Roth IRA Conversions 11/1/2011. Note. Cautions you need to know. Deb Repya, J.D, CLU, ChFC Vice President, Advanced Markets

|

|

|

- Owen Shelton

- 10 years ago

- Views:

Transcription

1 Allianz Life Insurance Company of North America Roth IRA Conversions Cautions you need to know Deb Repya, J.D, CLU, ChFC Vice President, Advanced Markets ENT 974 (R 6/2011) Our Mission: Allianz Life Insurance Company of North America is the trusted authority in insured retirement solutions for consumers working with a financial professional. Note This presentation is designed to provide general information on the subjects covered. Pursuant to IRS Circular 230, it is not, however, intended to provide specific legal or tax advice and cannot be used to avoid tax penalties or to promote, market, or recommend any tax plan or arrangement. Please note that Allianz Life Insurance Company of North America, its affiliated companies, and their representatives and employees do not give legal or tax advice. Please keep in mind that producers must be currently registered with a broker/dealer to recommend the liquidation of funds held in securities products, including those within an IRA or other retirement plan, for the purchase of an annuity. Please remember that converting your client s traditional IRA to a Roth IRA is a taxable event and could result in additional impacts to their personal tax situation, including the taxation of current Social Security benefit payments. Be sure to have your client consult with a qualified tax advisor before making any decisions regarding their IRA. It is generally preferable that your clients have funds to pay the taxes due upon conversion from funds outside of their IRA. If they elect to take a distribution from their IRA to pay the conversion taxes, please keep in mind the potential consequences, such as an assessment of product surrender charges or additional Internal Revenue Service penalties for premature distributions. This presentation is for educational purposes only. 2 1

2 Agenda 1. Increasing taxable income 2. Estimated tax payments 3. Taxation in retirement 4. Converting after tax IRAs 5. Withdrawl order 6. Entire interest value 3 1 Increasing taxableincome 4 2

3 Increasing taxable income Increased income may affect many tax issues Increased marginal rates Increased taxes on Social Security income Medical and miscellaneous deductions may be reduced (part of Schedule A, but treated separately) Exemptions and Schedule A deductions have, at times, been phased out based on income May push taxpayer into Alternative Minimum Tax (AMT) situation Increased Medicare Part B Premium Please keep in mind that producers must be currently registered with a broker/dealer to recommend the liquidation of funds held in securities products, including those within an IRA or other retirement plan, for the purchase of an annuity. 5 Increasing taxable income Monthly Part B premiums for 2011 Individuals with a MAGI of $85,000 or less Married couples with a MAGI of $170, or less Individuals with a MAGI above $85,000 up to $107,000 Married couples with a MAGI above $170,000 up to $214,000 Individuals with a MAGI above $107,000 up to $160,000 Married couples with a MAGI above $214,000 up to $320,000 Individuals with a MAGI above $160,000 up to $214,000 Married couples with a MAGI above $320,000 up to $428,000 Individuals with a MAGI above $214,000 Married couples with a MAGI above $428,000 Income related monthly adjustment amount $0.00 Modified adjust gross income (MAGI) Total monthly premium amount $ standard premium $46.10 $ $ $ $ $ $ $ If you are married and lived with your spouse at some time during the taxable year, but filed a separate tax return, the following chart will apply: Income related monthly adjustment amount Individuals with a MAGI of $85,000 or less $0.00 Total monthly premium amount $ standard premium Individuals with a MAGI above $85,000 up to $129,000 $ $ Individuals with a MAGI above $129,000 $ $ part b premium amounts for person with higher income levels. 3

4 Increasing taxable income Monthly Part B premiums for 2011 Individuals with a MAGI of $85,000 or less Married couples with a MAGI of $170, or less Individuals with a MAGI above $85,000 up to $107,000 Married couples with a MAGI above $170,000 up to $214,000 Individuals with a MAGI above $107,000 up to $160,000 Married couples with a MAGI above $214,000 up to $320,000 Individuals with a MAGI above $160,000 up to $214,000 Married couples with a MAGI above $320,000 up to $428,000 Individuals with a MAGI above $214,000 Married couples with a MAGI above $428,000 Income related monthly adjustment amount $0.00 Make sure you calculate the extra cost Modified adjust gross income (MAGI) Total monthly premium amount $ standard premium $46.10 $ $ $ A $44,000 conversion that moves the Medicare premium from $115.40/month to $161.50/month is an additional cost of 1.26% of the converted amount. $ $ $ $ If you are married and lived with your spouse at some time during the taxable year, but filed a separate tax return, the following chart will apply: A $50,000conversion that moves the Medicare premium Income related monthly from $161.50/month to $230.70/month adjustment is amount an additional cost of 1.66% of the converted amount. Individuals with a MAGI of $85,000 or less $0.00 Total monthly premium amount $ standard premium Individuals with a MAGI above $85,000 up to $129,000 $ $ Individuals with a MAGI above $129,000 $ $ part b premium amounts for person with higher income levels. 2 Estimated tax payments 8 4

Total monthly premium amount $115.40 standard premium $46.10 $161.50 $115.30 $230.")

5 Estimated tax payments Roth IRA conversions may require estimated tax payments so your clients don t end up with a penalty for underpayment of taxes. If your clients did a Roth conversion in 2010 and are splitting the conversion income between 2011 and 2012, remember to deposit the attributable taxes appropriately. Encourage your clients to work with their CPA or tax advisor on estimated tax payments and the exceptions to the payment requirements. 9 3 Taxation in retirement 10 5

6 Taxation in retirement Be cautious when converting just before retirement. Retirement can change the dynamics of one s tax scenario, resulting in a lower marginal tax bracket No Social Security/Medicare tax to pay No saving for retirement Increased deductions for those age 65 or over A maximum of 85% of Social Security is taxed 11 Taxation in retirement 2010 John & Mary age 60 Pre retirement income: John $ 86,750 Mary 86, ,500 SS/Medicare 1 13, (k) 17,350 Fed income tax 26,730 Excess income $116,147 The 401(k) contributions tib ti were made in the 28% marginal tax bracket This is the amount John and Mary need to replace in retirement 1 During 2011 the employee share of SS withholding has been reduced from 6.2% to 4.2%. Since this reduction is most likely temporary, we have illustrated 6.2% SS % Medicare withholding. This is a hypothetical example and does not represent actual clients. Please note the that 85% of the Social Security amount used in the illustration above is taxable. 12 6

contributions tib ti were made in the 28% marginal tax bracket This is the amount John and Mary need to replace in retirement 1 During 2011 the")

7 Taxation in retirement John & Mary age 60 John & Mary age 66 Pre retirement income: Retirement income: John $ 86,750 Rti Retirement tplans $116,713 Mary 86,750 Social Security 20, , ,713 SS/Medicare 1 13,273 SS/Medicare 0 401(k) 17, (k) 0 Fed income tax 26,730 Fed income tax 20,566 Excess income $116,147 Excess income $116,147 The 401(k) contributions tib ti were made in the 28% marginal tax bracket In this scenario the excess income has been replaced and they are $24,487 under the 28% tax bracket 1 During 2011 the employee share of SS withholding has been reduced from 6.2% to 4.2%. Since this reduction is most likely temporary, we have illustrated 6.2% SS % Medicare withholding. This is a hypothetical example and does not represent actual clients. Please note the that 85% of the Social Security amount used in the illustration above is taxable. 4 Converting after taxiras 14 7

8 Converting after tax IRAs IRA 1 $300,000 IRA 2 After tax $100,000 Untaxed All untaxed Please keep in mind that producers must be currently registered with a broker/dealer to recommend the liquidation of funds held in securities products, including those within an IRA or other retirement plan, for the purchase of an annuity. Encourage your clients to consult with a qualified tax advisor. This example is shown for educational purposes only. 15 Converting after tax IRAs After tax $100,000 IRA 1 $300,000 IRA 2 Can we convert just this IRA? Untaxed All untaxed Please keep in mind that producers must be currently registered with a broker/dealer to recommend the liquidation of funds held in securities products, including those within an IRA or other retirement plan, for the purchase of an annuity. Encourage your clients to consult with a qualified tax advisor. This example is shown for educational purposes only. 16 8

9 Converting after tax IRAs IRA 1$500,000 aggregated value $300,000 IRA 2 After tax $100,000 After Tax $100,000 Untaxed $400,000 Untaxed All untaxed 20% of any conversion will be considered after tax dollars This example is shown for educational purposes only. 17 Converting after tax IRAs After tax $100,000 IRA 1 $300,000 Untaxed IRA 2 While you can convert this IRA, 80% of its value will be taxable income. All untaxed Please keep in mind that producers must be currently registered with a broker/dealer to recommend the liquidation of funds held in securities products, including those within an IRA or other retirement plan, for the purchase of an annuity. Encourage your clients to consult with a qualified tax advisor. This example is shown for educational purposes only. 18 9

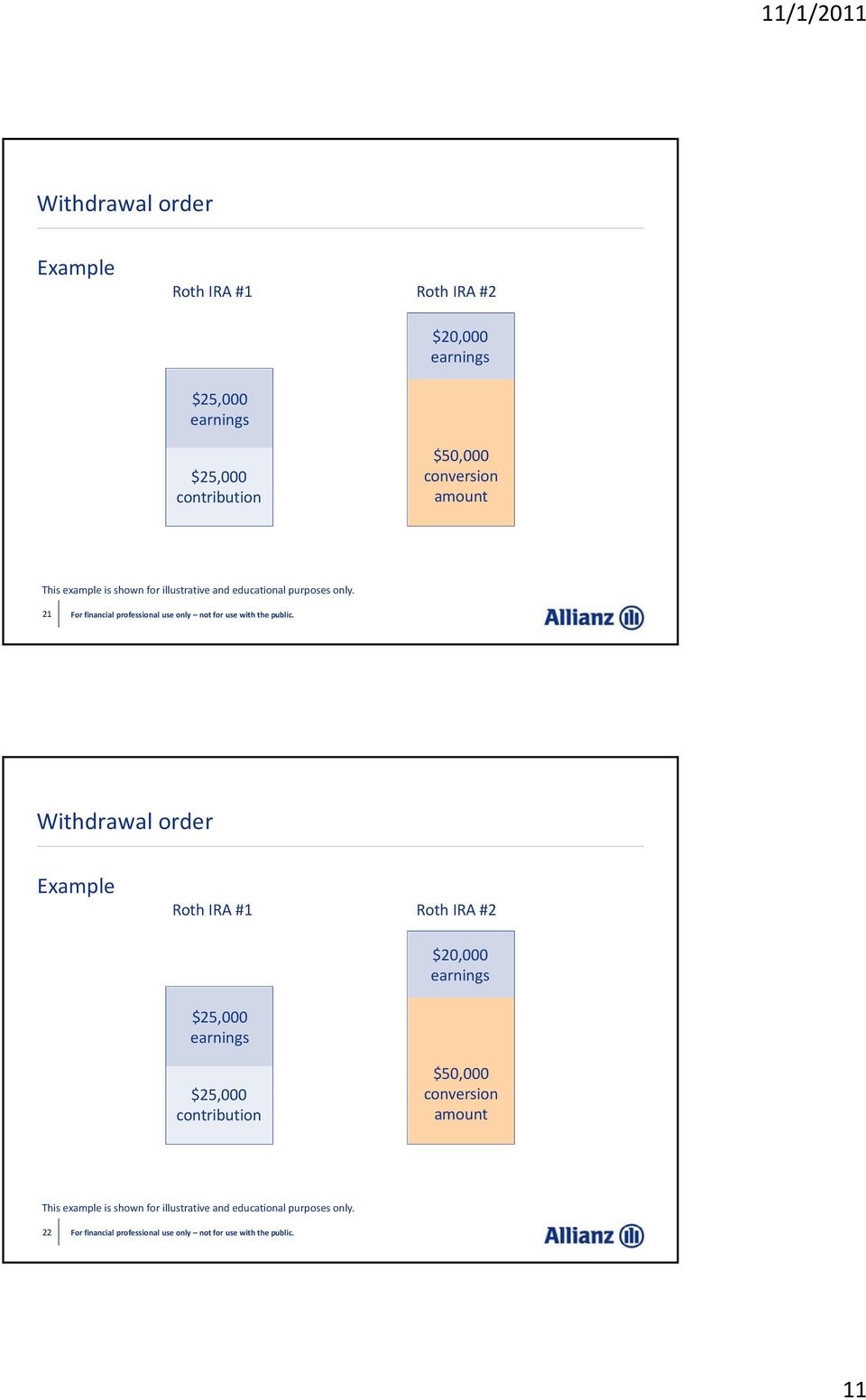

10 5 Withdrawal order 19 Withdrawal order Withdrawals from Roth IRAs can be complicated. Make sure your clients seek tax advice from a competent professional. Order of withdrawal: 1. Regular contributions and certain designated Roth IRA account rollover assets 2. Conversion contributions and retirement plan rollover assets (excluding designated Roth IRA account rollover assets) 1 3. Earnings and certain designated Roth IRA account rollover assets 1 Special rules apply if any of the conversion or rollover was nontaxable at the time of the transaction and if there has been more than one conversion or rollover. This example is shown for educational purposes only

11 Withdrawal order Example Roth IRA #1 Roth IRA #2 $20,000 earnings $25,000 earnings $25,000 contribution $50,000 conversion amount This example is shown for illustrative and educational purposes only. 21 Withdrawal order Example Roth IRA #1 Roth IRA #2 $20,000 earnings $25,000 earnings $25,000 contribution $50,000 conversion amount This example is shown for illustrative and educational purposes only

12 Withdrawal order Example No 10% penalty if at least 5 years from conversion or if exception applies $45,000 earnings $50,000 conversion amount No income tax or 10% penalty if the 5 year requirement is met, and meets one of: age 59½, death, disability, first time time homebuyer up to $10,000 and owner is at least age 59½ (exception can apply to the 10% penalty) $25,000 contribution Always available income tax free and penalty free This example is shown for illustrative and educational purposes only Entire interest value 24 12

13 Entire interest value When doing a conversion of a traditional IRA to a Roth IRA, the owner may pay income tax on an amount greater than the contract value. Please keep in mind that producers must be currently registered with a broker/dealer to recommend the liquidation of fund held in securities products, including those within an IRA or other retirement plan, for the purchase of an annuity. 25 Summary 1. Increasing taxable income 2. Estimated tax payments 3. Taxation in retirement 4. Converting after tax IRAs 5. Withdrawl order 6. Entire interest value 26 13

14 Allianz Life Insurance Company of North America (Allianz) This presentation is designed to provide general information on the subjects covered. Pursuant to IRS Circular 230, it is not, however, intended to provide specific legal or tax advice and cannot be used to avoid tax penalties or to promote, market, or recommend any tax plan or arrangement. Please note that Allianz Life Insurance Company of North America, its affiliated companies, and their representatives and employees do not give legal or tax advice. Encourage your clients to consult with their tax advisor or attorney. Guarantees are backed by the financial strength and claims paying ability of Allianz Life Insurance Company of North America. Not FDIC insured May lose value No bank or credit union guarantee Not a deposit Not insured by any federal government agency or NCUA/NCUSIF Products are issued by Allianz Life Insurance Company of North America, 5701 Golden Hills Drive, Minneapolis, MN Thank you. Any questions? 28 14

Understanding IRA distributions

Understanding IRA distributions A retirement distribution guide Allianz Life Insurance Company of New York Allianz Life Insurance Company of North America AMK-019-N Page 1 of 12 It s important to know

Understanding IRA distributions A retirement distribution guide Allianz Life Insurance Company of New York Allianz Life Insurance Company of North America AMK-019-N Page 1 of 12 It s important to know

1035 exchange. Understanding the. When exchanging or keeping a contract makes the most sense

Understanding the 1035 exchange When exchanging or keeping a contract makes the most sense Allianz Life Insurance Company of New York Allianz Life Insurance Company of North America AMK-283-N Page 1 of

Understanding the 1035 exchange When exchanging or keeping a contract makes the most sense Allianz Life Insurance Company of New York Allianz Life Insurance Company of North America AMK-283-N Page 1 of

Understanding IRAs. Thad Johnson, AIF, MBA 222 2nd Ave SE Hutchinson, MN 55350 320-587-3444 [email protected]

Thad Johnson, AIF, MBA 222 2nd Ave SE Hutchinson, MN 55350 320-587-3444 [email protected] Understanding IRAs Page 1 of 5, see disclaimer on final page Understanding IRAs An individual

Thad Johnson, AIF, MBA 222 2nd Ave SE Hutchinson, MN 55350 320-587-3444 [email protected] Understanding IRAs Page 1 of 5, see disclaimer on final page Understanding IRAs An individual

IRAs. AKD Consultants Adam Dworkin CPA 188 Whiting Street Suite 10 Hingham, MA 02043 781-556-5554 [email protected]

AKD Consultants Adam Dworkin CPA 188 Whiting Street Suite 10 Hingham, MA 02043 781-556-5554 [email protected] IRAs October 01, 2013 Page 1 of 8, see disclaimer on final page Both traditional and

AKD Consultants Adam Dworkin CPA 188 Whiting Street Suite 10 Hingham, MA 02043 781-556-5554 [email protected] IRAs October 01, 2013 Page 1 of 8, see disclaimer on final page Both traditional and

Understanding government pension offset and the windfall elimination provision

Understanding government pension offset and the windfall elimination provision Allianz Life Insurance Company of New York Allianz Life Insurance Company of North America ENT-1518-N Page 1 of 6 The basics

Understanding government pension offset and the windfall elimination provision Allianz Life Insurance Company of New York Allianz Life Insurance Company of North America ENT-1518-N Page 1 of 6 The basics

Preparing for Your Retirement: An IRA Review

Preparing for Your Retirement: An IRA Review How much of your earning power will be available for your use when you retire? What will happen to your standard of living when your income ceases at retirement?

Preparing for Your Retirement: An IRA Review How much of your earning power will be available for your use when you retire? What will happen to your standard of living when your income ceases at retirement?

The IRA Rollover. Making Sense Out of Your Retirement Plan Distribution

The IRA Rollover Making Sense Out of Your Retirement Plan Distribution Expecting a Distribution? You have been a participant in your employer s retirement plan for a number of years, and you have earned

The IRA Rollover Making Sense Out of Your Retirement Plan Distribution Expecting a Distribution? You have been a participant in your employer s retirement plan for a number of years, and you have earned

Converting taxable income into tax-free income

Converting taxable income into tax-free income Important information for people who still own a traditional IRA Consider the future impact of your IRA Do you own a traditional IRA? Many people nearing

Converting taxable income into tax-free income Important information for people who still own a traditional IRA Consider the future impact of your IRA Do you own a traditional IRA? Many people nearing

GENERAL INCOME TAX INFORMATION

NEW YORK STATE TEACHERS RETIREMENT SYSTEM GENERAL INCOME TAX INFORMATION TABLE OF CONTENTS Taxes on Loans from the Annuity Savings Fund 1 (Tier 1 and 2 Members Only) Taxes on the Withdrawal of the Annuity

NEW YORK STATE TEACHERS RETIREMENT SYSTEM GENERAL INCOME TAX INFORMATION TABLE OF CONTENTS Taxes on Loans from the Annuity Savings Fund 1 (Tier 1 and 2 Members Only) Taxes on the Withdrawal of the Annuity

No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not insured by any federal government agency

Understanding iras A Summary of Individual Retirement Accounts No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not insured by any federal government agency 1/15 23038-15A Contents

Understanding iras A Summary of Individual Retirement Accounts No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not insured by any federal government agency 1/15 23038-15A Contents

Roth IRAs. Funding a Roth IRA

The Roth IRA differs from the traditional IRA in that contributions are never deductible and, if certain requirements are met, account distributions are free of federal income tax. Funding a Roth IRA Annual

The Roth IRA differs from the traditional IRA in that contributions are never deductible and, if certain requirements are met, account distributions are free of federal income tax. Funding a Roth IRA Annual

Comparison Chart: Pre-Tax Deferrals, Designated Roth Deferrals, In-Plan Roth Rollovers, & Roth IRAs

Comparison Chart: Pre-Tax Deferrals, Designated Roth Deferrals, In-Plan Roth Rollovers, & s Caution: Please note that some of the items included on this grid are the result of Lincoln National Corporation

Comparison Chart: Pre-Tax Deferrals, Designated Roth Deferrals, In-Plan Roth Rollovers, & s Caution: Please note that some of the items included on this grid are the result of Lincoln National Corporation

KEY FACTORS WHEN CONSIDERING A ROTH IRA CONVERSION

KEY FACTORS WHEN CONSIDERING A ROTH IRA CONVERSION PERTINENT INFORMATION Mr. Kugler has accumulated $1,000,000 in a traditional IRA. Mrs. Kugler is the designated beneficiary (DB) and their daughter is

KEY FACTORS WHEN CONSIDERING A ROTH IRA CONVERSION PERTINENT INFORMATION Mr. Kugler has accumulated $1,000,000 in a traditional IRA. Mrs. Kugler is the designated beneficiary (DB) and their daughter is

IRA Opportunities. Traditional IRA vs. Roth IRA: Which is right for you? What kind of retirement funding vehicle is right for you?

IRA Opportunities. Traditional IRA vs. Roth IRA: Which is right for you? What kind of retirement funding vehicle is right for you? Now more than ever, an Individual Retirement Account (IRA) may help provide

IRA Opportunities. Traditional IRA vs. Roth IRA: Which is right for you? What kind of retirement funding vehicle is right for you? Now more than ever, an Individual Retirement Account (IRA) may help provide

IRA opportunities at UBS

IRA opportunities at UBS IRAs are highly popular and effective retirement savings vehicles that give your investment earnings the benefit of tax-favored treatment and provide an ideal supplement to employer-sponsored

IRA opportunities at UBS IRAs are highly popular and effective retirement savings vehicles that give your investment earnings the benefit of tax-favored treatment and provide an ideal supplement to employer-sponsored

Tax-smart ways to save and invest. TIAA-CREF Financial Essentials

Tax-smart ways to save and invest TIAA-CREF Financial Essentials Today s agenda: 1. Finding funds for saving 2. Tax law provisions promoting saving 3. TIAA-CREF savings opportunities 4. TIAA-CREF can help

Tax-smart ways to save and invest TIAA-CREF Financial Essentials Today s agenda: 1. Finding funds for saving 2. Tax law provisions promoting saving 3. TIAA-CREF savings opportunities 4. TIAA-CREF can help

Basics of IRAs ING FINANCIAL SOLUTIONS. Your future. Made easier. SM

Basics of IRAs t FDIC/NCUA Insured t A Deposit Of A Bank t Bank Guaranteed May Lose Value t Insured By Any Federal Government Agency ING FINANCIAL SOLUTIONS Your future. Made easier. SM Traditional IRA

Basics of IRAs t FDIC/NCUA Insured t A Deposit Of A Bank t Bank Guaranteed May Lose Value t Insured By Any Federal Government Agency ING FINANCIAL SOLUTIONS Your future. Made easier. SM Traditional IRA

How much can I deduct if I am an active participant in a qualified plan?... 2

Table of Contents What is an Individual Retirement Account (IRA)?...................................... 1 Who may establish a Traditional IRA?............................................... 1 How much

Table of Contents What is an Individual Retirement Account (IRA)?...................................... 1 Who may establish a Traditional IRA?............................................... 1 How much

ROTH IRA REQUIREMENTS

Regarding Roth Individual Retirement Annuity (IRA) Plans Described in Section 408A of the Internal Revenue Code This Disclosure Statement ( Disclosure ) presents a general overview of the federal laws

Regarding Roth Individual Retirement Annuity (IRA) Plans Described in Section 408A of the Internal Revenue Code This Disclosure Statement ( Disclosure ) presents a general overview of the federal laws

An IRA can put you in control of your retirement, whether you

IRAs: Powering Your Retirement One of the most effective ways to build and manage funds to help you meet your financial goals is through an Individual Retirement Account (IRA). An IRA can put you in control

IRAs: Powering Your Retirement One of the most effective ways to build and manage funds to help you meet your financial goals is through an Individual Retirement Account (IRA). An IRA can put you in control

10 common IRA mistakes

10 common mistakes Help protect your valuable retirement assets Not FDIC Insured May Lose Value No Bank Guarantee Not Insured by Any Government Agency You ve worked hard to build your retirement assets......

10 common mistakes Help protect your valuable retirement assets Not FDIC Insured May Lose Value No Bank Guarantee Not Insured by Any Government Agency You ve worked hard to build your retirement assets......

TIAA-CREF (found on website)

") TIAA-CREF (found on website) Retirement Security: IRA Basics ShareEmailPrint Even if you're already saving in a workplace retirement plan, think about investing in an individual retirement account (IRA)

TIAA-CREF (found on website) Retirement Security: IRA Basics ShareEmailPrint Even if you're already saving in a workplace retirement plan, think about investing in an individual retirement account (IRA)

Beginning in 2010, the Tax Increase Prevention and ROTH IRA CONVERSION

ROTH IRA CONVERSION Assessing Suitability of the Strategy for Individuals and their Heirs Executive Summary A Roth IRA conversion may benefit individuals during their retirement years by potentially reducing

ROTH IRA CONVERSION Assessing Suitability of the Strategy for Individuals and their Heirs Executive Summary A Roth IRA conversion may benefit individuals during their retirement years by potentially reducing

Protection Now. Income Later.

Protection Now. Income Later. Life Insurance Retirement Plan for Women AD-OC-749C What are two problems facing today s woman? 1 2 The Family s Financial Vulnerability. Whether you are part of a two-income

Protection Now. Income Later. Life Insurance Retirement Plan for Women AD-OC-749C What are two problems facing today s woman? 1 2 The Family s Financial Vulnerability. Whether you are part of a two-income

Advanced Markets Estate Planning for Non-Citizens in the United States

Estate Planning for Non-Citizens in the United States SINGLE LIFE SPOUSAL ACCESS TRUSTS: A LIFE INSURANCE ALTERNATIVE As large numbers of people from other countries settle in the United States (U.S.),

Estate Planning for Non-Citizens in the United States SINGLE LIFE SPOUSAL ACCESS TRUSTS: A LIFE INSURANCE ALTERNATIVE As large numbers of people from other countries settle in the United States (U.S.),

12/31/14. Retirement Account Distributions. General IRA Rules. Traditional IRA Distributions p. 90. Required Minimum Distributions [RMD]:

![12/31/14. Retirement Account Distributions. General IRA Rules. Traditional IRA Distributions p. 90. Required Minimum Distributions [RMD]:](/thumbs/24/3041478.jpg "12/31/14. Retirement Account Distributions. General IRA Rules. Traditional IRA Distributions p. 90. Required Minimum Distributions [RMD]:") Retirement Account Distributions Chapter 8 Pages 89-118 General IRA Rules Required Minimum Distributions [RMD]: Traditional IRA Yes ROTH IRA - for contributor and spouse No - for non-contributor Yes Traditional

Retirement Account Distributions Chapter 8 Pages 89-118 General IRA Rules Required Minimum Distributions [RMD]: Traditional IRA Yes ROTH IRA - for contributor and spouse No - for non-contributor Yes Traditional

Social Security and Your Retirement

Social Security and Your Retirement Important information for investors planning Social Security will not and was never designed to provide all of the income you ll need to live comfortably during retirement.

Social Security and Your Retirement Important information for investors planning Social Security will not and was never designed to provide all of the income you ll need to live comfortably during retirement.

INDIVIDUAL TAX STRATEGIES

BY SCOTT HENSLEY [email protected] DECEMBER 4, 2014 STANCIL & COMPANY CERTIFIED PUBLIC ACCOUNTANTS 4909 WINDY HILL DRIVE RALEIGH, NC 27609 919-872-1260 TOPICS TO BE COVERED TODAY WHAT IS TAX PLANNING

BY SCOTT HENSLEY [email protected] DECEMBER 4, 2014 STANCIL & COMPANY CERTIFIED PUBLIC ACCOUNTANTS 4909 WINDY HILL DRIVE RALEIGH, NC 27609 919-872-1260 TOPICS TO BE COVERED TODAY WHAT IS TAX PLANNING

U.S. Global Investors Mutual Funds-Forms 1099R and 1099Q Guide for Tax Year 2010

U.S. Global Investors Funds U.S. Global Investors Mutual Funds-Forms 1099R and 1099Q Guide for Tax Year 2010 U.S. Global Investors is committed to providing accuracy in reporting tax information related

U.S. Global Investors Funds U.S. Global Investors Mutual Funds-Forms 1099R and 1099Q Guide for Tax Year 2010 U.S. Global Investors is committed to providing accuracy in reporting tax information related

The Advantages of a Stretch IRA

Lifetime Retirement Planning with Wachovia Securities. The Advantages of a Stretch IRA Much is being heard these days about a concept called the Stretch IRA. This phrase is bandied about as being the answer

Lifetime Retirement Planning with Wachovia Securities. The Advantages of a Stretch IRA Much is being heard these days about a concept called the Stretch IRA. This phrase is bandied about as being the answer

Table of Contents. Section 1. Introduction Entities...2 IRS Approval...2

37788 X (1/16) Table of Contents Section 1. Introduction Entities...2 IRS Approval...2 Section 2. Right to revoke your IRA Revocation... 3 Section 3. Contributions Funding your IRA with new contributions...

37788 X (1/16) Table of Contents Section 1. Introduction Entities...2 IRS Approval...2 Section 2. Right to revoke your IRA Revocation... 3 Section 3. Contributions Funding your IRA with new contributions...

ROTH 401(k) FEATURE QUESTION & ANSWER (Q&A)

FEATURE QUESTION & ANSWER (Q&A)") ROTH 401(k) FEATURE QUESTION & ANSWER (Q&A) Purpose of Q&A: Beginning January 1, 2006, employers that sponsor 401(k) retirement plans may offer a new plan design feature after-tax Roth deferrals. The purpose

ROTH 401(k) FEATURE QUESTION & ANSWER (Q&A) Purpose of Q&A: Beginning January 1, 2006, employers that sponsor 401(k) retirement plans may offer a new plan design feature after-tax Roth deferrals. The purpose

Strength of Many. Convenience of One. Voya Select Advantage IRA. Mutual Fund Custodial Account

Strength of Many. Convenience of One. Voya Select Advantage IRA Mutual Fund Custodial Account Life brings change. C hange often comes from life events such as switching jobs or retiring. What impact will

Strength of Many. Convenience of One. Voya Select Advantage IRA Mutual Fund Custodial Account Life brings change. C hange often comes from life events such as switching jobs or retiring. What impact will

Roth IRA. Explore the Opportunity. 2 RBC Wealth Management

Roth IRA Explore the Opportunity 2 RBC Wealth Management N o w Y o u H a v e E v e n M o r e F l e x i b i l i t y i n H o w Y o u I n v e s t f o r Y o u r F u t u r e Retirement a time that you work

Roth IRA Explore the Opportunity 2 RBC Wealth Management N o w Y o u H a v e E v e n M o r e F l e x i b i l i t y i n H o w Y o u I n v e s t f o r Y o u r F u t u r e Retirement a time that you work

Roth 401(k) THE Alternative WAY TO SAVE FOR RETIREMENT

THE Alternative WAY TO SAVE FOR RETIREMENT") Roth 401(k) THE Alternative WAY TO SAVE FOR RETIREMENT An Additional Way to Reach Your Financial Destination Your company sponsored retirement plan offers an additional feature that may assist you in reaching

Roth 401(k) THE Alternative WAY TO SAVE FOR RETIREMENT An Additional Way to Reach Your Financial Destination Your company sponsored retirement plan offers an additional feature that may assist you in reaching

TRADITIONAL IRA AND ROTH IRA. Plan Today for a Secure Tomorrow

TRADITIONAL IRA AND ROTH IRA Plan Today for a Secure Tomorrow INVESTMENT-LED. INVESTOR-FOCUSED. As an investment-led firm, we evaluate every decision from an investment perspective in an effort to achieve

TRADITIONAL IRA AND ROTH IRA Plan Today for a Secure Tomorrow INVESTMENT-LED. INVESTOR-FOCUSED. As an investment-led firm, we evaluate every decision from an investment perspective in an effort to achieve

Traditional IRA and Roth IRA

Traditional IRA and Roth IRA Plan Today for a Secure Tomorrow lord abbett retirement services Bring an Unwavering Commitment to Your Retirement Plan Founded in 1929, Lord Abbett is an independent, privately

Traditional IRA and Roth IRA Plan Today for a Secure Tomorrow lord abbett retirement services Bring an Unwavering Commitment to Your Retirement Plan Founded in 1929, Lord Abbett is an independent, privately

How To Convert An Ira To A Roth Ira

Roth Conversion Frequently Asked Questions Brian Dobbis QPA, QKA, QPFC Retirement Analyst, Private Wealth Group 888-522-2388 A Roth individual retirement account (IRA) is a tax-deferred and potentially

Roth Conversion Frequently Asked Questions Brian Dobbis QPA, QKA, QPFC Retirement Analyst, Private Wealth Group 888-522-2388 A Roth individual retirement account (IRA) is a tax-deferred and potentially

STATE OF HAWAII EMPLOYEES RETIREMENT SYSTEM SPECIAL TAX NOTICE REGARDING ROLLOVER OPTIONS

ERS Notice 402(f) (1/2010) STATE OF HAWAII EMPLOYEES RETIREMENT SYSTEM SPECIAL TAX NOTICE REGARDING ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are eligible

ERS Notice 402(f) (1/2010) STATE OF HAWAII EMPLOYEES RETIREMENT SYSTEM SPECIAL TAX NOTICE REGARDING ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are eligible

Important Information Morgan Stanley SIMPLE IRA Summary

SIMPLE IRA Summary September 2013 Important Information Morgan Stanley SIMPLE IRA Summary The following is intended to provide you with basic information on the roles and services that Morgan Stanley Smith

SIMPLE IRA Summary September 2013 Important Information Morgan Stanley SIMPLE IRA Summary The following is intended to provide you with basic information on the roles and services that Morgan Stanley Smith

EXPLORING YOUR IRA OPTIONS. Whichever you choose traditional or Roth investing in an IRA is a good step toward saving for retirement.

EXPLORING YOUR IRA OPTIONS Whichever you choose traditional or Roth investing in an IRA is a good step toward saving for retirement. 2 EXPLORING YOUR IRA OPTIONS Planning for retirement can be a challenging

EXPLORING YOUR IRA OPTIONS Whichever you choose traditional or Roth investing in an IRA is a good step toward saving for retirement. 2 EXPLORING YOUR IRA OPTIONS Planning for retirement can be a challenging

TERMINATION FORM - 206

TERMINATION FORM - 206 Participant must be provided with the Special Tax Notice Regarding Plan Payments. I INSTRUCTIONS The Termination Form is used to process all types of plan distributions due to termination

TERMINATION FORM - 206 Participant must be provided with the Special Tax Notice Regarding Plan Payments. I INSTRUCTIONS The Termination Form is used to process all types of plan distributions due to termination

COORDINATING IRA DISTRIBUTIONS WITH SOCIAL SECURITY INCOME

COORDINATING IRA DISTRIBUTIONS WITH SOCIAL SECURITY INCOME By Thomas W. Batterman Selecting an improper IRA distribution strategy for individuals eligible for Social Security benefits can dramatically

COORDINATING IRA DISTRIBUTIONS WITH SOCIAL SECURITY INCOME By Thomas W. Batterman Selecting an improper IRA distribution strategy for individuals eligible for Social Security benefits can dramatically

Is Your Financial Portfolio an Unfinished Work? Color It with a Life Insurance Retirement Plan Protection Now, Income Later

Life Insurance Client Guide The Art of Retirement Is Your Financial Portfolio an Unfinished Work? Color It with a Life Insurance Retirement Plan Protection Now, Income Later AD-OC-770D 1 Picture Your Future

Life Insurance Client Guide The Art of Retirement Is Your Financial Portfolio an Unfinished Work? Color It with a Life Insurance Retirement Plan Protection Now, Income Later AD-OC-770D 1 Picture Your Future

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE. Tax-advantaged IRAs. Invest in your retirement savings while reducing taxes

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Taxadvantaged IRAs Invest in your retirement savings while reducing taxes Find the answers inside Why invest for retirement? p. 1 Discover three good reasons

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Taxadvantaged IRAs Invest in your retirement savings while reducing taxes Find the answers inside Why invest for retirement? p. 1 Discover three good reasons

Caution: Special rules apply to certain distributions to reservists and national guardsmen called to active duty after September 11, 2001.

Thorsen Clark Tracey Wealth Management 301 East Pine Street Suite 1100 Orlando, FL 32801 407-246-8888 407-897-4427 [email protected] tctwealthmanagement.com Roth IRAs

Thorsen Clark Tracey Wealth Management 301 East Pine Street Suite 1100 Orlando, FL 32801 407-246-8888 407-897-4427 [email protected] tctwealthmanagement.com Roth IRAs

NATIONAL WESTERN LIFE INSURANCE COMPANY YOUR ROLLOVER OPTIONS

NATIONAL WESTERN LIFE INSURANCE COMPANY YOUR ROLLOVER OPTIONS This notice explains how you can continue to defer federal income tax on your retirement savings and contains important information you will

NATIONAL WESTERN LIFE INSURANCE COMPANY YOUR ROLLOVER OPTIONS This notice explains how you can continue to defer federal income tax on your retirement savings and contains important information you will

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information you will

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information you will

Traditional or Roth IRA? Making the Right Choice for You!

Traditional or Roth IRA? Making the Right Choice for You! A Guide to Individual Retirement Accounts We ve selected some commonly asked questions from over 200 submitted after the IRA Basics webinar. Although

Traditional or Roth IRA? Making the Right Choice for You! A Guide to Individual Retirement Accounts We ve selected some commonly asked questions from over 200 submitted after the IRA Basics webinar. Although

1040 Review Guide: MARKETS ADVANCED. Using Your Clients 1040 to Identify Planning Opportunities

1040 Review Guide: Using Your Clients 1040 to Identify Planning Opportunities ADVANCED MARKETS Producers Guide to a 1040 Review At Transamerica, we re committed to providing you and your clients with the

1040 Review Guide: Using Your Clients 1040 to Identify Planning Opportunities ADVANCED MARKETS Producers Guide to a 1040 Review At Transamerica, we re committed to providing you and your clients with the

T. Rowe Price SIMPLE IRA SUMMARY & AGREEMENT

T. Rowe Price SIMPLE IRA SUMMARY & AGREEMENT June 2006 Important Change to the T. Rowe Price Traditional and Roth IRA Summary & Agreement and the T. Rowe Price SIMPLE IRA Summary & Agreement Please review

T. Rowe Price SIMPLE IRA SUMMARY & AGREEMENT June 2006 Important Change to the T. Rowe Price Traditional and Roth IRA Summary & Agreement and the T. Rowe Price SIMPLE IRA Summary & Agreement Please review

DISTRIBUTION FROM A PLAN NOT SUBJECT TO QJSA

DISTRIBUTION FROM A PLAN NOT SUBJECT TO QJSA This form must be preceded by or accompanied by the Special Tax Notice Regarding Plan Payments [Code (402(f)) Notice] PLAN INFORMATION Name of Plan: PARTICIPANT

DISTRIBUTION FROM A PLAN NOT SUBJECT TO QJSA This form must be preceded by or accompanied by the Special Tax Notice Regarding Plan Payments [Code (402(f)) Notice] PLAN INFORMATION Name of Plan: PARTICIPANT

SACRAMENTO METROPOLITAN FIRE DISTRICT GOVERNMENTAL 457 DEFERRED COMPENSATION PLAN

SACRAMENTO METROPOLITAN FIRE DISTRICT GOVERNMENTAL 457 DEFERRED COMPENSATION PLAN DEEMED IRA ACCOUNTS DISCLOSURE STATEMENT This Disclosure Statement summarizes the provisions relating to the deemed IRA

SACRAMENTO METROPOLITAN FIRE DISTRICT GOVERNMENTAL 457 DEFERRED COMPENSATION PLAN DEEMED IRA ACCOUNTS DISCLOSURE STATEMENT This Disclosure Statement summarizes the provisions relating to the deemed IRA

COLLIERS INTERNATIONAL USA, LLC And Affiliated Employers 401(K) Plan DISTRIBUTION ELECTION

Plan DISTRIBUTION ELECTION") 1. EMPLOYEE INFORMATION (Please print) COLLIERS INTERNATIONAL USA, LLC And Affiliated Employers 401(K) Plan DISTRIBUTION ELECTION Name: Address: Social Security No.: Birth Date: City: State: Zip: Termination

1. EMPLOYEE INFORMATION (Please print) COLLIERS INTERNATIONAL USA, LLC And Affiliated Employers 401(K) Plan DISTRIBUTION ELECTION Name: Address: Social Security No.: Birth Date: City: State: Zip: Termination

The Patient Protection and Affordable Care Act

Private Wealth Management Products & Services March 2010 The Patient Protection and Affordable Care Act Health care act includes variety of tax changes President Obama signed the Patient Protection and

Private Wealth Management Products & Services March 2010 The Patient Protection and Affordable Care Act Health care act includes variety of tax changes President Obama signed the Patient Protection and

DISTRIBUTION REQUEST FORM FICA ALTERNATIVE PLAN FOR FLORIDA STATE UNIVERSITY

DISTRIBUTION REQUEST FORM FICA ALTERNATIVE PLAN FOR FLORIDA STATE UNIVERSITY INSTRUCTIONS: Complete items one through four and send this form to the employer at the address printed at the bottom of the

DISTRIBUTION REQUEST FORM FICA ALTERNATIVE PLAN FOR FLORIDA STATE UNIVERSITY INSTRUCTIONS: Complete items one through four and send this form to the employer at the address printed at the bottom of the

Governmental 457(b) Application For Distribution

Application For Distribution") #1303-PS (5/14/2008) Governmental 457(b) Application For Distribution GENERAL INFORMATION Name of Plan Name of Employer Address City State Zip Name of Participant Date of Birth Complete the following section

#1303-PS (5/14/2008) Governmental 457(b) Application For Distribution GENERAL INFORMATION Name of Plan Name of Employer Address City State Zip Name of Participant Date of Birth Complete the following section

Questions and Answers about the Roth 401(k)

") THE RETIREMENT GROUP AT MERRILL LYNCH Q A Questions and Answers about the Roth 401(k) How the Roth 401(k) Works Q. What is the Roth 401(k) contribution option? A. The Roth 401(k) contribution option allows

THE RETIREMENT GROUP AT MERRILL LYNCH Q A Questions and Answers about the Roth 401(k) How the Roth 401(k) Works Q. What is the Roth 401(k) contribution option? A. The Roth 401(k) contribution option allows

Consider the advantages of the Roth 403(b)

") Consider the advantages of the Roth 403(b) Your plan offers a way of saving for retirement known as the Roth 403(b) What is it? It s a way to get your money tax-free in retirement. You can make tax-free

Consider the advantages of the Roth 403(b) Your plan offers a way of saving for retirement known as the Roth 403(b) What is it? It s a way to get your money tax-free in retirement. You can make tax-free

TAX SHELTERED ANNUITY ROLLOVER / PARTIAL WITHDRAWAL / FULL SURRENDER REQUEST

General American Retirement & Investment Services PO Box 19098 Greenville, SC 29602 Customer Service: 800-449-6447 Fax: 866-214-0926 TAX SHELTERED ANNUITY ROLLOVER / PARTIAL WITHDRAWAL / FULL SURRENDER

General American Retirement & Investment Services PO Box 19098 Greenville, SC 29602 Customer Service: 800-449-6447 Fax: 866-214-0926 TAX SHELTERED ANNUITY ROLLOVER / PARTIAL WITHDRAWAL / FULL SURRENDER

AN ANALYSIS OF ROTH CONVERSIONS 1

AN ANALYSIS OF ROTH CONVERSIONS In 1997, Congress introduced the Roth IRA, giving investors a new product for retirement savings. The Roth IRA is essentially a mirror image of the Traditional IRA, but

AN ANALYSIS OF ROTH CONVERSIONS In 1997, Congress introduced the Roth IRA, giving investors a new product for retirement savings. The Roth IRA is essentially a mirror image of the Traditional IRA, but