Issue Brief: Wyoming Medical Liability Insurance Company Summary

|

|

|

- Brendan Nicholson

- 10 years ago

- Views:

Transcription

1 04IB007 Issue Brief: Wyoming Medical Liability Insurance Company Summary June 2004 by: Matthew M. Sackett, Associate Research Analyst PURPOSE Provide a summary of the major insurance companies covering medical malpractice in the state of Wyoming, including a history of financial and settlement data. RESULTS IN BRIEF In the recent past, The Doctors Company (TDC) and OHIC Insurance Company (OHIC) have been the two major participants in the Wyoming medical malpractice market with a few other companies insuring a small number of physicians. OHIC's decision in March 2004 to no longer insure Wyoming physicians will change the overall structure of Wyoming's medical malpractice market. Utah Medical Insurance Association (UMIA), which has had a small presence in Wyoming since the late 90's, has been dramatically increasing its business in Wyoming over the last several months. Testimony from UMIA indicates continued expansion is expected in the future, although available capital may be a limiting factor. A few other companies also have a small share in the market and any interest in expanding presence in Wyoming is unknown. Overall, the net income of these companies has been relatively modest, and in fact, occasionally characterized by losses. For the most part, OHIC, TDC, and UMIA have had a net underwriting loss in the last 10 years, accounting for all business lines in all states. This means the premiums written have not covered the expenses during the year, which is regularly the case with insurance companies. Furthermore, TDC and OHIC have had a negative total net income over the last two years, which means underwriting income, when combined with other income sources, primarily investment income, have not sufficiently covered all expenses. UMIA has had positive net income over the last five years. The following information was taken from the three major insurance companies' audited annual reports over the last three years. LSO has not independently verified the accuracy of this data, and thus, the following conclusions are based solely on the information provided. THE DOCTORS COMPANY The Doctors Company (TDC) is owned by TDC Group. TDC Group wholly owns six other subsidiaries which include: The Doctors Management Company, Bernard Warschaw Insurance Sales Agency, Professional Underwriters Liability Insurance Company, The Doctors Company Insurance Services, The Doctors Life Insurance Company, and Underwriter for the Professions Insurance Company. TDC has written policies in every state plus Guam. In 2002, TDC insured percent of the Wyoming market. TDC's premium rates are comparably higher than OHIC's rates in Wyoming. OHIC OHIC Insurance Company is a subsidiary of Medical Liability Mutual Insurance Company (MLMIC). OHIC had the largest percent of Wyoming's market in 2002, providing insurance to percent of the Wyoming market. OHIC announced its intention to withdraw from the state in March 2004, leaving a large gap in coverage for other medical malpractice insurance companies to fill over the next several months. OHIC was insuring physicians in roughly 14 states but has WYOMING LEGISLATIVE SERVICE OFFICE 213 State Capitol Cheyenne, Wyoming TELEPHONE (307) FAX (307) [email protected] WEBSITE

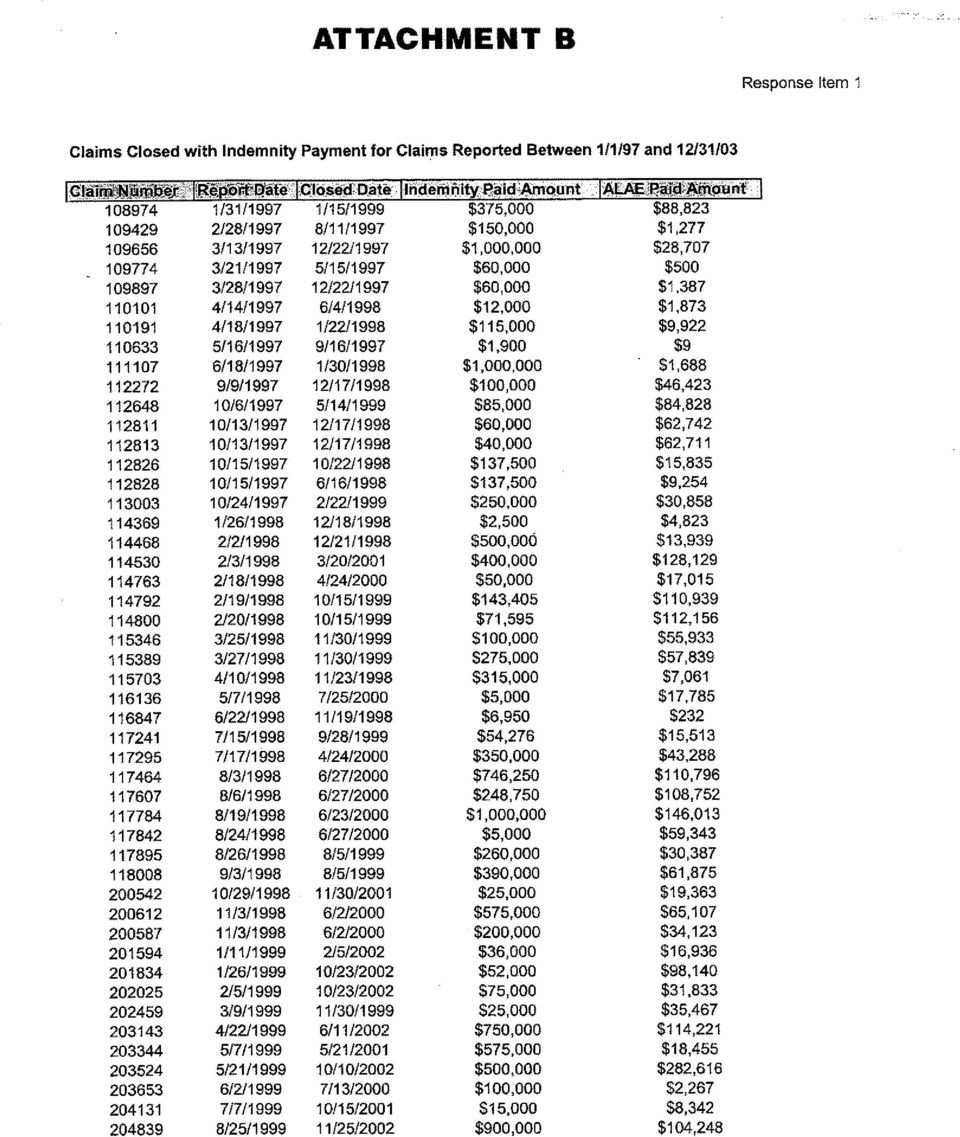

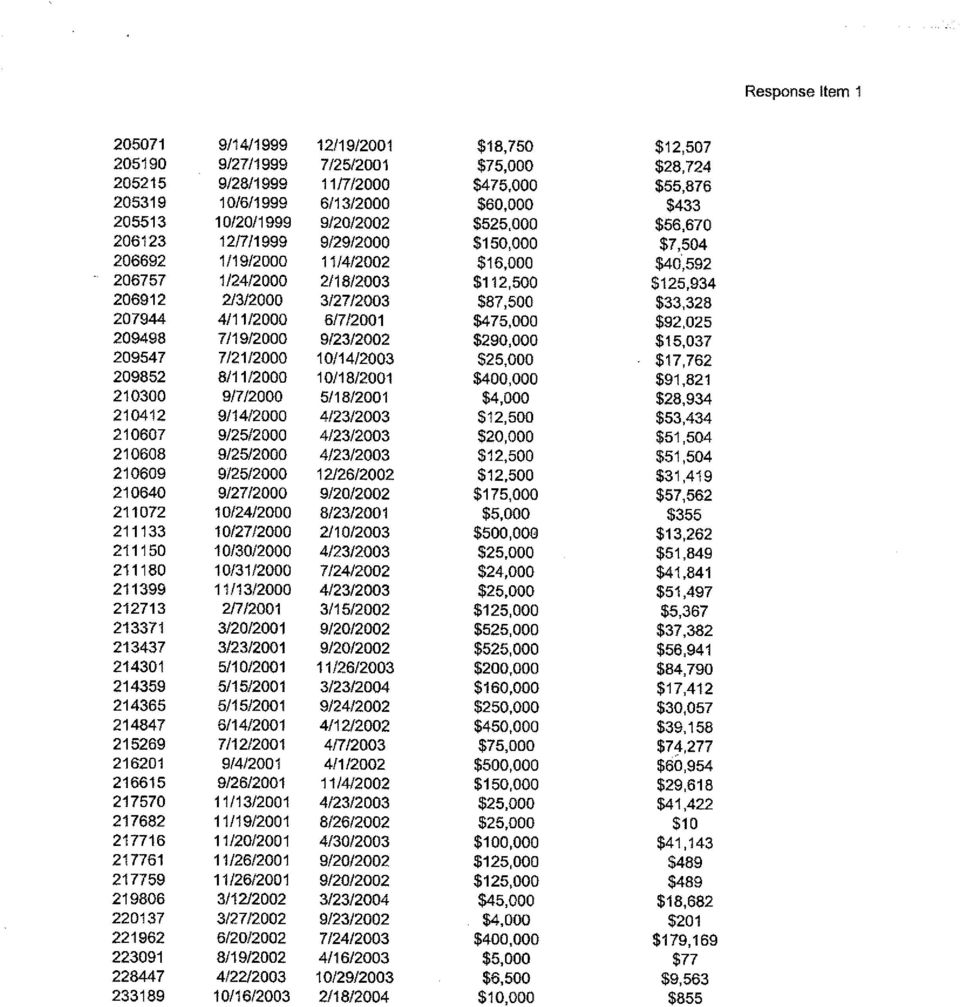

2 PAGE 2 OF 4 decided to withdraw from all but its home state of Ohio. UMIA Utah Medical Insurance Association, unlike TDC and OHIC, is a wholly owned company based in Salt Lake City, Utah. UMIA has historically written policies throughout the Rocky Mountain Region, including Idaho, Montana, Utah and Wyoming. They have had a relatively small presence in Wyoming's medical malpractice insurance market with only 1.23 percent of the market share in 2002, but UMIA has recently been increasing its presence substantially. This growth of new business is expected to continue given the departure of OHIC, according to several sources. Specifically, in discussions with several hospital personnel around the state, it appears that UMIA is providing more coverage and trying to increase its Wyoming market. FINANCIAL STATEMENTS Within the limits of our basis for analysis, in the last two years, TDC and OHIC have had negative net income (net loss). This is illustrated in Attachment A, which shows selected financial statistics over a 10-year history for each company. It should be noted that this is not Wyoming specific data, but it reflects the performance of the entire company, including all lines of insurance. It appears the net underwriting losses have been so large that the premium and investment income has not been able to cover those losses in all years. Over the 10-year history, TDC had an underwriting loss in all 10 years and OHIC had a loss in 8 of the last 10 years. TDC had a negative overall net income in two years and OHIC in three of those years. UMIA, whose five-year history is also provided in Attachment A, has had an overall positive net income every year, with a net underwriting loss in all five years. Over the last few years, there has been a drop in investment income for both TDC and OHIC. This could be a contributing factor to its overall loss in net income for the last two years. Knowledgeable parties indicate that the insurance industry is cyclical in nature, if one accepts this theory; peaks and valleys in investment income would be expected. UMIA's investment income has been relatively steady over the five-year history, considering the natural fluctuations in market returns. Determining the extent to which the attacks of September 11, 2001 impacted the investment performance of TDC, OHIC, or UMIA is difficult. There do not appear to be outstanding deviations from the investment income trend specifically identifiable in 2001 data. That is, there are no extraordinary dips in the trend data. The recent decline in investment income can most likely be attributed to the overall poorly performing financial markets and sluggish economy as a whole. It appears that TDC and OHIC have not been profitable over the last several years because of increased expenditures and overall declining investment income. On the other hand, UMIA has been profitable despite fluctuations in investment income. SETTLEMENTS, VERDICTS AND EXPENSES A summary of OHIC, UMIA and TDC's medical malpractice claim settlements and costs are shown in the following three tables. TDC and UMIA have provided very detailed information, while OHIC provided annual summaries. The settlement data in more recent years has an increasing chance of being adjusted upwards as new claims are filed. It should be noted that because UMIA has had a limited presence in Wyoming, it does not have a well-developed claims history. TDC settled all of its claims without going to trial for the data provided from January 1997 through December The average time from the reporting date to the closing date over those six years was 574 days. The average number of claims was 12.7 per year. During this period, TDC has incurred total settlement costs of $23,240,639 in Wyoming, which includes all settlement amounts and expenses used in defense against the claims, such as lawyer's fees. This amounts to an average cost per year of $3,320,091. The six-year average cost per claim is $261,131. These can be seen in Table 1. It should be noted that these numbers are subject to WYOMING LEGISLATIVE SERVICE OFFICE 213 State Capitol Cheyenne, Wyoming TELEPHONE (307) FAX (307) [email protected] WEBSITE

3 PAGE 3 OF 4 change with the possibility of more claims being settled, cases being tried, and expenses being incurred, especially for the more recent years. (See Attachment B for the full detail of settlement data from TDC.) Table 1. The Doctors Company Historical Settlement Data TOTALS Average Cost Indemnity Amount $ 3,583,900 $ 5,723,726 $ 4,331,750 $ 2,196,500 $ 3,000,000 $ 409,000 $ 16,500 $ 19,244,876 $ 2,751,625 ALAE Paid $ 446,837 $ 1,220,411 $ 874,239 $ 831,297 $ 417,337 $ 178,724 $ 10,418 $ 3,968,845 $ 568,466 Total Settlement Costs $ 4,030,737 $ 6,944,137 $ 5,205,989 $ 3,027,797 $ 3,417,337 $ 587,724 $ 26,918 $ 23,240,639 $ 3,320, Average Average Cost Per Claim $ 251,921 $ 315,643 $ 325,374 $ 178,106 $ 262,872 $ 195,908 $ 13,459 $ 261,131 Average Days to Settle Number of Claims Source: TDC Documents, 6/18/2004. Notes: (1) Settlement data in more recent years are increasingly likely to be adjusted upward as new claims are filed. (2) ALAE is the allocated loss adjustment expense. In 1994, OHIC had $90,000 in verdict(s) charges; all other years included only settlements, which can be seen in Table 2. It is not known if the verdict amount shown in 1994 was for one claim or more than one claim. The total expense for OHIC from 1991 through 2002 was almost $24 million, with an average yearly expense of $1,983,505. There was no data provided regarding the number of claims this represented or how long it took to close each claim. Table 2. OHIC Historical Settlement & Claims Data Year Settlements Verdicts Legal Exp. Other Exp. Total by Year 1991 $ 9,034 $ - $ 142,963 $ 43,348 $ 195, $ 87,208 $ - $ 31,381 $ 9,986 $ 128, $ 360,000 $ - $ 70,296 $ 25,102 $ 455, $ 1,741,892 $ 90,000 $ 478,121 $ 199,525 $ 2,509, $ 288,420 $ - $ 181,072 $ 62,529 $ 532, $ 5,546,892 $ - $ 948,437 $ 604,762 $ 7,100, $ 2,501,109 $ - $ 836,942 $ 384,696 $ 3,722, $ 910,973 $ - $ 476,239 $ 183,891 $ 1,571, $ 2,233,946 $ - $ 1,145,831 $ 485,612 $ 3,865, $ 1,783,030 $ - $ 463,513 $ 190,782 $ 2,437, $ 311,176 $ - $ 338,534 $ 231,884 $ 881, $ 215,000 $ - $ 120,669 $ 67,267 $ 402,936 Total $ 15,988,680 $ 90,000 $ 5,233,998 $ 2,489,384 $ 23,802,062 Average of Total Yearly Expense $ 1,983,505 Source: OHIC Documents 1/16/2004 UMIA has very little claims data available because of its limited presence in Wyoming, with approximately one percent of the market in Table 3 shows the claims history from 2002 through There are only five total claims; one of which has been closed with no indemnity paid and $6,039 in expenses. The other claims have not been closed so the final expense values cannot be determined accurately. These details are reflected below in Table 3. Again, it should also be noted that the data in more recent years is more likely to be adjusted upwards as new claims are filed. Date Reported Table 3. UMIA Claims History Date Closed Indemnity Paid Indemnity Reserve Expense Paid Expense Reserve $ $ 11/18/ $ 10,000 $ 11,252 25,000 Total - $ 10,000 $ 11,252 25,000 1/2/2003 8/7/ $ - $ 6,039 $ 6,039 1/13/ $ 500,000 $ 155,001 $ 200,000 1/28/ $ 10,000 $ 11,373 $ 25,000 Total - $ 510,000 $ 172,413 $ 231,039 5/4/ $ 25,000 $ - $ 8,500 Total - $ 25,000 $ - $ 8,500 Grand Totals $ 545,000 $ 183,665 $ 264,539 Source: UMIA documents, Note: These claims are grouped by Date Reported. WYOMING LEGISLATIVE SERVICE OFFICE 213 State Capitol Cheyenne, Wyoming TELEPHONE (307) FAX (307) [email protected] WEBSITE

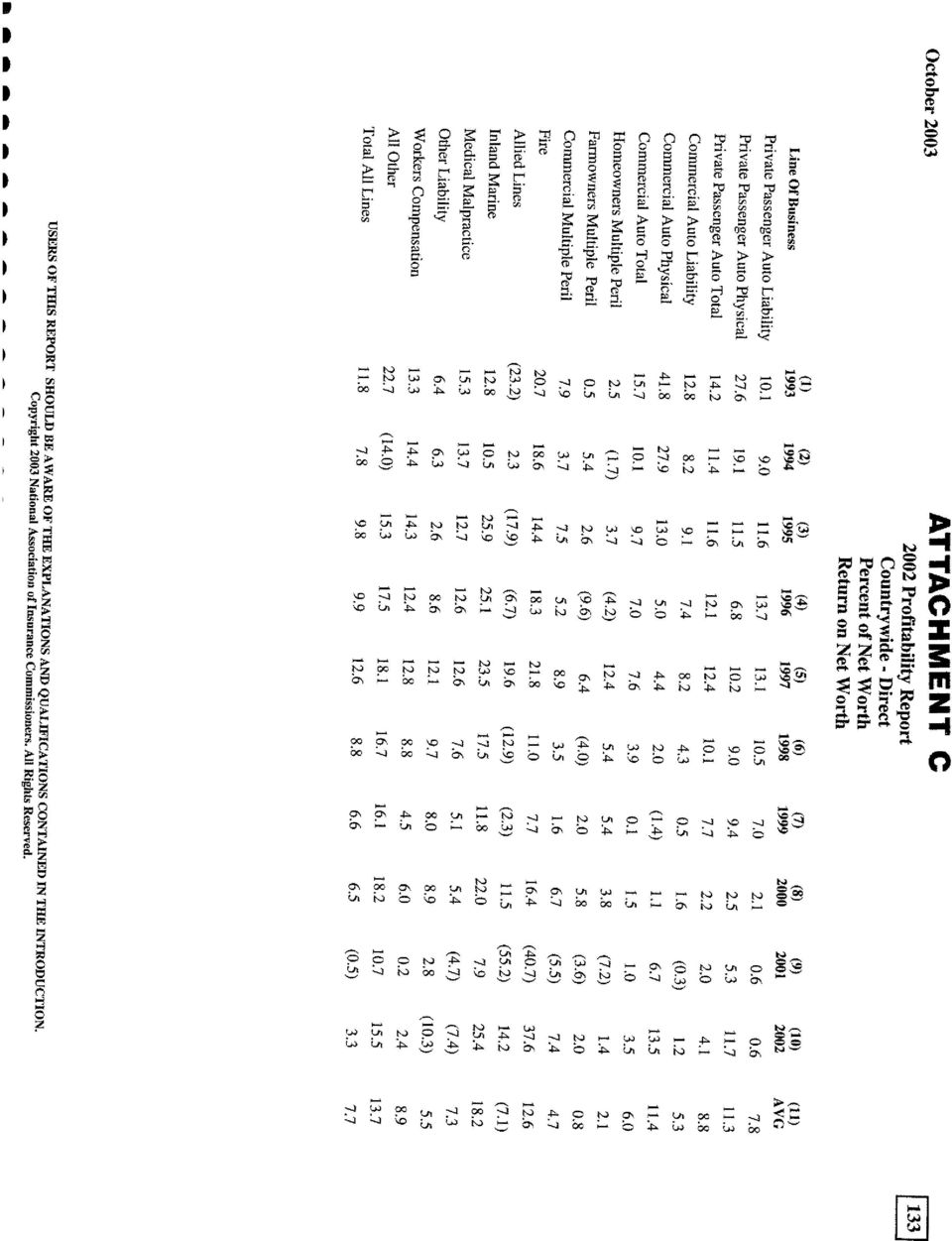

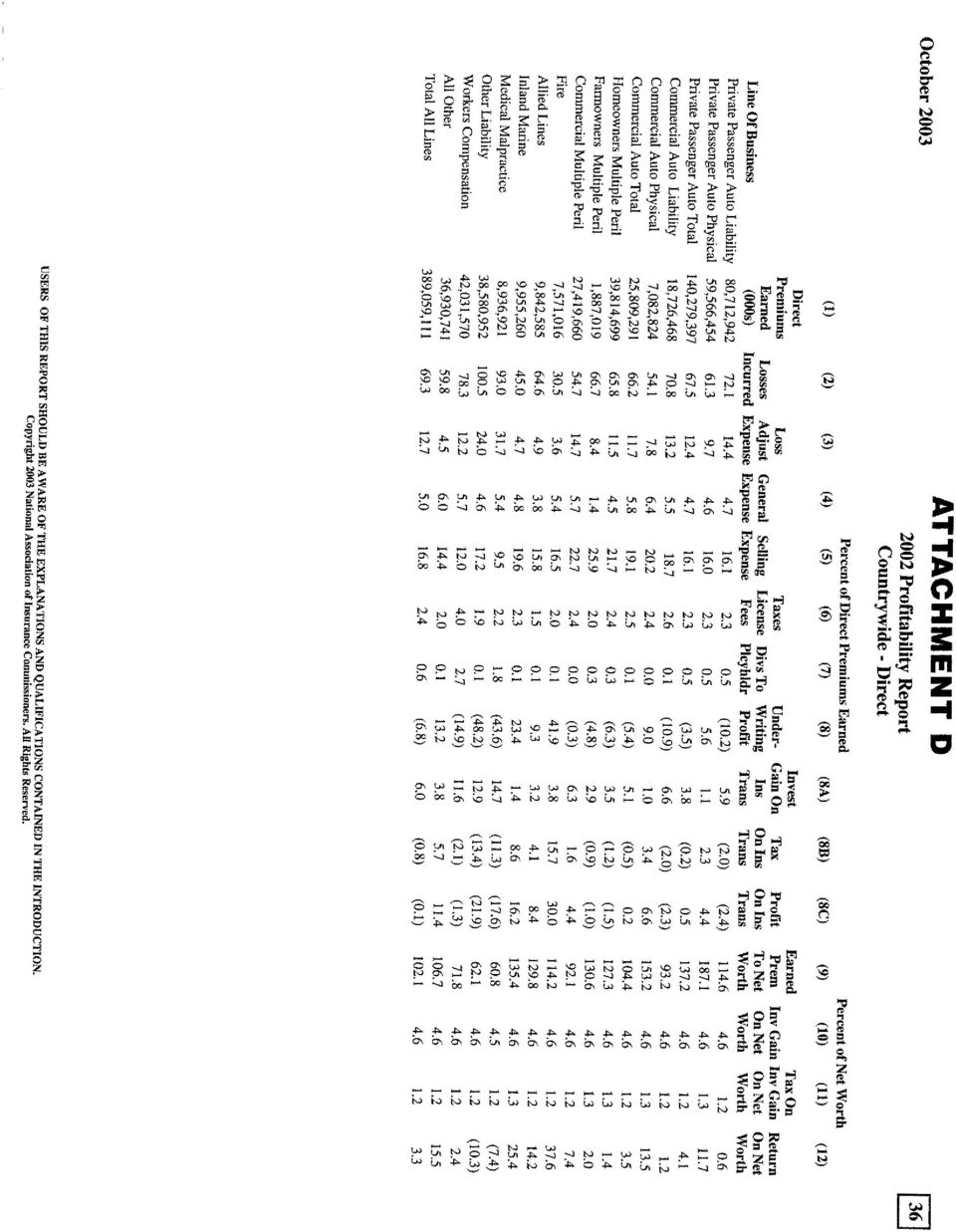

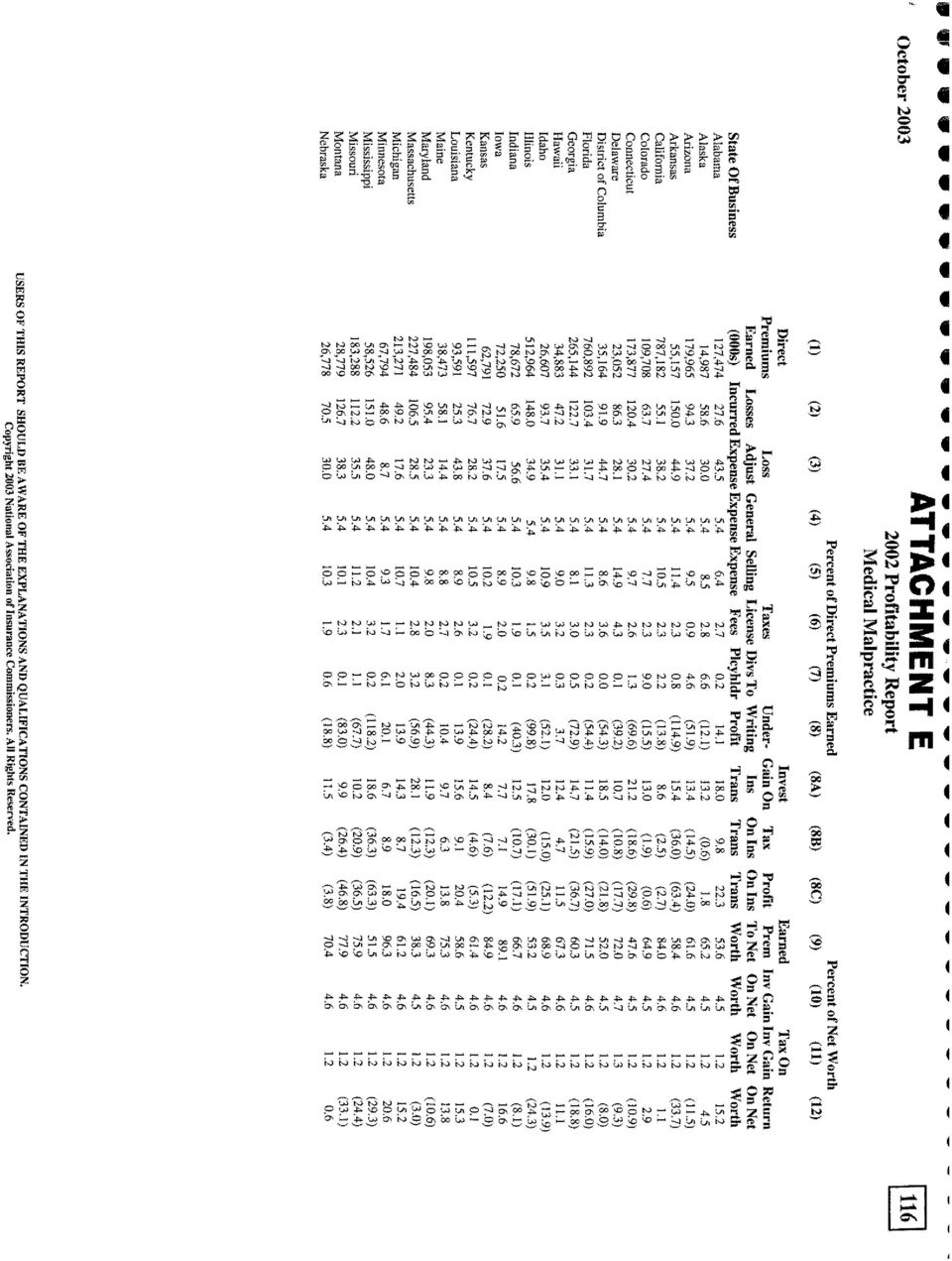

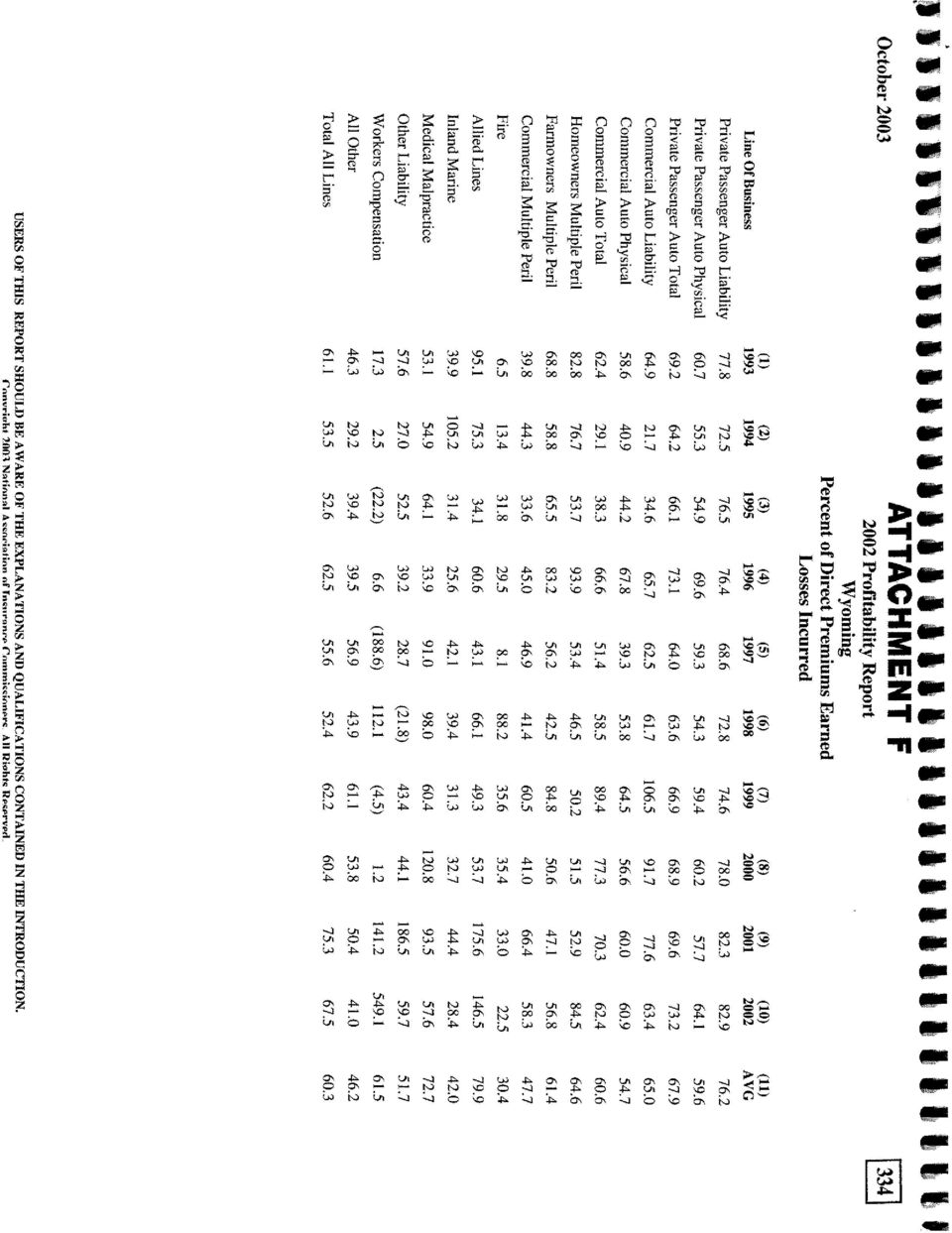

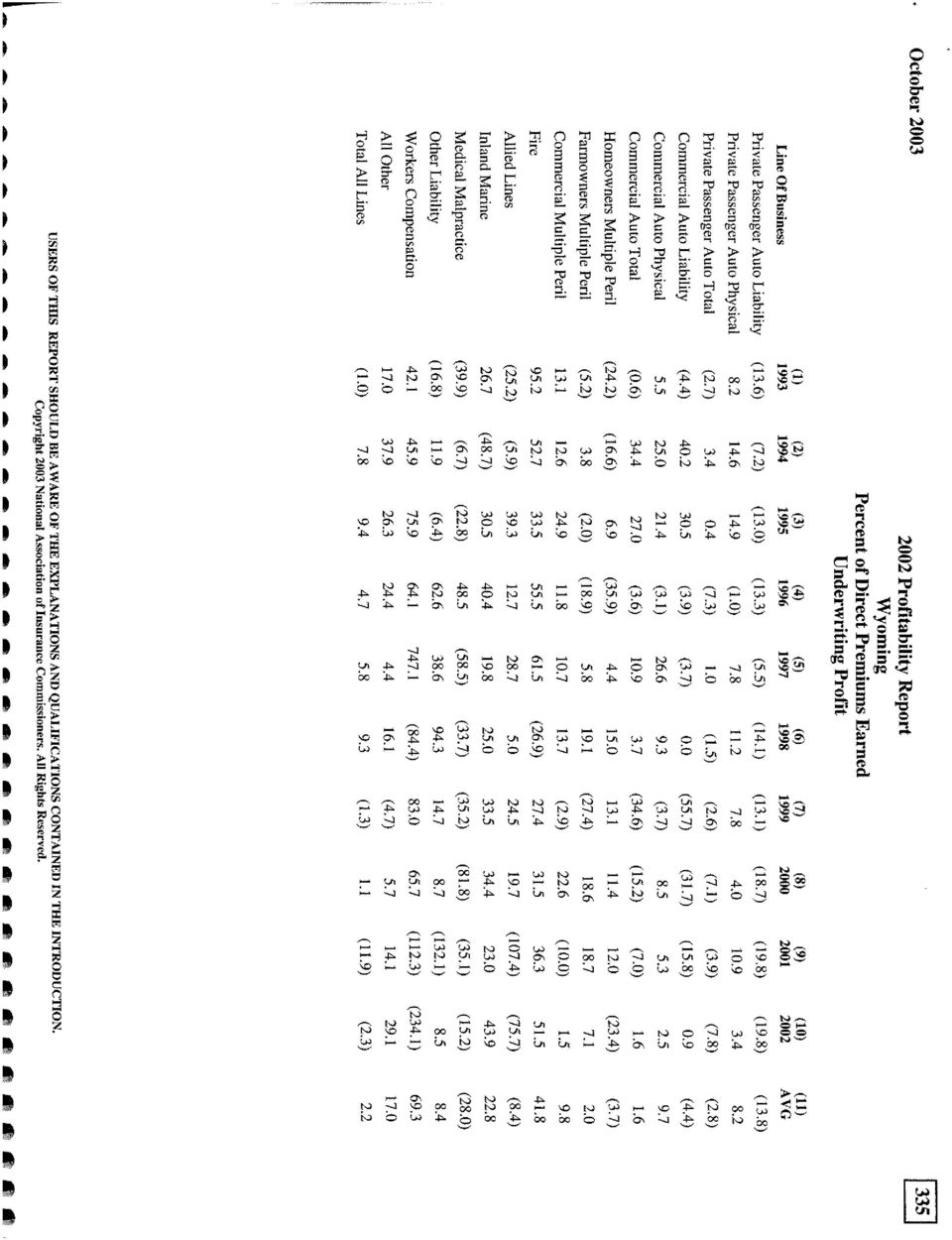

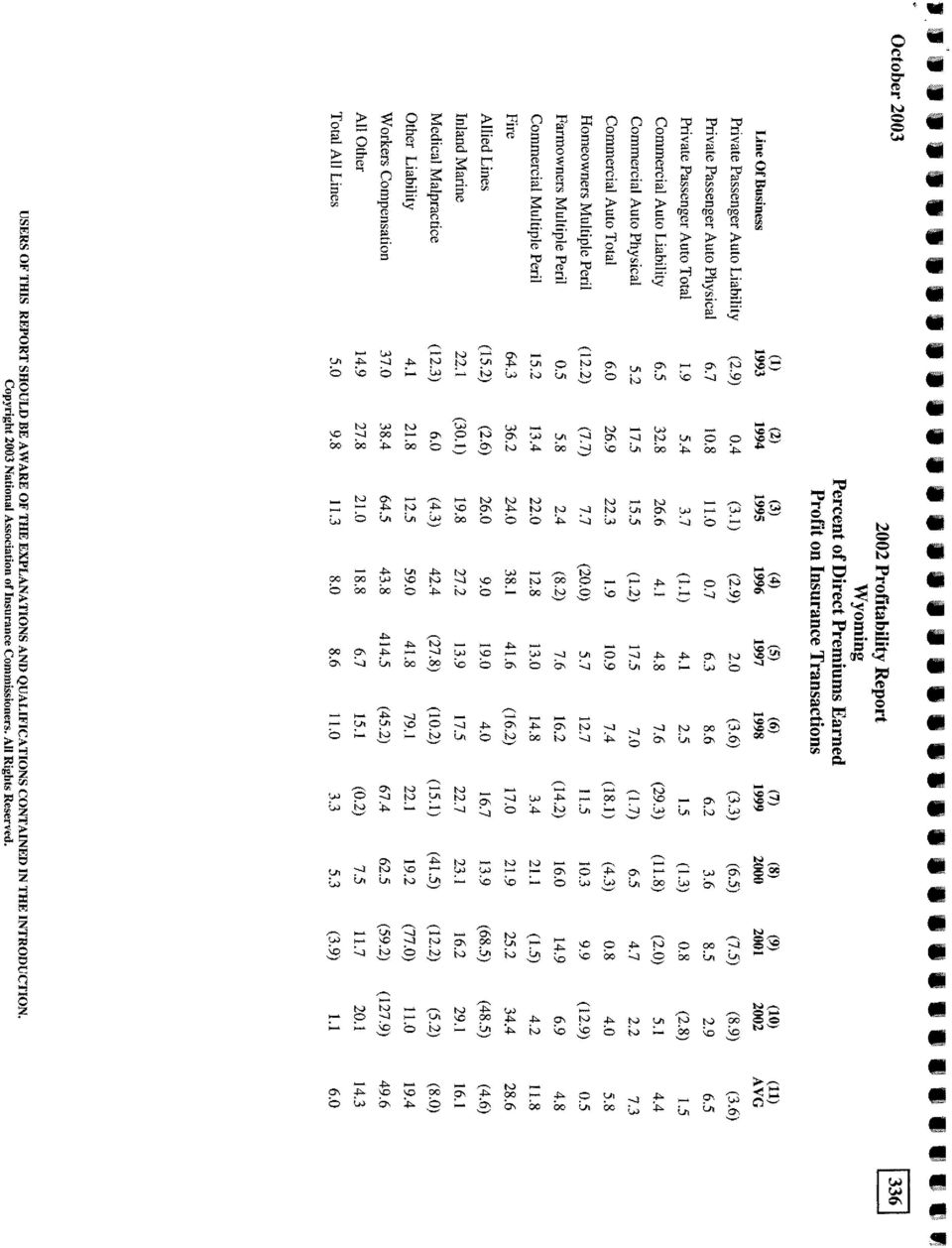

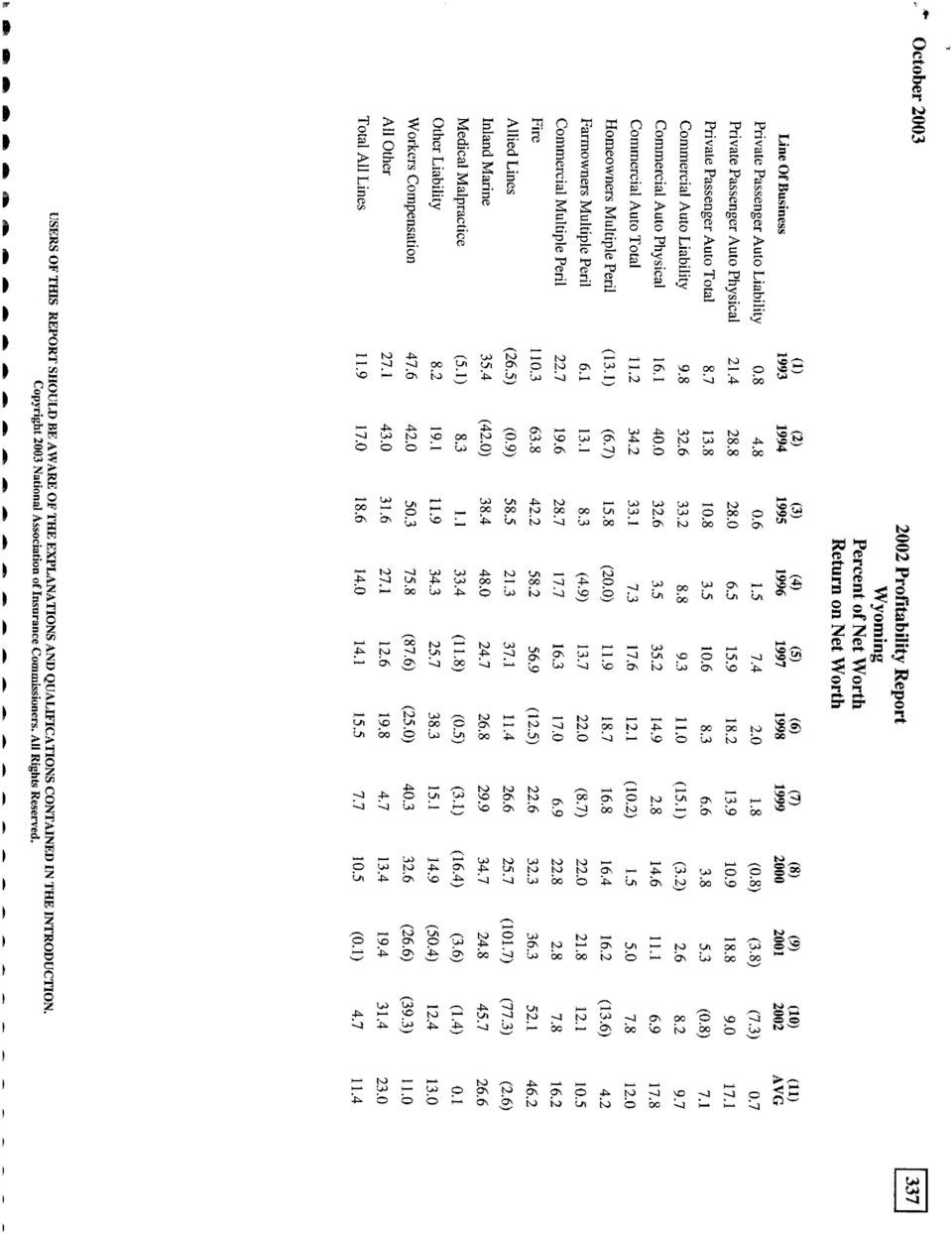

4 PAGE 4 OF 4 GENERAL INSURANCE INFORMATION According the Nation Association of Insurance Commissioners (NAIC) Profitability by Line by State report for the year 2002, the medical malpractice insurance industry has not been profitable in the last two years countrywide. There has been a steady decline in the return on net worth over the last 10 years and a negative return on net worth for the last two years. This data is illustrated in Attachment C. According to the same report, last year medical malpractice was one of two lines of property and casualty insurance that had a negative return on net worth, the other line being "other liability". Attachment D shows the nationwide direct premiums earned for all lines of insurance and the different expenses and transactions incurred as a percent of those direct premiums. It also shows the overall return on net worth as a percentage of the direct premiums earned. This shows more specifically where the large expenses and overall losses come from, as well as the overall returns for the year Attachment E compares all 50 state's medical malpractice insurance and shows each state's expenses as a percent of direct premiums earned. Nineteen states had a positive return on net worth, while 32 had a negative return on net worth. (Note, these numbers include the District of Columbia.) Wyoming had a return on net worth of percent of the direct premiums earned in In terms of rank, there were 20 states that had a higher return on net worth than Wyoming, and all but one of those had a positive return. The state with the highest return on net worth was Minnesota, with a return on net worth of 20.6 percent. In contrast, 30 states had a negative return on net worth that was worse than Wyoming's. The average return on net worth was a percent, with the biggest loss being a percent in Arkansas. These are all presented as a percentage of direct premiums earned for all lines of insurance and all regulated companies. Comparing medical liability insurance to the other lines of property and casualty insurance may further inform the relative performance of this type of business. Over the last 10 years, "allied lines" accounted for the highest percent of direct premiums earned (highest loss incurred) at 79.9 percent. Next, "private passenger auto liability" earned 76.2 percent. The average losses incurred for medical malpractice were 72.7 percent of the direct premiums earned. The 10-year average for underwriting profit was a - 28 percent of direct premiums earned, which was the lowest average of all insurance lines. "Private passenger auto liability" was next with a percent. Overall, the return on net worth for the 10-year history was 0.1 percent, but there were only three years, which reflected a positive return on net worth. The lowest average return was "allied lines" with a percent. "Medical malpractice" had the second lowest average return at 0.1 percent. Over the last six years, Wyoming medical malpractice insurance companies have (collectively) experienced a negative return on net worth; the worst year was 1996 with a 16.4 percent return. While there is no information for the most recent two years, by looking at the individual companies data, it appears to uphold the earlier years of overall losses for the medical malpractice industry. CONTACTS FOR ADDITIONAL INFORMATION Ken Vines, Insurance Commissioner, phone: (307) Wyoming specific information for all lines of insurance can be seen in Attachment F. Starting in 1993, Attachment F illustrates Wyoming's annual losses incurred, underwriting profit, profit on insurance transactions, and return on net worth. WYOMING LEGISLATIVE SERVICE OFFICE 213 State Capitol Cheyenne, Wyoming TELEPHONE (307) FAX (307) [email protected] WEBSITE

5

6

7

8

9

10

11

12

13

14

15

Percent change. Rank Most expensive states Average expenditure Rank Least expensive states Average expenditure

Page 1 of 7 Auto Insurance AAA s 2010 Your Driving Costs study found that the average cost to own and operate a sedan rose by 4.8 percent to $8,487 per year, compared with the previous year. Rising fuel,

Page 1 of 7 Auto Insurance AAA s 2010 Your Driving Costs study found that the average cost to own and operate a sedan rose by 4.8 percent to $8,487 per year, compared with the previous year. Rising fuel,

Minnesota Department of Commerce Medical Malpractice Insurance in Minnesota Data as of 12/31/2012

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Minnesota Department

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Minnesota Department

ANNUAL STUDY OF MEDICAL MALPRACTICE INSURANCE MARKET IN ARKANSAS

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE

A REPORT TO THE LEGISLATIVE COUNCIL AND THE SENATE AND HOUSE COMMITTEES ON INSURANCE AND COMMERCE OF THE ARKANSAS GENERAL ASSEMBLY (AS REQUIRED BY ACT 1007 OF 2003) ANNUAL STUDY OF MEDICAL MALPRACTICE

Fact Checker. A Check of the Facts in the Michigan Automobile and Home Insurance Consumer Advocate Report to the Governor, 2009

Fact Checker A Check of the Facts in the Michigan Automobile and Home Insurance Consumer Advocate Report to the Governor, 2009 Published by the Insurance Institute of Michigan 334 Townsend, Lansing, MI

Fact Checker A Check of the Facts in the Michigan Automobile and Home Insurance Consumer Advocate Report to the Governor, 2009 Published by the Insurance Institute of Michigan 334 Townsend, Lansing, MI

VERMONT DEPARTMENT OF BANKING, INSURANCE, SECURITIES, AND HEALTH CARE ADMINISTRATION

VERMONT DEPARTMENT OF BANKING, INSURANCE, SECURITIES, AND HEALTH CARE ADMINISTRATION TECHNIQUES TO STABILIZE VERMONT WORKERS COMPENSATION PREMIUM COSTS AND MINIMIZE THE IMPACT OF LARGE CLAIMS Prepared

VERMONT DEPARTMENT OF BANKING, INSURANCE, SECURITIES, AND HEALTH CARE ADMINISTRATION TECHNIQUES TO STABILIZE VERMONT WORKERS COMPENSATION PREMIUM COSTS AND MINIMIZE THE IMPACT OF LARGE CLAIMS Prepared

Texas Private Passenger Automobile Insurance Profitability, 1990 to 1998. A Report by the Center for Economic Justice. April 1999

Texas Private Passenger Automobile Insurance Profitability, 1990 to 1998 This report reviews the loss ratio experience of Texas private passenger automobile insurers from 1990 through 1998 and with particular

Texas Private Passenger Automobile Insurance Profitability, 1990 to 1998 This report reviews the loss ratio experience of Texas private passenger automobile insurers from 1990 through 1998 and with particular

MINIMUM CAPITAL & SURPLUS AND STATUTORY DEPOSITS AND WHO THEY PROTECT. By: Ann Monaco Warren, Esq. 573.634.2522

MINIMUM CAPITAL & SURPLUS AND STATUTORY DEPOSITS AND WHO THEY PROTECT By: Ann Monaco Warren, Esq. 573.634.2522 With the spotlight on the financial integrity and solvency of corporations in the U.S. by

MINIMUM CAPITAL & SURPLUS AND STATUTORY DEPOSITS AND WHO THEY PROTECT By: Ann Monaco Warren, Esq. 573.634.2522 With the spotlight on the financial integrity and solvency of corporations in the U.S. by

Massachusetts Insurance Federation Two Center Plaza 8 th Floor Boston, MA 02108

Massachusetts Insurance Federation Two Center Plaza 8 th Floor Boston, MA 02108 (617) 557-5538 STATEMENT OF THE MASSACHUSETTS INSURANCE FEDERATION TO THE DIVISION OF INSURANCE IN CONNECTION WITH ITS INFORMATIONAL

Massachusetts Insurance Federation Two Center Plaza 8 th Floor Boston, MA 02108 (617) 557-5538 STATEMENT OF THE MASSACHUSETTS INSURANCE FEDERATION TO THE DIVISION OF INSURANCE IN CONNECTION WITH ITS INFORMATIONAL

Advocate Magazine March 2011. Why medical malpractice still matters.

Advocate Magazine March 2011 Why medical malpractice still matters. Despite MICRA limitations, medical-negligence claims still have a crucial role in society BY BRUCE G. FAGEL We all know the statistics

Advocate Magazine March 2011 Why medical malpractice still matters. Despite MICRA limitations, medical-negligence claims still have a crucial role in society BY BRUCE G. FAGEL We all know the statistics

Medicaid Topics Impact of Medicare Dual Eligibles Stephen Wilhide, Consultant

Medicaid Topics Impact of Medicare Dual Eligibles Stephen Wilhide, Consultant Issue Summary The term dual eligible refers to the almost 7.5 milion low-income older individuals or younger persons with disabilities

Medicaid Topics Impact of Medicare Dual Eligibles Stephen Wilhide, Consultant Issue Summary The term dual eligible refers to the almost 7.5 milion low-income older individuals or younger persons with disabilities

Maryland Insurance Administration. 2009 Report on the Effect of Competitive Rating on the Insurance Markets in Maryland

Maryland Insurance Administration 2009 Report on the Effect of Competitive Rating on the Insurance Markets in Maryland January, 2010 Maryland Insurance Administration 2009 Report on the Effect of Competitive

Maryland Insurance Administration 2009 Report on the Effect of Competitive Rating on the Insurance Markets in Maryland January, 2010 Maryland Insurance Administration 2009 Report on the Effect of Competitive

State of Connecticut Insurance Department

State of Connecticut Insurance Department Commissioner Thomas R. Sullivan P.O. Box 816 153 Market Street Hartford, CT 06142-0816 (860) 297-3801 www.ct.gov/cid Connecticut Medical Malpractice Annual Report

State of Connecticut Insurance Department Commissioner Thomas R. Sullivan P.O. Box 816 153 Market Street Hartford, CT 06142-0816 (860) 297-3801 www.ct.gov/cid Connecticut Medical Malpractice Annual Report

NOTICE OF PROTECTION PROVIDED BY [STATE] LIFE AND HEALTH INSURANCE GUARANTY ASSOCIATION

![NOTICE OF PROTECTION PROVIDED BY [STATE] LIFE AND HEALTH INSURANCE GUARANTY ASSOCIATION](/thumbs/25/5402451.jpg "NOTICE OF PROTECTION PROVIDED BY [STATE] LIFE AND HEALTH INSURANCE GUARANTY ASSOCIATION") NOTICE OF PROTECTION PROVIDED BY This notice provides a brief summary of the [STATE] Life and Health Insurance Guaranty Association (the Association) and the protection it provides for policyholders. This

NOTICE OF PROTECTION PROVIDED BY This notice provides a brief summary of the [STATE] Life and Health Insurance Guaranty Association (the Association) and the protection it provides for policyholders. This

COMPANION PROPERTY & CASUALTY INSURANCE COMPANY

REPORT ON LIMITED SCOPE EXAMINATION OF COMPANION PROPERTY & CASUALTY INSURANCE COMPANY COLUMBIA, SOUTH CAROLINA OF THE Loss and Loss Expenses, Large Deductible Collateral Reserves and Reinsurance As of

REPORT ON LIMITED SCOPE EXAMINATION OF COMPANION PROPERTY & CASUALTY INSURANCE COMPANY COLUMBIA, SOUTH CAROLINA OF THE Loss and Loss Expenses, Large Deductible Collateral Reserves and Reinsurance As of

Maryland Insurance Administration s 2006 Report on the Availability and Affordability of Health Care Medical Professional Liability Insurance in

Maryland Insurance Administration s 2006 Report on the Availability and Affordability of Health Care Professional Liability Insurance in Maryland September 5, 2006 Maryland Insurance Administration's 2006

Maryland Insurance Administration s 2006 Report on the Availability and Affordability of Health Care Professional Liability Insurance in Maryland September 5, 2006 Maryland Insurance Administration's 2006

Ohio Medical Malpractice Commission. Statement of James Hurley, ACAS, MAAA Chairperson, Medical Malpractice Subcommittee American Academy of Actuaries

Ohio Medical Malpractice Commission Statement of James Hurley, ACAS, MAAA Chairperson, Medical Malpractice Subcommittee American Academy of Actuaries June 11, 2003 The American Academy of Actuaries is

Ohio Medical Malpractice Commission Statement of James Hurley, ACAS, MAAA Chairperson, Medical Malpractice Subcommittee American Academy of Actuaries June 11, 2003 The American Academy of Actuaries is

Changes in the Cost of Medicare Prescription Drug Plans, 2007-2008

Issue Brief November 2007 Changes in the Cost of Medicare Prescription Drug Plans, 2007-2008 BY JOSHUA LANIER AND DEAN BAKER* The average premium for Medicare Part D prescription drug plans rose by 24.5

Issue Brief November 2007 Changes in the Cost of Medicare Prescription Drug Plans, 2007-2008 BY JOSHUA LANIER AND DEAN BAKER* The average premium for Medicare Part D prescription drug plans rose by 24.5

Model Regulation Service January 2006 DISCLOSURE FOR SMALL FACE AMOUNT LIFE INSURANCE POLICIES MODEL ACT

Table of Contents Section 1. Section 2. Section 3. Section 4. Section 5. Section 6. Section 1. Model Regulation Service January 2006 Purpose Definition Exemptions Disclosure Requirements Insurer Duties

Table of Contents Section 1. Section 2. Section 3. Section 4. Section 5. Section 6. Section 1. Model Regulation Service January 2006 Purpose Definition Exemptions Disclosure Requirements Insurer Duties

Complaint Ratio Index Report of Maryland's Top 20 Auto Insurers for 1998

1 Complaint Ratio Index Report of Maryland's Top 20 Auto Insurers for 1998 A resource for consumers provided by the Maryland Insurance Administration 525 St. Paul Place Baltimore, MD 21202 1-800-492-6116

1 Complaint Ratio Index Report of Maryland's Top 20 Auto Insurers for 1998 A resource for consumers provided by the Maryland Insurance Administration 525 St. Paul Place Baltimore, MD 21202 1-800-492-6116

Malpractice Insurance

Malpractice Insurance A GUIDE FOR CHIROPRACTIC PRACTITIONERS Copyright 2013 NCMIC Insurance Company 14001 University Avenue, Clive, IA 50325-8258 2013, NCMIC Insurance Company, Clive, Iowa. All rights

Malpractice Insurance A GUIDE FOR CHIROPRACTIC PRACTITIONERS Copyright 2013 NCMIC Insurance Company 14001 University Avenue, Clive, IA 50325-8258 2013, NCMIC Insurance Company, Clive, Iowa. All rights

Medical Malpractice Insurance: Stable Losses/Unstable Rates October 10, 2002

Medical Malpractice Insurance: Stable Losses/Unstable Rates October 10, 2002 Introduction and Summary of Findings For the first time, Americans for Insurance Reform (AIR), a coalition of nearly 100 consumer

Medical Malpractice Insurance: Stable Losses/Unstable Rates October 10, 2002 Introduction and Summary of Findings For the first time, Americans for Insurance Reform (AIR), a coalition of nearly 100 consumer

Workers Compensation Cost Data

Workers Compensation Cost Data Edward M. Welch Workers Compensation Center School of Labor and Industrial Relations Michigan State University E-mail: [email protected] Web Page: http://www.lir.msu.edu/wcc/

Workers Compensation Cost Data Edward M. Welch Workers Compensation Center School of Labor and Industrial Relations Michigan State University E-mail: [email protected] Web Page: http://www.lir.msu.edu/wcc/

Associated With: Cincinnati Financial Corporation THE CINCINNATI INSURANCE COMPANIES

THE CINCINNATI INSURANCE COMPANIES Cincinnati Insurance Company A+ Cincinnati Specialty Undrs Ins A+ Cincinnati Casualty Company A+ Cincinnati Indemnity Company A+ Associated With: Cincinnati Financial

THE CINCINNATI INSURANCE COMPANIES Cincinnati Insurance Company A+ Cincinnati Specialty Undrs Ins A+ Cincinnati Casualty Company A+ Cincinnati Indemnity Company A+ Associated With: Cincinnati Financial

MASS MARKETING OF PROPERTY AND LIABILITY INSURANCE MODEL REGULATION

Table of Contents Model Regulation Service January 1996 MASS MARKETING OF PROPERTY AND LIABILITY INSURANCE MODEL REGULATION Section 1. Section 2. Section 3. Section 4. Section 5. Section 6. Section 7.

Table of Contents Model Regulation Service January 1996 MASS MARKETING OF PROPERTY AND LIABILITY INSURANCE MODEL REGULATION Section 1. Section 2. Section 3. Section 4. Section 5. Section 6. Section 7.

Appendix G: Summary of State Studies on Tort Reforms

Appendix G: Summary of State Studies on Tort Reforms ing Office, Medical Malpractice: SIX State Case Studies Show Claims and Insurance Costs Still Rise Despite Reforms, HRD-87-21 (Washington, DC U S Government

Appendix G: Summary of State Studies on Tort Reforms ing Office, Medical Malpractice: SIX State Case Studies Show Claims and Insurance Costs Still Rise Despite Reforms, HRD-87-21 (Washington, DC U S Government

DIRECTORS AND OFFICERS LIABILITY-NOT FOR PROFIT ORGANIZATION APPLICATION

DIRECTORS AND OFFICERS LIABILITY-NOT FOR PROFIT ORGANIZATION APPLICATION RSUI Indemnity Company Landmark American Insurance Company NOTICE: THIS IS A CLAIMS MADE AND REPORTED POLICY THAT APPLIES ONLY TO

DIRECTORS AND OFFICERS LIABILITY-NOT FOR PROFIT ORGANIZATION APPLICATION RSUI Indemnity Company Landmark American Insurance Company NOTICE: THIS IS A CLAIMS MADE AND REPORTED POLICY THAT APPLIES ONLY TO

The State of Competition in the Workers' Compensation Market 2015

Maine State Library Maine State Documents Insurance Documents Professional and Financial Regulation 12-30-2015 The State of Competition in the Workers' Compensation Market 2015 Maine Bureau of Insurance

Maine State Library Maine State Documents Insurance Documents Professional and Financial Regulation 12-30-2015 The State of Competition in the Workers' Compensation Market 2015 Maine Bureau of Insurance

ANNUAL REPORT BOARD OF COMMISSIONERS OF PUBLIC UTILITIES ON THE OPERATIONS CARRIED OUT UNDER THE AUTOMOBILE INSURANCE ACT

ANNUAL REPORT OF THE BOARD OF COMMISSIONERS OF PUBLIC UTILITIES ON THE OPERATIONS CARRIED OUT UNDER THE AUTOMOBILE INSURANCE ACT Chapter A-22, R.S.N. 1990, AS AMENDED FOR THE PERIOD APRIL 1, 2002 TO MARCH

ANNUAL REPORT OF THE BOARD OF COMMISSIONERS OF PUBLIC UTILITIES ON THE OPERATIONS CARRIED OUT UNDER THE AUTOMOBILE INSURANCE ACT Chapter A-22, R.S.N. 1990, AS AMENDED FOR THE PERIOD APRIL 1, 2002 TO MARCH

MEDICAL MALPRACTICE CLOSED CLAIM DATA COLLECTION UNDER CONNECTICUT PUBLIC ACT 05-275

MEDICAL MALPRACTICE CLOSED CLAIM DATA COLLECTION UNDER CONNECTICUT PUBLIC ACT 05-275 Introduction: Public Act 05-275 (the Act ) requires Medical Malpractice insurance providers to report closed claims

MEDICAL MALPRACTICE CLOSED CLAIM DATA COLLECTION UNDER CONNECTICUT PUBLIC ACT 05-275 Introduction: Public Act 05-275 (the Act ) requires Medical Malpractice insurance providers to report closed claims

MODEL REGULATION TO REQUIRE REPORTING OF STATISTICAL DATA BY PROPERTY AND CASUALTY INSURANCE COMPANIES

Model Regulation Service June 2004 MODEL REGULATION TO REQUIRE REPORTING OF STATISTICAL DATA Table of Contents Section 1. Section 2. Section 3. Section 4. Section 5. Section 6. Section 7. Section 8. Section

Model Regulation Service June 2004 MODEL REGULATION TO REQUIRE REPORTING OF STATISTICAL DATA Table of Contents Section 1. Section 2. Section 3. Section 4. Section 5. Section 6. Section 7. Section 8. Section

REPORT OF EXAMINATION OF THE WESTERN UNITED INSURANCE COMPANY AS OF DECEMBER 31, 2004

REPORT OF EXAMINATION OF THE WESTERN UNITED INSURANCE COMPANY AS OF DECEMBER 31, 2004 Participating State and Zone: California Filed January 12, 2006 TABLE OF CONTENTS PAGE SCOPE OF EXAMINATION... 1 COMPANY

REPORT OF EXAMINATION OF THE WESTERN UNITED INSURANCE COMPANY AS OF DECEMBER 31, 2004 Participating State and Zone: California Filed January 12, 2006 TABLE OF CONTENTS PAGE SCOPE OF EXAMINATION... 1 COMPANY

Report of Examination of. OHIC Insurance Company Columbus, Ohio. As of December 31, 2011

Report of Examination of OHIC Insurance Company Columbus, Ohio As of December 31, 2011 Table of Contents Subject Page Salutation... 1 Description of Company... 1 Scope of Examination... 1 Management and

Report of Examination of OHIC Insurance Company Columbus, Ohio As of December 31, 2011 Table of Contents Subject Page Salutation... 1 Description of Company... 1 Scope of Examination... 1 Management and

Washington, DC. A World-Class City for Captive Insurance

Washington, DC A World-Class City for Captive Insurance Washington, DC A World-Class City for Captive Insurance The Risk Finance Bureau regulates captive insurance companies, risk retention groups and

Washington, DC A World-Class City for Captive Insurance Washington, DC A World-Class City for Captive Insurance The Risk Finance Bureau regulates captive insurance companies, risk retention groups and

M&A in MPL: What Does It All Mean?

M&A in MPL: What Does It All Mean? Jeff Donaldson, FCAS, MAAA Overview Why are there acquisition opportunities in MPL? State of the market Underwriting cycle Loss cost trends Reserve evaluations Investment

M&A in MPL: What Does It All Mean? Jeff Donaldson, FCAS, MAAA Overview Why are there acquisition opportunities in MPL? State of the market Underwriting cycle Loss cost trends Reserve evaluations Investment

NO-FAULT AUTO INSURANCE IN MICHIGAN A Summary of Loss Trends and Estimates of the Benefits of Proposed Reforms

NO-FAULT AUTO INSURANCE IN MICHIGAN A Summary of Loss Trends and Estimates of the Benefits of Proposed Reforms Robert P. Hartwig, Ph.D., CPCU President & Economist Insurance Information Institute James

NO-FAULT AUTO INSURANCE IN MICHIGAN A Summary of Loss Trends and Estimates of the Benefits of Proposed Reforms Robert P. Hartwig, Ph.D., CPCU President & Economist Insurance Information Institute James

Private Passenger Automobile Tort Reform Rate Reductions: Fact versus Fiction

Private Passenger Automobile Tort Reform Rate Reductions: Fact versus Fiction 1. Executive Summary Insurers Reap Windfall Auto Insurance Profits As Insurance Department Fails to Meet Legislative Intent

Private Passenger Automobile Tort Reform Rate Reductions: Fact versus Fiction 1. Executive Summary Insurers Reap Windfall Auto Insurance Profits As Insurance Department Fails to Meet Legislative Intent

california Health Care Almanac Health Care Costs 101: California Addendum

california Health Care Almanac : California Addendum May 2012 Introduction Health spending represents a significant share of California s economy, but the amounts spent on health care rank among the lowest

california Health Care Almanac : California Addendum May 2012 Introduction Health spending represents a significant share of California s economy, but the amounts spent on health care rank among the lowest

List of State Residual Insurance Market Entities and State Workers Compensation Funds

List of State Residual Insurance Market Entities and State Workers Compensation Funds On November 26, 2002, President Bush signed into law the Terrorism Risk Insurance Act of 2002 (Public Law 107-297,

List of State Residual Insurance Market Entities and State Workers Compensation Funds On November 26, 2002, President Bush signed into law the Terrorism Risk Insurance Act of 2002 (Public Law 107-297,

Homeowners and Renters Insurance

Homeowners and Renters Insurance HOMEOWNERS INSURANCE EXPENDITURES The average homeowners insurance premium rose by 5.6 percent in 2012, following a 7.7 percent increase in 2011, according to a February

Homeowners and Renters Insurance HOMEOWNERS INSURANCE EXPENDITURES The average homeowners insurance premium rose by 5.6 percent in 2012, following a 7.7 percent increase in 2011, according to a February

Maryland Insurance Administration s 2005 Report on the Availability and Affordability of Health Care Medical Professional Liability Insurance in

Maryland Insurance Administration s 2005 Report on the Availability and Affordability of Health Care Medical Professional Liability Insurance in Maryland November, 2005 Maryland Insurance Administration's

Maryland Insurance Administration s 2005 Report on the Availability and Affordability of Health Care Medical Professional Liability Insurance in Maryland November, 2005 Maryland Insurance Administration's

Best s Rating: A- Report PROASSURANCE GROUP PROASSURANCE GROUP. Birmingham, Alabama

PROASSURANCE GROUP Birmingham, Alabama A- PROASSURANCE GROUP 100 Brookwood Place Birmingham, AL 35209 Web: www.proassurance.com Tel: 205-877-4400 Fax: 205-802-4799 AMB#: 18559 Publicly Traded Corporation:

PROASSURANCE GROUP Birmingham, Alabama A- PROASSURANCE GROUP 100 Brookwood Place Birmingham, AL 35209 Web: www.proassurance.com Tel: 205-877-4400 Fax: 205-802-4799 AMB#: 18559 Publicly Traded Corporation:

Homeowners and Renters Insurance

Homeowners and Renters Insurance HOMEOWNERS INSURANCE EXPENDITURES The average homeowners insurance premium rose by 6.0 percent in 2013, following a 5.6 percent increase in 2012, according to a February

Homeowners and Renters Insurance HOMEOWNERS INSURANCE EXPENDITURES The average homeowners insurance premium rose by 6.0 percent in 2013, following a 5.6 percent increase in 2012, according to a February

Guide to Malpractice Insurance for Naturopathic Physicians

Guide to Malpractice Insurance for Naturopathic Physicians Whether you re a new Naturopathic Physician or have been practicing for decades, making sure you have the right malpractice insurance policy is

Guide to Malpractice Insurance for Naturopathic Physicians Whether you re a new Naturopathic Physician or have been practicing for decades, making sure you have the right malpractice insurance policy is

ACE American Insurance Company

Named Applicant: Date: ACE American Insurance Company ACE Advantage ACE American Insurance Company National Association of REALTORS Professional Liability Name of insurance company to which Application

Named Applicant: Date: ACE American Insurance Company ACE Advantage ACE American Insurance Company National Association of REALTORS Professional Liability Name of insurance company to which Application

It s important to understand the process and react properly when it occurs.

Doctor, You ve Been Sued! It s important to understand the process and react properly when it occurs. By Howard S. Rosenbaum, DPM Malpractice suits are terrifying events for most podiatric physicians.

Doctor, You ve Been Sued! It s important to understand the process and react properly when it occurs. By Howard S. Rosenbaum, DPM Malpractice suits are terrifying events for most podiatric physicians.

Jane L. Cline, Insurance Commissioner Phone: 558-3394 ext. 140 Email: [email protected]

State of West Virginia A Review of Personal Automobile Insurance Provided by the Office of the West Virginia Insurance Commission March, 2004 Contacts for questions and comments on this report: Jane L.

State of West Virginia A Review of Personal Automobile Insurance Provided by the Office of the West Virginia Insurance Commission March, 2004 Contacts for questions and comments on this report: Jane L.

Between 1986 and 2010, homeowners and renters. A comparison of 25 years of consumer expenditures by homeowners and renters.

U.S. BUREAU OF LABOR STATISTICS OCTOBER 2012 VOLUME 1 / NUMBER 15 A comparison of 25 years of consumer expenditures by homeowners and renters Author: Adam Reichenberger, Consumer Expenditure Survey Between

U.S. BUREAU OF LABOR STATISTICS OCTOBER 2012 VOLUME 1 / NUMBER 15 A comparison of 25 years of consumer expenditures by homeowners and renters Author: Adam Reichenberger, Consumer Expenditure Survey Between

Significant Measures of State Unemployment Insurance Tax Systems

U.S. Department of Labor Office of Unemployment Insurance Division of Fiscal and Actuarial Services March 2014 Significant Measures of State Unemployment Insurance Tax Systems UPDATED 2012 Evaluating State

U.S. Department of Labor Office of Unemployment Insurance Division of Fiscal and Actuarial Services March 2014 Significant Measures of State Unemployment Insurance Tax Systems UPDATED 2012 Evaluating State

Overview of Tennessee s s Workers Compensation Market Conditions and Environment

Overview of Tennessee s s Workers Compensation Market Conditions and Environment Tennessee Advisory Council on Workers Compensation August 22, 2011 Mike Shinnick,, Workers Compensation Manager Tennessee

Overview of Tennessee s s Workers Compensation Market Conditions and Environment Tennessee Advisory Council on Workers Compensation August 22, 2011 Mike Shinnick,, Workers Compensation Manager Tennessee

LAWYERS PROFESSIONAL LIABILITY INSURANCE POLICY RENEWAL APPLICATION

LAWYERS PROFESSIONAL LIABILITY INSURANCE POLICY RENEWAL APPLICATION NOTICE: THE POLICY FOR WHICH THIS APPLICATION IS MADE IS A CLAIMS MADE AND REPORTED POLICY. SUBJECT TO ITS TERMS, THE POLICY APPLIES

LAWYERS PROFESSIONAL LIABILITY INSURANCE POLICY RENEWAL APPLICATION NOTICE: THE POLICY FOR WHICH THIS APPLICATION IS MADE IS A CLAIMS MADE AND REPORTED POLICY. SUBJECT TO ITS TERMS, THE POLICY APPLIES

This briefing paper summarizes the measures the Montana Legislature has put into place to improve the state's medical liability climate.

SRJ 35: Study of Health Care Medical Malpractice: Montana's Approach to Limiting Liability by Sue O'Connell, Research Analyst Prepared for the Children, Families, Health, and Human Services Interim Committee

SRJ 35: Study of Health Care Medical Malpractice: Montana's Approach to Limiting Liability by Sue O'Connell, Research Analyst Prepared for the Children, Families, Health, and Human Services Interim Committee

INSURANCE COMPANY HANDOUT:

INSURANCE COMPANY HANDOUT: HOW THE INDUSTRY USED TORT REFORM TO INCREASE PROFITS WHILE AMERICANS PREMIUMS SOARED ONE OF A SERIES OF REPORTS FROM THE AMERICAN ASSOCIATION FOR JUSTICE ON MEDICAL NEGLIGENCE

INSURANCE COMPANY HANDOUT: HOW THE INDUSTRY USED TORT REFORM TO INCREASE PROFITS WHILE AMERICANS PREMIUMS SOARED ONE OF A SERIES OF REPORTS FROM THE AMERICAN ASSOCIATION FOR JUSTICE ON MEDICAL NEGLIGENCE

2012 Medical Malpractice Annual Report

2012 Medical Malpractice Annual Report Closed from Jan. 1, 2008 through Dec. 31, 2011 August 2012 Rates and Forms Division Lisa Smego, CPCU, ARM, AIAF, ARC, AIE, Data Reporting Manager Eric Slavich, ACAS,

2012 Medical Malpractice Annual Report Closed from Jan. 1, 2008 through Dec. 31, 2011 August 2012 Rates and Forms Division Lisa Smego, CPCU, ARM, AIAF, ARC, AIE, Data Reporting Manager Eric Slavich, ACAS,

U.S. Homeowners Market

U.S. Homeowners Market Casualty Actuarial Society Spring Meeting Kelleen Arquette, FCAS, MAAA May 2013 2013 Towers Watson. All rights reserved. AGENDA Agenda Market Overview Market Definition Direct Written

U.S. Homeowners Market Casualty Actuarial Society Spring Meeting Kelleen Arquette, FCAS, MAAA May 2013 2013 Towers Watson. All rights reserved. AGENDA Agenda Market Overview Market Definition Direct Written

Subject: Military Personnel Strengths in the Army National Guard

United States General Accounting Office Washington, DC 20548 March 20, 2002 The Honorable John McHugh Chairman The Honorable Vic Snyder Ranking Member Military Personnel Subcommittee Committee on Armed

United States General Accounting Office Washington, DC 20548 March 20, 2002 The Honorable John McHugh Chairman The Honorable Vic Snyder Ranking Member Military Personnel Subcommittee Committee on Armed

GAO. MEDICAL MALPRACTICE INSURANCE Multiple Factors Have Contributed to Premium Rate Increases

GAO For Release on Delivery Expected at 2:00 p.m. EDT Wednesday, October 1, 2003 United States General Accounting Office Testimony Before the Subcommittee on Wellness and Human Rights, Committee on Government

GAO For Release on Delivery Expected at 2:00 p.m. EDT Wednesday, October 1, 2003 United States General Accounting Office Testimony Before the Subcommittee on Wellness and Human Rights, Committee on Government

INSURANCE COMPANY PROFESSIONAL LIABILITY INSURANCE APPLICATION

i NAME OF INSURANCE COMPANY TO WHICH APPLICATION IS MADE: (herein called the Company) INSURANCE COMPANY PROFESSIONAL LIABILITY INSURANCE APPLICATION IF A POLICY IS ISSUED, IT WILL BE ON A CLAIMS-MADE BASIS

i NAME OF INSURANCE COMPANY TO WHICH APPLICATION IS MADE: (herein called the Company) INSURANCE COMPANY PROFESSIONAL LIABILITY INSURANCE APPLICATION IF A POLICY IS ISSUED, IT WILL BE ON A CLAIMS-MADE BASIS

THE BURDEN OF HEALTH INSURANCE PREMIUM INCREASES ON AMERICAN FAMILIES AN UPDATE ON THE REPORT BY THE EXECUTIVE OFFICE OF THE PRESIDENT

THE BURDEN OF HEALTH INSURANCE PREMIUM INCREASES ON AMERICAN FAMILIES AN UPDATE ON THE REPORT BY THE EXECUTIVE OFFICE OF THE PRESIDENT INTRODUCTION In September 2009, the Executive Office of the President

THE BURDEN OF HEALTH INSURANCE PREMIUM INCREASES ON AMERICAN FAMILIES AN UPDATE ON THE REPORT BY THE EXECUTIVE OFFICE OF THE PRESIDENT INTRODUCTION In September 2009, the Executive Office of the President

Readopt with amendment, Ins 3800, effective 12-01-06 (Doc. #8754), to read as follows: CHAPTER Ins 3800 MEDICAL PROFESSIONAL LIABILITY INSURANCE

, to read as follows: CHAPTER Ins 3800 MEDICAL PROFESSIONAL LIABILITY INSURANCE") Adopted Rule 11/25/14 1 Readopt with amendment, Ins 3800, effective 12-01-06 (Doc. #8754), to read as follows: CHAPTER Ins 3800 MEDICAL PROFESSIONAL LIABILITY INSURANCE Statutory Authority: RSA 400-A;15,

Adopted Rule 11/25/14 1 Readopt with amendment, Ins 3800, effective 12-01-06 (Doc. #8754), to read as follows: CHAPTER Ins 3800 MEDICAL PROFESSIONAL LIABILITY INSURANCE Statutory Authority: RSA 400-A;15,