Construction-to-Perm FHA One Time Close. Construction Financing for Today's Market

|

|

|

- Anissa Grace O’Connor’

- 10 years ago

- Views:

Transcription

1 Construction-to-Perm FHA One Time Close Construction Financing for Today's Market

2 AGENDA Overview Construction-to-Perm Guidelines Eligibility Requirements Documentation Requirements (Closing and Endorsement) Builder Approval Structuring the Deal Draw Process Draws and Disbursements HUD-1 Settlement Statement Benefits

3 Overview Combines the Following Features: 1. A construction loan, which is a short-term interim loan for financing the cost of construction, and 2. The traditional long-term permanent mortgage that involves only one closing 3. Is considered a purchase transaction, for mortgage insurance and LTV purposes, and is made directly to the borrower 4. Standard FHA guidelines apply: 3.5% down payment or Land in Lieu of down payment and 6.0% seller concessions 5. No interest payments due during construction by either the builder or the buyer 6. Draws managed by experienced construction department 7. Works for lot purchase or existing land 8. No additional appraisal after closing 9. No additional credit pull/qualifying after closing 10. Borrowers can build anywhere

4 Guidelines Borrower cannot be their own contractor. Borrowers must be contracted with a builder in order to construct the home Borrower may not act as his/her own general contractor Sales price cannot change after closing. Borrower must provide a fully executed copy of contract agreement, which includes the builders price to build Builders may only used the fixed-cost method for agreements Any change orders (upgrades) after construction begins will out of pocket expense for borrower If builder is not owner of the land, provide separate land agreement

5 Guidelines Lot Ownership If purchased in past 6 months- provide settlement statement showing acquisition cost If borrower owns lot free-and-clear, document date of ownership and that there are no liens against the property Land equity Land equity may be used in lieu of down payment Owned less than 6 months/purchasing at closing - If value is lower than acquisition cost, value must be used in determining maximum mortgage amount Owned greater than 6 months - Or received as an acceptable gift in which case the value may be used instead of the cost If the builder owns the land - the total acquisition cost for the maximum mortgage purposes equals the borrowers purchase price

6 Guidelines Calculating the base loan amount The maximum mortgage amount is determined by applying the LTV limits to the lesser of the appraised value or the acquisition cost Unless, owned greater than 6 months Construction time 130 days construction period If construction period is exceeded, per diem charges will apply to the builder ($75 per day, per diem) Locks The permanent mortgage loan interest rate is locked at the time of closing with 150 day lock Note: Loan should not be locked while being processed. Use the float option for disclosures to prevent using construction days during processing.

7 Guidelines Payments Amortization must begin no later than the first of the month within 60 days from the date of 1) final inspection or 2) issuance of certificate of occupancy, whichever is later. Loans are not eligible for insurance until completion of the home UFMIP is remitted as normal, but not endorsed until completion Disclosure provided to borrower, with closing package, explaining 1. That the loan is not eligible for FHA mortgage insurance until after A) final inspection or B) issuance of a certificate of occupancy, whichever is later and 2. That FHA has no obligation until the mortgage is endorsed for insurance

8 Guidelines Draws & Disbursement Written approval from the borrower must be obtained before each draw payment is provided to the builder Closing documents include standard FHA documents plus Construction Rider or Allonge to the Note, and Construction Loan Agreement Loan Modification Notary sent to borrower to sign loan modification documents Modification confirms the existence of a permanent loan and that corresponding amortizing interest on the mortgage loan shall commence or commenced with 60 days of the property being 100% complete

9 Guidelines Endorsement documents include: A certification, signed by the borrower after conversion to the permanent loan, that the mortgaged property is free and clear of all liens other than the mortgage Verification that the construction loan has been fully drawn down All property related requirements for new construction

10 Builder Approval Completed Builder Approval Package Signed General Authorization Letter (included with Builder Profile and Registration packet) Acceptance letter from HUD acceptable 10- Year Warranty company Copy of State Builder License or Registration; Copy of Occupational or Business License; Copy of Declarations Page: Worker s Compensation Insurance & General Liability Insurance; Bank and Supplier Reference Copy of Principal(s) Resume; Copy of Articles of Incorporation; and 2009 Tax Returns business tax returns (for business) or personal tax return (for sole proprietor) Tax Returns business tax returns (for business) or personal tax return (for sole proprietor). If extension was filed, provide 2010 financials Year-to-Date Profit and Loss and Balance Sheet

or personal tax return (for sole proprietor). If extension was filed, provide 2010 financials.")

11 Builder Approval Step 1 Step 2 Step 3 Builder completes builder application Submits to American Southwest Mortgage (AMSW) AMSW reviews package for all items Submits Builder Package to investor Investor conducts reference checks, verifications, etc. Can take up to two weeks Step 4 Investor notifies AMSW of builder approval

12 Draws & Disbursements Program designed to reimburse builders after various stages of completion. Work is done, then costs are reimbursed. Borrower must sign off on all draws. No exceptions. Inspections to be done at each draw phase. Builder must submit Draw Request Form (Investor will provide this form to the builder after the loan has closed) Draws are typically disbursed within 48 hours of receiving all required documentation. Disbursements can be made either wire transfer or a check via USPS.

Draws are")

13 Draw Schedule Item $ 100, Land Cost $ 25, Total Cost $ 125, Holdback $ 12, Funds available $ 112, DISBURSEMENT SCHEDULE Funds Available Draw Amount Total Paid Out Closing Land paid in full at time of $112,500.0 $25,000.0 $25,000.0 Stage 1 Funding Immediately after $87,500.0 $8,750.0 $33,750.0 Stage 2 Funding $78,750.0 $11,812.5 $45,562.5 Stage 3 Funding $66,937.5 $22,089.3 $67,651.8 Stage 4 Funding $44,848.1 $21,527.1 $89,178.9 Stage 5 Funding $23,321.0 $23,321.0 $112,500.0 Holdback/Retainage Release - $12,500.0 $125,000.0

14 Draw Criteria Stage 1 Funding Stage 2 Funding Stage 3 Funding Investor will disburse 10% of available construction funds immediately after purchase. Excavation / Plans / Permits / Site Prep / Other miscellaneous costs Investor will disburse 15% of available construction funds at completion of following: Primary plumbing rough-in Footings, foundation & slab Investor will disburse 33% of available construction funds at completion of following: Framing & Sheathing Exterior Doors Windows Set Wiring rough-in Secondary plumbing rough-in Primary heating rough-in Secondary heating rough-in Fireplaces Roofing Approved frame inspection Stage 4 Funding Stage 5 Funding Investor will disburse 48% of available construction funds after completion of following. Insulation Sheetrock / Plaster Interior Trim & Doors Interior plumbing Investor will disburse remainder of available construction funds at completion of following: Furnace / AC or Evap. cooler Stucco, Veneer, Siding Exterior Painting Exterior Concrete Resilient Flooring / Carpeting Plumbing Fixtures Final Electrical Fixtures Appliances Finish Grade and Clean-Up Certificate of Occupancy An inspection must be completed by either a home inspector, original appraiser or engineer. They will certify that each item has been satisfactorily completed per the funding stage requirements. A signed inspection form by the borrower, builder and inspector, accompanied by digital pictures are necessary to show confirmation of completion.

15 Lender Calculation Worksheet Used to assist in constructing builders costs and builders net Must be signed by borrower, lender and builder Includes all fees except inspection fees Inspection fees are paid by the builder Inspections are order by the investor

16 File Flow Originator to Complete Loan Calculation Worksheet Borrower Approval Underwriting Doc Prep Closing/Funding Draw 3: Inspection Required Draw 2: Inspection Required Draw 1: Soft Cost (after purchase), Investor Purchases Loan Land Payoff at Closing Draw 4: Inspection Required Draw 5: Inspection Required Loan Modification Contingency Release 31 DAYS

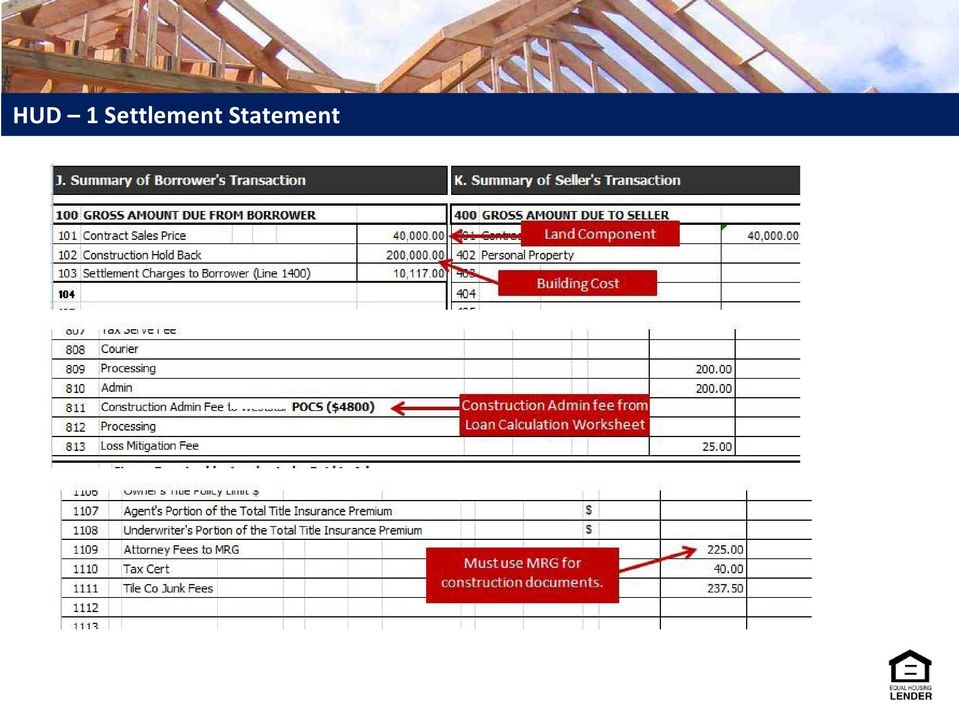

17 HUD 1 Settlement Statement

18 Builder Benefits Expand their potential and free up credit lines for other projects - Loans are made directly to the home buyer offering builders the flexibility and the capital to start new projects. Qualify, Close then Complete - As lending guidelines continue to tighten, the risk of losing would-be buyers represents tremendous risks for builders today. With the FHA One-Time Close, home buyers are qualified, closed, and then construction begins. Buyer fallout becomes ancient history - That's right, just like Eight Tracks, Atari and Record Albums, worry over buyer fallout will become a thing of the past! The home buyer owns the loan from the time they close - before construction begins. Once construction is complete, the loan will then roll into permanent financing. Simplified Draw Process Quick turnaround on draws means a faster, smoother process, and happy builders.

19 Buyer Benefits Low Down Payment Requirements - Typically, the buyer can get a loan with as little as 3.5% down payment. In some cases, if the buyer already owns the land, they get a loan with no money out-of-pocket by using the land as equity. Reduces Costs and Frustrations - Saves on closing costs and hassles by combining the lot loan, interim construction financing, and permanent mortgage loan into one convenient, cost saving package. Deferred Payment - Unlike a two-time close, no payments will be made during the construction process. Payment begins after completion when the buyer is already enjoying their new home. Rate Protection - With one-close, the rate is locked at the time of closing. Borrowers are protected from any uncertainty of a rate hike while the home is in construction.

20 Realtor Benefits Move land listings with financing designed with buyers and land listings in mind. Commission paid at closing, no waiting for the house to be completed Assures Realtors have a qualified buyer 96.5% financing expands the potential pool of buyers

21 Originator Benefits Originator Benefits Grow and strengthen your builder and realtor partnerships Qualify more borrowers for new construction, build on your lot, financing Help your realtor partners move those land listings Give peace of mind to your builders by offering a No Buyer Fallout During Construction Guarantee Stand out from the crowd by offering a specialty product that s sure to get you noticed

Dream It. FInance It. BuIlD It.

Dream It. FInance It. BuIlD It. Construction loans designed to your specifications You ve got You ve US! got US! Banking Loans Investments Tax & Payroll Insurance CONSTRUCTION/PERMANENT MORTGAGE PROGRAM

Dream It. FInance It. BuIlD It. Construction loans designed to your specifications You ve got You ve US! got US! Banking Loans Investments Tax & Payroll Insurance CONSTRUCTION/PERMANENT MORTGAGE PROGRAM

A consumer guide to construction financing.

A consumer guide to construction financing. Single Close Construction Loans Are you building a custom home? This guide is a valuable resource for anyone planning to build a custom home. It provides information

A consumer guide to construction financing. Single Close Construction Loans Are you building a custom home? This guide is a valuable resource for anyone planning to build a custom home. It provides information

FHA Streamline (K) Limited Repair Program

Limited Repair Program") Training Mortgage Professionals FHA Streamline (K) Limited Repair Program Facilitator: XXXXXXXXX The Streamline (K) Overview General Characteristics Eligible/Ineligible Improvements Documentation Requirements

Training Mortgage Professionals FHA Streamline (K) Limited Repair Program Facilitator: XXXXXXXXX The Streamline (K) Overview General Characteristics Eligible/Ineligible Improvements Documentation Requirements

PRMI 203K Streamline Loan. FHA Renovation Loan

PRMI 203K Streamline Loan FHA Renovation Loan Put the finishing touches on your borrowers Dream home. Purchase or Refinances Help you to sell more homes, and represent more buyers. Work with contractors

PRMI 203K Streamline Loan FHA Renovation Loan Put the finishing touches on your borrowers Dream home. Purchase or Refinances Help you to sell more homes, and represent more buyers. Work with contractors

Chapter 6. Special Underwriting

HUD 4155.1 Chapter 6, Table of Contents Table of Contents Chapter 6. Special Underwriting Section A. Special Underwriting Instructions Overview... 6-A-1 1. FHA s TOTAL Mortgage Scorecard... 6-A-2 2. Temporary

HUD 4155.1 Chapter 6, Table of Contents Table of Contents Chapter 6. Special Underwriting Section A. Special Underwriting Instructions Overview... 6-A-1 1. FHA s TOTAL Mortgage Scorecard... 6-A-2 2. Temporary

203K Loan Parameters

Full documentation only. 203K Loan Parameters AUS approval required, no manual underwriting permitted. Maximum DTI ratios of 31%/43% regardless of AUS findings. Both purchase or rate and term refinance

Full documentation only. 203K Loan Parameters AUS approval required, no manual underwriting permitted. Maximum DTI ratios of 31%/43% regardless of AUS findings. Both purchase or rate and term refinance

Home Building Basics

Home Building Basics Key points to consider before building your new home. Standard Requirements for Consumer Interim Construction Loans No Work Affidavit Performed by Surveyor and Recorded with Mortgage

Home Building Basics Key points to consider before building your new home. Standard Requirements for Consumer Interim Construction Loans No Work Affidavit Performed by Surveyor and Recorded with Mortgage

REPAIRING YOUR HOME CONSTRUCTION LOAN PROCEDURES 1-800-589-8850 WWW.FIRSTFEDLORAIN.COM

REPAIRING YOUR HOME CONSTRUCTION LOAN PROCEDURES 1-800-589-8850 WWW.FIRSTFEDLORAIN.COM FIRST FEDERAL SAVINGS AND LOAN ASSOCIATION OF LORAIN YOUR COMMUNITY BANK SINCE 1921 Toll Free 1-800-589-8850 3721

REPAIRING YOUR HOME CONSTRUCTION LOAN PROCEDURES 1-800-589-8850 WWW.FIRSTFEDLORAIN.COM FIRST FEDERAL SAVINGS AND LOAN ASSOCIATION OF LORAIN YOUR COMMUNITY BANK SINCE 1921 Toll Free 1-800-589-8850 3721

A CONSUMER S G UIDE TO C ONSTRUCTION F INANCING

A CONSUMER S G UIDE TO C ONSTRUCTION F INANCING ARE YOU BUILDING A CUSTOM HOME? This guide is a valuable resource for anyone planning to build a custom home. It provides information on the financing process,

A CONSUMER S G UIDE TO C ONSTRUCTION F INANCING ARE YOU BUILDING A CUSTOM HOME? This guide is a valuable resource for anyone planning to build a custom home. It provides information on the financing process,

Steps in the Construction Loan Process

Steps in the Construction Loan Process The following information is provided as a general guide to the construction loan process. For more specific information, please contact your lender and/or attorney.

Steps in the Construction Loan Process The following information is provided as a general guide to the construction loan process. For more specific information, please contact your lender and/or attorney.

Presents. FHA Streamlined(K) & 203(k) Training. July 20, 2011 7/18/2011. FHA Streamlined(k) Rehab Program

& 203(k) Training. July 20, 2011 7/18/2011. FHA Streamlined(k) Rehab Program") Presents FHA Streamlined(K) & 203(k) Training July 20, 2011 FHA Streamlined(k) Rehab Program Enables borrowers to finance both the purchase or refinance of a home and the cost of its rehabilitation through

Presents FHA Streamlined(K) & 203(k) Training July 20, 2011 FHA Streamlined(k) Rehab Program Enables borrowers to finance both the purchase or refinance of a home and the cost of its rehabilitation through

FHA REPAIR ESCROW GUIDELINES

FHA REPAIR ESCROW GUIDELINES Introduction Escrow holdbacks are used to facilitate loan closings for properties that require no more than $5000 of repairs to meet FHA s minimum property requirements. The

FHA REPAIR ESCROW GUIDELINES Introduction Escrow holdbacks are used to facilitate loan closings for properties that require no more than $5000 of repairs to meet FHA s minimum property requirements. The

Construction Financing Guide

Mark Negenman, Mortgage Specialist Axiom Mortgage Partners Construction Financing Guide www.mark.urbanmortgage.ca [email protected] 403.390.0887 i Construction Financing Guide Mark Negenman Urban Mortgage

Mark Negenman, Mortgage Specialist Axiom Mortgage Partners Construction Financing Guide www.mark.urbanmortgage.ca [email protected] 403.390.0887 i Construction Financing Guide Mark Negenman Urban Mortgage

Quick Reference Program Summary. The following is an outline of the underwriting and closing requirements of New Hampshire Housing.

Quick Reference Program Summary The following is an outline of the underwriting and closing requirements of New Hampshire Housing. Specific Program Rules are attached to this reference. A reservation cannot

Quick Reference Program Summary The following is an outline of the underwriting and closing requirements of New Hampshire Housing. Specific Program Rules are attached to this reference. A reservation cannot

Welcome to the world of Renovation loans

Welcome to the world of Renovation loans What is a 203K loan? How can a 203K loan be used? Advantages of 203K loans The process of obtaining a 203K loan Why we are the experts A 203K is FHA s Rehabilitation

Welcome to the world of Renovation loans What is a 203K loan? How can a 203K loan be used? Advantages of 203K loans The process of obtaining a 203K loan Why we are the experts A 203K is FHA s Rehabilitation

SECTION 4 REHABILITATION MORTGAGES 203(k) Standard & 203(k) Limited

Standard & 203(k) Limited") SECTION 4 REHABILITATION MORTGAGES 203(k) Standard & 203(k) Limited 4.1 Program Descriptions 4.2 Borrower Eligibility 4.3 Property Eligibility 4.4 Principal Residence Requirement 4.5 Rehabilitation Loan

SECTION 4 REHABILITATION MORTGAGES 203(k) Standard & 203(k) Limited 4.1 Program Descriptions 4.2 Borrower Eligibility 4.3 Property Eligibility 4.4 Principal Residence Requirement 4.5 Rehabilitation Loan

http://www.allregs.com/tpl/documentprint.aspx?did3=fbac4aa6751c4ea0b8e44256c659d9f...

Page 1 of 5 Lending Library / Correspondent Seller Guide / 500. Products / 508. HIP Full FHA 203(k) 508. HIP Full FHA 203(k) HIP Full FHA 203(k) Product Matrix/Guidelines The FHA 203(k) program (i.e. Full

Page 1 of 5 Lending Library / Correspondent Seller Guide / 500. Products / 508. HIP Full FHA 203(k) 508. HIP Full FHA 203(k) HIP Full FHA 203(k) Product Matrix/Guidelines The FHA 203(k) program (i.e. Full

FNMA HomeStyle Renovation

Product Types 10-30 year fixed Sales Focus HomeStyle enables homebuyers and homeowners to finance either the purchase or a refinance of a house and the cost of its rehabilitation through a single mortgage.

Product Types 10-30 year fixed Sales Focus HomeStyle enables homebuyers and homeowners to finance either the purchase or a refinance of a house and the cost of its rehabilitation through a single mortgage.

HOMESTYLE RENOVATION. Look at the possibilities

HOMESTYLE RENOVATION Look at the possibilities HOMESTREET: WHO ARE WE? Based in the Northwest, HomeStreet Bank if one of the largest community banks in the Northwest and Hawaii. HomeStreet began in 1921

HOMESTYLE RENOVATION Look at the possibilities HOMESTREET: WHO ARE WE? Based in the Northwest, HomeStreet Bank if one of the largest community banks in the Northwest and Hawaii. HomeStreet began in 1921

Your Blueprint For Constructing or Renovating Your Dream Home

Your Blueprint For Constructing or Renovating Your Dream Home An informational guide for completing a successful construction or remodel through the construction loan process. Provided to you by: Table

Your Blueprint For Constructing or Renovating Your Dream Home An informational guide for completing a successful construction or remodel through the construction loan process. Provided to you by: Table

VA Borrower Fees and Charges

VA Borrower Fees and OVERVIEW Purpose The VA home loan program involves a veteran s benefit. VA policy has evolved around the objective of helping the veteran to use his/her home loan benefit. Therefore,

VA Borrower Fees and OVERVIEW Purpose The VA home loan program involves a veteran s benefit. VA policy has evolved around the objective of helping the veteran to use his/her home loan benefit. Therefore,

How To Understand The Veteran Loan Policy

Chapter 8. Borrower Fees and Charges and the VA Funding Fee Overview In this Chapter This chapter contains the following topics. Topic Topic Name See Page 1 VA Policy on Fees and Charges Paid by the Veteran-Borrower

Chapter 8. Borrower Fees and Charges and the VA Funding Fee Overview In this Chapter This chapter contains the following topics. Topic Topic Name See Page 1 VA Policy on Fees and Charges Paid by the Veteran-Borrower

SLIDE 1 OUT OF 42. THE BASICS: 203(k) FHA Standard 203(k) Andrew Allen COPYRIGHT 2013 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED

FHA Standard 203(k) Andrew Allen COPYRIGHT 2013 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED") SLIDE 1 OUT OF 42 R THE BASICS: 203(k) FHA Standard 203(k) Andrew Allen SLIDE 2 OUT OF 42 FHA 203K Questions 203k Explained What is the FHA 203(k) Loan Program? What are the program guidelines? What types

SLIDE 1 OUT OF 42 R THE BASICS: 203(k) FHA Standard 203(k) Andrew Allen SLIDE 2 OUT OF 42 FHA 203K Questions 203k Explained What is the FHA 203(k) Loan Program? What are the program guidelines? What types

[LENDER] CONSTRUCTION LOAN AGREEMENT

![[LENDER] CONSTRUCTION LOAN AGREEMENT](/thumbs/26/9025823.jpg "[LENDER] CONSTRUCTION LOAN AGREEMENT") [LENDER] CONSTRUCTION LOAN AGREEMENT THIS IS A MODEL DOCUMENT FOR USE IN HOMESTYLE LOAN TRANSACTIONS. THIS FORM IS PROVIDED AS AN EXAMPLE AND IS NOT VALID AND ENFORCEABLE IN ALL JURISDICTIONS. LENDERS

[LENDER] CONSTRUCTION LOAN AGREEMENT THIS IS A MODEL DOCUMENT FOR USE IN HOMESTYLE LOAN TRANSACTIONS. THIS FORM IS PROVIDED AS AN EXAMPLE AND IS NOT VALID AND ENFORCEABLE IN ALL JURISDICTIONS. LENDERS

CONSTRUCTION AND PERMANENT LOAN FINANCING TERM SHEET

CONSTRUCTION AND PERMANENT LOAN FINANCING TERM SHEET This Term Sheet is to be utilized for disclosure of possible terms and conditions only. This is not to be construed as a commitment to lend. Terms and

CONSTRUCTION AND PERMANENT LOAN FINANCING TERM SHEET This Term Sheet is to be utilized for disclosure of possible terms and conditions only. This is not to be construed as a commitment to lend. Terms and

DREW MORTGAGE ASSOCIATES CUSTOMER IDENTIFICATION FORM

DREW MORTGAGE ASSOCIATES CUSTOMER IDENTIFICATION FORM Complete the required information for Borrower and each Co-Borrower. (Place completed form with the Loan File.) LOAN NUMBER: BORROWER NAME: Borrower

DREW MORTGAGE ASSOCIATES CUSTOMER IDENTIFICATION FORM Complete the required information for Borrower and each Co-Borrower. (Place completed form with the Loan File.) LOAN NUMBER: BORROWER NAME: Borrower

FHA Sections 220, 221 (d)(4) & 221 (d)(3)

(4) & 221 (d)(3)") FHA Sections 220, 221 (d)(4) & 221 (d)(3) FHA-Insured Financing for the New Construction or Substantial Rehabilitation Of Multifamily Rental Housing FHA Section 220 provides mortgage insurance for housing

FHA Sections 220, 221 (d)(4) & 221 (d)(3) FHA-Insured Financing for the New Construction or Substantial Rehabilitation Of Multifamily Rental Housing FHA Section 220 provides mortgage insurance for housing

HUD Real Estate Owned (REO) Loan Program Guide

Loan Program Guide") Table of Contents HUD Real Estate Owned (REO) Loan Program Guide Wholesale Lending January 9, 2014 Program Guide... 2 Pacific Union Financial Credit Philosophy... 2 Ability to Repay and Qualified Mortgages...

Table of Contents HUD Real Estate Owned (REO) Loan Program Guide Wholesale Lending January 9, 2014 Program Guide... 2 Pacific Union Financial Credit Philosophy... 2 Ability to Repay and Qualified Mortgages...

FHA Streamlined 203(k) Loan Program

Loan Program") FHA Streamlined 203(k) Loan Program 8/7/14 Overview FHA Streamlined 203(k) Program Through the Federal Housing Administration s (FHA) Streamlined 203(k) program, Borrowers can purchase or refinance their

FHA Streamlined 203(k) Loan Program 8/7/14 Overview FHA Streamlined 203(k) Program Through the Federal Housing Administration s (FHA) Streamlined 203(k) program, Borrowers can purchase or refinance their

CHAPTER 6: LOAN PURPOSES 7 CFR 3555.101

CHAPTER 6: LOAN PURPOSES 7 CFR 3555.101 6.1 INTRODUCTION SFHGLP loan funds can be used to acquire new or existing housing that will be the applicant s principal residence, and to pay costs associated with

CHAPTER 6: LOAN PURPOSES 7 CFR 3555.101 6.1 INTRODUCTION SFHGLP loan funds can be used to acquire new or existing housing that will be the applicant s principal residence, and to pay costs associated with

Disclosure Specialist Responsibilities. Lock Procedures. Processor Responsibilities. Appraisal Ordering

FHA 203K Streamline - Policies & Procedures FHA 203K Streamline will now be underwritten and funded in house. These applications should be originated in Mortgage Builder under the FHA203K-SR program code.

FHA 203K Streamline - Policies & Procedures FHA 203K Streamline will now be underwritten and funded in house. These applications should be originated in Mortgage Builder under the FHA203K-SR program code.

VA Allowable Closing Costs

VA Allowable Closing Costs VA limits the closing costs that the veteran can pay to obtain a home loan. Strict adherence to the limitations on borrower paid fees and charges is required on all VA loans.

VA Allowable Closing Costs VA limits the closing costs that the veteran can pay to obtain a home loan. Strict adherence to the limitations on borrower paid fees and charges is required on all VA loans.

Understanding 203k Loans 2 Hour Continuing Education Course Outline

1. Course overview and requirements. a. Course length of 2 hours with a 10 minute break each hour on the hour. b. Making sure all attendees have a course outline. c. There will be a 10 question test at

1. Course overview and requirements. a. Course length of 2 hours with a 10 minute break each hour on the hour. b. Making sure all attendees have a course outline. c. There will be a 10 question test at

COMMUNITY ACQUISITION REHABILITATION LOAN CARL CARL TERM SHEET AND GUIDELINES

COMMUNITY ACQUISITION REHABILITATION LOAN I. PROGRAM OBJECTIVE CARL CARL TERM SHEET AND GUIDELINES URBAN REDEVELOPMENT AUTHORITY OF PITTSBURGH PITTSBURGH COMMUNITY REINVESTMENT GROUP The main objective

COMMUNITY ACQUISITION REHABILITATION LOAN I. PROGRAM OBJECTIVE CARL CARL TERM SHEET AND GUIDELINES URBAN REDEVELOPMENT AUTHORITY OF PITTSBURGH PITTSBURGH COMMUNITY REINVESTMENT GROUP The main objective

More than 35 Mortgage Loan Officers who live and work in your neighborhood. Lending in MA, NH, RI, ME, CT & FL

Founded in 1855 More than 35 Mortgage Loan Officers who live and work in your neighborhood. Lending in MA, NH, RI, ME, CT & FL Largest servicer of mortgage loans headquartered in New England. Finances

Founded in 1855 More than 35 Mortgage Loan Officers who live and work in your neighborhood. Lending in MA, NH, RI, ME, CT & FL Largest servicer of mortgage loans headquartered in New England. Finances

Home Buyer s. Helpful Information to Find and Finance Your Next Home. www.colonialnationalmortgage.com 1-800-937-6001

Home Buyer s H A N D B O O K Helpful Information to Find and Finance Your Next Home www.colonialnationalmortgage.com 1-800-937-6001 The information herein is subject to change and is not an offer to extend

Home Buyer s H A N D B O O K Helpful Information to Find and Finance Your Next Home www.colonialnationalmortgage.com 1-800-937-6001 The information herein is subject to change and is not an offer to extend

Chapter 6. Refinancing Loans

Chapter 6. Refinancing Loans VA Pamphlet 26-7, Revised Overview In this Chapter This chapter contains the following topics. Topic Topic Name See Page 1 Interest Rate Reduction Refinancing Loans (IRRRLs)

Chapter 6. Refinancing Loans VA Pamphlet 26-7, Revised Overview In this Chapter This chapter contains the following topics. Topic Topic Name See Page 1 Interest Rate Reduction Refinancing Loans (IRRRLs)

Are you planning to use a Reverse Mortgage to Purchase a Home? Then the following checklist will be very handy.

Are you planning to use a Reverse Mortgage to Purchase a Home? Then the following checklist will be very handy. 1) The sale must be an Arm s Length Transaction which means that you must be buying from

Are you planning to use a Reverse Mortgage to Purchase a Home? Then the following checklist will be very handy. 1) The sale must be an Arm s Length Transaction which means that you must be buying from

Appraisal Standards and Guidelines chapter

Appraisal Standards and Guidelines chapter Union Capital requires appraisers and appraisal reports to meet USPAP and applicable Union Capital, FNMA, FHLMC, FHA and VA policies and requirements, as applicable.

Appraisal Standards and Guidelines chapter Union Capital requires appraisers and appraisal reports to meet USPAP and applicable Union Capital, FNMA, FHLMC, FHA and VA policies and requirements, as applicable.

Lending Guide. Section 604.02 Underwriwting Eligiblity Transactions

Continuity of Obligation A continuity of obligation is required for all refinance transactions. A continuity of obligation exists when one or more of the following occur: At least one borrower on the existing

Continuity of Obligation A continuity of obligation is required for all refinance transactions. A continuity of obligation exists when one or more of the following occur: At least one borrower on the existing

Financing Options to support Energy Efficiency & Contractors

Financing Options to support Energy Efficiency & Contractors Renovation Loan Overview Renovation Loans offer a buyer the opportunity to buy a property and close as-is, financing both the purchase and repair

Financing Options to support Energy Efficiency & Contractors Renovation Loan Overview Renovation Loans offer a buyer the opportunity to buy a property and close as-is, financing both the purchase and repair

City of Perris First Time Homebuyer Homebuyer Assistance Program (HAP) Lender Training

Lender Training") City of Perris First Time Homebuyer Homebuyer Assistance Program (HAP) Lender Training 2010 Agenda Staff Introductions HAP Program Summary HAP Program Requirements HAP Program Procedures Becoming an Approved

City of Perris First Time Homebuyer Homebuyer Assistance Program (HAP) Lender Training 2010 Agenda Staff Introductions HAP Program Summary HAP Program Requirements HAP Program Procedures Becoming an Approved

Introduction to Renovation Lending. Presented by: Jane King Freedom Mortgage

Introduction to Renovation Lending Presented by: Jane King Freedom Mortgage Agenda Renovation Lending Overview of renovation products Identifying the right borrower Identifying the right property Evaluating

Introduction to Renovation Lending Presented by: Jane King Freedom Mortgage Agenda Renovation Lending Overview of renovation products Identifying the right borrower Identifying the right property Evaluating

6176 VA IRRRL. DW0114 Page 1 of 8

6176 VA IRRRL Interest Rate The loan must be to reduce the interest rate. If refinancing an adjustable rate mortgage (ARM) loan to a fixed rate loan, an exception is made allowing the new interest rate

6176 VA IRRRL Interest Rate The loan must be to reduce the interest rate. If refinancing an adjustable rate mortgage (ARM) loan to a fixed rate loan, an exception is made allowing the new interest rate

First Mortgage Documents User Guide 139

HUD 1 Settlement Statement Line instructions General Instructions Information and amounts may be filled in by typewriter, hand printing, computer printing, or any other method producing clear and legible

HUD 1 Settlement Statement Line instructions General Instructions Information and amounts may be filled in by typewriter, hand printing, computer printing, or any other method producing clear and legible

Section 1: Loan Characteristics

Home Flex Quick Reference: Program Summary The following is an outline of the underwriting and closing requirements of New Hampshire Housing Home Flex program, which is available to lenders who have signed

Home Flex Quick Reference: Program Summary The following is an outline of the underwriting and closing requirements of New Hampshire Housing Home Flex program, which is available to lenders who have signed

Chapter 6: Refinancing Loans

VA Pamphlet 26-7, Revised Chapter 6: Refinancing Loans Chapter 6 Refinancing Loans Overview In this Chapter This chapter contains the following topics. Topic See Page 6.01 Interest Rate Reduction Refinancing

VA Pamphlet 26-7, Revised Chapter 6: Refinancing Loans Chapter 6 Refinancing Loans Overview In this Chapter This chapter contains the following topics. Topic See Page 6.01 Interest Rate Reduction Refinancing

Chapter 3. Maximum Mortgage Amounts on Refinance Transactions Table of Contents

Chapter 3, Table of Contents Chapter 3. Maximum Mortgage Amounts on Refinance Transactions Table of Contents Section A. Refinance Transaction Overview Overview... 3-A-1 1. General Information on Refinance

Chapter 3, Table of Contents Chapter 3. Maximum Mortgage Amounts on Refinance Transactions Table of Contents Section A. Refinance Transaction Overview Overview... 3-A-1 1. General Information on Refinance

All contents copyright 2009 2011 by 203KMortgageLender.com. All rights reserved. No part of this document or the related files may be republished to

All contents copyright 2009 2011 by 203KMortgageLender.com. All rights reserved. No part of this document or the related files may be republished to any website, blog, ebook etc. without prior wri en permission.

All contents copyright 2009 2011 by 203KMortgageLender.com. All rights reserved. No part of this document or the related files may be republished to any website, blog, ebook etc. without prior wri en permission.

13 DOWNPAYMENT PROGRAMS

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Home Advantage Downpayment Assistance Program can

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Home Advantage Downpayment Assistance Program can

Construction Conversion and Renovation Mortgages

Conversion and Renovation Mortgages Use this summary of requirements to help you process, underwrite and deliver Conversion and Renovation Mortgages. For complete information on Conversion and Renovation

Conversion and Renovation Mortgages Use this summary of requirements to help you process, underwrite and deliver Conversion and Renovation Mortgages. For complete information on Conversion and Renovation

THE BASICS: Andrew Allen Updated 3/24/2015 COPYRIGHT 2013 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED

R THE BASICS: Andrew Allen Updated 3/24/2015 The Formula for Success = AFR s Wholesale division is the #1 203(k) lender in the country for sponsored originations. HomeStyle Questions HomeStyle Explained

R THE BASICS: Andrew Allen Updated 3/24/2015 The Formula for Success = AFR s Wholesale division is the #1 203(k) lender in the country for sponsored originations. HomeStyle Questions HomeStyle Explained

MICHIGAN STATE HOUSING DEVELOPMENT AUTHORITY LOW INCOME HOUSING TAX CREDIT PROGRAM COST CERTIFICATION GUIDELINES TABLE OF CONTENTS

MICHIGAN STATE HOUSING DEVELOPMENT AUTHORITY LOW INCOME HOUSING TAX CREDIT PROGRAM COST CERTIFICATION GUIDELINES TABLE OF CONTENTS 1. Cost Certification Guidelines PAGE I General 1 II Identity of Interest

MICHIGAN STATE HOUSING DEVELOPMENT AUTHORITY LOW INCOME HOUSING TAX CREDIT PROGRAM COST CERTIFICATION GUIDELINES TABLE OF CONTENTS 1. Cost Certification Guidelines PAGE I General 1 II Identity of Interest

APPENDIX A TO PART 3500 INSTRUCTIONS FOR COMPLETING HUD-1 AND HUD-1A SETTLEMENT STATEMENTS; SAMPLE HUD-1 AND HUD-1A STATEMENTS

APPENDIX A TO PART 3500 INSTRUCTIONS FOR COMPLETING HUD-1 AND HUD-1A SETTLEMENT STATEMENTS; SAMPLE HUD-1 AND HUD-1A STATEMENTS The following are instructions for completing the HUD-1 settlement statement,

APPENDIX A TO PART 3500 INSTRUCTIONS FOR COMPLETING HUD-1 AND HUD-1A SETTLEMENT STATEMENTS; SAMPLE HUD-1 AND HUD-1A STATEMENTS The following are instructions for completing the HUD-1 settlement statement,

Section C. Maximum Mortgage Amounts on Streamline Refinances Overview

Section C. Maximum Mortgage Amounts on Overview In This Section This section contains the topics listed in the table below. Topic Topic Name See Page 1 General Information on 3-C-2 2 Without an Appraisal

Section C. Maximum Mortgage Amounts on Overview In This Section This section contains the topics listed in the table below. Topic Topic Name See Page 1 General Information on 3-C-2 2 Without an Appraisal

New Home Buyer's Guide

New Home Buyer's Guide Contents Steps for buying a new, natural gas home p. 3 Mortgage payment calculator p. 4 Mortgage qualification guide p. 5 Mortgage application checklist p. 6 Real estate glossary

New Home Buyer's Guide Contents Steps for buying a new, natural gas home p. 3 Mortgage payment calculator p. 4 Mortgage qualification guide p. 5 Mortgage application checklist p. 6 Real estate glossary

We have a plan to make yours easier. The Citizens Guide to Construction-to-Permanent Financing

We have a plan to make yours easier. The Citizens Guide to Construction-to-Permanent Financing Table of Contents How it works 3 Getting started 4 The construction-to-permanent loan process 5 The construction

We have a plan to make yours easier. The Citizens Guide to Construction-to-Permanent Financing Table of Contents How it works 3 Getting started 4 The construction-to-permanent loan process 5 The construction

Section B. Maximum Mortgage Amounts on No Cash Out/Cash Out Refinance Transactions Overview

Section B. Maximum Mortgage Amounts on No Cash Out/Cash Out Refinance Transactions Overview In This Section This section contains the topics listed in the table below. Topic Topic Name See Page 1 No Cash

Section B. Maximum Mortgage Amounts on No Cash Out/Cash Out Refinance Transactions Overview In This Section This section contains the topics listed in the table below. Topic Topic Name See Page 1 No Cash

RESIDENCE TRANSACTION EXPENSES - HOME PURCHASE

Items Payable In Connection With Loan: (Section 800 on HUD-I) Loan Origination Charge Line 801 The FTR allows for up to 1% of the loan amount to be reimbursed if lender charges are assessed in lieu of

Items Payable In Connection With Loan: (Section 800 on HUD-I) Loan Origination Charge Line 801 The FTR allows for up to 1% of the loan amount to be reimbursed if lender charges are assessed in lieu of

Fifth Third Home Buying Guide. A Guide to Residential Home Buying.

Fifth Third Home Buying Guide A Guide to Residential Home Buying. Important Contacts and Numbers. Use this page to record important information as you move through the homebuying process. Realtor/Builder

Fifth Third Home Buying Guide A Guide to Residential Home Buying. Important Contacts and Numbers. Use this page to record important information as you move through the homebuying process. Realtor/Builder

CITY OF MURFREESBORO AFFORDABLE HOUSING ASSISTANCE PROGRAM POLICIES AND PROCEDURES

CITY OF MURFREESBORO AFFORDABLE HOUSING ASSISTANCE PROGRAM POLICIES AND PROCEDURES 100. Purpose The Murfreesboro Affordable Housing Assistance Program (the Program) encourages homeownership for low-income,

CITY OF MURFREESBORO AFFORDABLE HOUSING ASSISTANCE PROGRAM POLICIES AND PROCEDURES 100. Purpose The Murfreesboro Affordable Housing Assistance Program (the Program) encourages homeownership for low-income,

Name of course: Residential Construction Site Management (RCSM) Level 1

Level 1") Name of course: Residential Construction Site Management (RCSM) Level 1 Core (required courses) or Optional (elective course): Required Delivery Method: This is an online course only with no classroom

Name of course: Residential Construction Site Management (RCSM) Level 1 Core (required courses) or Optional (elective course): Required Delivery Method: This is an online course only with no classroom

NMLS ID: 110139 AmeriFirst Home Mortgage 800.466.5626

How do you turn a fixer upper into your dream home? The Solution the FHA 203(k) Loan! The purchase of a house that needs repair is often a catch-22 situation, because the bank won't lend the money to buy

How do you turn a fixer upper into your dream home? The Solution the FHA 203(k) Loan! The purchase of a house that needs repair is often a catch-22 situation, because the bank won't lend the money to buy

How To Buy A Home

HOME BUYER S H A N D B O O K Helpful Information To Find and Finance Your Next Home Buying a home is one of the most important financial decisions you'll ever make. A home can be an excellent investment

HOME BUYER S H A N D B O O K Helpful Information To Find and Finance Your Next Home Buying a home is one of the most important financial decisions you'll ever make. A home can be an excellent investment

MORTGAGE TERMS. Assignment of Mortgage A document used to transfer ownership of a mortgage from one party to another.

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

Section 2.08 - Jumbo Solution Second Mortgage

- In This Product Description This product description contains the following topics: Overview... 2 Related Bulletins... 3 Loan Terms... 4 Assumptions... 4 Eligible First and Second Mortgage Products...

- In This Product Description This product description contains the following topics: Overview... 2 Related Bulletins... 3 Loan Terms... 4 Assumptions... 4 Eligible First and Second Mortgage Products...

FHA MIP Rate and Duration Changes starting April 1, 2013 and June 3, 2013 By Bahman Davani, Member of CCAR s REALTOR /Lender Committee

FHA MIP Rate and Duration Changes starting April 1, 2013 and June 3, 2013 By Bahman Davani, Member of CCAR s REALTOR /Lender Committee The following changes to FHA Mortgage Insurance Premiums (MIP) will

FHA MIP Rate and Duration Changes starting April 1, 2013 and June 3, 2013 By Bahman Davani, Member of CCAR s REALTOR /Lender Committee The following changes to FHA Mortgage Insurance Premiums (MIP) will

The Reverse Mortgage Opportunity. Today s Solution to your Peace of Mind

The Reverse Mortgage Opportunity Today s Solution to your Peace of Mind The 2009 Retirement Environment 2008 Market downturn Net worth losses portfolio restrictions Age restrictions on employment Travel

The Reverse Mortgage Opportunity Today s Solution to your Peace of Mind The 2009 Retirement Environment 2008 Market downturn Net worth losses portfolio restrictions Age restrictions on employment Travel

CHAPTER 5. ALLOWABLE COSTS TO BE REPORTED ON FORM HUD-92330-A

CHAPTER 5. ALLOWABLE COSTS TO BE REPORTED ON FORM HUD-92330-A 5-1. DATE TO WHICH FORM HUD-92330-A IS COMPUTED. Form HUD-92330-A is completed to reflect the general contractor's cost of construction as

CHAPTER 5. ALLOWABLE COSTS TO BE REPORTED ON FORM HUD-92330-A 5-1. DATE TO WHICH FORM HUD-92330-A IS COMPUTED. Form HUD-92330-A is completed to reflect the general contractor's cost of construction as

Buying a Home. Do you know of any serious physical defects in the property? If so, how can you protect yourself against such defects?

Buying a Home What should I consider when buying a home? Document last updated 12/23/2014. For most people, a home purchase is the biggest single investment of their lives. It is, therefore, extremely

Buying a Home What should I consider when buying a home? Document last updated 12/23/2014. For most people, a home purchase is the biggest single investment of their lives. It is, therefore, extremely

What to Expect Next. A Step-By-Step Guide To Building Your New Home

What to Expect Next A Step-By-Step Guide To Building Your New Home Step 1: Homeowner signs the purchase agreement Step 4: Mortgage Company issues homeowner a commitment letter Step 2: Homeowner applies

What to Expect Next A Step-By-Step Guide To Building Your New Home Step 1: Homeowner signs the purchase agreement Step 4: Mortgage Company issues homeowner a commitment letter Step 2: Homeowner applies

The Chase Guaranteed Rural Housing Refinance Program Features

PROGRAM ELIGIBILITY Borrower Eligibility In order to be eligible for a Rural Development guaranteed loan, the Borrowers adjusted household income cannot exceed the maximum allowable income limit set forth

PROGRAM ELIGIBILITY Borrower Eligibility In order to be eligible for a Rural Development guaranteed loan, the Borrowers adjusted household income cannot exceed the maximum allowable income limit set forth

720-206-4539 Mark Allen Schmidt Colorado Mortgage Broker & Educator HECM for Purchase Consultant

720-206-4539 Mark Allen Schmidt Colorado Mortgage Broker & Educator HECM for Purchase Consultant A Summary Of How A HECM for Purchase Works (Home Equity Conversion Mortgage) A person 62+ years old can

720-206-4539 Mark Allen Schmidt Colorado Mortgage Broker & Educator HECM for Purchase Consultant A Summary Of How A HECM for Purchase Works (Home Equity Conversion Mortgage) A person 62+ years old can

Borrower Fees and Charges and the VA Funding Fee

VA Pamphlet 26-7, Revised Chapter 8: Borrower Fees and Charges and the VA Funding Fee Chapter 8 Borrower Fees and Charges and the VA Funding Fee Overview Introduction This chapter contains information

VA Pamphlet 26-7, Revised Chapter 8: Borrower Fees and Charges and the VA Funding Fee Chapter 8 Borrower Fees and Charges and the VA Funding Fee Overview Introduction This chapter contains information

Introduction to the Fannie Mae HomeStyle Renovation Mortgage. Presented by Damon Richardson, Program Specialist - American Financial Resources, Inc.

Introduction to the Fannie Mae HomeStyle Renovation Mortgage Presented by Damon Richardson, Program Specialist - American Financial Resources, Inc. About the Presenter With 12 years of mortgage industry

Introduction to the Fannie Mae HomeStyle Renovation Mortgage Presented by Damon Richardson, Program Specialist - American Financial Resources, Inc. About the Presenter With 12 years of mortgage industry

EXPAND HOMEOWNERSHIP PROGRAM

EXPAND HOMEOWNERSHIP PROGRAM Administrator Guidelines Published: March 12, 2015 Revised March 13, 2015 Updates are shown on Page 4! FANO EXPAND HOMEOWNERSHIP PROGRAM - Administrator Guidelines Page 2 Time

EXPAND HOMEOWNERSHIP PROGRAM Administrator Guidelines Published: March 12, 2015 Revised March 13, 2015 Updates are shown on Page 4! FANO EXPAND HOMEOWNERSHIP PROGRAM - Administrator Guidelines Page 2 Time

CHAPTER 4. COMPLETING FORM HUD-92330, MORTGAGOR'S CERTIFICATE OF ACTUAL COST

CHAPTER 4. COMPLETING FORM HUD-92330, MORTGAGOR'S CERTIFICATE OF ACTUAL COST 4-1. GENERAL INFORMATION AND DESIRED FORMAT. A. Heading of Form. Self-explanatory. B. Columns A, B, and C in the body of the

CHAPTER 4. COMPLETING FORM HUD-92330, MORTGAGOR'S CERTIFICATE OF ACTUAL COST 4-1. GENERAL INFORMATION AND DESIRED FORMAT. A. Heading of Form. Self-explanatory. B. Columns A, B, and C in the body of the

UMB Mortgage Solutions. Home Buying 101

UMB Mortgage Solutions Home Buying 101 1 Agenda Are You Ready to Buy a Home? Selecting a Lender Mortgage Loans Getting Started Home Checklist Purchase Contract Questions 2 Home buying Terms Mortgage Lender

UMB Mortgage Solutions Home Buying 101 1 Agenda Are You Ready to Buy a Home? Selecting a Lender Mortgage Loans Getting Started Home Checklist Purchase Contract Questions 2 Home buying Terms Mortgage Lender

THE BASICS: 203(k) Limited. FHA Limited 203(k) ssss. Andrew Allen Updated 10/20/15

Limited. FHA Limited 203(k) ssss. Andrew Allen Updated 10/20/15") SLIDE 1 R THE BASICS: Limited 203(k) ssss FHA Limited 203(k) Andrew Allen Updated 10/20/15 SLIDE 2 FHA Limited 203(k) Questions Limited 203(k) Explained What is the FHA Limited 203(k)s Loan Program? What

SLIDE 1 R THE BASICS: Limited 203(k) ssss FHA Limited 203(k) Andrew Allen Updated 10/20/15 SLIDE 2 FHA Limited 203(k) Questions Limited 203(k) Explained What is the FHA Limited 203(k)s Loan Program? What

203K Streamline. Help qualified borrowers purchase or refinance AND renovate..with a single loan!

203K Streamline Help qualified borrowers purchase or refinance AND renovate..with a single loan! Why FHA 203K Streamline Offers a solution that helps borrowers obtain financing that covers both the acquisition

203K Streamline Help qualified borrowers purchase or refinance AND renovate..with a single loan! Why FHA 203K Streamline Offers a solution that helps borrowers obtain financing that covers both the acquisition

Enhancements to Streamlined (k) Limited Repair Program

Limited Repair Program") U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER December 29, 2005 MORTGAGEE LETTER 2005-50 TO: ALL APPROVED MORTGAGEES

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER December 29, 2005 MORTGAGEE LETTER 2005-50 TO: ALL APPROVED MORTGAGEES

HUD-1. GFE vs. HUD-1: HUD-1 Introduction:

HUD-1 GFE vs. HUD-1: The new HUD-1 Settlement Statement (the HUD-1 ) is designed to allow the borrower to compare the document with the Good Faith Estimate (the GFE ) received before closing, including

HUD-1 GFE vs. HUD-1: The new HUD-1 Settlement Statement (the HUD-1 ) is designed to allow the borrower to compare the document with the Good Faith Estimate (the GFE ) received before closing, including

How To Get A Home Equity Conversion Mortgage For Purchase

An Introduction to Home Equity Conversion Mortgage (HECM) for Purchase Loan Home Buying in Reverse What is a HECM for Purchase Loan? A Home Equity Conversion Mortgage (HECM) for Purchase is an innovative

An Introduction to Home Equity Conversion Mortgage (HECM) for Purchase Loan Home Buying in Reverse What is a HECM for Purchase Loan? A Home Equity Conversion Mortgage (HECM) for Purchase is an innovative

`2 TERMS AND CONDITIONS

`2 TERMS AND CONDITIONS Each House Key Program Mortgage Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate FHA 203(b), 234 (c), HUD 184, VA, USDA Rural Development, and Conventional

`2 TERMS AND CONDITIONS Each House Key Program Mortgage Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate FHA 203(b), 234 (c), HUD 184, VA, USDA Rural Development, and Conventional

Guide to FHA Streamline Refinances. By J.J. Sawicki, CMP AVP Third Party Lending/Merrimack Mortgage

Guide to FHA Streamline Refinances By J.J. Sawicki, CMP AVP Third Party Lending/Merrimack Mortgage What is a streamline refinance? The FHA streamline refinance has become an increasingly attractive option

Guide to FHA Streamline Refinances By J.J. Sawicki, CMP AVP Third Party Lending/Merrimack Mortgage What is a streamline refinance? The FHA streamline refinance has become an increasingly attractive option

Chapter 7. Mortgage Insurance Premiums (MIPs) Table of Contents

Table of Contents") HUD 4155.2 Chapter 7, Table of Contents Chapter 7. Mortgage Insurance Premiums (MIPs) Table of Contents Chapter 7. Mortgage Insurance Premiums (MIPs) 1. Types of MIPs... 7-1 2. Up Front Mortgage Insurance

HUD 4155.2 Chapter 7, Table of Contents Chapter 7. Mortgage Insurance Premiums (MIPs) Table of Contents Chapter 7. Mortgage Insurance Premiums (MIPs) 1. Types of MIPs... 7-1 2. Up Front Mortgage Insurance