Credit Cards: Disentangling the Dual Use of Borrowing and Spending

|

|

|

- Elfrieda West

- 10 years ago

- Views:

Transcription

1 Staff Analytical Note/Note analytique du personnel Credit Cards: Disentangling the Dual Use of Borrowing and Spending by Olga Bilyk and Brian Peterson Bank of Canada staff analytical notes are short articles that focus on topical issues relevant to the current economic and financial context, produced independently from the Bank s Governing Council. This work may support or challenge prevailing policy orthodoxy. Therefore, the views expressed in this note are solely those of the authors and may differ from official Bank of Canada views. No responsibility for them should be attributed to the Bank.

2 Bank of Canada Staff Analytical Note December 2015 Credit Cards: Disentangling the Dual Use of Borrowing and Spending by Olga Bilyk and Brian Peterson Financial Stability Department Bank of Canada Ottawa, Ontario, Canada K1A 0G Bank of Canada

3 Acknowledgements Thanks to Gino Cateau and Marc-André Gosselin for invaluable comments that greatly improved the note. Abstract Over the past 15 years, aggregate credit card balances have been increasing, except for a brief spell in the aftermath of the financial crisis. Determining whether the growing balances are due to increased usage of credit cards as a method of payment or whether they reflect increased short-term borrowing is challenging because aggregate balances are snapshots of charges on credit cards before households make their monthly payments. In this note, we exploit household-level survey data to distinguish between the dual use of credit cards for borrowing or paying for purchases. We find that the growth in credit card balances over the past 15 years reflects increased usage of credit cards for payment (i.e., spending) rather than increased short-term borrowing. Bank classification: Credit and credit aggregates; Financial stability Résumé Les encours des cartes de crédit n ont cessé d augmenter depuis 15 ans, mis à part durant une courte période après la crise financière de Il est difficile d établir si cette augmentation tient à un emploi accru de la carte de crédit comme mode de paiement ou à l augmentation des emprunts de court terme. En effet, l encours global ne renseigne que sur la totalité des sommes portées sur les cartes de crédit à un moment donné, avant que les ménages effectuent leurs paiements mensuels. Dans cette note analytique, nous exploitons les données d une enquête réalisée auprès des ménages pour distinguer l usage des cartes de crédit comme instrument de paiement et comme instrument de crédit. Nos résultats montrent que la hausse des encours des cartes de crédit ces quinze dernières années est attribuable à une utilisation plus fréquente de la carte de crédit comme moyen de paiement des dépenses de consommation, et non comme source d emprunts de court terme. Classification de la Banque : Crédit et agrégats du crédit; Stabilité financière iii

4 Issue Over the past 15 years, aggregate credit card balances have been increasing except for a brief spell in the aftermath of the financial crisis. Determining whether the growing balances are due to increased use of credit cards as a method of payment or whether they reflect increased short-term borrowing is challenging. This is because aggregate balances are snapshots of credit card charges before households make their monthly payments. In this note, we exploit household-level survey data to distinguish between the two uses of credit cards for borrowing or paying for purchases. Key Messages The growth in credit card balances over the past 15 years reflects the increased use of credit cards for payment (i.e., spending) rather than increased short-term borrowing. The majority of credit card owners in Canada do not carry any credit card debt. The share of such households grew from 48 per cent in the early 2000s to 55 per cent in recent years. Examining the various ways credit cards are used at the household level, we find that highincome renters are among the heaviest credit card borrowers. This reflects the fact that these households lack access to cheaper forms of borrowing, such as home equity lines of credit (HELOCs). The extent to which borrowing by renters represents a vulnerability for the financial system is tempered by the fact that they have a relatively large capacity to repay, given their high income, and tend to have credit cards with lower interest rates.

5 2 1. Motivation: Dual Use and Aggregate Data Leading up to the financial crisis of , credit card balances for Canadian households increased steadily, according to data from Equifax. 1 In real terms, credit card balances grew two-fold from 1999 to 2009, reaching an all-time high of $87.1 billion in the latter year, as measured in constant 2014 dollars (Chart 1). Following the crisis, balances decreased to $79.8 billion in 2012 but subsequently grew to $83.3 billion as of 2015Q2. 2 Chart 1: Aggregate credit card balances increased over the past 15 years Constant 2014 dollars $ billions Source: Equifax Last observation: 2015Q2 To understand recent patterns in credit card balances, it is important to recognize the dual role of credit cards as a method of payment and as a means of borrowing. Consider two types of credit card users: the convenience user and the borrower. The convenience user relies on credit cards solely as a means of payment, making purchases with a credit card but repaying the outstanding balance fully within the allowable time limit. 3 In contrast, the borrower makes purchases with a credit card but does not fully repay the amount spent when it is due, thus facing interest charges on unpaid balances. The series displayed in Chart 1 does not discriminate between borrowing and spending, given that it tracks current balances on credit cards rather than balances outstanding after the last payment. 4 Does the growth in credit card balances over the past 15 years reflect increased use of credit cards for borrowing or for spending? The answer to this question can have implications for financial stability. For instance, excessive accumulation of unsecured interest-bearing credit card debt could represent a 1. A similar trend is found in chartered bank data. See Statistics Canada CANSIM Table Equifax provides a broader measure that is not affected by securitization and changes to accounting due to implementation of International Financial Reporting Standards. 2. Balances normalized by household income and per capita balances display a similar pattern, namely, increasing up to the crisis period and weaker post-crisis. 3. Technically, these types of users are enjoying some interest-free borrowing (referred as the float ) between the time they make a purchase and when they repay their balance after they receive their bill. 4. This is also true of credit card balances reported by chartered banks to the Office of the Superintendent of Financial Institutions (OSFI) and reported in Statistics Canada CANSIM Table

6 3 vulnerability for the financial system if it is concentrated among households with less-stable incomes. On the other hand, survey results have shown that households have increasingly been using credit cards as a means of payment. 5 Growing credit card balances because high-income households use credit cards as means of payment (for convenience or rewards) would not be a concern for financial stability. To distinguish between credit card usage by borrowers and that by convenience users, we need to examine how much a household repays on its credit card balances. Fortunately, Ipsos Reid s Canadian Financial Monitor (CFM) survey provides information that can help us distinguish between these two possibilities. 2. Dual Usage in Household-Level Data (CFM) In the CFM survey questionnaire, credit card owners are asked to consult their most recent credit card statements and report both their spending over the past month and the balances outstanding after making their latest payment. Using this information, Chart 2 documents the evolution of average balances and spending (per household with at least one credit card). We find that, over the period, average credit card spending per household increased by roughly one-third. In contrast, after peaking around 2010, average balances have been declining since then and, as of 2014, stand at levels observed in These results suggest that the aggregate trend observed in Chart 1 is most likely due to credit cards being used increasingly as a convenient method of payment rather than as a source of short-term borrowing. The decline in credit card borrowing implies that households have been switching to other types of consumer debt In this note, we do not examine the household s choice of a payment method. Henry, Huynh and Shen (2015) report that the share of credit cards among the payment choices reached 31 per cent in terms of volume and 46 per cent in terms of value in This is a 12 per cent and 5 per cent increase, respectively, compared with The growth has been attributed to the drop in the cash and debit share. For more information, see Henry, Huynh and Shen (2015). 6. Balances is a stock variable and includes items other than spending, such as balances carried from previous periods as well as transfers. Spending is a flow, measured on a monthly basis, and is only a fraction of accumulated balances. 7. Crawford and Faruqui ( ) argue that secured personal lines of credit have been the main drivers behind the growth of consumer credit since the mid-1990s, partly reflecting a substitution away from credit cards. For more information, see Crawford and Faruqui ( ).

7 4 Chart 2: Credit cards are increasingly being used as a payment method rather than a loan product Outstanding balances and spending per household with a credit card Means, constant 2014 dollars $ 3,500 3,000 2,500 2,000 1,500 1, Outstanding balances Spending Last observation: 2014 Analyzing the microdata, several stylized facts emerge that confirm our conjecture that convenience users are growing in importance, for several reasons. First, the majority of credit card owners in Canada do not carry any credit card debt and are therefore classified as convenience users. 8 Indeed, the proportion of such households grew from 48 per cent in the early 2000s to 55 per cent in recent years (Chart 3). Second, over time, convenience users have been spending more than borrowers (Chart 4). This result is robust to controlling for differences in income between convenience users and borrowers (see Chart A-1 in the Appendix). Third, the average balances carried by borrowers have dropped following the crisis. The microdata therefore suggest that convenience users are growing in importance when explaining movements in aggregate credit card balances. In the next section, we expand our understanding of the drivers behind credit card usage by controlling for some pertinent household characteristics. We use our results to explore vulnerabilities associated with credit card borrowing. 8. Among convenience users, a small number of households do not report any spending and are likely to resort to credit cards only in emergency situations.

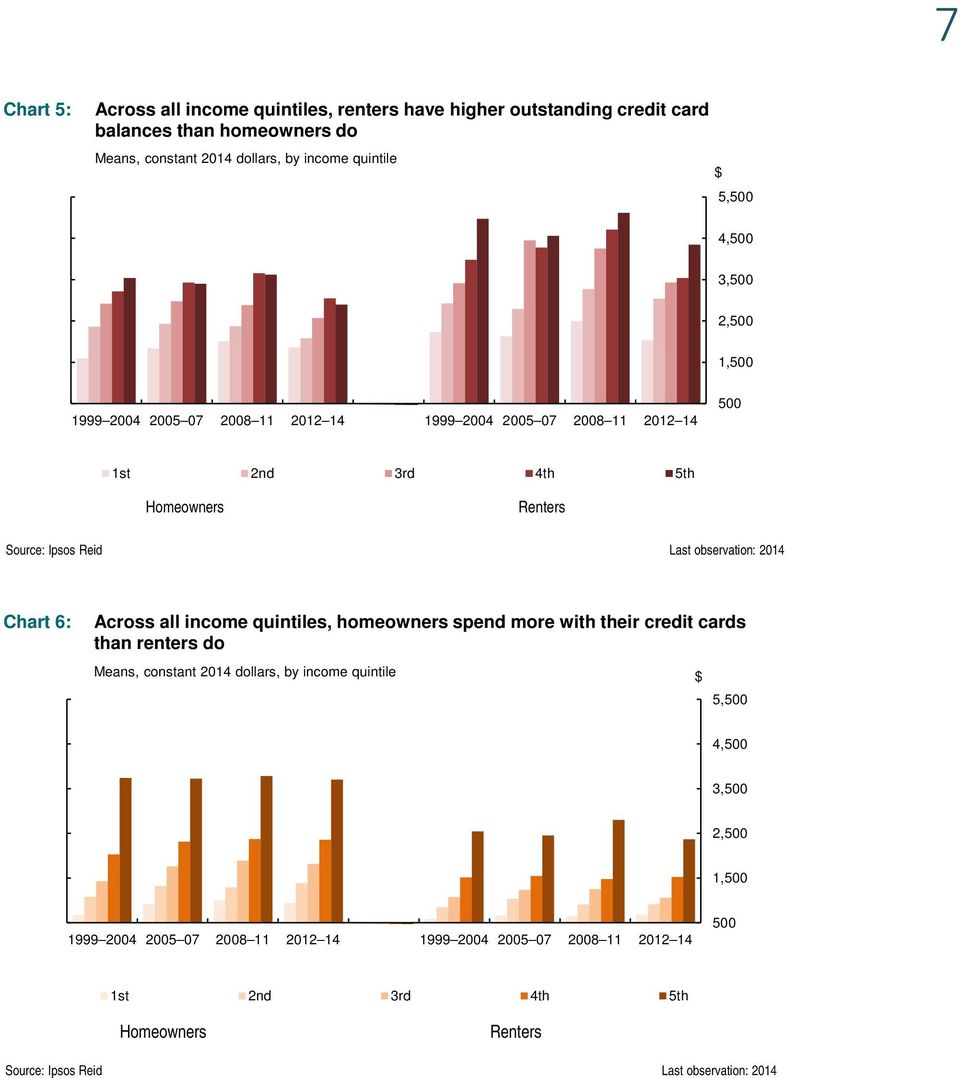

8 5 Chart 3: Share of convenience users increased compared with the early 2000s Proportion of households with no credit card debt % 55 Chart 4: Convenience users are incresingly spending more compared with borrowers $ 7,000 Means, constant 2014 dollars $ 3, ,000 5,000 2,500 2,000 1, Last observation: ,000 1, Average balances of borrowers (left axis) Average spending of convenience users (right axis) Average spending of borrowers (right axis) Last observation: Variety of Credit Card Usage in CFM and Potential Vulnerabilities Among the household characteristics likely to affect the use of credit cards are household income, age of household head, homeownership status and region of residence. Table A-1 summarizes information on the incidence of convenience users, as well as average balances and spending across these dimensions. 9 For the rest of this note, we focus on home ownership and income since they offer interesting insights on the characteristics of credit card borrowers and the extent to which credit card borrowing can pose a vulnerability to the financial system. Chart 5 compares outstanding credit card balances of homeowners and renters across different income quintiles while Chart 6 compares their spending. Both charts reveal significant differences in credit card usage by these different households. While borrowing and spending increase with income for both renters and homeowners, 10 renters borrow more, but spend less, than homeowners. Overall, households with the highest outstanding balances are highincome renters while spending is much more concentrated among high-income homeowners. The difference in borrowing across renters and homeowners reflects differences in access to alternative sources of short-term borrowing by these two groups of households. Homeowners can borrow against their house and access cheaper forms of borrowing, such as home equity lines of credit (HELOCs), while renters are more likely to rely on credit cards as a source of borrowing. The concentration of credit card debt among high-income renters, who have a greater ability to repay their debt given their higher income, is thus a natural outcome reflecting the constraints that these households face. Significantly, renters are also more likely to own low-interest credit cards. For instance, using the Methods-of- Payment Survey data, Henry, Huynh and Shen (2015) find that 16 per cent of renters have credit cards 9. Interesting observations in Table A-1 include households in Alberta and households aged 35 to 54 being among the heaviest borrowers on credit cards. Further, the incidence of convenience users among older households (age above 65) has been declining and their credit card balances have been growing over time, unlike other age groups. These are issues for further research. 10. Although, the top income quintile of homeowners borrows about the same as the fourth income quintile of homeowners.

9 6 with interest rates below 5 per cent compared with 11 per cent of home owners. 11 This moderates the extent to which credit card borrowing by these groups of households would represent a vulnerability for the financial system. Closer examination of Chart 5 and Chart 6 shows a broad decline in borrowing in the most recent years across all income groups for both renters and homeowners while there is no decline in spending. This observation further supports the view that spending via credit cards is growing in importance relative to borrowing. To summarize, credit cards have increasingly been used by Canadian households as a convenient payment method. Credit card borrowing has been declining and its pattern at the household level reflects the natural constraints that households face. Continued monitoring and deeper analysis is nevertheless warranted as credit card borrowing is risky unsecured credit at high interest rates. 11. Note that credit card interest rates were not available in the CFM before Between 2012 and 2014, highly indebted households (with credit card debt over $10,000) paid an average annual interest rate of 16.3 per cent compared with 18.3 per cent for convenience users. In the period, households admitting that a low interest rate was one of the features of their credit card had, on average, balances twice as high as those of the rest of the respondents.

10 7 Chart 5: Across all income quintiles, renters have higher outstanding credit card balances than homeowners do Means, constant 2014 dollars, by income quintile $ 5,500 4,500 3,500 2,500 1, st 2nd 3rd 4th 5th Homeowners Renters Last observation: 2014 Chart 6: Across all income quintiles, homeowners spend more with their credit cards than renters do Means, constant 2014 dollars, by income quintile $ 5,500 4,500 3,500 2,500 1, st 2nd 3rd 4th 5th Homeowners Renters Last observation: 2014

11 8 Appendix: Chart A-1: Covenience users spend more than borrowers do after controlling for differences in income Normalized by average household income for a given group 9.0 % % Average balances of borrowers (left axis) Average spending of convenience users (right axis) Average spending of borrowers (right axis) Last observation: 2014

Average spending of borrowers (right axis) Last observation:")

12 Table A-1: Heterogeneity of credit card usage in Canadian Financial Monitor data Incidence of convenience users (%) Average outstanding balances ($) Average spending ($) Region BC , , , , , , , , , ,202.9 AB , , , , , , , , , ,370.4 SK/MB , , , , , , , , , ,963.3 ON , , , , , , , , , ,017.1 QC , , , , , , , , , ,653.1 ATL , , , , , , , , , ,492.2 Income quintile 1st , , , , , nd , , , , , , , , , rd , , , , , , , , , , th , , , , , , , , , , th , , , , , , , , , ,599.3 Age < , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , ,993.1 >= , , , , , , , , , ,667.6 Home ownership Owner , , , , , , , , , ,279.6 Renter , , , , , , , ,020.1 Note: Constant 2014 dollars

13 References Crawford, A. and U. Faruqui What Explains Trends in Household Debt in Canada? Bank of Canada Review (Winter): Henry, C. S., K. P. Huynh and Q. R. Shen Methods-of-Payment Survey Results. Bank of Canada Discussion Paper No

What Explains Trends in Household Debt in Canada?

3 What Explains Trends in Household Debt in Canada? Allan Crawford, Adviser, and Umar Faruqui, Financial Stability Department The aggregate debt-to-income ratio of Canadian households has trended upward

3 What Explains Trends in Household Debt in Canada? Allan Crawford, Adviser, and Umar Faruqui, Financial Stability Department The aggregate debt-to-income ratio of Canadian households has trended upward

The Bank of Canada s Analytic Framework for Assessing the Vulnerability of the Household Sector

The Bank of Canada s Analytic Framework for Assessing the Vulnerability of the Household Sector Ramdane Djoudad INTRODUCTION Changes in household debt-service costs as a share of income i.e., the debt-service

The Bank of Canada s Analytic Framework for Assessing the Vulnerability of the Household Sector Ramdane Djoudad INTRODUCTION Changes in household debt-service costs as a share of income i.e., the debt-service

An Approach to Stress Testing the Canadian Mortgage Portfolio

Financial System Review December 2007 An Approach to Stress Testing the Canadian Mortgage Portfolio Moez Souissi I n Canada, residential mortgage loans account for close to 47 per cent of the total loan

Financial System Review December 2007 An Approach to Stress Testing the Canadian Mortgage Portfolio Moez Souissi I n Canada, residential mortgage loans account for close to 47 per cent of the total loan

The Credit Card Report May 4 The Credit Card Report May 4 Contents Visa makes no representations or warranties about the accuracy or suitability of the information or advice provided. You use the information

The Credit Card Report May 4 The Credit Card Report May 4 Contents Visa makes no representations or warranties about the accuracy or suitability of the information or advice provided. You use the information

SOURCES OF SME BUSINESS DEBT FINANCING IN ATLANTIC CANADA. By Theresa Shutt & Pierre Vanasse The Conference Board of Canada Ottawa, March 1999

SOURCES OF SME BUSINESS DEBT FINANCING IN ATLANTIC CANADA By Theresa Shutt & Pierre Vanasse The Conference Board of Canada Ottawa, March 1999 TABLE OF CONTENT Overview and Executive Summary....1 Introduction...8

SOURCES OF SME BUSINESS DEBT FINANCING IN ATLANTIC CANADA By Theresa Shutt & Pierre Vanasse The Conference Board of Canada Ottawa, March 1999 TABLE OF CONTENT Overview and Executive Summary....1 Introduction...8

FEDERAL RESERVE BULLETIN

FEDERAL RESERVE BULLETIN VOLUME 38 May 1952 NUMBER 5 Business expenditures for new plant and equipment and for inventory reached a new record level in 1951 together, they exceeded the previous year's total

FEDERAL RESERVE BULLETIN VOLUME 38 May 1952 NUMBER 5 Business expenditures for new plant and equipment and for inventory reached a new record level in 1951 together, they exceeded the previous year's total

Short Form Description / Sommaire: Carrying on a prescribed activity without or contrary to a licence

NOTICE OF VIOLATION (Corporation) AVIS DE VIOLATION (Société) Date of Notice / Date de l avis: August 29, 214 AMP Number / Numéro de SAP: 214-AMP-6 Violation committed by / Violation commise par : Canadian

NOTICE OF VIOLATION (Corporation) AVIS DE VIOLATION (Société) Date of Notice / Date de l avis: August 29, 214 AMP Number / Numéro de SAP: 214-AMP-6 Violation committed by / Violation commise par : Canadian

Appendix. Debt Position and Debt Management

Appendix Debt Position and Debt Management BUDGET '97 BUILDING ALBERTA TOGETHER Table of Contents Debt Position and Debt Management... 349 The Consolidated Balance Sheet and Net Debt... 350 Liabilities...

Appendix Debt Position and Debt Management BUDGET '97 BUILDING ALBERTA TOGETHER Table of Contents Debt Position and Debt Management... 349 The Consolidated Balance Sheet and Net Debt... 350 Liabilities...

Personnalisez votre intérieur avec les revêtements imprimés ALYOS design

Plafond tendu à froid ALYOS technology ALYOS technology vous propose un ensemble de solutions techniques pour vos intérieurs. Spécialiste dans le domaine du plafond tendu, nous avons conçu et développé

Plafond tendu à froid ALYOS technology ALYOS technology vous propose un ensemble de solutions techniques pour vos intérieurs. Spécialiste dans le domaine du plafond tendu, nous avons conçu et développé

OBSERVATION. TD Economics ARE CANADIANS PREPARED FOR HIGHER INTEREST RATES?

OBSERVATION TD Economics May, ARE CANADIANS PREPARED FOR HIGHER INTEREST RATES? Highlights With the Bank of Canada recently signalling that interest rates may rise sooner than many were anticipating, the

OBSERVATION TD Economics May, ARE CANADIANS PREPARED FOR HIGHER INTEREST RATES? Highlights With the Bank of Canada recently signalling that interest rates may rise sooner than many were anticipating, the

êéëé~êåü=üáöüäáöüí House Prices, Borrowing Against Home Equity, and Consumer Expenditures lîéêîáéï eçìëé=éêáåéë=~åç=äçêêçïáåö ~Ö~áåëí=ÜçãÉ=Éèìáíó

êéëé~êåü=üáöüäáöüí January 2004 Socio-economic Series 04-006 House Prices, Borrowing Against Home Equity, and Consumer Expenditures lîéêîáéï The focus of the study is to examine the link between house

êéëé~êåü=üáöüäáöüí January 2004 Socio-economic Series 04-006 House Prices, Borrowing Against Home Equity, and Consumer Expenditures lîéêîáéï The focus of the study is to examine the link between house

Household Borrowing and Spending in Canada

16 Household Borrowing and Spending in Canada Jeannine Bailliu, Katsiaryna Kartashova and Césaire Meh, Canadian Economic Analysis Department The sizable increase in the ratio of household debt to income

16 Household Borrowing and Spending in Canada Jeannine Bailliu, Katsiaryna Kartashova and Césaire Meh, Canadian Economic Analysis Department The sizable increase in the ratio of household debt to income

Student Loan Borrowing and Repayment Trends, 2015

Student Loan Borrowing and Repayment Trends, 2015 April 16, 2015 Andrew Haughwout, Donghoon Lee, Joelle Scally, Wilbert van der Klaauw The views presented here are those of the authors and do not necessarily

Student Loan Borrowing and Repayment Trends, 2015 April 16, 2015 Andrew Haughwout, Donghoon Lee, Joelle Scally, Wilbert van der Klaauw The views presented here are those of the authors and do not necessarily

Archived Content. Contenu archivé

ARCHIVED - Archiving Content ARCHIVÉE - Contenu archivé Archived Content Contenu archivé Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject

ARCHIVED - Archiving Content ARCHIVÉE - Contenu archivé Archived Content Contenu archivé Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject

Financial vulnerability of mortgage-indebted households in New Zealand evidence from the Household Economic Survey

ARTICLES Financial vulnerability of mortgage-indebted in New Zealand evidence from the Household Economic Survey Mizuho Kida Aggregate household debt more than doubled between 1 and 8, alongside similarly

ARTICLES Financial vulnerability of mortgage-indebted in New Zealand evidence from the Household Economic Survey Mizuho Kida Aggregate household debt more than doubled between 1 and 8, alongside similarly

Defining Housing Equity Withdrawal

Housing Reserve Equity Bank of Australia Bulletin February 23 Housing Equity The increase in housing prices in recent years has contributed to rising household wealth and has helped to underpin continued

Housing Reserve Equity Bank of Australia Bulletin February 23 Housing Equity The increase in housing prices in recent years has contributed to rising household wealth and has helped to underpin continued

the Québec government s debt

the Québec government s debt The Québec Government Debt Legal deposit - Bibliothèque et Archives nationales du Québec December 2007 ISBN 978-2-550-51549-4 (Print) ISBN 978-2-550-51550-0 (PDF) Gouvernement

the Québec government s debt The Québec Government Debt Legal deposit - Bibliothèque et Archives nationales du Québec December 2007 ISBN 978-2-550-51549-4 (Print) ISBN 978-2-550-51550-0 (PDF) Gouvernement

Banks Funding Costs and Lending Rates

Cameron Deans and Chris Stewart* Over the past year, lending rates and funding costs have both fallen in absolute terms but have risen relative to the cash rate. The rise in funding costs, relative to

Cameron Deans and Chris Stewart* Over the past year, lending rates and funding costs have both fallen in absolute terms but have risen relative to the cash rate. The rise in funding costs, relative to

The U.S. Housing Crisis and the Risk of Recession. 1. Recent Developments in the U.S. Housing Market Falling Housing Prices

Economic Spotlight ALBERTA FINANCE Budget and Fiscal Planning March 4, 2008 The U.S. Housing Crisis and the Risk of Recession Summary The worsening U.S. housing slump is spreading to the broader economy

Economic Spotlight ALBERTA FINANCE Budget and Fiscal Planning March 4, 2008 The U.S. Housing Crisis and the Risk of Recession Summary The worsening U.S. housing slump is spreading to the broader economy

Personal debt ON LABOUR AND INCOME

ON LABOUR AND INCOME Personal debt Although the economy and population are almost times the size of s, the two countries show several similarities. Both have relatively high per-capita income and living

ON LABOUR AND INCOME Personal debt Although the economy and population are almost times the size of s, the two countries show several similarities. Both have relatively high per-capita income and living

BILL C-665 PROJET DE LOI C-665 C-665 C-665 HOUSE OF COMMONS OF CANADA CHAMBRE DES COMMUNES DU CANADA

C-665 C-665 Second Session, Forty-first Parliament, Deuxième session, quarante et unième législature, HOUSE OF COMMONS OF CANADA CHAMBRE DES COMMUNES DU CANADA BILL C-665 PROJET DE LOI C-665 An Act to

C-665 C-665 Second Session, Forty-first Parliament, Deuxième session, quarante et unième législature, HOUSE OF COMMONS OF CANADA CHAMBRE DES COMMUNES DU CANADA BILL C-665 PROJET DE LOI C-665 An Act to

The Effects of Funding Costs and Risk on Banks Lending Rates

The Effects of Funding Costs and Risk on Banks Lending Rates Daniel Fabbro and Mark Hack* After falling for over a decade, the major banks net interest margins appear to have stabilised in a relatively

The Effects of Funding Costs and Risk on Banks Lending Rates Daniel Fabbro and Mark Hack* After falling for over a decade, the major banks net interest margins appear to have stabilised in a relatively

Actuarial Report. on the CANADA STUDENT LOANS PROGRAM

Actuarial Report on the CANADA STUDENT LOANS PROGRAM as at 31 July 2001 Office of the Superintendent of Financial Institutions Office of the Chief Actuary Bureau du surintendant des institutions financières

Actuarial Report on the CANADA STUDENT LOANS PROGRAM as at 31 July 2001 Office of the Superintendent of Financial Institutions Office of the Chief Actuary Bureau du surintendant des institutions financières

Each of the 16 Canadian medical schools has a psychiatry. Canadian Psychiatry Residency Training Programs: A Glance at the Management Structure

Brief Communication Canadian Psychiatry Residency Training Programs: A Glance at the Management Structure Louis T van Zyl, MB, ChB, MMedPsych, FRCPC 1, Paul R Davidson, PhD, CPsych 2 Objectives: To describe

Brief Communication Canadian Psychiatry Residency Training Programs: A Glance at the Management Structure Louis T van Zyl, MB, ChB, MMedPsych, FRCPC 1, Paul R Davidson, PhD, CPsych 2 Objectives: To describe

OSC EXEMPT MARKET REVIEW OSC NOTICE 45-712 APPENDIX C CAPITAL RAISING IN CANADA AND THE ONTARIO EXEMPT MARKET

OSC EXEMPT MARKET REVIEW OSC NOTICE 45-712 APPENDIX C CAPITAL RAISING IN CANADA AND THE ONTARIO EXEMPT MARKET 1 1. Introduction As a securities regulator, the Ontario Securities Commission is committed

OSC EXEMPT MARKET REVIEW OSC NOTICE 45-712 APPENDIX C CAPITAL RAISING IN CANADA AND THE ONTARIO EXEMPT MARKET 1 1. Introduction As a securities regulator, the Ontario Securities Commission is committed

Survey on use of Taser International 21ft cartridges

ARCHIVED - Archiving Content ARCHIVÉE - Contenu archivé Archived Content Contenu archivé Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject

ARCHIVED - Archiving Content ARCHIVÉE - Contenu archivé Archived Content Contenu archivé Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject

Archived Content. Contenu archivé

ARCHIVED - Archiving Content ARCHIVÉE - Contenu archivé Archived Content Contenu archivé Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject

ARCHIVED - Archiving Content ARCHIVÉE - Contenu archivé Archived Content Contenu archivé Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject

Archived Content. Contenu archivé

ARCHIVED - Archiving Content ARCHIVÉE - Contenu archivé Archived Content Contenu archivé Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject

ARCHIVED - Archiving Content ARCHIVÉE - Contenu archivé Archived Content Contenu archivé Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject

Presentation of the Gross External Debt Position

4 Presentation of the Gross External Debt Position Introduction 4. This chapter provides a table for the presentation of the gross external debt position and related memorandum tables. Data compiled using

4 Presentation of the Gross External Debt Position Introduction 4. This chapter provides a table for the presentation of the gross external debt position and related memorandum tables. Data compiled using

SUBJECT CANADA CUSTOMS INVOICE REQUIREMENTS. This Memorandum explains the customs invoice requirements for commercial goods imported into Canada.

MEMORANDUM D1-4-1 Ottawa, July 10, 2000 SUBJECT CANADA CUSTOMS INVOICE REQUIREMENTS This Memorandum explains the customs invoice requirements for commercial goods imported into Canada. Legislation For

MEMORANDUM D1-4-1 Ottawa, July 10, 2000 SUBJECT CANADA CUSTOMS INVOICE REQUIREMENTS This Memorandum explains the customs invoice requirements for commercial goods imported into Canada. Legislation For

Unrealized Gains in Stocks from the Viewpoint of Investment Risk Management

Unrealized Gains in Stocks from the Viewpoint of Investment Risk Management Naoki Matsuyama Investment Administration Department, The Neiji Mutual Life Insurance Company, 1-1 Marunouchi, 2-chome, Chiyoda-ku,

Unrealized Gains in Stocks from the Viewpoint of Investment Risk Management Naoki Matsuyama Investment Administration Department, The Neiji Mutual Life Insurance Company, 1-1 Marunouchi, 2-chome, Chiyoda-ku,

Small Business Lending *

Reserve Small Business Bank of Lending Australia Bulletin Small Business Lending * These notes were prepared in response to a request from the House of Representatives Standing Committee on Financial Institutions

Reserve Small Business Bank of Lending Australia Bulletin Small Business Lending * These notes were prepared in response to a request from the House of Representatives Standing Committee on Financial Institutions

Basel II, Pillar 3 Disclosure for Sun Life Financial Trust Inc.

Basel II, Pillar 3 Disclosure for Sun Life Financial Trust Inc. Introduction Basel II is an international framework on capital that applies to deposit taking institutions in many countries, including Canada.

Basel II, Pillar 3 Disclosure for Sun Life Financial Trust Inc. Introduction Basel II is an international framework on capital that applies to deposit taking institutions in many countries, including Canada.

Economic Impacts of MLS Home Sales and Purchases in Canada and the Provinces

Economic Impacts of MLS Home Sales and Purchases in Canada and the Provinces Economic Impacts of MLS Home Sales and Purchases in Canada and the Provinces Prepared for: The Canadian Real Estate Association

Economic Impacts of MLS Home Sales and Purchases in Canada and the Provinces Economic Impacts of MLS Home Sales and Purchases in Canada and the Provinces Prepared for: The Canadian Real Estate Association

Measuring Student Debt and Its Performance

Federal Reserve Bank of New York Staff Reports Measuring Student Debt and Its Performance Meta Brown Andrew Haughwout Donghoon Lee Joelle Scally Wilbert van der Klaauw Staff Report No. 668 April 2014 This

Federal Reserve Bank of New York Staff Reports Measuring Student Debt and Its Performance Meta Brown Andrew Haughwout Donghoon Lee Joelle Scally Wilbert van der Klaauw Staff Report No. 668 April 2014 This

Information. Canada s Life and Health Insurers. Canada s Financial Services Sector. Overview

Information Canada s Life and Health Insurers Canada s Financial Services Sector September 2002 Overview Canada s life and health insurance industry comprises 120 firms, down from 163 companies in 1990,

Information Canada s Life and Health Insurers Canada s Financial Services Sector September 2002 Overview Canada s life and health insurance industry comprises 120 firms, down from 163 companies in 1990,

In this chapter, we build on the basic knowledge of how businesses

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

Report to the Congress on the Profitability of Credit Card Operations of Depository Institutions

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM Report to the Congress on the Profitability of Credit Card Operations of Depository Institutions Submitted to the Congress pursuant to section 8 of the

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM Report to the Congress on the Profitability of Credit Card Operations of Depository Institutions Submitted to the Congress pursuant to section 8 of the

MANITOBA TRADE AND INVESTMENT CORPORATION ANNUAL REPORT 2012/13 SOCIÉTÉ DU COMMERCE ET DE L'INVESTISSEMENT DU MANITOBA RAPPORT ANNUEL 2012/13

MANITOBA TRADE AND INVESTMENT CORPORATION ANNUAL REPORT 2012/13 SOCIÉTÉ DU COMMERCE ET DE L'INVESTISSEMENT DU MANITOBA RAPPORT ANNUEL 2012/13 Board of Directors Conseil d administration Hugh Eliasson Chair

MANITOBA TRADE AND INVESTMENT CORPORATION ANNUAL REPORT 2012/13 SOCIÉTÉ DU COMMERCE ET DE L'INVESTISSEMENT DU MANITOBA RAPPORT ANNUEL 2012/13 Board of Directors Conseil d administration Hugh Eliasson Chair

International Diversification and Exchange Rates Risk. Summary

International Diversification and Exchange Rates Risk Y. K. Ip School of Accounting and Finance, University College of Southern Queensland, Toowoomba, Queensland 4350, Australia Summary The benefits arisen

International Diversification and Exchange Rates Risk Y. K. Ip School of Accounting and Finance, University College of Southern Queensland, Toowoomba, Queensland 4350, Australia Summary The benefits arisen

10 mistakes not to make in France!

10 mistakes not to make in France! Have you ever heard of false friends? No? Well, let us fix that! False friends are words that are identical in English and in French and so mistakenly lead you to think

10 mistakes not to make in France! Have you ever heard of false friends? No? Well, let us fix that! False friends are words that are identical in English and in French and so mistakenly lead you to think

Guideline. Commercial Lending Criteria. No: E-2 Date: June 1992

Canada Bureau du surintendant des institutions financières Canada 255 Albert Street 255, rue Albert Ottawa, Canada Ottawa, Canada K1A 0H2 K1A 0H2 Guideline Subject: No: E-2 Date: June 1992 This guideline

Canada Bureau du surintendant des institutions financières Canada 255 Albert Street 255, rue Albert Ottawa, Canada Ottawa, Canada K1A 0H2 K1A 0H2 Guideline Subject: No: E-2 Date: June 1992 This guideline

The Bank of Canada s Senior Loan Officer Survey

The Bank of Canada s Senior Loan Officer Survey Umar Faruqui, Paul Gilbert, and Wendy Kei, Department of Monetary and Financial Analysis Since 1999, the Bank of Canada has been conducting a quarterly survey

The Bank of Canada s Senior Loan Officer Survey Umar Faruqui, Paul Gilbert, and Wendy Kei, Department of Monetary and Financial Analysis Since 1999, the Bank of Canada has been conducting a quarterly survey

Sources of Short-Term Financing C H A P T E R E I G H T

Sources of -Term Financing C H A P T E R E I G H T Figure 8-1 Structure of corporate debt, 1998 PPT 8-1 35% 30% 25% 20% 15% 10% 5% 0% Accounts payable Bank loans Other short term loans term paper Bonds

Sources of -Term Financing C H A P T E R E I G H T Figure 8-1 Structure of corporate debt, 1998 PPT 8-1 35% 30% 25% 20% 15% 10% 5% 0% Accounts payable Bank loans Other short term loans term paper Bonds

Bond Mutual Funds. a guide to. A bond mutual fund is an investment company. that pools money from shareholders and invests

a guide to Bond Mutual Funds A bond mutual fund is an investment company that pools money from shareholders and invests primarily in a diversified portfolio of bonds. Table of Contents What Is a Bond?...

a guide to Bond Mutual Funds A bond mutual fund is an investment company that pools money from shareholders and invests primarily in a diversified portfolio of bonds. Table of Contents What Is a Bond?...

Household debt and consumption in the UK. Evidence from UK microdata. 10 March 2015

Household debt and consumption in the UK Evidence from UK microdata 10 March 2015 Disclaimer This presentation does not necessarily represent the views of the Bank of England or members of the Monetary

Household debt and consumption in the UK Evidence from UK microdata 10 March 2015 Disclaimer This presentation does not necessarily represent the views of the Bank of England or members of the Monetary

Canadian Consumer Credit Trends. Q3 2015 Prepared by: Equifax Analytical Services

Canadian Consumer Credit Trends Q3 2015 Prepared by: Equifax Analytical Services About Equifax Inc. Equifax is a global leader in consumer, commercial and workforce information solutions that provide businesses

Canadian Consumer Credit Trends Q3 2015 Prepared by: Equifax Analytical Services About Equifax Inc. Equifax is a global leader in consumer, commercial and workforce information solutions that provide businesses

GENWORTH MI CANADA INC.

Condensed Consolidated Interim Financial Statements (In Canadian dollars) GENWORTH MI CANADA INC. Three and six months ended June 30, 2015 and 2014 Condensed Consolidated Interim Statements of Financial

Condensed Consolidated Interim Financial Statements (In Canadian dollars) GENWORTH MI CANADA INC. Three and six months ended June 30, 2015 and 2014 Condensed Consolidated Interim Statements of Financial

EXTERNAL DEBT AND LIABILITIES OF INDUSTRIAL COUNTRIES. Mark Rider. Research Discussion Paper 9405. November 1994. Economic Research Department

EXTERNAL DEBT AND LIABILITIES OF INDUSTRIAL COUNTRIES Mark Rider Research Discussion Paper 9405 November 1994 Economic Research Department Reserve Bank of Australia I would like to thank Sally Banguis

EXTERNAL DEBT AND LIABILITIES OF INDUSTRIAL COUNTRIES Mark Rider Research Discussion Paper 9405 November 1994 Economic Research Department Reserve Bank of Australia I would like to thank Sally Banguis

VIREMENTS BANCAIRES INTERNATIONAUX

Les clients de Finexo peuvent financer leur compte en effectuant des virements bancaires depuis de nombreuses banques dans le monde. Consultez la liste ci-dessous pour des détails sur les virements bancaires

Les clients de Finexo peuvent financer leur compte en effectuant des virements bancaires depuis de nombreuses banques dans le monde. Consultez la liste ci-dessous pour des détails sur les virements bancaires

HAS FINANCE BECOME TOO EXPENSIVE? AN ESTIMATION OF THE UNIT COST OF FINANCIAL INTERMEDIATION IN EUROPE 1951-2007

HAS FINANCE BECOME TOO EXPENSIVE? AN ESTIMATION OF THE UNIT COST OF FINANCIAL INTERMEDIATION IN EUROPE 1951-2007 IPP Policy Briefs n 10 June 2014 Guillaume Bazot www.ipp.eu Summary Finance played an increasing

HAS FINANCE BECOME TOO EXPENSIVE? AN ESTIMATION OF THE UNIT COST OF FINANCIAL INTERMEDIATION IN EUROPE 1951-2007 IPP Policy Briefs n 10 June 2014 Guillaume Bazot www.ipp.eu Summary Finance played an increasing

Impact of Debt on Ontario Swine Farms

Impact of Debt on Ontario Swine Farms Prepared by: Randy Duffy and Ken McEwan University of Guelph, Ridgetown Campus November 2011 Funding support for this project. This project is funded in part through

Impact of Debt on Ontario Swine Farms Prepared by: Randy Duffy and Ken McEwan University of Guelph, Ridgetown Campus November 2011 Funding support for this project. This project is funded in part through

Household Finance and Consumption Survey

An Phríomh-Oifig Staidrimh Central Statistics Office Household Finance and Consumption Survey 2013 Published by the Stationery Office, Dublin, Ireland. Available from: Central Statistics Office, Information

An Phríomh-Oifig Staidrimh Central Statistics Office Household Finance and Consumption Survey 2013 Published by the Stationery Office, Dublin, Ireland. Available from: Central Statistics Office, Information

AUDITOR S REPORT. To the Members of the Legislative Assembly Province of Saskatchewan

AUDITOR S REPORT To the Members of the Legislative Assembly Province of Saskatchewan We have audited the statement of financial position of the Education Infrastructure Financing Corporation as at March

AUDITOR S REPORT To the Members of the Legislative Assembly Province of Saskatchewan We have audited the statement of financial position of the Education Infrastructure Financing Corporation as at March

Preparing Agricultural Financial Statements

Preparing Agricultural Financial Statements Thoroughly understanding your business financial performance is critical for success in today s increasingly competitive agricultural environment. Accurate records

Preparing Agricultural Financial Statements Thoroughly understanding your business financial performance is critical for success in today s increasingly competitive agricultural environment. Accurate records

NATIONAL SURVEY OF HOME EQUITY LOANS

NATIONAL SURVEY OF HOME EQUITY LOANS Richard T. Curtin Director, Surveys of Consumers Survey Research Center The October 1998 WP51 The 1988, 1994, and 1997 National Surveys of Home Equity Loans were sponsored

NATIONAL SURVEY OF HOME EQUITY LOANS Richard T. Curtin Director, Surveys of Consumers Survey Research Center The October 1998 WP51 The 1988, 1994, and 1997 National Surveys of Home Equity Loans were sponsored

ON LABOUR AND INCOME. JUNE 2002 Vol. 3, No. 6 HOUSING: AN INCOME ISSUE PENSIONS: IMMIGRANTS AND VISIBLE MINORITIES.

Catalogue no. 75-001-XIE ON LABOUR AND INCOME JUNE 2002 Vol. 3, No. 6 HOUSING: AN INCOME ISSUE PENSIONS: IMMIGRANTS AND VISIBLE MINORITIES Statistics Canada Statistique Canada Sophie Lefebvre HOUSING IS

Catalogue no. 75-001-XIE ON LABOUR AND INCOME JUNE 2002 Vol. 3, No. 6 HOUSING: AN INCOME ISSUE PENSIONS: IMMIGRANTS AND VISIBLE MINORITIES Statistics Canada Statistique Canada Sophie Lefebvre HOUSING IS

MasterIndex Report: Grocery Shopping Experience

2008 MasterIndex Report: Checking Out the Canadian Grocery Shopping Experience 2008 MasterIndex Report: Checking Out the Canadian Grocery Shopping Experience [ 1 ] 2008 MasterIndex Report Grocery shopping

2008 MasterIndex Report: Checking Out the Canadian Grocery Shopping Experience 2008 MasterIndex Report: Checking Out the Canadian Grocery Shopping Experience [ 1 ] 2008 MasterIndex Report Grocery shopping

Labour Market Outcomes of Young Postsecondary Graduates, 2005 to 2012

Catalogue no. 11-626-X No. 050 ISSN 1927-503X ISBN 978-0-660-03237-5 Economic Insights Labour Market Outcomes of Young Postsecondary Graduates, 2005 to 2012 by Kristyn Frank, Marc Frenette, and René Morissette

Catalogue no. 11-626-X No. 050 ISSN 1927-503X ISBN 978-0-660-03237-5 Economic Insights Labour Market Outcomes of Young Postsecondary Graduates, 2005 to 2012 by Kristyn Frank, Marc Frenette, and René Morissette

18 ECB STYLISED FACTS OF MONEY AND CREDIT OVER THE BUSINESS CYCLE

Box 1 STYLISED FACTS OF MONEY AND CREDIT OVER THE BUSINESS CYCLE Over the past three decades, the growth rates of MFI loans to the private sector and the narrow monetary aggregate M1 have displayed relatively

Box 1 STYLISED FACTS OF MONEY AND CREDIT OVER THE BUSINESS CYCLE Over the past three decades, the growth rates of MFI loans to the private sector and the narrow monetary aggregate M1 have displayed relatively

DHI a.s. Na Vrsich 51490/5, 100 00, Prague 10, Czech Republic ( [email protected], [email protected] )

") NOVATECH Rehabilitation strategies in wastewater networks as combination of operational, property and model information Stratégies de réhabilitation des réseaux d'égouts combinant des données d exploitation,

NOVATECH Rehabilitation strategies in wastewater networks as combination of operational, property and model information Stratégies de réhabilitation des réseaux d'égouts combinant des données d exploitation,

A PLAN FOR A DEBT-FREE ALBERTA

A PLAN FOR A DEBT-FREE ALBERTA Table of Contents Step 1 - Eliminating the Annual Deficit... 139 Step 2 - Eliminating the Net Debt... 139 Step 3 - Creating a Debt-Free Alberta... 142 Repaying Accumulated

A PLAN FOR A DEBT-FREE ALBERTA Table of Contents Step 1 - Eliminating the Annual Deficit... 139 Step 2 - Eliminating the Net Debt... 139 Step 3 - Creating a Debt-Free Alberta... 142 Repaying Accumulated

Liste d'adresses URL

Liste de sites Internet concernés dans l' étude Le 25/02/2014 Information à propos de contrefacon.fr Le site Internet https://www.contrefacon.fr/ permet de vérifier dans une base de donnée de plus d' 1

Liste de sites Internet concernés dans l' étude Le 25/02/2014 Information à propos de contrefacon.fr Le site Internet https://www.contrefacon.fr/ permet de vérifier dans une base de donnée de plus d' 1

Measuring Credit 1. Introduction. What Is Credit?

Measuring Credit 1 Introduction Central banks put significant emphasis on credit aggregates for understanding financial conditions in the economy. Measuring credit outstanding, however, is not straightforward,

Measuring Credit 1 Introduction Central banks put significant emphasis on credit aggregates for understanding financial conditions in the economy. Measuring credit outstanding, however, is not straightforward,

Vulnerability of new mortgage borrowers prior to the introduction of the LVR speed limit: Insights from the Household Economic Survey

Vulnerability of new mortgage borrowers prior to the introduction of the LVR speed limit: Insights from the Household Economic Survey AN215/2 Ashley Dunstan and Hayden Skilling March 215 Reserve Bank of

Vulnerability of new mortgage borrowers prior to the introduction of the LVR speed limit: Insights from the Household Economic Survey AN215/2 Ashley Dunstan and Hayden Skilling March 215 Reserve Bank of

Why a Floating Exchange Rate Regime Makes Sense for Canada

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Chambre de commerce du Montréal métropolitain Montreal, Quebec 4 December 2000 Why a Floating Exchange Rate Regime Makes Sense for Canada

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Chambre de commerce du Montréal métropolitain Montreal, Quebec 4 December 2000 Why a Floating Exchange Rate Regime Makes Sense for Canada

SENIOR HOME EQUITY INCREASES FOR THIRD STRAIGHT QUARTER

Contact: Katie Oehl Rasky Baerlein Strategic Communications [email protected] (202) 530-7709 SENIOR HOME EQUITY INCREASES FOR THIRD STRAIGHT QUARTER FOR IMMEDIATE RELEASE March 20, 2013 WASHINGTON, D.C.

Contact: Katie Oehl Rasky Baerlein Strategic Communications [email protected] (202) 530-7709 SENIOR HOME EQUITY INCREASES FOR THIRD STRAIGHT QUARTER FOR IMMEDIATE RELEASE March 20, 2013 WASHINGTON, D.C.

Saskatchewan Small Business Profile 2015

Saskatchewan Small Business Profile 2015 October 2015 Ministry of the Economy Performance and Strategic Initiatives Division economy.gov.sk.ca Table of Contents INTRODUCTION... 1 KEY FACTS... 3 1. SMALL

Saskatchewan Small Business Profile 2015 October 2015 Ministry of the Economy Performance and Strategic Initiatives Division economy.gov.sk.ca Table of Contents INTRODUCTION... 1 KEY FACTS... 3 1. SMALL

Mortgage Arrears in Ireland: Introducing the Enhanced Quarterly Statistics

8 Mortgage Arrears in Ireland: Introducing the Jean Goggin * Abstract This article introduces the recently expanded Residential Mortgage Arrears and Repossessions Statistics published by the Central Bank

8 Mortgage Arrears in Ireland: Introducing the Jean Goggin * Abstract This article introduces the recently expanded Residential Mortgage Arrears and Repossessions Statistics published by the Central Bank

Recent Developments in Small Business Finance

Reserve Bank of Australia Bulletin February Recent Developments in Small Business Finance This article focuses on recent trends in small business financing, including the interest rates and fees and charges

Reserve Bank of Australia Bulletin February Recent Developments in Small Business Finance This article focuses on recent trends in small business financing, including the interest rates and fees and charges