How To Guarantee A Loan

|

|

|

- Annice Bailey

- 5 years ago

- Views:

Transcription

1 Government Guaranteed Loan Participations & Pooled Securities

2 Small Business Guaranteed Loans SBA 7(a) Owner occupied real estate, working capital & equipment Up to $5MM, 25 YR, 75% - 85% guarantee USDA Business & Industry Rural area real estate, working capital & equipment Up to $10MM, 30 YR, 60 80% guarantee FSA Farm Ownership & Operating Farm ownership, livestock, equipment & operating loans Up to $1.302MM, 40 YR, 90% guarantee 2

3 You may be thinking.. Aren t SBA loans for borrowers with questionable credit? They can t even qualify for a conventional loan! 3

4 Guaranteed vs. Conventional Longer term loan meets lender s DSCR requirement; borrower prefers lower payment Specialized collateral represents inadequate liquidation value Lender doesn t have available capital or liquidity without government guarantee 4

5 What is the Nature of the Government Guaranteed Portion of an SBA 7(a) or USDA Loan? Depends on who is asking 5

6 Originating Lender Guarantee is conditional : may be compromised or lost if underwriting or servicing is not SBA/USDA compliant Guaranteed portion is not counted as a MBL and therefore not counted toward aggregate business lending cap (Part 723.1(b)(4)) 6

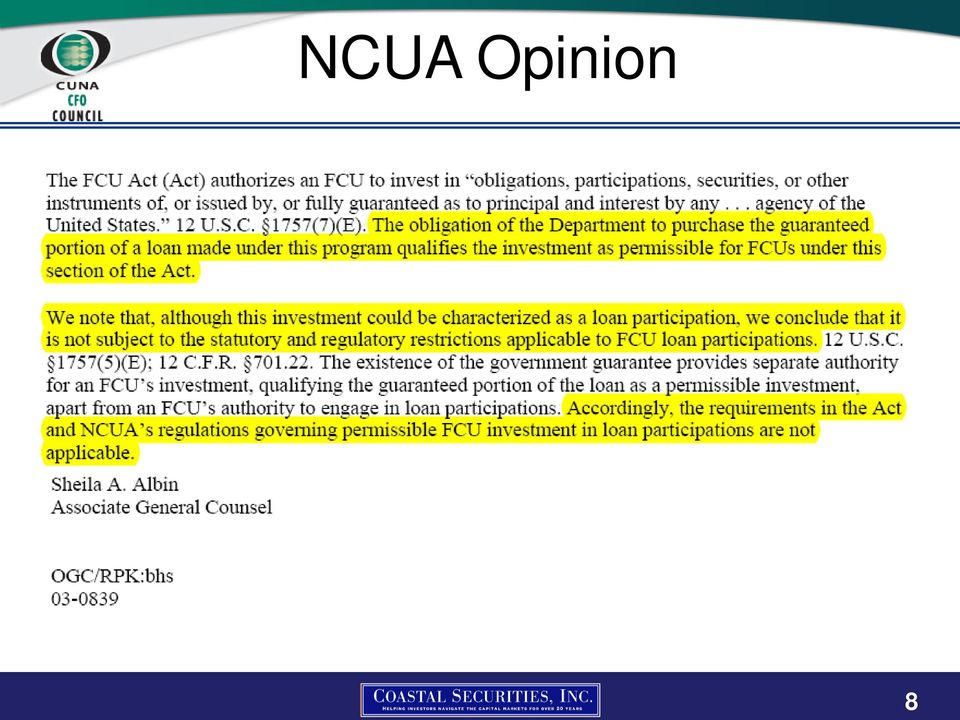

7 Secondary Market Investor Investor purchasing guaranteed portion receives an unconditional guarantee from the government Per NCUA General Counsel Opinion, the unconditional government guarantee transforms this loan participation into a permissible investment 7

8 NCUA Opinion 8

9 Participations vs. Guaranteed Loans Unguaranteed Loan Participations Secondary Market Guaranteed Loans Primary Risk Credit Risk Premium Risk Counterparty Risk Yes No Loan Underwriting Regulatory Full underwriting required Lending regulatory restrictions apply No credit review; evaluated more like a security Permissible investment; can be characterized as loan, not subject to participation & MBL regs Liquidity Limited Established active secondary market 9

10 Guaranteed Pools & Loans SBA 7(a) Pool Security SBA/USDA/FSA Loan Risk Premium Risk Premium Risk Guarantee Full Faith & Credit ; timely pay Full Faith & Credit Characteristics Multiple underlying loans Single loan Coupon M or Q reset (very few Fixed) No periodic cap/floor Indexed to Prime, LIBOR M, Q, Odd reset & Fixed With/without cap/floor Indices vary Payment Freq Monthly Pro Rata Pass Thru Monthly, Annual, etc Prepay Penalty 5/3/1 for loans >15YR; does not pass through to investor Wide Range, passes through to investor Settlement DTC Eligible (CUSIP) Physical Delivery 10

Physical Delivery")

11 Payment Flow Borrower $ Lender is servicer $ Investor Borrower $ Lender is servicer FTA $ Investor 11

12 What Happens if Loan Defaults? Demand can be made to originating lender when loan is 60 days in arrears If lender does not repurchase loan, demand is made to the Agency Interest will accrue up to 90 days from date of original demand letter to lender (USDA) or will not typically exceed 120 days from last interest paid-to date (SBA) 12

or will not typically")

13 Evaluating a Guaranteed Loan USDA Brecht Loan Annual Pay 2.18% % Net Fixed 3.25% Gross Fixed 12/12 Note; 12/23 Premium 13

14 SBA Pool Security SBA Pool Annual Pay P+.825% (4.075%) 15/15 Loans 1/13 Issue Date Monthly Reset 4/ Premium 14

15 Loan & Pool Examples Description Coupon Prepay Penalty M Adj Pool (P+.825%) 5YR Fixed/Q Adj Loan 4.75% (P+1.50%) 5YR Adj Loan 4.325% (P+1.075%) 5YR Adj Loan 2.75% (FM5+0%) Fixed Rate Loan Fixed Rate Loan Rem Term Prem BEY@ 5YR 10CPR 10 YR % 10/..3/2/1 25 YR % 2.47% 5/3/1 30 YR % 2.52% 17 YR % 1.89% 6.00% 10/..3/2/1 30 YR % 3.51% 3.975% 5/3/1 15 YR % 2.49% 15

16 You may be thinking.. Those loans to small businesses.. they are going bankrupt tomorrow! You are going to pay WHAT in premium??...those are going to payoff tomorrow! 16

17 Voluntary vs. Defaults Default $ 37% Voluntary $ 63% Source: SBA, Coastal Securities Monthly Prepayment Research Report

18 SBA Pool Historical CPR Recent speeds are ~ 50% of the long term CPR averages Source: SBA, Coastal Securities 4-13 factors 18

19 MBS Prepayment Comparison Max Avg Min σ G2AR G2AR YR SBA YR SBA SBA Pools exhibit ~50% the average 3-Mo CPR with 50% or less volatility than GNMA ARMs 19

20 Rate Shock Impact on Price As of 3/

21 Now from the Experts! Greg Gibson CFO/COO Northwest Federal Credit Union Cory Schwab VP Commercial and Secondary Market Loans Patelco Credit Union 21

22 Greg s 10 Commandments of GGLs 1. Do your homework, know the asset class and your goals 2. Know your balance sheet and make sure SBAs fit 3. Understand the risks GGLs mitigate and those they add 4. If you only dip your toe, you may end up getting a bath 5. Premiums command respect not necessarily fear 6. Know the major poolers for best supply and price 7. Compare product characteristics, pools vs. whole loans, SBA vs USDA, 7a vs 504 and find the best fit 8. Don t view these assets as BAGBD (buy and go brain dead) 9. GGL markets are cyclical, know entry and exit points 10. Proverbs 15:22

23 Coastal Securities Contacts Gerry Bennett Margaret Gilbert

24 Disclaimer Nothing contained herein is an offer to sell or the solicitation of an offer to buy any financial instrument. The opinions and recommendations presented do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own independent decisions regarding any securities or financial instruments mentioned herein and seek professional advice, including tax and accounting advice. Any indications of market valuation contained herein are based on current information that we consider reliable, but we do not guarantee it is accurate or complete and users should make whatever additional determinations of market value they deem appropriate. All assumptions, opinions and estimates constitute Coastal Securities Inc. s (CSI) judgment as of this date and, along with prices and yields, are subject to change without notice. Past performance is not indicative of future results. The yield and/or average life shown on loans, SBA pools, CMOs or mortgage backed securities consider prepayment assumptions that may or may not be met. Changes in prepayments may significantly affect yield and/or average life. CSI does not accept orders or instructions transmitted via or left on any phone voice or text mail system. Please be aware that communications received by or sent from our system are not confidential and subject to review by supervisory personnel. 23

How To Sell An Sba Loan At A Premium

Selling Your Small Business Administration (SBA) Loans To Coastal Securities March 2014 The Role of the Lending Bank Lending Bank - retains customer relationship as they continue to service their SBA loans.

Selling Your Small Business Administration (SBA) Loans To Coastal Securities March 2014 The Role of the Lending Bank Lending Bank - retains customer relationship as they continue to service their SBA loans.

Selling Your Small Business Administration (SBA) Loans To Coastal Securities. First Quarter 2015

Loans To Coastal Securities. First Quarter 2015") Selling Your Small Business Administration (SBA) Loans To Coastal Securities First Quarter 2015 The Role of the Lending Bank Lending Bank - retains customer relationship as they continue to service their

Selling Your Small Business Administration (SBA) Loans To Coastal Securities First Quarter 2015 The Role of the Lending Bank Lending Bank - retains customer relationship as they continue to service their

Government Guaranteed Business Lending

Government Guaranteed Business Lending Ideally suited to the mission of CU s to satisfy their members business loan needs Herb White, VP of Lending, Hudson Valley FCU Margaret Gilbert, Managing Director,

Government Guaranteed Business Lending Ideally suited to the mission of CU s to satisfy their members business loan needs Herb White, VP of Lending, Hudson Valley FCU Margaret Gilbert, Managing Director,

SBA 7(a) Government. Guaranteed Loan Program

Government. Guaranteed Loan Program") SBA 7(a) Government Guaranteed Loan Program SBA Overview The U.S. Small Business Administration (SBA) Was Created By Congress In 1953 To Assist And Counsel Small Business Growth And Prosperity, Thereby

SBA 7(a) Government Guaranteed Loan Program SBA Overview The U.S. Small Business Administration (SBA) Was Created By Congress In 1953 To Assist And Counsel Small Business Growth And Prosperity, Thereby

Best Practices in Asset Liability Management

Best Practices in Asset Liability Management Frank Wilary Principal Wilary Winn LLC September 22, 2014 1 Topics Covered Best practices related to ALM modeling Best practices related to managing the ALM

Best Practices in Asset Liability Management Frank Wilary Principal Wilary Winn LLC September 22, 2014 1 Topics Covered Best practices related to ALM modeling Best practices related to managing the ALM

Graduate School of Colorado SBA lending Presentation

Graduate School of Colorado SBA lending Presentation SBA lending course summary The course will provide an overview and comparison of SBA 7a, SBA 504 and USDA Business & Industry (B&I) loan programs. SBA

Graduate School of Colorado SBA lending Presentation SBA lending course summary The course will provide an overview and comparison of SBA 7a, SBA 504 and USDA Business & Industry (B&I) loan programs. SBA

MORTGAGE BACKED SECURITIES

MORTGAGE BACKED SECURITIES A Mortgage-Backed Security is created when the issuing Agency purchases a number of investment quality residential home mortgages from various banks, thrifts, or mortgage companies.

MORTGAGE BACKED SECURITIES A Mortgage-Backed Security is created when the issuing Agency purchases a number of investment quality residential home mortgages from various banks, thrifts, or mortgage companies.

Ginnie Mae HMBS Monthly Loan Level Disclosure Definitions Version 2.2

Ginnie Mae HMBS Monthly Loan Level Disclosure Definitions Version 2.2 The following four Sections provide the definitions, calculations, and descriptions of the data elements under Ginnie Mae s HMBS Monthly

Ginnie Mae HMBS Monthly Loan Level Disclosure Definitions Version 2.2 The following four Sections provide the definitions, calculations, and descriptions of the data elements under Ginnie Mae s HMBS Monthly

SBA 504 Non Bank Business Model. Presented by Sok Cordell

SBA 504 Non Bank Business Model Presented by Sok Cordell CH Capital Partners LLC (SBA Non Bank Lending Program) The information contained in this presentation has been obtained from sources believed to

SBA 504 Non Bank Business Model Presented by Sok Cordell CH Capital Partners LLC (SBA Non Bank Lending Program) The information contained in this presentation has been obtained from sources believed to

Ginnie Mae MBS Loan-Level Disclosure Definitions Version 1.4

The following four sections provide the definitions, calculations, and descriptions of the data elements under Ginnie Mae s MBS Loan-Level Disclosure: Section # Section Name 1 Definition of Terms 2 Definitions

The following four sections provide the definitions, calculations, and descriptions of the data elements under Ginnie Mae s MBS Loan-Level Disclosure: Section # Section Name 1 Definition of Terms 2 Definitions

Overview of GNMA Reverse Mortgage Backed Securities (HMBS) Evaluations

Evaluations") Overview of GNMA Reverse Mortgage Backed Securities (HMBS) Evaluations April 8, 2010 Matthew Brodin, Director-Evaluated Services Lynn Barry, Manager-Structured Group Interactive Data Pricing and Reference

Overview of GNMA Reverse Mortgage Backed Securities (HMBS) Evaluations April 8, 2010 Matthew Brodin, Director-Evaluated Services Lynn Barry, Manager-Structured Group Interactive Data Pricing and Reference

SMALL BUSINESS LENDING OPPORTUNITIES FOR CREDIT UNIONS

SMALL BUSINESS LENDING OPPORTUNITIES FOR CREDIT UNIONS February 14, 2012 Terrence K. McHugh President Commercial Alliance 1 Business Lending in Credit Unions 1998 regulation limits business lending in

SMALL BUSINESS LENDING OPPORTUNITIES FOR CREDIT UNIONS February 14, 2012 Terrence K. McHugh President Commercial Alliance 1 Business Lending in Credit Unions 1998 regulation limits business lending in

Mortgage-Related Securities

Raymond James Michael West, CFP, WMS Vice President Investments 101 West Camperdown Way Suite 600 Greenville, SC 29601 864-370-2050 x 4544 864-884-3455 [email protected] www.westwealthmanagement.com

Raymond James Michael West, CFP, WMS Vice President Investments 101 West Camperdown Way Suite 600 Greenville, SC 29601 864-370-2050 x 4544 864-884-3455 [email protected] www.westwealthmanagement.com

Summary of Mortgage Servicing Rules

February 12, 2013 Summary of Mortgage Servicing Rules The Consumer Financial Protection Bureau (CFPB) released its final rules on mortgage loan servicing on January 17, 2013. These new national standards

February 12, 2013 Summary of Mortgage Servicing Rules The Consumer Financial Protection Bureau (CFPB) released its final rules on mortgage loan servicing on January 17, 2013. These new national standards

COMMUNITY ADVANTAGE. Pilot Program Opportunity. Pilot program launched in February of 2011

COMMUNITY ADVANTAGE Pilot Program Opportunity Community Advantage History Pilot program launched in February of 2011 Pilot ends March 15, 2014 but may be extended dd or made permanent After initial launch,

COMMUNITY ADVANTAGE Pilot Program Opportunity Community Advantage History Pilot program launched in February of 2011 Pilot ends March 15, 2014 but may be extended dd or made permanent After initial launch,

Investing in Government Guaranteed Loans

IBI Credit Union Services Presents Investing in Government Guaranteed Loans The Risks and Benefits for Credit Unions 2011 By Timothy E. Thomas and Jared Livingston Our Objectives The purpose of this White

IBI Credit Union Services Presents Investing in Government Guaranteed Loans The Risks and Benefits for Credit Unions 2011 By Timothy E. Thomas and Jared Livingston Our Objectives The purpose of this White

Managing the Investment Portfolio

Managing the Investment Portfolio GSBC Executive Development Institute April 26, 2015 Portfolio Purpose & Objectives Tale of Two Balance Sheets o Components of Core Balance Sheet Originated loans Retail

Managing the Investment Portfolio GSBC Executive Development Institute April 26, 2015 Portfolio Purpose & Objectives Tale of Two Balance Sheets o Components of Core Balance Sheet Originated loans Retail

Mortgage-backed Securities

MÄLARDALEN UNIVERSITY PROJECT DEPARTMENT OF MATHEMATICS AND PHYSICS ANALYTICAL FINANCE, MT 1411 TEACHER: JAN RÖMAN 2004-12-16 Mortgage-backed Securities GROUP : CAROLINA OLSSON REBECCA NYGÅRDS-KERS ABSTRACT

MÄLARDALEN UNIVERSITY PROJECT DEPARTMENT OF MATHEMATICS AND PHYSICS ANALYTICAL FINANCE, MT 1411 TEACHER: JAN RÖMAN 2004-12-16 Mortgage-backed Securities GROUP : CAROLINA OLSSON REBECCA NYGÅRDS-KERS ABSTRACT

GLOSSARY OF TERMS. Amortization Repayment of a debt in regular installments of principal and interest, rather than interest only payments

GLOSSARY OF TERMS Ability to Repay (ATR) The Ability to Repay rule protects consumers from taking on mortgages that exceed their financial means, by mandating the documentation / proof of income and assets.

GLOSSARY OF TERMS Ability to Repay (ATR) The Ability to Repay rule protects consumers from taking on mortgages that exceed their financial means, by mandating the documentation / proof of income and assets.

HMBS Overview. Ginnie Mae s Program to Securitize Government Insured Home Equity Conversion Mortgages

HMBS Overview Ginnie Mae s Program to Securitize Government Insured Home Equity Conversion Mortgages Table of Contents Tab A: Program Overview Tab B: Home Equity Conversion Mortgage (HECM) Trends Tab C:

HMBS Overview Ginnie Mae s Program to Securitize Government Insured Home Equity Conversion Mortgages Table of Contents Tab A: Program Overview Tab B: Home Equity Conversion Mortgage (HECM) Trends Tab C:

Government National Mortgage Association

Prospectus Supplement (To Base Prospectus dated July 1, 2011) [Fixed Rate Collateral] Government National Mortgage Association $35,728,686.00 4.500 Ginnie Mae II Home Equity Conversion Mortgage-Backed

Prospectus Supplement (To Base Prospectus dated July 1, 2011) [Fixed Rate Collateral] Government National Mortgage Association $35,728,686.00 4.500 Ginnie Mae II Home Equity Conversion Mortgage-Backed

Appendix D: Questions and Answers Section 120. Questions and Answers on Risk Weighting 1-to-4 Family Residential Mortgage Loans

Questions and Answers on Risk Weighting 1-to-4 Family Residential Mortgage Loans 1. When do 1-to-4 family residential mortgages receive 100% risk weight? Any 1-to-4 family residential mortgage loan that

Questions and Answers on Risk Weighting 1-to-4 Family Residential Mortgage Loans 1. When do 1-to-4 family residential mortgages receive 100% risk weight? Any 1-to-4 family residential mortgage loan that

Financing Residential Real Estate. Lesson 12: VA-Guaranteed Loans

Financing Residential Real Estate Lesson 12: VA-Guaranteed Loans Introduction In this lesson we will cover: characteristics of VA loans, eligibility requirements, VA guaranty, VA loan amounts, and underwriting

Financing Residential Real Estate Lesson 12: VA-Guaranteed Loans Introduction In this lesson we will cover: characteristics of VA loans, eligibility requirements, VA guaranty, VA loan amounts, and underwriting

First Industries Fund

First Industries Fund First Industries is one of 19 programs in the June 2004 economic stimulus package. It provides $100 million for agriculture, and $50 million for tourism. Final guidelines were approved

First Industries Fund First Industries is one of 19 programs in the June 2004 economic stimulus package. It provides $100 million for agriculture, and $50 million for tourism. Final guidelines were approved

Structured Financial Products

Structured Products Structured Financial Products Bond products created through the SECURITIZATION Referred to the collection of Mortgage Backed Securities Asset Backed Securities Characteristics Assets

Structured Products Structured Financial Products Bond products created through the SECURITIZATION Referred to the collection of Mortgage Backed Securities Asset Backed Securities Characteristics Assets

MORTGAGE TERMS. Assignment of Mortgage A document used to transfer ownership of a mortgage from one party to another.

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

Static Pool Analysis: Evaluation of Loan Data and Projections of Performance March 2006

Static Pool Analysis: Evaluation of Loan Data and Projections of Performance March 2006 Introduction This whitepaper provides examiners with a discussion on measuring and predicting the effect of vehicle

Static Pool Analysis: Evaluation of Loan Data and Projections of Performance March 2006 Introduction This whitepaper provides examiners with a discussion on measuring and predicting the effect of vehicle

Debt Refinancing Under the 7(a) Program. Lynn G. Ozer Executive Vice President Government Guaranteed Lending

Program. Lynn G. Ozer Executive Vice President Government Guaranteed Lending") Debt Refinancing Under the 7(a) Program Lynn G. Ozer Executive Vice President Government Guaranteed Lending Debt Refinancing SBA-guaranteed loan proceeds may not be used to refinance debt originally used

Debt Refinancing Under the 7(a) Program Lynn G. Ozer Executive Vice President Government Guaranteed Lending Debt Refinancing SBA-guaranteed loan proceeds may not be used to refinance debt originally used

CONFERENCE OF STATE BANK SUPERVISORS AMERICAN ASSOCIATION OF RESIDENTIAL MORTGAGE REGULATORS NATIONAL ASSOCIATION OF CONSUMER CREDIT ADMINISTRATORS

CONFERENCE OF STATE BANK SUPERVISORS AMERICAN ASSOCIATION OF RESIDENTIAL MORTGAGE REGULATORS NATIONAL ASSOCIATION OF CONSUMER CREDIT ADMINISTRATORS STATEMENT ON SUBPRIME MORTGAGE LENDING I. INTRODUCTION

CONFERENCE OF STATE BANK SUPERVISORS AMERICAN ASSOCIATION OF RESIDENTIAL MORTGAGE REGULATORS NATIONAL ASSOCIATION OF CONSUMER CREDIT ADMINISTRATORS STATEMENT ON SUBPRIME MORTGAGE LENDING I. INTRODUCTION

SBA and USDA Lending 1/28/2014. Benefits of SBA Financing. Small Business Administration and United State Department of Agriculture

SBA and USDA Lending Small Business Administration and United State Department of Agriculture Work in Partnership with Banks Encourage Banks to Lend to Businesses by Guaranteeing loans to reduce Lender

SBA and USDA Lending Small Business Administration and United State Department of Agriculture Work in Partnership with Banks Encourage Banks to Lend to Businesses by Guaranteeing loans to reduce Lender

The SBA 504 Program: Details, Benefits, Challenges and How to Get Involved

The SBA 504 Program: Details, Benefits, Challenges and How to Get Involved January 29, 2015 Mark Abell, SVP & SBA Division Manager Vectra Bank Colorado What do you picture when you hear Small Business?

The SBA 504 Program: Details, Benefits, Challenges and How to Get Involved January 29, 2015 Mark Abell, SVP & SBA Division Manager Vectra Bank Colorado What do you picture when you hear Small Business?

9. Structured Products Settlement Procedures

9. Structured Products Settlement Procedures Chapter 9 Structured Products Settlement Procedures A. The Securities Industry and Financial Markets Association Recommended Settlement Guidelines for Secondary

9. Structured Products Settlement Procedures Chapter 9 Structured Products Settlement Procedures A. The Securities Industry and Financial Markets Association Recommended Settlement Guidelines for Secondary

USDA Rural Development/Special Loan Servicing

Guidance Lender (Loan Holder/Loan Servicer) Borrowers USDA Rural Development/Special Loan Servicing The Lender must be a Section 502 Single Family Housing Guaranteed Loan Program approved Lender. The current

Guidance Lender (Loan Holder/Loan Servicer) Borrowers USDA Rural Development/Special Loan Servicing The Lender must be a Section 502 Single Family Housing Guaranteed Loan Program approved Lender. The current

W i n t r u s t B a n k

W i n t r u s t B a n k 1 WHO ARE WE Wintrust Financial is a financial services holding company We provide traditional community banking services, commercial banking, wealth management, commercial insurance

W i n t r u s t B a n k 1 WHO ARE WE Wintrust Financial is a financial services holding company We provide traditional community banking services, commercial banking, wealth management, commercial insurance

MORTGAGE BANKING TERMS

MORTGAGE BANKING TERMS Acquisition cost: Add-on interest: In a HUD/FHA transaction, the price the borrower paid for the property plus any of the following costs: closing, repairs, or financing (except

MORTGAGE BANKING TERMS Acquisition cost: Add-on interest: In a HUD/FHA transaction, the price the borrower paid for the property plus any of the following costs: closing, repairs, or financing (except

Assumable mortgage: A mortgage that can be transferred from a seller to a buyer. The buyer then takes over payment of an existing loan.

MORTGAGE GLOSSARY Adjustable Rate Mortgage (ARM): A mortgage loan with payments usually lower than a fixed rate initially, but is subject to changes in interest rates. There are a variety of ARMs that

MORTGAGE GLOSSARY Adjustable Rate Mortgage (ARM): A mortgage loan with payments usually lower than a fixed rate initially, but is subject to changes in interest rates. There are a variety of ARMs that

Solomon Hess SBA Management LLC 4301 North Fairfax Drive Arlington VA 22203 703.356.3333 www.solomonhess.com March 19, 2014

Item 1 Cover Page Solomon Hess SBA Management LLC 4301 North Fairfax Drive Arlington VA 22203 703.356.3333 www.solomonhess.com March 19, 2014 Form ADV, Part 2; our Disclosure Brochure or Brochure as required

Item 1 Cover Page Solomon Hess SBA Management LLC 4301 North Fairfax Drive Arlington VA 22203 703.356.3333 www.solomonhess.com March 19, 2014 Form ADV, Part 2; our Disclosure Brochure or Brochure as required

ADVISORSHARES YIELDPRO ETF (NASDAQ Ticker: YPRO) SUMMARY PROSPECTUS November 1, 2015

SUMMARY PROSPECTUS November 1, 2015") ADVISORSHARES YIELDPRO ETF (NASDAQ Ticker: YPRO) SUMMARY PROSPECTUS November 1, 2015 Before you invest in the AdvisorShares Fund, you may want to review the Fund s prospectus and statement of additional

ADVISORSHARES YIELDPRO ETF (NASDAQ Ticker: YPRO) SUMMARY PROSPECTUS November 1, 2015 Before you invest in the AdvisorShares Fund, you may want to review the Fund s prospectus and statement of additional

Mortgage loans and mortgage-backed securities

Mortgage loans and mortgage-backed securities Mortgages A mortgage loan is a loan secured by the collateral of some specific real estate property which obliges the borrower to make a predetermined series

Mortgage loans and mortgage-backed securities Mortgages A mortgage loan is a loan secured by the collateral of some specific real estate property which obliges the borrower to make a predetermined series

The Mortgage Market. Concepts and Buzzwords. Readings. Tuckman, chapter 21.

The Mortgage Market Concepts and Buzzwords The Mortgage Market The Basic Fixed Rate Mortgage Prepayments mortgagor, mortgagee, PTI and LTV ratios, fixed-rate, GPM, ARM, balloon, GNMA, FNMA, FHLMC, Private

The Mortgage Market Concepts and Buzzwords The Mortgage Market The Basic Fixed Rate Mortgage Prepayments mortgagor, mortgagee, PTI and LTV ratios, fixed-rate, GPM, ARM, balloon, GNMA, FNMA, FHLMC, Private

ESCROW REQUIREMENTS UNDER TILA

Overview Escrow Requirements Reg. Z High Cost Mortgage and Counseling - Reg. Z & X Ability to Repay & Qualified Mortgages Reg. Z & X Mortgage Servicing Reg. Z & X Loan Originator Compensation Reg. Z Copies

Overview Escrow Requirements Reg. Z High Cost Mortgage and Counseling - Reg. Z & X Ability to Repay & Qualified Mortgages Reg. Z & X Mortgage Servicing Reg. Z & X Loan Originator Compensation Reg. Z Copies

PWM Structured Solutions. May 2011

PWM Structured Solutions May 2011 Payout at (%) Euro Put Option Iterations Key Features Hypothetical Payoff at (assuming 5.64% premium) Trade: Client Buys European Style OTC Put Option Underlyer: EURUSD

PWM Structured Solutions May 2011 Payout at (%) Euro Put Option Iterations Key Features Hypothetical Payoff at (assuming 5.64% premium) Trade: Client Buys European Style OTC Put Option Underlyer: EURUSD

Traditional Life Insurance Premium Financing

Traditional Life Insurance Premium Financing Cascade Wealth Preservation is the advanced planning destination. For years, high net worth individuals have faced the challenge of weighing the need to purchase

Traditional Life Insurance Premium Financing Cascade Wealth Preservation is the advanced planning destination. For years, high net worth individuals have faced the challenge of weighing the need to purchase

STATE OF NEW JERSEY DEPARTMENT OF BANKING AND INSURANCE STATEMENT ON SUBPRIME MORTGAGE LENDING

STATE OF NEW JERSEY DEPARTMENT OF BANKING AND INSURANCE STATEMENT ON SUBPRIME MORTGAGE LENDING I. INTRODUCTION AND BACKGROUND On June 29, 2007, the Federal Deposit Insurance Corporation (FDIC), the Board

STATE OF NEW JERSEY DEPARTMENT OF BANKING AND INSURANCE STATEMENT ON SUBPRIME MORTGAGE LENDING I. INTRODUCTION AND BACKGROUND On June 29, 2007, the Federal Deposit Insurance Corporation (FDIC), the Board

Glossary of Common Derivatives Terms

DRAFT: 10/03/07 Glossary of Common Derivatives Terms American Depository Receipts (ADRs). ADRs are receipts issued by a U.S. bank or trust company evidencing its ownership of underlying foreign securities.

DRAFT: 10/03/07 Glossary of Common Derivatives Terms American Depository Receipts (ADRs). ADRs are receipts issued by a U.S. bank or trust company evidencing its ownership of underlying foreign securities.

Recourse vs. Nonrecourse: Commercial Real Estate Financing Which One is Right for You?

Recourse vs. Nonrecourse: Commercial Real Estate Financing Which One is Right for You? Prepared by Bill White Director of Commercial Real Estate Lending In this white paper 1 Commercial real estate lenders

Recourse vs. Nonrecourse: Commercial Real Estate Financing Which One is Right for You? Prepared by Bill White Director of Commercial Real Estate Lending In this white paper 1 Commercial real estate lenders

SBA FORM 1088 (REVISED) SECONDARY MARKET ASSIGNMENT AND DISCLOSURE FORM MUST BE USED ON ALL TRANSFERS AFTER MARCH 31, 1988

SECONDARY MARKET ASSIGNMENT AND DISCLOSURE FORM MUST BE USED ON ALL TRANSFERS AFTER MARCH 31, 1988") SBA FORM 1088 (REVISED) SECONDARY MARKET ASSIGNMENT AND DISCLOSURE FORM MUST BE USED ON ALL TRANSFERS AFTER MARCH 31, 1988 SBA has revised the Form 1088, the Secondary Market Assignment and Disclosure

SBA FORM 1088 (REVISED) SECONDARY MARKET ASSIGNMENT AND DISCLOSURE FORM MUST BE USED ON ALL TRANSFERS AFTER MARCH 31, 1988 SBA has revised the Form 1088, the Secondary Market Assignment and Disclosure

Mortgage Strategies in the Current Economic Environment. Katie Hopkins SVP, Investment Strategies [email protected]

Mortgage Strategies in the Current Economic Environment Katie Hopkins SVP, Investment Strategies [email protected] Mortgage Market Trends page 2 Limited Mortgage Opportunities Fed products, 15yr

Mortgage Strategies in the Current Economic Environment Katie Hopkins SVP, Investment Strategies [email protected] Mortgage Market Trends page 2 Limited Mortgage Opportunities Fed products, 15yr

SBA Express Loan Program. www.sba.gov/for-lenders

SBA Express Loan Program SESSION WILL COVER History Lender eligibility issues Program parameters Loan processing Loan closing Practical uses Program Designed to: Increase lender participation Increase

SBA Express Loan Program SESSION WILL COVER History Lender eligibility issues Program parameters Loan processing Loan closing Practical uses Program Designed to: Increase lender participation Increase

Basics of Multifamily MBS July 31, 2012

Basics of Multifamily MBS July 31, 2012 Fannie Mae creates MBS supported by multifamily residential property mortgages. A pool of one or more multifamily mortgages -- which can be either fixed-rate or

Basics of Multifamily MBS July 31, 2012 Fannie Mae creates MBS supported by multifamily residential property mortgages. A pool of one or more multifamily mortgages -- which can be either fixed-rate or

Financing Residential Real Estate. Lesson 12: VA-Guaranteed Loans

Financing Residential Real Estate Lesson 12: VA-Guaranteed Loans Introduction In this lesson we will cover: characteristics of VA loans, eligibility requirements, VA guaranty, VA loan amounts, and underwriting

Financing Residential Real Estate Lesson 12: VA-Guaranteed Loans Introduction In this lesson we will cover: characteristics of VA loans, eligibility requirements, VA guaranty, VA loan amounts, and underwriting

A leveraged. The Case for Leveraged Loans. Introduction - What is a Leveraged Loan?

PENN Capital Management The Navy Yard Corporate Center 3 Crescent Drive, Suite 400 Philadelphia, PA 19112 Phone: 215-302-1501 www.penncapital.com For more information: Christian Noyes, Senior Managing

PENN Capital Management The Navy Yard Corporate Center 3 Crescent Drive, Suite 400 Philadelphia, PA 19112 Phone: 215-302-1501 www.penncapital.com For more information: Christian Noyes, Senior Managing

Daily Income Fund Retail Class Shares ( Retail Shares )

") Daily Income Fund Retail Class Shares ( Retail Shares ) Money Market Portfolio Ticker Symbol: DRTXX U.S. Treasury Portfolio No Ticker Symbol U.S. Government Portfolio Ticker Symbol: DREXX Municipal Portfolio

Daily Income Fund Retail Class Shares ( Retail Shares ) Money Market Portfolio Ticker Symbol: DRTXX U.S. Treasury Portfolio No Ticker Symbol U.S. Government Portfolio Ticker Symbol: DREXX Municipal Portfolio

Arkansas Development Finance Authority, a Component Unit of the State of Arkansas

Arkansas Development Finance Authority, a Component Unit of the State of Arkansas Combined Financial Statements and Additional Information for the Year Ended June 30, 2000, and Independent Auditors Report

Arkansas Development Finance Authority, a Component Unit of the State of Arkansas Combined Financial Statements and Additional Information for the Year Ended June 30, 2000, and Independent Auditors Report

Paragon 5. Financial Calculators User Guide

Paragon 5 Financial Calculators User Guide Table of Contents Financial Calculators... 3 Use of Calculators... 3 Mortgage Calculators... 4 15 Yr vs. 30 Year... 4 Adjustable Rate Amortizer... 4 Affordability...

Paragon 5 Financial Calculators User Guide Table of Contents Financial Calculators... 3 Use of Calculators... 3 Mortgage Calculators... 4 15 Yr vs. 30 Year... 4 Adjustable Rate Amortizer... 4 Affordability...

Member Payment Dependent Notes

Prospectus Member Payment Dependent Notes We may from time to time offer and sell Member Payment Dependent Notes issued by Lending Club. We refer to our Member Payment Dependent Notes as the Notes. We

Prospectus Member Payment Dependent Notes We may from time to time offer and sell Member Payment Dependent Notes issued by Lending Club. We refer to our Member Payment Dependent Notes as the Notes. We

NORTH ISLAND CREDIT UNION

NORTH ISLAND CREDIT UNION Policy Section: Business Services Policy Name: Member Business Lending Policy No: 500-05-01 Board Review & Approval: July 21, 2014 Effective Date: July 22, 2014 POLICY STATEMENT

NORTH ISLAND CREDIT UNION Policy Section: Business Services Policy Name: Member Business Lending Policy No: 500-05-01 Board Review & Approval: July 21, 2014 Effective Date: July 22, 2014 POLICY STATEMENT

Market Rate Ginnie Mae/Fannie Mae TBA Program

Mike Awadis Senior Vice President FirstSouthwest Company Market Rate Ginnie Mae/Fannie Mae TBA Program September 17, 2015 Contents About FirstSouthwest Company The Current Environment for HFAs TBA Market

Mike Awadis Senior Vice President FirstSouthwest Company Market Rate Ginnie Mae/Fannie Mae TBA Program September 17, 2015 Contents About FirstSouthwest Company The Current Environment for HFAs TBA Market

Optimize Your Liquidity and Profitability. Create Investment Securities from Your Mortgage Pipeline

Optimize Your Liquidity and Profitability Create Investment Securities from Your Mortgage Pipeline Optimize Your Liquidity and Profitability, and Manage Your Risks: Create Investment Securities from Your

Optimize Your Liquidity and Profitability Create Investment Securities from Your Mortgage Pipeline Optimize Your Liquidity and Profitability, and Manage Your Risks: Create Investment Securities from Your

Definitions. In some cases a survey rather than an ILC is required.

Definitions 1. What is the closing? The closing is a formal meeting at which both the buyer and seller meet to sign all the final documentation required for the buyer's mortgage loan. Once the closing

Definitions 1. What is the closing? The closing is a formal meeting at which both the buyer and seller meet to sign all the final documentation required for the buyer's mortgage loan. Once the closing

$3,000,000,000. Freddie Mac

PRICING SUPPLEMENT DATED August 14, 2015 (to the Offering Circular Dated February 19, 2015) $3,000,000,000 Freddie Mac GLOBAL DEBT FACILITY Variable Rate Debt Securities Due August 24, 2016 This Pricing

PRICING SUPPLEMENT DATED August 14, 2015 (to the Offering Circular Dated February 19, 2015) $3,000,000,000 Freddie Mac GLOBAL DEBT FACILITY Variable Rate Debt Securities Due August 24, 2016 This Pricing

Re: Comment Letter on the Proposed Amendments to NCUA s MBL Rule

August 31, 2015 National Credit Union Administration 1775 Duke St. Board Secretary Alexandria, VA 22314 RE: Comments on Proposed Rulemaking for Part 723; RIN 3133 AE37 Dear Gerard Poliquin, August 31,

August 31, 2015 National Credit Union Administration 1775 Duke St. Board Secretary Alexandria, VA 22314 RE: Comments on Proposed Rulemaking for Part 723; RIN 3133 AE37 Dear Gerard Poliquin, August 31,

BUYING REAL ESTATE WITH AN IRA AND A NON-RECOURSE LOAN

BUYING REAL ESTATE WITH AN IRA AND A NON-RECOURSE LOAN BY: Mathew Sorensen, Partner KYLER KOHLER OSTERMILLER & SORENSEN, LLP 3033 N. Central Avenue, Suite 415 Phoenix, AZ 85012 Phone 602-761-9798 www.sdirahandbook.com

BUYING REAL ESTATE WITH AN IRA AND A NON-RECOURSE LOAN BY: Mathew Sorensen, Partner KYLER KOHLER OSTERMILLER & SORENSEN, LLP 3033 N. Central Avenue, Suite 415 Phoenix, AZ 85012 Phone 602-761-9798 www.sdirahandbook.com

Settlement Disclosure Form

Settlement Disclosure Form This form is a statement of final loan terms and actual settlement costs. SETTLEMENT INFORMATION Date 11/9/2011 Agent Martha Jones Location ABC Settlement 54321 Random Blvd,

Settlement Disclosure Form This form is a statement of final loan terms and actual settlement costs. SETTLEMENT INFORMATION Date 11/9/2011 Agent Martha Jones Location ABC Settlement 54321 Random Blvd,

Overview of SBA Economic Development Programs and the Impact of the Recovery Act. April 21, 2010

Overview of SBA Economic Development Programs and the Impact of the Recovery Act April 21, 2010 1 Overview of Recovery Act: Goals 1. Restore Access to Capital for Small Businesses: Increase Lending across

Overview of SBA Economic Development Programs and the Impact of the Recovery Act April 21, 2010 1 Overview of Recovery Act: Goals 1. Restore Access to Capital for Small Businesses: Increase Lending across

b e r k e l e y p o i n t

Property Type Conventional Multifamily Multifamily Affordable Housing Student Housing Manufactured Housing Seniors Housing Products Fixed and Adjustable Rate Loans Early Rate Lock Interest-Only and Fully

Property Type Conventional Multifamily Multifamily Affordable Housing Student Housing Manufactured Housing Seniors Housing Products Fixed and Adjustable Rate Loans Early Rate Lock Interest-Only and Fully

Chapter 9 6/16/2010. Two Elements of a Mortgage Loan

Some Effects of Mortgage Debt McGraw-Hill/Irwin Chapter 9 Real Estate Finance: The Laws and Contracts 9-1 Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. More households can own

Some Effects of Mortgage Debt McGraw-Hill/Irwin Chapter 9 Real Estate Finance: The Laws and Contracts 9-1 Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. More households can own

Appraisal A written analysis prepared by a qualified appraiser and estimating the value of a property

REAL ESTATE BASICS Affordability Analysis An analysis of a buyer s ability to afford the purchase of a home, reviews income, liabilities, and available funds, and considers the type of mortgage a buyer

REAL ESTATE BASICS Affordability Analysis An analysis of a buyer s ability to afford the purchase of a home, reviews income, liabilities, and available funds, and considers the type of mortgage a buyer

1994- CalCAP established using bond proceeds

1 HISTORY OF CALCAP 1973- California Pollution Control Financing Authority established 1994- CalCAP established using bond proceeds January 2011- CalCAP receives first State Fund allocation April 2011-

1 HISTORY OF CALCAP 1973- California Pollution Control Financing Authority established 1994- CalCAP established using bond proceeds January 2011- CalCAP receives first State Fund allocation April 2011-

Sales Associate Course

Sales Associate Course Chapter Thirteen Types of Mortgages & Sources of Finance Copyright Gold Coast Schools 1 Types of Mortgages FHA - Federal Housing Administration VA - Veterans Administration Conventional

Sales Associate Course Chapter Thirteen Types of Mortgages & Sources of Finance Copyright Gold Coast Schools 1 Types of Mortgages FHA - Federal Housing Administration VA - Veterans Administration Conventional

State Farm Bank, F.S.B.

State Farm Bank, F.S.B. 2015 Annual Stress Test Disclosure Dodd-Frank Act Company Run Stress Test Results Supervisory Severely Adverse Scenario June 25, 2015 1 Regulatory Requirement The 2015 Annual Stress

State Farm Bank, F.S.B. 2015 Annual Stress Test Disclosure Dodd-Frank Act Company Run Stress Test Results Supervisory Severely Adverse Scenario June 25, 2015 1 Regulatory Requirement The 2015 Annual Stress

Public Policy and Innovation: Partnering with Capital Markets through Securitization. Antonio Baldaque da Silva November 2007

Public Policy and Innovation: Partnering with Capital Markets through Securitization Antonio Baldaque da Silva November 2007 Agenda 1. Motivation: Innovation and Public Policy 2. Traditional tools 3. Alternatives:

Public Policy and Innovation: Partnering with Capital Markets through Securitization Antonio Baldaque da Silva November 2007 Agenda 1. Motivation: Innovation and Public Policy 2. Traditional tools 3. Alternatives:

CITIZENS PROPERTY INSURANCE CORPORATION. INVESTMENT POLICY for. Claims Paying Fund (Taxable)

") CITIZENS PROPERTY INSURANCE CORPORATION INVESTMENT POLICY for Claims Paying Fund (Taxable) INTRODUCTION Citizens is a government entity whose purpose is to provide property and casualty insurance for those

CITIZENS PROPERTY INSURANCE CORPORATION INVESTMENT POLICY for Claims Paying Fund (Taxable) INTRODUCTION Citizens is a government entity whose purpose is to provide property and casualty insurance for those

APPENDIX IV-10 FORM HUD 1731 - PROSPECTUS GINNIE MAE I MORTGAGE-BACKED SECURITIES (CONSTRUCTION AND PERMANENT LOAN SECURITIES)

") GINNIE MAE 5500.3, REV. 1 APPENDIX IV-10 FORM HUD 1731 - PROSPECTUS GINNIE MAE I MORTGAGE-BACKED SECURITIES (CONSTRUCTION AND PERMANENT LOAN SECURITIES) Applicability: Purpose: Prepared by: Prepared in:

GINNIE MAE 5500.3, REV. 1 APPENDIX IV-10 FORM HUD 1731 - PROSPECTUS GINNIE MAE I MORTGAGE-BACKED SECURITIES (CONSTRUCTION AND PERMANENT LOAN SECURITIES) Applicability: Purpose: Prepared by: Prepared in:

GNMA Fund PRGMX. T. Rowe Price SUMMARY PROSPECTUS

SUMMARY PROSPECTUS PRGMX October 1, 2015 T. Rowe Price GNMA Fund A bond fund seeking income and high overall credit quality through investments in mortgage-backed securities issued by the Government National

SUMMARY PROSPECTUS PRGMX October 1, 2015 T. Rowe Price GNMA Fund A bond fund seeking income and high overall credit quality through investments in mortgage-backed securities issued by the Government National

Launching Member Business Lending: In House or CUSO: A Panel Discussion. November 9 th 2015

Launching Member Business Lending: In House or CUSO: A Panel Discussion November 9 th 2015 1 Moderator and Panelists: Moderator: Bob Stowell, SVP/COO, U.S. Federal CU, Burnsville, MN Panelists: Gwen Wong,

Launching Member Business Lending: In House or CUSO: A Panel Discussion November 9 th 2015 1 Moderator and Panelists: Moderator: Bob Stowell, SVP/COO, U.S. Federal CU, Burnsville, MN Panelists: Gwen Wong,

SBA 504 Expanded Refinancing Eligibility

SBA 504 Expanded Refinancing Eligibility When is a commercial mortgage considered eligible for refinancing under the new rules? 1. The loan must have funded at least 2 years ago 2. 85% of the loan proceeds

SBA 504 Expanded Refinancing Eligibility When is a commercial mortgage considered eligible for refinancing under the new rules? 1. The loan must have funded at least 2 years ago 2. 85% of the loan proceeds

USDA Business & Industry (B&I) Guaranteed Loan Program

Guaranteed Loan Program") USDA Business & Industry (B&I) Guaranteed Loan Program B&I Program To Create And Maintain Employment And Improve Economic And Environmental Climate In Rural Communities Administered By The Rural Business

USDA Business & Industry (B&I) Guaranteed Loan Program B&I Program To Create And Maintain Employment And Improve Economic And Environmental Climate In Rural Communities Administered By The Rural Business

20 Hour Mortgage Loan Originator SAFE Comprehensive Course Number: 1013 Provider ID: 1400024

20 Hour Mortgage Loan Originator SAFE Comprehensive Course Number: 1013 Provider ID: 1400024 Day 1 Agenda (1.0 hour) Session 1 - Part I: (1.0 hour) Session 1 - Part II: (1.5 hours) Session 2: Mortgage

20 Hour Mortgage Loan Originator SAFE Comprehensive Course Number: 1013 Provider ID: 1400024 Day 1 Agenda (1.0 hour) Session 1 - Part I: (1.0 hour) Session 1 - Part II: (1.5 hours) Session 2: Mortgage

Commercial Real Estate Comparison Pricing Summary

Wells Fargo Bank, N.A. Small Business Administration Lending Commercial Real Estate Comparison Pricing Summary Prepared For: Darrin Boyd Property Address: 6809 Corporate Drive Indianpolis, IN As of Date:

Wells Fargo Bank, N.A. Small Business Administration Lending Commercial Real Estate Comparison Pricing Summary Prepared For: Darrin Boyd Property Address: 6809 Corporate Drive Indianpolis, IN As of Date: