National Science Foundation Office of Inspector General 4201 Wilson Boulevard, Suite I-1135, Arlington, Virginia 22230

|

|

|

- Elwin Floyd

- 8 years ago

- Views:

Transcription

1 National Science Foundation Office of Inspector General 4201 Wilson Boulevard, Suite I-1135, Arlington, Virginia MEMORANDUM DATE: September 30, 2015 TO: Dale Bell, Director Division of Institution and Award Support Jamie French, Acting Director Division of Grants and Agreements FROM: SUBJECT: Dr. Brett M. Baker Assistant Inspector General for Audit Labor Effort Reporting under the Federal Demonstration Partnership Pilot Payroll Certification at Michigan Technological University, Report No Attached is the final report of our audit of Michigan Technological University s labor effort reporting under the Federal Demonstration Partnership s pilot payroll certification program. The report contains two findings on: 1) internal controls over the support for labor charges to NSF awards, and 2) information technology controls over the protection of payroll information. We have included Michigan Tech s response as an appendix to the final report. Please coordinate with our office during the six month resolution period, as specified by OMB Circular A-50, to develop a mutually agreeable resolution of the audit findings. Also, the findings should not be closed until NSF determines that all recommendations have been adequately addressed and the proposed corrective actions have been satisfactorily implemented. The Offices of Inspector General at NSF and the Department of Health and Human Services are auditing the implementation of pilot payroll certification systems at four universities. Individual reports will be prepared for each audit; then a capstone report will be prepared when all audits are completed to provide overall results and summarize issues identified at all four universities. This report presents the findings at Michigan Tech.

2 We appreciate the assistance from Michigan Tech officials, staff, and students that was extended to our auditors during this audit. If you have any questions, please contact Louise Nelson, Director of Audit Services, at (303) Attachment cc: France A. Córdova Richard Buckius Ruth David Michael Van Woert Larry Rudolph Ann Bushmiller Karen Tiplady Christina Sarris Allison Lerner Fae Korsmo Alex Wynnyk Rochelle Ray Louise Nelson Keith Nackerud Kaitlin McDonald

3 Labor Effort Reporting under the Federal Demonstration Partnership s Pilot Payroll Certification at Michigan Technological University National Science Foundation Office of Inspector General 09/30/2015 OIG TM 13-E-1-006

4 Table of Contents Introduction...1 Background...2 Audit Results...5 Findings 1. Michigan Tech Needs to Strengthen its Internal Controls to Ensure Labor Charges to NSF Awards are Adequately Supported Michigan Tech Needs to Strengthen its Information Technology Controls to Protect Payroll Information...8 Conclusion...8 Recommendations...9 Summary of Awardee Response and OIG Comments...10 OIG Contact and Staff Acknowledgements...11 Appendices A. Agency s Response to Draft Report...12 B. Audit Objectives, Scope, and Methodology...14 C. Sample Design, Methodology, and Results...16 D. Additional Details on Information Technology General Controls...21

5 Introduction Federal Demonstration Partnership (FDP) The FDP began in 1986 as an experiment between five Federal agencies (National Science Foundation, National Institutes of Health, Office of Naval Research, Department of Energy, and US Department of Agriculture), the Florida State University System and the University of Miami to test and evaluate a grant mechanism utilizing a standardized and simplified set of terms and conditions across all participating agencies. The result of the test was the establishment of expanded authorities throughout the nation, intended to reduce administrative tasks for both the Federal government and research institutions. One way in which the FDP wanted to reduce administrative tasks involves changing the amount and type of documentation required to support salary and wage charges to Federal awards. Historically, effort reports have been used as the main support for salary and wage charges to federal grants and contracts. Effort reporting is a person-based methodology that allocates each individual s salary to the various projects he/she worked on during the reporting period. FDP proposes a payroll certification system as an alternative to effort reporting. Payroll certification is a project-based methodology that relies on a project s principal investigator to certify that all salaries charged to the project are fair and reasonable in relation to the work performed. FDP asserts the alternative is preferable because: effort is difficult to measure; effort reports provide limited internal control; and effort reporting systems may be expensive to implement and maintain. Audits of the Pilot Payroll Certification Systems As agreed to by the Office of Management and Budget (OMB) and the Offices of Inspector General at NSF and the Department of Health and Human Services (HHS), these two OIGs are auditing the implementation of pilot payroll certification systems at four universities: University of California - Irvine; University of California - Riverside; Michigan Technological University (Michigan Tech); and George Mason University. HHS OIG is conducting the audits of the two University of California institutions, while NSF OIG is responsible for the audits at Michigan Tech and George Mason University. Although the audit plan and methodology was consistent across all pilot institutions, the results will differ depending on each institution s implementation of its respective pilot system as well as the nature of the grants and related guidance from the awarding agency (NSF and HHS). A capstone report will be prepared when all audits are completed to provide overall results and summarize issues identified at all four universities. This report presents the results of the audit work conducted at Michigan Technological University for its NSF awards. 1

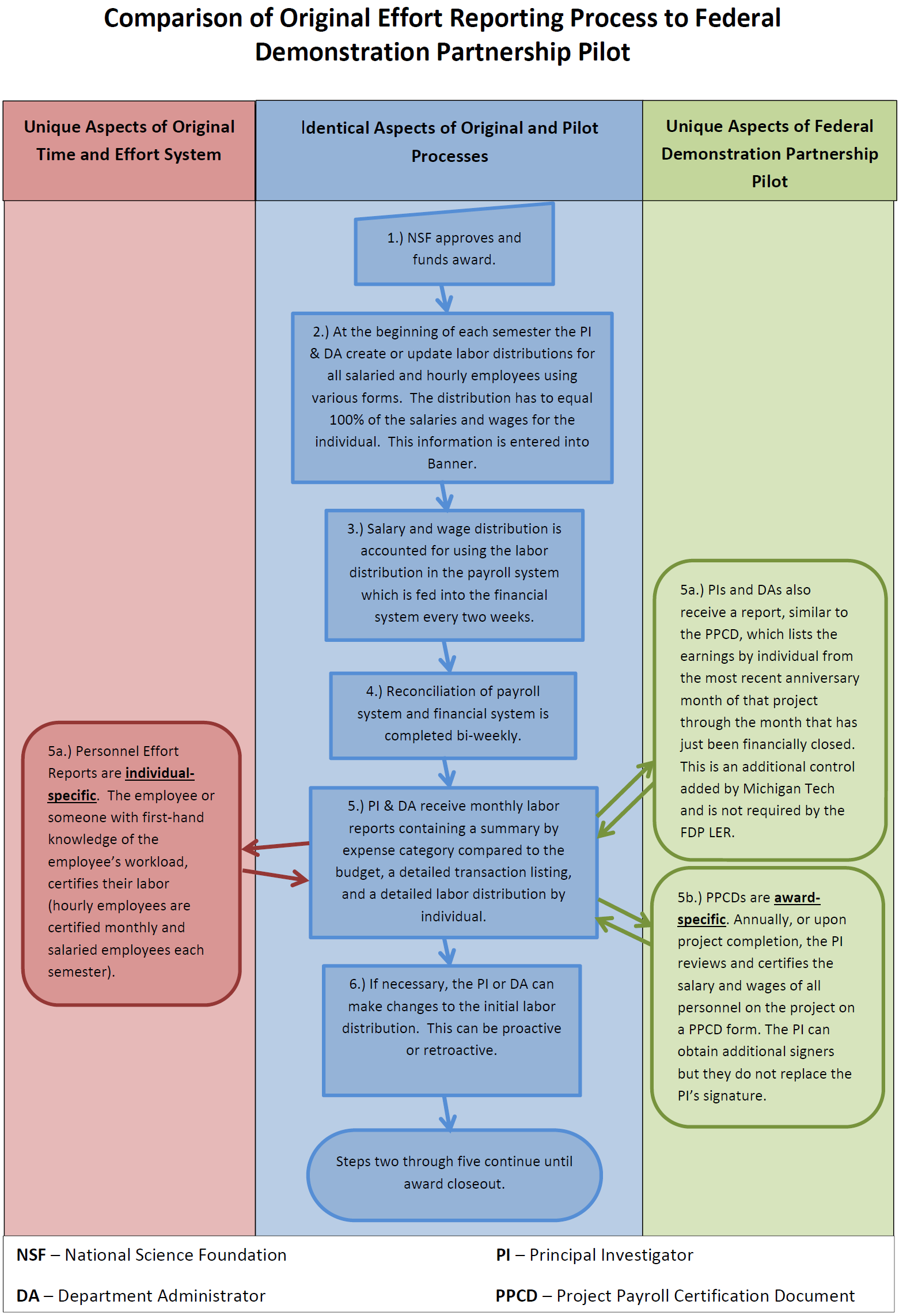

6 Background Our audit scope spanned labor charges at Michigan Technological University under both the effort reporting system and the pilot payroll certification process. Therefore, we first developed an understanding of both systems, as implemented by Michigan Tech. Effort Reporting System The effort reporting process at Michigan Tech began with entering each employee in the payroll allocation system using an Employee Status Change Form or Request for Account Distribution Change Form showing the salary level and accounts, including awards, to be charged. This initial allocation of effort for each staff person is entered into the Banner payroll allocation system, and the total allocation must equal 100 percent. For hourly employees/students, effort is similarly established using the student requisition/status change form. The initial distribution of effort may be amended during the semester, or between semesters, as needed, for changes in workload effort or changes in projects/activities. Such changes can be made using an Employee Status Change Form or Request for Account Distribution Change Form, and on the timesheet itself. However, the researchers (frequently graduate students) typically only work on one award at a time, so their effort was not often distributed across multiple awards or activities at the university. In fact, of the 826 employees who charged salaries to NSF during our audit period, 600 (73 percent) allocated full salaries (on a pay period basis) to a single NSF project account rather than to multiple projects. Each month the after-the-fact effort reports, for graduate, undergraduate, and hourly employees, are signed (for the pay periods in that month). Each semester the after-the-fact effort reports, for salaried employees (faculty and professional staff) are signed (for the pay periods in that semester). The effort reports are signed by either the employee or by someone with first-hand knowledge of the employee s workload. The signature certifies that the labor distribution supporting the award charges does reasonably reflect the individual s effort during the effort period and that the percentage of effort is reasonable. As non-faculty account for most of the labor effort charges to Michigan Tech s NSF awards (85 percent), the vast majority of salary charges were supported by biweekly timesheets. Biweekly timesheets signed by the employee were only required for hourly employees graduates, undergraduates and all non-faculty staff and accounted for 85 percent of labor charges. Pilot System Michigan Tech s process for initiating research salary charges was the same under the pilot as under the prior effort reporting process, as depicted in the following chart. The difference is that Michigan Tech s annual certifications (Project Payroll Certification Document, or PPCDs) included all salaries charged to the respective awards by all employees who worked on the project during the reporting year. The PPCD does include a percent of total compensation for the Principle Investigator s (PI) consideration. The PI is responsible for certifying annually that all individuals worked on this project, the salary and wage charges were accurate and reasonable in relation to the work performed, and the federal costing requirements as shown in the 2

7 instructions were met for all employees included on the report. The PI can obtain additional signers (CO-PIs, direct supervisors, and/or accounting/budget analyst specific to the sponsored project) to assist in verifying the accuracy of the salary and wage expense. This certification meets the requirements stated in the FDP pilot as well as OMB Circular A-21 requirements. The certification is to be completed and returned to the Sponsored Programs Accounting within 35 days of distribution. However, the certification does not report effort on other awards the individual worked on during the reporting period, which is a risk. Comparison of the Previous and Pilot Processes at Michigan Tech The following flowchart depicts the similarities and differences between the two processes at Michigan Tech. Both the prior effort reporting process and the pilot payroll certification process utilize payroll information maintained in the Banner system. 3

8 4

9 Audit Results We performed this audit to determine whether Michigan Tech s payroll certification system provided accountability over federal funds. An area of particular concern was whether the pilot system s shift away from certifying 100 percent of individual employee s effort put federal funds at an increased risk of improper allocation. We based our determination on assessments of Michigan Tech s controls designed to (1) ensure that the university charged allowable labor costs to its NSF awards and (2) secure the data used to support labor charges. To test the controls over the allowability of labor charges to NSF awards, we selected a sample of 180 payroll transactions for review. Our sample included transactions under both Michigan Tech s payroll certification pilot and the prior effort reporting system. While many of the steps under the pilot were unchanged from the prior system several were different, as discussed in this report. Overall, we found that Michigan Tech s system generally provided accountability over federal funds. However, Michigan Tech did not always comply with its documentation policies for payroll transactions under the effort reporting process as well as the payroll certification pilot. We also identified weaknesses in the controls over Banner, the system Michigan Tech uses for payroll allocation, under both the effort reporting system and the payroll certification pilot. Specifically, the university could improve its control and enforcement mechanisms over Banner and formalize processes, policies and procedures over the audit capabilities for Banner. As a result, the data retained in the Banner information system to support payroll charges to federal awards may not be secure and could be vulnerable to access by unauthorized users who could modify information. 1. Michigan Tech Needs to Strengthen its Internal Controls to Ensure Labor Charges to NSF Awards are Adequately Supported Michigan Tech requires the following documentation as support for labor charges to federal awards: Employee Personnel Action Form (EPAF) and/or timesheets for hourly employees/students; EPAF and/or Employee Status Change Form (ESCF) for faculty and professional staff working on federal awards; reallocation forms for after-the-fact changes for all employees; monthly and semester certification of work performed (effort reporting only); and annual certification (PPCD) of payroll expenses charged to each federal award (pilot only). Based on the type of transaction that was tested (initial labor charge or labor reallocation), at least one of these documents was required to support a specific sampled transaction. To test the effectiveness of Michigan Tech s internal controls over both payroll allocation systems, we selected a sample of 180 transactions, 1 representing $145,152 of costs charged to NSF awards, from a universe of 11,674 transactions, representing $9,552,835 in NSF payroll 1 See Appendix C for the sample design, methodology and results. 5

10 charges. The transaction universe included 68 transactions under the prior effort reporting process and 112 transactions under the payroll certification pilot. We found problems (which are detailed below) in 8 of the 180 sample transactions we tested, totaling $8,757. If the inaccuracies and lack of adequate supporting documentation found in the sampled transactions occurred with the same frequency across the population, we project that Michigan Tech lacked adequate supporting documentation for $145,152 out of the $9,552,835 salary costs claimed against NSF awards during the audit period. Fringe benefits and facilities and administrative (F&A) costs associated with the projected costs are $ and $ respectively. Our estimate was based on a universe of 11,674 total payroll transactions projecting the identified errors at 90 percent confidence. 2 The majority of the problematic transactions were the result of Michigan Tech failing to follow its own internal policies and procedures. The following sections describe the documentation issues identified in our audit. Timeliness of Certifications Our sample included 68 transactions under the prior effort reporting system. We found that 5 of the 68 transactions we tested under the prior effort reporting system at Michigan Tech had effort reports which were submitted late and one did not have a signed effort report. Michigan Tech effort reports were normally due three weeks after the effort reports were generated. The five effort reports were between 4 and 246 days late. The university stated that it generated and disseminated approximately 7,000 effort certifications each year, and that late certifications occurred, in part, because of the large number of annual certifications. The sixth transaction did not have a signed effort report. OMB A-21 requires after-the-fact certifications of effort on sponsored awards and so does Michigan Tech policy. Under the prior effort reporting system at Michigan Tech, effort reports are usually used for this requirement. Michigan Tech also has reallocation forms. These forms are used to document the movement of money related to a sponsored award. The reallocation forms are signed and meet the requirement of an after-the-fact certification of effort. Michigan Tech was able to provide a reallocation of funds form for 9% of the funds related to this one transaction. However, the remaining 91% of the funds charged to NSF did not have an effort report or other form of afterthe-fact certification of the effort, such as a reallocation of funds form. The remaining 112 sampled transactions were under the payroll certification pilot. There were no late or unsigned PPCDs under the payroll pilot. Michigan Tech needs to strengthen its internal controls over its payroll allocation and certification processes to ensure labor charges to NSF awards are adequately supported, as required by federal regulation, NSF, and university policy. 2 See Appendix C for complete details of the sample design, methodology, and results. 6

11 Policies and Procedures Our sample included 112 transactions under the payroll certification. We found the following 2 problems related to changing salary and wage distributions in the 112 transactions tested under the payroll certification pilot. First, Michigan Tech did not follow its policies for changing the salary and wage distributions for two employees. The university s policy provides three options for changing the initial salary and wage distributions for employees. Changing of the initial salary and wage distribution is needed when an employee, who was originally hired to work on one project, switches and works on a different project. In the first transaction, Michigan Tech relied on s and hand written notes to change the initial salary and wage distribution. Michigan Tech policy required these changes be documented on a biweekly timesheet or on the original hiring documents because the issue was identified before the submission of the biweekly payroll cycle. Michigan Tech stated that s indicated that a correction needed to be made quickly. If these two options could not be completed before the submission of the biweekly payroll cycle, Michigan Tech policy also allows for a reallocation after the biweekly payroll cycle. However, Michigan Tech did not follow any of these three procedures to change the initial salary and wage distributions. Second, Michigan Tech processed a second transaction based on hand written notes on a human resources document. University policy required the use of a reallocation of funds form since the change to the initial salary and wage distribution was made after the submission of the biweekly payroll cycle. When personnel involved in the payroll certification process do not follow university procedures, it raised concerns about the institution s internal controls. The remaining 68 sampled transactions were under the prior effort reporting system. There were no issues with adjusting the initial salary and wage distributions under the prior system. As stated previously, a primary concern of this audit was to determine whether the fact the pilot system does not require certifying 100 percent of each employee s effort increased the risk of improper allocations of payroll. We found that full allocations remain recorded and available within Michigan Tech s systems. Nonetheless, when PIs certify the salaries charged to their awards, they do not have records of full payroll allocations for employees who worked on their projects. Visibility over full payroll allocations provides greater assurance that project costs are accurate. Therefore, making full allocations available to PIs would be useful in assuring payroll charges to federal awards are accurate. Additionally, accounting for full allocations of employees time could be an important control to help ensure that overcharges and inaccurate charges do not occur. Based on the number and types of errors we identified from the transaction testing, Michigan Tech needs to strengthen its internal controls over its payroll allocation and certification processes to ensure labor charges to NSF awards are adequately supported, as required by federal regulation, NSF, and university policy. 7

12 2. Michigan Tech Needs to Strengthen its Information Technology Controls to Protect Payroll Information Both the prior effort reporting process and the pilot payroll certification process utilize payroll information maintained in the Banner system. Auditors identified the following areas in which IT controls needed to be strengthened:. National Institute of Standards and Technology Guidance (NIST) recommends organizations help prevent abuse of the system and its data. Michigan Tech can. NIST guidelines recommend employees. A general vulnerability in Banner was identified that could potentially allow unauthorized access to the entire system. We reported this issue to Michigan Tech immediately, and it is working to address this vulnerability. Michigan Tech did not have formalized processes, policies or procedures over the audit capabilities established for Banner, as recommended by NIST. In the absence of formalized system auditing, Michigan Tech cannot ensure that unauthorized system changes or system access is identified, and timely remediation action is executed. As a result of these IT control weaknesses, the data in the Banner information system used to support payroll charges to Federal awards may not be secure, and could put the reliability of information used as the basis for labor charges to federal awards at risk. These system weaknesses were identified under the prior effort reporting process and still existed during the pilot process. Therefore, the reliability of the payroll and effort reporting cost data used to support Michigan Tech labor charges is at risk until these control weaknesses are addressed. Conclusion Inappropriately changed salary and wage distributions under the pilot system was the main issue identified in the transactions sampled. Late effort certifications was the most prevalent issue identified under the prior effort reporting system. When effort reports are certified after work has been completed, there is a higher likelihood that labor will be charged incorrectly. In 8

13 addition, when internal controls are not adhered to it raises questions about the control environment. We concluded that these problems occurred because Michigan Tech did not follow its internal policies and procedures, and were not the result of inadequate controls over the pilot system. When reviewing the IT controls over the Banner information system, we identified many weaknesses that occurred because Michigan Tech failed to establish and enforce adequate controls. Given that the data for both the effort reporting and pilot processes was housed in Banner, these IT weaknesses were not attributable to the design of either the effort report or pilot certification systems but to the Banner system as a whole. Both the pilot system and the prior effort system rely on the people and systems involved and on the institution to have adequate internal controls to ensure that its policies and procedures are followed. If institutions use the pilot, they need to ensure that they have strong internal controls to ensure the payroll charges are adequately supported. If schools are going to certify the documentation less frequently, they have to be more diligent in ensuring that control procedures are communicated and adhered to on a consistent basis. Additionally, maintaining the full allocation of payroll to each individual s activities is important to ultimately ensure adequate support for Federal labor charges. Having direct visibility of each employee s full payroll allocation, including percentage allocations assigned to other awards or projects, is important to a PI to ensure the percentage assigned to his or her project is reasonable. Accounting for full allocations of employees time could be an important control to help ensure that overcharges and inaccurate charges do not occur. There are challenges with any payroll allocation system, and strong internal controls are the key to ensuring taxpayer funds are appropriately charged and adequately protected from misuse and abuse. Recommendations We recommend that NSF s Director of the Division of Institutional and Award Support (DIAS) direct Michigan Technological University to: 1. Enforce its written policies for the pilot payroll certification system. Specifically, Michigan Tech needs to ensure that processes for changing the salary and wage distributions of employees are adhered to. 2. Enhance internal controls over information technology as follows: a. Review current access privileges for finance and human resource personnel and revise current access permissions based on least privilege; b. Review the current termination notification process an implement necessary procedures to ensure timely removal of user access rights; and c. Review d. We recommend Michigan Tech formalize and implement policies and procedures for Banner auditing functions and processes. 9

14 Summary of Awardee Response and OIG Comments Recommendation 1 Response and OIG Comments Michigan Tech concurs with the recommendations and notes that in several instances they have implemented changes prior to receiving these recommendations. It acknowledges following the three existing procedures to change salary and wage distribution will strengthen their internal controls over payroll allocations, and they will continue to provide communication and education to the central and department administrators responsible for the changes to the initial salary and wage allocations. It also notes that the Payroll Certification pilot has strengthened its internal controls over its certification process. Michigan Tech s response also states that the audit report concludes that Michigan Tech has adequate controls over the pilot system. The audit report actually states, Overall, we found that Michigan Tech s system generally provided accountability over federal funds. The audit report noted specific concerns with the Payroll Certification pilot itself. Specifically, the audit report notes that an area of particular concern with the pilot was whether the pilot system s shift away from certifying 100 percent of individual employee s effort put federal funds at an increased risk of improper allocation. Michigan Tech states that the percent of total compensation for each individual employee is included on the PPCD, and that the PI had firsthand knowledge for the nature and scope of the work performed. The audit report notes that the PPCD does not report effort on other awards the individual worked on during the reporting period, which is a risk. When PIs certify the salaries charged to their awards, they do not have records of full payroll allocations for employees who worked on their projects. Visibility over full payroll allocations provides greater assurance that project costs are accurate. Therefore, making full allocations available to PIs would be useful in assuring payroll charges to federal awards are accurate. Additionally, accounting for full allocations of employees time could be an important control to help ensure that overcharges and inaccurate charges do not occur. Recommendation 2 Response and OIG Comments Michigan Tech concurs with the recommendations and notes that in several instances they have implemented changes prior to receiving these recommendations. Michigan Tech concurs that there are areas in which IT controls need to be strengthened. Michigan Tech also noted that they have implemented newly defined roles and job responsibilities regarding user access in Banner; are reviewing their nightly automated termination process to ensure timely removal of access; the was reviewed and the vulnerability has been addressed; they are in the process of identifying a Security Incident and Event Management tool to help with the maintenance, monitoring, and analysis of audit logs; implemented audit and logging controls on HR banner tables; and is formalizing and implementing policies and procedures related to the Banner auditing functions and processes. 10

15 OIG Contact and Staff Acknowledgements Louise Nelson, Director, Audit Services or In addition to Ms. Nelson, Daniel Buchtel, Keith Nackerud, Kenneth Lish, Catherine Walters, Brittany Moon, Jeremy Hall, and Jennifer Miller made key contributions to this report. 11

16 Appendix A: Auditee Response to Draft Report 12

17 13

18 Appendix B: Audit Objective, Scope and Methodology The objective of the audit was to determine whether Michigan Technological University s (Michigan Tech ) prior effort reporting and current pilot payroll certification processes had adequate controls to (1) ensure that the University charged allowable labor costs to its NSF awards and (2) secure the data used to support labor charges. The payroll certification pilot started at Michigan Tech in July The audit was announced on March 11, The audit scope encompassed the period of January 2, 2010 through March 31, We selected 180 of 11,674 transactions to test, totaling $145,152 of the $9,552,835 sample universe. See Appendix C for the sampling design, methodology and results. We gained an understanding of the payroll certification processes (both the pilot and the former processes used at Michigan Tech); payroll processes; how these processes relate to both the labor costs in Michigan Tech s general ledger, and how labor costs are charged to Federally sponsored awards. We also performed an on-site visit to obtain an understanding of the processes, procedures, and internal controls related to the scope and objectives of the audit. Our focus was on the labor certification process, labor effort recording and reporting, and accountability for labor costs charged to NSF awards. In order to ensure that we had a comprehensive universe of all payroll related transactions charged to Federal awards by Michigan Tech, we obtained reconciliations between the general ledger (GL) and the payroll subsidiary ledger; between the payroll subsidiary ledger and the payroll certification records; and also between the payroll sub ledger, payroll certification records and the GL; and, between the GL and the federal financial reports (FFR). We requested and analyzed all pertinent GL, payroll subsidiary ledger, and labor effort details (timesheets, appointment letters) and performed data analytics to target payroll-related transactions for detailed test work. We utilized data analytics to establish business rules that were utilized for risk assessment of the data and also to formulate strata. Under the data analytics process, 100% of all labor-related transactions were subject to review utilizing the business rules developed to test the transactions. We relied on the work of an HHS OIG statistical specialist, who used the HHS OIG Office of Audit Sampling Policies and Procedures and RATSTAT to select a simple random stratified variable sample for testing. We also relied on the work of an HHS OIG IT auditor to conduct the IT portion of the audit. For each employee for which a transaction was selected for review, we obtained and reviewed supporting documentation to determine whether labor costs were actually incurred, benefited NSF awards, and were accurately and timely recorded and charged to NSF awards. We also conducted on-site interviews of selected employees to obtain corroborating evidence of the documentation. 14

19 We tested the 180 sample transactions for allowability against the following criteria: Generally Accepted Accounting Principles (GAAP) National Institute of Standards and Technology guidance on information technology OMB Circular A-21, Cost Principles for Educational Institutions NSF Grant Policy Manual (GPM) NSF Grant Policy Guidance (GPG) Individual award agreements Michigan Tech Policies and Procedures We conducted this performance audit in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions. We held an exit conference with Michigan Tech officials on September 2,

20 Appendix C: Sample Design, Methodology, and Results We used stratified sampling to select a sample of 180 payroll transactions for testing during the audit. The sample design, methodology, and results are as follows: Sample Design and Methodology Population: The population contained all salary and wage transactions charged by Michigan Technological University (Michigan Tech) to its NSF awards for the period January 2, 2010, through March 31, Sampling Frame: Michigan Tech provided excel files of Michigan Tech s accounting system general ledger and payroll sub-ledger for the period January 2, 2010, through March 31, From these ledgers, we identified 13,942 individual payroll transactions (transaction) records totaling $8,902,323. The NSF OIG Data Analytics Team (DAT) imported the original excel files into its ACL tool (the ACL Project). After data analytics (see Sample Design, below), we removed all transactions equal to or less than $100. This included the removal of all negative dollar transactions. This resulted in a sample frame consisting of 11,674 transactions totaling $9,552,835. Sample Unit and Design: The sample unit was an individual payroll transaction. All transactions within the sampling frame underwent data analytics tests covering four areas of high risk: charges to expired awards, excess salary charges, high risk adjustments, and administrative salaries (e.g., indirect costs) charged directly to awards. Each area of high risk comprised a stratum for statistical sampling purposes. All transactions that did not fall within one of these 4 strata placed in Strata 5 entitled All Other Transactions. Details of the steps used in the development of the five strata and rules followed in assigning transactions were as follows: Stratum #1 - Charges to Expired Awards The DAT created a business rule to identify transactions either posted or earned in a pay period subsequent to the expiration date of the award. Stratum #2 - Excess Salary The DAT created five separate business rules to test for excess salary charges: labor charges that cumulatively exceed NSFs 2 month limitation for senior personnel, high risk payroll transactions, employee charges that exceed 100% in a labor distribution, payroll transactions posted to awards with no budgeted salary and wages, and employee charges that exceeded the maximum number of hours allowed for the pay cycle. Any transaction containing one or more of 16

21 the attributes tested in the business rules detailed below fell into this stratum. 2-month Salary Limit: The DAT conducted the 2 month salary limit for senior NSF project personnel test as follows: Requested appointment detail which included annual salary rates for the employees identified by Michigan Tech to be senior personnel. Michigan Tech provided this information. Used the appointment detail to calculate the 2 Month Limit Amount for each employee. The DAT developed a conservative decision rule wherein the rate used to calculate the 2 Month Limit Amount was the employee s appointment year highest base salary amount. Sorted all senior personnel payroll charges The appointment year for all senior personnel is based on the University s academic year. High Risk Pay Transactions: The second business rule identifies payroll transactions deemed high risk based on data analyst judgment and knowledge of the data, outliers present in the data, prior audit experience, and review of Michigan Tech policy and procedures. To aid in identifying potential high risk excess salary charges, the DAT first summarized (totaled) the transactions by (a) Account code;. Any transaction that was posted to the following high risk classifications fell into this stratum. Labor Distribution Exceeds 100%: The third business rule identifies payroll transactions in which the cumulative labor distribution to a particular index for a specific job event exceeds 100%. Transactions that either individually or cumulatively exceeded 100% for a labor distribution fell into this stratum. This test was limited to salaried personnel. Labor Charges to Awards with no Budgeted Salary & Wages: The fourth business rule identifies charges to awards with no budgeted salary. this stratum. Any transaction to an award that had no budgeted salary and wages fell into Labor Distribution Hours Exceeds Pay Cycle Maximum: The last business rule identifies transactions in which the cumulative number of hours worked exceeded the maximum number of hours allowed for the pay cycle. Michigan Tech only has a bi-weekly pay cycle, thus the number 17

22 of hours worked for any employee should never exceed 80 hours. Transactions that either individually or cumulatively exceeded the 80 hour bi-weekly pay period maximum number of hours fell into this stratum. Stratum #3 - High Risk Adjustments The DAT created a business rule to identify high risk adjustment transactions which we defined using auditor and data analyst judgment after gaining an understanding of the types of adjustments within the Michigan Tech data, reviewing Michigan Tech policies and procedures, and reviewing patterns within the data. Stratum #4 - Administrative Salaries The DAT created a business rule to identify transactions that appear to be administrative in nature and as such should not be directly charged to sponsored projects. The criteria used to define administrative type salaries included NSF grant policy guidance and OMB circulars, as well as auditor experience and data analyst judgment and knowledge of Michigan Tech s payroll data. The DAT summarized the transactions by (a) Account code; (b) Position Number/Job Title; and (c) NSF Budget Sub-Category. Stratum #5 - All Other Transactions Any salary and wage transactions that did not fall within any of the other stratum were placed within Stratum 5. The application of criteria to the various stratums resulted in the following sampling frame: Stratum Michigan Technological University Record Count Dollar Value Number of Sample Items Selected 1 - Charges to Expired Awards 68 52, Excess Salary 2,080 2,972, High Risk Adjustments , Admin Salaries 1,518 1,395, All Other Transactions 7,835 5,033, TOTALS 11,674 $9,552, Method for Selecting Sample Units: We arranged the transactions within each stratum in date order pursuant to the general ledger posting date as provided by Michigan Tech in its data. We then consecutively numbered the transactions within each stratum. After generating random numbers for each stratum using the U.S. Health and Human Services, Office of Inspector General, Office of Audit Services (HHS OIG/OAS) statistical software, we selected the corresponding frame items. 18

23 Sample Results Estimation Methodology: HHS OIG/OAS used the RAT-STATS variable appraisal program for stratified samples to estimate the amount of unallowable salary and wage costs claimed by Michigan Tech against NSF awards for the audit period. In addition, we provided the 8 sample transactions that were determined to be in error to Michigan Tech staff and asked them to provide us with the (1) Fringe Benefit and (2) Facilities & Administrative (F&A) costs associated with those transactions. HHS OIG then estimated the Fringe Benefits and F&A costs associated with the original sample transactions. Results: Payroll Transactions (Salary and Wage Costs) Stratum Frame Size Value of Frame Sample Size Value of Sample Number of Transactions in Error Value of Transactions in Error 1 68 $52, $23,196 2 $2, ,080 2,972, , , , , ,518 1,395, , ,835 5,033, , Total 11,674 $9,552, $145,152 8 $8, Results: Fringe Benefits Results: F&A COSTS Stratum Frame Size Sample Size Number of Transactions in Error Value of Transactions in Error $ , , , , Total 11, $1, Stratum Frame Size Sample Size Number of Transactions in Error Value of Transactions in Error $1,

24 2 2, , , , Total 11, $4, Total Estimated Value 3 of Salary and Associated Costs for Transactions in Error Category Point Estimate Lower Limit Upper Limit Salaries/Wages Fringe Benefits F&A Costs Totals $820,079 $151,349 $1,557,068 3 HHS OIG calculated the Estimates and Limits for a 90-Percent Confidence Interval. 20

25 Appendix D: Additional Details on Information Technology General Controls Appdetective was used to assess common security vulnerabilities found on Oracle databases. The Appdetective database security assessment identified one high-risk vulnerability. Michigan Tech did not have formalized processes, policies or procedures over the audit capabilities established for Banner. NIST Special Publication , Revision 3, Recommended Security Controls for Federal Information Systems and Organizations, AU-1, recommends the organization an audit and accountability policy that addresses purpose, scope, roles, responsibilities, management commitment, coordination among organizational entities, and compliance. In addition, NIST recommends the organization develop and documents procedures to facilitate the implementation of the audit and accountability policy and associated audit and accountability controls. 21

Labor Effort Reporting under the Federal Demonstration Project s Pilot Payroll Certification Program at George Mason University, Report No.

National Science Foundation Office of Inspector General 4201 Wilson Boulevard, Suite I-1135, Arlington, Virginia 22230 MEMORANDUM Date: July 31, 2015 To: Dale Bell, Director Division of Institution and

National Science Foundation Office of Inspector General 4201 Wilson Boulevard, Suite I-1135, Arlington, Virginia 22230 MEMORANDUM Date: July 31, 2015 To: Dale Bell, Director Division of Institution and

Joanne S. Tornow Office Head, Office of Information & Resources Management and Chief Human Capital Officer, National Science Foundation\

National Science Foundation Office of Inspector General 4201 Wilson Boulevard, Suite I-1135, Arlington, Virginia 22230 MEMORANDUM DATE: September 30, 2015 TO: FROM: Joanne S. Tornow Office Head, Office

National Science Foundation Office of Inspector General 4201 Wilson Boulevard, Suite I-1135, Arlington, Virginia 22230 MEMORANDUM DATE: September 30, 2015 TO: FROM: Joanne S. Tornow Office Head, Office

Audit of Payroll Distribution System California Institute of Technology Pasadena, California National Science Foundation Office of Inspector General

Audit of Payroll Distribution System California Institute of Technology Pasadena, California National Science Foundation Office of Inspector General March 30, 2007 OIG 07-01-013 XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Audit of Payroll Distribution System California Institute of Technology Pasadena, California National Science Foundation Office of Inspector General March 30, 2007 OIG 07-01-013 XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Revised Audit of the National Science Foundation s Travel Card Program, Report No. 15-2-008

National Science Foundation Office of Inspector General 4201 Wilson Boulevard, Suite I-1135, Arlington, Virginia 22230 MEMORANDUM DATE: August 18, 2015 TO: FROM: SUBJECT: Martha A. Rubenstein Chief Financial

National Science Foundation Office of Inspector General 4201 Wilson Boulevard, Suite I-1135, Arlington, Virginia 22230 MEMORANDUM DATE: August 18, 2015 TO: FROM: SUBJECT: Martha A. Rubenstein Chief Financial

Welcome to the Project Payroll Certification an alternative method to Effort Reporting training session. Presenters: Tammy LaBissoniere, Associate

Welcome to the Project Payroll Certification an alternative method to Effort Reporting training session. Presenters: Tammy LaBissoniere, Associate Director of Sponsored Programs Accounting Julie Seppala,

Welcome to the Project Payroll Certification an alternative method to Effort Reporting training session. Presenters: Tammy LaBissoniere, Associate Director of Sponsored Programs Accounting Julie Seppala,

Mary F. Santonastasso, Director Director, Division of Institution and Award Support

National Science Foundation Office of Inspector General 4201 Wilson Boulevard, Suite I-1135, Arlington, Virginia 22230 MEMORANDUM Date: March 31, 2015 To: Mary F. Santonastasso, Director Director, Division

National Science Foundation Office of Inspector General 4201 Wilson Boulevard, Suite I-1135, Arlington, Virginia 22230 MEMORANDUM Date: March 31, 2015 To: Mary F. Santonastasso, Director Director, Division

Effort Reporting Regulations

Effort Reporting Regulations Objectives Become familiar with the federal requirements for Effort Reporting Receive a broad understanding of what is Effort and Effort Reporting, and the relationship between

Effort Reporting Regulations Objectives Become familiar with the federal requirements for Effort Reporting Receive a broad understanding of what is Effort and Effort Reporting, and the relationship between

UNIVERSITY OF ARIZONA SAHRA CENTER 888 N. Euclid Ave. Tucson, AZ 85721

UNIVERSITY OF ARIZONA SAHRA CENTER 888 N. Euclid Ave. Tucson, AZ 85721 National Science Foundation Award Numbers EAR-9876800 Financial Schedules and Independent Auditors Reports For the Period January

UNIVERSITY OF ARIZONA SAHRA CENTER 888 N. Euclid Ave. Tucson, AZ 85721 National Science Foundation Award Numbers EAR-9876800 Financial Schedules and Independent Auditors Reports For the Period January

NASHVILLE STATE TECHNICAL COMMUNITY COLLEGE 120 WHITE BRIDGE ROAD NASHVILLE, TENNESSEE 37209

NASHVILLE STATE TECHNICAL COMMUNITY COLLEGE 120 WHITE BRIDGE ROAD NASHVILLE, TENNESSEE 37209 NATIONAL SCIENCE FOUNDATION AWARD NUMBERS DUE-9850307, DUE-0202249, DUE-0202397 FINANCIAL AUDIT OF FINANCIAL

NASHVILLE STATE TECHNICAL COMMUNITY COLLEGE 120 WHITE BRIDGE ROAD NASHVILLE, TENNESSEE 37209 NATIONAL SCIENCE FOUNDATION AWARD NUMBERS DUE-9850307, DUE-0202249, DUE-0202397 FINANCIAL AUDIT OF FINANCIAL

Audit of Effort Reporting System. Cornell University Ithaca, New York

Audit of Effort Reporting System Cornell University Ithaca, New York National Science Foundation Office of Inspector General June 30, 2009 OIG 09-1-008 Audit Performed by: WithumSmith+Brown 8403 Colesville

Audit of Effort Reporting System Cornell University Ithaca, New York National Science Foundation Office of Inspector General June 30, 2009 OIG 09-1-008 Audit Performed by: WithumSmith+Brown 8403 Colesville

NATIONAL SCIENCE FOUNDATION 4201 Wilson Boulevard ARLINGTON, VIRGINIA 22230

NATIONAL SCIENCE FOUNDATION 4201 Wilson Boulevard ARLINGTON, VIRGINIA 22230 OFFICE OF INSPECTOR GENERAL Date: January 31, 2012 To: Mary F. Santonastasso, Director Division of Institution and Award Support

NATIONAL SCIENCE FOUNDATION 4201 Wilson Boulevard ARLINGTON, VIRGINIA 22230 OFFICE OF INSPECTOR GENERAL Date: January 31, 2012 To: Mary F. Santonastasso, Director Division of Institution and Award Support

The Environmental Careers Organization Reported Outlays for Five EPA Cooperative Agreements

OFFICE OF INSPECTOR GENERAL Attestation Report Catalyst for Improving the Environment The Environmental Careers Organization Reported Outlays for Five EPA Cooperative Agreements Report No. 2007-4-00065

OFFICE OF INSPECTOR GENERAL Attestation Report Catalyst for Improving the Environment The Environmental Careers Organization Reported Outlays for Five EPA Cooperative Agreements Report No. 2007-4-00065

Howard University Needs To Improve Internal Controls Over Management of NSF Grant Funds

Howard University Needs To Improve Internal Controls Over Management of NSF Grant Funds National Science Foundation Office of Inspector General March 31, 2006 OIG 06-1-008 XXXXXXXXXXXX XXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Howard University Needs To Improve Internal Controls Over Management of NSF Grant Funds National Science Foundation Office of Inspector General March 31, 2006 OIG 06-1-008 XXXXXXXXXXXX XXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

NATIONAL SCIENCE FOUNDATION 4201 Wilson Boulevard ARLINGTON, VIRGINIA 22230

NATIONAL SCIENCE FOUNDATION 4201 Wilson Boulevard ARLINGTON, VIRGINIA 22230 OFFICE OF INSPECTOR GENERAL MEMORANDUM Date: March 31, 2011 To: Mary F. Santonastasso, Director Division of Institution and Award

NATIONAL SCIENCE FOUNDATION 4201 Wilson Boulevard ARLINGTON, VIRGINIA 22230 OFFICE OF INSPECTOR GENERAL MEMORANDUM Date: March 31, 2011 To: Mary F. Santonastasso, Director Division of Institution and Award

THE UNIVERSITY OF CALIFORNIA AT IRVINE S PILOT PAYROLL CERTIFICATION SYSTEM COULD NOT BE ASSESSED

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL THE UNIVERSITY OF CALIFORNIA AT IRVINE S PILOT PAYROLL CERTIFICATION SYSTEM COULD NOT BE ASSESSED Inquiries about this report may be

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL THE UNIVERSITY OF CALIFORNIA AT IRVINE S PILOT PAYROLL CERTIFICATION SYSTEM COULD NOT BE ASSESSED Inquiries about this report may be

Effort Certification. It s not rocket science..

Effort Certification It s not rocket science.. Your Presenters: Maggie Griscavage, University of Alaska Fairbanks Allison Weber, Los Angeles Biomedical Research Institute Michelle Dondanville, University

Effort Certification It s not rocket science.. Your Presenters: Maggie Griscavage, University of Alaska Fairbanks Allison Weber, Los Angeles Biomedical Research Institute Michelle Dondanville, University

U.S. Department of Justice Office of the Inspector General Audit Division

AUDIT OF THE OFFICE OF COMMUNITY ORIENTED POLICING SERVICES TECHNOLOGY PROGRAM AND SECURE OUR SCHOOLS GRANTS AWARDED TO THE WESTLAND POLICE DEPARTMENT WESTLAND, MICHIGAN U.S. Department of Justice Office

AUDIT OF THE OFFICE OF COMMUNITY ORIENTED POLICING SERVICES TECHNOLOGY PROGRAM AND SECURE OUR SCHOOLS GRANTS AWARDED TO THE WESTLAND POLICE DEPARTMENT WESTLAND, MICHIGAN U.S. Department of Justice Office

AUDIT OF NASA GRANTS AWARDED TO THE PHILADELPHIA COLLEGE OPPORTUNITY RESOURCES FOR EDUCATION

JULY 26, 2012 AUDIT REPORT OFFICE OF AUDITS AUDIT OF NASA GRANTS AWARDED TO THE PHILADELPHIA COLLEGE OPPORTUNITY RESOURCES FOR EDUCATION OFFICE OF INSPECTOR GENERAL National Aeronautics and Space Administration

JULY 26, 2012 AUDIT REPORT OFFICE OF AUDITS AUDIT OF NASA GRANTS AWARDED TO THE PHILADELPHIA COLLEGE OPPORTUNITY RESOURCES FOR EDUCATION OFFICE OF INSPECTOR GENERAL National Aeronautics and Space Administration

Timekeeping Case Study #1 [OIG Audit Report No. 11 15]

![Timekeeping Case Study #1 [OIG Audit Report No. 11 15]](/thumbs/27/10491628.jpg "Timekeeping Case Study #1 [OIG Audit Report No. 11 15]") Timekeeping Case Study #1 [OIG Audit Report No. 11 15] Finding: 1. This local government grantee claimed $8,940 of site supervisor salaries in January 2009 for work performed in December 2008. It provided

Timekeeping Case Study #1 [OIG Audit Report No. 11 15] Finding: 1. This local government grantee claimed $8,940 of site supervisor salaries in January 2009 for work performed in December 2008. It provided

May 22, 2012. Report Number: A-09-11-02047

May 22, 2012 OFFICE OF AUDIT SERVICES, REGION IX 90-7 TH STREET, SUITE 3-650 SAN FRANCISCO, CA 94103 Report Number: A-09-11-02047 Ms. Patricia McManaman Director Department of Human Services State of Hawaii

May 22, 2012 OFFICE OF AUDIT SERVICES, REGION IX 90-7 TH STREET, SUITE 3-650 SAN FRANCISCO, CA 94103 Report Number: A-09-11-02047 Ms. Patricia McManaman Director Department of Human Services State of Hawaii

August 2012 Report No. 12-048

John Keel, CPA State Auditor An Audit Report on The Texas Windstorm Insurance Association Report No. 12-048 An Audit Report on The Texas Windstorm Insurance Association Overall Conclusion The Texas Windstorm

John Keel, CPA State Auditor An Audit Report on The Texas Windstorm Insurance Association Report No. 12-048 An Audit Report on The Texas Windstorm Insurance Association Overall Conclusion The Texas Windstorm

Document Downloaded: Monday July 27, 2015. A-21 Task Force Document on Effort Reporting Requirement. Author: David Kennedy. Published Date: 11/14/2011

Document Downloaded: Monday July 27, 2015 A-21 Task Force Document on Effort Reporting Requirement Author: David Kennedy Published Date: 11/14/2011 COUNCIL ON GOVERNMENTAL RELATIONS 1200 New York Avenue,

Document Downloaded: Monday July 27, 2015 A-21 Task Force Document on Effort Reporting Requirement Author: David Kennedy Published Date: 11/14/2011 COUNCIL ON GOVERNMENTAL RELATIONS 1200 New York Avenue,

Effort Reporting Briefing for Investigators. University of California Systemwide Training

Effort Reporting Briefing for Investigators University of California Systemwide Training Agenda Effort Reporting Basics Key Effort Reporting Concepts Who must complete an effort report? Who should sign

Effort Reporting Briefing for Investigators University of California Systemwide Training Agenda Effort Reporting Basics Key Effort Reporting Concepts Who must complete an effort report? Who should sign

UND School of Medicine & Health Sciences Principal Investigator Reference Guide

UND School of Medicine & Health Sciences Principal Investigator Reference Guide TABLE OF CONTENTS Table of Contents 2 Introduction 3 Responsibilities of the Principal Investigator 4 Signing Legal Grant

UND School of Medicine & Health Sciences Principal Investigator Reference Guide TABLE OF CONTENTS Table of Contents 2 Introduction 3 Responsibilities of the Principal Investigator 4 Signing Legal Grant

Policy Statement The University is committed to ensuring that effort reports completed in connection with sponsored projects are accurate.

Effort Reporting: Certifying Effort on Sponsored Projects Scope This document sets forth the University s policy on certification of effort expended on sponsored project awards administered by Alabama

Effort Reporting: Certifying Effort on Sponsored Projects Scope This document sets forth the University s policy on certification of effort expended on sponsored project awards administered by Alabama

Staff Timesheets: Requirements and Issues

Staff Timesheets: Requirements and Issues 1 You need to know... The information in this session is based on CNCS and Federal laws, rules, and regulations; CNCS grant terms and provisions; and generally

Staff Timesheets: Requirements and Issues 1 You need to know... The information in this session is based on CNCS and Federal laws, rules, and regulations; CNCS grant terms and provisions; and generally

National Science Foundation Office of Inspector General 4201 Wilson Boulevard, Suite I-1135, Arlington, Virginia 22230

National Science Foundation Office of Inspector General 4201 Wilson Boulevard, Suite I-1135, Arlington, Virginia 22230 MEMORANDUM DATE: March 31, 2015 TO: FROM: SUBJECT: Jeffery M. Lupis, Director Division

National Science Foundation Office of Inspector General 4201 Wilson Boulevard, Suite I-1135, Arlington, Virginia 22230 MEMORANDUM DATE: March 31, 2015 TO: FROM: SUBJECT: Jeffery M. Lupis, Director Division

Audit Report. Food and Nutrition Service Food Stamp Program Administrative Costs New Jersey. U.S. Department of Agriculture

U.S. Department of Agriculture Office of Inspector General Northeast Region Audit Report Food and Nutrition Service Food Stamp Program Administrative Costs New Jersey Report No. 27002-25-Hy September 2008

U.S. Department of Agriculture Office of Inspector General Northeast Region Audit Report Food and Nutrition Service Food Stamp Program Administrative Costs New Jersey Report No. 27002-25-Hy September 2008

The University of Texas at Tyler Office of Sponsored Research (OSR) Time and Effort Reporting Policy

Time and Effort Reporting Policy") The University of Texas at Tyler Office of Sponsored Research (OSR) Time and Effort Reporting Policy Applicability This Time and Effort Reporting Policy applies to all individuals receiving funding in

The University of Texas at Tyler Office of Sponsored Research (OSR) Time and Effort Reporting Policy Applicability This Time and Effort Reporting Policy applies to all individuals receiving funding in

OFFICE OF INSPECTOR GENERAL. Audit Report

OFFICE OF INSPECTOR GENERAL Audit Report Select Financial Management Integrated System Business Process Controls Need Improvement Report No. 16-02 November 30, 2015 RAILROAD RETIREMENT BOARD EXECUTIVE

OFFICE OF INSPECTOR GENERAL Audit Report Select Financial Management Integrated System Business Process Controls Need Improvement Report No. 16-02 November 30, 2015 RAILROAD RETIREMENT BOARD EXECUTIVE

August 2014 Report No. 14-043

John Keel, CPA State Auditor A Report on On-site Audits of Residential Child Care Providers Report No. 14-043 A Report on On-site Audits of Residential Child Care Providers Overall Conclusion Three of

John Keel, CPA State Auditor A Report on On-site Audits of Residential Child Care Providers Report No. 14-043 A Report on On-site Audits of Residential Child Care Providers Overall Conclusion Three of

Eastern Illinois University. Policy on Effort Reporting

Eastern Illinois University Policy on Effort Reporting This document is a draft that was issued August 1, 2005. 1. Definition of Effort Effort is the proportion of time spent on professional activities

Eastern Illinois University Policy on Effort Reporting This document is a draft that was issued August 1, 2005. 1. Definition of Effort Effort is the proportion of time spent on professional activities

AUDIT REPORT 12-1 8. Audit of Controls over GPO s Fleet Credit Card Program. September 28, 2012

AUDIT REPORT 12-1 8 Audit of Controls over GPO s Fleet Credit Card Program September 28, 2012 Date September 28, 2012 To Director, Acquisition Services From Inspector General Subject Audit Report Audit

AUDIT REPORT 12-1 8 Audit of Controls over GPO s Fleet Credit Card Program September 28, 2012 Date September 28, 2012 To Director, Acquisition Services From Inspector General Subject Audit Report Audit

Effort Reporting Certifying Effort on Sponsored Projects

University of California, Berkeley Policy Issued: October 1, 2012 Effective Date: January 1, 2014 Supersedes: Effort Reporting Certifying Effort on Sponsored Projects, Issued September 1, 2009 Next Review

University of California, Berkeley Policy Issued: October 1, 2012 Effective Date: January 1, 2014 Supersedes: Effort Reporting Certifying Effort on Sponsored Projects, Issued September 1, 2009 Next Review

Proper Management of Federal Grants. Support for Salaries and Wages or Time & Effort Reporting

Proper Management of Federal Grants Support for Salaries and Wages or Time & Effort Reporting 1 USDA Forest Service Presenters Lynne Sholty Von Erkert Jaelith Hall-Rivera Guest from Office of Inspector

Proper Management of Federal Grants Support for Salaries and Wages or Time & Effort Reporting 1 USDA Forest Service Presenters Lynne Sholty Von Erkert Jaelith Hall-Rivera Guest from Office of Inspector

Office of Inspector General Evaluation of the Consumer Financial Protection Bureau s Consumer Response Unit

Office of Inspector General Evaluation of the Consumer Financial Protection Bureau s Consumer Response Unit Consumer Financial Protection Bureau September 2012 September 28, 2012 MEMORANDUM TO: FROM: SUBJECT:

Office of Inspector General Evaluation of the Consumer Financial Protection Bureau s Consumer Response Unit Consumer Financial Protection Bureau September 2012 September 28, 2012 MEMORANDUM TO: FROM: SUBJECT:

About the National Science Foundation:

About the National Science Foundation: The National Science Foundation (NSF) is charged with supporting and strengthening all research disciplines, and providing leadership across the broad and expanding

About the National Science Foundation: The National Science Foundation (NSF) is charged with supporting and strengthening all research disciplines, and providing leadership across the broad and expanding

FASHION INSTITUTE OF TECHNOLOGY SELECTED FINANCIAL MANAGEMENT PRACTICES. Report 2006-S-71 OFFICE OF THE NEW YORK STATE COMPTROLLER

Thomas P. DiNapoli COMPTROLLER OFFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE GOVERNMENT ACCOUNTABILITY Audit Objective... 2 Audit Results - Summary... 2 Background... 3 FASHION INSTITUTE OF

Thomas P. DiNapoli COMPTROLLER OFFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE GOVERNMENT ACCOUNTABILITY Audit Objective... 2 Audit Results - Summary... 2 Background... 3 FASHION INSTITUTE OF

Georgia State University Research Foundation, Inc. 30 Courtland Street Atlanta, Georgia 30303 National Science Foundation Award Number IBN-0349042

Georgia State University Research Foundation, Inc. 30 Courtland Street Atlanta, Georgia 30303 National Science Foundation Award Number IBN-0349042 Audit of Financial Schedules and Independent Auditors

Georgia State University Research Foundation, Inc. 30 Courtland Street Atlanta, Georgia 30303 National Science Foundation Award Number IBN-0349042 Audit of Financial Schedules and Independent Auditors

NATIONAL OCEANIC AND ATMOSPHERIC ADMINISTRATION. Opportunities to Strengthen Internal Controls Over Improper Payments PUBLIC RELEASE

U.S. DEPARTMENT OF COMMERCE Office of Inspector General NATIONAL OCEANIC AND ATMOSPHERIC ADMINISTRATION Opportunities to Strengthen Internal Controls Over Improper Payments Final Report No.BSD-16186-0001/July

U.S. DEPARTMENT OF COMMERCE Office of Inspector General NATIONAL OCEANIC AND ATMOSPHERIC ADMINISTRATION Opportunities to Strengthen Internal Controls Over Improper Payments Final Report No.BSD-16186-0001/July

Environmental Protection Agency Clean Water and Drinking Water State Revolving Funds ARRA Program Audit

Environmental Protection Agency Clean Water and Drinking Water State Revolving Funds ARRA Program Audit Audit Period: December 1, 2009 to February 12, 2010 Report number Issuance date: March 9, 2010 Contents

Environmental Protection Agency Clean Water and Drinking Water State Revolving Funds ARRA Program Audit Audit Period: December 1, 2009 to February 12, 2010 Report number Issuance date: March 9, 2010 Contents

How To Audit The Unemployment And Workers Compensation Charges By Thedetroit Public Schools

Audit of Unemployment and Workers Compensation Charges by the Detroit Public Schools Detroit, Michigan FINAL AUDIT REPORT Audit Control Number A05-90005 February 1999 Our mission is to promote the efficient

Audit of Unemployment and Workers Compensation Charges by the Detroit Public Schools Detroit, Michigan FINAL AUDIT REPORT Audit Control Number A05-90005 February 1999 Our mission is to promote the efficient

Office of the Inspector General U.S. Department of Justice

Office of the Inspector General U.S. Department of Justice Audit of the Office of Justice Programs Victim Assistance Formula Grants Awarded to the California Governor s Office of Emergency Services Mather,

Office of the Inspector General U.S. Department of Justice Audit of the Office of Justice Programs Victim Assistance Formula Grants Awarded to the California Governor s Office of Emergency Services Mather,

OFFICE OF INSPECTOR GENERAL

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL Physical And Occupational Therapy in Nursing Homes Cost of Improper Billings to Medicare JUNE GIBBS BROWN Inspector General AUGUST 1999

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL Physical And Occupational Therapy in Nursing Homes Cost of Improper Billings to Medicare JUNE GIBBS BROWN Inspector General AUGUST 1999

FEDERAL TRADE COMMISSION. Office of Inspector General

AR 14-00lA FEDERAL TRADE COMMISSION Office of Inspector General Audited Financial Statements for Fiscal Year 2013 Management Letter May 2 8, 2014 UNITED STATES OF AMERICA FEDERAL TRADE COMMISSION WASHINGTON,

AR 14-00lA FEDERAL TRADE COMMISSION Office of Inspector General Audited Financial Statements for Fiscal Year 2013 Management Letter May 2 8, 2014 UNITED STATES OF AMERICA FEDERAL TRADE COMMISSION WASHINGTON,

Financial Audit of Financial Schedules and I ndependent Auditors' Reports. For the Period September 1, 1995 to September 30, 2001

Bellevue Community College 3000 Landerholm Circle SE, N258 Bellevue, Washington 98007 National Science Foundation Award Numbers DUE-9553727 DUE-9813446 Financial Audit of Financial Schedules and I ndependent

Bellevue Community College 3000 Landerholm Circle SE, N258 Bellevue, Washington 98007 National Science Foundation Award Numbers DUE-9553727 DUE-9813446 Financial Audit of Financial Schedules and I ndependent

EPA Could Improve Its Information Security by Strengthening Verification and Validation Processes

OFFICE OF INSPECTOR GENERAL Audit Report Catalyst for Improving the Environment EPA Could Improve Its Information Security by Strengthening Verification and Validation Processes Report No. 2006-P-00002

OFFICE OF INSPECTOR GENERAL Audit Report Catalyst for Improving the Environment EPA Could Improve Its Information Security by Strengthening Verification and Validation Processes Report No. 2006-P-00002

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections. Examination Report

Fresno U.S. Department of Energy Office of Inspector General Office of Audits and Inspections Examination Report Community Action Partnership of San Bernardino County Weatherization Assistance Program

Fresno U.S. Department of Energy Office of Inspector General Office of Audits and Inspections Examination Report Community Action Partnership of San Bernardino County Weatherization Assistance Program

CITY UNIVERSITY OF NEW YORK EMPLOYEE ACCESS TO THE STUDENT INFORMATION MANAGEMENT SYSTEM AT SELECTED CAMPUSES. Report 2007-S-23

Thomas P. DiNapoli COMPTROLLER OFFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE GOVERNMENT ACCOUNTABILITY Audit Objective... 2 Audit Results - Summary... 2 Background... 3 Audit Findings and

Thomas P. DiNapoli COMPTROLLER OFFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE GOVERNMENT ACCOUNTABILITY Audit Objective... 2 Audit Results - Summary... 2 Background... 3 Audit Findings and

National Science Foundation 4201 Wilson Boulevard Arlington, Virginia 22230

National Science Foundation 4201 Wilson Boulevard Arlington, Virginia 22230 Office of Inspector General MEMORANDUM. DATE: September 30, 2011 TO: FROM: SUBJECT: Jeffrey M. Lupis, Director Division of Acquisition

National Science Foundation 4201 Wilson Boulevard Arlington, Virginia 22230 Office of Inspector General MEMORANDUM. DATE: September 30, 2011 TO: FROM: SUBJECT: Jeffrey M. Lupis, Director Division of Acquisition

Section J.10.2 of 2 CFR, Part 220, Compensation for Personal Services requires that the University maintain a payroll distribution 1 system that will:

Number: RASPL05 Title: Effort Reporting Policy Supersedes No: GRPL05 Effective Date: 07/01/2011 Last Reviewed: 01/30/13 Issuing Department: Research Accounting Services Submitted By: Patricia J. Russo,

Number: RASPL05 Title: Effort Reporting Policy Supersedes No: GRPL05 Effective Date: 07/01/2011 Last Reviewed: 01/30/13 Issuing Department: Research Accounting Services Submitted By: Patricia J. Russo,

AUDIT OF THE MACOMB COUNTY SHERIFF S OFFICE EQUITABLE SHARING PROGRAM ACTIVITIES MOUNT CLEMENS, MICHIGAN EXECUTIVE SUMMARY*

AUDIT OF THE MACOMB COUNTY SHERIFF S OFFICE EQUITABLE SHARING PROGRAM ACTIVITIES MOUNT CLEMENS, MICHIGAN EXECUTIVE SUMMARY* The Department of Justice (DOJ) Office of the Inspector General (OIG) conducted

AUDIT OF THE MACOMB COUNTY SHERIFF S OFFICE EQUITABLE SHARING PROGRAM ACTIVITIES MOUNT CLEMENS, MICHIGAN EXECUTIVE SUMMARY* The Department of Justice (DOJ) Office of the Inspector General (OIG) conducted

Audit of Grants Management at Dakota State University

Audit of Grants Management at Dakota State University National Science Foundation Office of the Inspector General February 28, 2005 OIG 05-6004 Memorandum Report Audit of Grants Management at Dakota State

Audit of Grants Management at Dakota State University National Science Foundation Office of the Inspector General February 28, 2005 OIG 05-6004 Memorandum Report Audit of Grants Management at Dakota State

Get a Head Start on Analytics and Audits for Proactive Preparation and Responses to Federal Audits

Get a Head Start on Analytics and Audits for Proactive Preparation and Responses to Federal Audits June 17, 2015 Anne Sullivan, Senior Director Marisa Zuskar, Director YOUR MISSION OUR SOLUTIONS Huron

Get a Head Start on Analytics and Audits for Proactive Preparation and Responses to Federal Audits June 17, 2015 Anne Sullivan, Senior Director Marisa Zuskar, Director YOUR MISSION OUR SOLUTIONS Huron

Procedures and Guidelines for External Grants and Sponsored Programs

Definitions: Procedures and Guidelines for External Grants and Sponsored Programs 1. Grant and Contract Financial Administration Office (Grants Office): The office within the Accounting Operations Area

Definitions: Procedures and Guidelines for External Grants and Sponsored Programs 1. Grant and Contract Financial Administration Office (Grants Office): The office within the Accounting Operations Area

AUDIT REPORT THE ADMINISTRATION OF CONTRACTS AND AGREEMENTS FOR LINGUISTIC SERVICES BY THE DRUG ENFORCEMENT ADMINISTRATION AUGUST 2002 02-33

AUDIT REPORT THE ADMINISTRATION OF CONTRACTS AND AGREEMENTS FOR LINGUISTIC SERVICES BY THE DRUG ENFORCEMENT ADMINISTRATION AUGUST 2002 02-33 THE ADMINISTRATION OF CONTRACTS AND AGREEMENTS FOR LINGUISTIC

AUDIT REPORT THE ADMINISTRATION OF CONTRACTS AND AGREEMENTS FOR LINGUISTIC SERVICES BY THE DRUG ENFORCEMENT ADMINISTRATION AUGUST 2002 02-33 THE ADMINISTRATION OF CONTRACTS AND AGREEMENTS FOR LINGUISTIC

OFFICE OF THE INDEPENDENT AUDITOR GENERAL/444 S.W. 2 ND AVENUE, SUITE 711/MIAMI, FLORIDA 33130-1910

C: The Honorable Mayor Tomas Regalado Tony Crapp, Jr., Chief Administrator/City Manager Members of the Audit Advisory Committee Larry M. Spring, Assistant City Manager/Chief Financial Officer Peter W.

C: The Honorable Mayor Tomas Regalado Tony Crapp, Jr., Chief Administrator/City Manager Members of the Audit Advisory Committee Larry M. Spring, Assistant City Manager/Chief Financial Officer Peter W.

U.S. Department of Agriculture Office of Inspector General Financial and IT Operations Audit Report

U.S. Department of Agriculture Office of Inspector General Financial and IT Operations Audit Report FISCAL YEAR 2000 NATIONAL FINANCE CENTER REVIEW OF INTERNAL CONTROLS NAT Report No. 11401-7-FM June 2001

U.S. Department of Agriculture Office of Inspector General Financial and IT Operations Audit Report FISCAL YEAR 2000 NATIONAL FINANCE CENTER REVIEW OF INTERNAL CONTROLS NAT Report No. 11401-7-FM June 2001

SIGAR. USAID s Higher Education Project: Audit of Costs Incurred by the University of Massachusetts APRIL

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 15-52 Financial Audit USAID s Higher Education Project: Audit of Costs Incurred by the University of Massachusetts APRIL 2015 SIGAR

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 15-52 Financial Audit USAID s Higher Education Project: Audit of Costs Incurred by the University of Massachusetts APRIL 2015 SIGAR

Documentation of salaries and wages is often necessary to support

Documentation of salaries and wages is often necessary to support charges to specific funding sources (resources), instructional settings (goals), and activities (functions). Some level of formalized time

Documentation of salaries and wages is often necessary to support charges to specific funding sources (resources), instructional settings (goals), and activities (functions). Some level of formalized time

ENROLLMENT MANAGEMENT DIVISION REVIEW OF TIME REPORTING

ENROLLMENT MANAGEMENT DIVISION REVIEW OF TIME REPORTING THE UNIVERSITY OF NEW MEXICO January 15, 2010 J.E. Gene Gallegos, Chair Carolyn J. Abeita, Vice Chair Jamie Koch Audit Committee Members G. Christine

ENROLLMENT MANAGEMENT DIVISION REVIEW OF TIME REPORTING THE UNIVERSITY OF NEW MEXICO January 15, 2010 J.E. Gene Gallegos, Chair Carolyn J. Abeita, Vice Chair Jamie Koch Audit Committee Members G. Christine

CHAPTER 4 EFFECTIVE INTERNAL CONTROLS OVER PAYROLL

CHAPTER 4 EFFECTIVE INTERNAL CONTROLS OVER PAYROLL INTRODUCTION AND LEARNING OBJECTIVES Every organization, including governments, require employees to assist in meeting their goals and objectives. The

CHAPTER 4 EFFECTIVE INTERNAL CONTROLS OVER PAYROLL INTRODUCTION AND LEARNING OBJECTIVES Every organization, including governments, require employees to assist in meeting their goals and objectives. The

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL. March 01, 2016

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL AUDIT SERVICES Philadelphia Audit Region Kevin Miller Executive Director Opportunities for Ohioans with Disabilities 150 E. Campus View

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL AUDIT SERVICES Philadelphia Audit Region Kevin Miller Executive Director Opportunities for Ohioans with Disabilities 150 E. Campus View

Framework for Audit Oversight INTERNATIONAL WORKSHOP ON ACCOUNTABILITY IN SCIENCE AND RESEARCH FUNDING JUNE 2 4, 2011

Framework for Audit Oversight 1 INTERNATIONAL WORKSHOP ON ACCOUNTABILITY IN SCIENCE AND RESEARCH FUNDING JUNE 2 4, 2011 Overview 2 Forensic Audit and Oversight Forensic Techniques Identify Anomalies Framework

Framework for Audit Oversight 1 INTERNATIONAL WORKSHOP ON ACCOUNTABILITY IN SCIENCE AND RESEARCH FUNDING JUNE 2 4, 2011 Overview 2 Forensic Audit and Oversight Forensic Techniques Identify Anomalies Framework

SCOPE OF WORK FOR PERFORMING INTERNAL CONTROL AND STATUTORY/REGULATORY COMPLIANCE AUDITS FOR RECIPIENTS OF SPECIAL MUNICIPAL AID

SCOPE OF WORK FOR PERFORMING INTERNAL CONTROL AND STATUTORY/REGULATORY COMPLIANCE AUDITS FOR RECIPIENTS OF SPECIAL MUNICIPAL AID State of New Jersey Department of Community Affairs Division of Local Government

SCOPE OF WORK FOR PERFORMING INTERNAL CONTROL AND STATUTORY/REGULATORY COMPLIANCE AUDITS FOR RECIPIENTS OF SPECIAL MUNICIPAL AID State of New Jersey Department of Community Affairs Division of Local Government

OFFICE OF INSPECTOR GENERAL. Audit Report

OFFICE OF INSPECTOR GENERAL Audit Report Audit of the Business Process Controls in the Financial Management Integrated System Report No. 14-10 August 01, 2014 RAILROAD RETIREMENT BOARD EXECUTIVE SUMMARY

OFFICE OF INSPECTOR GENERAL Audit Report Audit of the Business Process Controls in the Financial Management Integrated System Report No. 14-10 August 01, 2014 RAILROAD RETIREMENT BOARD EXECUTIVE SUMMARY

The CFPB Should Continue to Enhance Controls for Its Government Travel Card Program

O FFICE OF INSPECTOR GENERAL Audit Report 2016-FMIC-C-009 The CFPB Should Continue to Enhance Controls for Its Government Travel Card Program June 27, 2016 B OARD OF G OVERNORS OF THE F EDERAL R ESERVE

O FFICE OF INSPECTOR GENERAL Audit Report 2016-FMIC-C-009 The CFPB Should Continue to Enhance Controls for Its Government Travel Card Program June 27, 2016 B OARD OF G OVERNORS OF THE F EDERAL R ESERVE

Appendix 1 CJC CONTRACT MANAGEMENT POLICIES AND PROCEDURES. Criminal Justice Commission Contract Management Policies and Procedures

CJC CONTRACT MANAGEMENT POLICIES AND PROCEDURES SNYOPSIS: The CJC was created by a Palm Beach County ordinance in 1988. It has 21 public sector members representing local, state, and federal criminal justice

CJC CONTRACT MANAGEMENT POLICIES AND PROCEDURES SNYOPSIS: The CJC was created by a Palm Beach County ordinance in 1988. It has 21 public sector members representing local, state, and federal criminal justice

Department of Public Utilities Customer Information System (BANNER)

") REPORT # 2010-06 AUDIT of the Customer Information System (BANNER) January 2010 TABLE OF CONTENTS Executive Summary..... i Comprehensive List of Recommendations. iii Introduction, Objective, Methodology

REPORT # 2010-06 AUDIT of the Customer Information System (BANNER) January 2010 TABLE OF CONTENTS Executive Summary..... i Comprehensive List of Recommendations. iii Introduction, Objective, Methodology

Solution for Enterprise Asset. Management. System Vehicle Maintenance Facility Data. Management. Advisory Report. Report Number DR-MA-15-004

Solution for Enterprise Asset Management System Vehicle Maintenance Facility Data Management Advisory Report Report Number DR-MA-15-004 September 18, 2015 Highlights This management advisory discusses

Solution for Enterprise Asset Management System Vehicle Maintenance Facility Data Management Advisory Report Report Number DR-MA-15-004 September 18, 2015 Highlights This management advisory discusses

August 2008 Report No. 08-046

John Keel, CPA State Auditor A Report on On-site Audits of Residential Child Care Providers Report No. 08-046 A Report on On-site Audits of Residential Child Care Providers Overall Conclusion Three of

John Keel, CPA State Auditor A Report on On-site Audits of Residential Child Care Providers Report No. 08-046 A Report on On-site Audits of Residential Child Care Providers Overall Conclusion Three of

SAN DIEGO COMMUNITY COLLEGE DISTRICT

SAN DIEGO COMMUNITY COLLEGE DISTRICT Audit Report COLLECTIVE BARGAINING PROGRAM Chapter 961, Statutes of 1975, and Chapter 1213, Statutes of 1991 July 1, 2000, through June 30, 2002 STEVE WESTLY California

SAN DIEGO COMMUNITY COLLEGE DISTRICT Audit Report COLLECTIVE BARGAINING PROGRAM Chapter 961, Statutes of 1975, and Chapter 1213, Statutes of 1991 July 1, 2000, through June 30, 2002 STEVE WESTLY California

In Brief Why We Did This Audit What We Found What We Recommended

Smithsonian Institution Office of the Inspector General In Brief Administration of Continuation of Pay Program Report Number A-07-09-1, July 18, 2008 Why We Did This Audit This is the first of two reports

Smithsonian Institution Office of the Inspector General In Brief Administration of Continuation of Pay Program Report Number A-07-09-1, July 18, 2008 Why We Did This Audit This is the first of two reports

Question and Answer Transcript Follow-up to the December 7, 2011 webinar on: Proper Management of Federal Grants - Support of Salaries and Wages

Question and Answer Transcript Follow-up to the December 7, 2011 webinar on: Proper Management of Federal Grants - Support of Salaries and Wages Acronyms used in the Questions and Answers (alphabetical

Question and Answer Transcript Follow-up to the December 7, 2011 webinar on: Proper Management of Federal Grants - Support of Salaries and Wages Acronyms used in the Questions and Answers (alphabetical

SAN DIEGO STATE UNIVERSITY FOUNDATION OVERLOAD COMPENSATION OIG REPORT 04-1-002 03/02/2004-1 -

SAN DIEGO STATE UNIVERSITY FOUNDATION OVERLOAD COMPENSATION OIG REPORT 04-1-002 03/02/2004-1 - TABLE OF CONTENTS Introduction 3 Audit Results 5 Recommendations 10 Appendix A: Schedule of SDSUF Overload

SAN DIEGO STATE UNIVERSITY FOUNDATION OVERLOAD COMPENSATION OIG REPORT 04-1-002 03/02/2004-1 - TABLE OF CONTENTS Introduction 3 Audit Results 5 Recommendations 10 Appendix A: Schedule of SDSUF Overload