Can Tail Risk Be Hedged?

|

|

|

- Marjorie Russell

- 8 years ago

- Views:

Transcription

1 Can Tail Risk Be Hedged? Summary of Empirical Results Lisa R. Goldberg Ola Mahmoud (Marie Curie Fellow) 1 Peter Shepard Kurt Winkelmann August Ola Mahmoud was a Marie Curie Fellows at MSCI. The research leading to these results has received funding from the European Community s Seventh Framework Programme FP7-PEOPLE-ITN-2008 under grant agreement number PITN-GA (project name: RISK). The funding is gratefully acknowledged.

2 Contractual Tail Risk Hedging Strategies The cost of insurance We examine the cost of passive tail risk hedging via zero-cost collars. These are contractual option strategies limiting both the potential downside and upside to a specific range. Collars are created by purchasing an out-of-the-money put, aimed at capping losses, together with selling a call to finance the purchase of the put. We backtest the zero-cost collar strategy using the S&P 500 as the underlying. Market prices of 3- month-to-maturity call and put options on the S&P 500 going back to 2003 are matched up into five zero-cost put/call pairs, ranging from deep out-of-the-money ( widest collar) to very near the money ( narrowest collar). Figure 1 shows the performance of each of these collar strategies compared to the underlying. Transaction costs are taken into account by buying at the bid and selling at the ask price. Collars as downside protection strategies come at the cost of potential upside, with their success on limiting extreme losses coming into effect only during times of extreme market losses. As is well appreciated, when limiting both losses and gains to values that are close to the center of the returns distribution, the distribution tails at either ends narrow down considerably, resulting in stable but minimal cumulative performance ( narrowest collar of Figure 1). On the contrary, cutting out only the most extreme losses and gains via a very wide collar yields a typical high risk/high return performance comparable to that of the market itself ( widest collar of Figure 1). To obtain a clearer picture of how much of the potential upside is sacrificed for the sake of insurance, we look at the ratio of downside to upside return thresholds (Figure 2). Clearly, all of the zero-cost collars are very expensive downside protection instruments, with their downside generally exceeding the upside. We also see from Figure 2 that the wider the collar, the larger the ratio of downside to upside. Figure 1: Performance of zero-cost collar hedging strategies using 3-months-to-maturity put and call options on the S&P 500. Figure 2: Ratio of downside to upside returns of 4 of the zero-cost collar strategies on the S&P 500 of Figure 1. 2 of 12

3 Tail risk hedging and asset allocation We investigate the impact of hedging tail risk on long-term asset allocation. Our benchmark portfolio consists of 65% allocated in global equity (represented by the MSCI All Country World Index) and 35% in fixed income (represented by a CRSP Fama portfolio of bonds for maturities between 60 and 120 months). In the absence of option price data, we synthetically construct collars as fixed-return cutoffs. Our hypothetical symmetric collar caps total portfolio returns at 5%, and the asymmetric collar caps returns at 10% and 5%. To incorporate the effect of transaction costs, we subtract a constant from insured portfolios. Table 1 summarizes the main risk and return characteristics of some of the portfolio/insurance combinations we consider. Evidently, the market exhibits higher return and volatility and more negative skewness compared to its fixed income counterpart. In our benchmark 65/35 portfolio, some of these risks are offset. The effect of adding protection to the overall returns of this benchmark via synthetic collars is presented as portfolios 2a and 2b. In the table, 1-month (resp. 1-year) skewness and kurtosis refer to the skewness and kurtosis at the specified return horizon (i.e. monthly and yearly returns). Generally, the symmetric collar displays better return distribution qualities: the Sharpe ratio is slightly higher, and so is the overall 1-month and 1-year skew. On the other hand, the kurtosis is reduced, indicating that both insurance strategies indeed succeeded at slimming down the tails. The overall returns of both collar strategies are slightly lower than those of the benchmark. As it is no surprise that insurance strategies come at a cost, one may ask what asset allocation an investor could have chosen to achieve the same performance of an insured portfolio, and what the corresponding impact on its risk would have been. We see that an equal-weighted allocation (portfolio 3 in Table 1) yields a return and volatility comparable to those of the symmetric collar strategy. Note, however, that both the Sharpe ratio and the overall skewness have enhanced, indicating that changes in asset allocations may effectively lead to an implicit, non-contractual type of insurance. Portfolio Return Std Sharpe 1M Skew 1Y Skew 1M Kurtosis 1Y Kurtosis MSCI All World CRSP m Bonds : 65/ a: 65/35 w/(-10%,+5%) collar b: 65/35 w/(-5%,+5%) collar : 50/ a: Short (-10%,+5%) insurance b: 65/35, short (-10%,+5%) insurance Table 1: Summary statistics With the view of an economic equilibrium in mind, we investigate the effect of providing insurance. To this end, we study the return and risk attributes of portfolios which sell the collar hedging strategies. Purely selling the asymmetric collar (portfolio 4a) results in minimal returns and volatility which can be seen as a steady but limited source of income, similar to what a traditional long-term investor might seek. The safety of such a strategy is further reflected in its skew, which is significantly positive. It may 2 of 12

4 therefore be intriguing to consider our initial 65/35 asset allocation and sell rather than buy protection on it. Curiously, when comparing portfolios 4b and 2a of Table 1, we observe a better Sharpe ratio and a positive skewness when adding a short collar-hedge position. This outperformance naturally comes at the cost of larger excess kurtosis, as the extreme gains and losses taken over from the insurance buying counterpart amplify the size of the tails of the insurance-selling investment portfolio. Volatility-based insurance Volatility possesses certain characteristics which make it an attractive tradable asset. Just like interest rates, it appears to be mean reverting, hence tends to drop after periods of high volatility and rise after calm periods. It furthermore tends to increase during times of uncertainty. This seemingly regime dependent behavior allows investors to speculate on future levels of volatility. On the other hand, investors with portfolios that have natural exposure to volatility may want to hedge it away. A more intriguing use of volatility viewed as an asset class is portfolio diversification. The underlying assumption is the existence of significant negative correlation between the market returns and their volatility, especially during turbulent times; an empirical observation first pointed out by Black [] and since referred to as the leverage effect (see Figure 3). From this point of view, being long volatility can be a beneficial hedge against the tail risk of a long-only equity portfolio. Until recently, options were the only products giving exposure to volatility. The common strategy is to hedge the exposure of the option to the underlying in order to isolate the exposure to volatility. One of the main disadvantages to this approach is the constant need to rehedge large market moves will cause the option to be a directional bet on the underlying. An option s sensitivity to volatility will diminish when the underlying moves away from the strike price. Over the past few years, variance and volatility based investment products have emerged as alternative hedging vehicles, examples of which are variance swaps and futures on volatility indices. These are meant to provide pure exposure to volatility or variance, independent of the other risks that would accompany an option-based strategy. According to the Chicago Board Options Exchange (CBOE) [], trading of volatility has roughly doubled over the past few years. The volume of trading one such instrument, namely futures on the VIX, has almost grown to its ten-fold between 2007 and 2011, as illustrated in Figure 4. Figure 3: The Leverage Effect Figure 4: Total volume of VIX futures traded ( ) 3 of 12

5 In the context of Black s leverage effect, we next investigate the premia of trading variance for the purpose of insurance. Passive option-based insurance strategies such as zero-cost collars are meant to provide explicit protection against extreme events that affect the tail. Volatility-based strategies can implicitly provide the same kind of insurance against extreme down movements in the market, by explicitly hedging volatility. The variance risk premium Implied volatilities are a forward looking measure of the market s perception of its own variability. These are normally more reactive to anticipated changes and tend to differ from what has occurred recently. Indeed, traders use implied volatilities (of the most actively traded options) to monitor the market s opinion about the expected volatility level. Position-taking in pure volatility is therefore largely based on implied volatility forecasts. Indices of implied volatilities, such as the VIX, are meant to provide timely reflections of future market variability. They are calculated as a weighted average of option implied volatilities for various strikes and, in the context of the Black-Scholes framework, can be interpreted as the risk neutral estimate of future volatility [Derman]. These are generally higher than realized volatility levels. One aspect of this is the embedded market premium on out-of-the-money options used for insurance. Implied volatilities therefore contain important information regarding investors demand for portfolio insurance. The volatility (variance) risk premium refers precisely to this difference between realized and implied volatility (variance). It reflects the payoff an investor would get by betting on future volatility levels, for instance by purchasing variance swaps. Figure 5a illustrates the variance risk premium over time for the S&P 500. The estimates are obtained by subtracting, at each point in time, the observed VIX level from the 30-day forward looking realized one-day volatility. The distribution of the payoffs from variance swaps is displayed in Figure 5b. We see that the payoff is generally negative, and exhibits large positive jumps during periods of turbulence. The negative variance risk premium reflects intrinsic investor behaviours and expectations when it comes to buying and selling insurance. The highly negative premium combined with its strong positive skewness suggests that investors who buy insurance are willing to endure losses on average, in the hope of being rewarded when realized market volatility increases. The other transaction party, the insurance seller, is thereby able to generate a regular and stable stream of positive income, but has the occasional exposure to extreme losses. (relate to long and short horizon investment strategies) Figure 5a: The variance risk premium Figure 5b: Variance swap return distribution 2 of 12

6 The cost of hedging volatility Volatility and variance based strategies aim at exploiting information about the expected payoff embedded in variance risk premia. By entering a variance swap for instance, an investor bets on the future variance risk premium from the perspective of buying or selling downside protection. A VIX futures contract offers an alternative yet equivalent opportunity to gain the same exposure to variance as variance swaps. We test an insurance strategy on the S&P 500 which is long a futures contract on the VIX. We use a history of daily market prices for VIX futures for various expiries, with our focus on two maturities (1 month and 1 year). A contract is assumed to be settled daily and held until its expiry, at which point a new contract of the given maturity is purchased. Figure 6 shows how this strategy performs relative to the S&P 500. It displays the 1-month- and 1-yearto-expiration VIX futures strategies with and without incorporating transaction costs. Costs are accounted for by buying at the bid price. When incorporating costs, we see that none of the insurance strategies outperforms the market, except for the few months during the peak of the financial crisis. Comparing the short and long horizon strategies, the 1-year horizon clearly outperforms its shorter horizon counterpart (except for a steep dip in early 2009, which is quickly recovered from). However, the summary statistics of Table 2 show that the 1-month strategy possesses superior risk characteristics in terms of all its other moments (smaller volatility and kurtosis, and larger positive skewness). In fact, the market itself beats the 1-year insured portfolio not only in its performance, but also in its other moments. The dotted lines in Figure 6 show how both strategies would perform if we were to neglect transaction costs. The effect of the costs is most visible in the cumulative performances, which are enhanced significantly. On the other hand, the risk attributes are comparable to those of the corresponding strategies that account for the cost. Figure 6: Hedging the S&P 500 with VIX futures. Portfolio Volatility 1D Skewness 1M Skewness 1D Kurtosis 1M Kurtosis S&P S&P + 1M VIX Futures (with cost) S&P + 1M VIX Futures (no cost) S&P + 1Y VIX Futures (with cost) S&P + 1Y VIX Futures (no cost) Table 2: Summary statistics for the portfolios of Figure 6.

7 On the Importance of Higher Moments Insights into the skew It is generally acknowledged that investors dislike highly negative skewness and large excess kurtosis in their portfolios. At a short-term return horizon, the market usually exhibits such higher-moment characteristics, indicating that short-term investors may either expect higher compensation for these higher-moment risks, or that they may seek to hedge against the skew and kurtosis. From the Central Limit Theorem, we know that aggregating independent and identically distributed (i.i.d.) daily returns to obtain longer horizon returns would approach normality the longer the horizon. Both skewness and excess kurtosis would therefore be expected to converge to their Gaussian values of zero when the return horizon increases. This may point towards a less pressing need for long-horizon investors to account for higher moments in their investment and risk management. To understand these effects, we study high moments of the market at increasing horizons. Figure 1 displays skewness and kurtosis of logarithmic returns to the S&P 500 as a function of return horizon, ranging from daily to yearly returns. Our empirical setting uses a sufficiently large data set ( ) for the values of the skew and particularly the kurtosis to be meaningful. For comparison, we plot the same for simulated time series of returns that are assumed to be log-normal and i.i.d. These display the expected decay behavior: for 1 and 1 the 1-day skewness and kurtosis, respectively, daily i.i.d. returns at an -day horizon would have 1 / and / skewness and kurtosis, respectively. Observe that the kurtosis of the market does indeed fall off at longer horizons, though with some noise and at a decay rate that is naturally slower than its i.i.d. counterpart. Market skewness, however, does not converge to normality with longer horizons. In fact, it persists and roughly fluctuates around a value of 0.9 no matter what return horizon is taken. Figure 7: Skewness (left) and kurtosis (right) of logarithmic returns to the S&P 500 (January 1950 April 2011) as a function of return horizon ranging from 1-day to 1-year returns. How can an investor use these insights to decide on tail risk hedging strategies? On the one hand, the decaying of the kurtosis confirms that the long horizon investor is less affected by extreme events and should therefore be selling rather than buying insurance. On the other hand, the persistence of the skew implies that a long-horizon investor needs to worry about the skew as much as the short-horizon investor. Therefore, one conclusion to be drawn for the long-horizon investor is to only sell very deep insurance to short-term investors the higher moment risk which does not affect the long-term investor is kurtosis; i.e. only events that occur far in the tail do not matter in the long horizon. However, skewness matters. Selling any other level of insurance (protection against not so severe events) can lead

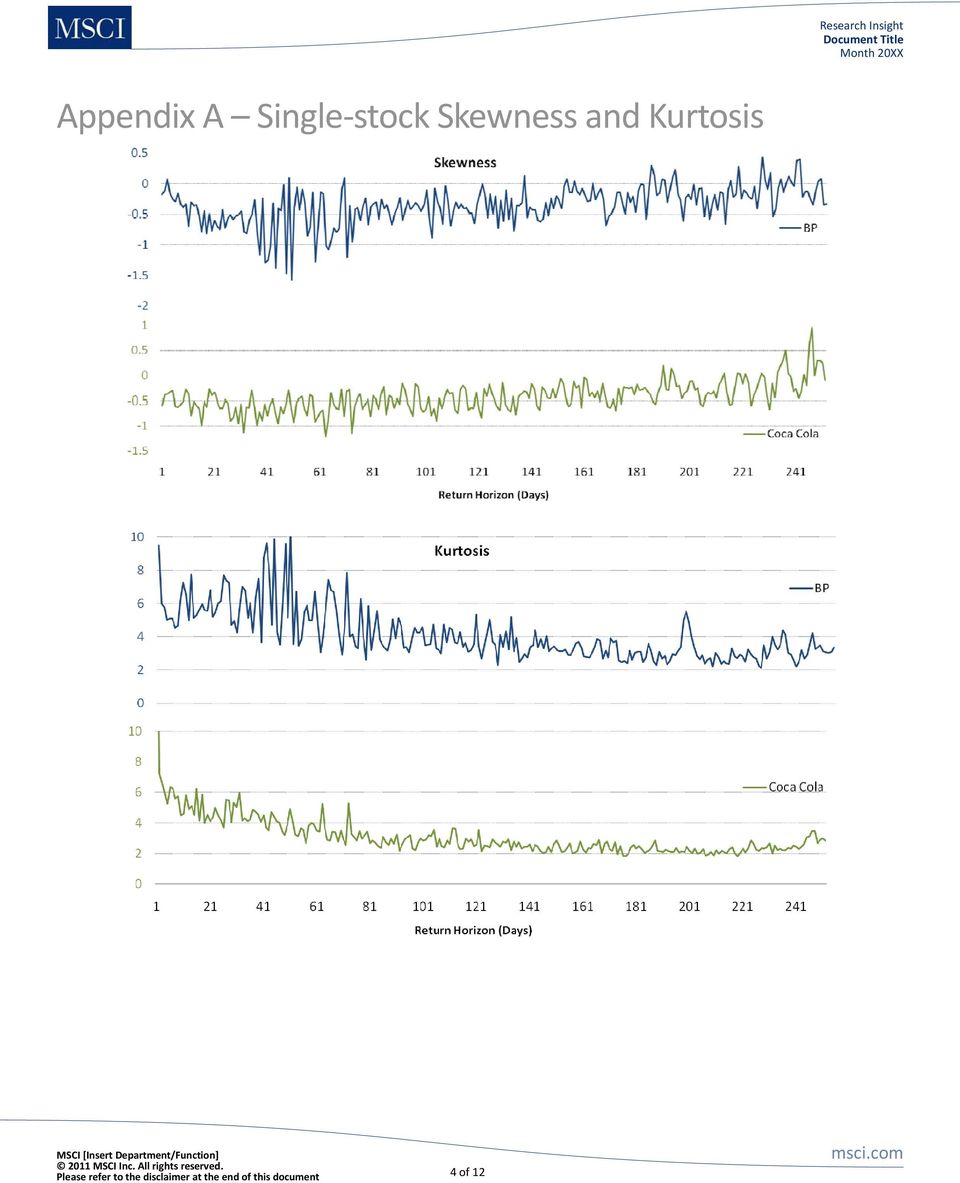

8 to significant losses, since one is just as much affected by the overall negative asymmetry as the shorthorizon investor. The persistence of the skew is a phenomenon mainly observable in markets or equity indices; the picture is quite different when looking at single name stocks, and therefore care needs to be taken as to the underlying one seeks insurance for. Appendix A replicates the graphs of Figure 1 for two singlenames, namely Coca Cola and BP. Higher moments & asset allocation strategies The passive/contractual insurance strategies we considered so far did not account for higher moments, but the resulting skew and kurtosis statistics of Table (?) suggest that an investor may need to explore other dimensions that are complementary to volatility. Consider again the simple setting of a two-asset portfolio fixed income and equity. We know that increasing the fixed income component decreases both volatility and expected return, and a straightforward mean-variance optimization will yield the optimal such combination according to a given risk appetite. A standard such combination is a 65/35 portfolio. If, as investors holding such an equity-dominant portfolio, we are now only interested in its skewness and kurtosis, we may ask ourselves: how much fixed income should we add to reduce higher moment risk? With the US market as the allocation universe (represented by MSCI USA and the Merrill Treasury Index), Figure 2 shows the volatility, skewness and kurtosis of portfolios representing a range of allocations to each asset, ranging from 100% in equity (far left) to 100% in fixed income (far right) at three return horizons. Note that the risks associated with skewness and kurtosis decrease significantly only when one goes beyond a 50% allocation to fixed income, and therefore, in this very simplified setting, one may conclude that a 35/65 allocation is preferred over a 65/35 allocation from the point of view of higher moment risks.

9 Figure 8: Volatility, skewness and kurtosis of an equity/fi portfolio as a function of allocation to fixed income Active higher-moment strategies A general comment on active hedging. First, active compared to passive makes more sense, as allocations should be dynamic and based on current market regimes. Some prerequisites: (i) good judgment of short-term future market conditions, either through subjective opinion or through statistical methods; (ii) feasibility of underlying methodology; (iii) limited costs. Traditional portfolio theory does not account for the impact of higher moments on decision making. Under the Capital Asset Pricing Model (CAPM) particularly, investors are mean-variance optimizers and do not have any preference regarding the skewness and kurtosis of their portfolios. Different asset-pricing models that account for higher moments have been developed as an attempt to extend the traditional CAPM. The intertemporal capital asset pricing model (ICAPM) is one such alternative proposed by Merton [cite], under which the state variables reflect changes in the distribution of future returns. In this factor model, one may take market volatility, skewness and kurtosis as state variables reflecting changes in investment opportunity set [Christofferson]. The equilibrium prices of risky assets are then determined by the conditional covariances between asset returns and changes in state variables. Note that investors remain mean-variance optimizers under the ICAPM, and higher moments affect their decision only indirectly at the level of their relationship with asset returns. A conceptually simpler approach is given by the four-moment CAPM [cite]. This model is based on the hypothesis that investors care about the skewness and kurtosis of their portfolios as much as they care about their returns and variance. Under this setting, they are mean-variance-skewness-kurtosis optimizers, and their utility function is derived by expanding it to the fourth instead of the second order. The main difficulty in higher moment optimization lies in the third- and fourth-order terms appearing in the objective function, making the optimization no longer convex [cite]. Moreover, the dimensionality of

10 the problem increases, making estimation of parameters such as co-skewness and co-kurtosis more challenging (possible third challenge: lack of good enough risk model?). Many approximations to optimization routines that incorporate higher moments have been investigated, most recently by Deutsche Bank [cite], who developed a so-called polynomial goal programming algorithm which aims at balancing the conflicting goals of minimizing variance and kurtosis and maximizing return and skewness. We study a simple, yet mathematically stable, alternative to accounting for higher moments in portfolio optimization, namely by replacing skewness and kurtosis with the convex measure of shortfall [Minimizing Shortfall]. Depending on the confidence level under consideration, expected shortfall can be regarded as a descriptive statistic of a portfolio s distribution. For example, by considering a 95% shortfall confidence level, we are measuring the fatness of the loss tail, whereas a 60% shortfall describes overall asymmetry [to be elaborated on]. Minimizing expected shortfall would thereby result in minimizing the risk associated with kurtosis and skewness, respectively. This framework would also enable a generalization of the mean-variance objective function to include all four moments by simply adding additional shortfall terms at the desired confidence levels. Portfolio Allocation Volatility Sharpe Ratio Skewness Excess Kurtosis 95% Shortfall MSCI USA % % Merrill US Treasury % % Minimum Variance % % Minimum Skewness % % Minimum Kurtosis % % 65/ % % 50/ % % Risk Parity % % Table 3: Summary statistics for portfolios of various asset allocation strategies. Table 3 summarizes the statistics of portfolios containing equity (MSCI USA) and fixed income (Merrill US Treasury), with the allocation to each decided by an optimization routine. For comparison, we also show what a typical 65/35 portfolio looks like, together with an equal-weighted allocation, and a portfolio under a risk parity strategy. The allocations to the minimum risk portfolios resemble that of a risk parity strategy, with the majority assigned to the safe fixed income asset. Their return and volatility attributes are all very similar. Note, however, that each minimum risk strategy did indeed minimize the risk under consideration. Most notable is the kurtosis optimization, which did indeed minimize tail risk in terms of kurtosis and 95% shortfall. [remark on: one risk minimized, at the expense of others increasing?] The allocations we obtain from the various optimizations lead us to consider that, just as is common with a risk parity strategy, a minimum-variance-kurtosis/maximum-return-skewness portfolio may be combined with leverage to yield maximum returns but minimum high-moment risks. Of course, the main concern with such a strategy is the extent to which taking on leverage is allowed.

11 Appendix A Single-stock Skewness and Kurtosis

12 Client Service Information is Available 24 Hours a Day clientservice@ Americas Europe, Middle East & Africa Asia Pacific Americas Atlanta Boston Chicago Montreal Monterrey New York San Francisco Sao Paulo Stamford Toronto (toll free) Amsterdam Cape Town Frankfurt Geneva London Madrid Milan Paris Zurich (toll free) China North China South Hong Kong Seoul Singapore Sydney Tokyo (toll free) (toll free) (toll free) Notice and Disclaimer This document and all of the information contained in it, including without limitation all text, data, graphs, charts (collectively, the Information ) is the property of MSCl Inc. or its subsidiaries (collectively, MSCI ), or MSCI s licensors, direct or indirect suppliers or any third party involved in making or compiling any Information (collectively, with MSCI, the Information Providers ) and is provided for informational purposes only. The Information may not be reproduced or redisseminated in whole or in part without prior written permission from MSCI. The Information may not be used to create derivative works or to verify or correct other data or information. For example (but without limitation), the Information many not be used to create indices, databases, risk models, analytics, software, or in connection with the issuing, offering, sponsoring, managing or marketing of any securities, portfolios, financial products or other investment vehicles utilizing or based on, linked to, tracking or otherwise derived from the Information or any other MSCI data, information, products or services. The user of the Information assumes the entire risk of any use it may make or permit to be made of the Information. NONE OF THE INFORMATION PROVIDERS MAKES ANY EXPRESS OR IMPLIED WARRANTIES OR REPRESENTATIONS WITH RESPECT TO THE INFORMATION (OR THE RESULTS TO BE OBTAINED BY THE USE THEREOF), AND TO THE MAXIMUM EXTENT PERMITTED BY APPLICABLE LAW, EACH INFORMATION PROVIDER EXPRESSLY DISCLAIMS ALL IMPLIED WARRANTIES (INCLUDING, WITHOUT LIMITATION, ANY IMPLIED WARRANTIES OF ORIGINALITY, ACCURACY, TIMELINESS, NON-INFRINGEMENT, COMPLETENESS, MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE) WITH RESPECT TO ANY OF THE INFORMATION. Without limiting any of the foregoing and to the maximum extent permitted by applicable law, in no event shall any Information Provider have any liability regarding any of the Information for any direct, indirect, special, punitive, consequential (including lost profits) or any other damages even if notified of the possibility of such damages. The foregoing shall not exclude or limit any liability that may not by applicable law be excluded or limited, including without limitation (as applicable), any liability for death or personal injury to the extent that such injury results from the negligence or wilful default of itself, its servants, agents or sub-contractors. Information containing any historical information, data or analysis should not be taken as an indication or guarantee of any future performance, analysis, forecast or prediction. Past performance does not guarantee future results. None of the Information constitutes an offer to sell (or a solicitation of an offer to buy), any security, financial product or other investment vehicle or any trading strategy. MSCI s indirect wholly-owned subsidiary Institutional Shareholder Services, Inc. ( ISS ) is a Registered Investment Adviser under the Investment Advisers Act of Except with respect to any applicable products or services from ISS (including applicable products or services from MSCI ESG Research Information, which are provided by ISS), none of MSCI s products or services recommends, endorses, approves or otherwise expresses any opinion regarding any issuer, securities, financial products or instruments or trading strategies and none of MSCI s products or services is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. The MSCI ESG Indices use ratings and other data, analysis and information from MSCI ESG Research. MSCI ESG Research is produced ISS or its subsidiaries. Issuers mentioned or included in any MSCI ESG Research materials may be a client of MSCI, ISS, or another MSCI subsidiary, or the parent of, or affiliated with, a client of MSCI, ISS, or another MSCI subsidiary, including ISS Corporate Services, Inc., which provides tools and services to issuers. MSCI ESG Research materials, including materials utilized in any MSCI ESG Indices or other products, have not been submitted to, nor received approval from, the United States Securities and Exchange Commission or any other regulatory body. Any use of or access to products, services or information of MSCI requires a license from MSCI. MSCI, Barra, RiskMetrics, ISS, CFRA, FEA, and other MSCI brands and product names are the trademarks, service marks, or registered trademarks of MSCI or its subsidiaries in the United States and other jurisdictions. The Global Industry Classification Standard (GICS) was developed by and is the exclusive property of MSCI and Standard & Poor s. Global Industry Classification Standard (GICS) is a service mark of MSCI and Standard & Poor s. About MSCI MSCI Inc. is a leading provider of investment decision support tools to investors globally, including asset managers, banks, hedge funds and pension funds. MSCI products and services include indices, portfolio risk and performance analytics, and governance tools. The company s flagship product offerings are: the MSCI indices which include over 148,000 daily indices covering more than 70 countries; Barra portfolio risk and performance analytics covering global equity and fixed income markets; RiskMetrics market and credit risk analytics; ISS governance research and outsourced proxy voting and reporting services; FEA valuation models and risk management software for the energy and commodities markets; and CFRA forensic accounting risk research, legal/regulatory risk assessment, and due-diligence. MSCI is headquartered in New York, with research and commercial offices around the world.

+ 41.44.220.9300 China North China South Hong Kong Seoul Singapore Sydney Tokyo 10800.852.1032 (toll free) 10800.152.1032 (toll free) + 852.2844.")

Market Insight: Analyzing Hedges for Liability-Driven Investors

Market Insight: Lisa R. Goldberg and Sang-Hoon Kim Abstract: Managing surplus risk enables pension plans and endowments to align their asset allocations with their future obligations. BarraOne s Correlation

Market Insight: Lisa R. Goldberg and Sang-Hoon Kim Abstract: Managing surplus risk enables pension plans and endowments to align their asset allocations with their future obligations. BarraOne s Correlation

MSCI Global Minimum Volatility Indices Methodology

MSCI Global Minimum Volatility Indices Methodology Table of Contents Section 1: Introduction... 3 Section 2: Characteristics of MSCI Minimum Volatility Indices... 3 Section 3: Constructing the MSCI Minimum

MSCI Global Minimum Volatility Indices Methodology Table of Contents Section 1: Introduction... 3 Section 2: Characteristics of MSCI Minimum Volatility Indices... 3 Section 3: Constructing the MSCI Minimum

Updated Stress Testing Features in RiskMetrics RiskManager

Updated Stress Testing Features in RiskMetrics RiskManager Predictive Stress Test for the 2009 Equity Market Rally. Audrey Costabile Christopher Finger Katarzyna Siudek 1 (Marie Curie Fellow) December

Updated Stress Testing Features in RiskMetrics RiskManager Predictive Stress Test for the 2009 Equity Market Rally. Audrey Costabile Christopher Finger Katarzyna Siudek 1 (Marie Curie Fellow) December

MSCI Quality Indices Methodology

Methodology Contents Contents... 2 Section 1: Introduction... 3 Section 2: Index Construction Methodology... 4 Section 2.1: Applicable Universe... 4 Section 2.2: Determination of Quality Score... 4 Section

Methodology Contents Contents... 2 Section 1: Introduction... 3 Section 2: Index Construction Methodology... 4 Section 2.1: Applicable Universe... 4 Section 2.2: Determination of Quality Score... 4 Section

Global Investing: The Importance of Currency Returns and Currency Hedging

Global Investing: The Importance of Currency Returns and Currency Hedging There is a continuing trend for investors to reduce their home bias in equity allocation and increase the allocation to international

Global Investing: The Importance of Currency Returns and Currency Hedging There is a continuing trend for investors to reduce their home bias in equity allocation and increase the allocation to international

MSCI CHINA AND USA INTERNET TOP 50 EQUAL WEIGHTED INDEX

INDEX METHODOLOGY MSCI CHINA AND USA INTERNET TOP 50 EQUAL WEIGHTED INDEX September 2014 SEPTEMBER 2014 CONTENTS 1 Introduction... 3 2 Constructing the MSCI China and USA Internet Top 50 Equal Weighted

INDEX METHODOLOGY MSCI CHINA AND USA INTERNET TOP 50 EQUAL WEIGHTED INDEX September 2014 SEPTEMBER 2014 CONTENTS 1 Introduction... 3 2 Constructing the MSCI China and USA Internet Top 50 Equal Weighted

Introducing the Loan Pool Specific Factor in CreditManager

Technical Note Introducing the Loan Pool Specific Factor in CreditManager A New Tool for Decorrelating Loan Pools Driven by the Same Market Factor Attila Agod, András Bohák, Tamás Mátrai Attila.Agod@ Andras.Bohak@

Technical Note Introducing the Loan Pool Specific Factor in CreditManager A New Tool for Decorrelating Loan Pools Driven by the Same Market Factor Attila Agod, András Bohák, Tamás Mátrai Attila.Agod@ Andras.Bohak@

MSCI AUSTRALIA SELECT HIGH DIVIDEND YIELD INDEX

INDEX METHODOLOGY MSCI AUSTRALIA SELECT HIGH DIVIDEND YIELD INDEX March 2014 MARCH 2014 CONTENTS 1 Introduction... 3 2 Constructing the MSCI Australia Select High Dividend Yield Index... 4 3 Maintaining

INDEX METHODOLOGY MSCI AUSTRALIA SELECT HIGH DIVIDEND YIELD INDEX March 2014 MARCH 2014 CONTENTS 1 Introduction... 3 2 Constructing the MSCI Australia Select High Dividend Yield Index... 4 3 Maintaining

Analyzing Market Response Using the Barra US Equity Model. Jyh Huei Lee, Jose Menchero, Frank Vallario. msci.com

US Market Report The on the US Equity Market Analyzing Market Response Using the Barra US Equity Model Jyh Huei Lee, Jose Menchero, Frank Vallario Introduction On May 1, 2013, the Federal Reserve announced

US Market Report The on the US Equity Market Analyzing Market Response Using the Barra US Equity Model Jyh Huei Lee, Jose Menchero, Frank Vallario Introduction On May 1, 2013, the Federal Reserve announced

MSCI Dividend Masters Indexes Methodology

Index Methodology MSCI es Methodology July 2014 msci.com Contents 1 Introduction... 3 2 Index Construction Methodology... 3 Section 2.1: Applicable Universe... 3 Section 2.2: Security Selection... 3 Section

Index Methodology MSCI es Methodology July 2014 msci.com Contents 1 Introduction... 3 2 Index Construction Methodology... 3 Section 2.1: Applicable Universe... 3 Section 2.2: Security Selection... 3 Section

MSCI Core Infrastructure Indexes Methodology

Index Methodology MSCI Core Infrastructure Indexes Methodology January 2015 msci.com Contents 1 Introduction... 3 2 Constructing MSCI Core Infrastructure Indexes... 3 2.1 Country and Constituent Selection...

Index Methodology MSCI Core Infrastructure Indexes Methodology January 2015 msci.com Contents 1 Introduction... 3 2 Constructing MSCI Core Infrastructure Indexes... 3 2.1 Country and Constituent Selection...

MSCI PRIVATE ASSET INVESTMENT CONFERENCE

MSCI PRIVATE ASSET INVESTMENT CONFERENCE Jun 30, 2015 Tokyo MSCI is pleased to invite you to the MSCI Private Asset Investment Conference which is widely reputed as the prime real estate investment event

MSCI PRIVATE ASSET INVESTMENT CONFERENCE Jun 30, 2015 Tokyo MSCI is pleased to invite you to the MSCI Private Asset Investment Conference which is widely reputed as the prime real estate investment event

Introduction. msci.com

Research Bulletin Reporting with Fair Value Adjusted Indexes! Introducing the New Introduction Nearly all U.S.-domiciled international equity mutual funds use fair value methodologies to adjust their daily

Research Bulletin Reporting with Fair Value Adjusted Indexes! Introducing the New Introduction Nearly all U.S.-domiciled international equity mutual funds use fair value methodologies to adjust their daily

Updated Stress Testing Features in RiskMetrics

Updated Stress Testing Features in RiskMetrics RiskManager Historical Scenarios for Fall 2008, Treatment of Yield Curve Shocks, and a Hectic Day Risk Setting Introduction MSCI has updated RiskMetrics RiskManager

Updated Stress Testing Features in RiskMetrics RiskManager Historical Scenarios for Fall 2008, Treatment of Yield Curve Shocks, and a Hectic Day Risk Setting Introduction MSCI has updated RiskMetrics RiskManager

INDEX METHODOLOGY MSCI REIT PREFERRED. Index Construction and Maintenance Methodology for the MSCI REIT Preferred Index.

INDEX METHODOLOGY MSCI REIT PREFERRED INDEX METHODOLOGY Index Construction and Maintenance Methodology for the MSCI REIT Preferred Index December 2014 DECEMBER 2014 CONTENTS 1 Introduction... 3 2 Defining

INDEX METHODOLOGY MSCI REIT PREFERRED INDEX METHODOLOGY Index Construction and Maintenance Methodology for the MSCI REIT Preferred Index December 2014 DECEMBER 2014 CONTENTS 1 Introduction... 3 2 Defining

Market Reclassification Implementation Q&A

Market Reclassification Implementation Q&A On June 11, 2013 MSCI announced the results of the 2013 Annual Market Classification Review. The purpose of this document is to address commonly asked questions

Market Reclassification Implementation Q&A On June 11, 2013 MSCI announced the results of the 2013 Annual Market Classification Review. The purpose of this document is to address commonly asked questions

MSCI Global Socially Responsible Indices Methodology

MSCI Global Socially Responsible Indices Methodology 1. Introduction Globally, investors are increasingly seeking to invest in accordance with their values such as religious beliefs, moral standards, or

MSCI Global Socially Responsible Indices Methodology 1. Introduction Globally, investors are increasingly seeking to invest in accordance with their values such as religious beliefs, moral standards, or

ESG and Fixed Income Investing

ESG and Fixed Income Investing ESG and Fixed Income Investing Laura Nishikawa, Head of ESG Fixed Income Research CSR Investing Summit New York, NY 22 July 2014 3 Introducing MSCI ESG Research ESG ratings

ESG and Fixed Income Investing ESG and Fixed Income Investing Laura Nishikawa, Head of ESG Fixed Income Research CSR Investing Summit New York, NY 22 July 2014 3 Introducing MSCI ESG Research ESG ratings

Introduction to RiskMetrics WealthBench

Introduction to RiskMetrics WealthBench RiskMetrics WealthBench WealthBench is a web based platform used by relationship managers and investment advisors in their investment planning processes to help

Introduction to RiskMetrics WealthBench RiskMetrics WealthBench WealthBench is a web based platform used by relationship managers and investment advisors in their investment planning processes to help

MSCI Announces the Results of the 2011 Annual Market Classification Review

MSCI Announces the Results of the 2011 Annual Market Classification Review Geneva June 21, 2011 MSCI Inc. (NYSE: MSCI), a leading provider of investment decision support tools worldwide, including indices,

MSCI Announces the Results of the 2011 Annual Market Classification Review Geneva June 21, 2011 MSCI Inc. (NYSE: MSCI), a leading provider of investment decision support tools worldwide, including indices,

MSCI CORE REAL ESTATE INDEXES METHODOLOGY

INDEX METHODOLOGY MSCI CORE REAL ESTATE INDEXES METHODOLOGY Index Construction and Maintenance Methodology for the MSCI Core Real Estate Indexes July 2016 JULY 2016 CONTENTS 1 Introduction... 3 2 Eligible

INDEX METHODOLOGY MSCI CORE REAL ESTATE INDEXES METHODOLOGY Index Construction and Maintenance Methodology for the MSCI Core Real Estate Indexes July 2016 JULY 2016 CONTENTS 1 Introduction... 3 2 Eligible

MSCI DIVERSIFIED MULTIPLE-FACTOR INDEXES METHODOLOGY

INDEX METHODOLOGY MSCI DIVERSIFIED MULTIPLE-FACTOR INDEXES METHODOLOGY October 2015 APRIL 2015 CONTENTS 1 Introduction... 3 2 Index Construction Methodology... 4 2.1 Applicable Universe... 4 2.2 Constituent

INDEX METHODOLOGY MSCI DIVERSIFIED MULTIPLE-FACTOR INDEXES METHODOLOGY October 2015 APRIL 2015 CONTENTS 1 Introduction... 3 2 Index Construction Methodology... 4 2.1 Applicable Universe... 4 2.2 Constituent

Results of MSCI 2015 Market Classification Review

Results of MSCI 2015 Market Classification Review China A Shares on Track for Inclusion MSCI and CSRC Will Form Working Group to Address Remaining Issues Geneva June 9, 2015 MSCI Inc. (NYSE: MSCI), the

Results of MSCI 2015 Market Classification Review China A Shares on Track for Inclusion MSCI and CSRC Will Form Working Group to Address Remaining Issues Geneva June 9, 2015 MSCI Inc. (NYSE: MSCI), the

Negative Interest Rates through the Lens of the Swiss Fixed Income Model

Negative Interest Rates through the Lens of the Swiss Fixed Income Model Introduction Investors continue to witness negative nominal interest rates in Switzerland and across many markets in the eurozone,

Negative Interest Rates through the Lens of the Swiss Fixed Income Model Introduction Investors continue to witness negative nominal interest rates in Switzerland and across many markets in the eurozone,

MSCI HEDGED INDEXES MSCI DAILY HEDGED INDEXES MSCI FX HEDGE INDEXES MSCI GLOBAL CURRENCY INDEXES

INDEX METHODOLOGY MSCI HEDGED INDEXES MSCI GLOBAL CURRENCY INDEXES July 2013 JULY 2013 CONTENTS Introduction... 5 1 Common Principles in the Calculation of MSCI Hedged, MSCI Daily Hedged, MSCI FX Hedge

INDEX METHODOLOGY MSCI HEDGED INDEXES MSCI GLOBAL CURRENCY INDEXES July 2013 JULY 2013 CONTENTS Introduction... 5 1 Common Principles in the Calculation of MSCI Hedged, MSCI Daily Hedged, MSCI FX Hedge

S&P DOW JONES INDICES AND MSCI ANNOUNCE REVISIONS TO THE GLOBAL INDUSTRY CLASSIFICATION STANDARD (GICS ) STRUCTURE IN 2016

STRUCTURE IN 2016") S&P DOW JONES INDICES AND MSCI ANNOUNCE REVISIONS TO THE GLOBAL INDUSTRY CLASSIFICATION STANDARD (GICS ) STRUCTURE IN 2016 New York, November 10, 2014 - S&P Dow Jones Indices, a leading provider of financial

S&P DOW JONES INDICES AND MSCI ANNOUNCE REVISIONS TO THE GLOBAL INDUSTRY CLASSIFICATION STANDARD (GICS ) STRUCTURE IN 2016 New York, November 10, 2014 - S&P Dow Jones Indices, a leading provider of financial

Multi-Asset Class Market Report: Hedging the Risk of $200 per Barrel

Multi-Asset Class Market Report: Hedging the Risk of $200 per Barrel Audrey Costabile and Zita Marossy Introduction Investors who believe that oil will not hit $200 per barrel may position themselves to

Multi-Asset Class Market Report: Hedging the Risk of $200 per Barrel Audrey Costabile and Zita Marossy Introduction Investors who believe that oil will not hit $200 per barrel may position themselves to

Why Currency Returns and Currency Hedging Matters

Research Insight Why Currency Returns and Currency Hedging Matters An Update on the MSCI Hedged Indices Jennifer Bender, Roman Kouzmenko, and Zoltan Nagy msci.com Overview With the growth of international

Research Insight Why Currency Returns and Currency Hedging Matters An Update on the MSCI Hedged Indices Jennifer Bender, Roman Kouzmenko, and Zoltan Nagy msci.com Overview With the growth of international

Minimum Volatility Equity Indexes

Minimum Volatility Equity Indexes Potential Tools for the Insurance Company November 2013 Overview Insurers looking for greater risk-adjusted returns from their portfolios often consider minimum volatility

Minimum Volatility Equity Indexes Potential Tools for the Insurance Company November 2013 Overview Insurers looking for greater risk-adjusted returns from their portfolios often consider minimum volatility

The Stock-Bond Relationship and.asset Allocation October 2009

The Stock-Bond Relationship and.asset Allocation October 2009 The relationship between stocks and bonds has important implications for asset allocation and risk diversification. This Research Bulletin

The Stock-Bond Relationship and.asset Allocation October 2009 The relationship between stocks and bonds has important implications for asset allocation and risk diversification. This Research Bulletin

New York, May 15, 2013. MSCI US Equity Indices

New York, May 15, 2013 MSCI US Equity Indices The following are changes in constituents for the MSCI US Equity Indices which will take place as of the close of May 31, 2013. SUMMARY OF THE CHANGES INCLUDED

New York, May 15, 2013 MSCI US Equity Indices The following are changes in constituents for the MSCI US Equity Indices which will take place as of the close of May 31, 2013. SUMMARY OF THE CHANGES INCLUDED

Frequently Asked Questions MSCI ESG RESEARCH. FAQs for the Corporate Community October 2014. msci.com

Frequently Asked Questions MSCI ESG RESEARCH for the Corporate Community MSCI ESG RESEARCH Frequently Asked Questions General: What is MSCI? MSCI is a leading provider of investment decision support tools

Frequently Asked Questions MSCI ESG RESEARCH for the Corporate Community MSCI ESG RESEARCH Frequently Asked Questions General: What is MSCI? MSCI is a leading provider of investment decision support tools

Vega Risk in RiskManager

Model Overview Lisa R. Goldberg Michael Y. Hayes Ola Mahmoud (Marie Cure Fellow) 1 Tamas Matrai 1 Ola Mahmoud was a Marie Curie Fellows at MSCI. The research leading to these results has received funding

Model Overview Lisa R. Goldberg Michael Y. Hayes Ola Mahmoud (Marie Cure Fellow) 1 Tamas Matrai 1 Ola Mahmoud was a Marie Curie Fellows at MSCI. The research leading to these results has received funding

Is There a Link Between GDP Growth and Equity Returns? May 2010

Is There a Link Between GDP Growth and Equity Introduction A recurring question in finance concerns the relationship between economic growth and stock market return. Recently, for example, some emerging

Is There a Link Between GDP Growth and Equity Introduction A recurring question in finance concerns the relationship between economic growth and stock market return. Recently, for example, some emerging

RESULTS OF MSCI 2016 MARKET CLASSIFICATION REVIEW

RESULTS OF MSCI 2016 MARKET CLASSIFICATION REVIEW MSCI will delay including China A shares in the MSCI Emerging Markets Index New York June 14, 2016 MSCI Inc. (NYSE: MSCI), a leading provider of global

RESULTS OF MSCI 2016 MARKET CLASSIFICATION REVIEW MSCI will delay including China A shares in the MSCI Emerging Markets Index New York June 14, 2016 MSCI Inc. (NYSE: MSCI), a leading provider of global

Effective downside risk management

Effective downside risk management Aymeric Forest, Fund Manager, Multi-Asset Investments November 2012 Since 2008, the desire to avoid significant portfolio losses has, more than ever, been at the front

Effective downside risk management Aymeric Forest, Fund Manager, Multi-Asset Investments November 2012 Since 2008, the desire to avoid significant portfolio losses has, more than ever, been at the front

MSCI Announces Results of the 2014 Annual Market Classification Review

MSCI Announces Results of the 2014 Annual Market Classification Review Geneva June 10, 2014 MSCI Inc. (NYSE: MSCI), a leading provider of indexes and other investment decision support tools worldwide,

MSCI Announces Results of the 2014 Annual Market Classification Review Geneva June 10, 2014 MSCI Inc. (NYSE: MSCI), a leading provider of indexes and other investment decision support tools worldwide,

FRANKLIN GLOBAL EQUITY INDEX

INDEX METHODOLOGY FRANKLIN GLOBAL EQUITY INDEX Mrig, Lokesh April 2016 APRIL 2016 CONTENTS 1 Introduction... 3 2 Index Construction Methodology... 4 2.1 Defining The Eligible Universe... 4 2.2 Determination

INDEX METHODOLOGY FRANKLIN GLOBAL EQUITY INDEX Mrig, Lokesh April 2016 APRIL 2016 CONTENTS 1 Introduction... 3 2 Index Construction Methodology... 4 2.1 Defining The Eligible Universe... 4 2.2 Determination

Risk Characteristics of Emerging Market Bonds

www.mscibarra.com Risk Characteristics of Emerging Market Bonds March 2010 David T. Owyong, PhD Anand S. Iyer, CFA 2010 MSCI Barra. All rights reserved. In 2009, emerging market bonds were among the top-performing

www.mscibarra.com Risk Characteristics of Emerging Market Bonds March 2010 David T. Owyong, PhD Anand S. Iyer, CFA 2010 MSCI Barra. All rights reserved. In 2009, emerging market bonds were among the top-performing

An Introduction to the Asset Class. Convertible Bonds

An Introduction to the Asset Class Convertible DESCRIPTION Convertible (CBs) are fixed income instruments that can be converted into a fixed number of shares of the issuer at the option of the investor.

An Introduction to the Asset Class Convertible DESCRIPTION Convertible (CBs) are fixed income instruments that can be converted into a fixed number of shares of the issuer at the option of the investor.

RISK MANAGEMENT TOOLS

RISK MANAGEMENT TOOLS Pavilion Advisory Group TM Pavilion Advisory Group is a trademark of Pavilion Financial Corporation used under license by Pavilion Advisory Group Ltd. in Canada and Pavilion Advisory

RISK MANAGEMENT TOOLS Pavilion Advisory Group TM Pavilion Advisory Group is a trademark of Pavilion Financial Corporation used under license by Pavilion Advisory Group Ltd. in Canada and Pavilion Advisory

A constant volatility framework for managing tail risk

A constant volatility framework for managing tail risk Alexandre Hocquard, Sunny Ng and Nicolas Papageorgiou 1 Brockhouse Cooper and HEC Montreal September 2010 1 Alexandre Hocquard is Portfolio Manager,

A constant volatility framework for managing tail risk Alexandre Hocquard, Sunny Ng and Nicolas Papageorgiou 1 Brockhouse Cooper and HEC Montreal September 2010 1 Alexandre Hocquard is Portfolio Manager,

MSCI Announces Market Classification Decisions

MSCI Announces Market Classification Decisions Geneva - June 15, 2009 - MSCI Inc. (NYSE: MXB), a leading provider of investment decision support tools worldwide, including indices and portfolio risk and

MSCI Announces Market Classification Decisions Geneva - June 15, 2009 - MSCI Inc. (NYSE: MXB), a leading provider of investment decision support tools worldwide, including indices and portfolio risk and

Factoring in the Emerging Markets Premium

Factoring in the Emerging Markets Premium Exploring Factor Indexes in Emerging Markets Raina Oberoi Raman Aylur Subramanian Anil Rao Philippe Durand Contents Contents... 2 Executive Summary... 3 I. Emerging

Factoring in the Emerging Markets Premium Exploring Factor Indexes in Emerging Markets Raina Oberoi Raman Aylur Subramanian Anil Rao Philippe Durand Contents Contents... 2 Executive Summary... 3 I. Emerging

S&P 500 Composite (Adjusted for Inflation)

") 12/31/1820 03/31/1824 06/30/1827 09/30/1830 12/31/1833 03/31/1837 06/30/1840 09/30/1843 12/31/1846 03/31/1850 06/30/1853 09/30/1856 12/31/1859 03/31/1863 06/30/1866 09/30/1869 12/31/1872 03/31/1876 06/30/1879

12/31/1820 03/31/1824 06/30/1827 09/30/1830 12/31/1833 03/31/1837 06/30/1840 09/30/1843 12/31/1846 03/31/1850 06/30/1853 09/30/1856 12/31/1859 03/31/1863 06/30/1866 09/30/1869 12/31/1872 03/31/1876 06/30/1879

THE U.S. INFRASTRUCTURE EFFECT INTERVIEW BY CAROL CAMERON

This interview originally appeared in the Summer 24 edition of InSIGHTS, a quarterly publication from S&P Dow Jones Indices. THE U.S. INFRASTRUCTURE EFFECT INTERVIEW BY CAROL CAMERON Every four years,

This interview originally appeared in the Summer 24 edition of InSIGHTS, a quarterly publication from S&P Dow Jones Indices. THE U.S. INFRASTRUCTURE EFFECT INTERVIEW BY CAROL CAMERON Every four years,

Investing In Volatility

Investing In Volatility By: Anish Parvataneni, CFA Portfolio Manager LJM Partners Ltd. LJM Partners, Ltd. is issuing a series a white papers on the subject of investing in volatility as an asset class.

Investing In Volatility By: Anish Parvataneni, CFA Portfolio Manager LJM Partners Ltd. LJM Partners, Ltd. is issuing a series a white papers on the subject of investing in volatility as an asset class.

NOVEMBER 2010 VOLATILITY AS AN ASSET CLASS

NOVEMBER 2010 VOLATILITY AS AN ASSET CLASS 2/11 INTRODUCTION Volatility has become a key word of the recent financial crisis with realised volatilities of asset prices soaring and volatilities implied

NOVEMBER 2010 VOLATILITY AS AN ASSET CLASS 2/11 INTRODUCTION Volatility has become a key word of the recent financial crisis with realised volatilities of asset prices soaring and volatilities implied

S&P DOW JONES INDICES AND MSCI ANNOUNCE FURTHER REVISIONS TO THE GLOBAL INDUSTRY CLASSIFICATION STANDARD (GICS ) STRUCTURE IN 2016

STRUCTURE IN 2016") S&P DOW JONES INDICES AND MSCI ANNOUNCE FURTHER REVISIONS TO THE GLOBAL INDUSTRY CLASSIFICATION STANDARD (GICS ) STRUCTURE IN 2016 New York, November 2, 2015 - S&P Dow Jones Indices, a leading provider

S&P DOW JONES INDICES AND MSCI ANNOUNCE FURTHER REVISIONS TO THE GLOBAL INDUSTRY CLASSIFICATION STANDARD (GICS ) STRUCTURE IN 2016 New York, November 2, 2015 - S&P Dow Jones Indices, a leading provider

Fixed Income Focus: Ireland & Portugal

In the past decade we have seen droves of investors driven to global fixed income markets in search of higher yields. While the global pool of fixed income securities more than doubled, we saw asset bubbles

In the past decade we have seen droves of investors driven to global fixed income markets in search of higher yields. While the global pool of fixed income securities more than doubled, we saw asset bubbles

Variance swaps and CBOE S&P 500 variance futures

Variance swaps and CBOE S&P 500 variance futures by Lewis Biscamp and Tim Weithers, Chicago Trading Company, LLC Over the past several years, equity-index volatility products have emerged as an asset class

Variance swaps and CBOE S&P 500 variance futures by Lewis Biscamp and Tim Weithers, Chicago Trading Company, LLC Over the past several years, equity-index volatility products have emerged as an asset class

IPD GLOBAL QUARTERLY PROPERTY FUND INDEX

IPD GLOBAL QUARTERLY PROPERTY FUND INDEX Contributing Managers and Funds March 2015 MARCH 2015 CONTRIBUTING MANAGERS AND FUNDS MARCH 2015 Asia Pacific Management House AMP Capital Investors AMP Capital

IPD GLOBAL QUARTERLY PROPERTY FUND INDEX Contributing Managers and Funds March 2015 MARCH 2015 CONTRIBUTING MANAGERS AND FUNDS MARCH 2015 Asia Pacific Management House AMP Capital Investors AMP Capital

De-Risking Solutions: Low and Managed Volatility

De-Risking Solutions: Low and Managed Volatility NCPERS May 17, 2016 Richard Yasenchak, CFA Senior Vice President, Client Portfolio Manager, INTECH FOR INSTITUTIONAL INVESTOR USE C-0416-1610 12-30-16 AGENDA

De-Risking Solutions: Low and Managed Volatility NCPERS May 17, 2016 Richard Yasenchak, CFA Senior Vice President, Client Portfolio Manager, INTECH FOR INSTITUTIONAL INVESTOR USE C-0416-1610 12-30-16 AGENDA

EVALUATING THE PERFORMANCE CHARACTERISTICS OF THE CBOE S&P 500 PUTWRITE INDEX

DECEMBER 2008 Independent advice for the institutional investor EVALUATING THE PERFORMANCE CHARACTERISTICS OF THE CBOE S&P 500 PUTWRITE INDEX EXECUTIVE SUMMARY The CBOE S&P 500 PutWrite Index (ticker symbol

DECEMBER 2008 Independent advice for the institutional investor EVALUATING THE PERFORMANCE CHARACTERISTICS OF THE CBOE S&P 500 PUTWRITE INDEX EXECUTIVE SUMMARY The CBOE S&P 500 PutWrite Index (ticker symbol

Best Practices for Investment Risk Management June 2009

Best Practices for Investment Risk Management Jennifer Bender Frank Nielsen A successful investment process requires a risk management structure that addresses multiple aspects of risk. Here we lay out

Best Practices for Investment Risk Management Jennifer Bender Frank Nielsen A successful investment process requires a risk management structure that addresses multiple aspects of risk. Here we lay out

DISCLAIMER. A Member of Financial Group

Tactical ETF Approaches for Today s Investors Jaime Purvis, Executive Vice-President Horizons Exchange Traded Funds April 2012 DISCLAIMER Commissions, management fees and expenses all may be associated

Tactical ETF Approaches for Today s Investors Jaime Purvis, Executive Vice-President Horizons Exchange Traded Funds April 2012 DISCLAIMER Commissions, management fees and expenses all may be associated

NOTES ON THE BANK OF ENGLAND OPTION-IMPLIED PROBABILITY DENSITY FUNCTIONS

1 NOTES ON THE BANK OF ENGLAND OPTION-IMPLIED PROBABILITY DENSITY FUNCTIONS Options are contracts used to insure against or speculate/take a view on uncertainty about the future prices of a wide range

1 NOTES ON THE BANK OF ENGLAND OPTION-IMPLIED PROBABILITY DENSITY FUNCTIONS Options are contracts used to insure against or speculate/take a view on uncertainty about the future prices of a wide range

Guarantees and Target Volatility Funds

SEPTEMBER 0 ENTERPRISE RISK SOLUTIONS B&H RESEARCH E SEPTEMBER 0 DOCUMENTATION PACK Steven Morrison PhD Laura Tadrowski PhD Moody's Analytics Research Contact Us Americas +..55.658 clientservices@moodys.com

SEPTEMBER 0 ENTERPRISE RISK SOLUTIONS B&H RESEARCH E SEPTEMBER 0 DOCUMENTATION PACK Steven Morrison PhD Laura Tadrowski PhD Moody's Analytics Research Contact Us Americas +..55.658 clientservices@moodys.com

The Fundamentals of Fundamental Factor Models

www.msci.com The Fundamentals of Fundamental Factor Models June 2010 Jennifer Bender Frank Nielsen 2010 MSCI. All rights reserved. 1 of 15 Electronic copy available at: http://ssrn.com/abstract=1707661

www.msci.com The Fundamentals of Fundamental Factor Models June 2010 Jennifer Bender Frank Nielsen 2010 MSCI. All rights reserved. 1 of 15 Electronic copy available at: http://ssrn.com/abstract=1707661

Emini Education - Managing Volatility in Equity Portfolios

PH&N Trustee Education Seminar 2012 Managing Volatility in Equity Portfolios Why Equities? Equities Offer: Participation in global economic growth Superior historical long-term returns compared to other

PH&N Trustee Education Seminar 2012 Managing Volatility in Equity Portfolios Why Equities? Equities Offer: Participation in global economic growth Superior historical long-term returns compared to other

Measuring Volatility in Australia

CONTRIBUTOR Berlinda Liu Director Global Research & Design berlinda_liu@spdji.com How is VIX computed? Select first and second month OTM puts and OTM calls Compute implied volatility for each maturity

CONTRIBUTOR Berlinda Liu Director Global Research & Design berlinda_liu@spdji.com How is VIX computed? Select first and second month OTM puts and OTM calls Compute implied volatility for each maturity

Capturing Equity Risk Premium Revisiting the Investment Strategy

Capturing Equity Risk Premium Revisiting the Investment Strategy Introduction: Equity Risk without Reward? Institutions with return-oriented investment portfolios have traditionally relied upon significant

Capturing Equity Risk Premium Revisiting the Investment Strategy Introduction: Equity Risk without Reward? Institutions with return-oriented investment portfolios have traditionally relied upon significant

INDEX SERIES FTSE PUBLICATIONS. FTSE ETF Issuer Services.

INDEX SERIES FTSE PUBLICATIONS FTSE ETF Issuer Services. BEIJING BOSTON DUBAI HONG KONG LONDON MILAN MUMBAI NEW YORK PARIS SAN FRANCISCO SHANGHAI SYDNEY TOKYO FTSE FTSE Group ( FTSE ) is a world-leader

INDEX SERIES FTSE PUBLICATIONS FTSE ETF Issuer Services. BEIJING BOSTON DUBAI HONG KONG LONDON MILAN MUMBAI NEW YORK PARIS SAN FRANCISCO SHANGHAI SYDNEY TOKYO FTSE FTSE Group ( FTSE ) is a world-leader

Dual Listing of the SGX EURO STOXX 50 Index Futures in Singapore

September 2011 Dual Listing of the SGX EURO STOXX 50 Index Futures in Singapore Mr Tobias Hekster Managing Director, True Partner Education Ltd Senior Strategist, Algorithmic Training Group of Hong Kong

September 2011 Dual Listing of the SGX EURO STOXX 50 Index Futures in Singapore Mr Tobias Hekster Managing Director, True Partner Education Ltd Senior Strategist, Algorithmic Training Group of Hong Kong

Life Settlements Investments

Title: Life Settlements Investments Authors: Craig Ansley Director, Capital Markets Research Julian Darby Consultant Date: February 2010 Synopsis: Life settlements is becoming an increasingly popular asset

Title: Life Settlements Investments Authors: Craig Ansley Director, Capital Markets Research Julian Darby Consultant Date: February 2010 Synopsis: Life settlements is becoming an increasingly popular asset

Volatility: A Brief Overview

The Benefits of Systematically Selling Volatility July 2014 By Jeremy Berman Justin Frankel Co-Portfolio Managers of the RiverPark Structural Alpha Fund Abstract: A strategy of systematically selling volatility

The Benefits of Systematically Selling Volatility July 2014 By Jeremy Berman Justin Frankel Co-Portfolio Managers of the RiverPark Structural Alpha Fund Abstract: A strategy of systematically selling volatility

Black-Scholes-Merton approach merits and shortcomings

Black-Scholes-Merton approach merits and shortcomings Emilia Matei 1005056 EC372 Term Paper. Topic 3 1. Introduction The Black-Scholes and Merton method of modelling derivatives prices was first introduced

Black-Scholes-Merton approach merits and shortcomings Emilia Matei 1005056 EC372 Term Paper. Topic 3 1. Introduction The Black-Scholes and Merton method of modelling derivatives prices was first introduced

Market Linked Certificates of Deposit

Market Linked Certificates of Deposit This material was prepared by Wells Fargo Securities, LLC, a registered brokerdealer and separate non-bank affiliate of Wells Fargo & Company. This material is not

Market Linked Certificates of Deposit This material was prepared by Wells Fargo Securities, LLC, a registered brokerdealer and separate non-bank affiliate of Wells Fargo & Company. This material is not

A Liquid Benchmark for Private Real Estate

A Liquid Benchmark for Private Real Estate Mark Clacy-Jones Roman Kouzmenko Bryan Reid Bert Teuben Contents Contents... 2 Executive Summary... 3 Introduction... 4 Private and Listed Real Estate Indexes...

A Liquid Benchmark for Private Real Estate Mark Clacy-Jones Roman Kouzmenko Bryan Reid Bert Teuben Contents Contents... 2 Executive Summary... 3 Introduction... 4 Private and Listed Real Estate Indexes...

WHITE PAPER CONVERTIBLE BONDS THE BEST OF BOTH WORLDS

WHITE PAPER CONVERTIBLE BONDS THE BEST OF BOTH WORLDS Convertible bonds have become an increasingly popular asset class in recent years, as issuers and investors have gained an improved understanding of

WHITE PAPER CONVERTIBLE BONDS THE BEST OF BOTH WORLDS Convertible bonds have become an increasingly popular asset class in recent years, as issuers and investors have gained an improved understanding of

MSCI Announces the Results of the 2012 Annual Market Classification Review

MSCI Announces the Results of the 2012 Annual Market Classification Review Geneva June 20, 2012 MSCI Inc. (NYSE: MSCI), a leading provider of investment decision support tools worldwide, including indices,

MSCI Announces the Results of the 2012 Annual Market Classification Review Geneva June 20, 2012 MSCI Inc. (NYSE: MSCI), a leading provider of investment decision support tools worldwide, including indices,

A case for high-yield bonds

By: Yoshie Phillips, CFA, Senior Research Analyst AUGUST 212 A case for high-yield bonds High-yield bonds have historically produced strong returns relative to those of other major asset classes, including

By: Yoshie Phillips, CFA, Senior Research Analyst AUGUST 212 A case for high-yield bonds High-yield bonds have historically produced strong returns relative to those of other major asset classes, including

Minimizing Downside Risk in Axioma Portfolio with Options

United States and Canada: 212-991-4500 Europe: +44 (0)20 7856 2424 Asia: +852-8203-2790 Minimizing Downside Risk in Axioma Portfolio with Options 1 Introduction The market downturn in 2008 is considered

United States and Canada: 212-991-4500 Europe: +44 (0)20 7856 2424 Asia: +852-8203-2790 Minimizing Downside Risk in Axioma Portfolio with Options 1 Introduction The market downturn in 2008 is considered

INSIGHT. Do we need corporate bonds? Credits in competition with treasuries and equities. For professional use only. Not for re-distribution.

INSIGHT For the Forth Quarter of 2009 Do we need corporate bonds? s in competition with treasuries and equities Do we need corporate bonds? s in competition with treasuries and equities Article written

INSIGHT For the Forth Quarter of 2009 Do we need corporate bonds? s in competition with treasuries and equities Do we need corporate bonds? s in competition with treasuries and equities Article written

} } Global Markets. Currency options. Currency options. Introduction. Options contracts. Types of options contracts

Global Markets Currency options Currency options Introduction Currency options have gained acceptance as invaluable tools in managing foreign exchange risk. They are extensively used and bring a much wider

Global Markets Currency options Currency options Introduction Currency options have gained acceptance as invaluable tools in managing foreign exchange risk. They are extensively used and bring a much wider

Active Versus Passive Low-Volatility Investing

Active Versus Passive Low-Volatility Investing Introduction ISSUE 3 October 013 Danny Meidan, Ph.D. (561) 775.1100 Low-volatility equity investing has gained quite a lot of interest and assets over the

Active Versus Passive Low-Volatility Investing Introduction ISSUE 3 October 013 Danny Meidan, Ph.D. (561) 775.1100 Low-volatility equity investing has gained quite a lot of interest and assets over the

Responding to the Call for Fossil-fuel Free Portfolios

FAQ Updated Responding to the Call for Fossil-fuel Free Portfolios What is fossil-free investing? Students, faculty and elected officials are asking college endowments and municipal and state pension funds

FAQ Updated Responding to the Call for Fossil-fuel Free Portfolios What is fossil-free investing? Students, faculty and elected officials are asking college endowments and municipal and state pension funds

Introduction to Equity Derivatives

Introduction to Equity Derivatives Aaron Brask + 44 (0)20 7773 5487 Internal use only Equity derivatives overview Products Clients Client strategies Barclays Capital 2 Equity derivatives products Equity

Introduction to Equity Derivatives Aaron Brask + 44 (0)20 7773 5487 Internal use only Equity derivatives overview Products Clients Client strategies Barclays Capital 2 Equity derivatives products Equity

A Case for Dividend Investing

A Case for Dividend Investing Many investors may be surprised to learn that dividends paid by companies have accounted for 45% of the total return for Australian equities over the last 10 years 1. Buying

A Case for Dividend Investing Many investors may be surprised to learn that dividends paid by companies have accounted for 45% of the total return for Australian equities over the last 10 years 1. Buying

Adaptive Asset Allocation

INVESTMENT INSIGHTS SERIES Adaptive Asset Allocation Refocusing Portfolio Management Toward Investor End Goals Introduction Though most investors may not be explicit in saying it, one of their primary

INVESTMENT INSIGHTS SERIES Adaptive Asset Allocation Refocusing Portfolio Management Toward Investor End Goals Introduction Though most investors may not be explicit in saying it, one of their primary

A case for high-yield bonds

By: Yoshie Phillips, CFA, Senior Research Analyst MAY 212 A case for high-yield bonds High-yield bonds have historically produced strong returns relative to those of other major asset classes, including

By: Yoshie Phillips, CFA, Senior Research Analyst MAY 212 A case for high-yield bonds High-yield bonds have historically produced strong returns relative to those of other major asset classes, including

9 Questions Every ETF Investor Should Ask Before Investing

9 Questions Every ETF Investor Should Ask Before Investing 1. What is an ETF? 2. What kinds of ETFs are available? 3. How do ETFs differ from other investment products like mutual funds, closed-end funds,

9 Questions Every ETF Investor Should Ask Before Investing 1. What is an ETF? 2. What kinds of ETFs are available? 3. How do ETFs differ from other investment products like mutual funds, closed-end funds,

International Investments

2008 AGI-Information Management Consultants May be used for personal purporses only or by libraries associated to dandelon.com network. International Investments Bruno Solnik H.E.C. SCHOOL of MANAGEMENT

2008 AGI-Information Management Consultants May be used for personal purporses only or by libraries associated to dandelon.com network. International Investments Bruno Solnik H.E.C. SCHOOL of MANAGEMENT

Interest Rates and Inflation: How They Might Affect Managed Futures

Faced with the prospect of potential declines in both bonds and equities, an allocation to managed futures may serve as an appealing diversifier to traditional strategies. HIGHLIGHTS Managed Futures have

Faced with the prospect of potential declines in both bonds and equities, an allocation to managed futures may serve as an appealing diversifier to traditional strategies. HIGHLIGHTS Managed Futures have

Target Date Versus Relative Risk: A Comparison of 2 Retirement Strategies

Versus Relative Risk: A Comparison of 2 Retirement Strategies MARCH 2014 CONTRIBUTOR Peter Tsui Director, Index Research & Design peter.tsui@spdji.com Target date funds have grown significantly over the

Versus Relative Risk: A Comparison of 2 Retirement Strategies MARCH 2014 CONTRIBUTOR Peter Tsui Director, Index Research & Design peter.tsui@spdji.com Target date funds have grown significantly over the

Rethinking Fixed Income

Rethinking Fixed Income Challenging Conventional Wisdom May 2013 Risk. Reinsurance. Human Resources. Rethinking Fixed Income: Challenging Conventional Wisdom With US Treasury interest rates at, or near,

Rethinking Fixed Income Challenging Conventional Wisdom May 2013 Risk. Reinsurance. Human Resources. Rethinking Fixed Income: Challenging Conventional Wisdom With US Treasury interest rates at, or near,

Sensex Realized Volatility Index

Sensex Realized Volatility Index Introduction: Volatility modelling has traditionally relied on complex econometric procedures in order to accommodate the inherent latent character of volatility. Realized

Sensex Realized Volatility Index Introduction: Volatility modelling has traditionally relied on complex econometric procedures in order to accommodate the inherent latent character of volatility. Realized

Overcoming the Limitations in Traditional Fixed Income Benchmarks

Title: Author: Overcoming the Limitations in Traditional Fixed Income Benchmarks Clive Smith Portfolio Manager Date: October 2011 Synopsis: The last decade has seen material shifts in the composition of

Title: Author: Overcoming the Limitations in Traditional Fixed Income Benchmarks Clive Smith Portfolio Manager Date: October 2011 Synopsis: The last decade has seen material shifts in the composition of

BlackRock Launches Retirement Income Indexes

BlackRock Launches Retirement Income Indexes Groundbreaking Indexes Give Investors Metric to Translate Retirement Savings into Retirement Income; Enables Better Planning, Midcourse Corrections During Critical

BlackRock Launches Retirement Income Indexes Groundbreaking Indexes Give Investors Metric to Translate Retirement Savings into Retirement Income; Enables Better Planning, Midcourse Corrections During Critical

Identifying the Differences Between VIX Spot and Futures

PRACTICE ESSENTIALS STRATEGY 201 U.S. Identifying the Differences Between VIX Spot and Futures CONTRIBUTOR Berlinda Liu berlinda.liu@spdji.com The S&P Dow Jones Indices Practice Essentials series is a

PRACTICE ESSENTIALS STRATEGY 201 U.S. Identifying the Differences Between VIX Spot and Futures CONTRIBUTOR Berlinda Liu berlinda.liu@spdji.com The S&P Dow Jones Indices Practice Essentials series is a

Perspectives September

Perspectives September 2013 Quantitative Research Option Modeling for Leveraged Finance Part I Bjorn Flesaker Managing Director and Head of Quantitative Research Prudential Fixed Income Juan Suris Vice

Perspectives September 2013 Quantitative Research Option Modeling for Leveraged Finance Part I Bjorn Flesaker Managing Director and Head of Quantitative Research Prudential Fixed Income Juan Suris Vice

The Credit Analysis Process: From In-Depth Company Research to Selecting the Right Instrument

Featured Solution May 2015 Your Global Investment Authority The Credit Analysis Process: From In-Depth Company Research to Selecting the Right Instrument In today s low yield environment, an active investment

Featured Solution May 2015 Your Global Investment Authority The Credit Analysis Process: From In-Depth Company Research to Selecting the Right Instrument In today s low yield environment, an active investment

Investment Insight Diversified Factor Premia Edward Qian PhD, CFA, Bryan Belton, CFA, and Kun Yang PhD, CFA PanAgora Asset Management August 2013

Investment Insight Diversified Factor Premia Edward Qian PhD, CFA, Bryan Belton, CFA, and Kun Yang PhD, CFA PanAgora Asset Management August 2013 Modern Portfolio Theory suggests that an investor s return

Investment Insight Diversified Factor Premia Edward Qian PhD, CFA, Bryan Belton, CFA, and Kun Yang PhD, CFA PanAgora Asset Management August 2013 Modern Portfolio Theory suggests that an investor s return

Option pricing in detail

Course #: Title Module 2 Option pricing in detail Topic 1: Influences on option prices - recap... 3 Which stock to buy?... 3 Intrinsic value and time value... 3 Influences on option premiums... 4 Option

Course #: Title Module 2 Option pricing in detail Topic 1: Influences on option prices - recap... 3 Which stock to buy?... 3 Intrinsic value and time value... 3 Influences on option premiums... 4 Option

corrected transcript FactSet Research Systems Inc. MANAGEMENT DISCUSSION SECTION

MANAGEMENT DISCUSSION SECTION Company Representative Welcome to Perspectives with FactSet. Today we ll be speaking with Phil Guziec, Derivatives Investing Strategist and Editor of the OptionInvestor Service

MANAGEMENT DISCUSSION SECTION Company Representative Welcome to Perspectives with FactSet. Today we ll be speaking with Phil Guziec, Derivatives Investing Strategist and Editor of the OptionInvestor Service

Target Date Funds: Debating To Versus Through

Target Date Funds: Debating To Versus Through Glenn Dial, Sr. VP, Head of Retirement Product Business Development, Allianz Global Investors Distributors LLC Scott Brooks, Head of US Retail Client Relations

Target Date Funds: Debating To Versus Through Glenn Dial, Sr. VP, Head of Retirement Product Business Development, Allianz Global Investors Distributors LLC Scott Brooks, Head of US Retail Client Relations

MSCI US REIT Index Methodology

Index Construction and Maintenance Methodology for the MSCI US REIT Index Contents Introduction... 3 Section 1: Defining REITs and the MSCI US REIT Index Eligible REITs... 4 Section 2: Free Float-Adjusting

Index Construction and Maintenance Methodology for the MSCI US REIT Index Contents Introduction... 3 Section 1: Defining REITs and the MSCI US REIT Index Eligible REITs... 4 Section 2: Free Float-Adjusting

Mechanics of Currency Hedged Indices

EQUITY 101 Global Mechanics of Currency Hedged Indices CONTRIBUTORS Sabrina Salemi Manager, Strategy and Global Equity Indices sabrina.salemi@spdji.com Philip Murphy, CFA Vice President, North American

EQUITY 101 Global Mechanics of Currency Hedged Indices CONTRIBUTORS Sabrina Salemi Manager, Strategy and Global Equity Indices sabrina.salemi@spdji.com Philip Murphy, CFA Vice President, North American

Identifying the Differences Between VIX Spot and Futures

PRACTICE ESSENTIALS STRATEGY 201 U.S. Identifying the Differences Between VIX Spot and Futures CONTRIBUTOR Berlinda Liu Berlinda.liu@spdji.com The S&P Dow Jones Indices Practice Essentials series is a

PRACTICE ESSENTIALS STRATEGY 201 U.S. Identifying the Differences Between VIX Spot and Futures CONTRIBUTOR Berlinda Liu Berlinda.liu@spdji.com The S&P Dow Jones Indices Practice Essentials series is a