ALM Seminar June 12-13, ALM Attribution Analysis. Moderator Robert Reitano

|

|

|

- Gerard Clark

- 10 years ago

- Views:

Transcription

1 ALM Seminar June 12-13, 2008 ALM Attribution Analysis Jonathan Hede Gary Hatfield Moderator Robert Reitano

2 ALM Seminar ALM Attribution Analysis Jonathan Hede, FSA, FCIA, MAAA, CFA June 12-13, 2008

3 Agenda 1) Traditional Attribution Analysis 2) ALM Attribution Analysis 3) Numerical Example 2

Numerical")

4 Traditional approach Asset performance measured against typical benchmark(s) Attribution performed only against benchmark Active asset management decisions not explicitly measured No separation of sources of value-added from ALM, passive position, active bets Capital and risk-adjusted performance cannot be properly factored in 3

5 Traditional approach major impediment to transparency Traditional measurement against benchmark cannot separate the value added by your ALM strategy from the value added or destroyed by active asset management Active asset management bets not explicitly disclosed ex ante nor measured ex post Unintended, implicit bets not recognized Result may reward a poorly matched position E.g. interest t rate exposure not from a deliberate view on rates 4

6 Traditional attribution analysis not transparent Benchmark may be inappropriate p benchmark and or targets frequently oversimplified for benefit of asset manager Entire process may cater more to needs of asset manager, not client asset manager requires specification of investment objectives, not financial objectives asset manager requires benchmark and targets that may bear little resemblance to actual liabilities value-added ALM strategies may disrupt performance measurement of asset manager Traditional asset management divorces assets from liabilities for benefit of asset manager 5

7 There is a better way Replace traditional benchmarks with actual liabilities Replace focus on narrow investment objectives with focus on overall financial objectives Change process so that ALM drives investment decisions ALM attribution analysis 6

8 ALM attribution analysis Identify value from both ALM and active management ALM strategies (excluding tactical credit views, security selection, rate anticipation, etc) Active asset management can adds value on top of ALM optimized portfolio Any bets (i.e., active positions) are recorded ex ante and measured ex post thus fully transparent Measure actual value added from active management, not just value against a benchmark Attribution not restricted to a particular measurement basis could be change in ES, accounting results or other financial objective(s) Impact of passive position / prior period decisions / noise 7

are recorded ex ante and measured ex post thus fully")

9 Assets managed separately under traditional approach Liabilities Vary with Interest rates Policyholder behavior Embedded options Mortality otatyand lapse Benchmark Asset-only Target duration Liability-Driven Replicating portfolio Min. Risk Portfolio Assets Managed against simplified proxy Assets divorced from liabilities Investment objectives must be specified Actual Interest Rate Risk Managed Risk 8

10 Shortfalls of traditional approach can be overcome Liabilities Assets Vary with Interest rates Policyholder behavior Embedded options Mortality and lapse Managed directly against liabilities Focus on overall financial objectives Assets and liabilities inextricably linked Actual Risk is Managed 9

11 Executing Asset Management within an ALM framework Asset Manager ALM / Investment Reporting Risk-Optimized Portfolio Financial Objectives Liability Cash Flows Client Credit Selection / Rate Anticipation Asset Universe Risk-optimized portfolio ALM / Portfolio Optimization ALM Manager 10

12 Numerical Example ALM attribution analysis Quantify impact / value added from ALM strategies Quantify impact / value added from active asset management Limitations of simple risk metrics Can be poor predictors of actual risk if limitations not understood or naively applied can lead to unexpected results Need for comprehensive, coherent approach 11

13 Attribution analysis decomposing sources of value added Gov t Yield Curve Mo 1Y 5Y 10Y 30Y 31-Dec Sep-07 Economic Surplus BOP 111,673 Change due to Yield Curve 2,292 Change due to Liabilities (19,982) Change due to Assets 26,718 Total Change 9,028 Economic Surplus EOP 120,701 Impact of ALM Strategies Change in ES Before Rebalance (5,045) Change in ES After Rebalance 9,028 Total 14,073 Impact of Active Asset Management Change in ES due to rate anticipation 1,213 Change in ES due to credit selection (750) Total

14 Avoid reliance on simple risk measures Change due to Yield Curve 2,292 Change predicted by Duration (190) Contribution predicted by Convexity (205) Change predicted by -D( i)+.5c ( i) 2 (395) Change predicted by Effective Duration (1,700) Change predicted by Effective Convexity (1,026) Change predicted by -D( i)+.5c ( i) 2 (2,726) Change predicted by Partial Duration 2,606 Change due to Liabilities (19,982) New Business (12,413) Change due to aging of cash flows (7,569) Change due to assumptions changes - Change due to Assets 26,718 New Business 14,399 Asset trades 2,244 Change due to aging of cash flows 10,075 Change due to assumptions changes - 13

15 Recap Traditional Approach No separation of sources of value-added from ALM, passive position, active bets ALM Attribution Replace focus on narrow investment objectives with focus on overall financial objectives Numerical results Decompose sources of value added, linkage to overall financial objectives Don t rely on over-simplified risk metrics 14

16 ALM Attribution Analysis ALM Seminar Toronto, June 2008 Gary Hatfield

17 Agenda Securian s approach for understanding sources of value Why do attribution? Attribution Issues/questions Summary

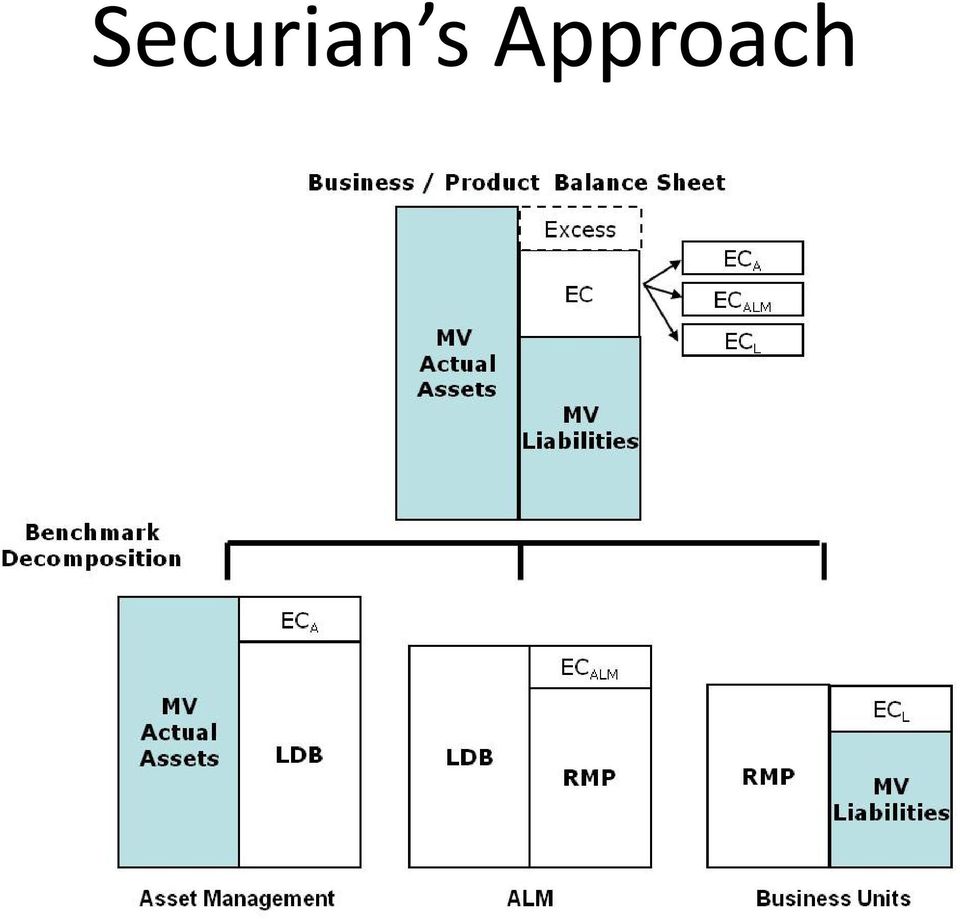

18 Securian s Approach

19 Securian s Approach Starts with liabilities Perform market consistent valuation of all liabilities Modeled in Prophet Uses risk ikneutral interest rate and equity scenarios Obtain key rate durations (up and down) and equity delta of each business unit (vegas and equity gamma to be considered later)

20 Securian s Approach For each business unit, construct a portfolio of risk free assets to offset liability Greeks. Asset palette consists of zero coupon bonds, swaptions, equity future and put options. Portfolios are referred to as Risk Minimizing Portfolios (RMPs). Functions as assets of business units balance sheets for the purpose of understanding economic value creation

.")

21 Securian s Approach RMP s in aggregate serve as the liability of the ALM Group Purpose is to Increase transparency of ALM choices Better understand dhow value is created over time via ALM

22 Securian s Approach Liability Driven Benchmark is the asset of the ALM Group s balance sheet Benchmark consists of investable, well known indices (e.g. Lehman intermediate credit A, Lehman CMBS,etc) Benchmark chosen through process resembling mean variance optimization Each asset class has an expected tdreturn above the risk ikfree rate For every given combination of benchmark assets, the mismatchfrom the liabilitydetermines a risk measure Goal is maximize the return relative to the risk measure(s) Subjective, iterative process

23 Why do attribution? Understand where value was created or destroyed Understand primary drivers of economic profit Helps to assess whether ALM choices are paying off Assess value add of asset management function

24 Attribution RMP constructed consists of zero coupon bonds, swaptions, equity forwards and put options LDB selected to be combination of various investible indices Both modeled in appropriate software (E.G. Factset/Derivatives Solution, Lehman Point, Blackrock Aladdin, etc.) Evaluation period from T= 0 to T = 1

25 Attribution ALM return = LDB RMP Asset Manager s Return = Actual Assets LDB Key is to understand the components of the changes (returns)

26 Components of change Carry changes Yield Curve Changes Volatility changes Spread changes Equity market Changes Cash flows

27 Carry interest est (coupons + accrual) Can be approximated by Yield * t Roll down Captures gain due to upward sloping yield curve not flattening Calculate l by valuing securities at time 1 using time 0 yield curve

28 Yield Curve Changes Shift e.g. ¼ ( Y2+ 5+ Y10+ 30) applied across curve Twist e.g. (Y30 Y1) applied with pivot point Butterfly (sometimes not bothered with) Shape (residual)

29 Volatility Changes Revalue with new set of swaption implied volatilities Might do equity implied here as well, but as separate impact

30 Spread Changes Captures the impact of changes in credit worthiness Captures changes in credit risk premia Also captures changes in risk premia for liquidity idi and convexity

31 Equity Markets Captures equity exposure inherent in liabilities and which is not hedged Need to adjust if hedging programs are in place for GMWB s etc.

32 Cash Flows For comparison of LDB to RMP, not really an issue For comparison of Actual Assets to LDB a very important consideration. Commonly accepted approach is Modified d Dietz: MV (1) MV (0) CFj Rmd = MV (0) + ( W j CFj ) j Where the W s represent the proportion of measuring period days that were after the particular cash flow. j

33 ALM performance Based on the relative performance of LDB versus RMP, an assessment of how the strategic ALM bets of thefirm paid off. Example (returns in bps): Int. Roll Shift Twist Shape Vol. Spread Equity Total LDB (100) (15) 30 (5) (25) 0 45 RMP (3) (5) 12 0 (50) 109 ALM net 50 5 (50) (12) 35 (17) (25) 50 (64)

34 Asset Management Return First look at the yield curve and volatility pieces described above (roll, shift, twist, shape, vol). These show how that yield curve and volatility positioning i of the assets relative to the LDB paid off. But also want more detail on how asset manager performed at what asset managers are supposed to be good at (not generally betting the yield curve) Want to look at: Sector Selection Security Selection

35 Sector Selection This measure the outperformance due to the asset manager s decisions to deviate from the chosen benchmark After pulling out the returns due to market risks, we are left with interest and spread returns.

36 Sector Selection Sector Selection = (W_act(i) W_LDB(i))(interest (i) + Spread(i)) where Wact(i) W_act(i) = the proportion of the actual portfolio invested in sector i W_LDB(i) = the proportion of the LDB invested in benchmark sector i Interest(i) = interest return from sector i Spread(i) = spread return from sector i

37 Security Selection There are other approaches, but one can simply take security selection return to be what s not explained by all theotherreturns returns

38 Issues/Questions How often to change Benchmark? If LDB = RMP is not reasonable, should ALM Committee get full credit for the difference? Is there some minimum level of credit risk that an insurer must take because it is central to the business model? Framework is total return oriented. But there are other considerations: Yield requirements Realized gains/loss limits Liquidity etc

39 Issue/Questions What risk measure(s) to use for setting LDB? EC 1 in 10 year risk measure Variance How to measure the credit risk ikassociated itd with the LDB choice? Need to make sure that metrics used for attribution align with investment mandate

40 Issues/Questions How best to deal with asset classed for which public benchmarks are not available? Private placements Commercial Whole loans Etc

41 Summary Decomposition of insurance balance sheet into underwriting, ALM and asset management balance sheets allows for clearer transparency as to where value is created and what kinds of bets are being made This also allows for a performance attribution that separates the ALM return due to the strategic choices of the firm from the tactical positioning of the asset manager Furthermore, it allows for explicit benchmarking of the asset manager s performance.

Asset Liability Management

December 4, 2008 Asset Liability Management performance metrics and risk attribution Charles Gilbert, FSA, FCIA, CFA, CERA Asset Liability Management Performance metrics and risk attribution Review of

December 4, 2008 Asset Liability Management performance metrics and risk attribution Charles Gilbert, FSA, FCIA, CFA, CERA Asset Liability Management Performance metrics and risk attribution Review of

ASSET MANAGEMENT ALM FRAMEWORK

ASSET MANAGEMENT within an ALM FRAMEWORK LE MÉRIDIEN SINGAPORE SEPTEMBER 6 7, 2007 Charles L. Gilbert, FSA, FCIA, CFA Traditional Asset Management Focus on asset returns Assets managed against benchmark

ASSET MANAGEMENT within an ALM FRAMEWORK LE MÉRIDIEN SINGAPORE SEPTEMBER 6 7, 2007 Charles L. Gilbert, FSA, FCIA, CFA Traditional Asset Management Focus on asset returns Assets managed against benchmark

Asset Liability Management Risk Optimization Of Insurance Portfolios

Asset Liability Management Risk Optimization Of Insurance Portfolios Charles L. Gilbert, FSA, FCIA, CFA, CERA Victor S.F. Wong, FSA, FCIA, CFA, CRM Many insurance company and pension portfolios are risk

Asset Liability Management Risk Optimization Of Insurance Portfolios Charles L. Gilbert, FSA, FCIA, CFA, CERA Victor S.F. Wong, FSA, FCIA, CFA, CRM Many insurance company and pension portfolios are risk

A Flexible Benchmark Relative Method of Attributing Returns for Fixed Income Portfolios

White Paper A Flexible Benchmark Relative Method of Attributing s for Fixed Income Portfolios By Stanley J. Kwasniewski, CFA Copyright 2013 FactSet Research Systems Inc. All rights reserved. A Flexible

White Paper A Flexible Benchmark Relative Method of Attributing s for Fixed Income Portfolios By Stanley J. Kwasniewski, CFA Copyright 2013 FactSet Research Systems Inc. All rights reserved. A Flexible

Autumn Investor Seminar. Workshops. Managing Variable Annuity Risk

Autumn Investor Seminar Workshops Managing Variable Annuity Risk Jean-Christophe Menioux Kevin Byrne Denis Duverne Group CRO CIO AXA Equitable Chief Financial Officer Paris November 25, 2008 Cautionary

Autumn Investor Seminar Workshops Managing Variable Annuity Risk Jean-Christophe Menioux Kevin Byrne Denis Duverne Group CRO CIO AXA Equitable Chief Financial Officer Paris November 25, 2008 Cautionary

Rethinking Fixed Income

Rethinking Fixed Income Challenging Conventional Wisdom May 2013 Risk. Reinsurance. Human Resources. Rethinking Fixed Income: Challenging Conventional Wisdom With US Treasury interest rates at, or near,

Rethinking Fixed Income Challenging Conventional Wisdom May 2013 Risk. Reinsurance. Human Resources. Rethinking Fixed Income: Challenging Conventional Wisdom With US Treasury interest rates at, or near,

Hedging at Your Insurance Company

Hedging at Your Insurance Company SEAC Spring 2007 Meeting Winter Liu, FSA, MAAA, CFA June 2007 2006 Towers Perrin Primary Benefits and Motives of Establishing Hedging Programs Hedging can mitigate some

Hedging at Your Insurance Company SEAC Spring 2007 Meeting Winter Liu, FSA, MAAA, CFA June 2007 2006 Towers Perrin Primary Benefits and Motives of Establishing Hedging Programs Hedging can mitigate some

LDI Fundamentals: Is Our Strategy Working? A survey of pension risk management metrics

LDI Fundamentals: Is Our Strategy Working? A survey of pension risk management metrics Pension plan sponsors have increasingly been considering liability-driven investment (LDI) strategies as an approach

LDI Fundamentals: Is Our Strategy Working? A survey of pension risk management metrics Pension plan sponsors have increasingly been considering liability-driven investment (LDI) strategies as an approach

Designing The Ideal Investment Policy Presented To The Actuaries Club of the Southwest & the Southeastern Actuarial Conference

Designing The Ideal Investment Policy Presented To The Actuaries Club of the Southwest & the Southeastern Actuarial Conference Presented by: Greg Curran, CFA & Michael Kelch, CFA AAM - Insurance Investment

Designing The Ideal Investment Policy Presented To The Actuaries Club of the Southwest & the Southeastern Actuarial Conference Presented by: Greg Curran, CFA & Michael Kelch, CFA AAM - Insurance Investment

A Flexible Benchmark-Relative Method of Attributing Returns for Balanced Portfolios

White Paper A Flexible Benchmark-Relative Method of Attributing Returns for Balanced Portfolios By Stanley J. Kwasniewski, CFA Copyright 2016 FactSet Research Systems Inc. All rights reserved. www.factset.com

White Paper A Flexible Benchmark-Relative Method of Attributing Returns for Balanced Portfolios By Stanley J. Kwasniewski, CFA Copyright 2016 FactSet Research Systems Inc. All rights reserved. www.factset.com

AXA s approach to Asset Liability Management. HELVEA Insurance Capital Adequacy and Solvency Day April 28th, 2005

AXA s approach to Asset Liability Management HELVEA Insurance Capital Adequacy and Solvency Day April 28th, 2005 ALM in AXA has always been based on a long-term view Even though Solvency II framework is

AXA s approach to Asset Liability Management HELVEA Insurance Capital Adequacy and Solvency Day April 28th, 2005 ALM in AXA has always been based on a long-term view Even though Solvency II framework is

VIX for Variable Annuities

White Paper VIX for Variable Annuities A study considering the advantages of tying a Variable Annuity fee to VIX March 2013 VIX for Variable Annuities A study considering the advantages of tying a Variable

White Paper VIX for Variable Annuities A study considering the advantages of tying a Variable Annuity fee to VIX March 2013 VIX for Variable Annuities A study considering the advantages of tying a Variable

SOA Annual Symposium Shanghai. November 5-6, 2012. Shanghai, China. Session 2a: Capital Market Drives Investment Strategy.

SOA Annual Symposium Shanghai November 5-6, 2012 Shanghai, China Session 2a: Capital Market Drives Investment Strategy Genghui Wu Capital Market Drives Investment Strategy Genghui Wu FSA, CFA, FRM, MAAA

SOA Annual Symposium Shanghai November 5-6, 2012 Shanghai, China Session 2a: Capital Market Drives Investment Strategy Genghui Wu Capital Market Drives Investment Strategy Genghui Wu FSA, CFA, FRM, MAAA

Disclosure of European Embedded Value as of March 31, 2015

UNOFFICIAL TRANSLATION Although the Company pays close attention to provide English translation of the information disclosed in Japanese, the Japanese original prevails over its English translation in

UNOFFICIAL TRANSLATION Although the Company pays close attention to provide English translation of the information disclosed in Japanese, the Japanese original prevails over its English translation in

IASB/FASB Meeting Week beginning 11 April 2011. Top down approaches to discount rates

IASB/FASB Meeting Week beginning 11 April 2011 IASB Agenda reference 5A FASB Agenda Staff Paper reference 63A Contacts Matthias Zeitler [email protected] +44 (0)20 7246 6453 Shayne Kuhaneck [email protected]

IASB/FASB Meeting Week beginning 11 April 2011 IASB Agenda reference 5A FASB Agenda Staff Paper reference 63A Contacts Matthias Zeitler [email protected] +44 (0)20 7246 6453 Shayne Kuhaneck [email protected]

FINANCIAL REPORTING FOR LIFE INSURANCE BUSINESS. V Rajagopalan R Kannan K S Gopalakrishnan

FINANCIAL REPORTING FOR LIFE INSURANCE BUSINESS V Rajagopalan R Kannan K S Gopalakrishnan 6th Global Conference of Actuaries; February 2004 PRESENTATION LAYOUT Fair value reporting Recent developments

FINANCIAL REPORTING FOR LIFE INSURANCE BUSINESS V Rajagopalan R Kannan K S Gopalakrishnan 6th Global Conference of Actuaries; February 2004 PRESENTATION LAYOUT Fair value reporting Recent developments

Portfolio Replication Variable Annuity Case Study. Curt Burmeister Senior Director Algorithmics

Portfolio Replication Variable Annuity Case Study Curt Burmeister Senior Director Algorithmics What is Portfolio Replication? To find a portfolio of assets whose value is equal to the value of a liability

Portfolio Replication Variable Annuity Case Study Curt Burmeister Senior Director Algorithmics What is Portfolio Replication? To find a portfolio of assets whose value is equal to the value of a liability

Canadian Life Insurance Company Asset/Liability Management Summary Report as at: 31-Jan-08 interest rates as of: 29-Feb-08 Run: 2-Apr-08 20:07 Book

Canadian Life Insurance Company Asset/Liability Management Summary Report as at: 31Jan08 interest rates as of: 29Feb08 Run: 2Apr08 20:07 Book Book Present Modified Effective Projected change in net present

Canadian Life Insurance Company Asset/Liability Management Summary Report as at: 31Jan08 interest rates as of: 29Feb08 Run: 2Apr08 20:07 Book Book Present Modified Effective Projected change in net present

Liability-Driven Investment Policy: Structuring the Hedging Portfolio

Strategic Research November 2007 Liability-Driven Investment Policy: Structuring the Hedging Portfolio KURT WINKELMANN Managing Director and Head Global Investment Strategies [email protected] (212)

Strategic Research November 2007 Liability-Driven Investment Policy: Structuring the Hedging Portfolio KURT WINKELMANN Managing Director and Head Global Investment Strategies [email protected] (212)

Practical Issues Relating to Setting Up a Hedging Program

Joint Regional Seminar 2007 Practical Issues Relating to Setting Up a Hedging Program Leong Chew, FSA, MAAA [email protected] +1-312-499-5667 1 Overview Hedging implementation: obstacles & challenges

Joint Regional Seminar 2007 Practical Issues Relating to Setting Up a Hedging Program Leong Chew, FSA, MAAA [email protected] +1-312-499-5667 1 Overview Hedging implementation: obstacles & challenges

Fixed Income Portfolio Management. Interest rate sensitivity, duration, and convexity

Fixed Income ortfolio Management Interest rate sensitivity, duration, and convexity assive bond portfolio management Active bond portfolio management Interest rate swaps 1 Interest rate sensitivity, duration,

Fixed Income ortfolio Management Interest rate sensitivity, duration, and convexity assive bond portfolio management Active bond portfolio management Interest rate swaps 1 Interest rate sensitivity, duration,

ING Insurance Economic Capital Framework

ING Insurance Economic Capital Framework Thomas C. Wilson Chief Insurance Risk Officer Kent University, September 5, 2007 www.ing.com Objectives of this session ING has been using economic capital internally

ING Insurance Economic Capital Framework Thomas C. Wilson Chief Insurance Risk Officer Kent University, September 5, 2007 www.ing.com Objectives of this session ING has been using economic capital internally

Market Value of Insurance Contracts with Profit Sharing 1

Market Value of Insurance Contracts with Profit Sharing 1 Pieter Bouwknegt Nationale-Nederlanden Actuarial Dept PO Box 796 3000 AT Rotterdam The Netherlands Tel: (31)10-513 1326 Fax: (31)10-513 0120 E-mail:

Market Value of Insurance Contracts with Profit Sharing 1 Pieter Bouwknegt Nationale-Nederlanden Actuarial Dept PO Box 796 3000 AT Rotterdam The Netherlands Tel: (31)10-513 1326 Fax: (31)10-513 0120 E-mail:

Featured article: Evaluating the Cost of Longevity in Variable Annuity Living Benefits

Featured article: Evaluating the Cost of Longevity in Variable Annuity Living Benefits By Stuart Silverman and Dan Theodore This is a follow-up to a previous article Considering the Cost of Longevity Volatility

Featured article: Evaluating the Cost of Longevity in Variable Annuity Living Benefits By Stuart Silverman and Dan Theodore This is a follow-up to a previous article Considering the Cost of Longevity Volatility

Fixed Income Arbitrage

Risk & Return Fixed Income Arbitrage: Nickels in Front of a Steamroller by Jefferson Duarte Francis A. Longstaff Fan Yu Fixed Income Arbitrage Broad set of market-neutral strategies intended to exploit

Risk & Return Fixed Income Arbitrage: Nickels in Front of a Steamroller by Jefferson Duarte Francis A. Longstaff Fan Yu Fixed Income Arbitrage Broad set of market-neutral strategies intended to exploit

ALM Stress Testing: Gaining Insight on Modeled Outcomes

ALM Stress Testing: Gaining Insight on Modeled Outcomes 2013 Financial Conference Ballantyne Resort Charlotte, NC September 18, 2013 Thomas E. Bowers, CFA Vice President Client Services ZM Financial Systems

ALM Stress Testing: Gaining Insight on Modeled Outcomes 2013 Financial Conference Ballantyne Resort Charlotte, NC September 18, 2013 Thomas E. Bowers, CFA Vice President Client Services ZM Financial Systems

VIX for Variable Annuities - Part II

White Paper VIX for Variable Annuities - Part II A study considering the advantages of tying a Variable Annuity fee to VIX July 2013 VIX for Variable Annuities - Part II 2 Executive Summary This paper

White Paper VIX for Variable Annuities - Part II A study considering the advantages of tying a Variable Annuity fee to VIX July 2013 VIX for Variable Annuities - Part II 2 Executive Summary This paper

IAA PAPER VALUATION OF RISK ADJUSTED CASH FLOWS AND THE SETTING OF DISCOUNT RATES THEORY AND PRACTICE

Introduction This document refers to sub-issue 11G of the IASC Insurance Issues paper and proposes a method to value risk-adjusted cash flows (refer to the IAA paper INSURANCE LIABILITIES - VALUATION &

Introduction This document refers to sub-issue 11G of the IASC Insurance Issues paper and proposes a method to value risk-adjusted cash flows (refer to the IAA paper INSURANCE LIABILITIES - VALUATION &

Equity-based Insurance Guarantees Conference October 27-28, 2008. Pricing EAI Guarantees. Moderator Dr. K. (Ravi) Ravindran

Ravindran") Equity-based Insurance Guarantees Conference October 27-28, 2008 Pricing EAI Guarantees Noel Abkemeier, Eric Petersen Moderator Dr. K. (Ravi) Ravindran Equity Indexed Annuity Pricing Eric Petersen, F.S.A.

Equity-based Insurance Guarantees Conference October 27-28, 2008 Pricing EAI Guarantees Noel Abkemeier, Eric Petersen Moderator Dr. K. (Ravi) Ravindran Equity Indexed Annuity Pricing Eric Petersen, F.S.A.

Schroders Investment Risk Group

provides investment management services for a broad spectrum of clients including institutional, retail, private clients and charities. The long term objectives of any investment programme that we implement

provides investment management services for a broad spectrum of clients including institutional, retail, private clients and charities. The long term objectives of any investment programme that we implement

TABLE OF CONTENTS. Executive Summary 3. Introduction 5. Purposes of the Joint Research Project 6

TABLE OF CONTENTS Executive Summary 3 Introduction 5 Purposes of the Joint Research Project 6 Background 7 1. Contract and timeframe illustrated 7 2. Liability measurement bases 9 3. Earnings 10 Consideration

TABLE OF CONTENTS Executive Summary 3 Introduction 5 Purposes of the Joint Research Project 6 Background 7 1. Contract and timeframe illustrated 7 2. Liability measurement bases 9 3. Earnings 10 Consideration

Embedded Value Report

Embedded Value Report 2012 ACHMEA EMBEDDED VALUE REPORT 2012 Contents Management summary 3 Introduction 4 Embedded Value Results 5 Value Added by New Business 6 Analysis of Change 7 Sensitivities 9 Impact

Embedded Value Report 2012 ACHMEA EMBEDDED VALUE REPORT 2012 Contents Management summary 3 Introduction 4 Embedded Value Results 5 Value Added by New Business 6 Analysis of Change 7 Sensitivities 9 Impact

ETF Specific Data Point Methodologies

ETF Specific Data Point ethodologies orningstar ethodology Paper December 31 2010 2010 orningstar Inc. All rights reserved. The information in this document is the property of orningstar Inc. eproduction

ETF Specific Data Point ethodologies orningstar ethodology Paper December 31 2010 2010 orningstar Inc. All rights reserved. The information in this document is the property of orningstar Inc. eproduction

READING 23: FIXED-INCOME PORTFOLIO MANAGEMENT PART I. A- A Framework for Fixed-Income Portfolio Management

READING 23: FIXED-INCOME PORTFOLIO MANAGEMENT PART I A- A Framework for Fixed-Income Portfolio Management The basic features of the investment management process are the same for a fixed-income portfolio

READING 23: FIXED-INCOME PORTFOLIO MANAGEMENT PART I A- A Framework for Fixed-Income Portfolio Management The basic features of the investment management process are the same for a fixed-income portfolio

Risk and Investment Conference 2013. Brighton, 17 19 June

Risk and Investment Conference 03 Brighton, 7 9 June 0 June 03 Acquiring fixed income assets on a forward basis Dick Rae, HSBC and Neil Snyman, Aviva Investors 8 June 0 Structure of Presentation Introduction

Risk and Investment Conference 03 Brighton, 7 9 June 0 June 03 Acquiring fixed income assets on a forward basis Dick Rae, HSBC and Neil Snyman, Aviva Investors 8 June 0 Structure of Presentation Introduction

SURVEY ON ASSET LIABILITY MANAGEMENT PRACTICES OF CANADIAN LIFE INSURANCE COMPANIES

QUESTIONNAIRE SURVEY ON ASSET LIABILITY MANAGEMENT PRACTICES OF CANADIAN LIFE INSURANCE COMPANIES MARCH 2001 2001 Canadian Institute of Actuaries Document 20113 Ce questionnaire est disponible en français

QUESTIONNAIRE SURVEY ON ASSET LIABILITY MANAGEMENT PRACTICES OF CANADIAN LIFE INSURANCE COMPANIES MARCH 2001 2001 Canadian Institute of Actuaries Document 20113 Ce questionnaire est disponible en français

Options on 10-Year U.S. Treasury Note & Euro Bund Futures in Fixed Income Portfolio Analysis

White Paper Whitepaper Options on 10-Year U.S. Treasury Note & Euro Bund Futures in Fixed Income Portfolio Analysis Copyright 2015 FactSet Research Systems Inc. All rights reserved. Options on 10-Year

White Paper Whitepaper Options on 10-Year U.S. Treasury Note & Euro Bund Futures in Fixed Income Portfolio Analysis Copyright 2015 FactSet Research Systems Inc. All rights reserved. Options on 10-Year

!@# Agenda. Session 35. Methodology Modeling Challenges Scenario Generation Aggregation Diversification

INSURANCE & ACTUARIAL ADVISORY SERVICES!@# Session 35 Advanced Click to edit Economic Master Reserves title styleand Capital Matthew Clark FSA, CFA Valuation Actuary Symposium Austin, TX www.ey.com/us/actuarial

INSURANCE & ACTUARIAL ADVISORY SERVICES!@# Session 35 Advanced Click to edit Economic Master Reserves title styleand Capital Matthew Clark FSA, CFA Valuation Actuary Symposium Austin, TX www.ey.com/us/actuarial

Solvency Management in Life Insurance The company s perspective

Group Risk IAA Seminar 19 April 2007, Mexico City Uncertainty Exposure Solvency Management in Life Insurance The company s perspective Agenda 1. Key elements of Allianz Risk Management framework 2. Drawbacks

Group Risk IAA Seminar 19 April 2007, Mexico City Uncertainty Exposure Solvency Management in Life Insurance The company s perspective Agenda 1. Key elements of Allianz Risk Management framework 2. Drawbacks

GN47: Stochastic Modelling of Economic Risks in Life Insurance

GN47: Stochastic Modelling of Economic Risks in Life Insurance Classification Recommended Practice MEMBERS ARE REMINDED THAT THEY MUST ALWAYS COMPLY WITH THE PROFESSIONAL CONDUCT STANDARDS (PCS) AND THAT

GN47: Stochastic Modelling of Economic Risks in Life Insurance Classification Recommended Practice MEMBERS ARE REMINDED THAT THEY MUST ALWAYS COMPLY WITH THE PROFESSIONAL CONDUCT STANDARDS (PCS) AND THAT

How To Know Market Risk

Chapter 6 Market Risk for Single Trading Positions Market risk is the risk that the market value of trading positions will be adversely influenced by changes in prices and/or interest rates. For banks,

Chapter 6 Market Risk for Single Trading Positions Market risk is the risk that the market value of trading positions will be adversely influenced by changes in prices and/or interest rates. For banks,

How To Become A Life Insurance Agent

Traditional, investment, and risk management actuaries in the life insurance industry Presentation at California Actuarial Student Conference University of California, Santa Barbara April 4, 2015 Frank

Traditional, investment, and risk management actuaries in the life insurance industry Presentation at California Actuarial Student Conference University of California, Santa Barbara April 4, 2015 Frank

Asset Liability Management

e-learning and reference solutions for the global finance professional Asset Liability Management A comprehensive e-learning product covering Global Best Practices, Strategic, Operational and Analytical

e-learning and reference solutions for the global finance professional Asset Liability Management A comprehensive e-learning product covering Global Best Practices, Strategic, Operational and Analytical

Liability Driven investment by insurers: Topmost priority

Global Journal of Finance and Management. ISSN 0975-6477 Volume 6, Number 5 (2014), pp. 397-402 Research India Publications http://www.ripublication.com Liability Driven investment by insurers: Topmost

Global Journal of Finance and Management. ISSN 0975-6477 Volume 6, Number 5 (2014), pp. 397-402 Research India Publications http://www.ripublication.com Liability Driven investment by insurers: Topmost

SSgA CAPITAL INSIGHTS

SSgA CAPITAL INSIGHTS viewpoints Part of State Street s Vision thought leadership series A Stratified Sampling Approach to Generating Fixed Income Beta PHOTO by Mathias Marta Senior Investment Manager,

SSgA CAPITAL INSIGHTS viewpoints Part of State Street s Vision thought leadership series A Stratified Sampling Approach to Generating Fixed Income Beta PHOTO by Mathias Marta Senior Investment Manager,

Effective Stress Testing in Enterprise Risk Management

Effective Stress Testing in Enterprise Risk Management Lijia Guo, Ph.D., ASA, MAAA *^ Copyright 2008 by the Society of Actuaries. All rights reserved by the Society of Actuaries. Permission is granted

Effective Stress Testing in Enterprise Risk Management Lijia Guo, Ph.D., ASA, MAAA *^ Copyright 2008 by the Society of Actuaries. All rights reserved by the Society of Actuaries. Permission is granted

Session 9b L&H Insurance in a Low Interest Rate Environment. Christian Liechti

Session 9b L&H Insurance in a Low Interest Rate Environment Christian Liechti L&H Insurance in a Low Interest Rate Environment SOA Annual Symposium 24-25 June 2013 Macau, China Christian Liechti Swiss

Session 9b L&H Insurance in a Low Interest Rate Environment Christian Liechti L&H Insurance in a Low Interest Rate Environment SOA Annual Symposium 24-25 June 2013 Macau, China Christian Liechti Swiss

LDI for DB plans with lump sum benefit payment options

PRACTICE NOTE LDI for DB plans with lump sum benefit payment options Justin Owens, FSA, CFA, EA, Senior Asset Allocation Strategist Valerie Dion, CFA, FSA, Senior Consultant ISSUE: How does a lump sum

PRACTICE NOTE LDI for DB plans with lump sum benefit payment options Justin Owens, FSA, CFA, EA, Senior Asset Allocation Strategist Valerie Dion, CFA, FSA, Senior Consultant ISSUE: How does a lump sum

Variable Annuities Risk Management

Variable Annuities Risk Management Michele Bergantino Risk and Investment Conference Leeds - June 28, 2012 1 Contents VA Key Features VA Risk Management Conclusions Appendix A - VA Option Valuation, an

Variable Annuities Risk Management Michele Bergantino Risk and Investment Conference Leeds - June 28, 2012 1 Contents VA Key Features VA Risk Management Conclusions Appendix A - VA Option Valuation, an

GENERALI PANEUROPE LIMITED

GENERALI PANEUROPE LIMITED Considerations for Variable Annuity Writers when internalising their hedging activities Michael Sharpe 27th November 2014 1 Contents 1. About Generali PanEurope 2. Variable Annuities

GENERALI PANEUROPE LIMITED Considerations for Variable Annuity Writers when internalising their hedging activities Michael Sharpe 27th November 2014 1 Contents 1. About Generali PanEurope 2. Variable Annuities

Asset Liability Management and Investment Seminar May 2012. Session1: Asset Allocation for Insurance Company Liability Driven Investment.

Asset Liability and Investment Seminar May 2012 Session1: Asset Allocation for Insurance Company Liability Driven Investment Genghui Wu Asset Liability Liability Driven Investment Genghui Wu FSA, CFA,

Asset Liability and Investment Seminar May 2012 Session1: Asset Allocation for Insurance Company Liability Driven Investment Genghui Wu Asset Liability Liability Driven Investment Genghui Wu FSA, CFA,

Equity-Based Insurance Guarantees Conference November 18-19, 2013. Atlanta, GA. GAAP and Statutory Valuation of Variable Annuities

Equity-Based Insurance Guarantees Conference November 18-19, 2013 Atlanta, GA GAAP and Statutory Valuation of Variable Annuities Heather Remes GAAP and Statutory Valuation of Variable Annuities Heather

Equity-Based Insurance Guarantees Conference November 18-19, 2013 Atlanta, GA GAAP and Statutory Valuation of Variable Annuities Heather Remes GAAP and Statutory Valuation of Variable Annuities Heather

Life 2008 Spring Meeting June 16-18, 2008. Session 75, Selling Annuities through IMOs. Moderator Ghalid Bagus, FSA, FIA, MAAA

Life 2008 Spring Meeting June 16-18, 2008 Session 75, Selling Annuities through IMOs Moderator Ghalid Bagus, FSA, FIA, MAAA Authors Ghalid Bagus, FSA, FIA, MAAA Christopher L. Conklin, FSA, MAAA Yan Fridman,

Life 2008 Spring Meeting June 16-18, 2008 Session 75, Selling Annuities through IMOs Moderator Ghalid Bagus, FSA, FIA, MAAA Authors Ghalid Bagus, FSA, FIA, MAAA Christopher L. Conklin, FSA, MAAA Yan Fridman,

Liquidity premiums and contingent liabilities

Insights Liquidity premiums and contingent liabilities Craig Turnbull [email protected] The liquidity premium the concept that illiquid assets have lower prices than equivalent liquid ones has

Insights Liquidity premiums and contingent liabilities Craig Turnbull [email protected] The liquidity premium the concept that illiquid assets have lower prices than equivalent liquid ones has

For the Trustees of Defined Benefit Pension Schemes and their Investment Consultants Only.

LGIM SOLUTIONS LEGAL & GENERAL INVESTMENT MANAGEMENT Buy-Out Aware. For the Trustees of Defined Benefit Pension Schemes and their Investment Consultants Only. Preparing for the endgame: a fund range specifically

LGIM SOLUTIONS LEGAL & GENERAL INVESTMENT MANAGEMENT Buy-Out Aware. For the Trustees of Defined Benefit Pension Schemes and their Investment Consultants Only. Preparing for the endgame: a fund range specifically

Equity-Based Insurance Guarantees Conference November 18-19, 2013. Atlanta, GA. Development of Managed Risk Funds in the VA Market

Equity-Based Insurance Guarantees Conference November 18-19, 2013 Atlanta, GA Development of Managed Risk Funds in the VA Market Chad Schuster DEVELOPMENT OF MANAGED RISK FUNDS IN THE VA MARKET CHAD SCHUSTER,

Equity-Based Insurance Guarantees Conference November 18-19, 2013 Atlanta, GA Development of Managed Risk Funds in the VA Market Chad Schuster DEVELOPMENT OF MANAGED RISK FUNDS IN THE VA MARKET CHAD SCHUSTER,

Asset-Liability Management

Asset-Liability Management in today s insurance world Presentation to the Turkish Actuarial Society Jeremy Kent FIA Dominic Clark FIA Thanos Moulovasilis FIA 27 November 2013 Agenda ALM some definitions

Asset-Liability Management in today s insurance world Presentation to the Turkish Actuarial Society Jeremy Kent FIA Dominic Clark FIA Thanos Moulovasilis FIA 27 November 2013 Agenda ALM some definitions

Equity-Based Insurance Guarantees Conference November 12-13, 2012. Chicago, IL. Variable Annuity Risk Management Update

Equity-Based Insurance Guarantees Conference November 12-13, 2012 Chicago, IL Variable Annuity Risk Management Update Xiaohong Mo, FSA, MAAA, CFA Variable Annuity Risk Management Update Equity-Based Insurance

Equity-Based Insurance Guarantees Conference November 12-13, 2012 Chicago, IL Variable Annuity Risk Management Update Xiaohong Mo, FSA, MAAA, CFA Variable Annuity Risk Management Update Equity-Based Insurance

Olav Jones, Head of Insurance Risk

Getting you there. What is Risk Management of an Insurance Company, a view of a Head of Insurance Risk? Olav Jones, Head of Insurance Risk Olav Jones 29-11-2006 1 Agenda I. Risk Management in Insurance

Getting you there. What is Risk Management of an Insurance Company, a view of a Head of Insurance Risk? Olav Jones, Head of Insurance Risk Olav Jones 29-11-2006 1 Agenda I. Risk Management in Insurance

The Investment Implications of Solvency II

The Investment Implications of Solvency II André van Vliet, Ortec Finance, Insurance Risk Management Anthony Brown, FSA Outline Introduction - Solvency II - Strategic Decision Making Impact of investment

The Investment Implications of Solvency II André van Vliet, Ortec Finance, Insurance Risk Management Anthony Brown, FSA Outline Introduction - Solvency II - Strategic Decision Making Impact of investment

Fixed Income Attribution. The Wiley Finance Series

Brochure More information from http://www.researchandmarkets.com/reports/2216624/ Fixed Income Attribution. The Wiley Finance Series Description: Fixed income attribution is by its very nature a complex

Brochure More information from http://www.researchandmarkets.com/reports/2216624/ Fixed Income Attribution. The Wiley Finance Series Description: Fixed income attribution is by its very nature a complex

Rising rates: A case for active bond investing?

Rising rates: A case for active bond investing? Vanguard research August 11 Executive summary. Although the success of active management in fixed income has not been stellar Vanguard research has found,

Rising rates: A case for active bond investing? Vanguard research August 11 Executive summary. Although the success of active management in fixed income has not been stellar Vanguard research has found,

FIXED INCOME INVESTORS HAVE OPTIONS TO INCREASE RETURNS, LOWER RISK

1 FIXED INCOME INVESTORS HAVE OPTIONS TO INCREASE RETURNS, LOWER RISK By Michael McMurray, CFA Senior Consultant As all investors are aware, fixed income yields and overall returns generally have been

1 FIXED INCOME INVESTORS HAVE OPTIONS TO INCREASE RETURNS, LOWER RISK By Michael McMurray, CFA Senior Consultant As all investors are aware, fixed income yields and overall returns generally have been

The Empire Life Insurance Company

The Empire Life Insurance Company Condensed Interim Consolidated Financial Statements For the six months ended June 30, 2015 Unaudited Issue Date: August 7, 2015 DRAFT NOTICE OF NO AUDITOR REVIEW OF CONDENSED

The Empire Life Insurance Company Condensed Interim Consolidated Financial Statements For the six months ended June 30, 2015 Unaudited Issue Date: August 7, 2015 DRAFT NOTICE OF NO AUDITOR REVIEW OF CONDENSED

Application of Interest Rate Swaps in Indian Insurance Industry Amruth Krishnan Rohit Ajgaonkar Guide: G.LN.Sarma

Institute of Actuaries of India Application of Interest Rate Swaps in Indian Insurance Industry Amruth Krishnan Rohit Ajgaonkar Guide: G.LN.Sarma 21 st IFS Seminar Indian Actuarial Profession Serving the

Institute of Actuaries of India Application of Interest Rate Swaps in Indian Insurance Industry Amruth Krishnan Rohit Ajgaonkar Guide: G.LN.Sarma 21 st IFS Seminar Indian Actuarial Profession Serving the

Practical Applications of Stochastic Modeling for Disability Insurance

Practical Applications of Stochastic Modeling for Disability Insurance Society of Actuaries Session 8, Spring Health Meeting Seattle, WA, June 007 Practical Applications of Stochastic Modeling for Disability

Practical Applications of Stochastic Modeling for Disability Insurance Society of Actuaries Session 8, Spring Health Meeting Seattle, WA, June 007 Practical Applications of Stochastic Modeling for Disability

Equity-index-linked swaps

Equity-index-linked swaps Equivalent to portfolios of forward contracts calling for the exchange of cash flows based on two different investment rates: a variable debt rate (e.g. 3-month LIBOR) and the

Equity-index-linked swaps Equivalent to portfolios of forward contracts calling for the exchange of cash flows based on two different investment rates: a variable debt rate (e.g. 3-month LIBOR) and the

Investment Portfolio Management and Effective Asset Allocation for Institutional and Private Banking Clients

Investment Portfolio Management and Effective Asset Allocation for Institutional and Private Banking Clients www.mce-ama.com/2396 Senior Managers Days 4 www.mce-ama.com 1 WHY attend this programme? This

Investment Portfolio Management and Effective Asset Allocation for Institutional and Private Banking Clients www.mce-ama.com/2396 Senior Managers Days 4 www.mce-ama.com 1 WHY attend this programme? This

INVESTMENT RISK MANAGEMENT POLICY

INVESTMENT RISK MANAGEMENT POLICY BOARD APPROVED: DECEMBER 27, 2011 TABLE OF CONTENTS SECTION PAGE I. Purpose... 1 II. Policy Roles and Responsibilities... 1 III. Risk Guidelines... 2 IV. Measurement and

INVESTMENT RISK MANAGEMENT POLICY BOARD APPROVED: DECEMBER 27, 2011 TABLE OF CONTENTS SECTION PAGE I. Purpose... 1 II. Policy Roles and Responsibilities... 1 III. Risk Guidelines... 2 IV. Measurement and

Fixed Income Performance Attribution

Fixed Income Performance Attribution Mary Cait McCarthy August 2014 Content 1 2 3 4 5 6 What is Performance Attribution? Uses of Performance Attribution Drivers of Return in Fixed Income Returns Based

Fixed Income Performance Attribution Mary Cait McCarthy August 2014 Content 1 2 3 4 5 6 What is Performance Attribution? Uses of Performance Attribution Drivers of Return in Fixed Income Returns Based

Developments in Risk Attribution

Singapore 2004 Developments in Risk Attribution Investment Managers Association of Singapore September 23, 2004 Alex Carmichael Director Risk Solutions & Operations RiskMetrics Group Asia Pacific [email protected]

Singapore 2004 Developments in Risk Attribution Investment Managers Association of Singapore September 23, 2004 Alex Carmichael Director Risk Solutions & Operations RiskMetrics Group Asia Pacific [email protected]

Market Consistent Embedded Value Principles October 2009. CFO Forum

CFO Forum Market Consistent Embedded Value Principles October 2009 Contents Introduction. 2 Coverage. 2 MCEV Definitions...3 Free Surplus 3 Required Capital 3 Value of in-force Covered Business 4 Financial

CFO Forum Market Consistent Embedded Value Principles October 2009 Contents Introduction. 2 Coverage. 2 MCEV Definitions...3 Free Surplus 3 Required Capital 3 Value of in-force Covered Business 4 Financial

MetLife Investments Steve Kandarian Chief Investment Officer

June 2007 MetLife Investments Steve Kandarian Chief Investment Officer Safe Harbor Statement These materials contain statements which constitute forward-looking statements within the meaning of the Private

June 2007 MetLife Investments Steve Kandarian Chief Investment Officer Safe Harbor Statement These materials contain statements which constitute forward-looking statements within the meaning of the Private

Investment Portfolio Management Techniques for Fixed Income, Equity and Alternative Investments

Investment Portfolio Management Techniques for Fixed Income, Equity and Alternative Investments www.mce-ama.com/2400 Senior Managers Days 4 www.mce-ama.com 1 WHY attend this programme? Managing an investment

Investment Portfolio Management Techniques for Fixed Income, Equity and Alternative Investments www.mce-ama.com/2400 Senior Managers Days 4 www.mce-ama.com 1 WHY attend this programme? Managing an investment

The Short Dated Interest Rate Market Trading JIBAR Futures

JOHANNESBURG STOCK EXCHANGE Interest Rates The Short Dated Interest Rate Market Trading JIBAR Futures JIBAR Futures are Short Term Interest Rate (STIR) Futures based on the 3-month JIBAR (Johannesburg

JOHANNESBURG STOCK EXCHANGE Interest Rates The Short Dated Interest Rate Market Trading JIBAR Futures JIBAR Futures are Short Term Interest Rate (STIR) Futures based on the 3-month JIBAR (Johannesburg

Projection of the With-Profits Balance Sheet under ICA+ John Lim (KPMG) & Richard Taylor (AEGON) 11 November 2013

& Richard Taylor (AEGON) 11 November 2013") Projection of the With-Profits Balance Sheet under ICA+ John Lim (KPMG) & Richard Taylor (AEGON) 11 November 2013 Introduction Projecting the with-profits business explicitly is already carried out by

Projection of the With-Profits Balance Sheet under ICA+ John Lim (KPMG) & Richard Taylor (AEGON) 11 November 2013 Introduction Projecting the with-profits business explicitly is already carried out by

Assumptions Total Assets = 50,000,000 Net Surpluses Received = 480,000 Net Surpluses Received in one Month = 40,000

GAP ANALYSIS SACCO savers have an inherent preference for short-term liquid accounts, even when the interest rate in these accounts is subject to changes. Furthermore, borrowers have an inherent preference

GAP ANALYSIS SACCO savers have an inherent preference for short-term liquid accounts, even when the interest rate in these accounts is subject to changes. Furthermore, borrowers have an inherent preference

ERM Exam Core Readings Fall 2015. Table of Contents

i ERM Exam Core Readings Fall 2015 Table of Contents Section A: Risk Categories and Identification The candidate will understand the types of risks faced by an entity and be able to identify and analyze

i ERM Exam Core Readings Fall 2015 Table of Contents Section A: Risk Categories and Identification The candidate will understand the types of risks faced by an entity and be able to identify and analyze

The International Certificate in Banking Risk and Regulation (ICBRR)

") The International Certificate in Banking Risk and Regulation (ICBRR) The ICBRR fosters financial risk awareness through thought leadership. To develop best practices in financial Risk Management, the authors

The International Certificate in Banking Risk and Regulation (ICBRR) The ICBRR fosters financial risk awareness through thought leadership. To develop best practices in financial Risk Management, the authors

Hedging Variable Annuity Guarantees

p. 1/4 Hedging Variable Annuity Guarantees Actuarial Society of Hong Kong Hong Kong, July 30 Phelim P Boyle Wilfrid Laurier University Thanks to Yan Liu and Adam Kolkiewicz for useful discussions. p. 2/4

p. 1/4 Hedging Variable Annuity Guarantees Actuarial Society of Hong Kong Hong Kong, July 30 Phelim P Boyle Wilfrid Laurier University Thanks to Yan Liu and Adam Kolkiewicz for useful discussions. p. 2/4

Model for. Eleven factors to consider when evaluating bond holdings. Passage of time

PERFORMANCEAttribution A Model for FIXED-INCOME PORTFOLIOS Eleven factors to consider when evaluating bond holdings. BY NABIL KHOURY, MARC VEILLEUX & ROBERT VIAU Performance attribution analysis partitions

PERFORMANCEAttribution A Model for FIXED-INCOME PORTFOLIOS Eleven factors to consider when evaluating bond holdings. BY NABIL KHOURY, MARC VEILLEUX & ROBERT VIAU Performance attribution analysis partitions

Investment Management a creator of value in an insurance company. Zurich Financial Services March 2009 Second edition

Investment Management a creator of value in an insurance company Zurich Financial Services March 2009 Second edition Investment Management Insurance companies generally recognise the importance of separating

Investment Management a creator of value in an insurance company Zurich Financial Services March 2009 Second edition Investment Management Insurance companies generally recognise the importance of separating

Financial Engineering g and Actuarial Science In the Life Insurance Industry

Financial Engineering g and Actuarial Science In the Life Insurance Industry Presentation at USC October 31, 2013 Frank Zhang, CFA, FRM, FSA, MSCF, PRM Vice President, Risk Management Pacific Life Insurance

Financial Engineering g and Actuarial Science In the Life Insurance Industry Presentation at USC October 31, 2013 Frank Zhang, CFA, FRM, FSA, MSCF, PRM Vice President, Risk Management Pacific Life Insurance

Interest rate risk and how to manage it. University of Economics, 16/10/2014 Vladimir Sosovicka

Interest rate risk and how to manage it University of Economics, 16/10/2014 Vladimir Sosovicka 2 Content 1. Interest rate risk what is it? 2. Management of interest rate risk: Basic tools (bonds, BPV,

Interest rate risk and how to manage it University of Economics, 16/10/2014 Vladimir Sosovicka 2 Content 1. Interest rate risk what is it? 2. Management of interest rate risk: Basic tools (bonds, BPV,

Benchmarking Real Estate Performance Considerations and Implications

Benchmarking Real Estate Performance Considerations and Implications By Frank L. Blaschka Principal, The Townsend Group The real estate asset class has difficulties in developing and applying benchmarks

Benchmarking Real Estate Performance Considerations and Implications By Frank L. Blaschka Principal, The Townsend Group The real estate asset class has difficulties in developing and applying benchmarks

Solvency II and Predictive Analytics in LTC and Beyond HOW U.S. COMPANIES CAN IMPROVE ERM BY USING ADVANCED

Solvency II and Predictive Analytics in LTC and Beyond HOW U.S. COMPANIES CAN IMPROVE ERM BY USING ADVANCED TECHNIQUES DEVELOPED FOR SOLVENCY II AND EMERGING PREDICTIVE ANALYTICS METHODS H o w a r d Z

Solvency II and Predictive Analytics in LTC and Beyond HOW U.S. COMPANIES CAN IMPROVE ERM BY USING ADVANCED TECHNIQUES DEVELOPED FOR SOLVENCY II AND EMERGING PREDICTIVE ANALYTICS METHODS H o w a r d Z

LIFE INSURANCE RATING METHODOLOGY CREDIT RATING AGENCY OF

LIFE INSURANCE RATING METHODOLOGY CREDIT RATING AGENCY OF BANGLADESH LIMITED 1 CRAB S RATING PROCESS An independent and professional approach of the CRAB is designed to ensure reliable, consistent and

LIFE INSURANCE RATING METHODOLOGY CREDIT RATING AGENCY OF BANGLADESH LIMITED 1 CRAB S RATING PROCESS An independent and professional approach of the CRAB is designed to ensure reliable, consistent and

Glide path ALM: A dynamic allocation approach to derisking

Glide path ALM: A dynamic allocation approach to derisking Authors: Kimberly A. Stockton and Anatoly Shtekhman, CFA Removing pension plan risk through derisking investment strategies has become a major

Glide path ALM: A dynamic allocation approach to derisking Authors: Kimberly A. Stockton and Anatoly Shtekhman, CFA Removing pension plan risk through derisking investment strategies has become a major