John Harris MA, MBA, PhD, CGA, FCMA - member of the CIFP Education Committee. - worked in both administrative and teaching positions in higher

|

|

|

- April Harmon

- 8 years ago

- Views:

Transcription

1 Current Trends Financial Planning Issues The Economy The Federal Budget The Canada Job Grant Jobs Without People/People Without Jobs Is this a concern within the Financial Services industry (solving the puzzle)?

?")

2 John Harris MA, MBA, PhD, CGA, FCMA - member of the CIFP Education Committee. - worked in both administrative and teaching positions in higher education for the past fifteen years and is now a full-time Faculty Member in the School of Business at Seneca College (teaching Accounting & Financial Service courses). - Fellow of the Society of Management Accountants and a Senior Academic with CGA Canada. He has completed research and made presentations on a number of topics including Management Accounting & Performance Measurement for Ontario hospitals, Audit & Risk Management Practices in the Public Sector and Student Success Initiatives and Funding Issues at Ontario colleges & universities. - volunteers on other boards/committees. - For example, Board Treasurer for the Progress Career Planning Institute ( with a mission to offer career development services for people to realize their full potential. PCPI facilitates the annual Toronto IEP Conference, which is regarded as one of the most innovative and respectful events for Internationally Educated Professional newcomers seeking practical, effective career advice. - has contributed to the work of the Centre of Excellence at the Toronto Financial Services Alliance. The COE is focused on strengthening Toronto s talent pipeline, which is crucial to addressing the needs of employers, students, internationally educated professionals and educators.

3 Tax Planning Tool Kit by Jamie Golombek, Managing Director, Tax & Estate Planning, CIBC Private Wealth Management. Presentation by Jamie on the morning of the 29 th Some of the 10 tips: think of paying down debt as a form of after-tax investing. In fact, paying down debt is similar to contributing to a TFSA. For example, let s say you direct $1,000 of after-tax cash flow to pay down debt that carries a 5% interest rate. After one year, your debt load will have been reduced by $1,000 and you will have saved $50 ($1,000 x 5%) of interest expense. If, on the other hand, $1,000 of your after-tax earnings is used to make a contribution to a TFSA earning 5%, in one year s time, the after-tax value of your TFSA will be worth $1,050 ($1,000 x 1.05%). In both cases, your net worth will have increased by $1,050. So, when it comes to deciding between paying down debt and investing in a TFSA, since both options use after-tax funds, you could simply choose the investment (debt or TFSA) with the highest rate of return. Source:

of interest expense.")

4 Experts have been challenging the 70% figure for years. Fred Vettese Fred Vettese the real retirement that introduces an idea he calls the neutral retirement income target (NRIT) to improve that estimate. The goal of the NRIT is to determine how much of your current income goes to day-to-day consumption, and then to estimate the retirement income you will need to meet that same level of spending. Vettese found that in many cases, retirees could enjoy the same level of consumption on less than half of their pre-retirement income. Not only do retirees have significantly lower expenses, assuming they have paid off their mortgage and their kids have moved out, but they also enjoy an array of tax benefits that working people do not. Source:

5 Here s an example: Using a couple with a total income of $110,000 Vettese assumes the couple contribute 3.8% of their income to RRSPs, spend $1,100 a month on child-rearing and have monthly mortgage payments of $1,633. Once you deduct income taxes and payroll taxes (CPP and EI premiums), this couple is left with $46,600 to spend. After retirement, the couple would no longer be contributing to an RRSP, incurring child-rearing expenses or paying down a mortgage. They would pay no payroll taxes, and they would pay dramatically lower income taxes thanks to the pension credit, age credit and income splitting. As a result, they would need an income of just $48,300 to fund the same level of consumption they enjoyed while working. That is 44% of their preretirement income. Many Canadians will have different circumstances than this fictional couple and the specifics matter a lot. However, Vettese also includes examples for individuals with higher and lower income, no children and no spouse. The NRIT in each example is different, but it is usually in the ballpark of 50%".

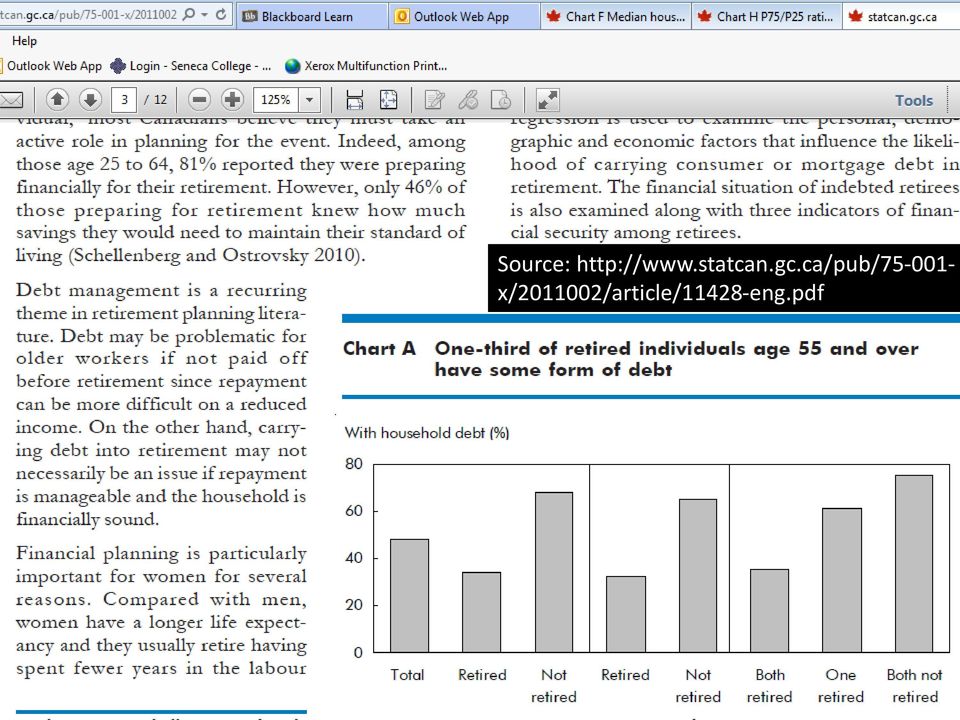

6 Statistics Canada s look at debt-toincome and debt-to-asset ratios by age cohort in Canada. The following findings were found from the study except: In 1977, young adults had debt equal to 35% of their total assets. Younger adults from the 1999 cohort had debt equal to 48% of assets. 1 in 3 retired individuals age 55 and over, whether single or in a couple, held average debt of about $60,000.

7 For the debt-to-assets ratio, the greatest contrast was between the most recent cohort and the previous ones. In 1977, young adults had debt equal to 35% of their total assets, a proportion that declined to just 3% by their late working years. Similarly, young adults in 1984 had debt equalling 32% of their assets, before declining to 10% in their late working years. In contrast, younger adults from the 1999 cohort had debt equalling 48% of assets, declining to 39% in their prime working years. This compares to 25% among prime-age individuals from the 1977 cohort. By all measures, the 1999 cohort was the most indebted. Source:

8 Source: x/ /article/11428-eng.pdf

9 Putting OAS just a bit further out of reach will induce more older workers to keep working an extra two years, the effect on younger workers will be A continued inability for young workers to find permanent jobs (decline in quality of jobs) Young workers will be less likely to be covered by a union. Employee benefits are increasingly withheld from young hires.

10 The Economy The near term, Canada will continue to be dominated by a struggling through for the Canadian economy while the world rights itself - source: Policy and Economic Analysis Program Rotman School of Management source: OX&actionID=view_attach&id=2&mimecache=1d37e964cfc90bf57817a2d9028c2a02

11

12 Economy May 18, 2013 Globe & Mail had the following article work-experience-should-it-be-part-of-thecurriculum/article /?service=mobile There is need for focus of connection between work and study will become even more important as finding a job becomes even more competitive. Sheldon Levy (Ryerson University) is quoted in the following link saying that there will be no new net jobs. All net job growth comes entirely from start-up firms. events/commentary/commentary-pdfs/empireclub_sheldon-levy-remarks_final

is quoted in the following link saying that there will be no new net jobs.")

13 The Economy Mark Carney, Central Bank, said Canada has been well-served by a sound and regulated banking sector, as well as low government debt that allowed policy-makers room to borrow on global markets to stimulate the economy. Carney said Canada cannot rest on its laurels, however. "In a rapidly shifting world, only sustained education, ingenuity and investment can maintain competitiveness," he said. "This means we must continuously invest in our workforce. With technology and trade transforming the workplace, the need to improve skills across the spectrum of work has never been greater. Without sustained and significant reforms, a decade of stagnation threatens (source: Globe and Mail ROB May22, 2013)

14 Source: Corp-Tax-highlights-from-the-2013-federal-budget /

15 The March 2013 Federal Budget can best be described as There were no increases in personal or corporate tax rates in the budget There was considerable focus on measures that will increase tax fairness and close perceived tax loopholes There was a focus on connecting Jobs Without People and People Without Jobs

16 Toronto Dominion (TD Economics) report stated that Ontario s postsecondary attainment rate is Higher than any other OECD member country (2013, roughly two-thirds of Ontarians possessed a postsecondary education credential). The higher education system in Canada is said not to be integrated with employer needs The study noted that Switzerland is a good example where there is greater integration between higher education and employer needs

17 The TD Economics report said the Switzerland system of connecting higher education with employer needs was superior to the system in Canada. In Switzerland there is A comparatively low level of youth unemployment in Switzerland as there is a dual apprenticeship system. The dual system has existed in Switzerland for over a century and is well developed as a cooperative effort between the government, educators and professional organizations. The majority of Swiss youth (approximately 70 percent) continue their education after compulsory schooling in vocational education. The dual system of vocational education is comprised of a practical course in a private or public company and parallel attendance at a vocational training school. Students go to school for one to one and a half days per week and engage in an apprenticeship for the rest of the week. The vocational school education complements the practical vocational experience gained on the job.

continue their education after compulsory schooling in vocational education.")

18 March 2013 Federal Budget for the first time, the Canada Job Grant will take Skills-training choices out of the hands of government and put them where they belong in the hands of employers and Canadians who want to work. Job seekers will train at community colleges, career colleges, polytechnics or union training halls, among others. Current Labour Market Agreements with the provinces and territories expire in The Government of Canada will negotiate new Agreements centered on the Canada Job Grant.

19 2007 Report

20 Toronto boasts a very highly skilled and diverse workforce that supports the finance sector. Toronto region's financial services sector employs approximately 229,000, which represents 62% of Ontario's and 29% of Canada s Financial Services sector employment. Financial Services is an equally significant contributor to the local economy, accounting for roughly 8% of the Toronto region's direct employment and roughly 14% of its GDP (19% for the city itself). The Canada Jobs Grant does not specifically address the need for funding to support employment in the Financial Services industry (focusing instead on promoting education in fields where there is high demand from employers, including in science, technology, engineering, mathematics and the skilled trades).

.")

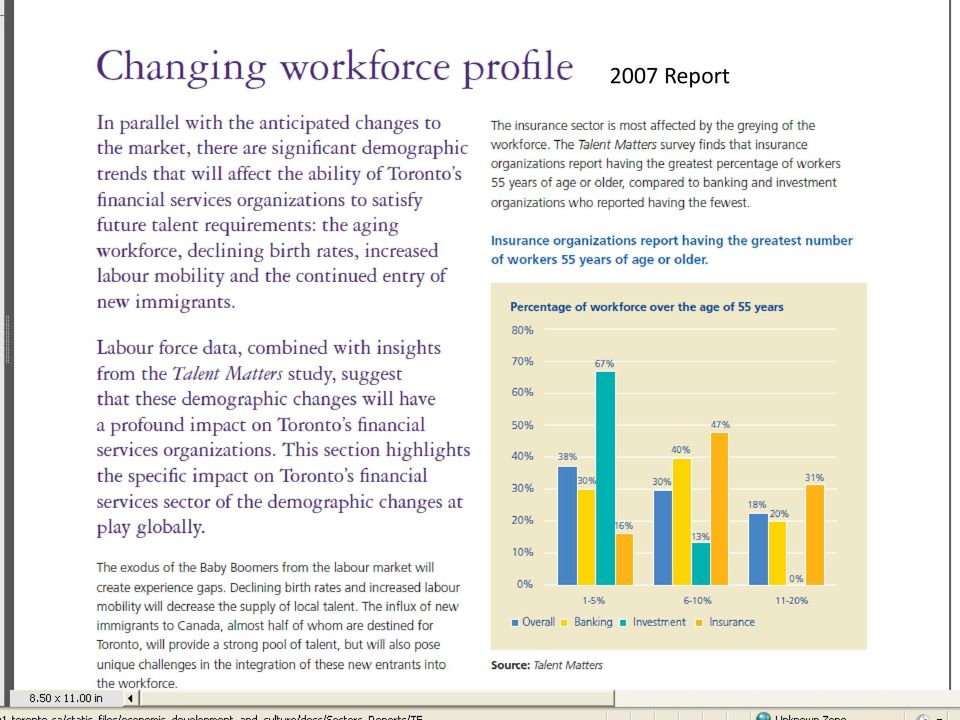

21 Concern should be placed on how best to staff the Financial Services Industry in Canada as There is a need for talent, particularly as the leading edge of the Baby Boom generation enters retirement. In 2007, 12.2% of the financial services workforce was 55 years of age or older and the average retirement age in the industry was 61. A further 20% of the workforce was between the ages of 45 and 54. The 2007 report stressed the need to invest energy, resources and commitment to develop and grow talent (from both international talent pools and through reach to domestic higher educational institutions).

22

23

24

25

26

27

28

29 Questions: 1) In the last 5 years (since the release of the Deloitte report), has your organization changed its practices related to developing talent portfolios or workforce plans to understand the financial consequences of talent decisions? If so, what has been the result?

30 Questions: 2) Can you see benefit in a greater reach to educational institutions (colleges and universities) in order to develop a more integrated education & training system like that in Switzerland (as referenced in the TD Economics report)? If so, do you believe that the Canada Job Grant could facilitate this more integrated system if the financial services industry could be recognized as an highdemand job area? If so, how?

ONTARIO RETIREMENT PENSION PLAN

THE ONTARIO RETIREMENT PENSION PLAN DISCUSSING A MADE-IN-ONTARIO SOLUTION ASSOCIATE MINISTER S MESSAGE Ask a child what they want to be when they grow up and they ll tell you. A doctor. An astronaut.

THE ONTARIO RETIREMENT PENSION PLAN DISCUSSING A MADE-IN-ONTARIO SOLUTION ASSOCIATE MINISTER S MESSAGE Ask a child what they want to be when they grow up and they ll tell you. A doctor. An astronaut.

How to Save for Retirement in Ontario, Canada?

1 Canadian Labour Congress Background for Individual Responses Questions from the Ministry of Finance Ontario Consulting with Ontarians on Canada s Retirement Income System How much income do you think

1 Canadian Labour Congress Background for Individual Responses Questions from the Ministry of Finance Ontario Consulting with Ontarians on Canada s Retirement Income System How much income do you think

THE WAY TO BUILDING A BETTER ONTARIO 2016 Ontario Pre-Budget Submission

THE WAY TO BUILDING A BETTER ONTARIO 2016 Ontario Pre-Budget Submission February 2016 Tel/Tél: 416.497.4110 Toll-free/Sans frais: 1.800.268.5763 Fax/Téléc: 416.496.6552 Who is Unifor Unifor is a new Canadian

THE WAY TO BUILDING A BETTER ONTARIO 2016 Ontario Pre-Budget Submission February 2016 Tel/Tél: 416.497.4110 Toll-free/Sans frais: 1.800.268.5763 Fax/Téléc: 416.496.6552 Who is Unifor Unifor is a new Canadian

Comments on Securing Our Retirement Future: Consulting with Ontarians on Canada s Retirement Income System

November 29, 2010 Ministry of Finance Retirement Income Security Submission c/o Communications & Corporate Affairs Branch 3rd Floor, Frost Building North 95 Grosvenor Street Toronto, ON M7A 1Z1 Re: Comments

November 29, 2010 Ministry of Finance Retirement Income Security Submission c/o Communications & Corporate Affairs Branch 3rd Floor, Frost Building North 95 Grosvenor Street Toronto, ON M7A 1Z1 Re: Comments

Public Consultation Package

Public Consultation Package Request for Comments Retirement Income Adequacy in Canada Yukon Finance March 2010 Whitehorse, Yukon March 2010 Message from the Premier and Minister of Finance The Yukon Government

Public Consultation Package Request for Comments Retirement Income Adequacy in Canada Yukon Finance March 2010 Whitehorse, Yukon March 2010 Message from the Premier and Minister of Finance The Yukon Government

pensions backgrounder #4

pensions backgrounder #4 Private Retirement Savings Part 4 in a Series The full series of pension backgrounders are contained in the National Union s Pensions Manual, Fourth Edition available from the

pensions backgrounder #4 Private Retirement Savings Part 4 in a Series The full series of pension backgrounders are contained in the National Union s Pensions Manual, Fourth Edition available from the

Private RRSPs and Small Business Owners - The Canadian Tax Dividend

Private Wealth Management Small Business Report October 19, 2010 April 17, 2007 Rethinking RRSPs for Business Owners: Why Taking a Salary May Not Make Sense by Jamie Golombek Abstract Traditionally, many

Private Wealth Management Small Business Report October 19, 2010 April 17, 2007 Rethinking RRSPs for Business Owners: Why Taking a Salary May Not Make Sense by Jamie Golombek Abstract Traditionally, many

The Great Divide: Income splitting strategies can lower your family s taxes by Jamie Golombek

March 2015 The Great Divide: Income splitting strategies can lower your family s taxes by Jamie Golombek While the new Family Tax Cut credit, which provides a form of income splitting, has been getting

March 2015 The Great Divide: Income splitting strategies can lower your family s taxes by Jamie Golombek While the new Family Tax Cut credit, which provides a form of income splitting, has been getting

PENSION INNOVATION FOR CANADIANS: THE TARGET BENEFIT PENSION PLAN

PENSION INNOVATION FOR CANADIANS: THE TARGET BENEFIT PENSION PLAN SUBMISSION TO THE DEPARTMENT OF FINANCE, CANADA, FROM THE CONGRESS OF UNION RETIREES OF CANADA, JUNE 23, 2014. The Congress of Union Retirees

PENSION INNOVATION FOR CANADIANS: THE TARGET BENEFIT PENSION PLAN SUBMISSION TO THE DEPARTMENT OF FINANCE, CANADA, FROM THE CONGRESS OF UNION RETIREES OF CANADA, JUNE 23, 2014. The Congress of Union Retirees

The Canadian Retirement Income Guide 2014 Edition. Maximizing your retirement income while minimizing your taxes

The Canadian Retirement Income Guide 2014 Edition Maximizing your retirement income while minimizing your taxes Introduction When you retire, not only does your daily routine change, but your pay cheque

The Canadian Retirement Income Guide 2014 Edition Maximizing your retirement income while minimizing your taxes Introduction When you retire, not only does your daily routine change, but your pay cheque

Employees Retirement Plan University of Windsor Pre-Retirement Seminar

Employees Retirement Plan University of Windsor Pre-Retirement Seminar Welcome! April 22, 2014 Presentation Overview Preparing for Retirement Sources of Retirement Income Types of Pension Plans Plan Definitions

Employees Retirement Plan University of Windsor Pre-Retirement Seminar Welcome! April 22, 2014 Presentation Overview Preparing for Retirement Sources of Retirement Income Types of Pension Plans Plan Definitions

John and Jane Client June 2015

John and Jane Client June 2015 Table Of Contents About This Plan 2 Assumptions 3 About You 4 Your Goals & Objectives 5 Opportunities, Concerns & Notes 6 Net Worth Statement 7 Sources of Income 8 Lifestyle

John and Jane Client June 2015 Table Of Contents About This Plan 2 Assumptions 3 About You 4 Your Goals & Objectives 5 Opportunities, Concerns & Notes 6 Net Worth Statement 7 Sources of Income 8 Lifestyle

CPP Enhancement: The Debate Takes Centre Stage

Enhancement of the Canada Pension Plan (CPP) is expected to be a major issue in the upcoming federal election. This article provides an overview of likely features of a CPP enhancement proposal along with

Enhancement of the Canada Pension Plan (CPP) is expected to be a major issue in the upcoming federal election. This article provides an overview of likely features of a CPP enhancement proposal along with

Income Protection Disability

Income Protection Disability Protecting loved ones from financial hardship in the event of premature death of a primary income earner is usually a high priority for most Canadians. Unfortunately, while

Income Protection Disability Protecting loved ones from financial hardship in the event of premature death of a primary income earner is usually a high priority for most Canadians. Unfortunately, while

Module 5 - Saving HANDOUT 5-7

HANDOUT 5-7 Savings Tools (detailed) 5 Contents High interest savings account This is a type of deposit account. The bank pays you interest. The rate changes with the prime rate set by the bank. This is

HANDOUT 5-7 Savings Tools (detailed) 5 Contents High interest savings account This is a type of deposit account. The bank pays you interest. The rate changes with the prime rate set by the bank. This is

Blinded by the Refund : Why TFSAs may beat RRSPs as better retirement savings vehicle for some Canadians by Jamie Golombek

January 2011 Blinded by the Refund : Why TFSAs may beat RRSPs as better retirement savings vehicle for some Canadians by Jamie Golombek With the introduction of Tax Free Savings Accounts (TFSAs) in 2009,

January 2011 Blinded by the Refund : Why TFSAs may beat RRSPs as better retirement savings vehicle for some Canadians by Jamie Golombek With the introduction of Tax Free Savings Accounts (TFSAs) in 2009,

Retirement plan awareness

René Morissette and Xuelin Zhang I N ADDITION TO WAGES, many employees receive benefits such as dental, life or supplemental medical insurance plans. Employer-sponsored retirement plans registered pension

René Morissette and Xuelin Zhang I N ADDITION TO WAGES, many employees receive benefits such as dental, life or supplemental medical insurance plans. Employer-sponsored retirement plans registered pension

BABY BOOMERS AND RETIREMENT

WHITE PAPER SEPTEMBER 2014 BABY BOOMERS AND RETIREMENT 1 Baby Boomers and Retirement White Paper, September 2014 Roy Ruppert, The Ruppert TABLE OF CONTENTS Introduction 3 Baby Boomers and Consumerism 6

WHITE PAPER SEPTEMBER 2014 BABY BOOMERS AND RETIREMENT 1 Baby Boomers and Retirement White Paper, September 2014 Roy Ruppert, The Ruppert TABLE OF CONTENTS Introduction 3 Baby Boomers and Consumerism 6

Province of Nova Scotia Department of Finance MECHANISMS FOR ENHANCING THE RETIREMENT INCOME SYSTEM IN CANADA

Province of Nova Scotia Department of Finance MECHANISMS FOR ENHANCING THE RETIREMENT INCOME SYSTEM IN CANADA The Government of Nova Scotia is working with other provinces and territories, and the Government

Province of Nova Scotia Department of Finance MECHANISMS FOR ENHANCING THE RETIREMENT INCOME SYSTEM IN CANADA The Government of Nova Scotia is working with other provinces and territories, and the Government

The Benefit of an RRSP, TFSA or Debt Repayment

February 2013 The RRSP, the TFSA and the Mortgage: Making the best choice Jamie Golombek It s important to save. Saving allows us to set aside some of our current earnings for enjoyment at a later time.

February 2013 The RRSP, the TFSA and the Mortgage: Making the best choice Jamie Golombek It s important to save. Saving allows us to set aside some of our current earnings for enjoyment at a later time.

Retirement Compensation Arrangement

tax efficient retirement planning tool business GUIDELINES Retirement Compensation Arrangement Supplement Retirement Income while providing Tax Deductible contributions RRSPs and Pension Plans provide

tax efficient retirement planning tool business GUIDELINES Retirement Compensation Arrangement Supplement Retirement Income while providing Tax Deductible contributions RRSPs and Pension Plans provide

Article. Retiring with debt. by Katherine Marshall. Component of Statistics Canada Catalogue no. 75-001-X Perspectives on Labour and Income

Component of Statistics Canada Catalogue no. 75-001-X Perspectives on Labour and Income Article Retiring with debt by Katherine Marshall April 27, 2011 Statistics Canada Statistique Canada Standard symbols

Component of Statistics Canada Catalogue no. 75-001-X Perspectives on Labour and Income Article Retiring with debt by Katherine Marshall April 27, 2011 Statistics Canada Statistique Canada Standard symbols

UNIVERSITY WORKS 2015 EMPLOYMENT REPORT

UNIVERSITY WORKS 2015 EMPLOYMENT REPORT University Works uses empirical data to report on the outcomes of university graduates in terms of employment levels and earnings, as well as average debt upon graduation.

UNIVERSITY WORKS 2015 EMPLOYMENT REPORT University Works uses empirical data to report on the outcomes of university graduates in terms of employment levels and earnings, as well as average debt upon graduation.

The Revised Pension Plan of

The Revised Pension Plan of A Guide to the Pension Plan for Queen s Staff and Faculty Prepared by Pension Services, Department of Human Resources Fleming Hall, Stewart-Pollock Wing 78 Fifth Field Company

The Revised Pension Plan of A Guide to the Pension Plan for Queen s Staff and Faculty Prepared by Pension Services, Department of Human Resources Fleming Hall, Stewart-Pollock Wing 78 Fifth Field Company

Federal Budget 2014 by Jamie Golombek

February 11, 2014 Federal Budget 2014 by Jamie Golombek The February 11, 2014 federal budget included various tax measures that will affect individuals, registered plans, employers and trusts. Rather than

February 11, 2014 Federal Budget 2014 by Jamie Golombek The February 11, 2014 federal budget included various tax measures that will affect individuals, registered plans, employers and trusts. Rather than

CanadaWorks 2025: The Role of Colleges and Vocational Schools in Achieving a Prosperous Future

CanadaWorks 2025: The Role of Colleges and Vocational Schools in Achieving a Prosperous Future CanadaWorks 2025 In April 2012, the Human Resources Professionals Association (HRPA), in partnership with

CanadaWorks 2025: The Role of Colleges and Vocational Schools in Achieving a Prosperous Future CanadaWorks 2025 In April 2012, the Human Resources Professionals Association (HRPA), in partnership with

BEING FINANCIALLY PREPARED FOR RETIREMENT The Scary Facts! $1.00 item in 1972, costs $3.78 today At the average rate of inflation, the price you pay for an item today will be double in 20 years almost

BEING FINANCIALLY PREPARED FOR RETIREMENT The Scary Facts! $1.00 item in 1972, costs $3.78 today At the average rate of inflation, the price you pay for an item today will be double in 20 years almost

Your Guide to Retirement Income Planning

Your Guide to Retirement Income Planning Your Guide to Retirement Income Planning 3 Your retirement income plan How to create secure income in retirement Your retirement will be as unique as you are. Travel,

Your Guide to Retirement Income Planning Your Guide to Retirement Income Planning 3 Your retirement income plan How to create secure income in retirement Your retirement will be as unique as you are. Travel,

PROPOSAL FOR A PROVINCIAL TAX CREDIT TO SUPPORT INVESTMENT IN ONTARIO'S SOCIAL ECONOMY - REGISTRATION OF INVESTMENTS

PROPOSAL FOR A PROVINCIAL TAX CREDIT TO SUPPORT INVESTMENT IN ONTARIO'S SOCIAL ECONOMY - REGISTRATION OF INVESTMENTS A BRIEF TO THE PARTNERSHIP PROJECT FROM THE ONTARIO SOCIAL ECONOMY ROUNDTABLE (OSER)

PROPOSAL FOR A PROVINCIAL TAX CREDIT TO SUPPORT INVESTMENT IN ONTARIO'S SOCIAL ECONOMY - REGISTRATION OF INVESTMENTS A BRIEF TO THE PARTNERSHIP PROJECT FROM THE ONTARIO SOCIAL ECONOMY ROUNDTABLE (OSER)

Tax-Free Savings Account (TFSA) now available!

now available!") Tax-Free Savings Account (TFSA) now available! Customer-owners have a new way to save money with the Tax-Free Savings Account (TFSA), now available at Metro Credit Union. You can save or invest money without

Tax-Free Savings Account (TFSA) now available! Customer-owners have a new way to save money with the Tax-Free Savings Account (TFSA), now available at Metro Credit Union. You can save or invest money without

2014 Year-End Tax Planning Tips for Seniors, Employees, Families and Students

2014 Year-End Tax Planning Tips for Seniors, Employees, Families and Students While the end of 2014 is approaching, there is still an opportunity for individuals to review their financial situation with

2014 Year-End Tax Planning Tips for Seniors, Employees, Families and Students While the end of 2014 is approaching, there is still an opportunity for individuals to review their financial situation with

Do You Have the Right Life Insurance?

Do You Have the Right Life Insurance? Having adequate life insurance should be an important part of your financial planning. The type(s) you choose will depend on your needs and goals. Life insurance was

Do You Have the Right Life Insurance? Having adequate life insurance should be an important part of your financial planning. The type(s) you choose will depend on your needs and goals. Life insurance was

The Compensation Conundrum: Will it be salary or dividends? by Jamie Golombek

December 2013 The Compensation Conundrum: Will it be salary or dividends? by Jamie Golombek With the year-end for most businesses fast approaching, owner-managers once again will begin to ponder the age-old

December 2013 The Compensation Conundrum: Will it be salary or dividends? by Jamie Golombek With the year-end for most businesses fast approaching, owner-managers once again will begin to ponder the age-old

Collins Barrow. Chartered Accountants

Income Tax for Small Business Presented by Jason Timmermans, BA, CA Partner KMD Introduction Information package What are you hoping to get out of today s session? Agenda Basics of Canadian income tax

Income Tax for Small Business Presented by Jason Timmermans, BA, CA Partner KMD Introduction Information package What are you hoping to get out of today s session? Agenda Basics of Canadian income tax

Mapping the Non-profit Sector

Mapping the Non-profit Sector Kathryn McMullen Grant Schellenberg Executive Summary December 2002 Document No. 1 CPRN Research Series on Human Resources in the Non-profit Sector, available at http://www.cprn.org

Mapping the Non-profit Sector Kathryn McMullen Grant Schellenberg Executive Summary December 2002 Document No. 1 CPRN Research Series on Human Resources in the Non-profit Sector, available at http://www.cprn.org

Introducing. Tax-Free Savings Accounts

Introducing Tax-Free Savings Accounts Tax-Free Savings Accounts A new way to save Tax-free savings accounts were introduced by the federal government in the 2008 budget as an incentive for Canadians to

Introducing Tax-Free Savings Accounts Tax-Free Savings Accounts A new way to save Tax-free savings accounts were introduced by the federal government in the 2008 budget as an incentive for Canadians to

How Can You Reduce Your Taxes?

RON GRAHAM AND ASSOCIATES LTD. 10585 111 Street NW, Edmonton, Alberta, T5M 0L7 Telephone (780) 429-6775 Facsimile (780) 424-0004 Email rgraham@rgafinancial.com How Can You Reduce Your Taxes? Tax Brackets.

RON GRAHAM AND ASSOCIATES LTD. 10585 111 Street NW, Edmonton, Alberta, T5M 0L7 Telephone (780) 429-6775 Facsimile (780) 424-0004 Email rgraham@rgafinancial.com How Can You Reduce Your Taxes? Tax Brackets.

Public Pensions. Economics 325 Martin Farnham

Public Pensions Economics 325 Martin Farnham Why Pensions? Typically people work between the ages of about 20 and 65. Younger people depend on parents to support them Older people depend on accumulated

Public Pensions Economics 325 Martin Farnham Why Pensions? Typically people work between the ages of about 20 and 65. Younger people depend on parents to support them Older people depend on accumulated

Income Taxes module. After covering the topics in the module booklets or web pages and this workshop, learners will be able to:

Income Taxes module Trainer s Introduction Most people are aware that they must file an income tax return in Canada, if only to claim back any excess taxes that were withheld from their income. Filing

Income Taxes module Trainer s Introduction Most people are aware that they must file an income tax return in Canada, if only to claim back any excess taxes that were withheld from their income. Filing

THE EMERGING RETIREMENT CRISIS

THE EMERGING RETIREMENT CRISIS PART ONE Ontarians Rank Retirement Income Security as a Top Concern 1 // THE EMERGING RETIREMENT CRISIS: PART ONE Letter from Jim Keohane, HOOPP Dwindling pension coverage

THE EMERGING RETIREMENT CRISIS PART ONE Ontarians Rank Retirement Income Security as a Top Concern 1 // THE EMERGING RETIREMENT CRISIS: PART ONE Letter from Jim Keohane, HOOPP Dwindling pension coverage

ENHANCING THE. Canada Pension Plan. canadianlabour.ca

ENHANCING THE Canada Pension Plan canadianlabour.ca What are we asking for? We are asking the federal government to double the Canada Pension Plan (CPP) retirement benefit for Canadians so that it replaces

ENHANCING THE Canada Pension Plan canadianlabour.ca What are we asking for? We are asking the federal government to double the Canada Pension Plan (CPP) retirement benefit for Canadians so that it replaces

Salary vs. dividends for business owners

Salary vs. dividends for business owners One of the most recurring questions business owners ask is - should they take salary or dividend income from their business? Some accountants suggest a bonus-down

Salary vs. dividends for business owners One of the most recurring questions business owners ask is - should they take salary or dividend income from their business? Some accountants suggest a bonus-down

TAX-FREE SAVINGS ACCOUNTS (TFSAs) Investor Guide

Investor Guide") TAX-FREE SAVINGS ACCOUNTS (TFSAs) Investor Guide Introduction Since its introduction in 1957, the Registered Retirement Savings Plan (RRSP) has been one of the best tax shelters available. Aside from RRSPs,

TAX-FREE SAVINGS ACCOUNTS (TFSAs) Investor Guide Introduction Since its introduction in 1957, the Registered Retirement Savings Plan (RRSP) has been one of the best tax shelters available. Aside from RRSPs,

Ryerson Retirement Pension Plan Summary

Ryerson Retirement Pension Plan Summary ABOUT THIS DOCUMENT This summary document has been prepared to provide a convenient and understandable source of information about the Ryerson Retirement Pension

Ryerson Retirement Pension Plan Summary ABOUT THIS DOCUMENT This summary document has been prepared to provide a convenient and understandable source of information about the Ryerson Retirement Pension

TIME FOR ACTION. CPP Expansion: A critical part of the solution. Prepared by the Pensions Committee FEI Canada Policy Forum May 1, 2014

TIME FOR ACTION CPP Expansion: A critical part of the solution Prepared by the Pensions Committee FEI Canada Policy Forum May 1, 2014 Debate has intensified on how best to help Canadians plan for retirement

TIME FOR ACTION CPP Expansion: A critical part of the solution Prepared by the Pensions Committee FEI Canada Policy Forum May 1, 2014 Debate has intensified on how best to help Canadians plan for retirement

Introduction 1 Key Findings 1 Recommendations 1 The Survey 2. 1. Retirement landscape in Canada 3. 2. Retirement aspirations and expectations 3

Contents Introduction 1 Key Findings 1 Recommendations 1 The Survey 2 1. Retirement landscape in Canada 3 2. Retirement aspirations and expectations 3 3. Planning for retirement 5 4. Making it easy to

Contents Introduction 1 Key Findings 1 Recommendations 1 The Survey 2 1. Retirement landscape in Canada 3 2. Retirement aspirations and expectations 3 3. Planning for retirement 5 4. Making it easy to

TO HELP YOU MAKE THE MOST OF YOUR RETIREMENT DAYS

RETIREMENT GUIDE TO HELP YOU MAKE THE MOST OF YOUR RETIREMENT DAYS Whether it s a long-term project or a dream that s about to come true, you likely have no shortage of ideas to fill up this exciting period

RETIREMENT GUIDE TO HELP YOU MAKE THE MOST OF YOUR RETIREMENT DAYS Whether it s a long-term project or a dream that s about to come true, you likely have no shortage of ideas to fill up this exciting period

Preparing for Retirement. A Guide for Employees. Human Resources

Preparing for Retirement A Guide for Employees 010 Human Resources Contents Introduction... 3 Canada Pension Plan Retirement Benefits... 4 Old Age Security... 6 Employment Insurance Benefits at Retirement...

Preparing for Retirement A Guide for Employees 010 Human Resources Contents Introduction... 3 Canada Pension Plan Retirement Benefits... 4 Old Age Security... 6 Employment Insurance Benefits at Retirement...

group insurance plans for small business

group insurance plans for small business Presented by: Stephen Cragg Financial Security Advisor Group Broker table of contents About me Group broker services Additional services I provide Fifteen advantages

group insurance plans for small business Presented by: Stephen Cragg Financial Security Advisor Group Broker table of contents About me Group broker services Additional services I provide Fifteen advantages

Preparing for Your Retirement: An IRA Review

Preparing for Your Retirement: An IRA Review How much of your earning power will be available for your use when you retire? What will happen to your standard of living when your income ceases at retirement?

Preparing for Your Retirement: An IRA Review How much of your earning power will be available for your use when you retire? What will happen to your standard of living when your income ceases at retirement?

CIFPs 11 th Annual National Conference. Frank Di Pietro, CFA, CFP Director, Tax & Estate Planning. May 2013

Tax & Estate Planning for Business Owners CIFPs 11 th Annual National Conference Frank Di Pietro, CFA, CFP Director, Tax & Estate Planning May 2013 DISCLAIMER The information provided is general in nature

Tax & Estate Planning for Business Owners CIFPs 11 th Annual National Conference Frank Di Pietro, CFA, CFP Director, Tax & Estate Planning May 2013 DISCLAIMER The information provided is general in nature

How To Maximize Your Retirement Savings From The Western Retirement Plan

Retirement Plan Summary july 2013 » Table of Contents Welcome to Your Retirement Journey...3 Important Note...4 Your Plan at a Glance...5 Your Responsibilities...6 Joining the Plan...7 Regular Full-time

Retirement Plan Summary july 2013 » Table of Contents Welcome to Your Retirement Journey...3 Important Note...4 Your Plan at a Glance...5 Your Responsibilities...6 Joining the Plan...7 Regular Full-time

SUBMIT YOUR COMPLETED 2015-16 STUDENT FINANCIAL ASSISTANCE APPLICATION TO:

SUBMIT YOUR COMPLETED 2015-16 STUDENT FINANCIAL ASSISTANCE APPLICATION TO: Student Financial Services Department of Post-Secondary Education, Training and Labour PO Box 6000, 440 King St. Fredericton,

SUBMIT YOUR COMPLETED 2015-16 STUDENT FINANCIAL ASSISTANCE APPLICATION TO: Student Financial Services Department of Post-Secondary Education, Training and Labour PO Box 6000, 440 King St. Fredericton,

Group Savings & Retirement & Someday starts here. Plan for life. The basics of. retirement planning

Group Savings & Retirement & Someday starts here Plan for life The basics of retirement planning Hello. Are you close to retiring? If you re almost there, then understanding retirement planning basics

Group Savings & Retirement & Someday starts here Plan for life The basics of retirement planning Hello. Are you close to retiring? If you re almost there, then understanding retirement planning basics

THE TAX-FREE SAVINGS ACCOUNT

THE TAX-FREE SAVINGS ACCOUNT The 2008 federal budget introduced the Tax-Free Savings Account (TFSA) for individuals beginning in 2009. The TFSA allows you to set money aside without paying tax on the income

THE TAX-FREE SAVINGS ACCOUNT The 2008 federal budget introduced the Tax-Free Savings Account (TFSA) for individuals beginning in 2009. The TFSA allows you to set money aside without paying tax on the income

Table 8.1.1: Comparison of Education Expenditures with Other Government Sectors, 1991/92-1997/98

8. Cost of Education 8.1 How do educational expenditures compare with expenditures for other major government sectors? The total government expenditure for the year 1995/96, the last year for which actual

8. Cost of Education 8.1 How do educational expenditures compare with expenditures for other major government sectors? The total government expenditure for the year 1995/96, the last year for which actual

In Focus February 20, 2013

Economics Canadians Retirement Future: Mind the Gap by Benjamin Tal and Avery Shenfeld In Focus February 2, 213 April 17, 27 Avery Shenfeld (416) 94-736 avery.shenfeld@cibc.ca Benjamin Tal (416) 96-3698

Economics Canadians Retirement Future: Mind the Gap by Benjamin Tal and Avery Shenfeld In Focus February 2, 213 April 17, 27 Avery Shenfeld (416) 94-736 avery.shenfeld@cibc.ca Benjamin Tal (416) 96-3698

The Canadian Retirement Income Guide 2015/16 Edition

The Canadian Retirement Income Guide 2015/16 Edition Maximizing your retirement income while minimizing your taxes Table of Contents: Introduction Page 3 The Six Sources of Retirement Income Page 4 1)

The Canadian Retirement Income Guide 2015/16 Edition Maximizing your retirement income while minimizing your taxes Table of Contents: Introduction Page 3 The Six Sources of Retirement Income Page 4 1)

Life insurance. Shedding light on. a practical guide to helping you achieve a lifetime of financial security

Shedding light on Life insurance a practical guide to helping you achieve a lifetime of financial security Learn more about: Safeguarding your loved ones Protecting your future Ensuring your dreams live

Shedding light on Life insurance a practical guide to helping you achieve a lifetime of financial security Learn more about: Safeguarding your loved ones Protecting your future Ensuring your dreams live

Planning Retirement. Information for BCGEU Pension Plan Members

Planning Retirement Information for BCGEU Pension Plan Members January 2012 PAGE ONE PAGE TWO PAGE THREE PAGE FOUR PAGE FIVE PAGE SIX PAGE SEVEN PAGE EIGHT PAGE NINE PAGE TWELVE TABLE OF CONTENTS Preparing

Planning Retirement Information for BCGEU Pension Plan Members January 2012 PAGE ONE PAGE TWO PAGE THREE PAGE FOUR PAGE FIVE PAGE SIX PAGE SEVEN PAGE EIGHT PAGE NINE PAGE TWELVE TABLE OF CONTENTS Preparing

A guide to Government of Canada services for seniors and their families

A guide to Government of Canada services for seniors and their families Services for Seniors Guide About this guide Who should use this guide? You will find the information in this guide useful if you

A guide to Government of Canada services for seniors and their families Services for Seniors Guide About this guide Who should use this guide? You will find the information in this guide useful if you

KNOWING WHEN TO AUTOMATE AND UPGRADE YOUR PAYROLL PROCESSING

KNOWING WHEN TO AUTOMATE AND UPGRADE YOUR PAYROLL PROCESSING Executive Briefing KNOWING WHEN TO AUTOMATE AND UPGRADE YOUR PAYROLL PROCESSING Many business owners and managers believe automating payroll

KNOWING WHEN TO AUTOMATE AND UPGRADE YOUR PAYROLL PROCESSING Executive Briefing KNOWING WHEN TO AUTOMATE AND UPGRADE YOUR PAYROLL PROCESSING Many business owners and managers believe automating payroll

Retirement Planning Workshop

Retirement Planning Workshop Agenda What is Retirement Planning? Why Plan for Retirement? 5 Key Risks to secure income Goal Setting Retirement Income Considerations Asset Accumulation Considerations Tom

Retirement Planning Workshop Agenda What is Retirement Planning? Why Plan for Retirement? 5 Key Risks to secure income Goal Setting Retirement Income Considerations Asset Accumulation Considerations Tom

Submission to the House of Commons Standing Committee on Finance Pre-budget Consultations

Submission to the House of Commons Standing Committee on Finance Pre-budget Consultations August 2013 Text conforms to word limits established by the Standing Committee on Finance. 1410-130 Albert St.

Submission to the House of Commons Standing Committee on Finance Pre-budget Consultations August 2013 Text conforms to word limits established by the Standing Committee on Finance. 1410-130 Albert St.

Executive Summary... 1. I. Introduction... 5. II. Saving for our Collective Old Age... 7. III. Macroeconomics of Savings and Investments...

TABLE OF CONTENTS Executive Summary... 1 I. Introduction... 5 II. Saving for our Collective Old Age... 7 III. Macroeconomics of Savings and Investments... 10 IV. Individual Households Incentives to Save...

TABLE OF CONTENTS Executive Summary... 1 I. Introduction... 5 II. Saving for our Collective Old Age... 7 III. Macroeconomics of Savings and Investments... 10 IV. Individual Households Incentives to Save...

Retirement Planning Your Retirement Transition Plan

Retirement Planning Your Retirement Transition Plan Planning Your Retirement Picture Your Perfect Retirement What do you want your retirement to look like? The definition of retirement has changed. Today,

Retirement Planning Your Retirement Transition Plan Planning Your Retirement Picture Your Perfect Retirement What do you want your retirement to look like? The definition of retirement has changed. Today,

This article, prepared by PARO s auditors Rosenswig McRae Thorpe LLP, outlines some points to consider in preparing your income tax returns.

2014 Edition for 2013 Returns This article, prepared by PARO s auditors Rosenswig McRae Thorpe LLP, outlines some points to consider in preparing your income tax returns. Remember that: RRSP Contribution

2014 Edition for 2013 Returns This article, prepared by PARO s auditors Rosenswig McRae Thorpe LLP, outlines some points to consider in preparing your income tax returns. Remember that: RRSP Contribution

Registered Retirement Income Funds

Registered Retirement Income Funds Registered Retirement Income Funds Most Canadians are familiar with registered retirement savings plans (RSPs). Many spend decades accumulating wealth in these tax deferred

Registered Retirement Income Funds Registered Retirement Income Funds Most Canadians are familiar with registered retirement savings plans (RSPs). Many spend decades accumulating wealth in these tax deferred

Participant s Guide to Group RRSPs

Participant s Guide to Group RRSPs Table of Contents What Is a Group Registered Retirement Savings Plan (RRSP)?... 2 How Does It Work? How Do I Get Started? Investment Options... 3 Variable RRSP Guaranteed

Participant s Guide to Group RRSPs Table of Contents What Is a Group Registered Retirement Savings Plan (RRSP)?... 2 How Does It Work? How Do I Get Started? Investment Options... 3 Variable RRSP Guaranteed

BBA Accounting Executive Summary

BBA Accounting Executive Summary Program Overview Business education continues to experience high demand from graduates of domestic high schools, mature students, working students and international students.

BBA Accounting Executive Summary Program Overview Business education continues to experience high demand from graduates of domestic high schools, mature students, working students and international students.

Preparing for retirement

What s in this fact sheet? This fact sheet explains the basics of retirement planning. For more information, contact the Human Resources Service, Pension Sector: Telephone: (613) 562-5800 ext. 1747 E-mail:

What s in this fact sheet? This fact sheet explains the basics of retirement planning. For more information, contact the Human Resources Service, Pension Sector: Telephone: (613) 562-5800 ext. 1747 E-mail:

G20 Labour and Employment Ministers Declaration Moscow, 18-19 July 2013

G20 Labour and Employment Ministers Declaration Moscow, 18-19 July 2013 1. We, the Ministers of Labour and Employment from G20 countries met in Moscow on July 18-19, 2013 to discuss the global labour market

G20 Labour and Employment Ministers Declaration Moscow, 18-19 July 2013 1. We, the Ministers of Labour and Employment from G20 countries met in Moscow on July 18-19, 2013 to discuss the global labour market

COMPLETING A BC SUPREME COURT FINANCIAL STATEMENT: WHY? HOW? WHAT HAPPENS NEXT?

COMPLETING A BC SUPREME COURT FINANCIAL STATEMENT: WHY? HOW? WHAT HAPPENS NEXT? WHY? Are you wondering why your lawyer has asked you to complete a BC Supreme Court Financial Statement ( FS ) when you have

COMPLETING A BC SUPREME COURT FINANCIAL STATEMENT: WHY? HOW? WHAT HAPPENS NEXT? WHY? Are you wondering why your lawyer has asked you to complete a BC Supreme Court Financial Statement ( FS ) when you have

Planning for Retirement: Are Canadians Saving Enough?

June 2007 Planning for Retirement: Are Canadians Saving Enough? Document 207055 This study was carried out by the Department of Statistics and Actuarial Science at the University of Waterloo, under the

June 2007 Planning for Retirement: Are Canadians Saving Enough? Document 207055 This study was carried out by the Department of Statistics and Actuarial Science at the University of Waterloo, under the

Income Splitting CONTENTS

June 2012 CONTENTS The attribution rules Family income splitting Business income splitting Income splitting through corporations Income splitting in retirement Summary Income Splitting With Canada s high

June 2012 CONTENTS The attribution rules Family income splitting Business income splitting Income splitting through corporations Income splitting in retirement Summary Income Splitting With Canada s high

Office of the Chief Actuary

Office of the Superintendent of Financial Institutions Canada Office of the Chief Actuary Bureau du surintendant des institutions financières Canada Bureau de l actuaire en chef Office of the Chief Actuary

Office of the Superintendent of Financial Institutions Canada Office of the Chief Actuary Bureau du surintendant des institutions financières Canada Bureau de l actuaire en chef Office of the Chief Actuary

WORKING PAPER 5: HOW TO PROVIDE RETIREMENT BENEFITS *

WORKING PAPER 5: HOW TO PROVIDE RETIREMENT BENEFITS * 1. Key challenge & overview People in precarious employment are less likely to have access to benefits, including retirement benefits. Retirement income

WORKING PAPER 5: HOW TO PROVIDE RETIREMENT BENEFITS * 1. Key challenge & overview People in precarious employment are less likely to have access to benefits, including retirement benefits. Retirement income

FINANCIAL PLANNING. Helping You Sail Successfully into the Future. Share this e-book

FINANCIAL PLANNING Helping You Sail Successfully into the Future Share this e-book Section 1 Introduction 1 Contents Section 2 What a financial plan IS NOT 2 Section 3 What a financial plan IS................

FINANCIAL PLANNING Helping You Sail Successfully into the Future Share this e-book Section 1 Introduction 1 Contents Section 2 What a financial plan IS NOT 2 Section 3 What a financial plan IS................

4Needs your WHAT S AFTER? ELIMINATE DEBT THE FEWER DEBTS, THE BETTER! Wills and Trusts; Reviewing These Are a Must

YOUR SOURCE FOR RETIREMENT PLANNING AND POSSIBILITIES e > N xt WHAT S AFTER? But first, some things to think about before 4Needs your retirement income should meet ELIMINATE DEBT THE FEWER DEBTS, THE BETTER!

YOUR SOURCE FOR RETIREMENT PLANNING AND POSSIBILITIES e > N xt WHAT S AFTER? But first, some things to think about before 4Needs your retirement income should meet ELIMINATE DEBT THE FEWER DEBTS, THE BETTER!

Tax Planning Opportunities Involving Professional Corporations

Tax Planning Opportunities Involving Professional Corporations A Discussion Paper Prepared by: Alan Koop, CA Prepared for: The Saskatchewan Provincial Court Judges Association Table of Contents Executive

Tax Planning Opportunities Involving Professional Corporations A Discussion Paper Prepared by: Alan Koop, CA Prepared for: The Saskatchewan Provincial Court Judges Association Table of Contents Executive

It's 2016 Do You Know What Your Tax Rate Is?

It's 2016 Do You Know What Your Tax Rate Is? Jamie Golombek Managing Director, Tax & Estate Planning, CIBC Wealth Strategies Group April 2016 There s been much discussion about tax rates this year, with

It's 2016 Do You Know What Your Tax Rate Is? Jamie Golombek Managing Director, Tax & Estate Planning, CIBC Wealth Strategies Group April 2016 There s been much discussion about tax rates this year, with

Federal Budget 2015: Highlights for Atlantic Canada

Federal Budget 2015: Highlights for Atlantic Canada The federal government is projecting a balanced budget in 2015/2016 with a notional surplus of $1.4 billion. However, this has been achieved by reducing

Federal Budget 2015: Highlights for Atlantic Canada The federal government is projecting a balanced budget in 2015/2016 with a notional surplus of $1.4 billion. However, this has been achieved by reducing

Introduction to Payroll. Employer, Payer, or Trustee

Introduction to Payroll The Canadian payroll system is a rather complex process, requiring employers to make proper distinctions between workers, collecting deductions from their income, remitting those

Introduction to Payroll The Canadian payroll system is a rather complex process, requiring employers to make proper distinctions between workers, collecting deductions from their income, remitting those

First-Time Buyer Guide

First-Time Buyer Guide Jake Abramowicz Mortgage Edge Cell 416 910 4448 Fax 1 888 819 4816 MBL 10680 FSCO M08003274 Getting Started Interested in purchasing a property? Your first step is determining if

First-Time Buyer Guide Jake Abramowicz Mortgage Edge Cell 416 910 4448 Fax 1 888 819 4816 MBL 10680 FSCO M08003274 Getting Started Interested in purchasing a property? Your first step is determining if

Are you a first-home buyer? BENEFIT FROM THE HBP WHILE STAYING ON COURSE FOR RETIREMENT!

Are you a first-home buyer? BENEFIT FROM THE HBP WHILE STAYING ON COURSE FOR RETIREMENT! Research and Drafting Julien Michaud (Autorité des marchés financiers) Contributors Vincent Ardouin (Cégep Marie-Victorin)

Are you a first-home buyer? BENEFIT FROM THE HBP WHILE STAYING ON COURSE FOR RETIREMENT! Research and Drafting Julien Michaud (Autorité des marchés financiers) Contributors Vincent Ardouin (Cégep Marie-Victorin)

Ontario Retirement Pension Plan Key Design Questions

Ontario Retirement Pension Plan Key Design Questions Submission to the Associate Minister of Finance Prepared by Canadian Bankers Association February 13, 2015 1 EXPERTISE CANADA BANKS ON LA RÉFÉRENCE

Ontario Retirement Pension Plan Key Design Questions Submission to the Associate Minister of Finance Prepared by Canadian Bankers Association February 13, 2015 1 EXPERTISE CANADA BANKS ON LA RÉFÉRENCE

Improving Retirement Income Coverage in Canada The ACPM Five-Point Plan

Improving Retirement Income Coverage in Canada Month 00, 2012 ACPM CONTACT INFORMATION Mr. Bryan Hocking Chief Executive Officer Association of Canadian Pension Management 1255 Bay Street, Suite 304 Toronto

Improving Retirement Income Coverage in Canada Month 00, 2012 ACPM CONTACT INFORMATION Mr. Bryan Hocking Chief Executive Officer Association of Canadian Pension Management 1255 Bay Street, Suite 304 Toronto

Election 2015: How proposed tax measures could affect you and your business

Election 2015: How proposed tax measures could affect you and your business October 2015 As the federal election draws closer, the political parties are promoting their platforms which encompass a wide

Election 2015: How proposed tax measures could affect you and your business October 2015 As the federal election draws closer, the political parties are promoting their platforms which encompass a wide

PLANNING MATTERS. New Tax Measures for Families Introduced. Quarterly Financial Planning Newsletter from Coleman Wealth

PLANNING MATTERS Quarterly Financial Planning Newsletter from Coleman Wealth Fall 2014-1 st Edition Welcome to Planning Matters, the Coleman Wealth Financial Planning Newsletter! We developed our new financial

PLANNING MATTERS Quarterly Financial Planning Newsletter from Coleman Wealth Fall 2014-1 st Edition Welcome to Planning Matters, the Coleman Wealth Financial Planning Newsletter! We developed our new financial

(*This release is based on an article published in Tax Notes, May 2004, CCH Canadian Limited)

") Estate Planning in the 21st Century - Life Insurance: Exploring the Corporate Edge - Part I* By David Louis, J.D., C.A., Tax Partner, Minden Gross and Michael Goldberg, Associate, Minden Gross (*This release

Estate Planning in the 21st Century - Life Insurance: Exploring the Corporate Edge - Part I* By David Louis, J.D., C.A., Tax Partner, Minden Gross and Michael Goldberg, Associate, Minden Gross (*This release

The 2004 Report of the Social Security Trustees: Social Security Shortfalls, Social Security Reform and Higher Education

POLICY BRIEF Visit us at: www.tiaa-crefinstitute.org. September 2004 The 2004 Report of the Social Security Trustees: Social Security Shortfalls, Social Security Reform and Higher Education The 2004 Social

POLICY BRIEF Visit us at: www.tiaa-crefinstitute.org. September 2004 The 2004 Report of the Social Security Trustees: Social Security Shortfalls, Social Security Reform and Higher Education The 2004 Social

A lifetime approach to retirement planning

Financial Planning Update A lifetime approach to retirement planning Unlike earlier generations, individuals planning to retire over the next two decades face a new set of challenges, including an uncertain

Financial Planning Update A lifetime approach to retirement planning Unlike earlier generations, individuals planning to retire over the next two decades face a new set of challenges, including an uncertain

an economic impact and future growth study of Ontario s high-value insurance sector

an economic impact and future growth study of Ontario s high-value insurance sector over 300 firms firms with less than 10% employment growth projected over next 3 years firms with more than 10% employment

an economic impact and future growth study of Ontario s high-value insurance sector over 300 firms firms with less than 10% employment growth projected over next 3 years firms with more than 10% employment

Volume URL: http://www.nber.org/books/feld87-2. Chapter Title: Individual Retirement Accounts and Saving

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Taxes and Capital Formation Volume Author/Editor: Martin Feldstein, ed. Volume Publisher:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Taxes and Capital Formation Volume Author/Editor: Martin Feldstein, ed. Volume Publisher:

Strengthening the Canada Pension Plan: Take it to the public

Strengthening the Canada Pension Plan: Take it to the public by Ken Battle, Sherri Torjman and Michael Mendelson November 2013 Strengthening the Canada Pension Plan: Take it to the public by Ken Battle,

Strengthening the Canada Pension Plan: Take it to the public by Ken Battle, Sherri Torjman and Michael Mendelson November 2013 Strengthening the Canada Pension Plan: Take it to the public by Ken Battle,

Understanding RSPs. Your Guide to Retirement Savings Plans

Understanding RSPs Your Guide to Retirement Savings Plans Getting Started Some retirement basics Getting Ahead Setting your retirement savings goals Getting the Most Maximizing your RSP growth Getting

Understanding RSPs Your Guide to Retirement Savings Plans Getting Started Some retirement basics Getting Ahead Setting your retirement savings goals Getting the Most Maximizing your RSP growth Getting

Investor Guide. RRIF Investing. Managing your money in retirement

Investor Guide RRIF Investing Managing your money in retirement 1 What s inside It s almost time to roll over your RRSP...3 RRIFs...4 Frequently asked questions...5 Manage your RRIF...8 Your advisor...10

Investor Guide RRIF Investing Managing your money in retirement 1 What s inside It s almost time to roll over your RRSP...3 RRIFs...4 Frequently asked questions...5 Manage your RRIF...8 Your advisor...10

THE CANADIAN CLUB OF MONTREAL REMARKS FOR DONALD A. GULOIEN PRESIDENT AND CHIEF EXECUTIVE OFFICER MONDAY, OCTOBER 6, 2014 MONTREAL

As Delivered THE CANADIAN CLUB OF MONTREAL REMARKS FOR DONALD A. GULOIEN PRESIDENT AND CHIEF EXECUTIVE OFFICER MONDAY, OCTOBER 6, 2014 MONTREAL 1 (Italicized text is spoken in French) Retirement Income

As Delivered THE CANADIAN CLUB OF MONTREAL REMARKS FOR DONALD A. GULOIEN PRESIDENT AND CHIEF EXECUTIVE OFFICER MONDAY, OCTOBER 6, 2014 MONTREAL 1 (Italicized text is spoken in French) Retirement Income

When to retire: Age matters!

When to retire: Age matters! The BMO Institute provides insights and strategies around wealth planning and financial decisions to better prepare you for a confident financial future. Contact the BMO Institute

When to retire: Age matters! The BMO Institute provides insights and strategies around wealth planning and financial decisions to better prepare you for a confident financial future. Contact the BMO Institute

Creating a Fairer Pension System in Canada: Ideas to Make Canada's Federal Government Employee Pension System Fair for Taxpayers and Employees

Pension Policy Creating a Fairer Pension System in Canada: Ideas to Make Canada's Federal Government Employee Pension System Fair for Taxpayers and Employees By William (Bill) Tufts and Lee Fairbanks KEY

Pension Policy Creating a Fairer Pension System in Canada: Ideas to Make Canada's Federal Government Employee Pension System Fair for Taxpayers and Employees By William (Bill) Tufts and Lee Fairbanks KEY