Proposed Five Year Financial Plan

|

|

|

- Felicity Manning

- 10 years ago

- Views:

Transcription

1 Proposed Five Year Financial Plan Received by Committee of the Whole on March 2, 2015

2 Table of Contents Executive Summary Highlights Summary Consolidated Fund Summary General Fund Summary General Government Services Protective Services Engineering Services Development Services Recreation and Cultural Services Fiscal Services Capital Capital Plan Capital Plan Capital Plan Capital Plan Capital Plan Revenues Recap of Reserves Reserves Sewer Fund Summary Sewer Fund Transmission of Taxes

3 1. Executive Summary: Council approved their Corporate Strategic Plan on April 28, These priorities have been the primary guidance for the Five Year Financial Plan. In the Corporate Strategic Plan, Council identified four strategic priorities: a. Fiscal Responsibility b. Town Centre c. Economic Revitalization d. Community Planning The 2015 budget integrates each of these priorities. a. Fiscal Responsibility: The District will strive towards long-term financial sustainability. It will prepare for the future by ensuring adequate contributions are made towards required long-term capital infrastructure needs while living within current means. The 2015 budget maintains a 2.49% tax increase. This increase includes contractually obligated increases to expenditures that equate to approximately 2% overall. Addressing the long-term contributions towards capital infrastructure needs, there is an additional $130,000 budgeted to be transferred into the Capital Asset Replacement Reserve. This is above and beyond the minimum required by bylaw. With long-term sustainability a critical element to strong fiscal responsibility an additional $291,000 is projected to be transferred into the Capital Asset Replacement Reserve. This is the revenue that is expected to be received from new assessment within the District which is called Non-market Change assessment. A 2.49% tax increase has been achieved in the current year while setting aside $612,939 into reserves for future use, of which $421,000 is not currently required by Bylaw. This represents strong fiscal responsibility. b. Town Centre: The Town Centre is a significant priority of Council. The District is striving towards making the Town Centre a vibrant, clean and well-maintained node. The initial focus will be on transportation flow, pedestrian safety improvements and meeting appropriate Page 2 of 44

4 maintenance standards. Implementation of the Town Centre Plan will require many different efforts, including some capital projects, land acquisition and road realignments. Considerable work is needed to improve sidewalks and pedestrian safety. Additionally, actions are required to improve the appearance and functionality of the area. The focus on the Town Centre began in 2013, has continued on through 2014 and continues throughout the Proposed Financial Plan. Some of the completed projects include; land purchases, Church Road Multi-use Trail, completion of the first phase of the Connector Wadams Way, construction of the Wadams Way Multi-use Trail. Included in 2015 of the Proposed Financial Plan are the following projects: 1. Design and begin construction of the second phase of the Connector (Phillips to Charters Rd.) 2. Hwy 14 Roundabout Construction 3. Improvements to Hwy 14 from Church Rd to Otter Point Rd. 4. Design and construction of sidewalks along Hwy 14 from Church Rd to Otter Point Rd. 5. Continued funding for Road and Sidewalk Improvement Program 6. Downtown Art Bench 7. Transit Stop Improvements Projects included in include: 1. Completion of the second phase of the Connector (Phillips to Charters Rd.) 2. Improved Rainwater Management in the Town Centre 3. Continued funding for Road and Sidewalk Improvement Program 4. Church Rd. widening (Sooke Rd to Helgeson Rd.) 5. Phase three of the Connector along Grant Rd. (Otter Point to Gatewood) c. Economic Revitalization: The District will strive towards developing appropriate mechanisms to facilitate and promote long-term community economic prosperity and resiliency. The Mayor s Advisory Panels and Promote Sooke Task force was created in 2013 and there continues to be funding going forward. Page 3 of 44

5 d. Community Planning The District will strive towards clarifying, simplifying and streamlining planning processes and instruments, which will respond to, enable and support investment and job growth in the community. Council desires to move forward with the implementation phase of several of the background studies or plans that have been completed in the past few years. In particular, Council wishes to: identify infrastructure upgrades, complete the DCC Bylaw review for sewers, and introduce Checklists and Templates to streamline development approvals. Much of the work on this began in 2013 and will continue in 2015 and years to follow. The 2015 budget has $50,000 allocated for funding the work on long term plans. Highlights: Strategic Plan: Strategic planning is an organization's process of defining its strategy, or direction, and making decisions on allocating its resources to pursue this strategy. In order to determine the direction of the organization, it is necessary to understand its current position and the possible avenues through which it can pursue a particular course of action. In many organizations this is viewed as a process for determining where an organization is going over the next year, or more typically 3 to 5 years. In 2014, Council established the Corporate Strategic Plan. This document guides many of the budget decisions included in the Proposed Financial Plan. In addition, the current Council has met to set a new Strategic Plan for 2015 and beyond. This plan will be coming forward at the same time as this budget and has been incorporated into this financial plan. Having a documented direction gives all stakeholders a better indication of the direction that the District is going. A strategic plan increases the efficiency within an organization as it provides clear direction for Council and staff. It is a guide to follow while also acting as a reference point when making decisions. Fire Equipment Reserve: Currently the District of Sooke has the Fire Protection Capital Reserve Fund Bylaw No. 7, This reserve account is to be funded by general revenue. Fire Rescue Page 4 of 44

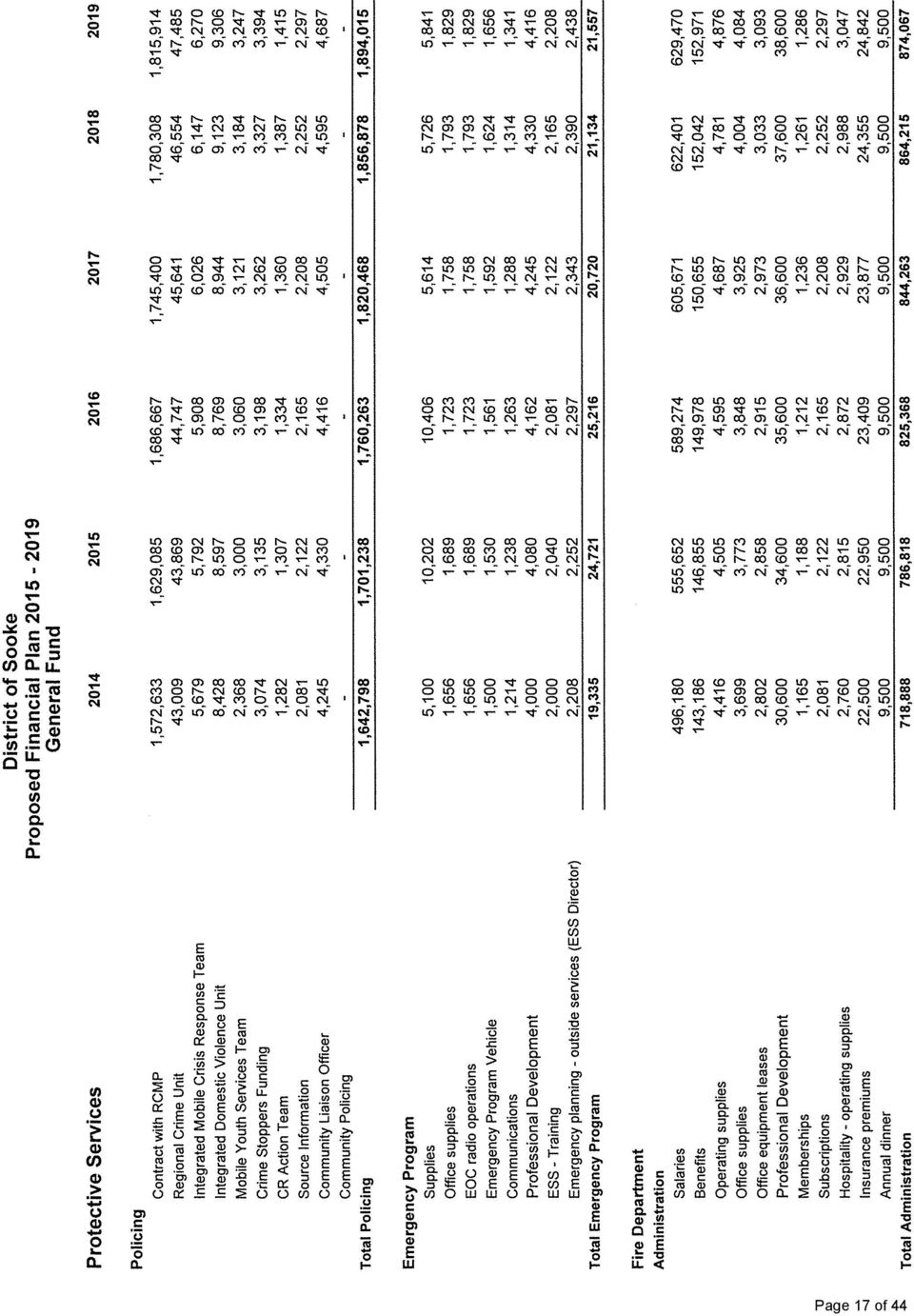

6 equipment, especially vehicles, are a significant expense for a municipality the size of the District of Sooke. Two approaches can be taken by an organization to fund the projected future costs of capital. Method 1: Method 2: As the requirement occurs, tax in that year for the full cost of the equipment. Estimate future costs and set aside funds in a savings account so that at the time of the purchase the required funding is available. Method 1 above, results in significant expense increases on a sporadic basis. In the year of a large purchase there is a spike in the capital expense which in turn results in a spike in the revenues required. Taxes would typically increase dramatically in these years, resulting in a large tax increases periodically. Method 2 above, allows a smoothing of the revenue required to cover the costs associated with these purchases. Under this scenario, costs are projected over a period of time and averaged to determine an average annual cost. The average annual cost then transferred into a savings account. In this situation the savings account is the Fire Protection Capital Reserve. This method eliminates the periodic tax increases as the reserve account is funded over a period of time to cover the periodic expenses that are not consistent year over year. Method 2 is the recommended policy. During 2015 staff will bring forward a more detailed capital asset replacement plan for fire equipment. This plan will outline the necessary annual funding into the savings account, Fire Protection Capital Reserve. For 2015, $100,000 has been allocated for transfer into the Fire Reserve account. Policing: The budgeted increase for the contract with the RCMP reflects increases in the per officer costs in addition to increases in the accommodation costs. As the RCMP has a March 31 year end, the 2014 budget numbers are based on RCMP forecast expenditures for and budgets for Sewer Parcel Tax: The base parcel tax has been budgeted to stay at the same level as 2014, $515. The parcel tax amount is subject to review on an annual basis based on the growth in the Sewer Specified Area in addition to the budgeted expenditures each year. Page 5 of 44

7 In 2013, Council approved a $37 increase to the base parcel tax from 2013 to 2017 to fund the repayment to the General Operating Fund. The sewer fund owed the general fund $588,460 for borrowings from 2006 to At the end of the 5 year repayment term this additional $37 will be eliminated. Sewer DCC Reserve and EPCOR Contract: Council made the policy decision in 2012 to begin using Wastewater DCC s to offset the principal payment on the Sewer debt. This amounts to $295,419 annually. The decision to use DCC funds to pay for the principal payment on debt that the District holds for the installation of the sewer system could have been made immediately after the District incurred the debt, as the project was listed in the DCC Bylaw and funds were being collected for the purpose of paying for those projects. The accumulation of DCC funds between 2004 and 2012 was made up of funds that were collected for the purpose of paying for the Sanitary Sewer DCC Program, as listed on the schedule attached to this report. The funds collected can only be used for these projects; therefore, using the DCC funds to pay for the principal portion of the loan is a fiscally responsible measure to ensure that these funds are used for the purpose that they were collected. It is in fact not fiscally responsible to use other funds to pay for a project when the DCC funds are available and they are solely for the purpose of paying for the project. Concern has been brought forward that the use of the DCC funds are depleting the sewer fund ability to cover future expenditures. In fact, the decision by Council in 2012 to begin correctly using the DCC funds to cover the debt principal has allowed the creation of another reserve account within the sewer fund where all surpluses in the sewer fund are deposited at the end of each year beginning in This reserve account provides the savings account to help cover and fund future sewer expenditures. As outlined in the proposed Five Year Financial Plan the Reserve for Future Sewer Expenditures is budgeted to grow from $301,424 to $1,396,219. During the same 5 year time frame the DCC fund is budgeted to decrease from $835,170 to $1,039. While it may appear that this decrease in the DCC Fund is not a good thing it must be noted again that the purpose of those funds is for the payment of the projects within the program and no other expenditures within the sewer system. Given that the DCC funds can only be used for the projects listed in the DCC program the decision to use the funds for this purpose is a fiscally sound decision. While the Page 6 of 44

8 DCC funds may not end up funding as much of the project as originally planned this does not mean that the funds that are collected shouldn t be used. As the funds have been collected for the purpose of paying for these projects even the complete use of the Wastewater DCC Reserve is not a sign of weak financial management or financial sustainability. Going forward staff will continue to closely monitor the Wastewater DCC Revenue being collected and deposited into the DCC reserve account to ensure that adequate funding is maintained within the sewer fund. Based on current projections, through 2026 when the sewer debt will be paid off, the DCC fund and the newly created reserve for future expenditures will adequately fund the principal on the sewer debt and the sewer fund will not be in a position that it will be borrowing from the general fund. The District s contract with EPCOR for operation and maintenance of the District s Sewer System expires on September 30, It is not possible at this time to estimate the impact this may have on future Sewer Fund expenditures. Reserve for Future Sewer Expenditures: All funds generated within the sewer fund must be retained within the fund. In the event that revenues are higher than expenditures in a given year these funds must be retained within the fund. Beginning in 2013, excess funds are transferred into a reserve account to cover future expenditures. This is a strong fiscal decision and creates a savings account for the sewer fund. Building Maintenance: Just like on a vehicle or a home, maintenance is required for the municipal hall. Maintenance has been neglected in some areas around the municipal hall in previous years, as outlined by the Occupational Health and Safety Committee. The 2013 budget included an increase in building maintenance expense to undertake some of the much needed maintenance around the municipal hall. The increase was continued in 2014 and is again continued in the 2015 budget to ensure that maintenance is regularly conducted and no longer neglected. If neglected, there may be significant health and safety issues for staff and members of the public who use the municipal hall. Professional Development: Page 7 of 44

9 Training offers many benefits to both the business and its employees. These can range from increased efficiency and productivity to increased morale, motivation and job satisfaction. Training also offers the following benefits: It ensures new employees acquire the necessary skills, knowledge, qualities and qualifications for the job they will be doing. It makes it easier for new employees to reach the level of performance expected of them by the business. Helps to identify the potential of employees which increases the job prospects and chances of promotion. Training also helps the business to make sure that it has the right person for the job when promotion opportunities arise. Long term costs can be reduced due to factors such as reducing waste and increasing labor productivity. If or when change occurs it helps employees deal with it more effectively and be more flexible, reducing resistance to change. Helps improve the image and reputation of the business because customers will have more confidence in well trained staff. In addition to the above benefits to continual training for staff, some members of staff belong to professional organizations that require that the individual undertake a minimum number of hours of training in order to maintain that professional designation. Where the organization requires that the member of staff have the designation, the organization should also support the staff member s professional development. The 2015 budget includes levels that are required for adequate staff training, including those that require a minimum level of training each year to maintain their professional designations. Human capital is the most valuable asset many organizations have. Adequate funding for training and development will increase employee moral, increase efficiency and increase service to the public. Plans: The proposed Financial Plan as presented incudes an annual budget for long-term plans. The establishment of operational plans must be done to guide and direct the direction of the community. They also provide direction to Council and staff along with acting as a consistent reference point. While the initial cost to develop the plan is generally the largest there are ongoing costs to renew, replace and redo the plans. Most plans are current at the time of their development; however they require updates to remain effective and current. Each of these stages is another major cost driver. The District of Sooke, in most cases, does not have the human capital in house to perform these stages in the life cycle of the plan. Staff always look for ways to minimize Page 8 of 44

10 the cost of external consultants, however, many plans require the expertise or time required of an external consultant to ensure the best end result. Inflation: The Proposed Five Year Financial Plan uses a 2% inflation factor for expenses. Inflationary increases are applied to revenues and expenses, except where specific increases or decreases are known or estimated. Vancouver Island Regional Library: Starting in 2012, Council decided to reflect the Vancouver Island Regional Library as a separate line item on the annual tax notice. While this is a separate line item on the tax notice, the funding must still be financed by general revenue primarily taxes. VIRL has projected significant increases in their budget for the next five years. These increases have been reflected in this Proposed Five Year Financial Plan. Amortization: Effective 2009, Local Governments have been required to account for Tangible Capital Assets under PSAB Capital assets must also be amortized (depreciated). Amortization is recorded as an expense on the annual financial statements. Effective 2013, amortization has been included in the budget numbers. Inclusion in the budget allows better comparability budget to actual on the annual financial statements. Amortization has a significant effect on the overall budgeted expenses for a number of the segments (Engineering, Protective, General Government, Sewer). As amortization is a non-cash expense, a corresponding revenue offset has been included on the Summary page for both General Fund and Sewer Fund. In addition, as the inclusion of amortization has significantly increased the total expense for most segments in the budget, a sub-total before amortization has been included to allow for better comparison of budgeted cash expenditures when comparing budgets. Non-Market Change: Each year, new development in the community increases the property assessment for the municipality. Increased assessment results in an increase in the tax base. This new tax money is traditionally used in one of two ways, or combination thereof; firstly, to offset tax increases in the current year, secondly, to increase reserves as a savings for use in future years. Page 9 of 44

11 Non-market change has been factored into this proposed budget based on preliminary Non-market change values received from BC Assessment. In keeping with Strategic Priority #1, Fiscal Responsibility, the Five Year Financial Plan includes a transfer directly into the Capital Asset Replacement Reserve for the projected tax revenues generated through the increase in assessed value resulting from the Non-market Change. 2. Summary: The Proposed Five Year Financial Plan addresses the short-term priorities of Council while continuing to address long-term fiscal responsibility. Funding is always a balance between current needs/wants and saving for future. Page 10 of 44

12 Page 11 of 44

13 Page 12 of 44

14 Page 13 of 44

15 Page 14 of 44

16 Page 15 of 44

17 Page 16 of 44

18 Page 17 of 44

19 Page 18 of 44

20 Page 19 of 44

21 Page 20 of 44

22 Page 21 of 44

23 Page 22 of 44

24 Page 23 of 44

25 Page 24 of 44

26 Page 25 of 44

27 Page 26 of 44

28 Page 27 of 44

29 Page 28 of 44

30 Page 29 of 44

31 Page 30 of 44

32 Page 31 of 44

33 Page 32 of 44

34 Page 33 of 44

35 Page 34 of 44

36 Page 35 of 44

37 Page 36 of 44

38 Page 37 of 44

39 Page 38 of 44

40 Page 39 of 44

41 Page 40 of 44

42 Page 41 of 44

43 Page 42 of 44

44 Page 43 of 44

45 Page 44 of 44

Official Community Plan Guiding Principles:

Live, Work, Play CORPORATE STRATEGIC PLAN 2014-2015 Official Community Plan Guiding Principles: Sooke s Thriveability; Sustainability; Environmental Stewardship; Economic Diversification; Smart Growth;

Live, Work, Play CORPORATE STRATEGIC PLAN 2014-2015 Official Community Plan Guiding Principles: Sooke s Thriveability; Sustainability; Environmental Stewardship; Economic Diversification; Smart Growth;

DISTRICT OF NORTH VANCOUVER GUIDE TO FINANCIAL STATEMENTS

DISTRICT OF NORTH VANCOUVER GUIDE TO FINANCIAL STATEMENTS DISTRICT OF NORTH VANCOUVER Our goal at North Vancouver District is to make information sharing and reporting convenient, accessible and relevant

DISTRICT OF NORTH VANCOUVER GUIDE TO FINANCIAL STATEMENTS DISTRICT OF NORTH VANCOUVER Our goal at North Vancouver District is to make information sharing and reporting convenient, accessible and relevant

Financial Statement Guide. A Guide to Local Government Financial Statements

Financial Statement Guide A Guide to Local Government Financial Statements January, 2012 Ministry of Community, Sport and 1 Financial Statement Guide Table of Contents Introduction Legislative Requirements

Financial Statement Guide A Guide to Local Government Financial Statements January, 2012 Ministry of Community, Sport and 1 Financial Statement Guide Table of Contents Introduction Legislative Requirements

A Quick Guide to Municipal Financial Statements MUNICIPAL AFFAIRS

A Quick Guide to Municipal Financial Statements MUNICIPAL AFFAIRS June 2010 Alberta Municipal Affairs (2010) A Quick Guide to Municipal Financial Statements Edmonton: Alberta Municipal Affairs For more

A Quick Guide to Municipal Financial Statements MUNICIPAL AFFAIRS June 2010 Alberta Municipal Affairs (2010) A Quick Guide to Municipal Financial Statements Edmonton: Alberta Municipal Affairs For more

TOWN OF LAKE COWICHAN. A Bylaw respecting the Financial Plan for the Town of Lake Cowichan

TOWN OF LAKE COWICHAN Bylaw No. 943-2014 A Bylaw respecting the Financial Plan for the Town of Lake Cowichan WHEREAS Section 165 of the Community Charter requires a Municipality to prepare and adopt, a

TOWN OF LAKE COWICHAN Bylaw No. 943-2014 A Bylaw respecting the Financial Plan for the Town of Lake Cowichan WHEREAS Section 165 of the Community Charter requires a Municipality to prepare and adopt, a

Department of Finance Policies and Procedures Reserve Funds Policy # Authorized by: City Council Date of issue: September 30, 2004

Department of Finance Policies and Procedures Reserve Funds Policy # Authorized by: City Council Date of issue: September 30, 2004 Revised: April 2011 Purpose The purpose of the Reserve Fund Policy is

Department of Finance Policies and Procedures Reserve Funds Policy # Authorized by: City Council Date of issue: September 30, 2004 Revised: April 2011 Purpose The purpose of the Reserve Fund Policy is

REPORT TO THE CAPITAL REGIONAL DISTRICT BOARD MEETING OF WEDNESDAY, MARCH 25, 2014

REPORT TO THE CAPITAL REGIONAL DISTRICT BOARD MEETING OF WEDNESDAY, MARCH 25, 2014 SUBJECT: BYLAW NO. 4016 2015 2019 FINANCIAL PLAN, 2015 ISSUE The purpose of this report is to request approval of Bylaw

REPORT TO THE CAPITAL REGIONAL DISTRICT BOARD MEETING OF WEDNESDAY, MARCH 25, 2014 SUBJECT: BYLAW NO. 4016 2015 2019 FINANCIAL PLAN, 2015 ISSUE The purpose of this report is to request approval of Bylaw

TABLE OF CONTENTS SECTION 1 - OBJECTIVES AND GUIDING PRINCIPLES... 2 SECTION 2 - OPERATING AND CAPITAL RESERVE FUNDS... 3

RESERVE AND SURPLUS POLICY Date Policy Adopted: October 5, 2009 Date Policy Amended: December 7, 2009 Council Resolution Number: RC09/656 Council Resolution Number: RC09/781 TABLE OF CONTENTS SECTION 1

RESERVE AND SURPLUS POLICY Date Policy Adopted: October 5, 2009 Date Policy Amended: December 7, 2009 Council Resolution Number: RC09/656 Council Resolution Number: RC09/781 TABLE OF CONTENTS SECTION 1

CITY OF PRINCE RUPERT 2014 FIVE YEAR FINANCIAL PLAN BYLAW NO. 3345, 2014

CITY OF PRINCE RUPERT 2014 FIVE YEAR FINANCIAL PLAN BYLAW NO. 3345, 2014 A BYLAW FOR THE CITY OF PRINCE RUPERT RESPECTING THE FIVE YEAR FINANCIAL PLAN FOR THE PERIOD 2014-2018 The Council of the City of

CITY OF PRINCE RUPERT 2014 FIVE YEAR FINANCIAL PLAN BYLAW NO. 3345, 2014 A BYLAW FOR THE CITY OF PRINCE RUPERT RESPECTING THE FIVE YEAR FINANCIAL PLAN FOR THE PERIOD 2014-2018 The Council of the City of

STAFF REPORT TO COUNCIL

STAFF REPORT TO COUNCIL CORPORATE SERVICES TO: MAYOR AND COUNCIL DATE: April 11, 2011 TO: FROM: SUBJECT: Mayor and Council Sandra Stibrany, Manager Financial Services RCMP New Facility Temporary Financing

STAFF REPORT TO COUNCIL CORPORATE SERVICES TO: MAYOR AND COUNCIL DATE: April 11, 2011 TO: FROM: SUBJECT: Mayor and Council Sandra Stibrany, Manager Financial Services RCMP New Facility Temporary Financing

Financial Plan #203-301B

The Corporation of the Township of Whitewater Region Financial Plan #203-301B Cobden Drinking Water System Licence #203-101 Beachburg Drinking Water System Licence #203-102 Haley Drinking Water System

The Corporation of the Township of Whitewater Region Financial Plan #203-301B Cobden Drinking Water System Licence #203-101 Beachburg Drinking Water System Licence #203-102 Haley Drinking Water System

TOWN OF VIEW ROYAL BYLAW NO. 862

TOWN OF VIEW ROYAL BYLAW NO. 862 A BYLAW TO AUTHORIZE THE FINANCIAL PLAN FOR THE YEARS 20132017 The Council of the Town of View Royal, in open meeting assembled, enacts as follows: 1. This Bylaw may be

TOWN OF VIEW ROYAL BYLAW NO. 862 A BYLAW TO AUTHORIZE THE FINANCIAL PLAN FOR THE YEARS 20132017 The Council of the Town of View Royal, in open meeting assembled, enacts as follows: 1. This Bylaw may be

City of Pitt Meadows. Taxation - Townhall Meeting February 19, 2015

City of Pitt Meadows Taxation - Townhall Meeting February 19, 2015 Agenda Mayor s Welcome Property Tax Assessment Explained Budget & Business Planning Process Tax Calculation Process Budget Components

City of Pitt Meadows Taxation - Townhall Meeting February 19, 2015 Agenda Mayor s Welcome Property Tax Assessment Explained Budget & Business Planning Process Tax Calculation Process Budget Components

LONDON CORPORATE ASSET MANAGEMENT PLAN 2014

LONDON CORPORATE ASSET MANAGEMENT PLAN 2014 ACKNOWLEDGEMENT Acknowledgement The Corporate Asset Management office would like to acknowledge the efforts of the staff of the individual City of London Service

LONDON CORPORATE ASSET MANAGEMENT PLAN 2014 ACKNOWLEDGEMENT Acknowledgement The Corporate Asset Management office would like to acknowledge the efforts of the staff of the individual City of London Service

City Planning - Council's Improvement Strategy

Warringah Council Policy Policy No. Number 1 Purpose of Policy The purpose of this policy is to establish the strategic financial planning and sustainability framework to guide Council when developing

Warringah Council Policy Policy No. Number 1 Purpose of Policy The purpose of this policy is to establish the strategic financial planning and sustainability framework to guide Council when developing

The Corporation of the City of Nelson

The Corporation of the City of Nelson Agenda 1. Introduction 2. Council Priorities & Strategic Direction 3. 2012 2016 Financial Plan Process 4. Proposed 2012 2016 Financial Plan Presentation 5. City Assets/Reserves/Debt

The Corporation of the City of Nelson Agenda 1. Introduction 2. Council Priorities & Strategic Direction 3. 2012 2016 Financial Plan Process 4. Proposed 2012 2016 Financial Plan Presentation 5. City Assets/Reserves/Debt

Fiscal Impact Analysis of the Annexation Proposed by the Town of Beaumont. Leduc County FINAL REPORT

Fiscal Impact Analysis of the Annexation Proposed by the Town of Beaumont Leduc County FINAL REPORT Suite 2220 Sun Life Place 10123 99 Street Edmonton, Alberta T5J 3H1 T 780.425.6741 F 780.426.3737 www.think-applications.com

Fiscal Impact Analysis of the Annexation Proposed by the Town of Beaumont Leduc County FINAL REPORT Suite 2220 Sun Life Place 10123 99 Street Edmonton, Alberta T5J 3H1 T 780.425.6741 F 780.426.3737 www.think-applications.com

The Corporation of the District of Saanich. Introduction of the Draft 2016 2020 Financial Plan

1'11 U.0"1 -ri nqylc..e... sp cw Fell> 2.lll.o

1'11 U.0"1 -ri nqylc..e... sp cw Fell> 2.lll.o

2011 2015 Financial Plan

2011 2015 Financial Plan Committee of the Whole March 8, 2011 Service Budgets Review AIM for Results Review of Budget Process Proposed budget overview presented to the Committee of the Whole January 25

2011 2015 Financial Plan Committee of the Whole March 8, 2011 Service Budgets Review AIM for Results Review of Budget Process Proposed budget overview presented to the Committee of the Whole January 25

2014 ASSET MANAGEMENT PLAN Building, Stormwater & Linear Transportation

2014 ASSET MANAGEMENT PLAN Building, Stormwater & Linear Transportation Version 1 Table of Contents Executive Summary... 5 1.1 Background... 5 1.2 State of Local Infrastructure... 5 1.3 Desired Levels

2014 ASSET MANAGEMENT PLAN Building, Stormwater & Linear Transportation Version 1 Table of Contents Executive Summary... 5 1.1 Background... 5 1.2 State of Local Infrastructure... 5 1.3 Desired Levels

London District Catholic School Board. Consolidated Financial Statements August 31, 2014

London District Catholic School Board Consolidated Financial Statements August 31, 2014 MANAGEMENT REPORT Management s responsibility for the consolidated financial statements The accompanying consolidated

London District Catholic School Board Consolidated Financial Statements August 31, 2014 MANAGEMENT REPORT Management s responsibility for the consolidated financial statements The accompanying consolidated

Water Rate Study & O.Reg.453/07 Water Financial Plan No.103-301A

March 2, 2012 dfa DFA Infrastructure International Inc. dfa DFA Infrastructure International Inc. 33 Raymond Street St. Catharines Ontario Canada L2R 2T3 Telephone: (905) 938-0965 Fax: (905) 937-6568 March

March 2, 2012 dfa DFA Infrastructure International Inc. dfa DFA Infrastructure International Inc. 33 Raymond Street St. Catharines Ontario Canada L2R 2T3 Telephone: (905) 938-0965 Fax: (905) 937-6568 March

Halton District School Board

Report and consolidated financial statements of Halton District School Board Table of contents Management Report... 1 Independent Auditor s Report... 2-3 Consolidated statement of financial position...

Report and consolidated financial statements of Halton District School Board Table of contents Management Report... 1 Independent Auditor s Report... 2-3 Consolidated statement of financial position...

CITY OF TERRACE BYLAW NO. 2047 2014

CITY OF TERRACE BYLAW NO. 2047 2014 "A BYLAW TO ADOPT THE 2014-2018 FINANCIAL PLAN." WHEREAS pursuant to Section 165 of the Community Charter, being Chapter 26 of the Statutes of British Columbia, 2003,

CITY OF TERRACE BYLAW NO. 2047 2014 "A BYLAW TO ADOPT THE 2014-2018 FINANCIAL PLAN." WHEREAS pursuant to Section 165 of the Community Charter, being Chapter 26 of the Statutes of British Columbia, 2003,

2011-2015 Five-Year Financial Plan Public Consultation and Information Package

2011-2015 Five-Year Financial Plan Public Consultation and Information Package Community Charter s.166: A council must undertake a process of public consultation regarding the proposed financial plan before

2011-2015 Five-Year Financial Plan Public Consultation and Information Package Community Charter s.166: A council must undertake a process of public consultation regarding the proposed financial plan before

Mission, Vision and Values

Mission, Vision and Values The City of Greater Sudbury is a growing, world-class community bringing talent, technology and a great northern lifestyle together. We are committed to providing excellent access

Mission, Vision and Values The City of Greater Sudbury is a growing, world-class community bringing talent, technology and a great northern lifestyle together. We are committed to providing excellent access

In this chapter, we build on the basic knowledge of how businesses

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

CITY OF COLEMAN, TEXAS FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR'S REPORT SEPTEMBER 30, 2014

CITY OF COLEMAN, TEXAS FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR'S REPORT SEPTEMBER 30, 2014 Becky Roberts, CPA 104 Pine Street, Suite 610 Abilene, Texas 79601 325-665-5239 [email protected]

CITY OF COLEMAN, TEXAS FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR'S REPORT SEPTEMBER 30, 2014 Becky Roberts, CPA 104 Pine Street, Suite 610 Abilene, Texas 79601 325-665-5239 [email protected]

CITY OF STANFIELD OREGON Adopted Budget for Fiscal Year 2015/16

CITY OF STANFIELD OREGON Adopted Budget for Fiscal Year 2015/16 BUDGET COMMITTEE ELECTED OFFICIALS TERM EXPIRES Mayor: Thomas McCann December 2016 Council President Don Tyrrell December 2016 Councilor

CITY OF STANFIELD OREGON Adopted Budget for Fiscal Year 2015/16 BUDGET COMMITTEE ELECTED OFFICIALS TERM EXPIRES Mayor: Thomas McCann December 2016 Council President Don Tyrrell December 2016 Councilor

EXPENDITURES SUMMARY 2014 2015 INCREASE BUDGET BUDGET (DECREASE) (Restated) Over 2014

(Restated) Over 2014") EXPENDITURES SUMMARY 2014 2015 INCREASE (Restated) Over 2014 Mayor and Council 879,500 900,000 20,500 Office of Chief Administrative Officer 577,500 598,500 21,000 Clerks 1,727,500 1,635,000 (92,500) Legal

EXPENDITURES SUMMARY 2014 2015 INCREASE (Restated) Over 2014 Mayor and Council 879,500 900,000 20,500 Office of Chief Administrative Officer 577,500 598,500 21,000 Clerks 1,727,500 1,635,000 (92,500) Legal

Tax Increment Financing Policy

Tax Increment Financing Policy BLEDA Adopted May 12, 2014 City Council Adopted May 28, 2014 For the purpose of this policy, the "City" shall also mean the Big Lake Economic Development Authority (BLEDA),

Tax Increment Financing Policy BLEDA Adopted May 12, 2014 City Council Adopted May 28, 2014 For the purpose of this policy, the "City" shall also mean the Big Lake Economic Development Authority (BLEDA),

Debt Reduction Plan 2005 Debt Reduction and the Offshore Offset Agreement

Debt Reduction Plan 2005 Debt Reduction and the Offshore Offset Agreement Honourable Peter Christie Minister of Finance April 28, 2005 Contents Summary..................................1 Introduction...............................3

Debt Reduction Plan 2005 Debt Reduction and the Offshore Offset Agreement Honourable Peter Christie Minister of Finance April 28, 2005 Contents Summary..................................1 Introduction...............................3

Capital Financing and Debt Management Policy

Capital Financing and Debt Management Policy Policy Statement A policy governing the use and administration of capital financing and debt Purpose This policy establishes objectives, standards of care,

Capital Financing and Debt Management Policy Policy Statement A policy governing the use and administration of capital financing and debt Purpose This policy establishes objectives, standards of care,

City Budget - A Glossary of Useful Terms

26 SECTION 26 Glossary 273 Glossary Account - The primary accounting field in the budget used to describe the type of the financial transaction. Actual - Actual level of expenditures/fte positions approved

26 SECTION 26 Glossary 273 Glossary Account - The primary accounting field in the budget used to describe the type of the financial transaction. Actual - Actual level of expenditures/fte positions approved

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

APPENDIX C: GLOSSARY Accrued Benefit Obligation: Accrued Benefit Liability: Accrual Accounting: Accumulated amortization: Accumulated surplus:

APPENDIX C: GLOSSARY Accrued Benefit Obligation: see Employee Benefits Liability Gross. Accrued Benefit Liability: see Employee Benefits Liability Net. Accrual Accounting: the accrual basis of accounting

APPENDIX C: GLOSSARY Accrued Benefit Obligation: see Employee Benefits Liability Gross. Accrued Benefit Liability: see Employee Benefits Liability Net. Accrual Accounting: the accrual basis of accounting

CITY OF SAN JOSE 2015-2016 PROPOSED OPERATING BUDGET FUND DESCRIPTIONS

Airport Capital s CITY OF SAN JOSE These Enterprise s account for the Airport s capital expenditures and revenues and consist of the following: Airport Capital Improvement ; Airport Revenue Bond Improvement

Airport Capital s CITY OF SAN JOSE These Enterprise s account for the Airport s capital expenditures and revenues and consist of the following: Airport Capital Improvement ; Airport Revenue Bond Improvement

CONSOLIDATED STATEMENT OF INCOME

CONSOLIDATED STATEMENT OF INCOME 4 th quarter (a) 3 rd quarter 4 th quarter 2009 Sales 40,157 40,180 36,228 Excise taxes (4,397) (4,952) (4,933) Revenues from sales 35,760 35,228 31,295 Purchases, net

CONSOLIDATED STATEMENT OF INCOME 4 th quarter (a) 3 rd quarter 4 th quarter 2009 Sales 40,157 40,180 36,228 Excise taxes (4,397) (4,952) (4,933) Revenues from sales 35,760 35,228 31,295 Purchases, net

Brief Report on Closing of Accounts (connection) for the Term Ended March 31, 2007

for the Term Ended March 31, 2007") MARUHAN Co., Ltd. Brief Report on Closing of (connection) for the Term Ended March 31, 2007 (Amounts less than 1 million yen omitted) 1.Business Results for the term ended on March, 2007 (From April 1,

MARUHAN Co., Ltd. Brief Report on Closing of (connection) for the Term Ended March 31, 2007 (Amounts less than 1 million yen omitted) 1.Business Results for the term ended on March, 2007 (From April 1,

Strategy. Appendix A Debt. History and Background. Purpose of Review

Appendix A Debt Strategy History and Background During the late I 980s and the early I 990s, the City of Winnipeg incurred significant debt for capital purposes. In the mid-i 990s, the cost to service

Appendix A Debt Strategy History and Background During the late I 980s and the early I 990s, the City of Winnipeg incurred significant debt for capital purposes. In the mid-i 990s, the cost to service

TOWN OF RICHMOND HILL WATER AND WASTEWATER ONTARIO REGULATION 453/07 FINANCIAL PLAN

TOWN OF RICHMOND HILL WATER AND WASTEWATER ONTARIO REGULATION 453/07 FINANCIAL PLAN Financial Plan #022-301 JUNE 3, 2010 CONTENTS Page 1. INTRODUCTION 1.1 Study Purpose 1-1 1.2 Background 1-1 1.2.1 Financial

TOWN OF RICHMOND HILL WATER AND WASTEWATER ONTARIO REGULATION 453/07 FINANCIAL PLAN Financial Plan #022-301 JUNE 3, 2010 CONTENTS Page 1. INTRODUCTION 1.1 Study Purpose 1-1 1.2 Background 1-1 1.2.1 Financial

2012-2016 Business Plan Summary

Owner: 2012-2016 Business Plan Summary Program Corporate, Operational & Council Services Service grouping Financial Management Service Type Internal Service Larry Palarchio, Director of Financial Planning

Owner: 2012-2016 Business Plan Summary Program Corporate, Operational & Council Services Service grouping Financial Management Service Type Internal Service Larry Palarchio, Director of Financial Planning

JUSTICE INSTITUTE OF BRITISH COLUMBIA

Financial Statements of JUSTICE INSTITUTE OF BRITISH COLUMBIA ABCD KPMG LLP Chartered Accountants Box 10426, 777 Dunsmuir Street Vancouver BC V7Y 1K3 Telephone (604) 691-3000 Telefax (604) 691-3031 Internet

Financial Statements of JUSTICE INSTITUTE OF BRITISH COLUMBIA ABCD KPMG LLP Chartered Accountants Box 10426, 777 Dunsmuir Street Vancouver BC V7Y 1K3 Telephone (604) 691-3000 Telefax (604) 691-3031 Internet

Municipal Accounting Manual

Municipal Accounting Manual March 2013 Updated: November 2015 1 Table of Contents Introduction......1 Municipal Financial Statements Overview...... 2 Municipal financial statement purpose...... 2 Municipal

Municipal Accounting Manual March 2013 Updated: November 2015 1 Table of Contents Introduction......1 Municipal Financial Statements Overview...... 2 Municipal financial statement purpose...... 2 Municipal

If this information is required in an accessible format, please contact 1-800-372-1100 ext. 2305

If this information is required in an accessible format, please contact 1-800-372-1100 ext. 2305 The Regional Municipality of Durham Report to: The Finance & Administration Committee From: R.J. Clapp,

If this information is required in an accessible format, please contact 1-800-372-1100 ext. 2305 The Regional Municipality of Durham Report to: The Finance & Administration Committee From: R.J. Clapp,

Policies & Procedures

Budget and Business Plan 2015 Policies & Procedures POLICIES & PROCEDURES Policies & Procedures Presentation of Halton Region s Financial Information General Guidelines Halton Region prepares and presents

Budget and Business Plan 2015 Policies & Procedures POLICIES & PROCEDURES Policies & Procedures Presentation of Halton Region s Financial Information General Guidelines Halton Region prepares and presents

Consolidated results for the third Quarter Period in FY2014

Consolidated results for the third Quarter Period in FY2014 2014/2/7 Company Name Watami Co., Ltd. Listing: First Section of Tokyo Stock Exchange Code Number 7522 URL http://www.watami.co.jp/ Representative

Consolidated results for the third Quarter Period in FY2014 2014/2/7 Company Name Watami Co., Ltd. Listing: First Section of Tokyo Stock Exchange Code Number 7522 URL http://www.watami.co.jp/ Representative

1 What, Why and How? Best Management Practice: BMP D: Create a Long- Term Financial Plan. Meaning of Terms

Best Management Practice: BMP D: Create a Long- Term Financial Plan 1 What, Why and How? What is a long- term financial plan? A long- term financial plan estimates what your revenues and expenses will

Best Management Practice: BMP D: Create a Long- Term Financial Plan 1 What, Why and How? What is a long- term financial plan? A long- term financial plan estimates what your revenues and expenses will

Council Strategic Plan 2015-2018. squamish.ca

Council Strategic Plan 2015-2018 squamish.ca 2 Summary Our Council began their 2014 2018 term with a strategic planning exercise. The exercise identified a number of areas of focus for Council and directed

Council Strategic Plan 2015-2018 squamish.ca 2 Summary Our Council began their 2014 2018 term with a strategic planning exercise. The exercise identified a number of areas of focus for Council and directed

Table of Contents. WATER AND WASTEWATER MODEL AND SITUATIONAL ANALYSIS 6 Model Development 6 10-Year Water/WW - Challenges, Risks and Opportunities 7

Table of Contents LONG-RANGE FINANCIAL PLAN INTRODUCTION 1 Water and Wastewater Financial Plan 2 What is a Long Range Financial Plan 3 Importance of a Long Range Financial Plan 4 General Approach to Preparing

Table of Contents LONG-RANGE FINANCIAL PLAN INTRODUCTION 1 Water and Wastewater Financial Plan 2 What is a Long Range Financial Plan 3 Importance of a Long Range Financial Plan 4 General Approach to Preparing

UNDERSTANDING CANADIAN PUBLIC SECTOR FINANCIAL STATEMENTS

June 2014 UNDERSTANDING CANADIAN PUBLIC SECTOR FINANCIAL STATEMENTS www.bcauditor.com TABLE OF CONTENTS Who Will Find this Guide Helpful 3 What a Set of Public Sector Financial Statements Includes 5 The

June 2014 UNDERSTANDING CANADIAN PUBLIC SECTOR FINANCIAL STATEMENTS www.bcauditor.com TABLE OF CONTENTS Who Will Find this Guide Helpful 3 What a Set of Public Sector Financial Statements Includes 5 The

Description of Fund Types and Funds

Financial activities for local government fall into three broad categories, governmental, proprietary, and fiduciary fund categories. Governmental funds are used to account for activities primarily supported

Financial activities for local government fall into three broad categories, governmental, proprietary, and fiduciary fund categories. Governmental funds are used to account for activities primarily supported

City of Brantford Water and Wastewater Ontario Regulation 453/07 Financial Plans. Financial Plan #063-301

City of Brantford Water and Wastewater Ontario Regulation 453/07 Financial Plans Financial Plan #063-301 May 26, 2015 Contents Page EXECUTIVE SUMMARY (i) 1. Introduction... 1-1 1.1 Study Purpose... 1-1

City of Brantford Water and Wastewater Ontario Regulation 453/07 Financial Plans Financial Plan #063-301 May 26, 2015 Contents Page EXECUTIVE SUMMARY (i) 1. Introduction... 1-1 1.1 Study Purpose... 1-1

EXPENDITURES SUMMARY 2015 2016 INCREASE BUDGET BUDGET (DECREASE) Over 2015 $ $ $

Over 2015 $ $ $") EXPENDITURES SUMMARY 2015 2016 INCREASE Mayor and Council 900,000 900,000 - Office of Chief Administrative Officer 598,500 598,500 - Clerks 1,635,000 1,659,500 24,500 Legal Services 2,686,000 2,777,000

EXPENDITURES SUMMARY 2015 2016 INCREASE Mayor and Council 900,000 900,000 - Office of Chief Administrative Officer 598,500 598,500 - Clerks 1,635,000 1,659,500 24,500 Legal Services 2,686,000 2,777,000

STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

TOWN OF HARRISBURG NORTH CAROLINA TABLE OF CONTENTS June 30, 2006. Independent Auditor's Report 1-2. Management s Discussion and Analysis 3-12

TOWN OF HARRISBURG NORTH CAROLINA TABLE OF CONTENTS June 30, 2006 Exhibit Page FINANCIAL SECTION: Independent Auditor's Report 1-2 Management s Discussion and Analysis 3-12 Basis Financial Statements:

TOWN OF HARRISBURG NORTH CAROLINA TABLE OF CONTENTS June 30, 2006 Exhibit Page FINANCIAL SECTION: Independent Auditor's Report 1-2 Management s Discussion and Analysis 3-12 Basis Financial Statements:

Asset Management Plan

Asset Management Plan Final Report May 2014 EXECUTIVE SUMMARY Adequate municipal infrastructure such as roads, bridges, and underground water and sewage pipes are essential to economic development, citizen

Asset Management Plan Final Report May 2014 EXECUTIVE SUMMARY Adequate municipal infrastructure such as roads, bridges, and underground water and sewage pipes are essential to economic development, citizen

COMPREHENSIVE ASSET MANAGEMENT STRATEGY

COMPREHENSIVE ASSET MANAGEMENT STRATEGY APPROVED BY SENIOR MANAGEMENT COMMITTEE ON AUGUST 23, 2012 (TO BE FINALIZED AFTER APPROVAL OF CAM POLICY BY COUNCIL) August 2012 Contents CONTENTS EXECUTIVE SUMMARY

COMPREHENSIVE ASSET MANAGEMENT STRATEGY APPROVED BY SENIOR MANAGEMENT COMMITTEE ON AUGUST 23, 2012 (TO BE FINALIZED AFTER APPROVAL OF CAM POLICY BY COUNCIL) August 2012 Contents CONTENTS EXECUTIVE SUMMARY

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods TABLE OF CONTENTS

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods 1.0 FINANCIAL FORECASTING METHODS 1.01 Introduction

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods 1.0 FINANCIAL FORECASTING METHODS 1.01 Introduction

Additional Revision to Brief Report of Settlement of Accounts for Full Fiscal Year Ending March 31, 2007

June 22, 2007 Company Name: ARUZE CORP. Name and Title of Representative: Kunihiko Yogo Representative Director and CEO (JASDAQ Code: 6425) Contact: Norihisa Kiriu General Manager Finance and Accounting

June 22, 2007 Company Name: ARUZE CORP. Name and Title of Representative: Kunihiko Yogo Representative Director and CEO (JASDAQ Code: 6425) Contact: Norihisa Kiriu General Manager Finance and Accounting

Budget Process. Budget Calendar. The City s fiscal year is July 1 through June 30.

Budget Process The City s fiscal year is July 1 through June 30. To establish the budget, the Finance Department develops a plan for expenditure of projected available resources for the coming fiscal year.

Budget Process The City s fiscal year is July 1 through June 30. To establish the budget, the Finance Department develops a plan for expenditure of projected available resources for the coming fiscal year.

PART C: GENERAL BUSINESS CREDIT

PART C: GENERAL BUSINESS CREDIT 15. CREDIT FOR INVESTING IN PROPERTY IN SOUTH CAROLINA South Carolina Code 12-14-60 allows a taxpayer a credit against income taxes for qualified manufacturing and productive

PART C: GENERAL BUSINESS CREDIT 15. CREDIT FOR INVESTING IN PROPERTY IN SOUTH CAROLINA South Carolina Code 12-14-60 allows a taxpayer a credit against income taxes for qualified manufacturing and productive

How To Vote On A School Board In Louisiana

1. Call to order and roll call. PRELIMINARY NOTICE AND AGENDA STATE BOND COMMISSION MEETING OF OCTOBER 15, 2015 10:00 A.M. - SENATE COMMITTEE ROOM A STATE CAPITOL BUILDING 2. Approval of the minutes of

1. Call to order and roll call. PRELIMINARY NOTICE AND AGENDA STATE BOND COMMISSION MEETING OF OCTOBER 15, 2015 10:00 A.M. - SENATE COMMITTEE ROOM A STATE CAPITOL BUILDING 2. Approval of the minutes of

The Town of Fort Frances

The Town of Fort Frances Long-Term Capital Financial Plan POLICY Resolution Number: 391 (Consent) 12/09 SECTION ADMINISTRATION AND FINANCE NEW: December 2009 REVISED: Supercedes Resolution No. Policy Number:

The Town of Fort Frances Long-Term Capital Financial Plan POLICY Resolution Number: 391 (Consent) 12/09 SECTION ADMINISTRATION AND FINANCE NEW: December 2009 REVISED: Supercedes Resolution No. Policy Number:

BRITISH COLUMBIA TRANSIT

Audited Financial Statements of BRITISH COLUMBIA TRANSIT Years ended March 31, 2005 and 2004 AUDITOR S REPORT BC TRANSIT 41 REPORT OF MANAGEMENT Years ended March 31, 2005 and 2004 The financial statements

Audited Financial Statements of BRITISH COLUMBIA TRANSIT Years ended March 31, 2005 and 2004 AUDITOR S REPORT BC TRANSIT 41 REPORT OF MANAGEMENT Years ended March 31, 2005 and 2004 The financial statements

VANCOUVER COMMUNITY COLLEGE

Financial Statements of VANCOUVER COMMUNITY COLLEGE KPMG Enterprise Metrotower II 4720 Kingsway, Suite 2400 Burnaby, BC V5H 4N2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 Internet www.kpmg.ca/enterprise

Financial Statements of VANCOUVER COMMUNITY COLLEGE KPMG Enterprise Metrotower II 4720 Kingsway, Suite 2400 Burnaby, BC V5H 4N2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 Internet www.kpmg.ca/enterprise