Fraud Risks in Higher Education

|

|

|

- Agatha Martin

- 10 years ago

- Views:

Transcription

1 iftonlar 2014 Cl Fraud Risks in Higher Education AACS Annual Conference November 17, 2014 CLAconnect.com Diane C. DiFebbo, CPA, CFE Brenda Scherer, CPA

2 Learning Objectives Understand how fraud can occur Learn procedures you can implement to prevent fraud Learn how to detect fraud 2

3 Fraud Headlines in 2014 Fast Train Owner and Three Admissions Reps arrested for Theft of Student Aid Miami, FL October 2014 Mother and Daughter Plead Guilty in Student Aid Fraud Investigation Richmond, VA Sept 2014 Former Merrimack kcollege Director of Financial i Aid Charged with Fraud Boston, MA July 2014 Cousins Sentenced dfor Role in Student t Loan Fraud Scheme Madison, WI July

4 Fraud Headlines in 2014 NYC Woman Pleads Guilty in Federal Court to Fraud in Connection with Federal Financial Aid to Attend Online State College June 2014 Record $8 Billion Tax Fraud Gets Ex Lawyer 15 Years June 2014 Former UGA registrar office employee charged with ih 42 counts of identity fraud and 19 counts of financial card fraud February 2014 Delta Air Lines employee from Minnesota accused of $22 million fraud July

5 The Fraud Problem: How Big is Fraud? Globally, organizations lose an estimated 5% of annual revenues Applied to 2013 Gross World Product: $3.7 Trillion potential total fraud loss Source: Association ofcertified FraudExaminers 2014 Report tothe the Nation onoccupational Fraud & Abuse 5

6 The Cost of Fraud 6

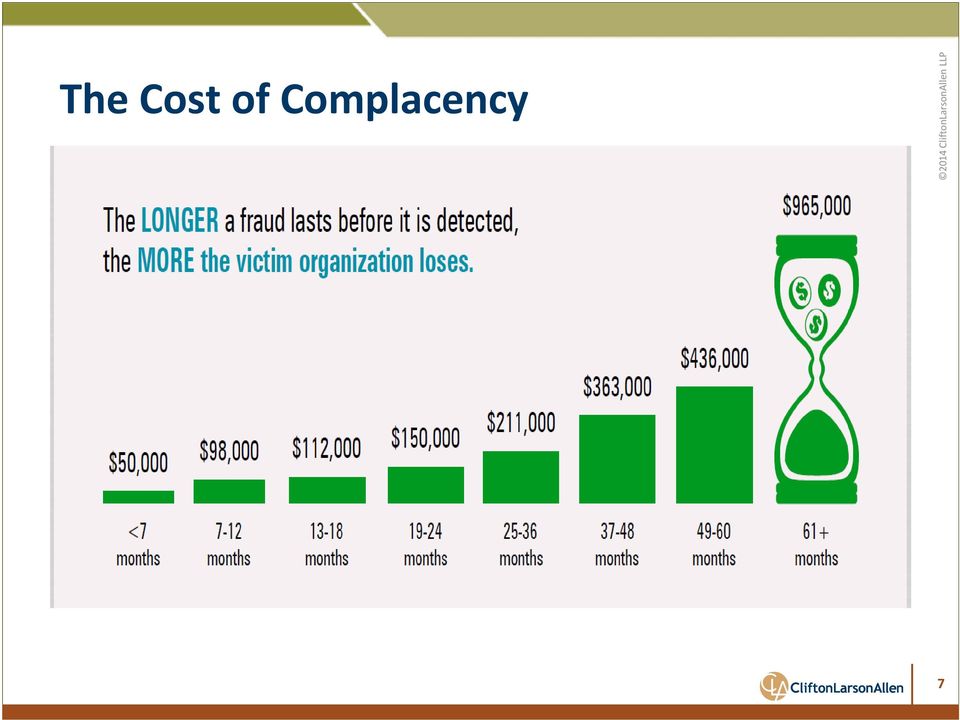

7 The Cost of Complacency 7

8 Types offraud Occupational fraud Asset misappropriation Corruption Financial statement fraud Student financial aid fraud 8

9 Common Situations Is this Your Organization? But Judy is the only person handling cash. It s very efficient that way I sign every check so there can t be any fraud I only trust Joe with that task Suzie would never do that to me. John has access to change pay rates, but he never would 9

10 How Harmful Can Fraud Be? Loss of assets Cost of investigation is very high Ability to prosecute is very low Loss of integrity/reputation Once the media reports it, possible Loss of students vendors, or at least restrictions Loss of vendors, or atleast restrictions Loss of employees Loss of focus on operations 10

11 Why Fraud Occurs Incentive/ Pressure The Fraud Triangle Opportunity Rationalize/ Attitude 11

12 Fraud Quiz The most common type of fraud is: a. Fraudulent financial reporting b. Misappropriation of assets c. Corruption (conflict of interest) d. Petty theft e. Identity theft 12

d.")

13 Fraud Quiz The average amount of time from inception to detection of fraud schemes is: a. 1 5 months b months c months d months e. Greater than 5 years 13

14 Real Life Example #1 Executive Vice President of an entity in Arizona Lived a lavish lifestyle Created seven false vendors which he used to bill the entity for personal items Occurred over a seven year period Employee was writing a book on how to embezzle funds from your employer! Theft of $11 million 14

15 Real Life Example #2 Prisoner working in the education department of that Prison with access to personal information Applied for aid in an online program Excess aid was given to the accused through a Higher One card Finance office became suspicious and contacted the online learning center to verify extent of participation Theft Loss: $467,500 over a 10 month period 15

16 Real Life Example #3 Fraud ring involving 65 individuals ring leader former SFA department student worker Individuals recruited for personal info Checks go to recruits to avoid duplicate address who would give the Leaders a cut of the returned financial aid Part time employee noticed the same handwriting on several applications Total Loss: $539,000 over a 15 month period 16

17 Real Life Example #4 Grandmother, children and grandchildren involved Family members enrolled and applied for aid at multiple online schools Financial Aid Director noticed a number of students using the same addresses and telephone numbers Theft Loss: Nearly $1 Million 17

18 Real Life Example #5 Employee was the secretary of a business Handled financial records including check writing Ability to transfer from the line of credit to the checking account to handle overdrafts Had access to business credit/debit cards Embezzlement was more than $200, over a three year period Other staff noticed funds weremissing from the business bank account Husband had lost job early on 18

19 Real Life Example #6 Representative of Bursar Office handled CPE and night classes Payment was required to be done by credit card Accounting reconciled credit card deposits to Bursar records (prepared by representative) Person was highly trusted Person was 45 Lived a very high h level llife style tl 19

Person was highly trusted Person was 45 Lived a very high h")

20 Real Life Examples #6 (Continued) The student would pay for classes using their credit card The Bursar would take one of their personal credit cards and make a refund for the exact payment The student got a receipt and a payment showed on their credit card and the class records were manipulated by the Representative One credit card company caught the pattern Theft Loss: $125,000 over one year 20

21 21

22 What Can You Do Set the tone at the top Strengthen your internal controls Be aware of Red Flags and act on what you see Know what s going on in your organization Perform random testing or other unpredictable procedures 22

23 Creating an Ethical Organization Culture Setting the tone at the top Establishing a code of conduct Creating a positive workplace environment Hiring and promoting ethical employees Providing ethics training Disciplining and prosecuting violators 23

24 Internal Testing / Identification YouCan Do Duplicate student social security numbers Duplicate student addresses Duplicate student last names Identical student coursework Increase in student withdrawals Withdrawals with similar names, addresses, zip codes 24

25 Fraud Controls Cost / Benefit In general, as control and security increases: occurrence decreases 25

26 Fraud Quiz Which measures are the most helpful in preventing fraud: a. Ethics training for employees b. Fraud audits c. Strong internal controls d. Background checks on new employees e. Willingness to prosecute 26

27 Fraud Quiz The age group that is most likely to commit fraud is: a. Less than 30 years old b years old c years old d years old e. greater than 60 years old 27

28 Fraud Quiz The education level of people who commit fraud is more likely to be those with: a. Post graduate degree b. Bachelors degree c. High school education d. Less than high school education e. Education level does not appear to be relevant 28

29 Fraud Quiz Frauds are generally detected by: a. Internal audit b. Tip from a vendor c. External audit d. Tip from a customer e. Tip from an employee 29

30 Other Fraud Stats 42% Employees 1 5 Years 66.8% Male 5.9% Education 30

31 Recovery oflosses 58% Of cases reported have no recovery 31

32 Questions 32

33 ftonlar 2014 Clif Diane C. DiFebbo, CPA, CFE Principal Brenda Scherer, CPA Manager CLAconnect.com twitter.com/ CLAconnect facebook.com/ cliftonlarsonallen linkedin.com/company/ cliftonlarsonallen 33

34 Addendum 34

35 Fraud Awareness Types of Controls Automated Controls controls that automatically occur. Examples: Computer passwords are implemented to automatically control access to the systems. Manual Controls controls that must be manually completed. Examples: Account reconciliations must be manually completed using the account statement and the general ledger history. 35

36 Fraud Controls Prevention Preventative Controls designed to prevent fraud before it has occurred. Examples: Multiple people or lock boxes for checks Timely account balancing and reconciling and reviewing Passwords and physical safeguards Authorization and limits Segregation of duties 36

37 Fraud Controls Detection Detective Controls designed to detect fraud after it has occurred. Examples: Exception reports Systems maintenance reports Documentation reviews Internal Audit/Periodic Sampling 37

38 Key Control Questions The following are questions that every organization should ask themselves when evaluating key internal control areas: 38

39 Accounts Payable and Disbursements Does your organization use purchase orders? Who creates new vendors? Does someone else approve new vendors? Can the same person create a vendor and enter an invoice for payment? Can the same person enter an invoice and cut a check? Do checks print without a signature on them? Who signs the checks? Is the check stock blank? Is it kept secured? 39

40 Payroll Are timesheets processed prior to being approved? Can those processing payroll change pay rates? If the reviewer changes pay rate or hours after review, would it be caught? Can those in accounting access the payroll system? 40

41 Cash Receipts Who receives cash in your organization? Are two employees present when counting cash? Does your organization use duplicate receipts and/or a cash control ll log? Does the person receiving cash have access to record receipts in the I/T system? Does someone outside of the accounting department receive bank statements? Who prepares the bank deposit? How often? 41

42 How to Identify Embezzlement in Your Employees Significant lifestyle changes Living beyond their means Rarely takes vacation Reluctant to provide information to management Tireless worker, seems indispensable Co workers are intimidated by them Typically, a repeat offender 42

43 Signs thatembezzlement is Occurring Increasing Accounts Payable or Receivable Expenses unusually high h or large increases Unexplained adjustments to G/L accounts Decreasing collection rates Increased adjustments on bank reconciliation Discrepancies between bank deposits and posting No cash in deposits Unusual payroll increases 43

44 Fraud Prevention Checklist 1. Is ongoing anti fraud training provided to all employees? 2. Is an effective fraud reporting mechanism in place? 3. Does management make it clear that t fraud will not be tolerated? 4. Are fraud risk assessments performed to identify and mitigate vulnerabilities to fraud? 5. Are strong anti fraud controls in place and operating effectively? 44

45 Fraud Prevention Checklist (Continued) 6. Can the internal audit department operate without undue influence fromsenior management? 7. Does the hiring process include background checks, drug screening, etc.? 8. Are employee support programs in place? 9. Does the culture promote an open door policy, where employees can speak freely about pressures? 10. Are surveys done to assess employee morale? 45

46 The OIG Report What they found Variations of the following: Ringleader solicits identifying informationfrom from individuals (often by promising a small portion of the financial aid proceeds and/or from incarcerated individuals). Ring leader completes and submits multiple financial aid applications (usually on line using the Department s FAFSA on the Web application) using the identifiers collected. Ring leader targets institutions with low tuition (i.e. public community colleges) or institutions that offer distance education programs 46

47 The OIG Report What they found Variations of the following: Ring leader applies for admission i and completes lt registration it ti process at open admissions schools where academic transcripts and test scores are not required Ring leader participates in just enough online instruction to qualify for a disbursement of financial aid for the term or other payment period Schools release financial aid credit balance, after deducting minimal institutional charges Ring leader distributes proceeds to some of the individuals who provided their identifiers Ring leader pockets most of the proceeds 47

48 The OIG Report What they found As of August 1, 2011, OIG had 100 open fraud ring investigations with 49 additional being evaluated for investigative merits Since 2005, OIG has assisted in the prosecution of 215 participants in 42 different fraud rings resulting in criminal convictions and $7.5 million in fines and restitution 48

49 The OIG Recommendations Type of Action Recommendation Legis lative Reduce cost of attendance for those enrolled via distance Regulat tory Require institutions to verify identity of those enrolled via distance learning Require institutions to retain IP addresses for those engaged in distance learning courses 49

50 The OIG Recommendations Type of Action Recommendation Admin nistrative Designate high school graduation status & statement of educational purpose for verification Develop edits to flag potential fraud participants in the Department s Central Processing System and National Student Loan Data System Explore a computer matching agreement with the Federal Bureau of Prisons and State prison systems Establish controls that prevent multiple PINs from being delivered to a single address without verification of identity Using current regulatory authority, establish repayment liabilities for fraud ring participants that are not prosecuted Ensure that pre trial diversions are recognized as convictions for purposes p of debarment or exclusion Issue Dear Colleague Letter that alerts institutions to the problem of fraud rings and reminds them of their obligations under existing regulations 50

Is There Anyway to Prevent Fraud? Bill Gady, CGA CPA Partner

Is There Anyway to Prevent Fraud? Bill Gady, CGA CPA Partner Learning Objectives: Understand how fraud can occur Learn procedures you can implement to prevent fraud Learn how to detect fraud Common Situations

Is There Anyway to Prevent Fraud? Bill Gady, CGA CPA Partner Learning Objectives: Understand how fraud can occur Learn procedures you can implement to prevent fraud Learn how to detect fraud Common Situations

Sharon Kurek, CPA, CFE Director of Internal Audit

Sharon Kurek, CPA, CFE Director of Internal Audit What You Will Take Aware With You Definition of Internal Auditing Scope of Audit Activities Risk and Control Process Common Audit Topics Fraud Awareness

Sharon Kurek, CPA, CFE Director of Internal Audit What You Will Take Aware With You Definition of Internal Auditing Scope of Audit Activities Risk and Control Process Common Audit Topics Fraud Awareness

Fraud Control Theory

13 Fraud Control Theory Using a variation of a saying from the 1960s, fraud happens. Like all costs of doing business, fraud must be managed. Management must recognize that people commit fraudulent acts

13 Fraud Control Theory Using a variation of a saying from the 1960s, fraud happens. Like all costs of doing business, fraud must be managed. Management must recognize that people commit fraudulent acts

How To Prevent Fraud On A Credit Card

Fraud Detection and Prevention Financial Management Advisory Council August 28, 2014 Sarah Mahugh, CPA, MBA Financial Audit Audit Manager Overview Fraud trends Fraud Risks and internal controls Case Studies

Fraud Detection and Prevention Financial Management Advisory Council August 28, 2014 Sarah Mahugh, CPA, MBA Financial Audit Audit Manager Overview Fraud trends Fraud Risks and internal controls Case Studies

Internal Controls for Small Organizations. Jen Parker, CPA Director of Accounting & Finance US Youth Soccer

Internal Controls for Small Organizations Jen Parker, CPA Director of Accounting & Finance US Youth Soccer Fraud Statistics: The following statistics about fraud and white collar crime are from the Association

Internal Controls for Small Organizations Jen Parker, CPA Director of Accounting & Finance US Youth Soccer Fraud Statistics: The following statistics about fraud and white collar crime are from the Association

Accounts Payable Best Practices

Accounts Payable Best Practices Presented by: Eddy Castaneda, CPA, MBA Accounts Payable Best Practices Top Practices AP Top Practices Document your current AP procedures Can identify overlapping work Can

Accounts Payable Best Practices Presented by: Eddy Castaneda, CPA, MBA Accounts Payable Best Practices Top Practices AP Top Practices Document your current AP procedures Can identify overlapping work Can

Making Your Fraud Vision 20 / 20. Thomas R. Strause, CIA, CFE, CBA, CISA, CFSA, CICA Partner FOS tstrause@fosaudit.

Making Your Fraud Vision 20 / 20 Thomas R. Strause, CIA, CFE, CBA, CISA, CFSA, CICA Partner [email protected] 610-603-5603 Topics to be Covered + Summary of Fraud Statistics ACFE 2014 Report + Current

Making Your Fraud Vision 20 / 20 Thomas R. Strause, CIA, CFE, CBA, CISA, CFSA, CICA Partner [email protected] 610-603-5603 Topics to be Covered + Summary of Fraud Statistics ACFE 2014 Report + Current

Avoiding Theft in Your Nonprofit Ohio Attorney General Mike DeWine

Avoiding Theft in Your Nonprofit Ohio Attorney General Mike DeWine 1 Dear Nonprofit Leader, The single greatest asset of a nonprofit is arguably its reputation. When theft or misappropriation of assets

Avoiding Theft in Your Nonprofit Ohio Attorney General Mike DeWine 1 Dear Nonprofit Leader, The single greatest asset of a nonprofit is arguably its reputation. When theft or misappropriation of assets

Fraud Awareness Training

UT System Administration General Compliance Training Fall 2014 This training will take approximately 20 minutes to complete Objectives What is occupational fraud Common myths about fraud Conditions for

UT System Administration General Compliance Training Fall 2014 This training will take approximately 20 minutes to complete Objectives What is occupational fraud Common myths about fraud Conditions for

Leveraging Your ERP System to Enhance Internal Controls

July 2015 Leveraging Your ERP System to Enhance Internal Controls Public Sector Entities By Melinda J. DeCorte, CPA, CFE, CGFM, and Jeanne M. Owings, Principal Audit Tax Advisory Risk Performance Even

July 2015 Leveraging Your ERP System to Enhance Internal Controls Public Sector Entities By Melinda J. DeCorte, CPA, CFE, CGFM, and Jeanne M. Owings, Principal Audit Tax Advisory Risk Performance Even

Internal Controls Best Practices

Internal Controls Best Practices This list includes the most common internal controls applied by small to medium sized businesses to their operations. It includes controls that apply to the processes most

Internal Controls Best Practices This list includes the most common internal controls applied by small to medium sized businesses to their operations. It includes controls that apply to the processes most

Steven Boyer Vice-President, Gallagher Bassett Services Inc.

Employee Dishonesty and Fraud Motive, Rationale & Opportunity Steven Boyer Vice-President, Gallagher Bassett Services Inc. Randall Wilson, CPA/CFF, CFE, Cr.FA Partner, National Practice Director Fraud

Employee Dishonesty and Fraud Motive, Rationale & Opportunity Steven Boyer Vice-President, Gallagher Bassett Services Inc. Randall Wilson, CPA/CFF, CFE, Cr.FA Partner, National Practice Director Fraud

NONPROFIT FINANCIAL MANAGEMENT SELF ASSESSMENT TOOL

NONPROFIT FINANCIAL MANAGEMENT SELF ASSESSMENT TOOL I. Financial Planning/Budget Systems 1. Organization has a comprehensive annual budget which includes all sources and uses of funds for all aspects of

NONPROFIT FINANCIAL MANAGEMENT SELF ASSESSMENT TOOL I. Financial Planning/Budget Systems 1. Organization has a comprehensive annual budget which includes all sources and uses of funds for all aspects of

September 28, 2011. Audit s Role in Governance, Risk Management and Internal Control

September 28, 2011 Internal Audit Overview Audit s Role in Governance, Risk Management and Internal Control Mission Provide independent, objective assurance and advisory services designed to add value

September 28, 2011 Internal Audit Overview Audit s Role in Governance, Risk Management and Internal Control Mission Provide independent, objective assurance and advisory services designed to add value

1. SEGREGATION OF DUTIES IS ESSENTIAL

The way a church handles money can present a positive or negative witness. Churches need to be diligent in handling money to encourage integrity and positive Biblical stewardship. Every step should be

The way a church handles money can present a positive or negative witness. Churches need to be diligent in handling money to encourage integrity and positive Biblical stewardship. Every step should be

MEMORANDUM INTERNAL CONTROL REQUIREMENTS FOR NON-PROFITS

DIVISION OF CHILD CARE AND EARLY CHILDHOOD EDUCATION HEALTH AND NUTRITION UNIT P O BOX 1437, SLOT S 155 501-320-8982 FAX: 501-682-2334 TDD: 501-682-1550 TO: NON-PROFIT INSTITUTIONS FROM: HEALTH AND NUTRITION

DIVISION OF CHILD CARE AND EARLY CHILDHOOD EDUCATION HEALTH AND NUTRITION UNIT P O BOX 1437, SLOT S 155 501-320-8982 FAX: 501-682-2334 TDD: 501-682-1550 TO: NON-PROFIT INSTITUTIONS FROM: HEALTH AND NUTRITION

Fraud Prevention, Detection and Response. Dean Bunch, Ernst & Young Fraud Investigation & Dispute Services

Fraud Prevention, Detection and Response. Dean Bunch, Ernst & Young Fraud Investigation & Dispute Services Agenda Fraud Overview Fraud Prevention Fraud Detection Fraud Response Questions Page 2 Fraud Overview

Fraud Prevention, Detection and Response. Dean Bunch, Ernst & Young Fraud Investigation & Dispute Services Agenda Fraud Overview Fraud Prevention Fraud Detection Fraud Response Questions Page 2 Fraud Overview

Sobel & Co. s Nonprofit and Social Services Group presents. Your Organization is Vulnerable: The Facts About Nonprofits and Fraud

Sobel & Co. s Nonprofit and Social Services Group presents Your Organization is Vulnerable: The Facts About Nonprofits and Fraud Why Smart People Do Dumb Things If you are above average intelligence -

Sobel & Co. s Nonprofit and Social Services Group presents Your Organization is Vulnerable: The Facts About Nonprofits and Fraud Why Smart People Do Dumb Things If you are above average intelligence -

Internal Controls and Fraud Detection & Prevention. Harold Monk and Jennifer Christensen

Internal Controls and Fraud Detection & Prevention Harold Monk and Jennifer Christensen 1 Common Fraud Statements Everyone in government has an honest and charitable heart. It may happen other places,

Internal Controls and Fraud Detection & Prevention Harold Monk and Jennifer Christensen 1 Common Fraud Statements Everyone in government has an honest and charitable heart. It may happen other places,

Detecting, Preventing, and Mitigating Identity Theft

THE RED FLAGS RULE Detecting, Preventing, and Mitigating Identity Theft Training for Ball State University s Identity Theft Protection Program What is the Red Flag Rule? Congress passed the Fair and Accurate

THE RED FLAGS RULE Detecting, Preventing, and Mitigating Identity Theft Training for Ball State University s Identity Theft Protection Program What is the Red Flag Rule? Congress passed the Fair and Accurate

Financial Services Group

Fraud Detection and Prevention Presented by: Carrie Kennedy, CPA, Partner Anthony Porter, CPA, Manager 1 The material appearing in this presentation is for informational purposes only and should not be

Fraud Detection and Prevention Presented by: Carrie Kennedy, CPA, Partner Anthony Porter, CPA, Manager 1 The material appearing in this presentation is for informational purposes only and should not be

Internal Controls over Cash for Small Nonprofits

Internal Controls over Cash for Small Nonprofits Internal controls may be a sensitive issue in small nonprofit organizations. These organizations are built on the concepts of honesty, truthfulness, and

Internal Controls over Cash for Small Nonprofits Internal controls may be a sensitive issue in small nonprofit organizations. These organizations are built on the concepts of honesty, truthfulness, and

MEMORANDUM. Municipal Officials. From: Karen Horn, Director, Public Policy and Advocacy; and Abby Friedman, Director, Municipal Assistance Center

MEMORANDUM To: Municipal Officials From: Karen Horn, Director, Public Policy and Advocacy; and Abby Friedman, Director, Municipal Assistance Center 89 Main Street, Suite 4 Montpelier, Vermont 05602-2948

MEMORANDUM To: Municipal Officials From: Karen Horn, Director, Public Policy and Advocacy; and Abby Friedman, Director, Municipal Assistance Center 89 Main Street, Suite 4 Montpelier, Vermont 05602-2948

INTERNAL CONTROL QUESTIONNAIRE OFFICE OF INTERNAL AUDIT UNIVERSITY OF THE VIRGIN ISLANDS

Cabinet Member or Representative responsible for completing this form: INSTRUCTIONS FOR COMPLETING THIS FORM: Answer each question by placing an X in the either the Yes, No,, or Applicable () column. Provide

Cabinet Member or Representative responsible for completing this form: INSTRUCTIONS FOR COMPLETING THIS FORM: Answer each question by placing an X in the either the Yes, No,, or Applicable () column. Provide

RED FLAGS OF FRAUD MAY 13, 2014 IIA AUSTIN CHAPTER

MAY 13, 2014 IIA AUSTIN CHAPTER 2014 by the Association of Certified Fraud Examiners, Inc. Revised: 3/26/14 No portion of this work may be reproduced or transmitted in any form or by any means electronic

MAY 13, 2014 IIA AUSTIN CHAPTER 2014 by the Association of Certified Fraud Examiners, Inc. Revised: 3/26/14 No portion of this work may be reproduced or transmitted in any form or by any means electronic

A Municipal Checklist for Internal Control-Part I, Cash Controls

A Municipal Checklist for Internal Control-Part I, Cash Controls I. General Internal Control & Banking 1 Is a professional (independent) audit done annually? 2 If you have an annual audit was the most

A Municipal Checklist for Internal Control-Part I, Cash Controls I. General Internal Control & Banking 1 Is a professional (independent) audit done annually? 2 If you have an annual audit was the most

Fraud: Real Stories, Real People, Real Impact

Fraud: Real Stories, Real People, Real Impact Chris Harper, CPA, MBA Senior Manager Types of Fraud Asset misappropriation Fraudulent financial reporting Identity theft Detection Skills The Fraud Triangle

Fraud: Real Stories, Real People, Real Impact Chris Harper, CPA, MBA Senior Manager Types of Fraud Asset misappropriation Fraudulent financial reporting Identity theft Detection Skills The Fraud Triangle

The policy and procedural guidelines contained in this handbook are designed to:

BASIC POLICY STATEMENT The Mikva Challenge is committed to responsible financial management. The entire organization including the board of directors, administrators, and staff will work together to make

BASIC POLICY STATEMENT The Mikva Challenge is committed to responsible financial management. The entire organization including the board of directors, administrators, and staff will work together to make

Payment Procedures. Corruption Prevention Department

Payment Procedures Corruption Prevention Department best practices 貪 CONTENTS Pages Introduction 1 Procedural Guidelines 1 Payment Methods 2 Autopay 2 Cheques 3 Petty Cash 3 Payment Records 4 Control and

Payment Procedures Corruption Prevention Department best practices 貪 CONTENTS Pages Introduction 1 Procedural Guidelines 1 Payment Methods 2 Autopay 2 Cheques 3 Petty Cash 3 Payment Records 4 Control and

ACCOUNTING RECORDS: HOW THEY ARE USED TO CONCEAL FRAUD. ROSANNE TERHART, CFE, CA Senior Manager BDO Canada LLP Vancouver, British Columbia Canada

Once an employee commits fraud, he has limited time to conceal the financial transaction in the accounting records. Learn how employees hide these fraudulent transactions and what to look for when reviewing

Once an employee commits fraud, he has limited time to conceal the financial transaction in the accounting records. Learn how employees hide these fraudulent transactions and what to look for when reviewing

THE ABC S OF DATA ANALYTICS

THE ABC S OF DATA ANALYTICS ANGEL BUTLER MAY 23, 2013 HOUSTON AREA SCHOOL DISTRICT INTERNAL AUDITORS (HASDIA) AGENDA Data Analytics Overview Data Analytics Examples Compliance Purchasing and Accounts Payable

THE ABC S OF DATA ANALYTICS ANGEL BUTLER MAY 23, 2013 HOUSTON AREA SCHOOL DISTRICT INTERNAL AUDITORS (HASDIA) AGENDA Data Analytics Overview Data Analytics Examples Compliance Purchasing and Accounts Payable

The Basics of Internal Controls

The Basics of Internal Controls Presented to: The Institute of Internal Auditors (IIA) Topeka Chapter April 7, 2009 Today s Objectives Provide Insight into Internal Controls! Risk and Fraud the basis for

The Basics of Internal Controls Presented to: The Institute of Internal Auditors (IIA) Topeka Chapter April 7, 2009 Today s Objectives Provide Insight into Internal Controls! Risk and Fraud the basis for

Audit Guide for Audit Committees of Small Nonprofit Organizations

Audit Guide for Audit Committees of Small Nonprofit Organizations A free resource provided by the Virginia Society of Certified Public Accountants Audit Guide for Small Nonprofit Organizations A free resource

Audit Guide for Audit Committees of Small Nonprofit Organizations A free resource provided by the Virginia Society of Certified Public Accountants Audit Guide for Small Nonprofit Organizations A free resource

5 Important Controls to Mitigate Employee Fraud

5 Important Controls to Mitigate Employee Fraud LMCIT WEBINAR : FEBRUARY 10, 2015 IN PARTNERSHIP WITH EIDE BAILLY Presenter: Jason Olson, MBA, CPA/CFF, CFE, CFI Presentation Disclaimer These seminar materials

5 Important Controls to Mitigate Employee Fraud LMCIT WEBINAR : FEBRUARY 10, 2015 IN PARTNERSHIP WITH EIDE BAILLY Presenter: Jason Olson, MBA, CPA/CFF, CFE, CFI Presentation Disclaimer These seminar materials

ASSOCIATED STUDENTS, INCORPORATED CALIFORNIA STATE UNIVERSITY, LONG BEACH DATE REVISED: 04/10/2013

Cash Handling BACKGROUND AND PURPOSE...1 POLICY STATEMENT...2 WHO SHOULD KNOW THIS POLICY...2 DEFINITIONS...2 STANDARDS AND PROCEDURES...3 1.0 CONDITIONS FOR EMPLOYMENT IN CASH HANDLING ENVIRONMENT...3

Cash Handling BACKGROUND AND PURPOSE...1 POLICY STATEMENT...2 WHO SHOULD KNOW THIS POLICY...2 DEFINITIONS...2 STANDARDS AND PROCEDURES...3 1.0 CONDITIONS FOR EMPLOYMENT IN CASH HANDLING ENVIRONMENT...3

ACCOUNTING AND FINANCIAL REPORTING REGULATION MANUAL

ACCOUNTING AND FINANCIAL REPORTING REGULATION MANUAL STATE BOARD OF ACCOUNTS 302 West Washington Street Room E418 Indianapolis, Indiana 46204-2769 Issued January 2011 Revised April 2012 TABLE OF CONTENTS

ACCOUNTING AND FINANCIAL REPORTING REGULATION MANUAL STATE BOARD OF ACCOUNTS 302 West Washington Street Room E418 Indianapolis, Indiana 46204-2769 Issued January 2011 Revised April 2012 TABLE OF CONTENTS

FINANCIAL CONTROLS POLICIES AND PROCEDURES FOR SMALL NONPROFIT ORGANIZATIONS

By Cindy Cumfer NOTE: These policies and procedures are designed for small nonprofits that do not have an administrator with financial expertise. They are set up to divide the fiscal control roles between

By Cindy Cumfer NOTE: These policies and procedures are designed for small nonprofits that do not have an administrator with financial expertise. They are set up to divide the fiscal control roles between

How To Manage Trust Account Money In Indiana

Trust Accounts and IOLTA April 24, 2014 Indianapolis Bar Association Applied Professionalism Course Presented by: Howard I. Gross, CPA/ABV/CFF, CFP & Samuel M. Pollom, JD, CPA BGBC Partners, LLP 300 N.

Trust Accounts and IOLTA April 24, 2014 Indianapolis Bar Association Applied Professionalism Course Presented by: Howard I. Gross, CPA/ABV/CFF, CFP & Samuel M. Pollom, JD, CPA BGBC Partners, LLP 300 N.

Guidelines for Congregations Internal Control Best Practices

Guidelines for Congregations Internal Control Best Practices A resource provided by the Office of the Treasurer of the Evangelical Lutheran Church in America Congregations should establish and maintain

Guidelines for Congregations Internal Control Best Practices A resource provided by the Office of the Treasurer of the Evangelical Lutheran Church in America Congregations should establish and maintain

GENERAL PAYROLL CONTROLS Dates in scope:

GENERAL PAYROLL CONTROLS Risk # Risk Expected Control Step # Testing Documents/Info Needed 1 Unauthorized initial pay rate 2 Unauthorized/unsupported deductions (statutory deductions and benefits). Initial

GENERAL PAYROLL CONTROLS Risk # Risk Expected Control Step # Testing Documents/Info Needed 1 Unauthorized initial pay rate 2 Unauthorized/unsupported deductions (statutory deductions and benefits). Initial

Types of Fraud and Recent Cases. Developing an Effective Anti-fraud Program from the Top Down

Types of and Recent Cases Developing an Effective Anti-fraud Program from the Top Down 1 Types of and Recent Cases Chris Grippa (404-817-5945) FIDS Senior Manager with Ernst & Young LLP Works with clients

Types of and Recent Cases Developing an Effective Anti-fraud Program from the Top Down 1 Types of and Recent Cases Chris Grippa (404-817-5945) FIDS Senior Manager with Ernst & Young LLP Works with clients

FRAUD RISK ASSESSMENT

FRAUD RISK ASSESSMENT All agencies are subject to fraud risks and need to complete a fraud risk assessment for their agency at least every biennium. A detailed fraud assessment needs to be performed by

FRAUD RISK ASSESSMENT All agencies are subject to fraud risks and need to complete a fraud risk assessment for their agency at least every biennium. A detailed fraud assessment needs to be performed by

PROPOSAL GRADUATE CERTIFICATE IN FORENSIC ACCOUNTING FRAUD INVESTIGATION TO BE OFFERED AT PURDUE UNIVERSITY CALUMET

Graduate Council Document 08-41a Approved by the Graduate Council on May 6, 2010 PROPOSAL GRADUATE CERTIFICATE IN FORENSIC ACCOUNTING & FRAUD INVESTIGATION TO BE OFFERED AT PURDUE UNIVERSITY CALUMET Proposal

Graduate Council Document 08-41a Approved by the Graduate Council on May 6, 2010 PROPOSAL GRADUATE CERTIFICATE IN FORENSIC ACCOUNTING & FRAUD INVESTIGATION TO BE OFFERED AT PURDUE UNIVERSITY CALUMET Proposal

Standard Procedures and Controls for the Title Industry. Prepared by the ALTA Internal Auditing Committee ALTA

Standard Procedures and Controls for the Title Industry Prepared by the ALTA Internal Auditing Committee ALTA The American Land Title Association, founded in 1907, is the national trade association and

Standard Procedures and Controls for the Title Industry Prepared by the ALTA Internal Auditing Committee ALTA The American Land Title Association, founded in 1907, is the national trade association and

WINONA STATE UNIVERSITY TRAVEL CREDIT CARD PROGRAM USERS GUIDE

WINONA STATE UNIVERSITY TRAVEL CREDIT CARD PROGRAM USERS GUIDE 1 WSU TRAVEL CARD PROGRAM Part 1. Authority MnSCU System Procedure 7.3.3 Credit Cards, provides authority for a college, university or office

WINONA STATE UNIVERSITY TRAVEL CREDIT CARD PROGRAM USERS GUIDE 1 WSU TRAVEL CARD PROGRAM Part 1. Authority MnSCU System Procedure 7.3.3 Credit Cards, provides authority for a college, university or office

Archdiocese of Chicago Parish Self-Assessment Checklist

Self-Assessment Questions 1. Are written Parish Finance Council guidelines and norms defined, documented, and available to all Parish Finance Council members? 2. Are Archdiocesan best practices communicated

Self-Assessment Questions 1. Are written Parish Finance Council guidelines and norms defined, documented, and available to all Parish Finance Council members? 2. Are Archdiocesan best practices communicated

Forensic Accounting. A Glimpse Into Forensic Accounting. Portland State University. 10.29.14 Professional Nancy Young, CPA, CISA, CFE Moss Adams, LLP

Forensic Accounting A Glimpse Into Forensic Accounting 10.29.14 Professional Nancy Young, CPA, CISA, CFE Moss Adams, LLP Summary by Michael Wong Manager of Presentations εα Portland State University Introduction

Forensic Accounting A Glimpse Into Forensic Accounting 10.29.14 Professional Nancy Young, CPA, CISA, CFE Moss Adams, LLP Summary by Michael Wong Manager of Presentations εα Portland State University Introduction

The Merchant. Skimming is No Laughing Matter. A hand held skimming device. These devices can easily be purchased online.

1 February 2010 Volume 2, Issue 1 The Merchant Serving Florida State University s Payment Card Community Individual Highlights: Skimming Scam 1 Skimming at Work 2 Safe at Home 3 Read your Statement 4 Useful

1 February 2010 Volume 2, Issue 1 The Merchant Serving Florida State University s Payment Card Community Individual Highlights: Skimming Scam 1 Skimming at Work 2 Safe at Home 3 Read your Statement 4 Useful

INTERNAL ACCOUNTING CONTROLS CHECKLIST FOR NTMA CHAPTERS

P R E C I S I O N INTERNAL ACCOUNTING CONTROLS CHECKLIST FOR NTMA CHAPTERS Presented at NTMA 2004 Annual Convention Palm Springs, CA February 2004 National Tooling & Machining Association 9300 Livingston

P R E C I S I O N INTERNAL ACCOUNTING CONTROLS CHECKLIST FOR NTMA CHAPTERS Presented at NTMA 2004 Annual Convention Palm Springs, CA February 2004 National Tooling & Machining Association 9300 Livingston

Preventing Fraud and Abuse of Public Funds: Local Governments Need to Do Better

Office of the State Comptroller Thomas P. DiNapoli State Comptroller Division of Local Government and School Accountability August 2010 Preventing Fraud and Abuse of Public Funds: Local Governments Need

Office of the State Comptroller Thomas P. DiNapoli State Comptroller Division of Local Government and School Accountability August 2010 Preventing Fraud and Abuse of Public Funds: Local Governments Need

Dear Consumer, What's in this packet: Identity Theft Victim Checklist Identity Theft Victim Worksheet Sample Letters

Dear Consumer, Sometimes an identity thief can strike even if you ve been very careful about protecting your personal information. If you suspect that your personal information has been stolen and used

Dear Consumer, Sometimes an identity thief can strike even if you ve been very careful about protecting your personal information. If you suspect that your personal information has been stolen and used

Tips to Prevent and Detect Workplace Fraud

40 Tips to Prevent and Detect Workplace Fraud an E-book developed for you by: Table of Contents preventive controls detective controls 1. culture of ethics 2. free of moral hazards 3. risk management policy

40 Tips to Prevent and Detect Workplace Fraud an E-book developed for you by: Table of Contents preventive controls detective controls 1. culture of ethics 2. free of moral hazards 3. risk management policy

Identity Theft Prevention Program Compliance Model

September 29, 2008 State Rural Water Association Identity Theft Prevention Program Compliance Model Contact your State Rural Water Association www.nrwa.org Ed Thomas, Senior Environmental Engineer All

September 29, 2008 State Rural Water Association Identity Theft Prevention Program Compliance Model Contact your State Rural Water Association www.nrwa.org Ed Thomas, Senior Environmental Engineer All

CHAPTER 9 CASH. Chapter 9. Copyright 2012 The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 9 CASH Chapter Opener: Thinking Critically Office expenditures may include petty cash disbursements for office supplies and postage. Cash expenditures might also include payments for rent and utilities.

CHAPTER 9 CASH Chapter Opener: Thinking Critically Office expenditures may include petty cash disbursements for office supplies and postage. Cash expenditures might also include payments for rent and utilities.

Fraud Policy FEBRUARY 2014

Fraud Policy FEBRUARY 2014 TABLE OF CONTENTS 1. Application of Policy... 2 2. Purpose of Policy... 2 3. Fraud Policy... 2 4. Definition of Fraud... 2 5. Duties and Responsibilities of an Employee or Contractor...

Fraud Policy FEBRUARY 2014 TABLE OF CONTENTS 1. Application of Policy... 2 2. Purpose of Policy... 2 3. Fraud Policy... 2 4. Definition of Fraud... 2 5. Duties and Responsibilities of an Employee or Contractor...

ATTESTATION REPORT OF DODGE COUNTY COURT JULY 1, 2013 THROUGH JUNE 30, 2015

ATTESTATION REPORT OF DODGE COUNTY COURT JULY 1, 2013 THROUGH JUNE 30, 2015 This document is an official public record of the State of Nebraska, issued by the Auditor of Public Accounts. Modification of

ATTESTATION REPORT OF DODGE COUNTY COURT JULY 1, 2013 THROUGH JUNE 30, 2015 This document is an official public record of the State of Nebraska, issued by the Auditor of Public Accounts. Modification of

Fraud Prevention Checklist for Small Businesses

Fraud Prevention Checklist for Small Businesses 11 Ways to Minimize the Risk and Impact PAYMENT SOLUTIONS Fraud can have a devastating impact on small businesses. Prevention and mitigation strategies can

Fraud Prevention Checklist for Small Businesses 11 Ways to Minimize the Risk and Impact PAYMENT SOLUTIONS Fraud can have a devastating impact on small businesses. Prevention and mitigation strategies can

1/17/2013 FRAUD RISK MANAGEMENT PROGRAM SESSION OBJECTIVE AND OUTLINE

FRAUD RISK MANAGEMENT PROGRAM SHERYL VACCA SENIOR VICE PRESIDENT AND CHIEF COMPLIANCE AND AUDIT OFFICER MIKE JENSON UCR AUDIT DIRECTOR SESSION OBJECTIVE AND OUTLINE Assist campus managers in the development

FRAUD RISK MANAGEMENT PROGRAM SHERYL VACCA SENIOR VICE PRESIDENT AND CHIEF COMPLIANCE AND AUDIT OFFICER MIKE JENSON UCR AUDIT DIRECTOR SESSION OBJECTIVE AND OUTLINE Assist campus managers in the development

BDO Consulting. Segregation of Duties Checklist

BDO Consulting Segregation of Duties Checklist August 2009 BDO Consulting s Fraud Prevention practice is pleased to present the 2009 Segregation of Duties Checklist. We have developed this tool to assist

BDO Consulting Segregation of Duties Checklist August 2009 BDO Consulting s Fraud Prevention practice is pleased to present the 2009 Segregation of Duties Checklist. We have developed this tool to assist

Direct Lending Fraud: One University s Response to Identity Fraud in Online Learning Vickie Fredrick Webster University 470 E Lockwood Ave, LH212

Direct Lending Fraud: One University s Response to Identity Fraud in Online Learning Vickie Fredrick Webster University 470 E Lockwood Ave, LH212 Saint Louis, Missouri 63119 (314)968-5911 [email protected]

Direct Lending Fraud: One University s Response to Identity Fraud in Online Learning Vickie Fredrick Webster University 470 E Lockwood Ave, LH212 Saint Louis, Missouri 63119 (314)968-5911 [email protected]

Preventing Fraud: The Importance of Internal Controls

Preventing Fraud: The Importance of Internal Controls Presented by: Scott Gold, CPA,BKD, LLP @ BKDForensics Today s Agenda Faces of fraud Real life examples: The latest schemes Lifestyles of the Rich and

Preventing Fraud: The Importance of Internal Controls Presented by: Scott Gold, CPA,BKD, LLP @ BKDForensics Today s Agenda Faces of fraud Real life examples: The latest schemes Lifestyles of the Rich and

The following figures summarize ways in which dut:es could be segregated with two, three and four people.

The following figures summarize ways in which dut:es could be segregated with two, three and four people. Segregation of Duties- Two people Accountant or other financial personnel 11,,. Rec()rdpl~dges

The following figures summarize ways in which dut:es could be segregated with two, three and four people. Segregation of Duties- Two people Accountant or other financial personnel 11,,. Rec()rdpl~dges

FRAUD PREVENTION STRATEGIES FOR HEALTH CARE A FORENSIC ACCOUNTANT S PERSPECTIVE

FRAUD PREVENTION STRATEGIES FOR HEALTH CARE A FORENSIC ACCOUNTANT S PERSPECTIVE CPAs & ADVISORS experience reach // S. Todd Burchett, CPA, ABV, ASA, CFF, CFE Partner [email protected] 210.268.1932 AGENDA

FRAUD PREVENTION STRATEGIES FOR HEALTH CARE A FORENSIC ACCOUNTANT S PERSPECTIVE CPAs & ADVISORS experience reach // S. Todd Burchett, CPA, ABV, ASA, CFF, CFE Partner [email protected] 210.268.1932 AGENDA

Avoid Trust Accounting Pitfalls through Proper Internal Controls

January 2015 Unique Monthly Visitors: 1,918 JANUARY 2015 Avoid Trust Accounting Pitfalls through Proper Internal Controls By Steven A. Davis and Marc Feigelson Many attorneys run into issues related to

January 2015 Unique Monthly Visitors: 1,918 JANUARY 2015 Avoid Trust Accounting Pitfalls through Proper Internal Controls By Steven A. Davis and Marc Feigelson Many attorneys run into issues related to

Presented by: Donald F. Conway, CPA Mercadien, P.C., Certified Public Accountants. Forensic Accounting, Political Corruption & White Collar Offenses

Presented by: Donald F. Conway, CPA Mercadien, P.C., Certified Public Accountants Forensic Accounting, Political Corruption & White Collar Offenses Defining Fraud The dictionary defines fraud as a deception

Presented by: Donald F. Conway, CPA Mercadien, P.C., Certified Public Accountants Forensic Accounting, Political Corruption & White Collar Offenses Defining Fraud The dictionary defines fraud as a deception

Identity theft. A fraud committed or attempted using the identifying information of another person without authority.

SUBJECT: Effective Date: Policy Number: Identity Theft Prevention 08-24-11 2-105.1 Supersedes: Page Of 2-105 1 8 Responsible Authority: Vice President and General Counsel DATE OF INITIAL ADOPTION AND EFFECTIVE

SUBJECT: Effective Date: Policy Number: Identity Theft Prevention 08-24-11 2-105.1 Supersedes: Page Of 2-105 1 8 Responsible Authority: Vice President and General Counsel DATE OF INITIAL ADOPTION AND EFFECTIVE

How to set up a people based. accounting system that makes your. small business work for you. Thomas G. Post. Certified Public Accountant 281-351-2688

How to set up a people based accounting system that makes your small business work for you. By Thomas G. Post Certified Public Accountant 281-351-2688 www.texastaxman.com 1 Title How to set up a people

How to set up a people based accounting system that makes your small business work for you. By Thomas G. Post Certified Public Accountant 281-351-2688 www.texastaxman.com 1 Title How to set up a people

5:31-7 Appendix B LOCAL AUTHORITIES - ACCOUNTING AND AUDITING IF ANY ARE NOT APPLICABLE, INSERT N/A AS YOUR ANSWER. FIRE DISTRICT YEAR UNDER AUDIT

5:31-7 Appendix B LOCAL AUTHORITIES - ACCOUNTING AND AUDITING AUDIT QUESTIONNAIRE FOR FIRE DISTRICT AUDITS EACH QUESTION MUST BE ANSWERED. PLEASE CIRCLE YES OR NO. IF ANY ARE NOT APPLICABLE, INSERT N/A

5:31-7 Appendix B LOCAL AUTHORITIES - ACCOUNTING AND AUDITING AUDIT QUESTIONNAIRE FOR FIRE DISTRICT AUDITS EACH QUESTION MUST BE ANSWERED. PLEASE CIRCLE YES OR NO. IF ANY ARE NOT APPLICABLE, INSERT N/A

Ouachita Baptist University. Identity Theft Policy and Program

Ouachita Baptist University Identity Theft Policy and Program Under the Federal Trade Commission s Red Flags Rule, Ouachita Baptist University is required to establish an Identity Theft Prevention Program

Ouachita Baptist University Identity Theft Policy and Program Under the Federal Trade Commission s Red Flags Rule, Ouachita Baptist University is required to establish an Identity Theft Prevention Program

Audit of Cash Balances

Audit of Cash Balances Chapter 23 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 23-1 Learning Objective 1 Show the relationship of cash in the bank to the various transaction

Audit of Cash Balances Chapter 23 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 23-1 Learning Objective 1 Show the relationship of cash in the bank to the various transaction

Generally Accepted Record Retention Guidelines

Document Name /Type Accident reports and claims (settled cases) Accommodation requests Accounts payable ledgers and schedules Accounts receivable ledgers and schedules Ads and Notices of overtime opportunities

Document Name /Type Accident reports and claims (settled cases) Accommodation requests Accounts payable ledgers and schedules Accounts receivable ledgers and schedules Ads and Notices of overtime opportunities

2. Is the mail log prepared by someone who does not participate in any other aspects of the revenue receipts process?

CASH AND CHECK HANDLING SELF ASSESSMENT Because of the relatively high risk associated with transactions involving cash, universities need to have a cash management program to safeguard cash and ensure

CASH AND CHECK HANDLING SELF ASSESSMENT Because of the relatively high risk associated with transactions involving cash, universities need to have a cash management program to safeguard cash and ensure

Wake Forest University. Identity Theft Prevention Program. Effective May 1, 2009

Wake Forest University Identity Theft Prevention Program Effective May 1, 2009 I. GENERAL It is the policy of Wake Forest University ( University ) to comply with the Federal Trade Commission's ( FTC )

Wake Forest University Identity Theft Prevention Program Effective May 1, 2009 I. GENERAL It is the policy of Wake Forest University ( University ) to comply with the Federal Trade Commission's ( FTC )

IDENTITY THEFT PROCEDURES

IDENTITY THEFT PROCEDURES FREQUENTLY ASKED QUESTIONS ABOUT IDENTITY THEFT INCIDENTS AND RED FLAGS Q1: How is a Red Flags incident different from a data security breach? A1: A data security breach is the

IDENTITY THEFT PROCEDURES FREQUENTLY ASKED QUESTIONS ABOUT IDENTITY THEFT INCIDENTS AND RED FLAGS Q1: How is a Red Flags incident different from a data security breach? A1: A data security breach is the

ACCOUNTS PAYABLE AUDIT RECOVERING LOST DOLLARS AT NO COST

ACCOUNTS PAYABLE AUDIT RECOVERING LOST DOLLARS AT NO COST 1 Our Objective To assist organizations in finding lost thousands of dollars in profits through duplicate payments, duplicate billings, overpayments,

ACCOUNTS PAYABLE AUDIT RECOVERING LOST DOLLARS AT NO COST 1 Our Objective To assist organizations in finding lost thousands of dollars in profits through duplicate payments, duplicate billings, overpayments,

INTERNAL CONTROL POLICIES

INTERNAL CONTROL POLICIES 2701 Internal Control Policy 2701.1 Addendum Internal Control Standard #1 Payments Cycle 2701.2 Addendum Internal Control Standard #2 Conversion Cycle 2701.3 Addendum Internal

INTERNAL CONTROL POLICIES 2701 Internal Control Policy 2701.1 Addendum Internal Control Standard #1 Payments Cycle 2701.2 Addendum Internal Control Standard #2 Conversion Cycle 2701.3 Addendum Internal

II. F. Identity Theft Prevention

II. F. Identity Theft Prevention Effective Date: May 3, 2012 Revises Previous Effective Date: N/A, New Policy I. POLICY: This Identity Theft Prevention Policy is adopted in compliance with the Federal

II. F. Identity Theft Prevention Effective Date: May 3, 2012 Revises Previous Effective Date: N/A, New Policy I. POLICY: This Identity Theft Prevention Policy is adopted in compliance with the Federal

3344-19-01 Identity theft prevention program and red flag compliance policy.

3344-19-01 Identity theft prevention program and red flag compliance policy. (A) Program adoption Cleveland state university has developed this identity theft prevention program ( program ) pursuant to

3344-19-01 Identity theft prevention program and red flag compliance policy. (A) Program adoption Cleveland state university has developed this identity theft prevention program ( program ) pursuant to

Fraud Waste and Abuse Training First Tier, Downstream and Related Entities. ONECare by Care1st Health Plan Arizona, Inc. (HMO) Revised: 10/2009

Revised: 10/2009") Fraud Waste and Abuse Training First Tier, Downstream and Related Entities ONECare by Care1st Health Plan Arizona, Inc. (HMO) Revised: 10/2009 Overview Purpose Care1st/ ONECare Compliance Program Definitions

Fraud Waste and Abuse Training First Tier, Downstream and Related Entities ONECare by Care1st Health Plan Arizona, Inc. (HMO) Revised: 10/2009 Overview Purpose Care1st/ ONECare Compliance Program Definitions

Lesson 4. Preventing and Policing White-Collar Crime

Preventing and Policing ASSIGNMENT 11 Read this introduction and then read pages 260 294 in White- Collar Crime: The Essentials. White-collar crime is clearly complex and multifaceted. No single theory

Preventing and Policing ASSIGNMENT 11 Read this introduction and then read pages 260 294 in White- Collar Crime: The Essentials. White-collar crime is clearly complex and multifaceted. No single theory

AUDIT AND FINANCE COMMITTEE Wednesday, February 25, 2009

Item: AF: I 1a AUDIT AND FINANCE COMMITTEE Wednesday, February 25, 2009 SUBJECT: REVIEW OF AUDITS: REPORT NO. FAU 08/09 1, AUDIT OF UNDERGRADUATE ADMISSIONS FOR THE FALL 2008 SEMESTER PROPOSED COMMITTEE

Item: AF: I 1a AUDIT AND FINANCE COMMITTEE Wednesday, February 25, 2009 SUBJECT: REVIEW OF AUDITS: REPORT NO. FAU 08/09 1, AUDIT OF UNDERGRADUATE ADMISSIONS FOR THE FALL 2008 SEMESTER PROPOSED COMMITTEE

Leveraging Big Data to Mitigate Health Care Fraud Risk

Leveraging Big Data to Mitigate Health Care Fraud Risk Jeremy Clopton, CPA, CFE, ACDA Senior Managing Consultant BKD, LLP Forensics & Valuation Services Introduction Health Care Is Victimized by Fraud

Leveraging Big Data to Mitigate Health Care Fraud Risk Jeremy Clopton, CPA, CFE, ACDA Senior Managing Consultant BKD, LLP Forensics & Valuation Services Introduction Health Care Is Victimized by Fraud

Diploma in Forensic Accounting (Level 4) Course Structure & Contents

Course Structure & Contents") Brentwood Open Learning College Diploma in Forensic Accounting (Level 4) Course Structure & Contents Diploma in Forensic Accounting Course Structure & Contents Page 1 Unit 1 Introduction Forensic Accounting

Brentwood Open Learning College Diploma in Forensic Accounting (Level 4) Course Structure & Contents Diploma in Forensic Accounting Course Structure & Contents Page 1 Unit 1 Introduction Forensic Accounting