 30 physical inventory in order to allow that reconciliation to be completed before other June 30 closing activities occur. To enable each organization to conduct store reconciliation activity throughout the year and thereby reduce problems during the April reconciliation activity, the Bureau of Fiscal Services (BFS) will submit interim store ledger balances as of October and January of each fiscal year. PROCEDURES 1. Each organization shall take a physical inventory of its store as of April 30. The April physical inventory store report will have the following: name of institution, appropriation, account cumber, account classification, responsibility area, item description, unit by type (case, can, bushel, etc.), size (case of 6, 12, 24 or #10 can, etc.), number of units, unit price, unit total (number times price), and grand total. Special care must be taken to ensure all purchases are recorded on the store records as the goods are received. This activity must occur even though the invoice paying for these items may not have been processed for payment. Failure to do so will result in the recorded issues creating an unacceptable negative inventory value. 2. In mid-may, BFS will provide each organization the final ledger values of their store accounts. In most cases the store accounts are recorded in responsibility area 071. However, certain organizations may also be using areas 075 and 077. Separate sheets will be utilized for each responsibility area s activity. The information will be provided in the format shown on the attached sheet. Select only those lines that pertain to store accounts within each appropriation. A brief explanation of each column is as follows: a. 4-digit account identifies the characters the computer uses to select the proper account for columns 2 and 3. b. 5-digit account represents expense account for current year store purchases. c. 5-digit account represents asset account to select prior fiscal period ending store account balance. d. Assets represents the dollar value of store account balances brought forward from the prior fiscal year. Page 1 of 5

will")

2 Page 2 of 5 e. Expenditures represents the dollar value of current year store account purchases as of April 30. f. Total represents the book value of the store accounts as of April 30 (column 4 plus column 5). Reconcile this amount to the physical store account inventory. 3. Each organization shall reconcile the April physical inventory to the April book values by using the Store Inventory Reconciliation Worksheet (F-80762). To accomplish the reconciliation, it may be necessary to account for items that were included on the physical inventory as of April 30 but were not paid for until later. Those on ledger adjustments should be recorded as an addition on the Store Inventory Reconciliation Worksheet (See item A of Attachment 1). If any adjustment, increase or decrease, is not on the ledger, a journal voucher must be prepared (see Attachment 2). Record the adjustment on the Store Inventory Reconciliation Worksheet (see item B of Attachment 1). Debits on the journal voucher will be recorded as additions on the Store Inventory Reconciliation Worksheet. Credits on the journal voucher will be recorded as deductions on the Store Inventory Reconciliation Worksheet. Any adjustment in any account in excess of $500 will require a detailed explanation. 4. Each organization shall have the April 30 physical Store Inventory Report, Store Inventory Reconciliation Worksheet (see Attachment 1), and the necessary Journal Vouchers completed and returned to BFS by June 17. FORMS Store Inventory Reconciliation Worksheet, F Journal Voucher, F store reconciliation entries ATTACHMENT 1 Sample Store Inventory Reconciliation Worksheet 2 Sample Journal Voucher 3 Store Inventory Report, per FMS CONTACTS Lead Accountant

.")

3 ATTACHMENT 1 Page 3 of 5

4 ATTACHMENT 2 Page 4 of 5

5 ATTACHMENT 3 Page 5 of 5

LEHMAN COLLEGE: DEPARTMENTAL RETENTION SCHEDULE 11/8/2013 ACCOUNTS PAYABLE. List of cost center codes for all College expenditures

AP-1 Appropriations of Expenditure Codes List of cost center codes for all College expenditures 6 years after superseded or obsolete General 9[9] b AP-2 Metrics Reports Reports prepared for the VP of Administration

AP-1 Appropriations of Expenditure Codes List of cost center codes for all College expenditures 6 years after superseded or obsolete General 9[9] b AP-2 Metrics Reports Reports prepared for the VP of Administration

TOWN OF CARLYLE POLICY MANUAL

TOWN OF CARLYLE POLICY MANUAL POLICY DESCRIPTION: POLICY NUMBER: IAC 0010 Internal Accounting Controls DATE APPROVED: March 26, 2008 DATE REVISED: October 12, 2011 Purpose of Policy: To promote and protect

TOWN OF CARLYLE POLICY MANUAL POLICY DESCRIPTION: POLICY NUMBER: IAC 0010 Internal Accounting Controls DATE APPROVED: March 26, 2008 DATE REVISED: October 12, 2011 Purpose of Policy: To promote and protect

CENTRAL SUSQUEHANNA INTERMEDIATE UNIT Application: Fund Accounting. Account Classes Directory Set Up Learning Guide

CENTRAL SUSQUEHANNA INTERMEDIATE UNIT Application: Fund Accounting Account Classes Directory Set Up Learning Guide 2009 Central Susquehanna Intermediate Unit, USA Table of Contents INTRODUCTION...3 Account

CENTRAL SUSQUEHANNA INTERMEDIATE UNIT Application: Fund Accounting Account Classes Directory Set Up Learning Guide 2009 Central Susquehanna Intermediate Unit, USA Table of Contents INTRODUCTION...3 Account

3. ACCOUNTING. 3.3 Capital Assets 3.3.4 Capital Asset System Accounting

3. ACCOUNTING 3.3 Capital Assets 3.3.4 Capital Asset System Accounting 3.3.4.10 Once the capital asset system is in operation, the government needs to make sure that assets which should be capitalized

3. ACCOUNTING 3.3 Capital Assets 3.3.4 Capital Asset System Accounting 3.3.4.10 Once the capital asset system is in operation, the government needs to make sure that assets which should be capitalized

CREDIT CARD PROCEDURES OBJECTIVE..2 OVERVIEW..2 DEPARTMENT S CREDIT CARD PROCEDURES...3 FINANCIAL SERVICES PROCEDURES... 5 BANK RECONCILIATION 6

CREDIT CARD PROCEDURES TABLE OF CONTENTS OBJECTIVE..2 OVERVIEW..2 DEPARTMENT S CREDIT CARD PROCEDURES...3 FINANCIAL SERVICES PROCEDURES... 5 BANK RECONCILIATION 6 APPENDIX A..16 APPENDIX B...18 OBJECTIVE

CREDIT CARD PROCEDURES TABLE OF CONTENTS OBJECTIVE..2 OVERVIEW..2 DEPARTMENT S CREDIT CARD PROCEDURES...3 FINANCIAL SERVICES PROCEDURES... 5 BANK RECONCILIATION 6 APPENDIX A..16 APPENDIX B...18 OBJECTIVE

The learners shall be able to

Grade: 12 Course Title: Fundamentals of Accountancy, Business and Management 2 Semester: 1 st Semester, 1 st Quarter No. of Hours/ Semester: 80 hours/ semester Prerequisite: Fundamentals of Accountancy,

Grade: 12 Course Title: Fundamentals of Accountancy, Business and Management 2 Semester: 1 st Semester, 1 st Quarter No. of Hours/ Semester: 80 hours/ semester Prerequisite: Fundamentals of Accountancy,

How To Perform Fund Accounting On A Fiscal Year 2009

CENTRAL SUSQUEHANNA INTERMEDIATE UNIT Application: Fund Accounting Fund Accounting - Learning Guide 2009 Central Susquehanna Intermediate Unit, USA Table of Contents INTRODUCTION...3...4 Run Option Fields...4

CENTRAL SUSQUEHANNA INTERMEDIATE UNIT Application: Fund Accounting Fund Accounting - Learning Guide 2009 Central Susquehanna Intermediate Unit, USA Table of Contents INTRODUCTION...3...4 Run Option Fields...4

3) The client side of the Service Fee Bookings MUST be closed with FOP of CC (Not CC Merchant)

The client side of the Service Fee Bookings MUST be closed with FOP of CC (Not CC Merchant)") Sabre Card Services The Sabre Card Services reconciliation option allows TBO users to daily close individual items in TBO that reconcile to the customer's Sabre Card Services' file by transaction, and

Sabre Card Services The Sabre Card Services reconciliation option allows TBO users to daily close individual items in TBO that reconcile to the customer's Sabre Card Services' file by transaction, and

ILLINOIS DEPARTMENT OF CENTRAL MANAGEMENT SERVICES CLASS SPECIFICATION CLASS TITLE POSITION CODE EFFECTIVE

ILLINOIS DEPARTMENT OF CENTRAL MANAGEMENT SERVICES CLASS SPECIFICATION CLASS TITLE POSITION CODE EFFECTIVE ACCOUNT CLERK I 00111 7-1-85 ACCOUNT CLERK II 00112 4-1-90 ACCOUNT TECHNICIAN I 00115 12-1-02

ILLINOIS DEPARTMENT OF CENTRAL MANAGEMENT SERVICES CLASS SPECIFICATION CLASS TITLE POSITION CODE EFFECTIVE ACCOUNT CLERK I 00111 7-1-85 ACCOUNT CLERK II 00112 4-1-90 ACCOUNT TECHNICIAN I 00115 12-1-02

Schools Using EPM as their Payroll Provider

Schools Using EPM as their Payroll Provider We strongly recommend that schools using EPM as their payroll provider manage their payroll costs using the Payroll Control Ledger Code. This is because EPM

Schools Using EPM as their Payroll Provider We strongly recommend that schools using EPM as their payroll provider manage their payroll costs using the Payroll Control Ledger Code. This is because EPM

ACCT 652 Accounting. Review of last week. Should you always take discounts? 5/17/15. ACCT652 Week 4 1

ACCT 652 Accounting Week 4 Special Journals, Cash, and Internal Controls Some slides Times Mirror Higher Education Division, Inc. Used by permission Michael D. Kinsman, Ph.D. Review of last week Some highlights

ACCT 652 Accounting Week 4 Special Journals, Cash, and Internal Controls Some slides Times Mirror Higher Education Division, Inc. Used by permission Michael D. Kinsman, Ph.D. Review of last week Some highlights

Cash Receipts, Cash Payments, and Banking Procedures

9-1 McGraw-Hill 2009 The McGraw-Hill Companies, Inc. All rights reserved. Cash Receipts, Cash Payments, and Banking Procedures Section 1: Cash Receipts Section Objectives 1. Record cash receipts in a cash

9-1 McGraw-Hill 2009 The McGraw-Hill Companies, Inc. All rights reserved. Cash Receipts, Cash Payments, and Banking Procedures Section 1: Cash Receipts Section Objectives 1. Record cash receipts in a cash

JOB READY ASSESSMENT BLUEPRINT ACCOUNTING-BASIC - PILOT. Test Code: 4100 Version: 01

JOB READY ASSESSMENT BLUEPRINT ACCOUNTING-BASIC - PILOT Test Code: 4100 Version: 01 Specific Competencies and Skills Tested in this Assessment: Journalizing Apply the accounting equation to journalize

JOB READY ASSESSMENT BLUEPRINT ACCOUNTING-BASIC - PILOT Test Code: 4100 Version: 01 Specific Competencies and Skills Tested in this Assessment: Journalizing Apply the accounting equation to journalize

Study Guide - Final Exam Accounting I

Study Guide - Final Exam Accounting I True/False Indicate whether the sentence or statement is true or false. 1. Entries in a sales journal affect account balances in both the accounts receivable ledger

Study Guide - Final Exam Accounting I True/False Indicate whether the sentence or statement is true or false. 1. Entries in a sales journal affect account balances in both the accounts receivable ledger

Repairing Your Accounting System

Repairing Your Accounting System Who is this paper for? This paper is for companies that have been using DBA Next-Generation for some time, but have struggled up to now with getting the accounting system

Repairing Your Accounting System Who is this paper for? This paper is for companies that have been using DBA Next-Generation for some time, but have struggled up to now with getting the accounting system

Objective Evidence. Unit of Measurement. Accounting Period Cycle. Business Entity. Going Concern. Adequate Disclosure. Matching Expenses with Revenue

Accounting Concept: A source document is prepared for each transaction Objective Evidence Accounting Concept: Business transactions are stated in numbers that have common values; that is, using a common

Accounting Concept: A source document is prepared for each transaction Objective Evidence Accounting Concept: Business transactions are stated in numbers that have common values; that is, using a common

LODGE AUDIT PROGRAM. A guide to conducting an audit of Lodge and Building Association Financial Records. Prepared by

LODGE AUDIT PROGRAM A guide to conducting an audit of Lodge and Building Association Financial Records. Prepared by Committee on Finance & Update by the Grand Secretary 2009 Most Worshipful Grand Lodge

LODGE AUDIT PROGRAM A guide to conducting an audit of Lodge and Building Association Financial Records. Prepared by Committee on Finance & Update by the Grand Secretary 2009 Most Worshipful Grand Lodge

Trouble Shooting Guide for Reconciling AR Account 12000001

This guide could be used to identify differences which exist when an agency tries to reconcile AR Account 12000001 Trial Balance amount to the Grant Open Invoice Items query TN_AR18_OPEN_GRANT_ITEMS. Step

This guide could be used to identify differences which exist when an agency tries to reconcile AR Account 12000001 Trial Balance amount to the Grant Open Invoice Items query TN_AR18_OPEN_GRANT_ITEMS. Step

Advanced Accounting. Chapter 4: Financial Reporting for a Departmentalized Business

Advanced Accounting Chapter 4: Financial Reporting for a Departmentalized Business Financial statements are used to summarize financial info and then are used to evaluate the financial position and progress

Advanced Accounting Chapter 4: Financial Reporting for a Departmentalized Business Financial statements are used to summarize financial info and then are used to evaluate the financial position and progress

CHAPTER 12 INTER-ENTITY TRANSACTIONS

CHAPTER 12 INTER-ENTITY TRANSACTIONS 1. INTRODUCTION. a. Purpose. The chapter establishes the principles and procedures of financing and accounting for costs of work performed by one DOE office or site/facility

CHAPTER 12 INTER-ENTITY TRANSACTIONS 1. INTRODUCTION. a. Purpose. The chapter establishes the principles and procedures of financing and accounting for costs of work performed by one DOE office or site/facility

Receiving Payment in Foreign Currency

Receiving Payment in Foreign Currency Contents An Example Preparing PCLaw for Foreign Currency Receiving Funds in Foreign Currency Performing Month End Procedures An Example To better illustrate the procedures

Receiving Payment in Foreign Currency Contents An Example Preparing PCLaw for Foreign Currency Receiving Funds in Foreign Currency Performing Month End Procedures An Example To better illustrate the procedures

Asset Management Reconciliation Procedures

Asset Management Reconciliation Procedures Purpose: To ensure the Asset Management Module is in sync with the General Ledger; thereby allowing for accurate and timely recording of OCO expenditures. 1.

Asset Management Reconciliation Procedures Purpose: To ensure the Asset Management Module is in sync with the General Ledger; thereby allowing for accurate and timely recording of OCO expenditures. 1.

Instructions for Schedule M-3 (Form 1065)

") 2015 Instructions for Schedule M-3 (Form 1065) Net Income (Loss) Reconciliation for Certain Partnerships Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

2015 Instructions for Schedule M-3 (Form 1065) Net Income (Loss) Reconciliation for Certain Partnerships Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

REGULAR PAYROLL ACCOUNTING

REGULAR PAYROLL ACCOUNTING Millersville University uses the Human Resource System (HRS) to handle its payroll process for both regular employees and student employees. The Human Resource Information System

REGULAR PAYROLL ACCOUNTING Millersville University uses the Human Resource System (HRS) to handle its payroll process for both regular employees and student employees. The Human Resource Information System

10-1. Auditing Business Process. Objectives Understand the Auditing of the Enteties Business. Process

10-1 Auditing Business Process Auditing Business Process Objectives Understand the Auditing of the Enteties Business Process Identify the types of transactions in different Business Process Asses Control

10-1 Auditing Business Process Auditing Business Process Objectives Understand the Auditing of the Enteties Business Process Identify the types of transactions in different Business Process Asses Control

COMPLETION OF THE ACCOUNTING CYCLE - Closing Entries -

COMPLETION OF THE ACCOUNTING CYCLE - Closing Entries - Worksheet Overview Trial Balance Adjustments Adjusted Trial Balance Income Statement Balance Sheet Account Titles Debit Credit Debit Credit Debit

COMPLETION OF THE ACCOUNTING CYCLE - Closing Entries - Worksheet Overview Trial Balance Adjustments Adjusted Trial Balance Income Statement Balance Sheet Account Titles Debit Credit Debit Credit Debit

9-1-1 OFFICE. State Fiscal Year 2014-2015 Instructions for Wireless Fund Reconciliation Package. Effective January 1, 2015

9-1-1 OFFICE State Fiscal Year 2014-2015 Instructions for Wireless Fund Reconciliation Package Effective January 1, 2015 Revised June 29, 2015 I. Overview... 1 II. General Instructions... 2 III. Required

9-1-1 OFFICE State Fiscal Year 2014-2015 Instructions for Wireless Fund Reconciliation Package Effective January 1, 2015 Revised June 29, 2015 I. Overview... 1 II. General Instructions... 2 III. Required

Chapter 15: Accounts Payable and Purchases

Accounting Research Manager - Audit Private Accounting Research Manager Miller Interpretations and Other Resources Knowledge-Based Audit Procedures Chapter 15: Accounts Payable and Purchases Chapter 15:

Accounting Research Manager - Audit Private Accounting Research Manager Miller Interpretations and Other Resources Knowledge-Based Audit Procedures Chapter 15: Accounts Payable and Purchases Chapter 15:

FBLA: ACCOUNTING I. Competency: Journalizing

Competency: Journalizing 1. Prepare a multi-column journal for recording data. 2. Record transactions such as accounts receivables and accounts payables in appropriate journals. 3. Journalize or record

Competency: Journalizing 1. Prepare a multi-column journal for recording data. 2. Record transactions such as accounts receivables and accounts payables in appropriate journals. 3. Journalize or record

Introductory Governmental Accounting Part I. For State and Local Governments

Introductory Governmental Accounting Part I For State and Local Governments FINANCIAL MANAGEMENT CERTIFICATE TRAINING PROGRAM INTRODUCTORY GOVERNMENTAL ACCOUNTING PART I COURSE OBJECTIVES Upon completion

Introductory Governmental Accounting Part I For State and Local Governments FINANCIAL MANAGEMENT CERTIFICATE TRAINING PROGRAM INTRODUCTORY GOVERNMENTAL ACCOUNTING PART I COURSE OBJECTIVES Upon completion

Accounting and Administrative Manual Section 100: Accounting and Finance

No.: G-03 Page: 1 of 6 General: The application of good financial management requires the prompt reconciliation of accounts. Since departmental revenue and expenditure accounts are scrutinized monthly

No.: G-03 Page: 1 of 6 General: The application of good financial management requires the prompt reconciliation of accounts. Since departmental revenue and expenditure accounts are scrutinized monthly

FINANCIAL AND PURCHASING RECORDS. Includes records showing a summary of receipts, disbursements and other activity against each account.

FINANCIAL AND PURCHASING RECORDS FN-1 Account Distribution Summaries (Treasurer s Report) Includes records showing a summary of receipts, disbursements and other activity against each account. Weekly/Monthly-

FINANCIAL AND PURCHASING RECORDS FN-1 Account Distribution Summaries (Treasurer s Report) Includes records showing a summary of receipts, disbursements and other activity against each account. Weekly/Monthly-

Records Retention Guidelines for Businesses, Individuals & Accounting Firms

Records Retention Guidelines for Businesses, Individuals & Accounting Firms Following are charts devised for individuals, businesses, and accounting firms. These charts may be used as a guideline for most

Records Retention Guidelines for Businesses, Individuals & Accounting Firms Following are charts devised for individuals, businesses, and accounting firms. These charts may be used as a guideline for most

Accounts Receivable Reconciliation Instructions. Using Reconciliation Template in Excel

Accounts Receivable Reconciliation Instructions Using Reconciliation Template in Excel 1 Log in to E-Print and print out the report called "FBM092_DelTo" for the month which you are reconciling 2 In the

Accounts Receivable Reconciliation Instructions Using Reconciliation Template in Excel 1 Log in to E-Print and print out the report called "FBM092_DelTo" for the month which you are reconciling 2 In the

In the event of a tie, the score on the last ten questions will be used as a tie-breaker.

NEW YORK STATE ASSOCIATION FUTURE BUSINESS LEADERS OF AMERICA SPRING DISTRICT MEETING ACCOUNTING I 2010 TEST DIRECTIONS 1. Complete the information requested on the answer sheet. PRINT your name on the

NEW YORK STATE ASSOCIATION FUTURE BUSINESS LEADERS OF AMERICA SPRING DISTRICT MEETING ACCOUNTING I 2010 TEST DIRECTIONS 1. Complete the information requested on the answer sheet. PRINT your name on the

Accruals, Deferrals,

12-1 McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Chapter Accruals, Deferrals, 12 and the Worksheet Section 1: Calculating and Recording Adjustments Section Objectives 1. Determine

12-1 McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Chapter Accruals, Deferrals, 12 and the Worksheet Section 1: Calculating and Recording Adjustments Section Objectives 1. Determine

M O N T H E N D / Q U A R T E R L Y / Y E A R E N D C H E C K L I S T S & P R O C E D U R E S ACCOUNTS RECEIVABLE ACCOUNTS PAYABLE

M O N T H E N D / Q U A R T E R L Y / Y E A R E N D C H E C K L I S T S & P R O C E D U R E S ACCOUNTS RECEIVABLE ACCOUNTS PAYABLE PAYROLL GENERAL LEDGER PROCOM SOLUTIONS, INC. OAKLAND CENTER 8980-A ROUTE

M O N T H E N D / Q U A R T E R L Y / Y E A R E N D C H E C K L I S T S & P R O C E D U R E S ACCOUNTS RECEIVABLE ACCOUNTS PAYABLE PAYROLL GENERAL LEDGER PROCOM SOLUTIONS, INC. OAKLAND CENTER 8980-A ROUTE

Audit Program for Accounts Payable and Purchases

Form AP 50 Index Audit Program for Accounts Payable and Purchases Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an understanding

Form AP 50 Index Audit Program for Accounts Payable and Purchases Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an understanding

STATE OF NEVADA Department of Administration Division of Human Resource Management CLASS SPECIFICATION TITLE GRADE EEO-4 CODE

STATE OF NEVADA Department of Administration Division of Human Resource Management CLASS SPECIFICATION TITLE GRADE EEO-4 CODE ACCOUNTANT TECHNICIAN III 34 C 7.140 SERIES DISCUSSION Positions allocated

STATE OF NEVADA Department of Administration Division of Human Resource Management CLASS SPECIFICATION TITLE GRADE EEO-4 CODE ACCOUNTANT TECHNICIAN III 34 C 7.140 SERIES DISCUSSION Positions allocated

Go to Tools General Ledger Setup Ledger Codes and Tab 5: Ledger Codes

Debit Card Functionality in FMS6 The SIMS Spring 2015 release introduced functionality to assist schools to record the use of debit cards to pay for goods and services. Prior to this release, payments

Debit Card Functionality in FMS6 The SIMS Spring 2015 release introduced functionality to assist schools to record the use of debit cards to pay for goods and services. Prior to this release, payments

FINACS INVENTORY Page 1 of 9 INVENTORY TABLE OF CONTENTS. 1. Stock Movement...2 2. Physical Stock Adjustment...7. (Compiled for FINACS v 2.12.

FINACS INVENTORY Page 1 of 9 INVENTORY TABLE OF CONTENTS 1. Stock Movement...2 2. Physical Stock Adjustment...7 (Compiled for FINACS v 2.12.002) FINACS INVENTORY Page 2 of 9 1. Stock Movement Inventory

FINACS INVENTORY Page 1 of 9 INVENTORY TABLE OF CONTENTS 1. Stock Movement...2 2. Physical Stock Adjustment...7 (Compiled for FINACS v 2.12.002) FINACS INVENTORY Page 2 of 9 1. Stock Movement Inventory

Introduction to Governmental Accounting

Introduction to Governmental Accounting Karin Slater, CPFO Montrose County School District RE-1J February 25, 2016 Introductions Introduction to Governmental Accounting Name Entity or Government Position

Introduction to Governmental Accounting Karin Slater, CPFO Montrose County School District RE-1J February 25, 2016 Introductions Introduction to Governmental Accounting Name Entity or Government Position

Inventory Control System Administration Manual

Inventory Control System Administration Manual Confidential Information This document contains proprietary and valuable, confidential trade secret information of APPX Software, Inc., Richmond, Virginia

Inventory Control System Administration Manual Confidential Information This document contains proprietary and valuable, confidential trade secret information of APPX Software, Inc., Richmond, Virginia

Vol I - Part 3 - Chapter 3000 PAYMENTS TO THE OFFICE OF PERSONNEL MANAGEMENT FOR HEALTH BENEFITS, GROUP LIFE INSURANCE, AND CIVIL SERVICE RETIREMENT

Vol I - Part 3 - Chapter 3000 PAYMENTS TO THE OFFICE OF PERSONNEL MANAGEMENT FOR HEALTH BENEFITS, GROUP LIFE INSURANCE, AND CIVIL SERVICE RETIREMENT Section 3010 - SCOPE AND APPLICABILITY This chapter

Vol I - Part 3 - Chapter 3000 PAYMENTS TO THE OFFICE OF PERSONNEL MANAGEMENT FOR HEALTH BENEFITS, GROUP LIFE INSURANCE, AND CIVIL SERVICE RETIREMENT Section 3010 - SCOPE AND APPLICABILITY This chapter

Prince Hall Grand Chapter, Order of the Eastern Star, Rite of Adoption, Hawaii and its Jurisdictions Inc. Basic Audit Procedures for All Chapters

Prince Hall Grand Chapter, Order of the Eastern Star, Rite of Adoption, Hawaii and its Jurisdictions Inc. Basic Audit Procedures for All Chapters Audit Committee The Audit Committee requires three members

Prince Hall Grand Chapter, Order of the Eastern Star, Rite of Adoption, Hawaii and its Jurisdictions Inc. Basic Audit Procedures for All Chapters Audit Committee The Audit Committee requires three members

TheFinancialEdge. Sample Reports Guide

TheFinancialEdge Sample Reports Guide 091708 2008 Blackbaud, Inc. This publication, or any part thereof, may not be reproduced or transmitted in any form or by any means, electronic, or mechanical, including

TheFinancialEdge Sample Reports Guide 091708 2008 Blackbaud, Inc. This publication, or any part thereof, may not be reproduced or transmitted in any form or by any means, electronic, or mechanical, including

Invoicing Internal Procedure

Office of Research and Sponsored Programs Invoicing Internal Procedure Issued: January, 2008 Implemented: March, 2008 BACKGROUND San Francisco State University (SFSU) receives funding for sponsored projects

Office of Research and Sponsored Programs Invoicing Internal Procedure Issued: January, 2008 Implemented: March, 2008 BACKGROUND San Francisco State University (SFSU) receives funding for sponsored projects

Intuit QuickBooks Enterprise Solutions 10.0 Complete List of Reports

Intuit QuickBooks Enterprise Solutions 10.0 Complete List of Reports Intuit QuickBooks Enterprise Solutions, for growing businesses, is the most powerful QuickBooks product. It has the capabilities and

Intuit QuickBooks Enterprise Solutions 10.0 Complete List of Reports Intuit QuickBooks Enterprise Solutions, for growing businesses, is the most powerful QuickBooks product. It has the capabilities and

SECTION 500 REPORTING INSTRUCTIONS SCHEDULE RFA RECONCILIATION OF INPATIENT AND OUTPATIENT DATA SETS REVENUE TO FINANCIAL DATA

SECTION 500 REPORTING INSTRUCTIONS SCHEDULE RFA RECONCILIATION OF INPATIENT AND OUTPATIENT DATA SETS REVENUE TO FINANCIAL DATA Overview Schedule RFA is provided to enable each hospital to reconcile, within

SECTION 500 REPORTING INSTRUCTIONS SCHEDULE RFA RECONCILIATION OF INPATIENT AND OUTPATIENT DATA SETS REVENUE TO FINANCIAL DATA Overview Schedule RFA is provided to enable each hospital to reconcile, within

Michigan School Loan Revolving Fund General Instructions for Completing Annual Repayment Activity Application

Michigan School Loan Revolving Fund General Instructions for Completing Annual Repayment Activity Application It is a statutory requirement that the district submit a completed Annual Repayment Activity

Michigan School Loan Revolving Fund General Instructions for Completing Annual Repayment Activity Application It is a statutory requirement that the district submit a completed Annual Repayment Activity

Bookkeeping Proficiency

Bookkeeping Proficiency (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Bookkeeping Proficiency (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Office of Programme Planning, Budget and Accounts Accounts Division revised 2008

Office of Programme Planning, Budget and Accounts Accounts Division revised 2008 Schedule No. Series Title Description Total ACCT Accounts Division ACCT101 Accounts Receivable used to produce receivable

Office of Programme Planning, Budget and Accounts Accounts Division revised 2008 Schedule No. Series Title Description Total ACCT Accounts Division ACCT101 Accounts Receivable used to produce receivable

Welcome to the internal reconciliation topic. 4-2-1

Welcome to the internal reconciliation topic. 4-2-1 In this topic, we discuss how to utilize the process of internal reconciliation, both system and user reconciliations, in G/L accounts and business partners.

Welcome to the internal reconciliation topic. 4-2-1 In this topic, we discuss how to utilize the process of internal reconciliation, both system and user reconciliations, in G/L accounts and business partners.

Self-test Comprehensive Problems II 综 合 自 测 题 II

Self-test Comprehensive Problems II 综 合 自 测 题 II Part One (30%) 1. Give the Chinese/English of the following terms: (5%) subsidiary ledger 统 制 账 户 purchase requisition 现 金 溢 缺 petty cash fund 永 续 盘 存 制

Self-test Comprehensive Problems II 综 合 自 测 题 II Part One (30%) 1. Give the Chinese/English of the following terms: (5%) subsidiary ledger 统 制 账 户 purchase requisition 现 金 溢 缺 petty cash fund 永 续 盘 存 制

Advanced District Concepts: More Fun With the Worksheet! 2014 Student Activity Conference

ACCOUNTING Advanced District Concepts: More Fun With the Worksheet! 2014 Student Activity Conference UIL Accounting 2014 SAC Advanced District Concepts: Worksheet -2- Suggested Solving Strategy and Detailed

ACCOUNTING Advanced District Concepts: More Fun With the Worksheet! 2014 Student Activity Conference UIL Accounting 2014 SAC Advanced District Concepts: Worksheet -2- Suggested Solving Strategy and Detailed

How To Reconcile Account Balance In Gpa

No.: G02 Page: 1 of 9 General: Depository bank account reconciliations must be submitted monthly to Statewide Fund Accounting prior to the end of the month following the period of the reconciliation. Earlier

No.: G02 Page: 1 of 9 General: Depository bank account reconciliations must be submitted monthly to Statewide Fund Accounting prior to the end of the month following the period of the reconciliation. Earlier

= Debt Service = Sub-Imprest = Non City Trust = Pool & Satellite = Miscellaneous

A. DEPARTMENT BANK ACCOUNTS AND INVESTMENTS Katrina Stauffer Division Chief Accounting Compliance Phone: 212/669-7861 Fax: 212/815-8784 Room 200 South E-mail: agencybankaccount@comptroller.nyc.gov Critical

A. DEPARTMENT BANK ACCOUNTS AND INVESTMENTS Katrina Stauffer Division Chief Accounting Compliance Phone: 212/669-7861 Fax: 212/815-8784 Room 200 South E-mail: agencybankaccount@comptroller.nyc.gov Critical

End User Reports. September 2013. Office of Budget & Planning

End User Reports September 2013 Office of Budget & Planning Table of Contents 1. Access Report in Adaptive Planning... 3 2. Report Viewing... 3 3. Available Budget Reports... 5 Proposed FY14 Budget vs.

End User Reports September 2013 Office of Budget & Planning Table of Contents 1. Access Report in Adaptive Planning... 3 2. Report Viewing... 3 3. Available Budget Reports... 5 Proposed FY14 Budget vs.

Agenda. Lecture Chapter 9 Quiz Chapter 8 Exercises & Problem Chapter 8. Objective. Cash Receipts. Cash Receipts, Payments, & Banking Procedures

Cash Receipts, Payments, & Banking Procedures Agenda Lecture Chapter 9 Quiz Chapter 8 Exercises & Problem Chapter 8 Cash Receipts, Payments, & Banking Procedures Objective Cash Receipts 1.cash receipts

Cash Receipts, Payments, & Banking Procedures Agenda Lecture Chapter 9 Quiz Chapter 8 Exercises & Problem Chapter 8 Cash Receipts, Payments, & Banking Procedures Objective Cash Receipts 1.cash receipts

CHAPTER Asset Management

CHAPTER 5 Asset Management 8/22/2012 Draft 63 of 106 Capital Asset* Maintenance and Reconciliation Responsible Positions Reviewed by Whom: Risk Type(s) The process of updating the general ledger to reflect

CHAPTER 5 Asset Management 8/22/2012 Draft 63 of 106 Capital Asset* Maintenance and Reconciliation Responsible Positions Reviewed by Whom: Risk Type(s) The process of updating the general ledger to reflect

OFFICE OF THE STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT SERVICES

OFFICE OF THE STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT SERVICES AND ECONOMIC DEVELOPMENT TECHNICAL ASSISTANCE Comptroller OFFICE OF THE STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT SERVICES & ECONOMIC

OFFICE OF THE STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT SERVICES AND ECONOMIC DEVELOPMENT TECHNICAL ASSISTANCE Comptroller OFFICE OF THE STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT SERVICES & ECONOMIC

ACCOUNTING POLICY AND PROCEDURES (APP) MANUAL. TOPIC: Section 9 FMS Processing 1.2 EFFECTIVE DATE: 06/28/1985

MANUAL. TOPIC: Section 9 FMS Processing 1.2 EFFECTIVE DATE: 06/28/1985") STATE OF WISCONSIN DEPARTMENT OF HEALTH SERVICES DIVISION OF ENTERPRISE SERVICES BUREAU OF FISCAL SERVICES ACCOUNTING POLICY AND PROCEDURES (APP) MANUAL TOPIC: Section 9 FMS Processing 1.2 EFFECTIVE DATE:

STATE OF WISCONSIN DEPARTMENT OF HEALTH SERVICES DIVISION OF ENTERPRISE SERVICES BUREAU OF FISCAL SERVICES ACCOUNTING POLICY AND PROCEDURES (APP) MANUAL TOPIC: Section 9 FMS Processing 1.2 EFFECTIVE DATE:

CHAPTER II GENERAL LEDGER ACCOUNTS

CHAPTER II GENERAL LEDGER ACCOUNTS A general ledger is basic to an accounting system. The General Ledger of a fund is a summary record containing the balance of assets, liabilities, deferred revenues,

CHAPTER II GENERAL LEDGER ACCOUNTS A general ledger is basic to an accounting system. The General Ledger of a fund is a summary record containing the balance of assets, liabilities, deferred revenues,

Fundamentals of Financial Accounting

Fundamentals of Financial Accounting CHAPTER I Accounting in action. What is accounting? Accounting is the recording of financial transactions plus storing, sorting, retrieving, summarizing, and presenting

Fundamentals of Financial Accounting CHAPTER I Accounting in action. What is accounting? Accounting is the recording of financial transactions plus storing, sorting, retrieving, summarizing, and presenting

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY. True-False Statements

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 9. 2 K 17. 4

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 9. 2 K 17. 4

Chapter 2. Analyzing transactions

1 Chapter 2 Analyzing transactions 2 Learning objectives 1. Explain the steps in the accounting cycle and each step s supporting documentation 2. Explain the purpose of source documents 3. Describe an

1 Chapter 2 Analyzing transactions 2 Learning objectives 1. Explain the steps in the accounting cycle and each step s supporting documentation 2. Explain the purpose of source documents 3. Describe an

SHIP Annual Report Webinar 2015. Sponsored by the Florida Housing Finance Corporation s Affordable Housing Catalyst Program

SHIP Annual Report Webinar 2015 Sponsored by the Florida Housing Finance Corporation s Affordable Housing Catalyst Program What will be covered What s New: 13/14 Topics Using the Annual Report website

SHIP Annual Report Webinar 2015 Sponsored by the Florida Housing Finance Corporation s Affordable Housing Catalyst Program What will be covered What s New: 13/14 Topics Using the Annual Report website

CONTROL AGENCIES POLICIES AND PROCEDURES MANUAL

1... 2 1.1 ISIS Overview... 2 1.1.1 Advantage Financial System (AFS)...2 1.1.2 Advanced Governmental Purchasing System (AGPS)...2 1.1.3 Contract Financial Management Subsystem (CFMS)...2 1.1.4 Human Resources

1... 2 1.1 ISIS Overview... 2 1.1.1 Advantage Financial System (AFS)...2 1.1.2 Advanced Governmental Purchasing System (AGPS)...2 1.1.3 Contract Financial Management Subsystem (CFMS)...2 1.1.4 Human Resources

Determining Correct Cost of Sales and Inventory Value GL Accounts

Vetstar Documentation Title: Cost of Sales General Ledger Posting Description Vetstar supports posting cost of sales to the appropriate general ledger account as part of end of day processing. This document

Vetstar Documentation Title: Cost of Sales General Ledger Posting Description Vetstar supports posting cost of sales to the appropriate general ledger account as part of end of day processing. This document

Attachment 14 Financial Monitoring Tool November 2008

Office of Housing and Community Partnerships Attachment 14 Financial Monitoring Tool November 2008 Prepared by: Ohio Department of Development Community Development Division Office of Housing and Community

Office of Housing and Community Partnerships Attachment 14 Financial Monitoring Tool November 2008 Prepared by: Ohio Department of Development Community Development Division Office of Housing and Community

UNIVERSITY OF CALIFORNIA, RIVERSIDE ACCOUNTING SERVICES SELF SUPPORTING OPERATIONS FISCAL YEAR END CLOSING May 22, 2012

UNIVERSITY OF CALIFORNIA, RIVERSIDE ACCOUNTING SERVICES SELF SUPPORTING OPERATIONS FISCAL YEAR END CLOSING May 22, 2012 What is Fiscal Year Closing? At the department level it is the process of closing

UNIVERSITY OF CALIFORNIA, RIVERSIDE ACCOUNTING SERVICES SELF SUPPORTING OPERATIONS FISCAL YEAR END CLOSING May 22, 2012 What is Fiscal Year Closing? At the department level it is the process of closing

VOLUME 1, CHAPTER 7: UNITED STATES STANDARD GENERAL LEDGER (USSGL) SUMMARY OF MAJOR CHANGES. All changes are denoted by blue font.

SUMMARY OF MAJOR CHANGES. All changes are denoted by blue font.") VOLUME 1, CHAPTER 7: UNITED STATES STANDARD GENERAL LEDGER (USSGL) SUMMARY OF MAJOR CHANGES All changes are denoted by blue font. Substantive revisions are denoted by an * symbol preceding the section,

VOLUME 1, CHAPTER 7: UNITED STATES STANDARD GENERAL LEDGER (USSGL) SUMMARY OF MAJOR CHANGES All changes are denoted by blue font. Substantive revisions are denoted by an * symbol preceding the section,

204 Reports Included with Version 7.0!

204 Reports Included with Version 7.0! Accounts Payable Aged A/P summary by name Aged A/P summary by number Detailed A/P activity by name Detailed A/P activity by number Detailed aged A/P by name Detailed

204 Reports Included with Version 7.0! Accounts Payable Aged A/P summary by name Aged A/P summary by number Detailed A/P activity by name Detailed A/P activity by number Detailed aged A/P by name Detailed

Click the Entries tab to enter transactions that originated at the bank.

Reconciling Bank Statements If this is the first time you have reconciled a bank statement for this company, you must prepare your bank accounts. See Chapter 4, Setting Up Bank Services, in the Tax and

Reconciling Bank Statements If this is the first time you have reconciled a bank statement for this company, you must prepare your bank accounts. See Chapter 4, Setting Up Bank Services, in the Tax and

Baseline Assessment. Date Accounting 1

Name Baseline Assessment Date Accounting 1 Part 1: Instructions: Place a check mark under the column for each account to determine which Financial the accounts belongs on. Financial Information 1. Cash

Name Baseline Assessment Date Accounting 1 Part 1: Instructions: Place a check mark under the column for each account to determine which Financial the accounts belongs on. Financial Information 1. Cash

Table of Contents. Line Descriptions 82.18 What should I know about the individual lines in schedule X?

SECTION 82 COMBINED SCHEDULE X Table of Contents Overview 82.1 What is schedule X? 82.2 What are schedules P, A, and S? 82.3 How is schedule X organized? 82.4 How are schedules A and S derived from schedule

SECTION 82 COMBINED SCHEDULE X Table of Contents Overview 82.1 What is schedule X? 82.2 What are schedules P, A, and S? 82.3 How is schedule X organized? 82.4 How are schedules A and S derived from schedule

Job Ready Assessment Blueprint. Accounting-Basic. Test Code: 4000 / Version: 01. Copyright 2012. All Rights Reserved.

Job Ready Assessment Blueprint Accounting-Basic Test Code: 4000 / Version: 01 Copyright 2012. All Rights Reserved. General Assessment Information Blueprint Contents General Assessment Information Written

Job Ready Assessment Blueprint Accounting-Basic Test Code: 4000 / Version: 01 Copyright 2012. All Rights Reserved. General Assessment Information Blueprint Contents General Assessment Information Written

1. Storeroom supplies -- For items stocked in the Palmer storeroom, use the Requisition for Supplies Form.

DISBURSEMENT PROCESSES Millersville University uses the Accounts Payable module of Banner Finance System to process vendor payments. After payroll, payments for goods and/or services represent the second

DISBURSEMENT PROCESSES Millersville University uses the Accounts Payable module of Banner Finance System to process vendor payments. After payroll, payments for goods and/or services represent the second

Chapter 3. Governmental Operating Statement Accounts; Budgetary Accounting

Chapter 3 Governmental Operating Statement Accounts; Budgetary Accounting 1 Definitions! General Fund (GF) " General Administration " Traditional Services! Special Revenue Fund (SRF) " Revenue used for

Chapter 3 Governmental Operating Statement Accounts; Budgetary Accounting 1 Definitions! General Fund (GF) " General Administration " Traditional Services! Special Revenue Fund (SRF) " Revenue used for

DoD Financial Management Regulation Volume 4, Chapter 9 January 1995 ACCOUNTS PAYABLE

CHAPTER 9 0901 GENERAL ACCOUNTS PAYABLE 090101. Purpose. This chapter provides guidance to be followed in recording and liquidating amounts payable by DoD Components. The processes described in this chapter

CHAPTER 9 0901 GENERAL ACCOUNTS PAYABLE 090101. Purpose. This chapter provides guidance to be followed in recording and liquidating amounts payable by DoD Components. The processes described in this chapter

Accounting 1. Lesson Plan. Topic: Accounting for Uncollectible Accounts Receivable Unit: 4 Chapter 21

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Accounting for Uncollectible Accounts Receivable Unit: 4 Chapter 21 I. Objective(s): By the end of today s lesson, the student will be able

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Accounting for Uncollectible Accounts Receivable Unit: 4 Chapter 21 I. Objective(s): By the end of today s lesson, the student will be able

AAT Level 2 Diploma in Accounting and Business

AAT Diploma in Accounting and Business Qualification specification Version date: July 2014 Ofqual qualification number: 60100229 1 Purpose statement Who is this qualification for? The purpose of this qualification

AAT Diploma in Accounting and Business Qualification specification Version date: July 2014 Ofqual qualification number: 60100229 1 Purpose statement Who is this qualification for? The purpose of this qualification

For illustrative purposes only, we will look at the logical flow of the Data Pro Job Cost package as a general contractor might use it.

ACCOUNTING FLOW OF JOB COST / TIME BILLING The Data Pro Job Costing Series has a number of component parts that create both the reporting capability and the accounting flow through the modules. These component

ACCOUNTING FLOW OF JOB COST / TIME BILLING The Data Pro Job Costing Series has a number of component parts that create both the reporting capability and the accounting flow through the modules. These component

Dr. M.D. Chase Accounting Principles Examination 2J Page 1

Accounting Principles Examination 2J Page 1 Code 1 1. The term "net sales" refers to gross sales revenue reduced by sales discounts and transportation-in. 2. The cost of goods available for sale in a given

Accounting Principles Examination 2J Page 1 Code 1 1. The term "net sales" refers to gross sales revenue reduced by sales discounts and transportation-in. 2. The cost of goods available for sale in a given

Accounting. Chapter 22

Accounting Chapter 22 Merchandise inventory on hand is typically the largest asset of a merchandising business Cost of Merchandise inventory is reported on both the balance sheet and income statement The

Accounting Chapter 22 Merchandise inventory on hand is typically the largest asset of a merchandising business Cost of Merchandise inventory is reported on both the balance sheet and income statement The

Prerequisite: None or as established by individual college. 3.0 semester credit hours/4.5 quarter credit hours/45 contact hours

I. CATALOG DESCRIPTION ACCT-1200 Principles of Accounting I Prerequisite: None or as established by individual college This course is designed to provide introductory knowledge of accounting principles,

I. CATALOG DESCRIPTION ACCT-1200 Principles of Accounting I Prerequisite: None or as established by individual college This course is designed to provide introductory knowledge of accounting principles,

Chapter 5 Accrual Adjustments and Financial Statement Preparation. Revenue recognition Matching expenses to revenues Expenses related to periods

Chapter 5 Accrual Adjustments and Financial Statement Preparation Revenue recognition Matching expenses to revenues Expenses related to periods 1 The Measurement of Income major function of accounting

Chapter 5 Accrual Adjustments and Financial Statement Preparation Revenue recognition Matching expenses to revenues Expenses related to periods 1 The Measurement of Income major function of accounting

Statement of Cash Flows

THE CONTENT AND VALUE OF THE STATEMENT OF CASH FLOWS The cash flow statement reconciles beginning and ending cash by presenting the cash receipts and cash disbursements of an enterprise for an accounting

THE CONTENT AND VALUE OF THE STATEMENT OF CASH FLOWS The cash flow statement reconciles beginning and ending cash by presenting the cash receipts and cash disbursements of an enterprise for an accounting

COMPUTERIZED ACCOUNTING I Curriculum Content Frameworks

COMPUTERIZED ACCOUNTING I Curriculum Content Frameworks Please note: All assessment questions will be taken from the knowledge portion of these frameworks. Prepared by Loretta Burgess, Greenbrier High

COMPUTERIZED ACCOUNTING I Curriculum Content Frameworks Please note: All assessment questions will be taken from the knowledge portion of these frameworks. Prepared by Loretta Burgess, Greenbrier High

In the event of a tie, the score on the last ten questions will be used as a tie-breaker.

NEW YORK STATE ASSOCIATION FUTURE BUSINESS LEADERS OF AMERICA SPRING DISTRICT MEETING ACCOUNTING II 2010 TEST DIRECTIONS 1. Complete the information requested on the answer sheet. PRINT your name on the

NEW YORK STATE ASSOCIATION FUTURE BUSINESS LEADERS OF AMERICA SPRING DISTRICT MEETING ACCOUNTING II 2010 TEST DIRECTIONS 1. Complete the information requested on the answer sheet. PRINT your name on the

COST PLUS AWARD FEE CONTRACT ADMINISTRATION DESKGUIDE

COST PLUS AWARD FEE CONTRACT ADMINISTRATION DESKGUIDE 1. Introduction. This Guide does not cover all aspects of administering a cost plus award fee (CPAF) contract. As all of the Directorates of Contracting

COST PLUS AWARD FEE CONTRACT ADMINISTRATION DESKGUIDE 1. Introduction. This Guide does not cover all aspects of administering a cost plus award fee (CPAF) contract. As all of the Directorates of Contracting

Chapter 13 Bank Reconciliations

Chapter 13 Bank Reconciliations The Bank Reconciliation module of school cash allows Treasurers to quickly perform bank reconciliations and print month-end reports for the Principal s review and approval.

Chapter 13 Bank Reconciliations The Bank Reconciliation module of school cash allows Treasurers to quickly perform bank reconciliations and print month-end reports for the Principal s review and approval.

Class 1-Permanent Record

Campus: District Department: Fiscal Services Classification Length of Retention for Class 3 records Supervisor of Destruction 1 = Permanent Record A = Upon acceptance of District Audit 1 = District Designee

Campus: District Department: Fiscal Services Classification Length of Retention for Class 3 records Supervisor of Destruction 1 = Permanent Record A = Upon acceptance of District Audit 1 = District Designee

Monthly Closing & Reconciliations. Presented by Bronwyn Duprey

Monthly Closing & Reconciliations Presented by Bronwyn Duprey Introduction Data Flow File Types Reconciling within an application Reconciling applications to General Ledger STO Reconciliation Tools Other

Monthly Closing & Reconciliations Presented by Bronwyn Duprey Introduction Data Flow File Types Reconciling within an application Reconciling applications to General Ledger STO Reconciliation Tools Other

UW-EXTENSION BUSINESS SERVICES POLICY AND PROCEDURE DOCUMENT (BSPPD) #18 CAPITAL EQUIPMENT

#18 CAPITAL EQUIPMENT") UW-EXTENSION BUSINESS SERVICES POLICY AND PROCEDURE DOCUMENT (BSPPD) #18 CAPITAL EQUIPMENT INTRODUCTION UW-System policy F33 establishes a systemwide policy on the accountability for capital equipment.

UW-EXTENSION BUSINESS SERVICES POLICY AND PROCEDURE DOCUMENT (BSPPD) #18 CAPITAL EQUIPMENT INTRODUCTION UW-System policy F33 establishes a systemwide policy on the accountability for capital equipment.

Accounts Payable and Inventory Management

Accounts Payable and Inventory Management 2013 SedonaOffice Users Conference Presented by: Lisa Gambatese & Laurie Goodrich Table of Contents Accounts Payable G/L Account Defaults (AP) 4 A/P Setup Processing

Accounts Payable and Inventory Management 2013 SedonaOffice Users Conference Presented by: Lisa Gambatese & Laurie Goodrich Table of Contents Accounts Payable G/L Account Defaults (AP) 4 A/P Setup Processing

keeping a running balance

keeping a running balance Record checks, a check card payment, an ATM transaction and a deposit in the checkbook register below. Include the date, description, and amount of each entry. Calculate the balance.

keeping a running balance Record checks, a check card payment, an ATM transaction and a deposit in the checkbook register below. Include the date, description, and amount of each entry. Calculate the balance.