Eric Ming Financial Markets Standard Chartered Bank (China) Limited May 2009

|

|

|

- Frank Dennis

- 9 years ago

- Views:

Transcription

1 Hedging in China Eric Ming Financial Markets Standard Chartered Bank (China) Limited May 2009

Limited May")

2 Content Standard d Chartered Bank Introduction ti FX Market Analysis USD/CNY Historical Trend USD/CNY Forecast USD/CNY Hedging Tools Major Currency against USD USD Interest est Rate Right time to hedge? CNY Interest Rate - Introduction CNY Yield Enhancement Product 2

3 Standard Chartered Bank Dalian Beijing Tianjin Qingdao Nanjing Suzhou Shanghai Ningbo Nanchang Hangzhou Chengdu Chongqing SCB (China) Branches: 15 Rep Offices: 1 Sub-branches: 37 Village Bank: 1 Guangzhou Xiamen Zhuhai Shenzhen 3

4 Standard Chartered Bank s Opened 1 st branch in Shanghai Pioneered the re-opening of branches & representative offices Established China Headquarters in Shanghai Obtained the license for Foreign Currency Derivatives 2005 Obtained the license for CNY Fixed Income Trading Obtained the license for CNY FX Forward 2006 Obtained the license for CNY FX Swap Shanghai Branch 1911 Launched RMB consumer banking services to PRC citizens 2007 One of the first 4 foreign banks become locally incorporated First foreign bank who gets license for onshore Commodity Derivatives 2008 Obtained the license for Equity Derivatives Beijing Branch 1923 Obtained premium dealership for PBOC paper and underwriting license of China Government Bond 4

5 Financial Markets China Achievements China Foreign Exchange Trade System (CFETS) Excellent Trading Bank Awards Excellent Member 2007 in the interbank RMB market Excellent Member 2008 on the interbank FX market Outstanding Dealer Awards China Foreign Exchange Trade System/National Interbank Funding Center Excellent Member 2005 in the interbank RMB market 2007 China Foreign Exchange Trade System/National Interbank Funding Center Excllent Member 2005 in the interbank FX market Our fixed income trader is awarded as the Outstanding Dealer Our FX traders are awarded as the Outstanding Dealer from on the FX interbank market for consecutive 4 years 5

6 SCB Financial Market Capability Financial Markets Asset Management Exposure Management Currency Linked Deposit Rate Linked Deposit Currency Interest Rate PCD (only FCY notional) PPCD No Touch, Touch, Wedding Cake, Range Accrual, etc Commodity Linked Deposit & Equity Linked Deposit CNY Extendible Deposit Spot, Forward, CCS (both FX&CNY) Option Strategy: Range Forward, Knockout Forward, Bonus Forward, etc. Option Strips: Participating Strip, Knock Out Forward Strip, At- Expiry Knock Out Strip, etc. Plain IRS, FRA,CNY Fixed Rate Loan Cap, Collar, Swaption, Inarrear Swap, Quanto, etc LIBOR Spread, Inverse Floater, Capped Floater, Multi- Callable, etc. Commodity Hedging 6

7 FX Market Analysis 7

8 USD/CNY Historical Graph PBoC start to float the spot Accelerating CNY appreciation, 1 Y NDF implied 16% annual appreciation Where is the next? 8

9 USD/CNY Recent 1 Year Movement 9

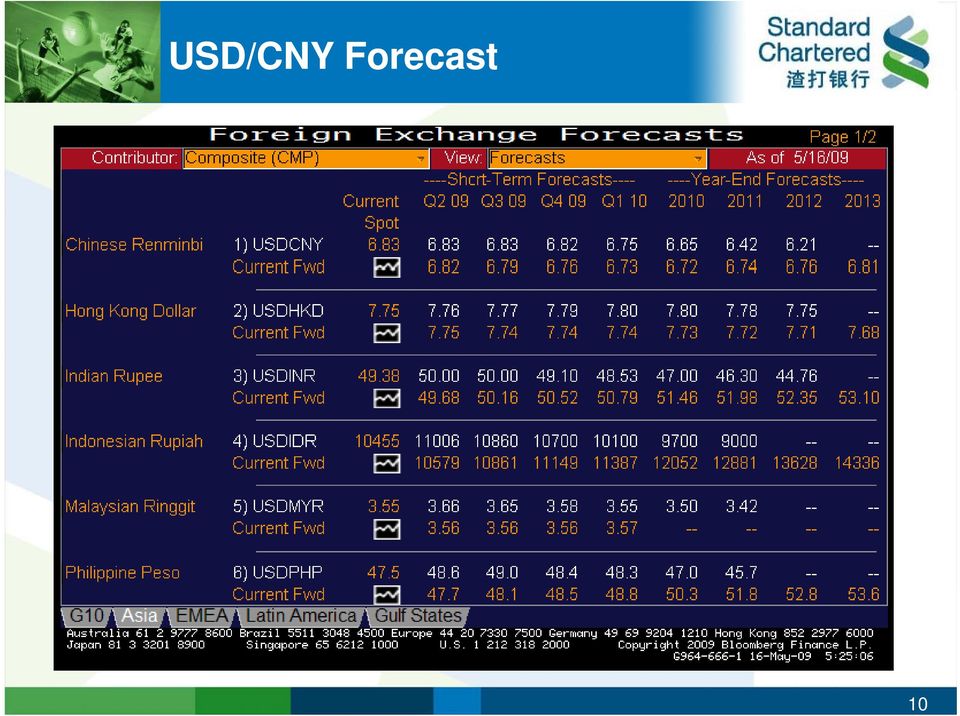

10 USD/CNY Forecast 10

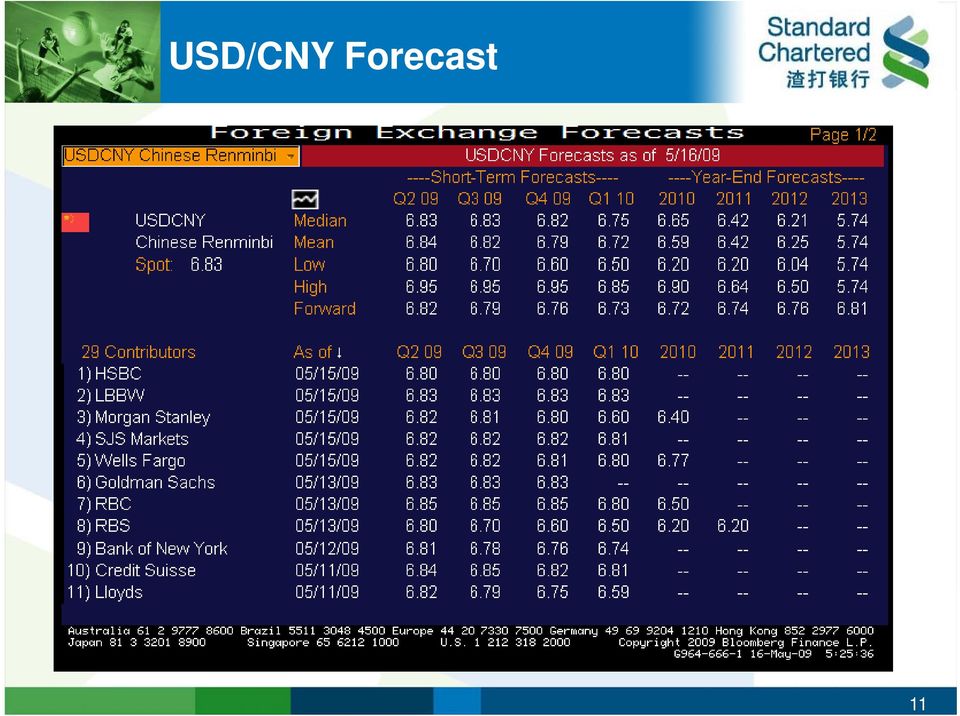

11 USD/CNY Forecast 11

12 USD/CNY Forecast 12

13 USD/CNY onshore Hedging Tool Vanilla Forward Par Forward Structured Forward 13

14 CNY Vanilla Forward Forward contract characteristics: an obligation to buy or sell a currency in the future principle amount,exchange rate and settlement day will fixed on the trade day How to calculate Forward? Forward = Spot + Swap points Client sell USD against CNY eg e.g 18 May 2009 USD/CNY Spot month Swap Point month Forward * For tenor between 1-3 months, notional under USD 50 mio will not affect the market liquidity 14

15 CNY Vanilla Forward Advantages: FX rate fixed on the trade day, disregard of the volatility of the FX markets Zero cost Easy to understand and execute Tenor can be adjusted (extended or early settled) based on real cash flow of the client Risks: On settlement day,if the Forward rate is worse than the Spot rate,forward contract may not in the money 15

16 SCB Forward Procedure Pre-deal preparation: Set up Limits Open the accounts Sign dealing mandate supported by Board of Resolution and FX terms and Conditions If the tenor is less than 1 year, no need to sign further; if the tenor is longer than 1 year, need to sign ISDA Trade Day: Over the phone,quote the FX forward rate with SCB Settlement: Deliver the required supporting documents to SCB which is as the same as spot transaction requires Make sure account balance is sufficient to cater for the settlement of the forward contract Deliver the instruction to SCB,in turn SCB will effect the payment upon the instruction The final settlement can be adjusted (early take up or extend) according to the real cash flow schedule. 16

according to the real cash flow")

17 Forward Policy Environment Business All FX deals which h can be done through h FX spot exchange are also permitted to Scope be traded through FX forward exchange; According to the updated regulation, the supporting document for the hedging is only required to be submitted to the bank on the settlement date. Documents Required by SAFE Trade Day: no supporting document is needed. Settlement Day: The requirement is as the same as documents for FX Spot For USD 1 mio and above 1. IC card 2. Contract and Invoice (original or copy plus company seal) 3. TT, i.e. Instruction, fax is acceptable if sign i-6 17

18 USD Index USD continuously depreciate starting from year 2000, until the financial crisis in 2008 From long term perspective, USD has the depreciation pressure One of the most Important factor to influence the index:risk appetite 18

19 Major Currency GBP/USD EUR/USD USD/CHF USD/XAU 19

20 USD Interest Rate Hedging 20

21 Interest Rate Swap - Sample Floating rate Bank Client Fixed rate t 21

22 USD Interest Rate Outlook Fed Funds Target rate was cut from 1% to currently 0.25%, as far as the rate cuts are concerned, the game is over. However, Fed pledged to keep the low rate for an extended period of time Quantitative easing strategies are made official and will become the main focus for the H As part of quantitative measures, Fed is ready and willing to buy vast amount of treasury supply, which signals that the yields will stay very low for much of 2009 In addition to the monetary easing, progress has been made in improving liquidity, as indicated by the gradual easing of LIBOR in the recent weeks USD 1Month & 3Month & 6Month LIBOR USD 1M LIBOR USD 3M LIBOR USD 6M LIBOR Source: Bloomberg Jan-00 Oct-00 Aug-01 Jun-02 Apr-03 Feb-04 Dec-04 Oct-05 Jul-06 May-07 Mar-08 Jan-09 22

23 USD Interest Rate - right time to hedge? 10 years Government Bonds Yield vs. Swap rate White line is USD 10 years swap rate Orange line is USD 10 years Bond yield 23

24 USD liability Right time to hedge 3M LIBOR and v.s. 2 years Swap rate 2 years Swap rate is at historical low close to 3M LIBOR 24

25 USD Vanilla Swap - Liability Indicative Terms & Conditions Trade Rationale Currency Start Maturity Client pays Client receives USD Spot 2 Year 1.33%, p.a, qtly, A/360 3m LIBOR, p.a, qtly, A/360 3m LIBOR 0.785% Risks: USD rates are at historical low, with the fact that there is limited magnitude of rates to be cut further, it is a very good timing for the client to pay fixed rate to hedge its liabilities Client will lock in the 2 years rate at 1.33% client will have a negative carry of 54.5bps (from today s Libor fixing of 0.785%) Note: Indicative pricing as of 15 May

26 USD Cancellable Swap - Liability Indicative Terms & Conditions Currency Start Maturity Client pays Client receives Early Termination USD Spot 2 Year USD 2y Swap Rate 1.33% 3m LIBOR 0.785% 1.25%, p.a, qtly, A/360 3m LIBOR, p.a, qtly, A/360 SCB has the right to cancel the deal at the end of year 1 at no cost. Note: Indicative pricing as of 13 Feb 2009 Trade Rationale USD rates are at historical low, with the fact that there is limited magnitude of rates to be cut further, it is a very good timing for the client to pay fixed rate to hedge its liabilities Client will enjoy a low fixed cost for the first 12 months, with cost further lowering by 8bps (from 2y vanilla IRS ref 1.33%) If after 1 Year the structure is not called, client is locked into the fixed rate, which protects the client against rising interest rates Risks: If it s called by SCB after 1 Year, client will be left with an unhedged position client will have a negative carry of 46.5bps (from today s Libor fixing of 0.785%) Scenario Analysis 1) Non Call until maturity 2) Call after 12 months 26

27 CNY Interest Rate hedging 27

28 CNY Interest Rate Swap SCB has both Onshore and Offshore franchise Onshore IRS market started t in 2006, and SCB China was one of the four market makers. In Q1 2009, SCB China s trading volume is 170bn RMB while the whole market is 800bn RMB In offshore IRS market, SCB is one of the top 5 banks CNY IRS is actively traded between inter-bank members 28

29 Index Graphs 29

30 Market Reference Index 7 day repo: It is the short term interbank funding rate. Banks which borrow money put securities (normally government bonds) into banks which lend money as collaterals. 7 day repo rate is one of the most important market interest rates in china, which effectively reflects market liquidity and cost of funding. Shibor 3M: Most people may be more familiar 3M Libor, 3M Hibor, etc. PBoC is keen to develop Shibor Rates to be the benchmark rates, and it is also viewed as a steppingstone to accomplish the marketization of interest rate market. Shibor OIS (overnight index swap) : Like 7 day repo, o/n rate is one day interbank funding cost, but it is without collaterals. 1Y Depo: 1 Year PBoC deposit rate 30

31 CNY Interest Rate Swap SCB is one of the 63 China onshore IRS trading banks Index Four indexes onshore total trading volume since 1 Jan 2008 is over CNY 417 Bn; the most liquid one is the 7day repo IRS CNY Bn 7 day repo IRS 309 3M Shibor IRS 56 Shibor OIS 35 1Y Depo IRS 17 Total

32 CNY Interest Rate Swap - Sample A vanilla CNY Depo IRS SCB receive fixed 2.50% from client for 5 years with Notional: CNY 100,000,000.00; ; Trade Day: 01 Feb 2009 Fixed Leg Client Pays Notional: CNY 100 mio Tenor: 5 years, annual fixing, Act/365 Fixed rate 2.50% Floating Leg Client receives Notional: CNY 100 mio Tenor: 5 years, annual fixing, Act/365 Floating rate: PBoC 1y Deposit rate (current 2.25%) 32

33 CNY Interest Rate Swap - Sample Liability side hedging i.e. corporate clients 1Y PBoC Depo Bank Client Fixed rate 2.50% 1Y PBoC Lending Loan Bank Client Total Payoff = 2.5% + ( 1Y PBoC Lending 1Y PBoC Depo ) Given most times PBoC will do symmetry rates hike or cut for Lending and Depo, the spread between them is very stable. This means Client almost locked up its funding cost. 33

34 CNY liability Cost Reduction -CNY Quanto Products Underlying currency of the swap : CNY In the swap formula, the reference index used is in another currency e.g. USD LIBOR, HKD 5Y CMS etc Settlement currency is still in CNY 34

35 CNY Structured Deposit 35

36 PBoC rate CNY Structured Deposit Tenor Interest (p.a.) Current 0.36% 1 Day Call 0.81% 7 Day Call 1.35% Agreed 1.17% 3 Months 1.71% 6 Months 1.98% 1 Year 2.25% 25% 36

37 Looking for Higher Return Time Deposit Interest Principal VS. Enhanced Interest Principal CNY Time Deposit CNY Structured Deposit Return from structured deposit > = < Time deposit interest 37

38 3 months LIBOR Historical Graph 3 months LIBOR 38

39 LIBOR Daily Range Accrual: Indicative Price Based on 13 May 2009 market condition: Notional Amount: CNY20 million Tenor: 180 days Reference Index: 3 months LIBOR Reference Index: [0, 7%] Annual Interest: 1.70%+0.4% * n/n (p.a.) n= The actual number of days while reference index is within the Reference Range N = The actual number of days in respective calculation period Reference 6 months CNY time deposit rate : 1.98% p.a. Prevailing 3m Libor : 0.88 % (as of 13 May 2009) 39

40 LIBOR Daily Range Accrual: Indicative Price Based on 13 May 2009 market condition: Notional Amount: CNY20 million Tenor: 365 days Reference Index: 3 months LIBOR Reference Index: [0, 8%] Annual Interest: 2.25%+0.05% * n/n (p.a.) n= The actual number of days while reference index is within the Reference Range N = The actual number of days in respective calculation period Reference 12 months CNY time deposit rate: 2.25% 25% p.a. Prevailing 3m Libor : 0.88 % (as of 13 May 2009) 40

41 CNY Structured Deposit Summary Indicative Price CNY Structured Deposit Linked to 3 month LIBOR Range 1 Week 2-3 Weeks 1 month 3 months 6 months 12 months Tenor 7 Days 14/21 Days 30 Days 90 Days 180 Days 365 Days Interest 1.70% 1.80% 1.90% 2.00% 2.10% 2.30% 41

42 Extendible Structured Deposit Yield Enhancement - Offer investors the opportunity to enjoy an enhanced yield in initial interest period as compared with traditional CNY term deposit; Protection against Rates Cut - Offer investors the one-time option, not obligation, to extend the deposits at guaranteed interests rate in predetermined d extendible interest t period to protect t against potential PBOC rates cut; Tenor Flexible - from 1 month and as long as total of initial and extendible interest periods within 6 months No FX exposure - Denomination of principal and interest payments both remain in CNY 42

43 Extendible Structured Deposit Principal: Tenor: If to Extend, CNY50,000,000 Initial Interest Period: 1 month Extendible Interest Period: 1 month Principal: i CNY50,000, Interests: CNY50,000,000*1.35%*30/365 At maturity of 1 month Principal: CNY50,000,000 Interests: CNY50,000, *1.90% 90%*30/365 Decide to extend or not 5 business days before the maturity If NOT to Extend, Simply enter another deposit with higher yield Interest Rate: Initial Interest Rate: 1.90% p.a. Extendible Interest Rate: 1.35% p.a. 43

44 Indicative Pricing Tenor Initial Interest Rate Extendible Interest Rate 1+1 month 1.90% 1.35% 2+2 months 1.95% 1.35% 3+3 months 2.00% 1.71% Above pricing is indicative only subject to market movement. If the extendible structured deposits can not be held till maturity, break funding cost will be charged subject to market conditions. 44

45 Disclaimer This document is issued by Standard Chartered Bank (SCB) and contains indicative terms of prospective transactions. It is for discussion purposes only and does not constitute any offer, recommendation, or solicitation to any person to enter into any transaction or adopt any hedging, trading or investment strategy, nor does it constitute any prediction of likely future movements in rates or prices or any representation that any such future movements will not exceed those shown in any illustration. The indicate terms are neither complete nor final and are subject to further discussion and negotiation. The terms of any transaction entered into will be recorded in a written confirmation or other document. SCB has no fiduciary duty towards you, and assumes no responsibility to advise on and makes no representation as to the appropriateness or possible consequences of the prospective transaction. SCB and.or a connected company, may have a position in any of the instruments or currencies mentioned in this document. You are advised to make your own independent judgement with respect to any matter contained herein. In the UK SCB conducts designated investment business only with Market Counterparties and Intermediate Customers and this document is directed only at such persons. Other persons should not rely on this document. Standard Chartered Bank is incorporated in England with limited liability by Royal Charter 1853 Reference ZC18. The principal office of the Company is situated in England at 1 Aldermandbury Square, London EC2V 7SB. Standard Chartered Bank is authorised and regulated by the FSA under FSA regulation number VAT number GB

CNH Market--A Burgeoning Offshore RMB Market

CNH Market--A Burgeoning Offshore RMB Market Liu Chenggang from Bank of China September, 2011 Contents I. Evolution of CNH Market II. Introduction ti of CNH Market III. Future Development of CNH Market

CNH Market--A Burgeoning Offshore RMB Market Liu Chenggang from Bank of China September, 2011 Contents I. Evolution of CNH Market II. Introduction ti of CNH Market III. Future Development of CNH Market

FX Option Solutions. FX Hedging & Investments

FX Option Solutions FX Hedging & Investments Contents 1. Liability side 2 Case Study I FX Hedging Case Study II FX Hedging 2. Asset side 30 FX Deposits 1 1. Liability side Case Study I FX Hedging Long

FX Option Solutions FX Hedging & Investments Contents 1. Liability side 2 Case Study I FX Hedging Case Study II FX Hedging 2. Asset side 30 FX Deposits 1 1. Liability side Case Study I FX Hedging Long

FX Strategies. in the Post-Crisis World. Eddie Wang Head of FX Structuring, Asia. Hong Kong October 2009

FX Strategies in the Post-Crisis World Eddie Wang Head of FX Structuring, Asia Hong Kong October 2009 Contents ONE Key Trends in the Post-Crisis World TWO FX Hedging Strategies THREE FX Investment Strategies

FX Strategies in the Post-Crisis World Eddie Wang Head of FX Structuring, Asia Hong Kong October 2009 Contents ONE Key Trends in the Post-Crisis World TWO FX Hedging Strategies THREE FX Investment Strategies

Overview of Offshore RMB

Overview of Offshore RMB Jaunary 214 Lee Beng-Hong Head of Markets, China Macro background Liberalization of RMB China fully liberalized the use of RMB for cross border trade settlement in March 212 close

Overview of Offshore RMB Jaunary 214 Lee Beng-Hong Head of Markets, China Macro background Liberalization of RMB China fully liberalized the use of RMB for cross border trade settlement in March 212 close

Advanced forms of currency swaps

Advanced forms of currency swaps Basis swaps Basis swaps involve swapping one floating index rate for another. Banks may need to use basis swaps to arrange a currency swap for the customers. Example A

Advanced forms of currency swaps Basis swaps Basis swaps involve swapping one floating index rate for another. Banks may need to use basis swaps to arrange a currency swap for the customers. Example A

FX Strategies. In the Low Yield Environment. Eddie Wang Head of FX Structuring, Asia. Hong Kong October 2010

FX Strategies In the Low Yield Environment Eddie Wang Head of FX Structuring, Asia Hong Kong October 2010 Contents 01 Key Trends 02 FX Hedging Strategies 03 FX Investment Strategies SECTION 01 Key Trends

FX Strategies In the Low Yield Environment Eddie Wang Head of FX Structuring, Asia Hong Kong October 2010 Contents 01 Key Trends 02 FX Hedging Strategies 03 FX Investment Strategies SECTION 01 Key Trends

RMB solutions for importers and exporters

RMB solutions for importers and exporters Unravel the complexities of RMB Mind the gap The potential Share of world trade vs payments The proof of the pudding Percentage of China s trade in RMB RMB 13th

RMB solutions for importers and exporters Unravel the complexities of RMB Mind the gap The potential Share of world trade vs payments The proof of the pudding Percentage of China s trade in RMB RMB 13th

Equity-index-linked swaps

Equity-index-linked swaps Equivalent to portfolios of forward contracts calling for the exchange of cash flows based on two different investment rates: a variable debt rate (e.g. 3-month LIBOR) and the

Equity-index-linked swaps Equivalent to portfolios of forward contracts calling for the exchange of cash flows based on two different investment rates: a variable debt rate (e.g. 3-month LIBOR) and the

Structure Products Asia 2006

Structure Products Asia 2006 China Structured Products : Innovation and Evolution Chin-Chong Liew Partner and Head of Derivatives & Structured Products Asia (Ex-Japan) 23 November 2006 Hong Kong 2 Chinese

Structure Products Asia 2006 China Structured Products : Innovation and Evolution Chin-Chong Liew Partner and Head of Derivatives & Structured Products Asia (Ex-Japan) 23 November 2006 Hong Kong 2 Chinese

Swaps: complex structures

Swaps: complex structures Complex swap structures refer to non-standard swaps whose coupons, notional, accrual and calendar used for coupon determination and payments are tailored made to serve client

Swaps: complex structures Complex swap structures refer to non-standard swaps whose coupons, notional, accrual and calendar used for coupon determination and payments are tailored made to serve client

Renminbi (RMB) corporate and treasury services in London

corporate and treasury services in London") Renminbi (RMB) corporate and treasury services in London City of London RENMINBI SERIES London offers an extensive range of RMB corporate banking services including: o Corporate accounts; o Term deposits;

Renminbi (RMB) corporate and treasury services in London City of London RENMINBI SERIES London offers an extensive range of RMB corporate banking services including: o Corporate accounts; o Term deposits;

Fixed Income Portfolio Management. Interest rate sensitivity, duration, and convexity

Fixed Income ortfolio Management Interest rate sensitivity, duration, and convexity assive bond portfolio management Active bond portfolio management Interest rate swaps 1 Interest rate sensitivity, duration,

Fixed Income ortfolio Management Interest rate sensitivity, duration, and convexity assive bond portfolio management Active bond portfolio management Interest rate swaps 1 Interest rate sensitivity, duration,

DCI Investment Trust. Da Cheng China RMB Fixed Income Fund. Addendum to the Explanatory Memorandum dated January 2012 ( Explanatory Memorandum )

") DCI Investment Trust Da Cheng China RMB Fixed Income Fund Addendum to the Explanatory Memorandum dated January 2012 ( Explanatory Memorandum ) IMPORTANT NOTE: This Addendum is supplemental to and forms

DCI Investment Trust Da Cheng China RMB Fixed Income Fund Addendum to the Explanatory Memorandum dated January 2012 ( Explanatory Memorandum ) IMPORTANT NOTE: This Addendum is supplemental to and forms

The table below shows Capita Asset Services forecast of the expected movement in medium term interest rates:

Annex A Forecast of interest rates as at September 2015 The table below shows Capita Asset Services forecast of the expected movement in medium term interest rates: NOW Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Annex A Forecast of interest rates as at September 2015 The table below shows Capita Asset Services forecast of the expected movement in medium term interest rates: NOW Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Managing Currency Mismatch. May 2010

Managing Currency Mismatch May 2010 FX Volatility 2 Very High Volatility in Asian Currencies Currency Performance % 140 130 120 110 100 90 80 70 60 50 40 Jan-06 Jun-06 Dec-06 Jun-07 Dec-07 May-08 Nov-08

Managing Currency Mismatch May 2010 FX Volatility 2 Very High Volatility in Asian Currencies Currency Performance % 140 130 120 110 100 90 80 70 60 50 40 Jan-06 Jun-06 Dec-06 Jun-07 Dec-07 May-08 Nov-08

Overview of RMB Internationalisation

Overview of RMB Internationalisation Candy Ho Head of RMB Business Development, Asia Pacific Date: 8 May 2013 Why is RMB important? China overtook US as the largest goods trading nation in 2012 China:

Overview of RMB Internationalisation Candy Ho Head of RMB Business Development, Asia Pacific Date: 8 May 2013 Why is RMB important? China overtook US as the largest goods trading nation in 2012 China:

INTEREST RATE SWAP (IRS)

") INTEREST RATE SWAP (IRS) 1. Interest Rate Swap (IRS)... 4 1.1 Terminology... 4 1.2 Application... 11 1.3 EONIA Swap... 19 1.4 Pricing and Mark to Market Revaluation of IRS... 22 2. Cross Currency Swap...

INTEREST RATE SWAP (IRS) 1. Interest Rate Swap (IRS)... 4 1.1 Terminology... 4 1.2 Application... 11 1.3 EONIA Swap... 19 1.4 Pricing and Mark to Market Revaluation of IRS... 22 2. Cross Currency Swap...

Derivatives, Measurement and Hedge Accounting

Derivatives, Measurement and Hedge Accounting IAS 39 11 June 2008 Contents Derivatives and embedded derivatives Definition Sample of products Accounting treatment Measurement Active market VS Inactive

Derivatives, Measurement and Hedge Accounting IAS 39 11 June 2008 Contents Derivatives and embedded derivatives Definition Sample of products Accounting treatment Measurement Active market VS Inactive

ECONOMIC REVIEW(A Monthly Issue) March, April, 2015 2014

March, April, 2015 2014") ECONOMIC REVIEW(A Monthly Issue) March, April, 2015 2014 Economics & Strategic Planning Department http://www.bochk.com Effects The of Reasons CNH Exchange Why the Rate Singapore on Offshore Economy RMB

ECONOMIC REVIEW(A Monthly Issue) March, April, 2015 2014 Economics & Strategic Planning Department http://www.bochk.com Effects The of Reasons CNH Exchange Why the Rate Singapore on Offshore Economy RMB

FIN 684 Fixed-Income Analysis From Repos to Monetary Policy. Funding Positions

FIN 684 Fixed-Income Analysis From Repos to Monetary Policy Professor Robert B.H. Hauswald Kogod School of Business, AU Funding Positions Short-term funding: repos and money markets funding trading positions

FIN 684 Fixed-Income Analysis From Repos to Monetary Policy Professor Robert B.H. Hauswald Kogod School of Business, AU Funding Positions Short-term funding: repos and money markets funding trading positions

The FTSE China Onshore Bond Index Series

Research The FTSE China Onshore Bond Index Series ftserussell.com May 2015 China is now the world s largest economy (when measured by purchasing power parity (PPP) 1 ) and the largest trading nation 2.

Research The FTSE China Onshore Bond Index Series ftserussell.com May 2015 China is now the world s largest economy (when measured by purchasing power parity (PPP) 1 ) and the largest trading nation 2.

Financial Risk Management

176 Financial Risk Management For the year ended 31 December 2014 1. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES s major financial instruments include cash and bank balances, time deposits, principal-protected

176 Financial Risk Management For the year ended 31 December 2014 1. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES s major financial instruments include cash and bank balances, time deposits, principal-protected

Introduction to Fixed Income (IFI) Course Syllabus

Course Syllabus") Introduction to Fixed Income (IFI) Course Syllabus 1. Fixed income markets 1.1 Understand the function of fixed income markets 1.2 Know the main fixed income market products: Loans Bonds Money market instruments

Introduction to Fixed Income (IFI) Course Syllabus 1. Fixed income markets 1.1 Understand the function of fixed income markets 1.2 Know the main fixed income market products: Loans Bonds Money market instruments

HSBC India Global Markets overview PUBLIC

HSBC India Global Markets overview Part 1. Hedging FX and Rate Exposures FX and Rates Market Overview FX Spot and Forwards Very Liquid spot market estimated daily volume of USD 5 billion Over 15 active

HSBC India Global Markets overview Part 1. Hedging FX and Rate Exposures FX and Rates Market Overview FX Spot and Forwards Very Liquid spot market estimated daily volume of USD 5 billion Over 15 active

ONIA Swap Index. The derivatives market reference rate for the Euro

ONIA Swap Index The derivatives market reference rate for the Euro Contents Introduction 2 What is an EONIA Swap? 3-4 EONIA Swap Index The new benchmark 5-8 EONIA 9-10 Basis Swaps 10 IRS vs. EONIA Swap

ONIA Swap Index The derivatives market reference rate for the Euro Contents Introduction 2 What is an EONIA Swap? 3-4 EONIA Swap Index The new benchmark 5-8 EONIA 9-10 Basis Swaps 10 IRS vs. EONIA Swap

Floating rate Payments 6m Libor. Fixed rate payments 1 300000 337500-37500 2 300000 337500-37500 3 300000 337500-37500 4 300000 325000-25000

Introduction: Interest rate swaps are used to hedge interest rate risks as well as to take on interest rate risks. If a treasurer is of the view that interest rates will be falling in the future, he may

Introduction: Interest rate swaps are used to hedge interest rate risks as well as to take on interest rate risks. If a treasurer is of the view that interest rates will be falling in the future, he may

Important Facts Statement

Bank of China (Hong Kong) Limited Important Facts Statement Currency Linked Deposits - Premium Deposits Currency Linked Deposits 13 April 2015 This is a structured investment product which is NOT protected

Bank of China (Hong Kong) Limited Important Facts Statement Currency Linked Deposits - Premium Deposits Currency Linked Deposits 13 April 2015 This is a structured investment product which is NOT protected

Managing Interest Rate Exposure

Managing Interest Rate Exposure Global Markets Contents Products to manage Interest Rate Exposure...1 Interest Rate Swap Product Overview...2 Interest Rate Cap Product Overview...8 Interest Rate Collar

Managing Interest Rate Exposure Global Markets Contents Products to manage Interest Rate Exposure...1 Interest Rate Swap Product Overview...2 Interest Rate Cap Product Overview...8 Interest Rate Collar

CHAPTER 6. Different Types of Swaps 1

CHAPTER 6 Different Types of Swaps 1 In the previous chapter, we introduced two simple kinds of generic swaps: interest rate and currency swaps. These are usually known as plain vanilla deals because the

CHAPTER 6 Different Types of Swaps 1 In the previous chapter, we introduced two simple kinds of generic swaps: interest rate and currency swaps. These are usually known as plain vanilla deals because the

Pricing and Strategy for Muni BMA Swaps

J.P. Morgan Management Municipal Strategy Note BMA Basis Swaps: Can be used to trade the relative value of Libor against short maturity tax exempt bonds. Imply future tax rates and can be used to take

J.P. Morgan Management Municipal Strategy Note BMA Basis Swaps: Can be used to trade the relative value of Libor against short maturity tax exempt bonds. Imply future tax rates and can be used to take

The new ACI Diploma. Unit 2 Fixed Income & Money Markets. Effective October 2014

The new ACI Diploma Unit 2 Fixed Income & Money Markets Effective October 2014 8 Rue du Mail, 75002 Paris - France T: +33 1 42975115 - F: +33 1 42975116 - www.aciforex.org The new ACI Diploma Objective

The new ACI Diploma Unit 2 Fixed Income & Money Markets Effective October 2014 8 Rue du Mail, 75002 Paris - France T: +33 1 42975115 - F: +33 1 42975116 - www.aciforex.org The new ACI Diploma Objective

1.2 Structured notes

1.2 Structured notes Structured notes are financial products that appear to be fixed income instruments, but contain embedded options and do not necessarily reflect the risk of the issuing credit. Used

1.2 Structured notes Structured notes are financial products that appear to be fixed income instruments, but contain embedded options and do not necessarily reflect the risk of the issuing credit. Used

Industrial and Commercial Bank of China Limited Dealing frequency: Daily on each business day *

APRIL 2016 This statement provides you with key information about Income Partners RMB Bond Fund (the Sub-Fund ). This statement is a part of the offering document and must be read in conjunction with the

APRIL 2016 This statement provides you with key information about Income Partners RMB Bond Fund (the Sub-Fund ). This statement is a part of the offering document and must be read in conjunction with the

Chinese Yuan Non-Deliverable Forward Transactions

Chinese Yuan Non-Deliverable Forward Transactions By entering into Chinese Yuan Non-Deliverable Forward Transactions ( NDF ) with Bank of China (Hong Kong) Limited (the Bank ), you can buy or sell Chinese

Chinese Yuan Non-Deliverable Forward Transactions By entering into Chinese Yuan Non-Deliverable Forward Transactions ( NDF ) with Bank of China (Hong Kong) Limited (the Bank ), you can buy or sell Chinese

How To Understand A Rates Transaction

International Swaps and Derivatives Association, Inc. Disclosure Annex for Interest Rate Transactions This Annex supplements and should be read in conjunction with the General Disclosure Statement. NOTHING

International Swaps and Derivatives Association, Inc. Disclosure Annex for Interest Rate Transactions This Annex supplements and should be read in conjunction with the General Disclosure Statement. NOTHING

INR Volatility - Hedging Options & Effective Strategies

INR Volatility - Hedging Options & Effective Strategies The purpose of the article is to draw attention on the recent volatility in Indian Rupee, various hedging options and effective hedging strategies.

INR Volatility - Hedging Options & Effective Strategies The purpose of the article is to draw attention on the recent volatility in Indian Rupee, various hedging options and effective hedging strategies.

Eurodollar Futures, and Forwards

5 Eurodollar Futures, and Forwards In this chapter we will learn about Eurodollar Deposits Eurodollar Futures Contracts, Hedging strategies using ED Futures, Forward Rate Agreements, Pricing FRAs. Hedging

5 Eurodollar Futures, and Forwards In this chapter we will learn about Eurodollar Deposits Eurodollar Futures Contracts, Hedging strategies using ED Futures, Forward Rate Agreements, Pricing FRAs. Hedging

Understanding Futures on the DTCC GCF Repo Index

Understanding Futures on the DTCC GCF Repo Index White Paper June 2014 This material may not be reproduced or redistributed in whole or in part without the express, prior written consent of Intercontinental

Understanding Futures on the DTCC GCF Repo Index White Paper June 2014 This material may not be reproduced or redistributed in whole or in part without the express, prior written consent of Intercontinental

RMB: A New Trade and Settlement Currency

IMAGE AREA IMAGERY MAY BE INSERTED HERE (must be from approved source eg istock, Shutterstock or approved HSBC imagery) OR GREY AREA DELETED AND LEFT BLANK WHITE RMB: A New Trade and Settlement Currency

IMAGE AREA IMAGERY MAY BE INSERTED HERE (must be from approved source eg istock, Shutterstock or approved HSBC imagery) OR GREY AREA DELETED AND LEFT BLANK WHITE RMB: A New Trade and Settlement Currency

1. 2015 Gross Borrowing Requirements and Funding Plan

1 1. 2015 Gross Borrowing Requirements and Funding Plan 1.1 Gross Borrowing requirements The Treasury expects its 2015 gross borrowing requirements to amount to EUR 39.90 billion. This represents an increase

1 1. 2015 Gross Borrowing Requirements and Funding Plan 1.1 Gross Borrowing requirements The Treasury expects its 2015 gross borrowing requirements to amount to EUR 39.90 billion. This represents an increase

Introductory Guide to RMB Currency Futures

Introductory Guide to RMB Currency Futures RMB Internationalisation The opening up of Mainland China now is creating more and more business opportunities. China is the second largest economy and a major

Introductory Guide to RMB Currency Futures RMB Internationalisation The opening up of Mainland China now is creating more and more business opportunities. China is the second largest economy and a major

INDUSTRIAL AND COMMERCIAL BANK OF CHINA ICBC: Your Global Portal to RMB Market. July 2012

ICBC: Your Global Portal to RMB Market July 2012 Content General Introduction Investment in RMB Services Solution 1 General Introduction to Renminbi (RMB) RMB Renminbi (commonly abbreviated as RMB) is

ICBC: Your Global Portal to RMB Market July 2012 Content General Introduction Investment in RMB Services Solution 1 General Introduction to Renminbi (RMB) RMB Renminbi (commonly abbreviated as RMB) is

Interest Rate Swap. Product Disclosure Statement

Interest Rate Swap Product Disclosure Statement A Product Disclosure Statement is an informative document. The purpose of a Product Disclosure Statement is to provide you with enough information to allow

Interest Rate Swap Product Disclosure Statement A Product Disclosure Statement is an informative document. The purpose of a Product Disclosure Statement is to provide you with enough information to allow

Risk and Investment Conference 2013. Brighton, 17 19 June

Risk and Investment Conference 03 Brighton, 7 9 June 0 June 03 Acquiring fixed income assets on a forward basis Dick Rae, HSBC and Neil Snyman, Aviva Investors 8 June 0 Structure of Presentation Introduction

Risk and Investment Conference 03 Brighton, 7 9 June 0 June 03 Acquiring fixed income assets on a forward basis Dick Rae, HSBC and Neil Snyman, Aviva Investors 8 June 0 Structure of Presentation Introduction

Product Disclosure Statement

Product Disclosure Statement Australia - June 2015 Associated Foreign Exchange Australia Pty Ltd. ABN: 85 119 392 586 ACN: 119 392 586 AFSL Number: 305246 Global Payment and Risk Management Solutions Table

Product Disclosure Statement Australia - June 2015 Associated Foreign Exchange Australia Pty Ltd. ABN: 85 119 392 586 ACN: 119 392 586 AFSL Number: 305246 Global Payment and Risk Management Solutions Table

8. Eurodollars: Parallel Settlement

8. Eurodollars: Parallel Settlement Eurodollars are dollar balances held by banks or bank branches outside the country, which banks hold no reserves at the Fed and consequently have no direct access to

8. Eurodollars: Parallel Settlement Eurodollars are dollar balances held by banks or bank branches outside the country, which banks hold no reserves at the Fed and consequently have no direct access to

FIN 472 Fixed-Income Securities Forward Rates

FIN 472 Fixed-Income Securities Forward Rates Professor Robert B.H. Hauswald Kogod School of Business, AU Interest-Rate Forwards Review of yield curve analysis Forwards yet another use of yield curve forward

FIN 472 Fixed-Income Securities Forward Rates Professor Robert B.H. Hauswald Kogod School of Business, AU Interest-Rate Forwards Review of yield curve analysis Forwards yet another use of yield curve forward

An Overview of Offshore RMB Market. Nov 2013

An Overview of Offshore RMB Market Nov 2013 Contents 1. Outlook of RMB Internationalisation 2. Implications for Offshore RMB Bonds 2 Section 1 Outlook of RMB Internationalisation 3 RMB The next international

An Overview of Offshore RMB Market Nov 2013 Contents 1. Outlook of RMB Internationalisation 2. Implications for Offshore RMB Bonds 2 Section 1 Outlook of RMB Internationalisation 3 RMB The next international

Learning Curve An introduction to the use of the Bloomberg system in swaps analysis Received: 1st July, 2002

Learning Curve An introduction to the use of the Bloomberg system in swaps analysis Received: 1st July, 2002 Aaron Nematnejad works in the fixed income analytics team at Bloomberg L.P. in London. He graduated

Learning Curve An introduction to the use of the Bloomberg system in swaps analysis Received: 1st July, 2002 Aaron Nematnejad works in the fixed income analytics team at Bloomberg L.P. in London. He graduated

Derivatives Market Trading Division July 2012. Understanding RMB Currency Futures Contract (USD/CNH)

") Derivatives Market Trading Division July 2012 Understanding RMB Currency Futures Contract (USD/CNH) Part A Trading Arrangements Table of Contents 1 Key Milestones of Development of Offshore RMB market

Derivatives Market Trading Division July 2012 Understanding RMB Currency Futures Contract (USD/CNH) Part A Trading Arrangements Table of Contents 1 Key Milestones of Development of Offshore RMB market

Important Facts. Currency Linked Deposit Mar 2015

Important Facts Currency Linked Deposit Mar 2015 Important tice: This is a structured product involving derivatives. The investment decision is yours but you should not invest in currency linked deposit

Important Facts Currency Linked Deposit Mar 2015 Important tice: This is a structured product involving derivatives. The investment decision is yours but you should not invest in currency linked deposit

TREASURY PRODUCTS AND SERVICES MANAGING FINANCIAL RISKS, ENHANCING RETURNS, ACHIEVEING INVESTMENT GOALS 2016

TREASURY PRODUCTS AND SERVICES MANAGING FINANCIAL RISKS, ENHANCING RETURNS, ACHIEVEING INVESTMENT GOALS 2016 CONTENT PIRAEUS BANK BULGARIA RELIABLE PARTNER IN THE PRESENT VOLATILE FINANCIAL WORLD FOREIGN

TREASURY PRODUCTS AND SERVICES MANAGING FINANCIAL RISKS, ENHANCING RETURNS, ACHIEVEING INVESTMENT GOALS 2016 CONTENT PIRAEUS BANK BULGARIA RELIABLE PARTNER IN THE PRESENT VOLATILE FINANCIAL WORLD FOREIGN

The UK Retail Bond Market H1 2011 Performance Update

1. Introduction The UK Retail Bond Market H1 2011 Performance Update Over the last 6 months, 7 transactions have been launched in the retail bond market in the UK, raising 540 million - with a further

1. Introduction The UK Retail Bond Market H1 2011 Performance Update Over the last 6 months, 7 transactions have been launched in the retail bond market in the UK, raising 540 million - with a further

RMB Internationalization & Hong Kong. Graham Coker Trade Director, Transaction Services UK & Ireland

RMB Internationalization & Hong Kong Graham Coker Trade Director, Transaction Services UK & Ireland RMB Internationalisation China s Market Reform Agenda RMB is called CNY onshore and CNH offshore. Hong

RMB Internationalization & Hong Kong Graham Coker Trade Director, Transaction Services UK & Ireland RMB Internationalisation China s Market Reform Agenda RMB is called CNY onshore and CNH offshore. Hong

Russian RUB FX spot & derivatives markets in 2014

Russian RUB FX spot & derivatives markets in 2014 Dmitry Piskulov, Ph.D. (econ.) Chairman of NFEA Board; Member of Monetary Policy Council of Association of regional banks Russia Moscow, 20 November 2014

Russian RUB FX spot & derivatives markets in 2014 Dmitry Piskulov, Ph.D. (econ.) Chairman of NFEA Board; Member of Monetary Policy Council of Association of regional banks Russia Moscow, 20 November 2014

RMB Internationalization and RMB Offshore Markets Development

RMB Internationalization and RMB Offshore Markets Development Dr. Qin Xiao Former Chairman, China Merchants Group and China Merchants Bank Council Member, Hong Kong Financial Services Development Council

RMB Internationalization and RMB Offshore Markets Development Dr. Qin Xiao Former Chairman, China Merchants Group and China Merchants Bank Council Member, Hong Kong Financial Services Development Council

Hot Topics in Financial Markets Lecture 1: The Libor Scandal

Hot Topics in Financial Markets Lecture 1: The Libor Scandal Spot and Forward Interest Rates Libor Libor-Dependent Financial Instruments The Scandal 2 Spot Interest Rates Bond Market The yield on a bond

Hot Topics in Financial Markets Lecture 1: The Libor Scandal Spot and Forward Interest Rates Libor Libor-Dependent Financial Instruments The Scandal 2 Spot Interest Rates Bond Market The yield on a bond

Trading the Yield Curve. Copyright 1999-2006 Investment Analytics

Trading the Yield Curve Copyright 1999-2006 Investment Analytics 1 Trading the Yield Curve Repos Riding the Curve Yield Spread Trades Coupon Rolls Yield Curve Steepeners & Flatteners Butterfly Trading

Trading the Yield Curve Copyright 1999-2006 Investment Analytics 1 Trading the Yield Curve Repos Riding the Curve Yield Spread Trades Coupon Rolls Yield Curve Steepeners & Flatteners Butterfly Trading

A Best Practice Oversight Approach for Securities Lending

A Best Practice Oversight Approach for Securities Lending At its core, securities lending is an investment overlay strategy. It s an investment product that complements existing investment strategies allowing

A Best Practice Oversight Approach for Securities Lending At its core, securities lending is an investment overlay strategy. It s an investment product that complements existing investment strategies allowing

Introduction to swaps

Introduction to swaps Steven C. Mann M.J. Neeley School of Business Texas Christian University incorporating ideas from Teaching interest rate and currency swaps" by Keith C. Brown (Texas-Austin) and Donald

Introduction to swaps Steven C. Mann M.J. Neeley School of Business Texas Christian University incorporating ideas from Teaching interest rate and currency swaps" by Keith C. Brown (Texas-Austin) and Donald

Monetary Policy of the Bank of Russia

Monetary Policy of the Bank of Russia Ksenia Yudaeva, Ph.D., First Deputy Governor Geneva, February 25 2 Inflation Targeting in Russia: Motivation & Challenges Motivation: Unanchored inflation Expectations

Monetary Policy of the Bank of Russia Ksenia Yudaeva, Ph.D., First Deputy Governor Geneva, February 25 2 Inflation Targeting in Russia: Motivation & Challenges Motivation: Unanchored inflation Expectations

Hedge Accounting (w.r.t.) Forward Contracts

Forward Contracts") Hedge Accounting (w.r.t.) Forward Contracts Agenda Introduction to Hedging Definitions Types of hedging relationships Fair value hedge Cash flow hedge Net investment hedge AS-11 V/s. AS-30 framework Hedging

Hedge Accounting (w.r.t.) Forward Contracts Agenda Introduction to Hedging Definitions Types of hedging relationships Fair value hedge Cash flow hedge Net investment hedge AS-11 V/s. AS-30 framework Hedging

Introduction. Taxes Supported. E tax Payment Service

Introduction To allow corporate clients to pay taxes (levied by both State Tax Bureau and Local Tax Bureau) electronically, HSBC Bank (China) Company Limited (HSBC China) has completed the system development

Introduction To allow corporate clients to pay taxes (levied by both State Tax Bureau and Local Tax Bureau) electronically, HSBC Bank (China) Company Limited (HSBC China) has completed the system development

GLOBAL MARKETS UPDATE

April 29, 2005 GLOBAL MARKETS UPDATE Global Business Opportunities in Financial Market Risk Management Union Bank of California Global Markets Published by UBOC Global Markets. This report has been prepared

April 29, 2005 GLOBAL MARKETS UPDATE Global Business Opportunities in Financial Market Risk Management Union Bank of California Global Markets Published by UBOC Global Markets. This report has been prepared

How do CFDs work? CFD trading is similar to traditional share dealing, with a few exceptions.

What is a CFD? A CFD is an agreement to exchange the difference between the opening and closing prices of the share, index or commodity between the time at which a contract is opened and the time at which

What is a CFD? A CFD is an agreement to exchange the difference between the opening and closing prices of the share, index or commodity between the time at which a contract is opened and the time at which

Application of Interest Rate Swaps in Indian Insurance Industry Amruth Krishnan Rohit Ajgaonkar Guide: G.LN.Sarma

Institute of Actuaries of India Application of Interest Rate Swaps in Indian Insurance Industry Amruth Krishnan Rohit Ajgaonkar Guide: G.LN.Sarma 21 st IFS Seminar Indian Actuarial Profession Serving the

Institute of Actuaries of India Application of Interest Rate Swaps in Indian Insurance Industry Amruth Krishnan Rohit Ajgaonkar Guide: G.LN.Sarma 21 st IFS Seminar Indian Actuarial Profession Serving the

The Money Market. Juan Barragan ECP January 2009

The Money Market Juan Barragan ECP January 2009 The Money Market Central Banks They drive the Money Market. They make funds available to commercial banks. They ensure liquidity. Funds available for a short

The Money Market Juan Barragan ECP January 2009 The Money Market Central Banks They drive the Money Market. They make funds available to commercial banks. They ensure liquidity. Funds available for a short

Fixed-Income Securities. Assignment

FIN 472 Professor Robert B.H. Hauswald Fixed-Income Securities Kogod School of Business, AU Assignment Please be reminded that you are expected to use contemporary computer software to solve the following

FIN 472 Professor Robert B.H. Hauswald Fixed-Income Securities Kogod School of Business, AU Assignment Please be reminded that you are expected to use contemporary computer software to solve the following

Managing FX Risk when trading with Australia. Mark Coulam Senior Manager, Treasury Solutions.

Managing FX Risk when trading with Australia Mark Coulam Senior Manager, Treasury Solutions. Reducing Volatility in your business What does your business have exposure to? Where does it occur? Quantify

Managing FX Risk when trading with Australia Mark Coulam Senior Manager, Treasury Solutions. Reducing Volatility in your business What does your business have exposure to? Where does it occur? Quantify

Impact of Treasury s OTC Derivatives Legislation on the Foreign Exchange Market. Corporations participate in the foreign exchange market to:

ISDA International Swaps and Derivatives Association, Inc. 360 Madison Avenue, 16th Floor New York, NY 10017 United States of America Telephone: 1 (212) 901-6000 Facsimile: 1 (212) 901-6001 email: [email protected]

ISDA International Swaps and Derivatives Association, Inc. 360 Madison Avenue, 16th Floor New York, NY 10017 United States of America Telephone: 1 (212) 901-6000 Facsimile: 1 (212) 901-6001 email: [email protected]

DERIVATIVES Presented by Sade Odunaiya Partner, Risk Management Alliance Consulting DERIVATIVES Introduction Forward Rate Agreements FRA Swaps Futures Options Summary INTRODUCTION Financial Market Participants

DERIVATIVES Presented by Sade Odunaiya Partner, Risk Management Alliance Consulting DERIVATIVES Introduction Forward Rate Agreements FRA Swaps Futures Options Summary INTRODUCTION Financial Market Participants

How a thoughtful FX strategy can give Fund Managers a competitive edge

How a thoughtful FX strategy can give Fund Managers a competitive edge Executive summary Each alternative investment fund takes a different approach to its investment strategy, but the ultimate goals are

How a thoughtful FX strategy can give Fund Managers a competitive edge Executive summary Each alternative investment fund takes a different approach to its investment strategy, but the ultimate goals are

Security Bank Treasury FX and Rates Hedging Division Gearing Up for External Competitiveness November 19, 2014. Treasury FXRH

Security Bank Treasury FX and Rates Hedging Division Gearing Up for External Competitiveness November 19, 2014 HEDGING, DERIVATIVES AND SPECULATION HEDGING Making an investment to reduce the risk of adverse

Security Bank Treasury FX and Rates Hedging Division Gearing Up for External Competitiveness November 19, 2014 HEDGING, DERIVATIVES AND SPECULATION HEDGING Making an investment to reduce the risk of adverse

ANZ ETFS PHYSICAL RENMINBI ETF. (ASX Code: ZCNH)

") ANZ ETFS PHYSICAL RENMINBI ETF (ASX Code: ZCNH) INVESTMENT BUILDING BLOCKS FOR A CHANGING WORLD Introducing a suite of innovative exchange traded funds (ETFs) designed for Australian investors by ANZ

ANZ ETFS PHYSICAL RENMINBI ETF (ASX Code: ZCNH) INVESTMENT BUILDING BLOCKS FOR A CHANGING WORLD Introducing a suite of innovative exchange traded funds (ETFs) designed for Australian investors by ANZ

Interest Rate Futures Pricing, Hedging, Trading Analysis and Applications

Interest Rate Futures Pricing, Hedging, Trading Analysis and Applications Vincent Chia Last Updated on 30 Nov 2010 [email protected] Agenda 1. Financial Instruments 2. Pricing Methodology

Interest Rate Futures Pricing, Hedging, Trading Analysis and Applications Vincent Chia Last Updated on 30 Nov 2010 [email protected] Agenda 1. Financial Instruments 2. Pricing Methodology

Learning Curve Interest Rate Futures Contracts Moorad Choudhry

Learning Curve Interest Rate Futures Contracts Moorad Choudhry YieldCurve.com 2004 Page 1 The market in short-term interest rate derivatives is a large and liquid one, and the instruments involved are

Learning Curve Interest Rate Futures Contracts Moorad Choudhry YieldCurve.com 2004 Page 1 The market in short-term interest rate derivatives is a large and liquid one, and the instruments involved are

CHAPTER 22: FUTURES MARKETS

CHAPTER 22: FUTURES MARKETS PROBLEM SETS 1. There is little hedging or speculative demand for cement futures, since cement prices are fairly stable and predictable. The trading activity necessary to support

CHAPTER 22: FUTURES MARKETS PROBLEM SETS 1. There is little hedging or speculative demand for cement futures, since cement prices are fairly stable and predictable. The trading activity necessary to support

SLVO Silver Shares Covered Call ETN

Filed pursuant to Rule 433 Registration Statement No. 333-180300-03 April 15, 2014 SLVO Silver Shares Covered Call ETN Credit Suisse AG, Investor Solutions April 2014 Executive Summary Credit Suisse Silver

Filed pursuant to Rule 433 Registration Statement No. 333-180300-03 April 15, 2014 SLVO Silver Shares Covered Call ETN Credit Suisse AG, Investor Solutions April 2014 Executive Summary Credit Suisse Silver

Introduction of Free Trade Zone RMB Bond Business

Introduction of Free Trade Zone RMB Bond Business Yidan WANG [email protected] April 2016 London Contents Company Overview Business Background Business Model Future Plan 第 四 章 A brief look into

Introduction of Free Trade Zone RMB Bond Business Yidan WANG [email protected] April 2016 London Contents Company Overview Business Background Business Model Future Plan 第 四 章 A brief look into

LOCKING IN TREASURY RATES WITH TREASURY LOCKS

LOCKING IN TREASURY RATES WITH TREASURY LOCKS Interest-rate sensitive financial decisions often involve a waiting period before they can be implemen-ted. This delay exposes institutions to the risk that

LOCKING IN TREASURY RATES WITH TREASURY LOCKS Interest-rate sensitive financial decisions often involve a waiting period before they can be implemen-ted. This delay exposes institutions to the risk that

Online Share Trading Currency Futures

Online Share Trading Currency Futures Wealth warning: Trading Currency Futures can offer significant returns BUT also subject you to significant losses if the market moves against your position. You may,

Online Share Trading Currency Futures Wealth warning: Trading Currency Futures can offer significant returns BUT also subject you to significant losses if the market moves against your position. You may,

The RMB market in France Becoming a global currency

The RMB market in France Becoming a global currency 元 (Renminbi): BECOMING A GLOBAL CURRENCY Over the last few years, the Renminbi (RMB) internationalization has been growing steadily. Measures have been

The RMB market in France Becoming a global currency 元 (Renminbi): BECOMING A GLOBAL CURRENCY Over the last few years, the Renminbi (RMB) internationalization has been growing steadily. Measures have been

Introduction to Derivative Instruments Part 1 Link n Learn

Introduction to Derivative Instruments Part 1 Link n Learn June 2014 Webinar Participants Elaine Canty Manager Financial Advisory Deloitte & Touche Ireland [email protected] +353 1 417 2991 Christopher

Introduction to Derivative Instruments Part 1 Link n Learn June 2014 Webinar Participants Elaine Canty Manager Financial Advisory Deloitte & Touche Ireland [email protected] +353 1 417 2991 Christopher

The Central Bank from the Viewpoint of Law and Economics

The Central Bank from the Viewpoint of Law and Economics Handout for Special Lecture, Financial Law at the Faculty of Law, the University of Tokyo Masaaki Shirakawa Governor of the Bank of Japan October

The Central Bank from the Viewpoint of Law and Economics Handout for Special Lecture, Financial Law at the Faculty of Law, the University of Tokyo Masaaki Shirakawa Governor of the Bank of Japan October

Interest Rate and Currency Swaps

Interest Rate and Currency Swaps Eiteman et al., Chapter 14 Winter 2004 Bond Basics Consider the following: Zero-Coupon Zero-Coupon One-Year Implied Maturity Bond Yield Bond Price Forward Rate t r 0 (0,t)

Interest Rate and Currency Swaps Eiteman et al., Chapter 14 Winter 2004 Bond Basics Consider the following: Zero-Coupon Zero-Coupon One-Year Implied Maturity Bond Yield Bond Price Forward Rate t r 0 (0,t)

A strong year for retail bonds

A strong year for retail bonds The Orderbook for Retail Bonds (ORB) opened 1 February 2010, with the aim of promoting both a transparent secondary market in bonds for retail investors as well as developing

A strong year for retail bonds The Orderbook for Retail Bonds (ORB) opened 1 February 2010, with the aim of promoting both a transparent secondary market in bonds for retail investors as well as developing

OTC Derivatives: Benefits to U.S. Companies

OTC Derivatives: Benefits to U.S. Companies International Swaps and Derivatives Association May 2009 1 What are derivatives? Derivatives are financial instruments that: Transfer risk from one party to

OTC Derivatives: Benefits to U.S. Companies International Swaps and Derivatives Association May 2009 1 What are derivatives? Derivatives are financial instruments that: Transfer risk from one party to

Treasury Floating Rate Notes

Global Banking and Markets Treasury Floating Rate Notes DATE: April 2012 Recommendation summary The USD 7trn money market should support significant FRN issuance from the Treasury. This would diversify

Global Banking and Markets Treasury Floating Rate Notes DATE: April 2012 Recommendation summary The USD 7trn money market should support significant FRN issuance from the Treasury. This would diversify

Cash Flow Hedge Basics, Interest Rate Swap Valuations & Foreign Currency Topics. Presented By: Ruth Hardie & Jim Shepard

Cash Flow Hedge Basics, Interest Rate Swap Valuations & Foreign Currency Topics Presented By: Ruth Hardie & Jim Shepard Agenda CNH vs. CNY: ASC 830 & ASC 815 Implications Valuing an Interest Rate Swap

Cash Flow Hedge Basics, Interest Rate Swap Valuations & Foreign Currency Topics Presented By: Ruth Hardie & Jim Shepard Agenda CNH vs. CNY: ASC 830 & ASC 815 Implications Valuing an Interest Rate Swap

Chapter 16: Financial Risk Management

Chapter 16: Financial Risk Management Introduction Overview of Financial Risk Management in Treasury Interest Rate Risk Foreign Exchange (FX) Risk Commodity Price Risk Managing Financial Risk The Benefits

Chapter 16: Financial Risk Management Introduction Overview of Financial Risk Management in Treasury Interest Rate Risk Foreign Exchange (FX) Risk Commodity Price Risk Managing Financial Risk The Benefits

How To Invest In Stocks And Bonds

Review for Exam 1 Instructions: Please read carefully The exam will have 21 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation

Review for Exam 1 Instructions: Please read carefully The exam will have 21 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation

Collateral consistent derivatives pricing

Collateral consistent derivatives pricing FRIC Practitioner Seminar, CBS Martin D. Linderstrøm, [email protected] Counterparty Credit & Funding Risk Agenda The intuition behind collateral consistent

Collateral consistent derivatives pricing FRIC Practitioner Seminar, CBS Martin D. Linderstrøm, [email protected] Counterparty Credit & Funding Risk Agenda The intuition behind collateral consistent

Note 8: Derivative Instruments

Note 8: Derivative Instruments Derivative instruments are financial contracts that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity prices

Note 8: Derivative Instruments Derivative instruments are financial contracts that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity prices

VALUATION OF PLAIN VANILLA INTEREST RATES SWAPS

Graduate School of Business Administration University of Virginia VALUATION OF PLAIN VANILLA INTEREST RATES SWAPS Interest-rate swaps have grown tremendously over the last 10 years. With this development,

Graduate School of Business Administration University of Virginia VALUATION OF PLAIN VANILLA INTEREST RATES SWAPS Interest-rate swaps have grown tremendously over the last 10 years. With this development,

The U.S. Dollar Rally: Understanding its impact on your business

David Coomer, CPA [email protected] 937.226.0070 Rick Jones [email protected] 513.386.7447 The U.S. Dollar Rally: Understanding its impact on your business Agenda Introduction and Overview The Foreign

David Coomer, CPA [email protected] 937.226.0070 Rick Jones [email protected] 513.386.7447 The U.S. Dollar Rally: Understanding its impact on your business Agenda Introduction and Overview The Foreign

Commercial paper collateralized by a pool of loans, leases, receivables, or structured credit products. Asset-backed commercial paper (ABCP)

") GLOSSARY Asset-backed commercial paper (ABCP) Asset-backed security (ABS) Asset-backed securities index (ABX) Basel II Call (put) option Carry trade Collateralized debt obligation (CDO) Collateralized

GLOSSARY Asset-backed commercial paper (ABCP) Asset-backed security (ABS) Asset-backed securities index (ABX) Basel II Call (put) option Carry trade Collateralized debt obligation (CDO) Collateralized

The Chinese corporate credit bond market. Broad prospects for development

The Chinese corporate credit bond market Broad prospects for development Dear Mr. Martin Scheck, Mr. Spencer Lake, Distinguished Guests, Ladies and Gentlemen, Good Morning! I am very pleased to attend

The Chinese corporate credit bond market Broad prospects for development Dear Mr. Martin Scheck, Mr. Spencer Lake, Distinguished Guests, Ladies and Gentlemen, Good Morning! I am very pleased to attend

FX Options. Dan Juhl Larsen FX Options trader at Saxo Bank. Moscow 19 Marts 2014

FX Options Dan Juhl Larsen FX Options trader at Saxo Bank Moscow 19 Marts 2014 4 June 2013 Disclaimer None of the information contained herein constitutes an offer (or solicitation of an offer) to buy

FX Options Dan Juhl Larsen FX Options trader at Saxo Bank Moscow 19 Marts 2014 4 June 2013 Disclaimer None of the information contained herein constitutes an offer (or solicitation of an offer) to buy