EXECUTIVE SUMMARY BACKGROUND

|

|

|

- MargaretMargaret Beasley

- 10 years ago

- Views:

Transcription

1

2

3

4

5 EXECUTIVE SUMMARY BACKGROUND Title XIX of the Social Security Act (the Act) established the Medicaid program to pay for the medical assistance costs of certain individuals and families with limited incomes and resources. Section 1905(a)(13) of the Act allows optional Medicaid coverage of rehabilitative services, generally defined as medical or remedial services recommended by physicians or other licensed practitioners for the maximum reduction of physical or mental disability and to restore an individual to their highest functional level. Indiana elected to include this optional Medicaid coverage under a State program referred to as the Medicaid Rehabilitation Option (MRO). Under the MRO program, community providers, including community mental health centers, provide mental health services and are separately reimbursed for Medicaid services and administrative costs. The administrative costs are funded under a unique provider arrangement whereby the non-federal share consists of certified expenditures of public funds that are incurred by the providers without an associated direct payment of State funds. This funding arrangement, referred to as the Indiana Mental Health Funds Recovery Program (Recovery Program), pays the providers the calculated Federal share of the certified expenditures. In accordance with Section 1903(a)(7) of the Act, Federal reimbursement is permitted for administrative costs necessary to properly and efficiently administer State Medicaid plans. The Federal Government generally reimburses the States at a matching rate of 50 percent. Administrative costs incurred in support of the State plan are subject to the cost principles contained in the Office of Management and Budget (OMB) Circular A-87. Indiana Administrative Cost Reimbursement The Indiana Family and Social Services Administration (State agency) uses a series of steps to calculate the Federal share of certified expenditures. A quarterly statewide time study establishes the amount of time expended by provider staff to perform Medicaid administrative activities and is used to allocate provider administrative costs to various activity groups within its claim. The allocated costs are reduced by applying provider Medicaid eligibility rates and applicable Federal reimbursement rates to the costs in these Medicaid eligible activity groups. Provider claims are consolidated into one claim for Federal reimbursement, which in fiscal year (FY) 2003 amounted to about $21 million. At the request of CMS, we reviewed the Recovery Program administrative claiming process associated with the State agency s Medicaid Rehabilitation Option. OBJECTIVE The objective was to determine whether Medicaid administrative costs incurred by community providers were claimed and paid in accordance with applicable State and Federal regulations. i

6 SUMMARY OF FINDINGS Based on our assessment of State agency claims oversight procedures and reviews at selected community mental health centers, Federal reimbursement for the Medicaid Recovery Program was overstated by $328,151. Our review of State agency oversight procedures disclosed $223,244 in unrecovered net overpayments identified by contracted auditors. This amount is offset by $44,590 of underclaimed costs due to contractor claims processing errors. Our review at three selected community mental health centers disclosed net overpayments of $149,497 for costs that were improperly claimed during FY 2003 due to flawed cost allocations, claiming errors, unallowable costs and an incomplete sampling universe. The State agency had not recovered most of the audit-identified overpayments because it mistakenly believed a two-year Federal payment and overpayment recovery limit had lapsed. In regard to overpayments identified at the three individually audited centers, provider oversight procedures were not adequate to ensure that claims were accurate and allowable. We also noted that documentation supporting FY 2003 enhanced claims for administrative activities needing skilled medical expertise was insufficient. Because documentation requirements existing during the audit period were met, we are only recommending enhanced contract audit procedures to ensure that providers meet the State agency s improved documentation requirements in the future. RECOMMENDATIONS We recommend that the State agency: refund $223,244 to the Federal Government for net administrative cost overpayments made to various providers for periods prior to January 1, 2003 as identified during external audits, refund $104,907 to the Federal Government for additional net administrative cost overpayments identified during our audit, improve the accuracy of administrative cost reimbursement procedures by reconciling data between the providers and the claims processing contractor, require external auditors to review time study documentation and activity logs and notes to ensure that claimed administrative costs are properly supported by the providers, and emphasize that the providers develop internal review systems to ensure that claimed cost data is accurate and allowable. STATE S COMMENTS Indiana agreed to repay the net Federal overpayments identified during State contracted provider audits covering periods prior to January 1, 2003 and has modified its procedures to refund all audit adjustments that identify Federal overpayments regardless of the time elapsed. Indiana also ii

7 agreed to refund $104,907 for additional net administrative cost overpayments that were identified during our audit and has implemented improvements to help eliminate future errors. In addition, the State agreed with our other procedural recommendations and has made further changes to improve the claiming process. The State s comments are summarized in the report and are presented in their entirety as an appendix. iii

8 TABLE OF CONTENTS INTRODUCTION...1 Page BACKGROUND...1 Indiana Administrative Cost Reimbursement...1 OBJECTIVE, SCOPE, AND METHODOLOGY...2 Objective...2 Scope...2 Methodology...3 FINDINGS AND RECOMMENDATIONS...4 APPENDIX STATE AGENCY OVERSIGHT...4 Unrecovered Audit Findings...4 Claims Processing Errors...5 CLAIMING BY SELECTED PROVIDERS...5 Flawed Cost Allocations...5 Claiming Errors...6 Unallowable Costs...6 Incomplete Sampling Universe...7 INSUFFICIENT TIME STUDY DOCUMENTATION...7 RECOMMENDATIONS...8 STATE S COMMENTS...8 STATE S COMMENTS iv

9 INTRODUCTION BACKGROUND Title XIX of the Social Security Act (the Act) established the Medicaid Program to pay for the medical assistance costs of certain individuals and families with limited incomes and resources. Section 1905(a)(13) of the Act allows optional Medicaid coverage of rehabilitative services, generally defined as medical or remedial services recommended by physicians or other licensed practitioners for the maximum reduction of physical or mental disability and to restore an individual to their highest functional level. Each State administers its Medicaid program in accordance with a State plan approved by the Centers for Medicare & Medicaid Services (CMS). Although a State has flexibility in designing its State plan and operating its Medicaid program, it must comply with broad Federal requirements. In Indiana, the Indiana Family and Social Services Administration (the State agency) administers the Medicaid program and elected to include optional Medicaid coverage for rehabilitative services under its Medicaid Rehabilitation Option (MRO) program. Under the MRO program, community providers, including community mental health centers, provide mental health services and are separately reimbursed for Medicaid services and administrative costs. The administrative costs for these activities are funded under a unique provider arrangement whereby the non-federal share consists of certified expenditures of public funds that are incurred by the providers without an associated direct matching payment of State funds. This funding arrangement, referred to as the Indiana Mental Health Funds Recovery Program (Recovery Program), results in direct Federal reimbursement for the calculated Federal share of the certified expenditures. Section 1903(a)(7) of the Act permits reimbursement for the costs of Medicaid administrative activities necessary for the proper and efficient administration of the State plan. The Federal Government generally reimburses States for administrative costs at a matching rate of 50 percent. Administrative costs incurred in support of the State plan are subject to the cost principles contained in the Office of Management and Budget (OMB) Circular A-87. Indiana Administrative Cost Reimbursement Effective on October 1, 1999, CMS approved a State Plan Amendment (SPA) granting the State agency s Division of Mental Health and Addiction (Mental Health) responsibility for the operational oversight of Medicaid administrative cost reimbursement under the Recovery Program. Mental Health also has the authority to enter into contractual agreements with external entities to furnish services including claims processing and payment, time study sampling, technical support, and administrative cost audits of providers. In 2004, Mental Health issued State policies for administrative cost reimbursement in its Indiana Mental Health Funds Recovery Program Manual. The manual provides detailed claiming instructions for participating providers. To determine provider reimbursement for the Recovery Program, Mental Health uses a series of steps to calculate the Federal share of certified expenditures. A quarterly statewide time study

10 establishes the amount of time expended by provider staff to perform Medicaid administrative activities. The time study is the foundation for the Recovery Program administrative claim and proportionally allocates each provider s administrative costs to various activity groups within its claim. Some Medicaid eligible activity groups are subject to a proportional reduction based on the provider s Medicaid eligibility rate, while other activities, such as Medicaid outreach, are not subject to this reduction. Finally, the reported costs associated with each activity group are subject to Medicaid Federal share reimbursement at rates of zero, 50, or 75 percent. Activities requiring the use of skilled medical expertise that are performed by skilled professional medical personnel (SPMP) are eligible for the enhanced 75 percent reimbursement rate. Other allowable Medicaid activities are reimbursed at 50 percent, while ineligible activities are not reimbursed. Ultimately, the Federal reimbursement becomes a portion, usually between about five and ten percent, of the provider s overall administrative costs. As a part of the claiming methodology, each participating provider is responsible for certifying that i) reported costs are accurate, eligible, and unrelated to other Federal funding and ii) sufficient State and local dollars were expended to support the claim. The claimed amounts for all Recovery Program providers are consolidated into one claim for Federal reimbursement. For Federal fiscal year (FY) 2003, 41 community mental health center providers received Federal reimbursement of about $21 million. OBJECTIVE, SCOPE, AND METHODOLOGY Objective The objective was to determine whether Medicaid administrative costs incurred by community providers were claimed and paid in accordance with applicable State and Federal regulations. Scope At the request of CMS, we evaluated the State agency s current oversight procedures for provider claims under its Medicaid Recovery Program and selected 3 of the 41 community mental health centers for on-site reviews of administrative cost reimbursements for FY 2003 (Center A, Center B, and Center C). For FY 2003, the three centers received about $4.8 million of the $21 million in Federal reimbursement received by the 41 centers. We limited our review of internal controls to understanding the State agency s and contractor s policies and procedures for claiming administrative costs incurred by the providers. Specifically, we reviewed the general policies and procedures that (1) the providers followed in reporting administrative costs and (2) the State agency used to calculate the providers claims for Federal reimbursement. Except as reported, we did not evaluate the overall effectiveness of controls at the State agency or contractor levels. We did not evaluate internal controls at the community mental health centers. In addition, we did not evaluate procedures used to support the certification of public expenditures or the distribution of provider reimbursement. We performed fieldwork at the offices of the State agency and at two community mental health centers in Indianapolis, Indiana and at one in Terre Haute, Indiana. 2

11 Methodology To accomplish our audit objective, we evaluated current administrative oversight and claiming methods and procedures at both the State agency and contractor levels. In addition, we reconciled FY 2003 documentation, retained by the State agency to support the reimbursed Federal share for each participating provider, to the CMS-64 quarterly Medicaid expense report. At the selected community mental health centers, we reviewed FY 2003 claim calculations and verified the appropriateness of the claimed costs and cost allocations. At the State agency and contractor levels, we: obtained an understanding of the State agency s approved methodology for administrative cost reimbursement and verified that Federal and State requirements were met, evaluated the extent of State agency and contractor oversight, including Recovery Program monitoring achieved through provider audits performed under contract between Mental Health and an external firm, held discussions with State agency and contractor officials to identify Recovery Program controls, reconciled Federally reimbursed amounts from the CMS-64 to summary supporting claim documentation retained at the State agency and contractor levels for each provider, and reviewed supporting documentation for 31 selected statewide time study participants who charged time at the enhanced 75 percent SPMP claim rate. At the three Providers, we: verified the accuracy of the administrative cost claim calculation, reconciled claimed costs to supporting accounting and financial records, and verified that selected costs were allowable and appropriately allocated and classified. We performed the audit in accordance with generally accepted government auditing standards. 3

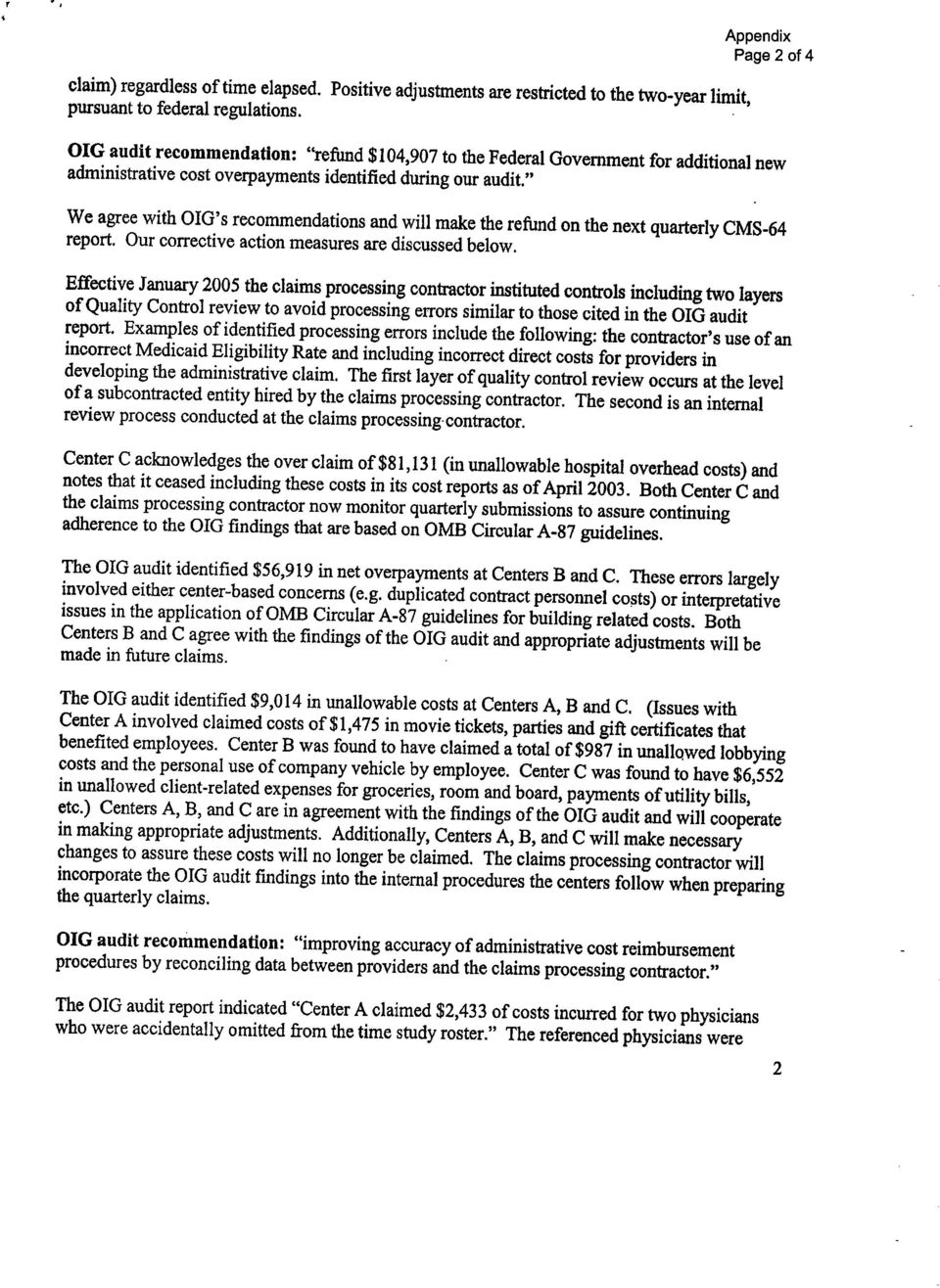

12 FINDINGS AND RECOMMENDATIONS Based on our assessment of State agency claims oversight procedures and reviews at selected community mental health centers, Federal reimbursement for the Medicaid Recovery Program was overstated by $328,151. Our review of State agency oversight procedures disclosed $223,244 in unrecovered net overpayments identified by contracted auditors. This amount is offset by $44,590 of underclaimed costs due to contractor claims processing errors. Our review at three selected community mental health centers disclosed net overpayments of $149,497 for costs that were improperly claimed during FY 2003 due to flawed cost allocations, claiming errors, unallowable costs and an incomplete sampling universe. The State agency had not recovered most of the audit-identified overpayments because it mistakenly believed a two-year Federal payment and overpayment recovery limit had lapsed. In regard to overpayments identified at the three individually audited centers, provider oversight procedures were not adequate to ensure that claims were accurate and allowable. In addition, documentation evaluated during our State agency oversight review disclosed that supporting FY 2003 documentation for 31 selected time study participants was insufficient to confirm the need for skilled medical expertise to perform some SPMP activities that were claimed at 75 percent. Because documentation requirements existing during the audit period were met, we are only recommending enhanced review procedures to ensure that providers maintain the improved documentation requirements adopted by the State agency in FY STATE AGENCY OVERSIGHT Our review of State agency oversight procedures disclosed net overpayments of $223,244 identified through external provider audits and $44,590 in underclaimed costs due to claims processing errors. Unrecovered Audit Findings The State agency had not recovered $223,244 in prior audit findings at various providers. Citing a two-year Federal claim-filing limit, the State agency disagreed that it should recover $202,340 of net provider overpayments that were claimed prior to January 1, 2003 and identified for audit adjustment by external auditors under contract with Mental Health. The State agency agreed that net overpayments of $20,904 identified through the same audit process for periods falling within the two-year Federal claim filing requirements should be recovered. Federal regulations (45 CFR 95.7) state,... we will pay a State... only if the State files a claim... within 2 years after the calendar quarter in which the State agency made the expenditure. The State agency concluded that it was inappropriate to recover overpayments, or to repay underpayments, for audit findings relating to administrative cost claims that were beyond an allowable two-year claiming period. It cited Federal regulations (45 CFR 95.7), which state... we will pay a State... only if the State files a claim... within 2 years after the calendar quarter in which the State agency made the expenditure. The State agency seemed unaware that an additional Federal regulation (45 CFR 95.19) stated that the two-year restriction does not apply to claims resulting from audit exceptions. The State agency can 4

13 recover the overpayments and should repay the Federal Government for its share of the net overpayments identified by prior audits. Claims Processing Errors The State agency underclaimed $44,590 as a result of reporting errors by the contractor hired to process claims. The contractor s use of a Medicaid eligibility rate of percent for a provider, instead of the provider s correct rate of percent, resulted in an underclaim of $29,426. In addition, another center correctly submitted indirect cost amounts for the quarter ended December 31, 2002 that were incorrectly processed by the contractor and resulted in underclaimed costs of $15,164. The SPA, Attachment 4.16A, page 1i, section C., 3., states,... DMH [Division of Mental Health] shall... demonstrate that adequate quality assurance controls are in place.... In the identified instances, the contractor attributed the probable cause of the errors to reliance on temporary employees for inputting claims data during the effected quarters. Quality assurance controls were inadequate. CLAIMING BY SELECTED PROVIDERS The selected centers received net overpayments totaling $149,497 due to flawed cost allocations, claiming errors, unallowable costs, and an incomplete sampling universe as described below. Flawed Cost Allocations Center C overclaimed $81,131 due to flawed cost allocations between the center and an affiliated hospital and also over-allocated the center s administrative costs to part-time employees. The center was overpaid $81,131 because hospital overhead costs that were not allocable to the center, including non-reimbursable inpatient, cafeteria, nursing overhead, and Medicare reimbursed intern and resident costs were inappropriately allocated into the center s indirect cost pool as Medicaid reimbursable administrative costs. Center C s existing cost allocation procedures also improperly allocated direct administrative costs to the personnel performing direct Medicaid administrative activities. Although the effect of this error could not be quantified, the allocation method incorrectly recognized all involved employees as full-time regardless of whether they held full or part-time employment status. The result was an over-allocation of the center s costs to part-time employees. The allocation occurred during all of FY 2003 but was corrected beginning April 1, OMB Circular A-87 states,... A cost is allocable to a particular cost objective if the goods or services involved are chargeable or assignable to such cost objective in accordance with relative benefits received. In the identified instances, the hospital s costs were either not allocable to the center, or the center s costs were allowable but had been allocated in a way that was disproportionate to the benefits received by the Medicaid program. 5

14 Claiming Errors We identified net overpayments of $56,919 at two centers (Center B and Center C) resulting from duplicated costs, calculation and claim submission errors, and incorrectly reported Federal revenue offsets. Overclaims and underclaims by the two centers are, as follows: Center B underclaimed net administrative costs by $55,960 for direct purchased services of $57,382 that were mistakenly omitted from the claim, overstated building-related costs of $2,863 that should not have been claimed, and overstated Federal revenue offsets of $1,441 caused by a transposition error and resulting in an underclaim. Center C overclaimed $112,879 for duplicated contract personnel costs of $75,919, understated Federal revenue offsets against direct costs resulting in an overclaim of $30,301, duplicated education, training and mileage costs and overstated rent of $3,680, and overstated direct costs of $2,979 due to the center s failure to update a prior quarterly calculation. The State agency s approved methodology states, The accuracy of the financial expenditure information that is submitted by the participating MCP [Managed Care Provider] is certified at the MCP level. The submitted certified data was not accurate in the identified instances. Unallowable Costs The three centers claimed $9,014 in unallowable direct and indirect costs for employee entertainment, political lobbying, personal use of company cars, and unallowable client-related expenses. Center A claimed costs of $1,475 for unallowable movie tickets, parties, and gift certificates that benefited employees. OMB Circular A-87 states, Costs of entertainment, including amusement, diversion, and social activities... are unallowable. The identified amounts fell within these specifically defined categories of unallowable costs. Center B claimed unallowable political lobbying costs of $674 that were included as itemized portions of organizational dues and $313 for personal use of company vehicles by employees. The center s cost allocation methodology specifically excluded allocation of these types of costs to the Medicaid cost pool. OMB Circular A-87 also specifically identifies these types of expenditures as being unallowable. Center C claimed $6,552 for unallowable client-related expenses consisting of groceries, room and board, payment of a client s utility bill, and a direct payment to a client for the purchase of clothing. The identified costs were not necessary... for the proper and efficient administration of the State plan pursuant to section 1903(a)(7) of the Act. 6

15 Incomplete Sampling Universe Center A claimed $2,433 of costs incurred for two physicians who were accidentally omitted from the time study roster. OMB Circular A-87 states, The sampling universe must include all of the employees whose salaries and wages are to be allocated based on sample results.... The identified costs were directly attributable to the identified individuals who were incorrectly excluded from the sampling universe. INSUFFICIENT TIME STUDY DOCUMENTATION As a part of our review of State agency oversight, the enhanced SPMP 75 percent Federal Medicaid reimbursement rate was evaluated by selecting 31 SPMP time study participants statewide. The reviewed documentation was generally insufficient to confirm the need for skilled professional medical expertise to perform the claimed administrative activities. The 75 percent enhanced Federal funding rate is available for administrative activities requiring skilled professional medical expertise. For 16 of the 31 time studies, the State agency provided no documentation beyond a time study form. Although the State agency provided Participant Activity Logs as additional supporting documentation for the remaining 15 selected time studies, the documentation was insufficient to confirm the need for skilled medical expertise during some charged SPMP time periods in 14 of these cases. Fire destroyed eight requested time studies that were, therefore, unavailable for review. The State agency provided other documentation to summarize and support the results of the destroyed time studies. This documentation was accepted in lieu of the actual time study for the eight participants. Federal regulations (42 CFR ) state... (c) Application of rates... (2) Rates of FFP in excess of 50 percent apply only to those portions of the individual s working time that are spent carrying out duties in the specified areas for which the higher rate is authorized. Additional guidance in the approved Indiana program methodology states, The requirement of the use of SPMP [skilled professional medical personnel] skills... is accounted for and documented in the time study results. Although Federal and State requirements did not address the level of supporting documentation required during FY 2003, subsequent Mental Health policy specifically requires the retention of supporting documentation in addition to the time study form. The Recovery Program Manual, issued during 2004, stipulates, The Participant Activity Log (PAL) needs to be completed in conjunction with the time study as supportive documentation in case of an audit. The manual also states that additional notes should be maintained as needed. Although the enhanced rate reimbursement differential was estimated at about $1.3 million for FY 2003, the lack of clearly defined documentation requirements during this period precluded recommendations other than procedural improvement to the SPMP documentation review process. Future provider audits should verify the implementation of the State agency s improved documentation requirements. 7

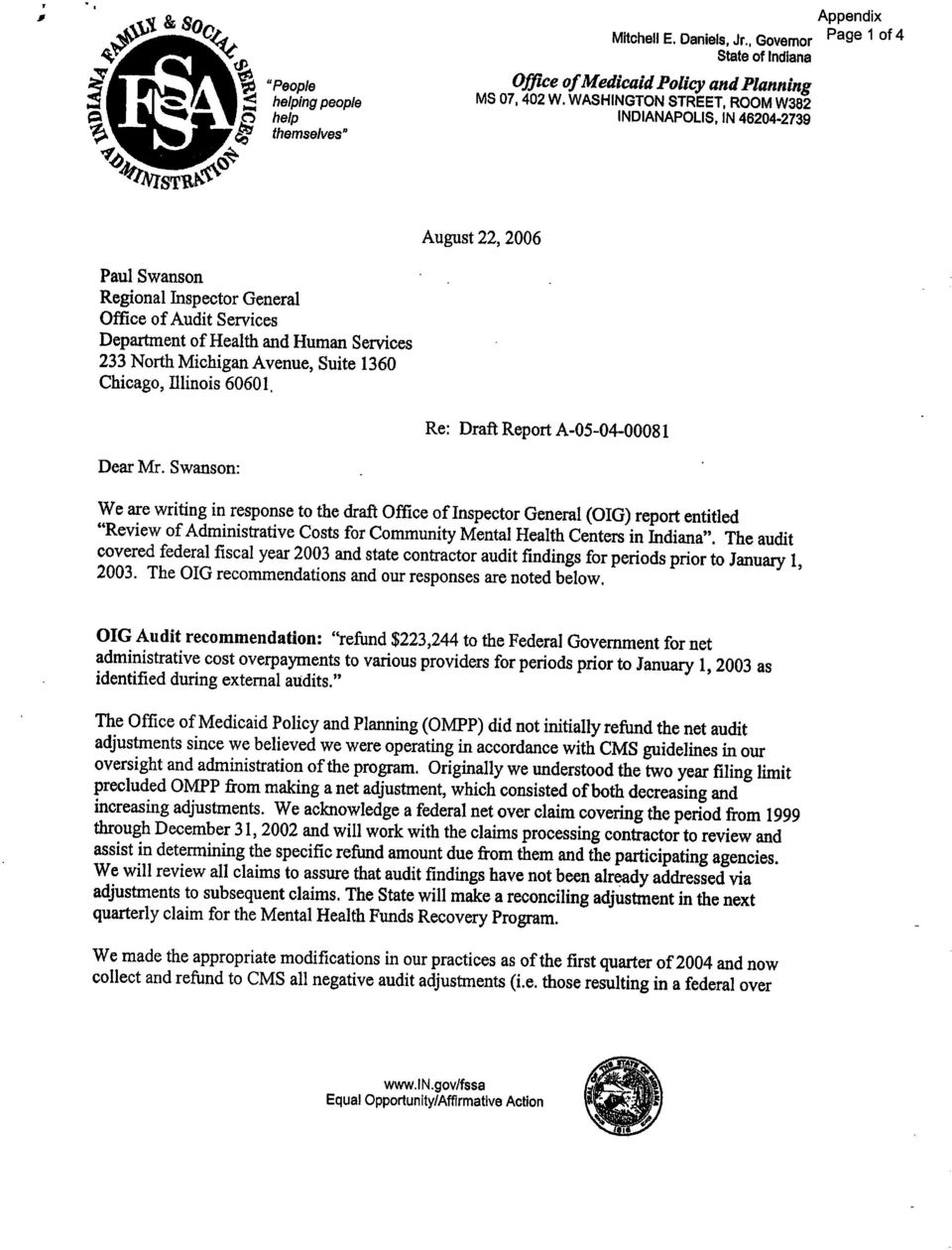

16 RECOMMENDATIONS We recommend that the State agency: refund $223,244 to the Federal Government for net administrative cost overpayments made to various providers for periods prior to January 1, 2003 as identified during external audits, refund $104,907 to the Federal Government for additional net administrative cost overpayments identified during our audit, improve the accuracy of administrative cost reimbursement procedures by reconciling data between the providers and the claims processing contractor, require external auditors to review time study documentation and activity logs and notes to ensure that claimed administrative costs are properly supported by the providers, and emphasize that the providers develop internal review systems to ensure that claimed cost data is accurate and allowable. STATE S COMMENTS Indiana agreed to repay the net Federal overpayment identified during State contracted provider audits covering periods prior to January 1, 2003 and has modified its procedures to refund all audit adjustments that identify Federal overpayments regardless of the time elapsed. Indiana further agreed to refund $104,907 for additional net administrative cost overpayments that were identified during our audit and has made changes to help eliminate future errors. Indiana also agreed with our procedural recommendations and stated that it has implemented revisions to improve the claim filing process. Specifically, it indicated that: contractor level claims processing procedures were enhanced to generally improve the accuracy of the claim submission process, beginning with the SFY 2007 audit cycle, the scope of Indiana s provider audits were expanded to include the review of time study documentation and activity logs and notes to verify that claimed costs are supported, and provider training and reporting requirements were modified to improve claiming accuracy through better provider understandings of the Recovery Program and the application of OMB Circular A-87. The State s written comments are presented in their entirety as an appendix. 8

17 APPENDIX

18

19

20

21

In total, Massachusetts overstated its Medicaid claim for reimbursement by $5,312,447 (Federal share).

.") Page 2 Wynethea Walker In total, Massachusetts overstated its Medicaid claim for reimbursement by $5,312,447 (Federal share). Massachusetts did not provide specific guidance to local education agencies

Page 2 Wynethea Walker In total, Massachusetts overstated its Medicaid claim for reimbursement by $5,312,447 (Federal share). Massachusetts did not provide specific guidance to local education agencies

COLORADO CLAIMED UNALLOWABLE MEDICAID NURSING FACILITY SUPPLEMENTAL PAYMENTS

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL COLORADO CLAIMED UNALLOWABLE MEDICAID NURSING FACILITY SUPPLEMENTAL PAYMENTS Inquiries about this report may be addressed to the Office

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL COLORADO CLAIMED UNALLOWABLE MEDICAID NURSING FACILITY SUPPLEMENTAL PAYMENTS Inquiries about this report may be addressed to the Office

Department of Health and Human Services. Centers for Medicare & Medicaid Services. Medicaid Integrity Program

Department of Health and Human Services Centers for Medicare & Medicaid Services Medicaid Integrity Program North Carolina Comprehensive Program Integrity Review Final Report Reviewers: Mark Rogers, Review

Department of Health and Human Services Centers for Medicare & Medicaid Services Medicaid Integrity Program North Carolina Comprehensive Program Integrity Review Final Report Reviewers: Mark Rogers, Review

Harlan Stewart, Director, Region X Office of Public Housing, 0APH. Joan S. Hobbs, Regional Inspector General for Audit, Seattle, Region X, 0AGA

Issue Date January 9, 2009 Audit Report Number 2009-SE-1001 TO: Harlan Stewart, Director, Region X Office of Public Housing, 0APH FROM: Joan S. Hobbs, Regional Inspector General for Audit, Seattle, Region

Issue Date January 9, 2009 Audit Report Number 2009-SE-1001 TO: Harlan Stewart, Director, Region X Office of Public Housing, 0APH FROM: Joan S. Hobbs, Regional Inspector General for Audit, Seattle, Region

Subject Third Party Liability Collections Under the Medicaid Program - Indiana Department of Public Welfare (A-05-91-00052)

") : + i ċ 2: +3*rw-, DEPARTMENT OF HEALTH & HUMAN SERVICES Office of Inspector General 2 8 c1 G %++a 4 Memorandum Inspector General Subject Third Party Liability Collections Under the Medicaid Program -

: + i ċ 2: +3*rw-, DEPARTMENT OF HEALTH & HUMAN SERVICES Office of Inspector General 2 8 c1 G %++a 4 Memorandum Inspector General Subject Third Party Liability Collections Under the Medicaid Program -

Review Of Hartford Hospital s Controls To Ensure Accuracy Of Wage Data Used For Calculating Inpatient Prospective Payment System Wage Indexes

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL Review Of Hartford Hospital s Controls To Ensure Accuracy Of Wage Data Used For Calculating Inpatient Prospective Payment System Wage

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL Review Of Hartford Hospital s Controls To Ensure Accuracy Of Wage Data Used For Calculating Inpatient Prospective Payment System Wage

DEPARTMENT OF HEALTH AND HUMAN SERVICES OFFICE OF AUDIT SERVICES 233 NORTH MICHIGAN AVENUE CHICAGO, ILLINOIS 60601. April 23,2002

DEPARTMENT OF HEALTH AND HUMAN SERVICES OFFICE OF AUDIT SERVICES 233 NORTH MICHIGAN AVENUE CHICAGO, ILLINOIS 60601 REGION V OFFICE OF INSPECTOR GENERAL UN: A-05-0 l-00044 April 23,2002 Mr. Michael O Keefe

DEPARTMENT OF HEALTH AND HUMAN SERVICES OFFICE OF AUDIT SERVICES 233 NORTH MICHIGAN AVENUE CHICAGO, ILLINOIS 60601 REGION V OFFICE OF INSPECTOR GENERAL UN: A-05-0 l-00044 April 23,2002 Mr. Michael O Keefe

Section 3.16 Comprehensive Community Services (CCS) 2012

2012") Section 3.16 Comprehensive Community Services (CCS) 2012 This section is applicable to audits of counties that participate in the CCS program. A list of participating counties is on the CCS website - http://www.dhs.wisconsin.gov/mh_bcmh/ccs/index.htm.

Section 3.16 Comprehensive Community Services (CCS) 2012 This section is applicable to audits of counties that participate in the CCS program. A list of participating counties is on the CCS website - http://www.dhs.wisconsin.gov/mh_bcmh/ccs/index.htm.

MONITORING PERFORMANCE

MONITORING PERFORMANCE Monitoring the performance of the contractor is a key function of proper contract administration. The purpose is to ensure that the contractor is performing all duties in accordance

MONITORING PERFORMANCE Monitoring the performance of the contractor is a key function of proper contract administration. The purpose is to ensure that the contractor is performing all duties in accordance

September 2005 Report No. 06-009

An Audit Report on The Health and Human Services Commission s Consolidation of Administrative Support Functions Report No. 06-009 John Keel, CPA State Auditor An Audit Report on The Health and Human Services

An Audit Report on The Health and Human Services Commission s Consolidation of Administrative Support Functions Report No. 06-009 John Keel, CPA State Auditor An Audit Report on The Health and Human Services

Audit Unit Policy 16 th Revision April 2006. Floyd Blodgett, Education Accounting and Auditing Analyst

Audit Unit Policy 16 th Revision April 2006 Floyd Blodgett, Education Accounting and Auditing Analyst This document describes the process by which the Vermont Department of Education (VTDOE) conducts its

Audit Unit Policy 16 th Revision April 2006 Floyd Blodgett, Education Accounting and Auditing Analyst This document describes the process by which the Vermont Department of Education (VTDOE) conducts its

FINANCIAL MANAGEMENT GUIDE FOR NON-PROFIT ORGANIZATIONS

FINANCIAL MANAGEMENT GUIDE FOR NON-PROFIT ORGANIZATIONS NATIONAL ENDOWMENT FOR THE ARTS OFFICE OF INSPECTOR GENERAL SEPTEMBER 2008 Questions about this guide may be directed to the National Endowment for

FINANCIAL MANAGEMENT GUIDE FOR NON-PROFIT ORGANIZATIONS NATIONAL ENDOWMENT FOR THE ARTS OFFICE OF INSPECTOR GENERAL SEPTEMBER 2008 Questions about this guide may be directed to the National Endowment for

8.300.22.1 ISSUING AGENCY: New Mexico Human Services Department (HSD). [8.300.22.1 NMAC - N, 8-1-11]

![8.300.22.1 ISSUING AGENCY: New Mexico Human Services Department (HSD). [8.300.22.1 NMAC - N, 8-1-11]](/thumbs/26/8880226.jpg "8.300.22.1 ISSUING AGENCY: New Mexico Human Services Department (HSD). [8.300.22.1 NMAC - N, 8-1-11]") TITLE 8 SOCIAL SERVICES CHAPTER 300 MEDICAID GENERAL INFORMATION PART 22 ELECTRONIC HEALTH RECORDS INCENTIVE PROGRAM 8.300.22.1 ISSUING AGENCY: New Mexico Human Services Department (HSD). [8.300.22.1 NMAC

TITLE 8 SOCIAL SERVICES CHAPTER 300 MEDICAID GENERAL INFORMATION PART 22 ELECTRONIC HEALTH RECORDS INCENTIVE PROGRAM 8.300.22.1 ISSUING AGENCY: New Mexico Human Services Department (HSD). [8.300.22.1 NMAC

AUDIT OF NASA GRANTS AWARDED TO THE PHILADELPHIA COLLEGE OPPORTUNITY RESOURCES FOR EDUCATION

JULY 26, 2012 AUDIT REPORT OFFICE OF AUDITS AUDIT OF NASA GRANTS AWARDED TO THE PHILADELPHIA COLLEGE OPPORTUNITY RESOURCES FOR EDUCATION OFFICE OF INSPECTOR GENERAL National Aeronautics and Space Administration

JULY 26, 2012 AUDIT REPORT OFFICE OF AUDITS AUDIT OF NASA GRANTS AWARDED TO THE PHILADELPHIA COLLEGE OPPORTUNITY RESOURCES FOR EDUCATION OFFICE OF INSPECTOR GENERAL National Aeronautics and Space Administration

THIS PAGE INTENTIONALLY LEFT BLANK

THIS PAGE INTENTIONALLY LEFT BLANK ACTION DELIVERY SERVICE, INC. DBA MEDICAL TRANSPORTATION SERVICE ALSO KNOWN AS MTS ASHLAND, KENTUCKY TABLE OF CONTENTS Title Page Independent Auditor s Report... 1 Compliance

THIS PAGE INTENTIONALLY LEFT BLANK ACTION DELIVERY SERVICE, INC. DBA MEDICAL TRANSPORTATION SERVICE ALSO KNOWN AS MTS ASHLAND, KENTUCKY TABLE OF CONTENTS Title Page Independent Auditor s Report... 1 Compliance

MICHIGAN AUDIT REPORT OFFICE OF THE AUDITOR GENERAL THOMAS H. MCTAVISH, C.P.A. AUDITOR GENERAL

MICHIGAN OFFICE OF THE AUDITOR GENERAL AUDIT REPORT THOMAS H. MCTAVISH, C.P.A. AUDITOR GENERAL The auditor general shall conduct post audits of financial transactions and accounts of the state and of all

MICHIGAN OFFICE OF THE AUDITOR GENERAL AUDIT REPORT THOMAS H. MCTAVISH, C.P.A. AUDITOR GENERAL The auditor general shall conduct post audits of financial transactions and accounts of the state and of all

DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs Need Improvement

Report No. DODIG-2015-068 I nspec tor Ge ne ral U.S. Department of Defense JA N UA RY 1 4, 2 0 1 5 DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs

Report No. DODIG-2015-068 I nspec tor Ge ne ral U.S. Department of Defense JA N UA RY 1 4, 2 0 1 5 DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs

MEDICAID SCHOOL-BASED ADMINISTRATIVE CLAIMING GUIDE

MEDICAID SCHOOL-BASED ADMINISTRATIVE CLAIMING GUIDE May 2003 MEDICAID SCHOOL-BASED ADMINISTRATIVE CLAIMING GUIDE TABLE OF CONTENTS I. INTRODUCTION...1 II. MEDICAID IN THE SCHOOL SETTING...3 III. INTERAGENCY

MEDICAID SCHOOL-BASED ADMINISTRATIVE CLAIMING GUIDE May 2003 MEDICAID SCHOOL-BASED ADMINISTRATIVE CLAIMING GUIDE TABLE OF CONTENTS I. INTRODUCTION...1 II. MEDICAID IN THE SCHOOL SETTING...3 III. INTERAGENCY

Non-Emergency Medical Transportation Reviews

Table of Contents Non-Emergency Medical Transportation Reviews Focusing on Compliance OIG 99-0269 BACKGROUND................................Pg 1 Non-emergency medical transportation expenditures have increased

Table of Contents Non-Emergency Medical Transportation Reviews Focusing on Compliance OIG 99-0269 BACKGROUND................................Pg 1 Non-emergency medical transportation expenditures have increased

AUDITOR GENERAL DAVID W. MARTIN, CPA

AUDITOR GENERAL DAVID W. MARTIN, CPA AGENCY FOR HEALTH CARE ADMINISTRATION ADMINISTRATIVE ACTIVITIES Operational Audit SUMMARY This operational audit of the Agency for Health Care Administration (Agency)

AUDITOR GENERAL DAVID W. MARTIN, CPA AGENCY FOR HEALTH CARE ADMINISTRATION ADMINISTRATIVE ACTIVITIES Operational Audit SUMMARY This operational audit of the Agency for Health Care Administration (Agency)

Allowable and Unallowable Costs Reference Guide Description Allowable Unallowable

1 Advertizing and Public Relations 200.421 Advertizing and Public relations costs for: Advertizing and Public relations costs for: The term advertising costs means the costs of advertising media and corollary

1 Advertizing and Public Relations 200.421 Advertizing and Public relations costs for: Advertizing and Public relations costs for: The term advertising costs means the costs of advertising media and corollary

APPLICATION CONTROLS AT THE NEW HAMPSHIRE MEDICAID STATE AGENCY IDENTIFICATION OF SUSPECT DUPLICATE CLAIMS

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL APPLICATION CONTROLS AT THE NEW HAMPSHIRE MEDICAID STATE AGENCY IDENTIFICATION OF SUSPECT DUPLICATE CLAIMS FEBRUARY 2005 A-01-04-00003

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL APPLICATION CONTROLS AT THE NEW HAMPSHIRE MEDICAID STATE AGENCY IDENTIFICATION OF SUSPECT DUPLICATE CLAIMS FEBRUARY 2005 A-01-04-00003

Performance Audit Report. Department of Human Resources The Maryland Energy Assistance Program and the Electric Universal Service Program

Performance Audit Report Department of Human Resources The Maryland Energy Assistance Program and the Electric Universal Service Program Accounting Records Cannot Be Relied Upon to Provide Accurate Expenditure

Performance Audit Report Department of Human Resources The Maryland Energy Assistance Program and the Electric Universal Service Program Accounting Records Cannot Be Relied Upon to Provide Accurate Expenditure

May 2006. American Speech-Language-Hearing Association 1. 2006 Focused Initiative on Health Care Reimbursement. Last updated February 2009.

Summary of the Department of Health and Human Services Office of Inspector General's (OIG) Findings of the Delivery of Medicaid Speech- Language Pathology Services in the Schools 1 May 2006 Lack of documentation

Summary of the Department of Health and Human Services Office of Inspector General's (OIG) Findings of the Delivery of Medicaid Speech- Language Pathology Services in the Schools 1 May 2006 Lack of documentation

Florida Medicaid. Medicaid Certified School Match Program Coverage and Limitations Handbook. Agency for Health Care Administration

Florida Medicaid Medicaid Certified School Match Program Coverage and Limitations Handbook Agency for Health Care Administration This page is intentionally blank. This page is intentionally blank. UPDATE

Florida Medicaid Medicaid Certified School Match Program Coverage and Limitations Handbook Agency for Health Care Administration This page is intentionally blank. This page is intentionally blank. UPDATE

Indirect Cost Rate Agreement Guide for Non-Profit Organizations

U.S. Department of Veterans Affairs Homeless Providers Grant and Per Diem Program Indirect Cost Rate Agreement Guide for Non-Profit Organizations Based on the Cost Principles and Procedures Required under

U.S. Department of Veterans Affairs Homeless Providers Grant and Per Diem Program Indirect Cost Rate Agreement Guide for Non-Profit Organizations Based on the Cost Principles and Procedures Required under

NOT ALL COMMUNITY SERVICES BLOCK GRANT RECOVERY ACT COSTS CLAIMED

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL NOT ALL COMMUNITY SERVICES BLOCK GRANT RECOVERY ACT COSTS CLAIMED ON BEHALF OF THE COMMUNITY ACTION PARTNERSHIP OF NATRONA COUNTY FOR

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL NOT ALL COMMUNITY SERVICES BLOCK GRANT RECOVERY ACT COSTS CLAIMED ON BEHALF OF THE COMMUNITY ACTION PARTNERSHIP OF NATRONA COUNTY FOR

Indiana Department of Child Services (DCS)

") Indiana Department of Child Services (DCS) Child Placing Agency (CPA) 2015 Cost Report Instructions Published: February 16, 2015 Table of Contents INTRODUCTION... 4 CPA COST REPORT OVERVIEW... 4 COST REPORTING...

Indiana Department of Child Services (DCS) Child Placing Agency (CPA) 2015 Cost Report Instructions Published: February 16, 2015 Table of Contents INTRODUCTION... 4 CPA COST REPORT OVERVIEW... 4 COST REPORTING...

North Carolina Medicaid Administrative Claiming (MAC) Program for School-Based Services

Program for School-Based Services") North Carolina Medicaid Administrative Claiming (MAC) Program for School-Based Services Financial and Business Services Summer Conference Training Research Triangle Park, North Carolina July 25, 2013 Overview

North Carolina Medicaid Administrative Claiming (MAC) Program for School-Based Services Financial and Business Services Summer Conference Training Research Triangle Park, North Carolina July 25, 2013 Overview

Ohio Medicaid Program

Ohio Medicaid Program A Compliance Audit by the: Medicaid/Contract Audit Section September 2011 AOS/MCA-12-005C September 29, 2011 Michael Linville, LPN 4932 Lebanon Rd. South Lebanon, OH 45065 Dear Mr.

Ohio Medicaid Program A Compliance Audit by the: Medicaid/Contract Audit Section September 2011 AOS/MCA-12-005C September 29, 2011 Michael Linville, LPN 4932 Lebanon Rd. South Lebanon, OH 45065 Dear Mr.

The Environmental Careers Organization Reported Outlays for Five EPA Cooperative Agreements

OFFICE OF INSPECTOR GENERAL Attestation Report Catalyst for Improving the Environment The Environmental Careers Organization Reported Outlays for Five EPA Cooperative Agreements Report No. 2007-4-00065

OFFICE OF INSPECTOR GENERAL Attestation Report Catalyst for Improving the Environment The Environmental Careers Organization Reported Outlays for Five EPA Cooperative Agreements Report No. 2007-4-00065

THIS PAGE INTENTIONALLY LEFT BLANK

THIS PAGE INTENTIONALLY LEFT BLANK WINTON TRANSPORTATION, LLC NOW KNOWN AS UNIVERSAL TRANSPORTATION SYSTEMS, LLC BUTLER COUNTY TABLE OF CONTENTS Title Page Independent Auditor s Report... 1 Compliance

THIS PAGE INTENTIONALLY LEFT BLANK WINTON TRANSPORTATION, LLC NOW KNOWN AS UNIVERSAL TRANSPORTATION SYSTEMS, LLC BUTLER COUNTY TABLE OF CONTENTS Title Page Independent Auditor s Report... 1 Compliance

REIMBURSEMENT FOR DRUG MEDI-CAL SERVICES

38 REIMBURSEMENT FOR DRUG MEDI-CAL SERVICES Effective July 1, 2012, the administration of the Drug Medi-Cal Program (DMC) is transferred from the State Department of Alcohol and Drug Programs (ADP) to

38 REIMBURSEMENT FOR DRUG MEDI-CAL SERVICES Effective July 1, 2012, the administration of the Drug Medi-Cal Program (DMC) is transferred from the State Department of Alcohol and Drug Programs (ADP) to

Payments for Inmate Health Care Services. Department of Corrections and Community Supervision

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Payments for Inmate Health Care Services Department of Corrections and Community Supervision

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Payments for Inmate Health Care Services Department of Corrections and Community Supervision

New York State Office of Alcoholism and Substance Abuse Services

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE GOVERNMENT ACCOUNTABILITY New York State Office of Alcoholism and Substance Abuse Services Chemical Dependency Program Payments to Selected Contractors

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE GOVERNMENT ACCOUNTABILITY New York State Office of Alcoholism and Substance Abuse Services Chemical Dependency Program Payments to Selected Contractors

Rebates and Discounts on Physician-Administered Drugs. Medicaid Program Department of Health

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Rebates and Discounts on Physician-Administered Drugs Medicaid Program Department of Health

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Rebates and Discounts on Physician-Administered Drugs Medicaid Program Department of Health

MEDICARE CREDIT BALANCE REPORT CERTIFICATION PAGE

DEPAR ARTMENT OF HEALTH AND HUMAN SERVICES Form Approved OMB No. 0938-0600 MEDICARE CREDIT BALANCE REPORT CERTIFICATION PAGE The Credit Balance Report is required under the authority of sections 1815(a),

DEPAR ARTMENT OF HEALTH AND HUMAN SERVICES Form Approved OMB No. 0938-0600 MEDICARE CREDIT BALANCE REPORT CERTIFICATION PAGE The Credit Balance Report is required under the authority of sections 1815(a),

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL AUDIT OF COMMUNITY SERVICE AND OTHER SELECTED GRANTS AT KENTUCKY AUTHORITY FOR EDUCATIONAL TELEVISION, INC., KET-TV, LEXINGTON, KENTUCKY

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL AUDIT OF COMMUNITY SERVICE AND OTHER SELECTED GRANTS AT KENTUCKY AUTHORITY FOR EDUCATIONAL TELEVISION, INC., KET-TV, LEXINGTON, KENTUCKY

Conference Call #1-888-494-4032 Access Code #9786079493 A Training Session Given to DHS Providers October, 2014

DHS Mission: To assist our customers to achieve maximum self-sufficiency, independence and health through the provision of seamless, integrated services for individuals, families and communities. Conference

DHS Mission: To assist our customers to achieve maximum self-sufficiency, independence and health through the provision of seamless, integrated services for individuals, families and communities. Conference

State of New York Unified Court System Financial Planning & Control Manual. Subject: Internal Controls Contractual Security Services

IX/1.000 Replacement Page: 1 1.000 Table of Contents 1.010 - Introduction 1.020 State Reimbursed 1.020.1 Allowable Security Services 1.020.2 Non-reimbursable Security Services 1.030 - Internal Controls

IX/1.000 Replacement Page: 1 1.000 Table of Contents 1.010 - Introduction 1.020 State Reimbursed 1.020.1 Allowable Security Services 1.020.2 Non-reimbursable Security Services 1.030 - Internal Controls

Average Daily Membership Audit Report Primavera Technical Learning Center Arizona Online Instruction Program Fiscal Years 2012, 2013 and 2014

Arizona Department of Education The Audit Unit 1535 W. Jefferson St., Bin 19 Phoenix, Arizona 85007 602-364-4061 Average Daily Membership Audit Report Primavera Technical Learning Center Arizona Online

Arizona Department of Education The Audit Unit 1535 W. Jefferson St., Bin 19 Phoenix, Arizona 85007 602-364-4061 Average Daily Membership Audit Report Primavera Technical Learning Center Arizona Online

STATE OF NEVADA DEPARTMENT OF PERSONNEL STATEWIDE PAYROLL SYSTEM AUDIT REPORT

STATE OF NEVADA DEPARTMENT OF PERSONNEL STATEWIDE PAYROLL SYSTEM AUDIT REPORT Table of Contents Page Executive Summary... 1 Introduction... 6 Background... 6 Scope and Objective... 7 Findings and Recommendations...

STATE OF NEVADA DEPARTMENT OF PERSONNEL STATEWIDE PAYROLL SYSTEM AUDIT REPORT Table of Contents Page Executive Summary... 1 Introduction... 6 Background... 6 Scope and Objective... 7 Findings and Recommendations...

OFFICE OF INFORMATION TECHNOLOGY 9-1-1 STATE GRANT COMPLIANCE SUPPLEMENT -----------------------------------------------------------

OFFICE OF INFORMATION TECHNOLOGY 9-1-1 STATE GRANT COMPLIANCE SUPPLEMENT ----------------------------------------------------------- TABLE OF CONTENTS ------------------------------- NJFIS Account Number

OFFICE OF INFORMATION TECHNOLOGY 9-1-1 STATE GRANT COMPLIANCE SUPPLEMENT ----------------------------------------------------------- TABLE OF CONTENTS ------------------------------- NJFIS Account Number

Effort Reporting Regulations

Effort Reporting Regulations Objectives Become familiar with the federal requirements for Effort Reporting Receive a broad understanding of what is Effort and Effort Reporting, and the relationship between

Effort Reporting Regulations Objectives Become familiar with the federal requirements for Effort Reporting Receive a broad understanding of what is Effort and Effort Reporting, and the relationship between

Dennis G. Smith Director, Center for Medicaid and State Operations

DEPARTMENT OF HEALTH & HUMAN SERVICES Office of Inspector General 5 Washington, D.C. 20201 TO: Dennis G. Smith Director, Center for Medicaid and State Operations FROM: /P epky inspector General for Audit

DEPARTMENT OF HEALTH & HUMAN SERVICES Office of Inspector General 5 Washington, D.C. 20201 TO: Dennis G. Smith Director, Center for Medicaid and State Operations FROM: /P epky inspector General for Audit

Report Number: A-03-04-002 13

DEPARTMENT OF HEALTH & HUMAN SERVICES OFFICE OF INSPECTOR GENERAL OFFICE OF AUDIT SERVICES 150 S. INDEPENDENCE MALL WEST SUITE 3 16 PHILADELPHIA, PENNSYLVANIA 19 106-3499 Report Number: A-03-04-002 13

DEPARTMENT OF HEALTH & HUMAN SERVICES OFFICE OF INSPECTOR GENERAL OFFICE OF AUDIT SERVICES 150 S. INDEPENDENCE MALL WEST SUITE 3 16 PHILADELPHIA, PENNSYLVANIA 19 106-3499 Report Number: A-03-04-002 13

School Based Health Services: Medicaid Cost Report and Cost Settlement Training FY 2014-2015

School Based Health Services: Medicaid Cost Report and Cost Settlement Training FY 2014-2015 State of West Virginia Department of Health and Human Services Bureau of Medical Services November 2015 Agenda

School Based Health Services: Medicaid Cost Report and Cost Settlement Training FY 2014-2015 State of West Virginia Department of Health and Human Services Bureau of Medical Services November 2015 Agenda

U.S. Chemical Safety and Hazard Investigation Board Should Determine the Cost Effectiveness of Performing Improper Payment Recovery Audits

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL U.S. Chemical Safety and Hazard Investigation Board Should Determine the Cost Effectiveness of Performing Improper Payment Recovery Audits

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL U.S. Chemical Safety and Hazard Investigation Board Should Determine the Cost Effectiveness of Performing Improper Payment Recovery Audits

93.994 MATERNAL AND CHILD SERVICES BLOCK GRANT TO THE STATES

APRIL 2011 93.994 MATERNAL AND CHILD SERVICES BLOCK GRANT TO THE STATES State Project/Program: SCHOOL NURSE FUNDING INITIATIVE U. S. Department of Health and Human Services Health Resources and Services

APRIL 2011 93.994 MATERNAL AND CHILD SERVICES BLOCK GRANT TO THE STATES State Project/Program: SCHOOL NURSE FUNDING INITIATIVE U. S. Department of Health and Human Services Health Resources and Services

perform cost settlements to ensure that future final payments for school-based services are based on actual costs.

Page 2 Kerry Weems perform cost settlements to ensure that future final payments for school-based services are based on actual costs. In written comments on our draft report, the State agency concurred

Page 2 Kerry Weems perform cost settlements to ensure that future final payments for school-based services are based on actual costs. In written comments on our draft report, the State agency concurred

General Information. the ratio between the total indirect expenses and some direct cost base.

These guidelines include information related to: General Information A. Definition of Indirect Costs B. Types of Indirect Rates C. Determination of Indirect Cost Rates and Cost Allocation D. Submissions

These guidelines include information related to: General Information A. Definition of Indirect Costs B. Types of Indirect Rates C. Determination of Indirect Cost Rates and Cost Allocation D. Submissions

Office of Inspector General Office of Audit

EMPLOYMENT AND TRAINING ADMINISTRATION Atlanta Office of Inspector General Office of Audit THE CITY OF ATLANTA, GEORGIA DID NOT ADEQUATELY MANAGE WELFARE-TO- WORK AND WORKFORCE INVESTMENT ACT GRANTS Date

EMPLOYMENT AND TRAINING ADMINISTRATION Atlanta Office of Inspector General Office of Audit THE CITY OF ATLANTA, GEORGIA DID NOT ADEQUATELY MANAGE WELFARE-TO- WORK AND WORKFORCE INVESTMENT ACT GRANTS Date

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL. July 13, 2015

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL AUDIT SERVICES Chicago/Kansas City Audit Region July 13, 2015 Control Number ED-OIG/A05O0005 Dr. June St. Clair Atkinson State Superintendent

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL AUDIT SERVICES Chicago/Kansas City Audit Region July 13, 2015 Control Number ED-OIG/A05O0005 Dr. June St. Clair Atkinson State Superintendent

Contents. Staff Involved with ARMAC Time Study 11. Time Study and Reimbursement Methodology 12. Monitoring 15. Attachment I 18.

Arkansas Medicaid Administrative Claiming (ARMAC) Resource Guide FFaal lll 2000066 Arrkkaann ss aa ss Deeppaarrt ttmeennt o f EEdduuccaat ttiionn, io,, SSppeecci iial a ll EEdduuccaat ttiionn io Unni iitt

Arkansas Medicaid Administrative Claiming (ARMAC) Resource Guide FFaal lll 2000066 Arrkkaann ss aa ss Deeppaarrt ttmeennt o f EEdduuccaat ttiionn, io,, SSppeecci iial a ll EEdduuccaat ttiionn io Unni iitt

North Carolina Division of Medical Assistance

North Carolina Division of Medical Assistance Medicaid Administrative Claiming for Adults and Children (MAC) Operation Guide Implementation Effective Date July 1, 2014 Page 1 Table of Contents 1. Introduction...

North Carolina Division of Medical Assistance Medicaid Administrative Claiming for Adults and Children (MAC) Operation Guide Implementation Effective Date July 1, 2014 Page 1 Table of Contents 1. Introduction...

NO. 160. AN ACT RELATING TO THE COORDINATION, FINANCING AND DISTRIBUTION OF LONG-TERM CARE SERVICES. (H.782)

") NO. 160. AN ACT RELATING TO THE COORDINATION, FINANCING AND DISTRIBUTION OF LONG-TERM CARE SERVICES. (H.782) It is hereby enacted by the General Assembly of the State of Vermont: Sec. 1. DEFINITIONS For

NO. 160. AN ACT RELATING TO THE COORDINATION, FINANCING AND DISTRIBUTION OF LONG-TERM CARE SERVICES. (H.782) It is hereby enacted by the General Assembly of the State of Vermont: Sec. 1. DEFINITIONS For

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA PERFORMANCE AUDIT STATE HEALTH PLAN RISK ASSESSMENT SEPTEMBER 2011 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR PERFORMANCE AUDIT STATE HEALTH PLAN RISK ASSESSMENT

STATE OF NORTH CAROLINA PERFORMANCE AUDIT STATE HEALTH PLAN RISK ASSESSMENT SEPTEMBER 2011 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR PERFORMANCE AUDIT STATE HEALTH PLAN RISK ASSESSMENT

SAMPLE INDIRECT COST PROPOSAL FORMAT FOR NONPROFIT ORGANIZATIONS

SAMPLE INDIRECT COST PROPOSAL FORMAT FOR NONPROFIT ORGANIZATIONS A. INTRODUCTION Name of Organization (nonprofit) is a nonprofit located in Anytown, USA. The nonprofit administers a variety of programs

SAMPLE INDIRECT COST PROPOSAL FORMAT FOR NONPROFIT ORGANIZATIONS A. INTRODUCTION Name of Organization (nonprofit) is a nonprofit located in Anytown, USA. The nonprofit administers a variety of programs

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission National Archives www.archives.gov/nhprc June 17, 2015 Table of Contents USE OF THE

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission National Archives www.archives.gov/nhprc June 17, 2015 Table of Contents USE OF THE

Documentation of salaries and wages is often necessary to support

Documentation of salaries and wages is often necessary to support charges to specific funding sources (resources), instructional settings (goals), and activities (functions). Some level of formalized time

Documentation of salaries and wages is often necessary to support charges to specific funding sources (resources), instructional settings (goals), and activities (functions). Some level of formalized time

MEDICARE RECOVERY AUDIT CONTRACTORS AND CMS S ACTIONS TO ADDRESS IMPROPER PAYMENTS, REFERRALS OF POTENTIAL FRAUD, AND PERFORMANCE

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL MEDICARE RECOVERY AUDIT CONTRACTORS AND CMS S ACTIONS TO ADDRESS IMPROPER PAYMENTS, REFERRALS OF POTENTIAL FRAUD, AND PERFORMANCE Daniel

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL MEDICARE RECOVERY AUDIT CONTRACTORS AND CMS S ACTIONS TO ADDRESS IMPROPER PAYMENTS, REFERRALS OF POTENTIAL FRAUD, AND PERFORMANCE Daniel

[46 DEPARTMENT. %",,. Washington, D.C. 20201 FROM: SUBJECT: Neil Donovan Director, Audit Liaison Staff Centers for Medicare & Medicaid Services TO:

[46 DEPARTMENT ' ' \~'''v'cts OF HEALTH & HUMAN SERVICES Office of Inspector General %",,. Washington, D.C. 20201 TO: FROM: SUBJECT: Neil Donovan Director, Audit Liaison Staff Centers for Medicare & Medicaid

[46 DEPARTMENT ' ' \~'''v'cts OF HEALTH & HUMAN SERVICES Office of Inspector General %",,. Washington, D.C. 20201 TO: FROM: SUBJECT: Neil Donovan Director, Audit Liaison Staff Centers for Medicare & Medicaid

AUG 1 3 2003. ctor General. State of California: Review of Public Health Preparedness and Response for Bioterrorism Program Funds (A-09-02-0 1007)

") DEPARTMENT OF HEALTH & HUMAN SERVICES Off ice of Inspector General AUG 1 3 2003 Washington, D.C. 20201 TO: Julie L. Gerberding, M.D., M.P.H. Director Centers for Disease Control and Prevention FROM: Dara

DEPARTMENT OF HEALTH & HUMAN SERVICES Off ice of Inspector General AUG 1 3 2003 Washington, D.C. 20201 TO: Julie L. Gerberding, M.D., M.P.H. Director Centers for Disease Control and Prevention FROM: Dara

August 2014 Report No. 14-043

John Keel, CPA State Auditor A Report on On-site Audits of Residential Child Care Providers Report No. 14-043 A Report on On-site Audits of Residential Child Care Providers Overall Conclusion Three of

John Keel, CPA State Auditor A Report on On-site Audits of Residential Child Care Providers Report No. 14-043 A Report on On-site Audits of Residential Child Care Providers Overall Conclusion Three of

Medicaid Claims Processing Activity April 1, 2012 through September 30, 2012 Medicaid Program Department of Health

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Medicaid Claims Processing Activity April 1, 2012 through September 30, 2012 Medicaid Program

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Medicaid Claims Processing Activity April 1, 2012 through September 30, 2012 Medicaid Program

The University of Georgia Service Center Policy

TABLE OF CONTENTS The University of Georgia Service Center Policy 1. INTRODUCTION... 4 2. SCOPE... 4 2.1. Recharge Activities... 4 2.2. Service Centers... 4 2.3. Specialized Service Centers... 4 3. INTENT....

TABLE OF CONTENTS The University of Georgia Service Center Policy 1. INTRODUCTION... 4 2. SCOPE... 4 2.1. Recharge Activities... 4 2.2. Service Centers... 4 2.3. Specialized Service Centers... 4 3. INTENT....

William J. Daley, Regional Counsel, 6AC. Henry S. Czauski, Acting Director of Departmental Enforcement Center, CV

Issue Date March 21, 2008 Audit Report Number 2008-FW-1008 TO: Gretchen Marchand Director, Multifamily Housing Division, 6JHMLAX William J. Daley, Regional Counsel, 6AC Henry S. Czauski, Acting Director

Issue Date March 21, 2008 Audit Report Number 2008-FW-1008 TO: Gretchen Marchand Director, Multifamily Housing Division, 6JHMLAX William J. Daley, Regional Counsel, 6AC Henry S. Czauski, Acting Director

Commonwealth of Kentucky School District Medicaid SBHS Cost Report August 2013

Commonwealth of Kentucky School District Medicaid SBHS Cost Report August 2013 Agenda 1 Fairbanks Introduction 2 Medicaid Program 3 Kentucky Medicaid School Based Program 4 Program Enhancements- SBHS Cost

Commonwealth of Kentucky School District Medicaid SBHS Cost Report August 2013 Agenda 1 Fairbanks Introduction 2 Medicaid Program 3 Kentucky Medicaid School Based Program 4 Program Enhancements- SBHS Cost