Small Business Finance How to Reach the Missing Middle. Thorsten Beck

|

|

|

- Amice Marshall

- 8 years ago

- Views:

Transcription

1 Small Business Finance How to Reach the Missing Middle Thorsten Beck

2 Do SMEs matter? Source: Stein, Goland and Schiff (2010)

3 Access to finance the size gap Source: Beck, Maimbo, Faye and Triki (2011)

4 Financing is an important obstacle Source: Beck, Maimbo, Faye and Triki (2011)

5 and these obstacles are more binding for SMEs Growth constraints across firms of different sizes 0.0% -2.0% Financing Legal Corruption -4.0% -6.0% -8.0% Small Medium Large -10.0% -12.0% Source: Beck, Demirguc-Kunt and Maksimovic (2005)

.")

6 which can result in a missing middle Growth differential following initial size (average growth of Ivorian firms minus average growth of German firms). Source: Sleuwagen and Goedhuys (2002)

.")

7 Unpacking the universe of SMEs Different segments to be distinguished Microenterprises: informal, household- or family based Small enterprises formal; often missing middle Medium-size enterprises: aspiring, export-oriented etc. Differentiation between subsistence and transformational enterprises is critical for Discussion on job creation Interventions and policies for easing financing constraints We need different policies and approaches for these different groups!

8 SME Finance and Growth No growth effect from the size of the SME segment, but its dynamism Indirect effects through financial deepening: Sound and effective financial systems benefit small firms more than large firms Financial deepening allows more entrepreneurship, firm dynamism and innovation Financial deepening allows better exploitation of growth and investment opportunities and achieving optimal size Financial deepening allows better resource allocation, more efficient corporate organization and more formality Ultimately, sustainable financial deepening can contribute to job creation, through SME Finance

9 Value added (usd) SMEs, entry and exit of firms Average value added 1,600,000 1,400,000 1,200,000 United Kingdom 1,000, ,000 Italy 600, , , Age of the firm (years) Source: Klapper, Laeven and Rajan (2006)

Source: Klapper, Laeven and")

10 Why are SMEs left out? Transaction costs Fixed cost component of credit provision effectively impedes outreach to smaller and costlier clients Inability of financial institutions to exploit scale economies Risk Related to information asymmetries between borrower and lender Ex-ante: High risk borrowers are the ones most likely to look for external finance Increases in the risk premium raise the risk of the pool of interested borrowers Lenders will use non-price criteria to screen debtors/projects Ex-post: The agent (borrower) has incentives that are inconsistent with the principal s (lender) interests Agents may divert resources to riskier activities, loot assets, etc. Heavier reliance on collateral These challenges arise both on the country- and bank-level SMEs therefore often squeezed between retail (large number!) and large enterprise finance (more manageable risk, scale)

has incentives that are inconsistent with the principal s (lender) interests Agents")

11 Significant credit gap for SMEs in developing countries Source: Stein, Goland and Schiff (2010)

12 Who finances SMEs and how? Limited financing sources mostly banks, limited if any access to capital market Demand-side constraints: resistance again sharing control Supplier credit, internal finance Bank lending: relationship vs. transaction based lending Relationship: bank repeatedly interacts with clients in order to obtain and exploit proprietary borrower information ( soft information) Transaction: typical one-off loans where bank bases its lending decisions on verifiable information and assets ( hard information) Relationship lending traditionally seen as appropriate tool for lending to SMEs as they tend to be more opaque and less able to post collateral Recently transaction lending proposed as alternative lending technique, especially useful for larger and non-local banks Important question: who uses which type of lending technique: small vs. large; domestic vs. foreign

Relationship lending traditionally seen as appropriate tool for lending to SMEs as they tend to")

13 Relationship vs. transaction-based lending: the evidence Cross-country and country-specific evidence shows banks use both relationship and transaction based lending techniques Different banks use different techniques: Large and foreign-owned banks use predominantly transaction-based lending Domestic and smaller banks use predominantly relationship lending Country-level evidence for Bolivia shows that foreign banks use transaction-based and domestic banks relationship-based lending for the same client group Evidence speaks for a diverse banking sector with different approaches to SMEs Evidence on Central and East Europe: a higher share of relationship-based lender reduces access to credit for SMEs less during recession; no difference in boom periods (Beck et al., 2015); similar finding for country studies on Italy (Bolton et al., 2014; Presbitero et al., 2014) Important side note: not clear mapping of foreign/domestic with relationship and transaction-based lender

14 Relationship vs. transaction-based lending evidence from Bolivia Domestic Foreign 2 0 Interest rate Collateral probability (times ten) Maturity (in months)

15 Looking beyond banks Secondary or alternative tiers of capital markets Works best in financial systems, which already have deep capital markets Private equity, venture capital, angel financing Seems a good idea for mid-sized firms that do not have scale or track record to tap public equity or debt Large literature on (mostly positive) effect of equity funds on firm-level outcomes for the U.S. Limited evidence for other countries Mezzanine financing forms Often regulatory restrictions; scale problems New financing arrangements: Crowd funding Peer-to-peer lending Jury still out: enough scale, risk management? Regulatory implications (new forms of shadow banking?)

16 Policies and institutions to ease small firms financing constraints Institutional framework Creditor rights, contract enforcement Collateral registries Transparency Credit information sharing (e.g.: Central and Eastern Europe) Reputation collateral Reduction in informality Accounting and auditing standards Banking market structure and competition No clear mapping from ownership structure into successful SME outreach But lack of competition can undermine SME lending Easier to lend to corporates, consumers and governments No need to innovate

Reputation collateral Reduction in informality Accounting and auditing standards Banking market")

17 Small business finance in between micro and SME finance Increase information UID program in India, link unique ID to credit information FIP in Indonesia Reduce distance between bank and client Mobile banking (e.g. Kenya) Agency model (e.g. India) Look beyond traditional banks for financial service provision Look beyond banking and debt OTC equity exchange for India for mid-sized companies Private equity, venture capital, angel financing (diaspora resources, remittances?)

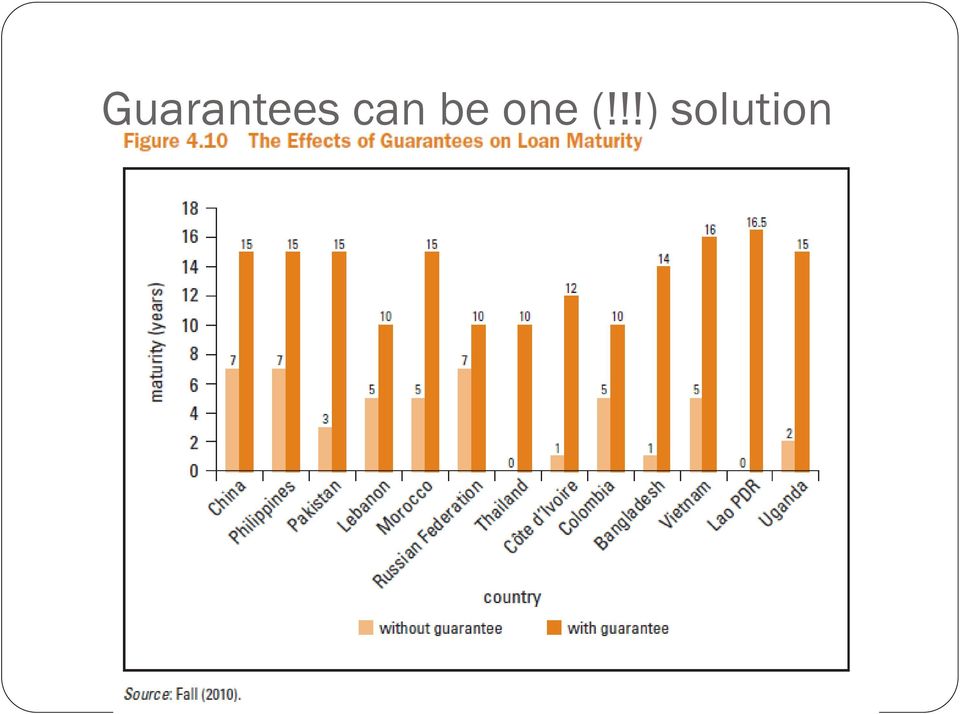

18 Small Business Financing Government s Role Focusing on contestability of financial markets Low entry barriers Infrastructure open to all financial institutions No regulatory barriers to innovation Challenge funds Pro-market activism Do not replace markets, but help overcome market failures Well-designed, limited (time, resources etc.) interventions might help Demonstration effect for private sector Trial and error, no one size fits all Providing infrastructure, overcoming scale problems Post offices as platform for financial service provision Platform for factoring (Mexico) Subsidizing transaction costs of lenders (NOT interest rates) Partial credit guarantee schemes Additionality vs. sustainability Successful examples, e.g. in Chile

Subsidizing transaction costs of lenders (NOT interest rates) Partial credit guarantee schemes Additionality vs.")

solution")

19 Guarantees can be one (!!!) solution

20 Looking forward Need more evidence-based policy making Different methodologies for different questions Policy and institutions: cross-country/reform implementation Financial innovation: on financial institution level Understanding SMEs financing constraints and how to alleviate them Co-ordinated Country Case Studies - Innovation and Growth, Raising Productivity in Developing Countries (DFID funded) Research in Southeast Europe and Caucasus: role of collateral and maturity structure on small enterprises investment choices (funded by EFSE) DGGF Evaluation Microcredit vs. small business lending What can one learn from the other? More focus on demand-side constraints looking beyond the firm to the entrepreneur

DGGF Evaluation Microcredit vs. small business lending What can one learn from the other?")

21 Conclusions SMEs are the private sector of developing countries Critical to differentiate between different segments of the SME population Different financial service providers: banks, MFIs, capital markets Different lending techniques and complementary services: technical training, business development Policy levers on different levels: Long-term institution building Competition and innovation Providing the market a helping hand

22 Thank you Thorsten Beck

Prof. Thorsten Beck Cass Business School London

Prof. Thorsten Beck Cass Business School London DUTCH GOOD GROWTH FUND One Year Anniversary 1 st July 2015 The Hague Small Business Finance How to Reach the Missing Middle Thorsten Beck Do SMEs matter?

Prof. Thorsten Beck Cass Business School London DUTCH GOOD GROWTH FUND One Year Anniversary 1 st July 2015 The Hague Small Business Finance How to Reach the Missing Middle Thorsten Beck Do SMEs matter?

Two trillion and counting

Two trillion and counting Assessing the credit gap for micro, small, and medium-size enterprises in the developing world OCTOBER 2010 Peer Stein International Finance Corporation Tony Goland McKinsey &

Two trillion and counting Assessing the credit gap for micro, small, and medium-size enterprises in the developing world OCTOBER 2010 Peer Stein International Finance Corporation Tony Goland McKinsey &

Finance and Poverty Alleviation: Evidence and policies. Thorsten Beck

Finance and Poverty Alleviation: Evidence and policies Thorsten Beck Motivation Large variation in in income inequality and poverty levels across countries What are policies to reduce inequality and poverty?

Finance and Poverty Alleviation: Evidence and policies Thorsten Beck Motivation Large variation in in income inequality and poverty levels across countries What are policies to reduce inequality and poverty?

Access to Finance: Role of Public Sector. Initiative for Policy Dialogue Financial Markets Reform Task Force Manchester, UK July 26-27, 27, 2006

Access to Finance: Role of Public Sector Initiative for Policy Dialogue Financial Markets Reform Task Force Manchester, UK July 26-27, 27, 2006 Background Material De la Torre, A., J.C. Gozzi Valdez, and

Access to Finance: Role of Public Sector Initiative for Policy Dialogue Financial Markets Reform Task Force Manchester, UK July 26-27, 27, 2006 Background Material De la Torre, A., J.C. Gozzi Valdez, and

The Importance of Credit Bureaus in Lending Decisions

The Importance of Credit Bureaus in Lending Decisions Lessons Learned from International Experience Peer Stein, Principal Investment Officer August 24, 2004 Challenges for the Financial Industry Historically:

The Importance of Credit Bureaus in Lending Decisions Lessons Learned from International Experience Peer Stein, Principal Investment Officer August 24, 2004 Challenges for the Financial Industry Historically:

Thierry Tressel Lead Economist, Research Group, World Bank 2015 High Level Caribbean Forum, Sept. 3-4 2015, St. Kitts

Thierry Tressel Lead Economist, Research Group, World Bank 215 High Level Caribbean Forum, Sept. 3-4 215, St. Kitts Policy issue Focus on SMEs: they are the biggest contributors to employment across countries,

Thierry Tressel Lead Economist, Research Group, World Bank 215 High Level Caribbean Forum, Sept. 3-4 215, St. Kitts Policy issue Focus on SMEs: they are the biggest contributors to employment across countries,

Access to Financial Services in Developing Countries: Identification of Obstacles. Liliana Rojas-Suárez July 2006

Access to Financial Services in Developing Countries: Identification of Obstacles Liliana Rojas-Suárez July 2006 Background Even though banks are the most important providers of financial services Evolution

Access to Financial Services in Developing Countries: Identification of Obstacles Liliana Rojas-Suárez July 2006 Background Even though banks are the most important providers of financial services Evolution

Access to Finance: Impacts of Publicly Supported Venture Capital and Loan Guarantees

Access to Finance: Impacts of Publicly Supported Venture Capital and Loan Guarantees Authors : Dr. Ronnie Ramlogan & Dr. John Rigby Presented by : Arslan Austin Innovation IV SS 2014 Introduction Innovation

Access to Finance: Impacts of Publicly Supported Venture Capital and Loan Guarantees Authors : Dr. Ronnie Ramlogan & Dr. John Rigby Presented by : Arslan Austin Innovation IV SS 2014 Introduction Innovation

SMALL- AND MEDIUM-SIZED ENTERPRISE FINANCE IN AFRICA

AFRICA GROWTH INITIATIVE WORKING PAPER 16 JULY 2014 SMALL- AND MEDIUM-SIZED ENTERPRISE FINANCE IN AFRICA Thorsten Beck and Robert Cull Thorsten Beck is a professor of banking and finance at the Cass Business

AFRICA GROWTH INITIATIVE WORKING PAPER 16 JULY 2014 SMALL- AND MEDIUM-SIZED ENTERPRISE FINANCE IN AFRICA Thorsten Beck and Robert Cull Thorsten Beck is a professor of banking and finance at the Cass Business

SME Banking-Africa. A Unique Opportunity for the Continent

SME Banking-Africa A Unique Opportunity for the Continent Key Messages More to be done The opportunity Challenges in SME financing Profitable segment A proposed solution 2 SMEs in Africa- The Missing Middle

SME Banking-Africa A Unique Opportunity for the Continent Key Messages More to be done The opportunity Challenges in SME financing Profitable segment A proposed solution 2 SMEs in Africa- The Missing Middle

EU-CELAC Business Summit eucelac-bizsummit2015.eu. Wednesday 10 th June 2015, 14:30-16:30 Concept Note for Workshop 3

EU-CELAC Business Summit eucelac-bizsummit2015.eu Wednesday 10 th June 2015, 14:30-16:30 Concept Note for Workshop 3 Access to finance and financial instruments The important role of Small and Medium-sized

EU-CELAC Business Summit eucelac-bizsummit2015.eu Wednesday 10 th June 2015, 14:30-16:30 Concept Note for Workshop 3 Access to finance and financial instruments The important role of Small and Medium-sized

EU-CELAC Business Summit eucelac-bizsummit2015.eu. Wednesday 10 th June 2015, 14:30-16:30 Concept Note for Workshop 3

Working Party on Latin America and the Caribbean (COLAC) m.d. : 90/15 source : EEAS for : Information date : 29-04 - 2015 EU-CELAC Business Summit eucelac-bizsummit2015.eu Wednesday 10 th June 2015, 14:30-16:30

Working Party on Latin America and the Caribbean (COLAC) m.d. : 90/15 source : EEAS for : Information date : 29-04 - 2015 EU-CELAC Business Summit eucelac-bizsummit2015.eu Wednesday 10 th June 2015, 14:30-16:30

A conceptual paper on factors influencing Financial Institutions on lending technologies to technology-based SMEs in the northern region of Malaysia

A conceptual paper on factors influencing Financial Institutions on lending technologies to technology-based SMEs in the northern region of Malaysia Wan Sallha Binti Yusoff & Chuthamas Chittithaworn School

A conceptual paper on factors influencing Financial Institutions on lending technologies to technology-based SMEs in the northern region of Malaysia Wan Sallha Binti Yusoff & Chuthamas Chittithaworn School

Loan guarantee funds. Inclusive rural financial services. Introduction

Loan guarantee funds Inclusive rural financial services Introduction For more than seven decades, loan guarantee funds (LGFs) have been used extensively internationally in different market segments and

Loan guarantee funds Inclusive rural financial services Introduction For more than seven decades, loan guarantee funds (LGFs) have been used extensively internationally in different market segments and

Section A Introduction This section asks for information that aims to identify the independence and ownership situation of your business.

Access to Finance Purpose of this survey Access to finance is crucial to business success and an important factor for economic growth in Europe following the economic crisis in 2007. The purpose of this

Access to Finance Purpose of this survey Access to finance is crucial to business success and an important factor for economic growth in Europe following the economic crisis in 2007. The purpose of this

Raise the anchor. FEATURE 4 March 2015. One of the most reliable growth stimuli for SMEs is value chain financing.

Raise the anchor FEATURE 4 March 2015 One of the most reliable growth stimuli for SMEs is value chain financing. Qamar Saleem, Martin Hommes and Aksinya Sorokina explain how this works and why it is good

Raise the anchor FEATURE 4 March 2015 One of the most reliable growth stimuli for SMEs is value chain financing. Qamar Saleem, Martin Hommes and Aksinya Sorokina explain how this works and why it is good

SMEs Access to Financial Services: Bankers Eye. Evelyn Mweta Richard, Neema Geoffrey Mori

Chinese Business Review, ISSN 1537-1506 February 2012, Vol. 11, No. 2, 217-223 D DAVID PUBLISHING SMEs Access to Financial Services: Bankers Eye Evelyn Mweta Richard, Neema Geoffrey Mori University of

Chinese Business Review, ISSN 1537-1506 February 2012, Vol. 11, No. 2, 217-223 D DAVID PUBLISHING SMEs Access to Financial Services: Bankers Eye Evelyn Mweta Richard, Neema Geoffrey Mori University of

6. SME Access to Finance

44 Enterprises in Asia: Fostering Dynamism in SMEs 6. SME Access to Finance 6.1 Are SMEs Credit Constrained? Theoretically, there are good reasons why the availability (and cost) of credit may be more

44 Enterprises in Asia: Fostering Dynamism in SMEs 6. SME Access to Finance 6.1 Are SMEs Credit Constrained? Theoretically, there are good reasons why the availability (and cost) of credit may be more

FINANCE AND BUSINESS DEVELOPMENT SERVICES FOR ENTREPRENEURSHIP DEVELOPMENT: (SME lending in Kenya, from microfinance institution to SME bank )

") FINANCE AND BUSINESS DEVELOPMENT SERVICES FOR ENTREPRENEURSHIP DEVELOPMENT: (SME lending in Kenya, from microfinance institution to SME bank ) What is K-Rep Bank Vision - Mission- To be the financial services

FINANCE AND BUSINESS DEVELOPMENT SERVICES FOR ENTREPRENEURSHIP DEVELOPMENT: (SME lending in Kenya, from microfinance institution to SME bank ) What is K-Rep Bank Vision - Mission- To be the financial services

European Union SME policies. Ulla Hudina

European Union SME policies Ulla Hudina EU Finance Day for SMEs, Athens, 20th January 2009 Supporting SMEs SMEs backbone of EU economy: important players in all value chains; 23 million SMEs (99 % of all

European Union SME policies Ulla Hudina EU Finance Day for SMEs, Athens, 20th January 2009 Supporting SMEs SMEs backbone of EU economy: important players in all value chains; 23 million SMEs (99 % of all

Development of the Corporate Credit Information Database and Credit Guarantee System

Development of the Corporate Credit Information Database and Credit Guarantee System Hachinohe University Research Institute, Japan; University of Malaya, Malaysia; De La Salle University, Philippines;

Development of the Corporate Credit Information Database and Credit Guarantee System Hachinohe University Research Institute, Japan; University of Malaya, Malaysia; De La Salle University, Philippines;

Small and Medium-Size Enterprises:

Tilburg University Small and medium-size enterprises Beck, T.H.L.; Demirgüç-Kunt, A. Published in: Journal of Banking and Finance Publication date: 2006 Link to publication Citation for published version

Tilburg University Small and medium-size enterprises Beck, T.H.L.; Demirgüç-Kunt, A. Published in: Journal of Banking and Finance Publication date: 2006 Link to publication Citation for published version

Delegations will find attached the draft Council conclusions on a Capital Markets Union, as prepared by the Economic and Financial Committee.

Council of the European Union Brussels, 16 June 2015 (OR. en) 9852/15 EF 110 ECOFIN 473 SURE 14 UEM 223 NOTE From: To: Subject: General Secretariat of the Council Permanenet Representatives Committee (Part

Council of the European Union Brussels, 16 June 2015 (OR. en) 9852/15 EF 110 ECOFIN 473 SURE 14 UEM 223 NOTE From: To: Subject: General Secretariat of the Council Permanenet Representatives Committee (Part

Perspectives on Venture Capital and Fixed Income Markets

Perspectives on Venture Capital and Fixed Income Markets Parag Saxena International Business Forum on Financing for Development Doha, Qatar, November 2008 Today s Discussion: Three Significant Forces for

Perspectives on Venture Capital and Fixed Income Markets Parag Saxena International Business Forum on Financing for Development Doha, Qatar, November 2008 Today s Discussion: Three Significant Forces for

5. Funding Available for IP-Rich Businesses

20 IP Finance Toolkit 5. Funding Available for IP-Rich Businesses Introduction As the Banking on IP? report notes; SMEs first port of call for finance is often a bank. Figures quoted in the report show

20 IP Finance Toolkit 5. Funding Available for IP-Rich Businesses Introduction As the Banking on IP? report notes; SMEs first port of call for finance is often a bank. Figures quoted in the report show

Restoring Financing and Growth To Europe s SMEs. Jeffrey Anderson Senior Director for European Affairs (formerly)

") Restoring Financing and Growth To Europe s SMEs Jeffrey Anderson Senior Director for European Affairs (formerly) 1. Introduction & Report Focus 2. SMEs in Europe 3. Main Findings 4. Four sets of Impediments

Restoring Financing and Growth To Europe s SMEs Jeffrey Anderson Senior Director for European Affairs (formerly) 1. Introduction & Report Focus 2. SMEs in Europe 3. Main Findings 4. Four sets of Impediments

Chapter 14. Understanding Financial Contracts. Learning Objectives. Introduction

Chapter 14 Understanding Financial Contracts Learning Objectives Differentiate among the different mechanisms of external financing of firms Explain why mechanisms of external financing depend upon firm

Chapter 14 Understanding Financial Contracts Learning Objectives Differentiate among the different mechanisms of external financing of firms Explain why mechanisms of external financing depend upon firm

Improving Access to Finance for SMEs: International Good Experiences and Lessons for Mongolia

Improving Access to Finance for SMEs: International Good Experiences and Lessons for Mongolia Bataa Ganbold Currently Visiting Research Fellow at the IDE-JETRO (Institute of Developing Economies under

Improving Access to Finance for SMEs: International Good Experiences and Lessons for Mongolia Bataa Ganbold Currently Visiting Research Fellow at the IDE-JETRO (Institute of Developing Economies under

ENTERPRISE DEVELOPMENT STRATEGY Small- and Medium-Sized Enterprises. I. Introduction

ENTERPRISE DEVELOPMENT STRATEGY Small- and Medium-Sized Enterprises I. Introduction I.1 Current Challenge: Most countries in the region are undergoing reforms that are opening their economies to greater

ENTERPRISE DEVELOPMENT STRATEGY Small- and Medium-Sized Enterprises I. Introduction I.1 Current Challenge: Most countries in the region are undergoing reforms that are opening their economies to greater

Perspectives on Venture Capital and Fixed Income Markets. ChileGlobal Seminar September 26, 2007

Perspectives on Venture Capital and Fixed Income Markets ChileGlobal Seminar September 26, 2007 Today s Discussion: Three Significant Forces for National Economic Growth Venture Capital Fixed Income Markets

Perspectives on Venture Capital and Fixed Income Markets ChileGlobal Seminar September 26, 2007 Today s Discussion: Three Significant Forces for National Economic Growth Venture Capital Fixed Income Markets

Working capital: Keep the ball rolling

Working capital: Keep the ball rolling Author : Michael Byrne Date : March 9, 2011 Working capital is considered the life line of any company, allowing the company to grow, expand operations, and weather

Working capital: Keep the ball rolling Author : Michael Byrne Date : March 9, 2011 Working capital is considered the life line of any company, allowing the company to grow, expand operations, and weather

COMMISSION OF THE EUROPEAN COMMUNITIES

COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 29.6.2006 COM(2006) 349 final COMMUNICATION FROM THE COMMISSION TO THE COUNCIL, THE EUROPEAN PARLIAMENT, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE AND

COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 29.6.2006 COM(2006) 349 final COMMUNICATION FROM THE COMMISSION TO THE COUNCIL, THE EUROPEAN PARLIAMENT, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE AND

Eurostat's 2010 Survey Questionnaire on Access to Finance

From: Entrepreneurship at a Glance 2012 Access the complete publication at: http://dx.doi.org/10.1787/entrepreneur_aag-2012-en Eurostat's 2010 Survey Questionnaire on Access to Finance Please cite this

From: Entrepreneurship at a Glance 2012 Access the complete publication at: http://dx.doi.org/10.1787/entrepreneur_aag-2012-en Eurostat's 2010 Survey Questionnaire on Access to Finance Please cite this

Non-traded financial contracts

11-1 Introduction Financial contracts are made between lenders and borrowers Non-traded financial contracts are tailor-made to fit the characteristics of the borrower In business financing, the differences

11-1 Introduction Financial contracts are made between lenders and borrowers Non-traded financial contracts are tailor-made to fit the characteristics of the borrower In business financing, the differences

Access to finance for. SMEs. István NÉMETH European Commission DG for Internal Market, Industry, Entrepreneurship and SMEs

Access to finance for SMEs István NÉMETH European Commission DG for Internal Market, Industry, Entrepreneurship and SMEs Why EU intervention needed? EU financial instruments for SMEs Building on success

Access to finance for SMEs István NÉMETH European Commission DG for Internal Market, Industry, Entrepreneurship and SMEs Why EU intervention needed? EU financial instruments for SMEs Building on success

Bank Financing for SMEs around the World

Public Disclosure Authorized Pol i c y Re s e a rc h Wo r k i n g Pa p e r 4785 WPS4785 Public Disclosure Authorized Public Disclosure Authorized Bank Financing for SMEs around the World Drivers, Obstacles,

Public Disclosure Authorized Pol i c y Re s e a rc h Wo r k i n g Pa p e r 4785 WPS4785 Public Disclosure Authorized Public Disclosure Authorized Bank Financing for SMEs around the World Drivers, Obstacles,

SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL, AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT

: MICRO, SMALL, AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT") Women s Entrepreneurship Support Sector Development Program (RRP ARM 45230) SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL, AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT A. Overview 1. Significance of micro, small,

Women s Entrepreneurship Support Sector Development Program (RRP ARM 45230) SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL, AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT A. Overview 1. Significance of micro, small,

Financing your business. Dr. T. R. Heidrick Poole Professor in Technology Management Faculty of Engineering/School of Business U of A

Financing your business Dr. T. R. Heidrick Poole Professor in Technology Management Faculty of Engineering/School of Business U of A Risk Capital ct. d Earns returns through participation in the future

Financing your business Dr. T. R. Heidrick Poole Professor in Technology Management Faculty of Engineering/School of Business U of A Risk Capital ct. d Earns returns through participation in the future

SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities

: MICRO, SMALL AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities") Small Business and Entrepreneurship Development Project (RRP UZB 42007-014) SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT 1 Sector Road Map 1. Sector Performance, Problems,

Small Business and Entrepreneurship Development Project (RRP UZB 42007-014) SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT 1 Sector Road Map 1. Sector Performance, Problems,

List of provisions for consumer protection

List of provisions for consumer protection Type of provision Lending platforms Equity and/or Debt platforms Maximum amount of investment for 40.000 Euro 20.000 Euro consumers on the platform Maximum frequency

List of provisions for consumer protection Type of provision Lending platforms Equity and/or Debt platforms Maximum amount of investment for 40.000 Euro 20.000 Euro consumers on the platform Maximum frequency

AL 98-9 Subject: Access to Financing for Minority Small Businesses Date: July 15, 1998

AL 98-9 Subject: Access to Financing for Minority Small Businesses Date: July 15, 1998 TO: Chief Executive Officers of all National Banks, Department and Division Heads, and all Examining Personnel PURPOSE

AL 98-9 Subject: Access to Financing for Minority Small Businesses Date: July 15, 1998 TO: Chief Executive Officers of all National Banks, Department and Division Heads, and all Examining Personnel PURPOSE

Public consultation on Building a Capital Markets Union

Case Id: 6793f8c7-c6ef-45dd-8987-665fe5775337 Date: 13/05/2015 23:30:38 Public consultation on Building a Capital Markets Union Fields marked with * are mandatory. Introduction The purpose of the Green

Case Id: 6793f8c7-c6ef-45dd-8987-665fe5775337 Date: 13/05/2015 23:30:38 Public consultation on Building a Capital Markets Union Fields marked with * are mandatory. Introduction The purpose of the Green

Salvatore Zecchini Chairman OECD Working Party on SMEs and Entrepreneurship

FOSTERING SMEs AND ENTREPRENEURSHIP FINANCING AFTER THE CRISIS Confindustria - OECD MiSE - Roma 7th July 2014 Salvatore Zecchini Chairman OECD Working Party on SMEs and Entrepreneurship 1 Six years after

FOSTERING SMEs AND ENTREPRENEURSHIP FINANCING AFTER THE CRISIS Confindustria - OECD MiSE - Roma 7th July 2014 Salvatore Zecchini Chairman OECD Working Party on SMEs and Entrepreneurship 1 Six years after

Liberia Leasing Investment Forum

Finance Leasing in Liberia: Unlocking Accelerated Market and Business Development GROWING COMPETITIVE AND EFFECTIVE LEASING MARKETS Collins David-Ikpe Past chairman, Equipment Leasing Association of Nigeria

Finance Leasing in Liberia: Unlocking Accelerated Market and Business Development GROWING COMPETITIVE AND EFFECTIVE LEASING MARKETS Collins David-Ikpe Past chairman, Equipment Leasing Association of Nigeria

Micro, Small and Medium Enterprises Financing in India - Issues and Concerns

Micro, Small and Medium Enterprises Financing in India - Issues and Concerns Dr. C.S. Prasad* Micro, Small and Medium enterprises (MSME) constitute the dominant form of business organisation worldwide.

Micro, Small and Medium Enterprises Financing in India - Issues and Concerns Dr. C.S. Prasad* Micro, Small and Medium enterprises (MSME) constitute the dominant form of business organisation worldwide.

Commercialization of Microfinance

8/16/2011 1 13 Commercialization of Microfinance Robert Lensink (RUG/WUR) Presentation for the UMM Conference in Frankfurt Schedule 8/16/2011 2 13 Some preliminary remarks Recent trend: commercialization

8/16/2011 1 13 Commercialization of Microfinance Robert Lensink (RUG/WUR) Presentation for the UMM Conference in Frankfurt Schedule 8/16/2011 2 13 Some preliminary remarks Recent trend: commercialization

Making Small Business Finance Profitable

Making Small Business Finance Profitable Key Lessons Learned about Applying New Technologies to SME Finance Peer Stein, Banking Advisory Group December 5, 2002 Shifting the Productivity Frontier Productivity

Making Small Business Finance Profitable Key Lessons Learned about Applying New Technologies to SME Finance Peer Stein, Banking Advisory Group December 5, 2002 Shifting the Productivity Frontier Productivity

Small Business Summit 2011. www.cba.co.za

Small Business Summit 2011 THE BUSINESS OF CREDIT BUREAUX AND SMMEs REALITY Credit built into modern economic infrastructures Responsible access to credit dependent on sound risk and affordability assessment

Small Business Summit 2011 THE BUSINESS OF CREDIT BUREAUX AND SMMEs REALITY Credit built into modern economic infrastructures Responsible access to credit dependent on sound risk and affordability assessment

How To Support A Business In Europe

Support for Research, Development and Innovation Introduction: «Financial instruments for SMEs and larger companies provided by the European Union and the European Investment Bank» Seminar on «Financial

Support for Research, Development and Innovation Introduction: «Financial instruments for SMEs and larger companies provided by the European Union and the European Investment Bank» Seminar on «Financial

Discussion. 1. Warren Mundy and Mark Bryant

Discussion 1. Warren Mundy and Mark Bryant This paper by Professor Gregory Udell provides an assessment of the existing academic literature on the issue of small to medium-sized enterprise (SME) access

Discussion 1. Warren Mundy and Mark Bryant This paper by Professor Gregory Udell provides an assessment of the existing academic literature on the issue of small to medium-sized enterprise (SME) access

Factoring financing alternative for SMEs

Factoring financing alternative for SMEs Laura Giurca Vasilescu Faculty of Economy and Business Administration University of Craiova, Romania laura_giurca_vasilescu@yahoo.com Abstract Financing is necessary

Factoring financing alternative for SMEs Laura Giurca Vasilescu Faculty of Economy and Business Administration University of Craiova, Romania laura_giurca_vasilescu@yahoo.com Abstract Financing is necessary

Banking SMEs around the world: Lending practices, business models, drivers and obstacles

Banking SMEs around the world: Lending practices, business models, drivers and obstacles Thorsten Beck (World Bank) Asli Demirgüç-Kunt (World Bank) María Soledad Martínez Pería (World Bank) FIRST DRAFT

Banking SMEs around the world: Lending practices, business models, drivers and obstacles Thorsten Beck (World Bank) Asli Demirgüç-Kunt (World Bank) María Soledad Martínez Pería (World Bank) FIRST DRAFT

ERC Insights. June 2014 FINANCING GROWTH

ERC Insights June 2014 FINANCING GROWTH Recent ERC research provides new insights into bank borrowing among UK SMEs and emphasises the potential value of effective company boards in helping firms to access

ERC Insights June 2014 FINANCING GROWTH Recent ERC research provides new insights into bank borrowing among UK SMEs and emphasises the potential value of effective company boards in helping firms to access

Finance and Small Business

Small Business Management 4 2011 Finance and Small Business Notices: go to your own bank and ask for the Business Start-up Pack This should contain useful info (printed and in CD format). Take a look at

Small Business Management 4 2011 Finance and Small Business Notices: go to your own bank and ask for the Business Start-up Pack This should contain useful info (printed and in CD format). Take a look at

Central Banks and the Development Agenda The CBN Experience Sadiq Usman 1 Presentation Outline 2 Slide Introduction Brief on Nigeria The recent Banking Crisis CBN Developmental Activities CBN Interventions

Central Banks and the Development Agenda The CBN Experience Sadiq Usman 1 Presentation Outline 2 Slide Introduction Brief on Nigeria The recent Banking Crisis CBN Developmental Activities CBN Interventions

CHAPTER 7 ACCESS TO FINANCE. 1. Access to finance is important for the private sector in developing countries

CHAPTER 7 ACCESS TO FINANCE Private sector companies, particularly small and medium-size enterprises (SMEs), perceive lack of access to finance as one of their main constraints. Businesses in less-developed

CHAPTER 7 ACCESS TO FINANCE Private sector companies, particularly small and medium-size enterprises (SMEs), perceive lack of access to finance as one of their main constraints. Businesses in less-developed

Impact Investing Lab Financing innovation: the role of Angel Investing

Impact Investing Lab Financing innovation: the role of Angel Investing December 3rd, 2014 www.iban.it Entrepreneurship: a definition

Impact Investing Lab Financing innovation: the role of Angel Investing December 3rd, 2014 www.iban.it Entrepreneurship: a definition

Measuring banking sector development

Financial Sector Indicators Note: 1 Part of a series illustrating how the (FSDI) project enhances the assessment of financial sectors by expanding the measurement dimensions beyond size to cover access,

Financial Sector Indicators Note: 1 Part of a series illustrating how the (FSDI) project enhances the assessment of financial sectors by expanding the measurement dimensions beyond size to cover access,

On Corporate Debt Restructuring *

On Corporate Debt Restructuring * Asian Bankers Association 1. One of the major consequences of the current financial crisis is the corporate debt problem being faced by several economies in the region.

On Corporate Debt Restructuring * Asian Bankers Association 1. One of the major consequences of the current financial crisis is the corporate debt problem being faced by several economies in the region.

Determinants of Bank Long-term Lending Behavior: Evidence from Russia

1 Determinants of Bank Long-term Lending Behavior: Evidence from Russia Lucy Chernykh* Bowling Green State University, USA Alexandra K. Theodossiou Texas A&M University, Corpus Christi, USA We investigate

1 Determinants of Bank Long-term Lending Behavior: Evidence from Russia Lucy Chernykh* Bowling Green State University, USA Alexandra K. Theodossiou Texas A&M University, Corpus Christi, USA We investigate

EU Capital Markets Union Green Paper Grant Thornton s response to consultation document Filed 13 May 2015

EU Capital Markets Union Green Paper Grant Thornton s response to consultation document Filed 13 May 2015 Please note, the Appendix contained at the end of the document includes a standalone piece submitted

EU Capital Markets Union Green Paper Grant Thornton s response to consultation document Filed 13 May 2015 Please note, the Appendix contained at the end of the document includes a standalone piece submitted

FOURTEEN. Access to Financing for Small and Medium Enterprises CHAPTER STYLIZED FACTS

CHAPTER FOURTEEN Access to Financing for Small and Medium Enterprises I N Latin America and around the world, small and medium enterprises (SMEs) comprise a large share of firms, employment, and gross

CHAPTER FOURTEEN Access to Financing for Small and Medium Enterprises I N Latin America and around the world, small and medium enterprises (SMEs) comprise a large share of firms, employment, and gross

EFFECTS OF BANK MERGERS AND ACQUISITIONS ON SMALL BUSINESS LENDING

EFFECTS OF BANK MERGERS AND ACQUISITIONS ON SMALL BUSINESS LENDING Allen N. Berger Board of Governors of the Federal Reserve System Wharton Financial Institutions Center RIETI Policy Symposium Japan s

EFFECTS OF BANK MERGERS AND ACQUISITIONS ON SMALL BUSINESS LENDING Allen N. Berger Board of Governors of the Federal Reserve System Wharton Financial Institutions Center RIETI Policy Symposium Japan s

Secured Transactions and Collateral Registries Program

Secured Transactions and Collateral Registries Program Access to Finance, IFC Amman, Jordan, June 25, 2013 Alejandro Alvarez de la Campa Global Product Leader STCR OUTLINE 1. Definition of Secured Transactions

Secured Transactions and Collateral Registries Program Access to Finance, IFC Amman, Jordan, June 25, 2013 Alejandro Alvarez de la Campa Global Product Leader STCR OUTLINE 1. Definition of Secured Transactions

Crowdfunding in the EU

Crowdfunding in the EU Identification First name -open reply-(compulsory) Family name -open reply-(compulsory) What category describes you best? -single choice reply-(compulsory) Organisation's name -open

Crowdfunding in the EU Identification First name -open reply-(compulsory) Family name -open reply-(compulsory) What category describes you best? -single choice reply-(compulsory) Organisation's name -open

THE ACCESS OF SMALL AND MEDIUM SIZE ENTERPRISES TO BANKING FINANCING AND CURRENT CHALLANGES: THE CASE OF EU COUNTRIES

THE ACCESS OF SMALL AND MEDIUM SIZE ENTERPRISES TO BANKING FINANCING AND CURRENT CHALLANGES: THE CASE OF EU COUNTRIES Angela Roman 1 Valentina Diana Rusu 2 ABSTRACT: Bank loans are a vital resource for

THE ACCESS OF SMALL AND MEDIUM SIZE ENTERPRISES TO BANKING FINANCING AND CURRENT CHALLANGES: THE CASE OF EU COUNTRIES Angela Roman 1 Valentina Diana Rusu 2 ABSTRACT: Bank loans are a vital resource for

IV ISSUES IN SME FINANCING

IV ISSUES IN SME FINANCING IV.1 Introduction The development literature focuses a good deal of attention on issues faced by SME in accessing finance. Traditionally, the focus is on obstacles created by

IV ISSUES IN SME FINANCING IV.1 Introduction The development literature focuses a good deal of attention on issues faced by SME in accessing finance. Traditionally, the focus is on obstacles created by

The Determinants of Global Factoring By Leora Klapper

The Determinants of Global Factoring By Leora Klapper Factoring services can be traced historically to Roman times. Closer to our own era, factors arose in England as early as the thirteenth century, as

The Determinants of Global Factoring By Leora Klapper Factoring services can be traced historically to Roman times. Closer to our own era, factors arose in England as early as the thirteenth century, as

OSC EXEMPT MARKET REVIEW OSC NOTICE 45-712 APPENDIX C CAPITAL RAISING IN CANADA AND THE ONTARIO EXEMPT MARKET

OSC EXEMPT MARKET REVIEW OSC NOTICE 45-712 APPENDIX C CAPITAL RAISING IN CANADA AND THE ONTARIO EXEMPT MARKET 1 1. Introduction As a securities regulator, the Ontario Securities Commission is committed

OSC EXEMPT MARKET REVIEW OSC NOTICE 45-712 APPENDIX C CAPITAL RAISING IN CANADA AND THE ONTARIO EXEMPT MARKET 1 1. Introduction As a securities regulator, the Ontario Securities Commission is committed

SME Credit Scoring: Key Initiatives, Opportunities, and Issues

The World Bank Group March 2006 Issue No. 10 AccessFinance A Newsletter Published by the Financial Sector Vice Presidency Access to Finance Thematic Group SME Credit Scoring: Key Initiatives, Opportunities,

The World Bank Group March 2006 Issue No. 10 AccessFinance A Newsletter Published by the Financial Sector Vice Presidency Access to Finance Thematic Group SME Credit Scoring: Key Initiatives, Opportunities,

CASE STORY ON GENDER DIMENSION OF AID FOR TRADE. Banking on Women Pays Off: Creating Opportunities for Women Entrepreneurs

CASE STORY ON GENDER DIMENSION OF AID FOR TRADE Banking on Women Pays Off: Creating Opportunities for Women Entrepreneurs Banking on Women Pays Off Creating Opportunities for Women Entrepreneurs International

CASE STORY ON GENDER DIMENSION OF AID FOR TRADE Banking on Women Pays Off: Creating Opportunities for Women Entrepreneurs Banking on Women Pays Off Creating Opportunities for Women Entrepreneurs International

POTENTIAL RESEARCH OPPORTUNITY FOR SECURED TRANSACIONS REFORM IN COLOMBIA

POTENTIAL RESEARCH OPPORTUNITY FOR SECURED TRANSACIONS REFORM IN COLOMBIA Alejandro Alvarez de la Campa, IFC Boston, September 16, 2011 OUTLINE 1) SECURED TRANSACTIONS: WHAT, WHY, HOW? 2) POTENTIAL IMPACT

POTENTIAL RESEARCH OPPORTUNITY FOR SECURED TRANSACIONS REFORM IN COLOMBIA Alejandro Alvarez de la Campa, IFC Boston, September 16, 2011 OUTLINE 1) SECURED TRANSACTIONS: WHAT, WHY, HOW? 2) POTENTIAL IMPACT

SBP s Seminar on Housing Microfinance. Low Income Housing and Housing Finance

SBP s Seminar on Housing Microfinance Low Income Housing and Housing Finance Syed Farhan Fasihuddin September 06, 2012 sfasihuddin@ifc.org Karachi, Pakistan Content 1. Terminology 2. Low Income Housing

SBP s Seminar on Housing Microfinance Low Income Housing and Housing Finance Syed Farhan Fasihuddin September 06, 2012 sfasihuddin@ifc.org Karachi, Pakistan Content 1. Terminology 2. Low Income Housing

ROLE OF THE BANKING SECTOR IN PROMOTING GROWTH & DEVELOPMENT OF SMALL AND MEDIUM ENTERPRISES ADDRESS DR. C. L. DHLIWAYO ACTING GOVERNOR MARCH 2014

ROLE OF THE BANKING SECTOR IN PROMOTING GROWTH & DEVELOPMENT OF SMALL AND MEDIUM ENTERPRISES ADDRESS BY DR. C. L. DHLIWAYO ACTING GOVERNOR AT THE 2 ND SME BANKING & MICROFINANCE SUMMIT 2014 MARCH 2014

ROLE OF THE BANKING SECTOR IN PROMOTING GROWTH & DEVELOPMENT OF SMALL AND MEDIUM ENTERPRISES ADDRESS BY DR. C. L. DHLIWAYO ACTING GOVERNOR AT THE 2 ND SME BANKING & MICROFINANCE SUMMIT 2014 MARCH 2014

Improving access to finance for small and medium-sized enterprises

Report by the Comptroller and Auditor General Department for Business, Innovation & Skills and HM Treasury Improving access to finance for small and medium-sized enterprises HC 734 SesSIon 2013-14 1 November

Report by the Comptroller and Auditor General Department for Business, Innovation & Skills and HM Treasury Improving access to finance for small and medium-sized enterprises HC 734 SesSIon 2013-14 1 November

Impact Assessment (IA)

") Title: SME Credit Data IA No: N/A Lead department or agency: HM Treasury Other departments or agencies: N/A Impact Assessment (IA) Date: Stage: Final Source of intervention: Domestic Type of measure: Primary

Title: SME Credit Data IA No: N/A Lead department or agency: HM Treasury Other departments or agencies: N/A Impact Assessment (IA) Date: Stage: Final Source of intervention: Domestic Type of measure: Primary

ABL Step 1 An Introduction. How SIPPA can change the Lending Environment and Access to Credit

ABL Step 1 An Introduction How SIPPA can change the Lending Environment and Access to Credit Traditional Bank vs ABL Bank Focused on Credit Status Over reliance on Real Estate Vulnerable to Economic Cycles

ABL Step 1 An Introduction How SIPPA can change the Lending Environment and Access to Credit Traditional Bank vs ABL Bank Focused on Credit Status Over reliance on Real Estate Vulnerable to Economic Cycles

SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL, AND MEDIUM-SIZED ENTERPRISES. 1. Sector Performance, Problems, and Opportunities

: MICRO, SMALL, AND MEDIUM-SIZED ENTERPRISES. 1. Sector Performance, Problems, and Opportunities") Inclusive Micro, Small, and Medium-Sized Enterprises Development Project (RRP MLD 43566) SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL, AND MEDIUM-SIZED ENTERPRISES Sector Road Map 1. Sector Performance, Problems,

Inclusive Micro, Small, and Medium-Sized Enterprises Development Project (RRP MLD 43566) SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL, AND MEDIUM-SIZED ENTERPRISES Sector Road Map 1. Sector Performance, Problems,

PROGRESS REPORT ON G20/OECD HIGH LEVEL PRINCIPLES ON SME FINANCING OECD REPORT TO G20 FINANCE MINISTERS AND CENTRAL BANK GOVERNORS.

PROGRESS REPORT ON G20/OECD HIGH LEVEL PRINCIPLES ON SME FINANCING OECD REPORT TO G20 FINANCE MINISTERS AND CENTRAL BANK GOVERNORS September 2015 At their meeting in April 2015, the G20 Finance Ministers

PROGRESS REPORT ON G20/OECD HIGH LEVEL PRINCIPLES ON SME FINANCING OECD REPORT TO G20 FINANCE MINISTERS AND CENTRAL BANK GOVERNORS September 2015 At their meeting in April 2015, the G20 Finance Ministers

Your bid for growth funds. Supporting your business with financing decisions

Your bid for growth funds Supporting your business with financing decisions Contents 3 Introduction 4 Preparing your application 6 Assessing applications 8 What Barclays considers 9 Funding solutions 10

Your bid for growth funds Supporting your business with financing decisions Contents 3 Introduction 4 Preparing your application 6 Assessing applications 8 What Barclays considers 9 Funding solutions 10

保 理 在 中 国 情 境 下 的 融 资 作 用

所 属 领 域 : 资 产 证 券 化 Category: Asset securitization 发 表 语 言 : 英 文 In English 保 理 在 中 国 情 境 下 的 融 资 作 用 The financing role of factoring in China context Shuzhen Chen 1 School of Management, University of

所 属 领 域 : 资 产 证 券 化 Category: Asset securitization 发 表 语 言 : 英 文 In English 保 理 在 中 国 情 境 下 的 融 资 作 用 The financing role of factoring in China context Shuzhen Chen 1 School of Management, University of

Measures to support access to finance for SMEs. Funding for Lending... 2. The National Loan Guarantee Scheme (NLGS)... 2

... 2") Measures to support access to finance for SMEs Contents Funding for Lending... 2 The National Loan Guarantee Scheme (NLGS)... 2 Enterprise Finance Guarantee (EFG)... 3 Business Finance Partnership (BFP)...

Measures to support access to finance for SMEs Contents Funding for Lending... 2 The National Loan Guarantee Scheme (NLGS)... 2 Enterprise Finance Guarantee (EFG)... 3 Business Finance Partnership (BFP)...

Facilitating Remittances to Help Families and Small Businesses

G8 ACTION PLAN: APPLYING THE POWER OF ENTREPRENEURSHIP TO THE ERADICATION OF POVERTY The UN Commission on the Private Sector and Development has stressed that poverty alleviation requires a strong private

G8 ACTION PLAN: APPLYING THE POWER OF ENTREPRENEURSHIP TO THE ERADICATION OF POVERTY The UN Commission on the Private Sector and Development has stressed that poverty alleviation requires a strong private

THE EURO AREA BANK LENDING SURVEY 3RD QUARTER OF 2014

THE EURO AREA BANK LENDING SURVEY 3RD QUARTER OF 214 OCTOBER 214 European Central Bank, 214 Address Kaiserstrasse 29, 6311 Frankfurt am Main, Germany Postal address Postfach 16 3 19, 666 Frankfurt am Main,

THE EURO AREA BANK LENDING SURVEY 3RD QUARTER OF 214 OCTOBER 214 European Central Bank, 214 Address Kaiserstrasse 29, 6311 Frankfurt am Main, Germany Postal address Postfach 16 3 19, 666 Frankfurt am Main,

Microfinance within the EU banking industry: policy and practice

Microfinance within the EU banking industry: policy and practice This report has been written by the European Banking Federation s Working Group of experts in the financing of Small and Medium-sized Enterprises

Microfinance within the EU banking industry: policy and practice This report has been written by the European Banking Federation s Working Group of experts in the financing of Small and Medium-sized Enterprises

How To Invest In A Farm Business

Impact Investment AFI Summit Discussion August 18, 2015 Catalyzing Investments Over Time Impact Investing S SCALE OF OUTREACH c a l e Institution Building Governance Project-based TA SUSTAINABILITY Why

Impact Investment AFI Summit Discussion August 18, 2015 Catalyzing Investments Over Time Impact Investing S SCALE OF OUTREACH c a l e Institution Building Governance Project-based TA SUSTAINABILITY Why

Banking Services for Everyone? Barriers to Bank Access and Use around the World. Thorsten Beck, Asli Demirguc-Kunt and Maria Soledad Martinez Peria *

Public Disclosure Authorized Banking Services for Everyone? Barriers to Bank Access and Use around the World WPS4079 Thorsten Beck, Asli Demirguc-Kunt and Maria Soledad Martinez Peria * Public Disclosure

Public Disclosure Authorized Banking Services for Everyone? Barriers to Bank Access and Use around the World WPS4079 Thorsten Beck, Asli Demirguc-Kunt and Maria Soledad Martinez Peria * Public Disclosure

British Business Bank Growth Loans Pilot

British Business Bank Growth Loans Pilot Delivering Help to Grow 26 th March 2015 Content Welcome and Introduction The Evidence Base: Research Findings The Growth Loans Pilot Application Process and Next

British Business Bank Growth Loans Pilot Delivering Help to Grow 26 th March 2015 Content Welcome and Introduction The Evidence Base: Research Findings The Growth Loans Pilot Application Process and Next

Women s Finance in the MENA region

Women s Finance in the MENA region This document is an adaptation by AFAEMME of the report Ready for Growth: solutions to increase access to finance for women-owned businesses in the Middle East and North

Women s Finance in the MENA region This document is an adaptation by AFAEMME of the report Ready for Growth: solutions to increase access to finance for women-owned businesses in the Middle East and North

SECTOR ASSESSMENT (SUMMARY): FINANCE 1. 1. Sector Performance, Problems, and Opportunities

: FINANCE 1. 1. Sector Performance, Problems, and Opportunities") Country Partnership Strategy: Bangladesh, 2011 2015 SECTOR ASSESSMENT (SUMMARY): FINANCE 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities 1. The finance sector in Bangladesh is diverse,

Country Partnership Strategy: Bangladesh, 2011 2015 SECTOR ASSESSMENT (SUMMARY): FINANCE 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities 1. The finance sector in Bangladesh is diverse,

Financing in China. Export Development Canada. November, 2012. Chris Evans, Ontario Region

Financing in China Export Development Canada Chris Evans, Ontario Region November, 2012 About Export Development Canada (EDC) Canada s Export Credit Agency Crown corporation wholly owned by Government

Financing in China Export Development Canada Chris Evans, Ontario Region November, 2012 About Export Development Canada (EDC) Canada s Export Credit Agency Crown corporation wholly owned by Government

Chapter 6. Financing of innovative entrepreneurs

Chapter 6. Financing of innovative entrepreneurs Ukraine has entrepreneurial talent and a relatively strong risk-taking attitude. These are major ingredients for any policy intervention seeking to promote

Chapter 6. Financing of innovative entrepreneurs Ukraine has entrepreneurial talent and a relatively strong risk-taking attitude. These are major ingredients for any policy intervention seeking to promote

University meets Microfinance. Do our clients grow? - Microfinance vs. SME Finance

University meets Microfinance Do our clients grow? - Microfinance vs. SME Finance July 2012 Definition(s) of MSME Definitions vary greatly between countries, financial regulators and financial institutions.

University meets Microfinance Do our clients grow? - Microfinance vs. SME Finance July 2012 Definition(s) of MSME Definitions vary greatly between countries, financial regulators and financial institutions.

Banking Services for Everyone? Barriers to Bank Access and Use Around the World

Banking Services for Everyone? Barriers to Bank Access and Use Around the World Thorsten Beck, Asli Demirguc-Kunt and Maria Soledad Martinez Peria * First draft: October 2006 This draft: February 2007

Banking Services for Everyone? Barriers to Bank Access and Use Around the World Thorsten Beck, Asli Demirguc-Kunt and Maria Soledad Martinez Peria * First draft: October 2006 This draft: February 2007

Mexico Country Profile 2010. Region: Latin America & Caribbean Income Group: Upper middle income Population: 105,280,515 GNI per capita: US$8,340.

Mexico Country Profile 2010 Region: Latin America & Caribbean Income Group: Upper middle income Population: 105,280,515 GNI per capita: US$8,340.00 Contents Introduction Business Environment Obstacles

Mexico Country Profile 2010 Region: Latin America & Caribbean Income Group: Upper middle income Population: 105,280,515 GNI per capita: US$8,340.00 Contents Introduction Business Environment Obstacles

CONSULTATION ON PROMOTING SOCIAL INVESTMENT FUNDS AS PART OF THE SOCIAL BUSINESS INITIATIVE. European Commission s Consultation

CONSULTATION ON PROMOTING SOCIAL INVESTMENT FUNDS AS PART OF THE SOCIAL BUSINESS INITIATIVE European Commission s Consultation Response by RESEAU FINANCEMENT ALTERNATIF Chaussée d'alsemberg 303-309 1190

CONSULTATION ON PROMOTING SOCIAL INVESTMENT FUNDS AS PART OF THE SOCIAL BUSINESS INITIATIVE European Commission s Consultation Response by RESEAU FINANCEMENT ALTERNATIF Chaussée d'alsemberg 303-309 1190

AN ENABLING ENVIRONMENT FOR MICROBUSINESS AND THE RULE OF LAW Mike Dennis Department of State

AN ENABLING ENVIRONMENT FOR MICROBUSINESS AND THE RULE OF LAW Mike Dennis Department of State UNCITRAL Colloquium on Microfinance Vienna, January 16-18, 2013 1 An Enabling Environment for Microbusiness

AN ENABLING ENVIRONMENT FOR MICROBUSINESS AND THE RULE OF LAW Mike Dennis Department of State UNCITRAL Colloquium on Microfinance Vienna, January 16-18, 2013 1 An Enabling Environment for Microbusiness

The Sovereign Wealth Fund Initiative Fall 2012

The Sovereign Wealth Fund Initiative Fall 2012 Growing a Middle East- Middle Class: Where Small Investment Goes a Long Way Summary By Elissa McCarter Vice President of Development Finance CHF International

The Sovereign Wealth Fund Initiative Fall 2012 Growing a Middle East- Middle Class: Where Small Investment Goes a Long Way Summary By Elissa McCarter Vice President of Development Finance CHF International

Determinants of Capital Structure in Developing Countries

Determinants of Capital Structure in Developing Countries Tugba Bas*, Gulnur Muradoglu** and Kate Phylaktis*** 1 Second draft: October 28, 2009 Abstract This study examines the determinants of capital

Determinants of Capital Structure in Developing Countries Tugba Bas*, Gulnur Muradoglu** and Kate Phylaktis*** 1 Second draft: October 28, 2009 Abstract This study examines the determinants of capital

Commonwealth Caribbean Regional Conference. Investing in Youth Exploring Strategies for Sustainable Employment. Financing and Financial Mechanisms

Commonwealth Caribbean Regional Conference Investing in Youth Exploring Strategies for Sustainable Employment Financing and Financial Mechanisms Presented by Ian Chinapoo May 25 th, 2011 Outline: Background

Commonwealth Caribbean Regional Conference Investing in Youth Exploring Strategies for Sustainable Employment Financing and Financial Mechanisms Presented by Ian Chinapoo May 25 th, 2011 Outline: Background