Opportunities Exist to Achieve Operational Efficiencies in the Board s Management of Information Technology Services

|

|

|

- Jade Webster

- 8 years ago

- Views:

Transcription

1 O F F I C E O F IN S P E C TO R G E N E R A L Audit Report 2014-IT-B-003 Opportunities Exist to Achieve Operational Efficiencies in the Board s Management of Information Technology Services February 26, 2014 B O A R D O F G O V E R N O R S O F T H E F E D E R A L R E S E R V E S Y S T E M C O N S U M E R F I N A N C I A L P R O T E C T I O N B U R E A U

2 Report Contributors Khalid Hasan, OIG Manager Andrew Gibson, Auditor-in-Charge Adam Raley, IT Auditor Joshua Dieckert, IT Auditor Peter Sheridan, Senior OIG Manager for Information Technology Audits Andrew Patchan Jr., Associate Inspector General for Information Technology Abbreviations Board EA Division of IT IT ITIL OIG SDLC SDM Board of Governors of the Federal Reserve System enterprise architecture Division of Information Technology information technology Information Technology Infrastructure Library Office of Inspector General systems development life cycle systems development methodology

3 Executive Summary: Opportunities Exist to Achieve Operational Efficiencies in the Board s Management of Information Technology Services 2014-IT-B-003 February 26, 2014 Purpose Our audit objective was to determine how information technology (IT) services are managed across the divisions of the Board of Governors of the Federal Reserve System (Board) and identify areas where operational efficiencies could be achieved. Background The Board relies on a variety of IT services to accomplish its mission. The Board has developed a strategic framework for that highlights as key priorities the achievement of operational efficiencies and the reduction of costs. In support of these strategic priorities, the Board recently completed a survey of the scope and costs of IT services performed by individual divisions. Findings We identified three challenges that could hinder the Board s ability to achieve operational efficiencies and cost savings in its management of IT services. First, we found that Board divisions do not track costs for IT services in a consistent manner. Second, we found that over half of Board divisions perform their own applications development and help-desk activities, often utilizing differing processes, procedures, and tools. Third, we found that the Board has not completed actions to define IT standards, services, and technologies currently in use across Board divisions; those needed to meet future goals and objectives; and a plan to transition to the future state. A key contributing cause of our findings is the Board s decentralized governance structure for managing IT services. Recommendations To assist the Board in achieving operational efficiencies in its management of IT services, we recommend that the Director of the Division of Information Technology (Division of IT) work with the Chief Operating Officer and the Division of Financial Management to identify and define specific cost centers for IT in consultation with Board divisions and implement a consistent process to account for and track costs for IT services across Board divisions. We also recommend that the Director of the Division of IT implement across Board divisions a common systems development life cycle policy and associated procedures. Finally, we suggest that the Director of the Division of IT work with Board divisions to identify IT standards, services, and technologies currently in use across Board divisions and those needed to meet future strategic goals and objectives, and then define a transition plan. The Director of the Division of IT concurred with our recommendations and outlined actions that have been taken or will be implemented to address our recommendations. Access the full report: For more information, contact the OIG at or visit

4 Summary of Recommendations, OIG Report No IT-B-003 Rec. no. Report page no. Recommendation Responsible office 1 5 Work with the Chief Operating Officer and the Division of Financial Management to identify and define specific cost centers for information technology in consultation with Board divisions and implement a consistent process to account for and track costs for information technology services across Board divisions. Division of Information Technology 2 7 Implement across Board divisions a common systems development life cycle policy and associated procedures. Division of Information Technology

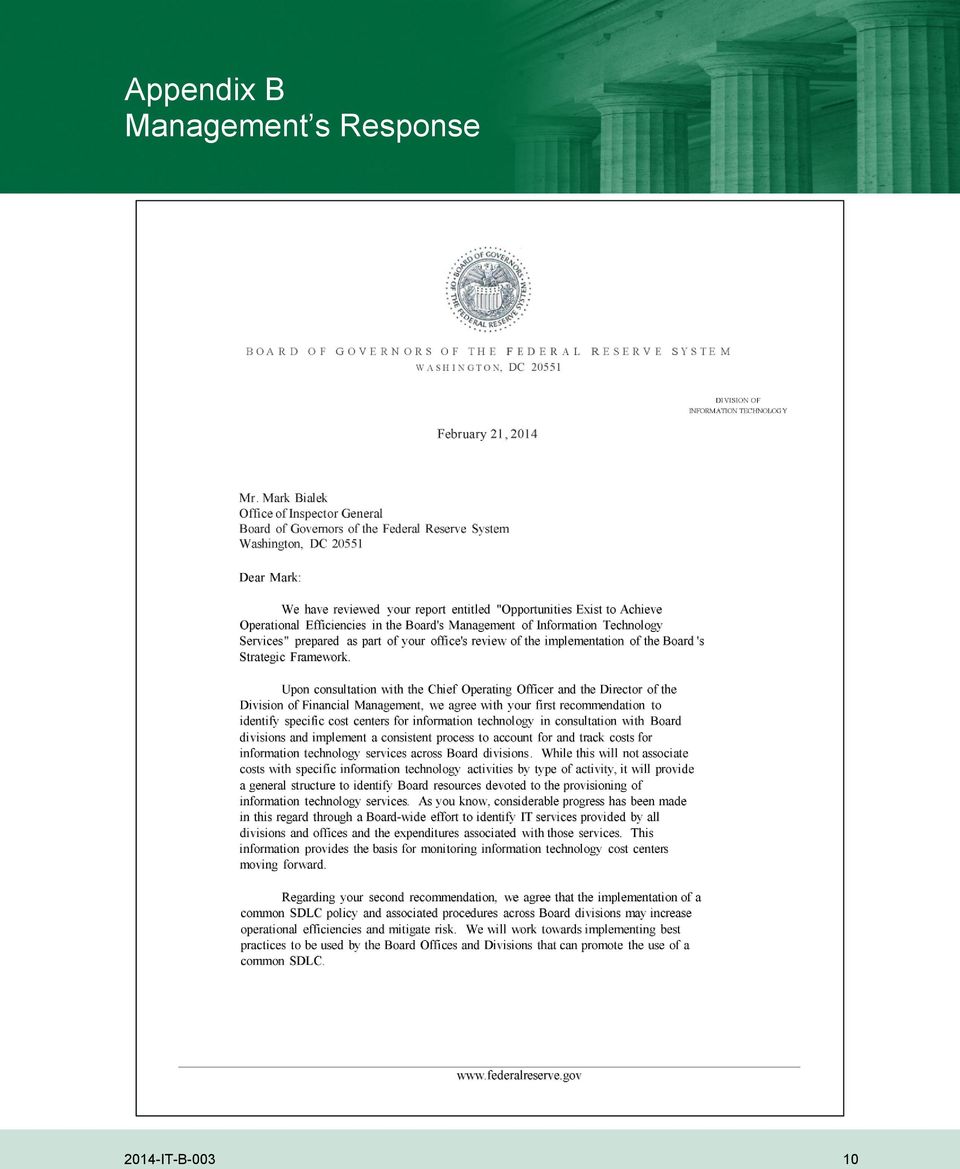

5 February 26, 2014 MEMORANDUM TO: FROM: SUBJECT: Sharon Mowry Director, Division of Information Technology Board of Governors of the Federal Reserve System Andrew Patchan Jr. Associate Inspector General for Information Technology OIG Report No IT-B-003: Opportunities Exist to Achieve Operational Efficiencies in the Board s Management of Information Technology Services Attached is the Office of Inspector General s report on the subject audit. Our audit objective was to determine how information technology services are managed across the divisions of the Board of Governors of the Federal Reserve System (Board) and identify areas where operational efficiencies could be achieved. We provided you with a draft of our report for review and comment. In your response, you concurred with our recommendations and outlined actions that have been taken or will be implemented to address our recommendations. We have included your response as appendix B to our report. We appreciate the cooperation that we received from Board staff during our review. Please contact me if you would like to discuss this report or any related issues. cc: Donald Hammond Michell Clark William Mitchell Geary Cunningham Wayne Edmondson

6

7 Contents DISCUSSION DRAFT Restricted Introduction... 1 Objectives... 1 Background... 1 Finding 1: The Board Does Not Track Costs for IT Services in a Consistent Manner... 3 Recommendation... 5 Management s Response... 5 OIG Comment... 5 Finding 2: The Board Has Not Implemented Consistent Processes for Applications Development and Help-Desk Services... 6 Recommendation... 7 Management s Response... 7 OIG Comment... 7 Other Matter for Management s Consideration... 8 Appendix A: Scope and Methodology... 9 Appendix B: Management s Response... 10

8 Introduction Objectives The Board of Governors of the Federal Reserve System (Board) has developed a strategic framework for that highlights as key priorities the achievement of operational efficiencies and the reduction of costs. In support of these strategic priorities, our audit objective was to determine how information technology (IT) services are managed across Board divisions and identify areas where operational efficiencies could be achieved. Appendix A provides our detailed scope and methodology. Background The Board relies on a variety of IT services to accomplish its mission. These services include applications management, help-desk operations, compliance management, and technical operations management. The Board s governance structure for managing IT services consists of centralized and decentralized organizational responsibilities. The Division of Information Technology (Division of IT) provides centralized IT services that are leveraged by Board divisions. These services include setup and maintenance of Microsoft Windows based computers, applications development, and help-desk operations. The Director of the Division of IT is responsible for ensuring that these centrally provided IT services are budgeted for and implemented in accordance with the Board s policies and procedures. Individual Board divisions also perform IT services in support of their business needs. In some instances, these services overlap with those provided centrally by the Division of IT. For example, several Board divisions engage in their own systems development and help-desk activities for applications supporting their business processes. In other instances, Board divisions perform IT services to support specific needs. For example, one division maintains a network of Apple Macintosh computers for desktop publishing and video editing. Another division maintains a separate Linux-based infrastructure to support research and statistical applications used by economists and researchers. These decentralized IT services are implemented and managed by the divisions in which they are performed. An increasing percentage of the Board s total costs for IT services are occurring outside the Division of IT and are thus being managed in a decentralized manner. Figure 1 below highlights the total costs for IT services at the Board from 2008 to During this time, IT services costs have grown at an average annual rate of 15 percent to a total of $146 million in Costs attributable to the Division of IT have grown by about 10 percent per year on average, while those incurred by other Board divisions have grown by approximately 23 percent per year on average. As a result, while the Division of IT accounted for 61 percent of the Board s total expenditures for IT services in 2008, this amount had decreased to 52 percent by IT-B-003 1

9 Figure 1: Board IT Services Costs, $160,000,000 $140,000,000 Division of IT Other Board Divisions $120,000,000 $100,000,000 $80,000,000 $60,000,000 $40,000,000 $20,000,000 $ Source: Total costs were obtained from the Board s financial management system by utilizing cost centers used by divisions to track IT services costs IT-B-003 2

10 Finding 1: The Board Does Not Track Costs for IT Services in a Consistent Manner We found that the Board does not have a consistent process to track costs for IT services across Board divisions. Some divisions account for costs using specific IT services accounting classifications, while others use general program categories. We attribute this inconsistency to the Board s decentralized budgeting processes and the absence of policies and procedures for accounting for IT services costs. As a result, the Board cannot readily and accurately measure the cost and performance of IT services across Board divisions, which impacts the Board s ability to comprehensively identify and prioritize areas for achievement of operational efficiencies and cost savings in IT services. As part of its budgeting process, the Board uses cost centers to group expenses related to the Board s programs. For example, to account for expenses related to its records management program, the Board has established Records as a cost center. However, costs centers for IT services are not used across divisions in a consistent manner, and the cost centers that the majority of divisions use do not reflect the specific IT service activity being performed. With respect to applications development, different cost centers used by divisions include Research and Information Systems, Information Technology, Application Design & Development, and Applications Analysis. Similarly, we found that costs for other IT services, such as help desk and technical operations, were being tracked by divisions using different cost centers. Table 1 shows the specific cost centers divisions use to track costs for IT services IT-B-003 3

11 Table 1: Cost Centers Used to Track IT Services Costs at the Board Board division Cost centers Banking Supervision & Regulation Information Technology Information Security and Continuity Technology Delivery & Support Board Members Web Communications & Development Information Solutions Consumer & Community Affairs Technology Development Information Management International Finance Research & Information Systems Management Technology Governance Information Systems Risk Management Law Enforcement Tech Services Admin Systems Automation Programming Technology Governance Reserve Bank Operations & Payment Systems Information Systems Research & Statistics Automation & Research Computing Application Design & Development Economic Data Management Information Technology Directorate-IT Management & Software Support Information Security IT Administration & Special Projects Consumer & PubWeb Systems General Systems Support Financial & Regulatory Systems Network Systems SECY & FOMC Systems Financial Systems Monetary Reports & Internal Accounting C-SCAPE Income Source: OIG compilation of information from Board divisions annual budget documentation, a The eight Board divisions listed in the table perform IT services internally or provide them to other divisions. The other four Board divisions rely completely on the Division of IT for IT services and are not listed separately in the table. b To track costs for IT services it performs, the OIG utilizes a General Program Direction cost center. This approach is consistent with that utilized by the other four divisions that rely completely on the Division of IT for IT services. We believe that a consistent approach to accounting for IT services expenses across Board divisions could provide key information on areas in which operational efficiencies and cost savings could be achieved. Best practices for IT services management, as outlined in the Information Technology Infrastructure Library (ITIL), 1 note the importance of developing a cost model for IT services. Specifically, ITIL states that a cost model for IT services can 1. ITIL is a globally recognized best-practices framework for managing IT services. Originally published by the UK government, ITIL has been used by public and private organizations worldwide IT-B-003 4

12 provide a framework to link costs to specific IT services as well as a standard format by which to analyze and report on IT services to facilitate decision making. Recommendation We recommend that the Director of the Division of IT 1. Work with the Chief Operating Officer and the Division of Financial Management to identify and define specific cost centers for IT in consultation with Board divisions and implement a consistent process to account for and track costs for IT services across Board divisions. Management s Response The Director of the Division of IT agreed with our recommendation and noted that a Boardwide effort to identify IT services provided by all divisions and the expenditures associated with those services will provide a basis for monitoring IT costs centers moving forward. OIG Comment In our opinion, the corrective actions described by the Director of the Division of IT are generally responsive to our recommendation. We plan to follow up on the planned corrective actions to ensure that our recommendation is fully addressed IT-B-003 5

13 Finding 2: The Board Has Not Implemented Consistent Processes for Applications Development and Help-Desk Services We found that over half of Board divisions perform applications development and help-desk services, often using differing processes, procedures, and tools. For example, several Board divisions perform SharePoint development, Intranet and Internet site maintenance, and programming using SQL server and SAS technologies. Several divisions also develop and maintain econometric applications to support research on monetary policy. We found that processes and tools used by Board divisions in support of applications development activities in these areas, such as for project risk assessment, change management, and ensuring section 508 compliance, vary across divisions. We attribute inconsistent application management processes to the absence of a common systems development life cycle (SDLC) policy and associated operating procedures for use across Board divisions. As a result, the Board is not realizing operational efficiencies in applications management that could result from the implementation of consistent processes and standardized tools. An SDLC refers to the overall process of developing, implementing, maintaining, and retiring information systems. According to the National Institute of Standards and Technology, each agency should have a documented and repeatable SDLC policy and guideline that supports its business need and that complements its unique culture. 2 The Division of IT has established a systems development methodology (SDM) that provides a framework for development projects managed by the division. The SDM specifically applies to Division of IT projects that result in releases, phases, or versions, and it includes activities for risk assessment, change management, and compliance. However, the other Board divisions are not required to follow the SDM, and two Board divisions told us that they relied largely on best practices and not the SDM when they developed large-scale systems. During our audit, the Board completed a review of help-desk and other IT services that identified similar concerns regarding differing processes and tools used across Board divisions. The Board has begun evaluating options to standardize help-desk services across Board divisions; thus, we are not providing specific recommendations related to achieving operational efficiencies for help-desk services. The Board also completed a survey of the scope of IT services performed by individual divisions that highlighted the variety of applications management activities being performed across Board divisions. This survey noted that approximately 40 percent of the Board s total IT services costs are for applications management activities. Given that applications management represents a significant portion of total IT services costs at the Board, we believe that consistent processes for applications development, operations, and maintenance could lead to operational efficiencies and cost savings. 2. National Institute of Standards and Technology Special Publication , Revision 2, Security Considerations in the Systems Development Life Cycle, October IT-B-003 6

14 Recommendation We recommend that the Director of the Division of IT 2. Implement across Board divisions a common SDLC policy and associated procedures. Management s Response The Director of the Division of IT agreed with our recommendation and noted that the division will work toward implementing best practices to be used by Board divisions that can promote the use of a common SDLC. OIG Comment In our opinion, the corrective actions described by the Director of the Division of IT are generally responsive to our recommendation. We plan to follow up on the planned corrective actions to ensure that our recommendation is fully addressed IT-B-003 7

15 Other Matter for Management s Consideration The Division of IT has developed a strategic plan that notes the importance of leveraging enterprise architecture (EA) principles to increase IT standardization and effectiveness across Board divisions. EA consists of a blueprint that describes how an organization operates in terms of business processes and technology, how it intends to operate in the future, and how it plans to transition to the future state. EA would also include the development and implementation of Board-wide IT standards that could be leveraged to achieve cost savings. We found, however, that the Division of IT s efforts to develop an EA have not included all the technologies and services used across Board divisions. Further, Board divisions are not required to follow the EA standards that the Division of IT creates, resulting in inconsistent IT services processes, procedures, and tools used across Board divisions. The U.S. Government Accountability Office has noted that many successful private and public organizations have utilized EA to implement operations and technology environments that maximize attainment of strategic objectives. 3 The Division of IT has developed standards and guidelines for the current and future state of software, hardware, router, and database technologies used within the division. Further, an Architecture Review Board was recently established to ensure that the Division of IT s projects align with these standards and guidelines. However, other Board divisions are not required to adhere to the standards, the guidelines, or the Architecture Review Board s processes. The absence of a Board-wide EA stems from decentralized IT and strategic management processes that until recently have not prioritized operational efficiencies and cost reduction as Boardwide goals. We recognize that the development and implementation of an EA across Board divisions would entail a concerted effort over a period of time and would require collaboration and coordination; however, such an effort could provide a foundation for achieving operational efficiencies and cost savings. As such, we suggest that the Director of the Division of IT work with Board divisions to identify IT standards, services, and technologies currently in use across Board divisions and those needed to meet future strategic goals and objectives, and then define a transition plan. 3. U.S. Government Accountability Office, Enterprise Architecture: Leadership Remains Key to Establishing and Leveraging Architectures for Organizational Transformation, GAO , August IT-B-003 8

16 Appendix A Scope and Methodology To accomplish our audit objective, we interviewed IT management in Board divisions, developed an inventory of IT services being performed across Board divisions, and analyzed Board divisions budgets and processes for accounting for IT services costs. To obtain total IT services costs, we queried the Board s financial system by specific cost centers used by Board divisions. We obtained these cost centers by analyzing information contained in the 2008 to 2012 budget documentation prepared by each division and validated this information with division specific staff. We also analyzed the results of internal reviews completed by the Board on IT services, including for help-desk operations and software/hardware provisioning. To identify operational efficiencies, we assessed the Board s management practices for IT services against best practices stipulated in ITIL. ITIL divides IT services into four general categories: Applications management: Involves the design, development, testing, and improvement of applications Service (help) desk: Serves as a central point of contact for handling IT support Compliance management: Ensures compliance with applicable laws and regulations Technical operations management: Involves control and maintenance of the IT infrastructure required to deliver services (e.g., change control and configuration management) We based our inventory of IT services across Board divisions on these general IT services categories. We conducted our fieldwork from May 2013 to June We conducted this performance audit in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe the evidence we obtained provides a reasonable basis for our conclusions IT-B-003 9

17 Appendix B Management s Response 2014-IT-B

18 2014-IT-B

19

Audit of the Board s Data Center Relocation

O F F I C E O F IN S P E C TO R G E N E R A L Audit Report 2014-IT-B-002 Audit of the Board s Data Center Relocation February 7, 2014 B O A R D O F G O V E R N O R S O F T H E F E D E R A L R E S E R V

O F F I C E O F IN S P E C TO R G E N E R A L Audit Report 2014-IT-B-002 Audit of the Board s Data Center Relocation February 7, 2014 B O A R D O F G O V E R N O R S O F T H E F E D E R A L R E S E R V

2014 Audit of the Board s Information Security Program

O FFICE OF I NSPECTOR GENERAL Audit Report 2014-IT-B-019 2014 Audit of the Board s Information Security Program November 14, 2014 B OARD OF G OVERNORS OF THE F EDERAL R ESERVE S YSTEM C ONSUMER FINANCIAL

O FFICE OF I NSPECTOR GENERAL Audit Report 2014-IT-B-019 2014 Audit of the Board s Information Security Program November 14, 2014 B OARD OF G OVERNORS OF THE F EDERAL R ESERVE S YSTEM C ONSUMER FINANCIAL

Audit of the CFPB s Acquisition and Contract Management of Select Cloud Computing Services

O F F I C E O F IN S P E C TO R GENERAL Audit Report 2014-IT-C-016 Audit of the CFPB s Acquisition and Contract Management of Select Cloud Computing Services September 30, 2014 B O A R D O F G O V E R

O F F I C E O F IN S P E C TO R GENERAL Audit Report 2014-IT-C-016 Audit of the CFPB s Acquisition and Contract Management of Select Cloud Computing Services September 30, 2014 B O A R D O F G O V E R

2014 Audit of the CFPB s Information Security Program

O FFICE OF I NSPECTOR GENERAL Audit Report 2014-IT-C-020 2014 Audit of the CFPB s Information Security Program November 14, 2014 B OARD OF G OVERNORS OF THE F EDERAL R ESERVE S YSTEM C ONSUMER FINANCIAL

O FFICE OF I NSPECTOR GENERAL Audit Report 2014-IT-C-020 2014 Audit of the CFPB s Information Security Program November 14, 2014 B OARD OF G OVERNORS OF THE F EDERAL R ESERVE S YSTEM C ONSUMER FINANCIAL

Audit of Planned Physical and Environmental Controls for the Board s Data Center Relocation

O FFICE OF I NSPECTOR GENERAL Audit Report 2015-IT-B-001 Audit of Planned Physical and Environmental Controls for the Board s Data Center Relocation January 30, 2015 B OARD OF G OVERNORS OF THE F EDERAL

O FFICE OF I NSPECTOR GENERAL Audit Report 2015-IT-B-001 Audit of Planned Physical and Environmental Controls for the Board s Data Center Relocation January 30, 2015 B OARD OF G OVERNORS OF THE F EDERAL

The Board Continues to Follow a Structured Approach to Planning and Executing the Relocation of the Data Center

O FFICE OF INSPECTOR GENERAL Audit Report 2015-IT-B-017 The Board Continues to Follow a Structured Approach to Planning and Executing the Relocation of the Data Center September 16, 2015 B OARD OF G OVERNORS

O FFICE OF INSPECTOR GENERAL Audit Report 2015-IT-B-017 The Board Continues to Follow a Structured Approach to Planning and Executing the Relocation of the Data Center September 16, 2015 B OARD OF G OVERNORS

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION The Internal Revenue Service Should Improve Server Software Asset Management and Reduce Costs September 25, 2014 Reference Number: 2014-20-042 This report

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION The Internal Revenue Service Should Improve Server Software Asset Management and Reduce Costs September 25, 2014 Reference Number: 2014-20-042 This report

Office of Audits and Evaluations Report No. AUD-13-007. The FDIC s Controls over Business Unit- Led Application Development Activities

Office of Audits and Evaluations Report No. AUD-13-007 The FDIC s Controls over Business Unit- Led Application Development Activities September 2013 Executive Summary The FDIC s Controls over Business

Office of Audits and Evaluations Report No. AUD-13-007 The FDIC s Controls over Business Unit- Led Application Development Activities September 2013 Executive Summary The FDIC s Controls over Business

September 1, 2000 Audit Report No. 00-038. Audit of the Information Technology Configuration Management Program

September 1, 2000 Audit Report No. 00-038 Audit of the Information Technology Configuration Management Program Federal Deposit Insurance Corporation Office of Audits Washington, D.C. 20434 Office of Inspector

September 1, 2000 Audit Report No. 00-038 Audit of the Information Technology Configuration Management Program Federal Deposit Insurance Corporation Office of Audits Washington, D.C. 20434 Office of Inspector

EPA Could Improve Processes for Managing Contractor Systems and Reporting Incidents

OFFICE OF INSPECTOR GENERAL Audit Report Catalyst for Improving the Environment EPA Could Improve Processes for Managing Contractor Systems and Reporting Incidents Report No. 2007-P-00007 January 11, 2007

OFFICE OF INSPECTOR GENERAL Audit Report Catalyst for Improving the Environment EPA Could Improve Processes for Managing Contractor Systems and Reporting Incidents Report No. 2007-P-00007 January 11, 2007

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Desktop and Laptop Software License Management June 25, 2013 Reference Number: 2013-20-025 This report has cleared the Treasury Inspector General for Tax

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Desktop and Laptop Software License Management June 25, 2013 Reference Number: 2013-20-025 This report has cleared the Treasury Inspector General for Tax

NATIONAL CREDIT UNION ADMINISTRATION OFFICE OF INSPECTOR GENERAL

NATIONAL CREDIT UNION ADMINISTRATION OFFICE OF INSPECTOR GENERAL SECURITY OF THE NCUA DATA CENTER Report # August 12, 2013 James Hagen Inspector General W. Marvin Stith, CISA Senior IT Auditor Table of

NATIONAL CREDIT UNION ADMINISTRATION OFFICE OF INSPECTOR GENERAL SECURITY OF THE NCUA DATA CENTER Report # August 12, 2013 James Hagen Inspector General W. Marvin Stith, CISA Senior IT Auditor Table of

VA Office of Inspector General

VA Office of Inspector General OFFICE OF AUDITS AND EVALUATIONS Department of Veterans Affairs Audit of Office of Information Technology s Strategic Human Capital Management October 29, 2012 11-00324-20

VA Office of Inspector General OFFICE OF AUDITS AND EVALUATIONS Department of Veterans Affairs Audit of Office of Information Technology s Strategic Human Capital Management October 29, 2012 11-00324-20

Office of Inspector General

DEPARTMENT OF HOMELAND SECURITY Office of Inspector General Security Weaknesses Increase Risks to Critical United States Secret Service Database (Redacted) Notice: The Department of Homeland Security,

DEPARTMENT OF HOMELAND SECURITY Office of Inspector General Security Weaknesses Increase Risks to Critical United States Secret Service Database (Redacted) Notice: The Department of Homeland Security,

Report of Audit OFFICE OF INSPECTOR GENERAL. Information Technology Infrastructure Project Management A-07-02. Tammy Rapp Auditor-in-Charge

OFFICE OF INSPECTOR GENERAL Report of Audit Information Technology Infrastructure Project Management A-07-02 Tammy Rapp Auditor-in-Charge FARM CREDIT ADMINISTRATION Memorandum Office of Inspector General

OFFICE OF INSPECTOR GENERAL Report of Audit Information Technology Infrastructure Project Management A-07-02 Tammy Rapp Auditor-in-Charge FARM CREDIT ADMINISTRATION Memorandum Office of Inspector General

STATEMENT OF CHARLES EDWARDS DEPUTY INSPECTOR GENERAL U.S. DEPARTMENT OF HOMELAND SECURITY BEFORE THE

STATEMENT OF CHARLES EDWARDS DEPUTY INSPECTOR GENERAL U.S. DEPARTMENT OF HOMELAND SECURITY BEFORE THE COMMITTEE ON HOMELAND SECURITY SUBCOMMITTEE ON OVERSIGHT AND MANAGEMENT EFFICIENCY U.S. HOUSE OF REPRESENTATIVES

STATEMENT OF CHARLES EDWARDS DEPUTY INSPECTOR GENERAL U.S. DEPARTMENT OF HOMELAND SECURITY BEFORE THE COMMITTEE ON HOMELAND SECURITY SUBCOMMITTEE ON OVERSIGHT AND MANAGEMENT EFFICIENCY U.S. HOUSE OF REPRESENTATIVES

Improved Management Practices Needed to Increase Use of Exchange Network

OFFICE OF INSPECTOR GENERAL Audit Report Catalyst for Improving the Environment Improved Management Practices Needed to Increase Use of Exchange Network Report No. 2007-P-00030 August 20, 2007 Report Contributors:

OFFICE OF INSPECTOR GENERAL Audit Report Catalyst for Improving the Environment Improved Management Practices Needed to Increase Use of Exchange Network Report No. 2007-P-00030 August 20, 2007 Report Contributors:

NATIONAL CREDIT UNION ADMINISTRATION OFFICE OF INSPECTOR GENERAL

NATIONAL CREDIT UNION ADMINISTRATION OFFICE OF INSPECTOR GENERAL INDEPENDENT EVALUATION OF THE NATIONAL CREDIT UNION ADMINISTRATION S COMPLIANCE WITH THE FEDERAL INFORMATION SECURITY MANAGEMENT ACT (FISMA)

NATIONAL CREDIT UNION ADMINISTRATION OFFICE OF INSPECTOR GENERAL INDEPENDENT EVALUATION OF THE NATIONAL CREDIT UNION ADMINISTRATION S COMPLIANCE WITH THE FEDERAL INFORMATION SECURITY MANAGEMENT ACT (FISMA)

Software Inventory Management Greater Boston District

Software Inventory Management Greater Boston District Audit Report Report Number IT-AR-15-007 July 13, 2015 Highlights Effective software management practices are not in place to adequately protect and

Software Inventory Management Greater Boston District Audit Report Report Number IT-AR-15-007 July 13, 2015 Highlights Effective software management practices are not in place to adequately protect and

Audit of the Board s Information Security Program

Board of Governors of the Federal Reserve System Audit of the Board s Information Security Program Office of Inspector General November 2011 November 14, 2011 Board of Governors of the Federal Reserve

Board of Governors of the Federal Reserve System Audit of the Board s Information Security Program Office of Inspector General November 2011 November 14, 2011 Board of Governors of the Federal Reserve

How To Improve Mainframe Software Asset Management

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION The Internal Revenue Service Should Improve Mainframe Software Asset Management February 20, 2014 Reference Number: 2014-20-002 This report has cleared

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION The Internal Revenue Service Should Improve Mainframe Software Asset Management February 20, 2014 Reference Number: 2014-20-002 This report has cleared

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION The Enterprise Systems Management Program Is Making Progress to Improve Service Delivery and Monitoring, but Risks Remain September 12, 2008 Reference

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION The Enterprise Systems Management Program Is Making Progress to Improve Service Delivery and Monitoring, but Risks Remain September 12, 2008 Reference

Innovation and Technology Department

PERFORMANCE AUDIT Innovation and Technology Department IT Inventory Asset Management January 11, 2016 Office of the City Manager Internal Audit Division Cheryl Johannes, Internal Audit Manager PERFORMANCE

PERFORMANCE AUDIT Innovation and Technology Department IT Inventory Asset Management January 11, 2016 Office of the City Manager Internal Audit Division Cheryl Johannes, Internal Audit Manager PERFORMANCE

AUDIT REPORT REPORT NUMBER 14 10. Information Technology Microsoft Software Licenses March 27, 2014

AUDIT REPORT REPORT NUMBER 14 10 Information Technology Microsoft Software Licenses March 27, 2014 Date March 27, 2014 To Chief Information Officer From Inspector General Subject Audit Report Information

AUDIT REPORT REPORT NUMBER 14 10 Information Technology Microsoft Software Licenses March 27, 2014 Date March 27, 2014 To Chief Information Officer From Inspector General Subject Audit Report Information

IT Service Desk Unit Opportunities for Improving Service and Cost-Effectiveness

AUDITOR GENERAL S REPORT ACTION REQUIRED IT Service Desk Unit Opportunities for Improving Service and Cost-Effectiveness Date: September 18, 2013 To: From: Wards: Audit Committee Auditor General All Reference

AUDITOR GENERAL S REPORT ACTION REQUIRED IT Service Desk Unit Opportunities for Improving Service and Cost-Effectiveness Date: September 18, 2013 To: From: Wards: Audit Committee Auditor General All Reference

M. RICHARD PORRAS CHIEF FINANCIAL OFFICER AND SENIOR VICE PRESIDENT

March 31, 1999 M. RICHARD PORRAS CHIEF FINANCIAL OFFICER AND SENIOR VICE PRESIDENT JOHN F. KELLY VICE PRESIDENT, EXPEDITED AND PACKAGE SERVICES JAMES F. GRUBIAK VICE PRESIDENT, INTERNATIONAL BUSINESS UNIT

March 31, 1999 M. RICHARD PORRAS CHIEF FINANCIAL OFFICER AND SENIOR VICE PRESIDENT JOHN F. KELLY VICE PRESIDENT, EXPEDITED AND PACKAGE SERVICES JAMES F. GRUBIAK VICE PRESIDENT, INTERNATIONAL BUSINESS UNIT

FEMA Faces Challenges in Managing Information Technology

FEMA Faces Challenges in Managing Information Technology November 20, 2015 OIG-16-10 DHS OIG HIGHLIGHTS FEMA Faces Challenges in Managing Information Technology November 20, 2015 Why We Did This Audit

FEMA Faces Challenges in Managing Information Technology November 20, 2015 OIG-16-10 DHS OIG HIGHLIGHTS FEMA Faces Challenges in Managing Information Technology November 20, 2015 Why We Did This Audit

AUDIT REPORT PERFORMANCE AUDIT OF COMPUTER EQUIPMENT INVENTORY DEPARTMENT OF TECHNOLOGY, MANAGEMENT, AND BUDGET. February 2014

MICHIGAN OFFICE OF THE AUDITOR GENERAL AUDIT REPORT PERFORMANCE AUDIT OF COMPUTER EQUIPMENT INVENTORY DEPARTMENT OF TECHNOLOGY, MANAGEMENT, AND BUDGET February 2014 THOMAS H. MCTAVISH, C.P.A. AUDITOR GENERAL

MICHIGAN OFFICE OF THE AUDITOR GENERAL AUDIT REPORT PERFORMANCE AUDIT OF COMPUTER EQUIPMENT INVENTORY DEPARTMENT OF TECHNOLOGY, MANAGEMENT, AND BUDGET February 2014 THOMAS H. MCTAVISH, C.P.A. AUDITOR GENERAL

University of Oregon Information Technology Risk Assessment. December 2, 2015

December 2, 2015 Table of Contents EXECUTIVE SUMMARY... 3 BACKGROUND... 3 APPROACH... 4 IT UNITS... 5 NOTED STRENGTHS... 5 THEMES... 6 IT RISKS... 11 IT RISKS DESCRIPTIONS... 12 APPENDIX A: BAKER TILLY

December 2, 2015 Table of Contents EXECUTIVE SUMMARY... 3 BACKGROUND... 3 APPROACH... 4 IT UNITS... 5 NOTED STRENGTHS... 5 THEMES... 6 IT RISKS... 11 IT RISKS DESCRIPTIONS... 12 APPENDIX A: BAKER TILLY

Department of Homeland Security Office of Inspector General. Review of U.S. Coast Guard Enterprise Architecture Implementation Process

Department of Homeland Security Office of Inspector General Review of U.S. Coast Guard Enterprise Architecture Implementation Process OIG-09-93 July 2009 Contents/Abbreviations Executive Summary...1 Background...2

Department of Homeland Security Office of Inspector General Review of U.S. Coast Guard Enterprise Architecture Implementation Process OIG-09-93 July 2009 Contents/Abbreviations Executive Summary...1 Background...2

ARKANSAS GENERALLY SUPPORTED ITS CLAIM FOR FEDERAL MEDICAID REIMBURSEMENT

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL ARKANSAS GENERALLY SUPPORTED ITS CLAIM FOR FEDERAL MEDICAID REIMBURSEMENT Inquiries about this report may be addressed to the Office

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL ARKANSAS GENERALLY SUPPORTED ITS CLAIM FOR FEDERAL MEDICAID REIMBURSEMENT Inquiries about this report may be addressed to the Office

Results of Technical Network Vulnerability Assessment: EPA s Andrew W. Breidenbach Environmental Research Center

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Quick Reaction Report Catalyst for Improving the Environment Results of Technical Network Vulnerability Assessment: EPA s Andrew W. Breidenbach

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Quick Reaction Report Catalyst for Improving the Environment Results of Technical Network Vulnerability Assessment: EPA s Andrew W. Breidenbach

AUDIT REPORT REPORT NUMBER 14 08. Information Technology Professional Services Oracle Software March 25, 2014

AUDIT REPORT REPORT NUMBER 14 08 Information Technology Professional Services Oracle Software March 25, 2014 Date March 25, 2014 To Chief Information Officer Director, Acquisition Services From Inspector

AUDIT REPORT REPORT NUMBER 14 08 Information Technology Professional Services Oracle Software March 25, 2014 Date March 25, 2014 To Chief Information Officer Director, Acquisition Services From Inspector

AUDIT OF USAID s IMPLEMENTATION OF INTERNET PROTOCOL VERSION 6

OFFICE OF INSPECTOR GENERAL AUDIT OF USAID s IMPLEMENTATION OF INTERNET PROTOCOL VERSION 6 AUDIT REPORT NO. A-000-08-006-P September 4, 2008 WASHINGTON, DC Office of Inspector General September 4, 2008

OFFICE OF INSPECTOR GENERAL AUDIT OF USAID s IMPLEMENTATION OF INTERNET PROTOCOL VERSION 6 AUDIT REPORT NO. A-000-08-006-P September 4, 2008 WASHINGTON, DC Office of Inspector General September 4, 2008

AUDIT REPORT. The Department of Energy's Management of Cloud Computing Activities

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections AUDIT REPORT The Department of Energy's Management of Cloud Computing Activities DOE/IG-0918 September 2014 Department

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections AUDIT REPORT The Department of Energy's Management of Cloud Computing Activities DOE/IG-0918 September 2014 Department

THE INFORMATION TECHNOLOGY INFRASTRUCTURE

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL THE INFORMATION TECHNOLOGY INFRASTRUCTURE AND OPERATIONS OFFICE HAD INADEQUATE INFORMATION SECURITY CONTROLS Inquires about this report

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL THE INFORMATION TECHNOLOGY INFRASTRUCTURE AND OPERATIONS OFFICE HAD INADEQUATE INFORMATION SECURITY CONTROLS Inquires about this report

INFORMATION SECURITY AT THE HEALTH RESOURCES AND SERVICES ADMINISTRATION NEEDS IMPROVEMENT BECAUSE CONTROLS WERE NOT FULLY IMPLEMENTED AND MONITORED

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL INFORMATION SECURITY AT THE HEALTH RESOURCES AND SERVICES ADMINISTRATION NEEDS IMPROVEMENT BECAUSE CONTROLS WERE NOT FULLY IMPLEMENTED

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL INFORMATION SECURITY AT THE HEALTH RESOURCES AND SERVICES ADMINISTRATION NEEDS IMPROVEMENT BECAUSE CONTROLS WERE NOT FULLY IMPLEMENTED

THE STATUS OF ENTERPRISE ARCHITECTURE AND INFORMATION TECHNOLOGY INVESTMENT MANAGEMENT IN THE DEPARTMENT OF JUSTICE

THE STATUS OF ENTERPRISE ARCHITECTURE AND INFORMATION TECHNOLOGY INVESTMENT MANAGEMENT IN THE DEPARTMENT OF JUSTICE U.S. Department of Justice Office of the Inspector General Audit Division Audit Report

THE STATUS OF ENTERPRISE ARCHITECTURE AND INFORMATION TECHNOLOGY INVESTMENT MANAGEMENT IN THE DEPARTMENT OF JUSTICE U.S. Department of Justice Office of the Inspector General Audit Division Audit Report

Audit of Veterans Health Administration Blood Bank Modernization Project

Department of Veterans Affairs Office of Inspector General Audit of Veterans Health Administration Blood Bank Modernization Project Report No. 06-03424-70 February 8, 2008 VA Office of Inspector General

Department of Veterans Affairs Office of Inspector General Audit of Veterans Health Administration Blood Bank Modernization Project Report No. 06-03424-70 February 8, 2008 VA Office of Inspector General

How To Write A Network Vulnerability Assessment For The Environment Protection Agency

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Quick Reaction Report Catalyst for Improving the Environment Results of Technical Network Vulnerability Assessment: EPA s Ronald Reagan

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Quick Reaction Report Catalyst for Improving the Environment Results of Technical Network Vulnerability Assessment: EPA s Ronald Reagan

FDA STAFF MANUAL GUIDES, VOLUME III - GENERAL ADMINISTRATION INFORMATION RESOURCES MANAGEMENT INFORMATION TECHNOLOGY MANAGEMENT

SMG 3210.4 FDA STAFF MANUAL GUIDES, VOLUME III - GENERAL ADMINISTRATION 1. PURPOSE INFORMATION RESOURCES MANAGEMENT INFORMATION TECHNOLOGY MANAGEMENT INFORMATION TECHNOLOGY ASSET MANAGEMENT POLICY Effective

SMG 3210.4 FDA STAFF MANUAL GUIDES, VOLUME III - GENERAL ADMINISTRATION 1. PURPOSE INFORMATION RESOURCES MANAGEMENT INFORMATION TECHNOLOGY MANAGEMENT INFORMATION TECHNOLOGY ASSET MANAGEMENT POLICY Effective

MICHIGAN AUDIT REPORT OFFICE OF THE AUDITOR GENERAL THOMAS H. MCTAVISH, C.P.A. AUDITOR GENERAL

MICHIGAN OFFICE OF THE AUDITOR GENERAL AUDIT REPORT THOMAS H. MCTAVISH, C.P.A. AUDITOR GENERAL The auditor general shall conduct post audits of financial transactions and accounts of the state and of all

MICHIGAN OFFICE OF THE AUDITOR GENERAL AUDIT REPORT THOMAS H. MCTAVISH, C.P.A. AUDITOR GENERAL The auditor general shall conduct post audits of financial transactions and accounts of the state and of all

North Carolina's Information Technology Consolidation Audit

STATE OF NORTH CAROLINA PERFORMANCE AUDIT INFORMATION TECHNOLOGY CONSOLIDATION JANUARY 2013 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR PERFORMANCE AUDIT INFORMATION TECHNOLOGY CONSOLIDATION

STATE OF NORTH CAROLINA PERFORMANCE AUDIT INFORMATION TECHNOLOGY CONSOLIDATION JANUARY 2013 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR PERFORMANCE AUDIT INFORMATION TECHNOLOGY CONSOLIDATION

Software Development Processes

Software Development Processes Audit Report Report Number IT-AR-15-006 July 13, 2015 Highlights The Postal Service does not consistently manage software development risk. Background Organizations spend

Software Development Processes Audit Report Report Number IT-AR-15-006 July 13, 2015 Highlights The Postal Service does not consistently manage software development risk. Background Organizations spend

Hanh Do, Director, Information Systems Audit Division, GAA. HUD s Controls Over Selected Configuration Management Activities Need Improvement

Issue Date March 24, 2011 Audit Report Number 2011-DP-0006 TO: Douglas A. Criscitello, Chief Financial Officer, F Mercedes M. Márquez, Assistant Secretary for Community Planning and Development, D Jerry

Issue Date March 24, 2011 Audit Report Number 2011-DP-0006 TO: Douglas A. Criscitello, Chief Financial Officer, F Mercedes M. Márquez, Assistant Secretary for Community Planning and Development, D Jerry

OFFICE OF THE INSPECTOR GENERAL SOCIAL SECURITY ADMINISTRATION CONTRACT WITH DELL MARKETING, L.P., FOR MICROSOFT LICENSING AND MAINTENANCE

OFFICE OF THE INSPECTOR GENERAL SOCIAL SECURITY ADMINISTRATION CONTRACT WITH DELL MARKETING, L.P., FOR MICROSOFT LICENSING AND MAINTENANCE September 2011 A-06-10-10175 AUDIT REPORT Mis s ion By conducting

OFFICE OF THE INSPECTOR GENERAL SOCIAL SECURITY ADMINISTRATION CONTRACT WITH DELL MARKETING, L.P., FOR MICROSOFT LICENSING AND MAINTENANCE September 2011 A-06-10-10175 AUDIT REPORT Mis s ion By conducting

SAFETY AND SECURITY: Opportunities to Improve Controls Over Police Department Workforce Planning

SAFETY AND SECURITY: Opportunities to Improve Controls Over Police Department Audit Report OIG-A-2015-006 February 12, 2015 2 OPPORTUNITIES EXIST TO IMPROVE WORKFORCE PLANNING PRACTICES AND RELATED SAFETY

SAFETY AND SECURITY: Opportunities to Improve Controls Over Police Department Audit Report OIG-A-2015-006 February 12, 2015 2 OPPORTUNITIES EXIST TO IMPROVE WORKFORCE PLANNING PRACTICES AND RELATED SAFETY

Audit of NRC s Network Security Operations Center

Audit of NRC s Network Security Operations Center OIG-16-A-07 January 11, 2016 All publicly available OIG reports (including this report) are accessible through NRC s Web site at http://www.nrc.gov/reading-rm/doc-collections/insp-gen

Audit of NRC s Network Security Operations Center OIG-16-A-07 January 11, 2016 All publicly available OIG reports (including this report) are accessible through NRC s Web site at http://www.nrc.gov/reading-rm/doc-collections/insp-gen

Management Advisory Postal Service Transformation Plan (Report Number OE-MA-03-001)

") October 29, 2002 RALPH J. MODEN VICE PRESIDENT, STRATEGIC PLANNING SUBJECT: Management Advisory Postal Service Transformation Plan (Report Number ) This management advisory presents the results of our

October 29, 2002 RALPH J. MODEN VICE PRESIDENT, STRATEGIC PLANNING SUBJECT: Management Advisory Postal Service Transformation Plan (Report Number ) This management advisory presents the results of our

Office of Inspector General Evaluation of the Consumer Financial Protection Bureau s Consumer Response Unit

Office of Inspector General Evaluation of the Consumer Financial Protection Bureau s Consumer Response Unit Consumer Financial Protection Bureau September 2012 September 28, 2012 MEMORANDUM TO: FROM: SUBJECT:

Office of Inspector General Evaluation of the Consumer Financial Protection Bureau s Consumer Response Unit Consumer Financial Protection Bureau September 2012 September 28, 2012 MEMORANDUM TO: FROM: SUBJECT:

W September 14, 1998. Final Report on the Audit of Outsourcing of Desktop Computers (Assignment No. A-HA-97-047) Report No.

Report No.") W September 14, 1998 TO: FROM: SUBJECT: AO/Chief Information Officer W/Assistant Inspector General for Auditing Final Report on the Audit of Outsourcing of Desktop Computers (Assignment No. A-HA-97-047)

W September 14, 1998 TO: FROM: SUBJECT: AO/Chief Information Officer W/Assistant Inspector General for Auditing Final Report on the Audit of Outsourcing of Desktop Computers (Assignment No. A-HA-97-047)

Evaluation Report. The Social Security Administration s Cloud Computing Environment

Evaluation Report The Social Security Administration s Cloud Computing Environment A-14-14-24081 December 2014 MEMORANDUM Date: December 17, 2014 Refer To: To: From: The Commissioner Inspector General

Evaluation Report The Social Security Administration s Cloud Computing Environment A-14-14-24081 December 2014 MEMORANDUM Date: December 17, 2014 Refer To: To: From: The Commissioner Inspector General

Project Delays Prevent EPA from Implementing an Agency-wide Information Security Vulnerability Management Program

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Audit Report Catalyst for Improving the Environment Project Delays Prevent EPA from Implementing an Agency-wide Information Security Vulnerability

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Audit Report Catalyst for Improving the Environment Project Delays Prevent EPA from Implementing an Agency-wide Information Security Vulnerability

a Item Summar WHY ACTION IS NECESSARY: Board approval required for the expenditure of approximately $143,000 which is in excess of the $50,000 limit.

a Item Summar ACTION REOUESTED: WHY ACTION IS NECESSARY: Board approval required for the expenditure of approximately $143,000 which is in excess of the $50,000 limit. WHAT ACTION ACCOMPLISHES: The wireless

a Item Summar ACTION REOUESTED: WHY ACTION IS NECESSARY: Board approval required for the expenditure of approximately $143,000 which is in excess of the $50,000 limit. WHAT ACTION ACCOMPLISHES: The wireless

The Library of Congress

The Library of Congress Office of the Inspector General Information Technology Services The Library Should Explore Alternative Long Distance Telephone Service Providers Audit Report No. 2007 CA 101 March

The Library of Congress Office of the Inspector General Information Technology Services The Library Should Explore Alternative Long Distance Telephone Service Providers Audit Report No. 2007 CA 101 March

Department of Homeland Security Office of Inspector General

Department of Homeland Security Office of Inspector General Vulnerabilities Highlight the Need for More Effective Web Security Management (Redacted) OIG-09-101 September 2009 Office of Inspector General

Department of Homeland Security Office of Inspector General Vulnerabilities Highlight the Need for More Effective Web Security Management (Redacted) OIG-09-101 September 2009 Office of Inspector General

Office of Inspector General

Audit Report OIG-07-043 GENERAL MANAGEMENT: Departmental Offices Did Not Have An Effective Workers Compensation Program July 13, 2007 Office of Inspector General Department of the Treasury Contents Audit

Audit Report OIG-07-043 GENERAL MANAGEMENT: Departmental Offices Did Not Have An Effective Workers Compensation Program July 13, 2007 Office of Inspector General Department of the Treasury Contents Audit

REPORT 2014/001 INTERNAL AUDIT DIVISION. Audit of information and communications technology help desk operations at United Nations Headquarters

INTERNAL AUDIT DIVISION REPORT 2014/001 Audit of information and communications technology help desk operations at United Nations Headquarters Overall results relating to the adequacy and effectiveness

INTERNAL AUDIT DIVISION REPORT 2014/001 Audit of information and communications technology help desk operations at United Nations Headquarters Overall results relating to the adequacy and effectiveness

SECURITY WEAKNESSES IN DOT S COMMON OPERATING ENVIRONMENT EXPOSE ITS SYSTEMS AND DATA TO COMPROMISE

FOR OFFICIAL USE ONLY SECURITY WEAKNESSES IN DOT S COMMON OPERATING ENVIRONMENT EXPOSE ITS SYSTEMS AND DATA TO COMPROMISE Department of Transportation Report No. FI-2013-123 Date Issued: September 10,

FOR OFFICIAL USE ONLY SECURITY WEAKNESSES IN DOT S COMMON OPERATING ENVIRONMENT EXPOSE ITS SYSTEMS AND DATA TO COMPROMISE Department of Transportation Report No. FI-2013-123 Date Issued: September 10,

OFFICE OF INSPECTOR GENERAL. Audit Report

OFFICE OF INSPECTOR GENERAL Audit Report Audit of the Data Management Application Controls and Selected General Controls in the Financial Management Integrated System Report No. 14-12 September 30, 2014

OFFICE OF INSPECTOR GENERAL Audit Report Audit of the Data Management Application Controls and Selected General Controls in the Financial Management Integrated System Report No. 14-12 September 30, 2014

OFFICE OF INSPECTOR GENERAL. Audit Report

OFFICE OF INSPECTOR GENERAL Audit Report Audit of the Business Process Controls in the Financial Management Integrated System Report No. 14-10 August 01, 2014 RAILROAD RETIREMENT BOARD EXECUTIVE SUMMARY

OFFICE OF INSPECTOR GENERAL Audit Report Audit of the Business Process Controls in the Financial Management Integrated System Report No. 14-10 August 01, 2014 RAILROAD RETIREMENT BOARD EXECUTIVE SUMMARY

AUDIT REPORT. The Energy Information Administration s Information Technology Program

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections AUDIT REPORT The Energy Information Administration s Information Technology Program DOE-OIG-16-04 November 2015 Department

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections AUDIT REPORT The Energy Information Administration s Information Technology Program DOE-OIG-16-04 November 2015 Department

U.S. ELECTION ASSISTANCE COMMISSION OFFICE OF INSPECTOR GENERAL

U.S. ELECTION ASSISTANCE COMMISSION OFFICE OF INSPECTOR GENERAL FINAL REPORT: U.S. Election Assistance Commission Compliance with the Requirements of the Federal Information Security Management Act Fiscal

U.S. ELECTION ASSISTANCE COMMISSION OFFICE OF INSPECTOR GENERAL FINAL REPORT: U.S. Election Assistance Commission Compliance with the Requirements of the Federal Information Security Management Act Fiscal

Audit of Case Activity Tracking System Security Report No. OIG-AMR-33-01-02

Audit of Case Activity Tracking System Security Report No. OIG-AMR-33-01-02 BACKGROUND OBJECTIVES, SCOPE, AND METHODOLOGY FINDINGS INFORMATION SECURITY PROGRAM AUDIT FOLLOW-UP CATS SECURITY PROGRAM PLANNING

Audit of Case Activity Tracking System Security Report No. OIG-AMR-33-01-02 BACKGROUND OBJECTIVES, SCOPE, AND METHODOLOGY FINDINGS INFORMATION SECURITY PROGRAM AUDIT FOLLOW-UP CATS SECURITY PROGRAM PLANNING

Briefing Report: Improvements Needed in EPA s Information Security Program

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Briefing Report: Improvements Needed in EPA s Information Security Program Report No. 13-P-0257 May 13, 2013 Scan this mobile code to learn

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Briefing Report: Improvements Needed in EPA s Information Security Program Report No. 13-P-0257 May 13, 2013 Scan this mobile code to learn

AUDIT REPORT 12-1 8. Audit of Controls over GPO s Fleet Credit Card Program. September 28, 2012

AUDIT REPORT 12-1 8 Audit of Controls over GPO s Fleet Credit Card Program September 28, 2012 Date September 28, 2012 To Director, Acquisition Services From Inspector General Subject Audit Report Audit

AUDIT REPORT 12-1 8 Audit of Controls over GPO s Fleet Credit Card Program September 28, 2012 Date September 28, 2012 To Director, Acquisition Services From Inspector General Subject Audit Report Audit

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections Audit Report The Department of Energy's Management and Use of Mobile Computing Devices and Services DOE/IG-0908 April

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections Audit Report The Department of Energy's Management and Use of Mobile Computing Devices and Services DOE/IG-0908 April

SENIOR SYSTEMS ANALYST

CITY OF MONTEBELLO 109 DEFINITION Under general administrative direction of the City Administrator, provides advanced professional support to departments with very complex computer systems, programs and

CITY OF MONTEBELLO 109 DEFINITION Under general administrative direction of the City Administrator, provides advanced professional support to departments with very complex computer systems, programs and

Nelson R. Bregon, General Deputy Assistant Secretary for Community Planning and Development. James D. McKay Regional Inspector General for Audit, 4AGA

Issue Date July 26, 2006 Audit Report Number 2006-AT-1014 TO: Nelson R. Bregon, General Deputy Assistant Secretary for Community Planning and Development FROM: James D. McKay Regional Inspector General

Issue Date July 26, 2006 Audit Report Number 2006-AT-1014 TO: Nelson R. Bregon, General Deputy Assistant Secretary for Community Planning and Development FROM: James D. McKay Regional Inspector General

Service Asset & Configuration Management PinkVERIFY

-11-G-001 General Criteria Does the tool use ITIL 2011 Edition process terms and align to ITIL 2011 Edition workflows and process integrations? -11-G-002 Does the tool have security controls in place to

-11-G-001 General Criteria Does the tool use ITIL 2011 Edition process terms and align to ITIL 2011 Edition workflows and process integrations? -11-G-002 Does the tool have security controls in place to

POSTAL REGULATORY COMMISSION

POSTAL REGULATORY COMMISSION OFFICE OF INSPECTOR GENERAL FINAL REPORT INFORMATION SECURITY MANAGEMENT AND ACCESS CONTROL POLICIES Audit Report December 17, 2010 Table of Contents INTRODUCTION... 1 Background...1

POSTAL REGULATORY COMMISSION OFFICE OF INSPECTOR GENERAL FINAL REPORT INFORMATION SECURITY MANAGEMENT AND ACCESS CONTROL POLICIES Audit Report December 17, 2010 Table of Contents INTRODUCTION... 1 Background...1

Fiscal Year 2014 Federal Information Security Management Act Report: Status of EPA s Computer Security Program

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Information Technology Fiscal Year 2014 Federal Information Security Management Act Report: Status of EPA s Computer Security Program Report.

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Information Technology Fiscal Year 2014 Federal Information Security Management Act Report: Status of EPA s Computer Security Program Report.

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL Evaluation and Inspection Services Memorandum May 5, 2009 TO: FROM: SUBJECT: James Manning Acting Chief Operating Officer Federal Student

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL Evaluation and Inspection Services Memorandum May 5, 2009 TO: FROM: SUBJECT: James Manning Acting Chief Operating Officer Federal Student

Results of Technical Network Vulnerability Assessment: EPA s Region 1

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Results of Technical Network Vulnerability Assessment: EPA s Region 1 Report No. 12-P-0518 June 5, 2012 Scan this mobile code to learn more

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Results of Technical Network Vulnerability Assessment: EPA s Region 1 Report No. 12-P-0518 June 5, 2012 Scan this mobile code to learn more

Semiannual Report to Congress. Office of Inspector General

Semiannual Report to Congress Office of Inspector General Federal Election Commission 999 E Street, N.W., Suite 940 Washington, DC 20463 April 1, 2005 September 30, 2005 November 2005 TABLE OF CONTENTS

Semiannual Report to Congress Office of Inspector General Federal Election Commission 999 E Street, N.W., Suite 940 Washington, DC 20463 April 1, 2005 September 30, 2005 November 2005 TABLE OF CONTENTS

U.S. Department of Energy Office of Inspector General Office of Audits & Inspections

U.S. Department of Energy Office of Inspector General Office of Audits & Inspections Audit Report Follow-up Audit of the Department's Cyber Security Incident Management Program DOE/IG-0878 December 2012

U.S. Department of Energy Office of Inspector General Office of Audits & Inspections Audit Report Follow-up Audit of the Department's Cyber Security Incident Management Program DOE/IG-0878 December 2012

METRO REGIONAL GOVERNMENT Records Retention Schedule

Program: Administration IS Administration provides strategic planning, direction, and central management oversight of the Information Services that includes the following programs: Desktop Support Services,

Program: Administration IS Administration provides strategic planning, direction, and central management oversight of the Information Services that includes the following programs: Desktop Support Services,

EPA Needs to Strengthen Its Privacy Program Management Controls

OFFICE OF INSPECTOR GENERAL Audit Report Catalyst for Improving the Environment EPA Needs to Strengthen Its Privacy Program Management Controls Report No. 2007-P-00035 September 17, 2007 Report Contributors:

OFFICE OF INSPECTOR GENERAL Audit Report Catalyst for Improving the Environment EPA Needs to Strengthen Its Privacy Program Management Controls Report No. 2007-P-00035 September 17, 2007 Report Contributors:

The Importance of Information Delivery in IT Operations

The Importance of Information Delivery in IT Operations David Williams Notes accompany this presentation. Please select Notes Page view. These materials can be reproduced only with written approval from

The Importance of Information Delivery in IT Operations David Williams Notes accompany this presentation. Please select Notes Page view. These materials can be reproduced only with written approval from

Has Your Organization Out-Grown Your Helpdesk? A guide to determine when your company is at the right stage to shift to a Service Desk.

Has Your Organization Out-Grown Your Helpdesk? A guide to determine when your company is at the right stage to shift to a Service Desk. 1 P a g e Has Your Organization Out-Grown Your Helpdesk? A guide

Has Your Organization Out-Grown Your Helpdesk? A guide to determine when your company is at the right stage to shift to a Service Desk. 1 P a g e Has Your Organization Out-Grown Your Helpdesk? A guide

2007 Follow-Up Report on the Audit of Information Technology January 2005

2007 Follow-Up Report on the Audit of Information Technology January 2005 Natural Sciences & Engineering Research Council of Canada & Social Sciences & Humanities Research Council of Canada October 2007

2007 Follow-Up Report on the Audit of Information Technology January 2005 Natural Sciences & Engineering Research Council of Canada & Social Sciences & Humanities Research Council of Canada October 2007

IT Vendor Due Diligence. Jennifer McGill CIA, CISA, CGEIT IT Audit Director Carolinas HealthCare System December 9, 2014

IT Vendor Due Diligence Jennifer McGill CIA, CISA, CGEIT IT Audit Director Carolinas HealthCare System December 9, 2014 Carolinas HealthCare System (CHS) Second largest not-for-profit healthcare system

IT Vendor Due Diligence Jennifer McGill CIA, CISA, CGEIT IT Audit Director Carolinas HealthCare System December 9, 2014 Carolinas HealthCare System (CHS) Second largest not-for-profit healthcare system

NASA S PROCESS FOR ACQUIRING INFORMATION TECHNOLOGY SECURITY ASSESSMENT AND MONITORING TOOLS

MARCH 18, 2013 AUDIT REPORT OFFICE OF AUDITS NASA S PROCESS FOR ACQUIRING INFORMATION TECHNOLOGY SECURITY ASSESSMENT AND MONITORING TOOLS OFFICE OF INSPECTOR GENERAL National Aeronautics and Space Administration

MARCH 18, 2013 AUDIT REPORT OFFICE OF AUDITS NASA S PROCESS FOR ACQUIRING INFORMATION TECHNOLOGY SECURITY ASSESSMENT AND MONITORING TOOLS OFFICE OF INSPECTOR GENERAL National Aeronautics and Space Administration

AUDIT OF NASA S EFFORTS TO CONTINUOUSLY MONITOR CRITICAL INFORMATION TECHNOLOGY SECURITY CONTROLS

SEPTEMBER 14, 2010 AUDIT REPORT OFFICE OF AUDITS AUDIT OF NASA S EFFORTS TO CONTINUOUSLY MONITOR CRITICAL INFORMATION TECHNOLOGY SECURITY CONTROLS OFFICE OF INSPECTOR GENERAL National Aeronautics and Space

SEPTEMBER 14, 2010 AUDIT REPORT OFFICE OF AUDITS AUDIT OF NASA S EFFORTS TO CONTINUOUSLY MONITOR CRITICAL INFORMATION TECHNOLOGY SECURITY CONTROLS OFFICE OF INSPECTOR GENERAL National Aeronautics and Space

March 22, 2002 Audit Report No. 02-008. The FDIC s Efforts To Implement a Single Sign-on Process

March 22, 2002 Audit Report No. 02-008 The FDIC s Efforts To Implement a Single Sign-on Process 1 Federal Deposit Insurance Corporation Washington, D.C. 20434 Office of Audits Office of Inspector General

March 22, 2002 Audit Report No. 02-008 The FDIC s Efforts To Implement a Single Sign-on Process 1 Federal Deposit Insurance Corporation Washington, D.C. 20434 Office of Audits Office of Inspector General

Office of Inspector General

INFORMATION TECHNOLOGY: The Bureau of the Public Debt s Certificate Policy Statement Should Be Updated OIG-03-009 October 24, 2002 Office of Inspector General ******* The Department of the Treasury Contents

INFORMATION TECHNOLOGY: The Bureau of the Public Debt s Certificate Policy Statement Should Be Updated OIG-03-009 October 24, 2002 Office of Inspector General ******* The Department of the Treasury Contents

EPA Can Better Assure Continued Operations at National Computer Center Through Complete and Up-to-Date Documentation for Contingency Planning

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Information Technology EPA Can Better Assure Continued Operations at National Computer Center Through Complete and Up-to-Date Documentation

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Information Technology EPA Can Better Assure Continued Operations at National Computer Center Through Complete and Up-to-Date Documentation

GAO INFORMATION TECHNOLOGY. SBA Needs to Strengthen Oversight of Its Loan Management and Accounting System Modernization

GAO United States Government Accountability Office Report to the Chairman, Committee on Small Business, House of Representatives January 2012 INFORMATION TECHNOLOGY SBA Needs to Strengthen Oversight of

GAO United States Government Accountability Office Report to the Chairman, Committee on Small Business, House of Representatives January 2012 INFORMATION TECHNOLOGY SBA Needs to Strengthen Oversight of

Department of Homeland Security Office of Inspector General. The Performance of 287(g) Agreements FY 2011 Update

Agreements FY 2011 Update") Department of Homeland Security Office of Inspector General The Performance of 287(g) Agreements FY 2011 Update OIG-11-119 September 2011 Office ofinspector General U.S. Department of Homeland Security

Department of Homeland Security Office of Inspector General The Performance of 287(g) Agreements FY 2011 Update OIG-11-119 September 2011 Office ofinspector General U.S. Department of Homeland Security

Internal Audit. Audit of HRIS: A Human Resources Management Enabler

Internal Audit Audit of HRIS: A Human Resources Management Enabler November 2010 Table of Contents EXECUTIVE SUMMARY... 5 1. INTRODUCTION... 8 1.1 BACKGROUND... 8 1.2 OBJECTIVES... 9 1.3 SCOPE... 9 1.4

Internal Audit Audit of HRIS: A Human Resources Management Enabler November 2010 Table of Contents EXECUTIVE SUMMARY... 5 1. INTRODUCTION... 8 1.1 BACKGROUND... 8 1.2 OBJECTIVES... 9 1.3 SCOPE... 9 1.4

AUDIT REPORT. Follow-up on the Department of Energy's Acquisition and Maintenance of Software Licenses

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections AUDIT REPORT Follow-up on the Department of Energy's Acquisition and Maintenance of Software Licenses DOE/IG-0920

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections AUDIT REPORT Follow-up on the Department of Energy's Acquisition and Maintenance of Software Licenses DOE/IG-0920

Position Description: Chief Information Officer Department: Information Technology Information Technology FLSA Status: Exempt. Revised: October, 2014

Position Description: Chief Information Officer Department: Information Technology Division: Information Technology FLSA Status: Exempt Location: Griffiss Revised: October, 2014 PURPOSE: I. Assure the

Position Description: Chief Information Officer Department: Information Technology Division: Information Technology FLSA Status: Exempt Location: Griffiss Revised: October, 2014 PURPOSE: I. Assure the

Office of Inspector General

Audit Report OIG-14-034 Not Sufficiently Documented April 21, 2014 Office of Inspector General Department of the Treasury Contents Audit Report Background... 2 Results of Audit... 4 OCC Has Updated Guidance

Audit Report OIG-14-034 Not Sufficiently Documented April 21, 2014 Office of Inspector General Department of the Treasury Contents Audit Report Background... 2 Results of Audit... 4 OCC Has Updated Guidance

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Affordable Care Act: Tracking of Health Insurance Reform Implementation Fund Costs Could Be Improved September 18, 2013 Reference Number: 2013-13-115 This

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Affordable Care Act: Tracking of Health Insurance Reform Implementation Fund Costs Could Be Improved September 18, 2013 Reference Number: 2013-13-115 This

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Virtual Server Technology Has Been Successfully Implemented, but Additional Actions Are Needed to Further Reduce the Number of Servers and Increase Savings

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Virtual Server Technology Has Been Successfully Implemented, but Additional Actions Are Needed to Further Reduce the Number of Servers and Increase Savings

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections Audit Report The Department of Energy's Weatherization Assistance Program Funded under the American Recovery and Reinvestment

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections Audit Report The Department of Energy's Weatherization Assistance Program Funded under the American Recovery and Reinvestment

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION The Internal Revenue Service September 14, 2010 Reference Number: 2010-10-115 This report has cleared the Treasury Inspector General for Tax Administration

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION The Internal Revenue Service September 14, 2010 Reference Number: 2010-10-115 This report has cleared the Treasury Inspector General for Tax Administration

GOVERNMENT INFORMATION SECURITY REFORM ACT STATUS OF EPA S COMPUTER SECURITY PROGRAM

Office of Inspector General Audit Report GOVERNMENT INFORMATION SECURITY REFORM ACT STATUS OF EPA S COMPUTER SECURITY PROGRAM Report Number: 2001-P-00016 September 7, 2001 Inspector General Division Conducting

Office of Inspector General Audit Report GOVERNMENT INFORMATION SECURITY REFORM ACT STATUS OF EPA S COMPUTER SECURITY PROGRAM Report Number: 2001-P-00016 September 7, 2001 Inspector General Division Conducting

Office of Inspector General

Audit Report OIG-15-003 INFORMATION TECHNOLOGY: Fiscal Service s Management of Cloud Computing Services Needs Improvement October 8, 2014 Office of Inspector General Department of the Treasury Contents

Audit Report OIG-15-003 INFORMATION TECHNOLOGY: Fiscal Service s Management of Cloud Computing Services Needs Improvement October 8, 2014 Office of Inspector General Department of the Treasury Contents

Page 1 of 5. IS 335: Information Technology in Business Lecture Outline Computer Technology: Your Need to Know

Lecture Outline Computer Technology: Your Need to Know Objectives In this discussion, you will learn to: Describe the activities of information systems professionals Describe the technical knowledge of

Lecture Outline Computer Technology: Your Need to Know Objectives In this discussion, you will learn to: Describe the activities of information systems professionals Describe the technical knowledge of